Embed Size (px)

Citation preview

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

The Hartford’s Investor Presentation on

Talcott Resolution

April 11, 2013

Hartford, Connecticut

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Agenda

9:00 – 9:05 Safe Harbor Sabra Purtill

9:05 – 9:15 Welcome and Overview Liam McGee

9:15 – 9:50 Talcott Resolution Beth Bombara

9:50 – 10:10 Risk Management and Hedging Bob Rupp

10:10 – 10:30 Coffee Break

10:30 – 11:15 VA Metrics and Capital Margins Chris Swift

11:15 – 12:15 Q&A session Panel

12:15 – 1:30 Luncheon with Management

2

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Safe Harbor

Some of the statements in this presentation should be considered forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as "anticipates,"

"intends," "plans," "seeks," "believes," "estimates," "expects," "projects" and similar references to the future. Examples of forward-looking statements include, but are not limited to, statements the company makes regarding future results of

operations. The Hartford cautions investors that these forward-looking statements are not guarantees of future performance, and actual results may differ materially. Investors should consider the important risks and uncertainties that may

cause actual results to differ. These important risks and uncertainties include: challenges related to The Hartford's and its subsidiaries' (collectively, the "Company") current operating environment, including continuing uncertainty about the

strength and speed of the recovery in the United States and other key economies and the impact of governmental stimulus and austerity initiatives, sovereign credit concerns, a sustained low interest rate environment, higher tax rates and

other potentially adverse developments on financial, commodity and credit markets and consumer and business spending and investment and the effect of these events on our returns in investment portfolios and our hedging costs associated

with our variable annuities business; the risks, challenges and uncertainties associated with our capital management plan and our strategic realignment to focus on our property and casualty, group benefits and mutual fund businesses, place

our Individual Annuity business into run-off and the sale of the Individual Life, Woodbury Financial Services and the Retirement Plans businesses; execution risk related to the continued reinvestment of our investment portfolios and refinement

of our hedge program for our run-off annuity block; the capital self-sufficiency of the Company’s Talcott Resolution business in stress scenarios; market risks associated with our business, including changes in interest rates, credit spreads,

equity prices, market volatility and foreign exchange rates, and implied volatility levels, as well as continuing uncertainty in key sectors such as the global real estate market; the possibility of unfavorable loss development including with

respect to long-tailed exposures; the possibility of a pandemic, earthquake, or other natural or man-made disaster that may adversely affect our businesses; weather and other natural physical events, including the severity and frequency of

storms, hail, winter storms, hurricanes and tropical storms, as well as climate change and its potential impact on weather patterns; risk associated with the use of analytical models in making decisions in key areas such as underwriting,

capital, reserving, and catastrophe risk management; the uncertain effects of emerging claim and coverage issues; the Company's ability to effectively price its property and casualty policies, including its ability to obtain regulatory consents to

pricing actions or to non-renewal or withdrawal of certain product lines; the impact on our statutory capital of various factors, including many that are outside the Company's control, which can in turn affect our credit and financial strength

ratings, cost of capital, regulatory compliance and other aspects of our business and results; risks to our business, financial position, prospects and results associated with negative rating actions or downgrades in the Company's financial

strength and credit ratings or negative rating actions or downgrades relating to our investments; the impact on our investment portfolio if our investment portfolio is concentrated in any particular segment of the economy; volatility in our

earnings and potential material changes to our results resulting from our adjustment of our risk management program to emphasize protection of economic value; the potential for differing interpretations of the methodologies, estimations and

assumptions that underlie the valuation of the Company's financial instruments that could result in changes to investment valuations; the subjective determinations that underlie the Company's evaluation of other-than-temporary impairments

on available-for-sale securities; losses due to nonperformance or defaults by others; the potential for further acceleration of deferred policy acquisition cost amortization; the potential for further impairments of our goodwill or the potential for

changes in valuation allowances against deferred tax assets; the possible occurrence of terrorist attacks and the Company's ability to contain its exposure, including the effect of the absence or insufficiency of applicable terrorism legislation on

coverage; the difficulty in predicting the Company's potential exposure for asbestos and environmental claims; the response of reinsurance companies under reinsurance contracts and the availability, pricing and adequacy of reinsurance to

protect the Company against losses; actions by our competitors, many of which are larger or have greater financial resources than we do; the Company's ability to distribute its products through distribution channels, both current and future;

the cost and other effects of increased regulation as a result of the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, which, among other effects, vests a Financial Services Oversight Council with the

power to designate "systemically important" institutions, will require central clearing of, and/or impose new margin and capital requirements on, derivatives transactions, and created a new "Federal Insurance Office" within the U.S. Department

of the Treasury; unfavorable judicial or legislative developments; the potential effect of other domestic and foreign regulatory developments, including those that could adversely impact the demand for the Company's products, operating costs

and required capital levels; regulatory limitations on the ability of the Company and certain of its subsidiaries to declare and pay dividends; the Company's ability to maintain the availability of its systems and safeguard the security of its data in

the event of a disaster, cyber or other information security incident or other unanticipated event; the risk that our framework for managing operational risks may not be effective in mitigating material risk and loss to the Company; the potential

for difficulties arising from outsourcing relationships; the impact of changes in federal or state tax laws; regulatory requirements that could delay, deter or prevent a takeover attempt that shareholders might consider in their best interests; the

impact of potential changes in accounting principles and related financial reporting requirements; the impact of any future errors in financial reporting; the Company's ability to protect its intellectual property and defend against claims of

infringement; the company’s ability to implement its capital plan, and other factors described in such forward-looking statements and other factors described in The Hartford's 2012 Annual Report on Form 10-K, and other filings The Hartford

makes with the Securities and Exchange Commission.

Any forward-looking statement made by the company in this presentation speaks only as of the date of this presentation. Factors or events that could cause the company's actual results to differ may emerge from time to time, and it is not

possible for the company to predict all of them. The company undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise.

USE OF NON-GAAP FINANCIAL MEASURES: The discussion in this presentation of The Hartford’s financial performance includes financial measures that are not derived from generally accepted accounting principles, or GAAP. Information

regarding these non-GAAP financial measures, including reconciliations to the most directly comparable GAAP financial measures, is provided in the appendix to this presentation.

.

3

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Liam McGee, Chairman, President & CEO

1

Welcome and Overview

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

A Sharper Focus to Create Shareholder Value

Creating Shareholder Value

A sharper focus on businesses with: • Strong market positions • Capital generation • Low capital markets sensitivity • High return potential

Leading

Property &

Casualty

Franchise

Major Group

Benefits

Company

Top Performing

Mutual Funds

Reducing Size

and Risk of

Talcott

Resolution

2

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

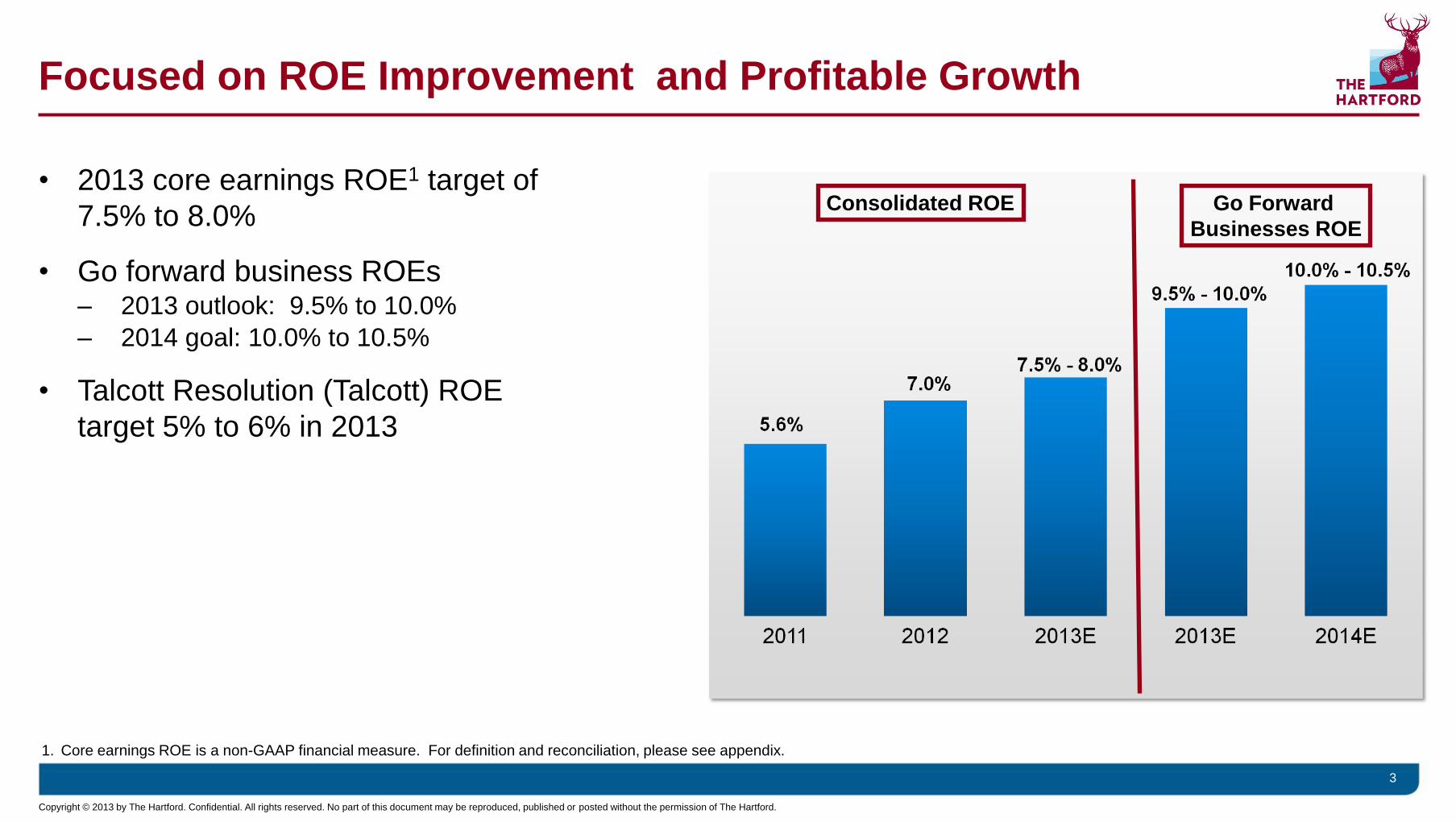

Focused on ROE Improvement and Profitable Growth

• 2013 core earnings ROE1 target of

7.5% to 8.0%

• Go forward business ROEs – 2013 outlook: 9.5% to 10.0%

– 2014 goal: 10.0% to 10.5%

• Talcott Resolution (Talcott) ROE

target 5% to 6% in 2013

3

1. Core earnings ROE is a non-GAAP financial measure. For definition and reconciliation, please see appendix.

Consolidated ROE Go Forward

Businesses ROE

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

4

The Hartford’s Risk Profile Has Been Materially Reduced

Dec. 31,

2009

Mar. 31,

2013E4

Risk

Reduction

Distressed Investments1 $13 billion $1 billion 93%

Debt Leverage2 31.9% 26.9%5 5 points

Variable Annuity NAR3 $6.2 billion $1.6 billion 74%

1. Distressed investments are general account investments with market values at 80% or less of book value

2. Debt leverage calculated as rating agency adjusted debt to total capitalization

3. Variable Annuity (VA) net amount at risk (NAR) is calculated by adding U.S. Guaranteed Minimum Withdrawal Benefit (GMWB) and Japan Guaranteed Minimum Income Benefits (GMIB) NAR

