Embed Size (px)

Citation preview

The guide for hard-to-findinformation on benefit products,services and industry data

Caremark is a leading provider of fully integrated pharmacy benefit management services, specialty pharmacy services, anddisease management programs to more than 2,000 health plansponsors nationally. We provide health management solutions

that improve health outcomes while enabling benefit plan sponsorsand plan members to maximize their healthcare investment.

If you would like additional copies of the 2005 Benefits Barometer,or prefer someone from Caremark to contact you,

please call 800.927.3727 or email us at [email protected].

The 2005 Benefits Barometer was produced by Caremark Inc. with the cooperation of

Thomson Financial Services, New York, NY.

The 2005 Benefits Barometer draws onnumerous sources for data providingreaders with a profile of current

employee benefit plan designs as well as valu-able benchmarking information.

This year’s publication includes moreentries and draws from more resources thanever before. The following sources are mostfrequently cited for the Benefits Barometer:

• Caremark–Drug trend information, costprojections and other data relating to pharma-cy benefit management was provided byCaremark, Scottsdale, AZ. For more informa-tion, call 800.927.3727.

• The Bureau of Labor Statistics’ NationalCompensation Survey - Compensation CostTrends. This study generates quarterly index-es measuring fluctuations in labor costs andannual data. Visit www.bls.gov for statistics.

• The EBN-Hay Survey on BenefitsManagement, which this year included nearly700 benefit executives who are readers of EBN.The complete online survey findings are avail-able for purchase at www.BenefitNews.com.

• Hewitt Associates. Findings from sourcessuch as the Hewitt Health Value Initiative, adatabase representing more than 2,000 healthplans in 139 U.S. markets, including 300 majoremployers and 18.23 million health plan par-ticipants was used. More information is avail-able at www.hewitt.com.

• The Kaiser Family Foundation and HealthResearch and Educational Trust (HRET)Employer Health Benefits Survey of 2004. Thissurvey reports findings from more than 1,925randomly selected public and private employ-ers. For more information, contact the HenryJ. Kaiser Family Foundation at www.kff.org.

• The MetLife Study of Employee BenefitsTrends of 2003. The national study of employ-ee benefits trends surveyed both employeesand employers during the third quarter of2003. Visit www.metlife.com to learn moreabout what this survey revealed.

• Mercer. The 2003 Coping with theEconomy Survey, with 242 organizationsresponding, reflected trends in the retirementand health care industries. Contact MercerHuman Resource Consulting at www.mercerhr.com.

• U.S. Centers for Medicare & MedicaidServices (CMS), Office of the Actuary,National Health Expenditures. Both historicaland projected statistics measure spending forhealth care in the U.S. by type of service deliv-ered and source of funding for those services.Go to www.cms.hhs.gov to learn more.

A research resource for benefit professionals featuring statistical

snapshots of benefit plan costs,plan designs and the benefits

management function

BenefitsBarometer

4

Employment cost indexChanges in wages and salaries and in benefit costs, private industry, 1994-2004

12-month percent changes in employment cost index, not seasonally adjusted

Compensation June June June June June Component 2000 2001 2002 2003 2004Civilian workers

Compensation costs 4.4 3.9 4.0 3.7 3.9 Wages and salaries 4.0 3.7 3.5 2.7 2.5 Benefit costs 5.3 4.5 5.0 6.3 7.2Private industry

Compensation costs 4.6 4.0 4.0 3.5 4.0 Wages and salaries 4.1 3.8 3.6 2.6 2.6 Benefit costs 5.7 4.8 5.1 6.1 7.3State and local government

Compensation costs 3.5 3.6 3.6 4.1 3.4 Wages and salaries 3.7 3.7 3.2 3.1 1.9 Benefit costs 3.1 3.4 4.6 6.8 6.6

20042003200220012000199919981997199619951994

Wages and salaries

+2.6

Benefits +6.8

Source: Bureau of Labor Statistics, 2004

Source: Bureau of Labor Statistics, 2004

1%

2%

3%

4%

5%

6%

7%

8%

Source: Bureau of Labor Statistics, 2004

Employer costs for employee compensation, June 2004Compensation Civilian State and local Privatecomponent workers government industry

Wages and salaries 70.9% 68.9% 71.4%

Benefits 29.1 31.1 28.6

➤ Paid leave 6.6 7.7 6.4

➤ Supplemental pay 2.4 .9 2.7

➤ Insurance 7.7 10.3 7.1

• Health benefits 7.3 9.9 6.6

➤ Retirement & savings 4.1 6.2 3.5

• Defined benefit 2.5 5.5 1.7

• Defined contribution 1.6 .7 1.8

➤ Legally required 8.1 5.9 8.7

➤ Other benefits .2 .2 .2

BENEFIT COST HIGHLIGHTS

Total Health Care Spending in 2002:Where did the money go?

Other Spending = Long-term care, administrative & other expenditures.Source: Federal Trade Commission & Dept. of Justice Report: Improving Health Care: A Dose of Competition, July 2004.

