Embed Size (px)

Citation preview

0

The future of self-connect

and the implications for the Dutch aviation sector

Presented by:

Kata CserepVice President ICF International

18 May 2016

The Hague, Netherlands

11

Today’s Agenda

Self-connect today

Top candidates for growth

Dutch Aviation: threat or

opportunity?

Where next?

22

Self-connections Today

33

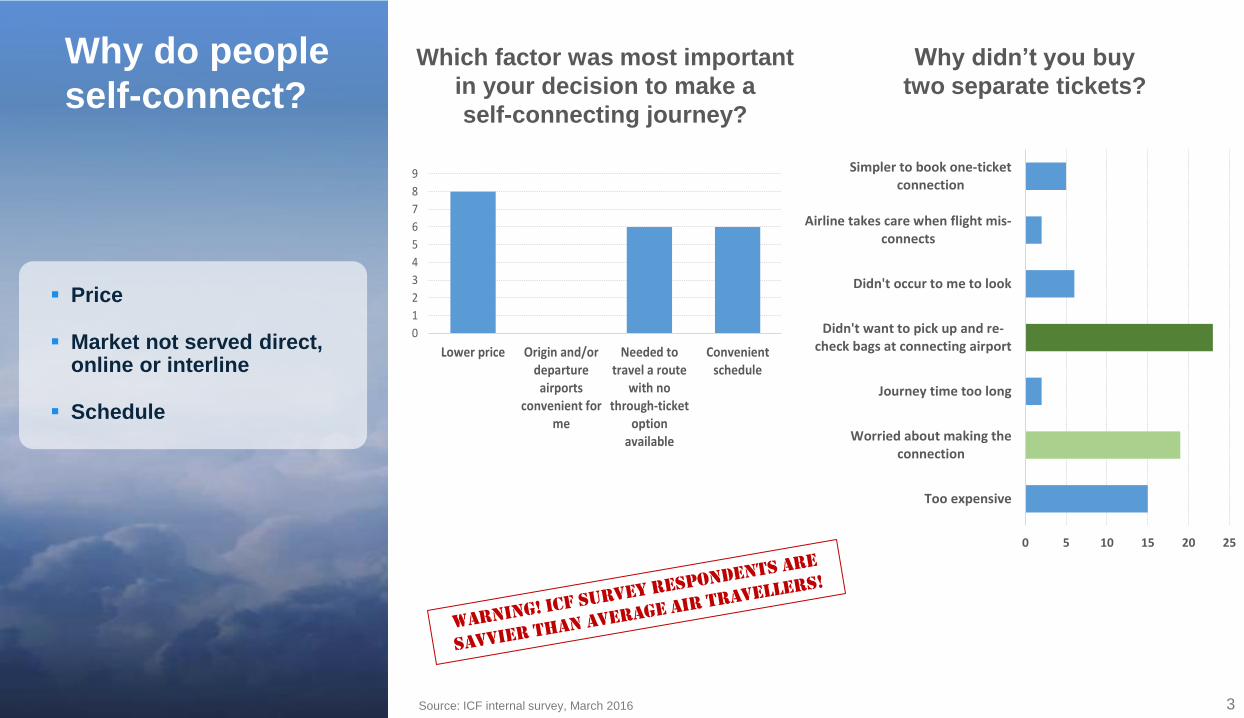

Why do people

self-connect?

Source: ICF internal survey, March 2016

0

1

2

3

4

5

6

7

8

9

Lower price Origin and/ordepartureairports

convenient forme

Needed totravel a route

with nothrough-ticket

optionavailable

Convenientschedule

Which factor was most important in your decision to make a self-connecting

journey?

0 5 10 15 20 25

Too expensive

Worried about making theconnection

Journey time too long

Didn't want to pick up and re-check bags at connecting airport

Didn't occur to me to look

Airline takes care when flight mis-connects

Simpler to book one-ticketconnection

Why didn't you buy two separate tickets?

Price

Market not served direct, online or interline

Schedule

Which factor was most important

in your decision to make a

self-connecting journey?

Why didn’t you buy

two separate tickets?

44

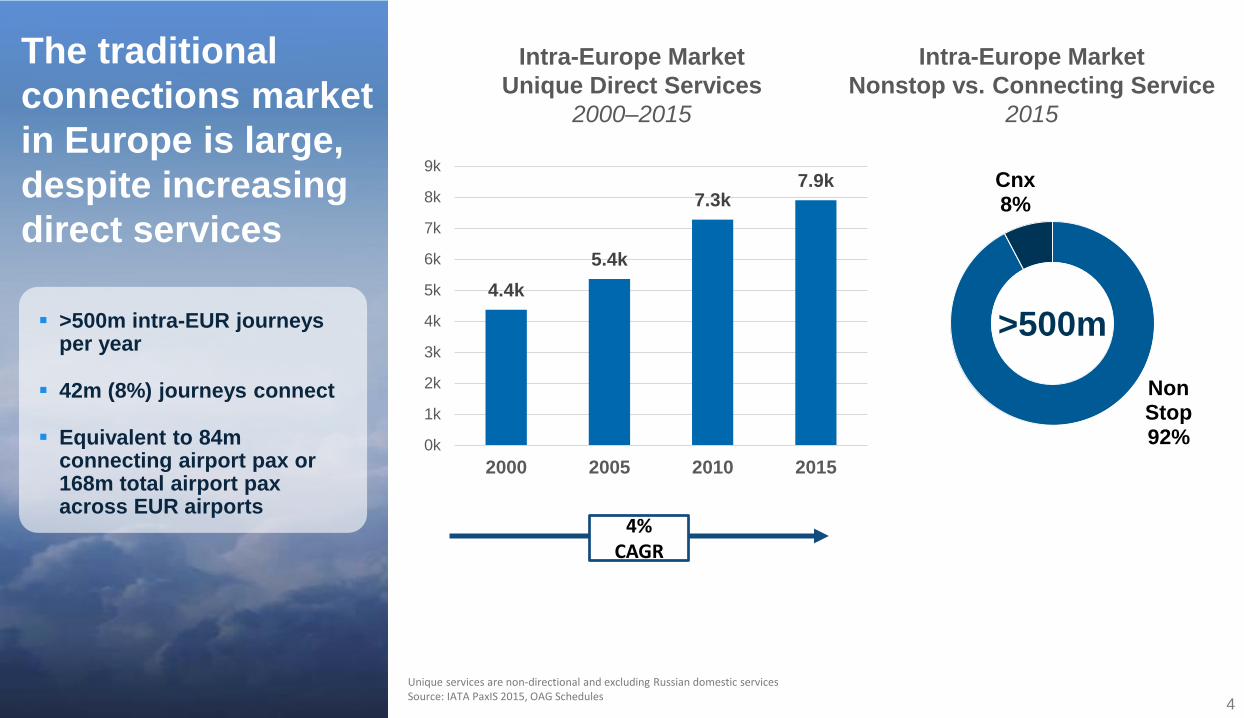

The traditional

connections market

in Europe is large,

despite increasing

direct services

Unique services are non-directional and excluding Russian domestic servicesSource: IATA PaxIS 2015, OAG Schedules