4. NAR and distressed investments are actual; Debt leverage is Dec. 31, 2012 pro forma for debt tender, DAC write-off and sale of Individual Life and Retirement Plans

5. See appendix for calculation

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

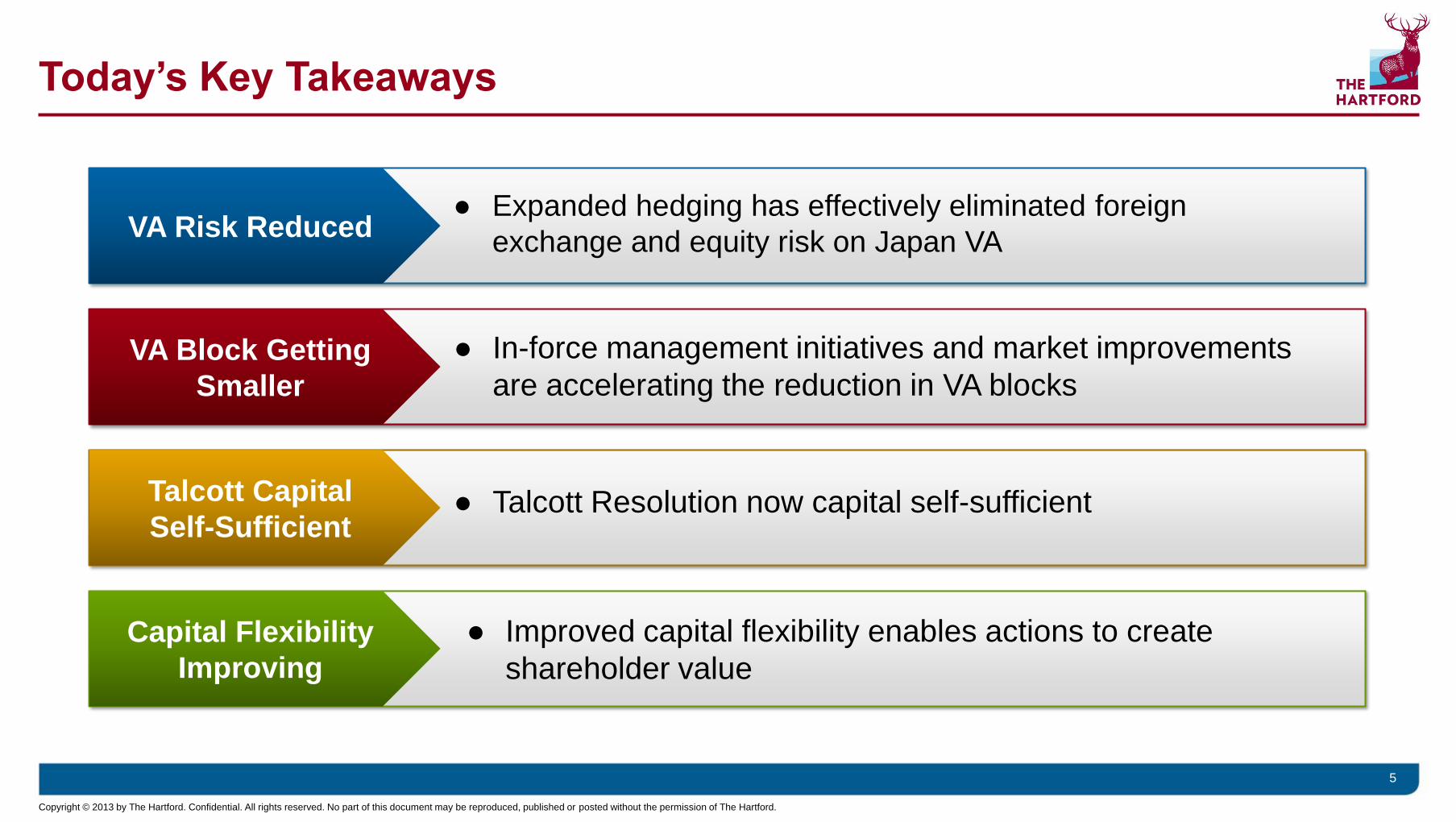

Today’s Key Takeaways

5

VA Risk Reduced

VA Block Getting

Smaller

Talcott Capital

Self-Sufficient

Capital Flexibility

Improving

● Expanded hedging has effectively eliminated foreign

exchange and equity risk on Japan VA

● In-force management initiatives and market improvements

are accelerating the reduction in VA blocks

● Talcott Resolution now capital self-sufficient

● Improved capital flexibility enables actions to create

shareholder value

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

1

Beth Bombara, President, Talcott Resolution

Talcott Resolution

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

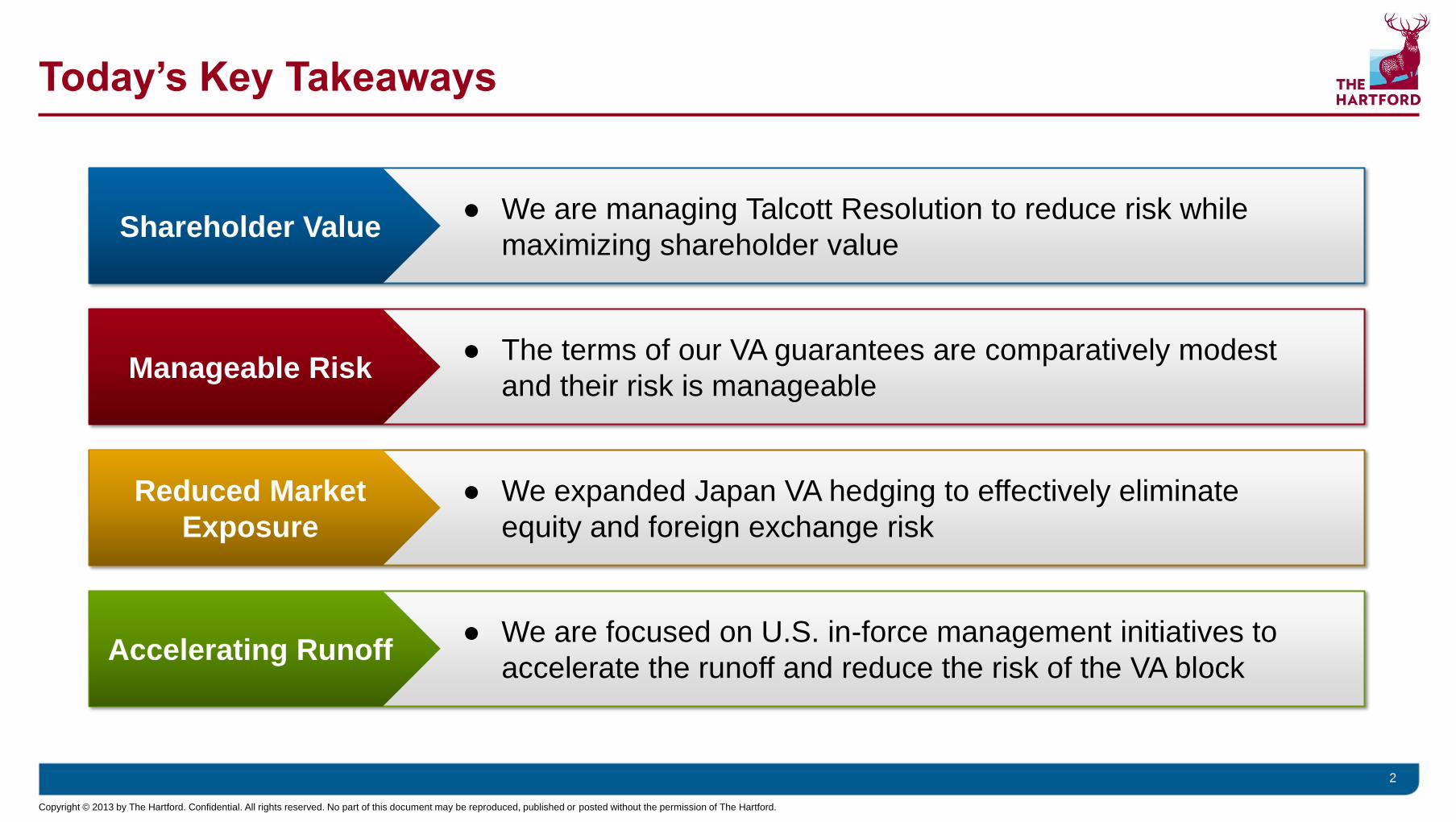

Today’s Key Takeaways

2

● We are managing Talcott Resolution to reduce risk while

maximizing shareholder value Shareholder Value

Manageable Risk

Reduced Market

Exposure

Accelerating Runoff

● The terms of our VA guarantees are comparatively modest

and their risk is manageable

● We expanded Japan VA hedging to effectively eliminate

equity and foreign exchange risk

● We are focused on U.S. in-force management initiatives to

accelerate the runoff and reduce the risk of the VA block

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

3

Agenda

U.S. VA Overview

Talcott Today

Japan VA Overview

Expanded Japan Hedging

U.S. In-Force Management Initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Talcott Resolution Account Value1

$162.7 Billion as of Mar. 31, 2013 • Variable Annuity (VA) Block:

– >50% of Talcott account value

• Non-VA Block:

– Private Placement Life Insurance

(COLI/BOLI): Experience-rated mortality risk

– Institutional: Interest rate risk

– Fixed Annuity: Interest rate risk

4

1. Total account value includes the separate account and general account. Figure excludes the account value associated with the Retirement Plans and Individual Life businesses

VA

58%

FA

9%

Institutional

10%

PPLI

23%

Talcott Resolution is Predominately Variable Annuity

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

5

VA Account Value ~70% U.S. and ~30% Japan

VA Account Value By Country $94.2 Billion as of Mar. 31, 2013

*Total Account Value = Separate Account + General Account

Japan

29%

U.K.

