Embed Size (px)

Citation preview

The Financial Reporting Environment, Reporting Discretion, and Earnings Management: US GAAP vs. IFRS

Mark Evans Indiana University

Richard Houston University of Alabama

Michael Peters Villanova University

Jamie Pratt* Indiana University

October 2012

* Corresponding author. Kelley School of Business, 1309 E. 10th Street, Bloomington, Indiana 47405, email: [email protected]. We appreciate comments received from participants at the 2012 Midwest Summer Accounting Research Conference at the University of Minnesota and an Indiana University Brown Bag Workshop.

The Financial Reporting Environment, Reporting Discretion, and Earnings Management: US GAAP vs. IFRS

ABSTRACT

In this study we examine the effect of characteristics of the financial reporting environment on the level of financial reporting discretion perceived by managers and the likelihood and method of earnings management. We focus primarily on the effects of financial reporting standards (US GAAP vs. IFRS), while simultaneously considering other important characteristics of the reporting environment and how they interact with the standards—firm domicile, firm ownership, audit quality, firm size, and the direction of the earnings adjustment. Using a web-based case completed by 615 experienced financial officers from the US, Europe and Asia, we find that financial officers under IFRS perceive higher levels of reporting discretion than those under U.S. GAAP, and the perception of higher levels of reporting discretion leads to both a greater likelihood of earnings management and a preference for the use of accruals over real methods. While we generate no evidence that IFRS, compared to U.S. GAAP, leads to a greater likelihood of earnings management, we do observe that U.S. firms under U.S. GAAP show a strong preference for real activities over accruals methods, while all other firms (U.S. firms under IFRS and non-U.S. firms) are either indifferent between the two methods or prefer accruals. We also find that firms adjusting earnings upward strongly prefer real activities, while firms adjusting earnings downward are either indifferent (US GAAP users) or prefer accruals (IFRS users). These findings contribute to research concerning whether differences in financial reporting environments are associated with differences in the perception of allowable reporting discretion, and the inclination to manage earnings via real activities or accruals. They also suggest that adopting IFRS in the US may have little effect on the overall level of earnings management, but instead may encourage firms to substitute accruals for real activities when managing earnings. Keywords: Accounting standards; earnings management; regulation JEL Codes: M40; M41; M48

2

I. INTRODUCTION

In this study we examine the effect of characteristics of the financial reporting

environment on the level of financial reporting discretion perceived by managers and the

likelihood and method of earnings management. We focus primarily on the effects of financial

reporting standards (US GAAP vs. IFRS), while simultaneously considering other important

characteristics of the reporting environment and how they interact with the standards. These

characteristics include firm domicile (US vs. non-US), firm ownership (public vs. private), audit

quality (Big 4 vs. non-Big 4), firm size, and the direction of the earnings adjustment (upward vs.

downward).1

We collected data using a web-based exercise completed by 615 experienced financial

officers whose firms report under U.S. GAAP or IFRS and are domiciled in the U.S., Europe, or

Asia. Participants completed a short case in which they were asked to assume that their firms

were approaching year-end, and were provided with monetary values for both expected

unmanaged earnings (the firm’s best guess of what earnings would be if left unadjusted) and an

important benchmark. We then asked participants whether in this situation their entities would

use allowable reporting discretion to increase, decrease, or not adjust earnings and, if they

thought their entities would adjust earnings, by how much.2 We also asked participants to

indicate which methods (real vs. accruals) their entities would use to adjust earnings as well as

various questions about their entities (e.g., reporting system, auditors, size, ownership, and

benchmarks) and themselves (e.g., age, experience, and certification).

1 The direction of the earnings adjustment is not a characteristic of the reporting environment per se, but we argue later that the regulatory pressures controlling upward earnings management are quite different from those controlling downward earnings management. 2 Allowable reporting discretion is defined as the level of reporting discretion that the financial officer believes can be exercised either through operating, investing, or financing decisions (real activities) or accounting choices (accruals) without violating generally accepted accounting principles.

3

We report four primary findings: (1) compared to financial officers under US GAAP,

financial officers under IFRS perceived greater levels of allowable reporting discretion; (2)

greater levels of perceived allowable reporting discretion were associated with a greater

likelihood of earnings management and a preference for accruals methods over real activities; (3)

financial officers from US firms under US GAAP indicated that their firms preferred real

methods for earnings management, while non-US officers and those under IFRS (US and non-

US firms) indicated that their firms were either indifferent between real and accruals methods or

preferred accruals methods; and (4) compared to firms adjusting earnings upward, firms

adjusting earnings downward relied more heavily on accruals vis-à-vis real methods.

These results contribute to research concerning the effects of regulation on earnings

management (Leuz, Nanda, Wysocki 2003; Lang, Raedy, and Wilson 2006) and the use of real

vs. accruals methods (Ewert and Wagenhofer 2005), while identifying a possible consequence

associated with the adoption of IFRS in the U.S. (DeFond 2010; Pownall and Schipper 1999).

Our evidence suggests, for example, that adopting IFRS in the US would allow greater levels of

reporting discretion, but would not necessarily lead to more earnings management. Instead, it

may lead to differences in the methods used to manage earnings - more accruals and less real

activities. A related implication for standard-setters is that simply tightening accounting

standards may not lead to less earnings management; it may lead instead to less reliance on

accruals and more reliance on real activities.

We build on archival research that examines reporting discretion across different

domiciles and the value relevance of earnings across different accounting standards. Leuz et al.

(2003) and Lang et al. (2006), for example, show that firms located in highly regulated domiciles

are less likely to engage in earnings management by accruals; other studies show U.S. GAAP

4

earnings to be of higher quality than earnings determined using IFRS (Barth, Landsman, Lang,

and Williams 2012); and still others show that US GAAP and IFRS lead to comparable levels of

earnings quality (Gordon et al., 2010; Hughes and Sander 2008). This line of research examines

earnings management via accruals, and we extend it by studying both real and accruals methods,

allowing us to identify whether management reacts to different reporting environments by

changing the likelihood of earnings management and/or changing the method of earnings

management. In addition, these studies focus primarily on income-increasing adjustments. We

examine both earnings-increasing and earnings-decreasing adjustments, and find that real

activities are preferred when increasing earnings, while accruals methods are preferred when

decreasing earnings.

Our study also builds on existing research examining whether and how firms trade-off

real and accruals methods in response to changes in the level of regulation (Cohen et al., 2008;

Cohen and Zarowin 2010). This research focuses on U.S. firms under U.S. GAAP, and

considers regulatory changes created by SOX (Cohen et al., 2008). We also examine whether

and how firms tradeoff real and accruals methods in response to differences in the reporting

environment, but we focus on the effects of IFRS vs. US GAAP, and simultaneously consider the

main and interactive effects related to firm domicile, the direction of the earnings adjustment,

firm ownership, quality of auditor, and firm size – all of which represent important

characteristics of the reporting environment faced by the firm. Hail et al. (2010a, 2010b) note

that the effects of changes in accounting standards on earnings management may not be

predictable due to the variety of factors contributing to the level of regulation faced by the firm.

Our extension addresses this issue by simultaneously examining the effects of a number of

reporting environment characteristics, and we find that they interact in determining the

5

likelihood and method of earnings management. US firms under US GAAP, for example, appear

to prefer real activities, while all other firms (US firms under IFRS and non-US firms under both

US GAAP and IFRS) are either indifferent between real activities and accruals or prefer

accruals.

We base our method of data collection on Graham, Harvey, and Rajgopal (2005) by

asking experienced financial officers to complete a web-based exercise. We expand on Graham

et al. (2005) by including firms in non-U.S. settings, firms that report using IFRS, and asking

financial officers to respond to a case that includes manipulations of the setting designed to

induce firms to adjust earnings upward in one condition and downward in another. These

differences allow us to investigate whether many of the Graham et al. (2005) findings hold in

settings not included in their study. For example, Graham et al. (2005) find that U.S. managers

strongly prefer adjusting earnings via real activities over accruals. We replicate their results, but

extend them by showing that this conclusion may be limited to U.S. firms operating under U.S.

GAAP adjusting earnings upward. U.S. firms operating under IFRS, non-U.S. firms, and firms

adjusting earnings downward all exhibited a lower preference for real activities and, in some

cases, actually preferred accruals.

