Embed Size (px)

Citation preview

The Game Has ChangedStrategy For A Value Driven World

Steve JenkinsSenior Advisor

November 13, 2016

2Confidential and Proprietary © 2016 Sg2

Sg2, a Vizient company, is the health care industry’s premier provider ofmarket data and information.

Our analytics and expertise help hospitals, health systems and leading suppliersunderstand market dynamics and capitalize on opportunities for growth.

Industry-LeadingConsulting

UnmatchedExpertise andIntelligence

PowerfulAnalytics

Sg2 OFFERINGS

DataResources

Meet Sg2

3Confidential and Proprietary © 2016 Sg2

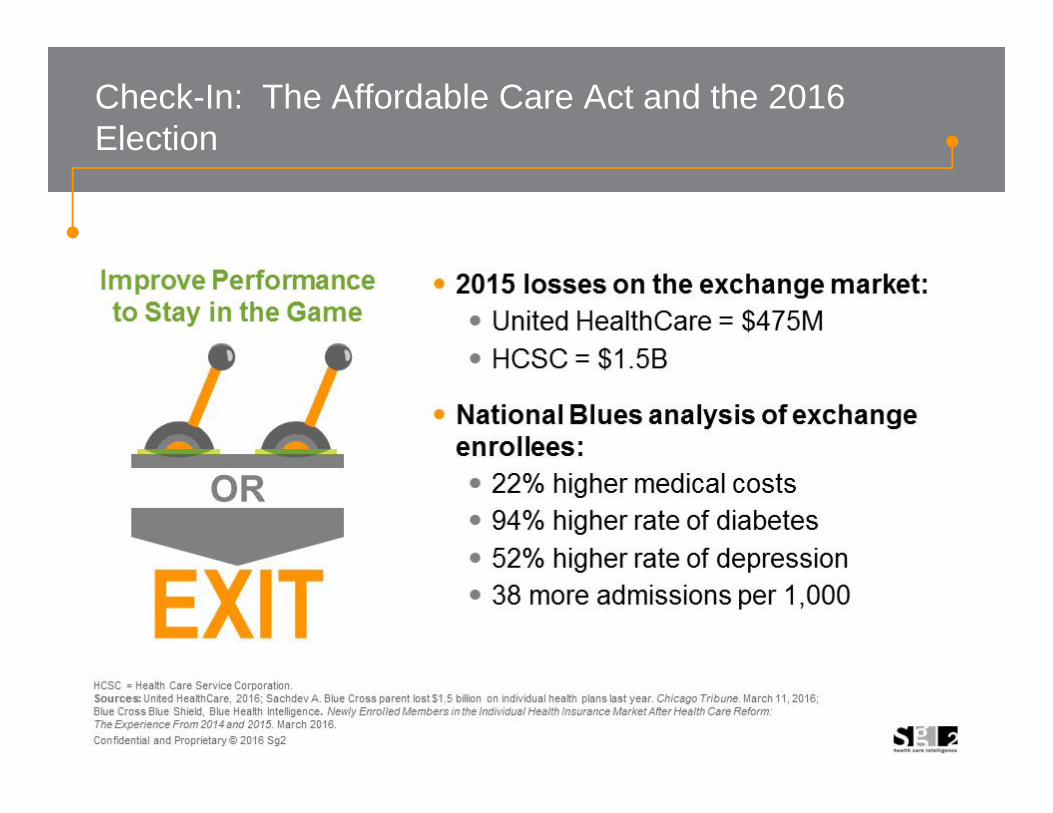

Check-In: The Affordable Care Act and the 2016Election

4Confidential and Proprietary © 2016 Sg2

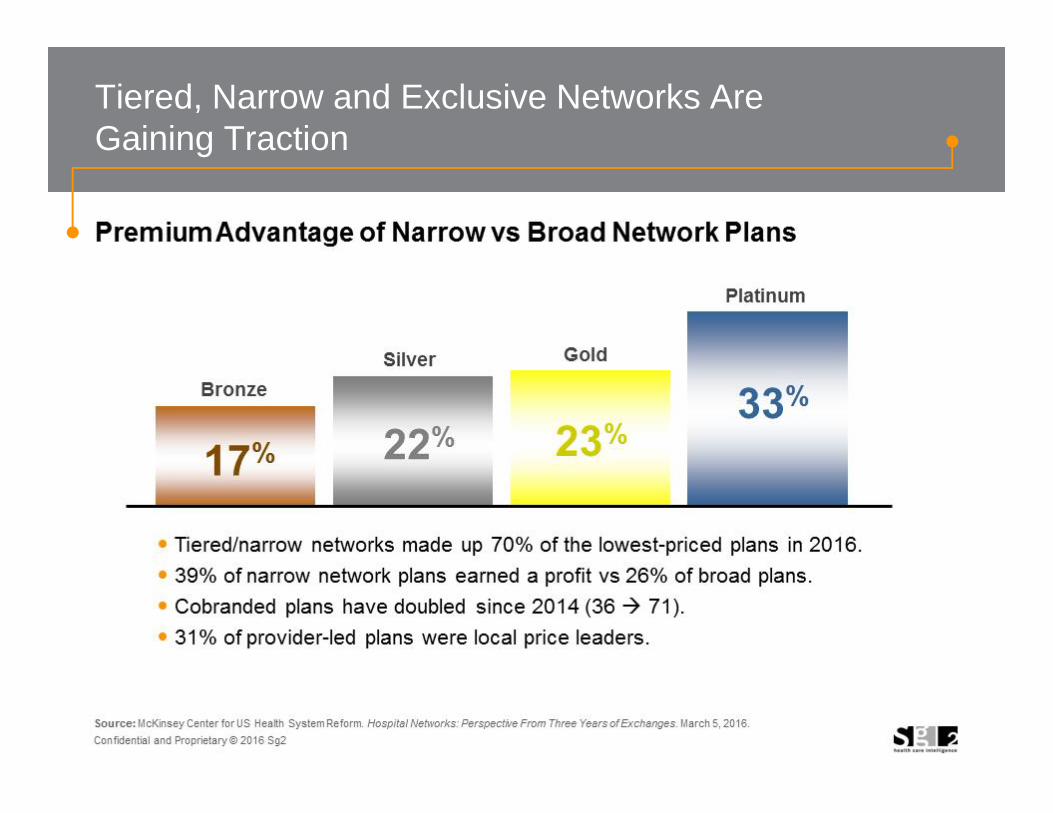

Tiered, Narrow and Exclusive Networks AreGaining Traction

5Confidential and Proprietary © 2016 Sg2

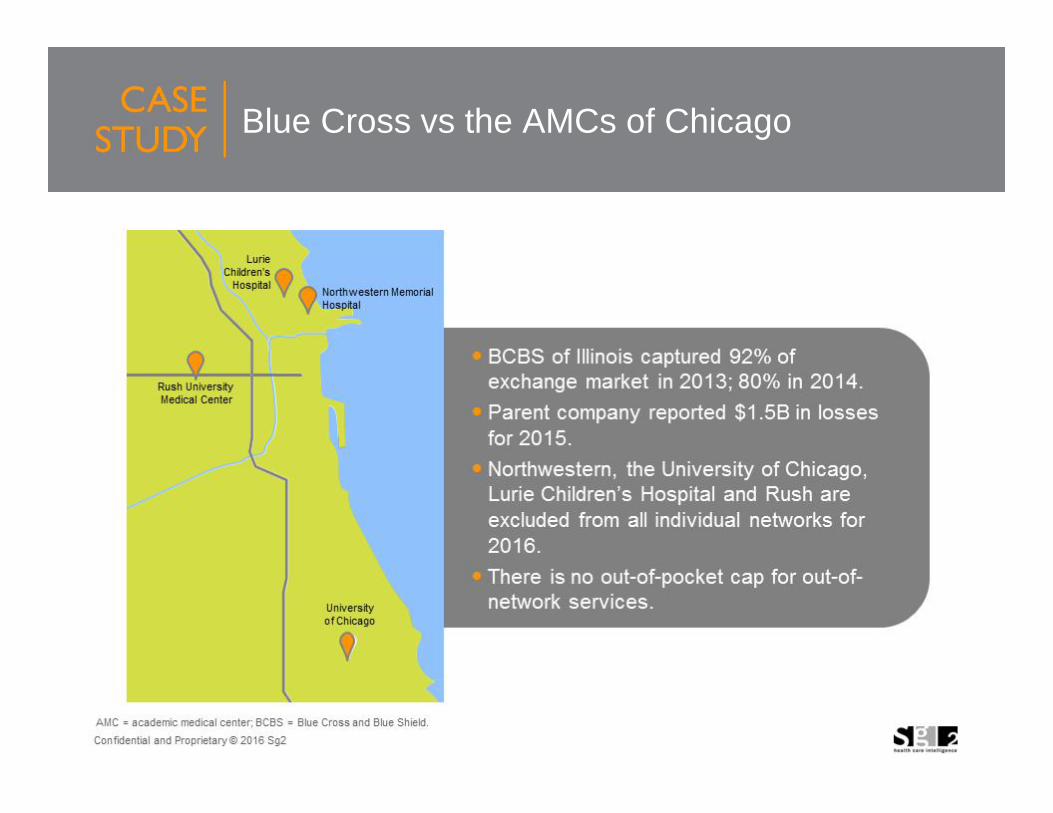

Blue Cross vs the AMCs of Chicago

6Confidential and Proprietary © 2016 Sg2

AdvancedInnovativeTraditionalData Not Available

Composite RiskReadiness by Market

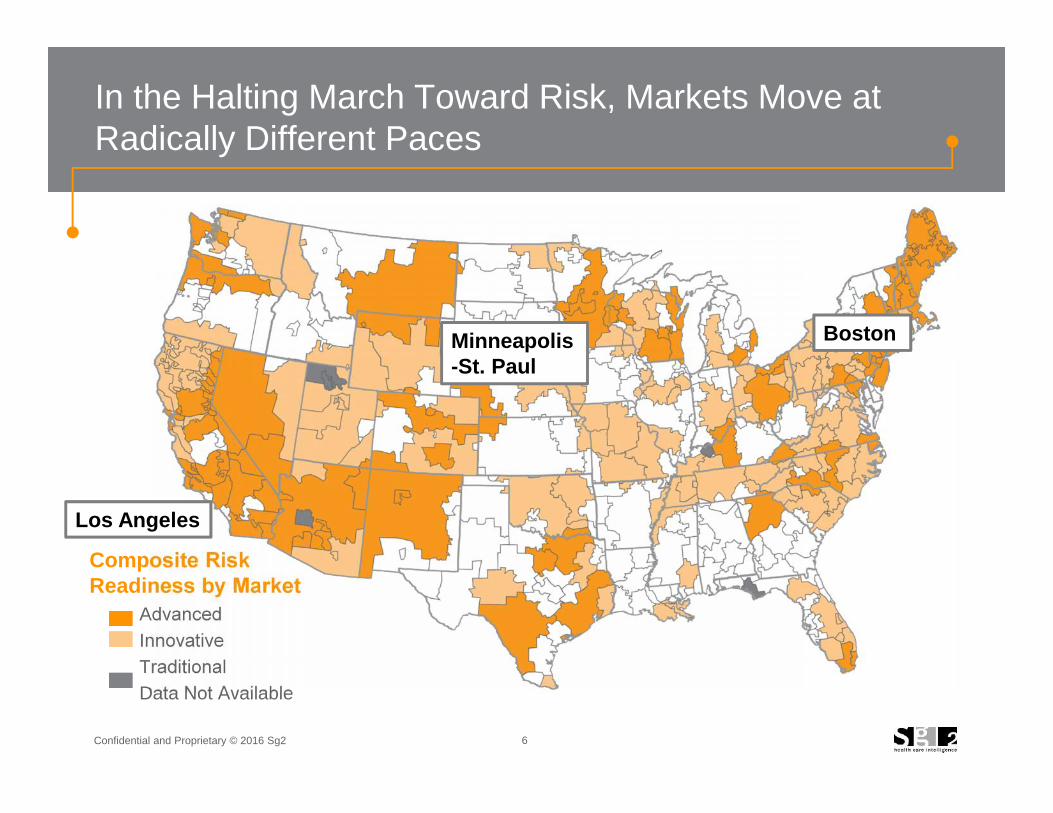

In the Halting March Toward Risk, Markets Move atRadically Different Paces

