Embed Size (px)

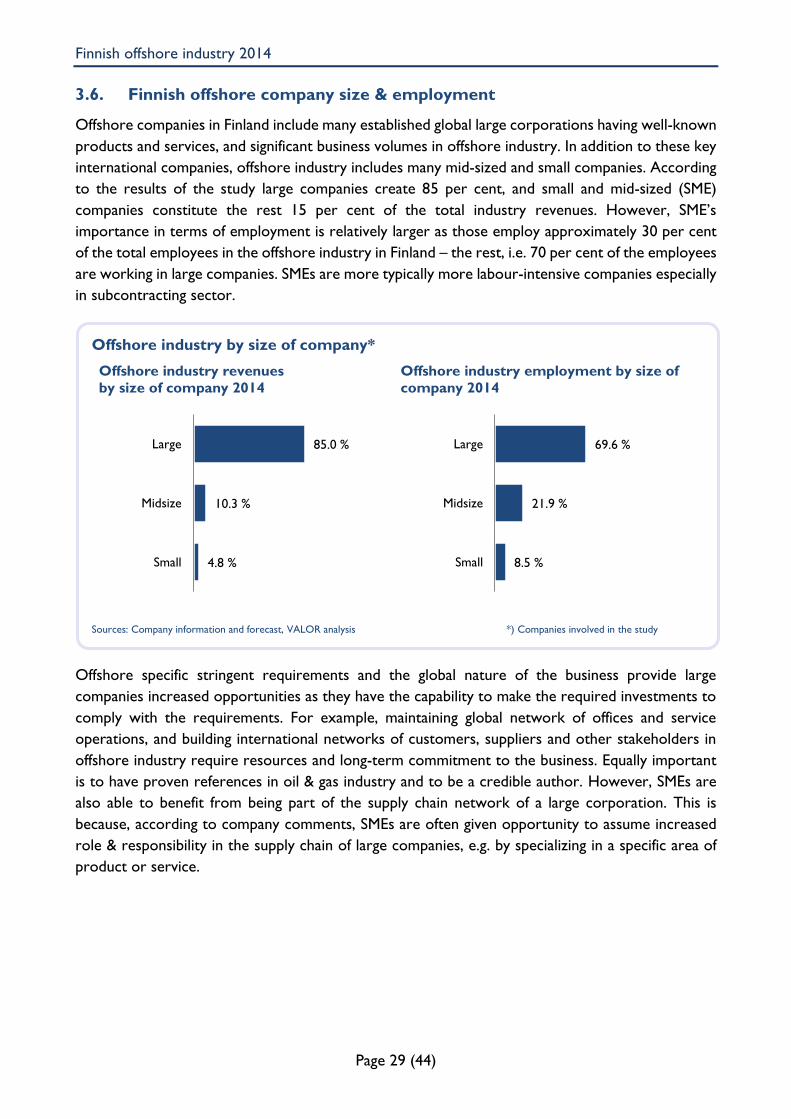

Citation preview

The Finnish Offshore Industry 2014

This study describes Finnish offshore industry, its structure and business volumes as well as future outlook. This report is a continuum to the Finnish

Offshore Industry -reports conducted in 2012 and 2013. The project team is commissioned by Prizztech Oy (www.prizz.fi) and the report is also supporting the work of Ministry of Employment and the Economy (MEE) Maritime industry operational environment development programme. Financially the study is

supported by MEE.

Finnish offshore industry 2014

Page 1 (44)

Forewords

As Finland's ambassador to the Kingdom of Norway I have had the pleasure of

working closely with Finnish foreign trade and promotion of Finnish know-how in

one of the most lucrative markets in today's Europe. Norway, being one of the few

truly thriving economies in Europe at the moment, is also a close partner, and a

natural market for the Finnish expertise.

The Norwegian Continental Shelf is still going strong. The future expectations look

bright, nearly 50 years after the start of the Norwegian oil and gas adventure. The

Norwegian Petroleum Directorate's forecasts indicate that profitable production and

high level of activity will continue for many decades to come. A record number of

fields are being developed, and large new discoveries have been made. Currently many smaller discoveries

are under evaluation. The future of the offshore industry in Norway looks promising.

It is only natural that the Finnish offshore industry turns its eyes to Norway: The Norwegian continental shelf

forms currently the world's biggest offshore market. I am convinced that there is room for Finnish know-

how in this market. In many ways our two countries form a "match made in heaven": Finland has a lot to

offer when it comes to knowledge needed in the Arctic conditions, our technological competence, highly

educated work force, and our ability to perform and deliver. The statistics of our bilateral trade relations

show that there is room for improvement: Norway is (only!) Finland's 11th biggest export destination with a

2.9 % share of our entire export value. Norway is the 14th biggest import country with 2 % of the total import

to Finland.

As this report shows the Finnish expertise stands out and can make a difference in the harsh conditions of

the High North. But the reasons for Finnish-Norwegian cooperation don't stop there: we share a common

Nordic language, our business cultures are quite similar and the common cultural background makes

cooperation easy. Besides, cooperation across the borders can open up a whole new network of customers

and possible contractors – and this goes both ways.

The Finnish business life is not the only one eyeing up Norway. Official Finland delivers as well: the

establishment of a bilateral Arctic partnership with Norway aims at creating even better common ground for

cooperation and economic activity between our two countries. A "group of wise persons" consisting of

representatives named by the Finnish, Swedish and Norwegian prime ministers, is currently working on a

report that looks more closely into cooperation possibilities in the High North. All this is not just a proof of

further development potential in our relations, but it also shows the importance that the authorities in all

three countries attach to this cooperation.

An even closer cooperation and closer business ties will undoubtedly benefit both Finland and Norway.

Whether you need reliable partners, highly qualified work force, good solutions, or world-class expertise, I

am confident that Finnish expertise can offer a competitive option. We have the will and we have the know-

how, and we are ready to deliver. Hence I state with pride: "Look to Finland"!

Maimo Henriksson

Ambassador of Finland to the Kingdom of Norway

Finnish offshore industry 2014

Page 2 (44)

Key figures

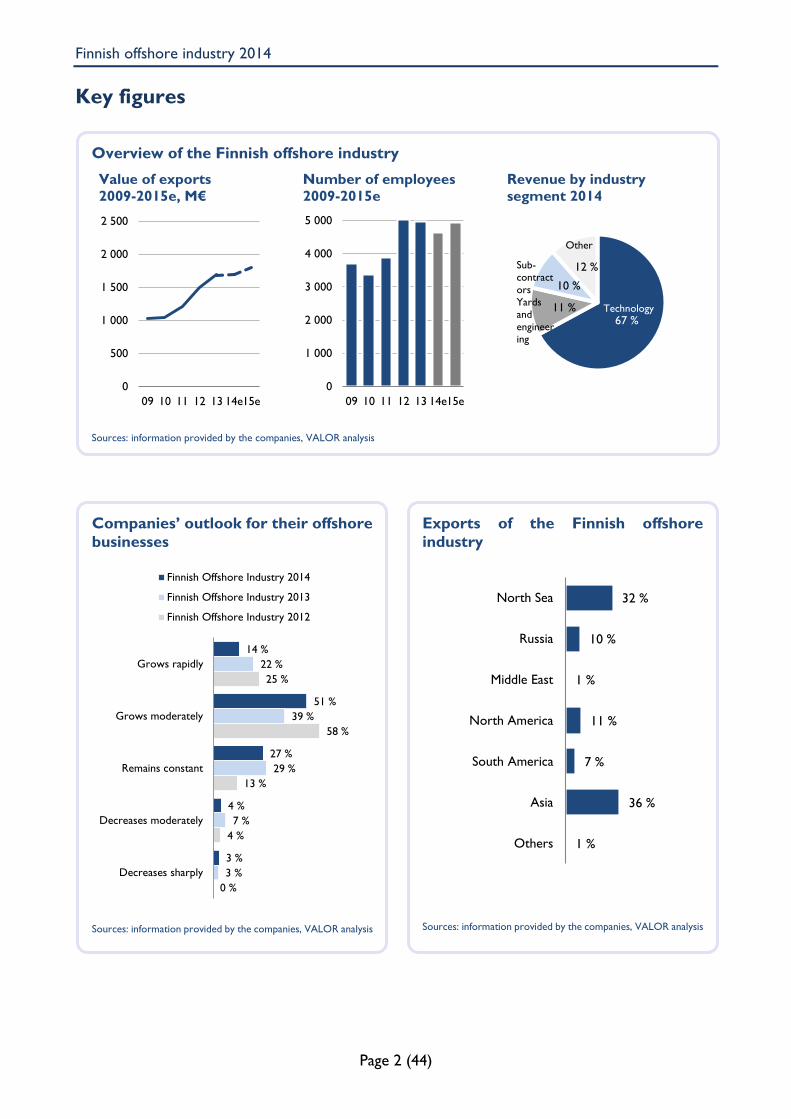

Overview of the Finnish offshore industry

Value of exports

2009-2015e, M€

Number of employees

2009-2015e

Revenue by industry

segment 2014

Sources: information provided by the companies, VALOR analysis

0

500

1 000

1 500

2 000

2 500

09 10 11 12 13 14e15e

0

1 000

2 000

3 000

4 000

5 000

09 10 11 12 13 14e15e

67 %11 %

10 %

12 %

TechnologyYardsand

engineering

Sub-contract

ors

Other

Companies’ outlook for their offshore

businesses

Sources: information provided by the companies, VALOR analysis

14 %

51 %

27 %

4 %

3 %

22 %

39 %

29 %

7 %

3 %

25 %

58 %

13 %

4 %

0 %

Grows rapidly

Grows moderately

Remains constant

Decreases moderately

Decreases sharply

Finnish Offshore Industry 2014

Finnish Offshore Industry 2013

Finnish Offshore Industry 2012

Exports of the Finnish offshore

industry

Sources: information provided by the companies, VALOR analysis

32 %

10 %

1 %

11 %

7 %

36 %

1 %

North Sea

Russia

Middle East

North America

South America

Asia

Others

Finnish offshore industry 2014

Page 3 (44)

Executive Summary

In this report offshore industry is defined as including businesses conducting or supporting offshore oil & gas

exploration and production as well as other production and related activity at sea (for example, offshore

wind and wave energy and seabed mining).

In this report offshore industry is defined as including businesses conducting or supporting offshore oil & gas

exploration and production as well as other production and related activity at sea (for example, offshore

wind and wave energy and seabed mining).

Today in 2014, the Finnish offshore industry comprises of approximately 150 active companies and to whom

offshore business is of increasing importance. The Finnish offshore industry experienced substantial growth

in exports in years between 2010 and 2012 but decreasing slightly in 2014 compared to previous year. The

total exports of the industry are expected to be around 1.7 billion euros in 2014. Technology is the most

important offshore industry segment in Finland accounting to approximately 1.3 billion euros, or around 70 %

of the industry’s revenues. Particularly strong Finnish players in this area include companies such as Wärtsilä,

Rolls-Royce, ABB, and Steerprop, specializing in propulsion, power and engine technologies. The industry

employs approximately 5 000 persons in Finland and the companies participated in this study are planning to

recruit more than 150 employees for offshore business in next two years.

Finnish companies are known for their high technological expertise and uncompromising quality in offshore.

Companies emphasize that quality is viewed holistically covering not only traditional aspect of product quality,

like technical properties and durability, but also reliability of delivery, and communication and cooperation

through entire supply chain. Other important competitive strengths of the Finnish offshore industry include

e.g. Arctic know-how, geographical location near Norway and Russia, engineering work, project management

and supporting political environment.

Norway is regarded as one of the leading offshore markets and Finnish companies often quote Norway as

their home country in offshore business. Norwegian offshore companies are one of the most technologically

demanding and savviest customers and their decision criteria is based more on managing risk rather than low

purchase price. Russia is also considered important for the Finnish offshore industry due to their share in

Arctic offshore and proximity to Finland. Other important markets include Brazil, Asia, Gulf of Mexico

(GOM) and West-Africa.

Finnish offshore companies emphasize that they invest robustly in technological innovativeness and quality,

aspects on which they will ground competitiveness also in the future. Specifically, companies regard advanced

service concepts, such as preventive maintenance, HSEQ, subsea and project management – even by assuming

EPCM (engineering, procurement and construction management) projects – as important product and service

key success factors for them in the future.

Finnish companies have a multiple of partners and other stakeholders with whom they cooperate in offshore.

Particularly technology companies are active in investing in their network of supply chain in order to ensure

the most stringent quality requirements are complied also in the future. Important partners outside offshore

industry include e.g. universities and other research institutions, and Finnish government and government

owned companies and facilities. Finally, Finnish companies also recon that intellectual property rights (IPR)

management is becoming more and more important in offshore business.

