Embed Size (px)

Citation preview

@ 2016 Deloite Financial Advisory 1

The Hotel Property HandbookInvestment & Financing Keys

Balearic Islands Snapshot

Financial Advisory I Real Estate - Hospitality

October 2017

@ 2016 Deloite Financial Advisory 2

The Hotel Property HandbookBalearic Islands Snapshot

Javier García-Mateo, MRICS

PartnerFinancial Advisory ‖ Real Estate

[email protected]: +34 659 90 02 15

Ana Granado, MRICS

DirectorFinancial Advisory ‖ Real Estate

[email protected]: +34 630 78 44 73

Jose María Espejo

Senior ManagerFinancial Advisory ‖ Real Estate

[email protected]: +34 918 232 692

Jordi Schoenenberger

PartnerHospitality Industry [email protected]: +34 932 543 932

Fernando Baldellou

PartnerHead of Financial Advisory – Hospitality [email protected]: +34 914 432 514

@ 2016 Deloite Financial Advisory 3

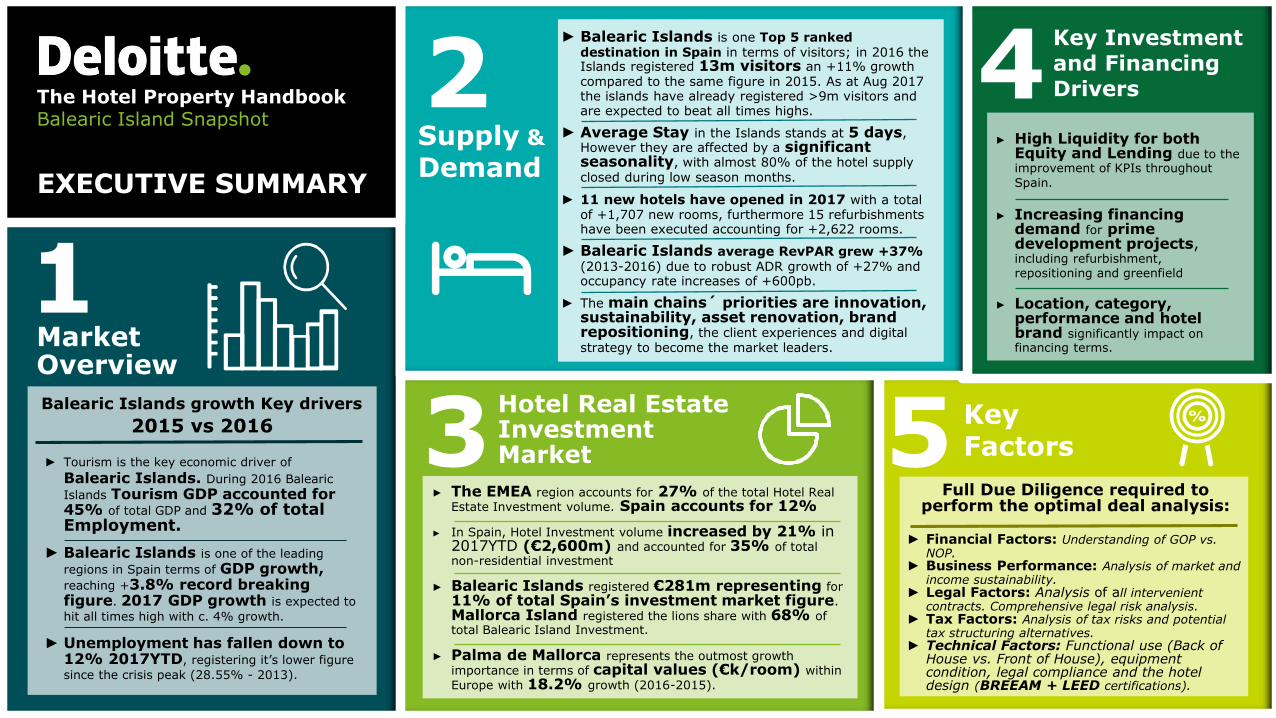

5 Key Factors

Full Due Diligence required to perform the optimal deal analysis:

► Financial Factors: Understanding of GOP vs. NOP.

► Business Performance: Analysis of market and income sustainability.

► Legal Factors: Analysis of all intervenient contracts. Comprehensive legal risk analysis.

► Tax Factors: Analysis of tax risks and potential tax structuring alternatives.

► Technical Factors: Functional use (Back of House vs. Front of House), equipment condition, legal compliance and the hotel design (BREEAM + LEED certifications).

Key Investment and Financing Drivers

► High Liquidity for both Equity and Lending due to the improvement of KPIs throughout

Spain.

► Increasing financing demand for prime development projects, including refurbishment, repositioning and greenfield

► Location, category, performance and hotel brand significantly impact on financing terms.Market

Overview

1

► Tourism is the key economic driver of

Balearic Islands. During 2016 Balearic

Islands Tourism GDP accounted for 45% of total GDP and 32% of total Employment.

► Balearic Islands is one of the leading

regions in Spain terms of GDP growth, reaching +3.8% record breaking figure. 2017 GDP growth is expected to

hit all times high with c. 4% growth.

► Unemployment has fallen down to 12% 2017YTD, registering it’s lower figure

since the crisis peak (28.55% - 2013).

2015 vs 2016

Balearic Islands growth Key drivers

► Balearic Islands is one Top 5 ranked destination in Spain in terms of visitors; in 2016 the Islands registered 13m visitors an +11% growth compared to the same figure in 2015. As at Aug 2017 the islands have already registered >9m visitors and are expected to beat all times highs.