>500m intra-EUR journeys per year

42m (8%) journeys connect

Equivalent to 84m connecting airport pax or 168m total airport paxacross EUR airports

Non Stop92%

Cnx8%

>500m4.4k

5.4k

7.3k7.9k

0k

1k

2k

3k

4k

5k

6k

7k

8k

9k

2000 2005 2010 2015

4% CAGR

Intra-Europe Market

Unique Direct Services

2000–2015

Intra-Europe Market

Nonstop vs. Connecting Service

2015

55

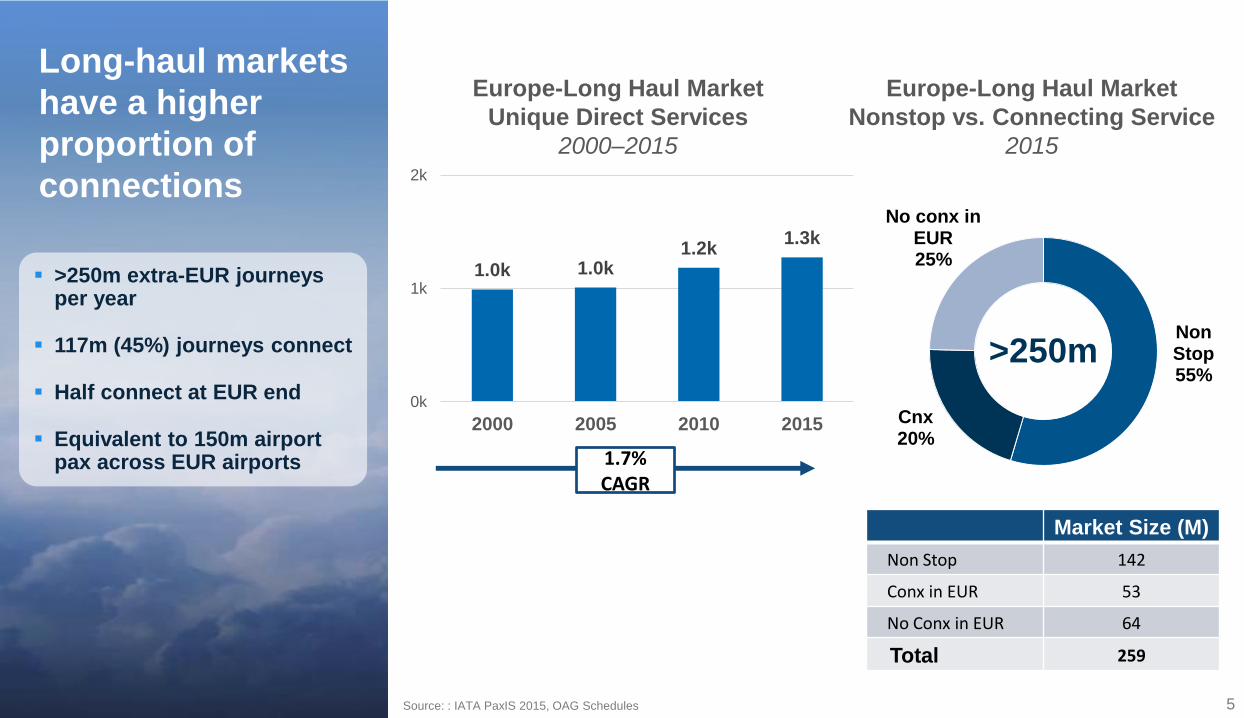

Long-haul markets

have a higher

proportion of

connections

Source: : IATA PaxIS 2015, OAG Schedules

Market Size (M)

Non Stop 142

Conx in EUR 53

No Conx in EUR 64

Total 259

>250m extra-EUR journeys per year

117m (45%) journeys connect

Half connect at EUR end

Equivalent to 150m airport pax across EUR airports

1.0k 1.0k1.2k

1.3k

0k

1k

2k

2000 2005 2010 2015

1.7% CAGR

Non Stop55%

Cnx20%

No conx in EUR25%

>250m

Europe-Long Haul Market

Unique Direct Services

2000–2015

Europe-Long Haul Market

Nonstop vs. Connecting Service

2015

66

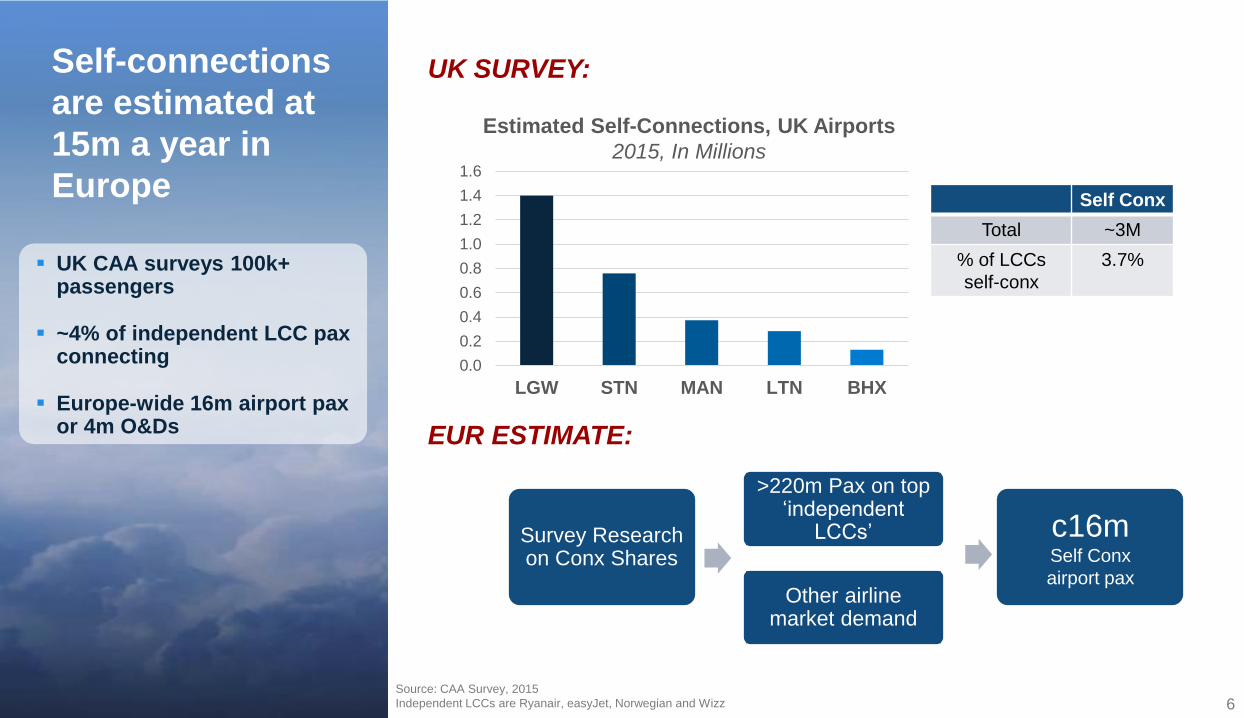

Self-connections

are estimated at

15m a year in

Europe

Source: CAA Survey, 2015

Independent LCCs are Ryanair, easyJet, Norwegian and Wizz

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

LGW STN MAN LTN BHX

Self Conx

Total ~3M

% of LCCs

self-conx

3.7%

UK SURVEY:

Survey Research on Conx Shares

Other airline market demand

c16mSelf Conx

airport pax

>220m Pax on top ‘independent

LCCs’

UK CAA surveys 100k+ passengers

~4% of independent LCC paxconnecting

Europe-wide 16m airport paxor 4m O&Ds EUR ESTIMATE:

Estimated Self-Connections, UK Airports

2015, In Millions

77

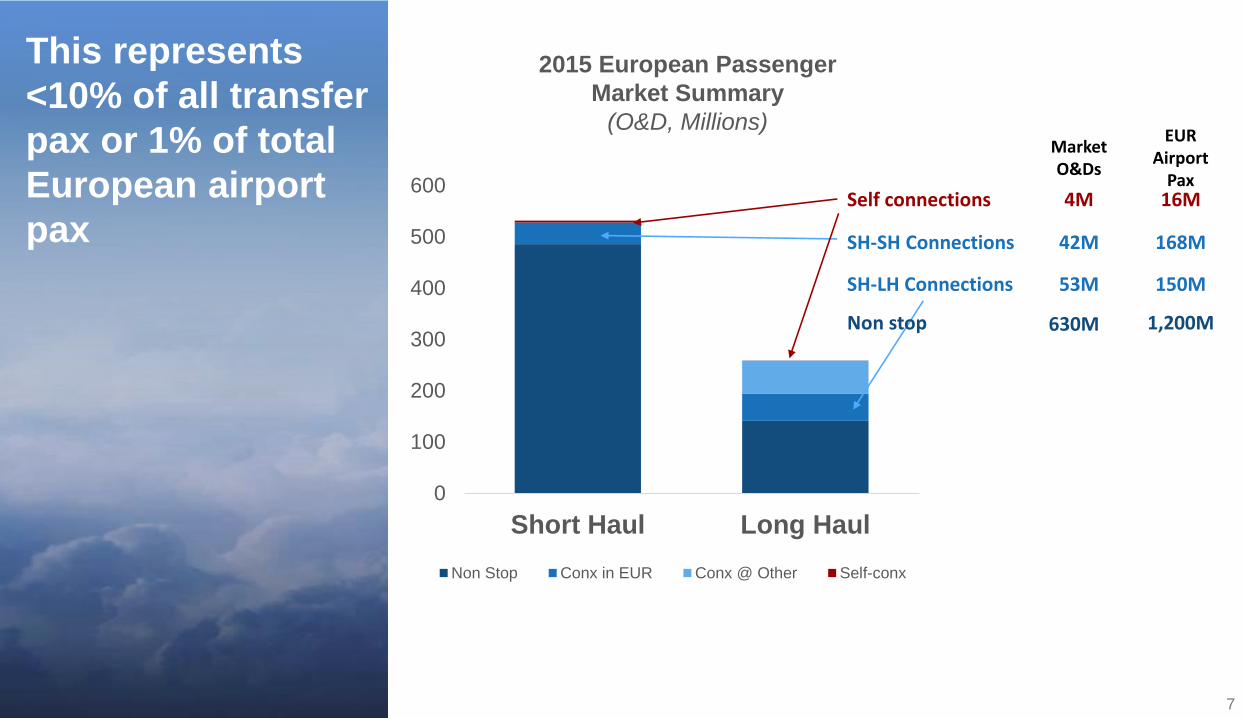

This represents

<10% of all transfer

pax or 1% of total

European airport

pax

0

100

200

300

400

500

600

Short Haul Long Haul

Non Stop Conx in EUR Conx @ Other Self-conx

Self connections 4M 16M

MarketO&Ds

EUR Airport

Pax

SH-SH Connections 42M 168M

SH-LH Connections 53M 150M

Non stop 630M 1,200M

2015 European Passenger

Market Summary

(O&D, Millions)

88

Top Candidates for

Self-Connect

99

UNALIGNED CARRIERS

LONG HAUL LOW COST

NON HUB

Self-connect is

most likely to take

off at unaligned

carriers

Source: BP Statistical Review of World Energy June 2015, ICF International Analysis

Incremental passengers and revenue

are the name of the game…

…ideally without incremental cost

?

