Embed Size (px)

Citation preview

MEGH

1

The Future of the Wax Industry

MEGH

2

MontanCarnauba BeeswaxCandelillaHOF Waxes

PE Wax

PE

OxidizedParaffins Micros FT Waxes

World Wax Market

MEGH

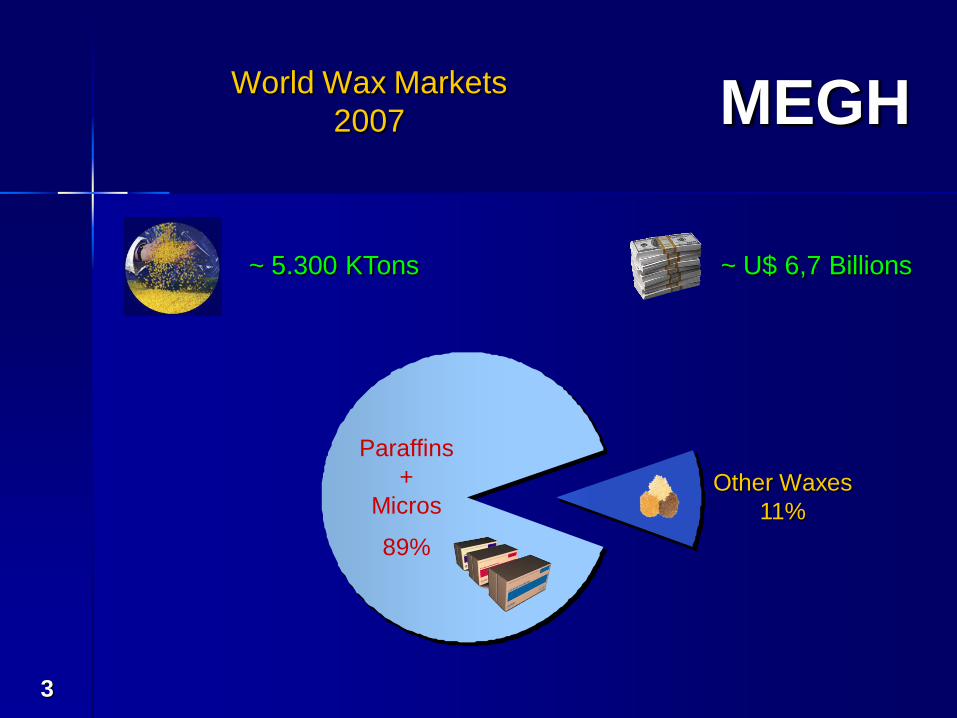

3

World Wax Markets

2007

Paraffins

+

Micros

89%

Other Waxes

11%

~ U$ 6,7 Billions~ 5.300 KTons

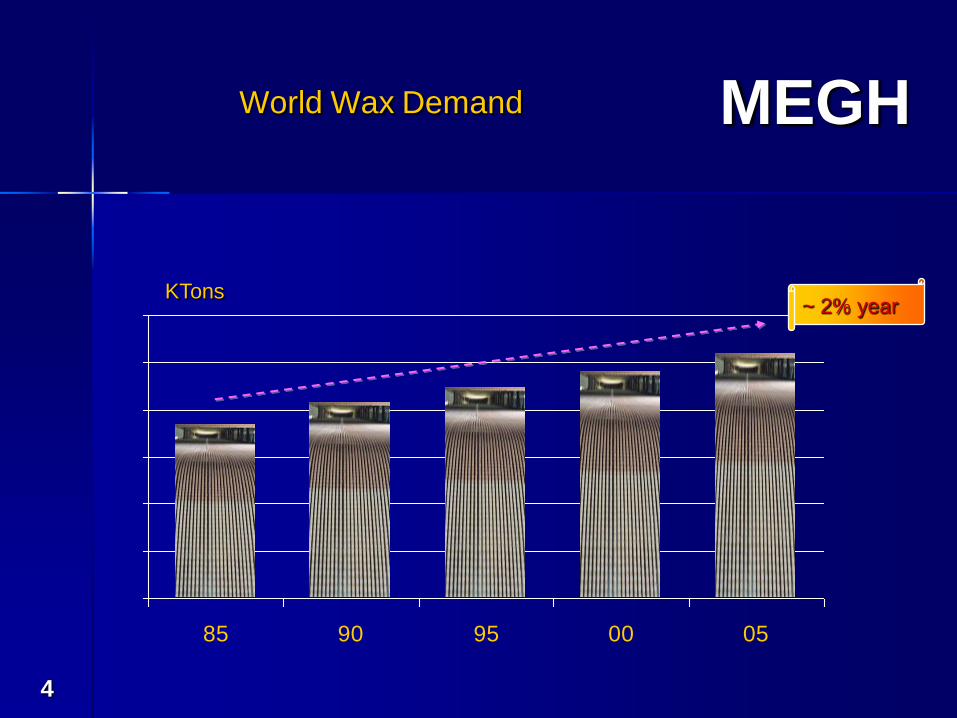

MEGH

4

85 90 95 00 05

KTons

World Wax Demand

~ 2% year

MEGH

5

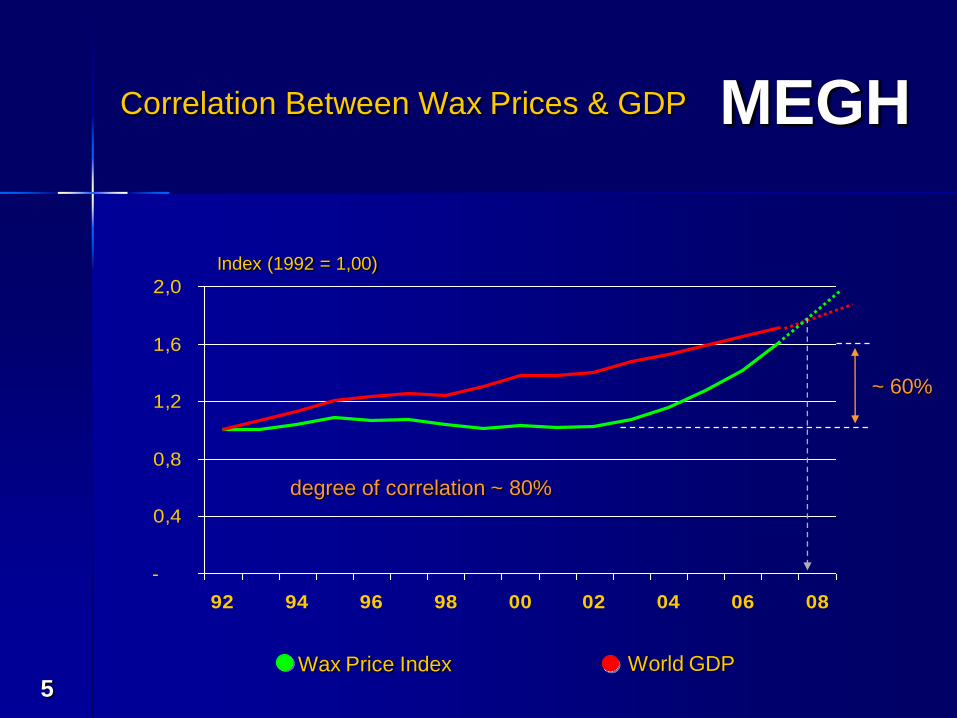

-

0,4

0,8

1,2

1,6

2,0

92 94 96 98 00 02 04 06 08

Wax Price Index World GDP

Index (1992 = 1,00)

Correlation Between Wax Prices & GDP

degree of correlation ~ 80%

~ 60%

MEGH

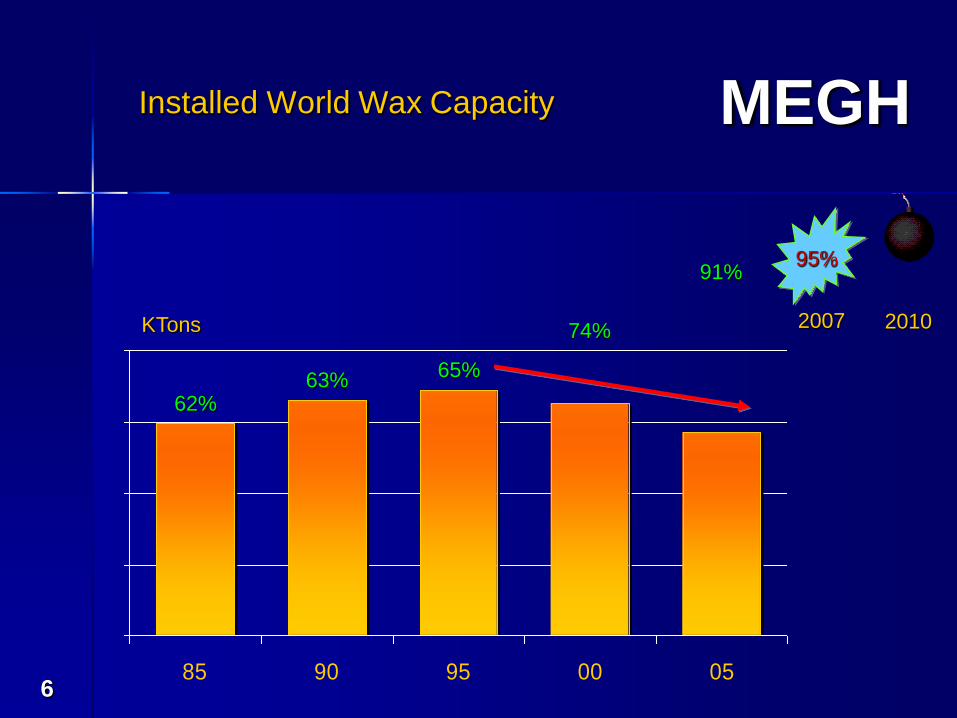

685 90 95 00 05

KTons

Installed World Wax Capacity

62%63%

65%

74%

91%95%

2007 2010

MEGH

7

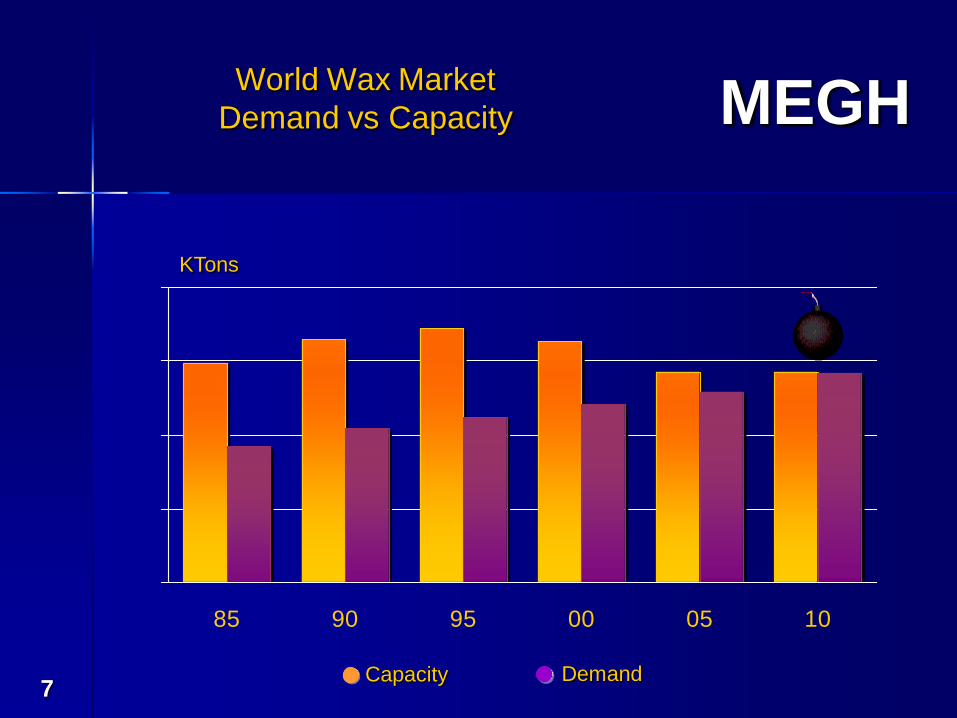

85 90 95 00 05 10

Capacity Demand

KTons

World Wax Market

Demand vs Capacity

MEGH

8

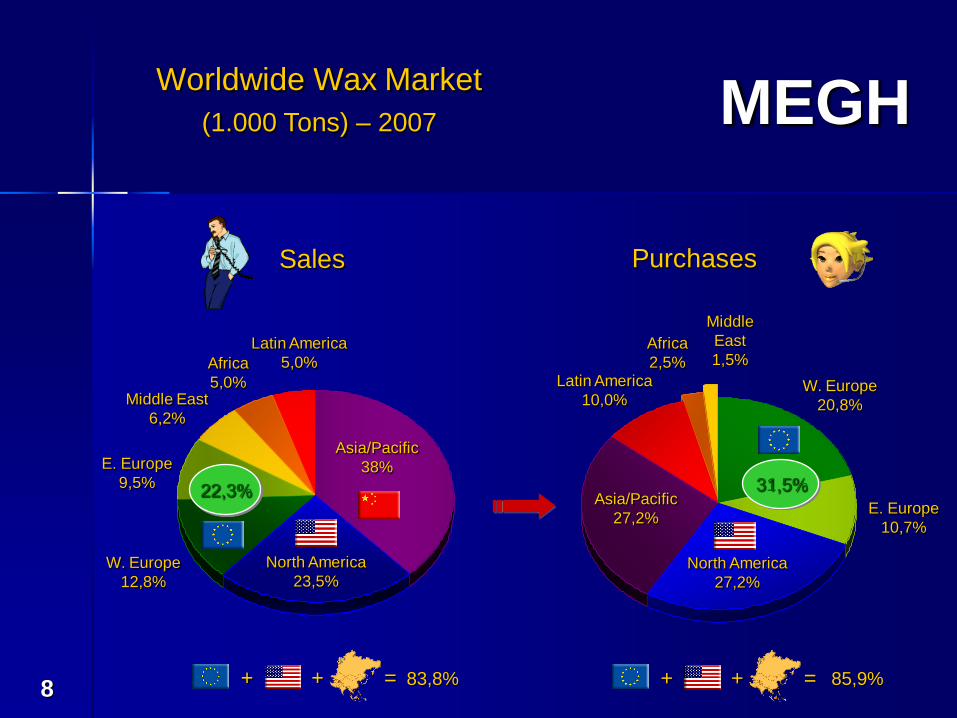

22,3%

North America

23,5%W. Europe

12,8%

E. Europe

9,5%

Middle East

6,2%

Africa

5,0%

Latin America

5,0%

Asia/Pacific

38%

North America

27,2%

Asia/Pacific

27,2%

W. Europe

20,8%

E. Europe

10,7%

Middle

East

1,5%Africa

2,5%Latin America

10,0%

31,5%

Sales

Worldwide Wax Market

(1.000 Tons) – 2007

Purchases

83,8% 85,9%+ + = + + =

MEGH

9

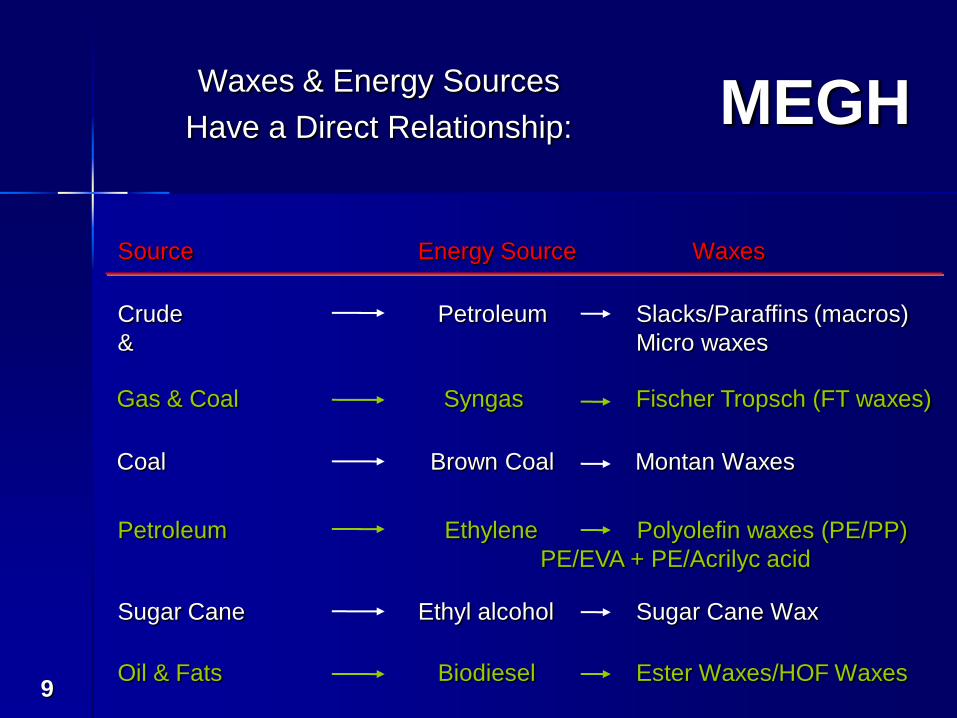

Waxes & Energy Sources

Have a Direct Relationship:

Source Energy Source Waxes

Coal Brown Coal Montan Waxes

Petroleum Ethylene Polyolefin waxes (PE/PP)

PE/EVA + PE/Acrilyc acid

Sugar Cane Ethyl alcohol Sugar Cane Wax

Oil & Fats Biodiesel Ester Waxes/HOF Waxes

Gas & Coal Syngas Fischer Tropsch (FT waxes)

Crude Petroleum Slacks/Paraffins (macros)

& Micro waxes

MEGH

10

Theorem 01

Once we know the different energy sector trends, we can begin to

understand the world wax trends.

MEGH

11

Paraffin Waxes

MEGH

12

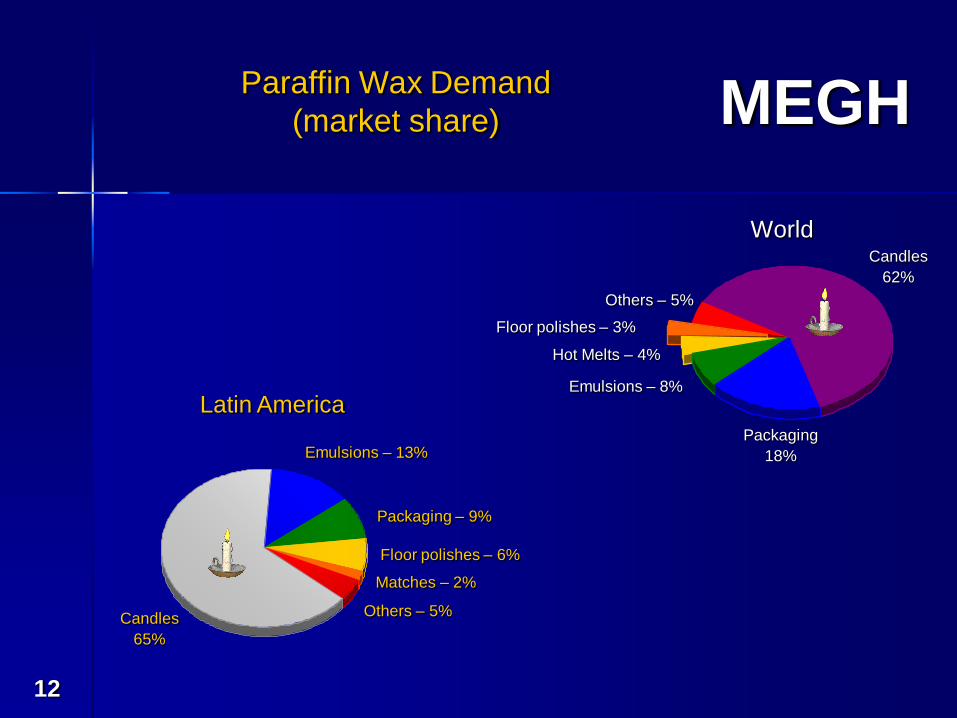

Candles

62%

Packaging

18%

Emulsions – 8%

Hot Melts – 4%

Floor polishes – 3%

Others – 5%

Paraffin Wax Demand

(market share)

World

Latin America

Candles

65%

Emulsions – 13%

Packaging – 9%

Floor polishes – 6%

Others – 5%

Matches – 2%

MEGH

13

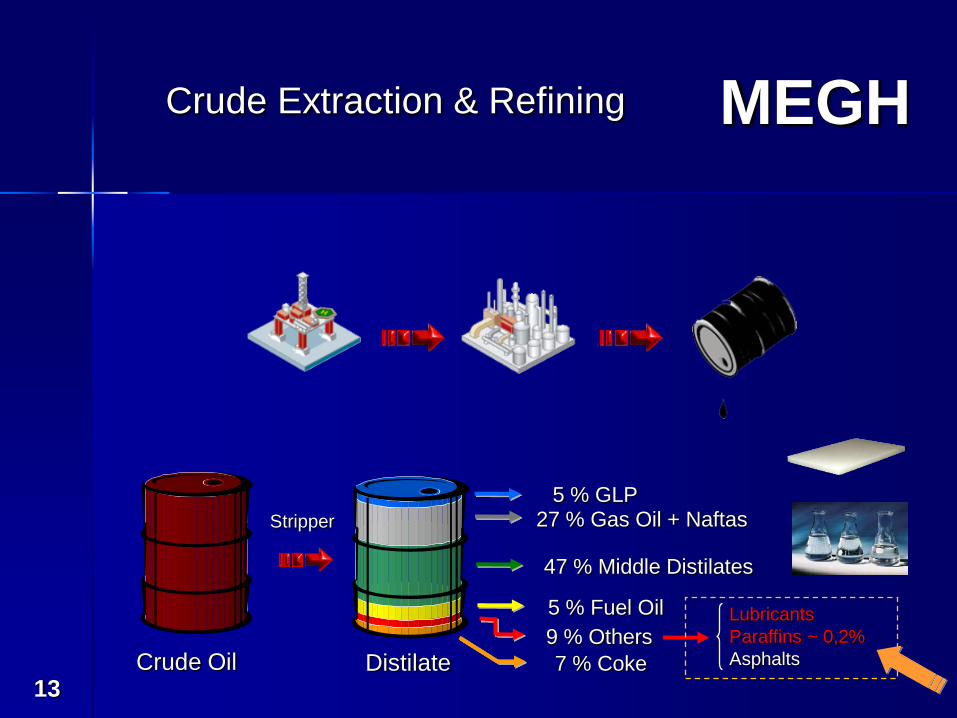

Crude Extraction & Refining

Crude Oil

5 % GLP

Distilate

27 % Gas Oil + Naftas

47 % Middle Distilates

5 % Fuel Oil

9 % Others

7 % Coke

Stripper

Lubricants

Paraffins ~ 0,2%

Asphalts

MEGH

14

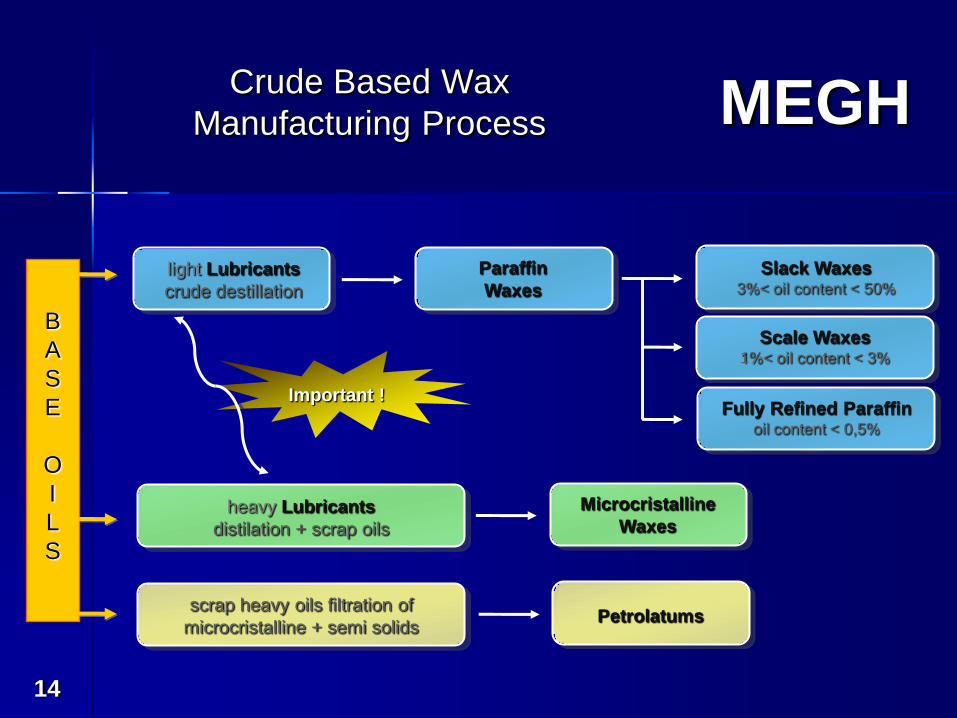

Crude Based Wax

Manufacturing Process

light Lubricants

crude destillation

Paraffin

Waxes

Slack Waxes3%< oil content < 50%

Scale Waxes1%< oil content < 3%

Fully Refined Paraffinoil content < 0,5%

heavy Lubricants

distilation + scrap oils

Microcristalline

Waxes

scrap heavy oils filtration of

microcristalline + semi solidsPetrolatums

Important !

B

A

S

E

O

I

L

S

MEGH

15

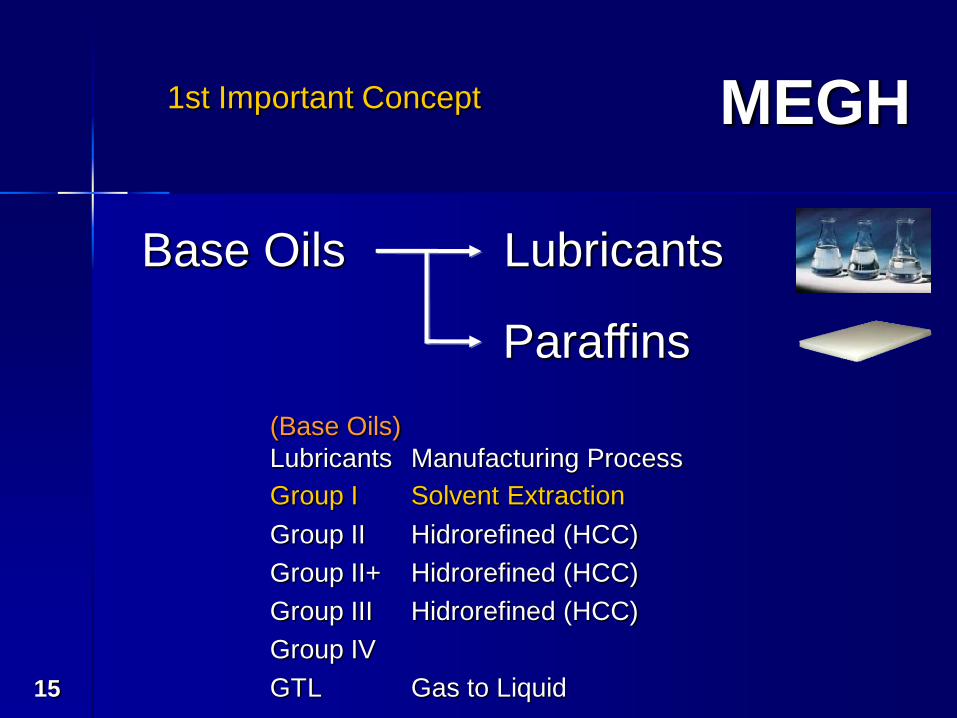

Base Oils Lubricants

Paraffins

1st Important Concept

(Base Oils)

Lubricants Manufacturing Process

Group I Solvent Extraction

Group II Hidrorefined (HCC)

Group II+ Hidrorefined (HCC)

Group III Hidrorefined (HCC)

Group IV

GTL Gas to Liquid

MEGH

16

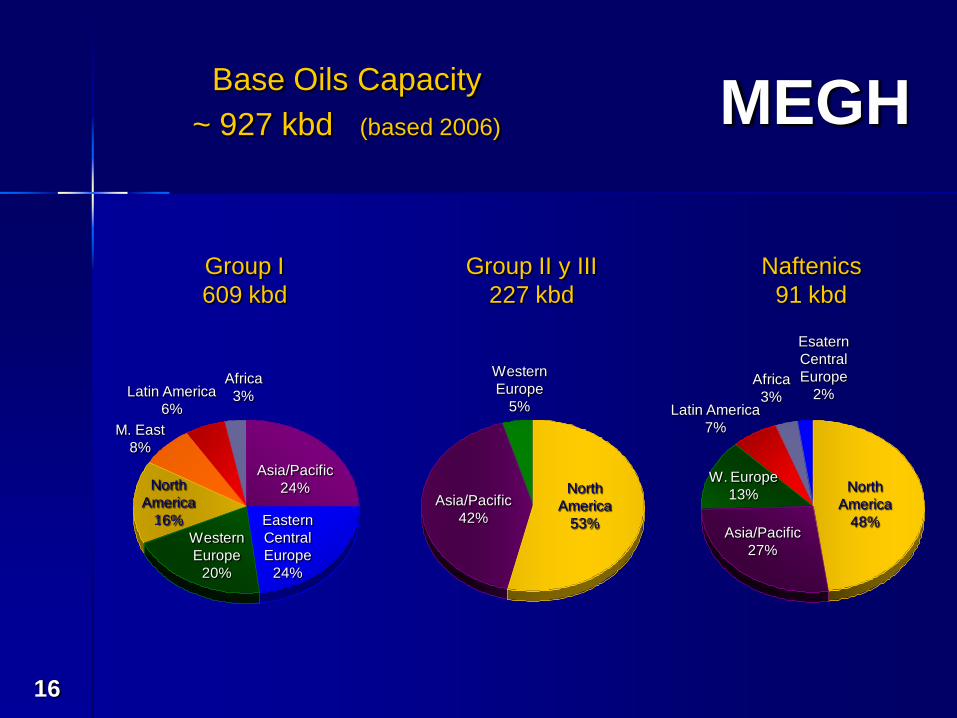

Base Oils Capacity

~ 927 kbd (based 2006)

