Embed Size (px)

Citation preview

© 2012 The Philadelphia Real Estate Council

Philadelphia Real Estate CouncilPhiladelphia Real Estate Council

White Paper by Robin BaroneWhite Paper by Robin Barone

November 2012

The Foreign Capital The Foreign Capital The Foreign Capital Marriage: Marriage: Marriage:

Prenuptial ConsiderationsPrenuptial ConsiderationsPrenuptial Considerations

© 2012 The Philadelphia Real Estate Council

Author Robin Barone is a real estate finance and investment professional. She has over 10 years of experience in capital strategies for REITs, real estate funds, and management companies. Ms. Barone holds an M.B.A. from INSEAD, an M.S. in Real Estate Investment from NYU, and a B.A. in Mathematics and Urban Studies from the University of Pennsylvania, where she completed an Honors thesis on “Housing Conversion as a Redevelopment Strategy in Cities.” Ms. Barone is an avid traveler, skier, and writer who has visited over 42 countries, with many adventures documented on her travel website. She resides in New York City and serves as an adjunct instructor at NYU’s Schack Institute of Real Estate. She can be reached at:

D uring the 10-plus years I have worked in real estate finance in New

York City, I have seen numerous waves of foreign capital enter and

leave the U.S. real estate market. I have seen Japanese real estate

investment replaced by German capital, followed by Irish, Korean, and most

recently Chinese investment dollars. We live in an increasingly interconnected

world; even though real estate and its operations are a local matter, fundraising

has become a global endeavor. Independent and institutional investors have

more choices than ever when it comes to investing in foreign real estate markets.

Since the United States receives approximately one-third of global real estate

investment, foreign investors are a capital source that cannot be ignored.

International investors have long regarded the US as the leading destination for

foreign capital due to its stability, secure returns, and consistent capital

appreciation. Appetite for investment in US debt and equity has increased year

after year. In the most recent international survey conducted by AFIRE

(Association of Foreign Investors in Real Estate) and the University of

Wisconsin, respondents identified the US as their favorite choice among

international real estate markets.

The Foreign Capital Marriage:

Prenuptial Considerations

By Robin Barone

2

Country providing the most stable and secure real estate investments (Source: AFIRE, 2011)

© 2012 The Philadelphia Real Estate Council

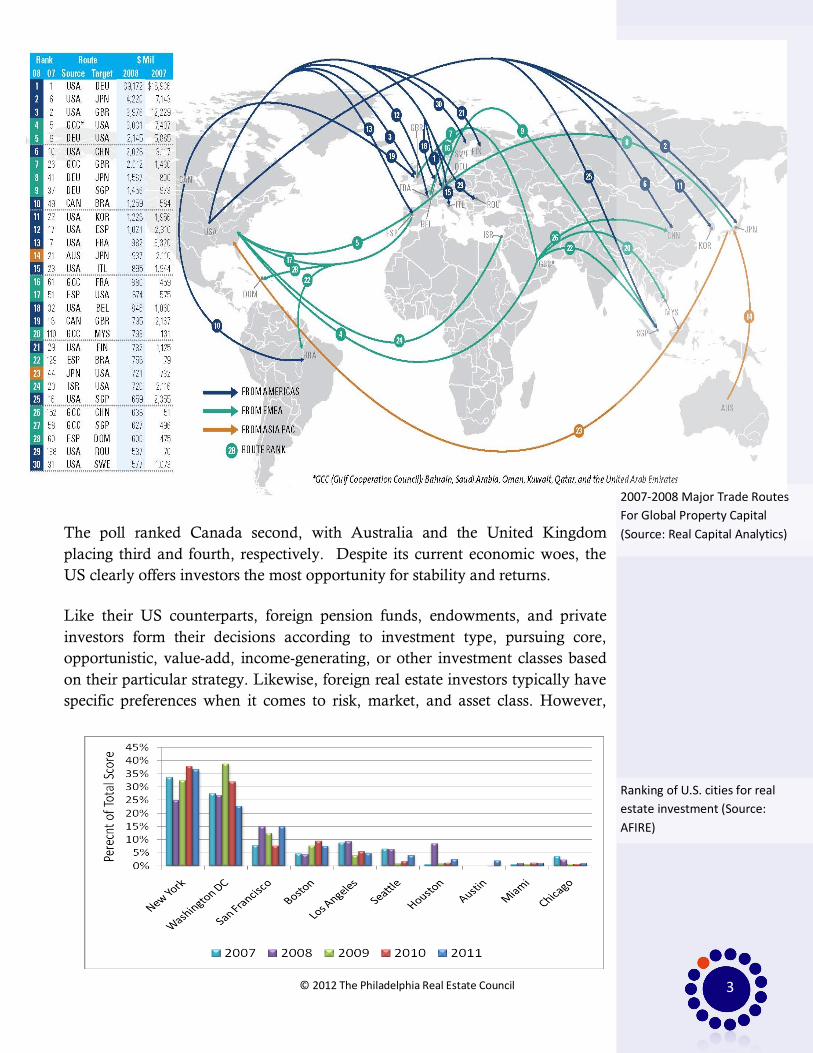

The poll ranked Canada second, with Australia and the United Kingdom

placing third and fourth, respectively. Despite its current economic woes, the

US clearly offers investors the most opportunity for stability and returns.

Like their US counterparts, foreign pension funds, endowments, and private

investors form their decisions according to investment type, pursuing core,

opportunistic, value-add, income-generating, or other investment classes based

on their particular strategy. Likewise, foreign real estate investors typically have

specific preferences when it comes to risk, market, and asset class. However,

3

2007-2008 Major Trade Routes

For Global Property Capital

(Source: Real Capital Analytics)

Ranking of U.S. cities for real

estate investment (Source:

AFIRE)

© 2012 The Philadelphia Real Estate Council

their approach to investment opportunities may differ from Americans’

according to cultural expectations or the maturity of their own financial system.

