Embed Size (px)

Citation preview

The Financial Bubble Experiment:Advanced Diagnostics and Forecasts of Bubble Terminations

Volume III

R. Woodard, D. Sornette, J. Berninger

(The Financial Crisis Observatory)∗

Department of Management, Technology and Economics,ETH Zurich, Kreuzplatz 5, CH-8032 Zurich, Switzerland

(Dated: 2 May 2011)

This is a summary of the third installment of the Financial Bubble Experiment (FBE), wherewe identified 27 asset bubbles in November 2010 and revealed their names on 2 May 2011. Herewe provide the following original documents packaged as one in the following sequence:

1. the initial public summary document of the FBE Vol. III, uploaded on 12 November 2010as v1 at http://arxiv.org/abs/1011.2882 and which includes the digital fingerprint ofthe original Master document of the 27 assets (item 3 in this list);

2. the names, forecast quantiles and final analysis of the 27 bubbles released on 2 May2011;

3. the original Master document identifying the 27 assets, created on 12 November 2010 andwhose checksum (digital fingerprint) appears in the document of item 1).

For the purpose of verifying the checksums of the original Master document (item 3 in the abovelist), it and the rest of the contents of this summary document can be found individually onlineat http://www.er.ethz.ch/fco/index.

The checksums of the document in item 3 are:

Document name

SHA256SUM 4994beab18293be021d751d513b6fec0776fde9cf74c0098f7da8657487d950d

SHA512SUM ee20582b696a2ce880870b513e7b9e7ebb67bfbe62e2cad50dd18276a5158765af6fdf88d9fef6e047526c40478a865c722cab041386aa8efdd95da24dd9239d

TABLE I. Checksums of Financial Bubble Experiment Vol. III forecast document.

The tables on the following page list the names and forecast quantiles of the 27 assets andare reproduced from item 2 above.

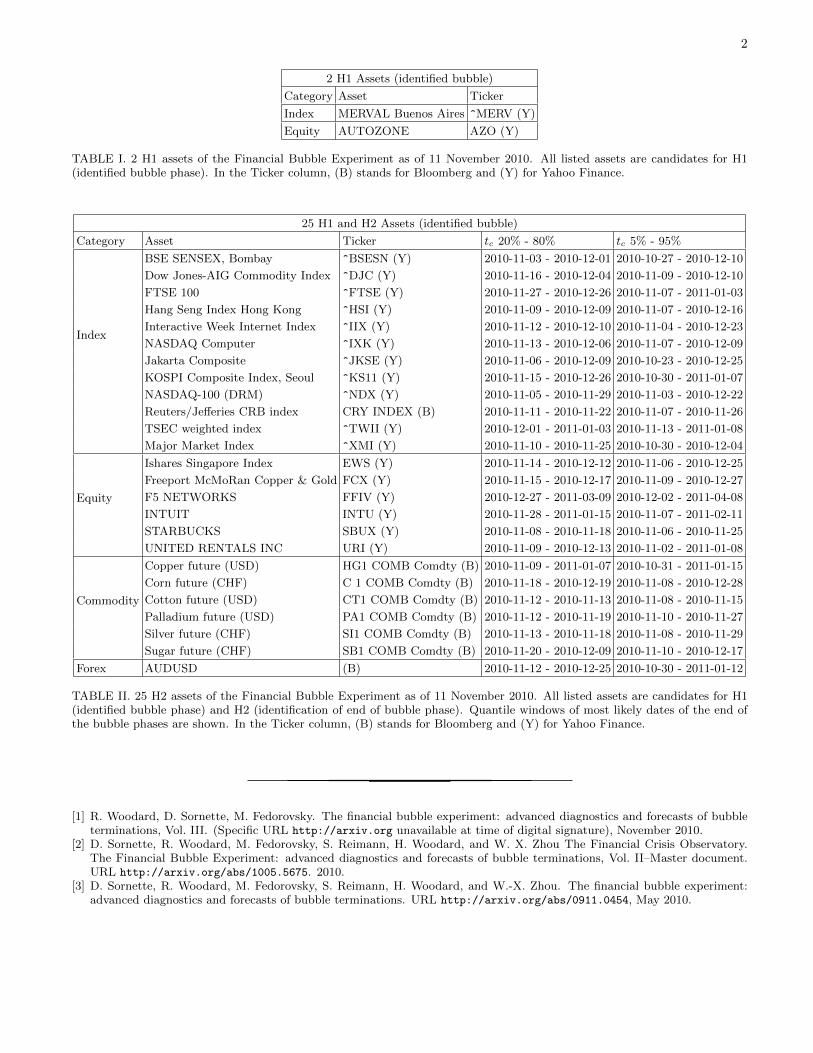

2 H1 Assets (identified bubble)

Category Asset Ticker H1 C

Index MERVAL Buenos Aires ^MERV (Y) 1 *

Equity AUTOZONE AZO (Y) 1

TABLE II. 2 H1 assets of the Financial Bubble Experiment as of 12 November 2010. All listed assetsare candidates for H1 (identified bubble phase). In the Ticker column, (B) stands for Bloomberg and(Y) for Yahoo Finance. Columns ‘H1’ and ‘H2’ show a somewhat subjective score of -1 (worst), 0 or1 (best), reflecting the quality of the forecasts. This scoring is discussed further in Section III of themain analysis document available at http://www.er.ethz.ch/fco/index. Column ‘C’ has an asterisk ifan asset had a major correction within 3 days of t2 =2010-11-10 (the last data observation used in ouranalysis). This correlated dynamics also is discussed in Section III of the same analysis document.

25 H1 and H2 Assets (identified bubble)

Category Asset Ticker tc 20% - 80% tc 5% - 95% H1 H2 C

Index

BSE SENSEX, Bombay ^BSESN (Y) 2010-11-03 - 2010-12-01 2010-10-27 - 2010-12-10 0 1 *

Dow Jones-AIG Comm. ^DJC (Y) 2010-11-16 - 2010-12-04 2010-11-09 - 2010-12-10 1 1 *

FTSE 100 ^FTSE (Y) 2010-11-27 - 2010-12-26 2010-11-07 - 2011-01-03 1 1 *

Hang Seng Index ^HSI (Y) 2010-11-09 - 2010-12-09 2010-11-07 - 2010-12-16 1 1 *

Interactive Week Internet ^IIX (Y) 2010-11-12 - 2010-12-10 2010-11-04 - 2010-12-23 1 1 *

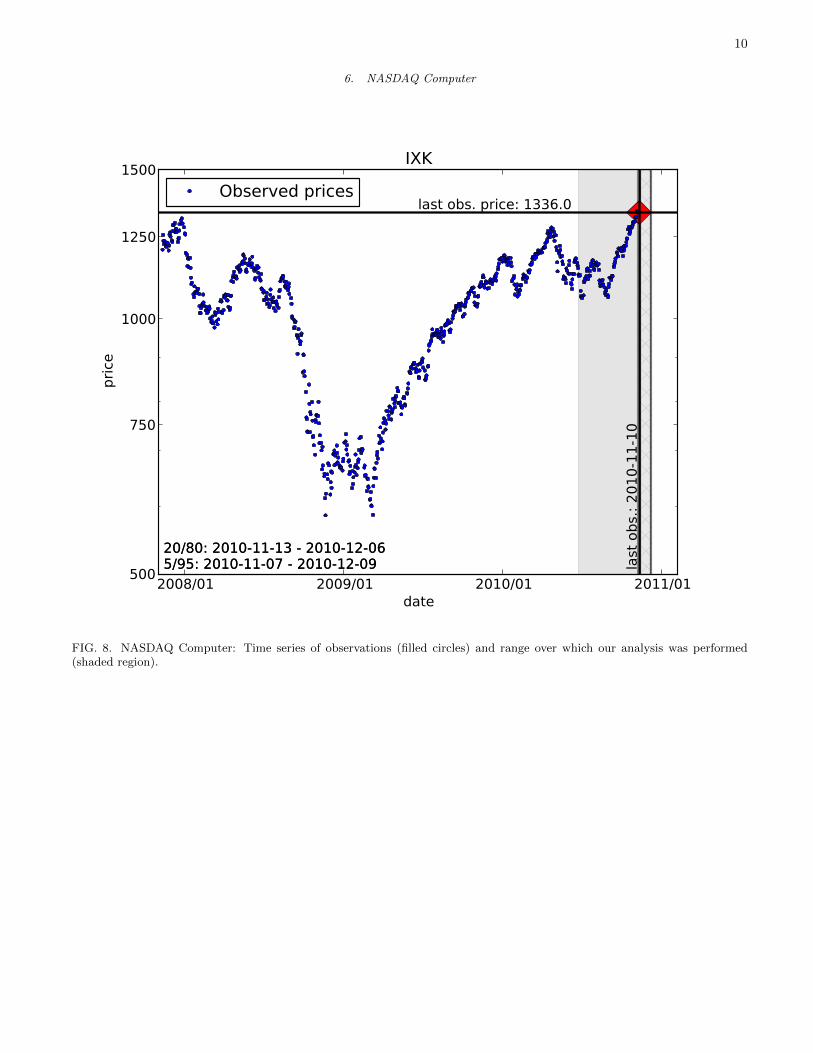

NASDAQ Computer ^IXK (Y) 2010-11-13 - 2010-12-06 2010-11-07 - 2010-12-09 1 1 *

Jakarta Composite ^JKSE (Y) 2010-11-06 - 2010-12-09 2010-10-23 - 2010-12-25 0 0

KOSPI Composite Index ^KS11 (Y) 2010-11-15 - 2010-12-26 2010-10-30 - 2011-01-07 1 0 *

NASDAQ-100 (DRM) ^NDX (Y) 2010-11-05 - 2010-11-29 2010-11-03 - 2010-12-22 1 1 *

Reuters/Jefferies CRB CRY INDEX (B) 2010-11-11 - 2010-11-22 2010-11-07 - 2010-11-26 1 1 *

TSEC weighted index ^TWII (Y) 2010-12-01 - 2011-01-03 2010-11-13 - 2011-01-08 1 -1 *

Major Market Index ^XMI (Y) 2010-11-10 - 2010-11-25 2010-10-30 - 2010-12-04 1 1 *

Equity

Ishares Singapore Index EWS (Y) 2010-11-14 - 2010-12-12 2010-11-06 - 2010-12-25 1 1 *

Freeport McMoRan FCX (Y) 2010-11-15 - 2010-12-17 2010-11-09 - 2010-12-27 1 1 *

F5 NETWORKS FFIV (Y) 2010-12-27 - 2011-03-09 2010-12-02 - 2011-04-08 1 1

INTUIT INTU (Y) 2010-11-28 - 2011-01-15 2010-11-07 - 2011-02-11 0 0 *

STARBUCKS SBUX (Y) 2010-11-08 - 2010-11-18 2010-11-06 - 2010-11-25 1 -1

UNITED RENTALS INC URI (Y) 2010-11-09 - 2010-12-13 2010-11-02 - 2011-01-08 1 -1

Commodity

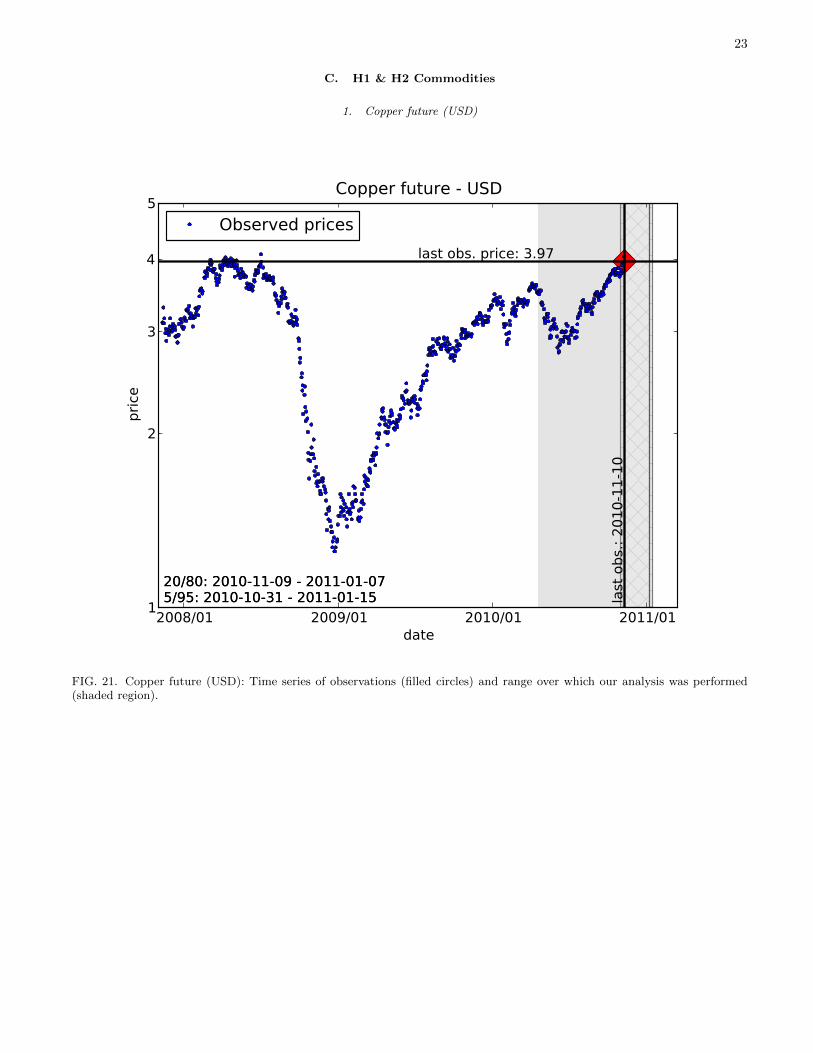

Copper future (USD) HG1 COMB Comdty (B) 2010-11-09 - 2011-01-07 2010-10-31 - 2011-01-15 1 1 *

