Embed Size (px)

Citation preview

Sustainability in Dubai – the story so far

Segment Performance

Wellness in the Workplace

SustainabilityOutlook

core-me.com

THE GREEN ISSUESustainability and Wellness in Dubai - 2017

32

This publicationThis document was published in June 2017.The data used in the charts and tables is thelatest available at the time of going to press.Sources are included for all the charts. We haveused a standard set of notes and abbreviationsthroughout the document.

CONTENTS

Foreword

LEED-certified space by region

Office market performance

Residential market performance

Wellness in the workplace

Smoke-free buildings and regulations

Outlook

54

H1 2017

ForewordThe United Arab Emirates are the flag bearers of sustainability within the region, despite restrictive climatic conditions and a relatively young real estate market. The UAE ranks amongst the top 10 countries to hold LEED (Leadership in Energy and Environment Design) certifications outside the United States. Meanwhile, Dubai ranks 3rd amongst global cities with the highest number of green buildings (under both LEED and BREEAM).

This marks an important step forward for sustainability in the region, where Dubai takes the lead with over 550 projects currently undertaking LEED certification. The market has seen a significant surge in certificate completions over the last 5 years, with 54% being Gold rated, the second highest rating achievable in a LEED certification.

Government buildings are leading the trend with Dubai Chamber of Commerce, DEWA buildings and many district cooling plants either certified or in the process of doing so; while in the private sector, manufacturing and logistics operators form the majority of LEED-certified occupiers. Furthermore, Dubai has the highest ratio of projects being certified with 81% of in-progress projects across global cities, indicative of a burgeoning interest in sustainability.

Despite the positive steps taken toward a green strategy, we areseeing a paradox develop, with the residential market strongly lagging behind the commercial market. In this Green Issue, we analyse the shift in user preferences and drivers affecting the upcoming trends in sustainability and wellness – albeit in the backdrop of maturing, yet challenging market conditions.

SUSTAINABILITY AND WELLNESS IN DUBAI

Type of LEED certifications in Dubai(for completed buildings)

Growth of LEED certifications in Dubai

Category of LEED in-progress projects in Dubai

LEED certified vsin-progress projects in global cities

Source: USGBCSource: USGBC and BREEAM CertifiedLEED In progressBREEAM

Platinum 11%

Duba

i

0 500 1000 1500 2000 2500

Certified 10%

Silver 25%

Gold 54%

20072006 2008 2009 2010 2011 2012 2013 2014 2015 2016

Existing buildings 7%

Homes 1%

Interiors 7%

Core & Shell 13%

New Construction 72%

Green buildings in global cities(both in progress and completed)