Minneapolis-St. Paul

Boston

Los Angeles

7Confidential and Proprietary © 2016 Sg2

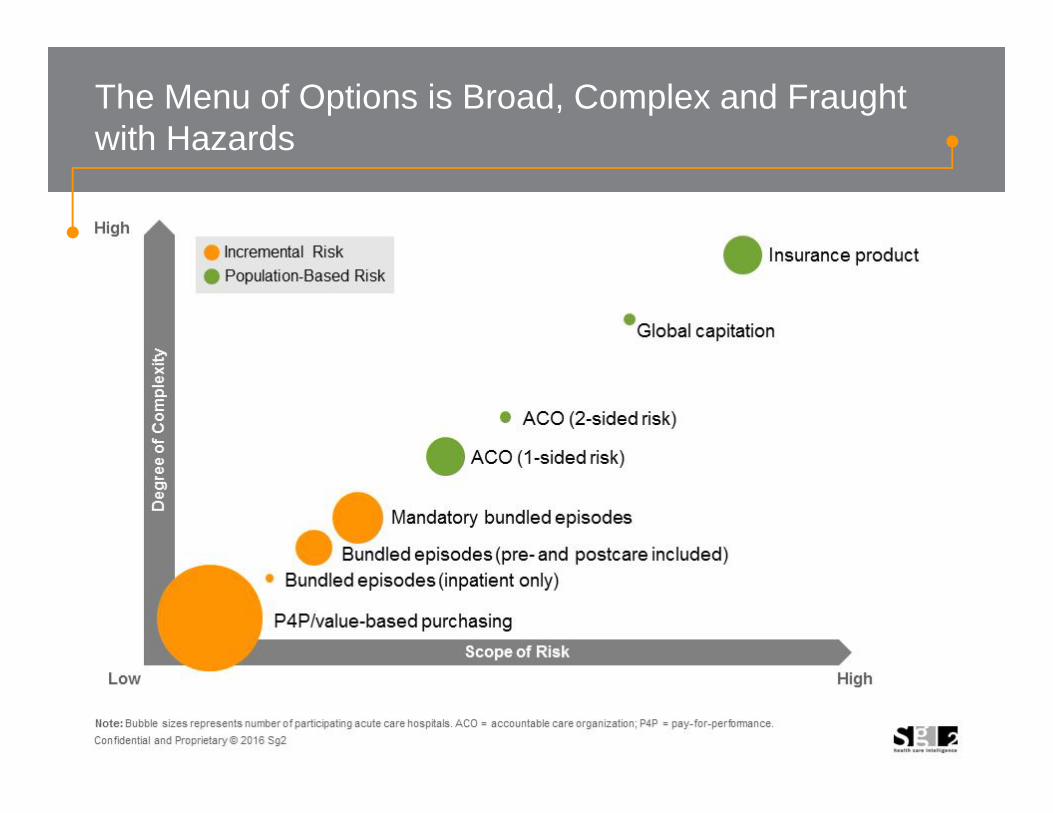

The Menu of Options is Broad, Complex and Fraughtwith Hazards

8Confidential and Proprietary © 2014 Sg2

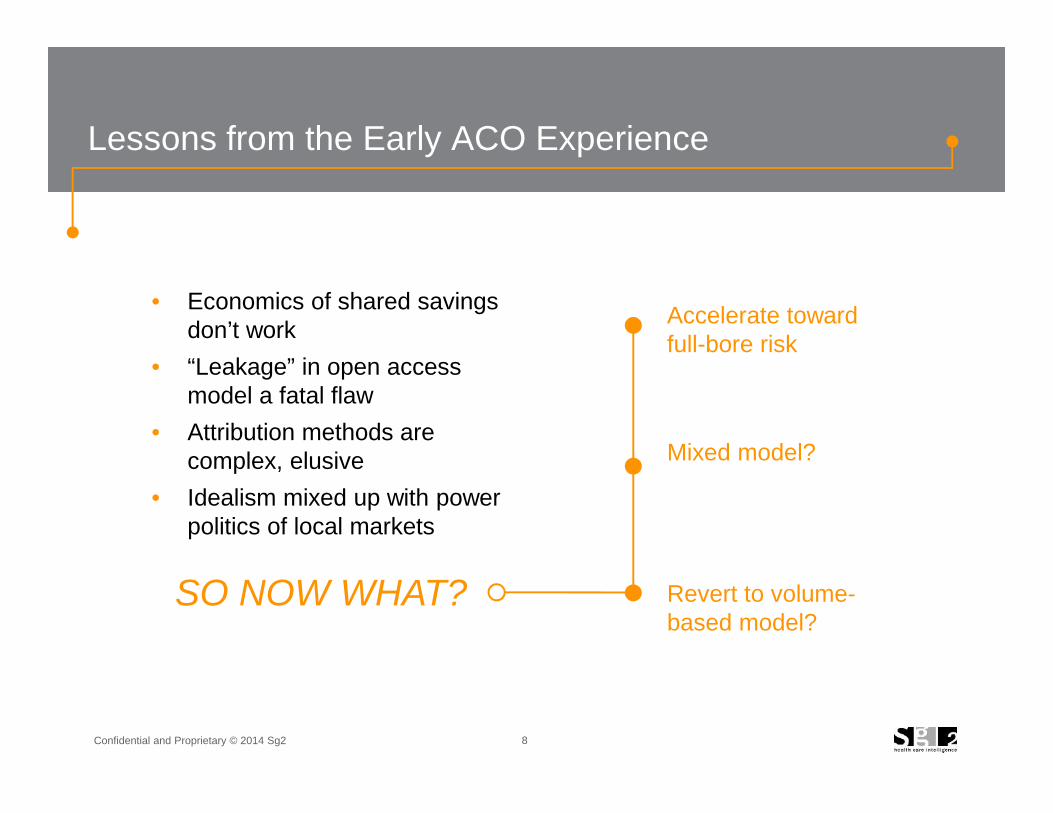

Lessons from the Early ACO Experience

Accelerate towardfull-bore risk

Mixed model?

Revert to volume-based model?

• Economics of shared savingsdon’t work

• “Leakage” in open accessmodel a fatal flaw

• Attribution methods arecomplex, elusive

• Idealism mixed up with powerpolitics of local markets

SO NOW WHAT?

