Embed Size (px)

Citation preview

1

THE GOODS AND SERVICES TAX APPEAL TRIBUNAL OF MALAYSIA

CASE NO.18 OF 2016 ,GOODS AND SERVICES TAX APPEAL TRIBUNAL

BETWEEN

GEOWSSB ….. APPELLANT

AND

THE DIRECTOR GENERAL OF CUSTOMS ….. RESPONDENT

Before : PUAN ASLINA JONED ….. CHAIRMAN (SITTING ALONE)

Venue : THE CUSTOMS APPEAL TRIBUNAL COURT OF MALAYSIA,

PUTRAJAYA

Dates of Mention : 17.03.2016

Dates of Hearing : 26.04.2016, 18.05.2016 and19.05. 2016

THE APPEAL

This was an appeal made pursuant to subsection 126(1) of the Goods

and Services Tax Act 2014 [Act 762] by GEOWSSB hereinafter referred

to as the Appellant, against the decision of the Honourable Director

General of Customs dated 15th January 2016 hereinafter referred to as the

Respondent.

2

THE FACTS

The Appellant is a company incorporated in 1999 which carries on a

business providing diagnostic, rapid response rectification, maintenance

and overhaul of commercial aircraft engine. The Appellant’s sister company,

GEESM carries out repair, maintenance and installation services for

aircrafts.

Sometime in 2005, the Appellant secured a 20 year contract with Air Asia to

repair and maintain the latter’s fleet of aircrafts. As GEESM is a joint

venture company owned by Malaysia Airline System Berhad (MAS) by 30%

share, the Agreement was entered between Appellant and Air Asia in order

to maintain commercial independence. As the Appellant does not hold the

requisite DCA Certification, the actual work for repair, maintenance and

installation is subcontracted to GEESM. (the Agreement)

On 1st April 2015, the Goods and Services Tax Act 2014 [Act 762] came

into force. The Appellant upon consulting its tax advisors, took the position

that the Agreement is a supply which qualifies for zero rated under para 3,

item 1(d) Second Schedule of GST (Zero-Rated Supply) Order 2014.

On 7th July 2015, the Director General of Customs issued a DG’s Decision

6 of 2015 suggesting an unclear position where contracted supplier of the

service outsources the work to a third party who holds the DCA certification.

Concerned, the Appellant consulted its advisors and wrote a letter to the

Respondent dated 26th March 2015 mentioning that the legal position is

clear and the supply pursuant to the Agreement qualifies as a zero rated

supply. The Appellant’s tax representative, Pricewaterhouse Coopers

Taxation Services Sdn. Bhd. also wrote a letter to the DG of Customs dated

4th December 2015 attaching the letter dated 26th March 2015.

3

The DG of Customs responded to those letters by issuing a letter dated 15th

January 2016 confirming that the supply made was subject to the standard

rate GST of 6%. The letter is reproduced as follows :

4

Dissatisfied with the DG’s decision, the Appellant filed an appeal at the

Tribunal on 17th January 2016.

