Embed Size (px)

Citation preview

THE GREAT RECESSIONTHE GREAT RECESSIONAND THE DEVELOPING WORLDAND THE DEVELOPING WORLD

JOSÉ ANTONIO OCAMPOJOSÉ ANTONIO OCAMPO

COLUMBIA UNIVERSITYCOLUMBIA UNIVERSITY

FIVE PHASES OF THE CRISIS

Ag 07/Mar 08: Crisis in the market for asset-backed securities

Mar-Sept 14 08: Growing distrust in financial agents after collapse of Bear Stearns.

Sept 14-March 08: Global financial and economic collapse

2nd and 3rd quarters 09: “Green shoots”

Since 4th quarter 09: the return of global imbalances

The developing countries largely escaped the first two phases, were severely affected by the third, and had diverse outcomes during the fourth and fifth.

INDUSTRIAL PRODUCTION (1)

70

75

80

85

90

95

100

105

110

115

120

Jan

_0

6

Mar

_0

6

May

_0

6

Jul_

06

Sep

_0

6

No

v_0

6

Jan

_0

7

Mar

_0

7

May

_0

7

Jul_

07

Sep

_0

7

No

v_0

7

Jan

_0

8

Mar

_0

8

May

_0

8

Jul_

08

Sep

_0

8

No

v_0

8

Jan

_0

9

Mar

_0

9

May

_0

9

Jul_

09

Sep

_0

9

No

v_0

9

Advanced Economies Emerging Economies

INDUSTRIAL PRODUCTION (2)

70

75

80

85

90

95

100

105

110

115

120

Jan

_0

6

Mar

_0

6

May

_0

6

Jul_

06

Sep

_0

6

No

v_0

6

Jan

_0

7

Mar

_0

7

May

_0

7

Jul_

07

Sep

_0

7

No

v_0

7

Jan

_0

8

Mar

_0

8

May

_0

8

Jul_

08

Sep

_0

8

No

v_0

8

Jan

_0

9

Mar

_0

9

May

_0

9

Jul_

09

Sep

_0

9

No

v_0

9

Asia Central and Eastern Europe

Latin America Africa and Middle East

WHY WAS THIS NOT A GREAT DEPRESSION?

Adoption of the most massive Keynesian package in history, by developed and several developing countries (with great diversity).

Massive financial bailouts (helped to avoid further recession, but have not contributed to the recovery)

Existence of an alternative engine: a large economy (China) that the space and willingness to adopt strongly expansionary policies.

… but risks are still present!

Remittances: affected migrants to the US, Europe and Russia, not the Gulf countries, and mainly small economies

Financial conditions generated a sharp but short effect, that affected mainly middle-income countries

The trade shock (in volume and price terms) has been more severe, and affected all countries

