Embed Size (px)

Citation preview

The Growth of Finance, Financial Innovation, and

Systemic Risk

Lecture 5

BGSE Summer School in Macroeconomics, July 2013

Nicola Gennaioli, Universita’ Bocconi, IGIER and CREI

Banks and Sovereign Default Risk2

Link between government default and private sector turmoil

Russia 1998, but also Pakistan, Ecuador and Argentina (IMF 2002)

European debt crisis: joint fragility of governments and private banks

Government Default and Private Credit

3

• After sovereign default, the flow of private credit comes to a halt

4

5

6

7

• Private credit flow systematically drops after a default episode

The Default-Private Credit Link

8

Two potential stories for the above correlations:

Greek-style default:

financial distress in the government → banks are hurt because they hold government bonds → credit crunch

Irish-style default:

private banking crisis → government nationalizes (or bails out) banks → government is over-indebted, twin crisis follows

Can we distinguish between these two views?

Do they have different implications?

9

-140.00%

-120.00%

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

01/0

1/20

09

01/0

2/20

0901

/03/

2009

01/0

4/20

0901

/05/

2009

01/0

6/20

0901

/07/

2009

01/0

8/20

09

01/0

9/20

0901

/10/

2009

01/1

1/20

0901

/12/

2009

01/0

1/20

10

01/0

2/20

1001

/03/

2010

01/0

4/20

1001

/05/

2010

01/0

6/20

1001

/07/

2010

01/0

8/20

10

01/0

9/20

1001

/10/

2010

01/1

1/20

1001

/12/

2010

01/0

1/20

11

01/0

2/20

1101

/03/

2011

01/0

4/20

1101

/05/

2011

EU Banks' Stock Returns and Exposure to PIGS BondsCAR of [(High Exposure to PIGS Bonds) - (Low Exposure to PIGS Bonds)] Portfolio

Ireland downgrade

Greek budget disclosed

Greek Bailout approved

Portuguese Bailout approvedIrish Bailout

agreed

Greek Bailout committed

Irish Bailout first press leaks

Greek budget cuts announced

Upon arrival of bad news, banks holding government bonds suffer…

A First Pass Assessment

Some preliminary support for Greek style default: financial distress in the government → banks are

hurt because they hold government bonds → credit crunch

Irish-style is also important, but let’s start with Greece A theory of Irish style default should still explain

why the government default triggers a sharp credit contraction

Two crucial questions: If government bonds are deadly, why do banks hold them? What about the government default decision?

10

Literature Background (I)11

Government default decision: Traditional literature on sovereign debt (see Eaton

and Fernandez 1995) assumes that government defaults can selectively discriminate between foreign and domestic bondholders.

In this theory, the cost of default is external punishment (e.g. exclusion from international financial markets).

In this theory, the government trades off the benefit from defaulting in terms of increasing current consumption, with the cost of being excluded from future borrowing (or trade).

Literature Background (II)12

Difficulties with the traditional theory: Observed exclusion is short lived. To rationalize

why countries default so infrequently need output cost (Arellano 2008).

Theoretical problems with the sustainability of penalties

Most important: In the traditional theory, perfect discrimination

implies that banks will be spared from default. That is, when the government defaults, domestic banks will be spared…

Some Observation13

Banks exposed to the domestic government are perceived to be in trouble when sovereign debt markets are in strain.

Markets do not expect (perfect) bailouts: Hard for the government to selectively default, Hard for the government to finance a bailout during a