► Average Stay in the Islands stands at 5 days, However they are affected by a significant seasonality, with almost 80% of the hotel supply closed during low season months.

► 11 new hotels have opened in 2017 with a total of +1,707 new rooms, furthermore 15 refurbishments have been executed accounting for +2,622 rooms.

► Balearic Islands average RevPAR grew +37% (2013-2016) due to robust ADR growth of +27% and occupancy rate increases of +600pb.

► The main chains´ priorities are innovation, sustainability, asset renovation, brand repositioning, the client experiences and digital strategy to become the market leaders.

2Supply &

Demand

4

3Hotel Real Estate Investment Market

The Hotel Property HandbookBalearic Island Snapshot

EXECUTIVE SUMMARY

► The EMEA region accounts for 27% of the total Hotel Real Estate Investment volume. Spain accounts for 12%

► In Spain, Hotel Investment volume increased by 21% in 2017YTD (€2,600m) and accounted for 35% of total non-residential investment

► Balearic Islands registered €281m representing for

11% of total Spain’s investment market figure.

Mallorca Island registered the lions share with 68% of total Balearic Island Investment.

► Palma de Mallorca represents the outmost growth importance in terms of capital values (€k/room) within

Europe with 18.2% growth (2016-2015).

@ 2016 Deloite Financial Advisory 4

Cap

ital

Val

ues

Gro

wth

(%

)2

01

5-2

01

6

Capital Valu

e p

er

room

(2015-1

6)

(8.1%) (13.9%)

(6.2%)

(4.0%)

0.5% 1.7% 6.6% 13.9% (3.7%)

(1.1%)7.9% 11.0% 4.6% 15.5% (6.7%)

18.2%

€800k

€600k

€400k

€200k

€100k

-

€200k

€400k

€600k

€800k P

ari

s

Lo

nd

on

Zü

ric

h

Ge

nev

a

Ro

me

Flo

ren

ce

Am

ste

rda

m

Ba

rcelo

na

Mila

n

Mu

nic

h

Co

pen

ha

ge

n

Mad

rid

Eu

rop

e

Du

blin

Ed

inb

urg

h

Palm

a M

allo

rca

The Hotel Property HandbookBalearic Island Snapshot

EXECUTIVE SUMMARY

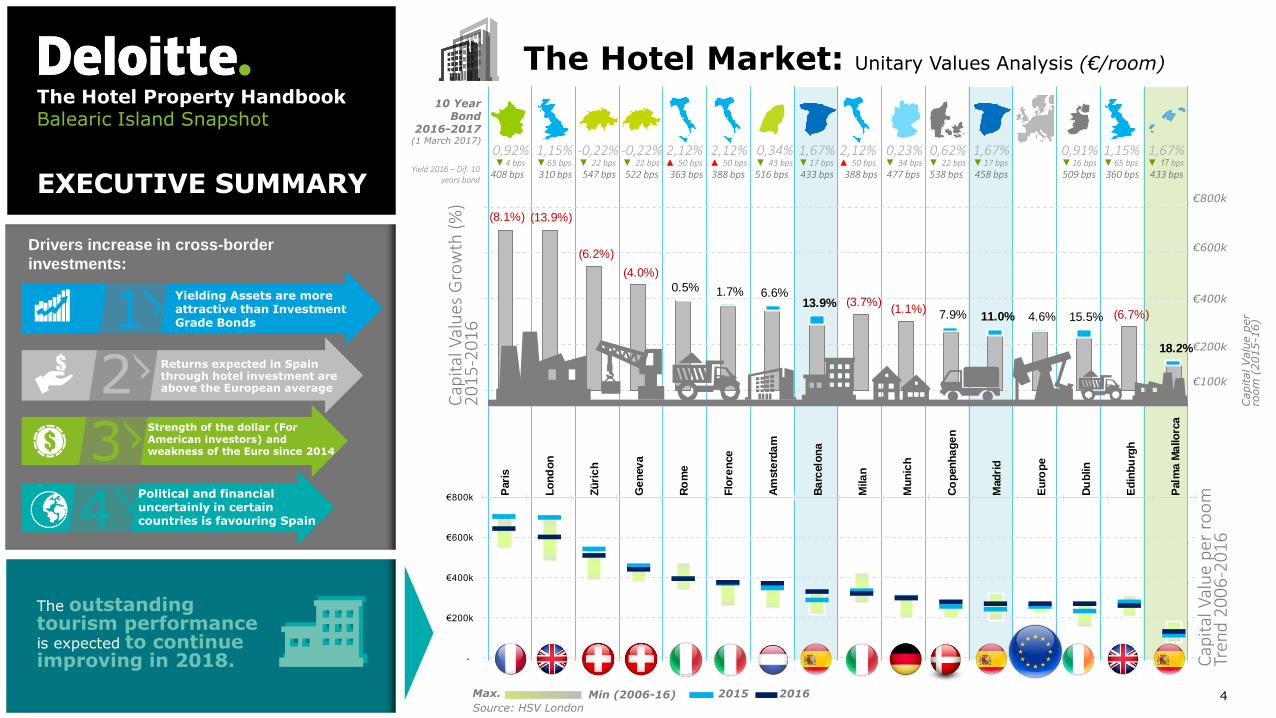

Drivers increase in cross-border

investments:

2

3

1

4

Yielding Assets are more attractive than Investment Grade Bonds

Strength of the dollar (For American investors) and weakness of the Euro since 2014

Political and financial uncertainly in certain countries is favouring Spain

Cap

ital

Val

ue

per

ro

om

Tr

end

20

06

-20

16

Max. Min (2006-16) 2015 2016

Source: HSV London

The Hotel Market: Unitary Values Analysis (€/room)

The outstanding tourism performanceis expected to continue improving in 2018.