Our approach to data collection also allows us to avoid certain weaknesses inherent in

related archival studies. Dechow et al. (2010) notes, for example, that archival methods must

rely on indirect measures of earnings management, making it difficult to separate measures of

earnings management from measures of general performance. Key constructs such as

unmanaged earnings and the benchmarks most important to the firm must be measured

indirectly. DeFond (2010) argues further that this issue, a construct validity problem, may not

6

be resolvable with archival methods because actual performance measures are unobservable.3

Ewert and Wagenhofer (2005, 1115) point out that archival research often ignores adjustments

via real activities and that this exclusion likely affects the estimation of earnings management

and may overestimate the impact of various institutional safeguards to control it. Our design

circumvents these difficulties by clearly identifying unmanaged earnings, asking financial

officers to consider benchmarks important to their firms, and eliciting direct measures of the

direction, amount, and method of the earnings adjustments.4

In the next section we expand on the related literature, followed by the development of

the hypotheses. Subsequent sections describe the experimental design, results, and conclusions.

II. LITERATURE REVIEW

Earnings management occurs when management uses either its reporting discretion

(accruals) or its influence over operating, investing, or financing decisions (real activities) to

achieve a desired reporting outcome. The literature in this area is extensive and includes both

archival and experimental methods (e.g., see Healy and Wahlen 1999; Fields et al. 2001; Libby

and Seybert 2009). Three streams of research are particularly relevant to this study: (1)

differences in reporting quality between U.S. GAAP and IFRS; (2) the use of real and accruals

earnings management; and (3) the effects of principles vs. rules-based accounting.

3 Schipper (1989), Kasznik (1999), McNichols (2000), Dechow and Skinner (2000), Fields et al. (2001), Lev (2003), Schipper and Vincent (2003), Dechow et al. (2003), and Ayers et al. (2006) all discuss difficulties inherent in archival studies that attempt to infer various dimensions of reporting discretion and earnings management. Healy and Wahlen (1999) and Fields et al. (2001), for example, argue that an important limitation of archival studies is the difficulty of determining whether the measure of earnings management is attributable to operational or reporting decisions. 4 In the parlance of List (2011) and Harrison and List (2004), our study uses a “framed field experiment,” which mimics a lab experiment, except that it uses participants “drawn from the market of interest” (experienced financial officers) and conducts the study “in the natural environment of the subject” (participants make accounting and operating decisions in response to relevant expectations; List 2011, 4-5).

7

With regard to the first stream of literature, archival-based empirical research generally

shows that firms in countries using IFRS tend to engage in more earnings management than

firms in countries using U.S. GAAP. Barth et al. (2012) find that U.S. firms using U.S. GAAP

exhibit higher levels of accounting quality than non-U.S. firms using IFRS. Alford et al. (1993),

Land and Lang (2002), and Lang et al. (2003) generally show that U.S. firms using U.S. GAAP

engage in less earnings management than non-U.S. firms, and Lang et al. (2003) show further

that non-U.S. firms cross-listed in the U.S. practice less earnings management than non-U.S.

firms not cross-listed in the U.S.

In an attempt to separate the effects of differences in accounting standards from the

effects of differences in jurisdictions, Lang et al. (2006) and Bradshaw and Miller (2008)

compared measures of accounting quality of U.S. firms reporting under U.S. GAAP to that of

non-US firms required to file SEC Form 20-F reconciliations. These studies either found or

assumed that U.S. firms generally reported higher quality information, suggesting differences

across countries in how accounting standards are applied. Overall, this research area suggests

that earnings quality is greatest in U.S. firms operating under U.S. GAAP, followed by non-U.S.

firms cross-listed on U.S. exchanges, and non-U.S. firms operating under either IFRS or local

GAAP (Bradshaw and Miller 2008).5

The second stream of research—the use of real activities and accruals methods—can be

divided into two groups. The first group examines the relative preferences in general for real and

accruals earnings management. Graham et al. (2005) examine a wide range of issues, including

reporting discretion, and focus on U.S. managers, who primarily work for publicly-traded firms,

operate under U.S. GAAP, and adjust earnings upward. They find that this group prefers real

5 In contrast, in a working paper, Ahmed, Neel, and Wang (2012) find that accounting quality decreases after mandatory adoption of IFRS across 20 countries.

8

activities over accruals methods. Nelson et al. (2002) surveyed auditors and asked them to recall

client attempts to manage earnings. The auditors were more likely to recall clients’ use of

accruals over real activities. The authors recognize, however, that real earnings management is

unlikely to be a major concern for auditors because it involves no accounting manipulation.

In a review of the behavioral research in this area, Libby and Seybert (2009) note that

much evidence exists that management engages in both real and accruals methods, but none

documents conditions under which each method is preferred. However, a recent archival paper

(Zang 2012) identifies differential costs between real and accruals earnings management and

provides evidence that based on these costs firms tradeoff the use of real and accruals methods.

Another group of studies focuses on the use of real vs. accruals methods in response to

changes in the regulatory environment. Several papers suggest that tighter reporting standards

may cause firms to substitute real activities for accruals methods (Schipper 2003; Demski 2004;

and Ewert and Wagenhofer 2005). Additional research provides archival-based empirical

support for this form of substitution based on changes due to SOX regulations (Cohen et al.

2008) and in the presence of seasoned equity offerings (Cohen and Zarowin 2010). Two recent

working papers address real and accruals earnings management in an international setting.

Enomoto, Kimura, and Yamaguchi (2012) find that real activities are preferred over accruals

methods in countries where investor protection is strong; and Ipino and Parbonetti (2011) find a

decrease in accruals methods after mandatory IFRS adoption, but only in countries with strong

legal enforcement.

The third stream of research examines the impact of rules and principles-based

accounting systems on the audit function and financial reporting discretion. Trompeter (1994),

Hronsky and Houghton (2001), and Ng and Tan (2003), for example, show that auditors are

9

more likely to allow earnings management when transactions involve less precise accounting

standards. Mayhew et al. (2001) suggest that earnings management via accruals methods is more

likely under principles-based systems because it is easier to justify estimates to auditors when

standards are less precise. Hackenbrack and Nelson (1996) find that auditors also use the

imprecision in accounting standards to justify an accounting treatment consistent with their

incentives. Kadous and Mercer (2012) show that jurors return fewer verdicts for violations of

imprecise standards, and Backof, Bamber, and Carpenter (2011) find that under IFRS auditors

are more likely to agree with management earnings adjustments via accruals methods. These

findings generally support the argument that more discretionary, principles-based accounting

systems impose lower regulatory costs, yielding more earnings management via accruals

methods.6

Our study contributes to the research summarized above by directly documenting the

presumption that financial officers under IFRS perceive higher levels of allowable reporting

discretion than financial officers under U.S. GAAP. We are also the first to provide evidence

that adopting IFRS in the U.S. may not affect the overall likelihood of earnings management, but

instead may affect the mix of earnings management methods used. That is, firms may substitute

accruals for real activities when faced with the additional allowable reporting discretion

introduced by IFRS, a more principles-based accounting system. We also show that the

preference for accruals vs. real activities depends on an interaction between the system of

financial standards and the domicile of the firm. US firms under US GAAP prefer adjusting

earnings via real activities, while non-US firms and firms under IFRS (US and non-US) are

either indifferent or prefer accruals methods. Finally, we introduce to the literature the finding

6 In contrast, in a working paper, Folsom, Hribar, Mergenthaler, and Peterson (2012) provide evidence that accounting quality—as measured by informativeness, persistence, and predictive ability—increases in more principles-based GAAP standards.

10

that management’s preference for real vs. accruals methods depends on the direction of the

earnings adjustment – income-increasing adjustments rely primarily on real activities; income-

decreasing adjustments rely primarily on accruals methods.

III. THEORY AND HYPOTHESES

The financial reporting environment imposes constraints on management’s reporting

discretion, and the effectiveness of these constraints is determined by two dimensions. The

environment must first provide a means of identifying when a reporting violation has occurred

and, in the event that a violation is identified, the environment must include a significant

expected consequence to the violating firm. Leeway (or lack of guidance, monitoring, or

enforcement) in either of these two dimensions increases the extent to which management

perceives that it is allowed to use reporting discretion to achieve performance goals.