1010

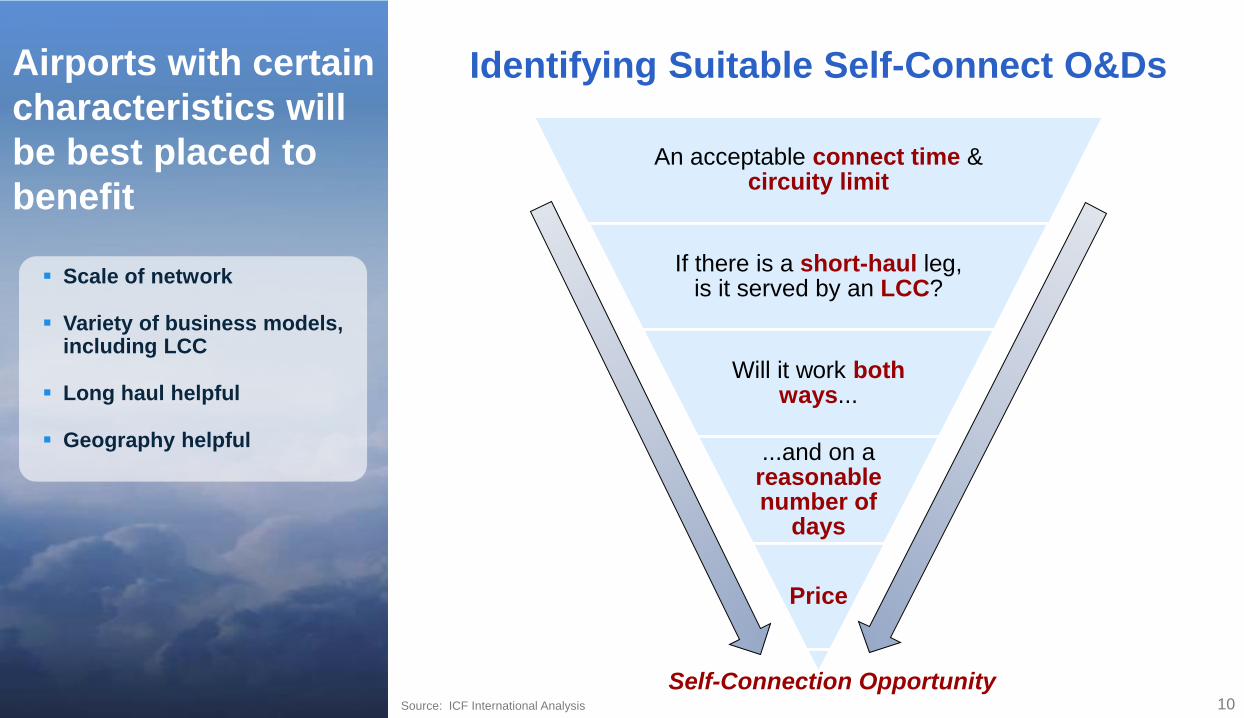

Airports with certain

characteristics will

be best placed to

benefit

Source: ICF International Analysis

Identifying Suitable Self-Connect O&Ds

Self-Connection Opportunity

An acceptable connect time &circuity limit

If there is a short-haul leg, is it served by an LCC?

Will it work both ways...