Returns expected in Spain through hotel investment are above the European average

10 Year Bond

2016-2017(1 March 2017)

Yield 2016 – Dif. 10 years bond

2,12%▲ 50 bps

1,67%▼ 17 bps

1,15%▼65 bps

0,92%▼4 bps

1,15%▼65 bps

0,23%▼ 34 bps

0,91%▼16 bps

2,12%▲ 50 bps

2,12%▲ 50 bps

1,67%▼17 bps

1,67%▼17 bps

0,34%▼ 43 bps

0,62%▼ 22 bps

-0,22%▼ 22 bps

-0,22%▼ 22 bps

363 bps 433 bps310 bps408 bps 360 bps477 bps 509 bps388 bps 388 bps433 bps 458 bps516 bps 538 bps522 bps547 bps

@ 2016 Deloite Financial Advisory 5

750 576 519 607 932

2,702 2,145 2,600

150 279 88 120 596

674 930 428

1,467 591

571 751

2,242

1,263

660 595 644

687 365

867

2,297

1,894 3,769

2,277

1,460

1,056

544

807

2,520

5,313

4,895

1,781

4,470

3,189

2,087

3,151

8,587

11,845 12,398

7,334

-

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017YTD

Top 10 Spanish single asset transactions:

A total pipeline investment volume of €800m is expected to be traded in Spain

Spanish Investment Market

Source: Deloitte

Source: Deloitte

EXECUTIVE SUMMARY

Total Hotel investment volume in

Spain as at 2017YTD: €2,600m

Short Term Medium Term Long Term TOTAL

75%100%

17%

8%

In 2017YTD the Hotel investment volume has exceed by 21% the investment volume of 2016. Hotel typology represents 35% of the total investment volume

Source: Deloitte Data Base and third party sources

For more information see CHAPTER 3 (Investment Market)

35%Hotel

+21%

Hotels

Logistic

Retail High Street

Retail Shopping Centre

Offices

# Asset UnitsPrice

(€m)Typology

1 Ritz-Carlton Abama 461 183 Vacational

2 Hotel Villaitana 390 101 Vacational

3 Jardin Tropical 390 101 Vacational

4 Sol Príncipe 799 89 Vacational

5 Hotel Silken 240 80 Urban

6 Hilton Diagonal Mar Barcelona (55%)238 80 Urban

7 Ritz-Carlton Abama 50% 461 75 Vacational

8 Sol Palmanova 653 73 Vacational

9 Silken Puerta de América 315 48 Vacational

10 AC Malaga Palacio 214 48 Urban

The Hotel Property HandbookBalearic Island Snapshot

Balearic Islands

€281mMallorca68%

Ibiza32%

@ 2016 Deloite Financial Advisory 6

European Yields & Capital Values (2016):

For more information see CHAPTER 4 (Key Investment and Financing Drivers)

in the full report.

Source: Deloitte Data Base

EXECUTIVE SUMMARY

European Investment Market

3 Spanish transactions are includedwithin the Top 10 European deals.

Amounting to €987m, these Spanish transactions account for 30% of the

Top 20 investment volume

Balearic Islands Investment Market: 2016-2017YTDBalearic Islands, with €281m of hotel investment volume in 2017YTD, is playing a main role within the Spanish market representing a 11% share.

Source: Deloitte Data Base and third party sources

For more information see CHAPTER 3 (Investment Market)

City CountryCapital Value

(€k per room)

Lease Yield

2016

Paris France €644k 5,00%

London UK €601k 4,25%

Zürich Switzerland €506k 5,25%

Geneva Switzerland €440k 5,00%

Rome Italy €394k 5,75%

Florence Italy €375k 6,00%

Amsterdam Netherland €371k 5,50%

Barcelona Spain €327k 6,00%

Milan Italy €318k 6,00%

Munich Germany €297k 5,00%

Copenhagen Denmark €276k 6,00%

Madrid Spain €268k 6,25%

Europe €267k 6,00%

The Hotel Property HandbookBalearic Island Snapshot

Year Q Asset Province * Rooms Price Vendor Buyer

2017 3T Sol Palmanova Mallorca 4* 653 72,600,000 Starmel (JV Starwood Capital y Meliá) London & Regional Properties

2017 2T Intertur Hotel Miami Ibiza Ibiza 3* 365 32,420,000 Intertur Hotels KKR y Dunas Capital

2017 3T Sol House Ibiza Ibiza 4* 275 30,600,000 Starmel (JV Starwood Capital y Meliá) London & Regional Properties

2017 2T Intertur Hotel Hawaii Mallorca & Suites Mallorca 4* 299 26,550,000 Intertur Hotels KKR y Dunas Capital

2016 3T Hotel Marble Stella Maris Ibiza 4* 300 25,000,000 n.d. Corendon Hotels

2017 2T Fergus Tobago Mallorca 3* 275 20,200,000 n.d. Hispania

2017 2T Intertur Hotel Hawaii Ibiza Ibiza 4* 210 18,650,000 Intertur Hotels KKR y Dunas Capital

2017 4T Hilton Sa Torre Mallorca 5* 104 18,100,000 HI Partners Blackstone

2017 2T Intertur Palmanova Bay Mallorca 4* 170 15,100,000 Intertur Hotels KKR y Dunas Capital

2016 1T Samoa Mallorca 3* 331 14,415,000 Grupo Hotasa Organización Alexandría

2016 2T Cartago Ibiza 3* 196 13,000,000 Real Estate San Miguel Hispania - SOCIMI

2017 1T Mar y Pins Mallorca n.d. n.d. 12,600,000 Hacienda Harald Fischl

2016 2T Olé Galeón Ibiza 4* 182 12,000,000 Real Estate San Miguel Hispania - SOCIMI