Each firm faces a unique reporting environment, and level of allowable reporting

discretion, determined by the characteristics of that environment. The set of reporting standards

under which a firm operates (U.S. GAAP or IFRS) represents one important element because it

provides a means for identifying when a reporting violation has occurred. Other important

elements of the reporting environment include firm domicile, firm ownership, auditor quality,

firm size, and even the direction of earnings adjustment because each influences the level of

allowable reporting discretion by affecting either the means of identifying a reporting violation

or the expected consequence.

We assume that management has incentives to use reporting discretion to adjust earnings

to achieve important benchmarks, and two kinds of discretion are available to do so: (1)

discretion over reporting decisions and (2) discretion over operating, investing, and financing

11

decisions. Earnings management via accruals methods is the use of reporting discretion to

achieve important benchmarks, and earnings management via real activities is the use of

discretion over operating, investing, and/or financing decisions to achieve important

benchmarks.

Firm management can respond to different levels of allowable reporting discretion by

changing its willingness to engage in earnings management and/or the mix of the methods used

to do so. In environments where allowable reporting discretion is relatively high, management

will be more willing to engage in earnings management and will prefer accruals over real

activities because accruals are precise and can be delayed until the end of the reporting period.

Adjustments via real activities must be implemented well in advance of year end, when

uncertainty exists with respect to both the effect on reported earnings of the chosen strategy and

the level of reported earnings if left unmanaged. Further, accruals do not directly disturb the

firm’s cash flows, while real activities typically do.

In reporting environments where allowable reporting discretion is relatively low,

management will practice earnings management less via accruals methods, relying more heavily

on real activities. The additional reporting regulations designed to restrict reporting discretion

force management to find a method other than accruals to achieve its reporting goals and

encourage the structuring of transactions around the “bright-line” standards. Consequently,

management will substitute real activities for accruals.7

A consensus exists that IFRS is more principles-based than U.S. GAAP (SEC 2003;

Dichev et al. 2012). Assuming that principles require greater use of management judgment than

rules, we predict that management of firms under IFRS perceives greater levels of allowable

7 These arguments are largely based on predictions from the model established by Ewert and Wagenhofer (2005), and Zang (2012) used many of these same arguments.

12

reporting discretion than management of firms under US GAAP. In addition, consistent with the

arguments articulated in this section, we predict that the likelihood of earnings management—

and the preference for accruals methods over real activities—is increasing in the level of

allowable reporting discretion perceived by management.

H1: Management of firms operating under IFRS perceives higher levels of allowable reporting discretion than management of firms operating under U.S. GAAP. H2: Firms whose management perceives higher levels of allowable reporting discretion are more likely to adjust earnings to meet benchmarks and tend to rely more heavily on accruals methods—and less heavily on real activities—than firms whose management perceives lower levels of allowable reporting discretion. H1 predicts that IFRS allows more reporting discretion than US GAAP, while H2

predicts that higher levels of reporting discretion lead to a greater likelihood of earnings

management and a preference for accruals methods over real activities. Consequently,

we predict that, compared to US GAAP, IFRS will lead to a greater likelihood of

earnings management and a preference for accruals over real activities.

H3: Firms operating under IFRS are more likely to adjust earnings to meet benchmarks and rely more heavily on accruals—and less heavily on real activities—than firms operating under U.S. GAAP.

IV. EXPERIMENTAL DESIGN

Participants

Participants consisted of 615 financial officers obtained from a business publication’s

(BP) research database, 191 (31 percent) of whom indicated that in the situation described in the

13

case their firm would adjust earnings.8 Table 1 reports descriptive statistics grouped by U.S.

GAAP and IFRS firms, and Table 2 reports descriptive statistics grouped by participants not

choosing to adjust earnings and participants choosing to adjust earnings. Panel A of Table 1

shows that 294 participants (48 percent) worked for U.S. firms and 321 (52 percent) worked for

non-U.S. firms (about evenly split between Europe and Asia).9 Both groups were dominated by

senior financial officers (almost 65 percent were CFOs, VPs or Directors of Finance).

Participants from both groups tended to be in their low to mid-forties; predominantly male (over

83 percent); have a professional accounting certification (almost 70 percent); and highly

experienced (about 20 years).

[Insert Tables 1 and 2 here]

Panel B of Table 1 shows that the firms varied from less than $100 million in sales (32

percent) to over $1 billion (21 percent); the reporting entity of about 61 percent was the firm as a

whole; over 76 percent were audited by a Big 4 auditor; and (not tabulated) manufacturing was

the industry most highly represented, followed by wholesale/retail, financial institutions, and

technology. Participants from the IFRS firms were younger (42 years vs. 44 years) and less

experienced (18 years vs. 21 years); and the IFRS firms tended to be smaller (46 percent with

<$100 million in sales vs. 24 percent for U.S. GAAP firms). Approximately 51 percent of the

firms were publicly-traded.

8 This percentage is similar to results in Burgstahler and Dichev (1997), who estimate the frequency with which firms use EM to avoid earnings decreases at 8-12 percent and to avoid losses at 30-44 percent, and Dichev et al. (2012), who find that CFOs believe about 20% of firms manage earnings in any given period. 9 European participants mostly were Northern European, with more than half from France, Germany, Spain, and the United Kingdom (other countries represented include Belgium, Denmark, Finland, Ireland, Switzerland, and Sweden). The data was collected after the mandatory adoption of IFRS by the European Union in 2005. About 80 percent of the Asian participants were from Hong Kong, India, the Philippines, and Singapore (other countries represented include China, Indonesia, Japan, and Malaysia). Most countries represented are in Leuz et al.’s (2010) analysis of reporting quality across domiciles; approximately 70 percent of the non-U.S. countries have environments that Leuz et al. classify into weaker regulatory clusters than that of the U.S.

14

Table 2 reveals no significant differences between participants who indicated that their

firms would adjust earnings and those who did not, except that those in the adjust earnings

sample were more (less) likely to be managers of profit centers (firms as a whole); and those

who chose to adjust earnings had less experience (18.3 years vs. 20.1 years). Sensitivity tests

reported later in the paper indicate that the differences identified above did not influence the

results.

Procedure

The experimental task involved a short case in which participants were asked to assume

that their firm was approaching year end, and they were provided with monetary values for both

expected unmanaged earnings and an important benchmark. We then asked participants whether

their entities would use allowable reporting discretion to increase or decrease earnings and, if so,

by how much. We also asked participants what methods (real and accruals) their entities would

use to adjust earnings, as well as various questions about their entity (e.g., reporting system,

auditors, size, ownership, important benchmarks) and themselves (i.e., demographics).

The case was designed to be completed on a web-based tool that allows researchers to

design studies and collect data. The case was extensively pilot-tested with current and former

financial officers, other academics, and representatives from the BP. We obtained participants

using an e-mail request sent by the BP. The request mentioned that we were investigating

legitimate tactics (operational and accounting) that companies use to influence reported earnings.

Participants were asked to click on a URL link to participate in the study and were told that, if

they participated, they would be eligible to receive one of four $250 American Express gift

cards. The e-mail message described the study as “a confidential survey,” and the request

reiterated that their identity would remain confidential. If respondents clicked on the link, they

15

were directed to the case.10 They saw the first page of a case titled “A Case for Financial

Officers,” and were told that the case consists of about 20 questions. A sample copy of the first

page of the case appears in Appendix A, which included a brief description of the situation

facing the financial officer.

The data used in this study is a subset of data gathered for other research purposes.11 In

total, requests in the U.S. were sent to 11,200 financial officers from two distribution lists. The

first included 1,200 financial officers who agreed to respond to a given number of annual

requests from the BP to respond to surveys. Based on feedback from the BP, we expected a 10-

20 percent response rate from this group; we received 150 total responses, representing a 12.5

percent response rate. An additional 10,000 requests were sent to the BP’s general e-mail

distribution list, for which the BP estimated a one percent response rate. We received 217

responses, a 2.2 percent response rate. These response rates compare to recent rates reported in

the accounting literature; for example, Nelson et al. (2002) report a response rate of 16 percent in

their survey of auditors from one Big 5 accounting firm, and Graham et al. (2005) report a

response rate of 8.4 percent in their survey of CFOs. In Europe (Asia), 6,262 (6,000) requests

were sent and we received 240 (324) responses, representing a 3.8 (5.4) percent response rate; in

both cases, these response rates were consistent with what BP representatives predicted.