2%

U.S.

69%

VA Contracts By Country

1.3 Million as of Mar. 31, 2013

U.S.

68% Japan

31%

U.K.

1%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

6

Even Without In-Force Management Initiatives, VA Contracts

Expected To Decline By 50% By The End of 2017

-

500

1,000

1,500

2,000

2,500

2007 2012 2013 2014 2015 2016 2017 2018

Japan VA U.S. VA

-50%

-30%

Nu

mb

er

of

VA

co

ntr

ac

ts, in

th

ou

sa

nd

s

Projected1 Actual

1. Assumed 2012 organic attrition rate , exclusive of in-force management initiatives, and based on projected mortality, annuitization and surrender rates at Dec. 31, 2012.

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Effectively Manage and Reduce the Size and Risk of Talcott

7

Three key levers:

Manage

and reduce

size and risk

of

Talcott

• Third party transactions, at

reasonable terms

• Robust risk management and

hedge program

• In-force management initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

8

Agenda

U.S. VA Overview

Talcott Today

Japan VA Overview

Expanded Japan Hedging

U.S. In-Force Management Initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

9

Japan VA Primarily Comprised of Return of Premium Guarantees

$26.9 Billion as of Mar. 31, 2013

9

Japan VA Account Value

By Type of Guarantee

• 100% of guaranteed minimum income

benefit (GMIB) guarantees are return of

initial premium

– Payout over the annuitization period, not

lump sum

• 82% of guaranteed minimum death

benefit (GMDB) guarantees are return

of initial premium

GMIB & GMDB

$22.4 (83%)

GMDB Only

$1.8 (7%)

GMDB & Other Living Benefits

$2.7(10%)

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Account Value by Currency1

U.S. Dollar

23%

Euro

17% Yen

49%

10

Japan VA Account Value ~60% Fixed Income and ~40% Equities As of Mar 31, 2013

Account Value by Asset Type

Japan Equity

20%

Global Equity

9%

Global Equity

Hedged to Yen

13% Japan

Gov’t Bonds

16%

Global Gov’t

Bonds

42%

Other

11%

1Currency reflects the denomination of the sub-account.

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

11

Japan VA Economics Dramatically Improved Since Sept. 2012

Contracts ITM –

Average Moneyness

Retained NAR

($ in billions)

Japan GMIB – Retained NAR & Moneyness

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

$0

$1

$2

$3

$4

$5

$6

$7

3Q12 4Q12 Jan. 13 Feb. 13 Mar. 13

• Retained net amount at risk

has declined from $6.1 billion

to $1.3 billion

• The average moneyness1 of

in-the-money (ITM)2 GMIB

contracts has declined from

19% to 7%

• One-third of contracts are

out-of-the-money (OTM)2,

compared with 98% ITM at

Sept. 30, 2012

(IT

M)/

OT

M

1. For contracts that are in–the-money, percentage by which the average contract is in –the-money

2. In-the-money contracts have an account value that is less than its guaranteed value, at a point in time. Out-of the money contracts have an account value greater than the guaranteed value, at a point in time.

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Japan Surrenders Rose Sharply in 1Q13 as Moneyness Improved;

Majority of Block Beyond Surrender Charge Period

12

• 1Q13 annualized surrender

rate of 10%

• 68% of the GMIB block beyond

surrender charge period as of

Mar. 31, 2013 – 80% expected at year-end 2013

Japan GMIB – Annualized Surrender Rate

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q1 Q2 Q3 Q4 J F M

2012 2013

4%

11%

14%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

13

Agenda

U.S. VA Overview

Talcott Today

Japan VA Overview

Expanded Japan Hedging

U.S. In-Force Management Initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

14

Effectively Manage and Reduce the Size and Risk of Talcott

Three key levers

Manage

and reduce

size and risk

of

Talcott

• Third party transactions, at

reasonable terms

• Robust risk management and

hedge program

• In-force management initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Expanded Japan Hedging Effectively Eliminates

Equity and Foreign Exchange Risk

• Japan VA hedges now effectively eliminates equity and foreign exchange (FX)

risk

• Hedging strategy, coupled with current moneyness levels, significantly offsets

risk in Japan VA GMIB guarantees

• Expanded hedging program intended to preserve improved economics

• Talcott now capital self-sufficient

15

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Expanded Japan Hedge Meaningfully Reduces Surplus Volatility

16

Cumulative Impact to Surplus From Japan VA, Including Hedge

2013 through 2014 ($ in millions, before tax)

Based on cumulative 2013-2014 impact to surplus, including the HLIKK legal entity

$150

($1780)

($140)

$40

Before Expanded Hedging After Expanded Hedging

Base Scenario Stress Scenario

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Why Now? Limited Upside to Japan’s Economic Value Remains

• Much of the improvement in

economic value has already

occurred

• As favorable markets drive

account values above the

guaranteed values, the company

derives less marginal economic

value

• Expanded hedging will effectively

eliminate adverse impact of stress

market scenarios

– Will also increase hedging

costs, thereby eliminating

expected gross profits Declining Markets Improving Markets

Ma

rke

t C

on

sis

ten

t V

alu

e,

Ex

clu

din

g H

ed

gin

g Today’s

market

17

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Why Now? Because ITM Account Values Can Fund Future Payout

18

• For ITM accounts, GMIB account

value is 93% of guaranteed future

payout, as of Mar. 31, 2013

• To fully fund the guarantee, the

portfolio needs a 1% average

annual return during the 10 to 15

year payout phase

As of Mar. 31, 2013

($ in billions)

$14.6

$15.7

$14

$15

$16

ITM GMIB Account Value GMIB Guaranteed Payout

Over 10-15 year payout

period

Represents in-the-money contracts

~100 bp return/yr

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

$0.3

$4.0

$6.8

$2.3 $2.6

$1.3

$0.6 $1.1

$2.4

$1.0

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022+

Ma

rch

31

, 2

01

3

Ac

co

un

t V

alu

e

Capital Released as Contracts Annuitize or Surrender in Future

Annuitization eligibility assumes no surrenders and no deaths after March 31, 2013

19

GMIB Account Value by Year of Initial Annuitization Eligibility

As of Mar. 31, 2013

($ in billions)

• 50% of block eligible for

annuitization in next 3 years

– Expect 50-60% annuitization rates

for contracts 0-10% in the money in

the first year

– 20% expected in each year

thereafter

• If markets continue to rise,

surrender rates likely to increase

and annuitizations to decline

• Death benefit claims will be

funded by reserves

50% of AV

Average

Moneyness

(ITM)/OTM 8.2% 3.3% (2.0%) (8.1%) (10.8%) (1.8%) 4.4% (7.7%) (8.4%) (5.3%)

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Agenda

U.S. VA Overview

Talcott Today

Japan VA Overview

Expanded Japan Hedging

U.S. In-Force Management Initiatives

20

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

21

*Total Account Value = Separate Account + General Account

$65.5 Billion of Account Value as of Mar. 31, 2013

U.S. VA: GMDB Guarantee by Type

U.S. GMDB Is Significantly Reinsured

Gross NAR Retained NAR

$5.4

$1.5

($ in billions)

72% of

GMDB

NAR is

reinsured

$15.0 (23%)

$20.1 (31%)

$25.0 (38%)

$3.2 (5%)

$2.2 (3%)

Resets Return on Premium Rollups Capped Step Ups Full Step Ups

($ in billions)

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

22

*Total Account Value = Separate Account + General Account

• 66% of the Non-Lifetime guaranteed

minimum withdrawal benefit (GMWB)

NAR is covered by reinsurance with

third parties; the balance is covered

by dynamic hedging

– 37% by traditional reinsurance

– 29% by capital markets reinsurance

• Lifetime GMWB risks are managed

through U.S. Macro Hedge program

$65.5 Billion of Account Value as of Mar. 31, 2013

U.S. VA: Living Benefits by Type

No Living

Benefit

$31.4 (48%)

Non-Lifetime

GMWB

$21.2 (32%)

LifetimeWB

w/Caps

$10.2 (16%)

Uncapped

LifetimeWB

$2.7 (4%)

52% of U.S. VA Has Living Benefit Guarantee

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Contracts ITM –

Average Moneyness

Retained NAR

($ in billions)

(IT

M)/

OT

M

23

Almost 90% of U.S. VA Contracts are Above Guaranteed Values

U.S. GMWB – Retained NAR & Moneyness

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13

• Since Sept. 2011, retained

GMWB NAR has improved

from $2.5 billion to $0.3 billion

• At Mar. 31, 2013:

– 89% of contracts are OTM

– Of the 11% of contracts ITM,

average moneyness is 9%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

24

U.S. Surrender Rate Rose in 1Q13, Including

Enhanced Surrender Value Offer

• 65% of GMWB contracts were

beyond the surrender charge

period at Mar. 31, 2013

– 73% expected at year-end 2013

• U.S. GMWB policyholder

behavior has closely tracked

our assumptions

Annualized Surrender Rate on U.S. GMWB

0%

5%

10%

15%

20%

25%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Total Surrender Rate Total Surrender Rate Excluding ESV

2011 2012 2013

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

25

Agenda

U.S. VA Overview

Talcott Today

Japan VA Overview

Expanded Japan Hedging

U.S. In-Force Management Initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Effectively Manage and Reduce the Size and Risk of Talcott

26

Three key levers

Manage

and reduce

size and risk

of

Talcott

• Third party transactions, at

reasonable terms

• Robust risk management and

hedge program

• In-force management initiatives

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

In-Force Management Initiatives Reduce Size and Risk of U.S. VA

• Communications with distributors and contractholders

• Development and implementation of May 2013 product initiatives – Increases to certain rider fees and restrictions to asset allocations

• Enhanced Surrender Value1 (ESV) offer targeted at Lifetime Income contractholders – Block represents 8% of U.S. VA account value, but 52% of retained GMWB NAR

27

1. ESV offered by Hartford Life and Annuity Company and Hartford Life Insurance Company

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

$60,000

$80,000

Account Value Enhanced Surrender Value

ESV Provides Attractive Surrender Value While Accelerating

Runoff of Most Capital Intensive U.S. VA Block

28

Original Contract Terms1 Illustrative ESV Offer2

1. Illustrative example assumes $100,000 payment base, with current account value of $60,000 and $2,000 surrender charge.