THE TRANSMISION OF THE CRISIS

COUNTRIES SEVERELY AFFECTED BY FALL IN REMITTANCES

CountryImpact% GDP

Tajikistan -14.2%

Moldova -6.7%

Kyrgyz Republic -5.0%

Armenia -2.7%

Honduras -2.1%

Jamaica -1.7%

El Salvador -1.6%

Georgia -1.5%

Tonga -1.4%

Morocco -1.4%

Haiti -1.1%

Guyana -1.1%

Azerbaijan -1.0%

Guatemala -1.0%

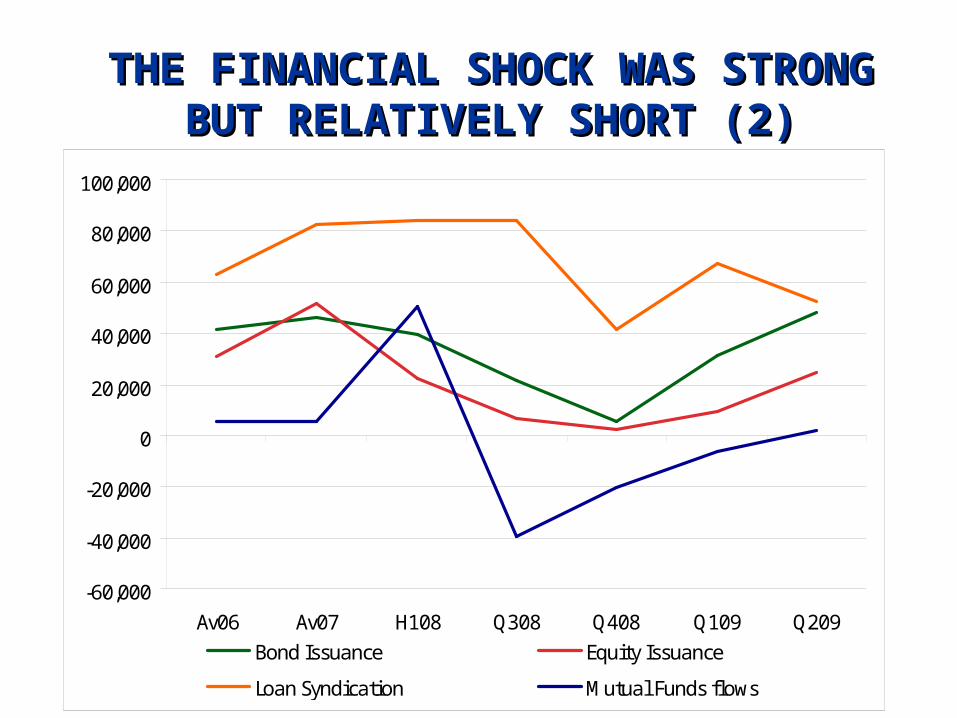

THE FINANCIAL SHOCK WAS STRONG THE FINANCIAL SHOCK WAS STRONG BUT RELATIVELY SHORT (1)BUT RELATIVELY SHORT (1)

Emerging Markets' Spreads and Yields, 1998-2010

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

1-Ja

n-98

1-Ja

n-99

1-Ja

n-00

1-Ja

n-01

1-Ja

n-02

1-Ja

n-03

1-Ja

n-04

1-Ja

n-05

1-Ja

n-06

1-Ja

n-07

1-Ja

n-08

1-Ja

n-09

1-Ja

n-10

Spreads Yields

THE FINANCIAL SHOCK WAS STRONG THE FINANCIAL SHOCK WAS STRONG BUT RELATIVELY SHORT (2)BUT RELATIVELY SHORT (2)

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

Av06 Av07 H108 Q308 Q408 Q109 Q209Bond Issuance Equity Issuance

Loan Syndication Mutual Funds flows

WORLD TRADE COLLAPSED, AND WORLD TRADE COLLAPSED, AND HAS NOT FULLY RECOVERED (1)HAS NOT FULLY RECOVERED (1)

70.00

75.00

80.00

85.00

90.00

95.00

100.00

105.00

110.00Ja

n_06

Mar

_0M

ay_0

Jul_

06Se

p_06

Nov

_0Ja

n_07

Mar

_0M

ay_0

Jul_

07Se

p_07

Nov

_0Ja

n_08

Mar

_0M

ay_0

Jul_

08Se

p_08

Nov

_0Ja

n_09

Mar

_0M

ay_0

Jul_

09Se

p_09

Nov

_0

Advanced Economies Emerging Economies

WORLD TRADE COLLAPSED, AND WORLD TRADE COLLAPSED, AND HAS NOT FULLY RECOVERED (2)HAS NOT FULLY RECOVERED (2)

70.00

75.00

80.00

85.00

90.00

95.00

100.00

105.00

110.00

Jan_

06M

ar_0

6M

ay_0

6Ju

l_06

Sep_

06N

ov_0

6Ja

n_07

Mar

_07

May

_07

Jul_

07Se

p_07

Nov

_07

Jan_

08M

ar_0

8M

ay_0

8Ju

l_08

Sep_

08N

ov_0

8Ja

n_09

Mar

_09

May

_09

Jul_

09Se

p_09

Nov

_09

Asia Central and Eastern EuropeLatin America Africa and Middle East

THE TRADE SHOCK HAD DIVERSETHE TRADE SHOCK HAD DIVERSEEFFECTS ACCORDING EFFECTS ACCORDING

TO SPECIALIZATION PATTERNSTO SPECIALIZATION PATTERNS

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

All DevelopingCountries

Energy(>40%)

Mineral( >40% )

Agricult. ( >40% )

Manufact ( >50% )

Diversif.

2001-07

2008

2009

2010

Greater policy space thanks to improvements in external balance sheets of countries (except in Central and Eastern Europe)

This was reflected in reduction in interest rates and reserve requirements, and foreign exchange interventions.

Public sector banks played a positive role, high dependence on external funding for banks a very negative one.

The fiscal space was also used by many, but not all countries. East Asia and the Gulf were aggressive; South Asia went ahead despite weak fiscal situation; Latin America and Africa are more mixed stories.

