Embed Size (px)

Citation preview

© 1995 American Accounting AssociationAccounting HorizonsVol 9 No. 4December 1995pp.118-127

COMMENTARY

Robert K. Elliott

Robert K. Elliott is Chairman, KPMG Peat Marwick LLP, AICPA Special Committee onAssurance Services.

The Future of Assurance Services:Implications for Academia

The AICPA Special Committee on Assur-ance Services was set up in response to a de-cline in the market vitality of the audit. (SeeElliott 1994a and 1994b for background.) Ourpurpose is to develop ideas and initiate stepsto refurbish the profession's product. This mis-sion was conceived in response to the currentand emergent audit/assurance environment,the obvious context for considering the vital-ity of the audit.

The current audit is surely very valuableto the capital markets and to our economy, butit is a mature product that has not been grow-ing. Over the last six years real accountingand auditing revenues for the top 60 firmshave been flat despite growing GDP. The mar-ket seems saturated; there is overcapacity andprice competition; and the inherent reliabil-ity of accounting data has increased with im-provements in business information systems.The audit service is generalized—a one-size-fits-all product—rather than tailored to theindividual needs of investors and creditors andother users, yet responding to individual cus-tomer needs is one of the great messages ofthe last decade of economic change. Mean-while, software that can do audit functions isa long-term threat. Imagine banks purchas-ing or developing such software and auditingtheir own debtors, institutional investors au-diting investees, or internal auditing bolsteredby advanced software that drastically reducesthe evidence needed for an audit opinion.

A large part of the immediate problem is

the limited usefulness of today's financialstatements. They don't, for example, reflect in-formation-age assets, such as information, ca-pacity for innovation, and human resources.As a consequence, they have been a decliningproportion of the information inputs to inves-tors' decision making. That translates into adeclining share of the information market-place for auditors (and, for that matter, finan-cial accountants). Were financial statementsas central to investors' decision making asthey were thirty years ago, there would berelatively little concern over the vitality of theaudit.

However, the Committee was not intendedto address improvements in financial report-ing. That was the job of the Special Commit-tee on Financial Reporting (the Jenkins Com-mittee), which completed its work last year.Its recommendations have not yet been en-acted, but it would nevertheless have beensuperfluous to appoint an additional commit-tee devoted to refurbishing financial reporting.

Our task is to refurbish the profession's"product" in a different sense: to identify newservices in the wider area of the assurancefunction, an area that includes the basic au-dit, but goes beyond it. This must take place

' Derived from data published in Accounting Tbday.

This article is adapted from Mr. Elliott's plenary addressat the AAA's annual meeting in Orlando on August 16,1995.

The Future of Assurance Services: Implications for Academia 119

with an eye to the future, for the committee ischarged to take a long-term view.

POTENTIAL SCOPE OFASSURANCE SERVICES

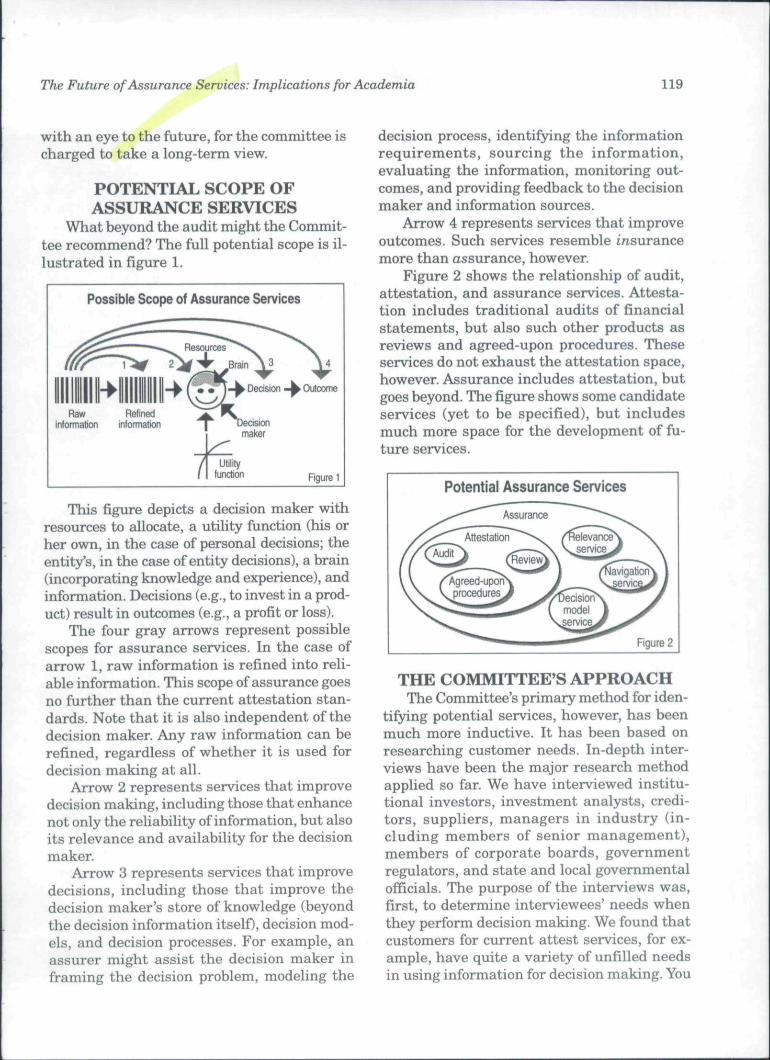

What heyond the audit might the Commit-tee recommend? The full potential scope is il-lustrated in figure 1.