5

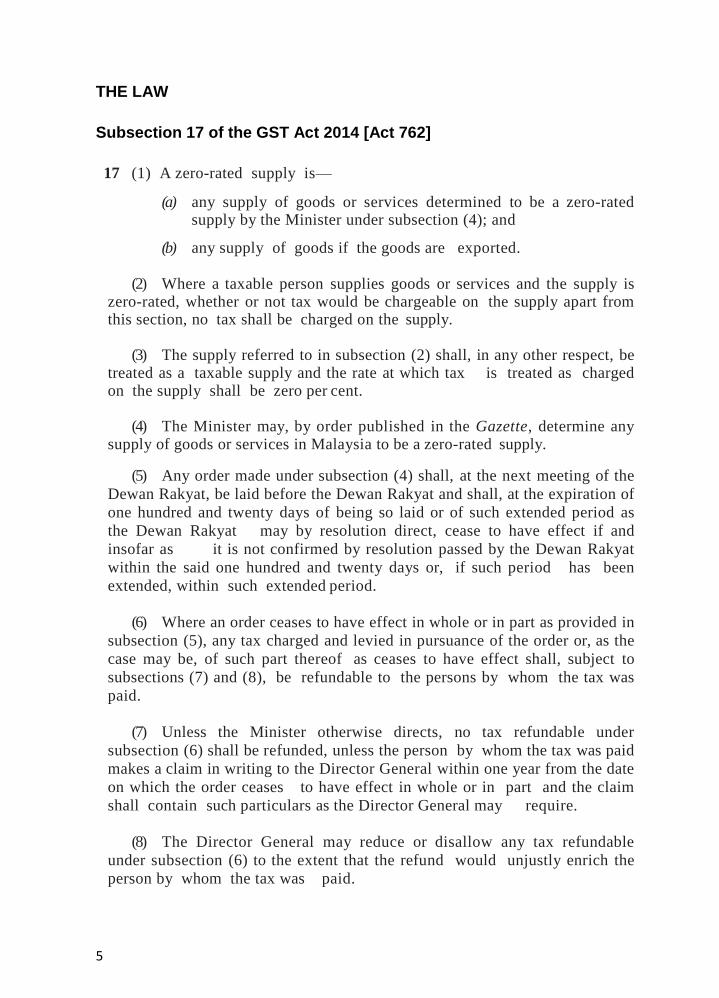

THE LAW

Subsection 17 of the GST Act 2014 [Act 762]

17 (1) A zero-rated supply is—

(a) any supply of goods or services determined to be a zero-rated supply by the Minister under subsection (4); and

(b) any supply of goods if the goods are exported.

(2) Where a taxable person supplies goods or services and the supply is zero-rated, whether or not tax would be chargeable on the supply apart from this section, no tax shall be charged on the supply.

(3) The supply referred to in subsection (2) shall, in any other respect, be treated as a taxable supply and the rate at which tax is treated as charged on the supply shall be zero per cent.

(4) The Minister may, by order published in the Gazette, determine any supply of goods or services in Malaysia to be a zero-rated supply.

(5) Any order made under subsection (4) shall, at the next meeting of the

Dewan Rakyat, be laid before the Dewan Rakyat and shall, at the expiration of

one hundred and twenty days of being so laid or of such extended period as

the Dewan Rakyat may by resolution direct, cease to have effect if and

insofar as it is not confirmed by resolution passed by the Dewan Rakyat

within the said one hundred and twenty days or, if such period has been

extended, within such extended period.

(6) Where an order ceases to have effect in whole or in part as provided in

subsection (5), any tax charged and levied in pursuance of the order or, as the

case may be, of such part thereof as ceases to have effect shall, subject to

subsections (7) and (8), be refundable to the persons by whom the tax was

paid.

(7) Unless the Minister otherwise directs, no tax refundable under

subsection (6) shall be refunded, unless the person by whom the tax was paid

makes a claim in writing to the Director General within one year from the date

on which the order ceases to have effect in whole or in part and the claim

shall contain such particulars as the Director General may require.

(8) The Director General may reduce or disallow any tax refundable

under subsection (6) to the extent that the refund would unjustly enrich the

person by whom the tax was paid.

6

(9) Where any goods are claimed to have been or were to be exported

and the supply of the goods is a zero-rated supply, not being goods zero-

rated if supplied for home consumption and—

(a) the goods are found in Malaysia after the date on which they were

claimed to have been or were to be exported; and

(b) the presence of the goods in Malaysia after that date has not been

approved by the Director General,

the tax that would have been chargeable on the supply but for the zero-

rating shall become due and payable forthwith by the supplier or by any

person in whose possession the goods are found in Malaysia and the goods

may be liable to seizure under this Act.

Item 1(d) Second Schedule of Goods and Services Tax (Zero-Rated

Supply) Order 2014

1. The following services which its supply directly benefit a person wholly in his

business capacity (and not in his private or personal capacity)

(d) repair, maintenance and installation services supplied in relation to a ship

or aircraft including parts incorporated.

Section 5 of the Goods and Services Tax Act 2014

5. (1) The Director General shall have the superintendence of all matters

relating to goods and services tax, subject to the direction and control of the

Minister.

(2) subject to the general direction and supervision of the Director

General, a senior officer of goods and services tax shall have and exercise all

powers conferred on the Director General under this Act other than those

conferred by sections 8, 62, 76, 77, 172 and 173.

(3) Any person other than an officer of customs may be appointed by or

employed with the concurrence of the Director General for any duty or service

relating to goods and services tax and the person shall be deemed to be an

officer of goods and services tax.

(4) The Director General may, by authorization in writing, confer on any officer of goods and services tax not being a senior officer of goods and

7

services tax all or any of the powers of a senior officer of goods and services tax for a period not exceeding ninety days in respect of any one authorization.

(5) Any officer of goods and services tax shall have the duties and powers to enforce and ensure due compliance with the provisions of this Act.

