Embed Size (px)

Citation preview

The Hidden Costs of

Networked LearningThe Impact of a Costing Framework on

Educational Practice

Professor Paul Bacsich and Charlotte Ash

Sheffield Hallam University, UK

Introduction Paul Bacsich and Charlotte Ash Sheffield Hallam University, UK 6 month study Funded by the JISC, part of the Funding Council

for Higher Education in the UK Aim - to produce a planning document and

financial schema that together accurately record the Hidden Costs of Networked Learning

Terminology

Networked Learning synonymous with ‘online learning’ and ‘technology

enhanced learning’ Hidden Costs

costs which are fundamentally unrecorded (staff and student personally incurred costs) or absorbed into larger budgets (and consequently can not be attributed an individual activity)

Examples of Hidden Costs Increased telephone call bills for students due to

Internet usage to access lecture notes, course conferencing and assignments

Entertainment expenses incurred by academic staff at conferences but not reimbursed by the Institution

The usage of research funding to bolster teaching resources - or visa versa

Barriers to Costing No agreement about which costs to take into account Reliable data unavailable - no systematic collecting Costs are unstable and evolving Some data is confidential and not publicly available

Moonen, 1997

Bacsich et al, 1999

Each previous methodology uses a different vocabulary - need to uniform before analysis

Study Methodology

detailed literature review of over

100 sources

sectoral survey of UK HEIs

seven case studies based on interviews with key staff

survey of students at Sheffield

Hallam University

consultation with other projectsand experts world-wide

Top Level Conclusions

From the Study

In order to accurately record the Costs of Networked Learning you must have a universally accepted

method of what costs to record and how in place from the start which takes into account all stakeholders

From the Literature

Much of the literature formed interesting background

reading but failed to travel far enough towards operational conclusions to be taken (individually) as

a basis

The KPMG, and later JPCSG, work was of interest - as was the US Flashlight work

Examples were taken from the training sector for their focus on Activity Based Costing

From the Sectoral Survey

The survey established that Networked Learning is taking place - quite extensively- in the UK

There is no accepted method of what to record and how - or even whether costs should be recorded

From the Case Studies

Six Universities chosen from the survey to represent

the sector, plus Sheffield Hallam University

Networked Learning is mainly delivered by a small number of enthusiasts but pockets of innovation are

starting to influence a wider audience

Universities were moving towards Networked Learning for similar reasons - improving access and

quality without increasing costs

Barriers

Barriers to Networked Learning

Lack of training in new technologies Lack of transparent tools Lack of pedagogical evidence to support a move Lack of standards Lack of water-proof network

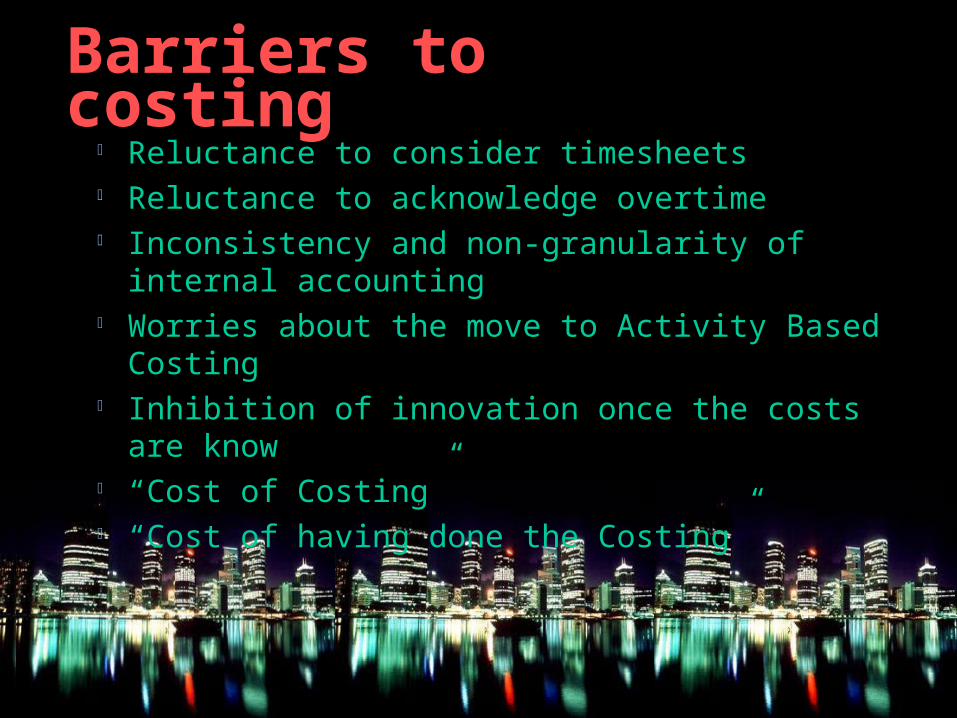

Barriers to costing Reluctance to consider timesheets Reluctance to acknowledge overtime Inconsistency and non-granularity of internal

accounting Worries about the move to Activity Based Costing Inhibition of innovation once the costs are know “Cost of Costing” “Cost of having done the Costing”

