Embed Size (px)

Citation preview

The future of tourism in Iceland Part I: Context – Icelandic tourism today

September 2013

Part I - context tourism in Iceland.pptx 1

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Context and structure of document

From October 2012– July 2013, BCG conducted an independent report on the long-term

tourism strategy of Destination Iceland. The project, which was carried out in Reykjavik, was

commissioned by a consortium of private Icelandic companies, including Icelandair Group,

Isavia, Blue Lagoon, and Holdur / Europcar.

This set of documents contains the output from the project. It is structured in 6 parts:

• Part I: Context - Icelandic tourism today

• Part II: Aspiration for destination Iceland and Iceland's target visitors

• Part III: Building the destination

• Part IV: Funding the vision

• Part V: Organising for success

• Part VI: Economic impact

This is the first of the six documents

Part I - context tourism in Iceland.pptx 2

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Agenda

• Part I: Context - Icelandic tourism today

• Part II: Aspiration for destination Iceland and Iceland's target visitors

• Part III: Building the destination

• Part IV: Funding the vision

• Part V: Organising for success

• Part VI: Economic impact

Part I - context tourism in Iceland.pptx 3

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

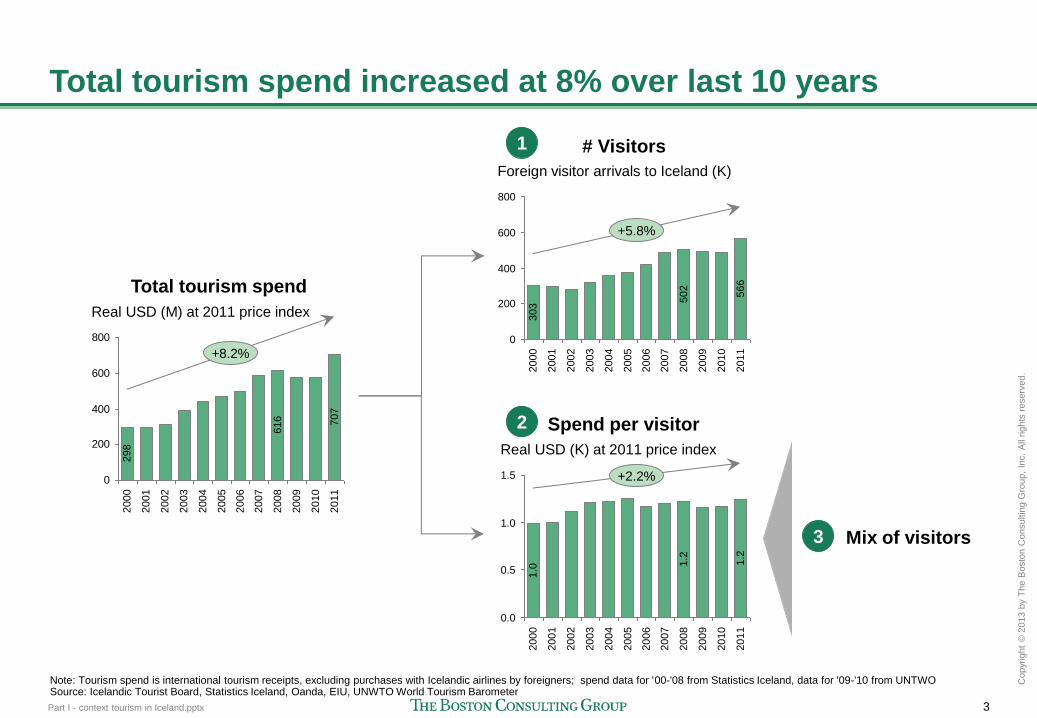

Total tourism spend

Total tourism spend increased at 8% over last 10 years

0

200

400

600

800

Real USD (M) at 2011 price index

2005

2001

+8.2%

2011

707

2009

2008

616

2007

2006

2000

298

2003

2004

2010

2002

Note: Tourism spend is international tourism receipts, excluding purchases with Icelandic airlines by foreigners; spend data for '00-'08 from Statistics Iceland, data for '09-'10 from UNTWO Source: Icelandic Tourist Board, Statistics Iceland, Oanda, EIU, UNWTO World Tourism Barometer

Spend per visitor

Real USD (K) at 2011 price index

2005

1.5

1.0

2001

0.5

+2.2%

2011

1.2

2009

2008

1.2

2007

2006

2004

2003

2000

1.0

0.0

2010

2002

# Visitors

800

2005

600

400

2001

200

+5.8%

2011

566

2009

2008

502

2007

2006

2004

2003

2000

303

Foreign visitor arrivals to Iceland (K)