COUNTER-CYCLICAL POLICIES

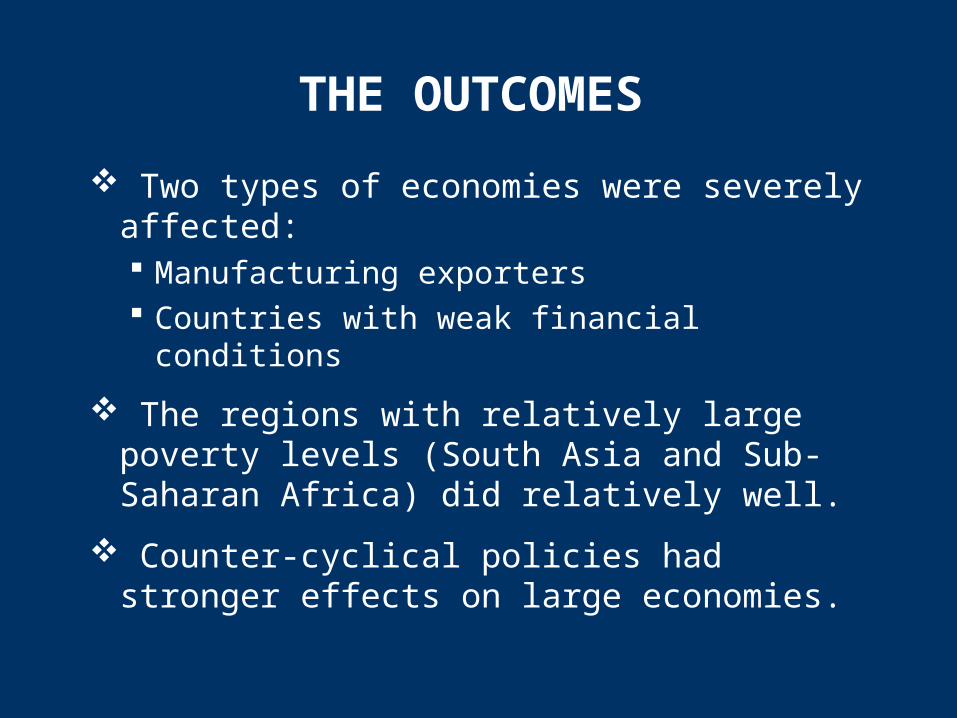

THE OUTCOMES

Two types of economies were severely affected: Manufacturing exporters Countries with weak financial conditions

The regions with relatively large poverty levels (South Asia and Sub-Saharan Africa) did relatively well.

Counter-cyclical policies had stronger effects on large economies.

REGIONS WITH GOOD OR FAIR PERFORMANCE

0.00 2.00 4.00 6.00 8.00 10.00 12.00

China

South Asia

Africa

Western Asia, exclTurkey

2003-07

2009

REGIONS WITH POOR PERFORMANCE

-8.00 -6.00 -4.00 -2.00 0.00 2.00 4.00 6.00 8.00 10.00

East Asia, excl.China

Latin America

New EU members

TransitionEconomies

2003-07

2009

SOCIAL OUTCOMES

Around 80 million additional indigents, relative to a situation of continued growth.

This does not affect much the MDG targets.

Unemployment effects have been very diverse, largely concentrated in transition economies and, lo a lesser extent, Latin America. Loss of employment in manufacturing exports was very important worldwide.

Informal employment/working poor, and the lack of social protection are more important issues in developing countries.

WITH FEW EXCEPTIONS, GAINS IN REDUCING THE WORKING POOR

WERE REVERSED

0

10

20

30

40

50

60

70

80

90

2003

2008

2009

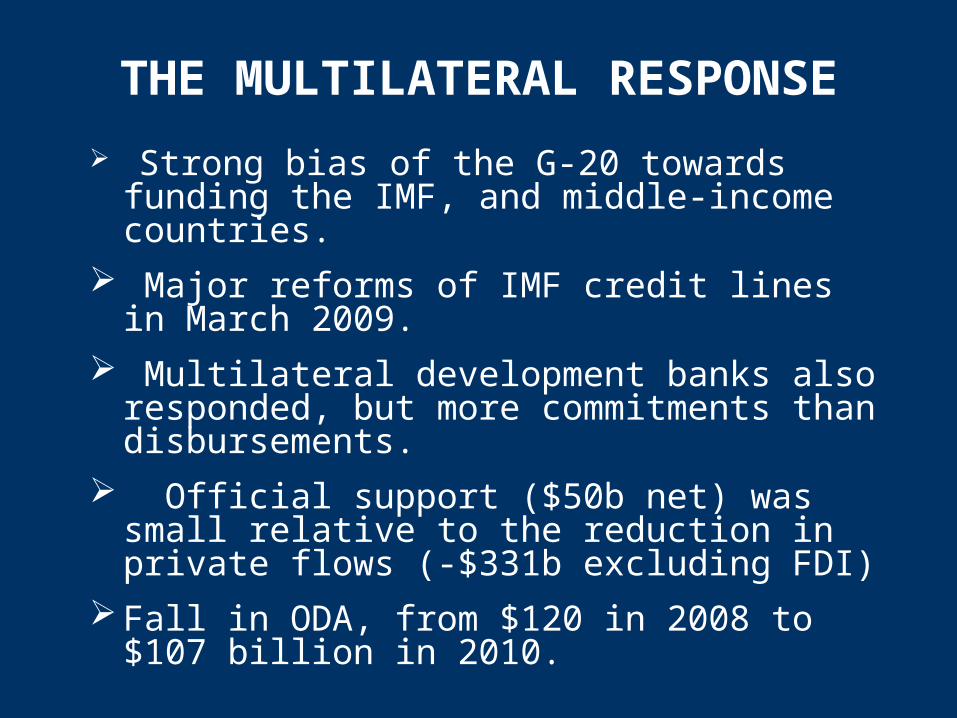

THE MULTILATERAL RESPONSE

Strong bias of the G-20 towards funding the IMF, and middle-income countries.