THE STANDARD OF PROOF

Act 762 does not stipulate the standard of proof to be imposed on disputing

parties in appeal cases argued before the Tribunal. However Section 149 of

Act 762 empowers this Tribunal to adopt such procedures as it thinks fit and

proper. Since the issues at hand are civil in nature, this Tribunal is of the

view that standard of proof applied in the civil courts which is to prove one’s

case on the balance of probabilities should be adopted. This standard of

proof is lighter as compared to standard of proof imposed on criminal cases

which is beyond reasonable doubt.

Pursuant to regulation 11(2) Goods and Services (Review and Appeal)

Regulation 2014, the Appellant has to start its case first followed by the

Respondent which is similar to appeal procedures in the higher courts.

The manner of sequence laid down by regulation 11 (2) implicitly imposes

the burden of proof on the Appellant to prove its case on the balance of

probabilities. Furthermore it is the duty of the Appellant to convince this

Tribunal that the disputed decision of the DG is wrong and ought to be

varied or set aside and substituted with a decision in its favour.

8

DECISIONS FROM OTHER JURISDICTION

The book Tolley’s Vat Cases 2015, Thirtieth Edition by Rhianon Davies

and David Rudling, compiles a plethora of cases discussing issue

concerning the identity of the person making supplies. For ease of

reference four related cases are hereby reproduced:

A company (N) operated a driving school. It provided the instructors who

worked for it with dual-control cars, for which it paid the insurance, car tax

and repairs. The instructors paid for petrol, oil and cleaning. The

instructors collected the fees and pair part of them to N. Until March 1977

these arrangements were not committed to writing, but thereafter each

instructor was required to sign a document headed ‘Conditions of

Employment’ providing, inter alia, for ‘commission’ to be paid to the

instructors and including the statement : ‘you are self-employed therefore it

is your responsibility to pay your tax and stamp your card.’ The instructors

were accepted as self-employed for income tax and national insurance

purposes. The tribunal held on the evidence that until March 1977 the

instructors provided the tuition as independent contractors, but that

thereafter they were employees of N, so that N was required to account for

VAT on the full amount of the tuition fees. New Way School of Motoring

Ltd, (1979) VATTR 57 (VTD 724) [New Way]

A trader (R) was the sole proprietor of four driving schools in different cities,

and was the controlling director of a company which also owned a driving

school. Instructors at the five schools were employed under franchise

agreements, by which they were to pay the schools on agreed weekly fee

and keep any remaining fees for themselves. However in practice, the

instructors paid the whole of their receipts to the school, which then returned

some of the receipts to the instructors. Customs issued assessments on

the basis that the driving tuition at the schools was provided by the schools.

9

R and the company appealed, contending that the tuition was provided by

the instructors rather than by the schools. The tribunal dismissed the

appeals holding on the evidence that pupils contracted for their tuition with

the schools and not with individual instructors. The instructors were agents

of the schools, and it was the schools which provided the tuition. E Reeds,

MAN/84/270 & MAN/86/105; Reeds School of Motoring (Nottingham)

Ltd, MAN/86/103 (VTD4578). [Reeds School Nottingham]

The decision in Reeds and Reeds School of Motoring (Nottingham) Ltd,

were not followed in subsequent case involving an associated company

which provided driving tuition in a different area. Payments were made to a

third company in the same ownership, rather than to the individual

instructors. The tribunal chairman (Mr. Simpson, sitting alone) held on the

evidence that the instructors were making supplies of driving tuition as

independent principals. The company’s role was ‘to provide a supporting

organization by which the instructors were provided with the means to give

tuition.’ The chairman observed that the tight control which the appellant

maintained over the instructor, ‘which in earlier days might have been

argued to suggest that the instructor’s business was really the appellant’s is

nowadays a common characteristic of franchise agreements, where the

franchisor does not carry on the business in question,’ but instead ‘licenses

another to do so under a name and method of operation which are, or are

intended to be, distinctive and well-known.’ The third company ‘was a mere

depositary, notwithstanding that it was controlled by (the same directors)

and that it acted on the instructions of the appellant.’ Reeds School of

Motoring (Sheffield) Ltd, MAN92/85 (VTD 13404). [Reeds School

Sheffield]

A trader (C) who owned a driving school appealed against a decision that

he should be registered for VAT, contending that the driving tuition was

provided by the individual instructors and that he was not liable to account

10

for VAT on takings which they retained. The tribunal dismissed his appeal,

applying New Way School of Motoring Ltd. C owned the cars, all of which

bore the name of the driving school. Although the instructors were

independent contractors, they were supplying the services of tuition on

behalf of C. The QB upheld this decision. On the evidence, the tribunal had

been justified in reaching the conclusion that the tuition was supplied by C.