0

2010

2002

1

2

Mix of visitors 3

Part I - context tourism in Iceland.pptx 4

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

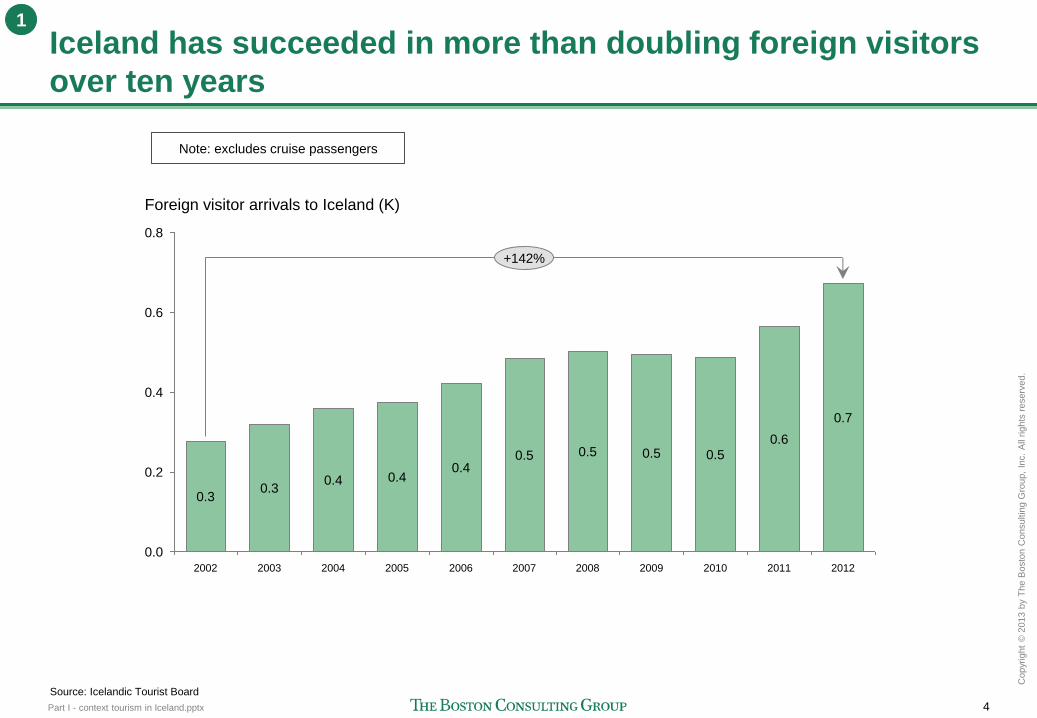

Iceland has succeeded in more than doubling foreign visitors

over ten years

Source: Icelandic Tourist Board

0.4

0.2

0.6

0.8

0.0

Foreign visitor arrivals to Iceland (K)

+142%

0.7

0.4 0.4 0.3

0.3

2012 2011

0.6

2008

0.5

2007

0.5

2006

0.4

2003 2005 2004 2010 2002 2009

0.5 0.5

1

Note: excludes cruise passengers

Part I - context tourism in Iceland.pptx 5

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

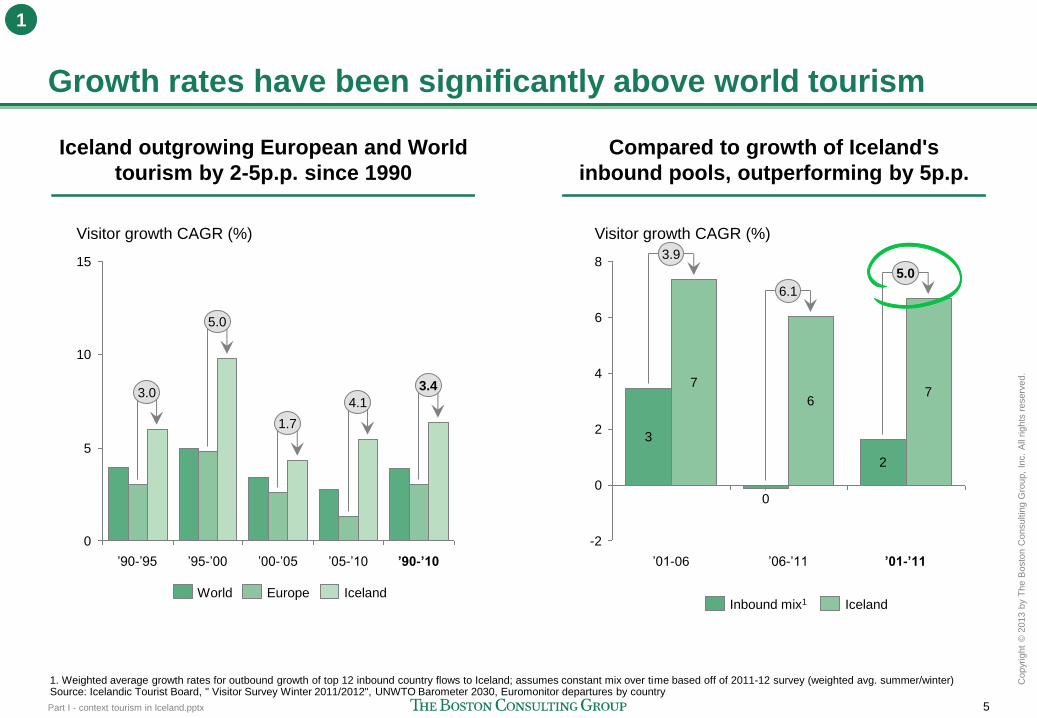

Growth rates have been significantly above world tourism

15

4.1

Visitor growth CAGR (%)

5.0

’90-’10

3.0

’90-’95 ’95-’00

10

’05-’10 ’00-’05

1.7

3.4

5

0

World Iceland Europe

Iceland outgrowing European and World

tourism by 2-5p.p. since 1990

Compared to growth of Iceland's

inbound pools, outperforming by 5p.p.

1. Weighted average growth rates for outbound growth of top 12 inbound country flows to Iceland; assumes constant mix over time based off of 2011-12 survey (weighted avg. summer/winter) Source: Icelandic Tourist Board, " Visitor Survey Winter 2011/2012", UNWTO Barometer 2030, Euromonitor departures by country

0

3

7 4

2

3.9

-2

’01-06

2

6

’06-’11

Visitor growth CAGR (%)