Physician & Clinical Services: 22%Hospital Care: 31%

Other Spending: 36%

Prescription Drugs: 11%

0

$150

$200

$250

2000 2001 2002 2003 2004

$135

$222

Health premiums soarAverage monthly employee contribution to cover

a family in an employer-sponsored health plan

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2000-2004; Exh. 6.1.

5

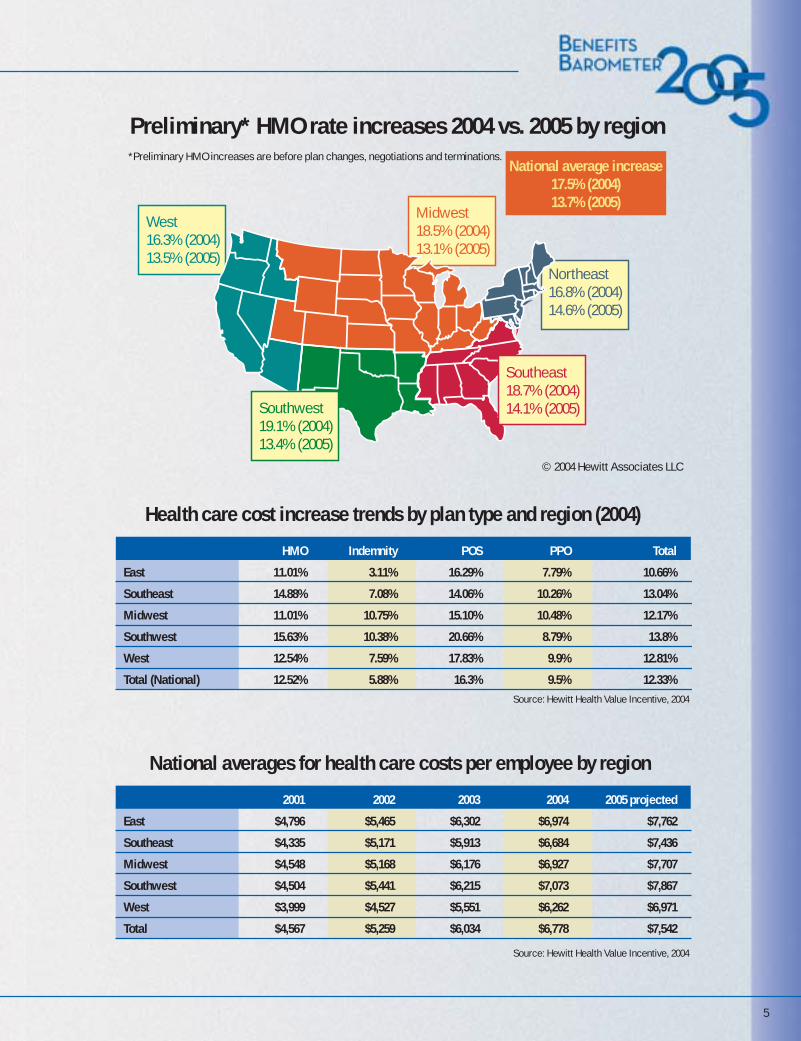

Source: Hewitt Health Value Incentive, 2004

Source: Hewitt Health Value Incentive, 2004

Health care cost increase trends by plan type and region (2004) HMO Indemnity POS PPO Total

East 11.01% 3.11% 16.29% 7.79% 10.66%

Southeast 14.88% 7.08% 14.06% 10.26% 13.04%

Midwest 11.01% 10.75% 15.10% 10.48% 12.17%

Southwest 15.63% 10.38% 20.66% 8.79% 13.8%

West 12.54% 7.59% 17.83% 9.9% 12.81%

Total (National) 12.52% 5.88% 16.3% 9.5% 12.33%

National averages for health care costs per employee by region 2001 2002 2003 2004 2005 projected

East $4,796 $5,465 $6,302 $6,974 $7,762

Southeast $4,335 $5,171 $5,913 $6,684 $7,436

Midwest $4,548 $5,168 $6,176 $6,927 $7,707

Southwest $4,504 $5,441 $6,215 $7,073 $7,867

West $3,999 $4,527 $5,551 $6,262 $6,971

Total $4,567 $5,259 $6,034 $6,778 $7,542

Northeast16.8% (2004)14.6% (2005)

National average increase17.5% (2004)13.7% (2005)

West 16.3% (2004)13.5% (2005)

Midwest 18.5% (2004)13.1% (2005)

Preliminary* HMO rate increases 2004 vs. 2005 by region *Preliminary HMO increases are before plan changes, negotiations and terminations.

Southwest 19.1% (2004)13.4% (2005)

Southeast18.7% (2004)14.1% (2005)

© 2004 Hewitt Associates LLC

6

Note: 2002 - 2006 data are projections; total drug spend includes uninsured expenditures.