...and on a reasonable number of

days

Price

Scale of network

Variety of business models, including LCC

Long haul helpful

Geography helpful

1111

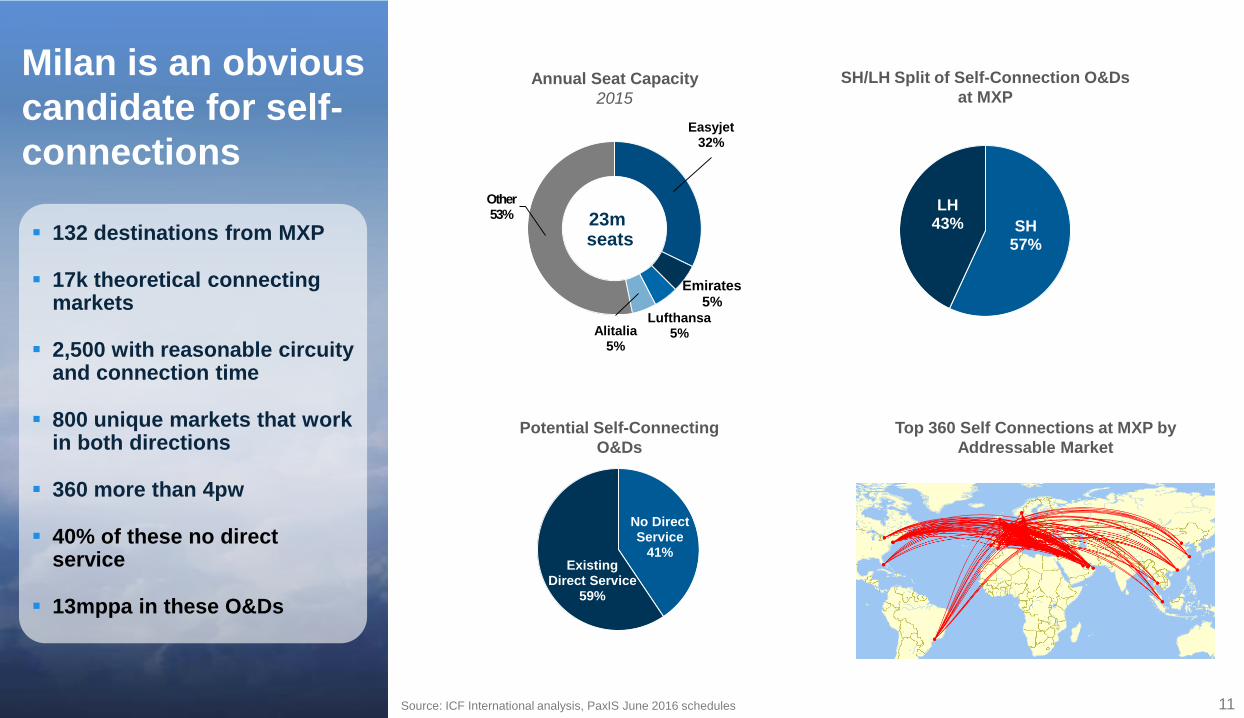

Milan is an obvious

candidate for self-

connections

Source: ICF International analysis, PaxIS June 2016 schedules

132 destinations from MXP

17k theoretical connecting markets

2,500 with reasonable circuity and connection time

800 unique markets that work in both directions

360 more than 4pw

40% of these no direct service

13mppa in these O&Ds

SH57%

LH43%

Easyjet32%

Emirates5%

Lufthansa5%Alitalia

5%

Other53% 23m

seats

SH/LH Split of Self-Connection O&Ds

at MXP

No Direct Service

41%Existing

Direct Service59%

Top 360 Self Connections at MXP by

Addressable Market

Annual Seat Capacity

2015

Potential Self-Connecting

O&Ds

1212

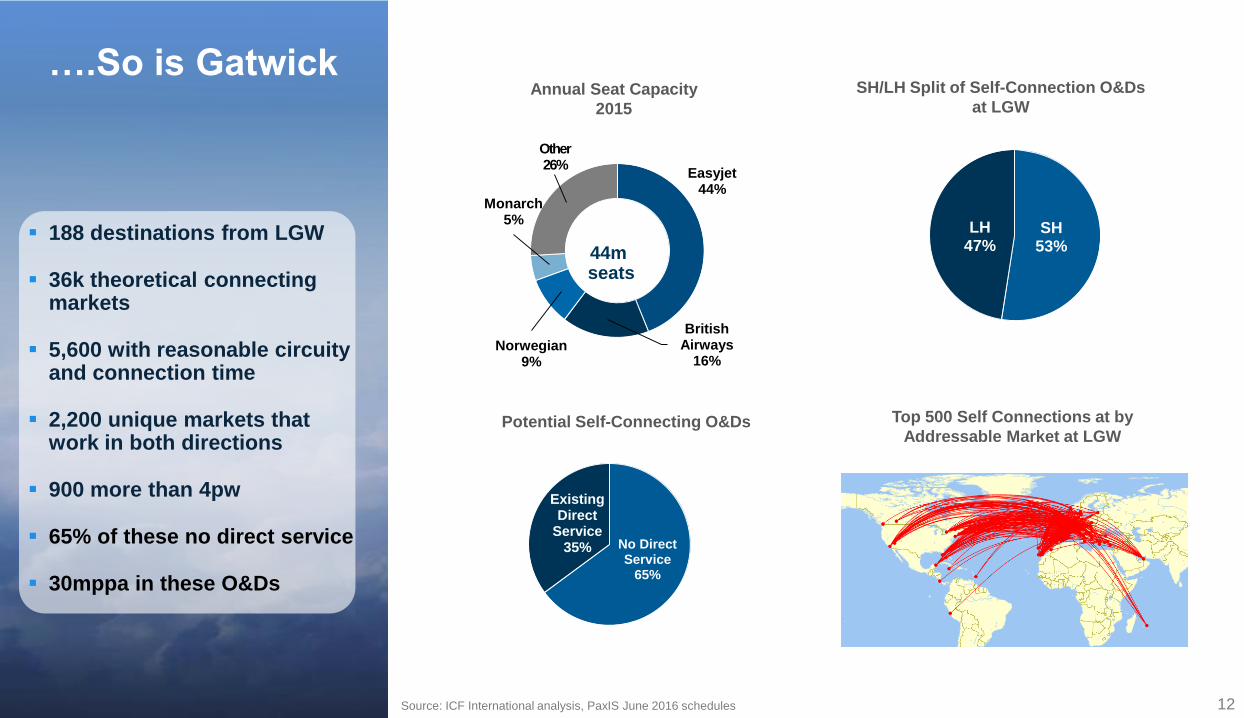

….So is Gatwick

Source: ICF International analysis, PaxIS June 2016 schedules

188 destinations from LGW

36k theoretical connecting markets

5,600 with reasonable circuity and connection time

2,200 unique markets that work in both directions

900 more than 4pw

65% of these no direct service

30mppa in these O&Ds

SH53%

LH47%

SH/LH Split of Self-Connection O&Ds

at LGW

No Direct Service

65%

Existing Direct

Service35%

Top 500 Self Connections at by

Addressable Market at LGWPotential Self-Connecting O&Ds

Easyjet44%

British Airways

16%Norwegian

9%

Monarch5%

Other26%

44m seats

Annual Seat Capacity

2015

1313

Dutch Aviation:

Threat or Opportunity?