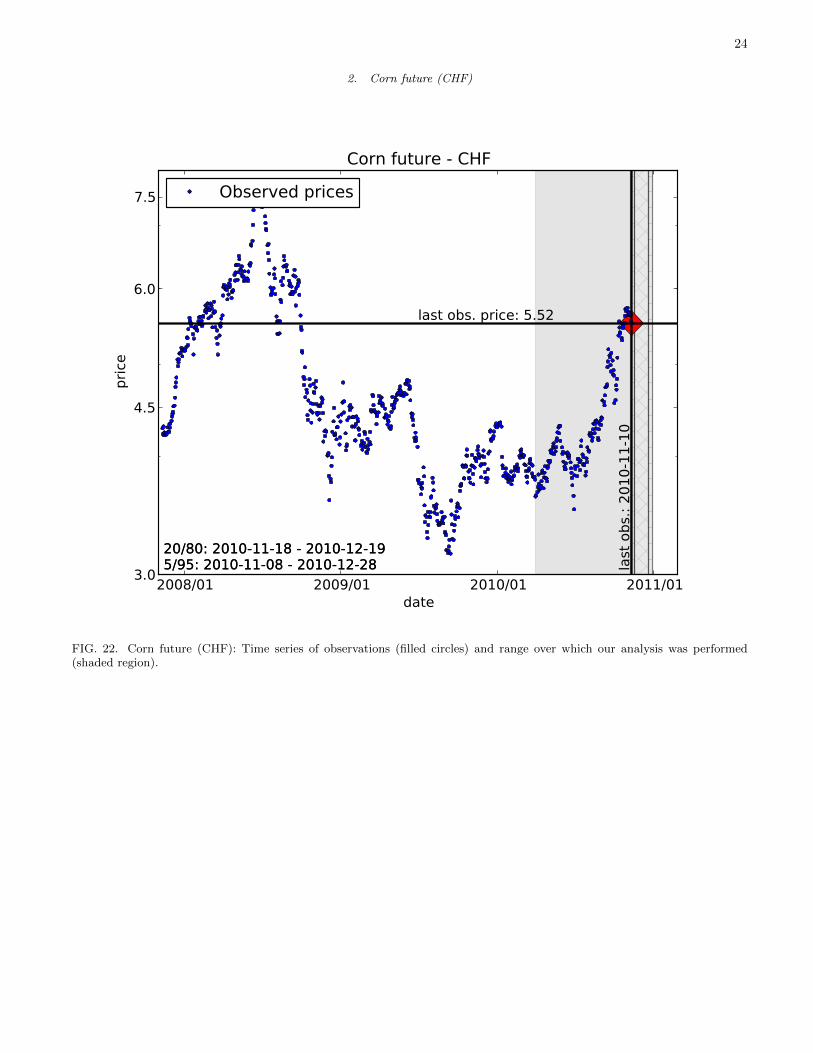

Corn future (CHF) C 1 COMB Comdty (B) 2010-11-18 - 2010-12-19 2010-11-08 - 2010-12-28 1 1 *

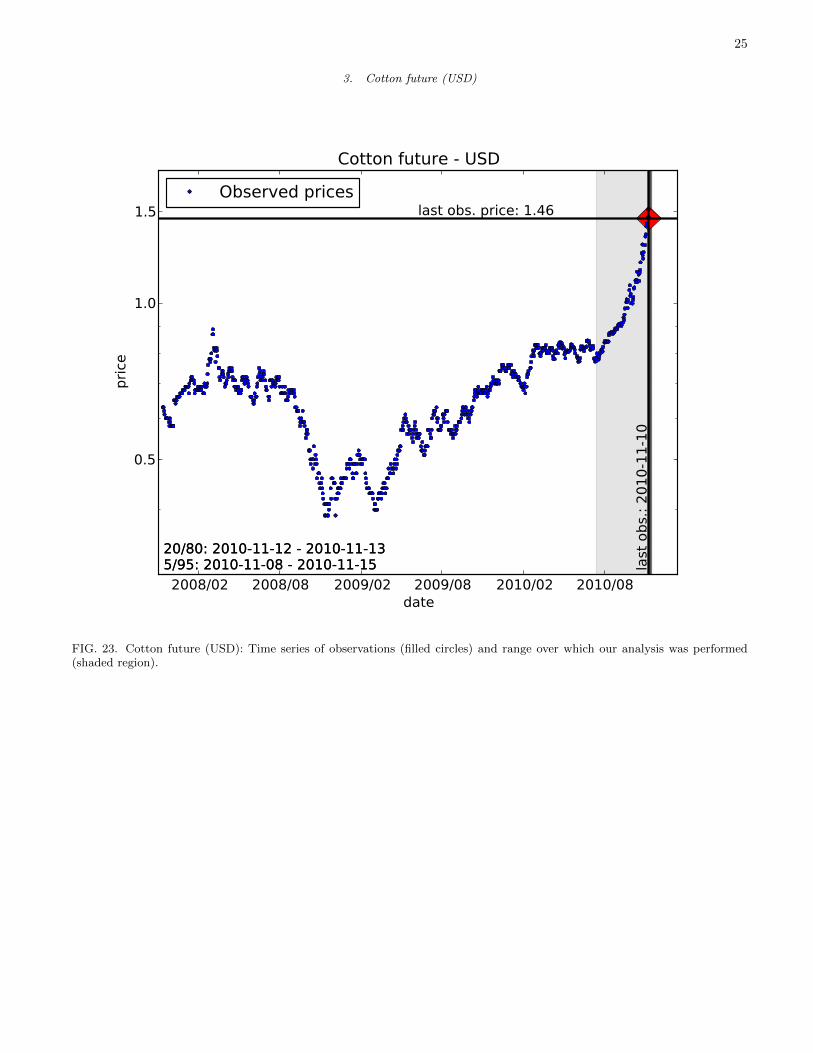

Cotton future (USD) CT1 COMB Comdty (B) 2010-11-12 - 2010-11-13 2010-11-08 - 2010-11-15 1 1 *

Palladium future (USD) PA1 COMB Comdty (B) 2010-11-12 - 2010-11-19 2010-11-10 - 2010-11-27 1 0 *

Silver future (CHF) SI1 COMB Comdty (B) 2010-11-13 - 2010-11-18 2010-11-08 - 2010-11-29 1 0 *

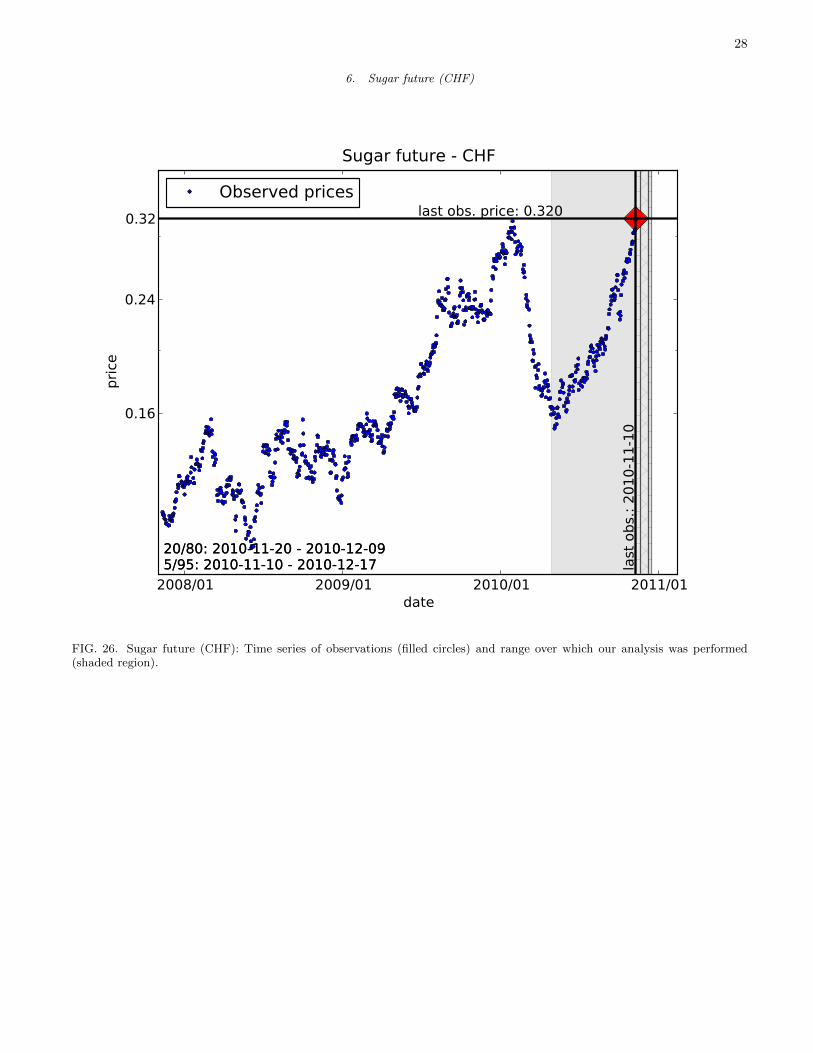

Sugar future (CHF) SB1 COMB Comdty (B) 2010-11-20 - 2010-12-09 2010-11-10 - 2010-12-17 1 1 *

Forex AUDUSD (B) 2010-11-12 - 2010-12-25 2010-10-30 - 2011-01-12 1 1 *

TABLE III. 25 H2 assets of the Financial Bubble Experiment as of 12 November 2010. All listed assetsare candidates for H1 (identified bubble phase) and H2 (identification of end of bubble phase). Quantilewindows of most likely dates of the end of the bubble phases are shown. Abbreviations (B), (Y), H1, H2and C are described in caption of Table II.

Item 1:Initial public summary document of

the FBE Vol. III,as uploaded on 12 November 2010 as v1

athttp://arxiv.org/abs/1011.2882

The Financial Bubble Experiment:Advanced Diagnostics and Forecasts of Bubble Terminations

Volume III–Master Document

R. Woodard, D. Sornette, M. Fedorovsky

(The Financial Crisis Observatory)∗

Department of Management, Technology and Economics,ETH Zurich, Kreuzplatz 5, CH-8032 Zurich, Switzerland

(Dated: 11 November 2010)

This is the third installment of the Financial Bubble Experiment. Here we provide the digitalfingerprint of an electronic document [1] in which we identify 27 bubbles in 27 different global assets;for 25 of these assets, we present windows of dates of the most likely ending time of each bubble.We will provide that document of the original analysis on 2 May 2011.

I. INTRODUCTION

The Financial Bubble Experiment (FBE) aims at testing the following two hypotheses:

• Hypothesis H1: Financial (and other) bubbles can be diagnosed in real-time before they end.

• Hypothesis H2: The termination of financial (and other) bubbles can be bracketed using probabilistic forecasts,with a reliability better than chance.

In a medical context, H1 corresponds to the diagnostic of cancer and H2 to the forecast of remaining life expectancy.The motivation of the Financial Bubble Experiment finds its roots in the failure of standard approaches. Indeed,

neither the academic nor professional literature provides a clear consensus for an operational definition of financialbubbles or techniques for their diagnosis in real time. Instead, the literature reflects a permeating culture that simplyassumes that any forecast of a bubble’s demise is inherently impossible.

Because back-testing is subjected to a host of possible biases, we propose the FBE as a real-time advanced forecastmethodology that is constructed to be free, as much as possible, of all possible biases plaguing previous tests ofbubbles. In particular, active researchers are constantly tweaking their procedures, so that predicted ‘events’ becomemoving targets. Only advance forecasts can be free of data-snooping and other statistical biases of ex-post tests. TheFBE aims at rigorously testing bubble predictability using methods developed in our group and by other scholarsover the last decade. The main concepts and techniques used for the FBE have been documented in numerous papers[2–6] and the book [7].

In the FBE, we propose a new method of delivering our forecasts where the results are revealed only after thepredicted event has passed but where the original date when we produced these same results can be publicly, digitallyauthenticated. Since our science and techniques involve forecasting, the best test of a forecast is to publicize it andwait to see how accurate it is, whether the wait involves days, weeks or months (we rarely make forecasts for longertime scales). We will do this and at the same time we want to delay the unveiling of our results until after theforecasted event has passed to avoid potential issues of liability, ethics and speculation. Also, we think that a full setof results showing multiple forecasts all at once is more revealing of the quality of our current methods than wouldbe a trickle of one such forecast every month or so. We also want to address the obvious criticism of cherry pickingsuccessful forecasts, as explained below. In order to be convincing, our experiment has to report all cases, be theysuccesses or failures.

The digital fingerprint of our first set of bubble forecasts was released on 2 November 2009 (with a hash update on6 November 2009). We added a new bubble forecast on 23 December 2009. The original forecasts and post-analysiswere presented publicly on 3 May 2010 and uploaded to the arxiv server on 14 May 2010. All versions are availableat [8].

This third set of forecasts presents the methodology described in [8] and the digital fingerprint of a single documentthat identifies and analyses 27 current asset bubbles (H1). For 25 of those 27 bubbles, the document also provideswindows of dates of the most likely ending time of each bubble. We will provide that original document of the analysison 2 May 2011.

2

II. DESCRIPTION OF THE METHODOLOGY OF THE FINANCIAL BUBBLE EXPERIMENT

Our method for this experiment is the following:

• We choose a series of dates with a fixed periodicity on which we will reveal our forecasts and make these datespublic by immediately posting them on our University web site and on the first version of our main publication,which we describe below. Specifically, our first publication of the forecasts was issued on 3 May 2010, withsuccessive deliveries every 6 months. The forecasts of the current document will be presented on 2 May 2011.However, we keep open the option of changing the periodicity of the future deliveries as the experiment unfoldsand we learn from it and from feedback of the scientific community.

• We then continue our current research involving analysis of thousands of global financial time series.

• When we have a confident forecast, we summarize it in a simple .pdf document.

• We do not make this document public. Instead, we make its digital fingerprint public. We generate two digitalfingerprints for each document, with the publicly available 256 and 512 bit versions of the SHA-2 hash algorithm[9] [10]. This creates two strings of letters and numbers that are unique to this file. Any change at all in thecontents of this file will result in different SHA-2 signatures.

• We create the first version of our main document (this one), containing a brief description of our theory andmethods, the SHA-2 hashes of our forecast and the date (2 May 2011) on which we will make the original .pdfdocument public.

• We upload this main ‘meta’ document to http://arxiv.org. This makes public our experiment and the SHA-2hashes of our forecast. In addition, it generates an independent timestamp documenting the date on which wemade (or at least uploaded) our forecast. arxiv.org automatically places the date of when the document wasfirst placed on its server as ‘v1’ (version 1). It is important for the integrity of the experiment that this date isdocumented by a trusted third party.

• We continue our research until we find our next confident forecast. We again put the forecast results in a .pdfdocument and generate the SHA-2 hashes. We now update our master document with the date and digitalfingerprint of this new forecast and upload this latest version of the master document to arxiv.org. The serverwill call this ‘v2’ (version 2) of the same document while keeping ‘v1’ publicly available as a way to ensureintegrity of the experiment (i.e., to ensure that we do not modify the SHA-2 hashes in the original document).Again, ‘v2’ has a timestamp created by arxiv.org.

• Notice that each new version contains the previous SHA-2 signatures, so that in the end there will be a list ofdates of publication and associated SHA-2 signatures.

• We continue this protocol until the future date (2 May 2011) at which time we upload our final version of themaster document. For this final version, we include the URL of a web site where the .pdf documents of all ofour past forecasts can be downloaded and independently checked for consistent SHA-2 hashes. For convenience,we will include a summary of all of our forecasts in this final document.

Note that the above method implies two aspects of the same important check to the integrity of our experiment:

1. We will reveal all forecasts, be they successful or not.

2. We will not simply ‘cherry-pick’ the results that we would want the community to see (with a few token, possibly,bad results). We do not have another simultaneous outlet where we are running a similar experiment, sincearxiv.org is a very visible international platform.