2016 3T Paradise Portinatx Ibiza 3* 134 11,000,000 Later Deruser Hispania - SOCIMI

2017 1T Gran Hotel de Sóller Mallorca 5* 38 10,000,000 Andreu Gelabert Sermeta

2016 3T Hilton Sa Torre Mallorca Mallorca 5* 104 8,400,000 Sa Torre Mallorca HI Partners

2017 2T Intertur Apartamentos Miami Ibiza Ibiza 2* 82 7,280,000 Intertur Hotels KKR y Dunas Capital

2016 2T Club San Miguel Ibiza 3* 106 7,000,000 Real Estate San Miguel Hispania - SOCIMI

2016 3T Hotel Kross Mallorca 3* 112 7,000,000 Banco Popular HM Hotels

2017 1T Blue Sea Arenal Tower Mallorca 3* 152 3,900,000 Blue Sea Portobello

2017 1T Blue Sea Gran Playa Mallorca 3* 139 3,500,000 Blue Sea Portobello

2017 1T Blue Sea La Pinta Mallorca 3* 130 3,300,000 Blue Sea Portobello

2017 1T Blue Sea Costa Verde Mallorca 3* 124 3,100,000 Blue Sea Portobello

2017 1T Blue Sea Don Jaime Mallorca 3* 120 3,000,000 Blue Sea Portobello

2016 1T Viva Alcudia Sun Village Mallorca 4* 203 n.d. Viva Hotels BQ Hoteles

2016 2T Universal Apartahotel Elisa Baleares 3* 54 + 17 n.d. n.d. Universal Hotels

2016 2T Es Figueral Nou Rural Hotel Mallorca 4* 25 n.d. n.d. Ferrer Hotels

2016 2T Bahía Cala Ratjada Mallorca 4* 119 n.d. n.d. Schauinsland-Reisen

2016 3T Allsun Lux de Mar Mallorca 4* 236 n.d. Edificios Fuentemar 16 18 Allsun

2016 4T Garden Lago Mallorca Apt 3* 89 n.d. Diamond Resorts Onahotels

@ 2016 Deloite Financial Advisory 7

100

102

110

123

100

106

104

124

100

108

140

161

80

90

100

110

120

130

140

150

160

170

Mallorca Island Menorca Island Ibiza & Formentera Island

100

111

124

137

100 105

113

124

100

105

115

126

100

106

119

137

100

110

117

130

95

100

105

110

115

120

125

130

135

140

2013 2014 2015 2016

Andalusía Catalonia

Community of Valencia Balearic Islands

Canary Islands Avrg. Vacational dest.

EXECUTIVE SUMMARY

The Hotel Property HandbookBalearic Island Snapshot

GROWTH

EMPLOYMENT

Tourism-related employments

accounts for 12% of Spain’s

employments

In contrast to previous estimates, 12% more UK tourists came to Spain during 2016

BREXIT

Tourism Business Confidence close

to max. levels since 2016

BUSINESS CONFIDENCE

CCI has experienced an

Uptrend since 2012 and is close to

max. levels

CONSUMERCONFIDENCE

The Spanish Tourism Industry is benefiting from the current geopolitical context

GEOPOLITICAL CONTEXT

grew by 3.2% during 2016.