Variable Measures

Reporting System. The reporting system (U.S. GAAP vs. IFRS) was measured by

asking the financial officers to respond to a question that asked: “Which set of financial reporting

10 We sent separate requests, each with its own URL link related to each of the versions of the case, to an equal number of financial officers for each URL in each geographic region (U.S., Europe, and Asia). 11 The case instrument contained twelve scenarios created by three variables: (1) expected unmanaged earnings was either above, equal to, or below the relevant benchmark; (2) dispersion around expected unmanaged earnings was either wide or narrow; and (3) the period of time prior to year-end was either one week or one month. The third variable was varied only within the U.S. sample. These variables appear in the tests associated with the likelihood of adjusting earnings reported later, but they are not the focus of this study and do not influence the results.

16

standards does your firm use?” Response choices included (1) Generally Accepted Accounting

Principles (U.S. GAAP); (2) International Financial Reporting Standards (IFRS); (3) Both U.S.

GAAP and IFRS; or (4) Other.12

Reporting Discretion. We measured the level of allowable reporting discretion

perceived by the financial officers by asking them to indicate the extent to which their reporting

entityt could use allowable reporting discretion to adjust earnings without violating generally

accepted accounting principles. They chose one of the following: Very little discretion (<1

percent of reported earnings); little discretion (1%- 2% of reported earnings); some discretion

(3% - 5% of reported earnings); Significant discretion (6% - 10% of reported earnings); or a

great deal of discretion (>10% of reported earnings).

Likelihood of Adjusting Earnings. We asked participants to indicate “without violating

GAAP, how would your reporting entity use allowable discretion to influence reported earnings.

This discretion could take the form of non-accounting decisions (e.g., operating, investing,

financing) or accounting choices (e.g., accounting estimates, assumptions, and/or methods).”

Participants responded by choosing “increase earnings,” “decrease earnings,” or “would not

change earnings.” The likelihood of adjusting earnings for a given group was determined by

dividing the number of participants in the group choosing to increase or decrease earnings by the

total number of group participants.

12 Ninety one of the 615 participants were from firms that reported using both U.S. GAAP and IFRS (29 U.S. and 62 non-U.S.). We classified the U.S. participants, who indicated that they use both U.S. GAAP and IFRS, as IFRS users based on the assumption that they are subsidiaries of parent companies located outside the U.S. We classified the non-U.S. participants, who indicated they use both U.S. GAAP and IFRS, as U.S. GAAP users based on the assumption that they are subsidiaries of parent companies located within the U.S. Consistent with this assumption, participants, who reported using both U.S. GAAP and IFRS, are significantly more likely to be a cost or profit center than those who report using either U.S. GAAP or IFRS (p < 0.01). Further, comparing the “U.S. GAAP and IFRS” users (n = 91) to the “U.S. GAAP or IFRS” users (n = 524) showed no other significant response differences. In tests reported later, we also exclude these participants, focusing only on US/US GAAP firms and non-US/IFRS firms. Results are similar to those reported from our main tests.

17

Method of Adjusting Earnings. We measured the relative preference for real activities

vs. accruals by asking the financial officers to respond to the following question: “How would

your reporting entity rely on the two forms of discretion to attain the increase (or decrease)

indicated in Question A1?” (11-point scale ranging from 1 = operating, investing, financing only

to 11 = accounting choices only).13

Other Important Characteristics of the Reporting Environment

In this section we discuss five firm-specific variables that may determine the level of

allowable discretion in the reporting environment (firm domicile, direction of earnings

adjustment, firm ownership, audit quality, and firm size). They are treated as control variables in

most of the tests reported later (Schipper 2005; Hail et al. 2010a).14

Firm Domicile: U.S. vs. Non-U.S. Much of the accounting literature concerned with

cross-national earnings management differences is based on the belief that the investor protection

environment is more effective in the U.S. than in non-U.S. settings (e.g., Leuz et al. 2010). A

long-standing tradition of conservative accounting exists in non-U.S. settings, and in some cases

regulators actually have encouraged earnings understatements (Joos and Lang 1994; Lamb et al.

1998; Garcia-Lara and Mora 2004). It appears, in general, that the cultural and business

environment operating in non-U.S. settings allows management more reporting discretion than is

allowed in the U.S. These arguments suggest that non-U.S. auditors are less concerned with

13 Respondents answered this question immediately after indicating the likelihoods that they would use in this situation a series of specific real and accrual methods. The answers to the questions related to the specific methods provided a validity check for the primary question used in the analysis. That is, those indicating a preference for real activities tended to attach greater likelihoods to the individual questions related to real methods, while those indicating a preference for accruals tended to attach greater likelihoods to the individual questions related to accruals methods. Additional analysis of these specific methods is provided later in the paper in Table 7. 14 Schipper (2005) recommends including regulatory environment factors as control variables, specifically arguing that domicile and ownership should be controlled for when evaluating reporting consequences between reporting regimes.

18

identifying reporting violations, and that the expected consequences are lower. Domicile was

determined directly from the respondent’s location, as separate requests were sent to addresses in

the U.S., Europe, and Asia.

Direction of Earnings Adjustment: Upward vs. Downward. Using discretion to adjust

earnings upward normally involves situations in which expected unmanaged earnings is below

the benchmark, and management is considering whether to increase earnings to avoid failing to

achieve the benchmark. Using discretion to adjust earnings downward normally involves a

situation where expected unmanaged earnings is above the benchmark, and management is

considering whether to decrease earnings to reduce the amount by which reported earnings

exceeds the benchmark. The cost to management of reporting earnings below the benchmark is

much higher than the cost of reporting earnings above the benchmark because under-

performance carries greater negative consequences for management than over-performance

(Beyer 2008; Healy and Wahlen 1999). The cost of losing one’s job, failing to receive a bonus,

and/or missing an analysts’ forecast, for example, are typically higher and more immediate than

the costs associated with setting a higher standard for next year’s performance.

These differential costs suggest that management has a stronger incentive to adjust

earnings upward in a weak year than to adjust earnings downward in a strong year. With this in

mind, auditors are more alert to and concerned with upward earnings adjustments. Similarly,

Barron et al. (2001) find that auditors are more likely to allow understatements than

overstatements, arguing that the auditor’s litigation exposure is higher for undiscovered

overstatements. Finally, conservatism is an important accounting measurement principle, which

may encourage auditors to more readily tolerate downward adjustments to earnings.

19

Together, these arguments suggest that the likelihood of identifying and acting on

potential reporting violations when management is adjusting earnings downward is lower than

when management is adjusting earnings upward. The direction of the earnings adjustment was

determined by noting whether management chose to increase or decrease earnings.15

Firm Ownership: Public vs. Private. Reporting regulations in the publicly-owned

environment allow less reporting discretion than in the privately-owned regulatory environment

because auditor monitoring is more thorough, SEC enforcement laws exist, and the threat and

expected consequences of litigation for both the auditor and management are larger. More

thorough auditor monitoring increases the likelihood of identifying reporting violations, and SEC

enforcement laws and litigation can lead to large negative consequences. The financial officers

indicated whether their firm was privately or publicly owned.

Audit Quality: Big 4 vs. Non-Big 4. The Big 4/non-Big 4 classification is often used as

a measure of audit quality, based on the premise that the additional resources available to Big 4

firms and their additional litigation and reputation exposure encourage stronger monitoring and

oversight of management’s reporting behavior. Big 4 auditors, therefore, are expected to allow

less reporting discretion than non-Big 4 auditors (Chi, Lisic, and Pevzner 2011). The financial

officers indicated whether their firm was audited by a Big 4 or non-Big 4 firm.