London

Lond

on

New York

New

Yor

k

Paris

Paris

Bengaluru

Beng

alur

u

Hong Kong

Hon

g Ko

ng

Singapore

Sing

apor

e

Sydney

Sydn

ey

20

15

10

5

0

19% 54% 51% 38% 69% 58% 47% 48%

62% 31% 42% 53% 52%81% 46% 49%

Dubai

76

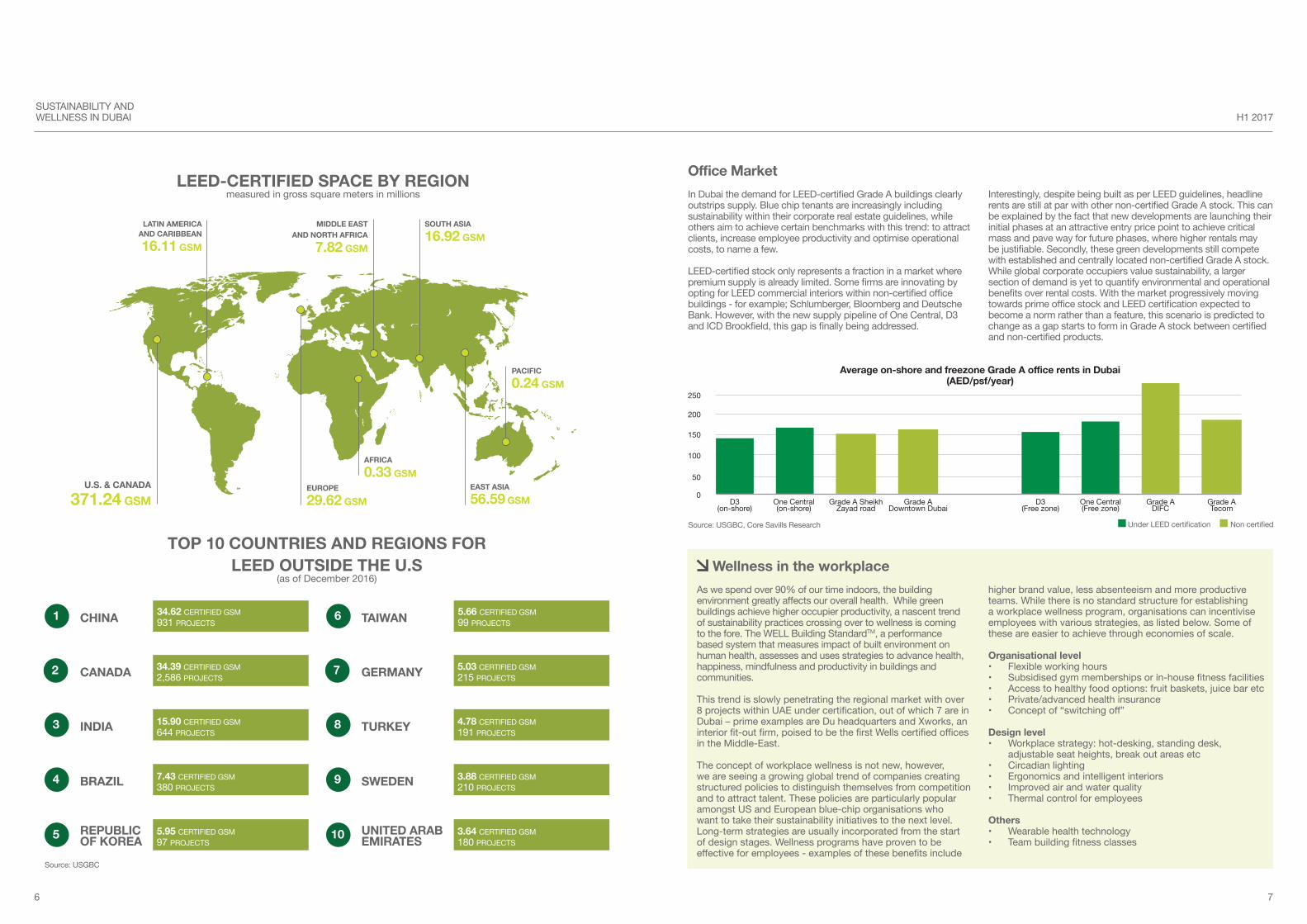

Office MarketIn Dubai the demand for LEED-certified Grade A buildings clearly outstrips supply. Blue chip tenants are increasingly including sustainability within their corporate real estate guidelines, while others aim to achieve certain benchmarks with this trend: to attract clients, increase employee productivity and optimise operational costs, to name a few.

LEED-certified stock only represents a fraction in a market where premium supply is already limited. Some firms are innovating by opting for LEED commercial interiors within non-certified office buildings - for example; Schlumberger, Bloomberg and Deutsche Bank. However, with the new supply pipeline of One Central, D3 and ICD Brookfield, this gap is finally being addressed.

SUSTAINABILITY AND WELLNESS IN DUBAI

Average on-shore and freezone Grade A office rents in Dubai(AED/psf/year)

250

Grade ATecom

Grade A DIFC

One Central (Free zone)

D3(Free zone)

Grade A Downtown Dubai

Grade A Sheikh Zayad road

One Central (on-shore)

D3 (on-shore)