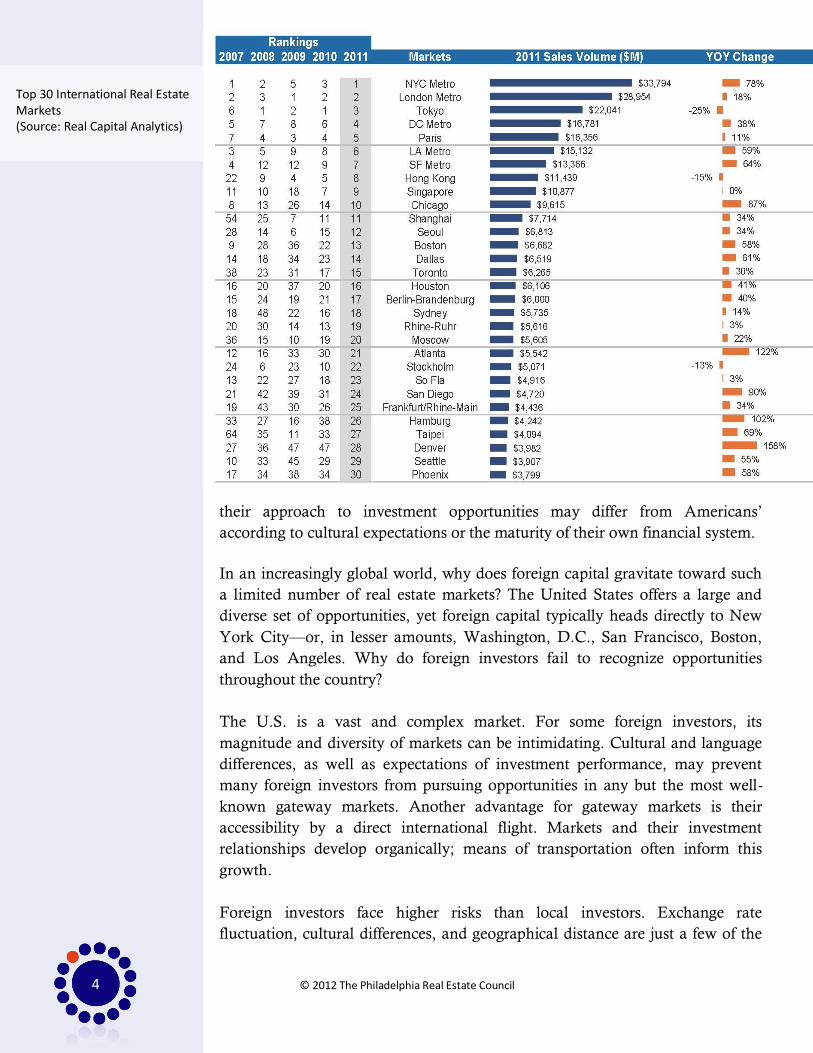

In an increasingly global world, why does foreign capital gravitate toward such

a limited number of real estate markets? The United States offers a large and

diverse set of opportunities, yet foreign capital typically heads directly to New

York City—or, in lesser amounts, Washington, D.C., San Francisco, Boston,

and Los Angeles. Why do foreign investors fail to recognize opportunities

throughout the country?

The U.S. is a vast and complex market. For some foreign investors, its

magnitude and diversity of markets can be intimidating. Cultural and language

differences, as well as expectations of investment performance, may prevent

many foreign investors from pursuing opportunities in any but the most well-

known gateway markets. Another advantage for gateway markets is their

accessibility by a direct international flight. Markets and their investment

relationships develop organically; means of transportation often inform this

growth.

Foreign investors face higher risks than local investors. Exchange rate

fluctuation, cultural differences, and geographical distance are just a few of the

4

Top 30 International Real Estate Markets (Source: Real Capital Analytics)

© 2012 The Philadelphia Real Estate Council

Why do foreign

investors prefer certain

markets? How do their

own cultures and

financial systems

influence these

preferences?

1. See Appendix, pp 21-22.

challenges international investors face when exploring an investment

opportunity in the U.S. To help resolve these challenges and open more of the

country to foreign investment, Americans must educate foreign investors and

highlight the opportunities in secondary markets. This is a daunting but

important endeavor.

To this end, it is essential to understand potential investors’ backgrounds. Why

do foreign investors prefer certain markets? How do their own cultures and

financial systems influence these preferences? Why do some investors prefer

long-term appreciation while others seek current yield? American property

owners, investment managers, and other real estate professionals must

understand the perspectives of foreign investors if they hope to see foreign

capital in their market.

Europe

For the past several years, Europe has produced ominous headlines and

recurring questions: Will Greece default? Will Germany support continued

bailouts? Will the economic entity known as the European Union even survive?

Though Germany continues in its role as the region’s economic driver, the

British pound remains a safe haven for capital, and other European nations

maintain their liquidity, member nations like Greece become increasingly

worrisome.

Investment opportunities in Europe are similar to those in the United States.

Europe’s markets are well developed and, under normal circumstances, its

capital markets supportive of transactions. Moreover, European investors

examine opportunities within an institutional framework and conduct due

diligence in a manner similar to that of U.S. investors.

In Real Capital Analytics’ country-by-country summary of foreign capital

invested in the U.S., European investors demonstrate the greatest foreign

commitment to U.S. real estate, both in annual amount and longevity as

investors.1

There are several reasons for this. The primary reasons are

geographical proximity and the historical ties between Europeans and

Americans. Not only is the U.S. a former British colony, it developed and grew

through extensive immigration from European countries at the turn of the

Twentieth Century. Many Europeans are familiar with U.S. cities and regions.

Because many European banks have offices in the U.S., there is a great deal of

5

© 2012 The Philadelphia Real Estate Council

2. Michael Atkins, MLA Risk

Advisory.

3. Guy Benn, Savills US..

familiarity with U.S. capital markets and their established processes.

Of all foreign investors, Europeans seem especially similar to Americans when

it comes to exploring investments and examining risk/return objectives.2

Europeans have an extremely “institutional” approach to their organization

structures and investment strategies. Extensive pools of potential investment

capital is held by insurance companies, pension funds and family offices.