Possible Scope of Assurance Services

Raw Refinedinformation information Decision

maker

Utilityfunction Figure 1

This figure depicts a decision maker withresources to allocate, a utility function (his orher own, in the case of personal decisions; theentity's, in the case of entity decisions), a hrain(incorporating knowledge and experience), andinformation. Decisions (e.g., to invest in a prod-uct) result in outcomes (e.g., a profit or loss).

The four gray arrows represent possiblescopes for assurance services. In the case ofarrow 1, raw information is refined into reli-ahle information. This scope of assurance goesno further than the current attestation stan-dards. Note that it is also independent of thedecision maker. Any raw information can berefined, regardless of whether it is used fordecision making at all.

Arrow 2 represents services that improvedecision making, including those that enhancenot only the reliability of information, but alsoits relevance and availability for the decisionmaker.

Arrow 3 represents services that improvedecisions, including those that improve thedecision maker's store of knowledge (beyondthe decision information itself), decision mod-els, and decision processes. For example, anassurer might assist the decision maker inframing the decision problem, modeling the

decision process, identifying the informationrequirements, sourcing the information,evaluating the information, monitoring out-comes, and providing feedback to the decisionmaker and information sources.

Arrow 4 represents services that improveoutcomes. Such services resemble insurancemore than assurance, however.

Figure 2 shows the relationship of audit,attestation, and assurance services. Attesta-tion includes traditional audits of financialstatements, but also such other products asreviews and agreed-upon procedures. Theseservices do not exhaust the attestation space,however. Assurance includes attestation, butgoes beyond. The figure shows some candidateservices (yet to be specified), but includesmuch more space for the development of fu-ture services.

Potential Assurance Services

Figure 2

THE COMMITTEE'S APPROACHThe Committee's primary method for iden-

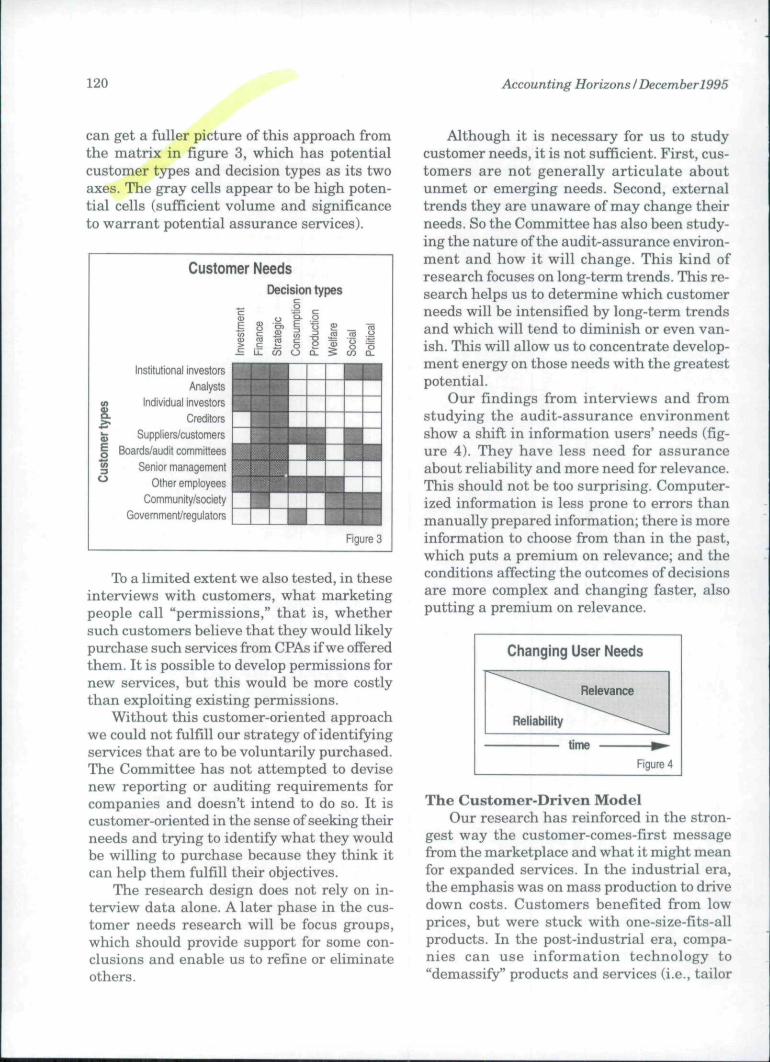

tifying potential services, however, has beenmuch more inductive. It has been based onresearching customer needs. In-depth inter-views have been the major research methodapplied so far. We have interviewed institu-tional investors, investment analysts, credi-tors, suppliers, managers in industry (in-cluding members of senior management),members of corporate boards, governmentregulators, and state and local governmentalofficials. The purpose of the interviews was,first, to determine interviewees' needs whenthey perform decision making. We found thatcustomers for current attest services, for ex-ample, have quite a variety of unfilled needsin using information for decision making. You

120 Accounting Horizons /Decemberl995

can get a fuller picture of this approach fromthe matrix in figure 3, which has potentialcustomer types and decision types as its twoaxes. The gray cells appear to be high poten-tial cells (sufficient volume and significanceto warrant potential assurance services).

