Embed Size (px)

Citation preview

The Future of Vegetable Oils in Central & Eastern Europe

by David JacksonDirector, LMC International Ltd

The market for oils in Eastern Europe

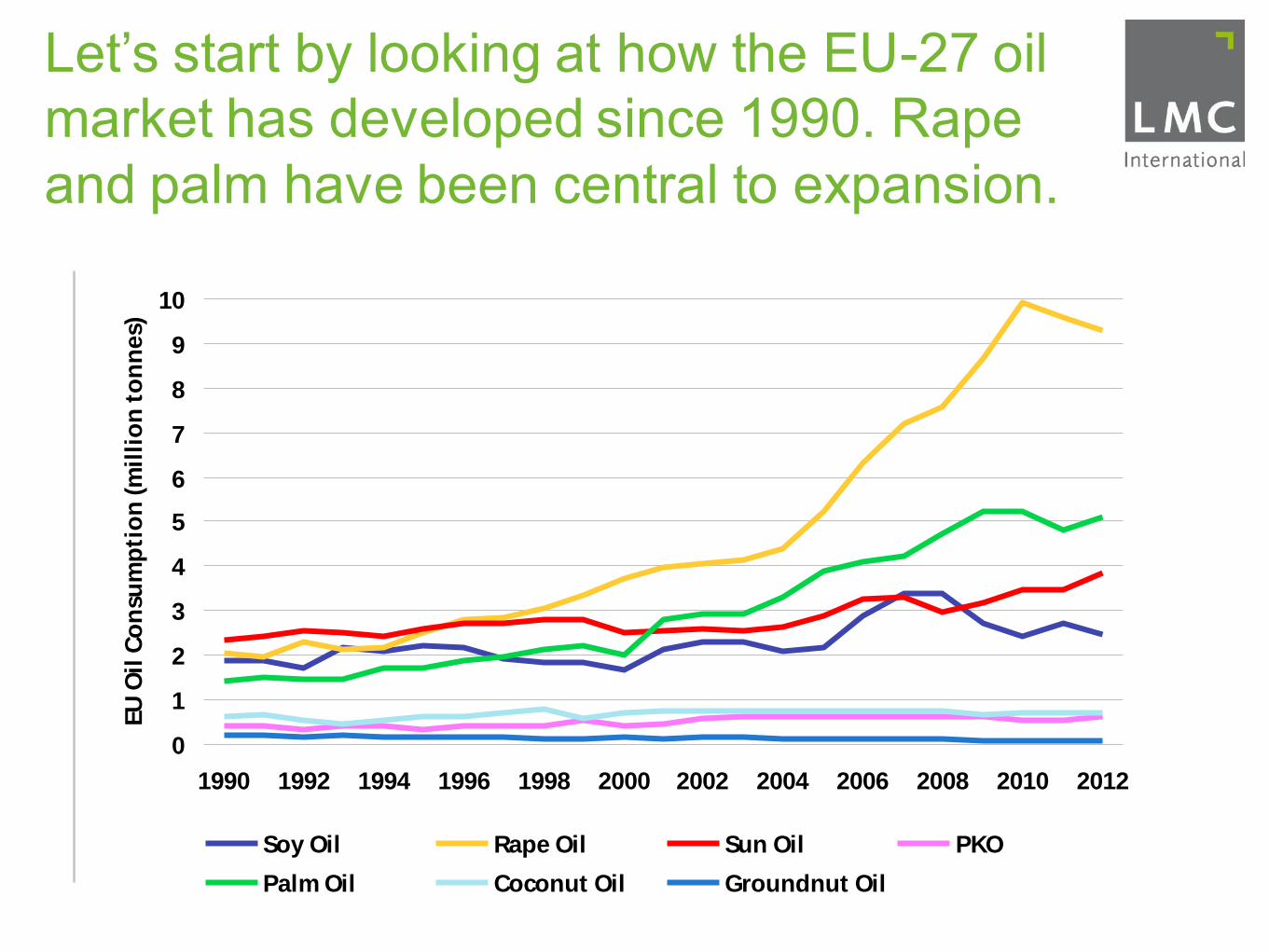

Let’s start by looking at how the EU-27 oil market has developed since 1990. Rape and palm have been central to expansion.

0

1

2

3

4

5

6

7

8

9

10

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

EU

Oil

Co

nsu

mp

tio

n (m

illi

on

to

nn

es)

Soy Oil Rape Oil Sun Oil PKO

Palm Oil Coconut Oil Groundnut Oil

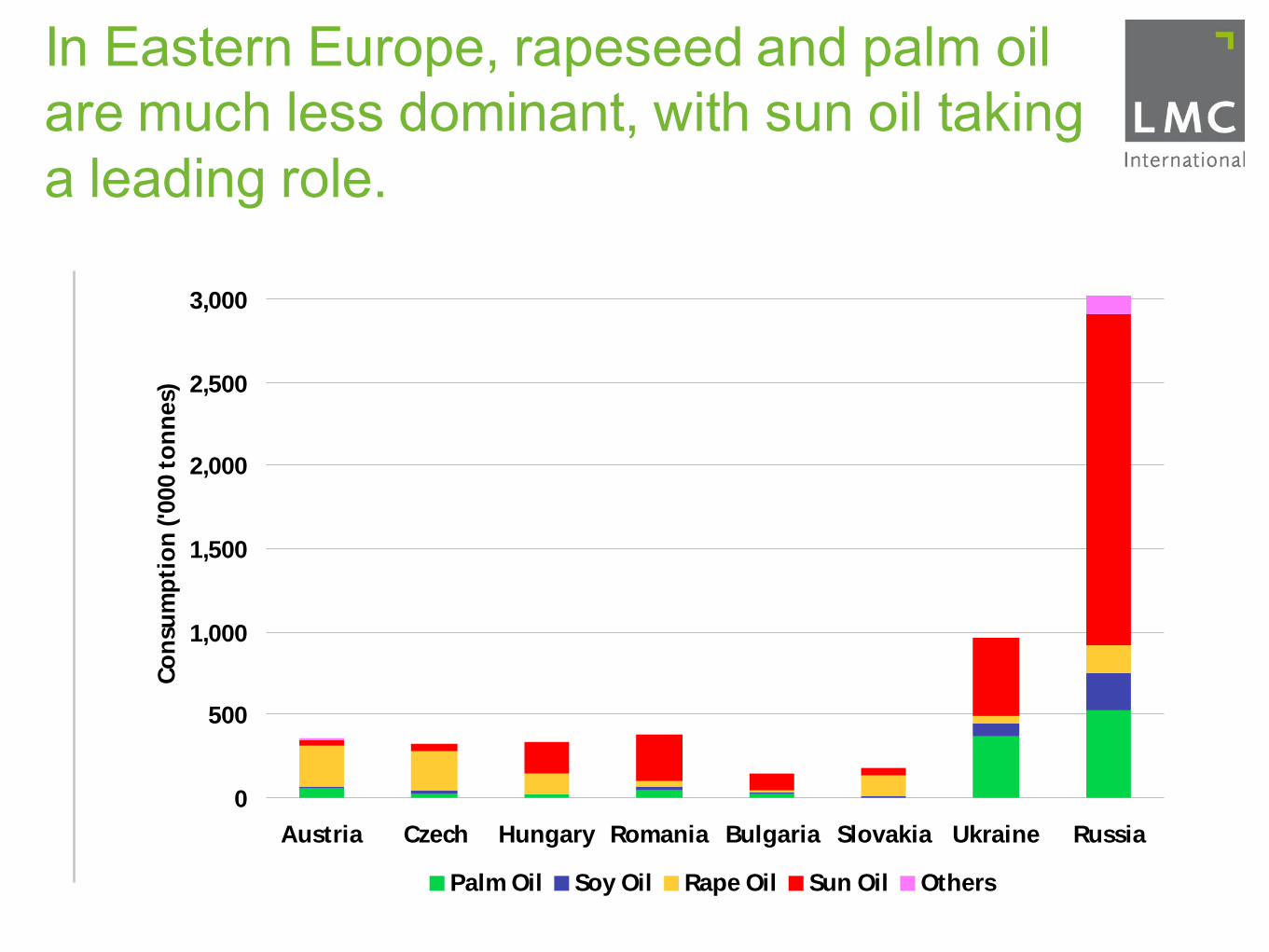

In Eastern Europe, rapeseed and palm oil are much less dominant, with sun oil taking a leading role.