Finnish offshore industry 2014

Page 4 (44)

Table of contents

Forewords ............................................................................................................................................................... 1

Key figures ............................................................................................................................................................... 2

Executive Summary ............................................................................................................................................... 3

Table of contents ................................................................................................................................................... 4

1. Introduction .................................................................................................................................................... 5

2. The Finnish offshore industry overview ................................................................................................... 7

2.1. Key Finnish offshore industry business areas ................................................................................. 7

2.2. Competitiveness and strengths of the Finnish offshore industry ............................................... 8

2.3. The Finnish offshore industry in global perspective .................................................................... 11

2.4. Arctic offshore markets for the Finnish cluster ........................................................................... 15

3. Offshore industry in Finland ..................................................................................................................... 18

3.1. Yards and engineering ........................................................................................................................ 20

3.2. Technology companies ...................................................................................................................... 22

3.3. Subcontractors .................................................................................................................................... 24

3.4. Material companies ............................................................................................................................. 26

3.5. Other identified offshore businesses .............................................................................................. 28

3.6. Finnish offshore company size & employment ............................................................................. 29

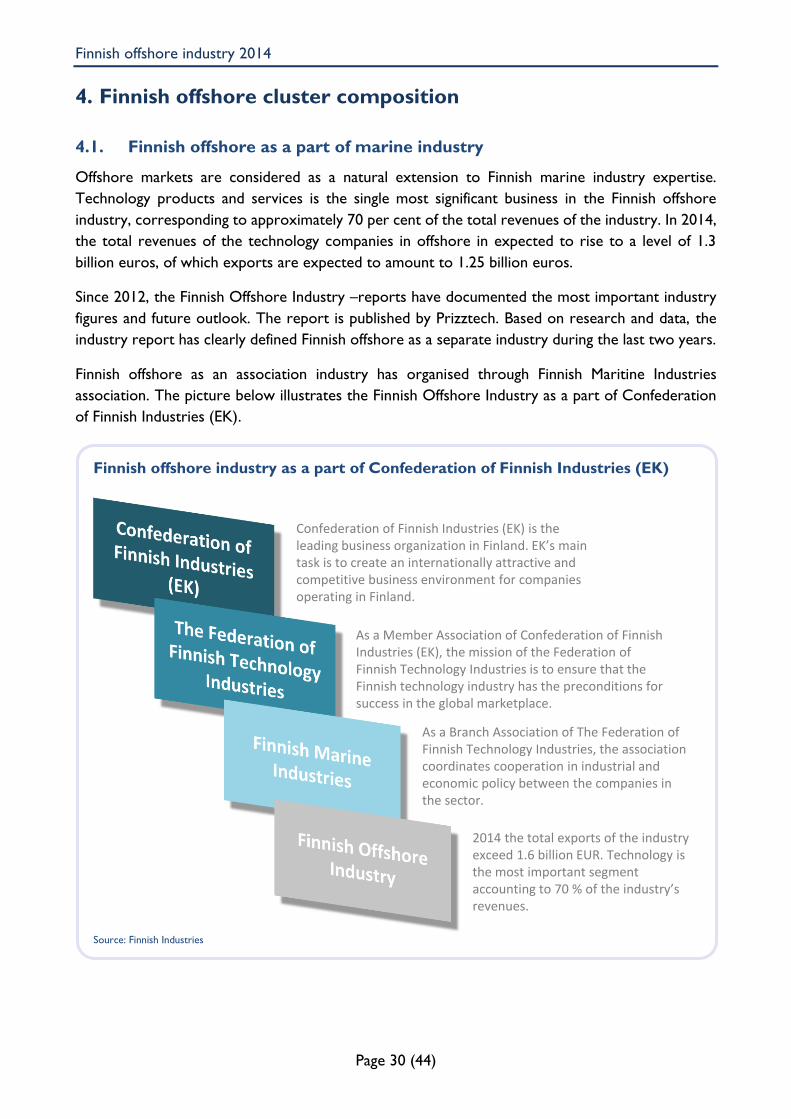

4. Finnish offshore cluster composition ...................................................................................................... 30

4.1. Finnish offshore as a part of marine industry ............................................................................... 30

4.2. Finnish offshore cluster geographically .......................................................................................... 31

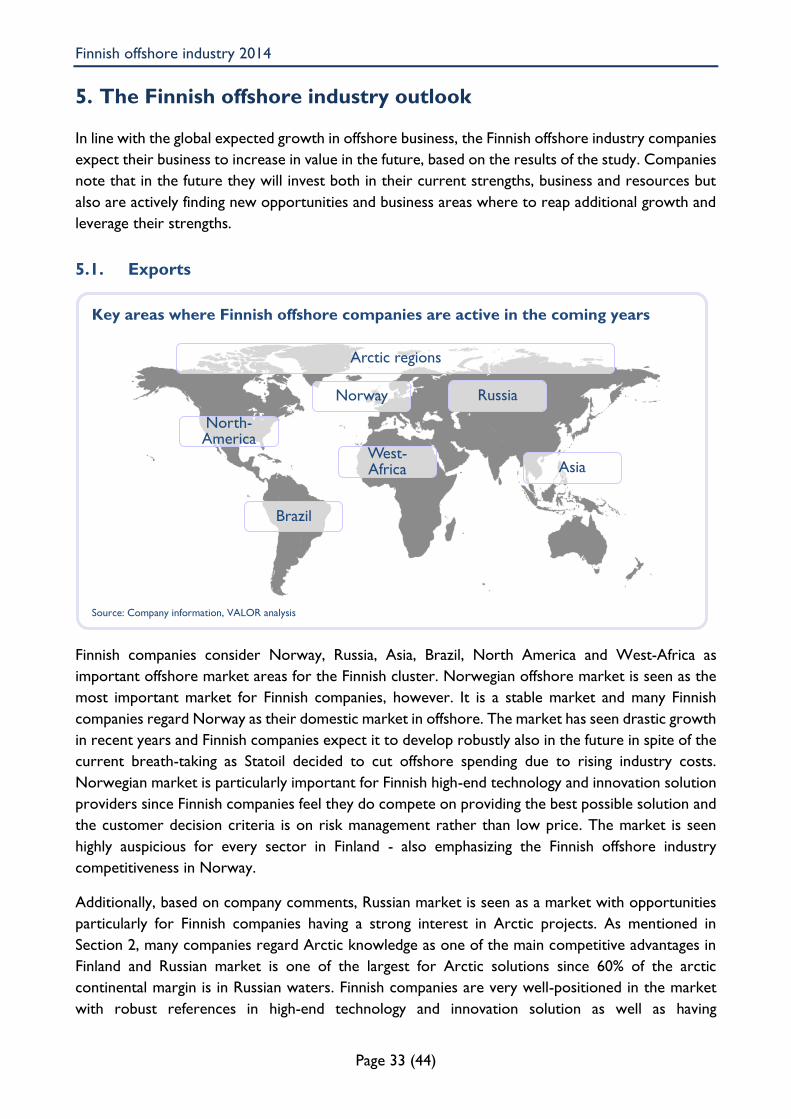

5. The Finnish offshore industry outlook ................................................................................................... 33

5.1. Exports .................................................................................................................................................. 33

5.2. Products and services ........................................................................................................................ 34

5.3. Resources ............................................................................................................................................. 36

6. Conclusion .................................................................................................................................................... 38

7. Methodology and reliability of the study................................................................................................ 41

7.1. Background and objectives ............................................................................................................... 41

7.2. Methodology ........................................................................................................................................ 41

7.3. Reliability of the study........................................................................................................................ 42

APPENDIX ............................................................................................................................................................ 44

Companies participated in the study .......................................................................................................... 44

Finnish offshore industry 2014

Page 5 (44)

1. Introduction

Finnish offshore industry 2014 –study describes Finnish offshore industry, its structure and business

volumes as well as future outlook. This report is a continuum to the Finnish Offshore Industry -

reports conducted in 2012 and 2013. The project team is commissioned by Prizztech Oy

(www.prizz.fi) and the report is also supporting the work of Ministry of Employment and the

Economy (MEE) Maritime industry operational environment development programme1. Financially

the study is supported by MEE.

This study is conducted by VALOR Partners Oy (www.valor.fi) and it was implemented between

June and August in 2014. The focus of the study is on Finland, and Finnish products and services for

the offshore industry. Additionally Norwegian and Russian market opportunities for the Finnish

companies, especially in the arctic region, have been studied in more depth and a summary of these

markets has been prepared in cooperation with Storvik & Co AS (www.storvik.com).

Finnish offshore industry has been recorded systematically by company interviews and a survey. The

Finnish offshore companies have been identified especially from yard and technology sectors,

including also their identified networks of supply chain, and by utilizing previous data from offshore

cluster in Finland including previous Offshore Industry studies. Despite the systematic approach of

the study, a small number of relevant companies that are not members of the Finnish Marine

Industries association, do not own internet visibility in offshore business or have not being

mentioned in numerous discussions with Finnish offshore companies are outside of the scope of this

study, however. Further discussion concerning the methodology is provided in Section 7.

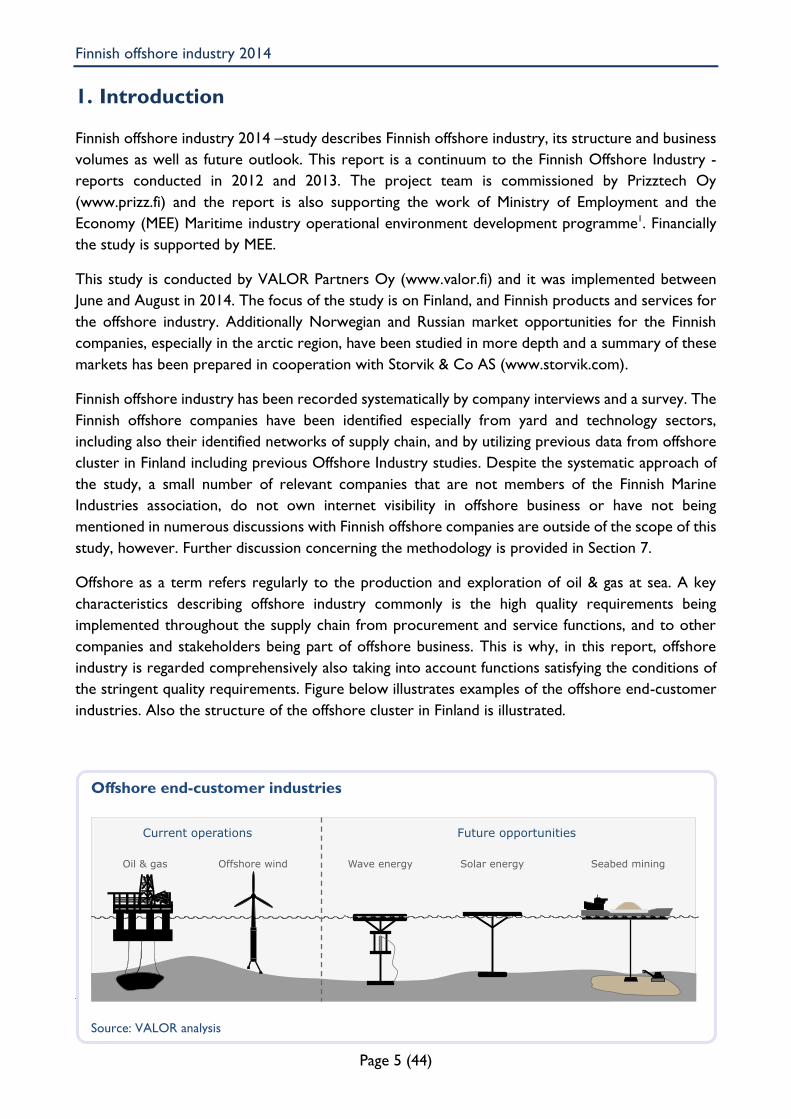

Offshore as a term refers regularly to the production and exploration of oil & gas at sea. A key

characteristics describing offshore industry commonly is the high quality requirements being

implemented throughout the supply chain from procurement and service functions, and to other

companies and stakeholders being part of offshore business. This is why, in this report, offshore

industry is regarded comprehensively also taking into account functions satisfying the conditions of

the stringent quality requirements. Figure below illustrates examples of the offshore end-customer

industries. Also the structure of the offshore cluster in Finland is illustrated.

1 In Finnish ”Meriteollisuuden toimintaympäristön kehittämisohjelma”

Offshore end-customer industries

Source: VALOR analysis

Oil & gas Offshore wind Seabed miningWave energy

Current operations Future opportunities

Solar energy

Finnish offshore industry 2014

Page 6 (44)

Based on the discussion above, in this report offshore industry is defined as including businesses

conducting or supporting offshore oil & gas exploration and production as well as other production

and related activity at sea (for example, offshore wind and wave energy and seabed mining). Instead,

offshore industry does not include oil & gas logistics related tanker or harbour activities since quality

requirements are not strictly shared with offshore industry.