J Cronin (t/a Cronin’s Driving School) v C & E Commrs, QB (1991) STC

333. (C.J Cronin) [C J Cronin]

Remarks :

1. The cases discussed above are persuasive judicial precedents which

may be adopted as a guidance in Malaysia since the Malaysian GST

Appeal Tribunal was only recently set up on 1st April 2015.

2. Even though the principle of the cases are not directly on point they

could serve as a guidance to show that Tribunals in other jurisdiction

do recognize business practices whereby supply may not always be

made directly by the tax payer. This includes concepts of agent,

franchise arrangement, subcontract agreement and the like.

THE SUBMISSION

The learned Counsel for the Appellant argued that Act 762 provides that

only the Minister has powers to make any determination pertaining to zero

rated supplies. He found support for his argument through subsections

17(1), (4) and (5) of the GST Act 2014 (Act 762).

He further argued that the DG is acting illegally by attempting to usurp the

power of the Minister through its invocation of the DG’s Decision No 6 of

2015. In doing so he relied on section 5 of Act 762.

11

The learned Counsel reiterated that the DG is not empowered to decide

what requirements are needed to qualify for zero rating of the Appellant’s

supplies. To prove his points he cited the cases of :

a. Kerajaan Malaysia v Wong Pot Heng (1997) 1 MLJ 437 [Wong

Pot Heng]

b. Majlis Agama Islam Wilayah Persekutuan v Victoria Jayaseele

(2016) 4 CLJ12 [MAIWP]

c. WT Ramsay Ltd v Inland Revenue Commission (1982) AC 300

[Ramsay]

d. Palm Oil Research and Development Board Malaysia & Asia v

Premium Vegetable Oils Sdn. Bhd. to another appeal (2005) 3

MLJ 97 [PORIM]

The learned Tribunal Officer for the Respondent pointed out that the role of

the DG under Act 762 is to ensure compliance of the Act. The learned

Tribunal Officer invited this Tribunal to agree with her that the DG’s decision

dated 15th January 2016 is correct in that the Appellant is subject to

standard rated GST as it does not hold a certificate of approval from the

Department of Civil Aviation. She also argued that the supply made by the

Appellant does not qualify as zero rated supply under para 3 item 1(d)

Second Schedule of GST (Zero-Rated Supply) Order 2014.

To support her argument she relied on the strength of :

a. subsection 2(1), sub section 5(1) and sub section 197(1) Act 762

b. para 3 Item 1(d),Second Schedule GST (Zero-Rated Supply)

Order 2014.

12

Further support was also found from the following authorities :

a. PORIM, supra

b. Wong Pot Heng,supra

c. Tan Seng Tin 2 Ors v PP (1970) 1 MLJ100

d. DG’s Decision No. 6 of 2015 dated 7th July 2015.

THE EVALUATION OF EVIDENCE AND FINDINGS

This Tribunal appreciates the in-depth research done by both learned

Counsel for the Appellant and learned Tribunal Officer for the Respondent

through their written submission. This Tribunal acknowledges that the

undisputed facts in this case are as follows:

The Appellant carries on a business of providing diagnostic, rapid response

rectification, maintenance and overhaul of commercial aircraft engine. Vide

a 20 year contract it supplied the services to Air Asia to maintain the latter’s

fleet of aircrafts. However the Appellant does not hold a certificate of

approval from the Department of Civil Aviation (DCA Certification). As such

the actual work for repair, maintenance and installation was subcontracted

to the Appellant’s sister company, GEESM.

Following the issuance of DG’s Decision No 6 of 2015, the Appellant

wrote a letter to the Respondent seeking a confirmation as follows:

“Our request.

We seek confirmation that our supply of repair, maintenance and installation

services of aircraft engines qualifies for zero-rating, on the basis that the

third party physically performing these services under a subcontracting

arrangement, holds the requisite certification.”

13

Vide letter dated 15th January 2016, the Respondent confirms that the

services supplied by the Appellant is subject to standard rated GST of 6%

as it does not hold a certificate of approval from DCA.

The role of a GST Tribunal is to hear and make decision on any appeal

against the decision of the Director General of Customs (The Respondent)

in respect of goods and service tax as stipulated by section 127(1) of Act

762.

Based on the matrix of facts presented during the proceedings, this Tribunal

warns itself that in order to arrive to a fair decision three (3) pertinent

questions have to be asked. The questions are as follows :

1) Is the Appellant a taxable person making a supply within Act 762?

2) Was the supply made a taxable supply which qualifies as a zero

rated GST?