0

500

1,000

1,500

2,000

2,500

3,000

Austria Czech Hungary Romania Bulgaria Slovakia Ukraine Russia

Co

nsu

mp

tio

n ('0

00 t

on

nes)

Palm Oil Soy Oil Rape Oil Sun Oil Others

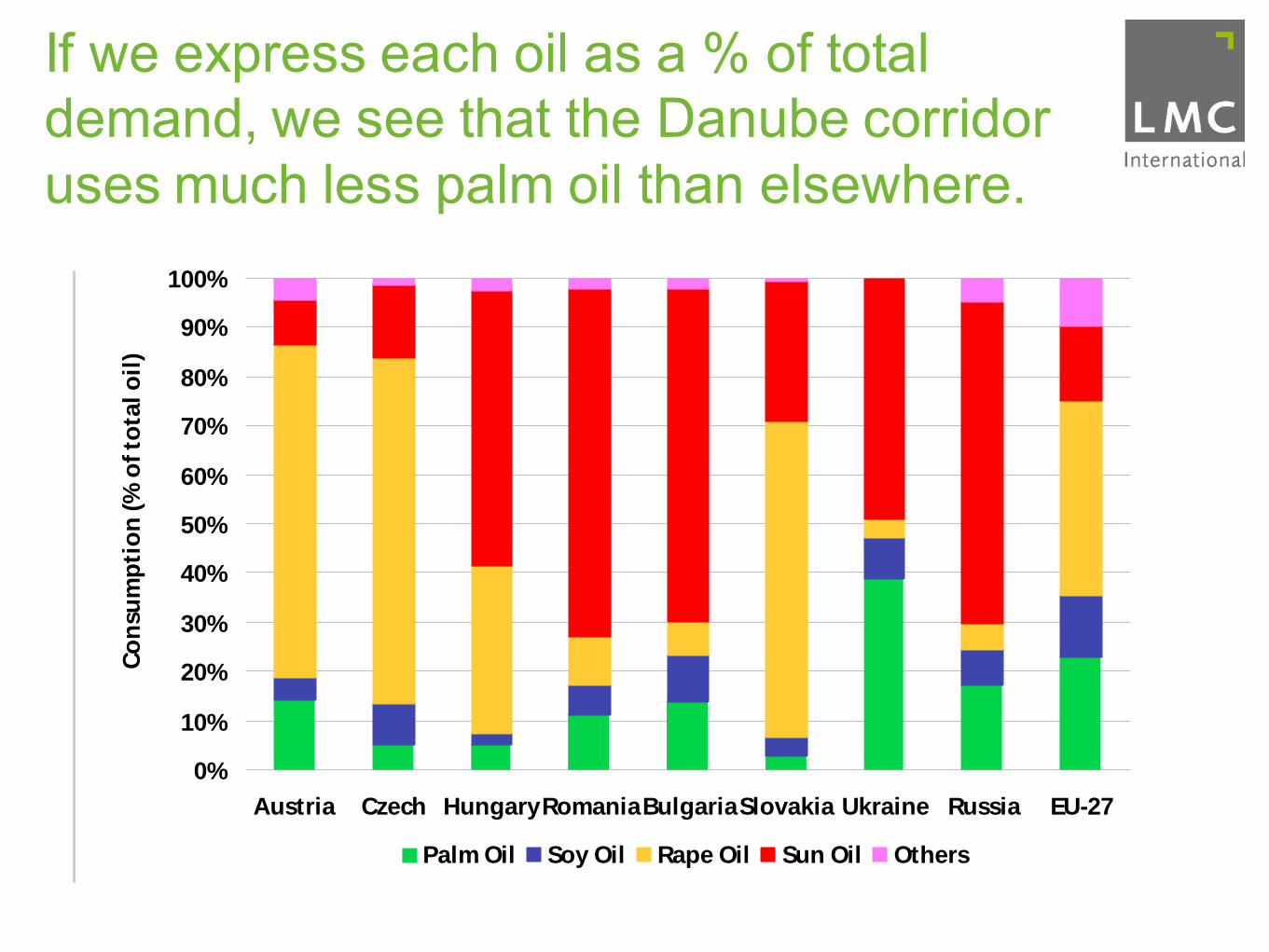

If we express each oil as a % of total demand, we see that the Danube corridor uses much less palm oil than elsewhere.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Austria Czech HungaryRomaniaBulgariaSlovakia Ukraine Russia EU-27

Co

nsu

mp

tio

n (%

of to

tal o

il)

Palm Oil Soy Oil Rape Oil Sun Oil Others

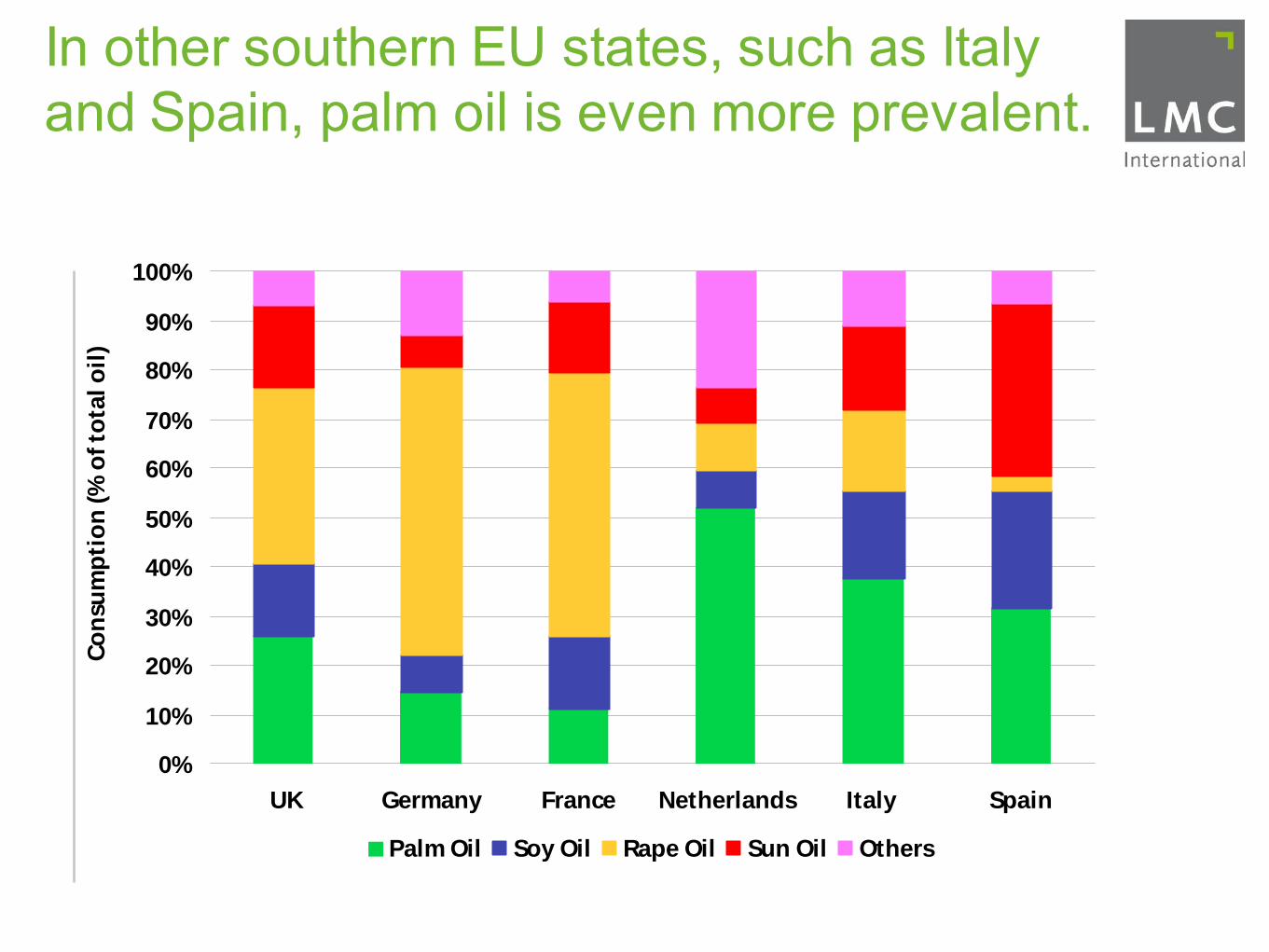

In other southern EU states, such as Italy and Spain, palm oil is even more prevalent.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UK Germany France Netherlands Italy Spain

Co

nsu

mp

tio

n (%

of to

tal o

il)