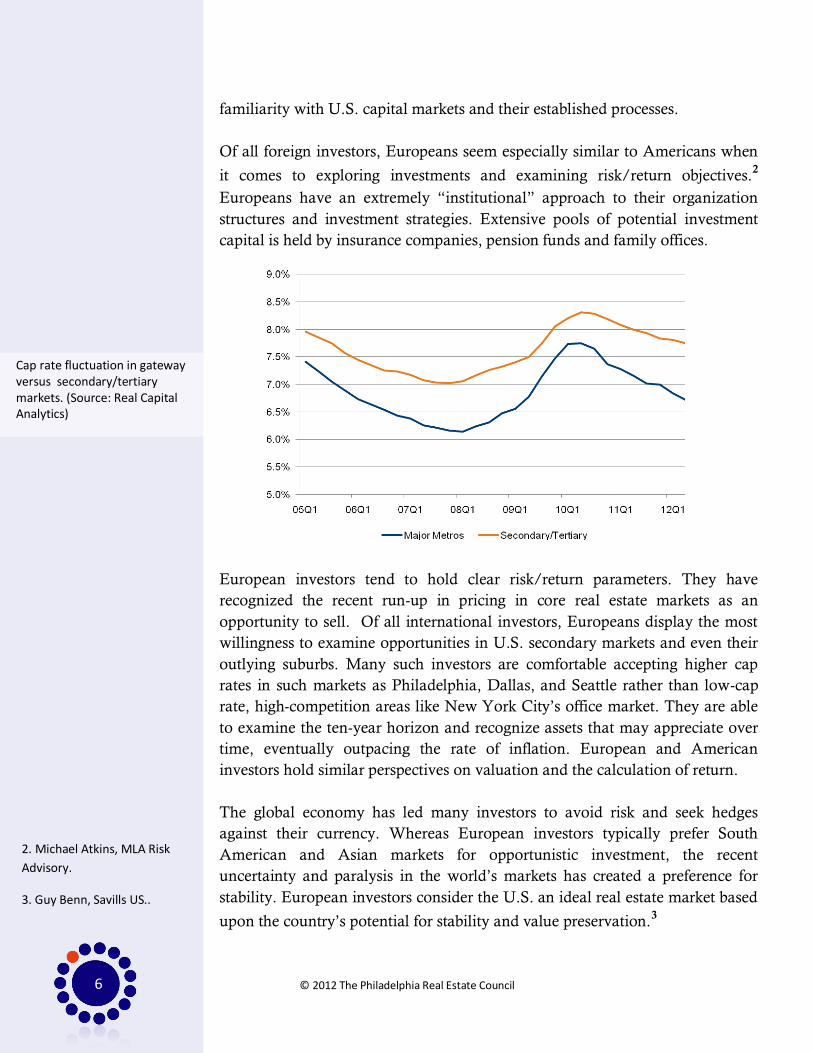

European investors tend to hold clear risk/return parameters. They have

recognized the recent run-up in pricing in core real estate markets as an

opportunity to sell. Of all international investors, Europeans display the most

willingness to examine opportunities in U.S. secondary markets and even their

outlying suburbs. Many such investors are comfortable accepting higher cap

rates in such markets as Philadelphia, Dallas, and Seattle rather than low-cap

rate, high-competition areas like New York City’s office market. They are able

to examine the ten-year horizon and recognize assets that may appreciate over

time, eventually outpacing the rate of inflation. European and American

investors hold similar perspectives on valuation and the calculation of return.

The global economy has led many investors to avoid risk and seek hedges

against their currency. Whereas European investors typically prefer South

American and Asian markets for opportunistic investment, the recent

uncertainty and paralysis in the world’s markets has created a preference for

stability. European investors consider the U.S. an ideal real estate market based

upon the country’s potential for stability and value preservation.3

6

Cap rate fluctuation in gateway versus secondary/tertiary markets. (Source: Real Capital Analytics)

© 2012 The Philadelphia Real Estate Council

Since they share the

United States’

institutional

background,

European investors

expect a certain degree

of transparency in

reporting the

performance of assets.

4. See Appendix A for data

provided by Real Capital Analytics

5. Conversation with Olivier

Thoral, AXA Equitable US

Of all European nations, Germany has the strongest presence in U.S. real estate

(followed by the British).4 Larger German organizations have established

locally operated investment platforms such as SEB, Jamestown, and

Paramount. German investors seem to prefer core assets, and their stable cash

flow, over opportunistic or development projects. They do, however,

understand the role of value creation and the effect of back-end appreciation on

a transaction’s returns. Holding a long-term perspective toward their

investments, they are typically more willing than other investors to consider

secondary markets.

As in investment, Europeans and Americans share many similarities when it

comes to underwriting real estate loans and transactions. Similar metrics and

due diligence procedures create a fairly consistent perspective among both

Europeans and Americans toward leads, valuations, and capital decisions.

Although European capital is typically institutionally organized, investment

decisions are largely consensus driven. Often, investment choices are made not

because they are the “best choice” (in retrospect) but simply the most popular.

Naturally, this democratic component of European investment may lengthen

transaction times.

Since they share the United States’ institutional background, European

investors expect a high degree of transparency regarding the performance of

assets. In exchange for this, they may be comfortable paying asset management

and performance fees. In general, European investors emphasize risk-adjusted

returns. They evaluate investments on a total return basis (income and

appreciation), not simply their current income.

Many larger European investors use subsidiaries as effective channels for U.S.

investment. As in the U.S., Europe’s insurance companies are a continuing

source of both real estate equity and debt. Given the lack of liquidity in many

European markets, a great deal of capital is focused on real estate loans in

Europe. Insurers such as AXA (French) and Zurich (Swiss) have recently

increased their presence in the United States and expanded their real estate

lending activity. AXA in particular prefers to invest in real estate as a sole

equity contributor. They will consider a variety of asset types and U.S. markets.

They also work with debt investments and hope to raise a debt platform as they

formalize their US real estate division.5

7

© 2012 The Philadelphia Real Estate Council

6. Conversation with Alexia

Gottschalch, Grovernor USA

7. “SEB ImmoInvest Real

Estate Fund to Be

Dissolved.” Reuters. May 7,

2012. Web.

Alternative organizations, such as U.K.-based Grosvenor, have chosen to buy

existing platforms with pre-established capital relationships in order to expand

their operations to the US.6 This serves as the quickest and most cost-efficient

way to deploy a significant amount of capital into real estate. Because such

firms as Grosvenor enjoy strong international reputations, they are able to focus

their energy on raising capital abroad while local real estate professionals

manage their portfolios domestically. Grosvenor found the greatest value lay in

acquiring local operations while leveraging its reputation to channel foreign

capital into the U.S. Not all European investors, however, possess Grosvenor’s

ability to raise and deploy such enormous sums of capital into a single

organization.

Because of Continental Europe’s boundaries and general lack of market growth,

European investors are especially proactive in their global real estate investment

strategies. Because of its stable markets, developed capital markets, and

established (and enforced) legal system, the U.S. has emerged as a safe harbor

for European capital—especially in light of the present state of Europe’s real

estate cycle. Since European real estate investments typically focus on long-

term stability and preservation of principal, as opposed to opportunistic

ventures, they show a preference for core markets.

The U.S. real estate market offers enough liquidity for European property

owners to sell assets and repatriate capital to the Continent. In many instances,

large investor groups, public and private, have invested heavily in U.S. real

estate during periods in which the strength of the euro exceeded that of the

dollar. Later, when the need arose, these banks and insurance companies could

sell these assets at a profit and replenish their home capital reserves.

Recently, sovereign and institutional investors have been forced to do this.

These European investors are now in the process of divesting foreign assets and

winding down portfolios, bringing capital home to strengthen their balance

sheets. German investors who entered and committed the greatest amount of

capital are among the leaders in this trend. Companies such as Bayern are

winding down portfolios, and lenders such as Eurohypo face questionable

futures. Major pension fund SEB has announced it will wind down its real

estate portfolios.7

8

© 2012 The Philadelphia Real Estate Council

8. “Mapping Global Capital

Markets.” McKinsey and

Company, 2009.

Middle East

A majority of the capital in the Middle East comes from its profits in the oil

industry. The region is unique in that a majority of the capital invested in real

estate is controlled by families and several major sovereign funds. In the Middle

East, it has long been recognized that the oil commodities in the area will

eventually be depleted. In preparation for that time, Middle Eastern investors

are searching for long-term, sustainable businesses in which to invest their

capital. Of all asset classes, they are most comfortable with “brick and mortar”

investments as well as “cash flow yielding” portfolios.