2. Illustrative example assumes $100,000 payment base. Under the ESV, the surrender charge is waived, and the contractholder is eligible to receive current account value plus 20% of the payment base; up to 90% of

the payment base. In some circumstances contract holders would only receive a waiver of surrender charges and other fees. See the annuity product prospectus for other illustrative examples.

$60,000 $58,000

Account Value Original Surrender Value

$100,000 Payment Base $100,000 Payment Base

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

29

ESV Acceptance Rate To Date Above Initial Expectations

Phase1

Cumulative

Acceptance Rate

To Date2 Mailing Date

Number of

Eligible Policies

Amount of Eligible

Account Value ($ in billions)

1 22% February 1, 2013 20,500 $2.2

2 12% March 1, 2013 14,000 $1.5

3 NA April 1, 2013 4,500 $0.4

1. Offers to contract holders were made in phases, based on state regulatory approvals

2. As of April 5, 2013

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Today’s Key Takeaways

30

● We are managing Talcott Resolution to reduce risk while

maximizing shareholder value Shareholder Value

Manageable Risk

Reduced Market

Exposure

Accelerating Runoff

● The terms of our VA guarantees are comparatively modest

and their risk is manageable

● We expanded Japan VA hedging to effectively eliminate

equity and FX risk

● We are focused on U.S. in-force management initiatives to

accelerate the runoff and reduce the risk of the VA block

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Bob Rupp, Executive Vice President and Chief Risk Officer

1

Risk Management and Hedging

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

U.S. GMWB Hedge Program

U.S. Macro Hedge Program

Japan Hedge Program

2

Agenda

Hedging Programs Overview

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

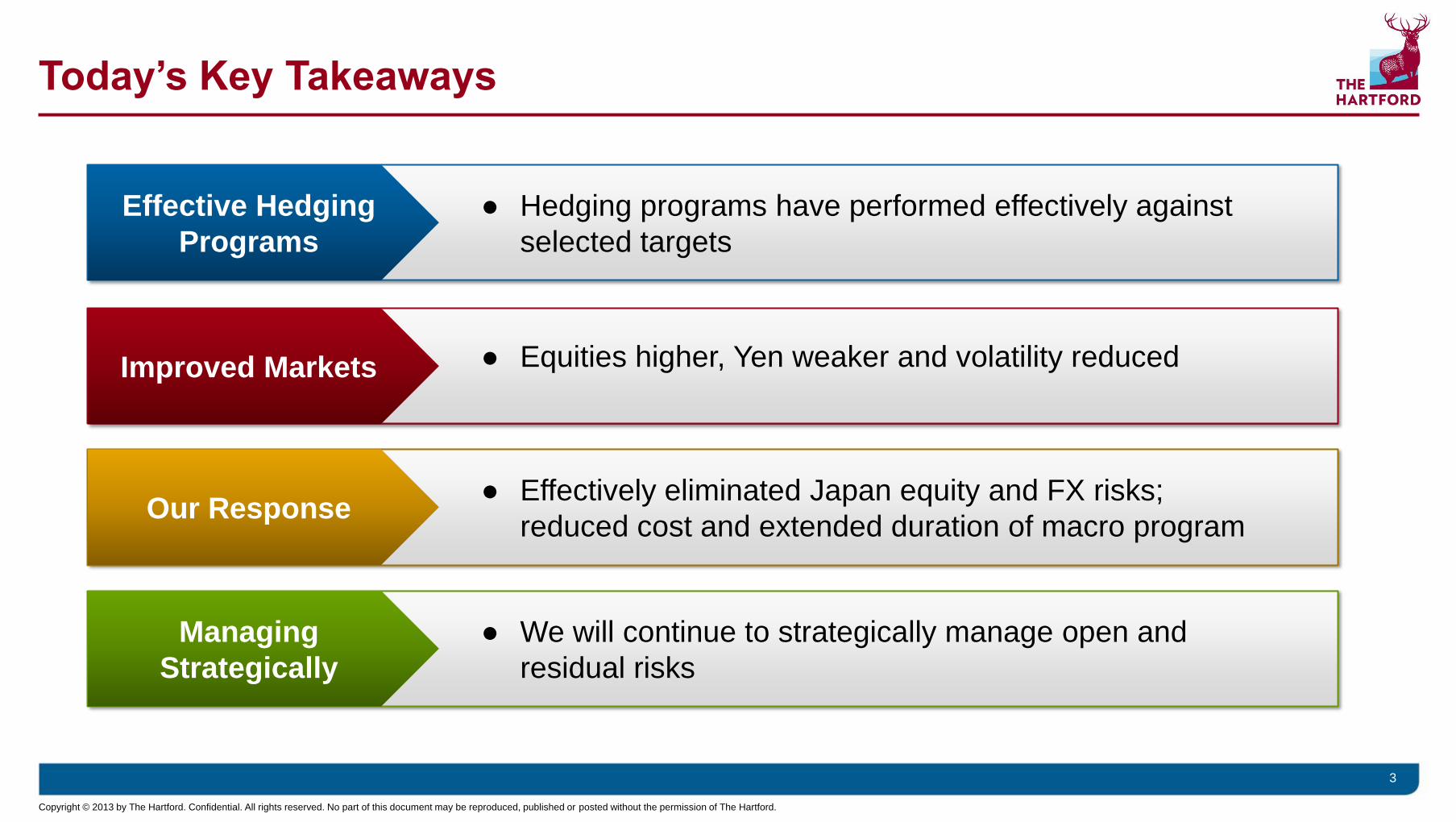

Today’s Key Takeaways

● Hedging programs have performed effectively against

selected targets

3

● Equities higher, Yen weaker and volatility reduced

● Effectively eliminated Japan equity and FX risks;

reduced cost and extended duration of macro program

● We will continue to strategically manage open and

residual risks

Effective Hedging

Programs

Improved Markets

Our Response

Managing

Strategically

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

4

Our Risks Are Covered by Comprehensive

and Effective Hedging Programs

U.S. 69%

UK 2%

Japan 29%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

5

Hedging Programs Target Primary Market Risks and

Strategically Manage Residual Risks

Targeted Risks Residual Risks

Equity Interest Rates

Foreign Exchange

U.S.

Japan

Europe

U.S.

Japan

Europe

Dollar/Yen

Euro/Yen

Pound/Yen

• Policyholder

Behavior

• Volatility

• Basis Risk

• Cross Greeks

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

U.S. GMWB Hedge Program • Overview

• Results

U.S. Macro Hedge Program

Japan Hedge Program

6

Agenda

Hedging Programs Overview

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

7

A Decade of Experience Hedging U.S. GMWB

• Target: Full hedge of

FAS 157/133 liability which is

correlated to economics

• Dynamically managed

Targeted Risks Program

• Instituted in 2003

• 52% of U.S. VA account

value includes withdrawal

benefit guarantees

• GAAP sensitivity largely

driven by residual risks

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

1 Risks reflected in target liability include equities, interest rates, and equity volatility (per FAS 157/133 calculation)

8

U.S. GMWB Hedges Have Been Effective Against Targets

Change in Hedge Target Liability1 Change in Hedge Assets

Change in Value of Hedge Asset and Target Liability

Ab

so

lute

Valu

e o

f C

han

ge (

$ i

n m

illi

on

s)