200

150

100

50

0

LATIN AMERICAAND CARIBBEAN

16.11 GSM

U.S. & CANADA

371.24 GSM

MIDDLE EAST AND NORTH AFRICA

7.82 GSM

EUROPE

29.62 GSM

AFRICA

0.33 GSM

PACIFIC

0.24 GSM

SOUTH ASIA

16.92 GSM

EAST ASIA

56.59 GSM

CHINA TAIWAN1 6

3 8

4 9

5 10

2 7

34.62 CERTIFIED GSM931 PROJECTS

5.66 CERTIFIED GSM99 PROJECTS

34.39 CERTIFIED GSM2,586 PROJECTS

5.03 CERTIFIED GSM215 PROJECTS

15.90 CERTIFIED GSM644 PROJECTS

4.78 CERTIFIED GSM191 PROJECTS

7.43 CERTIFIED GSM380 PROJECTS

3.88 CERTIFIED GSM210 PROJECTS

5.95 CERTIFIED GSM97 PROJECTS

3.64 CERTIFIED GSM180 PROJECTS

CANADA GERMANY

INDIA TURKEY

BRAZIL SWEDEN

REPUBLIC OF KOREA

UNITED ARAB EMIRATES

LEED-CERTIFIED SPACE BY REGIONmeasured in gross square meters in millions

TOP 10 COUNTRIES AND REGIONS FOR LEED OUTSIDE THE U.S

(as of December 2016) Wellness in the workplace

As we spend over 90% of our time indoors, the building environment greatly affects our overall health. While green buildings achieve higher occupier productivity, a nascent trend of sustainability practices crossing over to wellness is coming to the fore. The WELL Building StandardTM, a performance based system that measures impact of built environment on human health, assesses and uses strategies to advance health, happiness, mindfulness and productivity in buildings and communities.

This trend is slowly penetrating the regional market with over 8 projects within UAE under certification, out of which 7 are in Dubai – prime examples are Du headquarters and Xworks, an interior fit-out firm, poised to be the first Wells certified offices in the Middle-East.

The concept of workplace wellness is not new, however, we are seeing a growing global trend of companies creating structured policies to distinguish themselves from competition and to attract talent. These policies are particularly popular amongst US and European blue-chip organisations who want to take their sustainability initiatives to the next level. Long-term strategies are usually incorporated from the start of design stages. Wellness programs have proven to be effective for employees - examples of these benefits include

higher brand value, less absenteeism and more productive teams. While there is no standard structure for establishing a workplace wellness program, organisations can incentivise employees with various strategies, as listed below. Some of these are easier to achieve through economies of scale.

Organisational level• Flexible working hours• Subsidised gym memberships or in-house fitness facilities• Access to healthy food options: fruit baskets, juice bar etc• Private/advanced health insurance• Concept of “switching off”

Design level• Workplace strategy: hot-desking, standing desk,

adjustable seat heights, break out areas etc• Circadian lighting• Ergonomics and intelligent interiors• Improved air and water quality • Thermal control for employees

Others• Wearable health technology• Team building fitness classes

Interestingly, despite being built as per LEED guidelines, headline rents are still at par with other non-certified Grade A stock. This can be explained by the fact that new developments are launching their initial phases at an attractive entry price point to achieve critical mass and pave way for future phases, where higher rentals may be justifiable. Secondly, these green developments still compete with established and centrally located non-certified Grade A stock. While global corporate occupiers value sustainability, a larger section of demand is yet to quantify environmental and operational benefits over rental costs. With the market progressively moving towards prime office stock and LEED certification expected to become a norm rather than a feature, this scenario is predicted to change as a gap starts to form in Grade A stock between certified and non-certified products.

H1 2017

Source: USGBC

Source: USGBC, Core Savills Research Under LEED certification Non certified

98

OutlookWe expect the residential market to start pricing sustainable increments only when they become a significant differentiating factor on their own. i.e. when all the basic building features are improved at a level where units cannot be differentiated between one another within a location.

The office market is expected to react faster as the majority of new prime supply offers green certified workplaces. Once the green building stock is completed and experiencing higher occupancy levels, we anticipate it will exert a downward pressure on rents across other Grade A stock within the vicinity.