A distinguishing characteristic of investors from this region is the significant

effect of their faith on investment decisions. A majority of investors in this

region are Muslim and adhere to Islamic principles in their dealings. As such,

many of these investors deal exclusively with organizations, structures, and

opportunities that are compliant with Shariah law.

The first principal is to avoid paying or charging interest at all costs. The second

requires investors to avoid ventures that are unethical, either because of their

industry or financing structure. Shariah law does not allow investment in

business activities that include arms, alcohol, tobacco, pork, finance and

insurance, gambling, or biotechnology engaged in genetic experimentations.

Shariah-compliant financial structures may not have a debt-to-assets ratio over

30%, interest income greater than 5% of gross revenue, and accounts receivable

and cash comprising more than 50% of total assets.

Muslims represent a quarter of the world’s population, yet only 1% of

investment structures are Shariah compliant, according to a McKinsey study.

Still, there are numerous Shariah-compliant funds organized by Islamic

investors, international investment banks, and private American investment

managers. Most Islamic investors prefer to invest in structures that are officially

recognized as Shariah compliant or invest in consolidated platforms which they

believe represent their interests and respect their beliefs.

In the United States, real estate investment typically requires great amounts of

leverage. Because Shariah law restricts investors to low-leverage assets, Middle

Eastern investors tend to prefer asset classes such as multifamily and core office

properties. Unlike investors from other regions, they do not limit themselves to

any particular markets.8

9

© 2012 The Philadelphia Real Estate Council

Investors from this region consist of sovereign wealth funds and high net worth

individuals. Institutional organization and fiduciary concerns are minimal. A

distinguishing characteristic of these particular investors is that they are willing

to design and invest in their own management platforms. Historically, investor

groups such as Investcorp and Arcapita have taken the lead in the U.S. by

establishing significant, well-respected platforms. Now, other firms are

establishing management teams for Middle Eastern investments, both locally

and in the Middle East. These include Gold Oller in Philadelphia and the Abu

Dhabi Investment Authority’s self-made investment team.

The Abu Dhabi Investment Authority has expanded its activity in the US by

hiring Tom Arnold as its Head of Real Estate-Americas. ADIA has maintained

a strong roster of U.S.-focused real estate professionals. As the ADIA increases

its investment activity, it is unclear how much real estate activity it will

ultimately engage in. Because ADIA is not a U.S.-regulated pension fund or

transparent public entity, its commitments and investment capacity remain

unknown to outsiders. Kuwait Investment House and the Qatari Investment

Authority are two other sovereign investors demonstrating increased interest in

U.S. property.

Middle Eastern investors have shown a willingness to commit large sums of

capital to establishing investment platforms, understanding the long-term value

of consolidated asset management. For this reason, Middle Eastern investment

capital may be structured differently to avoid FIRPTA restrictions (see p. 16).

Often, a company or subsidiary in the U.S. will be established. The Middle

Eastern “parent” company will then lend it money. This “loan” is then invested

in real estate.

Although Middle Eastern capital appears institutionally organized, it does not

face public reporting requirements. Because of this lack of transparency, no one

really knows the extent of their capital available for foreign investment. One

thing, though, remains certain: as investors of Islamic background increase in

wealth, Islamic investment structures will become more prevalent, and

increasingly ideal, in U.S. markets.

10

© 2012 The Philadelphia Real Estate Council

9. Saminather, Nichola. “Australia’s $1.4 Trillion Pension Funds Chase Property Assets.” Bloomberg. May 14, 2012. Web.

Asia Pacific

Because of the vast geographical distance, among other reasons, there is less

investment between the U.S. and Asia relative to other international investment

partnerships. Although American culture is sprinkled throughout Asian markets

via Starbucks, McDonalds, and other brands, Asian investors sometimes

struggle to navigate the many complexities of U.S. real estate markets.

Although there is greater transparency among U.S. markets, the country’s

largest markets are similar in size to second- and third-tier cities in China,

Indonesia, and India. Asian and U.S. cities are not direct counterparts.

The U.S. faces a number of challenges when it comes to enticing investment

capital from the Asia-Pacific region. Besides being on opposite sides of the

world, these regions struggle with unfamiliar languages and market differences.

This lack of an established investment relationship between the U.S. and Asian

investors, some feel, contributes to a lack of familiarity with important cultural

nuances. Some feel Americans are more transparent and upfront while Asians

prefer to develop relationships over time. A cultural faux pas can terminate a

potentially fruitful business partnership before it has even begun.

Further, Asian banks have a minimal footprint in the U.S., allowing very little

exposure to U.S. opportunities. Also, real estate investment requires a large

capital commitment; without access to lenders familiar with their organization

and investment plans, Asian investors in U.S. real estate are disadvantaged

unless buying assets purely with their own capital.

The financial markets in Asia’s most developed economies offer a variety of

sophisticated investment opportunities for investors, which include pension

funds, family offices, and high net worth individuals. However, not all of these

investors have a clear understanding of the ways in which risk and return are

underwritten in U.S. markets. In this respect, there is a clear distinction

between the investment communities in Australia, Japan, and South Korea

versus those of emerging Asian economies such as China, India, and Indonesia.

Australian investors represent a strong, consistent source of investor capital due

to the nation’s Superannuation laws. “Superannuation” refers to Australia’s

mandatory public retirement scheme, which requires citizens to contribute to

their retirement. Australia’s retirement system is unique in its use of private,

compulsory contributions. Currently, employers are required to pay 9% of an

11

© 2012 The Philadelphia Real Estate Council

employee’s salary and wages into a superannuation fund. Between 2013 and

2020, this minimum contribution requirement will increase to 12%. Strict

government rules prevent access until individuals are older than 55. These

funds may be organized in a variety of ways: employer-run, retail trusts, self-

managed funds for small groups, and public sector employees’ funds.

Consolidated, these funds represent over $1.4 trillion of potential investment

capital.9

According to the Australian Prudential Regulatory Authority, these pension

funds have invested an annual average of 7% of their capital in direct real

estate and 3% in REITs. Their real estate focus is core properties with

sustainable income. With a limited supply of investment property

domestically, the majority of this capital goes abroad. Of these funds’

investments, up to 20% is allocated for North American opportunities,

including a minimum allocation for real estate.

Korean investors have proven experience in their investment in foreign real

estate, holding realistic expectations of return, especially when considering

core assets. Korean investors have also shown proficiency in valuing assets,

winning bids on acquisitions, and creating value in their investments. Many

Korean investors have shown a willingness to hold real estate assets for 7 to

10 years and prefer lower leverage than others, usually 50%-60%. Their

sources of capital include insurance companies, corporate pension funds, and

sovereign entities. Because many of their technology companies have

established successful U.S. subsidiaries, South Korea holds an established

business and investment relationship with the U.S. For many years, they have

observed the ways investments are made in the U.S. and have become

familiar with the nation’s different regions, markets, and asset classes.