Drug spend Percentage change

Drug spend continues to increase, but trend is slowing

Source: U.S. Centers for Medicare & Medicaid Services (CMS), Office of the Actuary, 2004

2001 2002 2003* 2004* 2005* 2007* 2009* 2011* 2013*

0% to 5% 13%

0

100

200

300

400

500

600

5%

10%

15%

20%

$ in

bill

ions

$140.8 $162.4 $184.1 $207.9 $233.6

15.9% 15.3%13.4% 12.9%

12.4%

$292.4 $360.1 $435.2 $519.8

11.7%10.7%

9.7% 9.2%

Ten-year look at drug spend as a proportion of health care costs

By what percentage did you project your health coverage

costs to increase from 2003 to 2004?

Note: 2004-2013 data are projectionsSource: U.S. Centers for Medicare & Medicaid Services (CMS),

Office of the Actuary, 2004

Source: 2004 EBN-Hay Survey on Benefits Management

3%

6%

9%

12%

15%

15.5% in 2013

13.6% in 2008

11.6% in 2004

5.8% in 1994

8.5% in 1999

1994 1996 1998 2000 2002 2004E 2006E 2008E 2010E 2012E 2013E

20% or more 8%

16% to 19% 10%

10% to 15% 46%

6% to 9% 23%

By what percentage did your pharmaceutical costs

increase from 2003 to 2004?

16% to 19%

15%

20% or more

8%

Source: 2004 EBN-Hay Survey on Benefits Management

0% to 5%

15%

6% to 9%

24%

10% to 15%

38%

0

1

2

3

4

5

6

7

8

Mas

s...8

%

Food

...6%

Mai

l/Onl

ine.

..5%

Clin

ic/O

ther

...5%

Chai

n...5

%

Ind.

..3%

Whether Ever Purchased Prescription Medication froma Foreign Country to Save Money Among Pharmacy Customers - By Type of Pharmacy Used Most Often

Among pharmacy customers, Mass merchant customers were the most likely (8%) to have purchased prescription medications from a foreign country to save money, independent customers (3%) were the least likely.

Source: 2004 Wilson Health Information, LLC.

BENEFIT COST HIGHLIGHTS

7

Drug plan cost-sharing

Source: Caremark Analytics & Outcomes, Book of Business Data©2004 Caremark Inc. All Rights Reserved.

Source: 2004 EBN-Hay Survey on Benefits Management

2003 retail and pharmacy sales $203.1 billion

What changes did you make in your pharmacy benefit plan for 2004 or

are you considering for 2005?

Supermarket12.3%

Source: National Association of Chain Drug Stores,2003 Community Pharmacy Results

Traditionalchainpharmacies42.0%

Mail order17.2%

Independentpharmacies

18.8%

Mass merchant9.6%

Increased co-pays 54%

Increased number of co-pay tiers 12%

Mandatory mail order for maintenance medication 8%

Mandatory generic where available 11%

Open formulary (where nonformulary brand has a higher co-pay than formulary brand) 13%

Closed formulary (where nonformulary brand drugs are reimbursed only with special approval) 2%

In 2003 and 2004, plans increased participant cost share.

Percent of participants covered

Source: 2004 EBN-Hay Survey on Benefits Management

How many employee co-payment tiers does your pharmacy benefit

have (excluding mail order)?None 2%One 1%Two 17%Three 74%Four or more 4%NA 2%

0% 10% 20% 30% 40% 50% 60% 70%

3- tier co-pay

52%

60%

63%

51%

53%

54%

21%

26%

31%

23%

19%

19%

11%

13%

15%

6%

12%

14%

Dispense as written penalty

Co-insurance

Retail refill restriction

Deductible

Maximum out-of-pocket

2002

2003

2004

8

Copay Coinsurance BothNeither Copay or Coinsurance – whichever

Four-Tier Three-Tier Two-TierPayment is the same regardless of type of drugOther/Don't know

Average copays for generic drugs, preferred drugs, nonpreferred and four-tier drugs

Generic

84% 3%3%10% 1%

84% 2%4%9% 1%

84% 2%5%8% 2%

17% 3%50% 31%

Preferred

Nonpreferred

Four-Tier

2000

27% 22%49% 2%

41% 1%41% 18%

55% 1%30% 13%

63% 2%23% 13%

65%3% 1%20% 10%

2001

2002

2003

2004

Distribution of covered workers with the following types of cost sharing for prescription drugs,

by drug type, 2004

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2004

Distribution of covered workers facing different cost-sharing

formulas for prescription drug benefits

Note: Tests found no statistically different distribution from the previous year shown at p<.05. No test was conducted between 2003 and 2004 due to the addition of a new category.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2004

* Estimate is statistically different from previous year at p<.05.^ Four-tier drug copay information was not obtanied prior to 2004.