III. BACKGROUND AND THEORY

Our theories of financial bubbles and crashes have been well-researched and documented over the past 15 years inmany papers and books. We refer the reader to the Bibliography. In particular, broad overviews can be found in[2–6]. In short, our theories are based on positive feedback on the growth rate of an asset’s price by price, returnand other financial and economic variables, which lead to faster-than-exponential (power law) growth. The positivefeedback is partially due to imitation and herding among humans, who are actively trading the asset. This signature is

3

quantitatively identified in a time series by a faster-than-exponential power law component, the existence of increasinglow-frequency volatility, these two ingredients occurring either in isolation or simultaneously with varying relativeamplitudes. A convenient representation has been found to be the existence of a power law growth decorated byoscillations in the logarithm of time. The simplest mathematical embodiment is obtained as the first order expansionof the log-periodic power law (LPPL) model and is shown in Eq. (1):

lnP = A+B|t− tc|α + C|t− tc|α cos[ω ln |t− tc|+ φ] (1)

where P is the price of the asset and t is time. There are 7 parameters in this nonlinear equation, whose relativeimportance and estimation are described in our previous papers [2–6]. Our past work has led to the hypothesis thatthe LPPL signals can be useful precursors to an ending (change of regime) of the bubble, either in a crash or aless-dramatic leveling off of the growth.

IV. METHODS

A. Bubble identification

As are our theories, our methods are documented elsewhere so we only briefly mention the general technique sothat the forecasts that we make public can be better understood. In short, we scan thousands of financial time serieseach week and identify regions in the series that are well-fit by Eq. (1). We divide each time series into sub-seriesdefined by start and end times, t1 and t2 and then fit each sub-series (t1, t2). We choose max(t2) as the date of themost recent available observation. Many sub-series are created according to the following parameters: dt1 = dt2 = 7days, min(t2 − t1) = 91 days and max(t2 − t1) = 1092 days.

After filtering all fits with an appropriate range of parameters, we select those assets that have the strongest LPPLsignatures. To improve statistics, we can calculate the residues between the model and the observations and use theresidues to create 10 synthetic datasets (bootstraps) that have similar statistics as the original time series. We fitEq. (1) to the synthetic data and then extrapolate this entire ensemble of LPPL models to six months beyond our lastobservation. One of the parameters in the LPPL equation is the “crash” time tc, which represents the most probabletime of the end of the bubble and change of regime. We identify the 20%/80% and 5%/95% quantiles of tc of thefits of the ensemble consisting of original fits and bootstrap fits. These two sets of quantiles, the date of the lastobservation and the number of fits in the ensemble are published in our forecasts.

B. Post-analysis

Once the .pdf documents with the full description of the forecasts are made public, the question arises as howto evaluate the quality of the diagnostics and how these results help falsify the two hypotheses? In a nutshell, theproblem boils down to qualifying (and quantifying) what is meant by (i) a successful diagnostic of the existence of abubble and (ii) a successful forecast of the termination of the bubble. In the end, one would like to develop statisticaltests to falsify the two hypotheses stated above, using the track record that the present financial bubble experimenthas the aim to construct. For instance, Chapter 9 of (Sornette, 2003) suggests a number of options, including the“statistical roulette”, Bayesian inference and error diagrams. Our main goal with this FBE is to timestamp ourforecasts as we simultaneously continue our search for adequate measures to qualify the quality of our forecasts.

This quantification is an active, ongoing subset of our research. We are currently developing and testing novelestimations methods that will be progressively implemented in future releases. For our previous forecasts, we quantifiedthe quality of the forecasts with four measures that we will continue to use in the final analysis:

• Drawdown analysis: Drawdown analysis simply identifies the largest drawdown observed between t2 (dateof forecast) and the date of the public ‘unveiling’ of the original forecasts. That is, we identify the largestdrawdown in all available data after t2. A drawdown is simply defined as the largest peak-to-trough drop inprice in a given region.

• Fraction of up days in a running window: We calculate one day close-to-close returns for each asset andmark them as positive (up) or non-positive (zero or down). The ratio of up days relative to the sum of up anddown days in a running window of 30, 60 or 90 days is plotted on top of the price observations.

• Derivative of observations: Another measure of the change of regime is provided by an estimation of the localgrowth rate. We use the Savitzky-Golay smoothing algorithm to calculate the first derivative of the observations,using a third order polynomial fit centered within windows of 120 and 180 days.

4

• Bubble index: A measure we are developing that quantifies the quality of the LPPL fits to the price timeseries.

We are developing other measures that will be used in future analysis.

V. BUBBLE FORECASTS

The checksums of the analysis document [1] that contains the names of the 27 assets are shown in Table I. Thisdocument showing all 27 assets and 25 forecasts, as well as analysis of each identified bubble, will be uploaded tohttp://www.er.ethz.ch/fco/ on 2 May 2011.

Document name

SHA256SUM 4994beab18293be021d751d513b6fec0776fde9cf74c0098f7da8657487d950d

SHA512SUM ee20582b696a2ce880870b513e7b9e7ebb67bfbe62e2cad50dd18276a5158765af6fdf88d9fef6e047526c40478a865c722cab041386aa8efdd95da24dd9239d

TABLE I. Checksums of Financial Bubble Experiment Vol. III forecast document.

[1] R. Woodard, D. Sornette, and M. Fedorovsky (The Financial Crisis Observatory), “The Financial Bubble Experi-ment: advanced diagnostics and forecasts of bubble terminations, Vol. III–assets document,” (2011), to be posted athttp://www.er.ethz.ch/fco/ on 2 May 2011.

[2] Z.-Q. Jiang, W.-X. Zhou, D. Sornette, R. Woodard, K. Bastiaensen, and P. Cauwels, Journal of Economic Behavior &Organization 74, 149 (2010), ISSN 0167-2681, http://www.sciencedirect.com/science/article/B6V8F-4YK2DY8-1/2/3e0bc3155eed4914a7987ddd9ca7789e.

[3] A. Johansen, D. Sornette, and O. Ledoit, J. Risk 1, 5 (1999).[4] A. Johansen and D. Sornette, Brussels Economic Review 49 (2006), (http://arXiv.org/abs/cond-mat/0210509).[5] D. Sornette and A. Johansen, Quant. Financ. 1, 452 (2001).[6] D. Sornette and W.-X. Zhou, Int. J. Forecast. 22, 153 (2006).[7] D. Sornette, Why Stock Markets Crash: Critical Events in Complex Financial Systems (Princeton University Press, Prince-

ton, 2003).[8] D. Sornette, R. Woodard, M. Fedorovsky, S. Reimann, H. Woodard, and W.-X. Zhou (The Financial Crisis Ob-

servatory), “The Financial Bubble Experiment: advanced diagnostics and forecasts of bubble terminations,” (2009),http://arxiv.org/abs/0911.0454.

[9] http://en.wikipedia.org/wiki/SHA_hash_functions.[10] http://eprint.iacr.org/2008/270.pdf.

Item 2:Final analysis of the 27 bubbles,

released on 2 May 2011.

The Financial Bubble Experiment:Advanced Diagnostics and Forecasts of Bubble Terminations

Volume III–Final Analysis

R. Woodard, D. Sornette, J. Berninger

(The Financial Crisis Observatory)∗

Department of Management, Technology and Economics,ETH Zurich, Kreuzplatz 5, CH-8032 Zurich, Switzerland

(Dated: 2 May 2011)

This is the third installment of the Financial Bubble Experiment. Here we provide analysis ofthe 27 bubbles identified in the electronic document [1], whose digital fingerprint was published onarxiv.org on 12 November 2010 [2]. The abstract is purposefully succinct and without summary andconclusions in order to avoid influencing the reader and allow him/her to form his/her conclusions.

CONTENTS

I. Introduction 3

II. Executive summary of the results 3A. H1: Identification of a bubble 4B. H2: Forecast of change of regime 4

III. Explanation of analysis measures 4

IV. Results of Simple Trading Strategies 6

V. Analysis of H1 Assets 8A. H1 Indexes 9

1. MERVAL Buenos Aires 9B. H1 Equities 11

1. AUTOZONE 11

VI. Analysis of H1 & H2 Assets 13A. H1 & H2 Indexes 14

1. BSE SENSEX, Bombay 142. Dow Jones-AIG Commodity Index 163. FTSE 100 184. Hang Seng Index Hong Kong 205. Interactive Week Internet Index 226. NASDAQ Computer 247. Jakarta Composite 268. KOSPI Composite Index, Seoul 289. NASDAQ-100 (DRM) 30

10. Reuters/Jefferies CRB index 3211. TSEC weighted index 3412. Major Market Index 36

B. H1 & H2 Equities 381. Ishares Singapore Index 382. Freeport McMoRan Copper & Gold 403. F5 NETWORKS 424. INTUIT 445. STARBUCKS 466. UNITED RENTALS INC 48

C. H1 & H2 Commodities 50

2

1. Copper future (USD) 502. Corn future (CHF) 523. Cotton future (USD) 544. Palladium future (USD) 565. Silver future (CHF) 586. Sugar future (CHF) 60

D. H1 & H2 Foreign Exchange 621. AUDUSD 62

VII. State of the Market at Time of Analysis (November 2010) 64

References 65

3

I. INTRODUCTION

We acknowledge the repetition of content both within the family of FBE III documents and among theFBE I-III documents over the past 1.5 years. The repetition is intentional and is for two reasons: 1)Since each document is posted at various times as an independent entity, we want each one to be self-contained to avoid a reader having to flip between multiple documents; 2) Each installment of the FBEthat we place on the arxiv must (by their rules) be a complete document. That is, we are not allowed tosimply update one arxiv document every six months with our new forecast. Not wanting to wear out ourwelcome, we will change the format of our next public forecast.

The Financial Bubble Experiment (FBE) aims at testing the following two hypotheses:

• Hypothesis H1: Financial (and other) bubbles can be diagnosed in real-time before they end.

• Hypothesis H2: The termination of financial (and other) bubbles can be bracketed using proba-bilistic forecasts, with a reliability better than chance.

In a medical context, H1 corresponds to the diagnostic of cancer and H2 to the forecast of remaining lifeexpectancy.

The motivation of the Financial Bubble Experiment finds its roots in the failure of standard approaches.Indeed, neither the academic nor professional literature provides a clear consensus for an operationaldefinition of financial bubbles or techniques for their diagnosis in real time. Instead, the literaturereflects a permeating culture that simply assumes that any forecast of a bubble’s demise is inherentlyimpossible.

Because back-testing is subjected to a host of possible biases, we propose the FBE as a real-timeadvanced forecast methodology that is constructed to be free, as much as possible, of all possible bi-ases plaguing previous tests of bubbles. In particular, active researchers are constantly tweaking theirprocedures, so that predicted ‘events’ become moving targets. Only advance forecasts can be free ofdata-snooping and other statistical biases of ex-post tests. The FBE aims at rigorously testing bubblepredictability using methods developed in our group and by other scholars over the last decade. Themain concepts and techniques used for the FBE have been documented in numerous papers [3–7] andthe book [8]. The FCO research team is currently developing and testing novel estimations methods thatwill be progressively implemented in future releases.

In the FBE, we propose a new method of delivering our forecasts where the results are revealed onlyafter the predicted event has passed but where the original date when we produced these same results canbe publicly, digitally authenticated. Since our science and techniques involve forecasting, the best test ofa forecast is to publicize it and wait to see how accurate it is, whether the wait involves days, weeks ormonths (we rarely make forecasts for longer time scales). We will do this and at the same time we wantto delay the unveiling of our results until after the forecasted event has passed to avoid potential issues ofliability, ethics and speculation. Also, we think that a full set of results showing multiple forecasts all atonce is more revealing of the quality of our current methods than would be a trickle of one such forecastevery month or so. We also want to address the obvious criticism of cherry picking successful forecasts,as explained below. In order to be convincing, our experiment has to report all cases, be they successesor failures.

The digital fingerprint of our first set of bubble forecasts was released on 2 November 2009 (with ahash update on 6 November 2009). We added a new bubble forecast on 23 December 2009. The originalforecasts and post-analysis were presented publicly on 3 May 2010 and uploaded to the arxiv serveron 14 May 2010. All versions are available at [9]. The digital fingerprint of the second set of forecastswas uploaded to the arxiv on 12 May 2010 and the names of the assets were revealed on 1 November2010 [10].

This third set of forecasts continues using the methodology described in [9, 10]. A document with thedigital fingerprint of a separate document identifying 27 asset bubbles (H1) was posted to the arxiv on11 November 2010 [2] (though a minor resubmission the following morning places the arxiv timestampas 12 November 2010). For 25 of those 27 bubbles, the ‘sealed’ document also provided windows of datesof the most likely ending time of each bubble (H2).

We now provide that document at http://www.er.ethz.ch/fco/ and analysis of our bubble identifi-cations and forecasts below.

II. EXECUTIVE SUMMARY OF THE RESULTS

The 2 H1 assets and 25 H2 assets (with forecast quantiles of the end of the bubbles) are shown in thefollowing sections with quantitative results. A complete visual representation is available in the figures

4

in Sections V-VI.We confirm ‘bubble’ by an ex-post inspection of the price times series: a major downward change

in the growth rate of the price time series within the six months after our analysis indicates that theasset had been in a bubble. Because the definition of what is a “major downward change” is prone topossible subjective and a posteriori tweaking, we offer several metrics described below: (i) drawdowns,(ii) fraction of up days in running windows, and (iii) derivative of the log-price (providing an estimate ofthe trend). In general, our bubble theory says that a bubble ends in a change of regime, that is, whenthe super-exponential growth rate ends. This could range from a simple lessening of the growth rateto a large crash. One of the most frequent types of change of regime that we observed in this currentexperiment occurred when the price time series exhibited a well-defined correction or crash within 6months immediately following the date of when the initial document was posted to the arxiv on 12November 2010 [2].

A. H1: Identification of a bubble

We support H1 by confirming that bubbles existed in 24 of the 27 assets at the time of the lastobservation of our forecasts, t2 = 10 November 2010.

B. H2: Forecast of change of regime

We support H2 by confirming that 17 of the 25 H2 assets showed substantial corrections in the quantilewindows that we forecast.

III. EXPLANATION OF ANALYSIS MEASURES

In the following subsections, we include figures for each asset. The figures share some common features,explained here. Details for each individual asset and measure are discussed below.

Axes and observations: Price (or value of the asset) is shown on the left vertical axis and calendardays are indicated on the bottom horizontal axis. The circles represent closing price observations ontrading days. Note that the price axis shows observations in their natural units on a logarithmic scale.

Large shaded region, vertical and horizontal black lines: The large grey shaded regions thatbegin near the left price axis and end at the solid black vertical line near the right vertical axis representthe domain of the observations used in our analysis. The vertical line itself sits at t2 = 10 November2010: the last observation used in the analysis. The price at t2 is represented by the solid black horizontalline.

Small hatched, shaded regions: Two hatched shaded regions begin in the vicinity of t2. Theyrepresent our forecast “danger” zones, where changes of regimes are most likely to occur. The inner,narrow one with diagonal hatching represents the 20-80% quantile interval and the outer, wider onewith horizontal hatching represents the 5-95% quantile interval. That is, these two numbers imply a 60%(respectively, 90%) probability for the end of the bubble to be located within the diagonally (respectively,horizontally) hatched zone. The hatched shaded regions are presented for all 27 assets, even the two(MERVAL and AZO) for which we did not publish forecasts.

