Embed Size (px)

Citation preview

The Global Economy

Business Cycle Indicators

© NYU Stern School of Business

Bloomberg calendar

• Why do we look at this stuff?

http://www.bloomberg.com/markets/ecalendar/index.html

Plan of attack

• Bloomberg calendar • Business cycle overview

• Pictures

• Forecasting

• Good indicators (the “cross-correlation function”)

• Forecasting revisited

• What have we learned?

Business cycle overview

Indicators Monetary Policy

Current Conditions

Theory: AS & AD

Future Conditions

Statistical Analysis

US GDP

Source: BEA via FRED.

US GDP growth (year-on-year)

Source: BEA via FRED.

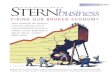

Components of US GDP growth

Source: BEA via FRED.

Components of US GDP growth

Source: BEA via FRED.

Employment (month-to-month change)

Source: BLS.

-100

0-5

000

500

Tho

usa

nds

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

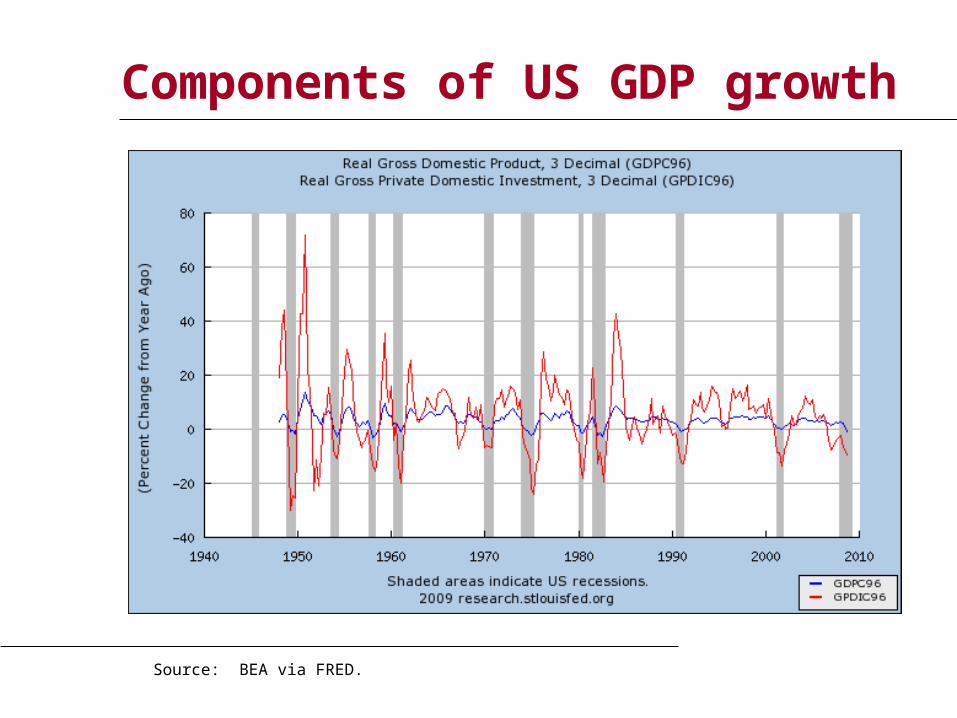

Housing starts

Source: Census.