Customer NeedsDecisio

.— oS o ^-E g a. EVi ^ B ^<u to CO c> ,E i= o

-£ ii_ CO o

Institutional investors ^ ^ ^ ^ H | ~Analysts ^ ^ ^ ^ H ~

« Individual investors ^ ^ ^ ^ H ~J : Creditors ^ ^ ^ ^ ^ ~^ Suppliers/customers [ ~ ^ ^ ^ ^ ^ |§ Boards/audit committees j ^ p H p i ^ ^

1 1

Pro

duct

ion

X-

mW

elfa

re

«

== Senior management t i | j | |" Other employees ^ ^ ^ ^ B ^ ^ ^ ^ H

Community/society [ ^ ^ ^ ^ ^ ^ ^ ^ j |Government/regulators | | | J j j J

11Figure 3

To a limited extent we also tested, in theseinterviews with customers, what marketingpeople call "permissions," that is, whethersuch customers believe that they would likelypurchase such services from CPAs if we offeredthem. It is possible to develop permissions fornew services, but this would be more costlythan exploiting existing permissions.

Without this customer-oriented approachwe could not fulfill our strategy of identifyingservices that are to be voluntarily purchased.The Committee has not attempted to devisenew reporting or auditing requirements forcompanies and doesn't intend to do so. It iscustomer-oriented in the sense of seeking theirneeds and trying to identify what they wouldbe willing to purchase because they think itcan help them fulfill their objectives.

The research design does not rely on in-terview data alone. A later phase in the cus-tomer needs research will be focus groups,which should provide support for some con-clusions and enable us to refine or ehminateothers.

Although it is necessary for us to studycustomer needs, it is not sufficient. First, cus-tomers are not generally articulate aboutunmet or emerging needs. Second, externaltrends they are unaware of may change theirneeds. So the Committee has also been study-ing the nature of the audit-assurance environ-ment and how it will change. This kind ofresearch focuses on long-term trends. This re-search helps us to determine which customerneeds will be intensified by long-term trendsand which will tend to diminish or even van-ish. This will allow us to concentrate develop-ment energy on those needs with the greatestpotential.

Our findings from interviews and fromstudying the audit-assurance environmentshow a shift in information users' needs (fig-ure 4). They have less need for assuranceabout reliability and more need for relevance.This should not be too surprising. Computer-ized information is less prone to errors thanmanually prepared information; there is moreinformation to choose fi"om than in the past,which puts a premium on relevance; and theconditions affecting the outcomes of decisionsare more complex and changing faster, alsoputting a premium on relevance.

Changing User Needs

Relevance

Reliability

timeFigure 4

The Customer-Driven ModelOur research has reinforced in the stron-

gest way the customer-comes-first messagefi*om the marketplace and what it might meanfor expanded services. In the industrial era,the emphasis was on mass production to drivedown costs. Customers benefited from lowprices, but were stuck with one-size-fits-allproducts. In the post-industrial era, compa-nies can use information technology to"demassify" products and services (i.e., tailor

The Future of Assurance Services: Implications for Academia 121

them to the specific needs of market segments,and ultimately individual customers) whilestill keeping costs low. Once technology makesthis possible, competition makes it inevitable.The result is a huge shift in power fi-om pro-ducers to consumers. This power shift has re-structured entire industries, and it will likelydo so to the accounting profession as well. Ifany producer's goods and services are not de-signed to meet customers' changing needs andtastes, some other producer will provide a sub-stitute and take over the laggard's marketposition.

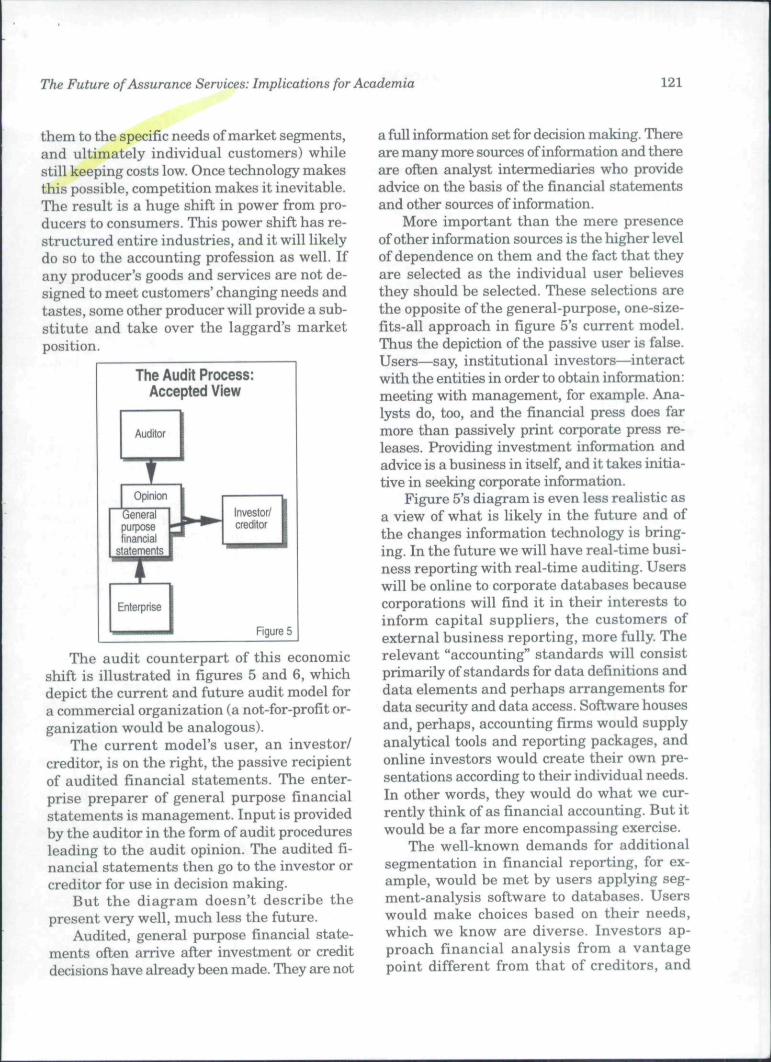

The Audit Process:Accepted View

Generalpurposefinancial

statements

Figure 5

The audit counterpart of this economicshift is illustrated in figures 5 and 6, whichdepict the current and future audit model fora commercial organization (a not-for-profit or-ganization would be analogous).