Because of this experience, many South Korean investors have displayed

quicker decision-making when presented with real estate opportunities that

meet their requirements. Additionally, many Korean investors are educated

in the West, or hire U.S. residents to help them navigate the local real estate

market. Initially, they have shown a preference for direct investments, core

assets, and primary U.S. markets.

Some speculate that, in addition to stability, Korean investors prefer Western

gateway markets largely because of their prestige. However, as they have

expanded their presence in U.S. real estate investment, they have looked

beyond markets that come with “bragging rights,” investing also in second-

tier cities in their pursuit of long-term returns. Because of their ease in moving

Many of the major

technology

companies have

established successful

U.S. subsidiaries;

there is a history of

business and

investment in the U.S.

12

© 2012 The Philadelphia Real Estate Council

10. Henri Arslanian. UBS Hong Kong. May 17, 2012.

capital internationally, South Korean investors may consider a number of

major international cities at the same time before selecting a destination for

their funds. They have not shown any preference among the U.S., the U.K., or

nations in mainland Europe. Rather, they simply consider where their money

will earn the greatest return. Whether in New York City, London, or Paris, no

investment opportunity is a de facto preference. All opportunities are examined

within an international context.

Japanese investors have been active in U.S. real estate since the 1980s. They

first invested in flagship properties in primary markets, which were often

purchased at peak prices. As a result, many Japanese investors experienced very

public real estate losses as the market waned and liquidity diminished

(including record losses after the purchase of Rockefeller Center). Currently, the

Japanese prefer to invest in REITs for their high levels of transparency,

liquidity, and opportunity for appreciation. Japanese investors generally prefer

to commit larger sums of money to an investment platform, as in the Mitsubishi

Estate’s sponsorship of The Rockefeller Group.

When it comes to overall capital commitments in the U.S., however, China is

quickly exceeding its neighbors. A tremendous amount of capital belonging to

Chinese businesses sits offshore in US and Hong Kong currencies. Much of this

capital will not be brought back, since Chinese investors often prefer to keep

their international business profits abroad rather than repatriate funds. This

tendency reflects a desire for both diversification and capital preservation.10

Chinese investors will consider US real estate for several reasons. First, there is

a shortage of real estate investment opportunities in their country. Second,

many Chinese investors consider real estate, as an asset, to be a wealth creator.

They are especially comfortable investing in residential real estate, a more

common investment alternative in China. In investing in U.S. and similar

economies, these investors are deploying profits from their high-growth

economy into assets that are part of more mature economies. This strategy

highlights conflicting investment perspectives. While investors in mature

economies typically view real estate as a hedge against inflation, investors from

emerging economies will examine real estate opportunities as potential wealth

creators, sources of income rather than value-preservation.

Because Chinese investors are relatively new to international real estate

investment, they are still developing familiarity with U.S. markets. This general

lack of familiarity may limit Chinese investors’ in secondary markets. It also

13

© 2012 The Philadelphia Real Estate Council

leads to an abundance of caution. In Asia, businesses are often driven by close

relationships. Most businesses start as family businesses and evolve into larger

enterprises. The emphasis of relationships, of trust, informs Chinese

investment decisions as well. Regardless of an opportunity’s transparency, it

seems, many Chinese investors will spend a tremendous amount of time

getting to know the opposite party. They must develop mutual trust and

respect before any contract is signed.

When it comes to foreign investments, Chinese investors are cautious about

taxes, and may prefer strategies that limit tax liabilities. For example, they are

extremely conscious of the United States’ FIRPTA policy,11

and will often

make use of BVI (offshore) financial structures. In general, they seem to prefer

stand-alone investments over co-mingled funds.

Among international investors, Asian investors show a unique appreciation

for industrial and logistics-oriented properties. They like the high yield and

triple net structure many of these investments provide. However, their choice

of investment requires the “sex appeal” of a primary market, such as San

Francisco, New York, Washington D.C., Los Angeles, or Chicago. They also

seem to prefer holding assets directly rather than indirectly through shares in a

company or fund.

As a whole, Asian investors are “addicted to yield.”12

Many prefer REIT

structures for their high returns and liquidity. They also tend to value current

income over long term appreciation, and often choose to invest in high-profile

and well-located assets. Since the financial downturn of 2008, some Asian

investors have viewed the US as an opportunity for “distressed,” potentially

profitable assets. However, there is a great divide between such investors’

objectives and the actual real estate market. Often, Asian investors have

proven less successful in the U.S. real estate market, primarily because their

return requirements are incompatible with the dynamics of U.S. real estate.