0

8

6

’01-’11

7

6.1

5.0

Iceland Inbound mix1

1

Part I - context tourism in Iceland.pptx 6

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

For example, Inspired by Iceland campaign successfully grew

tourist volume after Eyjafjallajökull eruption

Source: The Brooklyn Brothers

Primary objective to increase

visitor numbers

Success measured on

visitor numbers

1

Part I - context tourism in Iceland.pptx 7

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

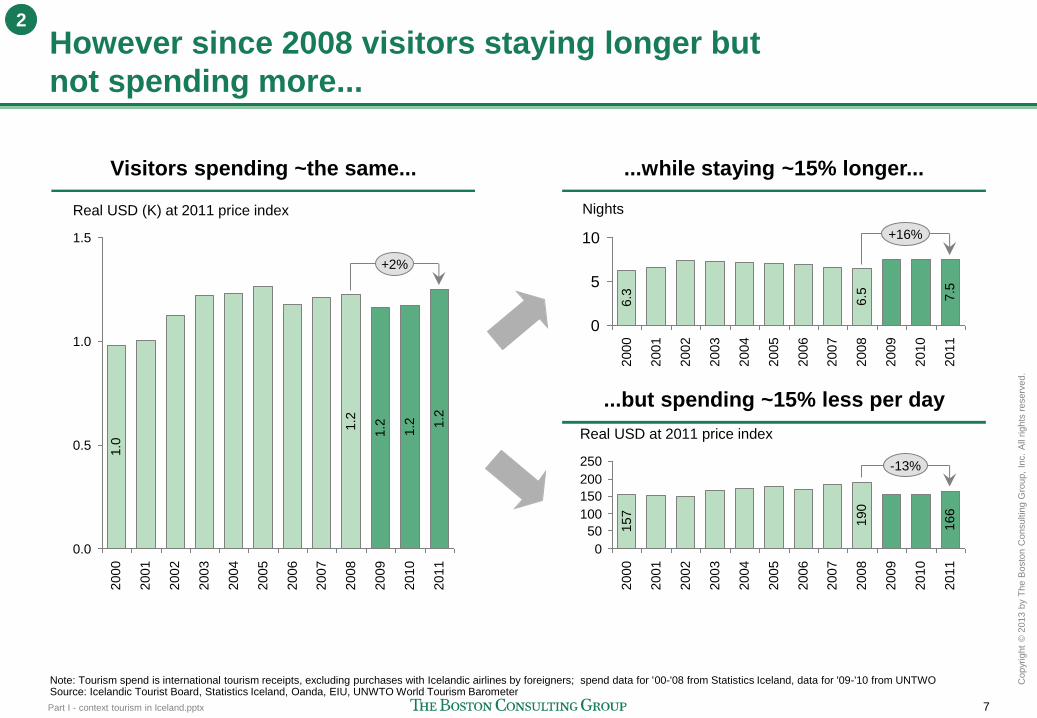

However since 2008 visitors staying longer but

not spending more...

Note: Tourism spend is international tourism receipts, excluding purchases with Icelandic airlines by foreigners; spend data for '00-'08 from Statistics Iceland, data for '09-'10 from UNTWO Source: Icelandic Tourist Board, Statistics Iceland, Oanda, EIU, UNWTO World Tourism Barometer

2002

2001

2003

-13%

2011

166

2010

2009

2008

190

2007

2006

2005

2004

157

2000

200

100

50

150

Real USD at 2011 price index

250

0

0

7.5

2009

Nights

2002

10

5

+16%

2011

2010

2008

6.5

2007

2006

2005

2004

2003

2001

2000

6.3

Visitors spending ~the same... ...while staying ~15% longer...

...but spending ~15% less per day

Real USD (K) at 2011 price index

1.5

1.0

0.5

0.0

2011

1.2

2010

+2%

2009

2008

1.2

2007

2006

2005

2004

2003

2002

2001

2000

1.0

1.2

1.2

2

Part I - context tourism in Iceland.pptx 8

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

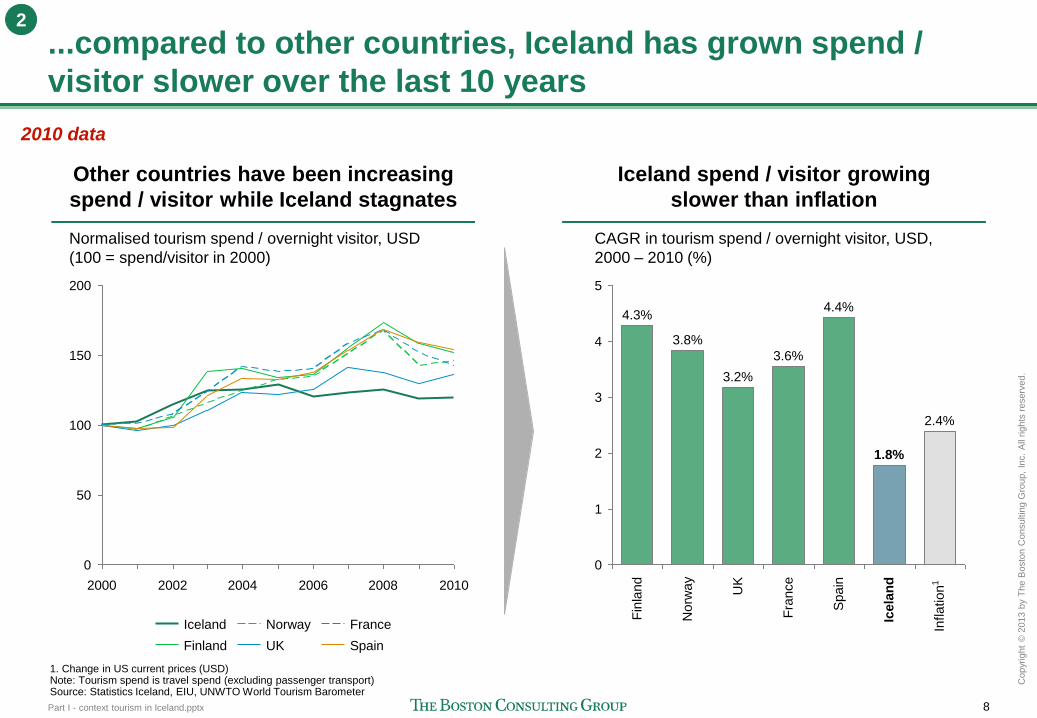

...compared to other countries, Iceland has grown spend /

visitor slower over the last 10 years

Normalised tourism spend / overnight visitor, USD

(100 = spend/visitor in 2000)