The current model's user, an investor/creditor, is on the right, the passive recipientof audited financial statements. The enter-prise preparer of general purpose financialstatements is management. Input is providedby the auditor in the form of audit proceduresleading to the audit opinion. The audited fi-nancial statements then go to the investor orcreditor for use in decision making.

But the diagram doesn't describe thepresent very well, much less the future.

Audited, general purpose financial state-ments ofi en arrive after investment or creditdecisions have already been made. They are not

a full information set for decision making. Thereare many more sources of information and thereare often analyst intermediaries who provideadvice on the basis of the financial statementsand other sources of information.

More important than the mere presenceof other information sources is the higher levelof dependence on them and the fact that theyare selected as the individual user believesthey should be selected. These selections arethe opposite of the general-purpose, one-size-fits-all approach in figure 5's current model.Thus the depiction of the passive user is false.Users—say, institutional investors—interactwith the entities in order to obtain information:meeting with management, for example. Ana-lysts do, too, and the financial press does farmore than passively print corporate press re-leases. Providing investment information andadvice is a business in itself, and it takes initia-tive in seeking corporate information.

Figure 5's diagram is even less realistic asa view of what is likely in the future and ofthe changes information technology is bring-ing. In the future we will have real-time busi-ness reporting with real-time auditing. Userswill be online to corporate databases becausecorporations will find it in their interests toinform capital suppliers, the customers ofexternal business reporting, more fully. Therelevant "accounting" standards will consistprimarily of standards for data definitions anddata elements and perhaps arrangements fordata security and data access. Software housesand, perhaps, accounting firms would supplyanalytical tools and reporting packages, andonline investors would create their own pre-sentations according to their individual needs.In other words, they would do what we cur-rently think of as financial accounting. But itwould be a far more encompassing exercise.

The well-known demands for additionalsegmentation in financial reporting, for ex-ample, would be met by users applying seg-ment-analysis software to databases. Userswould make choices based on their needs,which we know are diverse. Investors ap-proach financial analysis from a vantagepoint different from that of creditors, and

122 Accounting Horizons /December 1995

different investors take different approachesas well. Real-time database access with cho-sen analytical software would address thosedifferences.

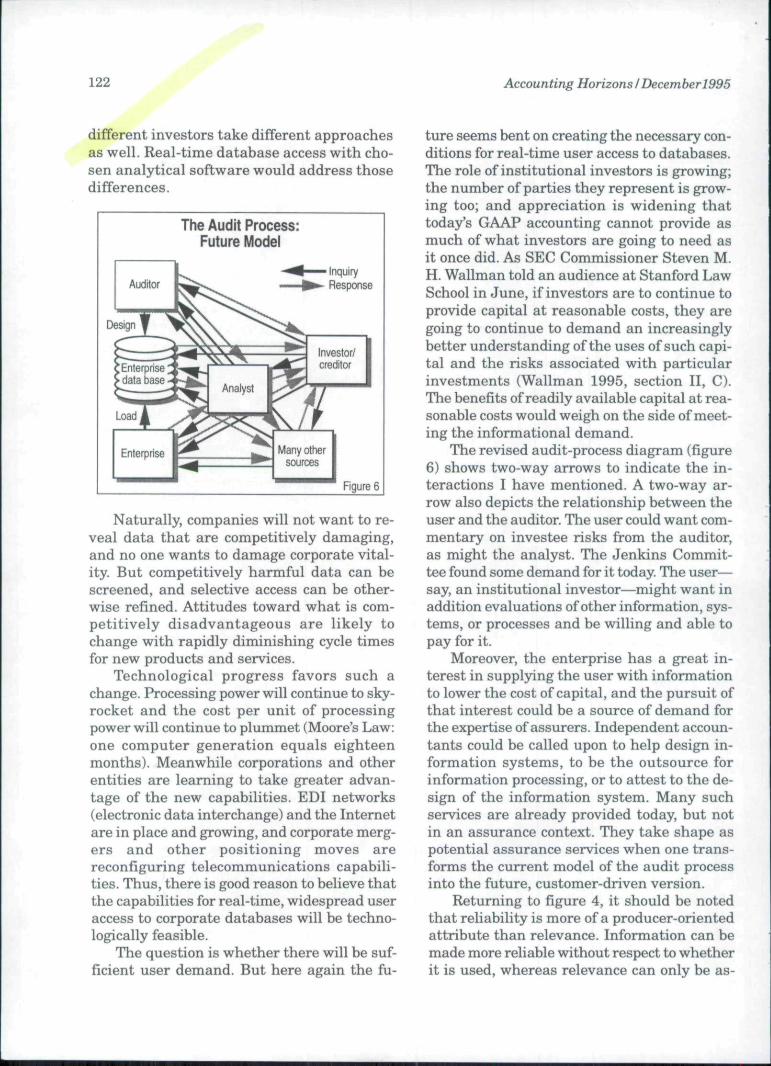

The Audit Process:Future Model

Auditor

Design

inquiryResponse

Investor/creditor

Many othersources

Figure 6

Naturally, companies will not want to re-veal data that are competitively damaging,and no one wants to damage corporate vital-ity. But competitively harmful data can bescreened, and selective access can be other-wise refined. Attitudes toward what is com-petitively disadvantageous are likely tochange with rapidly diminishing cycle timesfor new products and services.