SUSTAINABILITY AND WELLNESS IN DUBAI REAL ESTATE H1 2017

Very limited Limited Sizable section of the market Majority of the market

Residential type New sustainable homes Retrofitted sustainable homes Non sustainable prime residential

Non sustainable low-mid residential

Characteristics

Typically high build quality yet provides optimisation, in water and energy consumption and productive for users

High build quality products modified/upgraded to be sustainable in their building life cycle

Prime build quality products and finishes, although not having a sustainable building life cycle

Comparatively lower build quality and finishes

Smoke-free buildings and regulationsSmoke-free buildings are an additional characteristic to create a healthy community. In the past a number of fires caused by smoking have erupted in high-rise towers (The Torch in Dubai Marina, Tamweel Tower in JTL) which took years to renovate.A smoke-free policy can reduce the risk of fires in residential buildings and protect occupiers’ health, amongst other benefits.

Going smoke-free can influence bottom-line costs too. Tenants are in a favourable position to negotiate a lower insurance rate as the risk of fire is reduced and lower their maintenance fees such as AC cleaning. For landlords, a smoke-free building will add value to their asset, become an attractive amenity for future tenants and induce renovation cost savings in the long-term.

Organisations that choose to improve the quality of life of their employees introduce a smoke-free policy in the workplace for many reasons. Benefits for the business vary – staff members

Residential MarketThe current residential landscape largely consists of units which were built at a time when Dubai was an emerging market, at the surge of competing with global cities. Investors and end-users alike were not as discerning as they are today. A gap between these older and new developments has been forming, with a noticeable quality difference in build and finishing. This represents a pocket of opportunity in the market for landlords to upgrade their units to higher standards, by investing in refurbishments over and above their initial acquisition cost.

Anecdotal evidence suggests that typically, for every 1 Dh spentto renovate an old unit, the market will price the renovation and/or refurbishment at a ratio of 3:1. Hence, making every dirham invested above the acquisition price worth 3 to 4 times more when exiting. Landlords commonly resort to “easy wins” such as kitchen, bathrooms and flooring renovations to maximise their return on refurbishment cost.

However, there is a ceiling to how much a unit can be upgraded within a given location, after which it risks being pricedout of its submarket. Excessive upgrades will not be valued by the market (tenants or buyers alike) in a similar degree; it will eventually reach a point where the more one spends on upgrading a unit, the less marginal return (rent or price) it will incur.

For example, a large villa in The Springs (Type 1E or 2E) whenupgraded to a certain level, competes well with a non-upgradedvilla in The Meadows. Any further upgrading to the same unit will nevertheless price it out of its submarket, as it would then compete with an upgraded villa in The Meadows.

This illustrates the fact that the existing market has limited roomfor upgrades, hence basic refurbishments are largely preferredover sustainable and green renovations.

Few developers have started addressing this issue by bringing sustainable products to the market. Sustainable City, for instance, is a pioneer in green living in Dubai. Nevertheless, it is not commanding a distinctive premium over its peer communities in the vicinity, confirming the point illustrated above - although it certainly appeals to a limited market where occupiers are passionate about sustainable living.

For all these reasons, we do not foresee the residential market to witness a significant shift towards green initiatives. Until a large proportion of the market achieves these upgrades and reaches a higher level of uniform build and finishes quality, we do not expect owners to replace basic upgrades with more sophisticated building improvements such as energy efficiency and sustainability

are more productive and the number of smoking breaks reduces. Less chronic illness cases linked to smoking are recorded, which decreases sick leaves and overall workplace wellness.

Several international corporations have successfully deployed smoke-free policies over the past 15 years. They typically abide by 5 simple milestones or the “Gold Standard”: smoke-free workplace, healthy nutrition, physical activity, prevention (screening and early diagnostics) and health awareness. As a result, most have recorded less productivity loss annually, with 1/3rd to 1/2 less sick leave days a year amongst non-smokers than for their smoker colleagues.

Despite regulations led by the UAE Ministry of Health and their continued initiatives, this procedure is relatively under-implemented and not uniform. Recently, the Federal Tax Authority (FTA) announced a selective tax of 100/5 on tobacco to be applied in Q4 2017, another step in the right direction.