Asia/Pacific

24%

Eastern

Central

Europe

24%

Western

Europe

20%

North

America

16%

M. East

8%

Latin America

6%

Africa

3%

Group I

609 kbd

Asia/Pacific

42%

North

America

53%

Western

Europe

5%

Group II y III

227 kbd

North

America

48%Asia/Pacific

27%

W. Europe

13%

Latin America

7%

Africa

3%

Esatern

Central

Europe

2%

Naftenics

91 kbd

MEGH

17

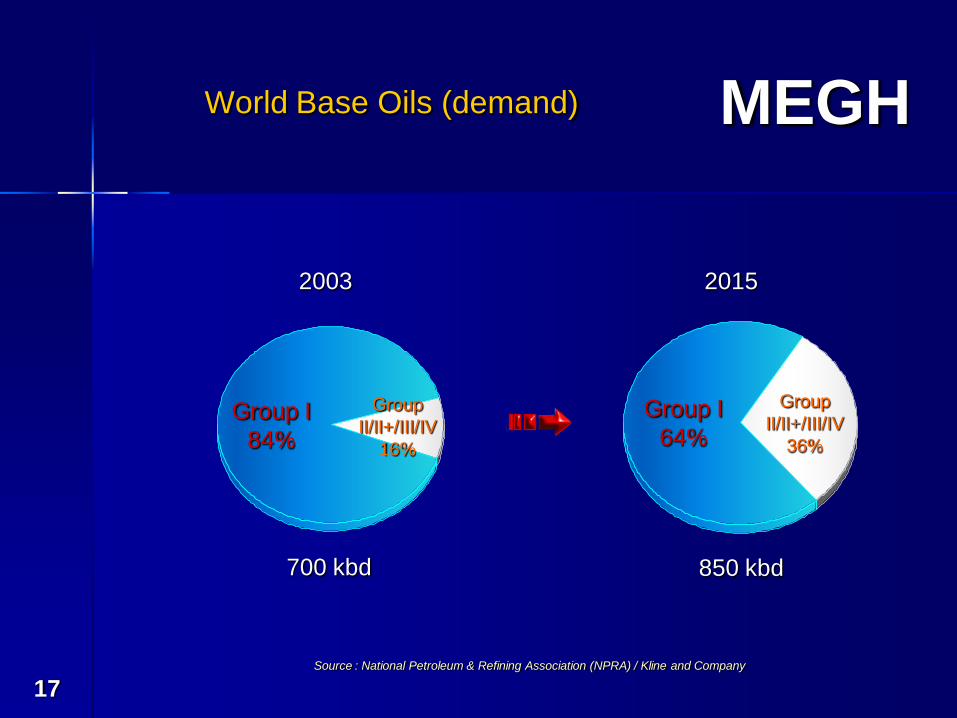

World Base Oils (demand)