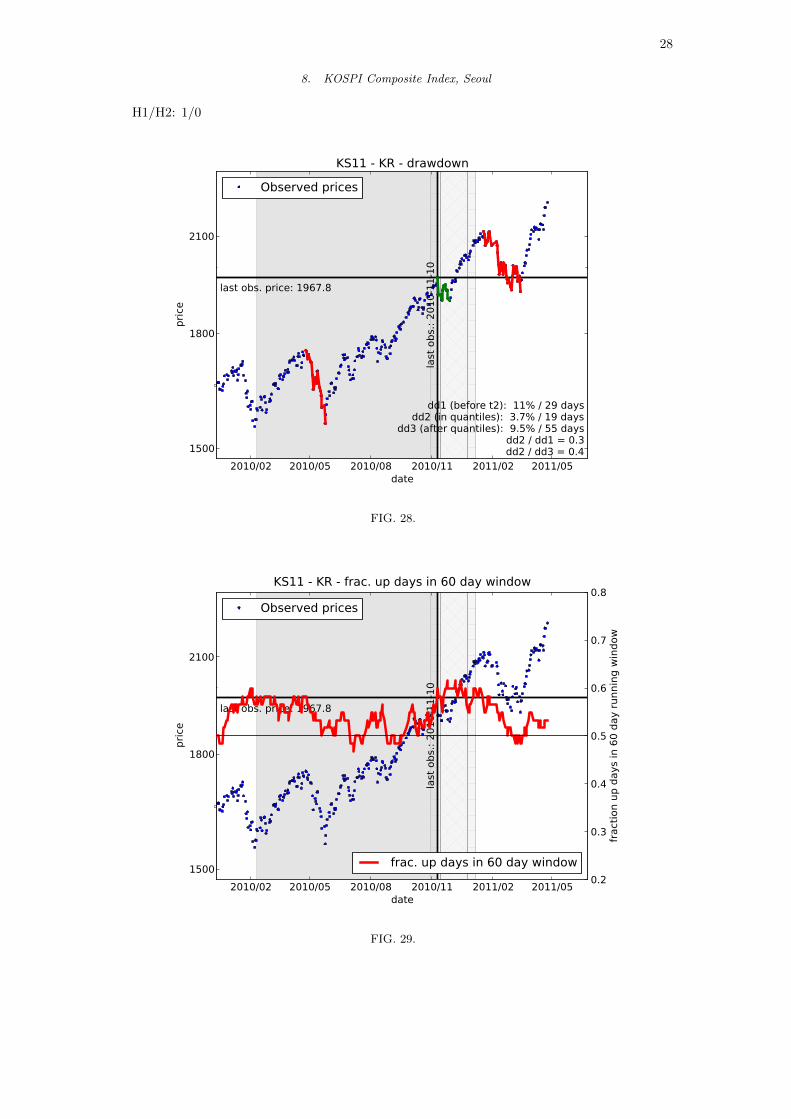

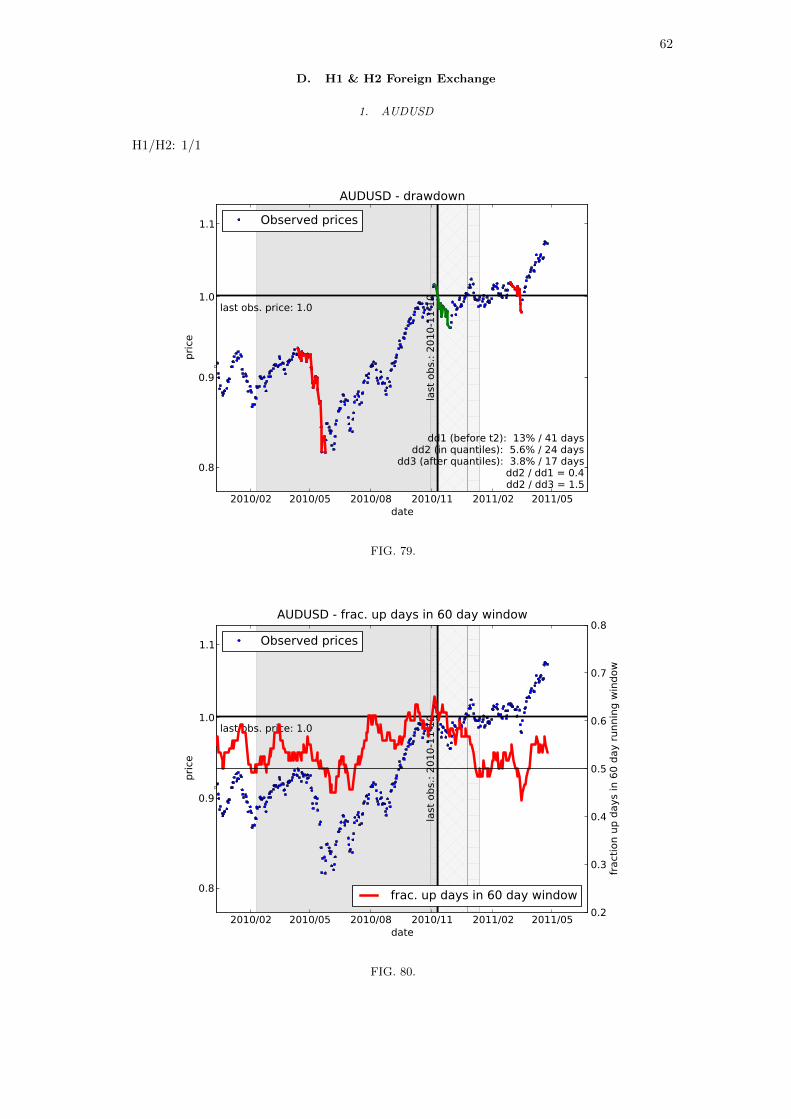

Drawdown analysis: Drawdown analysis figures show a solid red or green line connecting the pathof the largest drawdown observed in three distinct sections:

1. between the beginning of the domain of analysis (left edge of large shaded grey region) and t2 (redline);

2. between the 5% and 95% forecast windows (green line);

3. between the 95% quantile line and 27 April 2011 (red line).

5

The percentage drop and duration of each drawdown is indicated in text in the lower right corner ofeach figure. A drawdown is simply defined as the largest peak-to-trough drop in price in a given region.Defining the price at the peak as p1 and at the trough as p2 < p1, we give the percent drawdown of thelog return. That is, the drawdown percentage that we report on each drawdown plot is calculated asd = 100 log(p1/p2). Log returns are approximately equal to arithmetic returns (defined as 100(p1−p2)/p1)for small returns but are increasingly larger than the arithmetic return for larger returns.

Note that some forecast windows include dates just before t2, such as when the change in regime startedright at the end of our analysis window (obvious in hindsight but not at the time of publication!). Inthese cases, a drawdown can begin before t2. Also shown in the text is the ratio of the forecast maximumdrawdown to the maximum before and after drawdowns.

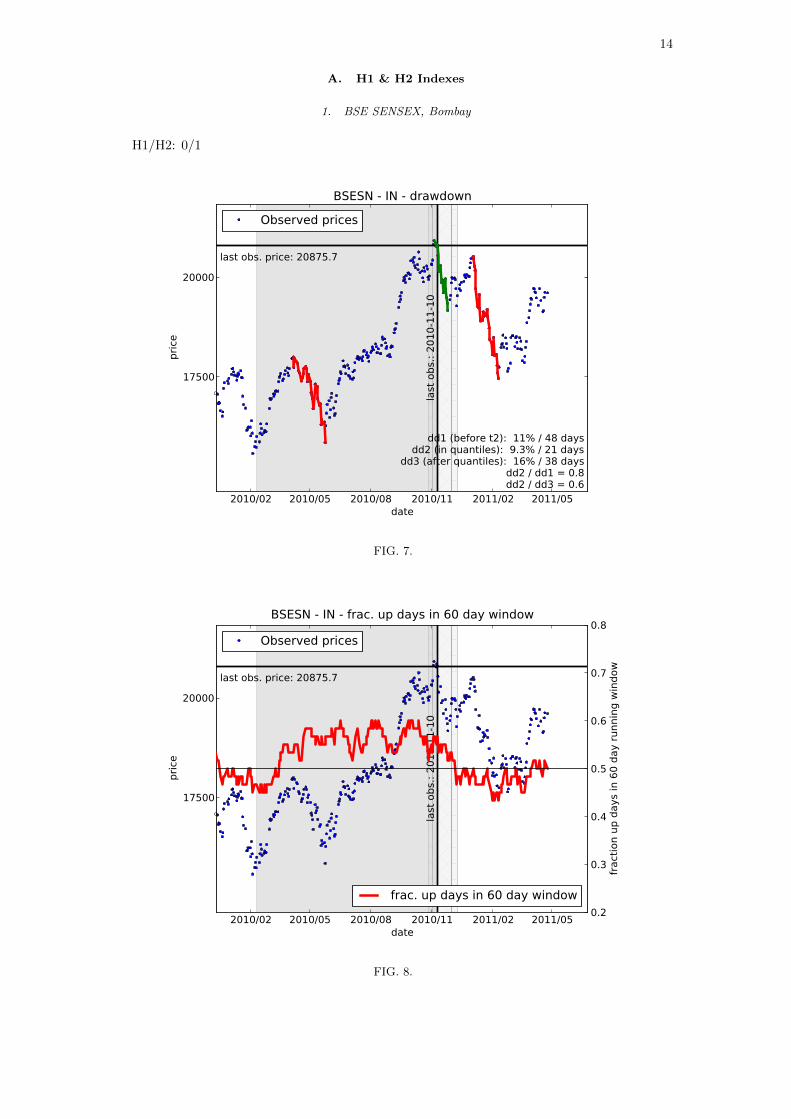

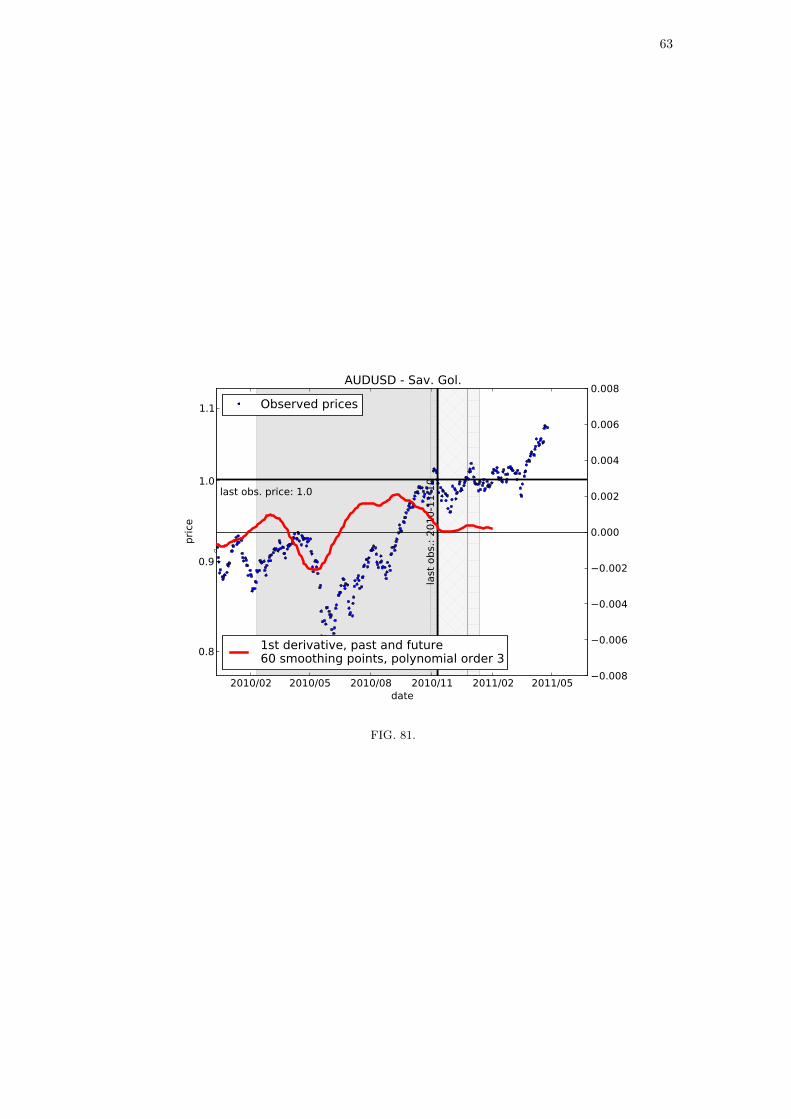

Fraction of up days in a running window: We calculate one day close-to-close returns for eachasset and mark them as positive (up) or non-positive (zero or down). The ratio of up days relative tothe sum of up and down days in a running window of 60 days is plotted on top of the price observations.The right vertical axis shows this fraction on a linear scale. Note that we do not include returns with avalue of zero in the calculation of this ratio. Also, the running window ends at the value plotted on thetime axis. That is, only present and past data is used in the running window, not future data.