05

001

000

150

02

000

Tho

usa

nds

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

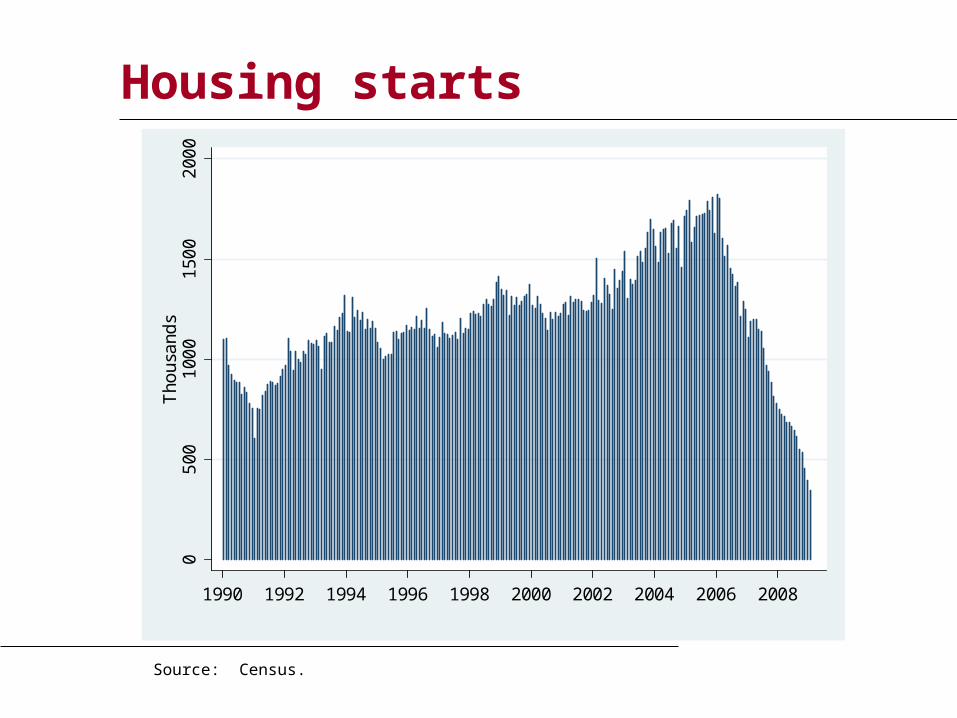

Recession futures

• Probability recession in 2009 (2 qtrs negative growth)

Source: Intrade.com.

Forecasting

• Can we forecast future economic conditions?

– Use information about the past & present to predict the future

• Basic idea: use patterns in the data

– In the past, “this” was followed by “that”

Forecasting: example

• Example: growth in industrial production (“IP”)

γt,t+k = log(IPt+k/IPt)/k = k-period growth rate in IP

• Why? How?

Forecasting: regressions

• Reminder: we’re forecasting

γt,t+k = log(IPt+k/IPt)/k = k-period growth rate in IP

[set k=12 months?]

• Estimate the regression

γt,t+k = a + b xt + residual

xt is an “indicator” of your choice

• Standard software produces estimates of a and b

• Note timing!!

Forecasting: fancy regressions

• Basic regression

γt,t+k = a + b xt + residual

– γt,t+k is what we’re trying to forecast

– xt is an “indicator” of your choice

• Variations – Use more than one x

– Add lags of x

– Add lags of γ

– Whatever works!

Forecasting: forecasts

• Recall: we’ve estimated a and b in

γt,t+k = a + b xt + residual

• Calculate predicted future growth rate

γt,t+k = a + b xt

– xt = value now (t) of indicator x

– γt,t+k = predicted growth from now (t) to the future (t+k)

• Make sure you understand the timing

Identifying good indicators

• What would you suggest? Why?

Identifying good indicators

• How do you find good indicators?

– Forecasting requires indicators that lead what you’re forecasting

– Ask friends, read reports, look at “cross-correlation function”

Identifying good indicators

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to Industrial Production

Nonfarm EmploymentCorrelations for Random Indicator X

Identifying good indicators

• Cross-correlation function (“ccf”)

– Correlations between two variables at different times

ccf(k) = Corr(xt,yt-k)

[plot this against k]

– If k<0: x leads y [or y lags x]

– If k>0: x lags y [or y leads x]

Identifying good indicators

• Pictures: plot ccf(k) v k

– y = IP growth

– x = indicator

– Does indicator lead or lag IP growth?