$0

$100

$200

$300

$400

$500

$600

$700

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

U.S. GMWB Hedge Program

U.S. Macro Hedge Program • Overview

• Program Enhancements

Japan Hedge Program

9

Agenda

Hedging Programs Overview

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

10

U.S. Macro Hedge Protects Statutory Surplus in Stress Scenarios

• Targets equity tail risk

• More static approach

• Protects statutory surplus in

stress scenarios

Targeted Risks Program

• Instituted in 2009

• Primarily options-based

coverage focused on GMDB

and other risks

• GAAP sensitivity includes

change in hedge assets only

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

10

13

16

19

22

25

1200

1300

1400

1500

1600

SPX Index VIX Index

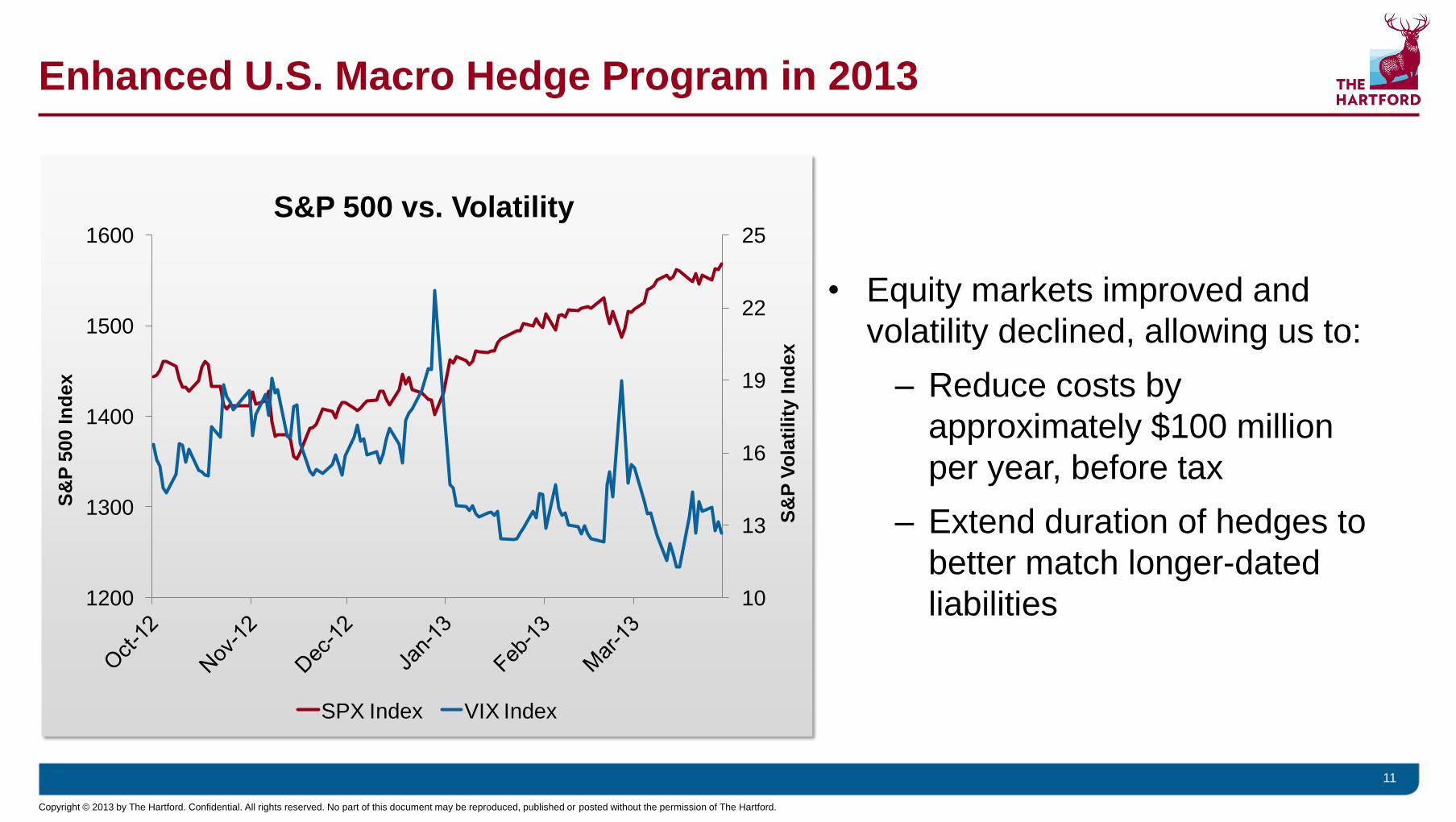

Enhanced U.S. Macro Hedge Program in 2013

11

S&P 500 vs. Volatility

• Equity markets improved and

volatility declined, allowing us to:

– Reduce costs by

approximately $100 million

per year, before tax

– Extend duration of hedges to

better match longer-dated

liabilities

S&

P 5

00 I

nd

ex

S&

P V

ola

tili

ty I

nd

ex

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

U.S. GMWB Hedge Program

U.S. Macro Hedge Program

Japan Hedge Program • Overview

• Results

• Market Developments

• Program Enhancements

Agenda

Hedging Programs Overview

12

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

13

Japan Hedge Program Targets “Tail” in VA Block

• Global equity, interest rates,

and FX

• Expanded program to

effectively eliminate equity

and FX risk in early 2013

• Dynamically managed

Targeted Risks Program

• Instituted in 2011

• Tail approach: designed to

increase/decrease hedge

target in response to market

movements

• GAAP sensitivity includes

change in hedge assets only

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Eco

no

mic

Valu

e o

f L

iab

ilit

y

Hedge

Coverage

• The Hartford’s economic value of the VA

liability changes with market movements

driven by equity, FX and interest rates

14

Japan Tail Hedge Program Dynamically

Responds to Market Movements

Declining Markets Improving Markets

Perc

en

t o

f L

iab

ilit

y H

ed

ged

100%

0%

• Tail hedge program accelerates hedge

protection in declining markets

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

15

Japan Tail Hedge Has Been Effective Against Target

Change in Hedge Target Liability1 Change in Hedge Assets

Ab

so

lute

Valu

e o

f C

han

ge (

$ i

n m

illi

on

s)

Change in Value of Hedge Assets and Target Liability

$0

$500

$1,000

$1,500

$2,000

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

1 Risks reflected in target liability include Japan tail claims from foreign currency, equities and interest rates

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

600

700

800

900

1000

1100

1200

1300

1400

1500

1600

1700

16

Market Developments:

Equity Markets Have Improved

SPX Index: +25%

1258

1569

Topix: +42%

1035

729

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Economic

Liability

Hedge

Coverage

17

Transitioned to Full Dynamic Hedging of Equity Risk

Hedge

Coverage

Declining Markets Improving Markets

Pe

rce

nt

of

Lia

bilit

y H

ed

ge

d

100%

0%

Tail Hedge Program Full Dynamic Hedging

Declining Markets Improving Markets

Pe

rce

nt

of

Lia

bilit

y H

ed

ge

d

100%

0%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

70

75

80

85

90

95

100

80

90

100

110

120

130

140

Market Developments:

Yen Has Weakened

18

USD/JPY Currency: +23%

76.9

94.2 Euro/JPY Currency: +21%

99.7

120.8

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

19

Transitioned to Full Dynamic Hedging of FX Risk

Economic

Liability

Hedge

Coverage Hedge

Coverage

Declining Markets Improving Markets

Pe

rce

nt

of

Lia

bilit

y H

ed

ge

d

100%

0%

Tail Hedge Program Full Dynamic Hedging

Declining Markets Improving Markets

Pe

rce

nt

of

Lia

bilit

y H

ed

ge

d

100%

0%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

0

1

2

3

0

0.5

1

1.5

Market Developments:

Interest Rates At or Near Historically Low Levels

20

Japan Rates: -30bps

0.7%

1.0%

U.S. Rates: -2bps

2.0% 2.0%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

21

Tail Hedge Program Remains in Place for Interest Rates

Hedge

Coverage

Declining Markets Improving Markets

Pe

rce

nt

of

Lia

bilit

y H

ed

ge

d

100%

0%

Tail Hedge Program

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Risk Mitigation After Risk Mitigation Before

22

Japan Equity and FX Risks Now Effectively Eliminated

Strategically

Managed Tail Full

Equity

Foreign Exchange

Interest Rates

Residual Risk

Strategically

Managed Tail Full

Equity

Foreign Exchange

Interest Rates

Residual Risk

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

23

Today’s Key Takeaways

● Hedging programs have performed effectively against

selected targets

● Equities higher, Yen weaker and volatility reduced

● Effectively eliminated Japan equity and FX risks;

reduced cost and extended duration of macro program

● We will continue to strategically manage open and

residual risks

Effective Hedging

Programs

Improved Markets

Our Response

Managing

Strategically

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

1

Chris Swift, Executive Vice President and Chief Financial Officer

VA Metrics and Capital Margins

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Agenda

VA Market Consistent Value (MCV) and cash flows

Capital margins and capital generation

First quarter 2013 actions and updates

2

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Today’s Key Takeaways

3

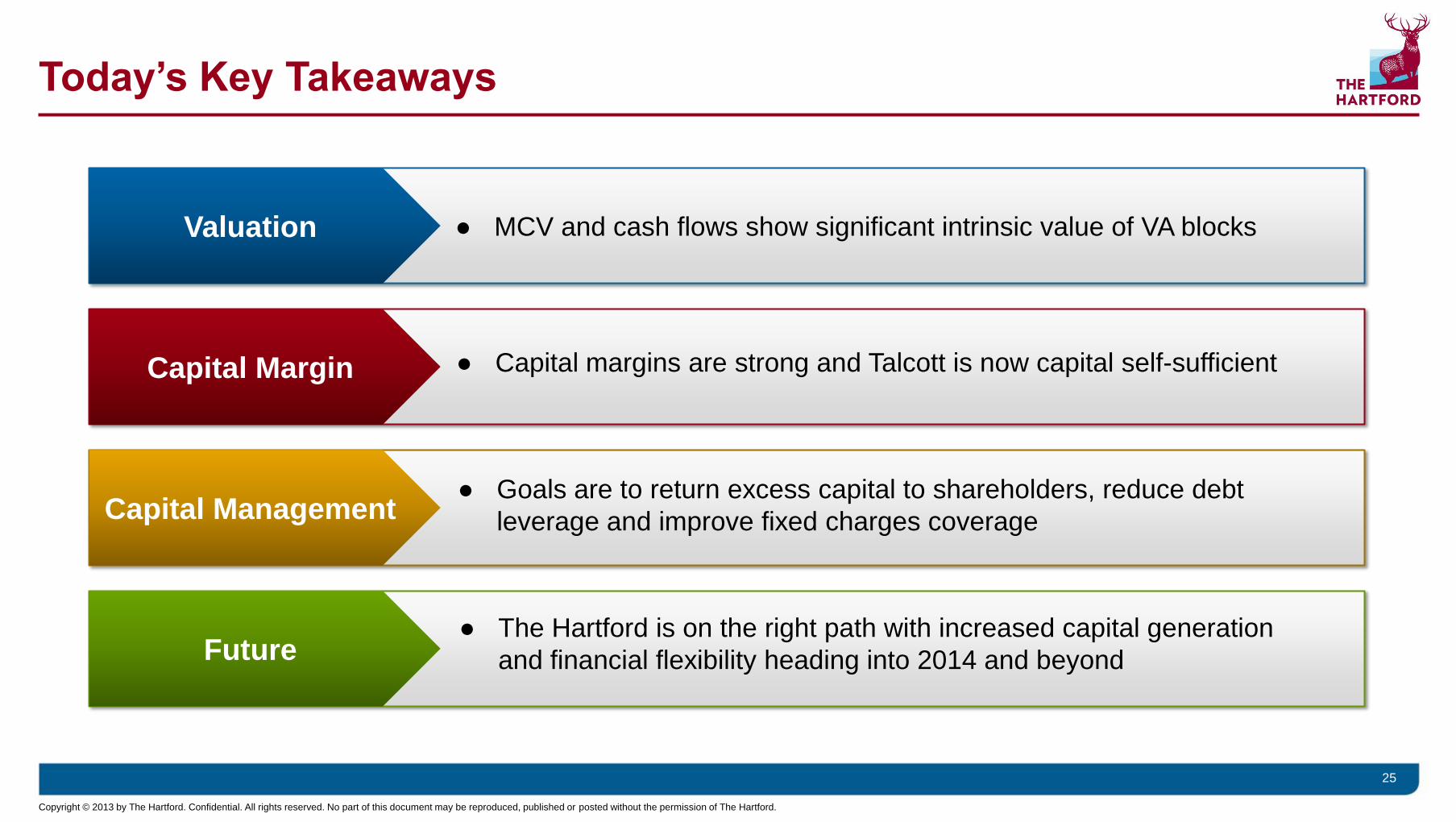

Valuation

Capital Margin

Capital Management

Future

● MCV and cash flows show significant intrinsic value of VA blocks

● Capital margins are strong and Talcott is now capital self-sufficient

● Goals are to return excess capital to shareholders, reduce debt

leverage and improve fixed charges coverage

● The Hartford is on the right path with increased capital generation

and financial flexibility heading into 2014 and beyond

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Significant 1Q13 Capital Activities

• $800 million debt tender closed in March – Reduced annual interest expense by $51 million, before

tax

• Repurchased $58 million of common shares and

warrants ($55 million shares, $3 million warrants)

through April 5, 2013

• Capital plan targets $1 billion net debt reduction in

2013-2014, inclusive of 1Q13 activity

• 2012 earnings to fixed charges coverage ratio2

improved from 4.0x to 4.8x pro forma

4

$7.1

$6.3

Dec. 31, 2012 Dec. 31, 2012 Pro Forma

4.0x

4.8x

2012 2012 Pro Forma

1 Dec. 31, 2012 pro forma for $800 million of debt purchased in March 2013 debt tender and conversion of the mandatory convertible preferred

2 Core earnings and core earnings before interest and taxes to fixed charges coverage ratio are non-GAAP financial measures. For definition and reconciliation, please see appendix.