Tourism accounts for 11.3%

of Spain’s GDP

SPAIN’S GDP

75.6 million tourists came to Spain in 2016 spending €77.6k million

RECORD FIGURES 2016

Spanish Tourism industry

acknowledged as the world’s most

competitive

TOURISM COMPETITIVENESS

Hotel assets are in greater demand as the tourism industry

is surpassing historical records

every year for a significant profitability increase

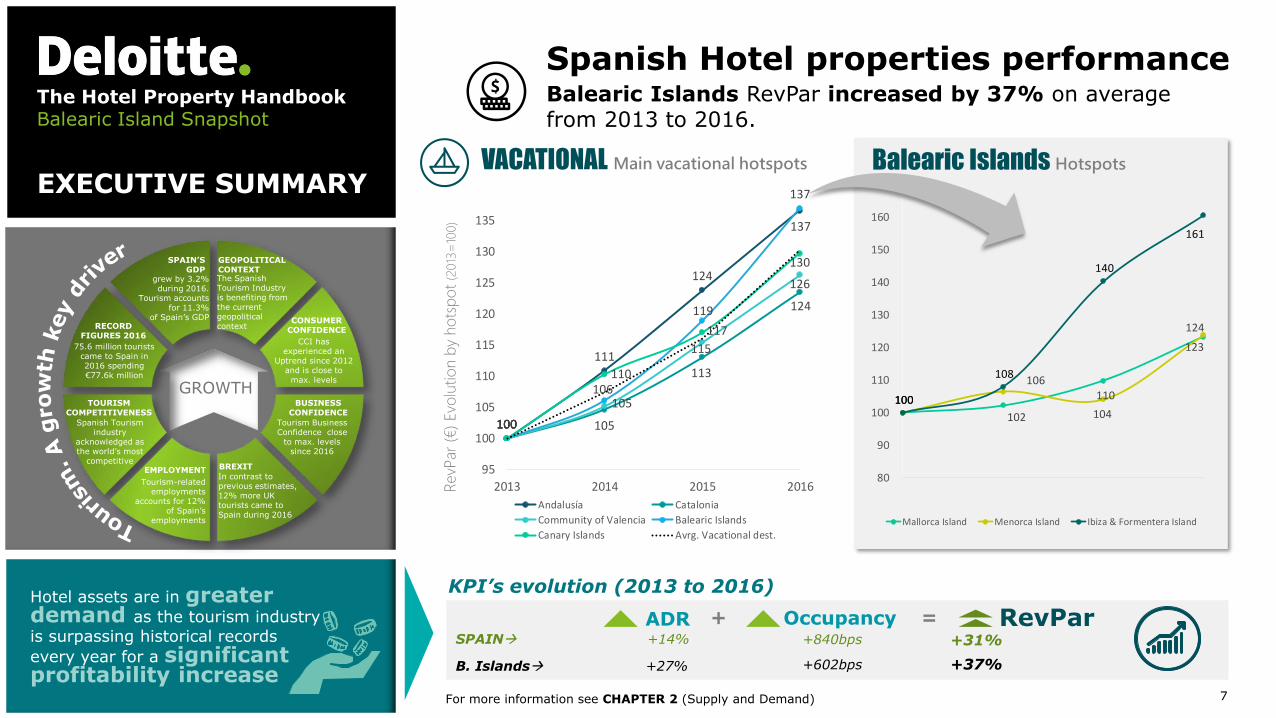

Balearic Islands Hotspots

RevP

ar(€

) Evo

lutio

n b

y ho

tsp

ot

(2013

=10

0)

VACATIONAL Main vacational hotspots

For more information see CHAPTER 2 (Supply and Demand)

Spanish Hotel properties performanceBalearic Islands RevPar increased by 37% on average from 2013 to 2016.

KPI’s evolution (2013 to 2016)

ADR RevParOccupancy+ =SPAIN +14% +840bps +31%

B. Islands +27% +602bps +37%

@ 2016 Deloite Financial Advisory 8

82 62 68 57 56 34 54 48

6,907

5,3965,745

5,120

3,124 2,825

5,6974,964

0

2000

4000

6000

8000

10000

12000

-

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014 2015 2016 2017 YTD

New Hotels # rooms

New openings25%

Refurbishment23%

Chain/Brand Conversion

52%

EXECUTIVE SUMMARY

The Hotel Property HandbookBalearic Island Snapshot

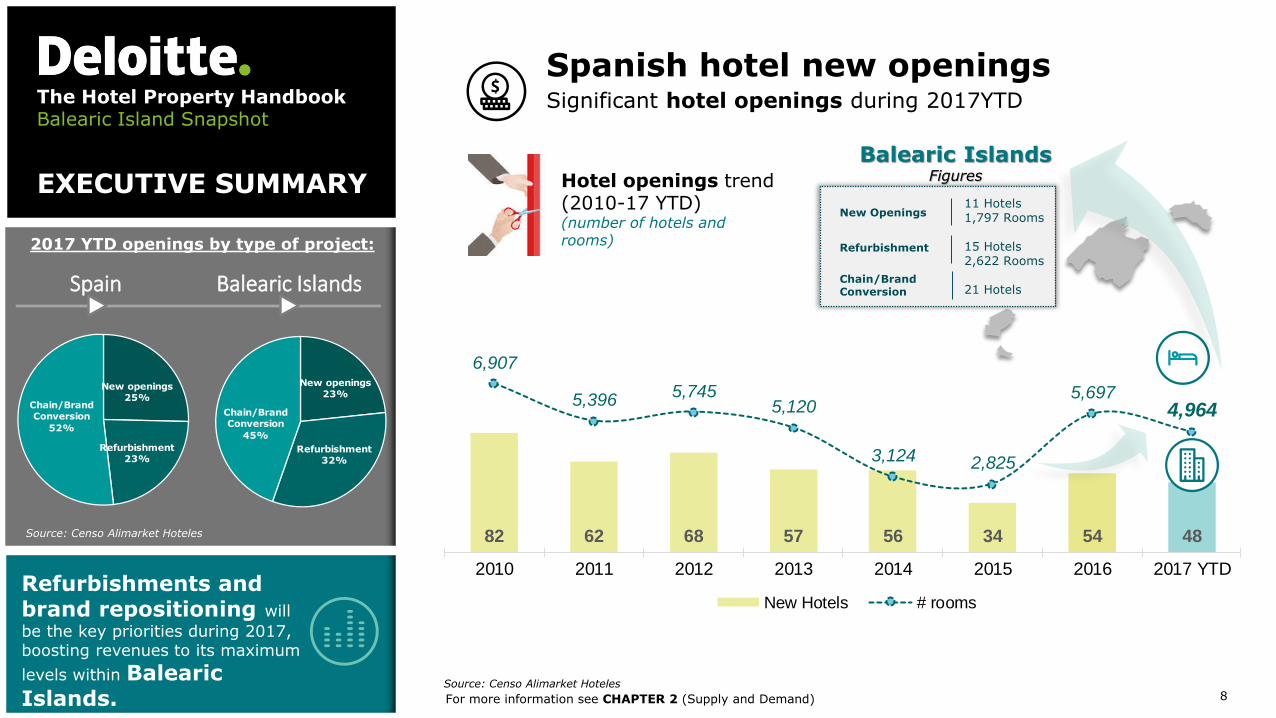

Refurbishments and brand repositioning will

be the key priorities during 2017,boosting revenues to its maximum

levels within Balearic Islands. For more information see CHAPTER 2 (Supply and Demand)

Spanish hotel new openingsSignificant hotel openings during 2017YTD

Hotel openings trend (2010-17 YTD) (number of hotels and rooms)