Identifying good indicators

• Mechanics of ccf calculations: see spreadsheet

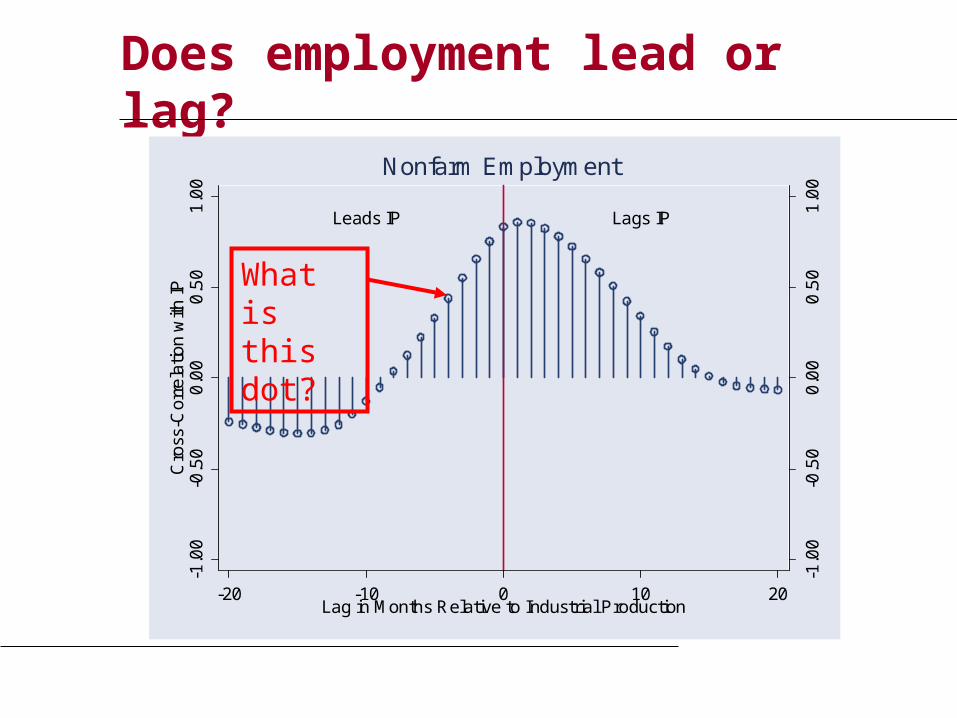

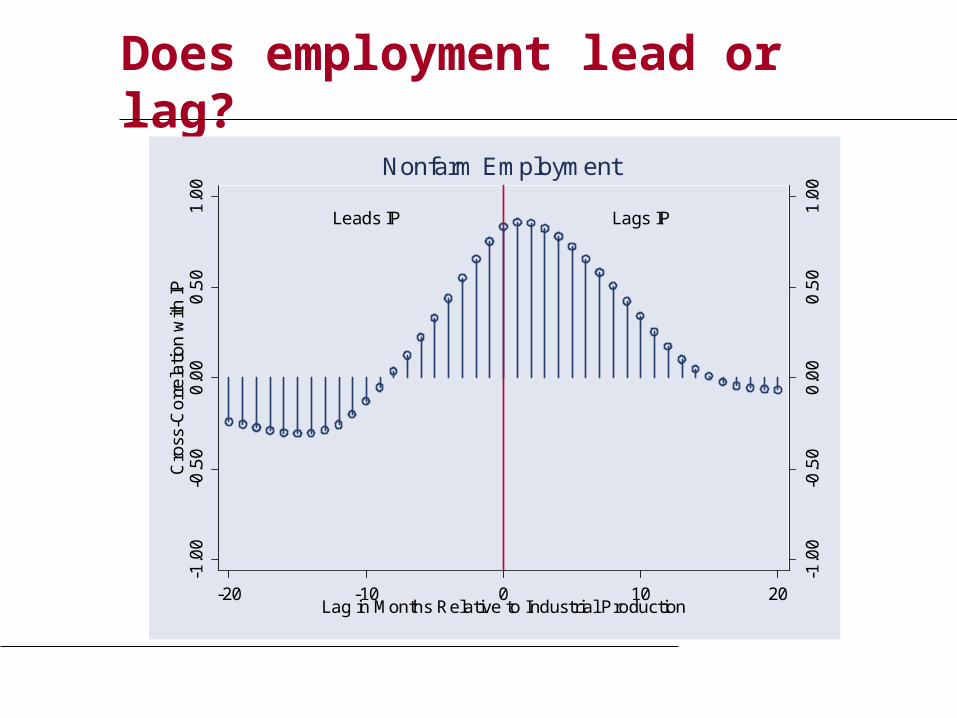

Does employment lead or lag?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to Industrial Production

Nonfarm Employment

What is this dot?