2003 2015

Group I

84%

Group I

64%

Group

II/II+/III/IV

16%

Group

II/II+/III/IV

36%

700 kbd 850 kbd

Source : National Petroleum & Refining Association (NPRA) / Kline and Company

MEGH

18

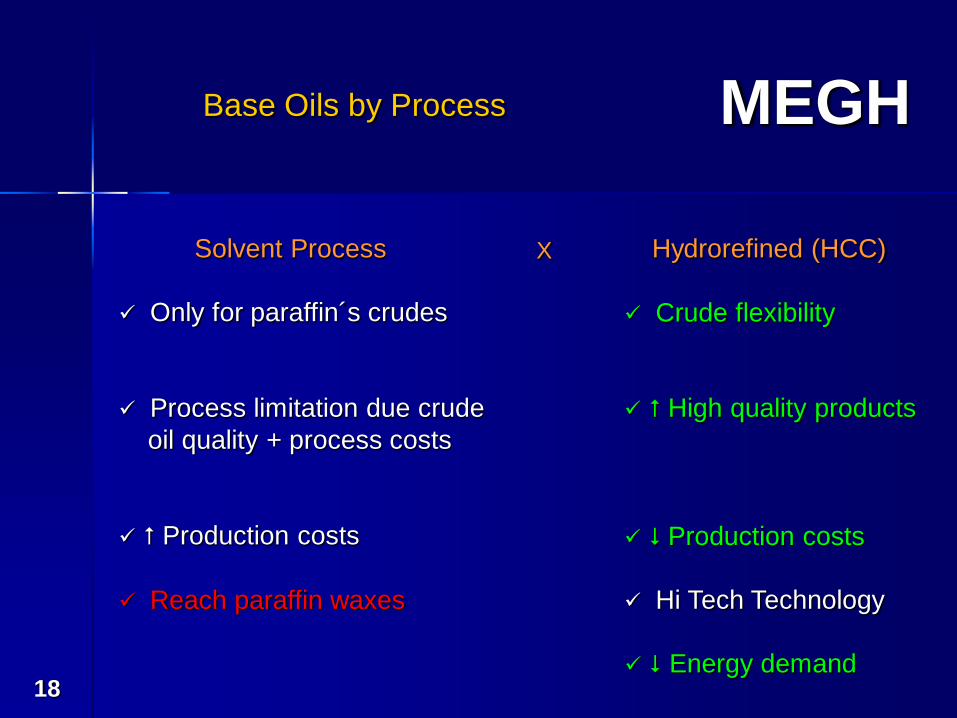

Base Oils by Process

Hydrorefined (HCC)Solvent Process X

Only for paraffin´s crudes

Process limitation due crude

oil quality + process costs

Production costs

Reach paraffin waxes

Crude flexibility

High quality products

Production costs

Hi Tech Technology

Energy demand

MEGH

19

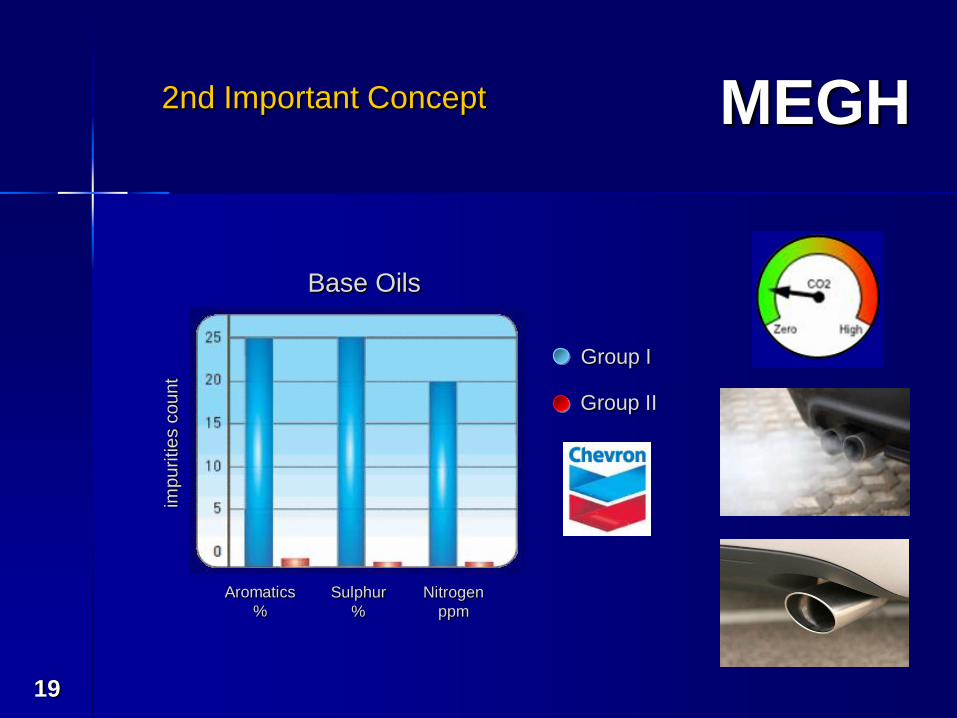

2nd Important Concept

impurities c

ount

Group I

Group II

Aromatics

%

Sulphur

%

Nitrogen

ppm

Base Oils

MEGH

20

MEGH

21

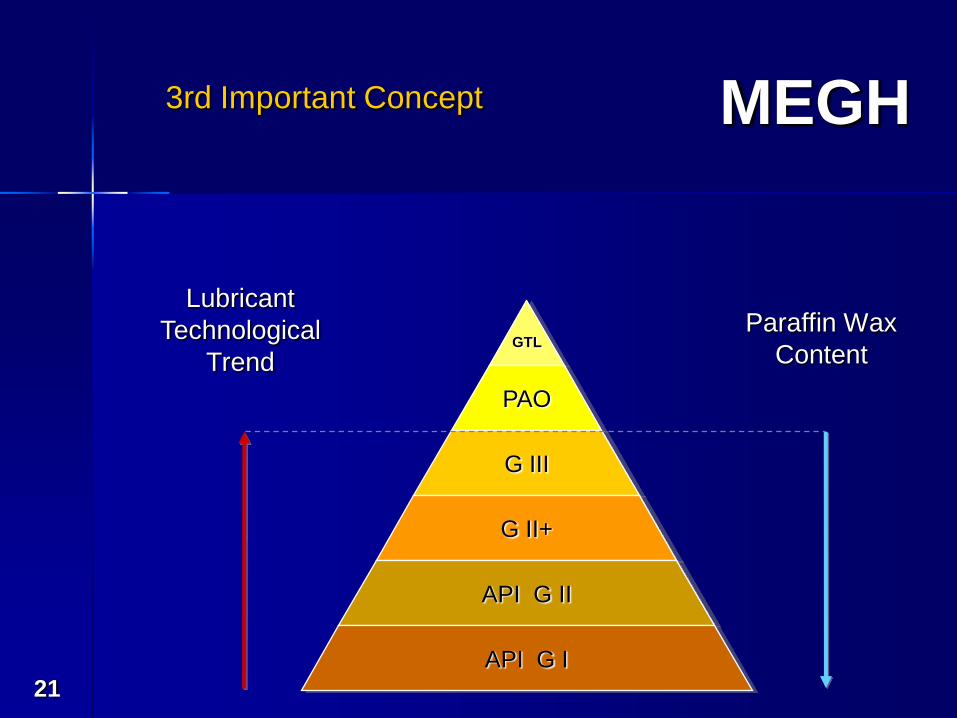

GTL

PAO

G III

G II+

API G II

API G I

3rd Important Concept

Lubricant

Technological

Trend

Paraffin Wax

Content

MEGH

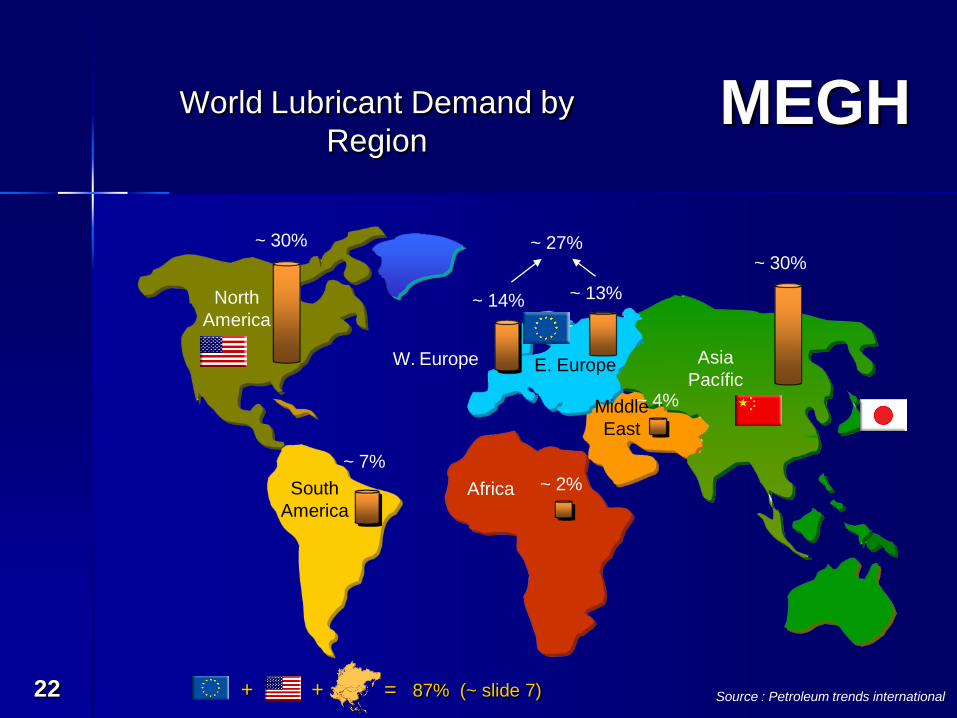

22

World Lubricant Demand by

Region

Source : Petroleum trends international

North

America

South

America

Asia

Pacífic

Africa

Middle

East

W. Europe E. Europe

~ 30%

~ 30%

~ 14% ~ 13%

~ 27%

~ 7%

~ 4%

~ 2%

87% (~ slide 7)+ + =

MEGH

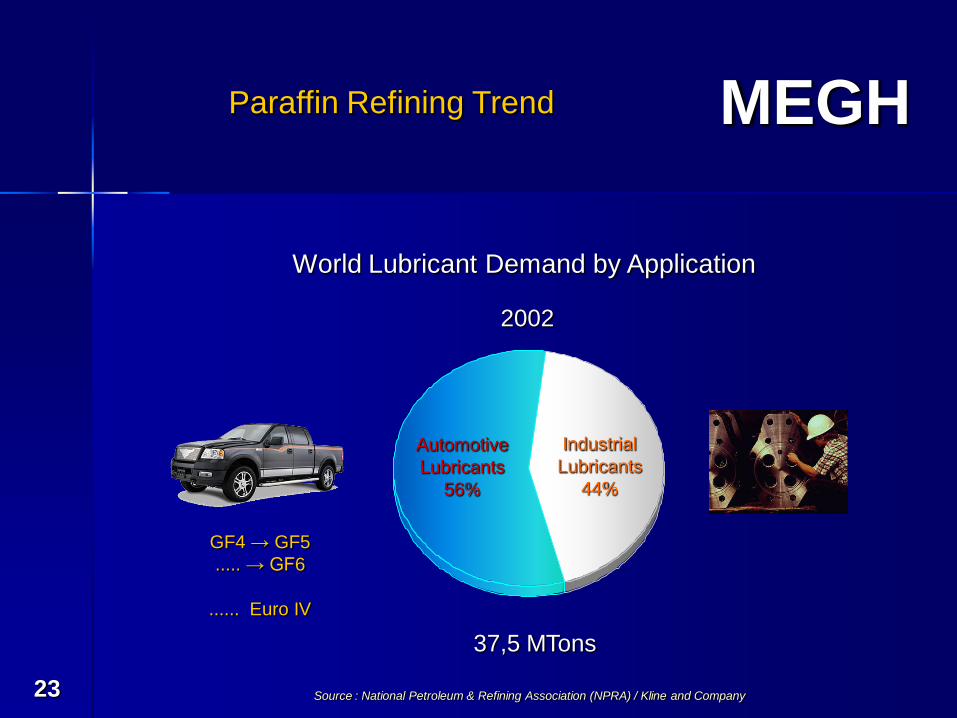

23

World Lubricant Demand by Application

2002

Automotive

Lubricants

56%

Industrial

Lubricants

44%

37,5 MTons

Paraffin Refining Trend

GF4 → GF5

..... → GF6

...... Euro IV

Source : National Petroleum & Refining Association (NPRA) / Kline and Company

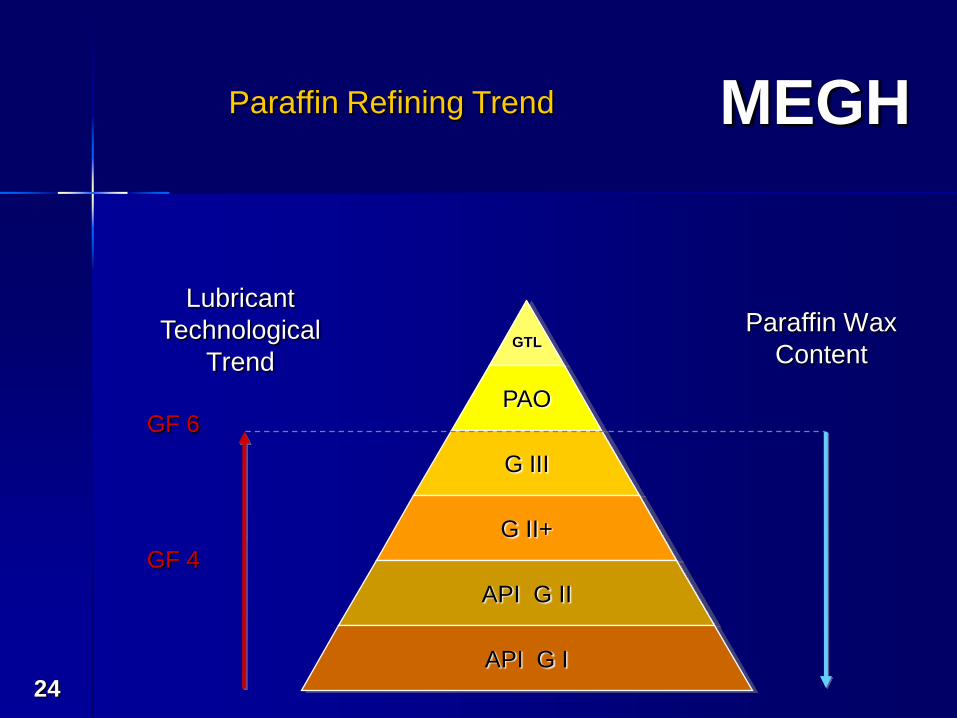

MEGH

24

GTL

PAO

G III

G II+

API G II

API G I

GF 4

GF 6

Paraffin Refining Trend

Lubricant

Technological

Trend

Paraffin Wax

Content

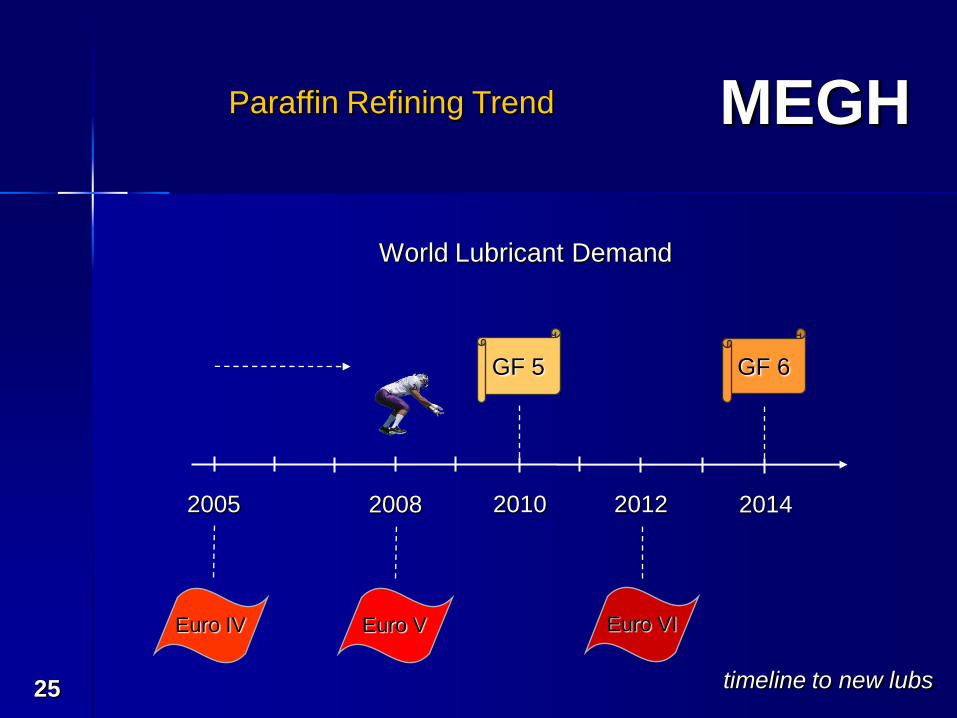

MEGH

25

World Lubricant Demand

2005 2008 2010 2012 2014

GF 6

Euro IV Euro V Euro VI

GF 5

timeline to new lubs

Paraffin Refining Trend

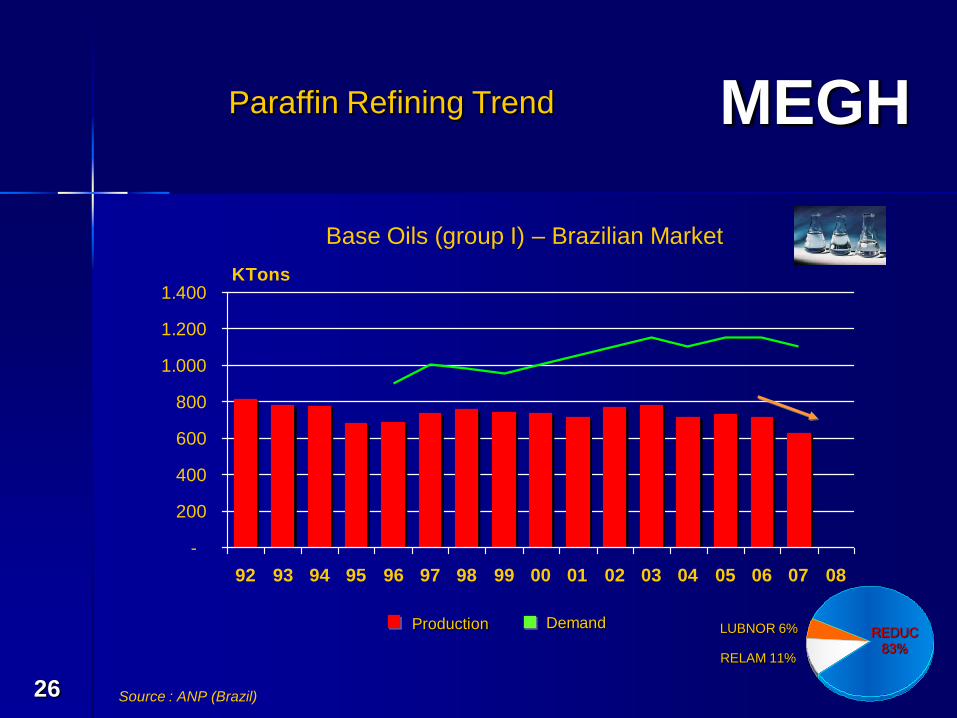

MEGH

26

-

200

400

600

800

1.000

1.200

1.400

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

KTons

Production Demand

Base Oils (group I) – Brazilian Market

REDUC

83%RELAM 11%

LUBNOR 6%

Source : ANP (Brazil)

Paraffin Refining Trend

MEGH

27

Equation Analysis:

+ +

Paraffin Refining Trend

MEGH

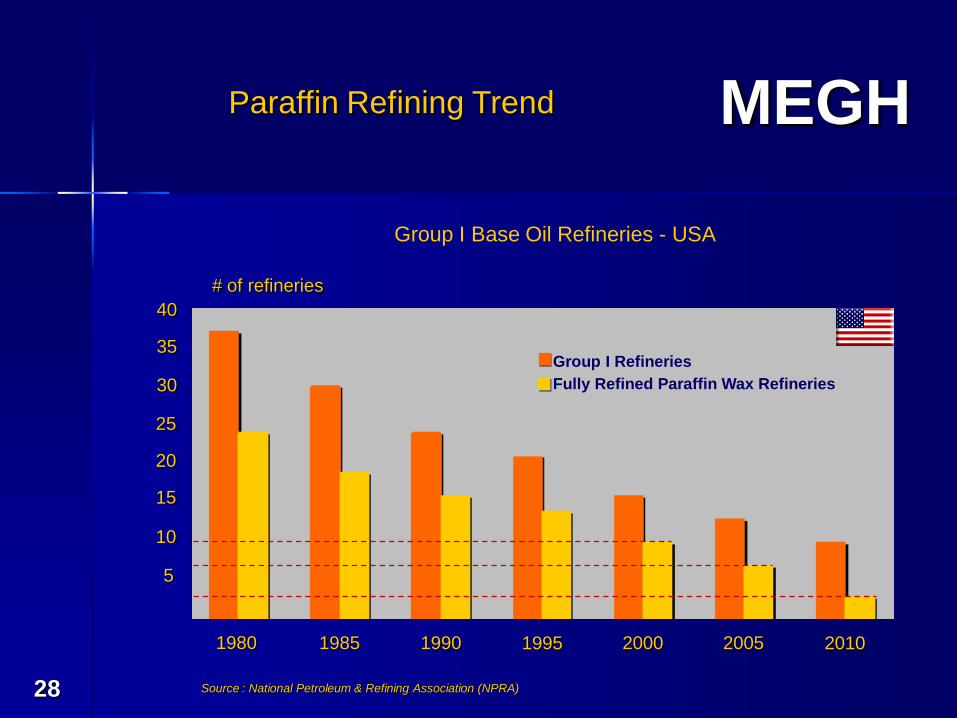

28

Group I Refineries

Fully Refined Paraffin Wax Refineries

# of refineries

1980 1985 1990 1995 2000 2005 2010

10

5

15

20

25

30

35

40

Group I Base Oil Refineries - USA

Source : National Petroleum & Refining Association (NPRA)

Paraffin Refining Trend

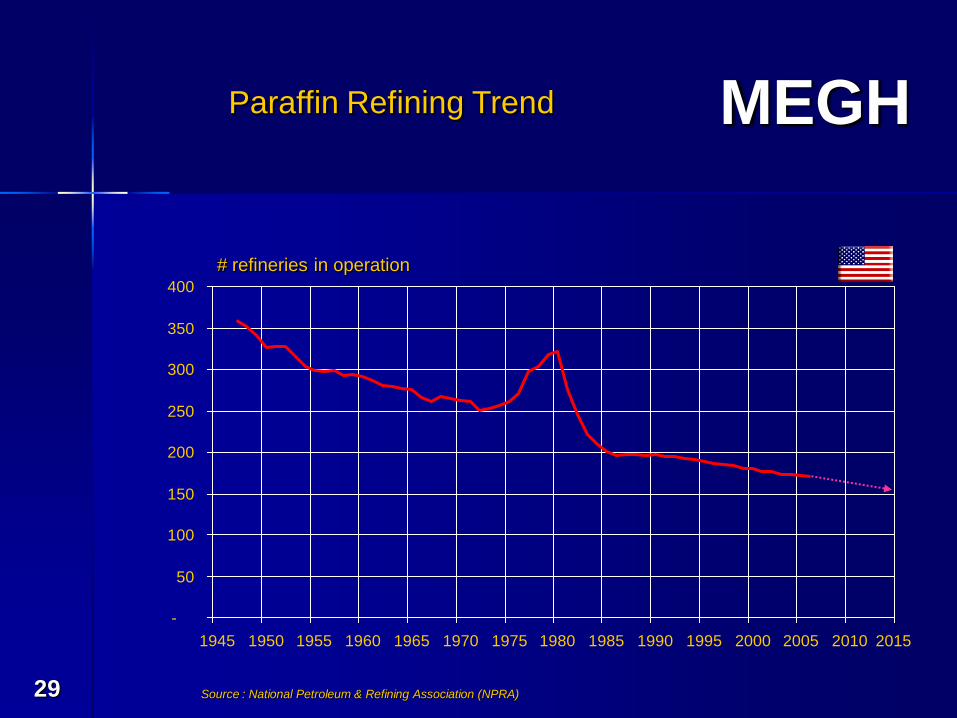

MEGH

29

-

50

100

150

200

250

300

350

400

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

# refineries in operation

2015

Source : National Petroleum & Refining Association (NPRA)