Palm Oil Soy Oil Rape Oil Sun Oil Others

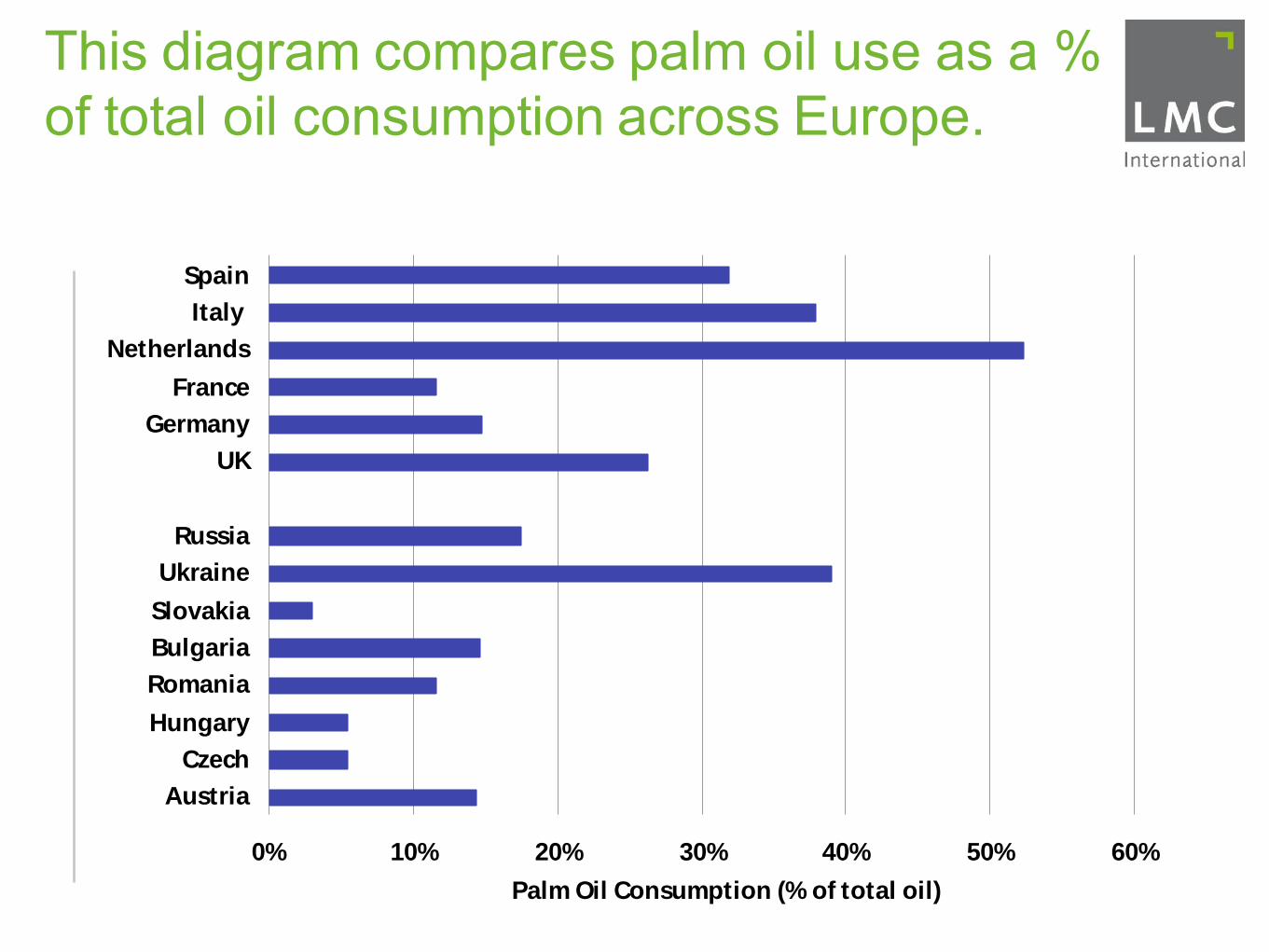

This diagram compares palm oil use as a % of total oil consumption across Europe.

0% 10% 20% 30% 40% 50% 60%

Austria

Czech

Hungary

Romania

Bulgaria

Slovakia

Ukraine

Russia

UK

Germany

France

Netherlands

Italy

Spain

Palm Oil Consumption (% of total oil)

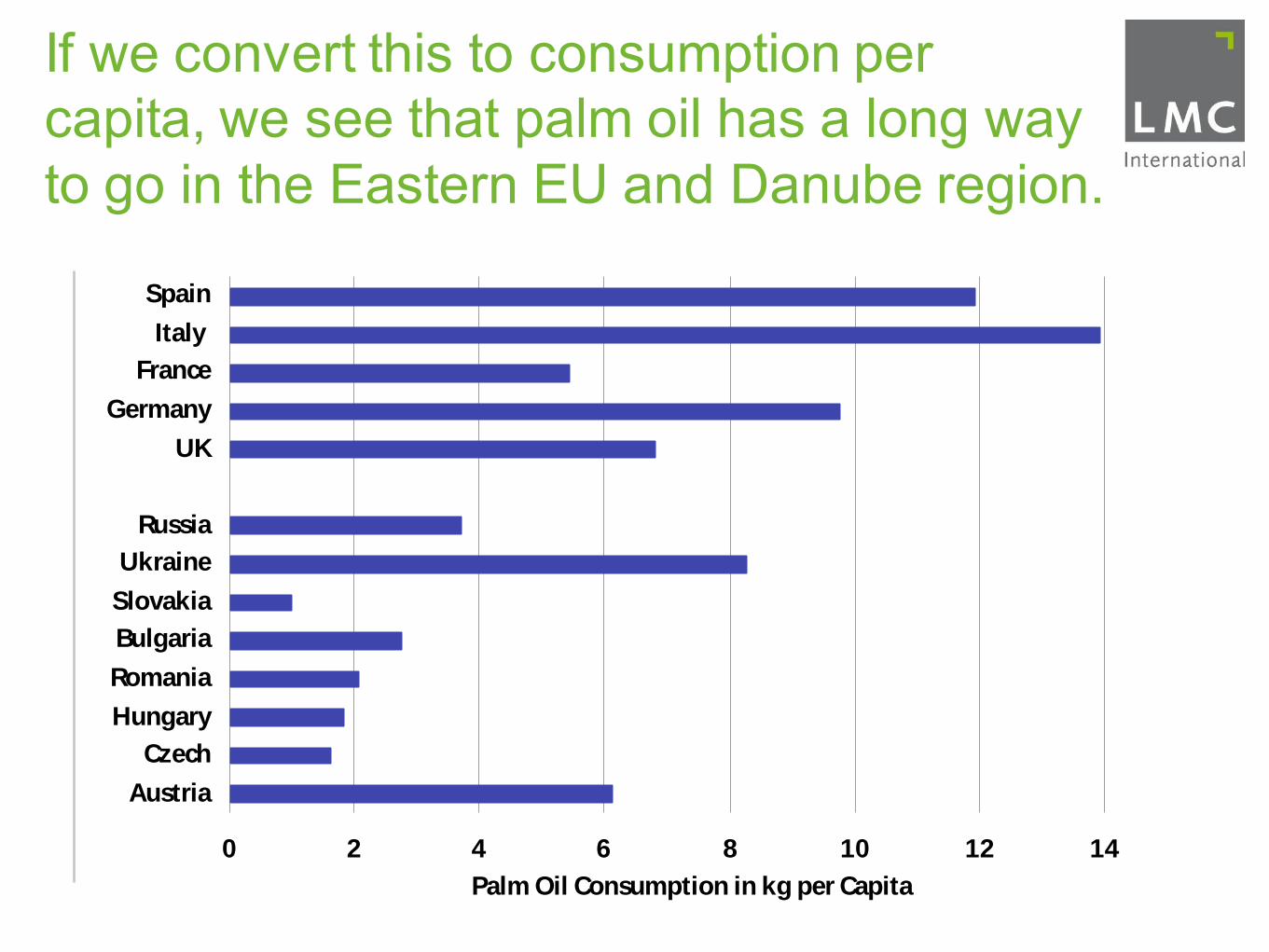

If we convert this to consumption per capita, we see that palm oil has a long way to go in the Eastern EU and Danube region.