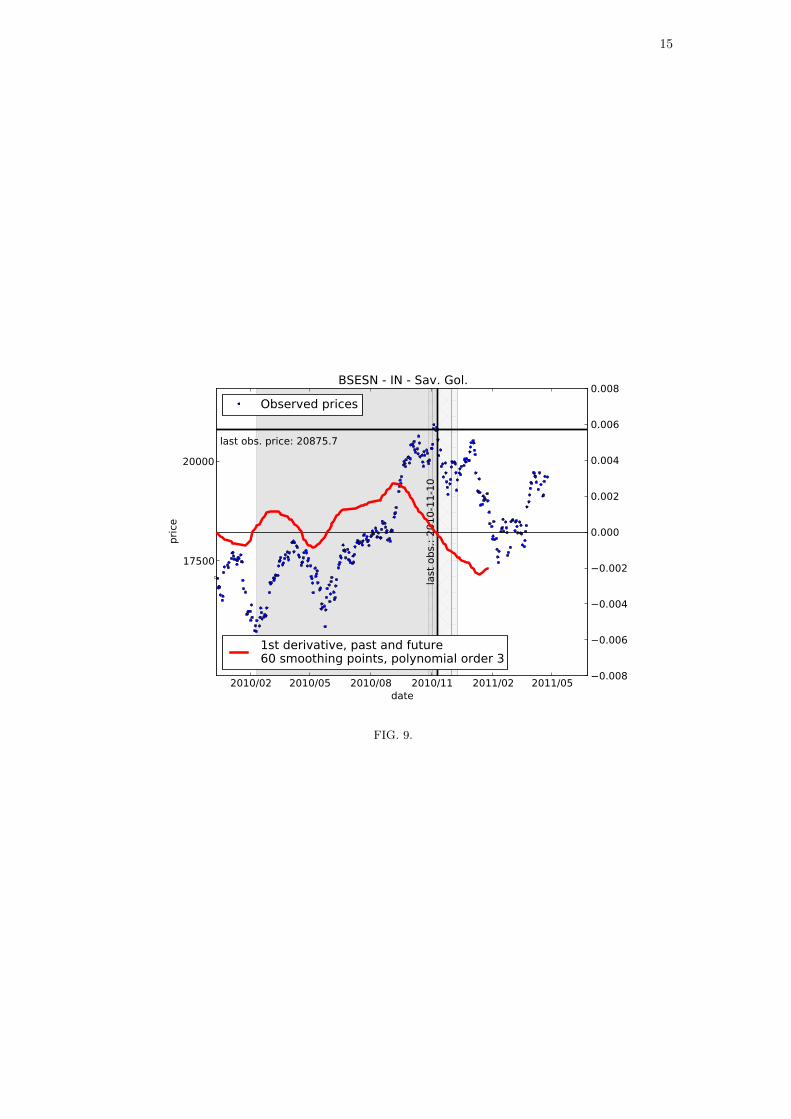

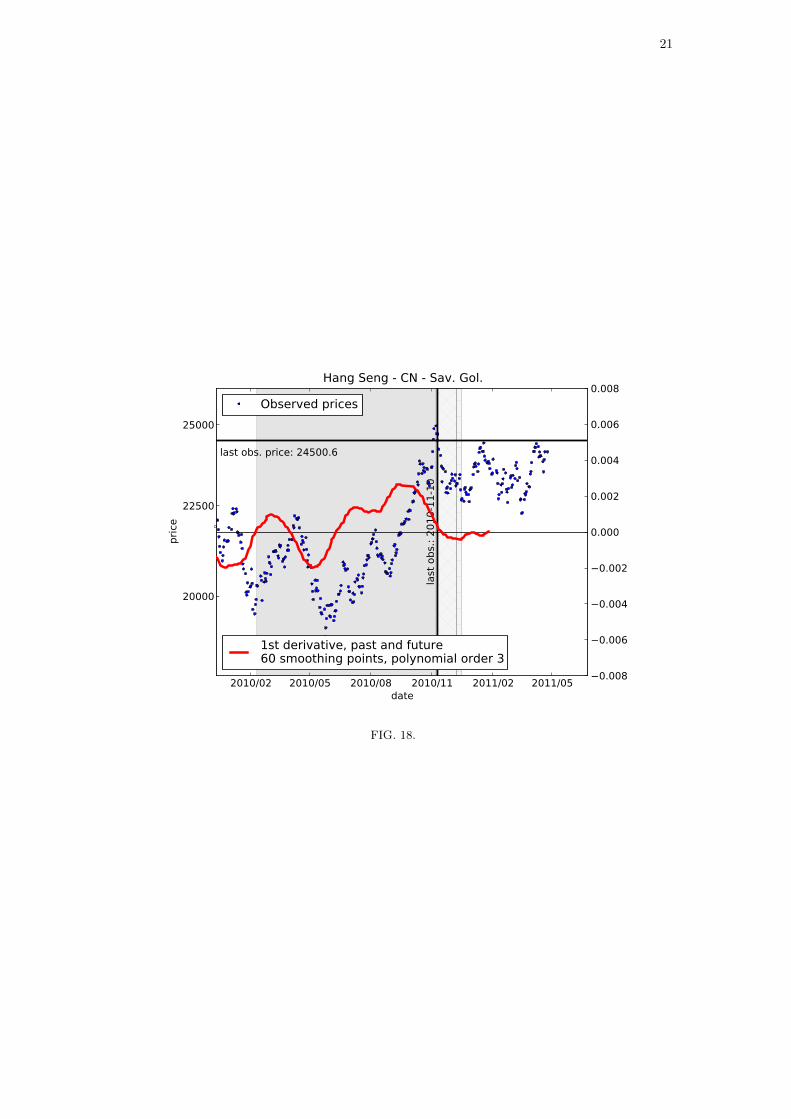

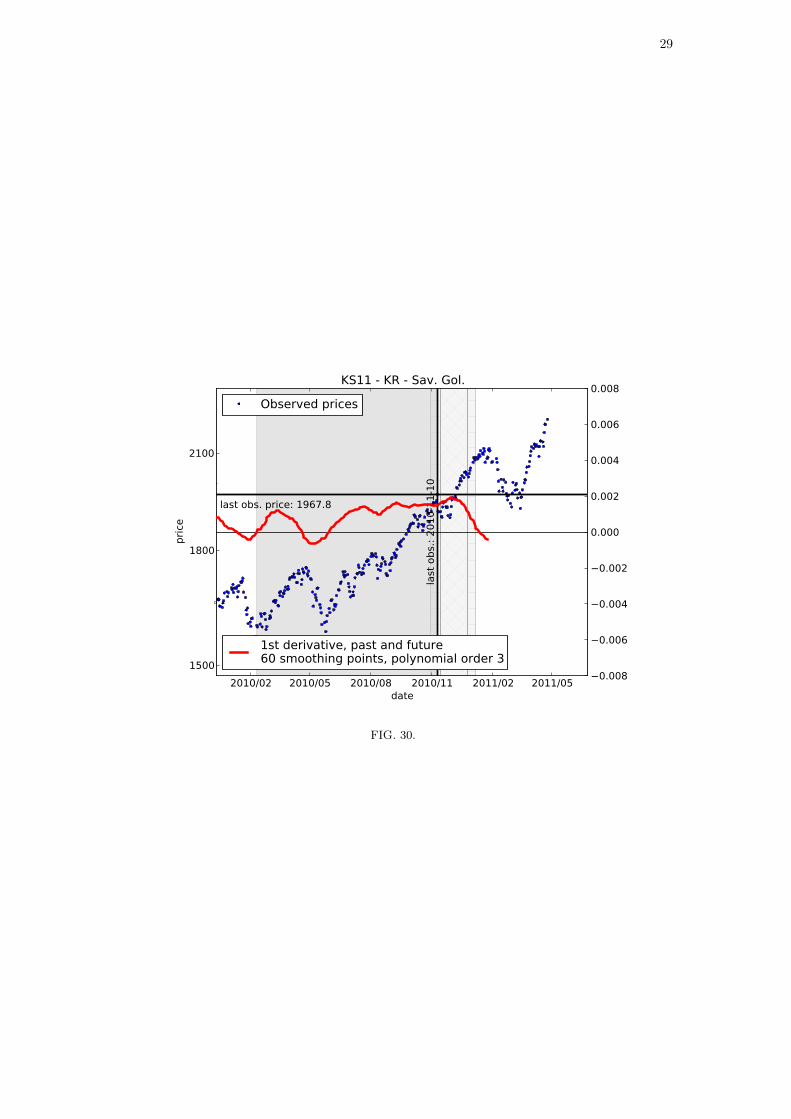

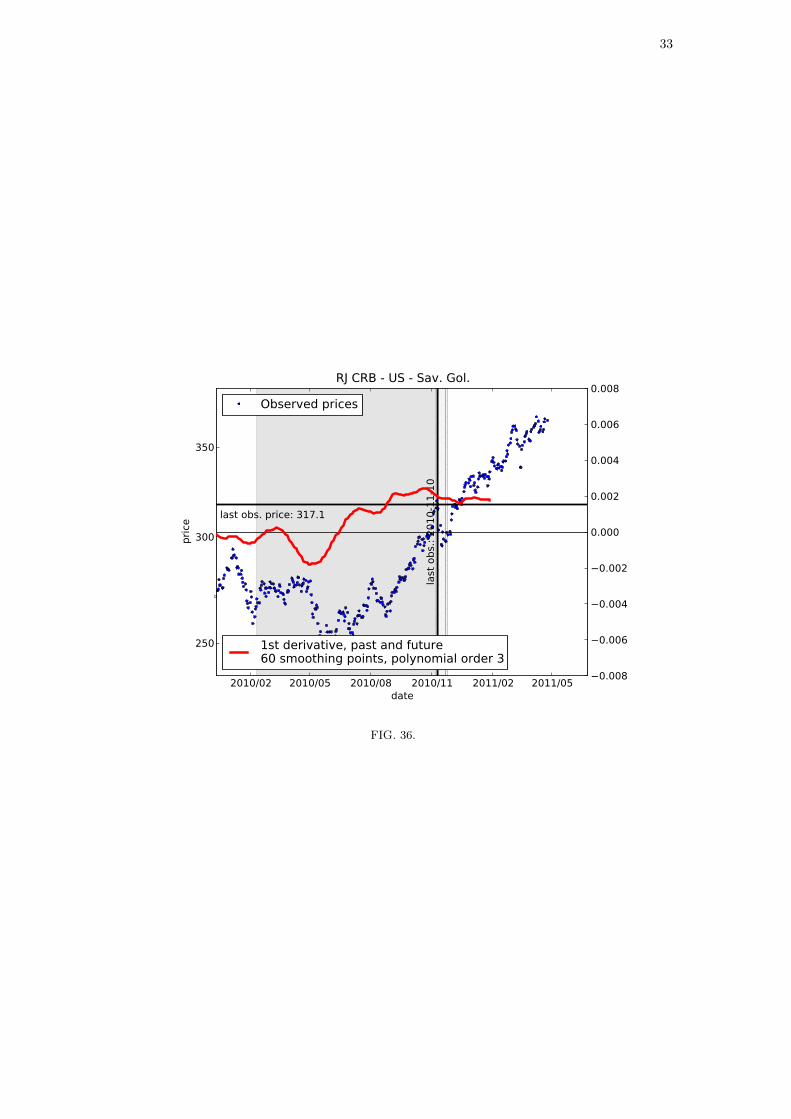

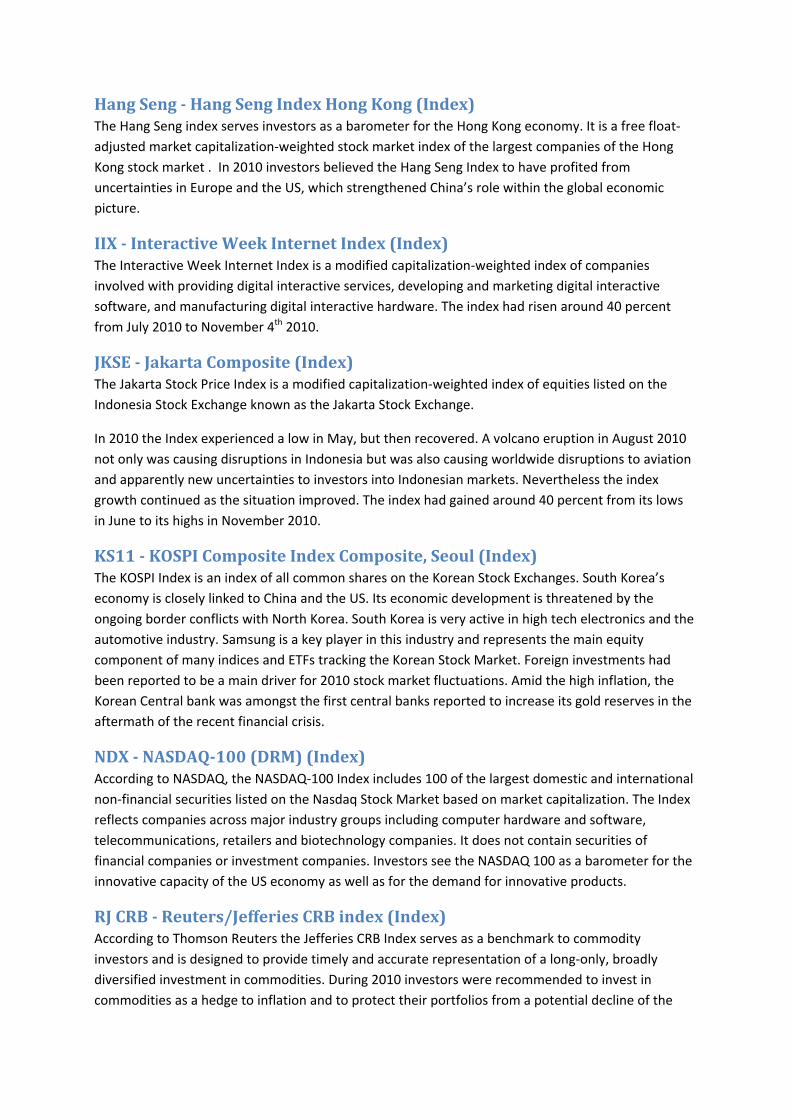

Derivative of observations: Another measure of the change of regime is provided by an estimationof the local growth rate. We use the Savitzky-Golay smoothing algorithm to calculate the first derivativeof the observations, using a third order polynomial fit centered within windows of 120 days (60 days past,60 days future). The scale of the estimated derivative is shown on the right vertical axis using linearscaling. Note that this right vertical axis has different limits for each asset, to reflect the different ordersof magnitude of some assets.

Scoring of forecasts (-1, 0, 1): An initial quantification of our forecasts is made with a simplescoring of -1, 0 or 1, which we use to indicate whether a major downward change in the growth rate ofthe price time series within the six months after t2 occurred. Specifically:

• -1: No major downward change after t2.

• 0: Signal unclear.

• 1: H1: Major downward change after t2; H2: change occurred within forecast quantile windows.

Potential correlated dynamics around t2. In 22 of 27 assets, a major downward change beganwithin 1-3 days on either side of our last analysis date t2 =2010-11-10. These assets are indicated witha ‘*’ in column ‘C’ of Tables II-III. This striking correlated dynamics will be discussed in a futurepublication.

An obvious criticism arises: if many of these assets began their major downward changes around 10November, it might appear as if we strategically waited until 12 November to confirm these major changesbefore publishing. Because support of our scientific hypotheses depends so much on advanced prediction,the timing of our statements is critical. Therefore, it is important that we address this potential criticism:

• Our submission to the arxiv on 12 November 2010 was made before U.S. markets opened, hence,at most, we could have used closing price data from 11 November (though we did not). In fact, wesubmitted on 11 November 2010 but a minor edit the next day made our ‘official’ timestamp 12November 2010.

• Most of the large drawdowns that began on or before 11 November 2010 certainly had not ended by12 November 2010. Only in hindsight can one look at a historical time series and say that “the largedrawdown started on that date”. Our point is that for an observer on 12 November 2010 lookingat just the 22 price time series that include closing prices only through 11 November 2010 (thoughwe used 10 November) and that share this correlated dynamics, it was entirely unclear whetherthe drops that had begun were only noisy fluctuations or the beginning of something larger. Twopossible exceptions to this are DJC and Sugar Future CHF, as they both exhibited major drawdownsby 12 November. Again, though, we did not take such an observation into account in our assetselection.

6

IV. RESULTS OF SIMPLE TRADING STRATEGIES

The true measure of success for any theory that attempts to forecast asset price movement must be interms of realized profit and loss using a trading strategy based on the theory. Proper trading strategiesand quantification of them lie outside the scope of this paper. To give a flavor, though, of what thesepresent results imply, we consider two of the simplest deterministic strategies using output of our analysis.We choose a date to sell short one share of each asset and a second date to buy it back and then calculatethe return without any attempt to include market friction, fees, etc. We use the closing price on each ofthese dates.

The date we open each position, when we sell short one share, is the latter of either t2 =10 November2010 or the date of the 5% quantile. We choose two buy back strategies. The first is closing the position(i.e., buying back the share) at the date of the 95% quantile. The second strategy involves using somefuture information, so would not be easily implementable: once we calculate the maximum drawdownwithin the quantiles window, we choose the first day after the end of this drawdown to buy the shareback. The results of both strategies are shown in Table I.