9Confidential and Proprietary © 2016 Sg2

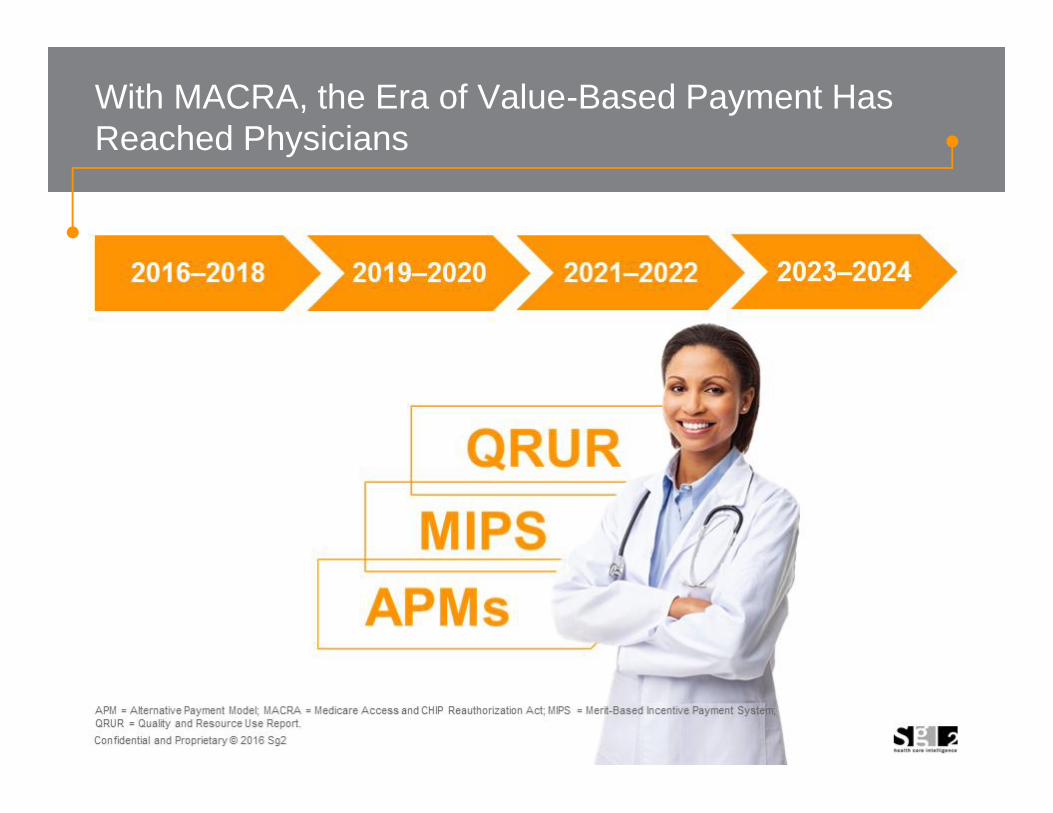

With MACRA, the Era of Value-Based Payment HasReached Physicians

10Confidential and Proprietary © 2016 Sg2

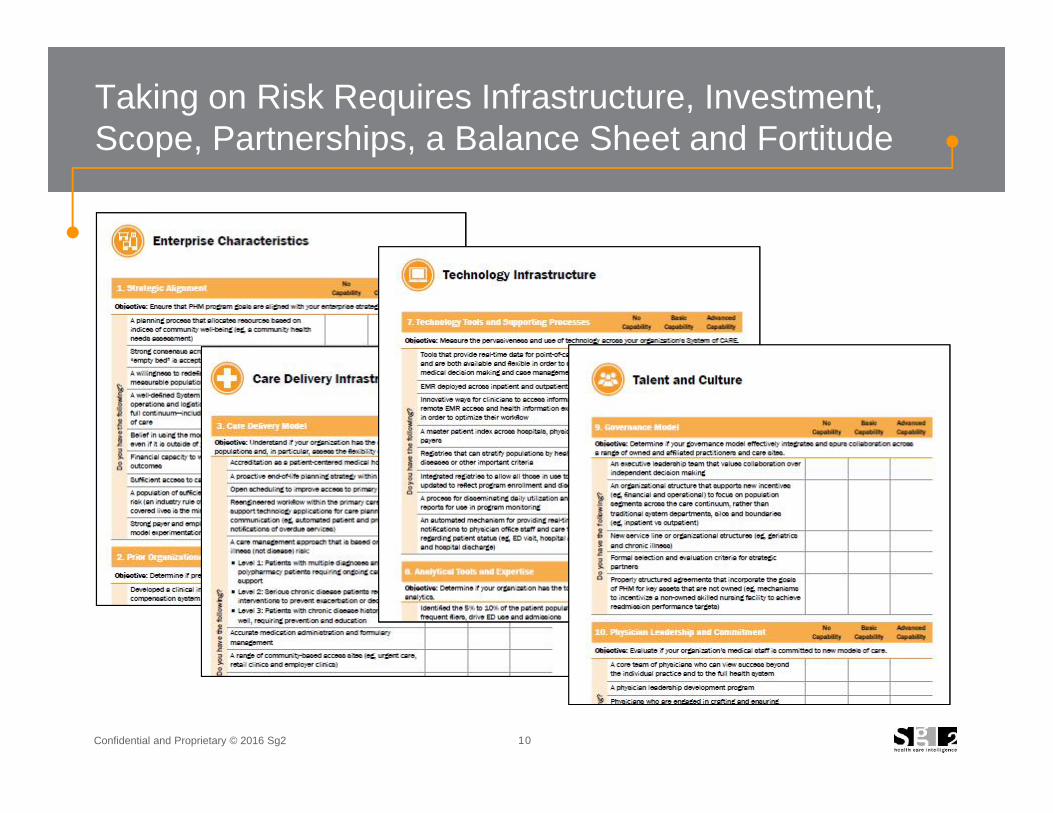

Taking on Risk Requires Infrastructure, Investment,Scope, Partnerships, a Balance Sheet and Fortitude