Specifically, this report consists of 7 chapters, this chapter being the first. The second section briefly

introduces the Finnish offshore industry and its business areas and main competitive strengths both

globally, and in specific in Norway and Russia and arctic region. Norway and Russia represent natural

markets for Finnish companies due to geographical proximity. Third chapter instead provides key

statistics and discusses the Finnish offshore industry by sector and Section 4 introduces offshore

cluster in Finland in broad context and discusses its role as part of the Finnish industry. Fourth

section also maps the Finnish offshore cluster geographically in Finland. The following part, chapter

5, provides insight concerning Finnish offshore industry’s outlook and Section 6 draws a conclusion

of the study. Finally, chapter 7 discusses the background and objectives, and the methodology of the

study. Appendix provides the list of companies contributed to the study either through interview

discussion or questionnaire.

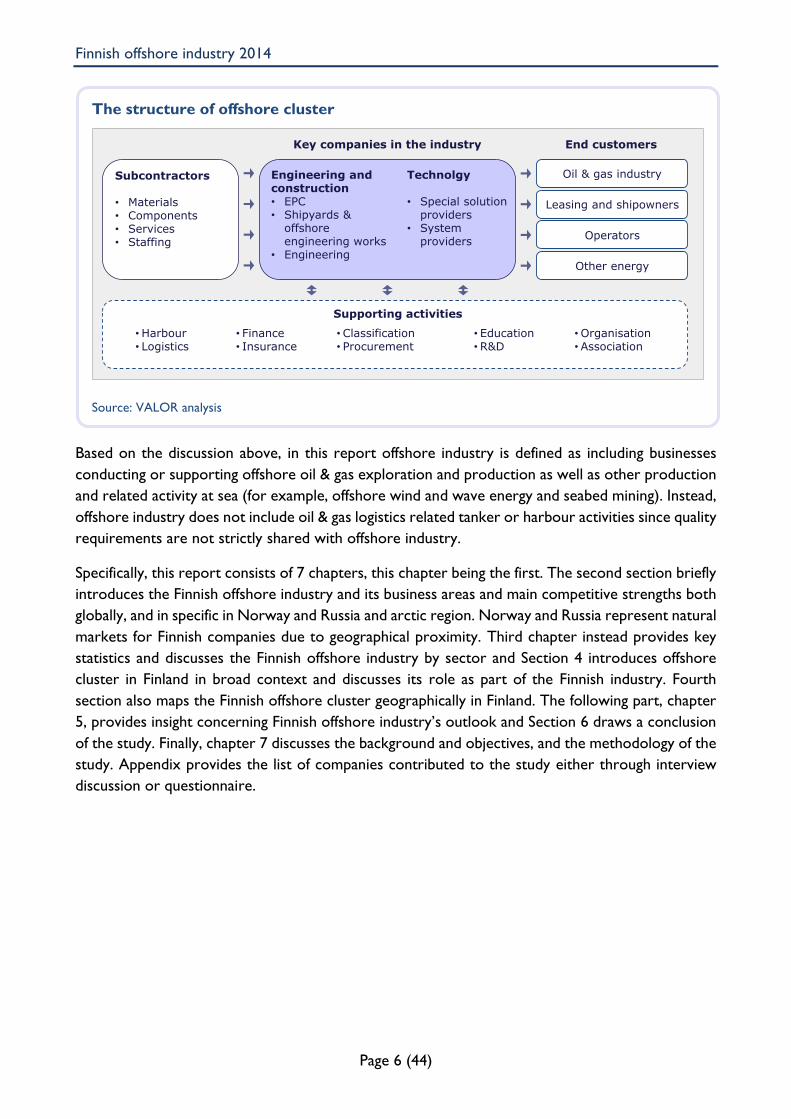

The structure of offshore cluster

Source: VALOR analysis

End customers

Oil & gas industry

Leasing and shipowners

Operators

Other energy

Key companies in the industry

Subcontractors

• Materials• Components• Services• Staffing

Supporting activities

• Harbour• Logistics

• Organisation• Association

• Education• R&D

• Finance• Insurance

Engineering and construction• EPC• Shipyards &

offshore engineering works

• Engineering

Technolgy

• Special solution providers

• System providers

• Classification• Procurement

Finnish offshore industry 2014

Page 7 (44)

2. The Finnish offshore industry overview

Today in 2014, the Finnish offshore industry is significant business in Finland and over 150 companies

operate actively in the industry, according to the results of the Finnish Offshore Industry study.

Moreover, the results of the survey reveal offshore companies expect the importance of the

offshore business to grow for them in the future. In this study, the Finnish offshore industry cluster

is divided in five different segments: Yards, engineering companies, subcontractors, technology

companies, material companies and other identified offshore business, including e.g. offshore wind

and shipping services.

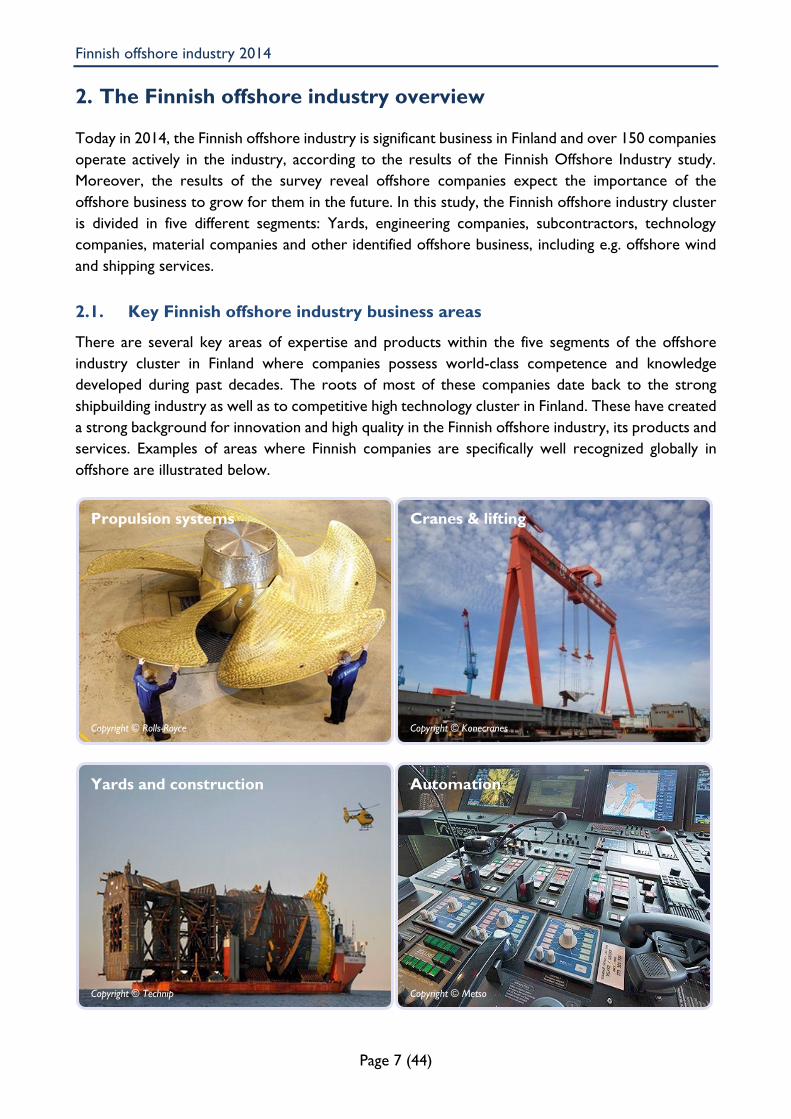

2.1. Key Finnish offshore industry business areas

There are several key areas of expertise and products within the five segments of the offshore

industry cluster in Finland where companies possess world-class competence and knowledge

developed during past decades. The roots of most of these companies date back to the strong

shipbuilding industry as well as to competitive high technology cluster in Finland. These have created

a strong background for innovation and high quality in the Finnish offshore industry, its products and

services. Examples of areas where Finnish companies are specifically well recognized globally in

offshore are illustrated below.

Propulsion systems

Copyright © Rolls-Royce

Cranes & lifting

Copyright © Konecranes

Yards and construction

Copyright © Technip

Automation

Copyright © Metso

Metso / Wärtsilä

Finnish offshore industry 2014

Page 8 (44)

2.2. Competitiveness and strengths of the Finnish offshore industry

One of the most prominent strengths of the Finnish offshore cluster is technological expertise and

innovativeness. Numerous companies in the Finnish offshore cluster are in a strong position globally

in providing technology solutions within selected areas, but the single largest product area in which

technological know-how has accumulated and expanded broadly during the past decades is

propulsion systems. In this product area Wärtsilä, Rolls-Royce, ABB and Steerprop are major global

players in their specific applications in their Finnish operations. Particularly Rolls-Royce Finland and

Wärtsilä have been able to deliver a large share of propulsion systems for advanced solutions in

offshore platforms and vessels used e.g. in drilling, production and supporting activities in offshore

worldwide. Steerprop and ABB are instead renowned for their solutions in powerful propulsion

systems. Moreover, it is important to note an internationally unique cluster of expertise has evolved

within supply chain to support the development of this unique cluster of propulsion systems in

Finland.

Manufacturing solutions

Copyright © Pemamek

Living & wellbeing

Copyright © Almaco

Materials

Copyright © Ovako Imatra

Other marine & arctic technology

Copyright © Arctech Helsinki

Finnish offshore industry 2014

Page 9 (44)

Rest of the technology sector include companies that are

specialised in selected application where they assume a

leadership role internationally. Typically these companies

have a background in maritime industry as well as in other

industries. For example Kemira is well-acknowledged

chemicals supplier, GS-Hydro is a globally established

company supplying non-welded piping systems, Marioff

provides fire protection systems customers world-wide and

Vaisala that is one of the most renowned high-end

environmental measurement systems and solutions

providers. Vacon and ABB instead provide customers

drives and other frequency convertors. These companies

possess strong references in providing offshore oil & gas

exploration and production solutions as well.

Finnish yards instead are players which have earned a strong

reference base in specific product areas where they are

particularly competitive. For example, majority of spar

platforms ever build has been constructed in Mäntyluoto yard in Pori - a yard that is nowadays

owned by Technip that is one of the largest global offshore corporations. Mäntyluoto yard has also

been awarded with many other offshore projects and has the capability to construct e.g. subsea

structures, and semi-submersible and FPSO platforms as well, however. Arctech Helsinki Shipyard

Oy, a company owned jointly by STX Finland Oy and United Shipbuilding Corporation with equal

shares, is specialised in Arctic shipbuilding technology and has constructed approximately 60 percent

of currently operational icebreakers in the world in Helsinki. These icebreakers and other special

vessels are also operating in offshore and have become a firm part of the global offshore cluster.

Equally important is to notice that icebreaker and Arctic project deliveries have been backed by the

expertise of numerous Finnish engineering and subcontractor companies. This has created the

grounds for the development of one the global Arctic maritime technology centres of excellence

and knowledge spillover in Finland. As an illustration, the government owned icebreaking and special

purpose vessel service provider, Arctia Shipping Oy, has taken the advantage of its ice management

know-how and is providing customers related services in Arctic offshore projects. Aker Arctic

Technology, on the other hand, is a company specialising in engineering services for the ice going

vessels, icebreakers and offshore. Based on company comments of this study, Finnish knowledge in

Arctic solutions is viewed highly important area of competence for offshore cluster in Finland

particularly in the future when offshore investments actuate in Arctic region.

In addition to the technological know-how and innovativeness, Finnish companies are also known

for their uncompromising quality in products and services, which stems from the fact that Finnish

offshore cluster is particularly advanced in project management. According to the company

comments, quality is viewed as a holistic concept covering traditional aspect of product quality, like

technical properties and product durability as well as reliability of delivery, and communication and

cooperation vertically both within customer as well as supply chain. This is a very important

consideration in offshore industry, especially in advanced solutions where high and rigid standards

Copyright © Vaisala

Copyright © Vacon

Finnish offshore industry 2014

Page 10 (44)

and quality requirements as well as full traceability are

expected and complied throughout the entire value chain

on daily basis. Companies also emphasize Finnish

companies do not ground their competitiveness on price,

e.g. if comparing to Asia and other low cost countries,

but rather on the highest level of quality – an area

whereof a premium is also paid in the offshore industry.

Many companies also note that Finnish engineering work

is very competent, which originates both from providing

tailored and advanced engineering solutions and modest

cost structure. Price competitiveness is particularly well-grounded if compared to other developed

countries. For example, according to the Union of Professional Engineers in Finland (IL), Finnish

engineering work cost on average slightly over 4 000 €/month (median 2 692 €/month) in 2013.

This is a level far below corresponding figure in e.g. Norway where according to NITO’s, The

Norwegian Society of Engineers and Technologists, who estimate a corresponding figure of

approximately 6 200 €/month for local engineering work2. Finnish engineers are also highly qualified

in education. According to study results, Finnish engineers in offshore are with a few exceptions

graduated with a diploma from university or applied university.

Another advantage for the Finnish offshore industry stems

from geographical location near two large offshore markets,

Norway and Russia. Geographical proximity is to reduce

costs associated with logistics and delivery time but the

advantage is also derived from enhanced customer

communication between Finnish company and customers.

Reduced response time is particularly important in offshore

business and operations where problems and issues may

escalate rapidly on massive scale. Besides, time zone and

cultural differences are all adding complexity in

communication, which is based on the discussed above

regarded as an important aspect of product and service

quality, creating a solid advantage for Finnish companies in

Norway and Russia.