Generic drugs

Preferred drugs

Nonpreferred drugs

Four-Tier drugs

2000

2001

2002

2003

2004

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2000, 2001, 2002, 2003, 2004

$0 $10 $20 $30 $40 $50

$7 $8*$9*$9*$10* $13$15*$17*$19*$21* $17$20$25*$29*$33* >>>>$48

BENEFIT COST HIGHLIGHTS

9

0%

3%

6%

9%

12%

15%

Increases in health insurance premiums compared to other indicators

Health insurance premiumsWorkers’ earningsOverall inflation

* Estimate is statistically different from the previous year shown at p<0.05.† Estimate is statistically different from the previous year shown at p<0.1.Note: Data on premium increases reflect the cost of health insurance premiums for a family of four.

Source: KFF/HRET Survey of Employer-Sponsored Health Benefits: 1999-2004; KPMG Survey of Employer-SponsoredHealth Benefits: 1993, 1996; The Health Insurance Association of America (HIAA): 1988, 1989, 1990; Bureau of Labor

Statistics, Consumer Price Index (U.S. City Average of Annual Inflation (April to April), 1988-2004; Bureau of LaborStatistics, Seasonally Adjusted Data from the Current Employment Statistics Survey (April to April), 1988-2004

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2004

1988 1990 1992 1994 1996 1998 2000 2002 2004

18%

12.0%

18.0%

14.0%

8.5%

0.8%

5.3%*

8.2%*10.9%*

12.9%*13.9%†

11.2%*

2.3%

2.2%

14%

10%

6%

2%

Premium increases, by plan type and funding arrangement, 2004*

11.4% 11.1% 10.0% 12.5% 12.4% 11.1% 10.3% 11.2% 13.1% 9.1%

* Tests found no statistically different estimates between fully insured and self-funded plans at p<.05.Note: Data on premium increases reflect the total cost of health insurance premiums for a family of four.

All Plans Conventional HMO PPO POS

Fully insured Self-funded

* Estimate is statistically different from All Firms at p<.05.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2004.

Percentage change in premiums for covered workers, by firm size, 2004

All Small Firms (3-199 workers)

(3-24 workers)

(25-49 workers)

(50-199 workers)

All Large Firms

(200 or more workers)

Midsize (200-999 workers)

Large (1,000-4,999 workers)

Jumbo (5,000+ workers)

All Firms

Average annual premiums for covered workers, by plan type, 2004

Single Family

Single Family

Single Family

Single Family

Single Family

Conventional

HMO

PPO

POS

All Plans

* Estimate of total premium is statistically different from All Plans by coverage type at p<.05.Note: Family coverage is defined as health coverage for a family of four.

Worker contribution Employer contribution

$468$2,382

$552$2,674

$573$2,691

$542$2,618

$558$2,661

$3,352 $7,220

$2,906 $6,830

$3,235 $7,526

$3,085 $7,195

$3,137 $7,289

$3,820

$3,458*

$9,602

$9,504*

$10,217*$3,808*

$3,627

$3,695$9,950

$9,813

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2004.

11.5%

13.6%

12.4%

9.1%*

11.1%

10.3%

10.7%

11.6%

11.2

10

Top concerns of benefits executivesVery or Somewhat Important 2004 2003Health plan costs 93% 97%Recruiting/retention 77% 75%Skills training 65% 64%Retirement planning education 49% 46%Benefits technology 47% 52%Voluntary/supplemental benefits 23% 27%

Benefits to help work/life balance

Employee decision support tools

Cost shifting to employees

Retirement planning

Wider array of voluntary benefits

401(k) investment education

Common platform for administration

Internet access for all employees

General financial planning

Employee self service on net

Outsourcing benefits administration

Build or expand benefits Web site

Source: 2004 EBN-Hay Survey on Benefits Management

Source: The MetLife Study of Employee Benefits Trends, 2003 Source: The MetLife Study of Employee Benefits Trends, 2003

100%80%0% 20% 40% 60%

43%39%

29%23%

26%21%

25%28%

22%20%

21%28%

20%22%

18%12%

14%13%

10%13%

8%11%

5%12%

Employer pays all

Employer pays some

Employee pays all

(Among those with products through workplace)

Auto

Medical

Banking services

Dental

Home/Renter insurance

Basic term life

AD&D

Disability

Vision care

Mortgage

Dependent term life

Financial plan

Optional/Supplemental life

Travel/Accident

Critical illness

Long term care

Group legal

Estate planning

Pet

Concierge

2003

2002

Most important employeebenefits strategies

Consumer product ownership –by source of workplace funding

HEALTH PLANS

11

Ten-year view of annual percentage change in national spending for selected health services

Percentage of large firms (200 or more workers) that report they were likely to make the following changes in 2004

Increase the amount employees pay for health insurance

Increase the amount employees pay for prescription drugs

Increase the amount employees pay for deductibles

Increase the amount employees pay for office visit copays or coinsurance

Introduce tiered cost sharing for doctor visits and hospital stays Restrict employee eligibility for coverage