3) Was the DG’s decision dated 15th January 2016 correct?

(1) Is the Appellant a “taxable person” making a supply?

Section 2 of Act 762 defines taxable person as:

“Taxable person means any person who is registered under Part IV”.

Part IV obligates registration of taxable person who makes total annual

supply of more than RM500,000.00 [Refer to (a) subsection 20(1) and

20(3)(a) of Act 762 and (b) Goods and Services Tax (Amount Taxable

Supply) Order 2014].

Section 4 of Act 762 defines supply as

4 (1) “subject to subsections (2) and (3), supply means all forms of supply,

including supply of imported services, done for a consideration and anything

14

which is not a supply of goods but is done for a consideration is a supply of

services”.

Under intense cross examination, the Respondent’s First Witness (SR1)

agreed that there is a sub-contract agreement between the Appellant and

GEESM to supply the services of repair, maintenance and installation of

aircraft to Air Asia. SR1 also agreed that there are two separate

arrangements under the sub-contract agreement. Under the first

arrangement, the Appellant bills Air Asia for the services and Air Asia will

then make the payment to the Appellant. Under the second agreement,

GEESM will then bill the Appellant for the services made to Air Asia on its

behalf.

SR1 also agreed to Counsel’s suggestion that in the DG’s letter, there was

no mention that the Appellant did not make any supply. He also admitted

that GEESM was given the certificate of approval by DCA and it is indeed

carrying out services of repair, maintenance and installation of aircraft.

SR1 also agreed that para 3 item 1(d) Second Schedule of the GST

(Zero-Rated Supply) Order 2014 did not state that such repair,

maintenance and installation services could not be sub-contracted.

The Respondent’s second witness (SR2) also agreed under cross

examination that the Appellant had subcontracted the service for repair,

maintenance and installation of aircrafts to GEESM and that it is an agent to

the Appellant. She further agreed that GEESM carries out such services for

Air Asia on behalf of the Appellant. She agreed in unison with SR1 that

para 3 item 1(d) of GST (Zero-Rated Supply) Order 2014 did not mention

that such services could not be sub contracted.

It is an undisputed fact that the Appellant does carry out a business of

repair, maintenance and installation services supplied in relation to a ship or

15

aircraft including parts incorporated as provided by para 3 item 1(d) of the

Second Schedule of the GST (Zero-Rated Supply) Order 2014 read with

subsection 17(1)(a) and 17 (4) of Act 762. Based on the

correspondences between both parties in this case, this Tribunal is satisfied

that the Appellant is a registered person holding GST No:001365442560.

This fact was neither disputed in the letter dated 15 January 2016 nor during

the proceedings before the Tribunal.

In sum this Tribunal finds that the Appellant has proven that it is indeed a

taxable person making a supply as contemplated by Act 762.

(2) Was the supply made a taxable supply which qualifies a zero rated

GST?

The Tribunal Officer pointed out that the Appellant does not qualify for zero-

rated GST treatment as the Appellant does not supply the services of repair,

maintenance and installation of aircraft directly to Air Asia. Instead the

Appellant supplied the services through a sub contract agreement to a 3rd

party i.e GEESM. She argued that the GST (Zero-Rated Supply) Order

2014 should be read literally to the effect that the services cannot be

subcontracted in order to qualify as zero-rated supply.

Counsel for the Appellant whilst citing the case of PORIM,supra responded

by stating that the case law authorities on this point are clear and must be

read strictly.

With respect this court does not agree with the Tribunal Officer’s argument.

A closer scrutiny of the DG’s letter dated 15th January 2016 at para 2

reveals that the DG at the point of making the decision agreed that para 3,

item 1(d) Second Schedule of (Zero-Rated Supply) Order 2014 does not

have any physical restriction or requirement confined to the supplier of

services. The said para is reproduced as follows:

16

“Dimaklumkan bahawa perkhidmatan pembaikian, penyenggaraan dan

pemasangan yang dibekalkan berhubung dengan sesuatu pesawat udara

termasuk alat ganti yang digabungkan, yang pembekalannya (dan bukan

dalam kapasiti peribadi atau persendiriannya) adalah berkadar sifar,

berdasarkan Jadual Kedua, Butiran 1(d) Perintah Cukai Barang dan

Perkhidmatan (Pembekalan Berkadar Sifar) 2014. Butiran ini secara amnya

tidak mempunyai sekatan atau keperluan yang terhad kepada pembekal

perkhidmatan secara fizikal.”