Finnish political atmosphere and intent has also become increasingly supportive for the development

of the offshore industry. The objective of the new MEE development programme for the maritime

industry's operational environment is to increase the competitiveness of and renew the Finnish

maritime industry so that the top level expertise remains in Finland. The programme recons Finland

has opportunities especially in offshore industry and arctic business. The programme supports

activities of Finnish companies and other market participants developing new and leveraging existing

know-how, products and services that create new opportunities in the offshore industry and arctic

2 According to the salary calculator at http://www.nito.no/Lonn/Hva-tjener-en-ingenior/Lonnskalkulator, a Norwegian engineer earns 588 427 NOK per year on average.

Copyright © Aker Arctic Technology

Copyright © National Energy Board of Canada

Finnish offshore industry 2014

Page 11 (44)

business for Finnish companies. Besides, the Finnish government has also shown its intention to

support maritime and offshore industry through ownership arrangements in e.g. engineering and

yard sectors.

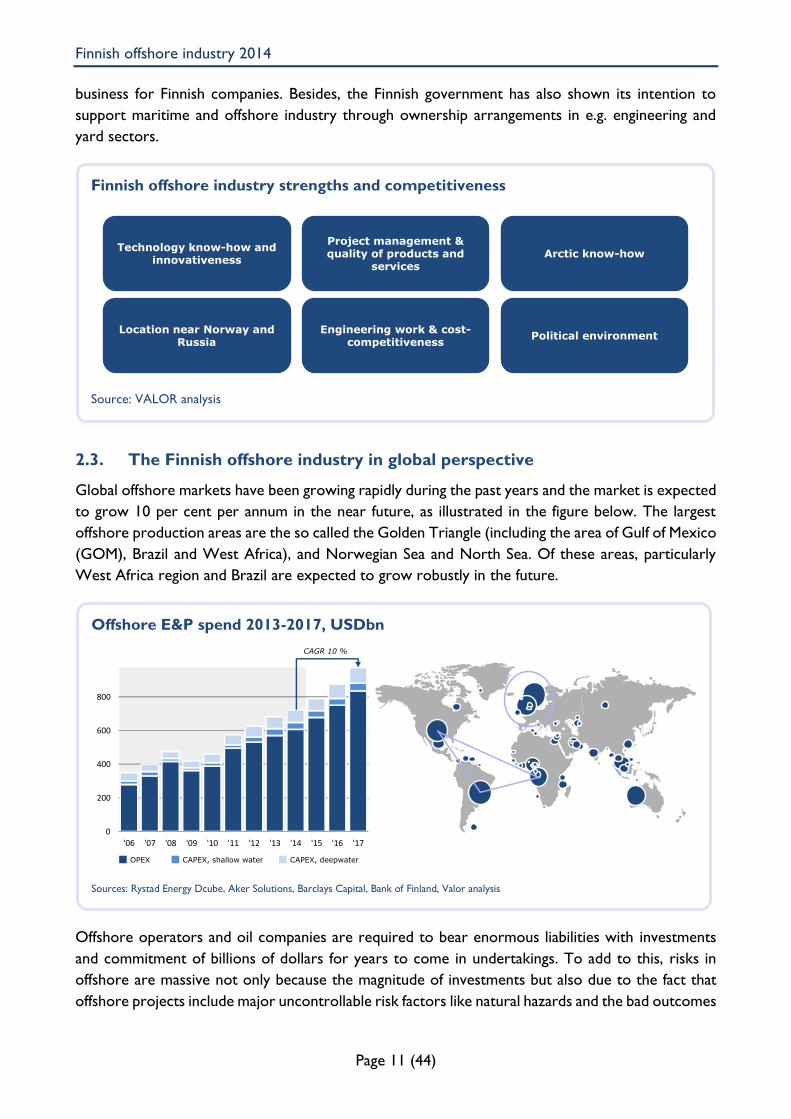

2.3. The Finnish offshore industry in global perspective

Global offshore markets have been growing rapidly during the past years and the market is expected

to grow 10 per cent per annum in the near future, as illustrated in the figure below. The largest

offshore production areas are the so called the Golden Triangle (including the area of Gulf of Mexico

(GOM), Brazil and West Africa), and Norwegian Sea and North Sea. Of these areas, particularly

West Africa region and Brazil are expected to grow robustly in the future.

Offshore operators and oil companies are required to bear enormous liabilities with investments

and commitment of billions of dollars for years to come in undertakings. To add to this, risks in

offshore are massive not only because the magnitude of investments but also due to the fact that

offshore projects include major uncontrollable risk factors like natural hazards and the bad outcomes

Finnish offshore industry strengths and competitiveness

Source: VALOR analysis

Technology know-how and innovativeness

Engineering work & cost-competitiveness

Project management & quality of products and

services

Political environmentLocation near Norway and

Russia

Arctic know-how

Offshore E&P spend 2013-2017, USDbn

Sources: Rystad Energy Dcube, Aker Solutions, Barclays Capital, Bank of Finland, Valor analysis

0

200

400

600

800

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

OPEX CAPEX, shallow water CAPEX, deepwater

CAGR 10 %

Finnish offshore industry 2014

Page 12 (44)

tend to escalate rapidly. This is why, typically operators and oil companies are large global

corporations, who are willing to acquire only the best possible technology and solution available in

order to ensure finest outcome for a given venture. This is why offshore industry extends its arms

on every corner of the world and includes globally integrated network of supply chain. Accordingly,

based on the results of this study, Finnish companies are also international by nature and their export

amounts to 85 - 90% of the total Finnish offshore industry revenue in 2014 with project deliveries

and exports to practically every continent of the world.

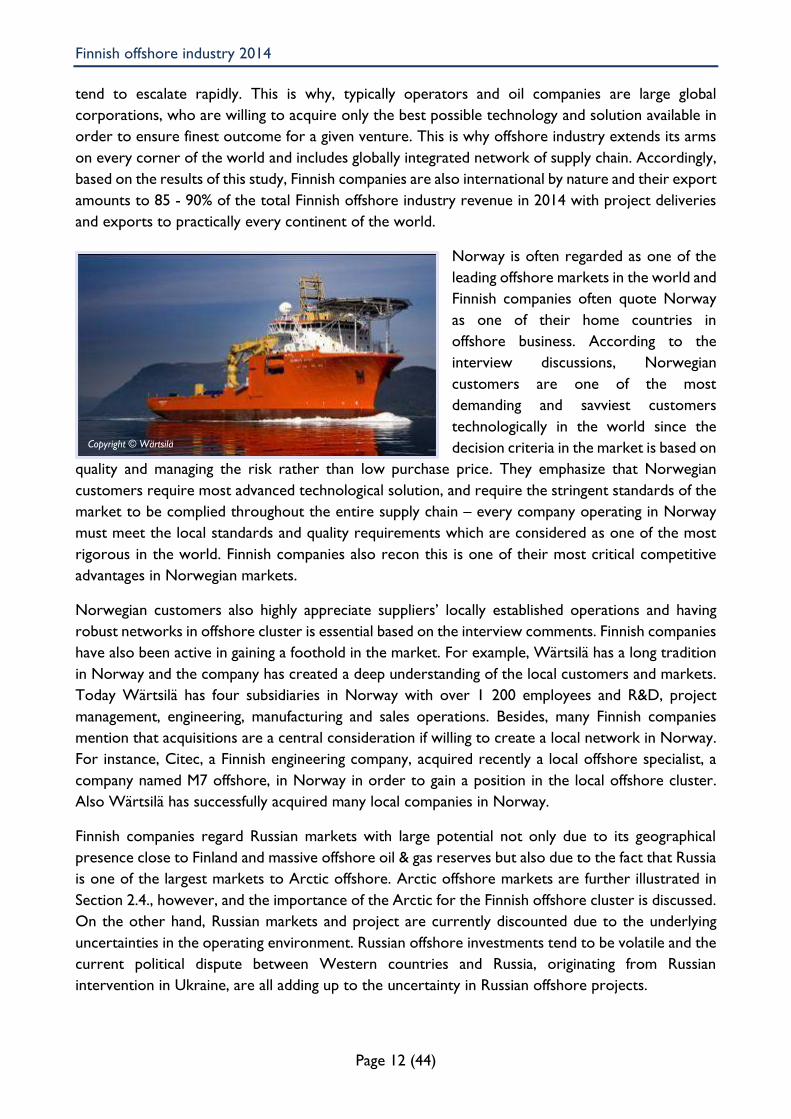

Norway is often regarded as one of the

leading offshore markets in the world and

Finnish companies often quote Norway

as one of their home countries in

offshore business. According to the

interview discussions, Norwegian

customers are one of the most

demanding and savviest customers

technologically in the world since the

decision criteria in the market is based on

quality and managing the risk rather than low purchase price. They emphasize that Norwegian

customers require most advanced technological solution, and require the stringent standards of the

market to be complied throughout the entire supply chain – every company operating in Norway

must meet the local standards and quality requirements which are considered as one of the most

rigorous in the world. Finnish companies also recon this is one of their most critical competitive

advantages in Norwegian markets.

Norwegian customers also highly appreciate suppliers’ locally established operations and having

robust networks in offshore cluster is essential based on the interview comments. Finnish companies

have also been active in gaining a foothold in the market. For example, Wärtsilä has a long tradition

in Norway and the company has created a deep understanding of the local customers and markets.

Today Wärtsilä has four subsidiaries in Norway with over 1 200 employees and R&D, project

management, engineering, manufacturing and sales operations. Besides, many Finnish companies

mention that acquisitions are a central consideration if willing to create a local network in Norway.

For instance, Citec, a Finnish engineering company, acquired recently a local offshore specialist, a

company named M7 offshore, in Norway in order to gain a position in the local offshore cluster.

Also Wärtsilä has successfully acquired many local companies in Norway.

Finnish companies regard Russian markets with large potential not only due to its geographical

presence close to Finland and massive offshore oil & gas reserves but also due to the fact that Russia

is one of the largest markets to Arctic offshore. Arctic offshore markets are further illustrated in

Section 2.4., however, and the importance of the Arctic for the Finnish offshore cluster is discussed.

On the other hand, Russian markets and project are currently discounted due to the underlying

uncertainties in the operating environment. Russian offshore investments tend to be volatile and the

current political dispute between Western countries and Russia, originating from Russian

intervention in Ukraine, are all adding up to the uncertainty in Russian offshore projects.

Copyright © Wärtsilä

Finnish offshore industry 2014

Page 13 (44)

Finnish companies and other stakeholders have also a long tradition of cooperating with Russian

partners and Finnish do have a competitive advantage in communicating with Russian customers and

other stakeholders. For example, Arctech Helsinki Shipyard is a company half owned by a Russian

company, United Shipbuilding Corporation (USC), and the yard has awarded with numerous ice

breaker deliveries to Russia. On the other hand Finnish companies Wellquip and Elomatic

Engineering have established together a joint venture with local partners in Russia in order to gain

a stake in the market. Interestingly, recently Elomatic and Wellquip decided to merge their

operations aiming in particular to achieve growth in the arctic marine business in the Russian and

Caspian Sea markets.

Other important market areas globally for Finnish

companies include Brazil, Asia and GOM. Brazil is a market

with vast offshore projects and reserves, and it is regarded

as one of the largest markets for offshore investments

globally. On top of that, majority of Brazilian offshore

undertakings are deepwater projects in harsh operational

environment providing increased demand for advanced

technological solutions. This is why many Finnish

companies have been lately active in the market, despite

the rigorous local content requirement that is adding

complexity for foreign companies in penetrating the

market. For example, Almaco, a Finnish accommodation

solution provider, has been able to establish itself in the

market through providing its flexible and innovative global

construction capabilities and solutions for Brazilian

customers. On the other hand, Wärtsilä have established

itself in the market by setting up a local manufacturing facility to meet the increasing market demand

particularly in the offshore market.

Asia instead is the main hub for offshore vessel and

platform construction activity in the world. Main Asian

offshore markets for Finnish companies include South

Korea, Singapore and China. Traditionally South Korea and

Singapore have been key markets for advanced offshore

platforms but China has also been active in the market

recently. Finnish companies are particularly strong in

delivering technological and engineering solutions in

selected product areas to the Asian markets. For example,

Finnish companies assume large market share in propulsion

systems in Asian offshore hub.

Conditions in GOM for offshore operations are aggressive and corrosive as the climate is warm,

humid and salty. This is why a special attention must be put on to the quality of the products and

services. Also, regulators are forcing companies in GOM to take a more systemic approach to drilling

safety - similar to those of applied in the North Sea that is the one of main market for Finnish

Copyright © Almaco

Copyright © Wärtsilä

Finnish offshore industry 2014

Page 14 (44)

offshore companies. This is why Finnish companies have a particularly well-established references

and perquisites in delivering solutions for projects in GOM. For example, Finnish yard sector has

earned strong references in the market in advanced solutions and most of the offshore platforms

constructed in Mäntyluoto operate in GOM.