1414

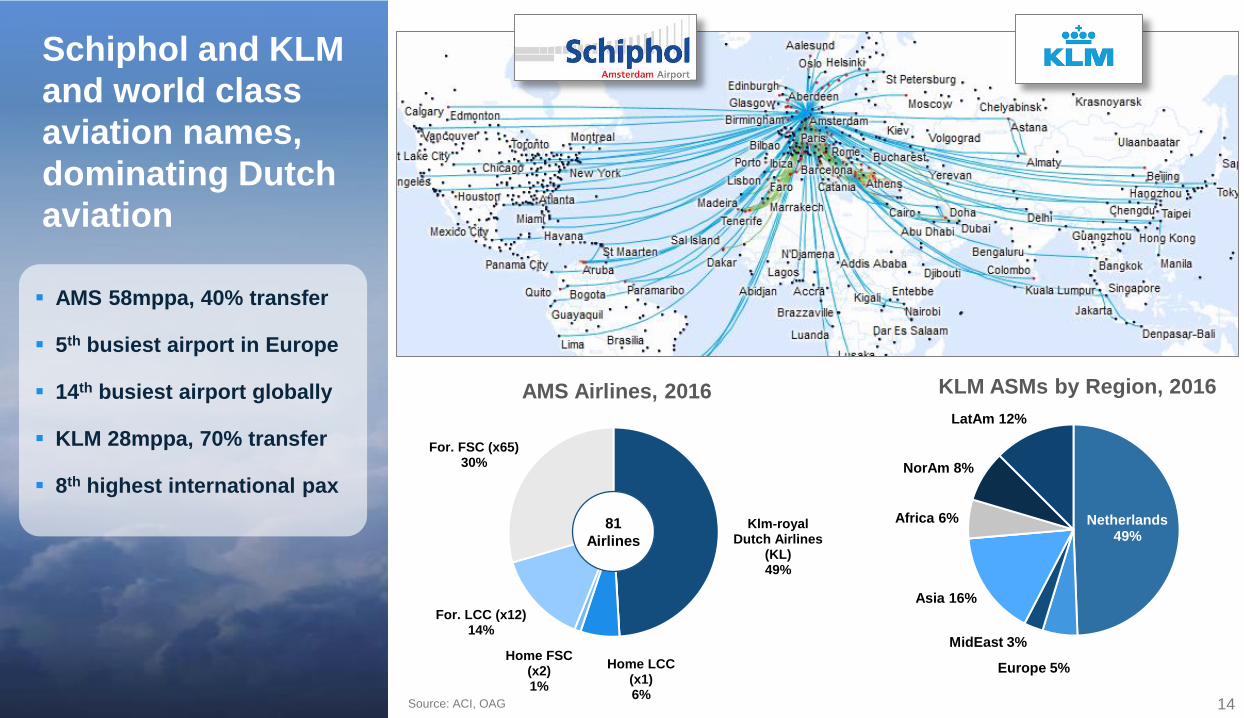

Schiphol and KLM

and world class

aviation names,

dominating Dutch

aviation

Source: ACI, OAG

AMS 58mppa, 40% transfer

5th busiest airport in Europe

14th busiest airport globally

KLM 28mppa, 70% transfer

8th highest international pax

Netherlands49%

Europe 5%

MidEast 3%

Asia 16%

Africa 6%

NorAm 8%

LatAm 12%

KLM ASMs by Region, 2016

Klm-royal Dutch Airlines

(KL)49%

Home LCC (x1) 6%

Home FSC (x2) 1%

For. LCC (x12) 14%

For. FSC (x65) 30%

81

Airlines

AMS Airlines, 2016

1515

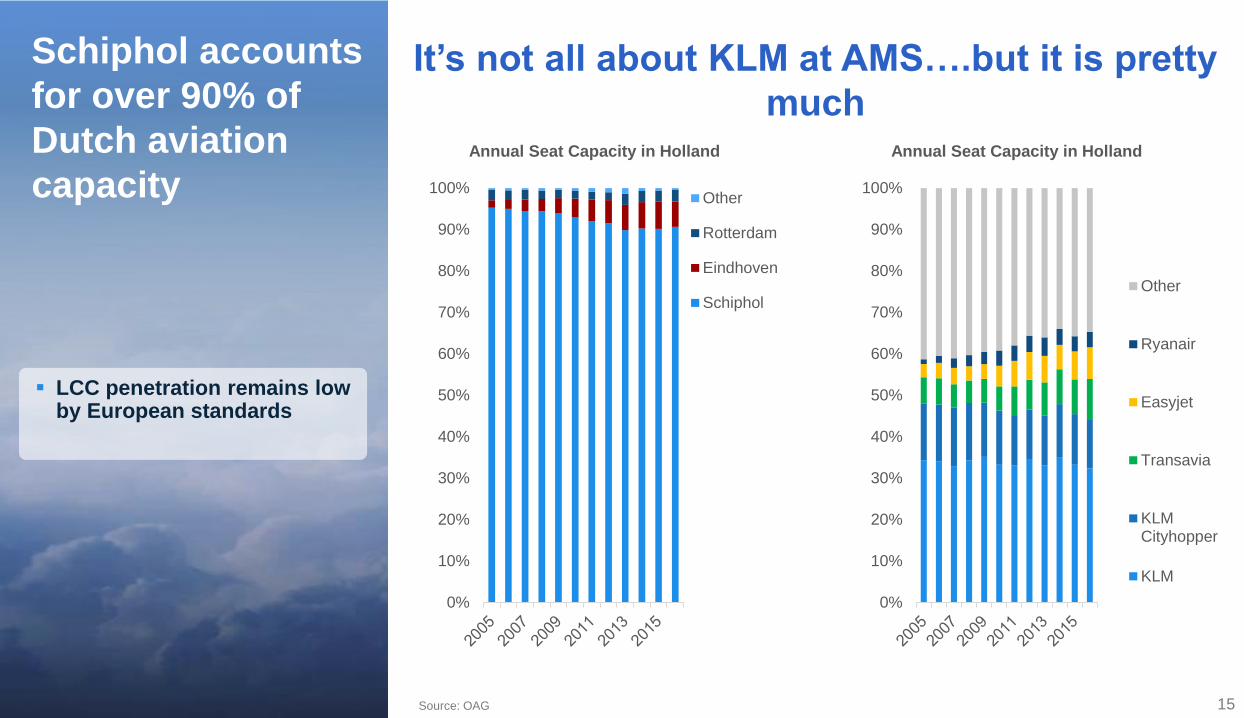

Schiphol accounts

for over 90% of

Dutch aviation

capacity

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Other

Rotterdam

Eindhoven

Schiphol

Source: OAG

It’s not all about KLM at AMS….but it is pretty

much

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Other

Ryanair

Easyjet

Transavia

KLMCityhopper

KLM

LCC penetration remains low by European standards

Annual Seat Capacity in Holland Annual Seat Capacity in Holland

1616

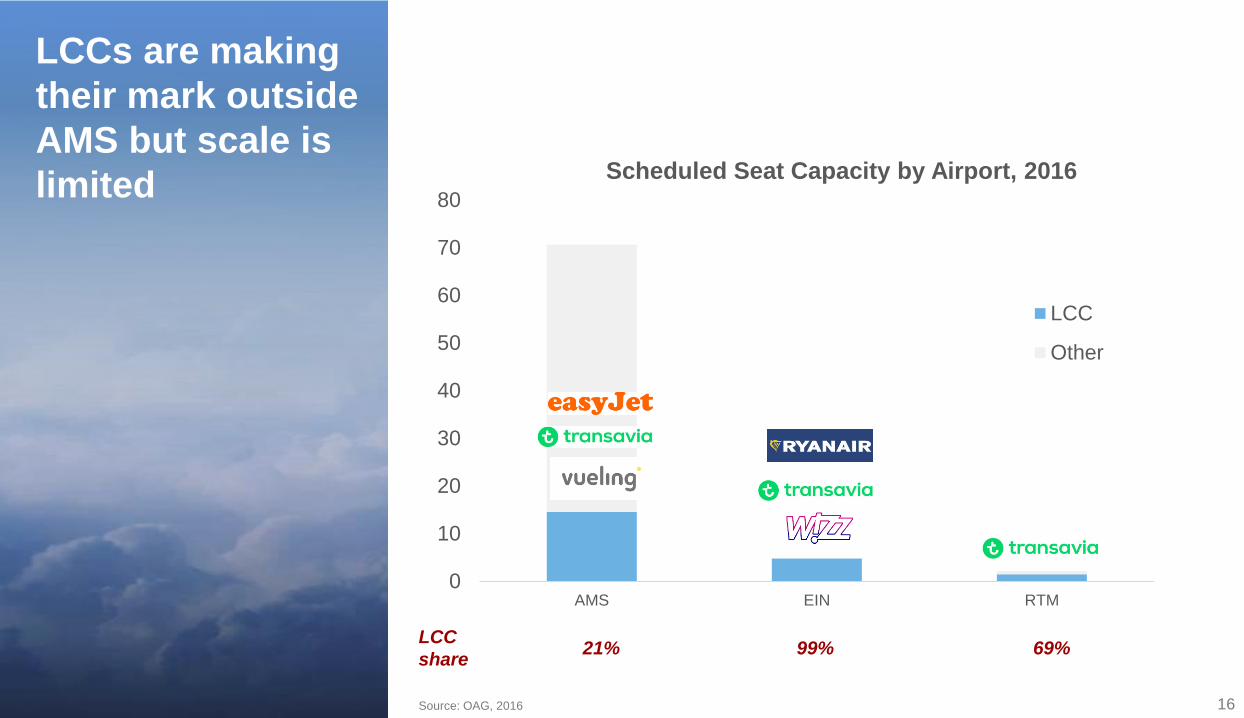

LCCs are making

their mark outside

AMS but scale is

limited

Source: OAG, 2016

0

10

20

30

40

50

60

70

80

AMS EIN RTM

LCC

Other

21% 69%99%

Scheduled Seat Capacity by Airport, 2016