Technological progress favors such achange. Processing power will continue to sky-rocket and the cost per unit of processingpower will continue to plummet (Moore's Law:one computer generation equals eighteenmonths). Meanwhile corporations and otherentities are learning to take greater advan-tage of the new capabilities. EDI networks(electronic data interchange) and the Internetare in place and growing, and corporate merg-ers and other positioning moves arereconfiguring telecommunications capabili-ties. Thus, there is good reason to believe thatthe capabilities for real-time, widespread useraccess to corporate databases will be techno-logically feasible.

The question is whether there will be suf-ficient user demand. But here again the fu-

ture seems bent on creating the necessary con-ditions for real-time user access to databases.The role of institutional investors is growing;the number of parties they represent is grow-ing too; and appreciation is widening thattoday's GAAP accounting cannot provide asmuch of what investors are going to need asit once did. As SEC Commissioner Steven M.H. Wallman told an audience at Stanford LawSchool in June, if investors are to continue toprovide capital at reasonable costs, they aregoing to continue to demand an increasinglybetter understanding of the uses of such capi-tal and the risks associated with particularinvestments (Wallman 1995, section II, C).The benefits of readily available capital at rea-sonable costs would weigh on the side of meet-ing the informational demand.

The revised audit-process diagram (figure6) shows two-way arrows to indicate the in-teractions I have mentioned. A two-way ar-row also depicts the relationship between theuser and the auditor. The user could want com-mentary on investee risks from the auditor,as might the analyst. The Jenkins Commit-tee found some demand for it today. The user—say, an institutional investor—might want inaddition evaluations of other information, sys-tems, or processes and be willing and able topay for it.

Moreover, the enterprise has a great in-terest in supplying the user with informationto lower the cost of capital, and the pursuit ofthat interest could be a source of demand forthe expertise of assurers. Independent accoun-tants could be called upon to help design in-formation systems, to be the outsource forinformation processing, or to attest to the de-sign of the information system. Many suchservices are already provided today, but notin an assurance context. They take shape aspotential assurance services when one trans-forms the current model of the audit processinto the future, customer-driven version.

Returning to figure 4, it should be notedthat reliability is more of a producer-orientedattribute than relevance. Information can bemade more reliable without respect to whetherit is used, whereas relevance can only be as-

The Future of Assurance Services: Implications for Academia 123

certained with respect to a particular decisionmaker faced with a particular decision.

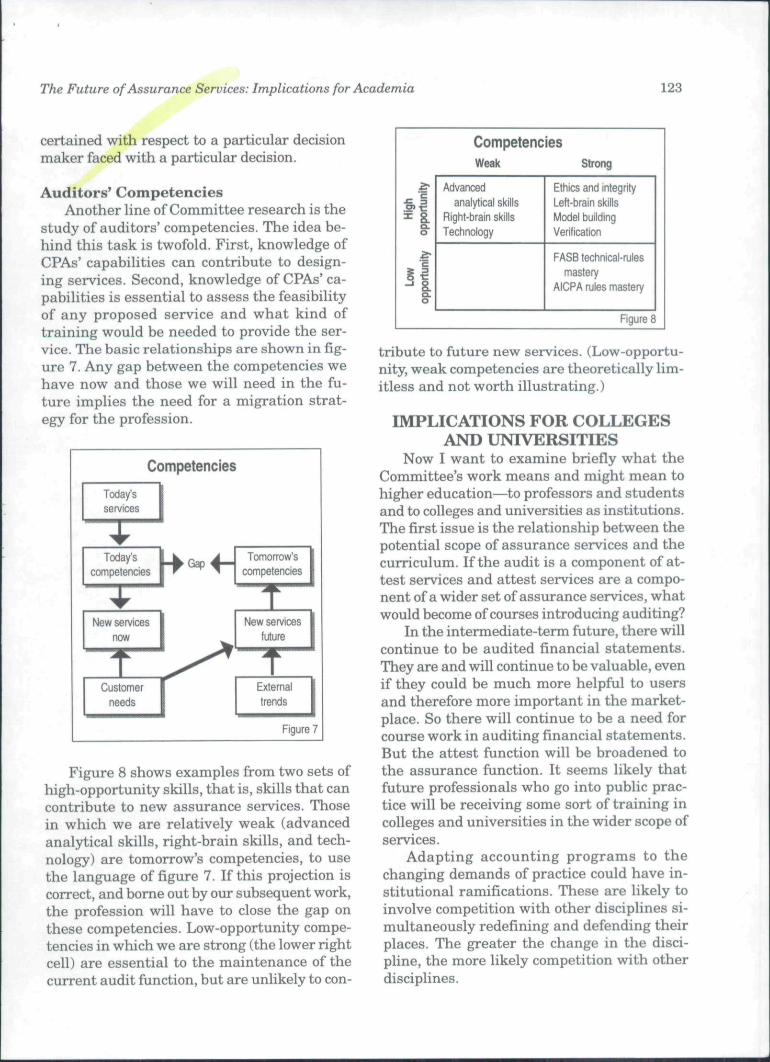

Auditors' CompetenciesAnother line of Committee research is the

study of auditors' competencies. The idea be-hind this task is twofold. First, knowledge ofCPAs' capabilities can contribute to design-ing services. Second, knowledge of CPAs' ca-pabilities is essential to assess the feasibilityof any proposed service and what kind oftraining would be needed to provide the ser-vice. The basic relationships are shown in fig-ure 7. Any gap between the competencies wehave now and those we will need in the fu-ture implies the need for a migration strat-egy for the profession.