Finally, it is also important to notice that many Finnish units have a unique position in networks of

numerous global large offshore corporations. The role of the Finnish division or unit is often in

research and development, production and advisory activities in the global network. Instead, sales,

after-sales and other cross-functional operations are usually assumed then by the international

network, having established presence globally and direct customer relationship. This kind of

structure helps in leveraging Finnish knowledge rapidly worldwide. For example, ABB has its global

knowledge centre for e.g. propulsion, motor technology, generators and drive products in Finland.

Rolls-Royce Finland instead is a subsidiary assuming main responsibility in R&D and advisory services

in propulsion systems globally.

Finnish offshore industry 2014

Page 15 (44)

2.4. Arctic offshore markets for the Finnish cluster

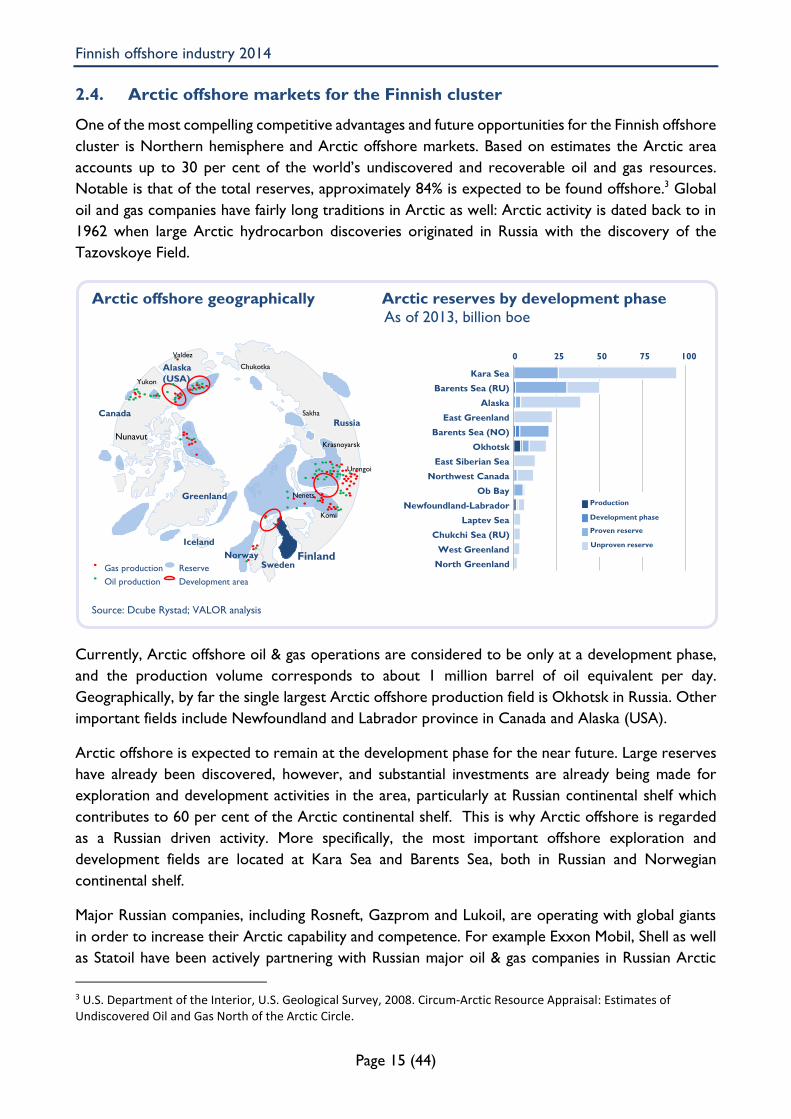

One of the most compelling competitive advantages and future opportunities for the Finnish offshore

cluster is Northern hemisphere and Arctic offshore markets. Based on estimates the Arctic area

accounts up to 30 per cent of the world’s undiscovered and recoverable oil and gas resources.

Notable is that of the total reserves, approximately 84% is expected to be found offshore.3 Global

oil and gas companies have fairly long traditions in Arctic as well: Arctic activity is dated back to in

1962 when large Arctic hydrocarbon discoveries originated in Russia with the discovery of the

Tazovskoye Field.

Currently, Arctic offshore oil & gas operations are considered to be only at a development phase,

and the production volume corresponds to about 1 million barrel of oil equivalent per day.

Geographically, by far the single largest Arctic offshore production field is Okhotsk in Russia. Other

important fields include Newfoundland and Labrador province in Canada and Alaska (USA).

Arctic offshore is expected to remain at the development phase for the near future. Large reserves

have already been discovered, however, and substantial investments are already being made for

exploration and development activities in the area, particularly at Russian continental shelf which

contributes to 60 per cent of the Arctic continental shelf. This is why Arctic offshore is regarded

as a Russian driven activity. More specifically, the most important offshore exploration and

development fields are located at Kara Sea and Barents Sea, both in Russian and Norwegian

continental shelf.

Major Russian companies, including Rosneft, Gazprom and Lukoil, are operating with global giants

in order to increase their Arctic capability and competence. For example Exxon Mobil, Shell as well

as Statoil have been actively partnering with Russian major oil & gas companies in Russian Arctic

3 U.S. Department of the Interior, U.S. Geological Survey, 2008. Circum-Arctic Resource Appraisal: Estimates of Undiscovered Oil and Gas North of the Arctic Circle.

Arctic offshore geographically Arctic reserves by development phase

As of 2013, billion boe

Source: Dcube Rystad; VALOR analysis

Alaska

(USA)

CanadaRussia

FinlandSweden

Norway

Iceland

Greenland

Valdez

Chukotka

Sakha

Krasnoyarsk

Urengoi

Komi

Nenets

Nunavut

Yukon

Gas production

Oil production

Reserve

Development area

0 25 50 75 100

Kara Sea

Barents Sea (RU)

Alaska

East Greenland

Barents Sea (NO)

Okhotsk

East Siberian Sea

Northwest Canada

Ob Bay

Newfoundland-Labrador

Laptev Sea

Chukchi Sea (RU)

West Greenland

North Greenland

Production

Development phase

Proven reserve

Unproven reserve

Finnish offshore industry 2014

Page 16 (44)

offshore operations. This

cooperation is expected to

continue despite recent

sanctions against Russia,

although sanctions may

postpone the Arctic oil &

gas projects in Russian

waters.

Arctic conditions are harsh

and the projects pursue

offshore companies to face

unique risks, requirements,

and challenges. The arctic

environment is

concurrently sensitive to

disruption and oil spills but

harsh and unforgiving due

to remoteness and extreme

weather conditions, particularly in areas with thick ice cap, permafrost or extreme wave conditions.

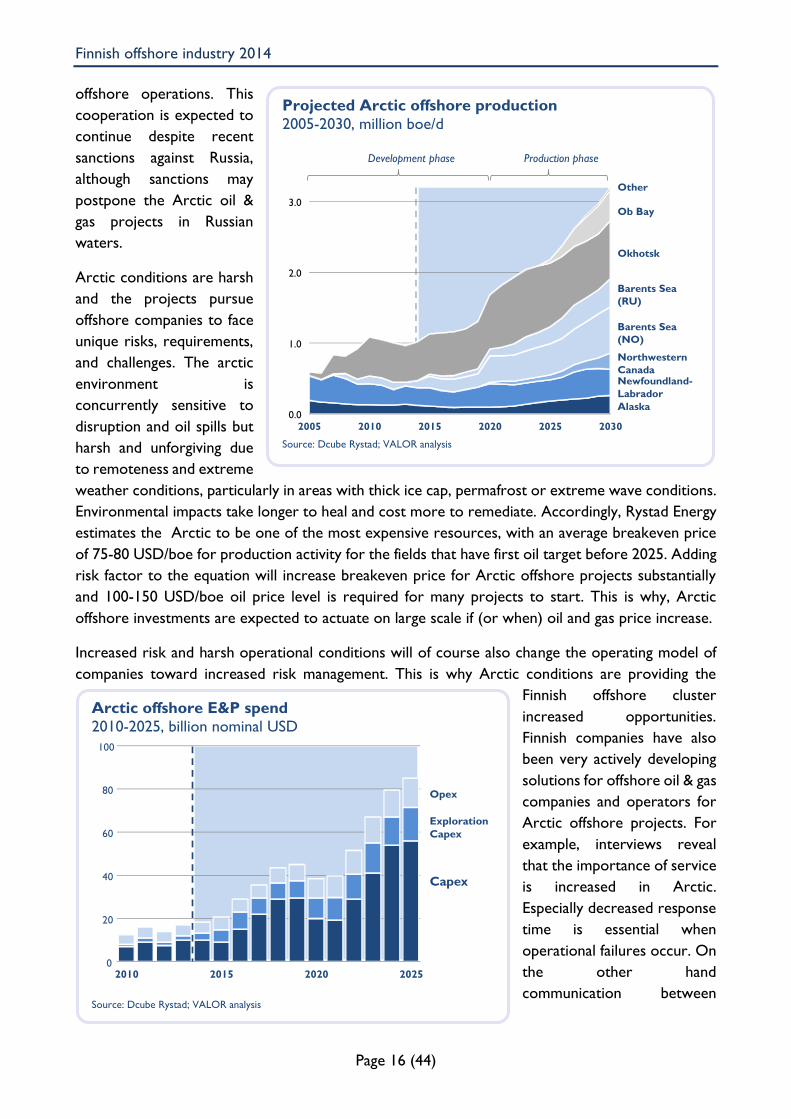

Environmental impacts take longer to heal and cost more to remediate. Accordingly, Rystad Energy

estimates the Arctic to be one of the most expensive resources, with an average breakeven price

of 75-80 USD/boe for production activity for the fields that have first oil target before 2025. Adding

risk factor to the equation will increase breakeven price for Arctic offshore projects substantially

and 100-150 USD/boe oil price level is required for many projects to start. This is why, Arctic

offshore investments are expected to actuate on large scale if (or when) oil and gas price increase.

Increased risk and harsh operational conditions will of course also change the operating model of

companies toward increased risk management. This is why Arctic conditions are providing the

Finnish offshore cluster

increased opportunities.

Finnish companies have also

been very actively developing

solutions for offshore oil & gas

companies and operators for

Arctic offshore projects. For

example, interviews reveal

that the importance of service

is increased in Arctic.

Especially decreased response

time is essential when

operational failures occur. On

the other hand

communication between

Arctic offshore E&P spend

2010-2025, billion nominal USD

Source: Dcube Rystad; VALOR analysis

Opex

Capex

Exploration

Capex

0

20

40

60

80

100

2010 2015 2020 2025

Projected Arctic offshore production

2005-2030, million boe/d

Source: Dcube Rystad; VALOR analysis

Alaska

Newfoundland-

Labrador

Northwestern

Canada

Barents Sea

(NO)

Okhotsk

Barents Sea

(RU)

Ob Bay

Other

Development phase Production phase

0.0

1.0

2.0

3.0

2005 2010 2015 2020 2025 2030

Finnish offshore industry 2014

Page 17 (44)

offshore field operator and company knowledge centre is enhanced. This is why Finnish location

near Arctic offshore fields, particularly Kara Sea and Barents Sea, is an important competitive

advantage.

Finnish companies have also substantial experience in working in Arctic conditions, partly due to

the country’s location in the Northern hemisphere. For example, Arctia Shipping has decades of

experience in ice-breaking and –management, and the company has also established itself as an Arctic

expert in offshore. Arctech Helsinki Shipyard has constructed over 60 per cent of the operational

ice-breakers in the world, as discussed above. Aker Arctic instead is targeting Arctic markets with

engineering solutions. Equally important is to note the experience of Arctic is extended throughout

the entire supply chain. Companies emphasize experience is vital asset in turning opportunities to

success in Arctic oil and gas projects.

For detailed discussion concerning Russian and Norwegian offshore market, please look into a more

detailed study of these regions also published by Prizztech in www-address [LINK:

www.prizz.fi/storvik_country_reports_addressess].