11Confidential and Proprietary © 2016 Sg2

SIX FUNDAMENTALSfor health system strategy in atime of change and uncertainty

Confidential and Proprietary © 2016 Sg2

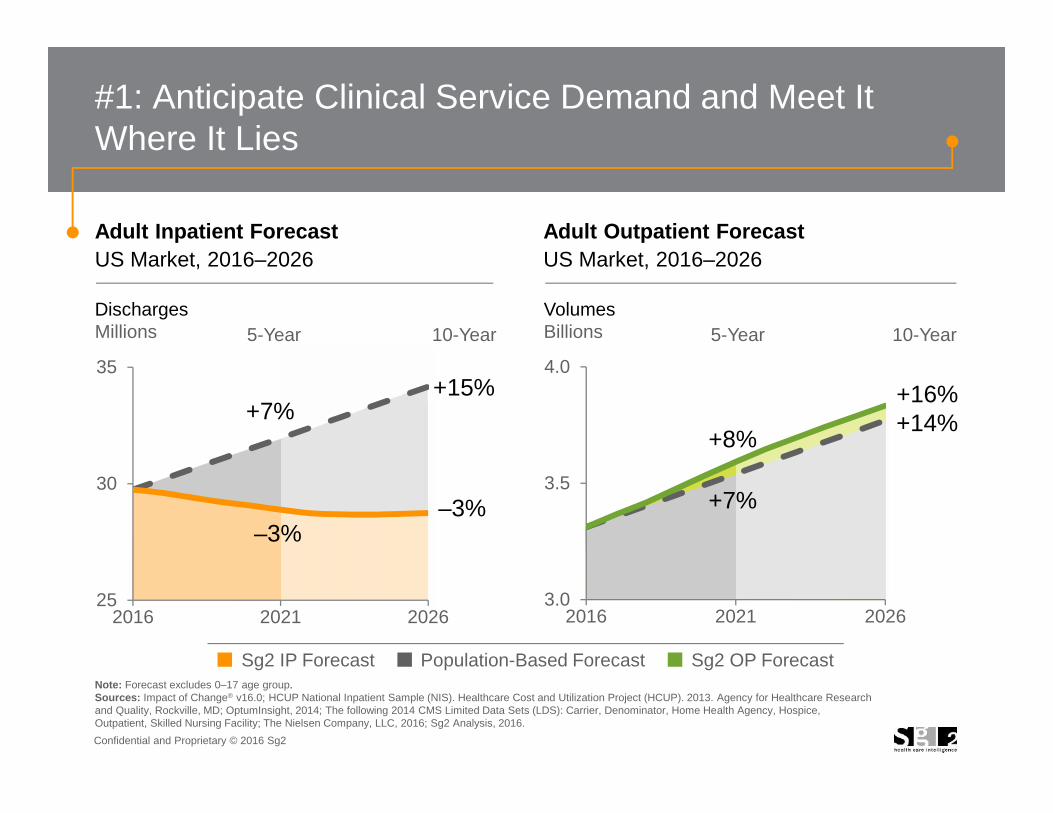

#1: Anticipate Clinical Service Demand and Meet ItWhere It Lies

25

30

35

2016 2021 20263.0

3.5

4.0

2016 2021 2026

Note: Forecast excludes 0–17 age group.Sources: Impact of Change® v16.0; HCUP National Inpatient Sample (NIS). Healthcare Cost and Utilization Project (HCUP). 2013. Agency for Healthcare Researchand Quality, Rockville, MD; OptumInsight, 2014; The following 2014 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice,Outpatient, Skilled Nursing Facility; The Nielsen Company, LLC, 2016; Sg2 Analysis, 2016.

Adult Inpatient ForecastUS Market, 2016–2026

Adult Outpatient ForecastUS Market, 2016–2026

Sg2 IP Forecast Population-Based Forecast Sg2 OP Forecast

VolumesBillions

+14%+16%

10-YearDischargesMillions 5-Year

+7%

+8%

5-Year

+7%

–3%

+15%

–3%

10-Year

13Confidential and Proprietary © 2016 Sg2

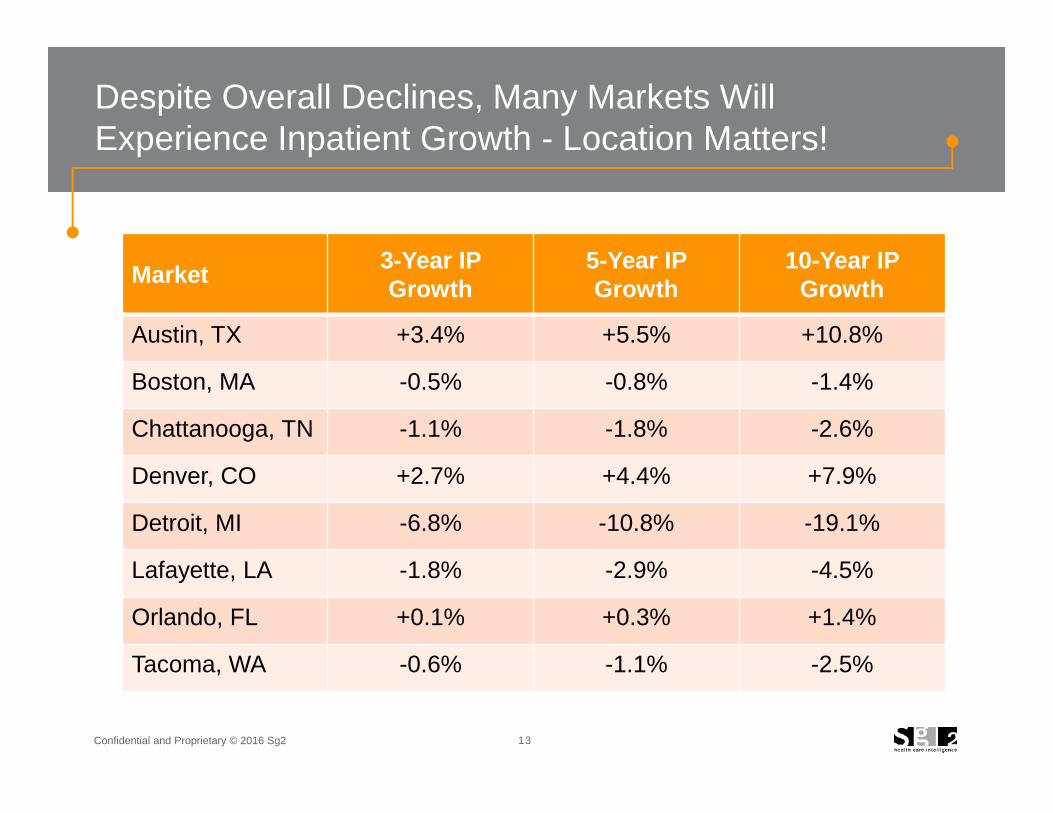

Despite Overall Declines, Many Markets WillExperience Inpatient Growth - Location Matters!