0

150

100

50

2010 2008 2006 2004 2002 2000

200

France

Finland

Iceland

UK

Norway

Spain

Other countries have been increasing

spend / visitor while Iceland stagnates

Iceland spend / visitor growing

slower than inflation

2010 data

4.3%

2

Fra

nce

CAGR in tourism spend / overnight visitor, USD,

2000 – 2010 (%)

Spain

1.8%

1

Icela

nd

4

2.4%

Inflation

1

3.6%

5

Fin

land

Norw

ay

UK

3

3.8%

3.2%

4.4%

0

1. Change in US current prices (USD) Note: Tourism spend is travel spend (excluding passenger transport) Source: Statistics Iceland, EIU, UNWTO World Tourism Barometer

2

Part I - context tourism in Iceland.pptx 9

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

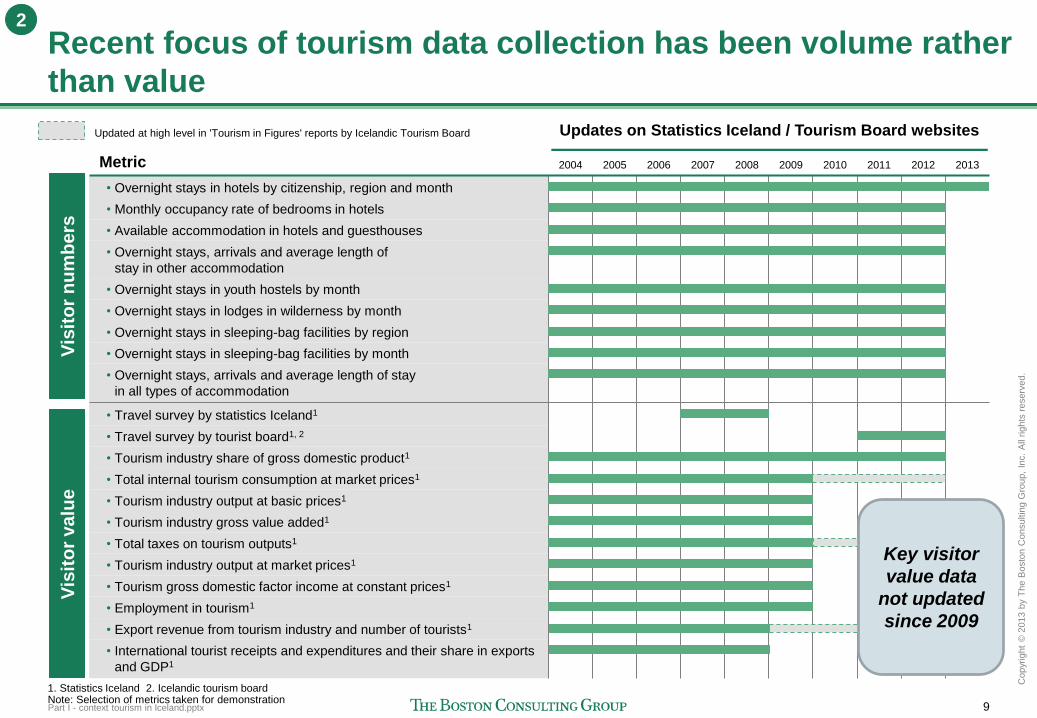

Recent focus of tourism data collection has been volume rather

than value

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

• Tourism industry share of gross domestic product1

• Tourism industry output at basic prices1

• Tourism industry gross value added1

• Total internal tourism consumption at market prices1

Metric

• Overnight stays, arrivals and average length of

stay in other accommodation

• Total taxes on tourism outputs1

• Export revenue from tourism industry and number of tourists1

• Travel survey by statistics Iceland1

• Overnight stays in lodges in wilderness by month

• Overnight stays in youth hostels by month

• Travel survey by tourist board1, 2

• Overnight stays in sleeping-bag facilities by month

• Overnight stays in hotels by citizenship, region and month

• Monthly occupancy rate of bedrooms in hotels

• International tourist receipts and expenditures and their share in exports

and GDP1

• Tourism gross domestic factor income at constant prices1

• Overnight stays, arrivals and average length of stay

in all types of accommodation

• Tourism industry output at market prices1

• Overnight stays in sleeping-bag facilities by region

• Employment in tourism1

• Available accommodation in hotels and guesthouses

Vis

ito

r n

um

be

rs

Vis

ito

r va

lue

1. Statistics Iceland 2. Icelandic tourism board Note: Selection of metrics taken for demonstration

Updates on Statistics Iceland / Tourism Board websites Updated at high level in 'Tourism in Figures' reports by Icelandic Tourism Board