Finnish offshore industry 2014

Page 18 (44)

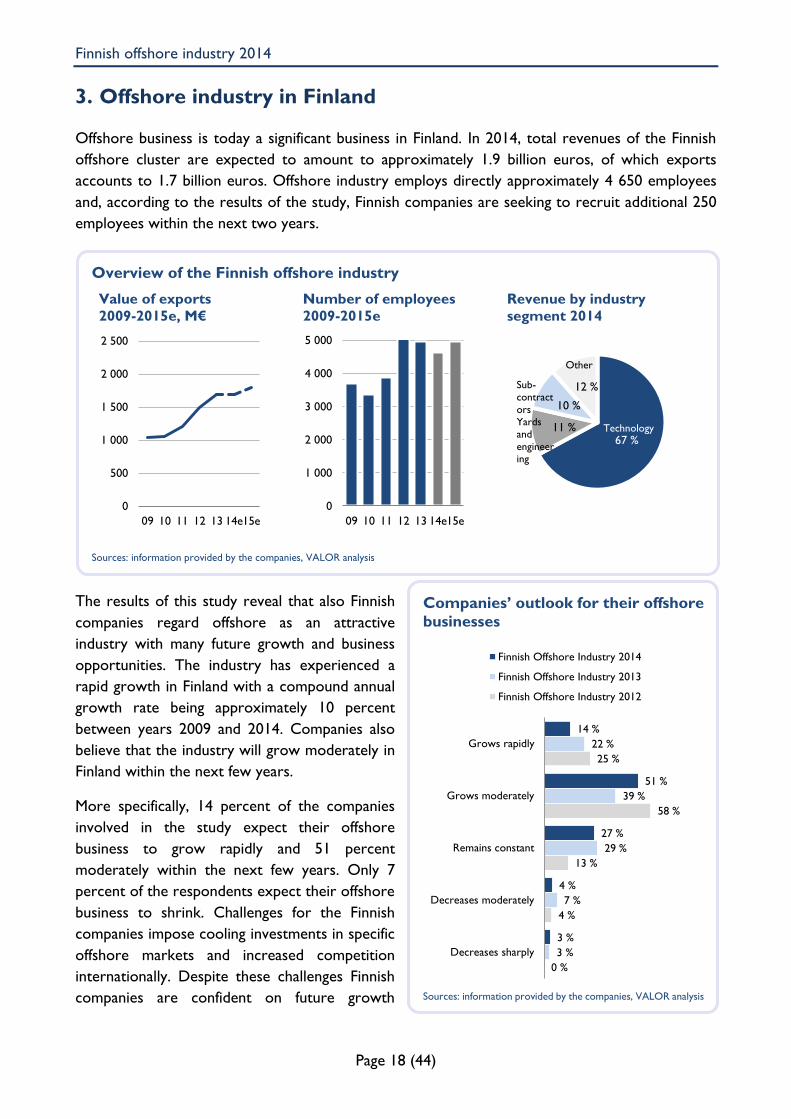

3. Offshore industry in Finland

Offshore business is today a significant business in Finland. In 2014, total revenues of the Finnish

offshore cluster are expected to amount to approximately 1.9 billion euros, of which exports

accounts to 1.7 billion euros. Offshore industry employs directly approximately 4 650 employees

and, according to the results of the study, Finnish companies are seeking to recruit additional 250

employees within the next two years.

The results of this study reveal that also Finnish

companies regard offshore as an attractive

industry with many future growth and business

opportunities. The industry has experienced a

rapid growth in Finland with a compound annual

growth rate being approximately 10 percent

between years 2009 and 2014. Companies also

believe that the industry will grow moderately in

Finland within the next few years.

More specifically, 14 percent of the companies

involved in the study expect their offshore

business to grow rapidly and 51 percent

moderately within the next few years. Only 7

percent of the respondents expect their offshore

business to shrink. Challenges for the Finnish

companies impose cooling investments in specific

offshore markets and increased competition

internationally. Despite these challenges Finnish

companies are confident on future growth

Overview of the Finnish offshore industry

Value of exports

2009-2015e, M€

Number of employees

2009-2015e

Revenue by industry

segment 2014

Sources: information provided by the companies, VALOR analysis

0

500

1 000

1 500

2 000

2 500

09 10 11 12 13 14e15e

0

1 000

2 000

3 000

4 000

5 000

09 10 11 12 13 14e15e

67 %11 %

10 %

12 %

TechnologyYardsand

engineering

Sub-contract

ors

Other

Companies’ outlook for their offshore

businesses

Sources: information provided by the companies, VALOR analysis

14 %

51 %

27 %

4 %

3 %

22 %

39 %

29 %

7 %

3 %

25 %

58 %

13 %

4 %

0 %

Grows rapidly

Grows moderately

Remains constant

Decreases moderately

Decreases sharply

Finnish Offshore Industry 2014

Finnish Offshore Industry 2013

Finnish Offshore Industry 2012

Finnish offshore industry 2014

Page 19 (44)

opportunities in those areas where they possess globally recognized know-how and proven

references, and thus are especially competitive, however. Finnish companies expect the growth of

their offshore business to settle down to a level of between 5 and 10 percent in the near future.

Nevertheless, in 2013, the total revenues of Finnish technology companies amounted to 1.25 billion

euros and the corresponding figure is expected to near 1.3 billion euros in 2014. Notable is that the

largest sub-sector in Finnish offshore technology sector, i.e. propulsion, motor and marine

technology, constitute approximately 65 - 70 per cent of the total Finnish offshore business. The

convergence between traditional marine industry and offshore has been one of the key factors

driving technology companies particularly in propulsions and motor technology sector to become

the single largest product and service area in the Finnish offshore industry. The rest of the core

technology sector in Finland comprises of companies with a background in other industries than

offshore, but regard offshore as important focus area them. These companies possess strong

technological expertise in a variety of technologies and businesses such as crane, automation, valve,

drives, or measurement technologies.

Finnish yard sector is instead in a process in finding new solutions on fuelling future growth and

opportunities. In spite of the fact that Mäntyluoto yard has mainly been focusing on Spar platforms

lately, it possess proven references of constructing other platforms as well. On the other hand, STX

Finland was acquired4 by Meyer Werft, one of the major German shipyards, and the Finnish Industry

Investment (FII), a Finnish government-owned investment company. Arctech Helsinki Shipyard has

demonstrated great confidence in gaining momentum in a specialized niche segment with continuous

innovations and the company has been awarded with 4 offshore ice-breaker contracts in 2014 so

far. It seems that also Arctech’s ownership structure strongly supports its business and growth. Also

a recently established offshore yard Rauma Marine Construction (RMC) is adding future

opportunities to Finnish offshore yard sector.

Finnish engineering companies have been active in finding

opportunities for growth and divergence from the

traditional setting of being closely related and inclined to

the operations of Finnish yards. Engineering companies

have set their sights abroad and created international

business and customers not only organically but also

through acquisitions and setting strategic partnerships. For

example, Elomatic and Wellquip decided to merge their

operations and Citec was able to establish itself in the

Norwegian offshore markets by taking over local M7

Offshore. On the other hand Deltamarin’s owners and management found a new partner to fuel

company growth by selling majority of its shares to AVIC International Investments Ltd., also

creating robust prerequisites for future expansion opportunities in offshore business as well.

Besides, the growth in offshore business, particularly in deepwater operations with operational

needs similar to those of maritime industry, has provided Finnish traditional maritime industry

engineering companies a new opportunity to expand the scope of their business. This all has enabled

4 As of 4.8.2014, the acquisition is still subject to clearance by the antitrust authorities and banks.

Copyright © Citec

Finnish offshore industry 2014

Page 20 (44)

Finnish engineering companies to expand their customer base and taking the advantage of the

growing offshore business. Many engineering companies regard offshore business has become more

and more important to them relative to their marine business.

Subcontractors, which have traditionally been inclined to domestic yard and technology sector, have

also been able to penetrate international markets and in 2013 nearly half of their revenues were of

international origin. Finnish subcontractors are typically engineering workshop companies

specialising in a product area or by material treatment method, such as casting or coating. They are

particularly competitive in highly customised delivers with short lead time and small series size, or

in a specific product area such as gears or casting. Subcontractors’ revenues are expected to be 225

million euros in 2014 in offshore industry.

In addition to abovementioned sectors, Finnish companies are also providing materials and other

service business in offshore industry. Finnish steel, tube, copper and chemical, and other material

companies supplying offshore industry are expected to generate revenues of approximately 150

million euros in 2014. Offshore business is one of the few growing segments for many material

companies and they are investing in the business robustly, study reveals. The sector covering other

services and products for offshore industry comprise of around 50 million euros business annually.

One of the most prominent actors in this sector is Arctia Shipping, a state owned company having

ice-breakers operating in the ice-management duties in the arctic offshore fields and development

areas.

Offshore business has increased its relative importance for those companies operating in the

industry against their other operations based on the study results. Offshore share of total revenues

of the companies of this study has increased from 7 percent in 2009 to 11 percent in 2013. Driving

forces behind the pattern of development include the underlying challenges in global traditional

marine industry and the trend of providing more advanced solutions in offshore industry and thus

more value-adding solutions especially when moving toward deeper waters.

3.1. Yards and engineering

Yards and engineering companies employ in total

approximately 1 200 persons in 2014 in offshore

business in Finland. In 2014 combined offshore

revenue is expected to be approximately 220

million euros of which around 95% is expected to

be exports, increasing from 70-80% share in 2009-

2012. The share of exports has increased rapidly

due to low activity in the Finnish multipurpose ice-

breaker investments and other offshore supply

vessels. The export share is expected to stay high in

the coming years as well.

’

Copyright © Arctech Helsinki Shipyard

Finnish offshore industry 2014

Page 21 (44)

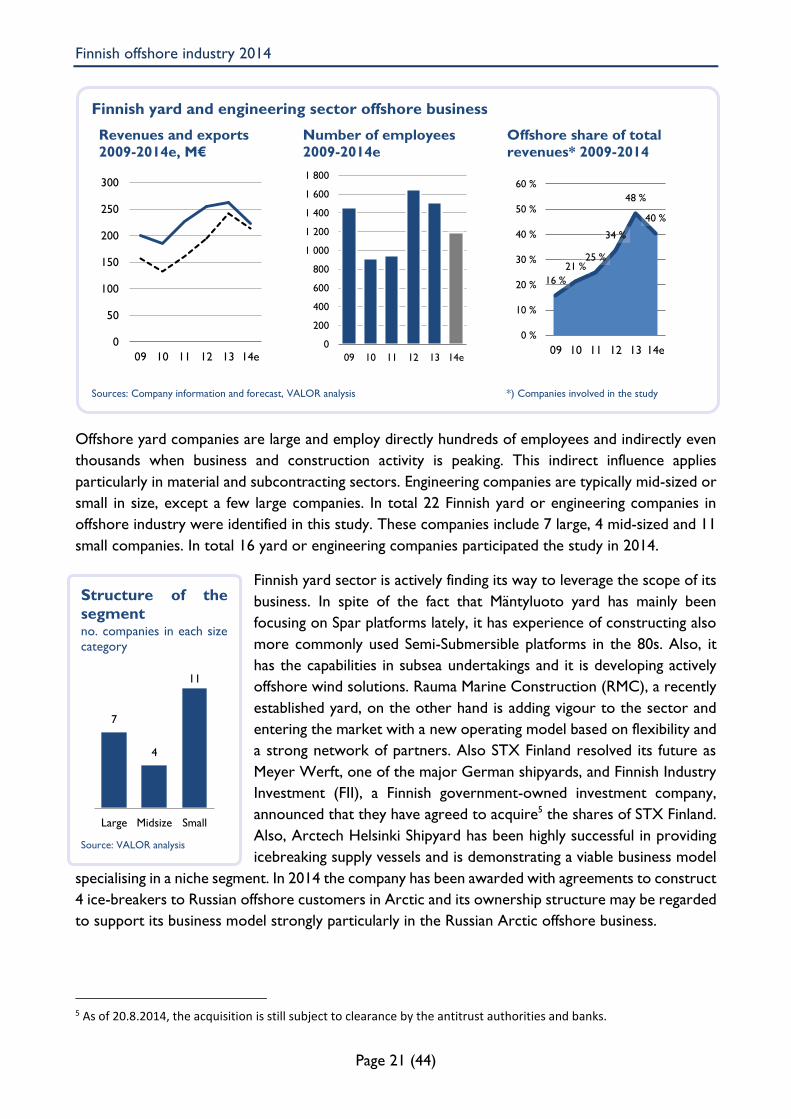

Offshore yard companies are large and employ directly hundreds of employees and indirectly even

thousands when business and construction activity is peaking. This indirect influence applies

particularly in material and subcontracting sectors. Engineering companies are typically mid-sized or

small in size, except a few large companies. In total 22 Finnish yard or engineering companies in

offshore industry were identified in this study. These companies include 7 large, 4 mid-sized and 11

small companies. In total 16 yard or engineering companies participated the study in 2014.

Finnish yard sector is actively finding its way to leverage the scope of its

business. In spite of the fact that Mäntyluoto yard has mainly been

focusing on Spar platforms lately, it has experience of constructing also

more commonly used Semi-Submersible platforms in the 80s. Also, it

has the capabilities in subsea undertakings and it is developing actively

offshore wind solutions. Rauma Marine Construction (RMC), a recently

established yard, on the other hand is adding vigour to the sector and

entering the market with a new operating model based on flexibility and

a strong network of partners. Also STX Finland resolved its future as

Meyer Werft, one of the major German shipyards, and Finnish Industry

Investment (FII), a Finnish government-owned investment company,

announced that they have agreed to acquire5 the shares of STX Finland.

Also, Arctech Helsinki Shipyard has been highly successful in providing

icebreaking supply vessels and is demonstrating a viable business model

specialising in a niche segment. In 2014 the company has been awarded with agreements to construct

4 ice-breakers to Russian offshore customers in Arctic and its ownership structure may be regarded

to support its business model strongly particularly in the Russian Arctic offshore business.