0 2 4 6 8 10 12 14

Austria

Czech

Hungary

Romania

Bulgaria

Slovakia

Ukraine

Russia

UK

Germany

France

Italy

Spain

Palm Oil Consumption in kg per Capita

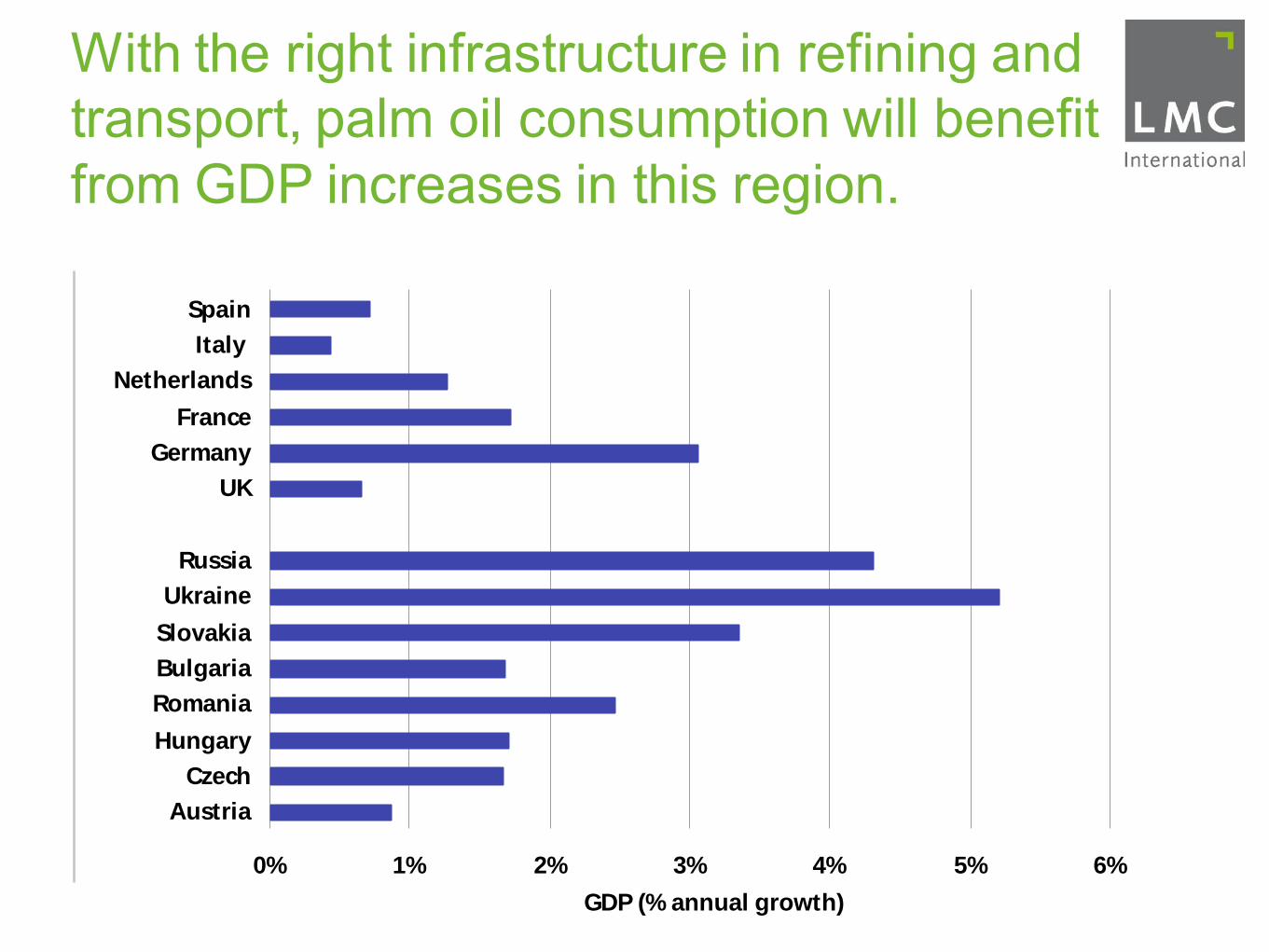

With the right infrastructure in refining and transport, palm oil consumption will benefit from GDP increases in this region.

0% 1% 2% 3% 4% 5% 6%

Austria

Czech

Hungary

Romania

Bulgaria

Slovakia

Ukraine

Russia

UK

Germany

France

Netherlands

Italy

Spain

GDP (% annual growth)

A new way of forecasting oil prices

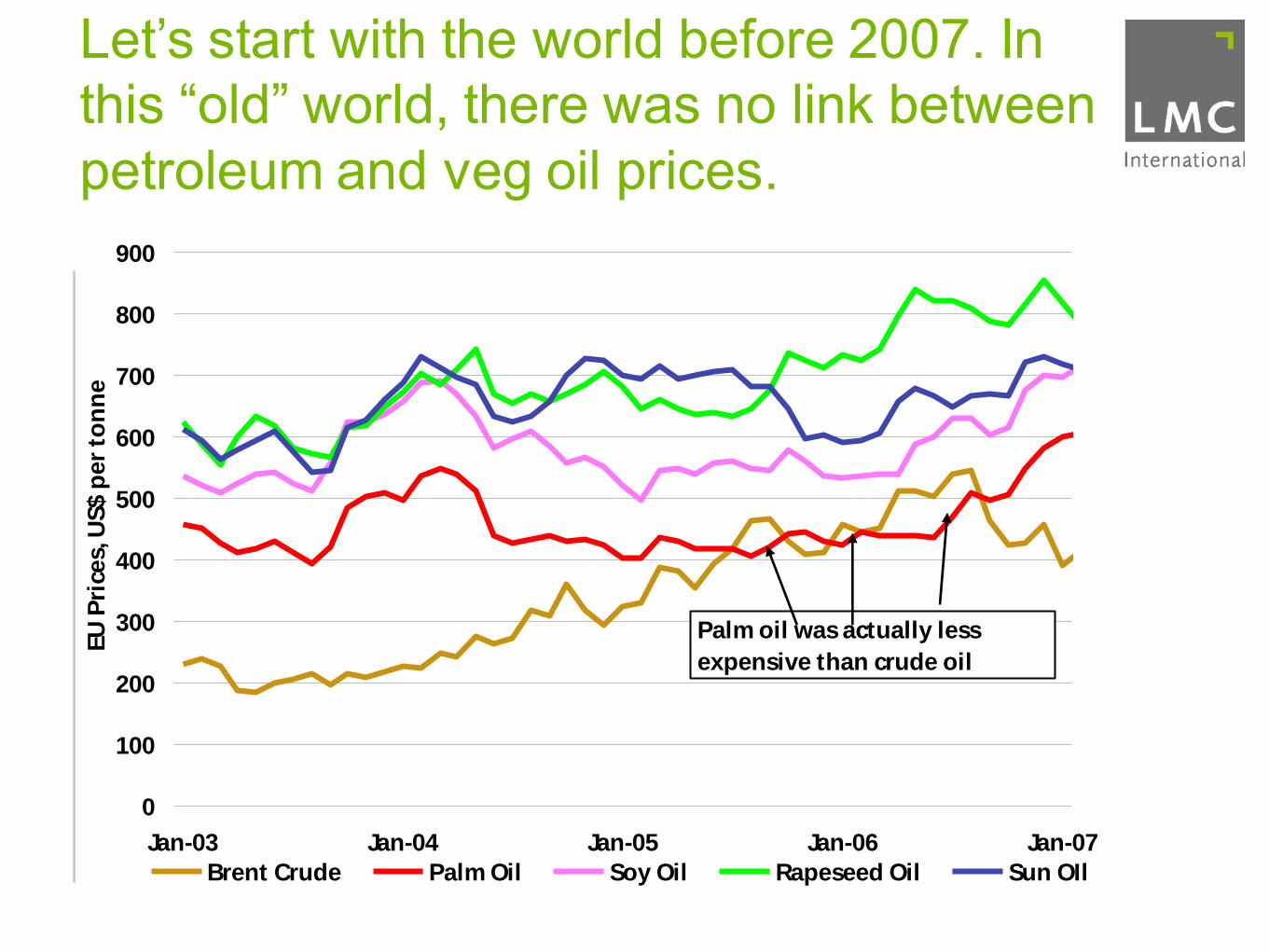

Let’s start with the world before 2007. In this “old” world, there was no link between petroleum and veg oil prices.

0

100

200

300

400

500

600

700

800

900

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07

EU

Pri

ces,

US$ p

er

ton

ne

Brent Crude Palm Oil Soy Oil Rapeseed Oil Sun OIl

Palm oil was actually less

expensive than crude oil

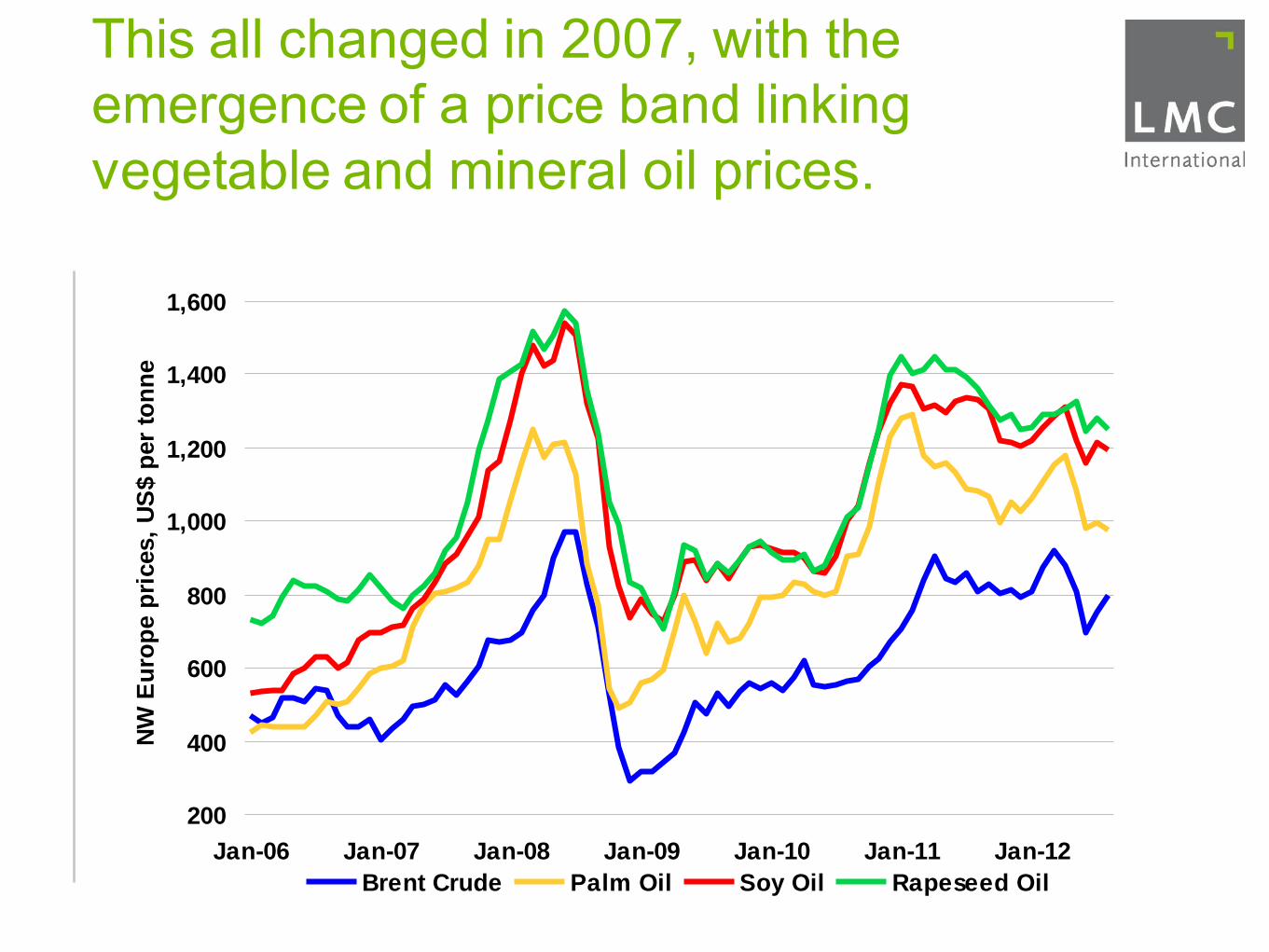

This all changed in 2007, with the emergence of a price band linking vegetable and mineral oil prices.