Computing cross-correlations

Reminder: • ccf(k) = corr[x(t),y(t-k)]

For k = 0: • ccf(0) = corr[x(t),y(t)]

Use data marked • Red for x• Blue for y

Date x(t) y(t)

1 2.43 8.47

2 1.19 2.29

3 0.13 7.36

4 0.56 6.39

5 0.38 6.02

6 0.96 0.22

7 1.87 3.60

Computing cross-correlations

Reminder: • ccf(k) = corr[x(t),y(t-k)]

For k = +1: • ccf(1) = corr[x(t),y(t-1)] • Means: x lags y

Use data marked • Red for x• Blue for y

Date x(t) y(t)

1 2.43 8.47

2 1.19 2.29

3 0.13 7.36

4 0.56 6.39

5 0.38 6.02

6 0.96 0.22

7 1.87 3.60

Computing cross-correlations

Reminder: • ccf(k) = corr[x(t),y(t-k)]

For k = –1: • ccf(-1) =

corr[x(t),y(t+1)] • Means: y lags x

Use data marked • Red for x• Blue for y

Date x(t) y(t)

1 2.43 8.47

2 1.19 2.29

3 0.13 7.36

4 0.56 6.39

5 0.38 6.02

6 0.96 0.22

7 1.87 3.60

Does employment lead or lag?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to Industrial Production

Nonfarm Employment

Unemployment?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to IP

Unemployment Rate

New claims for un ins?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to IP

Unemployment: New Claims

Housing starts?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to Industrial Production

Housing Starts

Building permits?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to Industrial Production

Building Permits

Consumer sentiment?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

IP

-20 -10 0 10 20Lag in Months Relative to Industrial Production

Consumer Sentiment

S&P 500 index?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

Indu

stri

al P

rodu

ctio

n

-20 -10 0 10 20Lag in Months Relative to Industrial Production

S&P 500 Index

Yield spread?

Leads IP Lags IP

-1.0

0-0

.50

0.0

00

.50

1.0

0

-1.0

0-0

.50

0.0

00

.50

1.0

0C

ross

-Cor

rela

tion

with

Indu

stri

al P

rodu

ctio

n

-20 -10 0 10 20Lag Relative to IP

Yield Spread (10y - Fed Funds)