5 As of 20.8.2014, the acquisition is still subject to clearance by the antitrust authorities and banks.

Finnish yard and engineering sector offshore business

Revenues and exports

2009-2014e, M€

Number of employees

2009-2014e

Offshore share of total

revenues* 2009-2014

Sources: Company information and forecast, VALOR analysis *) Companies involved in the study

0

50

100

150

200

250

300

09 10 11 12 13 14e0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

09 10 11 12 13 14e

16 %

21 %25 %

34 %

48 %

40 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

09 10 11 12 13 14e

Structure of the

segment no. companies in each size

category

Source: VALOR analysis

7

4

11

Large Midsize Small

Finnish offshore industry 2014

Page 22 (44)

Engineering companies have traditionally been very inclined to the volatility in the local yard business.

However, Finnish engineering companies have become more and more independent of the Finnish

yards’ by building business on their competence and increasing international presence and customer

base. This has been particularly viable model as Finnish engineering companies have been able to

benefit from offshore industry’s global growth. Companies are particularly competitive in designing

complex, innovative and unique vessels and platforms for offshore and companies have also found

their special niches in which they have world-class expertise. For instance, Aker Arctic is globally

recognised for its services on ice-going ships and Arctic vessel design. Deltamarin is on the other

hand specialized in providing comprehensive engineering and project management services for

offshore projects but it also possess world-class knowledge e.g. in designing floating platforms and

vessels, including drilling vessels, floaters and special vessels. Additionally, many Finnish engineering

companies specialize in designing highly detailed offshore structures and systems, including e.g.

accommodation, electrification, HVAC or construction process lines.

In 2014 export share of combined revenues of yards and

engineering companies is expected to be over 90 percent, which

is a consequence of the fact that markets for Finnish engineering

and yard sector are international due to limited number of end

customers in Finland. Key export markets to Finnish yards and

engineering companies include North Sea, Northern Europe,

Russia and North America. Also increasingly importantly is Asia,

which is the hub for offshore construction activity, and is

particularly interesting for engineering companies. It is also

important to notice that since the markets for the products and

services are truly global in nature, also the shifts in the structure

of the export markets are very rapid.

3.2. Technology companies

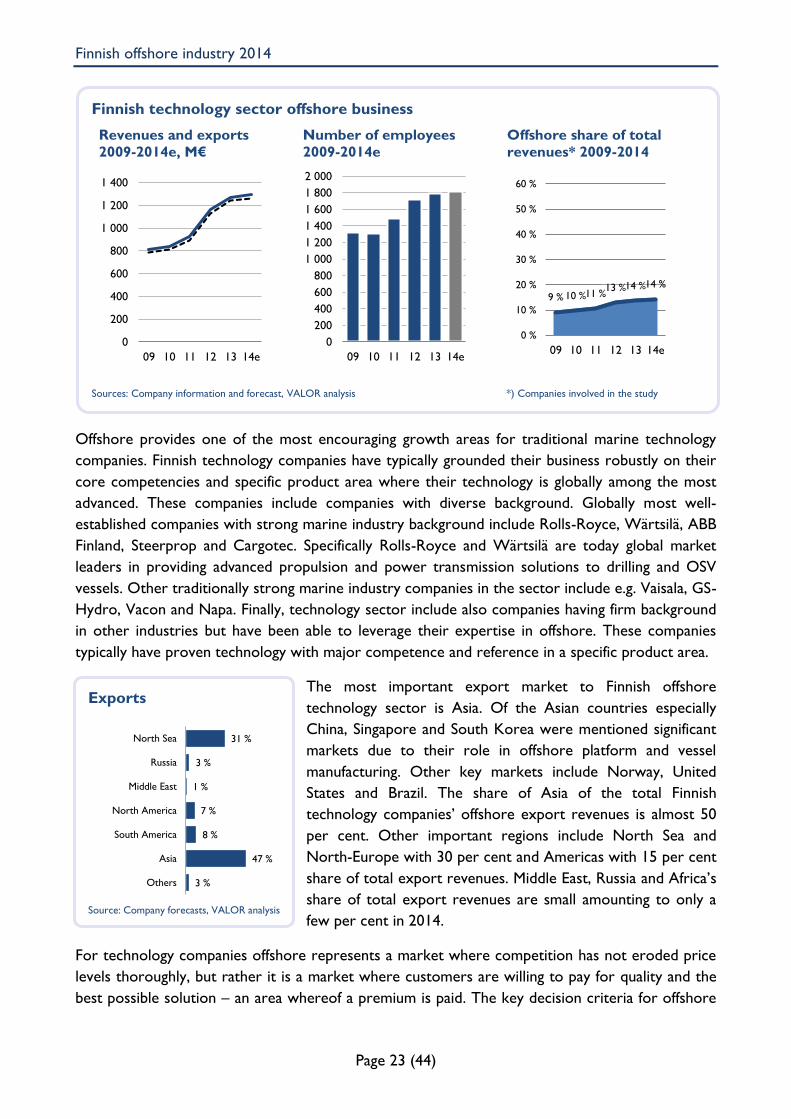

Finnish offshore technology companies are expected to employ approximately 1 800 person in 2014.

Companies are expected to generate about 1.30 billion euros in revenues annually in their offshore

business. Finnish companies are also very internationally oriented and each technology company is

exporting significant share of their revenue: Total exports amounted to 1.25 billion euros in this

sector in 2014, in other words, implying over 95 per cent of their business is in international markets.

Also offshore share of their total business has been growing steadily and according to the results of

the study today offshore equals to approximately 14 per cent of their total business compared to

only 9 per cent in 2009.

Exports

Source: Company forecasts, VALOR analysis

27 %

51 %

0 %

18 %

0 %

4 %

0 %

North Sea

Russia

Middle East

North America

South America

Asia

Others

Finnish offshore industry 2014

Page 23 (44)

Offshore provides one of the most encouraging growth areas for traditional marine technology

companies. Finnish technology companies have typically grounded their business robustly on their

core competencies and specific product area where their technology is globally among the most

advanced. These companies include companies with diverse background. Globally most well-

established companies with strong marine industry background include Rolls-Royce, Wärtsilä, ABB

Finland, Steerprop and Cargotec. Specifically Rolls-Royce and Wärtsilä are today global market

leaders in providing advanced propulsion and power transmission solutions to drilling and OSV

vessels. Other traditionally strong marine industry companies in the sector include e.g. Vaisala, GS-

Hydro, Vacon and Napa. Finally, technology sector include also companies having firm background

in other industries but have been able to leverage their expertise in offshore. These companies

typically have proven technology with major competence and reference in a specific product area.

The most important export market to Finnish offshore

technology sector is Asia. Of the Asian countries especially

China, Singapore and South Korea were mentioned significant

markets due to their role in offshore platform and vessel

manufacturing. Other key markets include Norway, United

States and Brazil. The share of Asia of the total Finnish

technology companies’ offshore export revenues is almost 50

per cent. Other important regions include North Sea and

North-Europe with 30 per cent and Americas with 15 per cent

share of total export revenues. Middle East, Russia and Africa’s

share of total export revenues are small amounting to only a

few per cent in 2014.

For technology companies offshore represents a market where competition has not eroded price

levels thoroughly, but rather it is a market where customers are willing to pay for quality and the

best possible solution – an area whereof a premium is paid. The key decision criteria for offshore

Finnish technology sector offshore business

Revenues and exports

2009-2014e, M€

Number of employees

2009-2014e

Offshore share of total

revenues* 2009-2014

Sources: Company information and forecast, VALOR analysis *) Companies involved in the study

0

200

400

600

800

1 000

1 200

1 400

09 10 11 12 13 14e

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

09 10 11 12 13 14e

9 % 10 %11 %13 %14 %14 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

09 10 11 12 13 14e

Exports

Source: Company forecasts, VALOR analysis

31 %

3 %

1 %

7 %

8 %

47 %

3 %

North Sea

Russia

Middle East

North America

South America

Asia

Others

Finnish offshore industry 2014

Page 24 (44)

customers include not only health, security, environment and quality (HSEQ) considerations but

also aspects such as product reliability, traceability, innovation and quality. This is why offshore is

seen as an attractive market for Finnish companies as they represent globally renowned high-end

technology solution and innovation sector.

In the study, in total 38 Finnish technology companies were identified

operating in offshore. Companies include 12 large, 19 mid-sized and

7 small companies. Of the 38 identified companies, 18 companies also

participated in the study. These 18 companies represent 95 of the

estimated total technology sector revenues. Finnish offshore

technology companies are mostly either large or mid-sized companies.

However, this tendency for them to be relatively large in size is

explained by the fact that companies need to be internationally

recognised and credible in order to be included in supplier short-lists

for the offshore projects and deliveries. For example, earlier

references, especially in offshore project, are considered essential for

technology companies in order to show they have proven solutions

available for offshore sector. Also it is becoming more and more

important to have a service network world-wide in order to increase

product availability in offshore.

To make a final note, a few Finnish offshore technology companies are established almost entirely

on global basis and do not have almost any operations in offshore in Finland. For example, Cagrotec’s

offshore business is entirely based abroad and employees, assets and service networks are located

in markets near offshore markets in e.g. Norway, Americas and Asia. Accordingly, by definition these

companies are excluded from the figures of this study and the corresponding business abroad is not

included in the Finnish offshore industry numbers. These born global companies, however, are

supporting the development of offshore knowledge and expertise in Finland, which is contributing

to the Finnish offshore industry.

3.3. Subcontractors

In 2014 subcontractors are expected to employ approximately 1 150 employees according to the

study. The total offshore revenues of the subcontractor sector are expected to amount to 230

million euros, of which around 100 million euros is exports.

Historically subcontractors have mostly relied on serving domestic customers mostly particularly in

Finnish in yard and technology sectors and export revenues have been modest. In 2010 exports

accounted to some 30 per cent of the offshore revenues, while the corresponding figure was almost

50 per cent in 2013. This implies that also Finnish subcontractors have been able to build

international business based on their competence by finding their market and customers abroad

recently especially in Norway. Based on the interview and questionnaire comments, Finnish

subcontractors regard specifically Norwegian very attractive market in the future as well and they

are actively looking for growth opportunities in the market. Finnish subcontractors are particularly

Structure of the

segment no. companies in each size

category

Source: VALOR analysis

12

19

7

Large Midsize Small

Finnish offshore industry 2014

Page 25 (44)

competitive in components and providing labour hire services for the construction and other project

in the market.

Many subcontractors are very important partners for large companies. Often large companies have

their own networks of trusted subcontractors backing them in offshore undertakings. For example,

Technip has cooperated actively with over 100 subcontractors during offshore undertakings in

Mäntyluoto yard and STX instead has its own network of subcontractors with marine based

background. Also technology companies, including Wärtsilä and Rolls-Royce Finland, have their own

network of proven workshops as partners. Often technology companies are willing to investing in

their subcontractor partners in order to support their own business. Subcontractors are significant

employers and they employ 25 per cent of total offshore employees in Finland making the sector

third largest employer in the industry alongside technology and yard sectors.

Finnish subcontractors are especially competitive in

offshore in heavy workshop engineering, welding,

assembly, machining, material coating and heat

treatment work, providing labour hire for projects,

and supplying components all the way from

engineering to assembly including e.g. fire protection

door, electrical equipment and other product as

comprehensive project deliveries. Majority of

subcontractors’ deliveries include projects with

detailed specifications and blueprint from

customers. Additionally, subcontractors have been

able to further commercialise their advanced products and services so that in practice they have

moved up in the hierarchy of supply chain and to become a company resembling a technology

provider. For example, in hydraulic heavy workshop engineering products and casted propellers are

Finnish subcontractor sector offshore business

Revenues and exports

2009-2014e, M€

Number of employees

2009-2014e

Offshore share of total

revenues* 2009-2014

Sources: Company information and forecast, VALOR analysis *) Companies involved in the study

0

50

100

150

200

250

09 10 11 12 13 14e

0

200

400

600

800

1 000

1 200

1 400

09 10 11 12 13 14e

18 %

28 %

19 %21 %

25 %

35 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

09 10 11 12 13 14e

’

Copyright © Telatek

Finnish offshore industry 2014

Page 26 (44)

products in which Finnish subcontractors have become strategic partners to selected technology

companies not only domestically but also internationally.

Finnish offshore subcontractors include for example, Hollming Works that is a subcontractor

specialised in manufacturing of medium weight and heavy engineering products, Leinovalu which is

a renowned in custom-made deliveries for advanced casted components and Telatek who is

specialised in manufacturing and repairing large, massive workpieces and working in demanding

condition. ATA Gears manufactures highly customized spiral bevel gears and has become of the

most renowned manufacturers of their special products in the world and has a position close to a

technology company in the supply chain.