LCC

share

1717

Klm50%

Easyjet8%

Transav…

Delta5%

Other32%

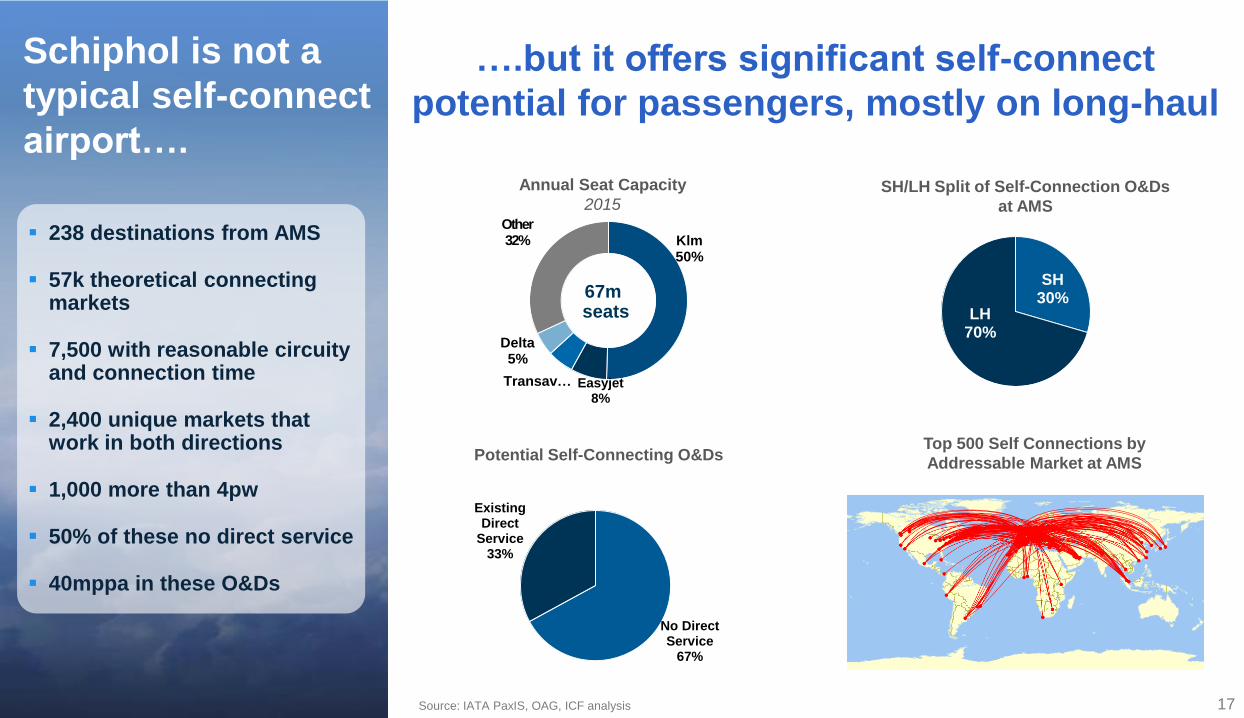

Schiphol is not a

typical self-connect

airport….

Source: IATA PaxIS, OAG, ICF analysis

….but it offers significant self-connect

potential for passengers, mostly on long-haul

238 destinations from AMS

57k theoretical connecting markets

7,500 with reasonable circuity and connection time

2,400 unique markets that work in both directions

1,000 more than 4pw

50% of these no direct service

40mppa in these O&Ds

No Direct Service

67%

Existing Direct

Service33%

SH/LH Split of Self-Connection O&Ds

at AMS

SH30%

LH70%

Top 500 Self Connections by

Addressable Market at AMS

Annual Seat Capacity

2015

Potential Self-Connecting O&Ds

67m seats

1818

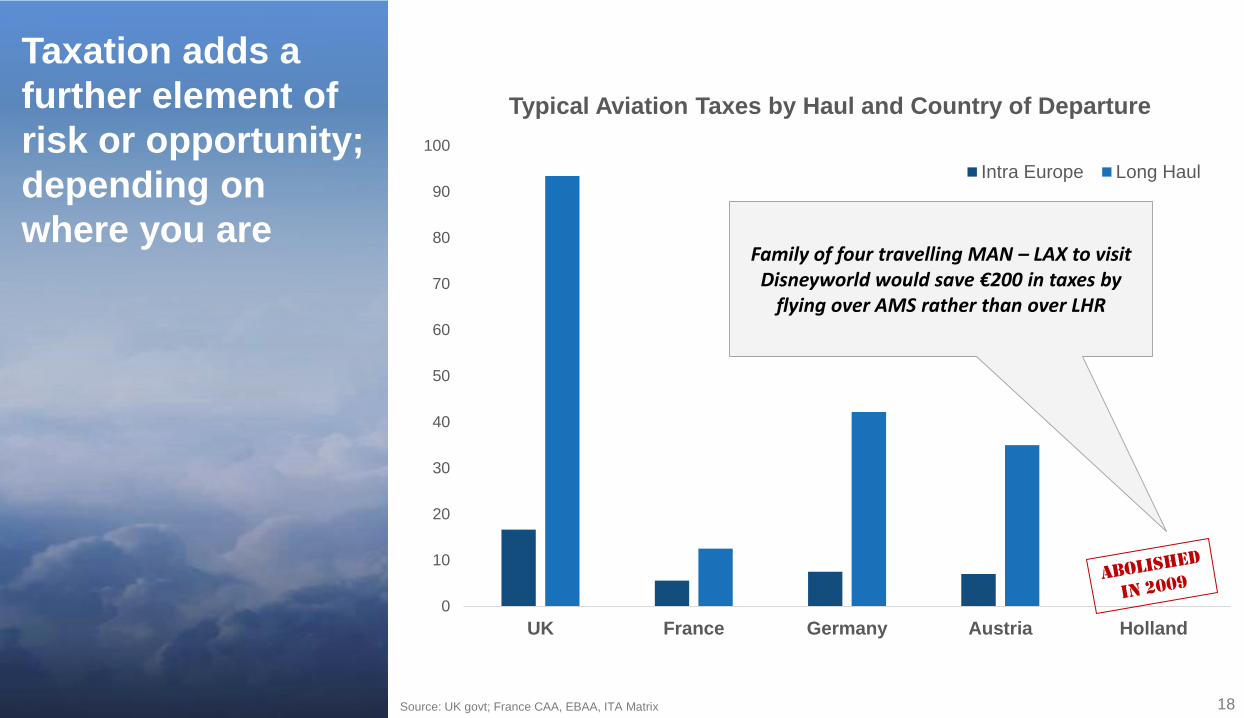

Taxation adds a

further element of

risk or opportunity;

depending on

where you are

Source: UK govt; France CAA, EBAA, ITA Matrix

Typical Aviation Taxes by Haul and Country of Departure

0

10

20

30

40

50

60

70

80

90

100

UK France Germany Austria Holland

Intra Europe Long Haul

Family of four travelling MAN – LAX to visit Disneyworld would save €200 in taxes by

flying over AMS rather than over LHR

1919

Where Next?