Source: Censo Alimarket Hoteles

Source: Censo Alimarket Hoteles

New Openings

Refurbishment

Chain/Brand Conversion

11 Hotels1,797 Rooms

15 Hotels2,622 Rooms

21 Hotels

Balearic Islands Figures

Spain Balearic Islands

2017 YTD openings by type of project:

New openings23%

Refurbishment32%

Chain/Brand Conversion

45%

@ 2016 Deloite Financial Advisory 9

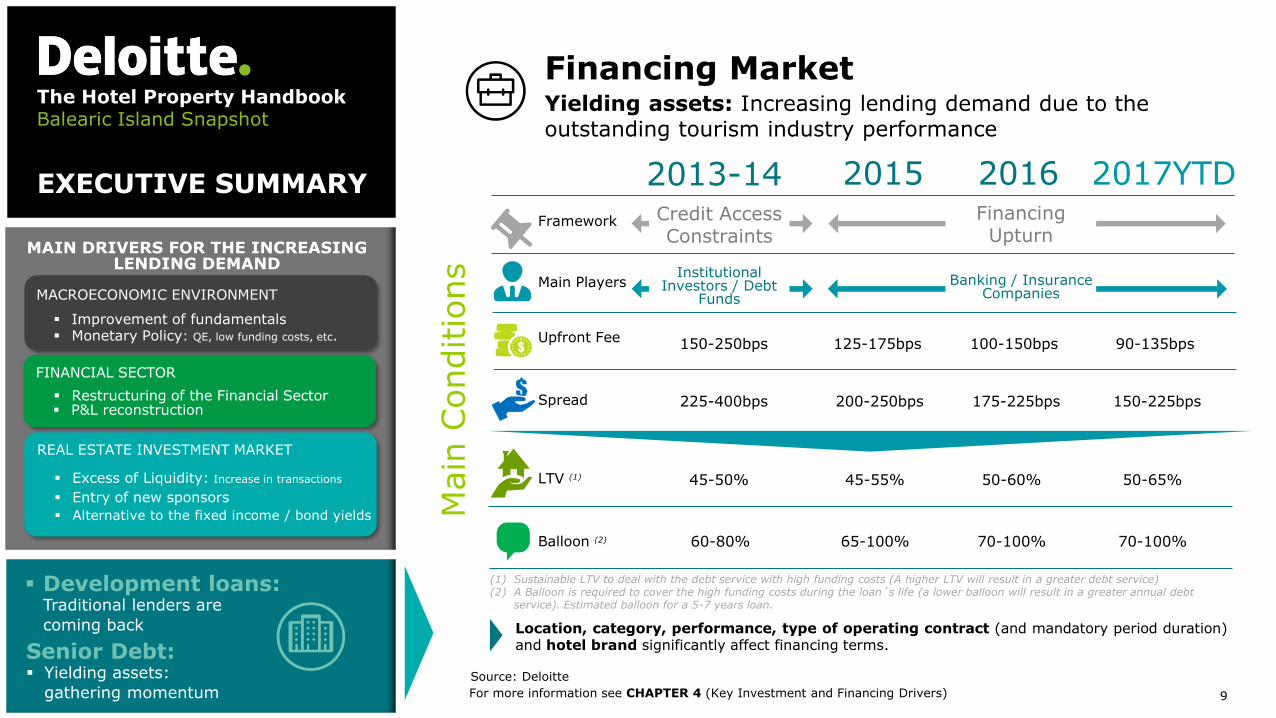

P&L reconstruction Restructuring of the Financial Sector

Improvement of fundamentals

Alternative to the fixed income / bond yields

Senior Debt: Yielding assets:

gathering momentum

MAIN DRIVERS FOR THE INCREASING LENDING DEMAND

Monetary Policy: QE, low funding costs, etc.

Excess of Liquidity: Increase in transactions

Entry of new sponsors

FINANCIAL SECTOR

REAL ESTATE INVESTMENT MARKET

MACROECONOMIC ENVIRONMENT

Yielding assets: Increasing lending demand due to the outstanding tourism industry performance

Financing MarketThe Hotel Property HandbookBalearic Island Snapshot

EXECUTIVE SUMMARY

Source: Deloitte

For more information see CHAPTER 4 (Key Investment and Financing Drivers)

Main

Conditio

ns

LTV (1)

Upfront Fee

Spread

45-50% 45-55%

2015 2016

150-250bps 125-175bps

225-400bps 200-250bps

Framework

Main Players

Balloon (2) 60-80% 65-100%

Credit Access Constraints

Financing Upturn

Institutional Investors / Debt

Funds

Banking / Insurance Companies

2013-14

50-60%

100-150bps

175-225bps

70-100%

Location, category, performance, type of operating contract (and mandatory period duration)and hotel brand significantly affect financing terms.

2017YTD

50-65%

90-135bps

150-225bps

70-100%

(1) Sustainable LTV to deal with the debt service with high funding costs (A higher LTV will result in a greater debt service)(2) A Balloon is required to cover the high funding costs during the loan´s life (a lower balloon will result in a greater annual debt

service). Estimated balloon for a 5-7 years loan.