Admittedly, this first strategy is rather naive and, in reality, would not be implemented because itcontinues (stupidly) to accumulate losses when a drawdown is followed by an upward correction, asillustrated for instance by the example of Copper futures. Note that time ‘passes through’ the profitablestrategy 2 to reach the unprofitable endpoint of strategy 1. That is, a human trader or more intelligentautomatic algorithm could implement a stop-gain buy back order at, for instance, 4% profit and a stop-loss buy back order at, say -1%. This would, sadly, eliminate some of the larger gains shown in BuyBack Strategy 2 but would also eliminate the large losses, making an overall profitable process with lessvolatility. Further, the (assumed) 4% profit is over the holding period for each asset, which is usually (inthese case) on the order of 1-2 months. Hence, an annualized return would be larger.

7

Sell Buy Back Strategy 1 Buy Back Strategy 2Name date price date price % ret date price % retAZO 2010-11-26 259.48 2011-01-24 251.49 3.1 2011-01-07 250.67 3.5EWS 2010-11-10 14.04 2010-12-29 13.68 2.6 2010-11-24 13.19 6.2FCX 2010-11-10 51.95 2010-12-29 59.33 -13.3 2010-11-18 49.72 4.4FFIV 2010-12-06 139.80 2011-04-25 105.71 28.0 2011-03-23 95.67 37.9INTU 2010-11-10 48.83 2011-02-11 50.62 -3.6 2010-11-24 45.65 6.7SBUX 2010-11-10 30.34 2010-11-22 30.87 -1.7 2010-11-17 29.99 1.2URI 2010-11-10 20.38 2010-12-31 22.75 -11.0 2010-12-16 22.50 -9.9BSESN 2010-11-10 20875.71 2010-12-10 19508.89 6.8 2010-11-29 19405.10 7.3DJC 2010-11-10 154.19 2010-12-13 155.99 -1.2 2010-11-18 146.56 5.1FTSE 2010-11-10 5816.90 2011-01-04 6013.90 -3.3 2010-12-01 5642.50 3.0Hang Seng 2010-11-10 24500.61 2010-12-16 22668.78 7.8 2010-12-17 22714.85 7.6IIX 2010-11-10 312.68 2010-12-27 310.85 0.6 2010-11-17 295.10 5.8IXK 2010-11-10 1336.04 2010-12-13 1365.22 -2.2 2010-11-17 1278.03 4.4JKSE 2010-11-10 3756.97 2010-12-21 3637.45 3.2 2010-12-01 3619.09 3.7KS11 2010-11-10 1967.85 2011-01-07 2086.20 -5.8 2010-11-30 1904.63 3.3MERV 2010-11-10 3310.97 2010-11-15 3270.78 1.2 2010-11-15 3270.78 1.2NDX 2010-11-10 2187.74 2010-12-27 2229.86 -1.9 2010-11-17 2100.00 4.1TWII 2010-11-15 8240.65 2011-01-10 8817.88 -6.8 2011-01-10 8817.88 -6.8XMI 2010-11-10 1245.15 2010-12-28 1261.25 -1.3 2010-12-01 1232.80 1.0Copper future 2010-11-10 3.97 2011-01-17 4.37 -9.8 2010-11-24 3.76 5.5Corn future 2010-11-10 5.52 2010-12-28 5.92 -6.9 2010-11-23 5.26 5.0Cotton future 2010-11-10 1.46 2010-11-15 1.39 4.9 2010-11-16 1.34 8.5Palladium future 2010-11-10 696.75 2010-11-29 693.00 0.5 2010-11-17 654.85 6.2Silver future 2010-11-10 26.18 2010-11-29 27.19 -3.8 2010-11-17 25.27 3.5Sugar future 2010-11-10 0.32 2010-12-17 0.32 1.3 2010-11-15 0.27 18.5AUDUSD 2010-11-10 1.00 2011-01-12 1.00 0.5 2010-11-30 0.96 4.2RJ CRB 2010-11-10 317.11 2010-11-26 301.13 5.2 2010-11-18 302.51 4.7Mean -0.3 5.4Mean (no FFIV, URI) -1.0 4.7

TABLE I: Results of simple trading strategies: We choose the latter of the two dates, t2 =10 November2010 or the date of the 5% quantile. We sell short a share of the asset at the closing price of this date.For Buy Back Strategy 1, we buy back the share at the closing price of the date of the 95% quantile.

Note that this first strategy is rather naive and, in reality, would not be implemented because itcontinues stupidly to accumulate losses when a drawdown is followed by an upward correction, as

illustrated for instance by the example of Copper futures. For Buy Back Strategy 2, we buy back theshare at the closing price of the day after the last day of the maximum drawdown found in thequantiles. Note that this second strategy uses future information in order to calculate when the

maximum drawdown would be, hence such a strategy could not be automatically implemented. Thebottom two rows show the simple mean values of the return columns, with the final row showing the

mean with the largest gain (FFIV) and largest loss (URI) removed.

8

V. ANALYSIS OF H1 ASSETS

In our initial document posted to the arxiv on 12 November 2010 [2], we diagnosed that the 2 assetsin this Section (see Table II) were in a bubble phase (H1) but we did not make forecasts of likely datesof change of regime (H2). For each asset, we present a figure showing the time series of the observationsand indicate the range over which our analysis was performed (the shaded area in each figure).

2 H1 Assets (identified bubble)Category Asset Ticker H1 CIndex MERVAL Buenos Aires ^MERV (Y) 1 *Equity AUTOZONE AZO (Y) 1

TABLE II: 2 H1 assets of the Financial Bubble Experiment as of 12 November 2010. All listed assets arecandidates for H1 (identified bubble phase). In the Ticker column, (B) stands for Bloomberg and (Y) forYahoo Finance. Columns ‘H1’ and ‘H2’ show a somewhat subjective score of -1 (worst), 0 or 1 (best),reflecting the quality of the forecasts. This scoring is discussed further in Section III of the main analysisdocument available at http://www.er.ethz.ch/fco/index. Column ‘C’ has an asterisk if an asset hada major correction within 3 days of t2 =2010-11-10 (the last data observation used in our analysis). Thiscorrelated dynamics also is discussed in Section III of the same analysis document.

We support H1 by confirming that bubbles existed in 24 of the 27 assets at the time of the lastobservation of our forecasts, t2 = 10 November 2010. These 24 include the 2 H1-only candidates of thissection and 22 of the 25 H1-H2 candidates of Section VI.

9

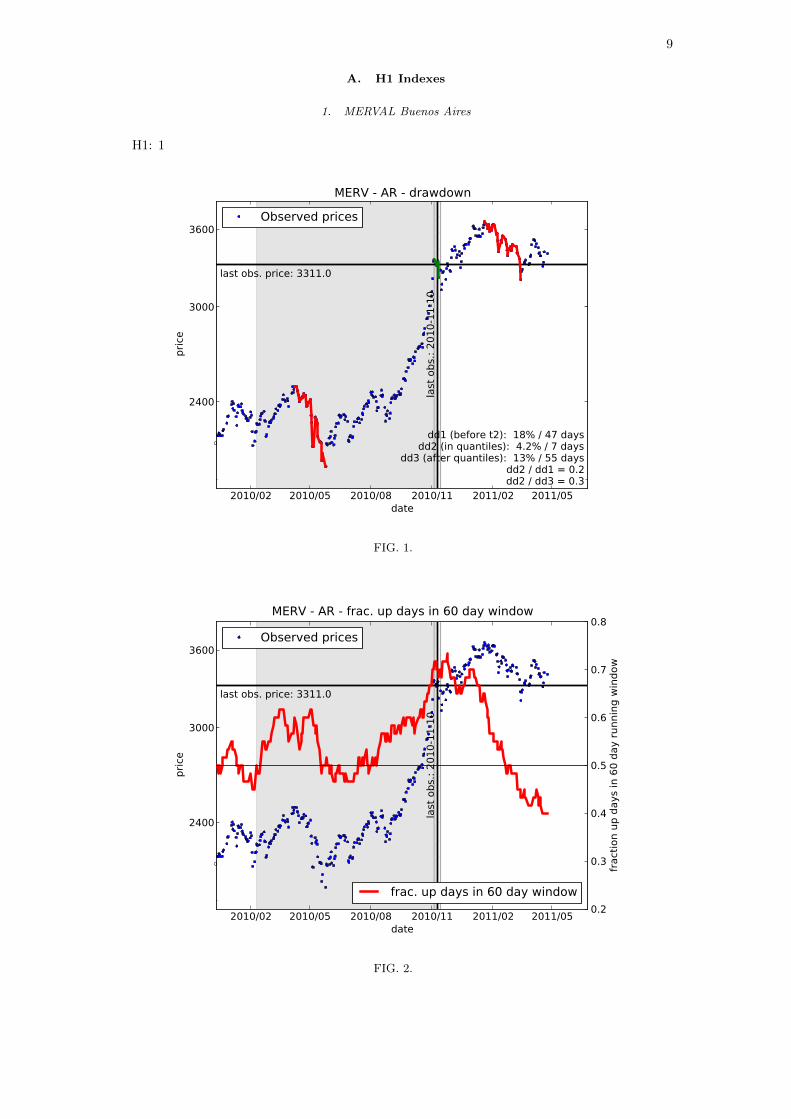

A. H1 Indexes

1. MERVAL Buenos Aires

H1: 1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

2400

3000

3600

pric

e

last obs. price: 3311.0

last

obs

.: 20

10-1

1-10

dd1 (before t2): 18% / 47 daysdd2 (in quantiles): 4.2% / 7 days

dd3 (after quantiles): 13% / 55 daysdd2 / dd1 = 0.2dd2 / dd3 = 0.3

MERV - AR - drawdown

Observed prices

FIG. 1.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

2400

3000

3600

pric

e

last obs. price: 3311.0

last

obs

.: 20

10-1

1-10

MERV - AR - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 2.

10

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

2400

3000

3600

pric

e

last obs. price: 3311.0

last

obs

.: 20

10-1

1-10

MERV - AR - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 3.

11

B. H1 Equities

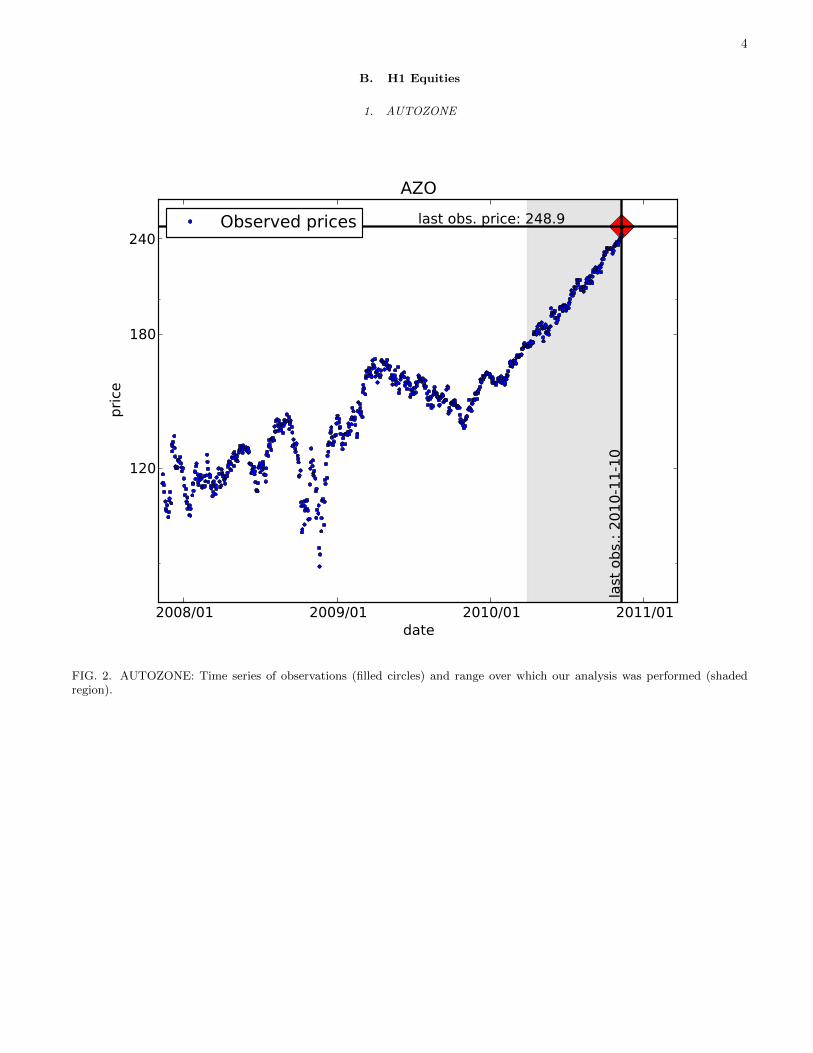

1. AUTOZONE

H1: 1

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

150

200

250

pric

e

last obs. price: 248.9

last

obs

.: 20

10-1

1-10

dd1 (before t2): 5.7% / 4 daysdd2 (in quantiles): 9.9% / 7 days

dd3 (after quantiles): 4.7% / 7 daysdd2 / dd1 = 1.7dd2 / dd3 = 2.1

AZO - US - drawdown

Observed prices

FIG. 4.

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

150

200

250

pric

e

last obs. price: 248.9

last

obs

.: 20

10-1

1-10

AZO - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 5.

12

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

150

200

250

pric

e

last obs. price: 248.9

last

obs

.: 20

10-1

1-10

AZO - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 6.

13

VI. ANALYSIS OF H1 & H2 ASSETS

In our initial document posted to the arxiv on 12 November 2010 [2], we diagnosed that the 25 assetsin this Section (see Table III) were all in a bubble phase (H1) and were likely to end within the quantileranges indicated in Table III (H2).