2020

The LCCs are

evolving,

competing with

each other and

with legacy

carriers

Source: OAG Data, ICF International Analysis

Own metal Cnx

LCC Alliance in Asia

2121

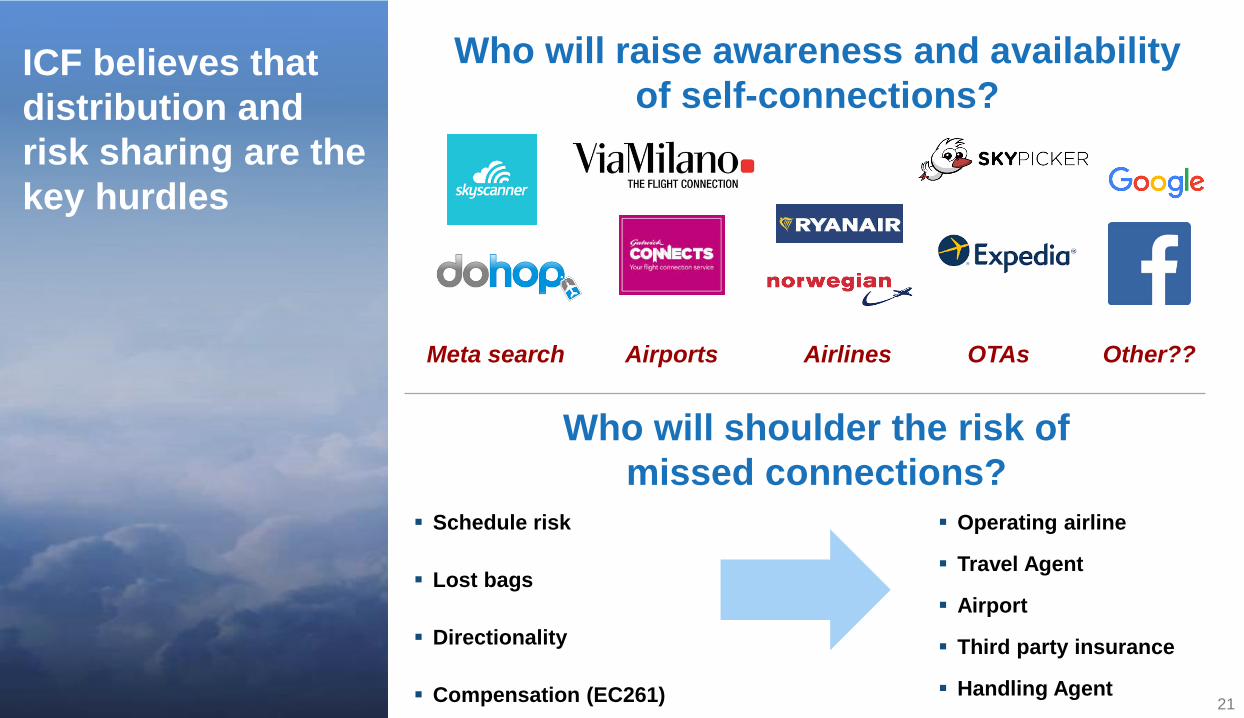

ICF believes that

distribution and

risk sharing are the

key hurdles

Who will raise awareness and availability

of self-connections?

Meta search Airports Airlines OTAs Other??

Who will shoulder the risk of

missed connections?

Schedule risk

Lost bags

Directionality

Compensation (EC261)

Operating airline

Travel Agent

Airport

Third party insurance

Handling Agent

2222

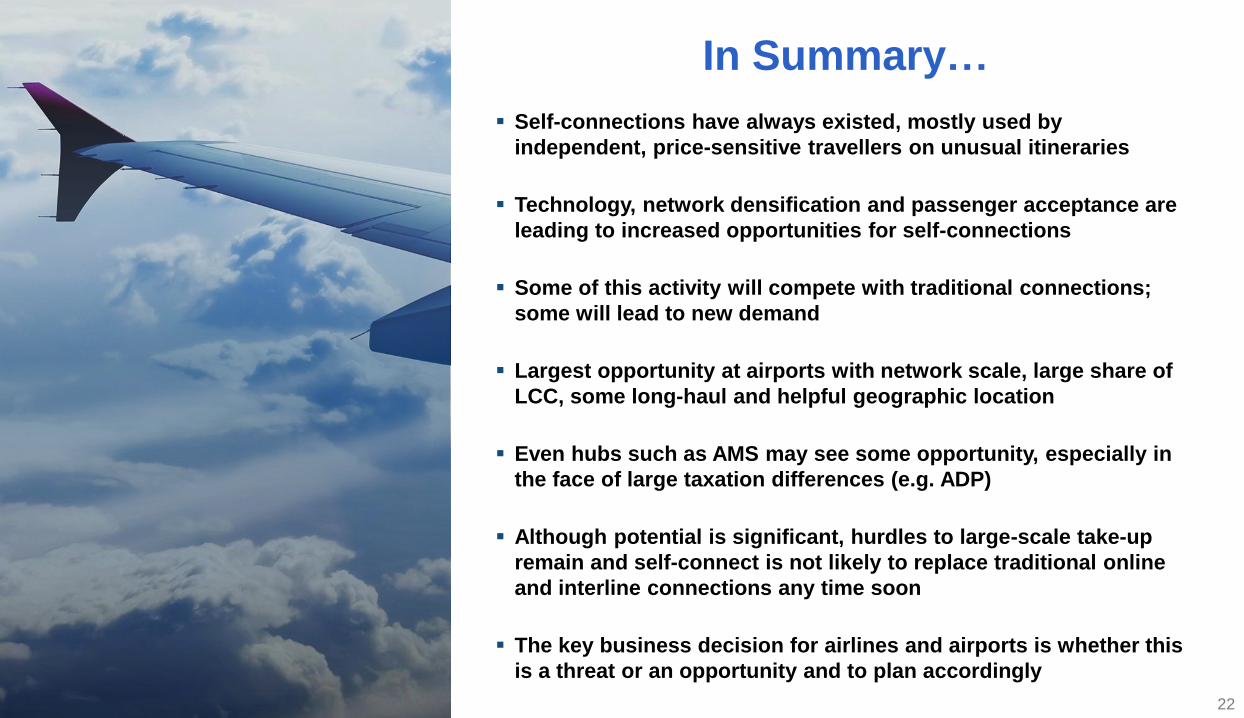

Self-connections have always existed, mostly used by

independent, price-sensitive travellers on unusual itineraries

Technology, network densification and passenger acceptance are

leading to increased opportunities for self-connections

Some of this activity will compete with traditional connections;

some will lead to new demand

Largest opportunity at airports with network scale, large share of

LCC, some long-haul and helpful geographic location

Even hubs such as AMS may see some opportunity, especially in

the face of large taxation differences (e.g. ADP)

Although potential is significant, hurdles to large-scale take-up

remain and self-connect is not likely to replace traditional online

and interline connections any time soon

The key business decision for airlines and airports is whether this

is a threat or an opportunity and to plan accordingly

In Summary…

23

For questions regarding this

presentation, please contact:

Kata CserepVice President Airports

[email protected] +44 203 096 4921

18 May 2016

The Hague, Netherlands

THANK YOU!

With thanks to Nishaan Rama and Rob Walker, ICF

2424

ICF is one of the world’s largest and

most experienced aviation & aerospace

consulting firms

53 years in business (founded 1963)

100+ professional staff

− Dedicated exclusively to aviation

and aerospace

− Blend of consulting professionals and

experienced aviation executives

Specialized, focused expertise and

proprietary knowledge

Broad functional capabilities

More than 10,000 private and public sector

assignments

Backed by parent company ICF International

(2014 revenue - $1.05B)

Global presence –– offices around the world

New York • Boston • Ann Arbor • London • Singapore • Beijing • Hong Kong

Airports

Airlines

Aerospace

& MRO

Aircraft Asset

Advisory

joined ICF in 2011

joined ICF in 2007

joined ICF in 2012

joined ICF in 2014