200

400

600

800

1,000

1,200

1,400

1,600

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

NW

Eu

rop

e p

rices,

US

$ p

er

ton

ne

Brent Crude Palm Oil Soy Oil Rapeseed Oil

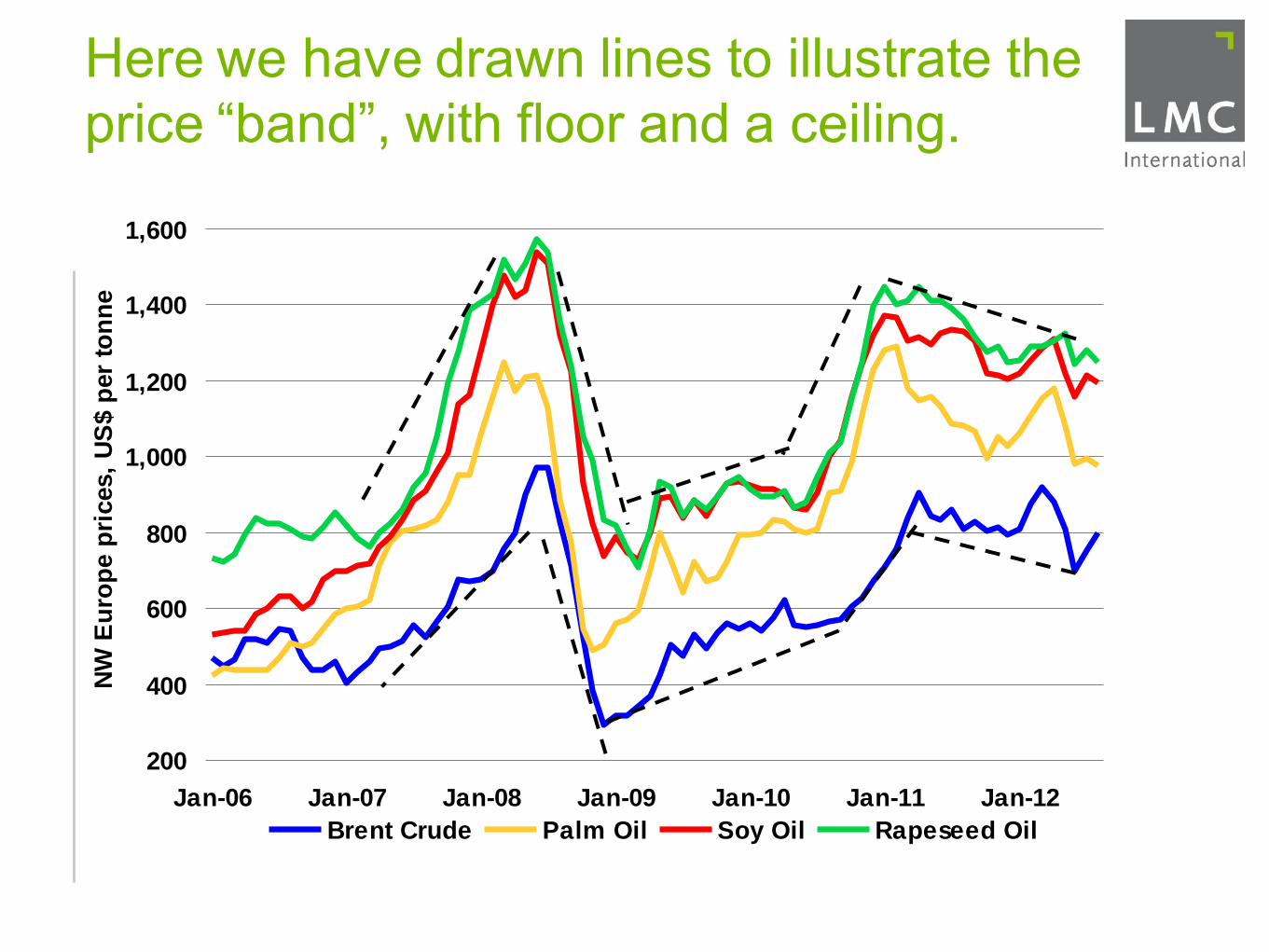

Here we have drawn lines to illustrate the price “band”, with floor and a ceiling.

200

400

600

800

1,000

1,200

1,400

1,600

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

NW

Eu

rop

e p

rices,

US

$ p

er

ton

ne

Brent Crude Palm Oil Soy Oil Rapeseed Oil

Why has the linkage emerged?

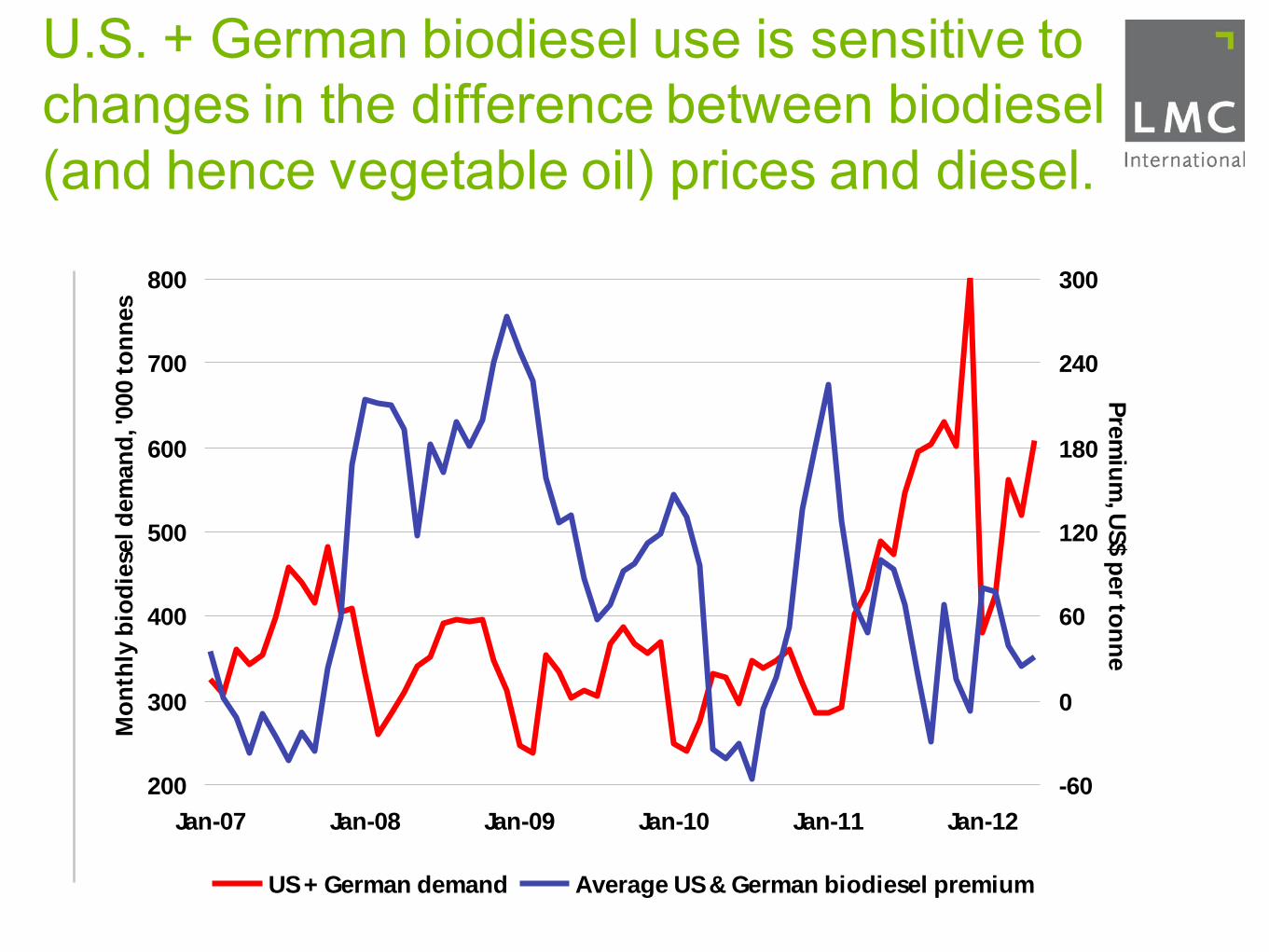

U.S. + German biodiesel use is sensitive to changes in the difference between biodiesel (and hence vegetable oil) prices and diesel.