This Tribunal finds that the statement at para 2 of the letter is an

acknowledgement by the DG that the law does not impose the requirement

that a direct supply of services must be made. As such the Tribunal

Officer’s argument to the contrary does not hold water. The Respondent’s

argument in respect of this issue must be confined to the clear wordings of

the letter dated 15th January 2016. The Tribunal Officer should not advance

an argument which was not the basis of the DG’s decision in the letter at the

time of making it.

Neither Act 762 nor GST (Review and Appeal) Regulation 2014 obligates

the Respondent to file a notice of reply/defence as a pleading. However

based on the arguments before this Tribunal it is clear that the Respondent

relied solely on the decision of the DG vide letter dated 15 January 2016 as

the basis of their reply/defence. As the Respondent’s case is premised on

the DG’s decision vide the said letter, any argument which is beyond what is

stated in the letter is not acceptable. The said letter is the basis of the

Respondent’s case which acts as the Respondent’s pleadings in the

absence of one. A pleadings ensures that the parties state their cases

from the onset of hearing and do not lose sight of the issues at hand

throughout the trial. It serves to prevent surprises from being sprung upon

the opposing side. Hence, the importance of the principle that a party has to

be bound by its own pleadings can never be stressed enough. The

17

Tribunal would be guided in making a decision within the confines of both

parties’ pleadings.

To this end the Tribunal is bound by the decision of the Court of Appeal in

another Tribunal in Ranjit Kumar A/P S. Gopal v Hotel Excelsior (2011) 3

AMR 38 whereby his Lordship Arifin Zakaria CJ, Mohd Ghazali Mohd

Yusof and Raus Sharif, FCJ held :

“………. pleadings in the industrial courts are as important as in the Civil

Courts. Section 30(5) of the act could not be used to override or

circumvent the basic rules of pleadings.[Ranjit Kumar]

In the case of Ramachandran, R v Industrial Court of Malaysia and Anor

(1997) 1 CLJ 147, the Court of Appeal has this to say :

“it is trite law that a party is bound by its pleadings. The Industrial Court

must scrutinize the pleadings and identify the issues, take evidence, hear

the parties arguments and finally pronounce its judgement having strict

regards to the issues.”[Ramachandran]

The Tribunal finds that the Appellant had complied with the requirement of

para 3, Item 1(d) Second Schedule of the GST (Zero-Rated Supply)

Order 2014 which states :

1. The following services which its supply directly benefit a person

wholly in his business capacity (and not in his private of personal

capacity)

(d) repair, maintenance and installation services applied in relation to

a ship or aircraft including parts incorporated.

Against this backdrop, this Tribunal holds that the Appellant has

successfully proven on a balance of probability that it is indeed carrying

18

out services which qualifies for zero-rated GST as determined by para 3

item (1)(d) of the GST ( Zero-Rated Supply) Order 2014.

(3) Was the DG’s decision dated 15 January 2016 correct?

As the first and second questions have been answered in the affirmative,

this Tribunal will now look at the third question. Was the DG correct in

invoking DG’s Decision 6/2015 by stating at para 3 and 4 of his letter dated

15th January 2016 that the Appellant’s supply of such service is subject to

standard rated of GST at 6%? The reason given by the DG was that the

services contemplated by para 3 item (1)(d) Second Schedule of the Zero

Rated Order 2014 only applies to supply made by someone who holds the

approval certificate from the DCA. As the Appellant does not hold the

certificate, it is not entitled for zero rated GST.

Having heard submissions by both counsel and Tribunal Officer, this court

agrees that the DG does not have the power to make decision pertaining

to zero-rated supplies. A cursory look at subsection 17(4) and 17(5) of Act

762 show that the law confers the powers to the Minister (and not the DG)

to determine any supply to be a zero-rated supply. This determination must

be tabled before the Dewan Rakyat and later gazetted as a legally binding

subsidiary legislation.

The Tribunal is bound by Federal Court’s decision in PORIM which is clear

on this point as follows :

“In Malaysia, the Federal Constitution has entrusted the law making

power to Parliament and the State Assembly of each of the several states of

the Federation. While the courts through the common law recognize the

power of Parliament to delegate some of its legislative power, it is equally

the constitutional duty of the courts to ensure that no excessive delegation

19

takes place. Hence the well settled principle that provision in a statute

conferring power on a member of the Executive to enact subsidiary

legislation must be construed strictly. This is particularly so where the

subsidiary legislation is one that imposes a financial levy – call it a tax or

charge or less or whatever you may upon the whole or any section of the

public.”

“In Wong Pot Heng,supra the Federal Court opined that a person is

empowered to make subsidiary legislation only when the Parent Act

provided the person with such powers.”