Firm Size. Managers in small firms are accountable for less capital owned by fewer

capital providers than are managers in large firms. Auditor monitoring is less thorough for small

firms because auditor litigation exposure is lower, thereby decreasing the likelihood of 15 Recall that the instrument included different scenarios of firm performance by the placement of the benchmark relative to expected unmanaged reported earnings: strong (unmanaged earnings > benchmark); average (unmanaged earnings = benchmark); and poor (unmanaged earnings < benchmark). We assumed that firms would adjust earnings toward the benchmark; consequently, we expected specific scenarios to induce upward and downward earnings adjustments. Of the 191 participants who chose to adjust earnings, 156 (82 percent) adjusted earnings toward the benchmark. Adjusting earnings away from the benchmark, however, was not considered unreasonable. Reasonable explanations for adjusting earnings away from the benchmark include “taking a bath” in the poor firm performance condition, and maximizing a bonus in the strong firm performance condition.

20

identifying and acting on reporting violations. The potential negative consequences for adjusting

earnings reported by small firms are less than in large firms because small-firm managers are

accountable to fewer capital providers for less capital. We measured firm size by asking the

financial officers to place their entities in one of the following categories based on annual sales:

<$100 million, $100 - $499 million, $500 million - $999 million, and >$1 billion.

Additional Questions16

Because we used the responses of financial officer as proxies for firm-level reporting

behavior, we assessed the extent to which each officer was involved in the firm’s discretionary

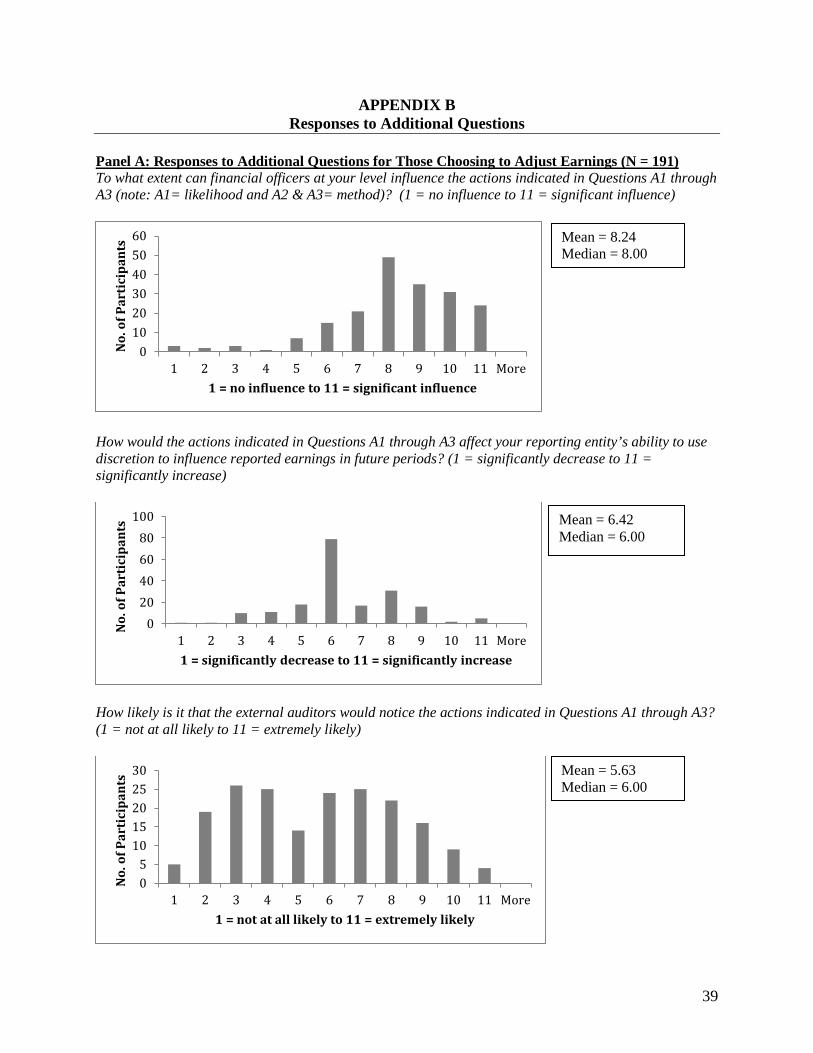

reporting decisions. Specifically, we asked participants to indicate “To what extent can financial

officers at your level influence the [earnings adjustment indicated earlier in the case]?” (1 = “No

influence” and 11 = “Significant influence”). The overall mean response of 8.24 (s.d. = 2.08)

significantly exceeds the scale midpoint (6.0), allowing us to conclude that the participants are

involved with their entities’ discretionary reporting decisions.

We also asked several additional questions about issues that may relate to discretionary

reporting, including (1) how discretionary accounting adjustments in a given period influence the

entity’s ability to use such discretion in future periods; (2) what is the likelihood that external

auditors would notice their discretionary adjustments; (3) if the external auditor noticed, what is

the likelihood that the auditor would raise questions about them; (4) how accurately can your

reporting entity predict reported earnings for the year; and (5) what is the importance of meeting

various benchmarks (e.g., analyst earnings forecasts, budgeted earnings, prior year’s earnings).

Few meaningful differences emerged between the U.S. GAAP and IFRS groups on these

questions. For both groups, over 84 percent believed that reported annual earnings could be 16 Appendix B includes summary statistics for responses to additional questions in graphical and/or tabular format.

21

predicted within five percent approximately one month prior to year end, and both groups

believed that using reporting discretion in the current period would have a moderate effect

(approximately 6.42 on an 11-point scale) on using discretion in future years.

In general, both groups believed that it was moderately unlikely (5.63 on an 11-point

scale) that the external auditor would notice their discretionary earnings adjustments, and neither

group believed that the external auditor was especially likely to “raise questions” about their

adjustment in the event that the auditor noticed them (6.11 on an 11-point scale). The

importance of the various benchmarks were largely the same across the two groups (budgeted

earnings was considered most important, followed by prior year’s earnings and employee bonus

threshold), but the financial officers under U.S. GAAP attributed greater importance to debt

covenants.17 Also, these results reveal that managers in our sample believe beating benchmarks

is important, in general, with 94% rating at least one benchmark at 5 (out of 7) in terms of

importance. In addition, 80% rate at least one benchmark at 6, and almost half rate at least one

benchmark at 7, or extremely important.

V. RESULTS

Univariate Tests

Univariate Pearson correlations among the primary variables are presented in Table 3.

Panel A reports results for the full sample. Most of the correlations are consistent with

expectations, and while many are significant, the size of the coefficients are not large enough to

present multicollinearity issues in the tests reported later in the paper. Specifically, firms

perceiving more reporting discretion are more likely to adjust earnings (ρ = 0.183), use IFRS (ρ

= -0.129), reside outside the U.S. (ρ = -0.100), be smaller and privately owned (ρ = -0.123 and -

17 This result is consistent with Dichev et al.’s (2012) finding that inside pressure to meet benchmarks is a significant factor in CFOs’ earnings management decisions.

22

0.103, respectively), and be audited by non-Big 4 firms (ρ = -0.119). In addition, firms under

U.S. GAAP tend to be larger (ρ = 0.166), and larger firms tend to be public (ρ = 0.327) and

audited by Big 4 auditors (ρ = 0.277). One somewhat surprising finding is that the inclination to

adjust earnings does not relate to the reporting system (ρ = -0.020) – that is, firms under IFRS

were neither more nor less likely to adjust earnings compared to firms under U.S. GAAP.

Panel B reports univariate correlation results for the sample of firms that indicated an

earnings adjustment. Results are generally consistent with Panel A and, as expected, the

preference for accruals (vis-à-vis real activities) is positively associated with higher levels of

perceived discretion (ρ = 0.156), and is higher for firms using IFRS (ρ = -0.153), non-U.S. firms

(ρ = -0.183), and firms adjusting earnings downward (ρ = -0.244).18

[Insert Table 3 here]

Hypotheses Tests

The tests of the hypotheses are contained in Tables 4, 5, and 6. Table 4 (Panel A) reports

the frequencies of the responses to the question asking respondents to indicate the level of

allowable discretionary influence over reported earnings, for all respondents and broken down by

US GAAP and IFRS. Both a Chi-square test (Chi-square = 10.83, p < 0.05) and a t-test

comparing the means across U.S. GAAP and IFRS (t = 3.21, p < 0.01) are significant, indicating

financial officers under IFRS perceive more reporting discretion than do financial officers under

U.S. GAAP.