Drop coverage entirely

Very likely Somewhat likely Not too likely Not at all likely Don't know

8.2 8.4

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

7.4

5.9 6.1 6.3

3.94.6

6.6

3.4

4.8

11.2

3.44.0

10.5

3.5

5.0

12.8

3.0

6.6

15.2

3.9

5.55.0

7.2

16.4

7.58.6

15.9

9.5

7.7

15.3

19.7

0%

5%

10%

15%

20%

Source: Kaiser Family Foundation, Trends and Indicators in the Changing Health Care Marketplace, 2004 Update,from Centers for Medicare and Medicaid Services, 2002 National Health Care Expenditures

Hospital care

Physician and clinical services

Prescription drugs

Source: Kaiser/HRET Survey of Employer Sponsored Health Benefits: 2004

52% 31% 9% 7% 1%

18% 37% 32% 12% 1%

14% 38% 32% 16% 1%

14% 38% 33% 14% 1%

2% 24% 39% 34% 2%

2% 7% 37% 53%

1% 4% 94% 1%

12

0%

20%

40%

60%

80%

100%

The largest percentage of your employees are covered in what type of medical plan (including being in several different plans of the same type)?Preferred Provider Organization 63% Traditional indemnity/fee-for-service 3% Point-of-Service 10% HMO 23% Health Reimbursement Account (company-paid) with high-deductible plan 1% Consumer-driven option, where the company contributes a specified amount per employee for medical coverage and the employee chooses from various plans 1%

Percentage of employers providing a choice of health plans, by firm size, 2004

Firms offering high-deductible health plans to employees

All Firms All Small Firms Midsize Firms* Large Firms* Jumbo Firms* (3-199 workers) (200-999 workers) (1,000-4,999 workers) (5,000+ workers)

All Firms2004 2005-20062003 2004 2005-20062003 2004 2005-20062003 2004 2005-20062003 2004 2005-2006†2003

All Small Firms(3-199 workers)

Midsize Firms(200-999 workers)

Large Firms(1,000-4,999 workers)

Jumbo Firms(5,000+ workers)

4%12%

84%

3%11%

86%

24%

33%

43%

50%

26%24%

72%

16%12%

One plan Two plans Three or more plans

Source: 2004 EBN-Hay Survey on Benefits Management

Growth in consumer-driven health plans

Consumer-driven health available currently or within 2005

Source: Milliman Group Health Insurance Survey, 2004

Offer a CDH plan

2003 survey 2004 survey

Offer a high-deductible

plan

Offer a tiered provider

network

0% 20% 40% 60% 80% 100%

29%

89%

48%

96%

17%

42%

*Distribution is statistically different from All Firms at p<.05. Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2004

*Estimate is statistically different from previous year shown at p<.05. †Column total is statistically different from All Firms at p<.05.Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2000, 2001, 2002, 2003, 2004.

Somewhat likely to offer Very likely to offer

0%

10%

20%

30%

40%

50%

5%10%

21%

6% 5%10%

20%

6% 5% 7%

28%

7% 5%9%*

25%

11%17% 20%

28%

22%

HEALTH PLANS

13

Average annual deductibles for covered workers, by plan type

* Estimate is statistically different from the previous year shown at p<.05. ^ Information was not obtained for HMO plans prior to 2003, or for POS plans in 1988 and 1993.Note: Average deductibles include covered workers who do not have a deductible or report a $0 deductible. For example, 30% of covered workers in PPO plans do not have a deductible for preferred providers. Among single workers enrolled in a PPO plan who do have a deductible greater than $0, the average annual preferred provider deductible is $410 and the average nonpreferred provider deductible is $595.

$0

$100

$200

$300

$400

$500

$600

$170 $175 $251* $275 $287 $289 $340 $466* $561* $558 ^ $70 $54 $113* $210 ^ $352 $409* $442 $575

PPO Preferred PPO Non-Preferred POS Preferred POS Non-Preferred Provider Provider Provider Provider

1993

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2000, 2002, 2003, 2004; KPMG Survey of Employer-Sponsored Health Benefits: 1993;The Health Insurance Association of America (HIAA): 1988

Employers offering retiree health coverage, by plan type

48%

29%27%

19%

7%14%

20% 16% 14% 14% 10%POS

27%30%

30% 33%27% 27%

HMO

35%43% 46%

54%58%

PPO

40%35%

31%28%

23% 21% 20%

Offer coverage to Medicare-eligible

15%11% 7% 5%

4%

2004200320011999199719951993

2004200320011999199719951993

Percent of all covered employees

Based on employers with 500 or more employees

TIP

41%46%

38%35%

29% 28% 28%

Offer coverage to pre-Medicare-eligible

.1% CDHP

Source: Mercer's National Survey of Employer-Sponsored Health Plans, 2004

National employee health plan enrollment

Source: Mercer's National Survey of Employer-Sponsored Health Plans, 2004

0%

10%

20%

30%

40%

50%

60%

20%

10%

30%

40%

50%

2000 2002 2003 2004

14

Examples of CarePatterns®, Caremark’s Disease Management Program Outcomes

Caremark is the first and only PBM to achieve Full Patient and Practitioner Accreditation from NCQA for asthma, CHF, coronary artery disease and diabetes disease management programs. (Effective 9/02-9/05)

BENEFITS MANAGEMENT

The CarePatterns Health Management Programs cover over 3 million lives nationally, and the first to receive both physicianand participant based NCQA accreditation. Outcomes are monitored and reported on clinical, quality and economic indicatorsfor each population. The Asthma program summarizes the improvement in key clinical measure achieved.