Market 3-Year IPGrowth

5-Year IPGrowth

10-Year IPGrowth

Austin, TX +3.4% +5.5% +10.8%

Boston, MA -0.5% -0.8% -1.4%

Chattanooga, TN -1.1% -1.8% -2.6%

Denver, CO +2.7% +4.4% +7.9%

Detroit, MI -6.8% -10.8% -19.1%

Lafayette, LA -1.8% -2.9% -4.5%

Orlando, FL +0.1% +0.3% +1.4%

Tacoma, WA -0.6% -1.1% -2.5%

14Confidential and Proprietary © 2016 Sg2

Sg2 ANALYTICS

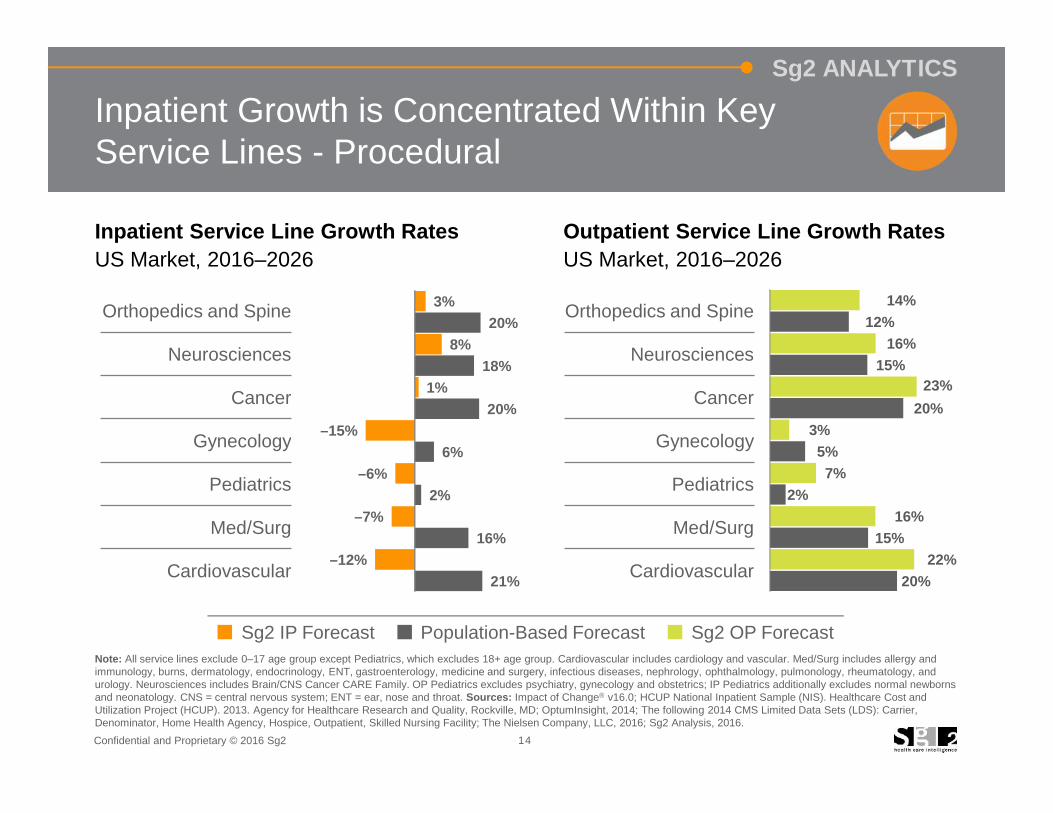

20%22%

15%16%

2%7%

5%3%

20%23%

15%16%

12%14%

21%–12%

16%–7%

2%–6%

6%–15%

20%1%

18%8%

20%3%

Inpatient Growth is Concentrated Within KeyService Lines - Procedural

Inpatient Service Line Growth RatesUS Market, 2016–2026

Outpatient Service Line Growth RatesUS Market, 2016–2026

Sg2 IP Forecast Population-Based Forecast Sg2 OP Forecast

Orthopedics and Spine

Neurosciences

Cancer

Gynecology

Pediatrics

Med/Surg

Cardiovascular

Orthopedics and Spine

Neurosciences

Cancer

Gynecology

Pediatrics

Med/Surg

Cardiovascular

Note: All service lines exclude 0–17 age group except Pediatrics, which excludes 18+ age group. Cardiovascular includes cardiology and vascular. Med/Surg includes allergy andimmunology, burns, dermatology, endocrinology, ENT, gastroenterology, medicine and surgery, infectious diseases, nephrology, ophthalmology, pulmonology, rheumatology, andurology. Neurosciences includes Brain/CNS Cancer CARE Family. OP Pediatrics excludes psychiatry, gynecology and obstetrics; IP Pediatrics additionally excludes normal newbornsand neonatology. CNS = central nervous system; ENT = ear, nose and throat. Sources: Impact of Change® v16.0; HCUP National Inpatient Sample (NIS). Healthcare Cost andUtilization Project (HCUP). 2013. Agency for Healthcare Research and Quality, Rockville, MD; OptumInsight, 2014; The following 2014 CMS Limited Data Sets (LDS): Carrier,Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; The Nielsen Company, LLC, 2016; Sg2 Analysis, 2016.

Confidential and Proprietary © 2016 Sg2

#2: Build a System of CARE Footprint That Is Relevantand Defensible on Your Local Market Chessboard

Geographic reach

System of CARE scope

Must-have clinical services

Must-have locations

Diversified strategy of“primary care”