Key visitor

value data

not updated

since 2009

2

Part I - context tourism in Iceland.pptx 10

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

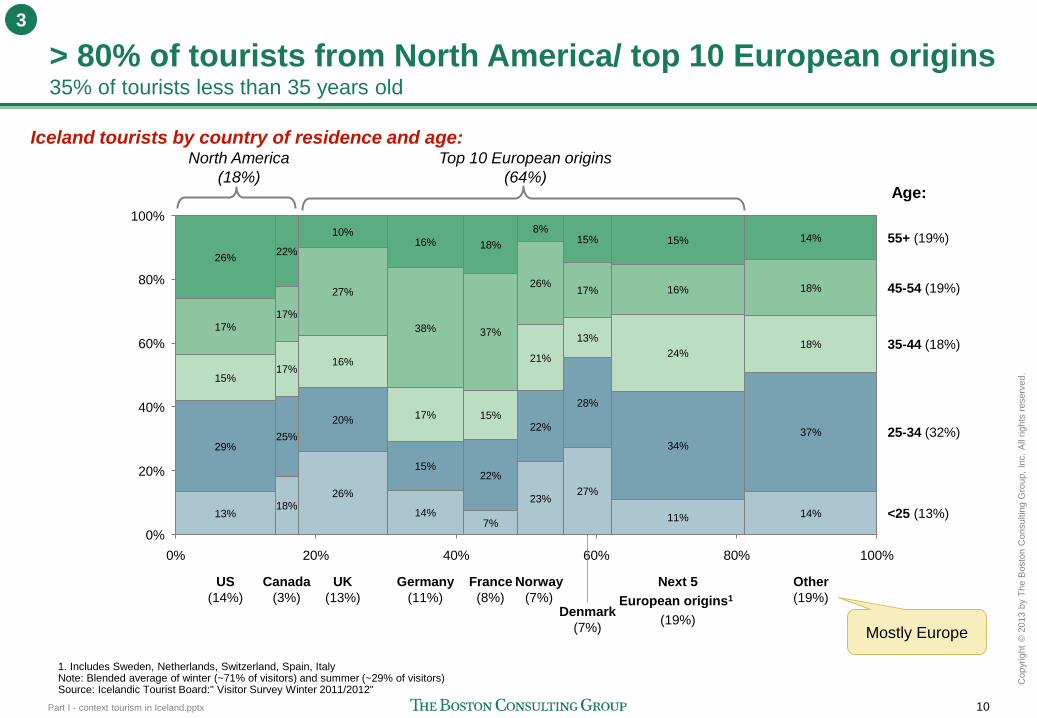

> 80% of tourists from North America/ top 10 European origins 35% of tourists less than 35 years old

40%

60%

80%

0%

100%

0%

40%

20%

20%

60%

100% 80%

27%

28%

13%

17%

15%

Norway

(7%)

23%

22%

21%

26%

France

(8%)

7%

22%

US

(14%)

13%

29%

15%

17%

26%

15%

37%

18%

Germany

(11%)

14%

15%

17%

38%

16%

UK

(13%)

26%

20%

27%

10%

Canada

(3%)

18%

25%

17%

17%

22%

16%

<25 (13%)

25-34 (32%)

Next 5

European origins1

(19%)

35-44 (18%)

45-54 (19%)

55+ (19%)

Other

(19%)

14%

37%

18%

18%

14% 8%

11%

34%

24%

16%

15%

Denmark

(7%)

1. Includes Sweden, Netherlands, Switzerland, Spain, Italy Note: Blended average of winter (~71% of visitors) and summer (~29% of visitors) Source: Icelandic Tourist Board:" Visitor Survey Winter 2011/2012"

Age:

Mostly Europe

Iceland tourists by country of residence and age: North America

(18%)

Top 10 European origins

(64%)

3

Part I - context tourism in Iceland.pptx 11

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

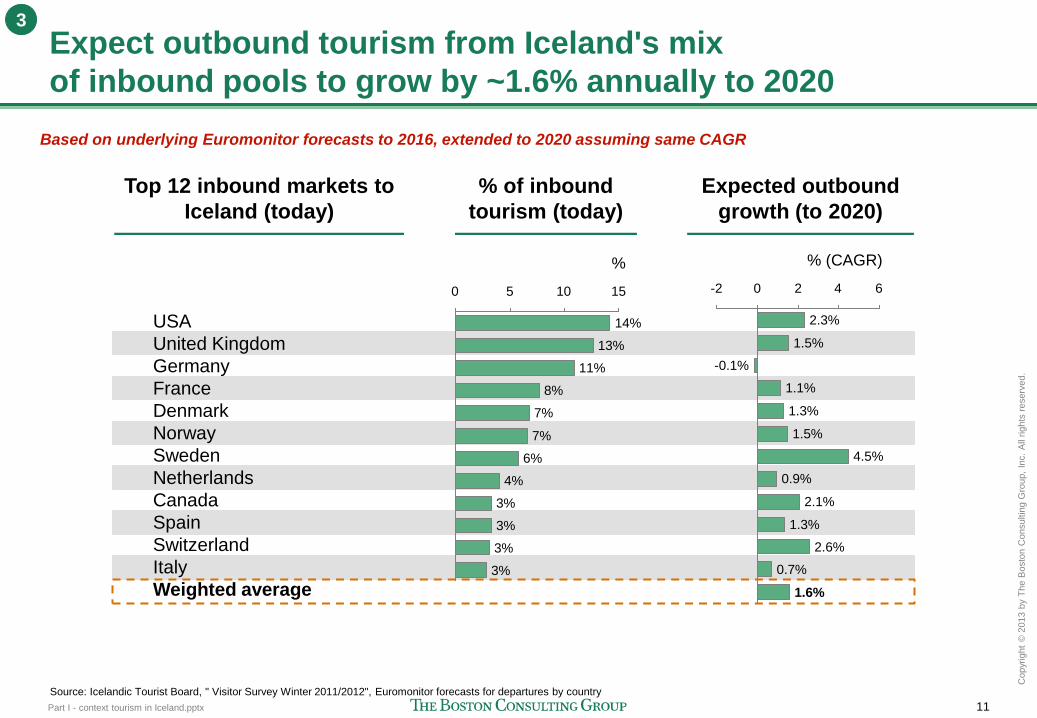

Expect outbound tourism from Iceland's mix

of inbound pools to grow by ~1.6% annually to 2020

Based on underlying Euromonitor forecasts to 2016, extended to 2020 assuming same CAGR