.

Total Debt ($ in billions)

Core Earnings Before Interest and Taxes

To Fixed Charges Coverage2

1

1

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Updated 2013 Outlook

• 2013 core earnings outlook updated to $1.45 billion to $1.55 billion

– Reflects $75 million increase in Talcott core earnings due to elimination of Japan VA DAC

amortization expense beginning in the second quarter of 2013

– No other changes

• 1Q13 net income results to include charges for:

– $600 million, after tax, for Japan VA DAC write-off

– $140 million, after tax, for extinguishment of debt

• 1Q13 catastrophe losses estimated at $22 million, after-tax, $35 million lower than

prior 1Q13 outlook of $57 million

• 1Q13 results will be released on April 29th

5

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Agenda

VA MCV and cash flows

Capital margins and capital generation

First quarter 2013 actions and updates

6

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

MCV

Cash Flows

• MCV is a better metric of economic value for VA liabilities – MCV is the basis of our hedging programs

7

VA MCV and Cash Flows Show Significant Intrinsic Value

MCV Value • MCV VA liability estimated at $500 million at Mar. 31, 2013

• Cash flows of our VA block indicate significant intrinsic value

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

What is Market Consistent Value (MCV)?

• MCV1 is similar to FAS 133/157 fair value for

GMWB accounting but applied to all VA

guarantees, including guarantee benefit riders

and base contract fees

• MCV does not reflect the price a buyer would

pay or receive for the block

• Does not include investment income on capital

or risk premiums for cost of capital

8

What is Included in Calculation of MCV?

Average of present value of cash flows from

>5,000 stochastic scenarios

Fees, claims and expense cash flows

Current observed market price inputs for

interest rates, FX, equity markets, volatility, etc.

Reflects present value of expected cash flows based on market consistent assumptions

1. The Hartford uses Market Consistent Value (MCV) as a measure of the risk and economic value of

its run-off variable annuity block. MCV may differ from financial metrics used by other companies to

measure the risk and value of an existing variable annuity block. Accordingly, investors should be

careful when comparing MCV to similar measures used by other companies. For more information on

MCV, please see the appendix to this presentation.

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

MCV Is a Better Measure of Economic Value

• MCV is a better measure of economic value

than either GAAP or statutory accounting

– Fair value metric using current market inputs

– Values all VA fees, benefits and expenses

• Is used as the basis for our hedging programs

• March 31, 2013 MCV of U.S. and Japan VA

liability estimated at $500 million, before tax

9

Market Consistent

Value ($ in billions)

Mar. 2013E

Asset (Liability)

U.S. $0.7

Japan (1.2)

Total ($0.5)

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Conversion of MCV to Statutory

($ in billions)

Mar. 2013E

MCV

Asset

(Liability)

A

Mar. 2013E

Statutory

Reserves2,3

B

Difference

(Before Tax)

A – B

U.S. $0.7 ($0.6) $1.3

Japan (1.2) (1.6) 0.4

Total ($0.5) ($2.2) $1.7

Conversion of MCV to GAAP

($ in billions)

Mar. 2013E

MCV

Asset

(Liability)

A

Mar. 2013E

GAAP1

Equivalent

Value

(Liability)2,

B

Difference

(Before Tax)

A – B

U.S. $0.7 $0.9 $(0.2)

Japan (1.2) (0.5) (0.7)

Total ($0.5) $0.4 ($0.9)

Comparison of MCV To GAAP and Statutory Reserves

10

Converting estimated statutory reserves

at Mar. 31, 2013 to an MCV basis implies

that statutory surplus would increase by

$1.7 billion, before tax

Converting estimated GAAP reserves,

net of DAC, at Mar. 31, 2013

to an MCV basis implies that

GAAP equity would be reduced by

$900 million, before tax

1. GAAP equivalent carrying value is FAS 157 & SOP 03-1 reserves, net DAC and reinsurance recoverable.

2. Liabilities are negative; assets are positive.

3. Statutory reserves are preliminary and include $800 million in HLIKK contingency reserves

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Three Scenarios Used for Cash Flow and

Capital Margin Projections

11

Dec. 31, 2013 Market Level By Scenario

Market Factor Base

Scenario

Favorable

Scenario

Stress

Scenario

March 31, 2013

Actual

S&P 500 1553 1650 900 1569

10 Year Treasury 1.99% 2.26% 1.25% 1.85%

Yen/$ 91.7 100.0 70.0 94.2

10 Year JGB1 0.75% 0.93% 0.60% 0.55%

Detailed assumptions for base, favorable and stress scenarios are provided in appendix

1. Japanese Government Bond (JGB)

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Net Present Value of Cash Flows Include VA Fees, Claims,

Expenses and Hedge Gains (Losses)

12

What is Included in Cash Flows?

Present Value (PV) of cash flows for one scenario with explicit assumptions for: • Interest rates

• Equity returns

• FX

• Volatility

• Dynamic policyholder behavior

Base contract fees and all rider fees, claims, and expenses

Liability cash flows only; no investment income on capital backing block

Modeled hedge gains and losses

Discounted at swap rates

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Base Scenario ($ in billions, Jan. 31, 2013)

Cas

h F

low

s

Cumulative Cash Flow Summary ($ in billions) U.S. Japan Total

PV of fees and expenses $4.4 $2.8 $7.1

PV of claims (0.8) (1.3) (2.0)

PV of net cumulative cash flows, before tax $3.6 $1.5 $5.1

PV of hedge gains (losses) (1.6) (2.0) (3.6)

PV of cumulative cash flow, before tax $2.0 $(0.5) $1.5

Base Scenario VA Cash Flows Are Positive

$1.5 Billion, Net of Hedges

13

• PV of cumulative cash flows from

U.S. and Japan blocks total $1.5

billion, before tax

• U.S. VA cash flows are positive,

with fees exceeding claims,

expenses and hedge losses by

$2.0 billion

• Japan cash flows are negative

$0.5 billion, including hedge

losses

-0.5

-0.3

-0.1

0.1

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Fees & Exp. Claims

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Positive Total Net Cash Flows in Favorable and Stress Scenarios

14

($ in billions)

U.S. Japan Total

Favorable Stress Favorable Stress Favorable Stress

PV of fees and expenses $4.6 $3.3 $3.0 $1.9 $7.6 $5.2

PV of claims (0.7) (3.3) (0.6) (7.0) (1.2) (10.3)

PV of net cumulative cash flows,

before tax1 $4.0 $(0.0) $2.4 $(5.1) $6.3 $(5.1)

PV of hedge gains (losses) (1.7) 0.6 (2.4) 5.1 (4.1) 5.7

PV of Cumulative cash

flow, before tax1 $2.3 $0.6 $0.0 $0.0 $2.3 $0.6

Cumulative net PV of VA cash flows are $0.6 billion positive in the stress scenario and $2.3

billion positive in the favorable scenario

1. Totals may not add up due to rounding

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

MCV

Cash Flows

• MCV is a better metric of economic value for VA liabilities – MCV is the basis of our hedging programs

15

VA MCV and Cash Flows Show Significant Intrinsic Value

MCV Value • MCV VA liability estimated at $500 million at Mar. 31, 2013

• Cash flows of our VA block indicate significant intrinsic value

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Agenda

VA MCV and cash flows

Capital margins and capital generation

First quarter 2013 actions and updates

16

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Principles

Goals

Capital Management Goals: Return Excess Capital to Shareholders and

Reduce Debt Leverage, Improve Fixed Charges Coverage

17

• Executing announced capital management plan

• Develop next phase of capital management plan Short term:

Future:

• Return excess capital to shareholders

• Reduce debt leverage to low 20s%; improve earnings1

to fixed charges coverage to 5x to 6x

• Capital sufficient to support and grow businesses and maintain

current ratings

• Talcott to remain capital self-sufficient

• Holding company resources support interest, dividends and capital

management

1. Core earnings before interest and taxes. See appendix for calculation.

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Beginning 2013 with Strong Capital Margin

• 2012 pro forma capital margin1 of $4.9 billion – Before capital management plan announced in Feb.

2013

• Pro forma risk-based capital (RBC) ratios remain

strong

– Hartford Life & Accident consolidated RBC ratio

remains strong, in excess of 400%

– White River Re RBC in excess of 150%

• P&C capital margin remains strong, despite the

impact of 2012 catastrophe losses and low

interest rates

18

$2.5B

$4.9B

2012 Actual 2012 Pro Forma 2

Capital Margin1 In Base Scenario ($ in billions)

1 Capital margin measured against an enterprise aggregate minimum to reflect U.S. Life Company Action Level RBC of 325%, White River Re Company Action Level RBC of 125%, and P&C capital

consistent with “AA” FSR. 2 2012 pro forma for sales of Individual Life and Retirement Plans and before impact of announced capital management plan.

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

~60% of Statutory Capital Allocated to Go Forward Businesses;

~40% Allocated to Talcott

The Hartford (NYSE:HIG)

Hartford Fire

Hartford Holdings

Mutual Funds

Hartford Life Inc.

Hartford Life & Accident

Hartford Life Ins. Co.

Hartford Life & Annuity

HLIKK (Japan)

White River Re

Talcott

Go Forward

$7.7

$1.5

$2.2

$1.4

$2.6

P&C

Group Benefits

International VA

U.S VA

Talcott Non-VA

2

3

$15.4 billion Total U.S. & Japan

Statutory Capital

Holding Co.