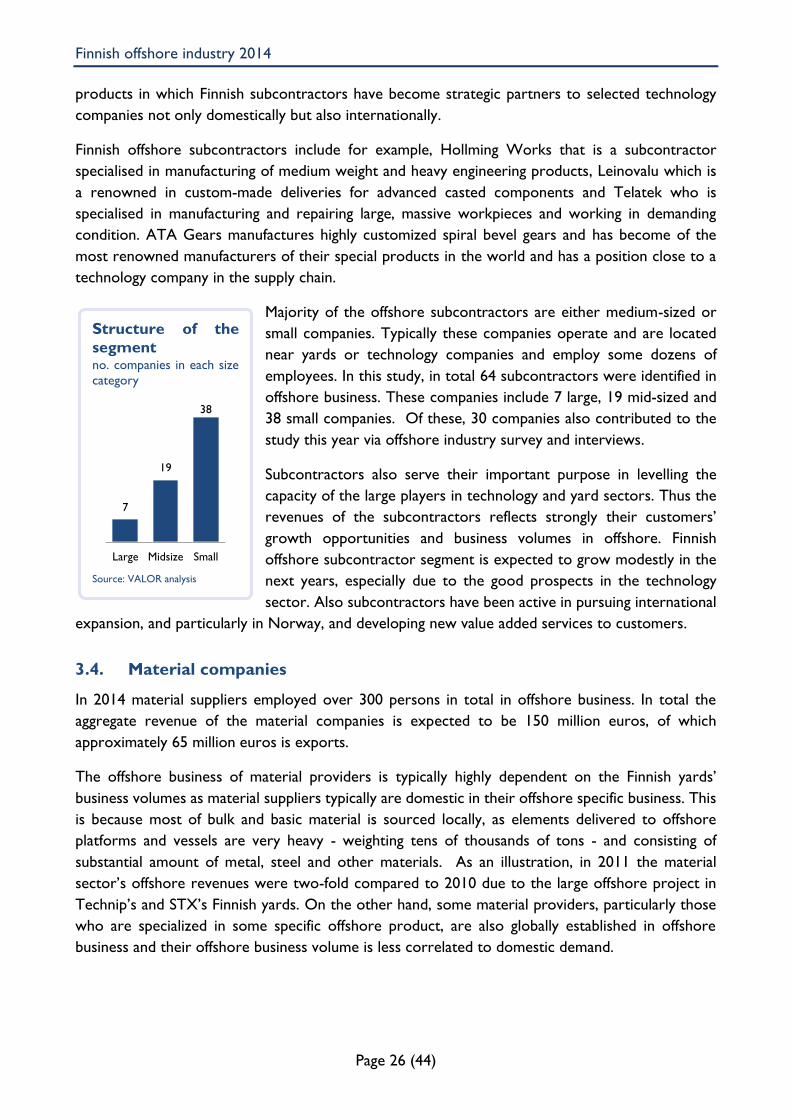

Majority of the offshore subcontractors are either medium-sized or

small companies. Typically these companies operate and are located

near yards or technology companies and employ some dozens of

employees. In this study, in total 64 subcontractors were identified in

offshore business. These companies include 7 large, 19 mid-sized and

38 small companies. Of these, 30 companies also contributed to the

study this year via offshore industry survey and interviews.

Subcontractors also serve their important purpose in levelling the

capacity of the large players in technology and yard sectors. Thus the

revenues of the subcontractors reflects strongly their customers’

growth opportunities and business volumes in offshore. Finnish

offshore subcontractor segment is expected to grow modestly in the

next years, especially due to the good prospects in the technology

sector. Also subcontractors have been active in pursuing international

expansion, and particularly in Norway, and developing new value added services to customers.

3.4. Material companies

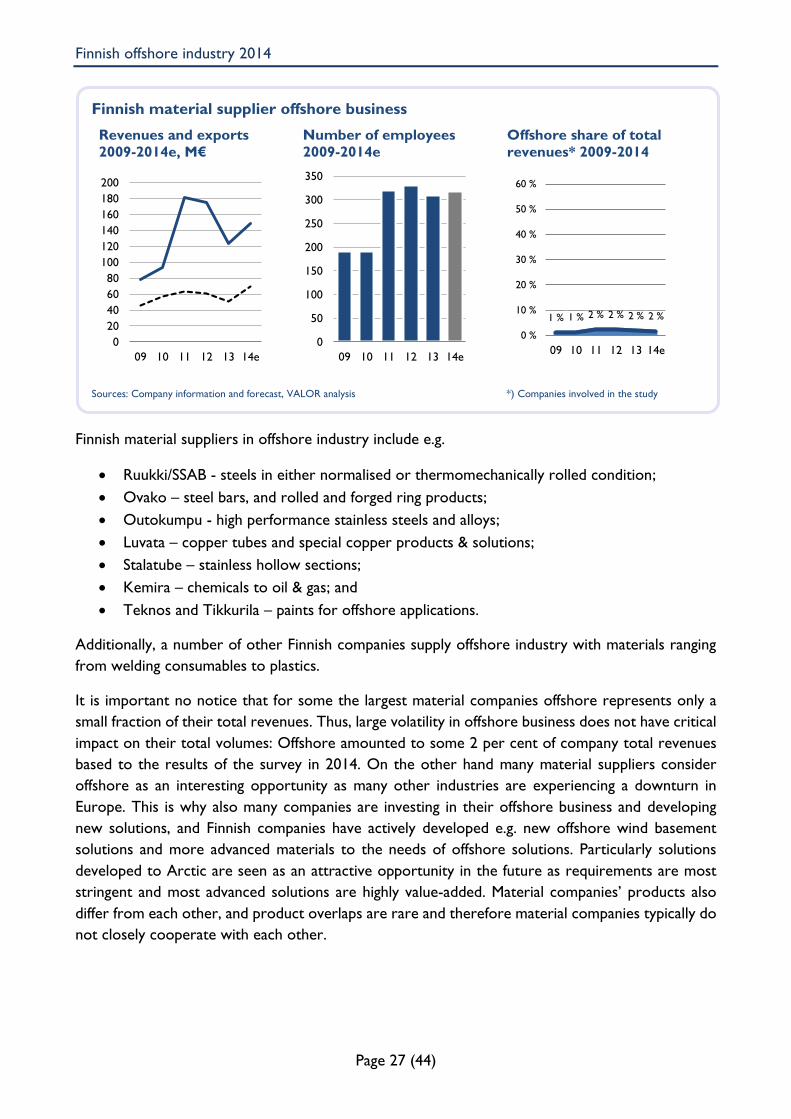

In 2014 material suppliers employed over 300 persons in total in offshore business. In total the

aggregate revenue of the material companies is expected to be 150 million euros, of which

approximately 65 million euros is exports.

The offshore business of material providers is typically highly dependent on the Finnish yards’

business volumes as material suppliers typically are domestic in their offshore specific business. This

is because most of bulk and basic material is sourced locally, as elements delivered to offshore

platforms and vessels are very heavy - weighting tens of thousands of tons - and consisting of

substantial amount of metal, steel and other materials. As an illustration, in 2011 the material

sector’s offshore revenues were two-fold compared to 2010 due to the large offshore project in

Technip’s and STX’s Finnish yards. On the other hand, some material providers, particularly those

who are specialized in some specific offshore product, are also globally established in offshore

business and their offshore business volume is less correlated to domestic demand.

Structure of the

segment no. companies in each size

category

Source: VALOR analysis

7

19

38

Large Midsize Small

Finnish offshore industry 2014

Page 27 (44)

Finnish material suppliers in offshore industry include e.g.

Ruukki/SSAB - steels in either normalised or thermomechanically rolled condition;

Ovako – steel bars, and rolled and forged ring products;

Outokumpu - high performance stainless steels and alloys;

Luvata – copper tubes and special copper products & solutions;

Stalatube – stainless hollow sections;

Kemira – chemicals to oil & gas; and

Teknos and Tikkurila – paints for offshore applications.

Additionally, a number of other Finnish companies supply offshore industry with materials ranging

from welding consumables to plastics.

It is important no notice that for some the largest material companies offshore represents only a

small fraction of their total revenues. Thus, large volatility in offshore business does not have critical

impact on their total volumes: Offshore amounted to some 2 per cent of company total revenues

based to the results of the survey in 2014. On the other hand many material suppliers consider

offshore as an interesting opportunity as many other industries are experiencing a downturn in

Europe. This is why also many companies are investing in their offshore business and developing

new solutions, and Finnish companies have actively developed e.g. new offshore wind basement

solutions and more advanced materials to the needs of offshore solutions. Particularly solutions

developed to Arctic are seen as an attractive opportunity in the future as requirements are most

stringent and most advanced solutions are highly value-added. Material companies’ products also

differ from each other, and product overlaps are rare and therefore material companies typically do

not closely cooperate with each other.

Finnish material supplier offshore business

Revenues and exports

2009-2014e, M€

Number of employees

2009-2014e

Offshore share of total

revenues* 2009-2014

Sources: Company information and forecast, VALOR analysis *) Companies involved in the study

0

20

40

60

80

100

120

140

160

180

200

09 10 11 12 13 14e

0

50

100

150

200

250

300

350

09 10 11 12 13 14e

1 % 1 % 2 % 2 % 2 % 2 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

09 10 11 12 13 14e

Finnish offshore industry 2014

Page 28 (44)

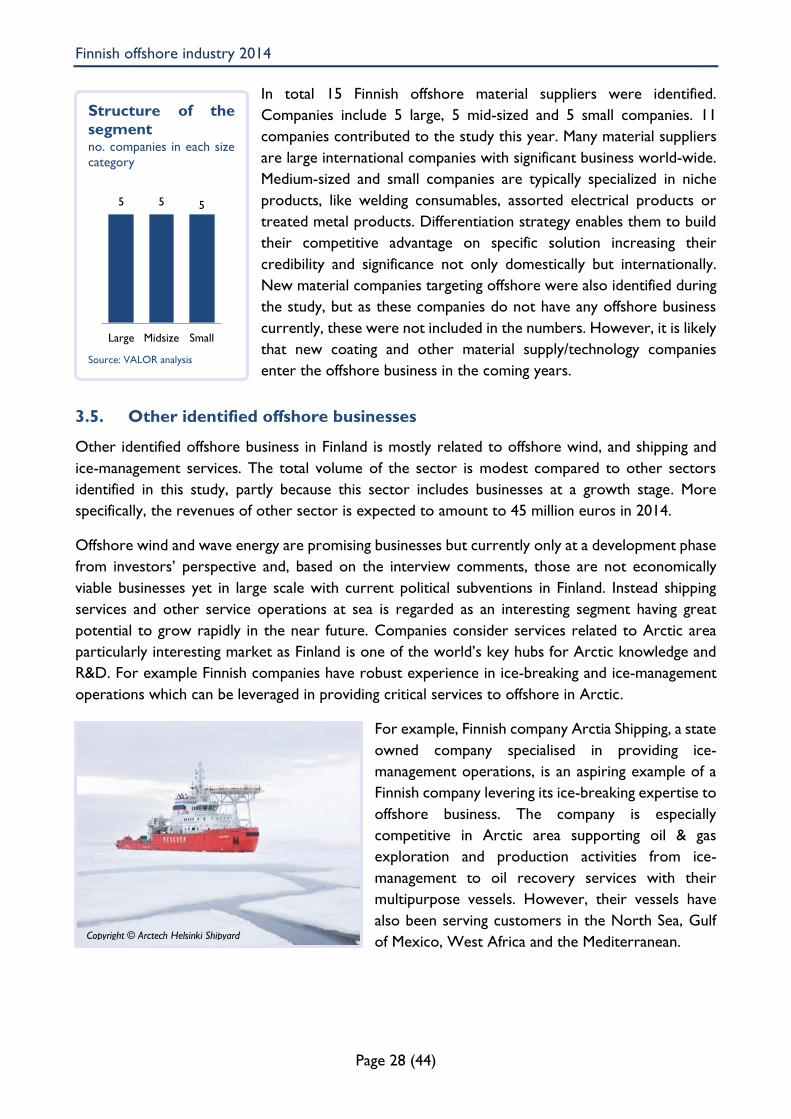

In total 15 Finnish offshore material suppliers were identified.

Companies include 5 large, 5 mid-sized and 5 small companies. 11

companies contributed to the study this year. Many material suppliers

are large international companies with significant business world-wide.

Medium-sized and small companies are typically specialized in niche

products, like welding consumables, assorted electrical products or

treated metal products. Differentiation strategy enables them to build

their competitive advantage on specific solution increasing their

credibility and significance not only domestically but internationally.

New material companies targeting offshore were also identified during

the study, but as these companies do not have any offshore business

currently, these were not included in the numbers. However, it is likely

that new coating and other material supply/technology companies

enter the offshore business in the coming years.

3.5. Other identified offshore businesses

Other identified offshore business in Finland is mostly related to offshore wind, and shipping and

ice-management services. The total volume of the sector is modest compared to other sectors

identified in this study, partly because this sector includes businesses at a growth stage. More

specifically, the revenues of other sector is expected to amount to 45 million euros in 2014.

Offshore wind and wave energy are promising businesses but currently only at a development phase

from investors’ perspective and, based on the interview comments, those are not economically

viable businesses yet in large scale with current political subventions in Finland. Instead shipping

services and other service operations at sea is regarded as an interesting segment having great