[Insert Table 4 here]

Panel B of Table 4 reports results of multivariate analyses (via ordered logistic

regression) in which the dependent variable was a coding of 1 (very little discretion) – 5 (a great

18 The direction of the earnings adjustment is not correlated with any of the other variables. This result validates the random assignment of firm performance scenarios discussed in footnotes 15 and 21.

23

deal of discretion), and the variable of interest is the reporting system (GAAP).19 We also

control for other regulatory factors, including domicile (U.S.), firm ownership (Public), audit

quality (Big 4), and firm size (Size).

We first test whether the reporting system is associated with perceived discretion

excluding control variables other than size. These results show that financial officers under

IFRS perceive more reporting discretion than those under U.S. GAAP (coefficient = -0.424, one-

tailed p-value = 0.004). Column 2 includes all control variables expected to affect the level of

perceived discretion. The coefficient for the reporting system (GAAP) remains negative and

significant (coefficient = -0.390, one-tailed p-value =0.002). The only significant control

variable is Big 4 (coefficient = -0.479, two-tailed p-value = 0.015), indicating that firms with Big

4 auditors perceive less reporting discretion than firms with non-Big 4 auditors. All tests support

H1 - financial officers using IFRS perceive more discretionary influence over reported earnings

than those using U.S. GAAP.20

[Insert Table 5 here]

Table 5 reports the effects of the level of perceived allowable reporting discretion

(Discretion) and reporting system (GAAP) on the likelihood of adjusting earnings. In Panel A,

we first report evidence consistent with Table 2, showing that the reporting system and the

likelihood of adjusting earnings are unrelated (Chi-Square = 0.258, p-value = 0.611). In Panel B,

we control for firm size (Size), domicile (US), audit quality (Big 4), ownership (Public), the

direction of the earnings adjustment (Increase), timing, and uncertainty in unmanaged earnings.21

19 An OLS regression was also used and produced substantively the same results. 20 In unreported tests, we included interactions among GAAP and control variables. None of these interactions was significant and we, therefore, exclude from our reported results. 21 Recall that we introduced three scenarios to participants: performance (high, average, low), timing, (one month vs. one week), and uncertainty in unmanaged earnings (high vs. low). The performance manipulation was used to induce upward and downward earnings adjustments and therefore correlates highly with the direction of the earnings adjustment.

24

Only two of the variables are significant: Discretion and Performance. The significant

coefficient for Discretion (0.430, one-tailed p-value = <.0001) supports H2, showing that higher

levels of perceived allowable reporting discretion lead to a higher likelihood of adjusting

earnings independent of the method. The significant coefficient for Performance (-0.628, p-

value = 0.001) shows that participants are more likely to adjust earnings when unmanaged

earnings is below a relevant benchmark compared to when unmanaged earnings is above a

relevant benchmark. None of the other variables are significant; importantly, the reporting

system variable (GAAP) is not significant. Contrary to H3, IFRS does not appear to lead to a

greater likelihood of adjusting earnings compared to U.S. GAAP.22

[Insert Table 6 here]

In Table 6 the dependent measure is participant responses to the question: “How would

your reporting entity rely on the two forms of discretion to attain the increase (or decrease)

indicated in Question A1?” This measure uses an 11-point scale with mean values significantly

below (above) the scale midpoint of “6” indicating a preference for real (accruals) methods. The

primary independent measures are the perception of allowable reporting discretion (Discretion)

and reporting system (GAAP), and the control variables include firm size (Size), domicile (US),

ownership (Public), audit quality (Big 4), and the direction of the earnings adjustment (Increase).

Panel A reports results of a multivariate analyses using an ordered logistic regression.23

Column 1 excludes all control variables except Size and includes Discretion and GAAP as the

test variables. Discretion is positive and significant (coefficient = 0.306, one-tailed p-value =

0.028), and GAAP is negative and significant (coefficient = -0.499, one-tailed p-value = 0.034).

22 In unreported tests, we included interactions among GAAP and control variables. None of these interactions was significant and we, therefore, exclude from our reported results. In addition, we include Discretion and GAAP one at a time in the regression in unreported tests; results reveal that Discretion is positive and significant while GAAP is insignificant, consistent with reported results. 23 An OLS regression was also used and produced substantively the same results.

25

These preliminary results are consistent with firms perceiving more discretion and firms under

IFRS preferring accruals methods compared to firms under U.S. GAAP.

In column 2 we include control variables representing the reporting environment and their

interactions with the reporting system (GAAP). We include both the control variables and their

interaction with GAAP because these variables may have a direct effect on the preference for

real vs. accruals methods as well as an effect on the relationship between the reporting system

and the choice of method.

Results from this more fully specified model indicate that Discretion remains positive and

significant (coefficient = 0.301, two-tailed p-value = 0.037), while GAAP becomes insignificant.

The interaction between US and GAAP, however, is negative and highly significant (coefficient

= -1.863, two-tailed p-value = 0.005). This result indicates that the reporting environment in the

U.S., coupled with relatively tight reporting standards (U.S. GAAP), encourages U.S. firms to

prefer real over accruals methods. Other main effects significant in the regression are US

(coefficient = 0.897, two-tailed p-value = 0.095) and Increase (coefficient = -1.280, two-tailed p-

value = 0.002). These results indicate that, overall, U.S. firms prefer real methods and firms

adjusting earnings downward prefer accruals methods.

In columns 3 and 4, we provide additional evidence on the preference for real vs. accruals

methods among US firms using US GAAP by excluding from the sample US participants using

IFRS, non-US participants using US GAAP, and participants indicating they report under both

standards. We conduct analyses on this reduced sample for three reasons. First, Barth et al.

(2010) and others argue (and support empirically) that US firms using US GAAP have greater

accounting quality than non-US firms using IFRS. Therefore, we present results using only these

two groups of firms for greater comparability with these studies. Second, excluding US/IFRS

26

firms and non-US/GAAP firms eliminates many (but not all) of the firms which have voluntarily

chosen to apply GAAP or IFRS, thus, helping to mitigate concerns about self-selection into a

particular reporting regime. Third, interpretation of interactions in ordered logistic regressions is

problematic. Therefore, we eschew the need to interact US and GAAP, for example, at the

expense of the inability to discern whether the documented effect is due to reporting system or

domicile. Results are consistent with those reported in columns 1 and 2. Importantly, US/GAAP

exhibit a preference for real methods, relative to non-US/IFRS firms (coefficient = -0.744, p-

value = 0.035).

In Panel B, we examine more closely the interaction effects by separately examining

double-sorts based on GAAP/IFRS with domicile (Non-US vs. US), ownership (Private vs.

Public), audit quality (Non-Big 4 vs. Big 4), and the direction of the earnings adjustment

(Decrease vs. Increase). Note first that the significant US * GAAP interaction is driven by U.S.

firms under U.S. GAAP indicating a strong preference for real over accruals methods, while non-

U.S. firms under U.S. GAAP and IFRS and U.S. firms under IFRS indicate indifference between

real and accruals methods.

Particularly interesting is the result that U.S. firms under U.S. GAAP show a strong

preference for real over accruals methods (4.527 < 6.0), while U.S. firms under IFRS are

indifferent (6.0 = 6.0). We examined the sample of firms in the US/IFRS cell (n = 40) and those

within the cell that chose to adjust earnings (n = 14), and found that their profile differed from

the overall sample in only one way – they were more likely to be a profit or cost center. In the

overall sample 39% of the firms are profit or cost centers, compared to 67% in the US/IFRS cell.

This observation suggests that a relatively large percent of the US/IFRS firms may have been

subsidiaries of non-U.S firms under IFRS operating in the U.S. This group provides a natural

27

testing ground for the consequences associated with adopting an IFRS-like reporting system in

the U.S. That is, differences between these firms and U.S. firms under U.S. GAAP may offer

insights into how U.S. firms would respond to such a change. We found that, compared to U.S.

firms under U.S. GAAP, these firms were more inclined to substitute accruals for real methods.

Panel B of Table 6 also shows that firms choosing to adjust earnings downward were less

inclined to rely on real methods compared to firms choosing to adjust earnings upward, who

displayed a clear preference for real methods regardless of reporting system. At the other

extreme, firms under IFRS that adjusted earnings downward showed a clear preference for

accruals over real methods.