1 Pro forma for the impact of the sales of the Individual Life and Retirement Plans businesses closed in Jan. 2013 and after the $1.5

billion dividend to the holding company

2 Includes $1.1 billion in HLIKK and $0.7 billion in Hartford Life Limited.

3 Includes approximately $450 million of statutory capital related to reinsurance recoverables from sale of Individual Life and

Retirement Plans.

Statutory Capital Allocation

as of Dec. 31, 2012, Pro Forma1

($ in billions)

Graphic is a simplified

version of The Hartford’s

organizational structure

for illustrative purposes.

19

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

2013 Capital Margin Scenarios Compared to 2011

• Business sales and changes – Individual Life and Retirement Plans sold

– U.S. VA in runoff

– Smaller VA block

– Expanded VA hedging

• Market levels – Improved for FX and equities

– Interest rates lower

• Assumption changes: – U.S. equity return, including dividends, reduced

from 9% to 6%

– Japan equity return reduced from 8% to 6%

– S&P 500 shocked to 900 in 2013 stress

scenario; was 800 in 2011

20

Key Market

Assumptions

2011

Base

Scenario At Dec. 31, 2011

2013

Base

Scenario At Dec. 31, 2013

S&P 500 1240 1553

10 Yr. Treasury 2.30% 1.99%

Yen/$ 76.7 91.7

10 Year JGB 1.07% 0.75%

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Talcott operations in aggregate are capital self-sufficient

Base

Scenario (S&P 1553)

Favorable

Scenario (S&P 1650)

Stress

Scenario (S&P 900)

December 2014 $5.5 $6.1 $2.2

Capital Margins Strong In Base, Favorable and Stress Scenarios

21

1 Capital margins measured against an enterprise aggregate minimum to reflect U.S. Life Company Action Level RBC of 325%, White River Re Company Action Level RBC of 125%,

and P&C capital consistent with “AA” FSR

Capital margins in 2014 are net of Feb. 2013 announced capital management plan

Projected Capital Margins1 from Scenarios

($ in billions)

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

($ in billions)

Favorable

Scenario (S&P 1650)

Stress

Scenario (S&P 900)

Projected Dec. 2014

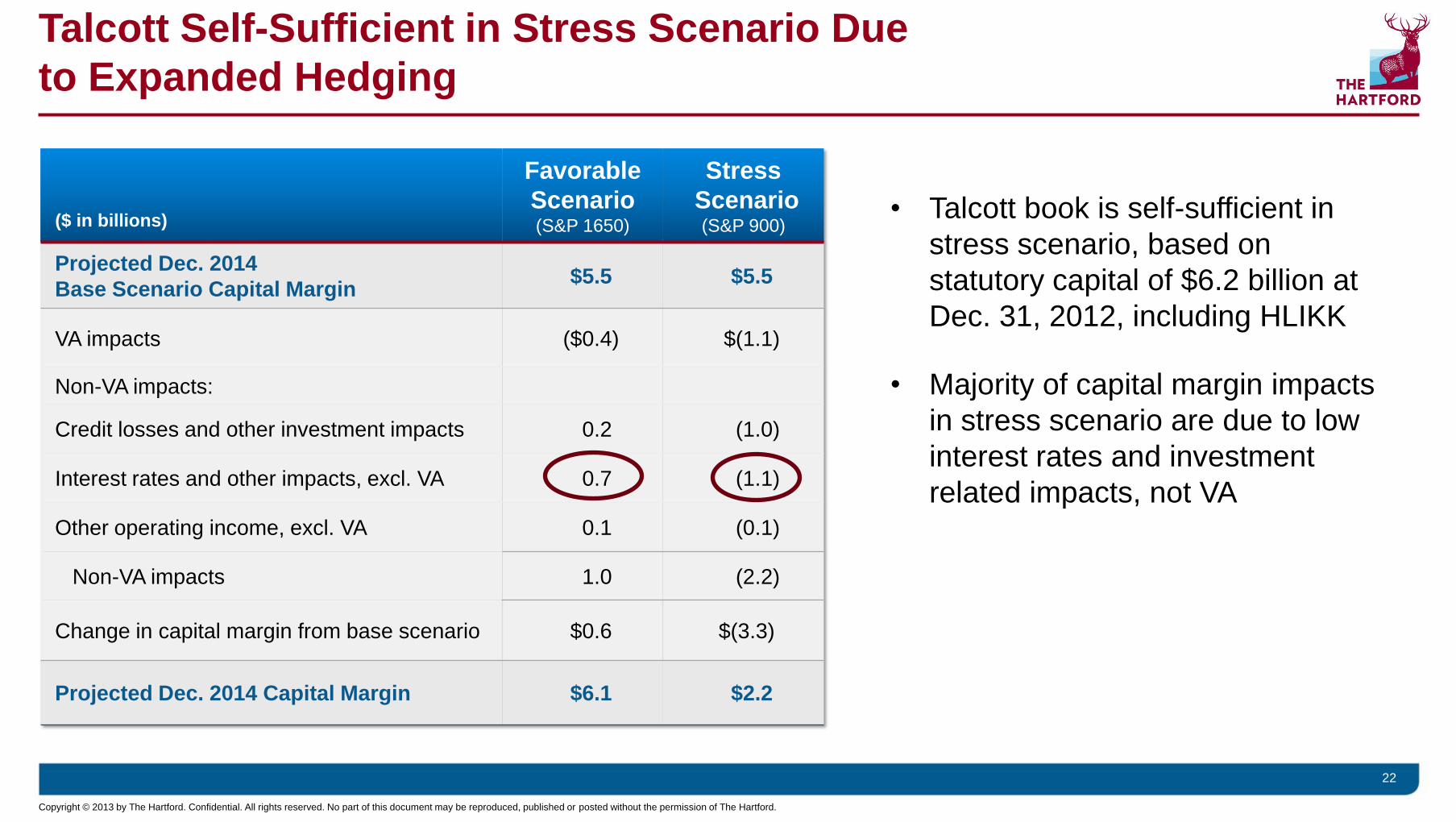

Base Scenario Capital Margin $5.5 $5.5

VA impacts ($0.4) $(1.1)

Non-VA impacts:

Credit losses and other investment impacts 0.2 (1.0)

Interest rates and other impacts, excl. VA 0.7 (1.1)

Other operating income, excl. VA 0.1 (0.1)

Non-VA impacts 1.0 (2.2)

Change in capital margin from base scenario $0.6 $(3.3)

Projected Dec. 2014 Capital Margin $6.1 $2.2

Talcott Self-Sufficient in Stress Scenario Due

to Expanded Hedging

22

• Talcott book is self-sufficient in

stress scenario, based on

statutory capital of $6.2 billion at

Dec. 31, 2012, including HLIKK

• Majority of capital margin impacts

in stress scenario are due to low

interest rates and investment

related impacts, not VA

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Talcott Capital

Self-Sufficient

Improved

Capital

Generation

Capital

Management

Improved Capital Generation Expected in 2014 and Beyond

• Talcott now capital self-sufficient

– Declining in-the-moneyness of the VA block and reduction in size of block will

reduce required capital over time

23

• Heading into 2014, capital flexibility provides opportunities for

additional actions

• Expect improved statutory capital generation from

go forward businesses

‒ Improved margins and profitable growth increase future capital generation

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

24

Conclusion

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Today’s Key Takeaways

25

Valuation

Capital Margin

Capital Management

Future

● MCV and cash flows show significant intrinsic value of VA blocks

● Capital margins are strong and Talcott is now capital self-sufficient

● Goals are to return excess capital to shareholders, reduce debt

leverage and improve fixed charges coverage

● The Hartford is on the right path with increased capital generation

and financial flexibility heading into 2014 and beyond

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

26

Question & Answer Period

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Appendix

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Variable Annuity – Key Definitions

• Guaranteed Minimum Income Benefits (GMIB) – potential benefits associated with contract guarantee that establishes a

minimum income amount, based on return of principal, which is in excess of account value

• Guaranteed Minimum Withdrawal Benefits (GMWB) – potential benefits associated with contract guarantee that establishes a

minimum periodic withdrawal amount that would continue beyond the point where account value is reduced to zero

• Guaranteed Minimum Death Benefits (GMDB) – value of benefit provided to beneficiary(ies) in excess of account value upon

death of the contract’s covered life/lives

• In the Money (ITM) – when a contract has an account value that is less than its guaranteed value, at a point in time

• Out of the Money (OTM) – when a contract has an account value that is greater than its guaranteed value, at a point in time

• Contracts ITM – Average Moneyness – for all contracts that are in the money, percentage by which the average contract is in the

money

• Average Moneyness of Total Block – weighted average differential between guaranteed value and account value for all contracts

• Retained Net Amount at Risk (NAR) – the difference between the guarantee and the account value for all in-the-money accounts

at a point in time, net of reinsurance, but excluding hedging impacts

1

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Market Scenarios Used in Cash Flow Examples

Base Favorable Stress

Interest Rate • Held flat for 2 years

• Follows forward rates

thereafter

• Follows Forward rates • 0 – 80bps decrease across term structure

in 2013

• Flat in 2014

• Follows forwards thereafter

FX • Flat

• USD/JPY 91.7

• EUR/JPY 124.5

• Yen weakens to 100 in 2013

• USD/JPY 100.0 at YE 2013

• EUR/JPY 135.8 at YE 2013

• Flat thereafter

• Yen strengthens to 70 in 2013

• USD/JPY 70.0 at YE 2013

• EUR/JPY 95.1 at YE 2013

• Flat thereafter

Equity • 4% index growth plus 1.8%

dividend yield in all years

• S&P 1553 at YE 2013

• Nikkei 11547 at YE 2013

• Equities increase 10% in 2013

• S&P 1650 at YE 2013

• Nikkei 12268 at YE 2013

• 4% index growth plus 1.8%

dividend yield thereafter

• All indices decline 40% in 2013

• S&P 900 at YE 2013

• Nikkei 6692 at YE 2013

• 4% index growth thereafter plus 1.8%

dividend yield thereafter

Investment

Related Impact,

Before Tax

• $(200) million in 2013 and

2014

• $0 million in 2013 and 2014 • $(1,200) million in 2013 and 2014

2

Note: Market indices were established based on January 31, 2013 market levels

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Favorable Market Scenario ($ in billions, 1/31/2013)

Ca

sh

Flo

ws

Cu

mu

lati

ve

Cas

h F

low

s

Cash Flow Summary U.S. Japan Total

PV fees and expenses $4.6 $3.0 $7.6

PV of claims (0.7) (0.6) (1.2)