200

300

400

500

600

700

800

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Mo

nth

ly b

iod

iese

l d

em

an

d, '

000 t

on

nes

-60

0

60

120

180

240

300

Pre

miu

m, U

S$ p

er to

nn

e

US + German demand Average US & German biodiesel premium

This link helps us forecast prices

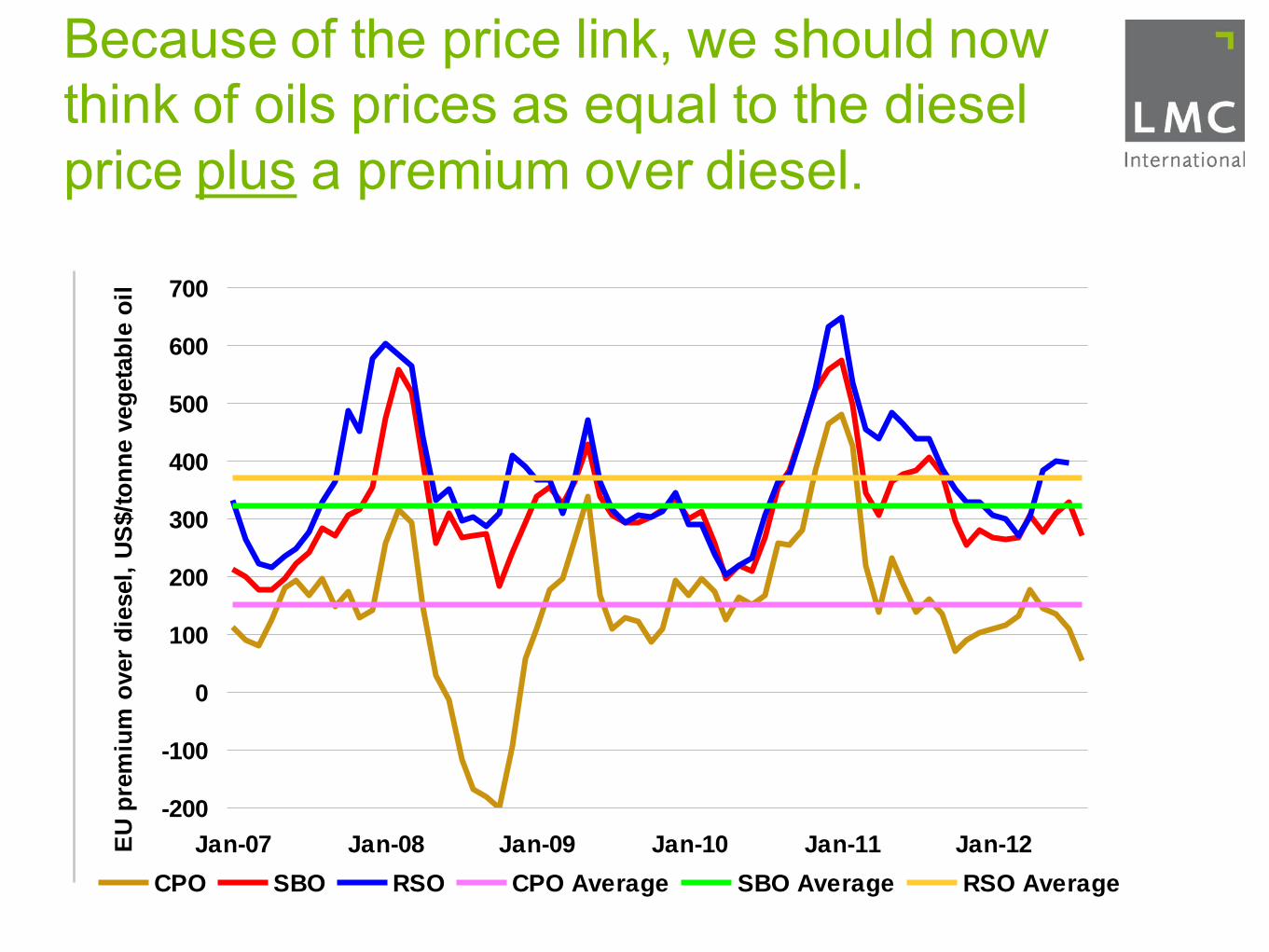

Because of the price link, we should now think of oils prices as equal to the diesel price plus a premium over diesel.

-200

-100

0

100

200

300

400

500

600

700

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12EU

pre

miu

m o

ver

die

sel,

US

$/t

on

ne v

eg

eta

ble

oil

CPO SBO RSO CPO Average SBO Average RSO Average

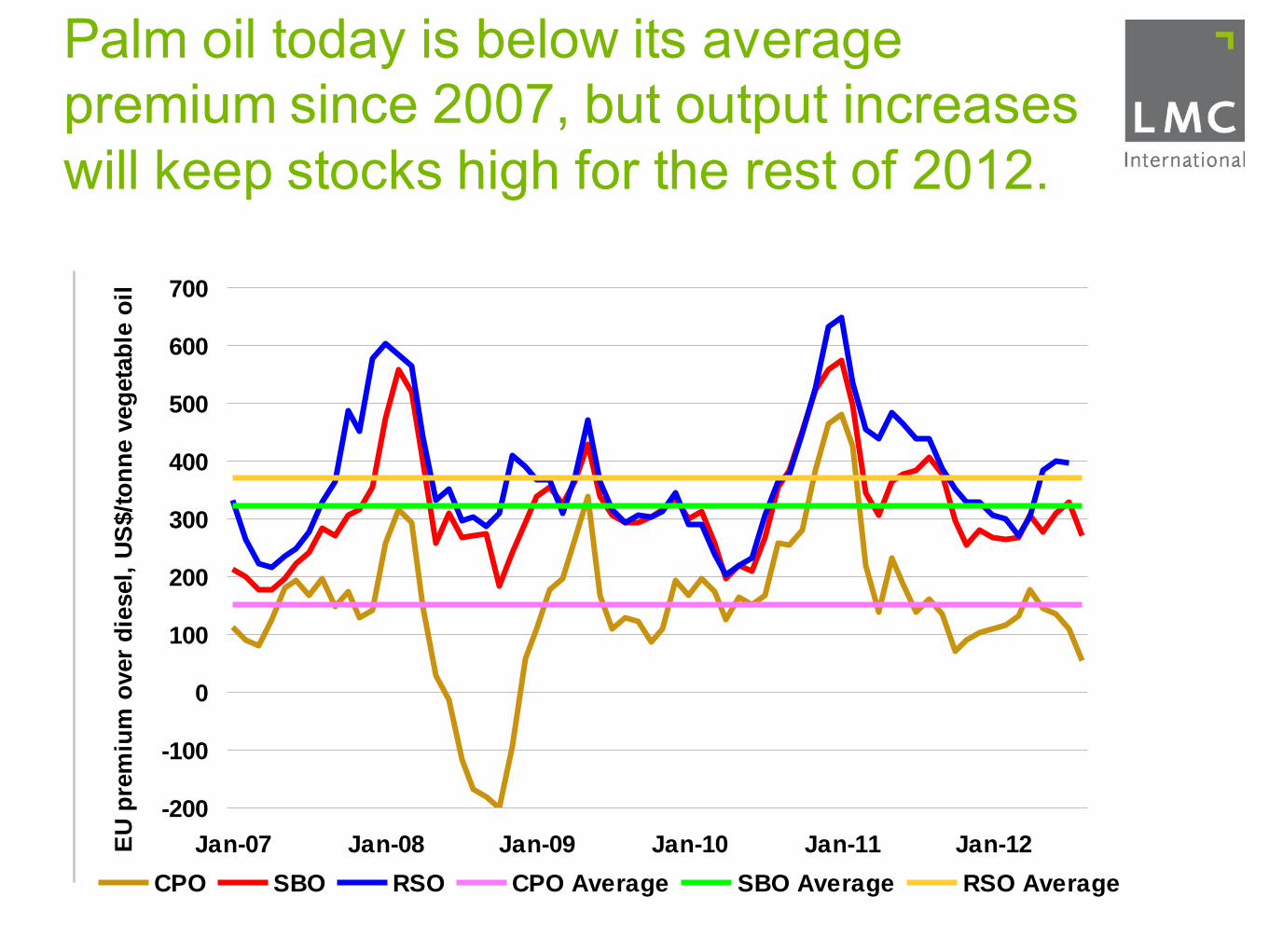

Palm oil today is below its average premium since 2007, but output increases will keep stocks high for the rest of 2012.