default episode

We need a theory of Greek-style default

A Model of Greek-Style Default

14

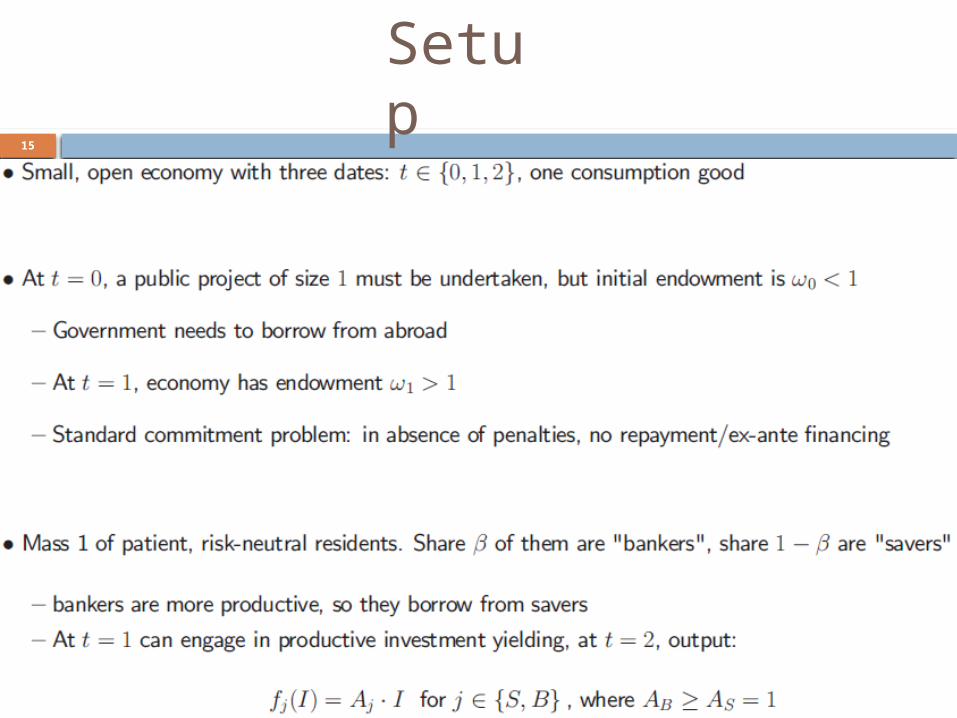

Setup15

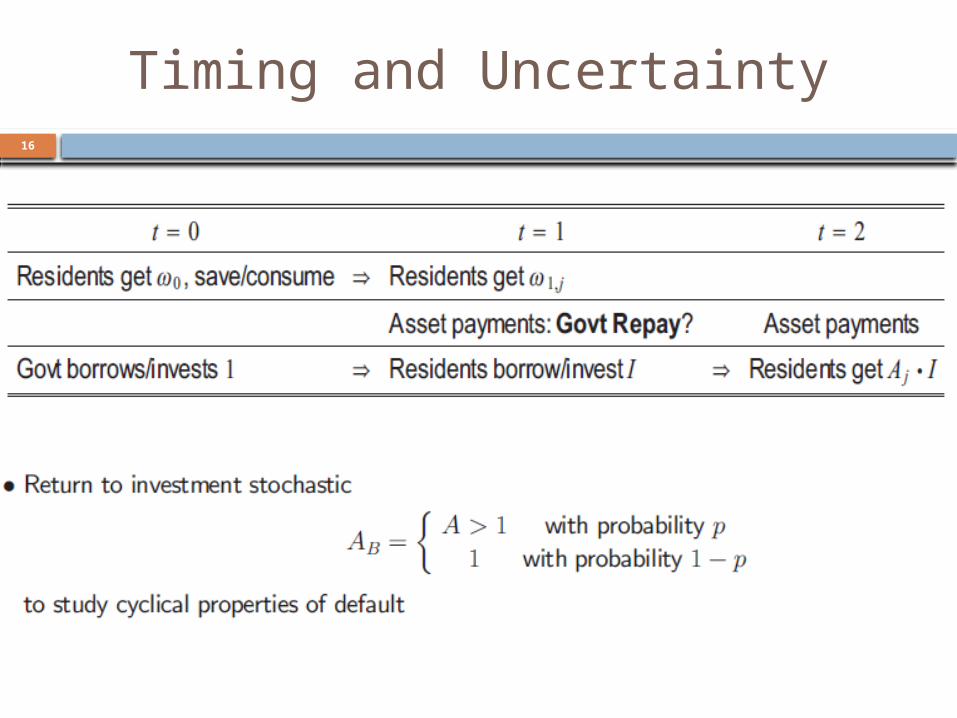

Timing and Uncertainty16

Financial Markets17

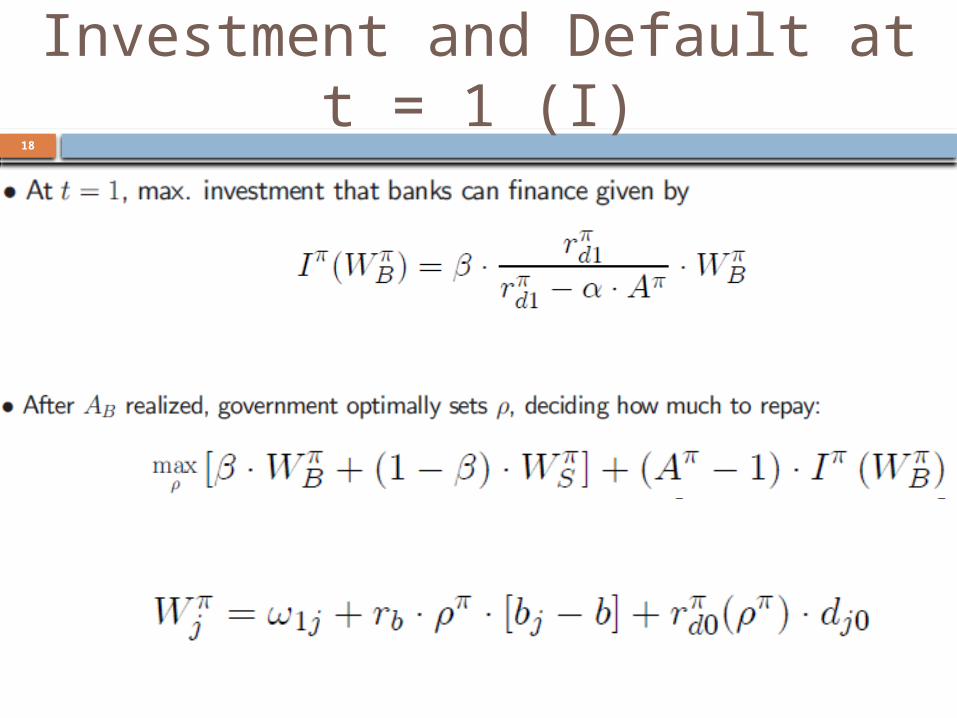

Investment and Default at t = 1 (I)

18

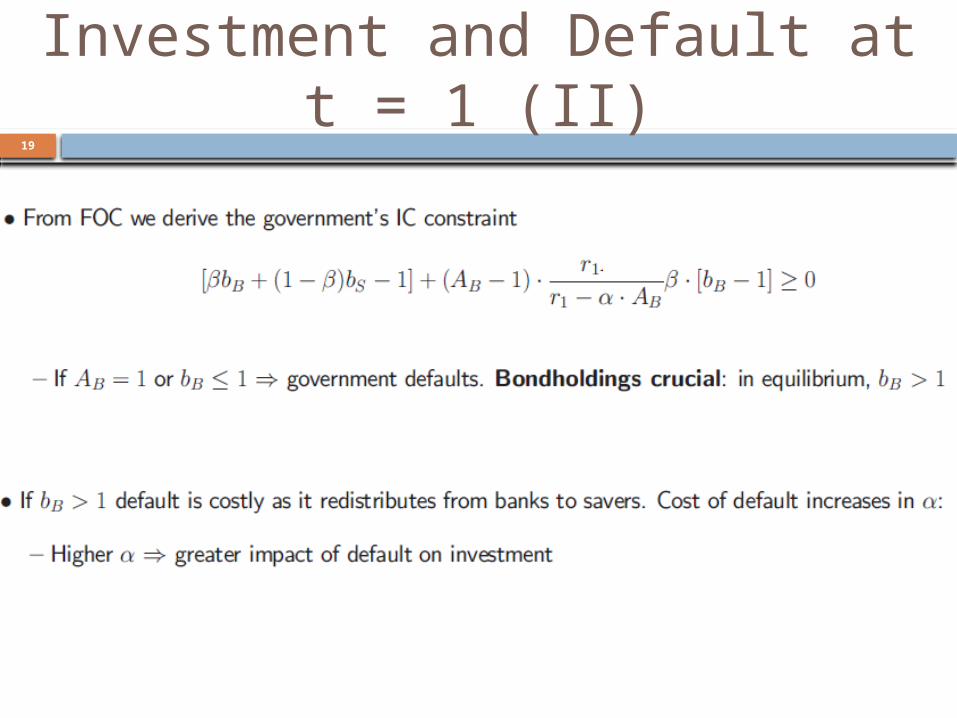

Investment and Default at t = 1 (II)

19

Investment and Default at t = 1 (III)

20

• Let’s step back, for a moment: - In this theory, the government repays because banks hold public bonds - If banks did not hold government bonds, the government would always default! - Not necessarily sound to clean up the banking sector from bonds - Yet, bonds create fragility if a crisis is to occur

• What determines banks’ bond-holdings in the first place?