25 H1 and H2 Assets (identified bubble)Category Asset Ticker tc 20% - 80% tc 5% - 95% H1 H2 C

Index

BSE SENSEX, Bombay ^BSESN (Y) 2010-11-03 - 2010-12-01 2010-10-27 - 2010-12-10 0 1 *Dow Jones-AIG Comm. ^DJC (Y) 2010-11-16 - 2010-12-04 2010-11-09 - 2010-12-10 1 1 *FTSE 100 ^FTSE (Y) 2010-11-27 - 2010-12-26 2010-11-07 - 2011-01-03 1 1 *Hang Seng Index ^HSI (Y) 2010-11-09 - 2010-12-09 2010-11-07 - 2010-12-16 1 1 *Interactive Week Internet ^IIX (Y) 2010-11-12 - 2010-12-10 2010-11-04 - 2010-12-23 1 1 *NASDAQ Computer ^IXK (Y) 2010-11-13 - 2010-12-06 2010-11-07 - 2010-12-09 1 1 *Jakarta Composite ^JKSE (Y) 2010-11-06 - 2010-12-09 2010-10-23 - 2010-12-25 0 0KOSPI Composite Index ^KS11 (Y) 2010-11-15 - 2010-12-26 2010-10-30 - 2011-01-07 1 0 *NASDAQ-100 (DRM) ^NDX (Y) 2010-11-05 - 2010-11-29 2010-11-03 - 2010-12-22 1 1 *Reuters/Jefferies CRB CRY INDEX (B) 2010-11-11 - 2010-11-22 2010-11-07 - 2010-11-26 1 1 *TSEC weighted index ^TWII (Y) 2010-12-01 - 2011-01-03 2010-11-13 - 2011-01-08 1 -1 *Major Market Index ^XMI (Y) 2010-11-10 - 2010-11-25 2010-10-30 - 2010-12-04 1 1 *

Equity

Ishares Singapore Index EWS (Y) 2010-11-14 - 2010-12-12 2010-11-06 - 2010-12-25 1 1 *Freeport McMoRan FCX (Y) 2010-11-15 - 2010-12-17 2010-11-09 - 2010-12-27 1 1 *F5 NETWORKS FFIV (Y) 2010-12-27 - 2011-03-09 2010-12-02 - 2011-04-08 1 1INTUIT INTU (Y) 2010-11-28 - 2011-01-15 2010-11-07 - 2011-02-11 0 0 *STARBUCKS SBUX (Y) 2010-11-08 - 2010-11-18 2010-11-06 - 2010-11-25 1 -1UNITED RENTALS INC URI (Y) 2010-11-09 - 2010-12-13 2010-11-02 - 2011-01-08 1 -1

Commodity

Copper future (USD) HG1 COMB Comdty (B) 2010-11-09 - 2011-01-07 2010-10-31 - 2011-01-15 1 1 *Corn future (CHF) C 1 COMB Comdty (B) 2010-11-18 - 2010-12-19 2010-11-08 - 2010-12-28 1 1 *Cotton future (USD) CT1 COMB Comdty (B) 2010-11-12 - 2010-11-13 2010-11-08 - 2010-11-15 1 1 *Palladium future (USD) PA1 COMB Comdty (B) 2010-11-12 - 2010-11-19 2010-11-10 - 2010-11-27 1 0 *Silver future (CHF) SI1 COMB Comdty (B) 2010-11-13 - 2010-11-18 2010-11-08 - 2010-11-29 1 0 *Sugar future (CHF) SB1 COMB Comdty (B) 2010-11-20 - 2010-12-09 2010-11-10 - 2010-12-17 1 1 *

Forex AUDUSD (B) 2010-11-12 - 2010-12-25 2010-10-30 - 2011-01-12 1 1 *

TABLE III: 25 H2 assets of the Financial Bubble Experiment as of 12 November 2010. All listed assetsare candidates for H1 (identified bubble phase) and H2 (identification of end of bubble phase). Quantilewindows of most likely dates of the end of the bubble phases are shown. Abbreviations (B), (Y), H1, H2and C are described in caption of Table II.

We support H2 by confirming that 17 of the 25 H2 assets showed substantial corrections in the quantilewindows that we forecast.

14

A. H1 & H2 Indexes

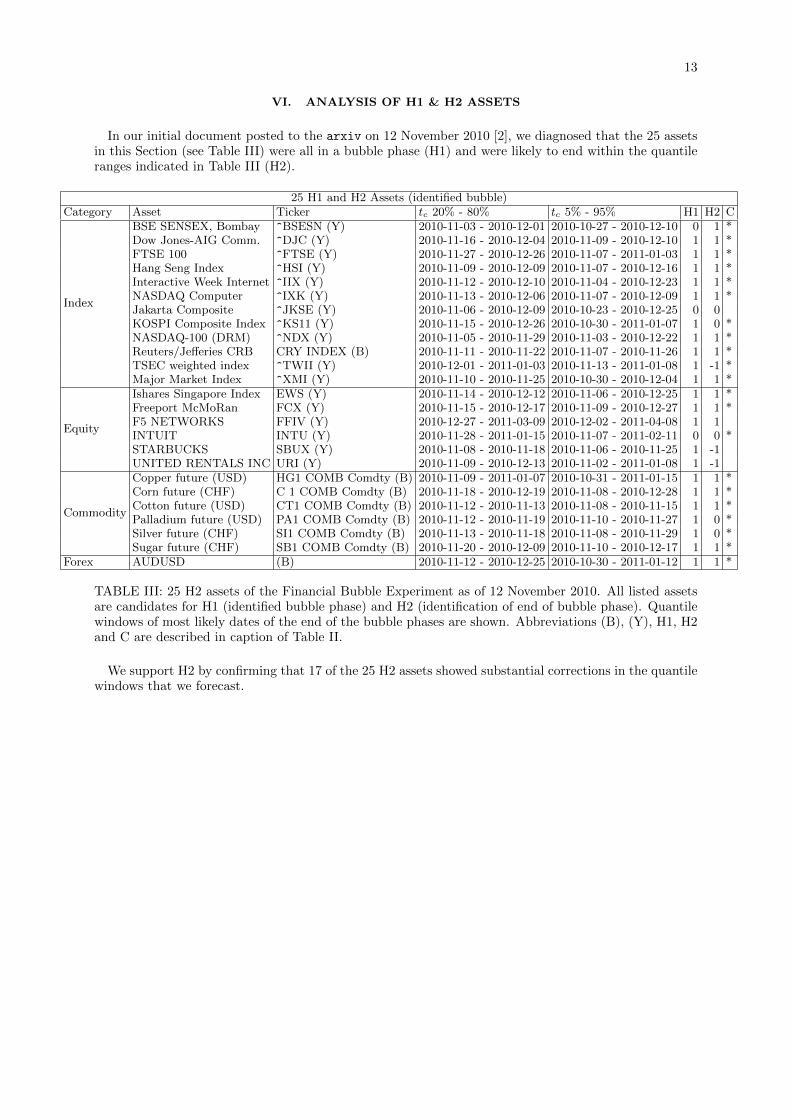

1. BSE SENSEX, Bombay

H1/H2: 0/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

17500

20000

pric

e

last obs. price: 20875.7

last

obs

.: 20

10-1

1-10

dd1 (before t2): 11% / 48 daysdd2 (in quantiles): 9.3% / 21 days

dd3 (after quantiles): 16% / 38 daysdd2 / dd1 = 0.8dd2 / dd3 = 0.6

BSESN - IN - drawdown

Observed prices

FIG. 7.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

17500

20000

pric

e

last obs. price: 20875.7

last

obs

.: 20

10-1

1-10

BSESN - IN - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 8.

15

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

17500

20000

pric

e

last obs. price: 20875.7la

st o

bs.:

2010

-11-

10

BSESN - IN - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 9.

16

2. Dow Jones-AIG Commodity Index

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

125

150

175pr

ice

last obs. price: 154.2

last

obs

.: 20

10-1

1-10

dd1 (before t2): 11% / 50 daysdd2 (in quantiles): 8.5% / 8 days

dd3 (after quantiles): 7.2% / 11 daysdd2 / dd1 = 0.7dd2 / dd3 = 1.2

DJC - US - drawdown

Observed prices

FIG. 10.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

125

150

175

pric

e

last obs. price: 154.2

last

obs

.: 20

10-1

1-10

DJC - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 11.

17

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

125

150

175

pric

e

last obs. price: 154.2

last

obs

.: 20

10-1

1-10

DJC - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 12.

18

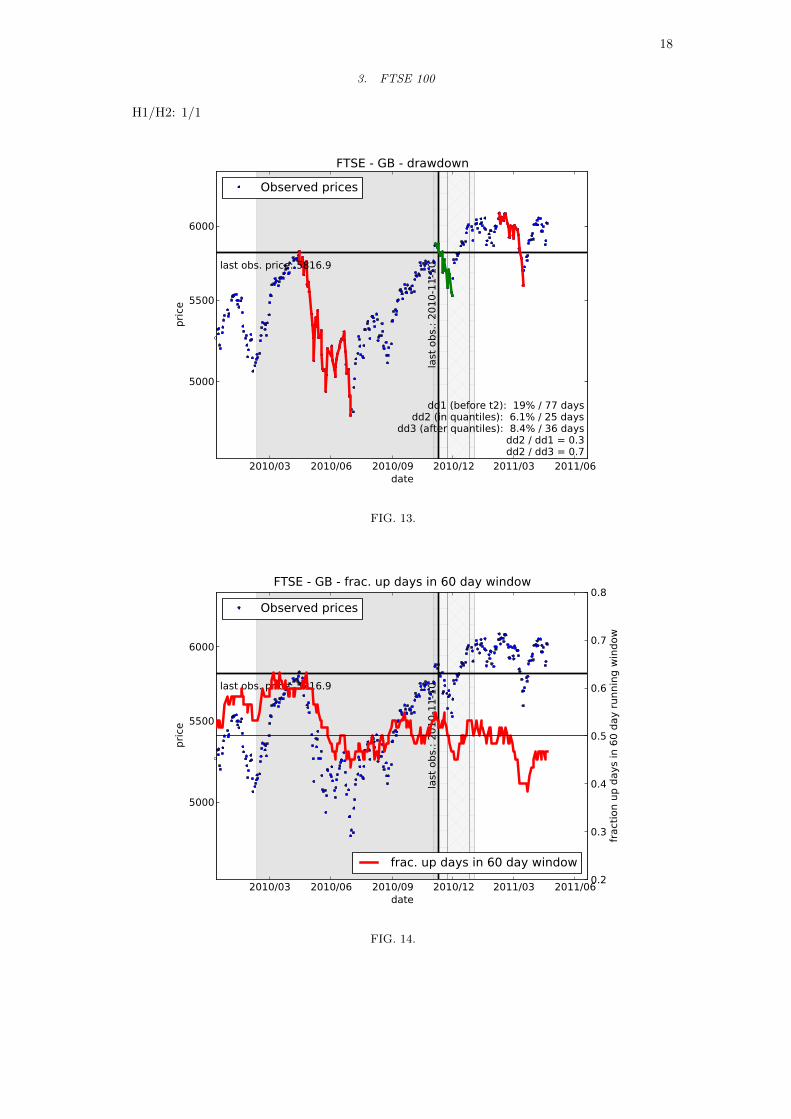

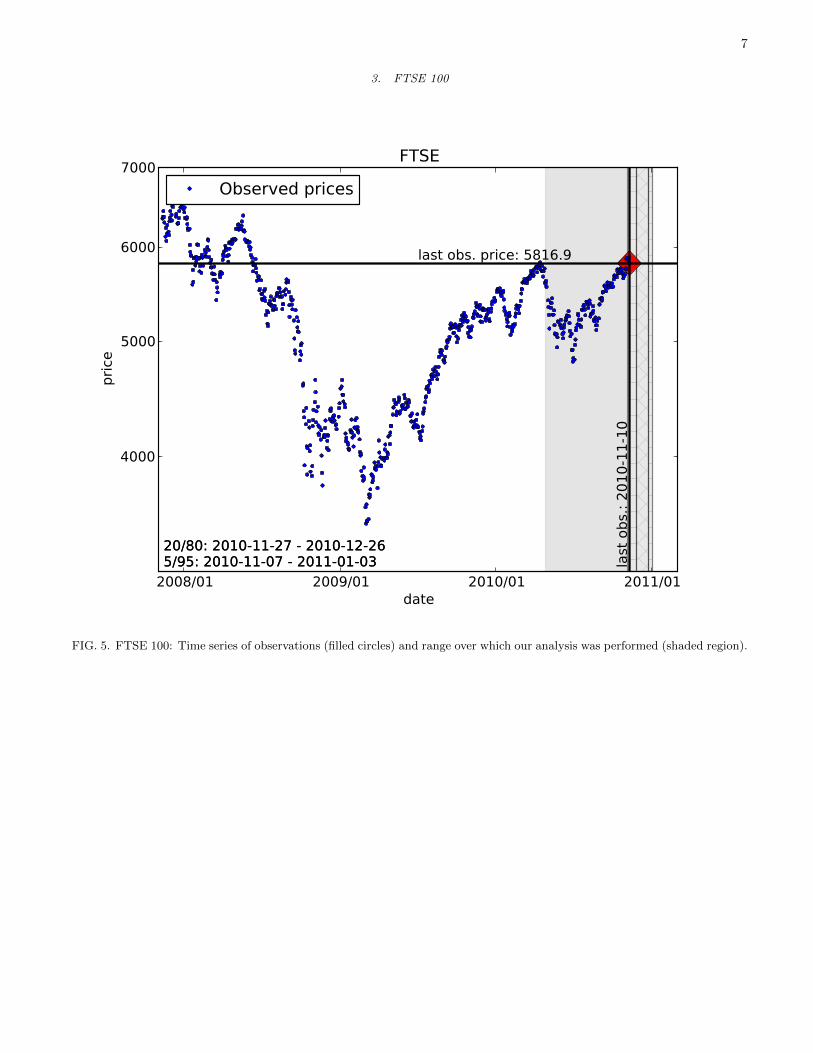

3. FTSE 100

H1/H2: 1/1

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

5000

5500

6000

pric

e

last obs. price: 5816.9

last

obs

.: 20

10-1

1-10

dd1 (before t2): 19% / 77 daysdd2 (in quantiles): 6.1% / 25 days

dd3 (after quantiles): 8.4% / 36 daysdd2 / dd1 = 0.3dd2 / dd3 = 0.7

FTSE - GB - drawdown

Observed prices

FIG. 13.

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

5000

5500

6000

pric

e

last obs. price: 5816.9

last

obs

.: 20

10-1

1-10

FTSE - GB - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 14.

19

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

5000

5500

6000

pric

e

last obs. price: 5816.9

last

obs

.: 20

10-1

1-10

FTSE - GB - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 15.

20

4. Hang Seng Index Hong Kong

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

20000

22500

25000

pric

e

last obs. price: 24500.6

last

obs

.: 20

10-1

1-10

dd1 (before t2): 15% / 46 daysdd2 (in quantiles): 9.6% / 38 days

dd3 (after quantiles): 9.1% / 57 daysdd2 / dd1 = 0.6dd2 / dd3 = 1.1

Hang Seng - CN - drawdown

Observed prices

FIG. 16.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

20000

22500

25000

pric

e

last obs. price: 24500.6

last

obs

.: 20

10-1

1-10

Hang Seng - CN - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 17.

21

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

20000

22500

25000

pric

e

last obs. price: 24500.6

last

obs

.: 20

10-1

1-10

Hang Seng - CN - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 18.

22

5. Interactive Week Internet Index

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02date

240

280

320

pric

e

last obs. price: 312.7

last

obs

.: 20

10-1

1-10

dd1 (before t2): 17% / 78 daysdd2 (in quantiles): 6.4% / 6 days

dd3 (after quantiles): 4.3% / 3 daysdd2 / dd1 = 0.4dd2 / dd3 = 1.5

IIX - US - drawdown

Observed prices

FIG. 19.

2010/02 2010/05 2010/08 2010/11 2011/02date

240

280

320

pric

e

last obs. price: 312.7

last

obs

.: 20

10-1

1-10

IIX - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 20.

23

2010/02 2010/05 2010/08 2010/11 2011/02date

240

280

320

pric

e

last obs. price: 312.7la

st o

bs.:

2010

-11-

10

IIX - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 21.