Channel strategy matchedto your clinical portfolio

Confidential and Proprietary © 2016 Sg2

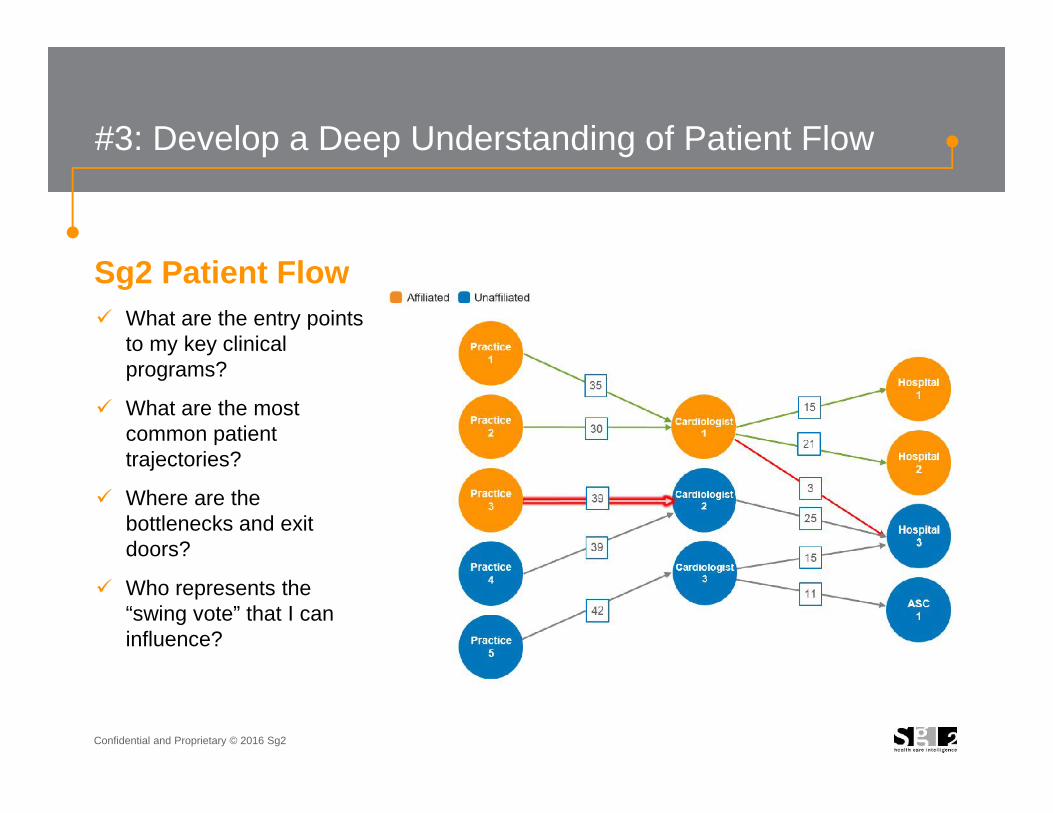

#3: Develop a Deep Understanding of Patient Flow

What are the entry pointsto my key clinicalprograms?

What are the mostcommon patienttrajectories?

Where are thebottlenecks and exitdoors?

Who represents the“swing vote” that I caninfluence?

Sg2 Patient Flow

17Confidential and Proprietary © 2016 Sg2

#4: Respond to the Access Needs of Consumers

INFORMATION: Consumers have more information (much of it poor)about treatment and provider options.

1234

PRICE SENSITIVITY: Consumers are bearing more of the cost ofhealth care.

CHOICES: Consumers have a broader array of options for where toseek care, particularly in the ambulatory arena.

GENERATIONAL SHIFT: Younger consumers have a differentrelationship with their physician and a different approach to seekinghealth care.

Forces driving increased role of the consumer in health care:

18Confidential and Proprietary © 2016 Sg2

Having a Consumer Strategy in Health Care MeansSolving for 3 Needs

Time Location Price

Confidential and Proprietary © 2016 Sg2

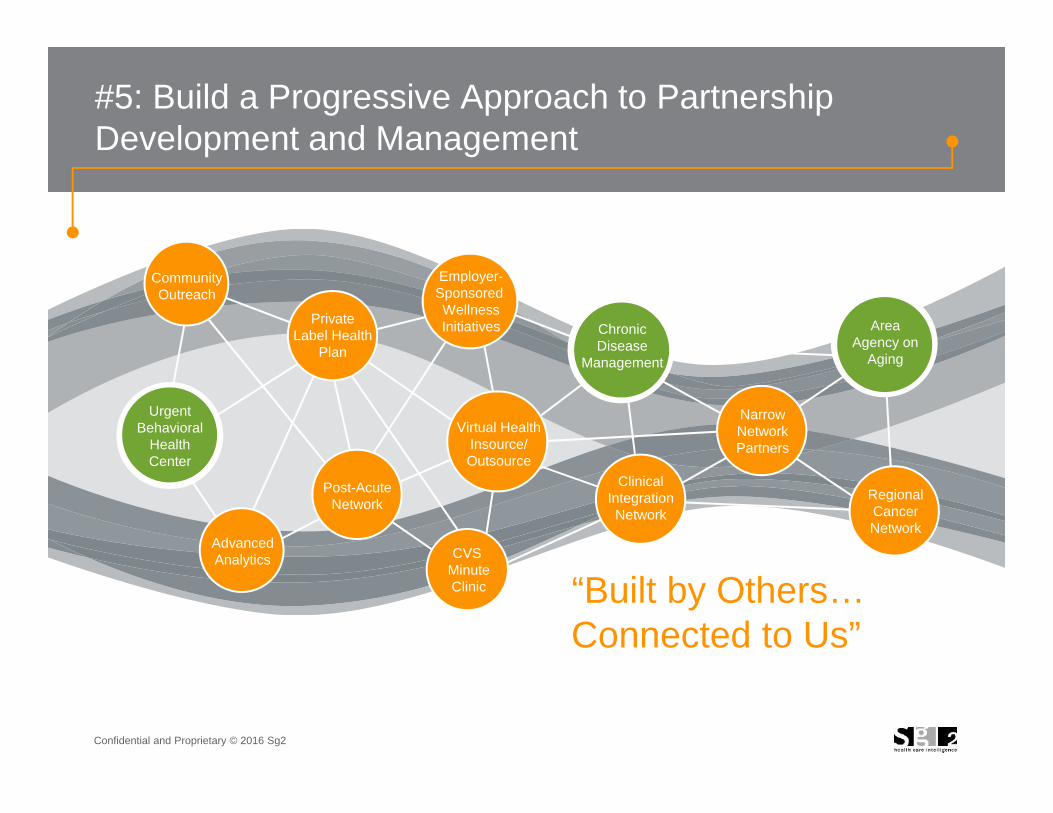

#5: Build a Progressive Approach to PartnershipDevelopment and Management

“Built by Others…Connected to Us”