Banks’ Demand for Bonds (I)21

Banks’ Demand for Bonds (II)22

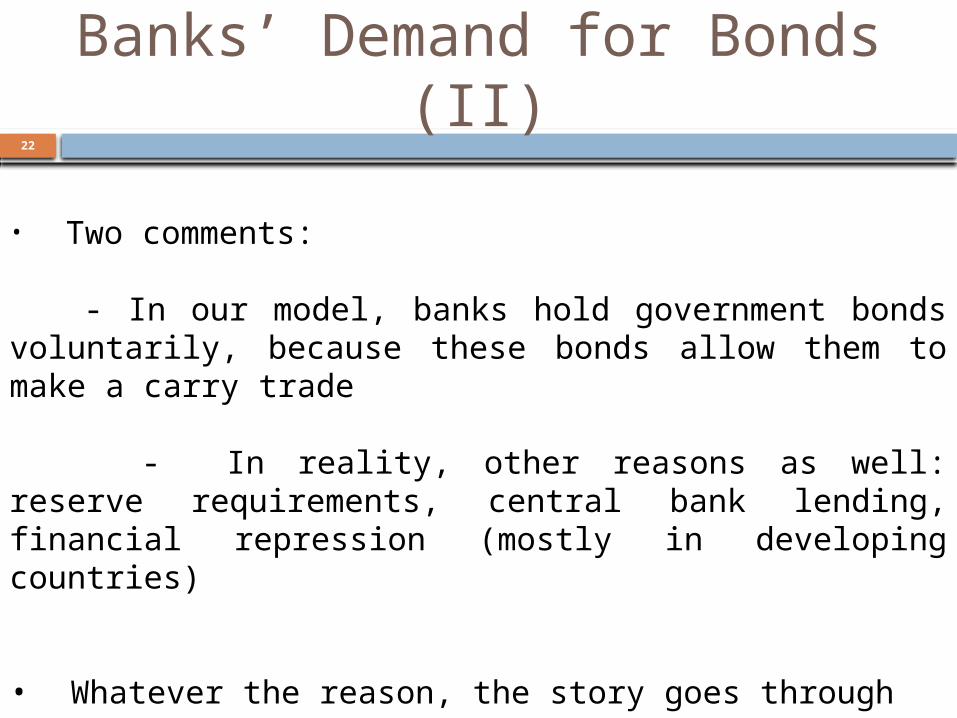

• Two comments:

- In our model, banks hold government bonds voluntarily, because these bonds allow them to make a carry trade

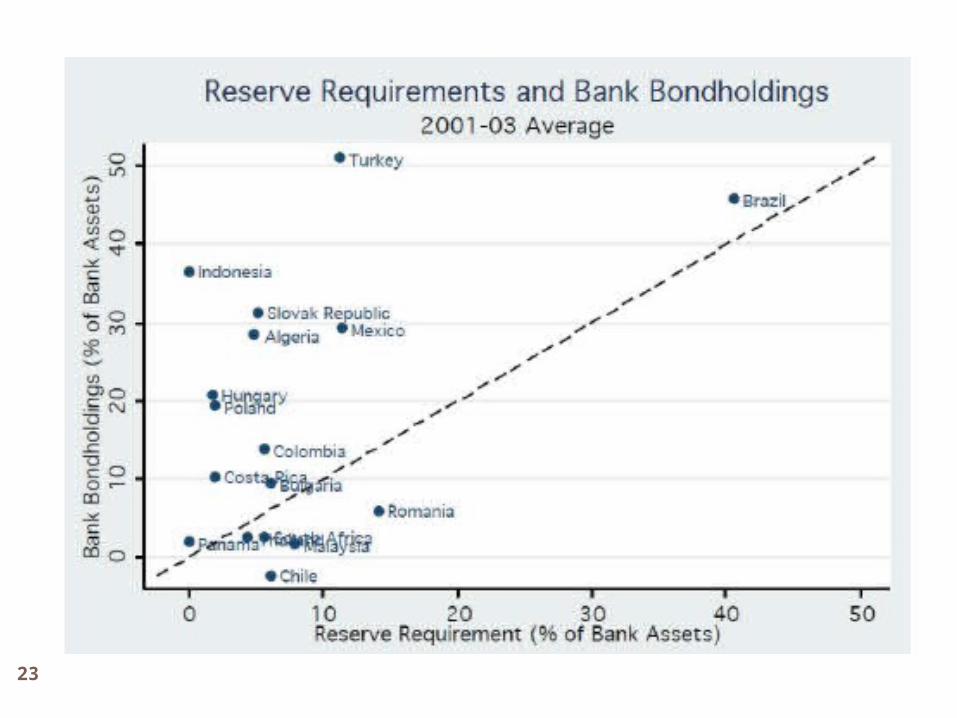

- In reality, other reasons as well: reserve requirements, central bank lending, financial repression (mostly in developing countries)