Source: Icelandic Tourist Board, " Visitor Survey Winter 2011/2012", Euromonitor forecasts for departures by country

Top 12 inbound markets to

Iceland (today)

USA

United Kingdom

Germany

France

Denmark

Norway

Sweden

Netherlands

Canada

Spain

Switzerland

Italy

Weighted average

% of inbound

tourism (today)

Expected outbound

growth (to 2020)

14%

%

3%

3%

3%

5 0 10 15

7%

7%

8%

11%

13%

6%

4%

3%

0.7%

0

% (CAGR)

2.6%

1.3%

2.1%

0.9%

4.5%

1.5%

1.3%

1.1%

-0.1%

1.5%

2.3%

-2 2 4 6

1.6%

3

Part I - context tourism in Iceland.pptx 12

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

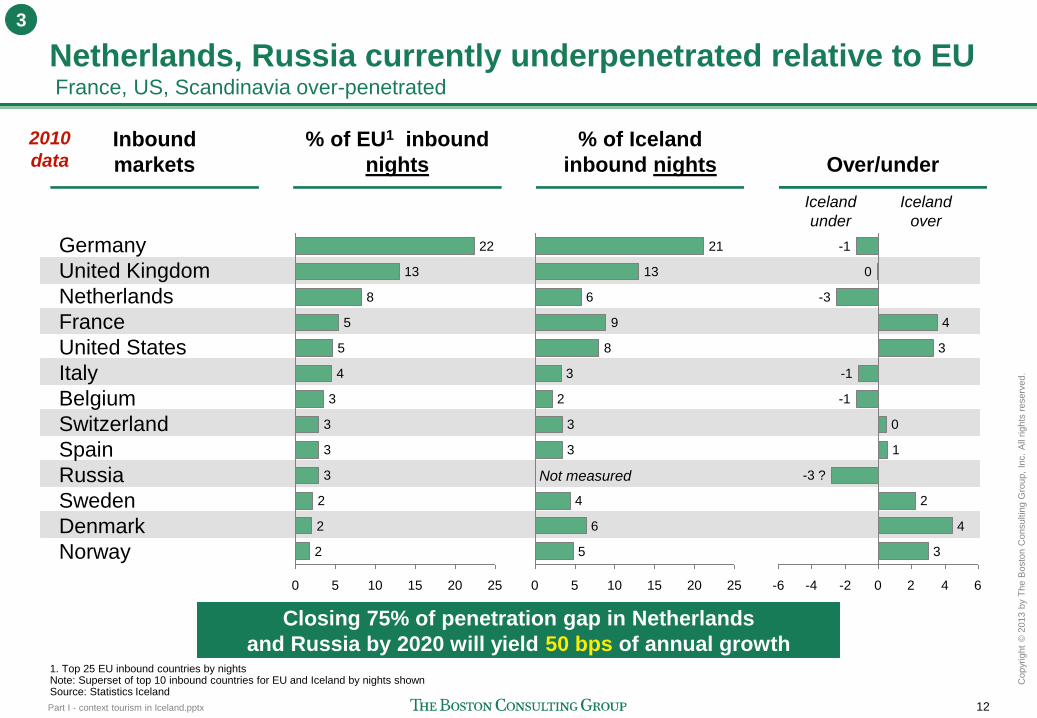

Netherlands, Russia currently underpenetrated relative to EU France, US, Scandinavia over-penetrated

Inbound

markets

Germany

United Kingdom

Netherlands

France

United States

Italy

Belgium

Switzerland

Spain

Russia

Sweden

Denmark

Norway

% of EU1 inbound

nights

% of Iceland

inbound nights Over/under

1. Top 25 EU inbound countries by nights Note: Superset of top 10 inbound countries for EU and Iceland by nights shown Source: Statistics Iceland

25 20 15 10 5 0

2

2

2

3

3

3

3

4

5

5

8

13

22

25 20 15 10 5 0

5

6

4

3

3

2

3

8

9

6

13

21

6 4 2 0 -2 -4 -6

3

4

2

-3 ?