Source: Caremark Inc. All Rights Reserved.

The CarePatterns Health Management Programs cover over 3 million lives nationally, and the first to receive both physicianand participant based NCQA accreditation. Outcomes are monitored and reported on clinical, quality and economic indicatorsfor each population. The Diabetes program summarizes the improvement in key clinical measure achieved.

Source: Caremark Inc. All Rights Reserved.

15

Specialty Pharmaceuticals

Source: Nov. 2004. ©2005 Caremark Inc. All Rights Reserved.

Source: JP Morgan Industry Update, “Specialty Pharmacy: Conduit of Growth for Biotechnology,” March 14, 2003.

©2005 Caremark Inc. All Rights Reserved.

Source: IMS Health, JP Morgan Industry Update, “Specialty Pharmacy: Conduit of Growth for Biotechnology,” March 14, 2003, Bear Stearns Health Care Distribution, “Specialty Pharmacy Services: Among the Fastest-Growing Areas of Health Care,” November 2003, Caremark Estimates. ©2005 Caremark Inc. All Rights Reserved.

Source: “Top 10 Areas of Research,” R&D Directions,Oct. 2004, Vol. 10, No.9, p.36.

©2005 Caremark Inc. All Rights Reserved.

Rank Area Number of Drugs in Development*1 Cancer 5742 Infections 1903 Pain/Inflammation 1774 Cardiovascular Disorders 1385 Psychological Disorders 1086 Respiratory Disorders 1077 Diabetes 938 Gastrointestinal Disorders 929 Blood Disorders 8210 Dermatological Disorders 72*Includes compounds in preclinical development, Phase I, Phase II, Phase III, and awaiting FDA approval.

16

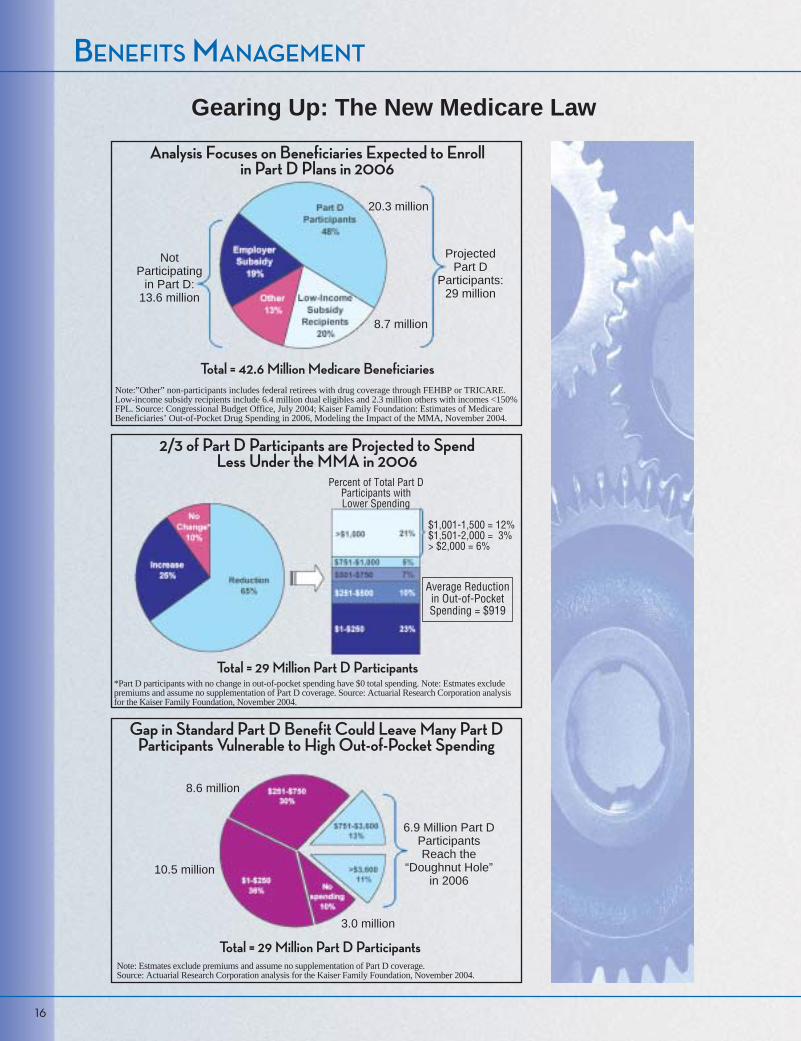

Gearing Up: The New Medicare Law

BENEFITS MANAGEMENT

Note:”Other” non-participants includes federal retirees with drug coverage through FEHBP or TRICARE.Low-income subsidy recipients include 6.4 million dual eligibles and 2.3 million others with incomes <150%FPL. Source: Congressional Budget Office, July 2004; Kaiser Family Foundation: Estimates of MedicareBeneficiaries’ Out-of-Pocket Drug Spending in 2006, Modeling the Impact of the MMA, November 2004.