This Tribunal agrees with the Counsel for the Appellant that neither Act 762

nor the GST (Zero-Rated Supply) Order 2014 delegates any power to the

Respondent to make any subsidiary legislation to govern the imposition of

GST or the zero rating of the Appellant’s supplies. The facts of those

cases however could be distinguished with the instant case.

Upon scrutiny, the Tribunal finds that the DG’s Decision 6 of 2015 does not

seek to add another category of services which qualifies for zero-rated

supply under para 3 item 1(a)-1(f) of GST (Zero-Rated Supply) Order

2014. What the DG’s Decision 6 of 2015 does is actually in tandem with

section 5(1) of Act 762 in that it is ‘superintending of all matter relating to

goods and service tax, subject to direction and control of the Minister. The

Act empowers the DG to make a decision or directive in respect of the

application of any provision in Act 762. The substance of DG’s Decision 6

of 2015 is directive in nature and not adding further category of type of

supply.

However this Tribunal finds that the DG’s decision vide letter dated 15th

January 2016 in invoking DG’s Decision 6 of 2015 was erroneous.

20

DCA Certification requirement is not a requirement under the law as

discussed earlier. As rightly testified by SR1 and SR2, DCA requirement is

necessary for the purposes of safety and qualification. The Tribunal holds it

is safety requirements regulated by DCA and not GST related.

Whilst it is not wrong for the DG to impose the requirement of DCA

Certificate of Approval, it is incorrect to decide that the Appellant is not

entitled to zero-rated GST since it does not hold the said DCA Letter Of

Approval. Such approach if taken will run contrary to the spirit and

intendment of section 2 Act 762 and para 3 item 1(d) Second Schedule

of GST (Zero-Rated Supply) Order 2014.

This Tribunal holds that the Tribunal Officer’s interpretation of services

under section 2 of Act 762 which is ‘anything done or to be done by a

supplier’ refers to the actual supplier and not a third party under sub

contract agreement” is flawed.

Upon close examination of section 2 of Act 762 this Tribunal discovers that

‘services means anything done or to be done including the granting,

assignment or surrender of any right or the making available of any facility

or benefit but excludes supply of goods or money.’

As rightly pointed out by the Counsel for Appellant, section 2 allows

granting of any right to a benefit, which is the service of maintenance to be

provided. This Tribunal finds that para 2 of letter dated 15th January 2016

conforms to this interpretation.

This Tribunal found guidance in the case of Mangin v Inland Revenue

Commisioners [1971] AC 739 which was referred to by the Federal Court in

the case of PORIM,supra as follows:

“…Thirdly, the object of the construction of a statute being to ascertain

the will of the legislature, it may be presumed that neither injustice nor

21

absurdity was intended. If therefore a literal interpretation would produce

such a result, and the language admits an interpretation which would avoid

it, then such interpretation may be adopted”

The Tribunal opines that the object of the section 2 Act 762 and para 3

item 1(d) Second Schedule of GST (Zero-Rated Supply ) Order 2014 is

to avoid manipulation of the Act by illegitimate businesses which are using

the backdoor to gain benefit from the zero rated treatment. The provisions

cannot be interpreted to cover legitimate business arrangement such as the

sub contract agreement entered between the Appellant and GEESM. If such

interpretation is to be allowed, it would bring about absurdity to the

intendment of the legislature as decided in the case of Mangin,supra.

Comparative studies between the Malaysian and Singapore legal position in

request of zero-rating of repair, maintenance and service of aircraft would

show that:

Singapore’s equivalent Zero Rate Order, GST (International Services)

Order specifically provides for the definition of a ‘qualified person,’ whilst the

Malaysia GST (Zero-Rated Supply) Order 2014 does not.

Singapore also recognizes that notwithstanding the requirement of a

qualified person, it would nevertheless be acceptable for a service provider

who is not a qualified person to qualify for zero-rating, provided such supply

of services is outsourced to a qualifying person. In the instant case GEESM

holds the DCA certification as it has qualifying person to carry out the

services of maintenance, repair and installation of services for aircraft.

The DG in deciding the instant case should have taken into account the fact

that the sub contract agreement entered in 2005 could not have

contemplated the implementation of GST at that point in time. The guideline

in DG’s Decision 6 of 2015 should not be applied arbitrarily as a one size

22

fits all solution. It has to be fitted in accordance to the fabric of each

particular case. This Tribunal strongly holds that an exception ought to have

been given to this case when applying DG’s Decision 6 of 2015 in view of

the legitimate sub contract agreement.