1

0

-1

-1

3

4

-3

0

-1

Not measured

2010

data

Iceland

over

Iceland

under

Closing 75% of penetration gap in Netherlands

and Russia by 2020 will yield 50 bps of annual growth

3

Part I - context tourism in Iceland.pptx 13

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

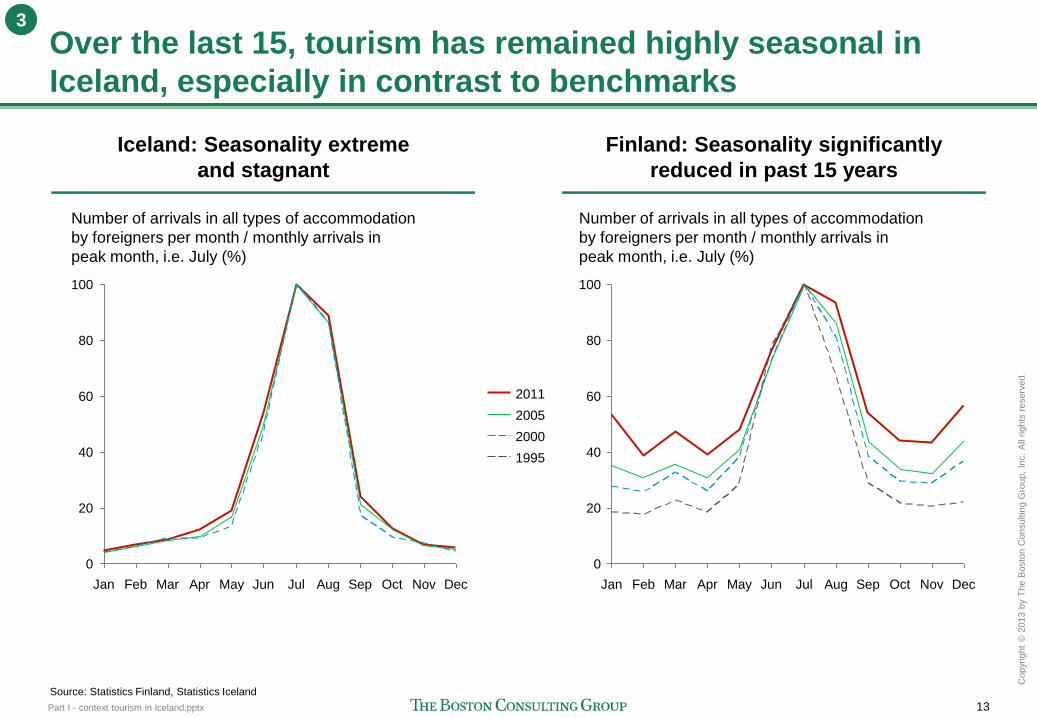

Over the last 15, tourism has remained highly seasonal in

Iceland, especially in contrast to benchmarks

Dec Nov Oct Sep Aug Jul Jun May Apr Mar Feb Jan

Number of arrivals in all types of accommodation

by foreigners per month / monthly arrivals in

peak month, i.e. July (%)

100

80

60

40

20

0

Finland: Seasonality significantly

reduced in past 15 years

Iceland: Seasonality extreme

and stagnant

Apr May Mar Feb Jan

Number of arrivals in all types of accommodation

by foreigners per month / monthly arrivals in

peak month, i.e. July (%)

100

80

60

40

20

0

Dec Nov Oct Sep Aug Jul Jun

1995

2000

2005

2011

Source: Statistics Finland, Statistics Iceland

3

Part I - context tourism in Iceland.pptx 14

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

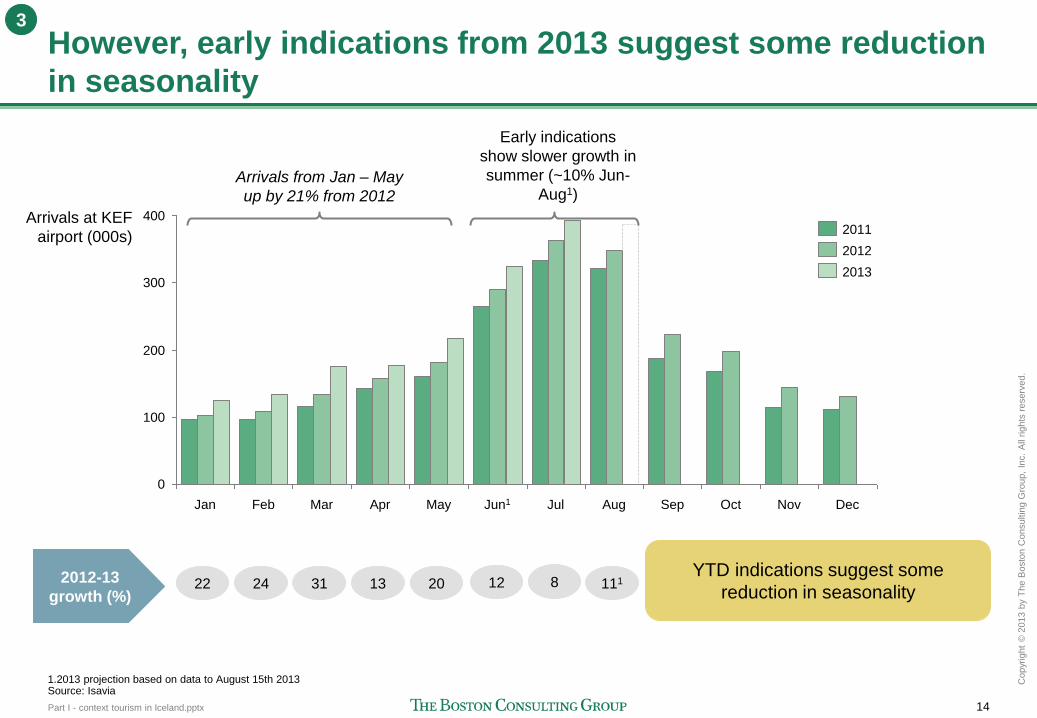

However, early indications from 2013 suggest some reduction

in seasonality

0

400

300

100

200

Arrivals at KEF

airport (000s)

Jan Dec Nov Oct Sep Aug Jul Jun1 May Apr Mar Feb

2013

2012

2011

1.2013 projection based on data to August 15th 2013 Source: Isavia

2012-13

growth (%) 22 24 31 13

YTD indications suggest some

reduction in seasonality 20 12

Arrivals from Jan – May

up by 21% from 2012

Early indications

show slower growth in

summer (~10% Jun-

Aug1)