*Part D participants with no change in out-of-pocket spending have $0 total spending. Note: Estmates excludepremiums and assume no supplementation of Part D coverage. Source: Actuarial Research Corporation analysisfor the Kaiser Family Foundation, November 2004.

Note: Estmates exclude premiums and assume no supplementation of Part D coverage. Source: Actuarial Research Corporation analysis for the Kaiser Family Foundation, November 2004.

Analysis Focuses on Beneficiaries Expected to Enrollin Part D Plans in 2006

2/3 of Part D Participants are Projected to SpendLess Under the MMA in 2006

Gap in Standard Part D Benefit Could Leave Many Part DParticipants Vulnerable to High Out-of-Pocket Spending

NotParticipating

in Part D:13.6 million

ProjectedPart D

Participants:29 million

20.3 million

8.7 million

Total = 42.6 Million Medicare Beneficiaries

Percent of Total Part DParticipants withLower Spending

$1,001-1,500 = 12%$1,501-2,000 = 3%> $2,000 = 6%

Average Reductionin Out-of-PocketSpending = $919

Total = 29 Million Part D Participants

Total = 29 Million Part D Participants

6.9 Million Part DParticipantsReach the

“Doughnut Hole”in 2006

8.6 million

10.5 million

3.0 million

17

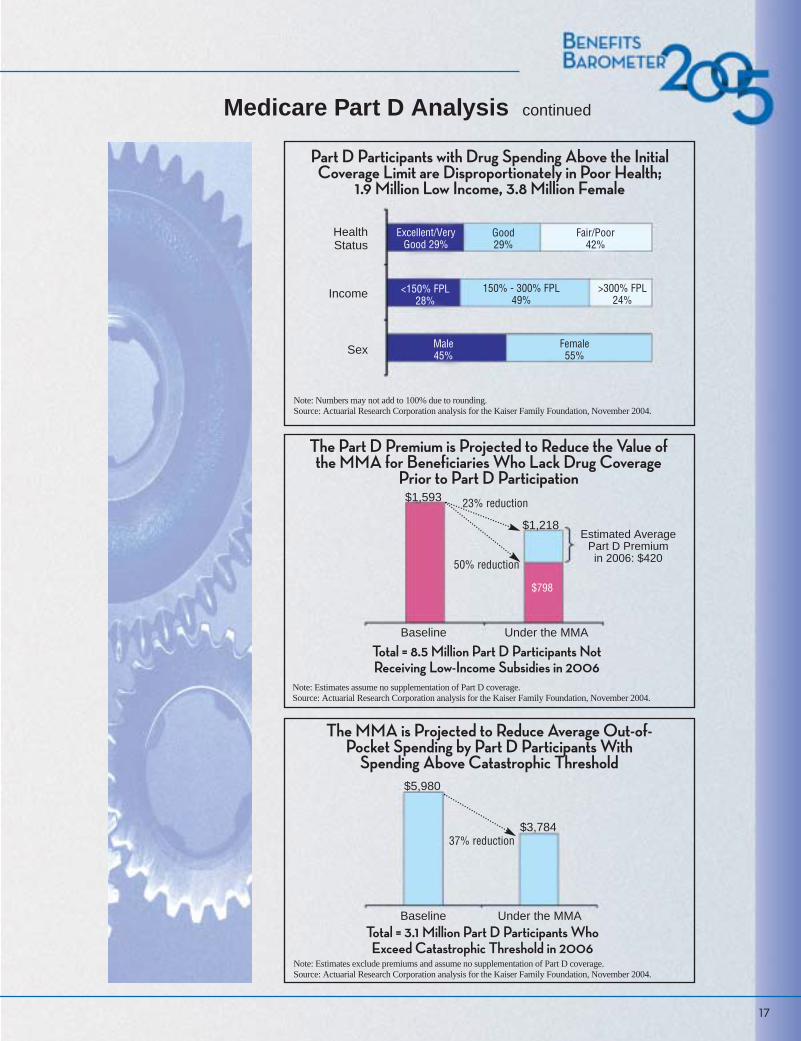

Medicare Part D Analysis continued

Part D Participants with Drug Spending Above the InitialCoverage Limit are Disproportionately in Poor Health;

1.9 Million Low Income, 3.8 Million Female

Note: Numbers may not add to 100% due to rounding.Source: Actuarial Research Corporation analysis for the Kaiser Family Foundation, November 2004.

HealthStatus

Income

Sex

The Part D Premium is Projected to Reduce the Value of the MMA for Beneficiaries Who Lack Drug Coverage

Prior to Part D Participation

Note: Estimates assume no supplementation of Part D coverage.Source: Actuarial Research Corporation analysis for the Kaiser Family Foundation, November 2004.