11. Ian Gobin, Appleby Global. 12. Timothy Gan, DBC Bank.

14

© 2012 The Philadelphia Real Estate Council

13. See graphs on following page.

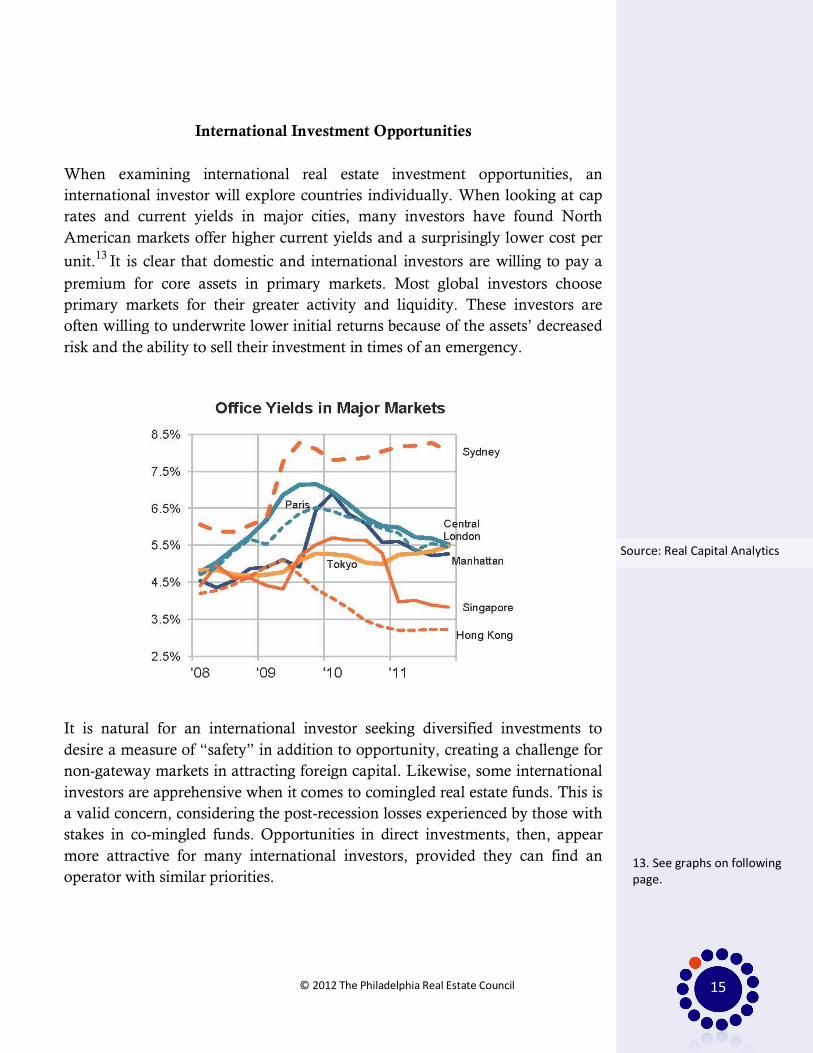

International Investment Opportunities

When examining international real estate investment opportunities, an

international investor will explore countries individually. When looking at cap

rates and current yields in major cities, many investors have found North

American markets offer higher current yields and a surprisingly lower cost per

unit.13

It is clear that domestic and international investors are willing to pay a

premium for core assets in primary markets. Most global investors choose

primary markets for their greater activity and liquidity. These investors are

often willing to underwrite lower initial returns because of the assets’ decreased

risk and the ability to sell their investment in times of an emergency.

It is natural for an international investor seeking diversified investments to

desire a measure of “safety” in addition to opportunity, creating a challenge for

non-gateway markets in attracting foreign capital. Likewise, some international

investors are apprehensive when it comes to comingled real estate funds. This is

a valid concern, considering the post-recession losses experienced by those with

stakes in co-mingled funds. Opportunities in direct investments, then, appear

more attractive for many international investors, provided they can find an

operator with similar priorities.

15

Source: Real Capital Analytics

© 2012 The Philadelphia Real Estate Council

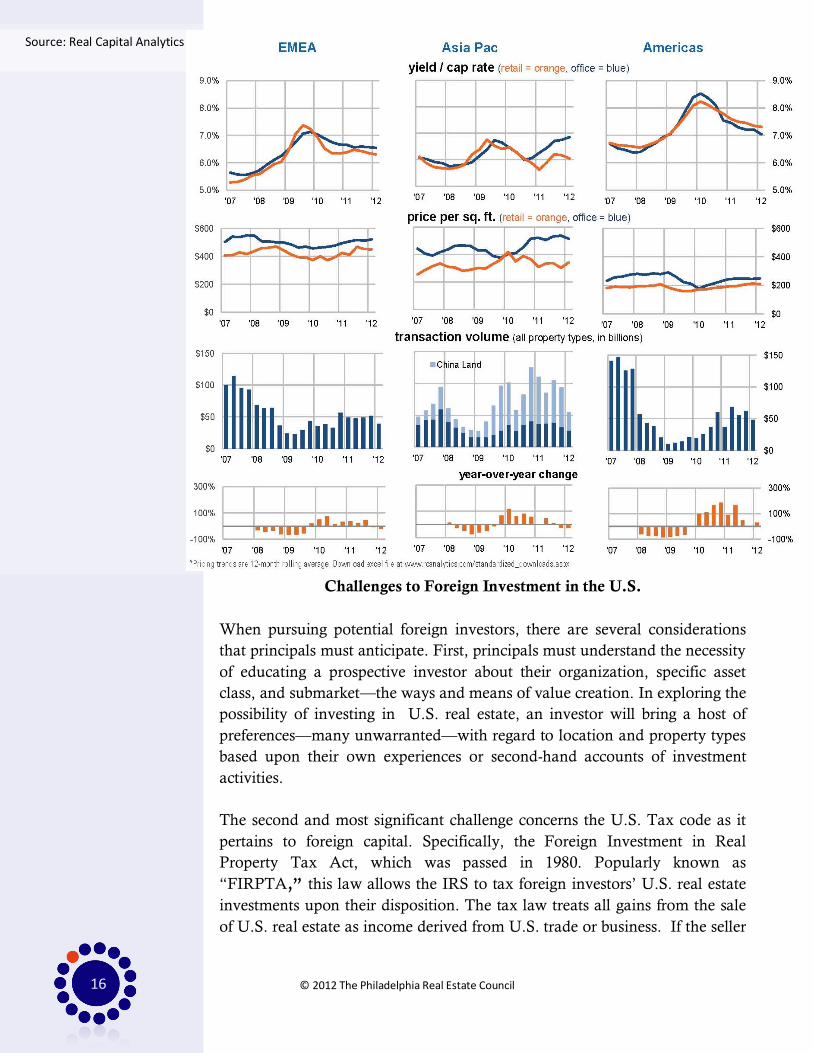

Challenges to Foreign Investment in the U.S.

When pursuing potential foreign investors, there are several considerations

that principals must anticipate. First, principals must understand the necessity

of educating a prospective investor about their organization, specific asset

class, and submarket—the ways and means of value creation. In exploring the

possibility of investing in U.S. real estate, an investor will bring a host of

preferences—many unwarranted—with regard to location and property types

based upon their own experiences or second-hand accounts of investment

activities.

The second and most significant challenge concerns the U.S. Tax code as it

pertains to foreign capital. Specifically, the Foreign Investment in Real

Property Tax Act, which was passed in 1980. Popularly known as

“FIRPTA,” this law allows the IRS to tax foreign investors’ U.S. real estate

investments upon their disposition. The tax law treats all gains from the sale

of U.S. real estate as income derived from U.S. trade or business. If the seller

16

Source: Real Capital Analytics

© 2012 The Philadelphia Real Estate Council

14. “FIRPTA Made Simple.” Association of Foreign Investors in Real Estate (AFIRE). 2011. Web.

of real estate in the U.S. is a foreign person, the buyer must withhold a tax

equal to 10% of the gross purchase price at sale. This law applies to all direct

and indirect real estate investment interests.14

International interests in land, buildings, timber, and minerals that are or have

been a US real property corporation are subject to taxation under FIRPTA.

Also subject to FIRPTA laws are foreign interests in REITs, sales of interests in

real property, and shares in certain U.S. corporations whose underlying assets

are real property.

The law specifically puts the burden of implementation on the buyer in a

transaction. It is not possible to avoid the U.S. tax on the sale of real property

by holding property indirectly (through U.S. corporations) and later disposing

of stock. Any ownership interest which possesses the right to share in any

appreciation in real assets’ value is subject to FIRPTA.

There are some exceptions. FIRPTA does not apply in the following situations:

A U.S. residence purchased for less than $300,000

The disposition of an asset that is not designated a U.S. Real Property

Interest (USRPI).

Interests of less than 5% in public or private companies, including REITs,

which have disposed of their interests in a taxable sale. (Although

partnerships, trusts, and REITs are not defined as “USRPI,” they are

nonetheless subject to FIRPTA laws.)

An interest in a position of credit is not subject to FIRPTA. Creditor

interests include mortgage interests and security interests in U.S. property

such as debt.