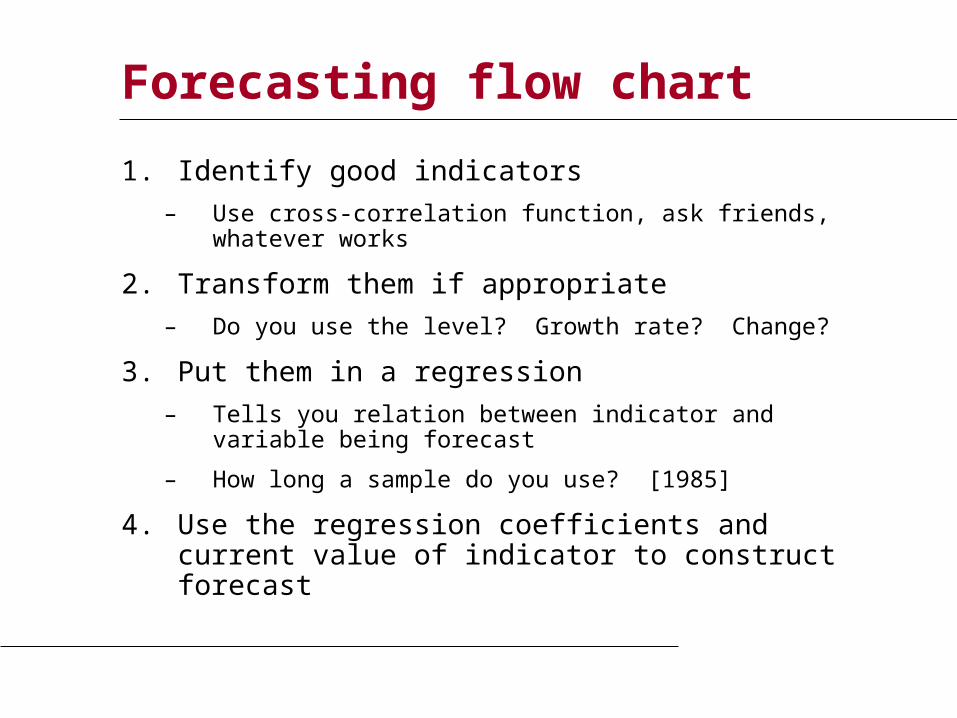

Forecasting flow chart

1. Identify good indicators

– Use cross-correlation function, ask friends, whatever works

2. Transform them if appropriate

– Do you use the level? Growth rate? Change?

3. Put them in a regression

– Tells you relation between indicator and variable being forecast

– How long a sample do you use? [1985]

4. Use the regression coefficients and current value of indicator to construct forecast

How well do we do?

• Forecasts have content

– Typical R2 > 0, < 0.50

– Most of what happens is not predicted

• Therefore: have a contingency plan

What have we learned?

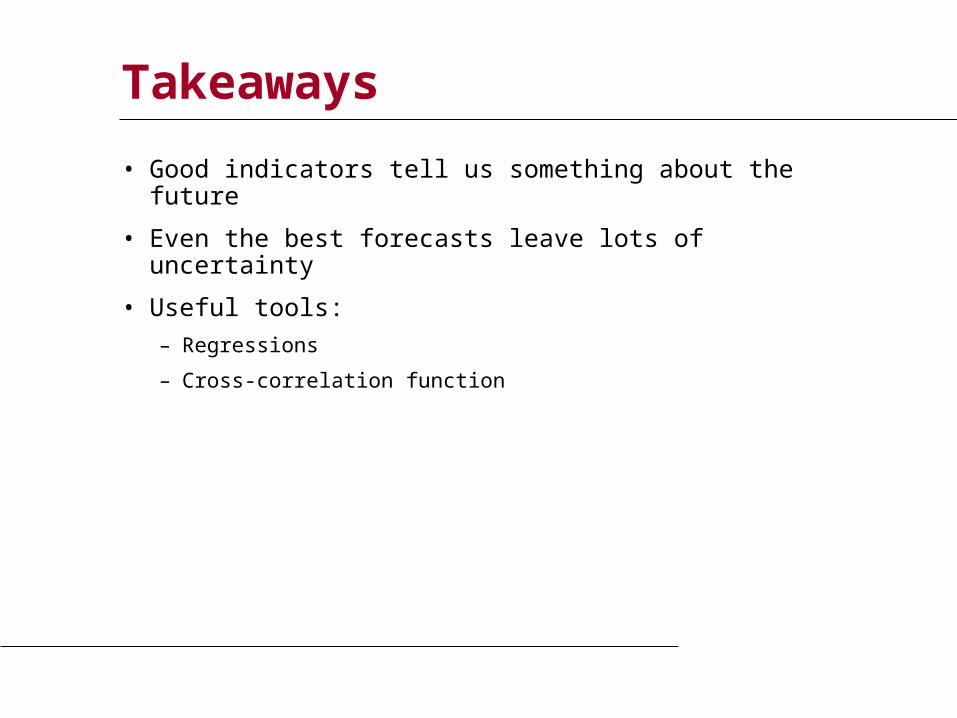

Takeaways

• Good indicators tell us something about the future

• Even the best forecasts leave lots of uncertainty

• Useful tools:

– Regressions

– Cross-correlation function

Enjoy the break

• See you in a couple weeks