Competencies

Today'sservices

Today'scompetencies

Tomorrow'scompetencies

1.New services

nowNew services

future

Customerneeds

Externaltrends

Figure 7

Figure 8 shows examples fi'om two sets ofhigh-opportunity skills, that is, skills that cancontribute to new assurance services. Thosein which we are relatively weak (advancedanalytical skills, right-brain skills, and tech-nology) are tomorrow's competencies, to usethe language of figure 7. If this projection iscorrect, and borne out by our subsequent work,the profession will have to close the gap onthese competencies. Low-opportunity compe-tencies in which we are strong (the lower rightcell) are essential to the maintenance of thecurrent audit function, but are unlikely to con-

CompetenciesWeak Strong

s.a.o

Advancedanalytical skills

Right-brain skillsTechnology

Ethics and integrityLeft-brain skillsModel buildingVerification

FASB technical-rulesmastery

AICPA rules mastery

Figure 8

tribute to future new services. (Low-opportu-nity, weak competencies are theoretically lim-itless and not worth illustrating.)

IMPLICATIONS FOR COLLEGESAND UNIVERSITIES

Now I want to examine briefiy what theCommittee's work means and might mean tohigher education—to professors and studentsand to colleges and universities as institutions.The first issue is the relationship between thepotential scope of assurance services and thecurriculum. If the audit is a component of at-test services and attest services are a compo-nent of a wider set of assurance services, whatwould become of courses introducing auditing?

In the intermediate-term future, there willcontinue to be audited financial statements.They are and will continue to be valuable, evenif they could be much more helpful to usersand therefore more important in the market-place. So there will continue to be a need forcourse work in auditing financial statements.But the attest function will be broadened tothe assurance function. It seems likely thatfuture professionals who go into public prac-tice will be receiving some sort of training incolleges and universities in the wider scope ofservices.

Adapting accounting programs to thechanging demands of practice could have in-stitutional ramifications. These are likely toinvolve competition with other disciplines si-multaneously redefining and defending theirplaces. The greater the change in the disci-pline, the more likely competition with otherdisciplines.

124 Accounting Horizons I December 1995

RESEARCH OPPORTUNITIESAcademic research could and should play

a major role in the way practitioners arriveat customer-driven services in the future. Thelong-standing issue over the relevance of aca-demic research on accounting and auditing topractitioners could become a thing of the past,hecause opportunities for research unmistak-ably needed by practitioners are now build-ing up like fast-flowing water arriving at adam. In many cases there is a one-to-one re-lationship between curriculum needs andthe research; in others, the curriculum needwill follow changes in practice aided by theresearch.

We need research in three basic areas:• Who are the potential customers for assur-

ance?• What are their assurance needs?• What technologies are needed to meet

those needs?Too little is known about the customers

and potential customers for assurance ser-vices. They are decision makers by definition,and the more obvious of them have been atleast interviewed by our Committee and bythe Jenkins Committee. But study commen-surate with the importance of the question—the full range of potential customers and theneeds of their decision-making processes—^hasnot been done. A broader range of identifiedcustomers and customer needs would affectapproaches to adapting curricula as well asassist practitioners in adapting to the future.

Following is a partial list of customerneeds that would affect the curriculum andthose that would present areas for research:Curriculum:• Decision model selection and specification.• Information requirements.• Information sourcing.• Information analysis and interpretation.• Implementation of decisions.• Outcome feedback.Research:• Relevance enhancement.• Decision processes and how they will

change under the influences of informa-tion technology.

The curriculum set is based on the se-quence of activities in decision making, A de-cision maker needs a decision model suited tothe demands of the decision. And based on thatmodel and the decision to be made, there willbe information requirements. When those re-quirements are defined, the information mustbe obtained, which means identifying sourcesand access, and also may mean cuttingthrough excess to isolate only what is needed.Once obtained, the information must be ana-lyzed. Finally, decisions made must be imple-mented, and feedback on outcomes should beobtained to refine the decision-making and in-formation-acquisition processes.

The counterpart research includes decisionprocesses and how they change, which would cre-ate input to refine the related curHcular segment.

We certainly need to understand as fullyas possible the range of needs for relevanceenhancement. This includes types of informa-tion needed because they are relevant or addrelevance, but would be more embracing. Sys-tems should be designed to capture and re-port the relevant, for example, and to avoidtime-consuming deluges of the irrelevant. Thisresearch would also create input to refine re-lated curricular segments.

Following is a partial list of the curricularand research opportunities on technologies tofulfill customer needs.Curriculum:• Communications.• Real-time focus.• Meeting customer needs on demand.• Systems.• Reliability by design.Research:• New modes of reliability enhancement:

• By design, not by inspection and correc-tion.

• Multivariate-triangulation and elec-tronic-data-interchange approaches.

• Information dual.• Massive redundancy.

• Real-time auditing.There is certainly a great need for research

on new modes of reliability enhancement andreal-time auditing.