Additional Tests: Specific EM Methods

Table 7 provides additional detail about the specific methods used to adjust earnings

indicated by participants and serves two purposes - first, it provides descriptive evidence on the

specific methods preferred by firms to adjust earnings upward or downward; second, it provides

validation of the relative preference for real vs. accruals methods presented in Table 6. In Table

7 we compare preferences for two groups that the analyses thus far suggest are very different

with respect to their preferences for real vs. accruals methods - US firms under US GAAP

adjusting earnings upward (preference for real methods) and US and non-US firms under IFRS

adjusting earnings downward (preference for accruals methods).

[Insert Table 7 here]

Recall that these questions were answered by participants who indicated earlier in the

exercise that their firms would adjust earnings either upward or downward. The respondents

were asked the extent to which their firms would rely on each method listed in the first column,

28

entitled Specific Method. The description of the methods was slightly altered depending on

whether the respondent had indicated an upward or downward earnings adjustment. Column 2

indicates whether the method is considered real or accruals-based, and columns 3 and 4 provide

the mean response and (standard deviation) to each method as well as its ranking for the two

divergent groups.

The US/US GAAP group significantly prefers real over accruals methods (mean = 4.56 <

6.00), while the other group significantly prefers accruals over real methods (mean = 6.75 >

6.00). The most common methods used by the US/US GAAP group involve delaying spending

on operating items and delaying the start of new projects, both real methods. The most common

methods used by the other group involve adjusting accounting estimates, assumptions, or

methods and adjusting the timing of accounting charges, all accruals methods. Interestingly, the

third most common method used by this group is also the most common method used by US/US

GAAP group, suggesting that adjusting spending on operating items is perhaps the most common

way to adjust earnings.

Robustness Tests: US and US GAAP Interaction Analyses

In this section we discuss tests designed to evaluate the robustness of our result that firms

using US GAAP and operating in the US prefer to use real methods to adjust earnings rather than

accruals methods (Tables 6 and 7). Specifically, we address concerns that this result is driven by

variables correlated with domicile or accounting standards, but currently omitted from the

analysis. The first variable we consider is the legal and regulatory environment of the country

(Barth et al. 2012). If our result is driven by countries with common law origins and strict legal

enforcement, rather than simply being located in the US, then restricting the sample to such

29

“high regulatory” countries would make the US and US GAAP interaction result insignificant.

We follow Leuz [2010] and Leuz, Nanda, and Wysocki [2003] and identify five countries in our

sample with common law origins, strict regulator enforcement, and transparent accounting

practices: United States, United Kingdom, Hong Kong, Malaysia, and Singapore. Untabulated

results of analyses using this restricted sample are similar to those reported in Table 6, and the

inferences are identical. This evidence suggests that the U.S. regulatory environment is unique,

even among countries with strong regulatory environments.

The second variable we consider is managerial experience. Results from Table 2

indicate that managers of US GAAP firms are more experienced than managers of firms using

IFRS. If our result is driven by experienced managers, rather than US GAAP, then including

experience as an additional control should render our results on the US and US GAAP

interaction insignificant. Untabulated results of analyses including experience as an additional

control variable are similar to those reported in Table 6, and the inferences are identical.

Finally, we include identification as a profit center as an additional control variable in our

analyses. We include this variable because profit centers in our sample are more likely to report

under US GAAP than IFRS (Table 1). Additionally, Table 2 reveals that managers of profit

centers are more likely to adjust earnings than managers of whole firms. These observations

raise the possibility that the results reported in Table 6 may not be generalizable to the entire

population. However, after including identification as a profit center as an additional control

variable, the results on the US and US GAAP interaction are similar to those reported in Table 6,

and the inferences are identical.24

24 Additional untabulated results reveal that entities reporting as profit centers are larger, more likely to be public, and more likely to be audited by Big 4 auditors, when compared with entities reporting as whole firms. Accordingly, our results showing that US GAAP firms prefer real methods are stronger for a sample of only profit

30

In summary, results from these robustness tests indicate that the regulatory environment

in the U.S. appears to be distinct in that the preference for real methods is uniquely concentrated

in the US, and not in other countries with strong regulations. Also, the preference for real

methods in adjusting earnings by US firms using US GAAP is not driven by managerial

experience or profit center reporting.

VI. SUMMARY AND CONCLUSIONS

In this study we use a web-based case to examine the effect of characteristics of the

financial reporting environment on the level of financial reporting discretion perceived by

managers and the likelihood and method of earnings management. We find that financial

officers under IFRS perceive higher levels of allowable reporting discretion than those under

U.S. GAAP, and the perception of higher levels of allowable reporting discretion leads to both a

greater likelihood of earnings management and a preference for the use of accruals over real

methods. While we generated no evidence that IFRS, compared to U.S. GAAP, leads to a

greater likelihood of earnings management, we do observe that U.S. firms under U.S. GAAP

show a strong preference for real activities over accruals, while all other firms (U.S. firms under

IFRS and non-U.S. firms) are either indifferent between the two methods or prefer accruals. We

also find that firms adjusting earnings upward strongly prefer real methods. In the case of firms

adjusting earnings downward, the preference for real vs. accruals methods depends on whether

they use U.S. GAAP or IFRS - U.S. GAAP users are indifferent and IFRS users prefer accruals.

These findings suggest that differences in the level of allowable reporting discretion

defined by the reporting environments are associated with differences in the relative preference

centers (coefficient on US GAAP = -0.771, p-value = 0.04, one-tailed) versus a sample of only whole firms (coefficient on US GAAP = -0.628, p-value = 0.11, one-tailed).

31

for real activities vs. accruals. They indicate to policymakers that reporting environments that

restrict managerial reporting discretion may not necessarily lead to less earnings management,

but instead may encourage management to substitute real activities for accruals. That is,

tightening reporting standards and increasing regulations may not lead to less overall earnings

management, but rather less reliance on accruals and more reliance on real activities.

The conclusion that the heavily regulated U.S. reporting environment may be doing little

to discourage earnings management in total, changing only the way in which it is practiced, may

offer a new perspective on the benefits of reporting regulations. Under this view the primary

consequence associated with reporting regulations may be more real-based earnings adjustments

at the expense of accruals-based adjustments. Granted, real methods are not directly a form of

“cooking the books.” They are, however, often conscious choices by management to disrupt the

cash flows generated by the firm’s operating, investing, and/or financing decisions in the interest

of achieving a reporting target. Is this type of earnings management somehow preferred to the

use of accruals? Examining tradeoffs between these two forms of earnings management may be

a fruitful avenue for future research.

Our findings also suggest, on the other hand, that higher levels of reporting discretion

may not lead to more earnings management, but instead may allow managers to substitute the

use of accruals for real activities. U.S. policymakers, for example, may be interested in knowing

that a primary consequence of adopting a more “principles-based” system of reporting standards

(like IFRS) may be to encourage a shift from real activities to accruals when adjusting earnings

to meet benchmarks.

While the reporting system is certainly an important part of the financial reporting

environments, our study also finds that these environments are comprised of many elements. By

32

themselves reporting standards alone may not lead to predictable differences in the level or

nature of the earnings management practiced in the jurisdiction covered by the standards. In the

U.S., firms using U.S. GAAP exhibit stronger preferences for real activities than firms under

IFRS. Outside the U.S., however, reporting standards appear to have no effect on the method

preference. We find further that the effect on earnings management of certain characteristics of

the reporting environment may be additive. At one extreme U.S. firms under U.S. GAAP

adjusting earnings upward demonstrate a strong preference for real activities over accruals; at the

other extreme, firms under IFRS (U.S. and non-U.S.) adjusting earnings downward demonstrate

a strong preference for accruals over real activities.

Finally, our results have implications for the interpretation of prior findings in the related

literature. The current difference in the overall amount of earnings management practiced in

U.S. and non-U.S. settings may not be as large as suggested in the existing literature. It may be

that the more highly regulated U.S. business environment may be forcing U.S. managers to rely

more heavily on real activities that are more difficult for researchers to detect. For example, the

Barth et al. (2012) finding that U.S. firms using U.S. GAAP exhibit higher levels of accounting

quality may apply only to accruals, and U.S. firms may be substituting real activities for

accruals. In addition, our findings suggest that the Graham et al. (2005) finding that U.S.

managers prefer real activities over accruals may be limited to U.S. firms, operating under U.S.