CommunityOutreach

AdvancedAnalytics

PrivateLabel Health

Plan

Post-AcuteNetwork

Employer-SponsoredWellnessInitiatives

Virtual HealthInsource/Outsource

CVSMinuteClinic

ClinicalIntegrationNetwork

NarrowNetworkPartners

RegionalCancerNetwork

UrgentBehavioral

HealthCenter

ChronicDisease

Management

AreaAgency on

Aging

20Confidential and Proprietary © 2016 Sg2

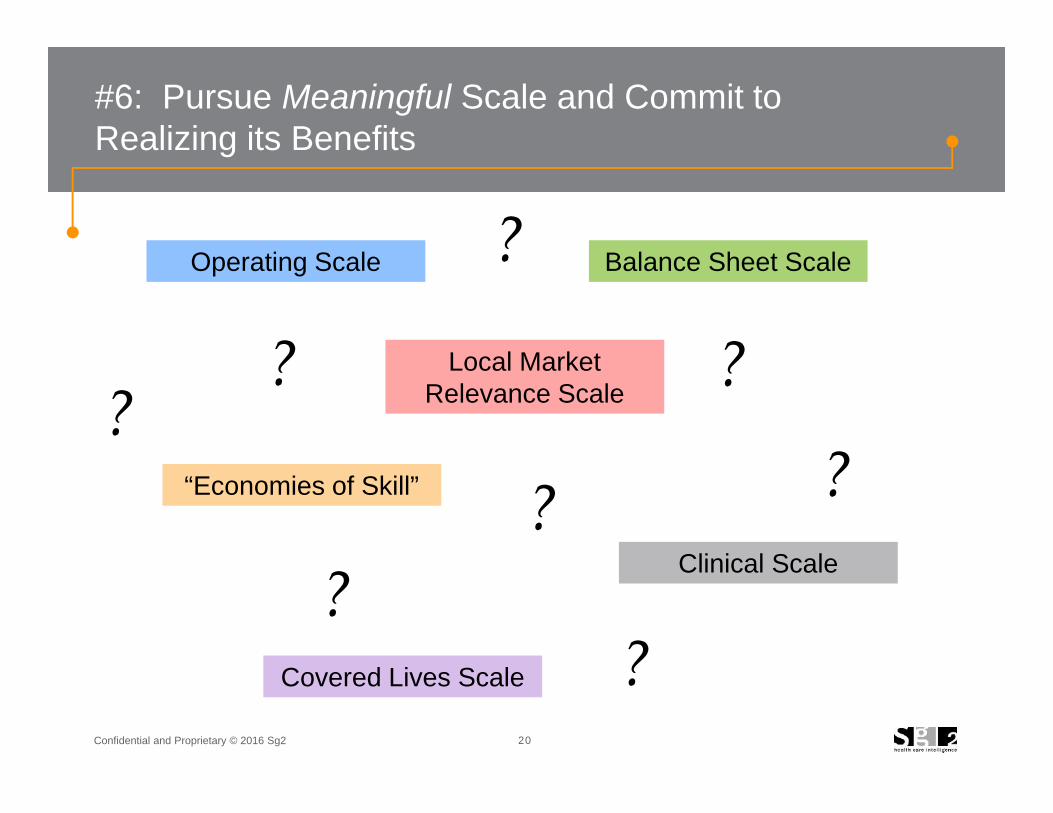

#6: Pursue Meaningful Scale and Commit toRealizing its Benefits

Operating Scale

Clinical Scale

“Economies of Skill”

Local MarketRelevance Scale

Balance Sheet Scale

?

?

?

?

?

?

?

Covered Lives Scale ?

21Confidential and Proprietary © 2016 Sg2

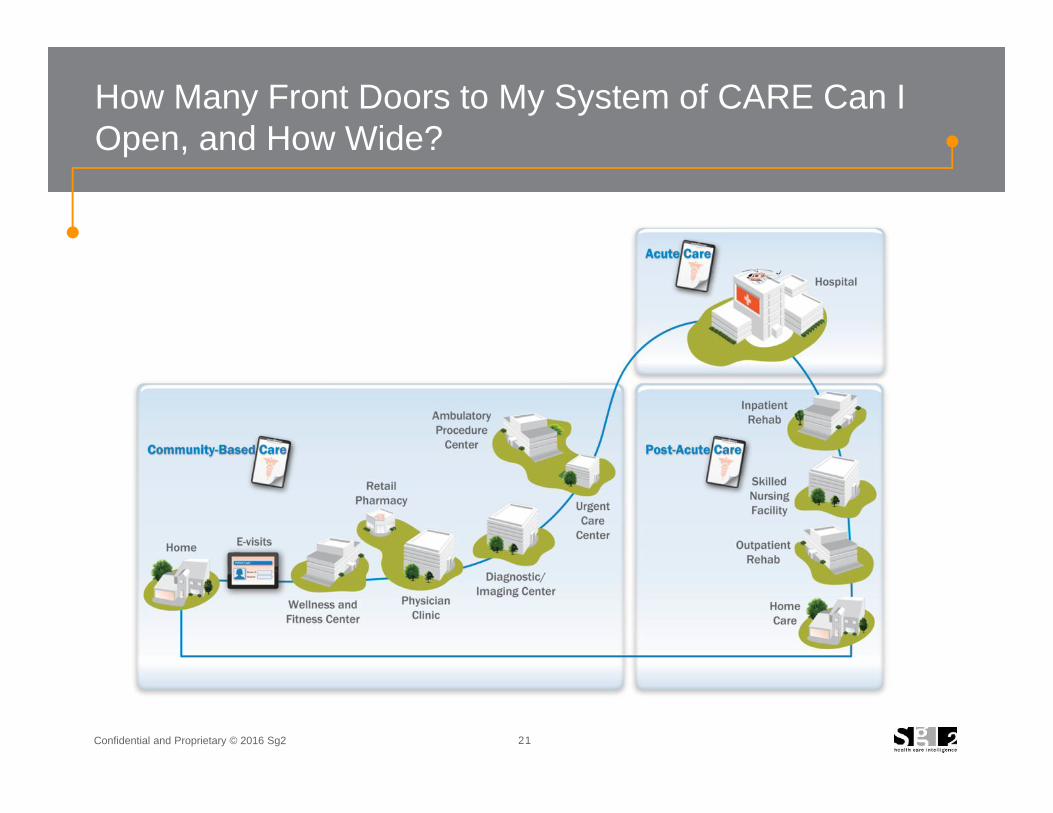

How Many Front Doors to My System of CARE Can IOpen, and How Wide?

Sg2 is the health care industry’s premier provider of marketdata and information. Our analytics and expertise help

hospitals and health systems understand market dynamicsand capitalize on opportunities for growth.

Sg2.com 847.779.5300