Paraffin Refining Trend

MEGH

30

0

1.000

2.000

3.000

4.000

5.000

6.000

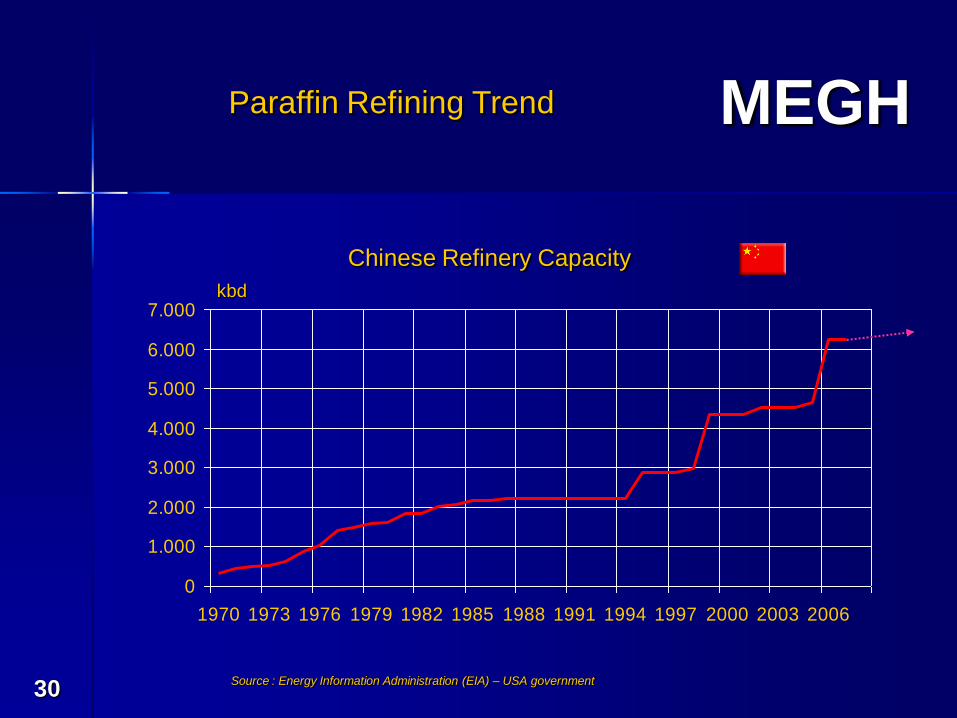

7.000

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

Chinese Refinery Capacity

kbd

Source : Energy Information Administration (EIA) – USA government

Paraffin Refining Trend

MEGH

31

0,0%

0,1%

0,2%

0,3%

0,4%

0,5%

0,6%

0,7%

0,8%

0,9%

1,0%

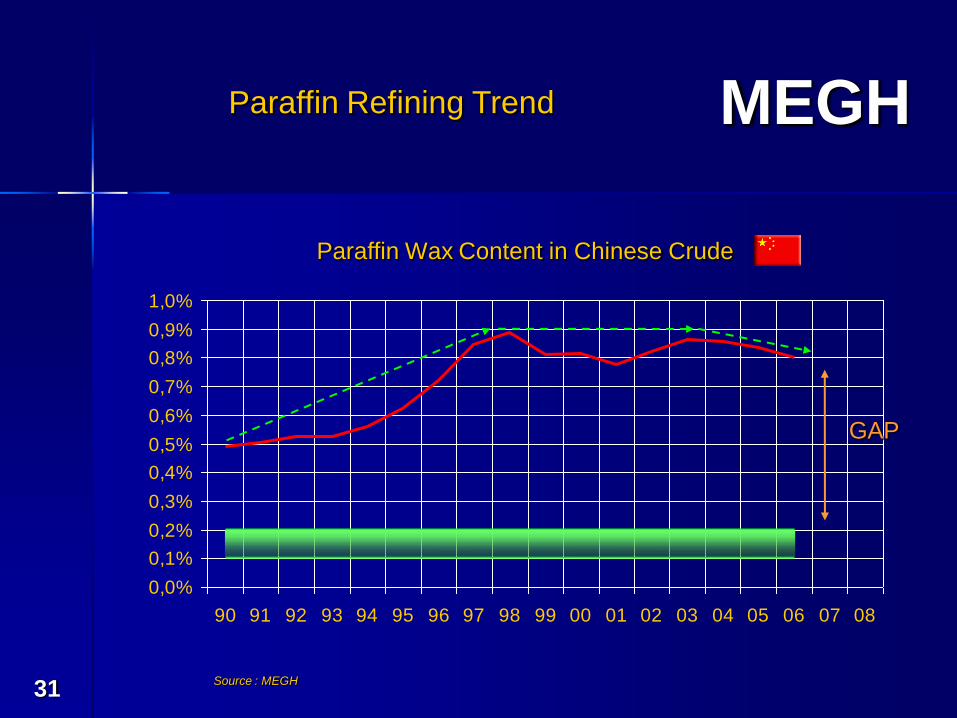

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Source : MEGH

Paraffin Wax Content in Chinese Crude

GAP

Paraffin Refining Trend

MEGH

32

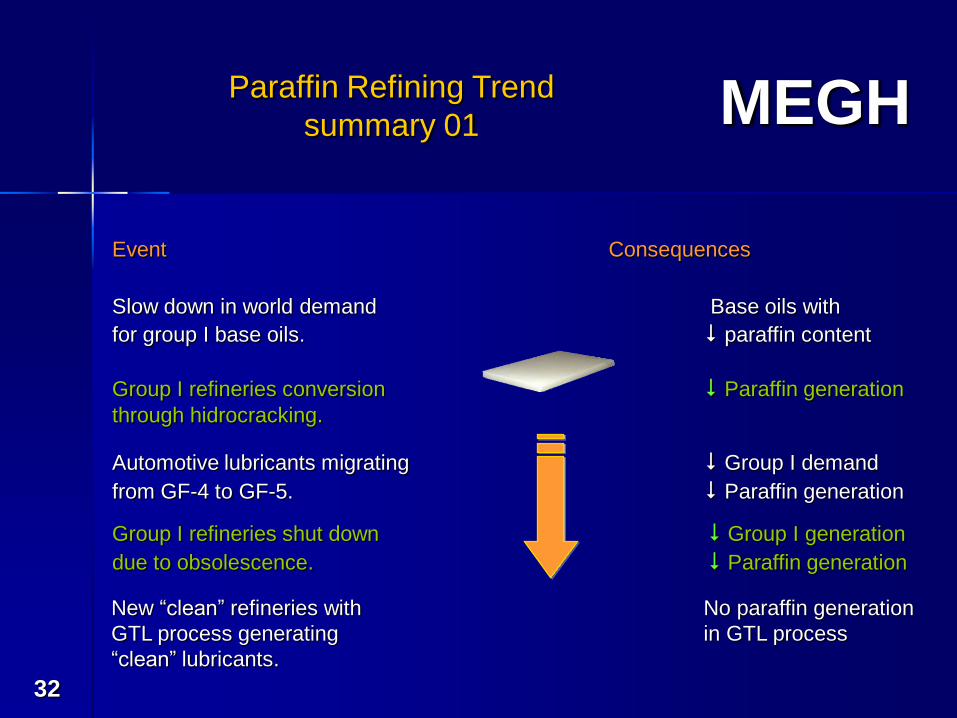

Slow down in world demand Base oils with

for group I base oils. paraffin content

Event Consequences

Group I refineries conversion Paraffin generation

through hidrocracking.

Automotive lubricants migrating Group I demand

from GF-4 to GF-5. Paraffin generation

Group I refineries shut down Group I generation

due to obsolescence. Paraffin generation

New “clean” refineries with No paraffin generation

GTL process generating in GTL process

“clean” lubricants.

Paraffin Refining Trend

summary 01

MEGH

33

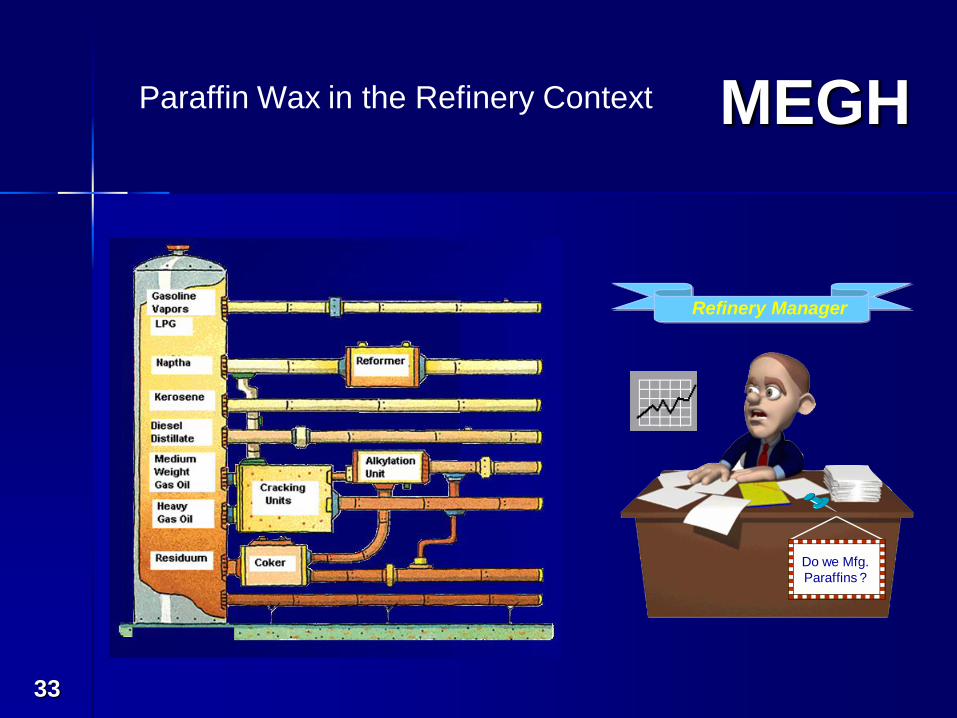

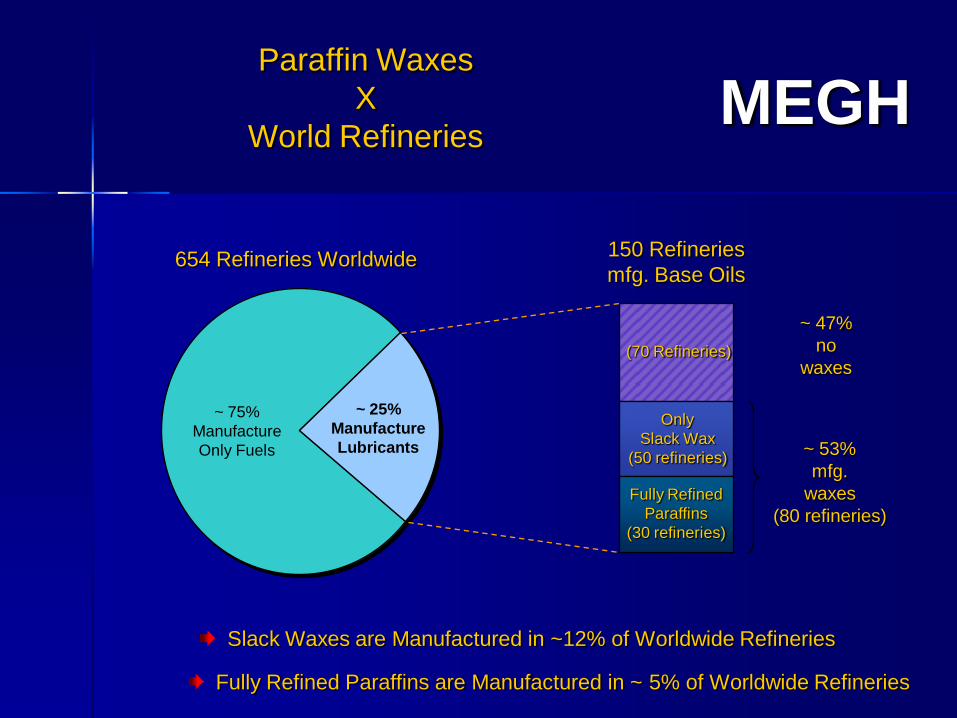

Paraffin Wax in the Refinery Context

Refinery Manager

Do we Mfg.

Paraffins ?

MEGHParaffin Waxes

X

World Refineries

~ 75%

Manufacture

Only Fuels

~ 25%

Manufacture

Lubricants

150 Refineries

mfg. Base Oils

~ 47%

no

waxes

Only

Slack Wax

(50 refineries)~ 53%

mfg.

waxes

(80 refineries)

654 Refineries Worldwide

Slack Waxes are Manufactured in ~12% of Worldwide Refineries

Fully Refined Paraffins are Manufactured in ~ 5% of Worldwide Refineries

Fully Refined

Paraffins

(30 refineries)

(70 Refineries)

MEGH

35

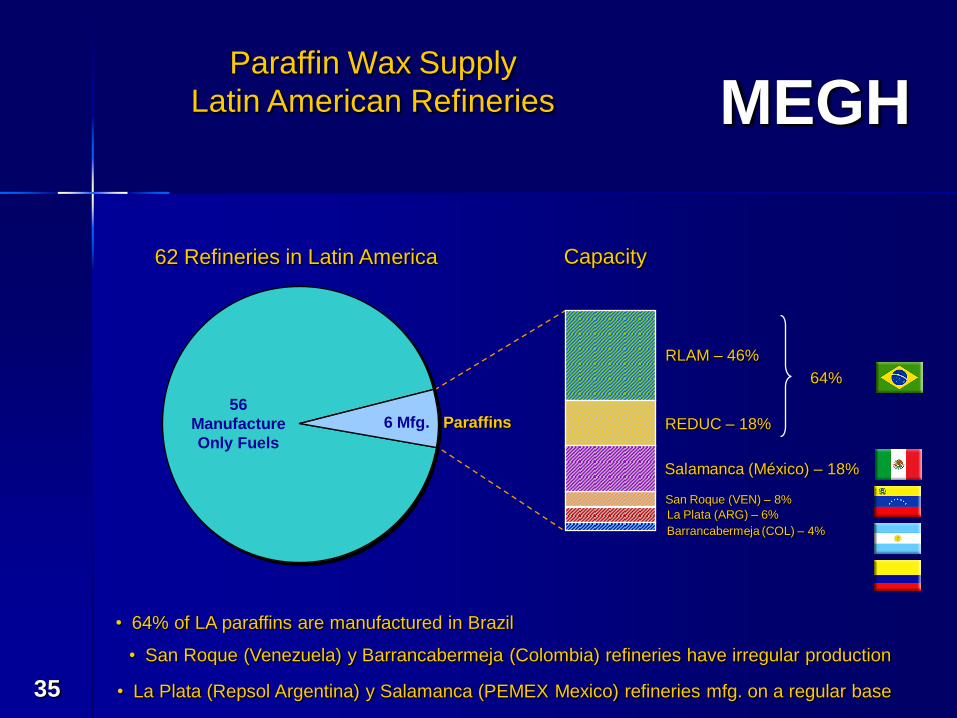

62 Refineries in Latin America

Paraffin Wax Supply

Latin American Refineries

6 Mfg. Paraffins

RLAM – 46%

REDUC – 18%

San Roque (VEN) – 8%

La Plata (ARG) – 6%

Barrancabermeja (COL) – 4%

Capacity

64%

56

Manufacture

Only Fuels

• 64% of LA paraffins are manufactured in Brazil

• San Roque (Venezuela) y Barrancabermeja (Colombia) refineries have irregular production

• La Plata (Repsol Argentina) y Salamanca (PEMEX Mexico) refineries mfg. on a regular base

Salamanca (México) – 18%

MEGH

36

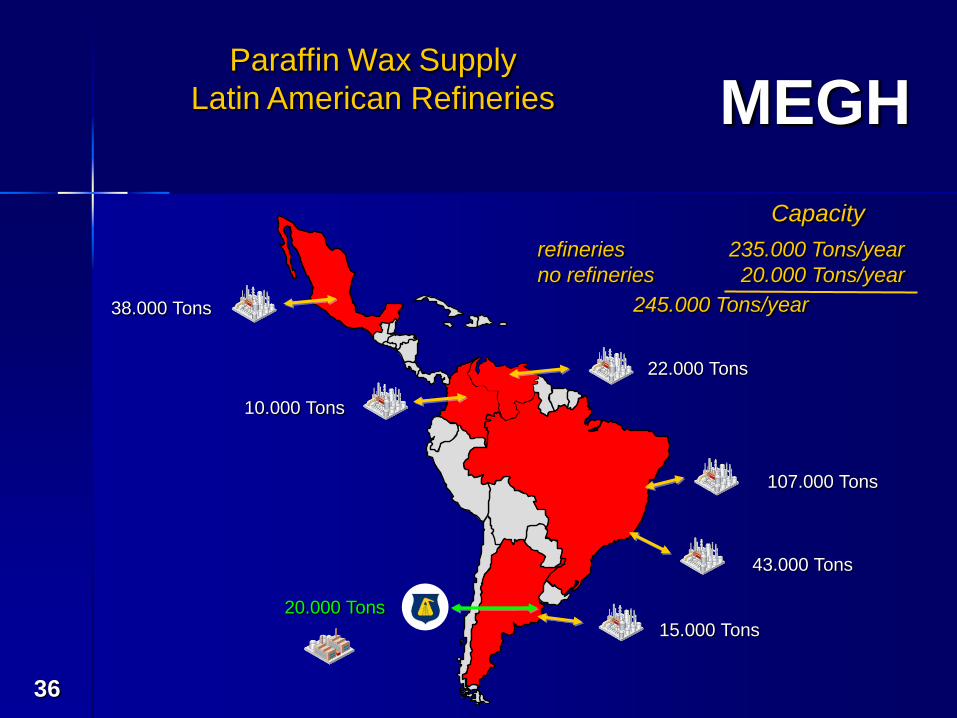

107.000 Tons

43.000 Tons

15.000 Tons

10.000 Tons

38.000 Tons

20.000 Tons

refineries 235.000 Tons/year

no refineries 20.000 Tons/year

245.000 Tons/year

Capacity

22.000 Tons

Paraffin Wax Supply

Latin American Refineries

MEGH

37

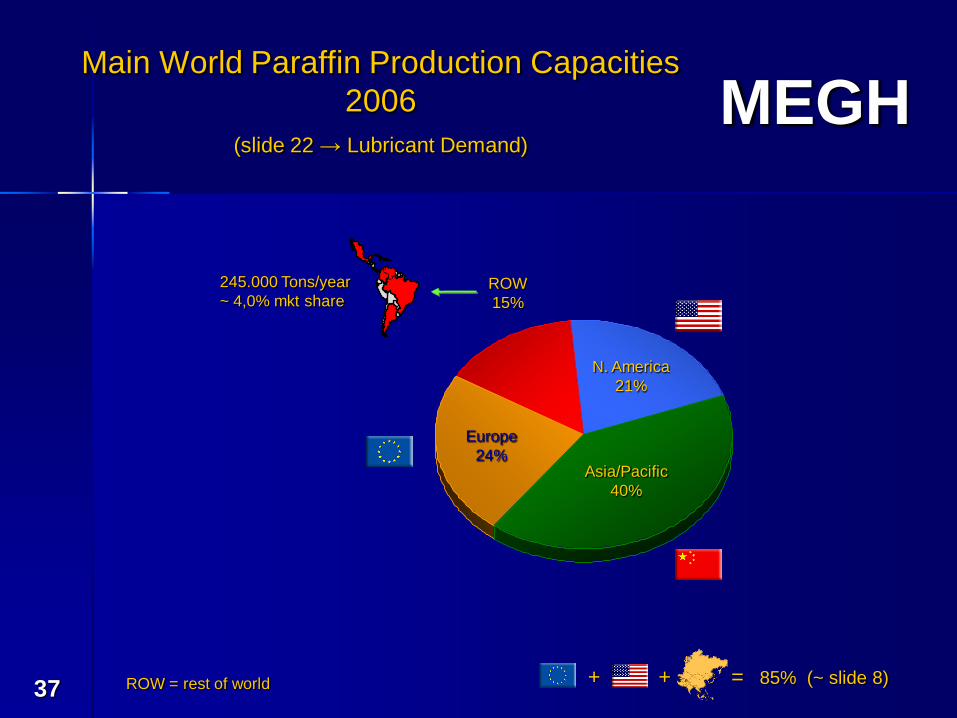

Main World Paraffin Production Capacities

2006

(slide 22 → Lubricant Demand)