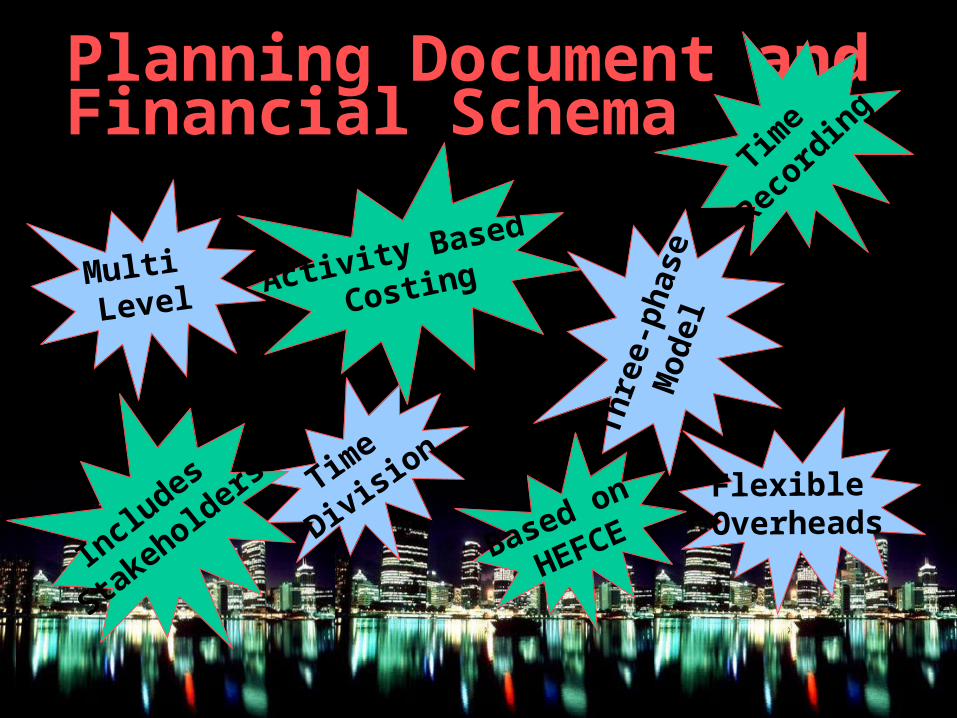

Planning Document and Financial Schema

Multi

Level

Activity Based Costing

Based on HEFCE

Time

Recor

ding

Flexible Overheads

Thr

ee-p

hase

Mod

el

Time Division

Inclu

des

Stakeholder

s

Caveats

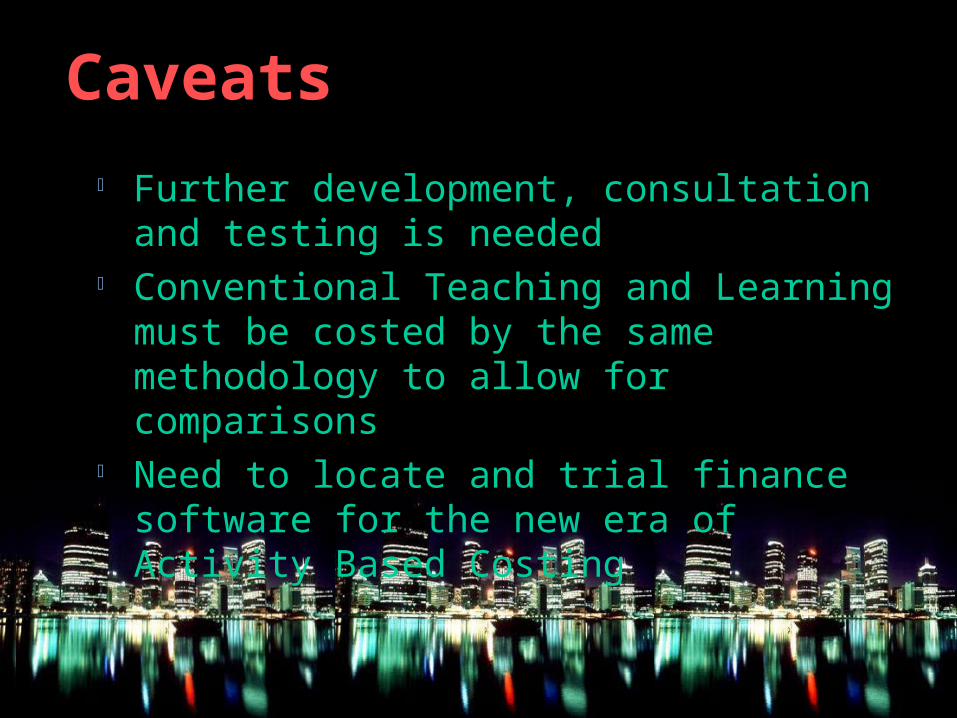

Further development, consultation and testing is needed

Conventional Teaching and Learning must be costed by the same methodology to allow for comparisons

Need to locate and trial finance software for the new era of Activity Based Costing

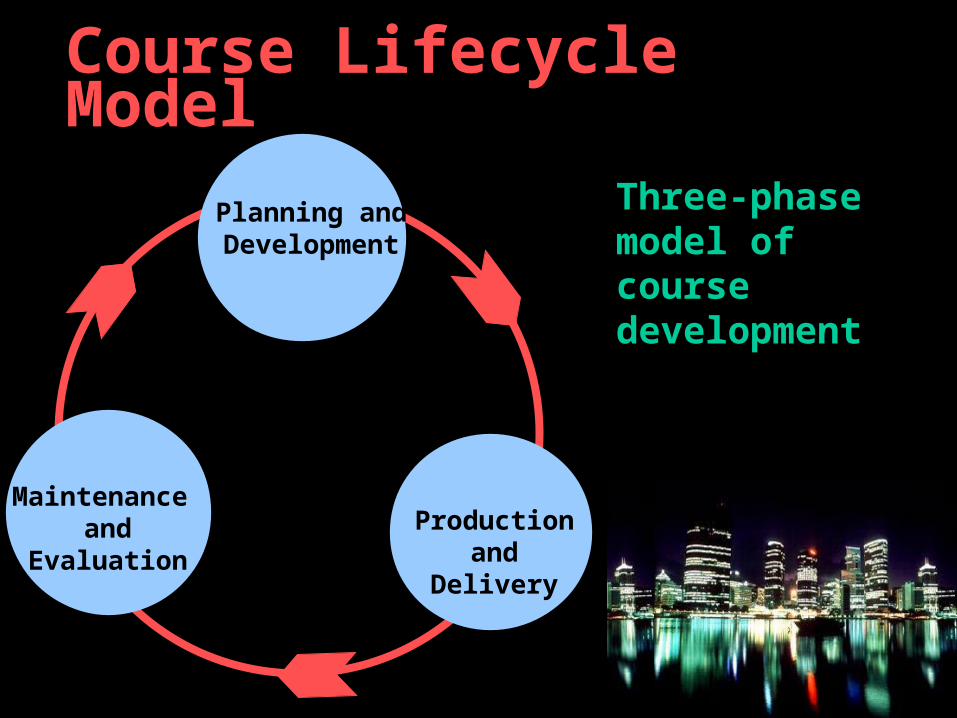

Course Lifecycle Model

Planning and Development

Production and Delivery

Maintenance and Evaluation

Three-phase model of course development

Impact on Stakeholders

Top Management Believe that Networked Learning is positive but

are often unwilling to channel the funds Believe that a costing framework will help track

the costs and encourage individuals to partake Pedagogical evidence needed to increase uptake -

cost is not necessarily the main barrier Agree with our approach as it is based on recent

announcements by the Funding Councils

Academic Staff Absorbing a large quantity of the Hidden Costs Self purchased home computers, Internet charges

and consumables Time is considered a main problem by academic

staff Academics on the whole support the study

conclusions but do not like the ideas of some form of time-sheet

Academic Management Welcome the approach as it may empower them to

negotiate with service depts on overhead issues Concerned about the implementation of an

academic staff time monitoring system Concern about the planning/financial focus of the

framework being applied to education Must engage in creative dialogue with

administrators using a common vocabulary

Service Departments

Concerned about charging on usage basis rather than by estimation

This includes the method of usage-based charging

Administration and finance staff

Brunt of additional work likely to fall on administrators

Greater co-ordination needed Finance awareness raising Managing customer expectation

Students

Not part of this paper

Further Work Harmonisation of our work with other countries

USA Canada Australia Europe

Further development, consideration and testing of the framework

Concentration in other areas - like further education

This presentation and details about the project can be found at -

http://www.shu.ac.uk/virtual_campus/cnl/

Thank you for listening