8

3

111

Part I - context tourism in Iceland.pptx 15

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

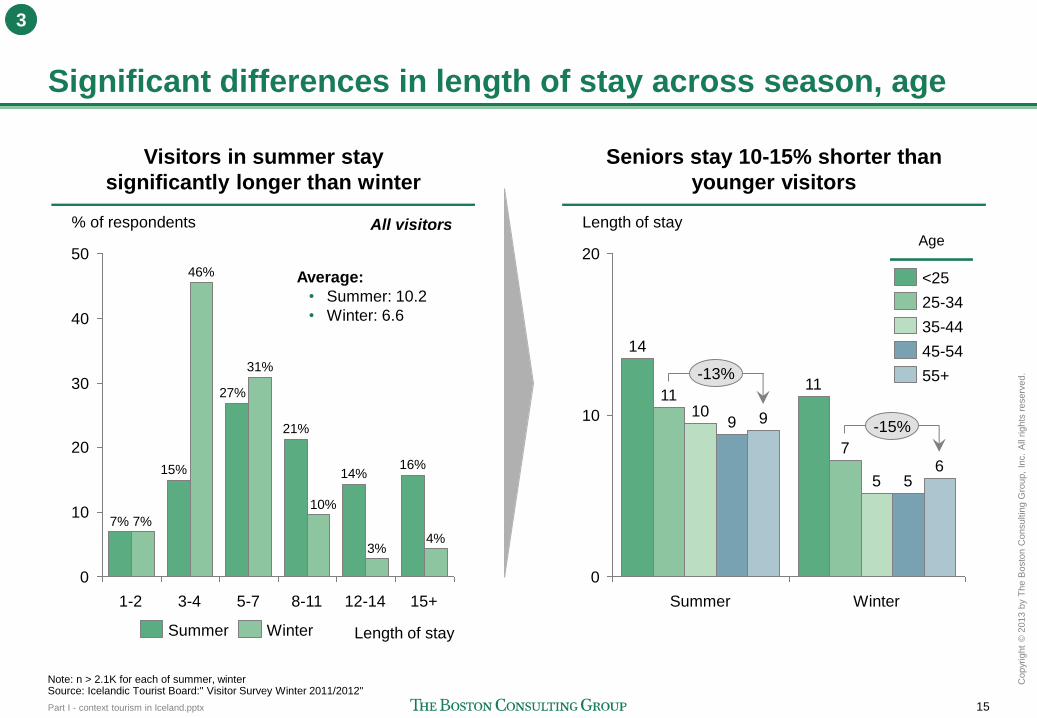

Significant differences in length of stay across season, age

% of respondents

50

40

30

20

10

0

Length of stay

15+

4%

16%

12-14

3%

14%

8-11

10%

21%

5-7

31%

27%

3-4

46%

15%

1-2

7% 7%

Note: n > 2.1K for each of summer, winter Source: Icelandic Tourist Board:" Visitor Survey Winter 2011/2012"

All visitors Length of stay

20

10

0

-15%

-13%

Winter

6 5 5

7

11

Summer

9 9 10

11

14

Visitors in summer stay

significantly longer than winter

Seniors stay 10-15% shorter than

younger visitors

Winter Summer

Average:

• Summer: 10.2

• Winter: 6.6

55+

45-54

35-44

25-34

<25

Age

3

Part I - context tourism in Iceland.pptx 16

Copyr

ight

© 2

013 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

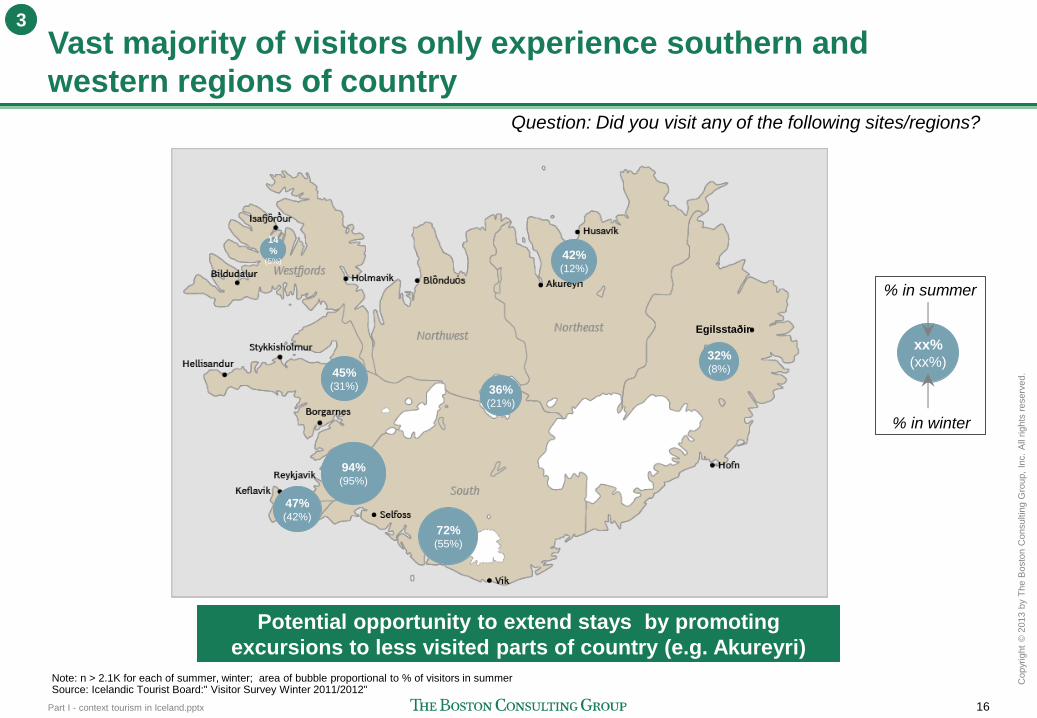

Vast majority of visitors only experience southern and

western regions of country Question: Did you visit any of the following sites/regions?

Potential opportunity to extend stays by promoting

excursions to less visited parts of country (e.g. Akureyri)

Note: n > 2.1K for each of summer, winter; area of bubble proportional to % of visitors in summer Source: Icelandic Tourist Board:" Visitor Survey Winter 2011/2012"

3

xx%

(xx%)

% in summer

% in winter

Egilsstaðir

94% (95%)

47% (42%)

14

% (5%)

45% (31%)

72% (55%)

36% (21%)

32% (8%)

42% (12%)

Egilsstaðir