245.000 Tons/year

~ 4,0% mkt share

ROW = rest of world

Asia/Pacific

40%

N. America

21%

Europe

24%

ROW

15%

85% (~ slide 8)+ + =

MEGH

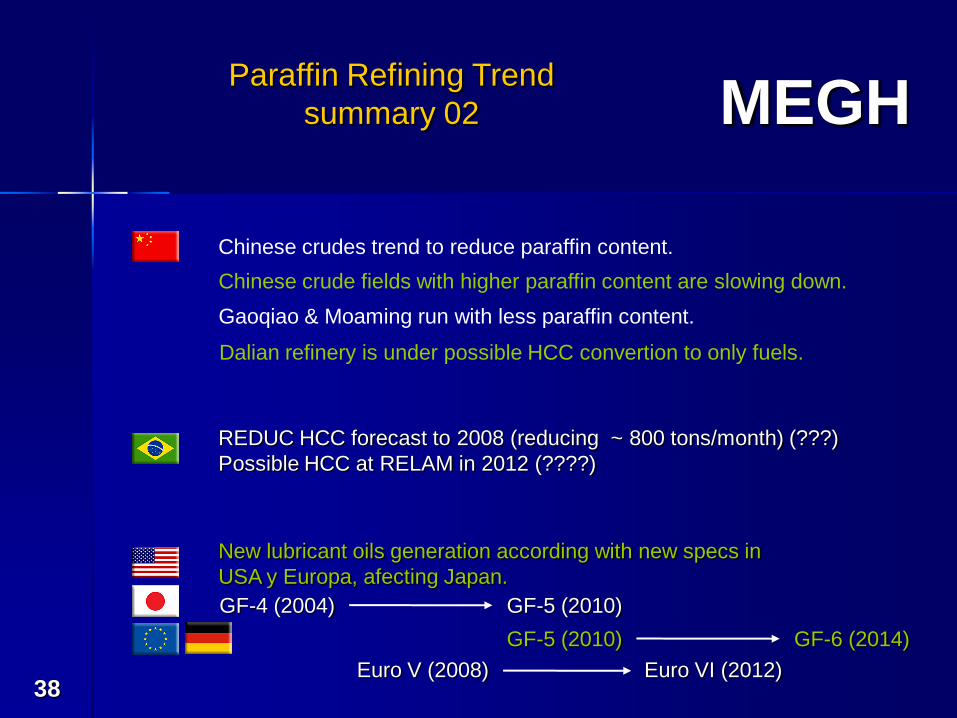

38

Chinese crudes trend to reduce paraffin content.

Chinese crude fields with higher paraffin content are slowing down.

Gaoqiao & Moaming run with less paraffin content.

Dalian refinery is under possible HCC convertion to only fuels.

REDUC HCC forecast to 2008 (reducing ~ 800 tons/month) (???)

Possible HCC at RELAM in 2012 (????)

New lubricant oils generation according with new specs in

USA y Europa, afecting Japan.

GF-4 (2004) GF-5 (2010)

Paraffin Refining Trend

summary 02

GF-5 (2010) GF-6 (2014)

Euro V (2008) Euro VI (2012)

MEGH

39 IV Enafave – João Pessoa (PB), november 2006

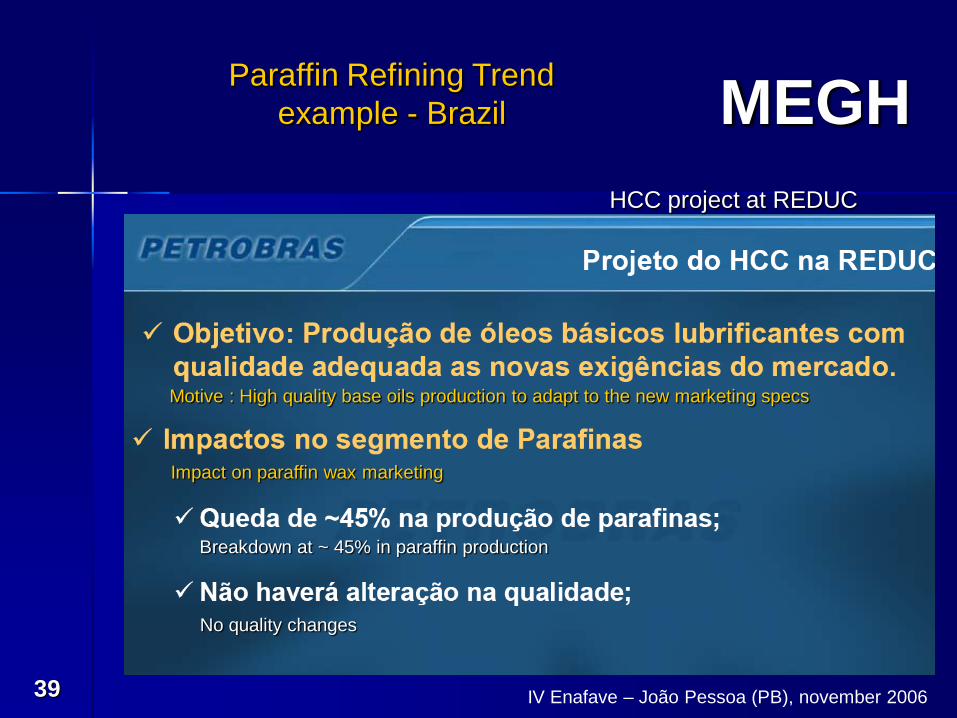

Paraffin Refining Trend

example - Brazil

HCC project at REDUC

Motive : High quality base oils production to adapt to the new marketing specs

Impact on paraffin wax marketing

Breakdown at ~ 45% in paraffin production

No quality changes

MEGH

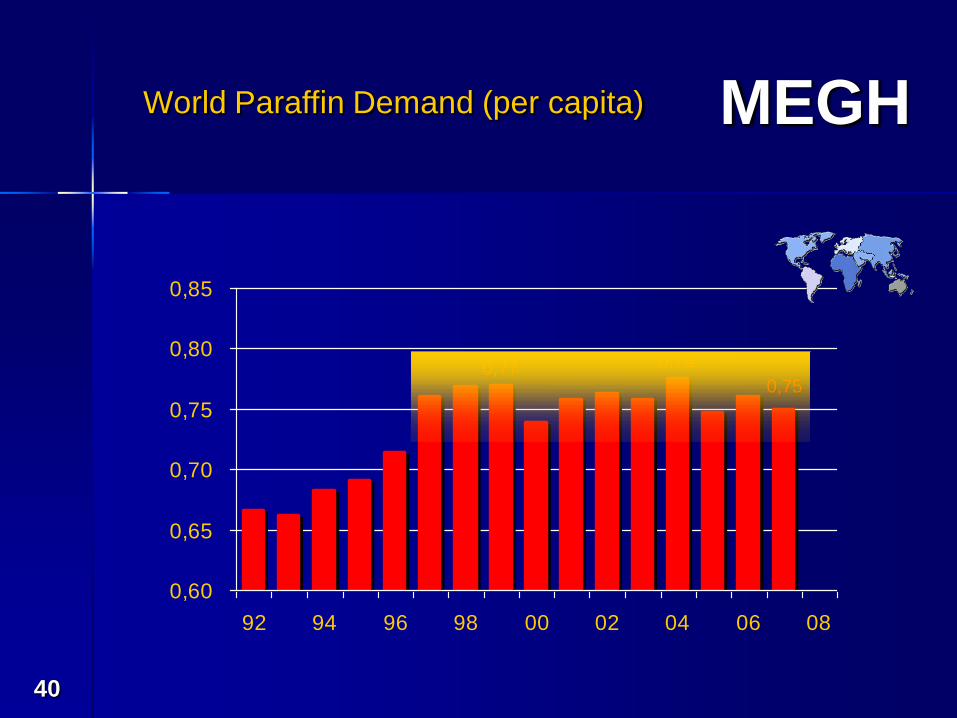

40

0,60

0,65

0,70

0,75

0,80

0,85

92 94 96 98 00 02 04 06 08

World Paraffin Demand (per capita)

0,75

0,780,77

MEGH

41

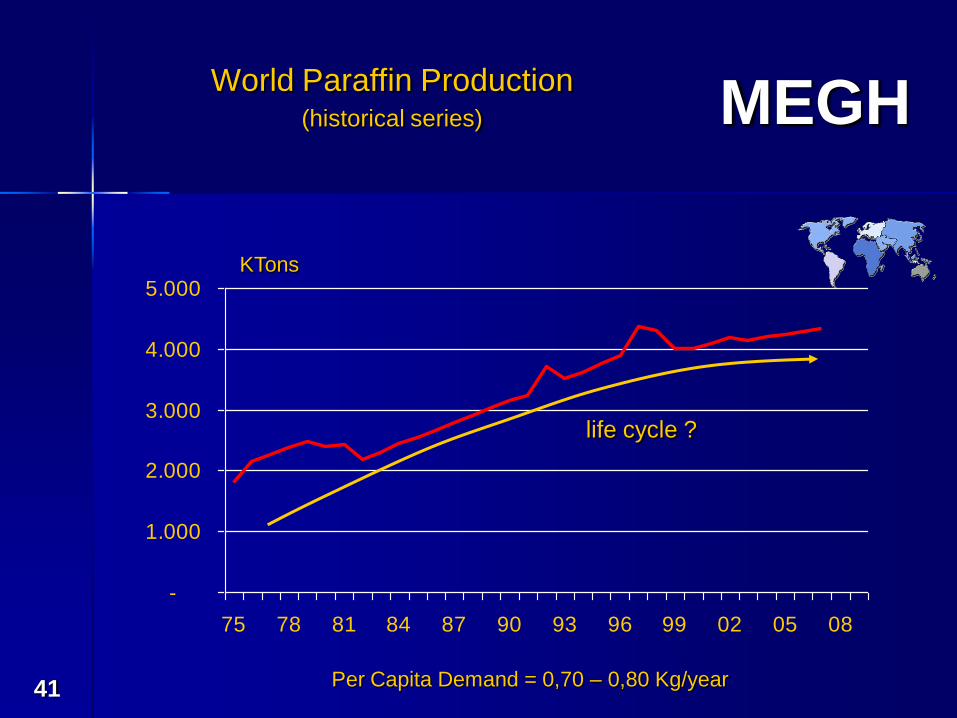

-

1.000

2.000

3.000

4.000

5.000

75 78 81 84 87 90 93 96 99 02 05 08

KTons

World Paraffin Production(historical series)

life cycle ?

Per Capita Demand = 0,70 – 0,80 Kg/year

MEGH

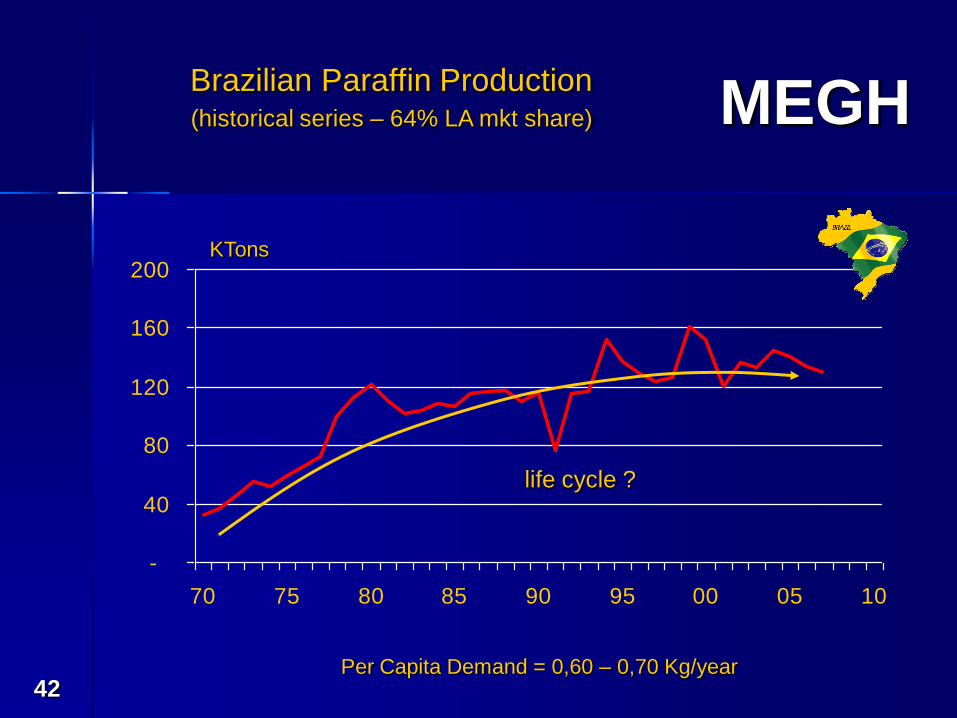

42

-

40

80

120

160

200

70 75 80 85 90 95 00 05 10

KTons

life cycle ?