• Whatever the reason, the story goes through

23

24

0.00

5.00

10.00

15.00

20.00

25.00

1 - Small 2 3 4 - Large

Bondholdings by Size Quartile all years

0.00

5.00

10.00

15.00

20.00

25.00

1 - Small 2 3 4 - Large

Bondholdings by Size Quartile during Sovereign Defaults years

Debt Sustainability (I)25

Debt Sustainability (II)26

Debt sustainability requires:

Strong financial institutions: developed private financial markets help the government commit to repay. This increases the cost for the government of interfering

with intermediation

Important role of financial intermediaries (intermediate β): if banks are too small, or if firms can obtain funds at arm’s length, the government has no incentive to save the banking sector

Empirical Predictions27

Government default is followed by a drop in private credit. This drop is stronger if:

Banks hold more government bonds

Financial institutions are stronger

Ex-ante probability of default decreases as:

Banks hold more government bonds

Financial institutions are stronger

Data28

29

30

Probability of default at t…

Data (New Paper)

Bank‐level data from BANKSCOPE dataset (Bureau van Dijk): Provides information on a broad range of bank characteristics BANKSCOPE suitable for international comparisons because data is harmonized

Crucial: BANKSCOPE reports banks’ holdings of public bonds However, does not say the nationality of the bonds We use IMF and EU stress test data to validate this information

Main sample: 4,723 banks in 151 countries; 25,132 bank‐year obs. Commercial, cooperative and savings banks account for 92% of our sample; investment

banks for 1.6%; rest are holdings, real estate, and other credit institutions Sample construction: start with full data; filter out duplicate records, banks with

negative value of assets, banks with total assets < $100,000, years < 1997 when coverage is less systematic. Get: 10,281 banks in 174 countries over 1998‐2010 (58,830 bank‐year observations)

Further impose: two consecutive years of data; data is available on size, leverage, risk taking, profitability, loans, Central Bank balances and other interbank ratiosIntro Data Hypotheses and Empirical Strategy

Results

Our Tests

1. Estimate banks’ demand for bondholdings (and of its various components)

Time-invariant (“normal times”) Bondholdings, both at bank and country level

Time-varying (“crisis times”) Bondholdings, both at bank and country level

2. Estimate effect of bondholdings (and of its various components) on banks’ changes in loans during default

Do banks more exposed to government bonds cut their loans more during default?

Which of the various components of bondholdings demand explain more of this variation?

Intro Data Hypotheses and Empirical Strategy

Results

Summary of Bondholdings Demand

Normal-time bondholdings account for 80% of total variation of bondholdings in our sample Largely explained by liquidity/insurance [risk taking (-), leverage (+),

fin dev (-)]

Default episodes alone explain 14% of time variation of bonds Banks take 16% more bonds during default Huge heterogeneity: esp. larger/more profitable banks load up on

government bonds during default Consistent with risk taking and/or government intervention through

moral suasion during crises

Next: do bondholdings affect changes in loans during default?

Intro Data Hypotheses and Empirical Strategy

Results

Bondholdings and Changes in Loans

Intro Data Hypotheses and Empirical Strategy

Results

35

Bottom Line

Powerful feedback effects between banks and sovereign default risk: A government facing a weak domestic banking

sector faces a hard time borrowing, but.. Financial development will enhance fragility in case

of default Similar to the banking crises studied earlier

Additional implication: a banking crisis can lead to sovereign default risk. Links with Irish-style crises Banking crisis reduces incentive to repay and tax

revenues Government can try to bail out failed banks

36

International Contagion

Bolton and Jeanne (2012) use the previous mechanism to generate contagion effects across countries. International banks hold diversified sovereign bonds

portfolios Default in one country hurts banks in many country This triggers a recession across countries, in turn

increasing the likelihoods of additional government defaults

Ex-ante, countries issue too much debt because they do not internalize the contagion effect on other countries

37

38

39

40

Irish-style Bailouts

From Acharya, Drechsler and Schanbl (2011)

Imagine that a highly levered banking sector enters a financial crisis. Why would it makes sense for the government to bail it out? Answer is related to micro-frictions/externalities

This paper: the government might default to relieve the private sector from debt overhang problems For given taxes, the government dilutes existing

government bondholders, reducing the government’s creditowrthiness

This increases the probability of twin defaults when future shocks hit

41

42

Correlation between sovereign cds and public debt before and after bailouts

43