This upgrade typically does not makeeconomic sense as the residential product

would be priced out of its submarket

First wave, happening gradually

Second wave, a probability

Source: Core Savills Research

1110

62 OFFICESAMERICAS & CARIBBEAN

135 OFFICESUK, IRELAND & CHANNEL ISLANDS

103 OFFICESEUROPE

272 OFFICESMIDDLE EAST &AFRICA

134 OFFICESASIA PACIFIC

GLOBAL PRESENCEOVER 700 OFFICES AND ASSOCIATES WORLDWIDE

RECENT MARKETLEADING RESEARCH PUBLICATIONS

Core - UAE Associate of SavillsAs one of the largest UAE property services firms, Core, UAE Associate of Savills, combines expert local market insight with the international strength provided by over 700 offices globally.

Core’s multi-lingual advisers share an entrepreneurial spirit with a commitment to cultivating long-term, collaborative client relationships. Our local roots, commitment, and attention to detail are backed by the global standards of Savills’ 150-year-old brand, giving our clients direct access to 30,000 experienced practitioners, with a deep understanding of specialist real estate services in over 60 countries.

Our bespoke residential and commercial property advice enables our clients to make informed real estate decisions both locally and abroad, through a single point of contact in any of the 15 languages spoken by our consultants, in one of our 3 offices, in Downtown Dubai, Jumeirah Lakes Towers and Abu Dhabi.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Core, UAE Associate of Savills, accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Core’s research team. © Core Real Estate Brokers.

Edward MacuraPartner - Head of [email protected]

Dubai Residential Market Update Summer 2016

Core ResearchDubai Property

core-me.com

DUBAI PROPERTY REVIEW2016 AND BEYOND

RESIDENTIAL MARKET SUMMARY

OFFICE MARKET SUMMARY

2017 ANDBEYOND

core-me.com

DUBAI RESIDENTIAL MARKET UPDATE

core-me.com

Supply and Demand Dynamics

Sales and Rental Market Analysis

Ready and Off-plan Transaction Analysis

Dubai Residential Market vs. World Cities

Q1 2017

DUBAI OFFICE MARKET SPOTLIGHT

core-me.com

Prime and secondary office market dynamics

Evolution of office supply

Upcoming demand trends

Dubai as a global commercial investment destination

May 2017

Dubai Residential Market Sentiment Survey 2016

Core ResearchDubai Property

core-me.com

Executive SummaryDubai Office Market Update Q3 2016

core-me.com

Dubai Property

IN FOCUS:Capitalising on a bottoming marketAn investment guide Year end 2016

Core ResearchDubai Property

core-me.com

Dubai Office Market UpdateQ3 2016

In Focus: Capitilising on a bottoming marketYear end 2016

Dubai Property Review 2016 and beyond

Dubai Residential Market Update Q1 2017

Dubai Office Market Spotlight

Dubai Retail Review 2017

Abu Dhabi MarketReview 2016-2017

Dubai Residential Market Update Summer 2016

Executive Summary Dubai Residential Market Sentiment Survey

ABU DHABI MARKET REVIEW2016 - 2017

RESIDENTIAL MARKET SUMMARY 2016

RESIDENTIALOUTLOOK 2017

OFFICE MARKET REVIEW

AREASTO WATCH

core-me.com

DUBAI RETAIL REVIEW2017

Supply and demand dynamics

Dubai retail vs other global cities

Upcoming retail trends

Looking ahead

core-me.com

Joel McQueenDirector - Head of [email protected]

Mathilde MontelManager - Public [email protected]

Prathyusha GurrapuSenior Manager - Researchand [email protected]

Head Office

Ground Floor, Building 6,Emaar Square, Downtown Dubai,Dubai, UAE

Tel: +971 4 388 3339Fax: +971 4 388 3308Mail: [email protected]

DMCC Office

7H, Seventh Floor, Almas Tower,Jumeirah Lake Towers,Dubai, UAE

Tel: +971 4 423 9933Fax: +971 4 425 0099Mail: [email protected]

Abu Dhabi Office

Office No. RU 04, Abu Dhabi National Exhibition Centre (ADNEC), Al Khaleej Al Arabi Street, Abu Dhabi, UAE

Tel: +971 2 556 7778Fax: +971 2 659 4165Mail: [email protected]