PV of net liabilities 4.0 2.4 6.3

PV of hedge (losses) (1.7) (2.4) (4.1)

PV of cumulative

cash flows $2.3 $0.0 $2.3

PV of Cash Flows is $2.3 Billion In Favorable Scenario

-0.5

-0.3

-0.1

0.1

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Fees & Exp. Claims

• In favorable market scenario, cash flows are

higher than base case by $0.8 billion, as

increased fees and lower expenses are offset

by higher hedge losses

• In this scenario, Japan VA cash flows are

breakeven

3

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Cas

h F

low

s

PV of Cash Flows is $0.6 Billion in Stress Scenario

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Fees & Exp. Claims

Cash Flow Summary U.S. Japan Total

PV of fees & expenses 3.3 1.9 5.2

PV claims (3.3) (7.0) (10.3)

PV net liabilities (0.0) (5.1) (5.1)

PV of hedge gains 0.6 5.1 5.7

PV of cumulative

cash flows $0.6 $0.0 $0.6

• In adverse scenario, cash flows are a positive

$0.6 billion

• U.S. is $0.6 billion but Japan is breakeven

• Hedge gains total $5.7 billion, more than

offsetting negative cash flows from contracts

Adverse Market Scenario ($ in billions, 1/31/2013)

4

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Expanded Japan Hedge Increases GAAP Volatility Due to

Asymmetric Accounting

• GAAP Impact – Impact on derivative sensitivity disclosures

Equity Market Returns -20% -10% +10%

Potential Net Fair Value

Impact $ 509 $247 ($248)

Yen Strengthens +/

Weakens - +20% +10% -10%

Potential Net Fair Value

Impact $1,131 $353 ($242)

As of 12/31/12 (Pre-tax/DAC )(1) As of 4/8/13 (Pre-tax/DAC )(2)

(1) These sensitivities are based on the following key market levels as of December 31, 2012: 1) S&P of 1,426 and FX rates of USDJPY @86.75 and EURJPY @114.46.

(2) These sensitivities are based on the following key market levels as of April 8, 2013: 1) S&P of 1,563 and FX rates of USDJPY @99.36 and EURJPY @129.26

Equity Market Returns -20% -10% +10%

Potential Net Fair Value

Impact $ 904 $456 ($489)

Yen Strengthens +/

Weakens - +20% +10% -10%

Potential Net Fair Value

Impact $1,415 $533 ($437)

5

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Non-VA Profile

Non-VA Account Value

$68.5 Billion as of Mar. 31, 2013

*Total Account Value = Separate Account + General Account

PPLI

55%

Institutional

24%

Japan Fixed

5%

U.S. Fixed

16%

PPLI

Account Value: $37.8 billion

Variable COLI and High Net Worth

Mortality exposure, mitigated by reinsurance and experience

rating

Institutional

Includes Structured Settlements, Terminal Funding,

Guaranteed Investment Products (GIPs), Consumer Notes and

The Hartford Pension Plan

Institutional Account Value: $16.4 billion

Covered Lives (in thousands) 180

Average Contract Term Duration (Years):10.9

U.S. Fixed

Fixed Annuity Account Value: $10.8 billion

Covered Lives (in thousands): 183

Average Contract Term Duration(Years):3.0

Japan Fixed

Fixed Annuity Account Value: $3.5 billion

Covered Lives (in thousands): 26

Average Contract Term Duration(Years):3.5

6

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Non-GAAP and Other Financial Measures

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Guidelines for Creating Presentations

Discussion of Non-GAAP and Other Financial Measures DISCUSSION OF NON-GAAP AND OTHER FINANCIAL MEASURES

The Hartford uses non-GAAP and other financial measures in this presentation to assist investors in analyzing the company's operating performance and financial condition for the periods presented herein.

Because The Hartford's calculation of these measures may differ from similar measures used by other companies, investors should be careful when comparing The Hartford's non-GAAP and other financial

measures to those of other companies. Definitions of the non-GAAP and other financial measures used in this presentation, and reconciliations of such non-GAAP financial measures to the most directly

comparable GAAP financial measure, can be found below. Definitions and calculations of financial measures used in this presentation can be found in The Hartford’s Investor Financial Supplement for the

fourth quarter of 2012, which is available on The Hartford’s website, http://ir.thehartford.com.

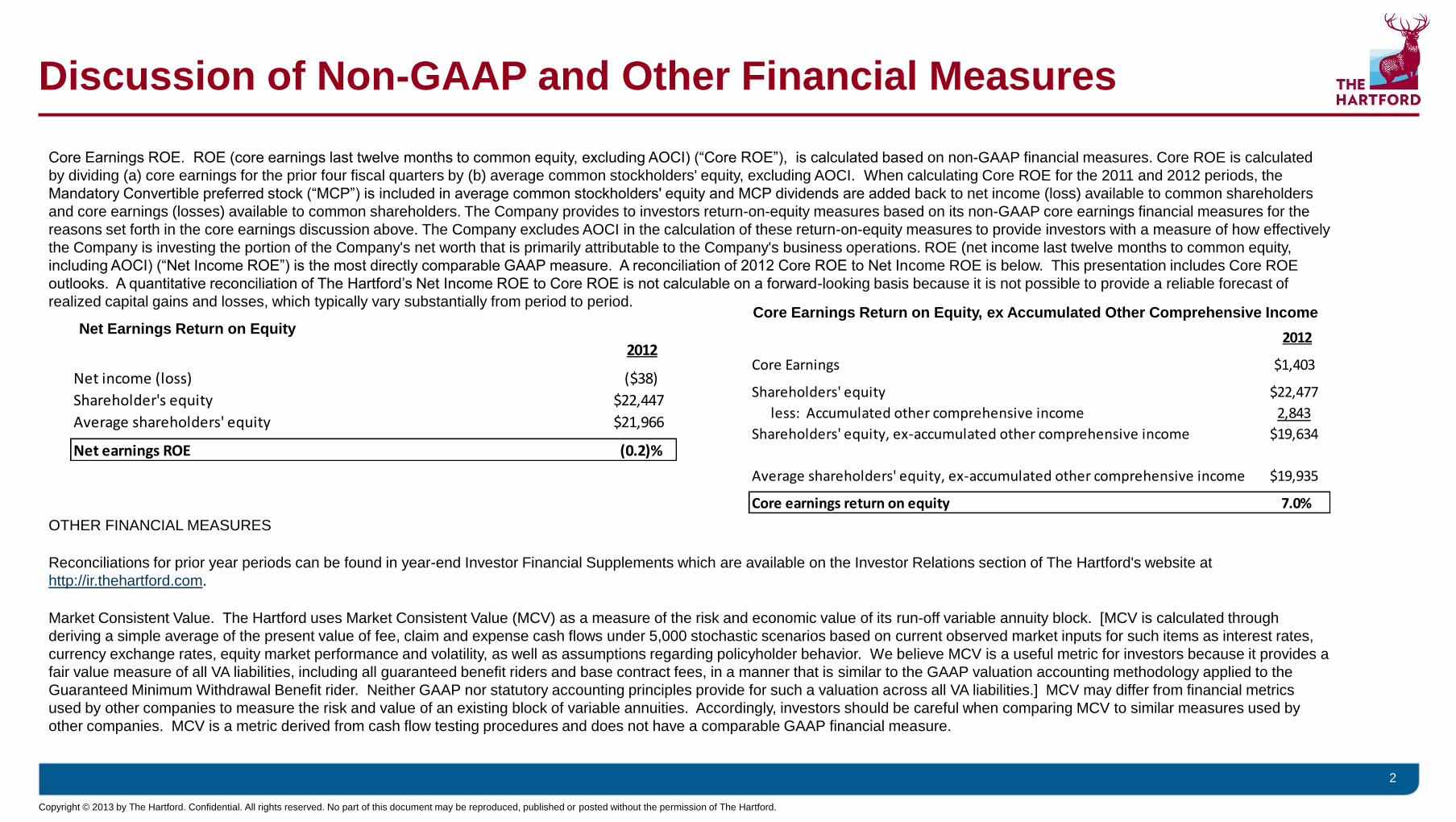

Core Earnings: The Hartford uses the non-GAAP financial measure core earnings as an important measure of the Company's operating performance. We believe that the measure core earnings provides

investors with a valuable measure of the performance of the Company's ongoing businesses because it reveals trends in our insurance and financial services businesses that may be obscured by including

the net effect of certain realized capital gains and losses, discontinued operations, loss on extinguishment of debt, gains and losses from disposal of businesses, certain restructuring charges and the impact

of Unlocks to deferred policy acquisition costs (“DAC”), sales inducement assets ("SIA"), unearned revenue reserve ("URR") and death and other insurance benefit reserve balances. Some realized capital

gains and losses are primarily driven by investment decisions and external economic developments, the nature and timing of which are unrelated to the insurance and underwriting aspects of our business.

Accordingly, core earnings excludes the effect of all realized gains and losses (after tax and the effects of DAC) that tend to be highly variable from period to period based on capital market conditions. The

Hartford believes, however, that some realized capital gains and losses are integrally related to our insurance operations, so core earnings includes net realized gains and losses such as net periodic

settlements on credit derivatives and net periodic settlements on the Japan fixed annuity cross-currency swap. These net realized gains and losses are directly related to an offsetting item included in the

income statement such as net investment income. Net income is the most directly comparable GAAP measure. Core earnings should not be considered as a substitute for net income and does not reflect the

overall profitability of the Company's business. Therefore, The Hartford believes that it is useful for investors to evaluate both net income and core earnings when reviewing the company's performance. A

reconciliation of core earnings to net income for the year ended December 31, 2012 can be found below. The 2013 earnings guidance presented in this release is based on core earnings (loss). A quantitative

reconciliation of The Hartford’s net income (loss) to core earnings (loss) is not calculable on a forward-looking basis because it is not possible to provide a reliable forecast of realized capital gains and losses,

which typically vary substantially from period to period.

($ in millions) 2012

Consolidated core earnings $1,403

Add:

Unlock impact on net income (loss) 31

Restructuring and other costs, after tax (129)

Income (loss) from discontinued operations (5)

Loss on extinguishment of debt, after tax (587)

Reinsurance loss on disposition, after tax (388)

Net realized capital gains (losses),

after tax and DAC, excluded from core earnings (363)

Net income (loss) ($38)

1

Copyright © 2013 by The Hartford. Confidential. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford.

Guidelines for Creating Presentations

Discussion of Non-GAAP and Other Financial Measures