-200

-100

0

100

200

300

400

500

600

700

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12EU

pre

miu

m o

ver

die

sel,

US

$/t

on

ne v

eg

eta

ble

oil

CPO SBO RSO CPO Average SBO Average RSO Average

Oil price relativities

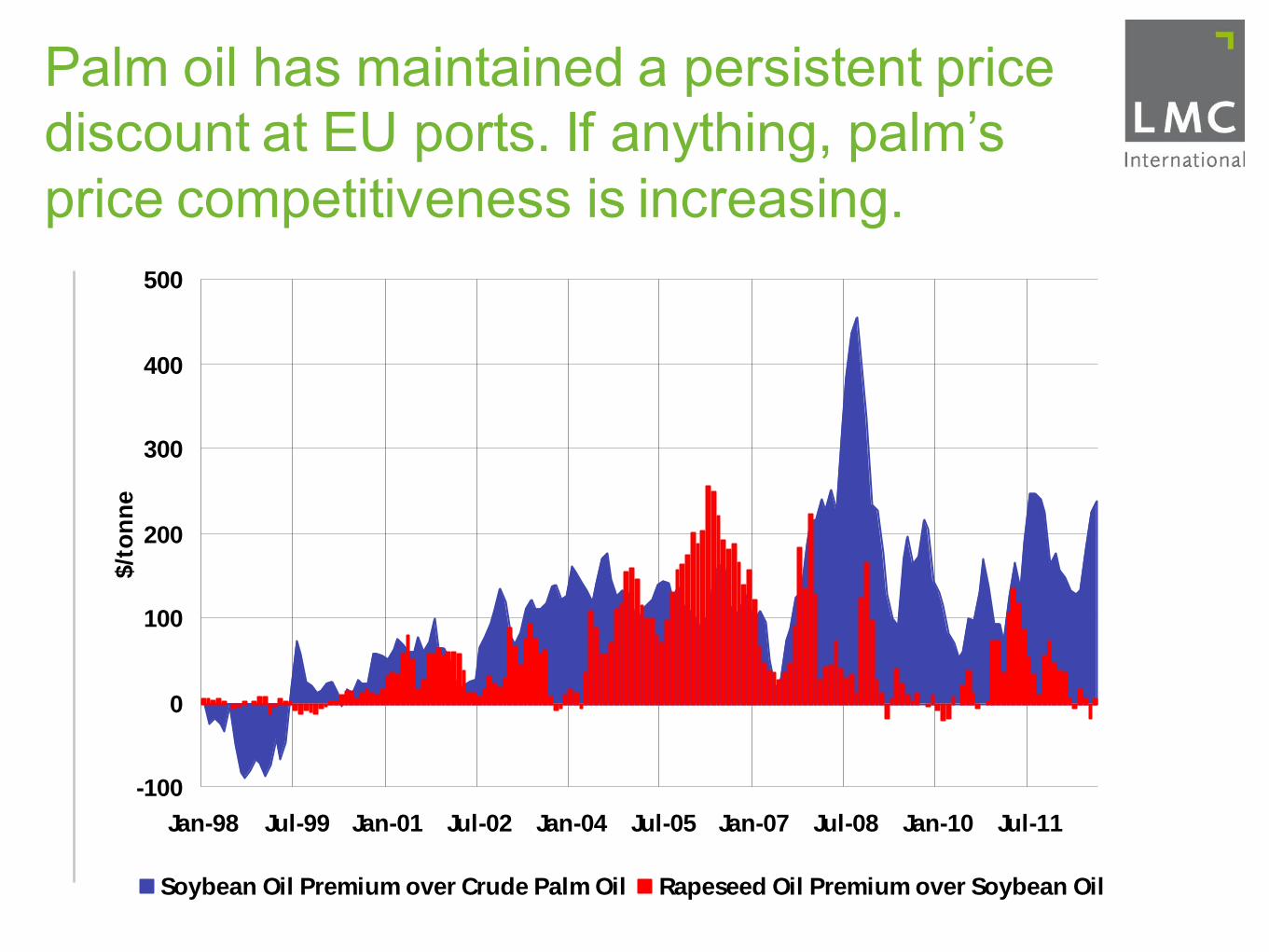

Palm oil has maintained a persistent price discount at EU ports. If anything, palm’s price competitiveness is increasing.

-100

0

100

200

300

400

500

Jan-98 Jul-99 Jan-01 Jul-02 Jan-04 Jul-05 Jan-07 Jul-08 Jan-10 Jul-11

$/t

on

ne

Soybean Oil Premium over Crude Palm Oil Rapeseed Oil Premium over Soybean Oil

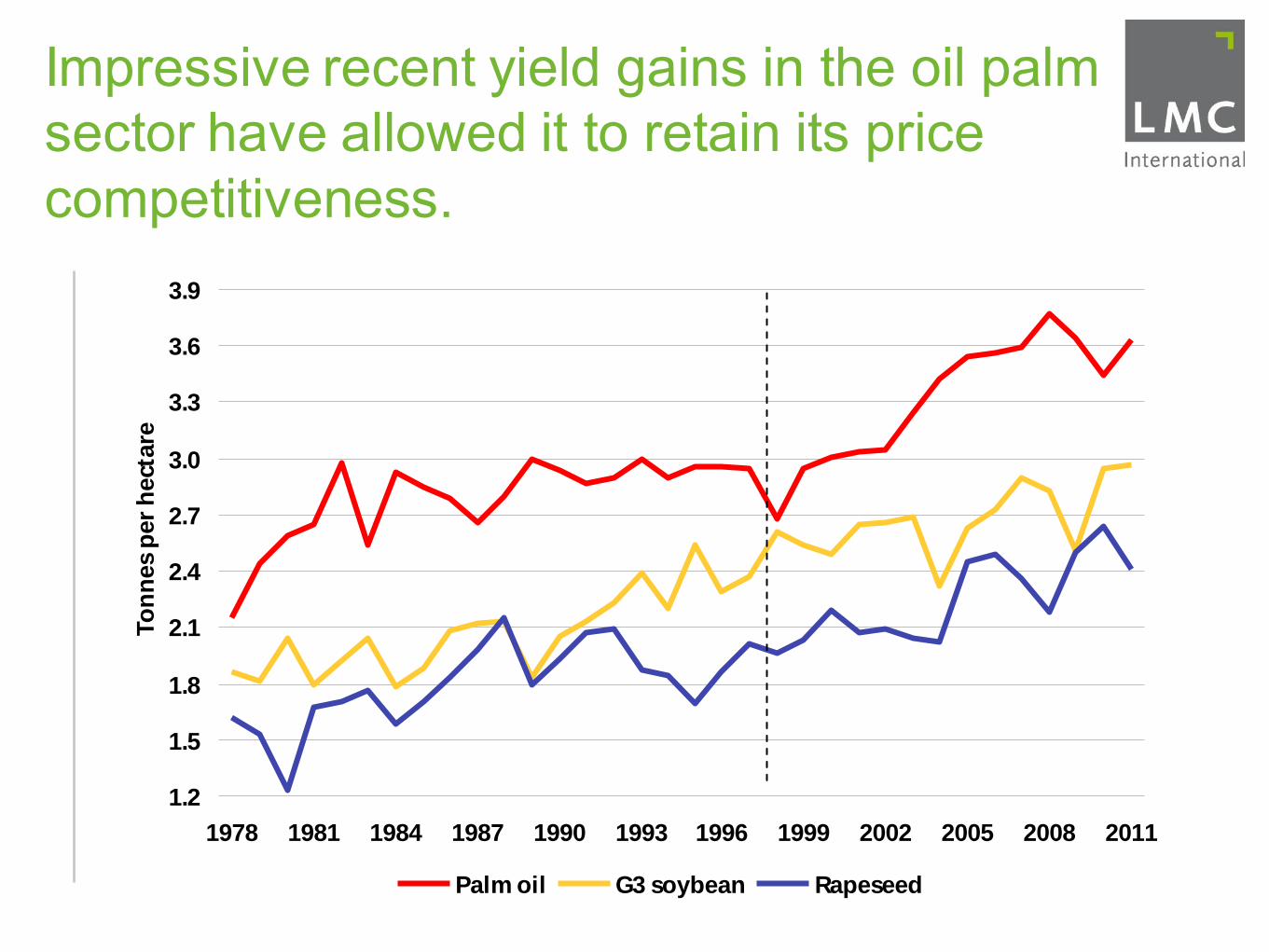

Impressive recent yield gains in the oil palm sector have allowed it to retain its price competitiveness.