Per Capita Demand = 0,60 – 0,70 Kg/year

Brazilian Paraffin Production(historical series – 64% LA mkt share)

MEGH

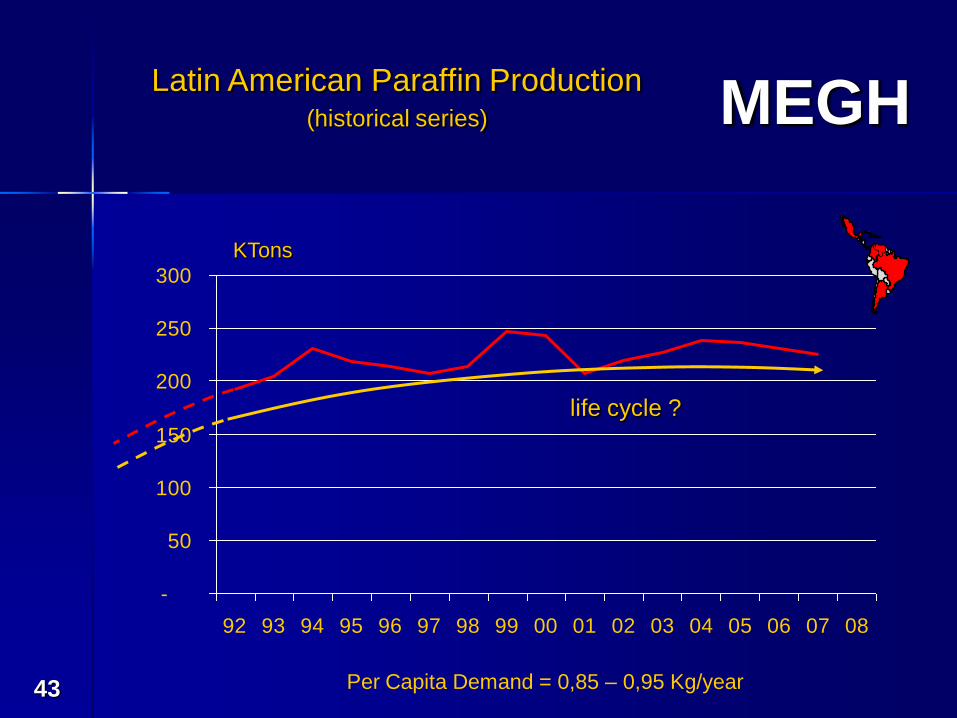

43

-

50

100

150

200

250

300

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

KTons

Per Capita Demand = 0,85 – 0,95 Kg/year

Latin American Paraffin Production(historical series)

life cycle ?

MEGH

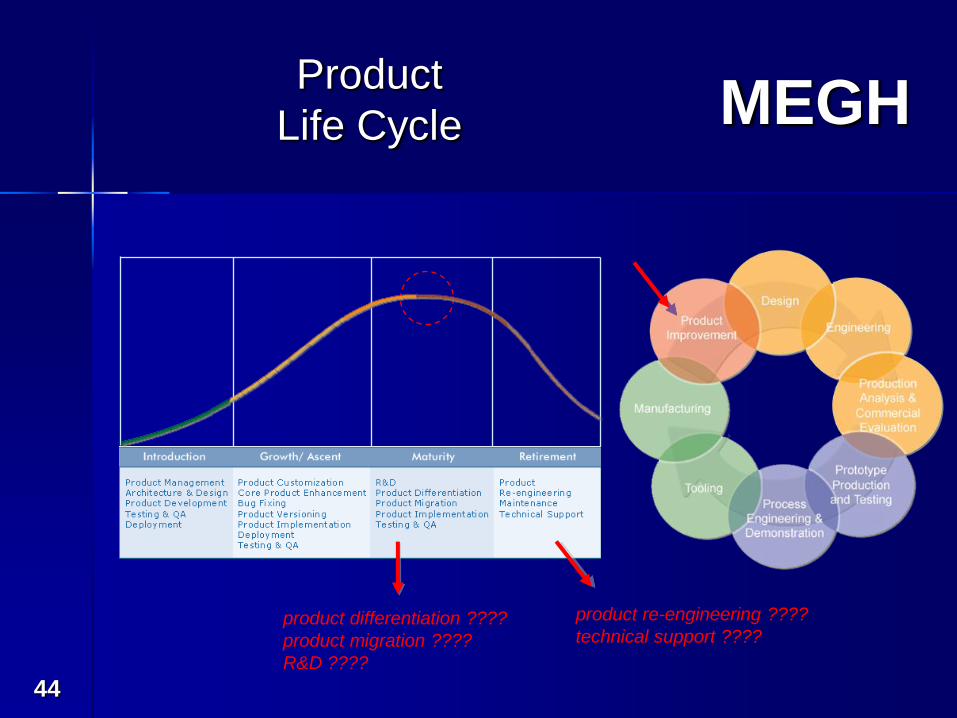

44

Product

Life Cycle

product differentiation ????

product migration ????

R&D ????

product re-engineering ????

technical support ????

MEGH

45

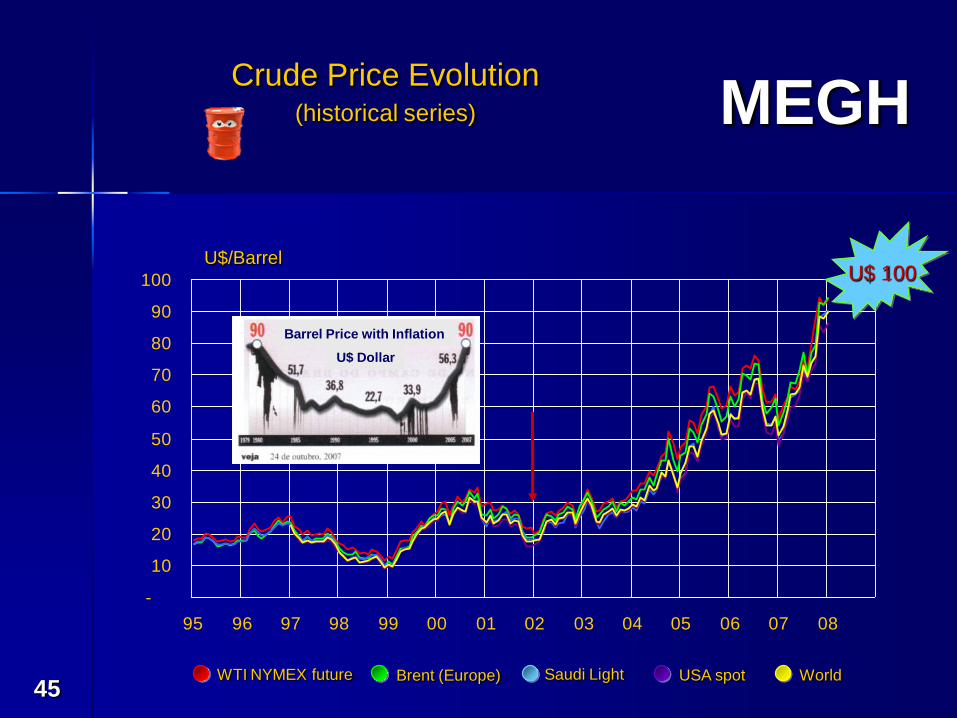

-

10

20

30

40

50

60

70

80

90

100

95 96 97 98 99 00 01 02 03 04 05 06 07 08

U$/Barrel

Crude Price Evolution(historical series)

U$ 100

Brent (Europe)WTI NYMEX future USA spotSaudi Light World

Barrel Price with Inflation

U$ Dollar

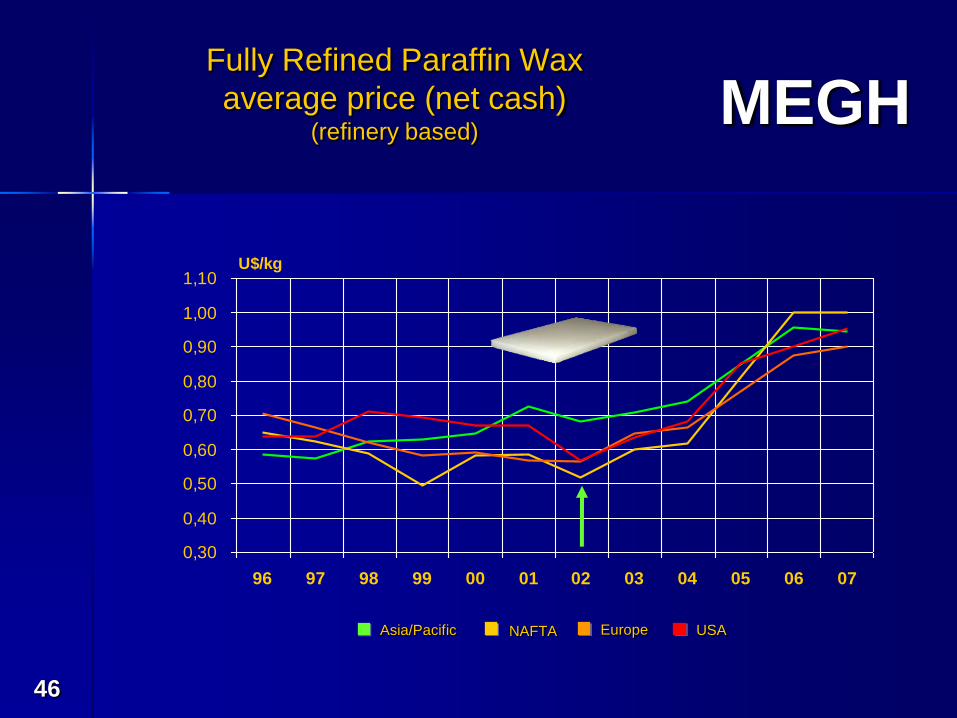

MEGH

46

0,30

0,40

0,50

0,60

0,70

0,80

0,90

1,00

1,10

96 97 98 99 00 01 02 03 04 05 06 07

U$/kg

Asia/Pacific NAFTA USAEurope

Fully Refined Paraffin Wax

average price (net cash)(refinery based)

MEGH

47

• The future of paraffin waxes will depend of which technology will

be used to manufacture lubricants (GTL/Fischer Tropsch).

• Cracking of heavy fractions, generating lighter fuels (Hidrocracking).

• Petroleum waxes are passing through their maturity phase going

to a decline phase in their life cycle.

• Paraffin demand has shown signs of slowing down in the last years.

• Substitute waxes are already a reality (ex: GTL waxes / HOFs).

Paraffin Refining Trend

Conclusions

MEGH

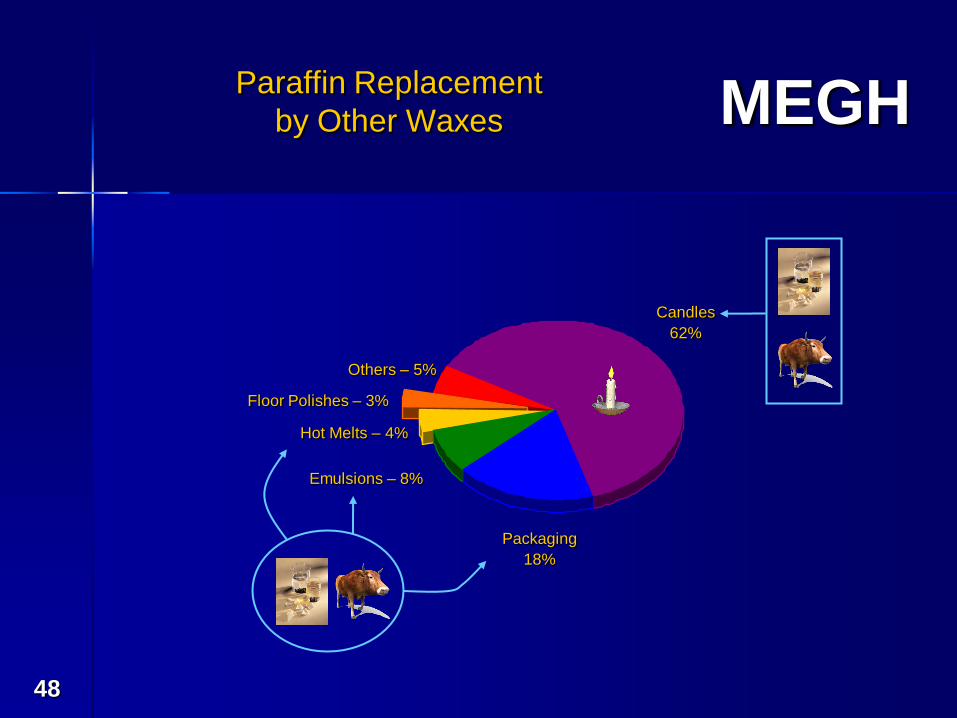

48

Floor Polishes – 3%

Candles

62%

Packaging

18%

Emulsions – 8%

Hot Melts – 4%

Others – 5%

Paraffin Replacement

by Other Waxes

MEGH

49

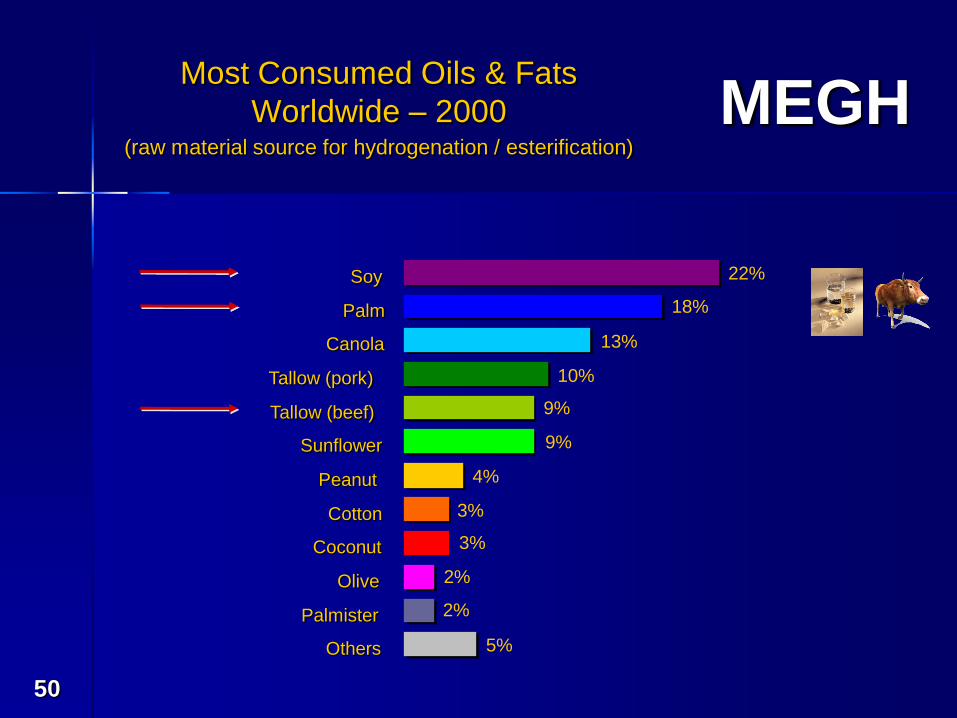

Oils & Fats

MEGH

50

Tallow (pork)

5%

2%

2%

3%

3%

4%

9%

9%

10%

13%

18%

22%Soy

Palm

Canola

Tallow (beef)

Sunflower

Peanut

Cotton

Coconut

Olive

Palmister

Others

Most Consumed Oils & Fats

Worldwide – 2000(raw material source for hydrogenation / esterification)