As the foregoing discussion would show Tribunals in other jurisdiction like

Singapore and the United Kingdom in deciding whether supply has been

made, do recognize existence of indirect supplier vide various business

arrangement including sub contract agreement.[refer to Neway,Reeds

School of Nottingham, Reeds School of Sheffield and CJ Cronin]

Singapore also recognizes service provider who does not hold DCA

Certificate as supplier as long as it is outsourced to a qualifying person. The

Singapore Inland Revenue Authority of Singapore (IRAS) provides for

definition of Qualifying Persons certificated by national Civil Aviation or

Military Authority. IRAS also explains the position where service is carried

by a non-qualified person:-

“Nevertheless the Comptroller recognizes that at times, the contractual

supplier of the repair services does not physically perform the actual repair

but outsources the repair services to a qualifying person. For this reason,

the contractual supplier may not be certificated by a national civil aviation or

military authority”

Question no 3 is a question of fact leading to a findings of fact which should

be confined to the peculiarity of the fact of this case only.

In summary, this Tribunal holds that the DG has erred in invoking DG’s

Decision No 6 of 2015 without taking into consideration the legitimate

business arrangement entered between the Appellant and the service

provider, GEESM which holds a DCA Certificate of Approval . Since the

DG’s decision in letter dated 15 January 2016 was erroneous, the

23

Appellant’s appeal is hereby allowed. The Tribunal finds that the Appellant’s

supply qualifies for zero rated GST under para 3 item 1(d) Second

Schedule of GST (Zero-Rated Supply) Order 2014.

THE OTHER ISSUE

Act 762 and GST (Review and Appeal) Regulation 2014 do not lay down

a complete procedure on filing of pleadings. Reg. 3(1) of GST (Review

and Appeal) Regulation 2014, states that every appeal lodged with the

Tribunal under section 126 of the Act shall be in Form B. However neither

the Act nor the Regulation imposes an obligation on the Respondent to

reply to the appeal. It is observed that this case and most of the other

cases before this Tribunal solely depend on the decision of the DG as a

reply to the appeal during the proceedings. In keeping with rule of fairness

and prudence it would be best practice for the Respondent to undertake

filing a reply to the notice appeal in future cases brought before this

Tribunal. This would greatly assist both parties in leading evidence and

arguing their case before the Tribunal. It is also important for the Tribunal to

ensure both parties maintain their pleaded case and do not raise issues

beyond what is stated in their pleadings to arrive at a just decision. [Ranjit

Kumar, supra and Ramachandran, supra]

24

THE CONCLUSION

In conclusion without regard to formality and technicality as stipulated by

section 142 Act 762, this Tribunal holds that the Appellant has successfully

proven its case on the balance of probabilities. As such the Appellant’s

appeal against the decision of the Director General of Customs dated 15

January 2016 is hereby allowed under section 147(c) of Act 762. In

consequence the decision by the Director General Of Customs dated 15th

January 2016 is set aside and substituted with the order that the supply

made by the Appellant is zero-rated supply by virtue of subsection

144(2)(c) of Act 762.

HANDED DOWN AND DATED THIS 31st day of January 2017

ASLINA BINTI JONED

CHAIRMAN

GOODS AND SERVICES TAX APPEAL TRIBUNAL

Dato’ Arief Emran Ariffin ( En. Jason Liang Ding Hui and Cik Kellie Alison Yap with

him) for the Appellant. Also present : Cik Petrine Soh, Cik Jocelyn Tan and

En Lee Hsin Ye.

Puan Kamaliah binti Hj. Kassim (En. Azawan Shah bin Amdan with her),

Tribunal Officer for the Respondent.

![[2020] UKUT 240 (AAC) IN THE UPPER TRIBUNAL Appeal No. CH ... · IN THE UPPER TRIBUNAL Appeal No. CH/1839/2017 ADMINISTRATIVE APPEALS CHAMBER On appeal from the First-tier Tribunal](https://img.pdfslide.us/doc/110x75/607addab5feb9b146f43ee46/2020-ukut-240-aac-in-the-upper-tribunal-appeal-no-ch-in-the-upper-tribunal.jpg)

![WORKERS COMPENSATION APPEAL TRIBUNAL WORKER … · 2010-06-22 · WORKERS COMPENSATION APPEAL TRIBUNAL BETWEEN: WORKER CASE ID # [personal information] APPELLANT AND: WORKERS COMPENSATION](https://img.pdfslide.us/doc/110x75/5e685bd4f92e4630d604f412/workers-compensation-appeal-tribunal-worker-2010-06-22-workers-compensation-appeal.jpg)