Total = 8.5 Million Part D Participants Not Receiving Low-Income Subsidies in 2006

Baseline Under the MMA

$1,593

$1,218Estimated Average

Part D Premium in 2006: $420

23% reduction

50% reduction

The MMA is Projected to Reduce Average Out-of-Pocket Spending by Part D Participants With

Spending Above Catastrophic Threshold$5,980

$3,784

Baseline Under the MMA

Note: Estimates exclude premiums and assume no supplementation of Part D coverage.Source: Actuarial Research Corporation analysis for the Kaiser Family Foundation, November 2004.

Total = 3.1 Million Part D Participants Who Exceed Catastrophic Threshold in 2006

37% reduction

Excellent/VeryGood 29%

<150% FPL28%

Male45%

Good29%

150% - 300% FPL49%

Female55%

Fair/Poor42%

>300% FPL24%

$798

18

Source: 2004 EBN/Hay Survey on Benefits Management

In the next year, which of the following benefits will you INTRODUCE for the first time, INCREASE the value of, MAINTAIN at the current level, DECREASE the value of (i.e., by increasing cost sharing, deductibles, etc.) or DROP? Note: N/A indicates a particular benefit is not offered nor will it be introduced.

INTRO INCR MNTN DECR DROP N/A

HEALTH PLANS:

Traditional indemnity plan 1% 1% 13% 2% 2% 81% Preferred Provider Network (PPO) 2% 5% 71% 11% 1% 12% HMO 2% 1% 35% 8% 2% 51% Point-of-Service 2% 2% 20% 3% 1% 71% Health Reimbursement Account with high-deductible plan option 16% 3% 4% 0% 0% 77% Consumer-driven voucher option 5% 1% 2% 0% 0% 90% Health Care Consumerism (Educating employees concerning

importance to them of containing costs and how to do it) 29% 31% 13% 0% 0% 28% Disease Management (Management of chronic disease where patient self-care can improve health) 23% 21% 22% 0% 0% 34% Health benefits for retirees 1% 1% 22% 5% 0% 71% Pharmacy 1% 4% 74% 15% 0% 7%

RETIREMENT PLANS:

Defined benefit (DB) plan 1% 1% 21% 2% 0% 74% Hybrid DB Plan (cash balance, etc.) 0% 0% 5% 0% 0% 92% Savings plans - 401(k)/403(b)/457 1% 9% 81% 2% 0% 8% Profit sharing plan 2% 3% 31% 1% 1% 61% ESOP 1% 1% 10% 1% 0% 87% Money purchase plan 0% 0% 4% 0% 0% 94% Broad-based stock option plan 1% 0% 5% 1% 0% 91% Stock purchase plan 1% 1% 12% 0% 0% 84%

OTHER BENEFITS:

Financial education/advice 9% 12% 31% 1% 0% 47% Full flex/cafeteria plan 3% 3% 39% 1% 0% 54% Flexible spending accounts 6% 7% 67% 1% 0% 19% Disability -- STD 3% 3% 80% 2% 0% 14% Disability -- LTD 2% 3% 87% 2% 0% 8% AD&D 2% 2% 88% 2% 0% 7% Voluntary whole/universal life 3% 3% 47% 1% 0% 46% Voluntary long-term care 12% 3% 25% 1% 0% 60% Mental health care 1% 2% 75% 2% 0% 21% EAP & substance abuse 5% 4% 70% 1% 0% 21% Child care (facility and/or cash subsidy) 0% 1% 8% 1% 0% 89% Child care referral services 1% 1% 22% 1% 0% 75% Eldercare 1% 1% 13% 0% 0% 84% Dental 2% 4% 88% 4% 0% 4% Vision 5% 4% 68% 2% 0% 22% Hearing 1% 1% 38% 0% 0% 61% Wellness 10% 19% 44% 2% 0% 26% Group legal 4% 1% 19% 1% 0% 75% Relocation assistance 1% 1% 40% 1% 0% 56% Transportation/parking assistance 1% 2% 26% 1% 0% 69% Paid time off plan 2% 5% 67% 2% 0% 24% Flexible hours 2% 5% 59% 1% 0% 34% Dependent care days 0% 1% 18% 1% 0% 80% Life insurance living benefits 0% 1% 36% 1% 0% 62% Employee self-service technology 13% 18% 16% 1% 0% 51% Work at home policy 2% 2% 36% 1% 0% 59% Domestic partner health coverage 5% 2% 22% 1% 0% 70% Casual dress day 1% 2% 77% 1% 0% 20% Convenience (concierge) services 2% 2% 10% 1% 0% 85% Training 4% 28% 57% 2% 0% 9%

BENEFITS MANAGEMENT

2211 Sanders RoadNorthbrook, IL 60062

800.927.3727www.caremark.com

©2005 Caremark. All Rights Reserved.

Reprinted from Benefit Source Book 2005. One State Street Plaza, 25th Floor, New York, NY 10004

20564-0904