However, any right to share in the appreciation of the interests, or option for

ownership or leasehold interest in real property, faces U.S. tax liability under

FIRPTA. For example, a loan on real property that includes an equity kicker

would be subject to FIRPTA.

The presence of this law is unique to real estate among asset classes. In real

estate investments, properties are often purchased with 10% to 30% equity

investment. FIRPTA, however, adds an additional expense to the total capital

requirements of the transaction, posing a challenge to the feasibility of an

otherwise profitable deal.

17

© 2012 The Philadelphia Real Estate Council

Foreign investors most commonly reduce their tax burden by structuring their

investments with a “blocker.” A blocker is an entity organized as a U.S.

corporation and therefore subject to U.S. corporate taxes. The corporation

shields investors from U.S. income taxes. Additionally, foreign investors do

not need to file a direct U.S. tax return or pay a branch profits tax. Under

these circumstances, the investor receives only dividend income (or interest).

If the blocker is organized in the U.S., income received by the corporation

will be taxed at the minimum rate of 35% plus applicable state taxes. The

blocker corporation may, however, be subject to FIRPTA taxes on the sale of

shares in the future.

In order to justify the onerous taxes associated with FIRPTA, and to generate

sufficient returns to offset their costs, foreign investors must be willing to

deploy significant amounts of capital. Organizations such as AFIRE actively

lobby for the repeal or revision of this tax law. At the very least, AFIRE hopes

to reduce the tax burden placed on foreign investors’ interest in U.S. real

estate. Repeal or revision of this law would significantly boost the flow of

capital into the U.S. Until then, this law remains the core impediment to

solidifying the United States’ status as a “safe haven” for global real estate

capital.

Nonetheless, it is possible to navigate this process with extensive legal and tax

advice. As a result of its high barrier to entry (in terms of organizational

costs), foreign investment in U.S. real estate is limited to two kinds of

investors. The first kind is willing to invest extremely large amounts of capital,

thereby diluting the high cost of investment. The second type pursues

extremely opportunistic investments and risk-adjusted returns. Despite these

hurdles, foreign capital remains committed to establishing and increasing its

presence in the U.S.

Following 9/11, other federal regulations created new challenges and

complications in foreign investment. For instance, the so-called “Know Your

Customer” rule in the Patriot Act adds paperwork to the investment process,

a complication that sometimes scares away potential investors.15

“FATCA,”

on the other hand, requires foreign financial institutions to enter into an

agreement with the U.S. Treasury to perform due diligence and account for

U.S. financial investments owned by foreign entities.16

Although these challenges can be overcome, they create an increased burden

on organizations that are often already under-staffed. The time spent in

15. Plotkin, Mark E. and B.J. Sanford. “Patriot Act: The Customer’s View of ‘Know Your Customer.’” Bloomberg Corporate Law Journal. 2006. 16. “Complying with FATCA: Eleven Key Challenges.” Ernst & Young, 2011. Web.

18

© 2012 The Philadelphia Real Estate Council

One of the key lessons

of this article is,

Foreign capital may

not be an appropriate

choice for you and

your business.

developing a relationship, educating the investor, and negotiating toward

mutually agreeable terms can be onerous and often unsuccessful. Many

investors, however, have overcome these challenges. The ways and means in

which they do so are largely influenced by the foreign investor’s national origin

and the means by which the capital was raised.

The Foreign Capital “Marriage”

Thanks to Bloomberg and a host of other resources, data on individual financial

markets is continuously available, allowing investors—both individual and

institutional—to make judgments and assess trends while the other half of the

world sleeps. How will capital respond? Where will it go? The world economy

seems increasing uncertain and increasingly volatile. In forming decisions,

modern investors must sift through an overwhelming amount of real-time

international data. The decision to buy and sell is time-consuming, costly, and

intimately involved—like a marriage. Further, real estate investors (whether

pursuing acquisition, disposition, development, or management), working in

such a big-ticket industry, struggle constantly with liquidity.

In comparing international capital to domestic capital in U.S. real estate, there

are several noticeable trends. First, European investors are gradually pulling

back their commitments, as they need to shift additional capital into European

matters. Second, Asian investors are increasingly invested in U.S. real estate,

and have, in the last five years, displaced European capital as the most

influential foreign region in U.S. real estate. It should be interesting to follow

the effects their particular focuses and biases have as a capital source.

Despite the high amount of foreign capital invested in the U.S., this only

accounts for approximately 7% of the nation’s real estate investment. Foreign

capital is present, but far from overwhelming the market.

How does an owner or operator gain the attention of foreign investors? One of

the key lessons of this article is, Foreign capital may not be an appropriate

choice for you and your business. Remember, domestic sources of private and

public capital are extensive, and many investors and institutions are gradually

increasing their allocations to the investment class. When examining the

perspective, risk tolerance, return expectations, and other attributes of foreign

investors, an operator needs to consider whether the extra time and effort to vet

and attract international capital will lead to a mutually successful relationship.

19

© 2012 The Philadelphia Real Estate Council

As 2012 comes to a close, uncertainty in the U.S. continues. What decisions

and regulatory changes will we see in President Obama’s second term? Will

Republicans’ congressional influence affect or simply stall the nation’s

economic growth? Investors wonder, Will the E.U. get a divorce? Will the

Chinese RMB appreciate? What role will countries like Brazil and Poland

play as their economies grow?

For decades, the U.S. was the poster child for economic success. The financial

turmoil of 2008-2009 dented the nation’s reputation as a safe haven for

foreign capital. But as China’s economy slows and becomes less transparent,

and Europe’s economic fate becomes increasingly uncertain, the U.S. is well

positioned to rebuild its reputation as a stable investment destination.

When considering foreign capital, a principal needs to identify potential

investors whose strengths and competitive advantages appropriately match

the principal’s own interests. Also, it is very important to select sources of

capital that will not interfere with future deals. Sophisticated owners

understand the importance of diversity in capital sources; the constraints of

current involvements must not hinder involvement with future investors.

Regardless of the source, the risks and potential benefits of any such

relationship must be considered with care. In a strange way, working with

investors in real estate is a sort of marriage. As in any marriage, it is best to

choose a spouse whose values and goals are aligned with your own.