The Future of Assurance Services: Implications for Academia 125

Reliability enhancement through designhas precedents, hut its future lies before it.Today we audit systems very much by inspec-tion of their performance. We evaluate gen-eral controls, which includes systems devel-opment, but systems-development proceduresmindful of inspection controls are not the sameas building reliability into design so that in-spections play a far smaller role—ideally, aremade unnecessary. They would be replaced bypreventive controls embedded in transactionprocessing systems. Auditing focused on in-spection controls and system outputs wouldbe replaced by auditing design and preventivecontrols directly. This is analogous to theprogress in quality management in manufac-turing, where quality assurance based on in-spection and rework has been largely replacedby the redesign of processes and products toeliminate the sources of defects.

Preventive controls are particularly impor-tant if we are to realize the potential of elec-tronic commerce. The dependence on systemintegrity in such a world was nicely capturedby Kevin Kelly (1995,208) when he wrote: "Anonline civilization requires online anonjrmity,online identification, online authentication,onhne reputations, online trust holders, onlinesignatures, online privacy, and online access."

A good design would employ devices tothwart intruders breaking security and oth-erwise violating the integrity of the system.Sensors can detect changes in physical condi-tions, and software agents can identifychanges in data and files that trigger notifi-cations to designated parties. They will playa great role not only in reliability enhance-ment through design, but also in real-timeauditing.

Sensors and software agents will monitortypes of transactions and data based on pre-determined ranges of acceptable transactiontypes and values. When the ranges are ex-ceeded, exception reports will be sent to theauditor for immediate investigation. Sensorsand software agents will also be important inassuring the reliability and integrity of infor-mation systems other than those for financialreporting. They can be particularly important

in executive decision making, because key riskand performance Indicators can be monitoredby sensors and software agents, with reportsprovided at predefined tolerances. To takesome mundane examples, cycle-time in-creases, levels of foreign currency exposure,excessive reject rates, cost overruns, and dis-appointing customer satisfaction ratings couldall be detected as promptly as managementbelieves is necessary for corrective action.

Our research on customer needs hasturned up some strong interest in monitoringand reporting these kinds of entity risk fea-tures. The interest illustrates awareness of theincrease in the volatility of the business envi-ronment. The stakes in successfully adaptingto the changing environment are growing, andthose responsible for guiding organizationsknow it. The environmental changes increasethe potential for new information services andadd to the challenge in performing both tra-ditional and newer services.

Consider an example of a challenge to re-liability enhancement that calls for research:complications caused by short-lived, joint busi-ness efforts.

More and more organizations are joininghands to perform mutually advantageoustasks from research and development to pro-duction and marketing. Variously designatedby the catchall term strategic alliances orcalled joint ventures, cooperative or collabo-rative relationships, technology swaps, andstill other names, they vary in their legal andeconomic characteristics. Many of these rela-tionships are intended to overcome potentialbarriers to doing business beyond the bordersof one's country; others are designed to pooldifferent competencies or other economic ad-vantages, such as licenses; and still others arecustomer-supplier relationships so close thetwo virtually share business objectives. Someare long-term relationships, others compara-tively brief. The increasing importance ofknowledge work in the evolving economy to-gether with advancing information technologyis likely to facilitate more short-term alliances,where organizations team for limited objec-tives in the near-term and dissolve the bond

126 Accounting Horizons/Decemberl995

when the objectives are achieved. Several sub-sidiaries of a single firm could be engaging insuch affiliations, weaving in and out of them.

As these forms proliferate, we will need abetter grasp of what they mean for account-ing, auditing, and other assurance services.The economic potential of an entity createdfor the express purpose of bringing togetherexpert personnel and technologies cannot beassessed effectively by focusing on the histori-cal cost of its physical assets. For some of theentities, arm's length transactions could be theexception rather than the rule. The definitionof the reporting entity could be blurred, bear-ing a less direct relationship to the legal en-tity, and the notion of going concern could beirrelevant when organizational goals areshort-term.

However, the closer relationships betweenentities that will develop as we move deeperinto the information age will also bring newopportunities for audit evidence. Project your-self, for a moment, into the coming era of real-time reporting, routine data interchangesamong customers and suppliers, and elec-tronic money. On the one hand, it will be diffi-cult to audit without greater knowledge of thevarious business parties connected to theauditee. On the other hand, the very level ofconnectedness would be a potential source ofevidence. The auditee would be located in aneconomic matrix, with its peers and partnerson other axes. Relationships between data onperformance and conditions for these partieswould he a form of audit evidence, achievingvalidity by triangulation.

Creating this kind of audit evidence wouldbe very challenging, but it is also potentiallyvery powerful, combining elements of what wenow call analytical review and confirmation.At this time it is an unexplored opportunity.

Further in the future is the "informationdual"—real-time information versions of re-porting entities. They will be real-time be-cause they will change as the entity changes.They will be constructed by algebraic com-puter languages and data from sensors andsoftware agents that monitor all features ofthe entity.^

Demand for the information dual willcome from its "real-time dials on the business"and its capacity to be deliberately modifiedin order to determine the effect of the change.Thus it will be possible for entities to try outdifferent policy scenarios and learn muchmore than they can today from their strate-gic planning. And because it is in real time,the information dual could be used to test tac-tical decisions and risk sensitivities as well.In addition, the information dual will allowmonitoring on a level more profound than isdone now, because the relationship betweenchanges in processes and changes in the or-ganization will be available. This too will con-tribute to demand.