Development loans: Traditional lenders are

coming back

@ 2016 Deloite Financial Advisory 10

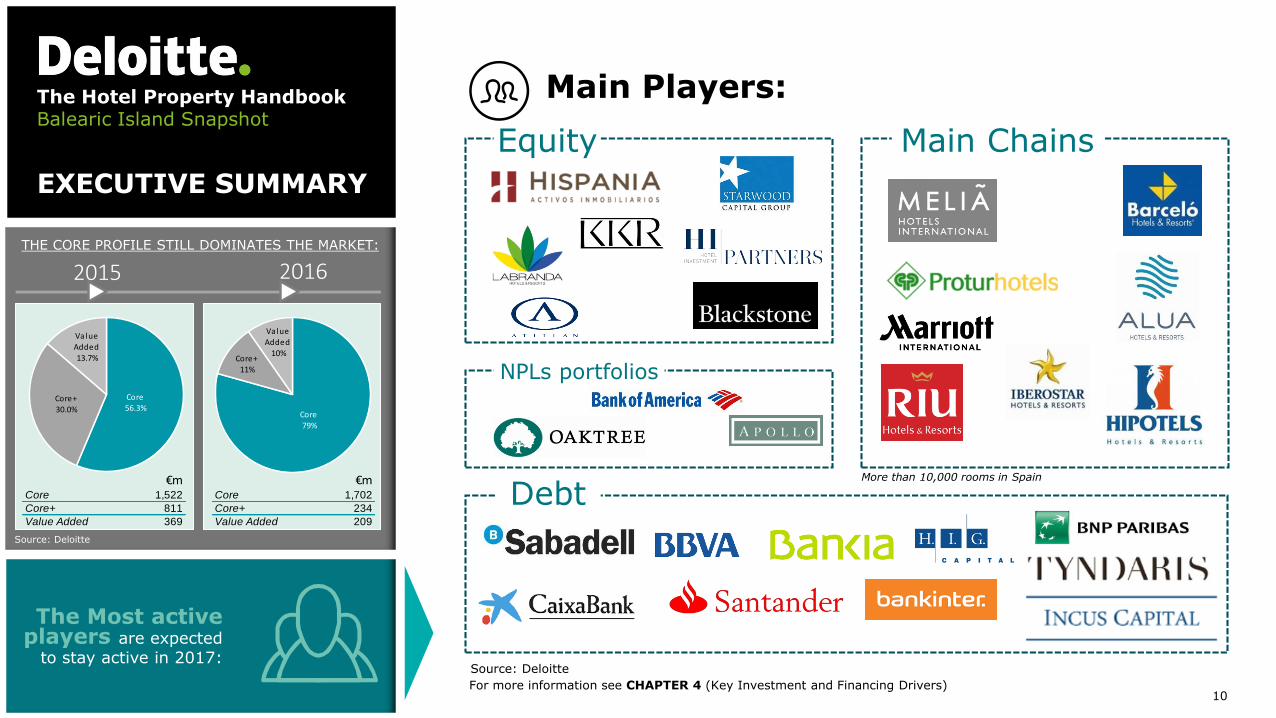

The Most active players are expected

to stay active in 2017:

Main Players:

Equity

Debt(€m)

2015 2016THE CORE PROFILE STILL DOMINATES THE MARKET:

Source: Deloitte

The Hotel Property HandbookBalearic Island Snapshot

EXECUTIVE SUMMARY

Source: Deloitte

For more information see CHAPTER 4 (Key Investment and Financing Drivers)