20

© 2012 The Philadelphia Real Estate Council

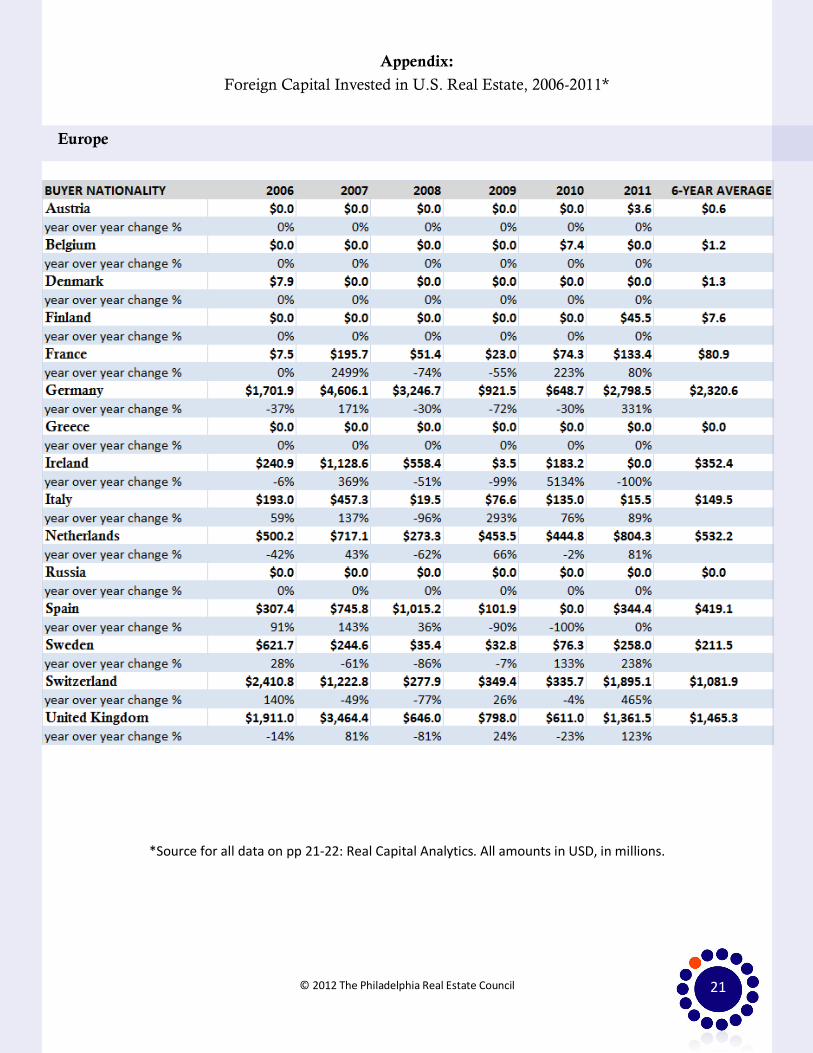

Appendix:

Foreign Capital Invested in U.S. Real Estate, 2006-2011*

21

Europe

*Source for all data on pp 21-22: Real Capital Analytics. All amounts in USD, in millions.

© 2012 The Philadelphia Real Estate Council

22

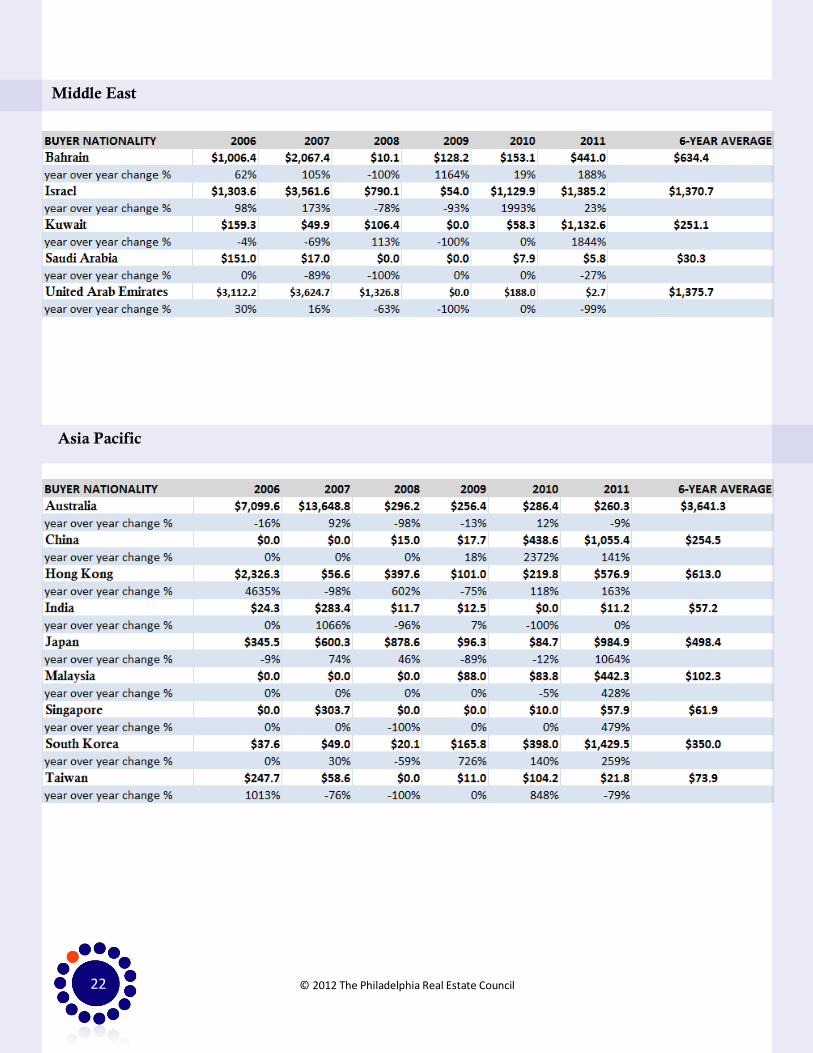

Middle East

Asia Pacific

© 2012 The Philadelphia Real Estate Council

Acknowledgments

This article and its research would not have been possible without the generous

assistance of the following institutions and individuals:

Europe: Michael Atkins, Guy Benn, Seth Schumer, Amaury de Parcevaux, Olivier

Thoral, and Ian Gobin

Asia: Gary Hollis, Henri Arslanian, Pierre Hennes, Patrick Turner, Nick Kim,

Nick Delf, Richard A. Johnson, Heather Grayson, Tim Murphy, Cheryl Sing,

Damian Manolis, Graham Mackie, Victor Ong, Jonathan Ng, Kobus van der

Wath, Tony Soh, Daniel McDonald, Stewart Aldcroft, Timothy Gan, David

Malone, Alex Jaffrey, and Jim Lindros.

Middle East: Michael Dowling, Enoch Lawrence, Richard Oller, Jake Hollinger,

and

Bruce Gelman.

Data provided with permission from the following organizations:

Association of Foreign Investors in Real Estate (AFIRE): Jim Fetgatter, Lexie

Miller

Real Capital Analytics: Bob White, Doug Murphy

Questions or comments?

Please contact the author, Robin Barone, at [email protected]

or PREC’s Research Associate, Eric Hawthorn, at [email protected]

This article is intended for informational purposes only. Neither PREC nor the author guarantee the accuracy or completeness of any information contained herein. None of this work is intended as a professional recommendation, and both the Philadelphia Real Estate Council and the white paper’s author disclaim any responsibility for any business decisions or losses resulting from information herein.

23