1.2

1.5

1.8

2.1

2.4

2.7

3.0

3.3

3.6

3.9

1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

To

nn

es

per

hect

are

Palm oil G3 soybean Rapeseed

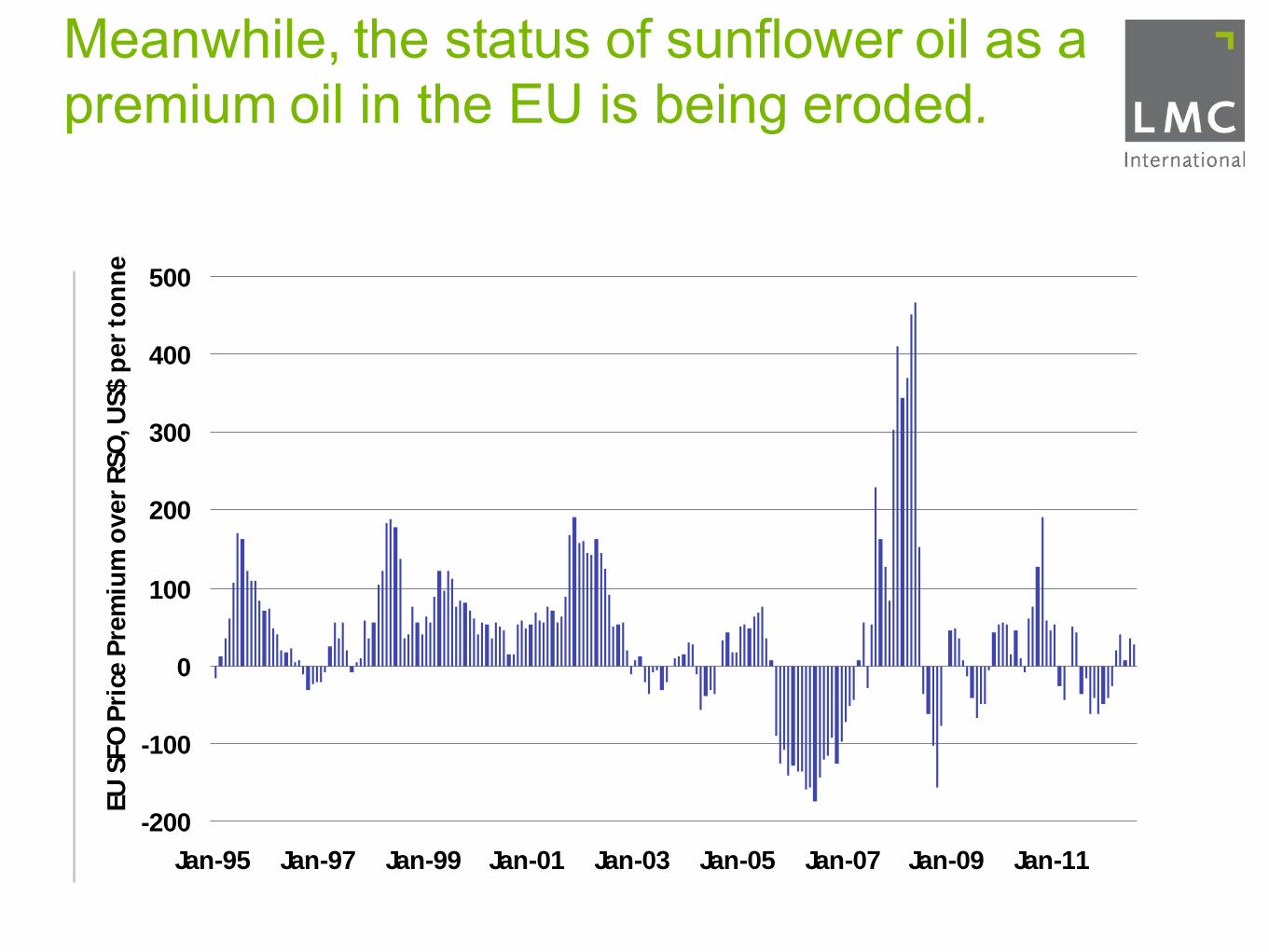

Meanwhile, the status of sunflower oil as a premium oil in the EU is being eroded.

-200

-100

0

100

200

300

400

500

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

EU

SFO

Pri

ce P

rem

ium

over

RSO

, US$ p

er

ton

ne

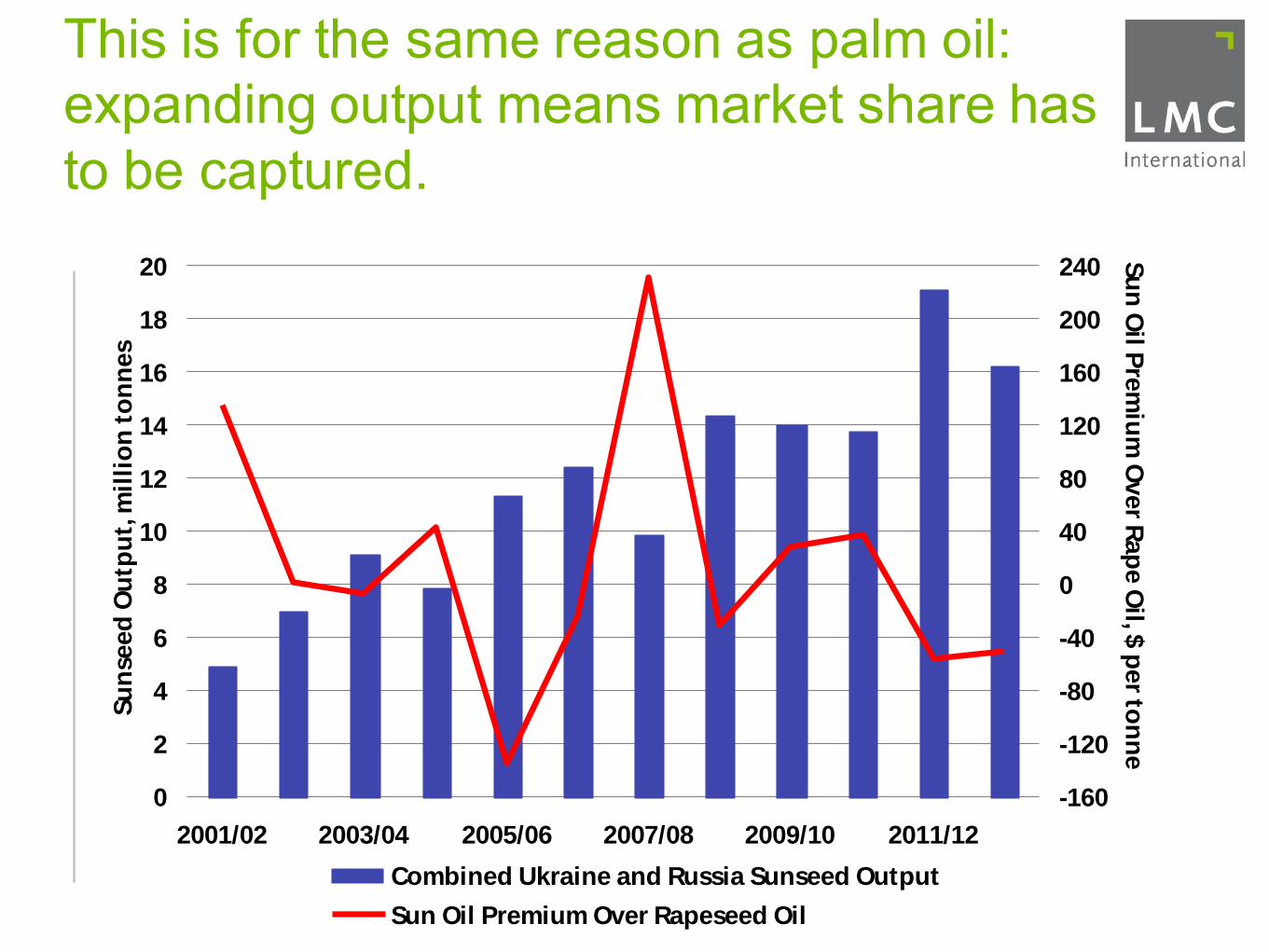

This is for the same reason as palm oil: expanding output means market share has to be captured.

0

2

4

6

8

10

12

14

16

18

20

2001/02 2003/04 2005/06 2007/08 2009/10 2011/12

Su

nse

ed

Ou

tpu

t, m

illi

on

to

nn

es

-160

-120

-80

-40

0

40

80

120

160

200

240

Su

n O

il Pre

miu

m O

ver R

ap

e O

il, $ p

er to

nn

e

Combined Ukraine and Russia Sunseed Output

Sun Oil Premium Over Rapeseed Oil

Conclusions

1.Palm oil consumption is relatively low in the Danube corridor. We would expect this to increase with GDP.

2. Palm prices will find it hard to increase in the next few months as production will be good.

3. Impressive yield gains have underpinned the palm price discount.

4. The sunflower oil premium has also weakened as output has expanded.

Conclusions

New York

1841 BroadwayNew York, NY 10023

USA

T +1 (212) 586-2427F +1 (212) 397-4756

Oxford (HQ)

4th Floor, Clarendon House52 Cornmarket Street,

Oxford OX1 3HJUK

T +44 1865 791737F +44 1865 791739

Kuala Lumpur

B-03-19, Empire SohoEmpire Subang

Jalan SS16/1, SS1647500 Subang Jaya

Selangor Darul EhsanMalaysia

T +603 5611 9337

© LMC International, 2012All rights reserved

This presentation and its contents are to be held confidential by the client, and are not to be disclosed, in whole or in part, in any manner, to a third party without the prior written consent of LMC International.

While LMC has endeavoured to ensure the accuracy of the data, estimates and forecasts contained in this presentation, any decisions based on them (including those involving investment and planning) are at the client’s own risk.

LMC International can accept no liability regarding information analysis and forecasts contained in this presentation.

Singapore

16 Collyer Quay #21-00Singapore 049318

T +65 6818 9231