Despite its potential advantages and thedemand they are likely to generate, the infor-mation dual will not spring full-blown on thebusiness community as soon as the technol-ogy reaches some threshold. Piecemeal intro-duction is almost inevitable. There will be in-formation duals for individual processes be-fore there are information duals for wholeentities, and there will be information dualsfor physical processes before they are con-structed for knowledge-work processes. Nev-ertheless, the information dual could one dayreplace GAAP assertions as the deliverable forfinancial reporting. Most of the advantagesthat could establish managerial demand forthe information dual would also make it prizedby investors. Whether or not that happens,any potential user of an information dualwould want to know whether it is reliable orin any way fi-audulent.

We need research on the information dualand its implications for attest work. What kindof contrihution could independent accountantsmake to users of the information dual? Theymight help to design information duals andmake them secure and auditable. When au-diting them, accountants would have to verifythe algebraic bases for the information dualsor the systems that developed and installedthem and to evaluate the validity and effec-

2 The information dual is discussed in more detail inElliott (1994a. 109-110).

The Future of Assurance Services: Implications for Academia 127

tiveness of the array of sensors and softwareagents. An important service might be toevaluate the way in which the informationdual was used—e.g., whether appropriate pro-cedures were in place to assess and follow-upon the findings available from the informa-tion dual. These kinds of tasks would call fora new, high level of understanding of comput-erization and measurement, for the informa-tion dual would effectively be an ongoing se-ries of measurements of the entity's processes,a series so rapid that it is available in realtime.

The realization of the information dual andaccompanying assurance work is more distantthan other potential features of the audit/as-surance environment, but research couldmake that day sooner.

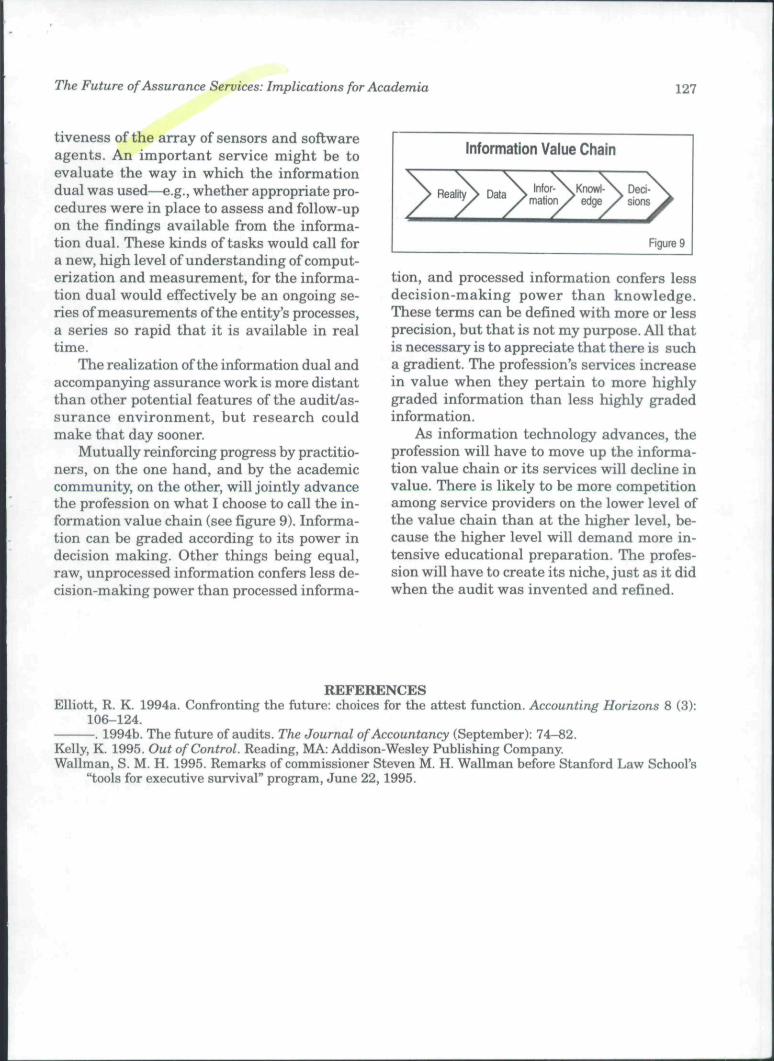

Mutually reinforcing progress by practitio-ners, on the one hand, and by the academiccommunity, on the other, will jointly advancethe profession on what I choose to call the in-formation value chain (see figure 9). Informa-tion can be graded according to its power indecision making. Other things being equal,raw, unprocessed information confers less de-cision-making power than processed informa-

Information Value Chain

Rgure 9

tion, and processed information confers lessdecision-making power than knowledge.These terms can be defined with more or lessprecision, but that is not my purpose. All thatis necessary is to appreciate that there is sucha gradient. The profession's services increasein value when they pertain to more highlygraded information than less highly gradedinformation.

As information technology advances, theprofession will have to move up the informa-tion value chain or its services will decline invalue. There is likely to be more competitionamong service providers on the lower level ofthe value chain than at the higher level, be-cause the higher level will demand more in-tensive educational preparation. The profes-sion will have to create its niche, just as it didwhen the audit was invented and refined.

REFERENCESElliott, R. K. 1994a. Confronting the future: choices for the attest function. Accounting Horizons 8 (3):

106-124.. 1994b. The future of audits. The Journal of Accountancy (September): 74-82.

Kelly, K. 1995. Out of Control. Reading, MA: Addison-Wesley Publishing Company.Wallman, S. M. H. 1995. Remarks of commissioner Steven M. H. Wallman before Stanford Law School's

"tools for executive survival" program, June 22, 1995.