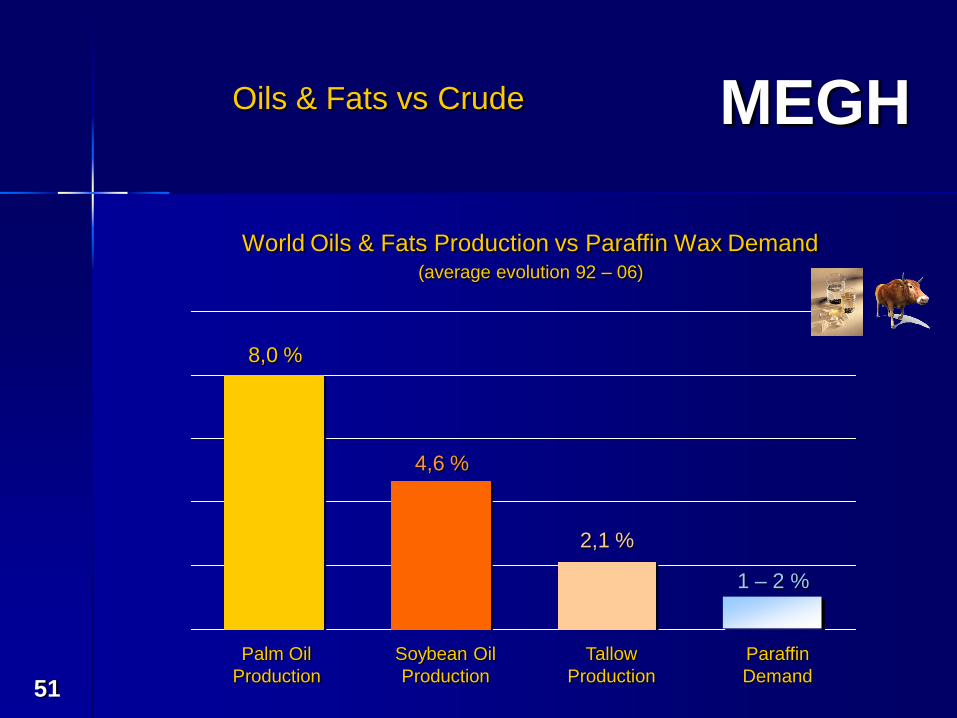

MEGH

51

1 – 2 %

2,1 %

4,6 %

8,0 %

Palm Oil

Production

Soybean Oil

Production

Tallow

Production

Paraffin

Demand

World Oils & Fats Production vs Paraffin Wax Demand(average evolution 92 – 06)

Oils & Fats vs Crude

MEGH

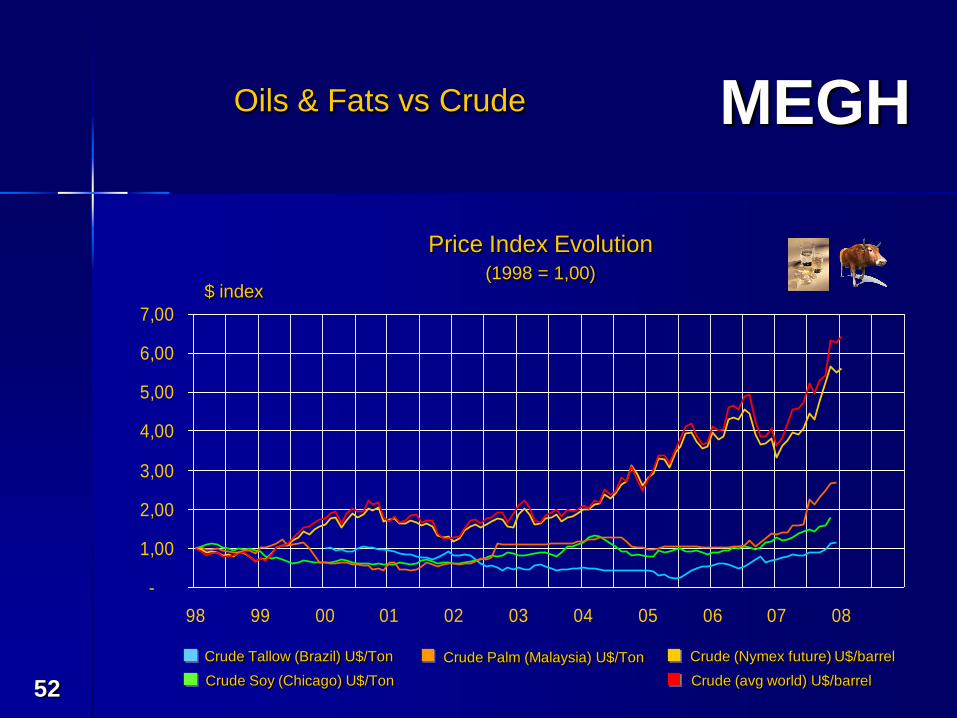

52

-

1,00

2,00

3,00

4,00

5,00

6,00

7,00

98 99 00 01 02 03 04 05 06 07 08

Crude Tallow (Brazil) U$/Ton

Crude Soy (Chicago) U$/Ton

Crude Palm (Malaysia) U$/Ton Crude (Nymex future) U$/barrel

Crude (avg world) U$/barrel

$ index

Price Index Evolution(1998 = 1,00)

Oils & Fats vs Crude

MEGH

53

Biodiesel

MEGH

54

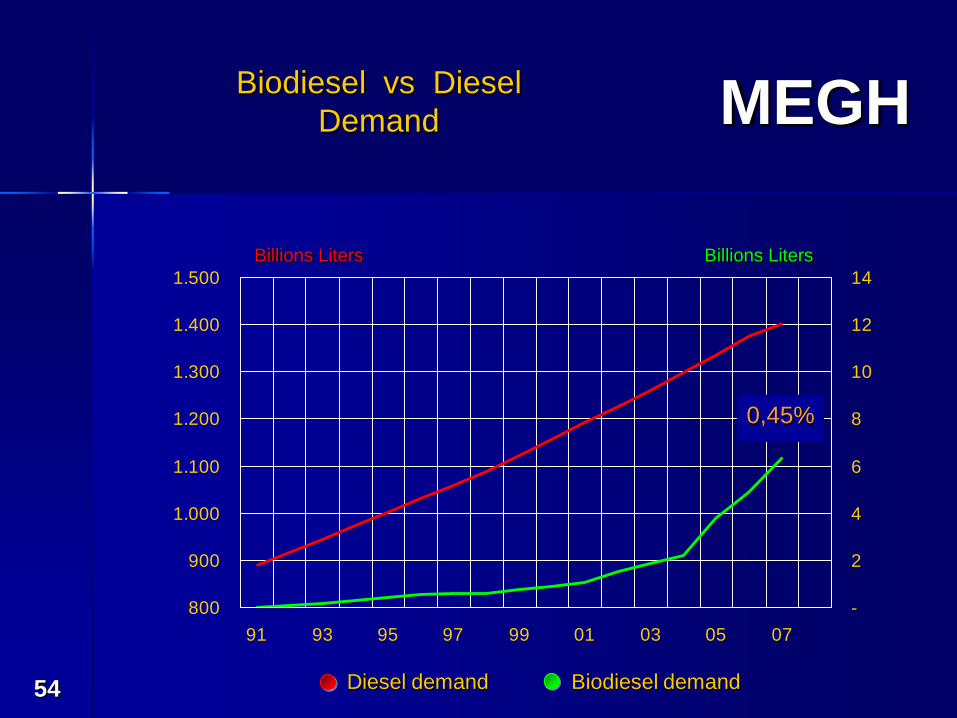

Biodiesel vs Diesel

Demand

800

900

1.000

1.100

1.200

1.300

1.400

1.500

91 93 95 97 99 01 03 05 07

-

2

4

6

8

10

12

14

Billions Liters Billions Liters

Biodiesel demandDiesel demand

0,45%

MEGH

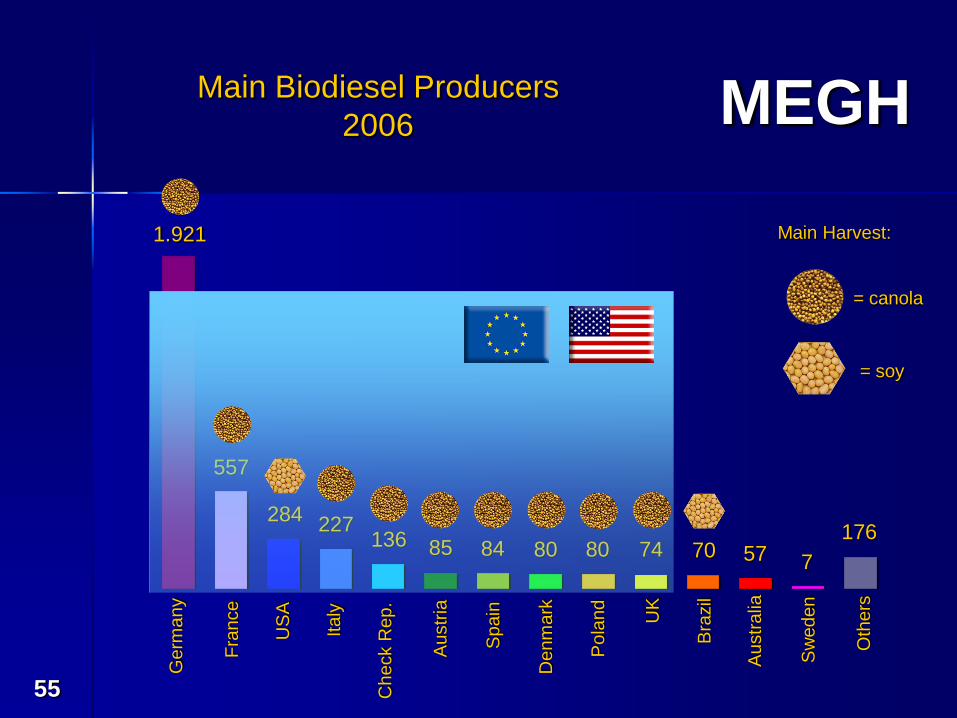

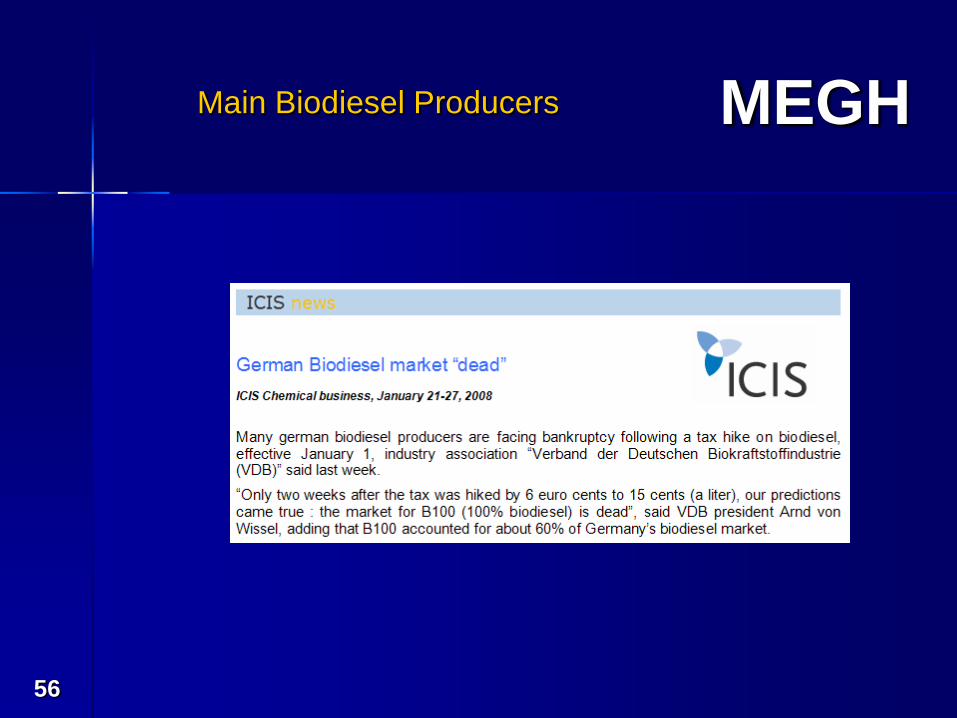

55

Main Biodiesel Producers

2006

Germ

any

Fra

nce

US

A

Italy

Check R

ep.

Austr

ia

Spain

Denm

ark

Pola

nd

UK

Bra

zil

Austr

alia

Sw

eden

Oth

ers

1.921

557

284227

136 85 84 80 80 74 70 57 7

176

= soy

= canola

Main Harvest:

MEGH

56

Main Biodiesel Producers

MEGH

57

-

0,50

1,00

1,50

2,00

2,50

3,00

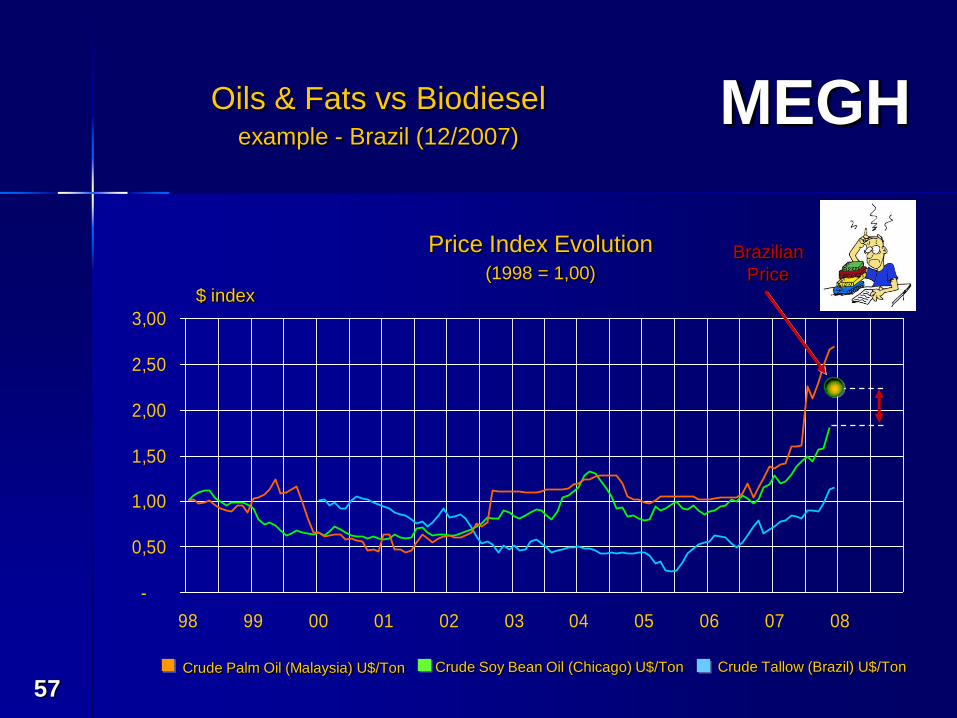

98 99 00 01 02 03 04 05 06 07 08

Crude Tallow (Brazil) U$/TonCrude Soy Bean Oil (Chicago) U$/TonCrude Palm Oil (Malaysia) U$/Ton

$ index

Price Index Evolution(1998 = 1,00)

Oils & Fats vs Biodieselexample - Brazil (12/2007)

Brazilian

Price

MEGH

58

Holy Hope

Candle Mfg.

MEGH

59

MEGH

60

![Megh Boleche Jabo Jabo by Humayun Ahmed [Part.2]easytoload.yolasite.com/resources/Megh Boleche Jabo Jabo.pdf · For More Books & Music VisitFor More Books & Music Visit MurchOna Forum](https://img.pdfslide.us/doc/110x75/5abbfe677f8b9a8f058d1915/megh-boleche-jabo-jabo-by-humayun-ahmed-part2-boleche-jabo-jabopdffor-more-books.jpg)

![Megh Boleche Jabo Jabo by Humayun Ahmed[Part[1].1]](https://img.pdfslide.us/doc/110x75/55292ad94a795977158b4656/megh-boleche-jabo-jabo-by-humayun-ahmedpart11.jpg)

![Megh Boleche Jabo Jabo by Humayun Ahmed[Part.2].PDF](https://img.pdfslide.us/doc/110x75/563dbb60550346aa9aaca20b/megh-boleche-jabo-jabo-by-humayun-ahmedpart2pdf.jpg)