Major reforms of IMF credit lines in March 2009.

Multilateral development banks also responded, but more commitments than disbursements.

Official support ($50b net) was small relative to the reduction in private flows (-$331b excluding FDI)

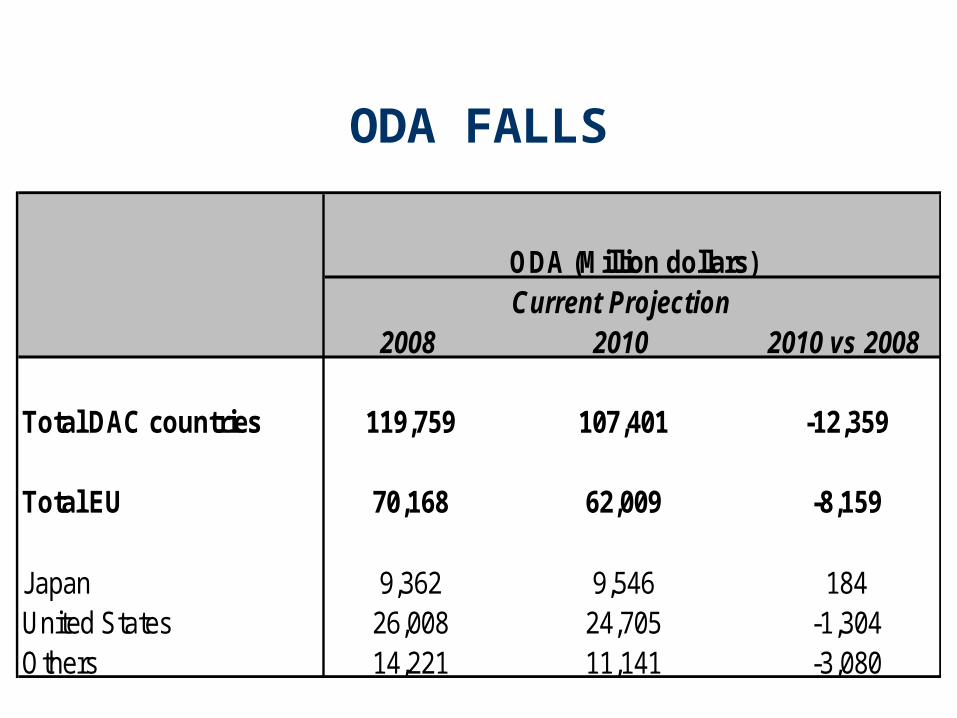

Fall in ODA, from $120 in 2008 to $107 billion in 2010.

WORLD BANK: LARGE INCREASE IN COMMITMENTS, LIMITED

DISBURSEMENTS

-3,000

-1,000

1,000

3,000

5,000

7,000

9,000

2004-08 Average 2009 2004-08 Average 2009 2004-08 Average 2009

IBRD and IDA commitments Gross disbursements Net Flows in repayments & interest

Asia Pacific Africa South Asia Latin America & Carr. East & Central Europe MENA

ODA FALLS

Current Projection2010 2010 vs 2008

Total DAC countries 119,759 107,401 -12,359

Total EU 70,168 62,009 -8,159

Japan 9,362 9,546 184United States 26,008 24,705 -1,304Others 14,221 11,141 -3,080

ODA (Million dollars)

2008

Mainstreaming counter-cyclical policies.

Time to look back at the domestic market, even to inward-looking strategies?

Since this has a bias in favor of large countries, a role for regional integration.

Placing employment generation at the center of all macro policies

And creating or improving social protection systems

RETHINKING THE PARADIGM

MAJOR GLOBAL ISSUES

How to avert early withdrawal of stimulus, and stable reform of finance.

If China is going to lead, how is it going to disseminate its growth to other economies?

Disorderly capital flows towards developing countries: the time to go back to capital controls?

Who is going to give confidence that countries running current account deficits would not face problems in the future?

How are the benefits from the new world growth pattern to be shared?

THE GREAT RECESSIONTHE GREAT RECESSIONAND THE DEVELOPING WORLDAND THE DEVELOPING WORLD

JOSÉ ANTONIO OCAMPOJOSÉ ANTONIO OCAMPO

COLUMBIA UNIVERSITYCOLUMBIA UNIVERSITY