Main Chains

More than 10,000 rooms in Spain

Core79%

Core+

11%

ValueAdded

10%

Core56.3%

Core+

30.0%

Value

Added13.7%

€mCore 1,522

Core+ 811

Value Added 369

€mCore 1,702

Core+ 234

Value Added 209

NPLs portfolios

@ 2016 Deloite Financial Advisory 11

The Hotel Property HandbookBalearic Island Snapshot

@ 2016 Deloite Financial Advisory 12

The Hotel Property HandbookBalearic Island Snapshot

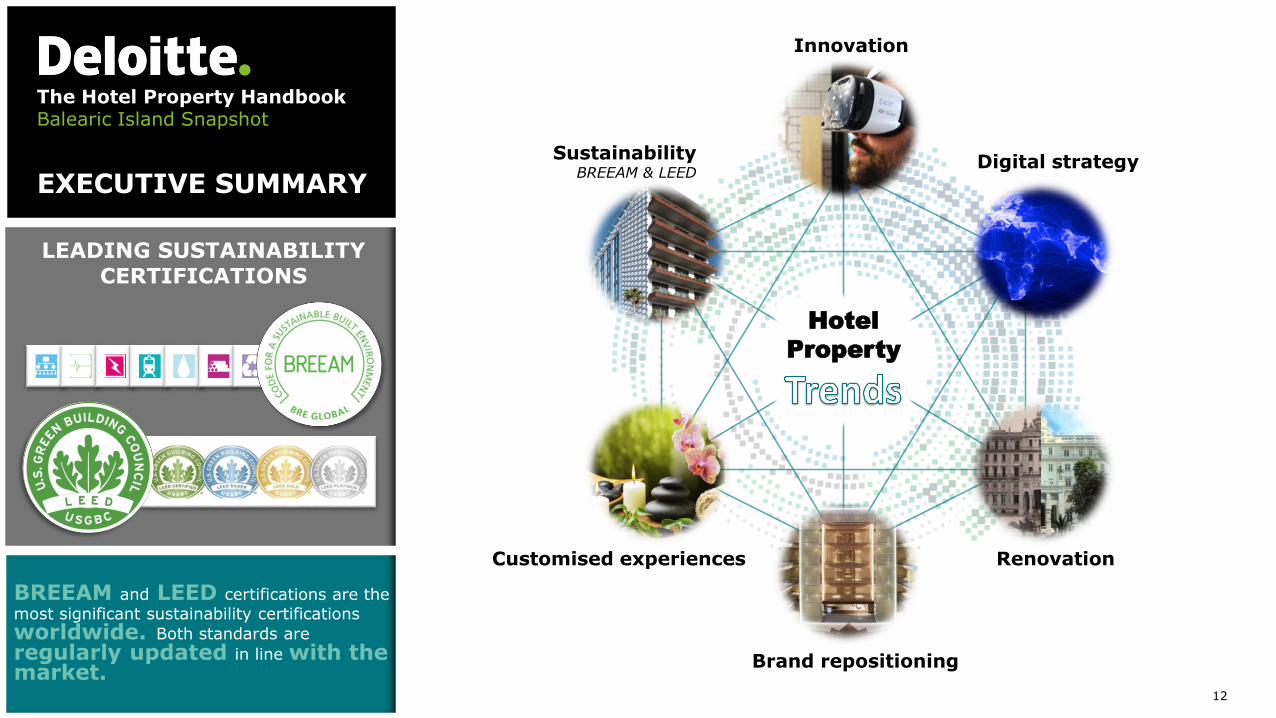

EXECUTIVE SUMMARY

Hotel

Property

Digital strategy

RenovationCustomised experiences

Brand repositioning

Innovation

SustainabilityBREEAM & LEED

BREEAM and LEED certifications are the

most significant sustainability certifications

worldwide. Both standards are

regularly updated in line with the market.

LEADING SUSTAINABILITY CERTIFICATIONS

@ 2016 Deloite Financial Advisory 13

The Hotel Property HandbookBalearic Island Snapshot

EXECUTIVE SUMMARY

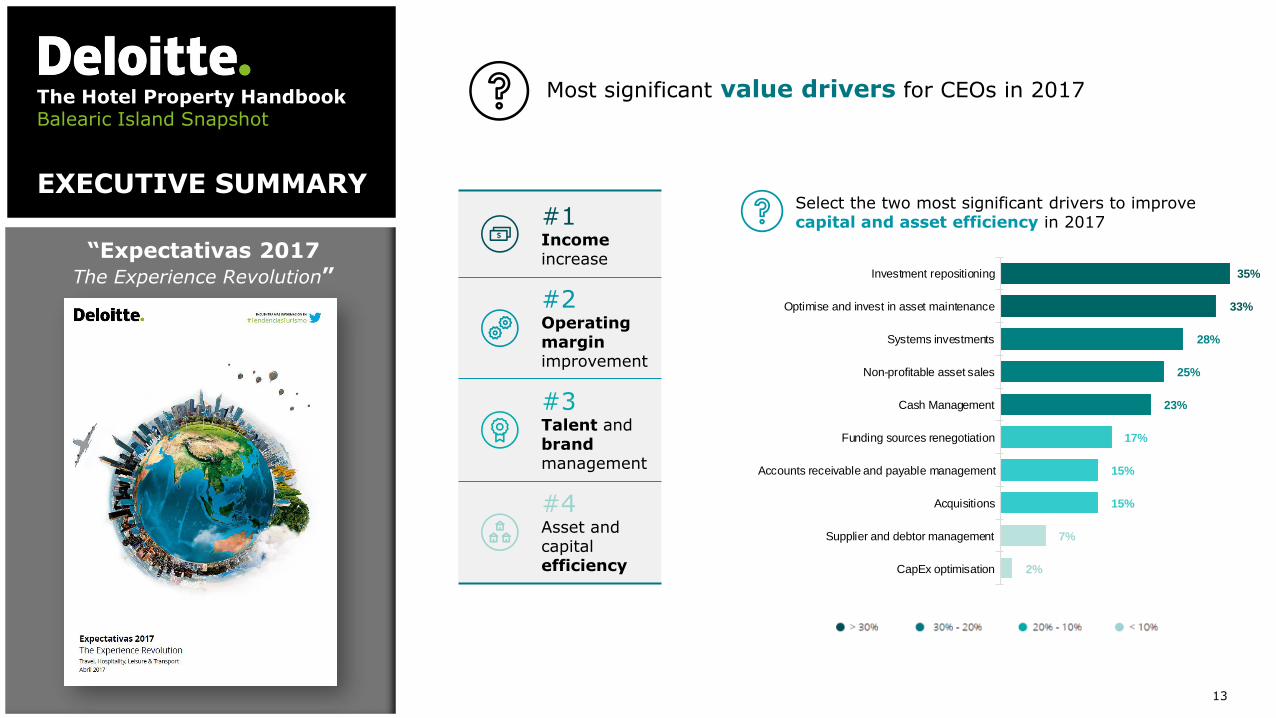

“Expectativas 2017The Experience Revolution”

Most significant value drivers for CEOs in 2017

Select the two most significant drivers to improve capital and asset efficiency in 2017#1

Incomeincrease

#2Operating margin improvement

#3Talent and brandmanagement

#4Asset and capital efficiency

35%

33%

28%

25%

23%

17%

15%

15%

7%

2%

Investment repositioning

Optimise and invest in asset maintenance

Systems investments

Non-profitable asset sales

Cash Management

Funding sources renegotiation

Accounts receivable and payable management

Acquisitions

Supplier and debtor management

CapEx optimisation

@ 2016 Deloite Financial Advisory 14

The Hotel Property HandbookSpain 2017

Javier García-Mateo, MRICS

PartnerFinancial Advisory ‖ Real Estate

[email protected]: +34 659 90 02 15

Ana Granado, MRICS

DirectorFinancial Advisory ‖ Real Estate

[email protected]: +34 630 78 44 73

Jose María Espejo

Senior ManagerFinancial Advisory ‖ Real Estate

[email protected]: +34 918 232 692

Jordi Schoenenberger

PartnerHospitality Industry [email protected]: +34 932 543 932

Fernando Baldellou

PartnerHead of Financial Advisory – Hospitality [email protected]: +34 914 432 514

@ 2016 Deloite Financial Advisory 15