GAAP, when adjusting earnings upward.

33

References

Ahmed, A., M. Neel, and D. Wang. 2012. Does Mandatory Adoption of IFRS Improve Accounting Quality? Preliminary Evidence. Working paper, Texas A&M University and University of Houston.

Alford, A., J. Jones, R. Leftwich, and M. Zmijewski, 1993. The Relative Information Content of

Accounting Disclosures in Different Countries. Journal of Accounting Research 31 (Supplement): 183-223.

Ayers, B. C., J. Jiang, and P. E. Yeung. 2006. Discretionary Accruals and Earnings Management:

An Analysis of Pseudo Earnings Targets. The Accounting Review 81 (3): 617-652. Backof, A., E.M. Bamber, and T. Carpenter. 2011. International Financial Reporting Standards

and Aggressive Reporting: An Investigation of Proposed Auditor Judgment Guidance. Working paper, University of Georgia.

Barron, O., J. Pratt, and J. Stice. 2001. Misstatement direction, litigation risk, and planned audit

investment. Journal of Accounting Research 39, 3: 449-462. Barth, M. E. W. Beaver, J. Hand, and W. Landsman. 2005. Accruals, accounting-based valuation

models, and the prediction of equity values. Journal of Accounting, Auditing & Finance 20: 311–345

Barth, M. E., W. R. Landsman, and M. H.Lang. 2008. International Accounting Standards and

Accounting Quality. Journal of Accounting Research 46 (June): 467-498. Barth, M. E., Landsman, W. R., Lang, M.H. and C. D. Williams. 2012. Are IFRS-Based and US

GAAP-Based Accounting Amounts Comparable? Journal of Accounting and Economics http://dx.doi.org/10.1016/j.jacceco.2012.03.001

Beyer, A. 2008. Financial analysts’ forecast revisions and managers’ reporting behavior.

Journal of Accounting and Economics 46, 2-3: 334-348. Bradshaw, M. T., and G. S. Miller. 2008. Will Harmonizing Accounting Standards Really

Harmonize Accounting? Evidence from Non-U.S. Firms Adopting US GAAP. Journal of Accounting, Auditing and Finance 23: 233-263.

Burgstahler, D., and I. Dichev. 1997. Earnings management to avoid earnings decreases and losses. Journal of Accounting and Economics 24, 1: 99-126.

Chi, W., L. Lisic, and M. Pevzner. 2011. Is Enhanced Audit Quality Associated with Greater

Real Earnings Management? Accounting Horizons 25, 2: 315-335. CEOs of the International Audit Network. 2008. Principles-Based Accounting Standards.

January. Also at http://www.iasplus.com/resource/0801principlesbased.pdf

34

Cohen, D., Dey, A., Lys, T., 2008. Real and accrual based earnings management in the Pre and Post Sarbanes Oxley periods. The Accounting Review 83: 757–787.

Cohen, D. A. and P. Zarowin. 2010. Accrual-based and real earnings management activities

around seasoned equity offerings. Journal of Accounting and Economics (50): 2-19 Dechow, P., R. Sloan, and A. Sweeney. 1995. Detecting Earnings Management. The Accounting

Review 70 (2): 193-225. Dechow, P. M. and D. J. Skinner. 2000. Earnings Management: Reconciling the Views of

Accounting Academics, Practitioners, and Regulators. Accounting Horizons (June): 235-50.

Dechow, P., W. Ge and C. Schrand. 2010. Understanding earnings quality: a review of the

proxies, their determinants and their consequences. Journal of Accounting and Economics 50, 2-3: 344-401.

Demski, J. S. 2004. Endogenous Expectations. The Accounting Review 79: 519-539. DeFelice, A. and M. G. Lamoreaux. 2010. The SEC’s IFRS Work Plan. Journal of Accountancy

(April): http://www.journalofaccountancy.com/Issues/2010/Apr/20102658.htm DeFond, Mark L. 2010. Earnings quality research: advances, challenges and future research.

Journal of Accounting and Economics 50, 2-3: 402-409. Dichev, I., J. Graham, C. Harvey, and S. Rajgopal. 2012. Earnings quality: evidence from the

field. Working paper, Duke University and Emory University. Enomoto, M., F. Kimura, and T. Yamaguchi. 2012. Accrual-Based and Real Earnings

Management: An International Comparison of Investor Protection. Working paper, Kobe University, Tohoku University, and Tohoku Gakuin University.

Ewert, R. and A. Wagenhofer. 2005. Economic Effects of Tightening Accounting Standards to

Restrict Earnings Management. The Accounting Review October: 1101-1124. Financial Accounting Foundation. 2009. Response to The Securities and Exchange

Commission’s (SEC) Roadmap for the Potential Use of Financial Statements Prepared In Accordance With International Financial Reporting Standards (IFRS) by U.S. Issuers. (March 11): Norwalk CT.

Fields, T. D., T. Z. Lys, and L.Vincent. 2001. Empirical Research on Accounting Choice.

Journal of Accounting and Economics 31(September): 255-307. Folsom, D., P. Hribar, R. Mergenthaler, and K. Peterson. 2012. Principles-Based Standards and

Earnings Attributes. Working paper, Lehigh University, University of Iowa, and University of Oregon.

35

Garcia-Lara, J. M., and A. Mora. 2004. Balance Sheet versus Earnings Conservatism in Europe.

European Accounting Review 13: 261-292. Gibbins, M. 2002. Discussion of: Evidence from auditors about managers and auditors’ earnings-

management decisions. The Accounting Review 77 (Supplement): 203-211. Gordon, E., B. Jorgensen, and C. Linthicum. 2010. Could IFRS replace US GAAP? A

comparison of earnings attributes and informativeness in the US market. Working paper, Temple University, University of Colorado, and UT-San Antonio.

Graham, G.R., C.R. Harvey, and S. Rajgopal. 2005. The Economic Implications of Corporate

Financial Reporting. Journal of Accounting and Economics 40: 3-73. Hackenbrack, K., and M. Nelson. 1996. Auditors’ Incentive-Compatible Application of

Professional Standards. The Accounting Review 71 (January): 43-60. Hail, L., C. Leuz, and P. Wysocki. 2010a. Global Accounting Convergence and the Potential

Adoption of IFRS by the United States (Part I): Conceptual Underpinnings and Economic Analysis. Accounting Horizons 24 (3): 355-394.

Hail, L., C. Leuz, and P. Wysocki. 2010b. Global Accounting Convergence and the Potential

Adoption of IFRS by the United States (Part II): Political Factors and Future Scenarios for U.S. Accounting Standards. Accounting Horizons 24 (4): 567-588.

Harrison, G. and J. List. 2004. Field Experiments. Journal of Economic Literature 42 (4): 1009-

55. Healy, P. M. and J. M. Wahlen. 1999. A Review of the Earnings Management Literature and its

Implications for Standard Setting. Accounting Horizons (December): 365-383. Hronsky, J. J. F., and K. A. Houghton. 2001. The meaning of a defined Accounting Concept:

Regulatory Changes and the Effect on Auditor Decision Making. Accounting, Organizations and Society 26 (2): 123-139.

Hughes, S. and J. Sander. 2008. The implications of IFRS adoption: the extent of convergence

and consistency between IFRS and US GAAP net income. Working paper, University of Vermont and Butler University.

Ipino, E. and A. Parbonetti. 2011. Mandatory IFRS Adoption: The Trade-off Between Accrual

and Real-Based Earnings Management. http://ssrn.com/abstract=2039711. Jones, H. 2012. “US Official ‘Optimistic’ on Global Accounting Move.” The Wall Street Journal

(February 20, 2012):1.

36

Joos, P. and M. Lang. 1994. The Effects of Accounting Diversity: Evidence from the European Union. Journal of Accounting Research 32 (Supplement): 141-168.

Kadous, K. and M. Mercer. 2012. Can reporting norms create a safe harbor? Jury verdicts

against auditors under precise and imprecise accounting standards. The Accounting Review 87, 2: 565-587.