24

6. NASDAQ Computer

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1200

1400

pric

e

last obs. price: 1336.0

last

obs

.: 20

10-1

1-10

dd1 (before t2): 19% / 70 daysdd2 (in quantiles): 4.8% / 8 days

dd3 (after quantiles): 9.7% / 27 daysdd2 / dd1 = 0.2dd2 / dd3 = 0.5

IXK - US - drawdown

Observed prices

FIG. 22.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1200

1400

pric

e

last obs. price: 1336.0

last

obs

.: 20

10-1

1-10

IXK - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 23.

25

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1200

1400

pric

e

last obs. price: 1336.0

last

obs

.: 20

10-1

1-10

IXK - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 24.

26

7. Jakarta Composite

H1/H2: 0/0

2009/06 2009/12 2010/06 2010/12 2011/06date

1600

2400

3200

pric

elast obs. price: 3757.0

last

obs

.: 20

10-1

1-10

dd1 (before t2): 16% / 25 daysdd2 (in quantiles): 6.2% / 20 days

dd3 (after quantiles): 12% / 19 daysdd2 / dd1 = 0.4dd2 / dd3 = 0.5

JKSE - ID - drawdown

Observed prices

FIG. 25.

2009/06 2009/12 2010/06 2010/12 2011/06date

1600

2400

3200

pric

e

last obs. price: 3757.0

last

obs

.: 20

10-1

1-10

JKSE - ID - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 26.

27

2009/06 2009/12 2010/06 2010/12 2011/06date

1600

2400

3200

pric

e

last obs. price: 3757.0

last

obs

.: 20

10-1

1-10

JKSE - ID - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 27.

28

8. KOSPI Composite Index, Seoul

H1/H2: 1/0

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1500

1800

2100

pric

e

last obs. price: 1967.8

last

obs

.: 20

10-1

1-10

dd1 (before t2): 11% / 29 daysdd2 (in quantiles): 3.7% / 19 days

dd3 (after quantiles): 9.5% / 55 daysdd2 / dd1 = 0.3dd2 / dd3 = 0.4

KS11 - KR - drawdown

Observed prices

FIG. 28.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1500

1800

2100

pric

e

last obs. price: 1967.8

last

obs

.: 20

10-1

1-10

KS11 - KR - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 29.

29

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1500

1800

2100

pric

e

last obs. price: 1967.8

last

obs

.: 20

10-1

1-10

KS11 - KR - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 30.

30

9. NASDAQ-100 (DRM)

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1800

2100

2400

pric

e

last obs. price: 2187.7

last

obs

.: 20

10-1

1-10

dd1 (before t2): 17% / 70 daysdd2 (in quantiles): 4.5% / 8 days

dd3 (after quantiles): 8.5% / 28 daysdd2 / dd1 = 0.3dd2 / dd3 = 0.5

NDX - US - drawdown

Observed prices

FIG. 31.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1800

2100

2400

pric

e

last obs. price: 2187.7

last

obs

.: 20

10-1

1-10

NDX - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 32.

31

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1800

2100

2400

pric

e

last obs. price: 2187.7

last

obs

.: 20

10-1

1-10

NDX - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 33.

32

10. Reuters/Jefferies CRB index

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

250

300

350

pric

e last obs. price: 317.1

last

obs

.: 20

10-1

1-10

dd1 (before t2): 11% / 41 daysdd2 (in quantiles): 7.7% / 8 days

dd3 (after quantiles): 7.1% / 8 daysdd2 / dd1 = 0.7dd2 / dd3 = 1.1

RJ CRB - US - drawdown

Observed prices

FIG. 34.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

250

300

350

pric

e last obs. price: 317.1

last

obs

.: 20

10-1

1-10

RJ CRB - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 35.

33

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

250

300

350

pric

e last obs. price: 317.1

last

obs

.: 20

10-1

1-10

RJ CRB - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 36.

34

11. TSEC weighted index

H1/H2: 1/-1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

7000

8000

9000

pric

e

last obs. price: 8450.6

last

obs

.: 20

10-1

1-10

dd1 (before t2): 14% / 55 daysdd2 (in quantiles): 2.7% / 4 days

dd3 (after quantiles): 10% / 46 daysdd2 / dd1 = 0.2dd2 / dd3 = 0.3

TWII - TW - drawdown

Observed prices

FIG. 37.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

7000

8000

9000

pric

e

last obs. price: 8450.6

last

obs

.: 20

10-1

1-10

TWII - TW - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 38.

35

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

7000

8000

9000

pric

e

last obs. price: 8450.6

last

obs

.: 20

10-1

1-10

TWII - TW - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 39.

36

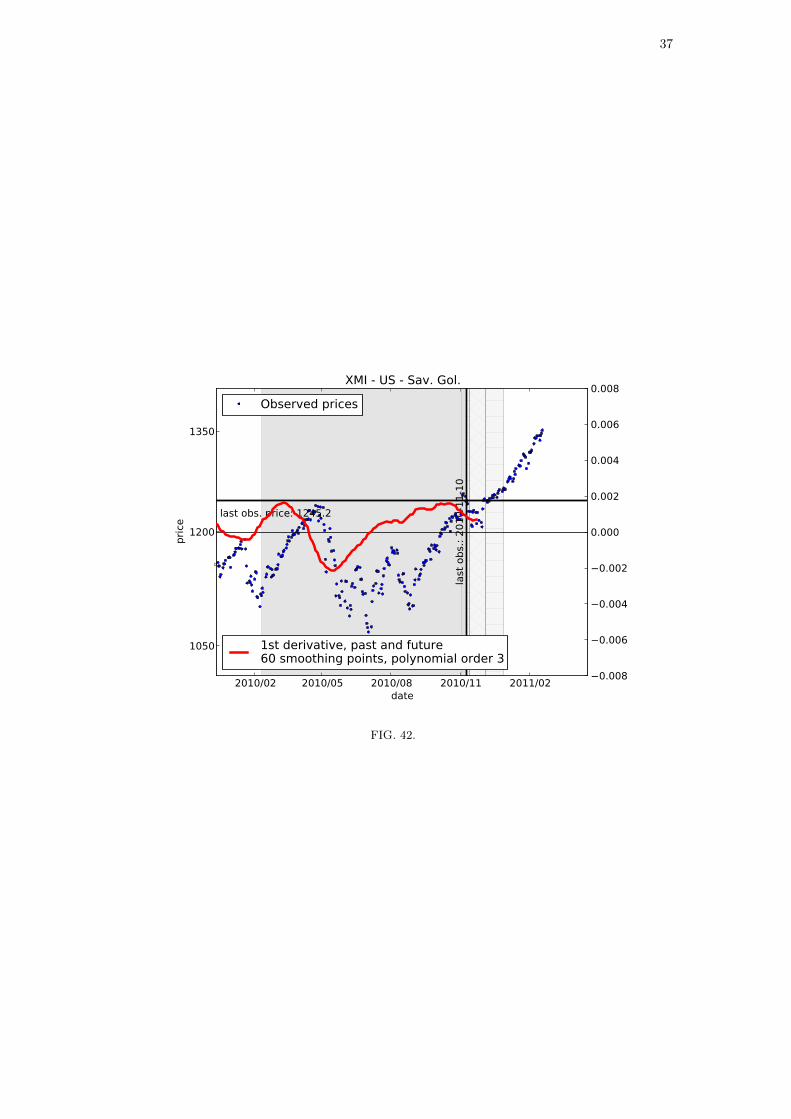

12. Major Market Index

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02date

1050

1200

1350

pric

e

last obs. price: 1245.2

last

obs

.: 20

10-1

1-10

dd1 (before t2): 14% / 70 daysdd2 (in quantiles): 3.9% / 25 days

dd3 (after quantiles): 1.7% / 4 daysdd2 / dd1 = 0.3dd2 / dd3 = 2.3

XMI - US - drawdown

Observed prices

FIG. 40.

2010/02 2010/05 2010/08 2010/11 2011/02date

1050

1200

1350

pric

e

last obs. price: 1245.2

last

obs

.: 20

10-1

1-10

XMI - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 41.

37

2010/02 2010/05 2010/08 2010/11 2011/02date

1050

1200

1350

pric

e

last obs. price: 1245.2

last

obs

.: 20

10-1

1-10

XMI - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 42.

38

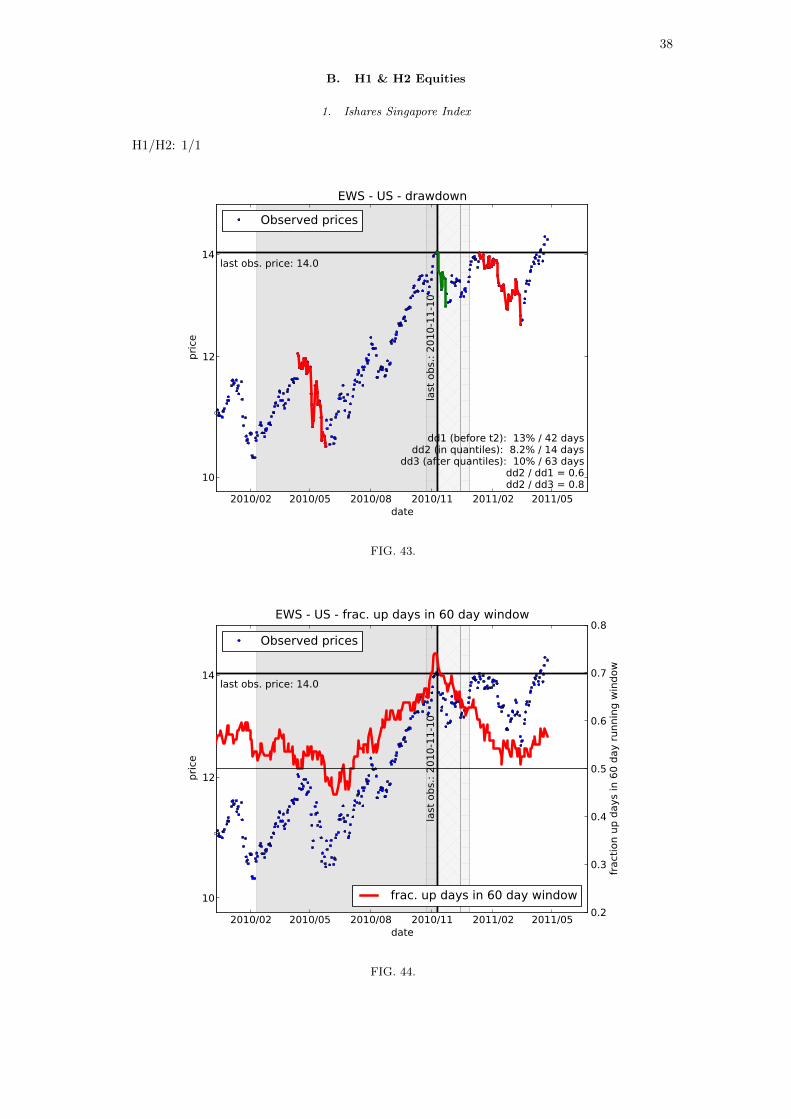

B. H1 & H2 Equities

1. Ishares Singapore Index

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

10

12

14

pric

e

last obs. price: 14.0

last

obs

.: 20

10-1

1-10

dd1 (before t2): 13% / 42 daysdd2 (in quantiles): 8.2% / 14 days

dd3 (after quantiles): 10% / 63 daysdd2 / dd1 = 0.6dd2 / dd3 = 0.8

EWS - US - drawdown

Observed prices

FIG. 43.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

10

12

14

pric

e

last obs. price: 14.0

last

obs

.: 20

10-1

1-10

EWS - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 44.

39

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

10

12

14

pric

e

last obs. price: 14.0la

st o

bs.:

2010

-11-

10

EWS - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 45.

40

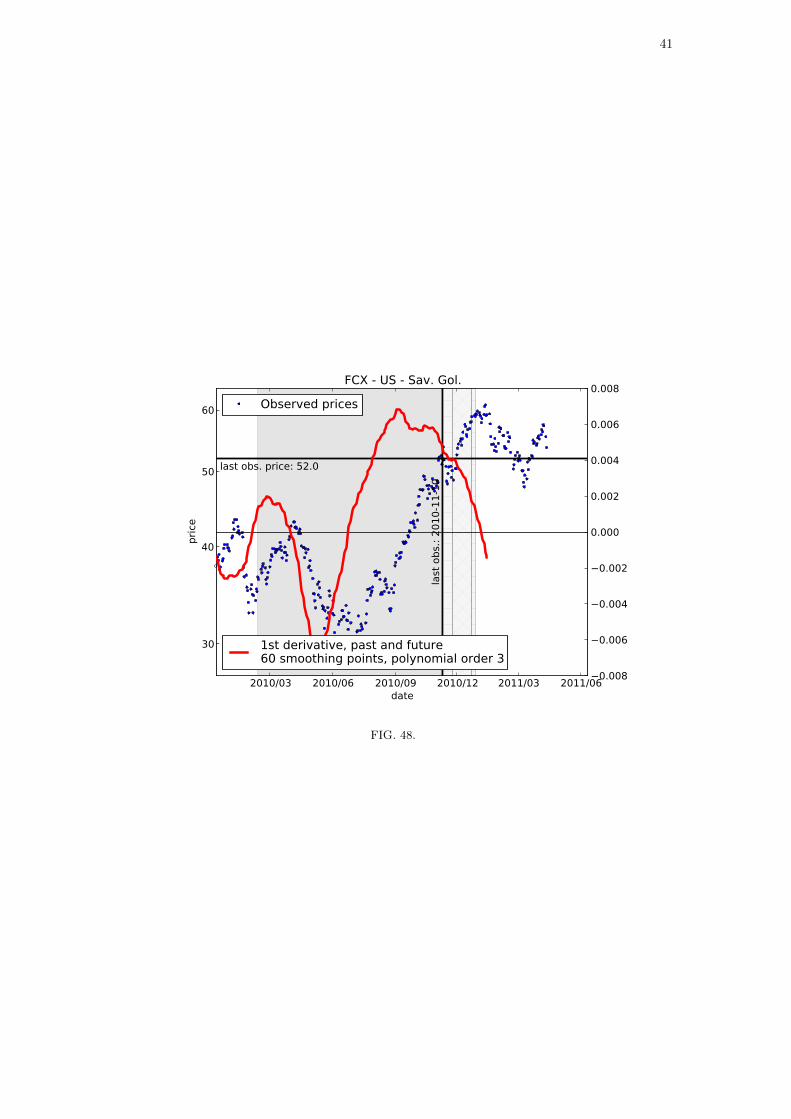

2. Freeport McMoRan Copper & Gold

H1/H2: 1/1

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

30

40

50

60pr

ice

last obs. price: 52.0

last

obs

.: 20

10-1

1-10

dd1 (before t2): 40% / 86 daysdd2 (in quantiles): 10% / 6 days

dd3 (after quantiles): 24% / 57 daysdd2 / dd1 = 0.3dd2 / dd3 = 0.4

FCX - US - drawdown

Observed prices

FIG. 46.

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

30

40

50

60

pric

e

last obs. price: 52.0

last

obs

.: 20

10-1

1-10

FCX - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 47.

41

2010/03 2010/06 2010/09 2010/12 2011/03 2011/06date

30

40

50

60

pric

e

last obs. price: 52.0

last

obs

.: 20

10-1

1-10

FCX - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 48.

42

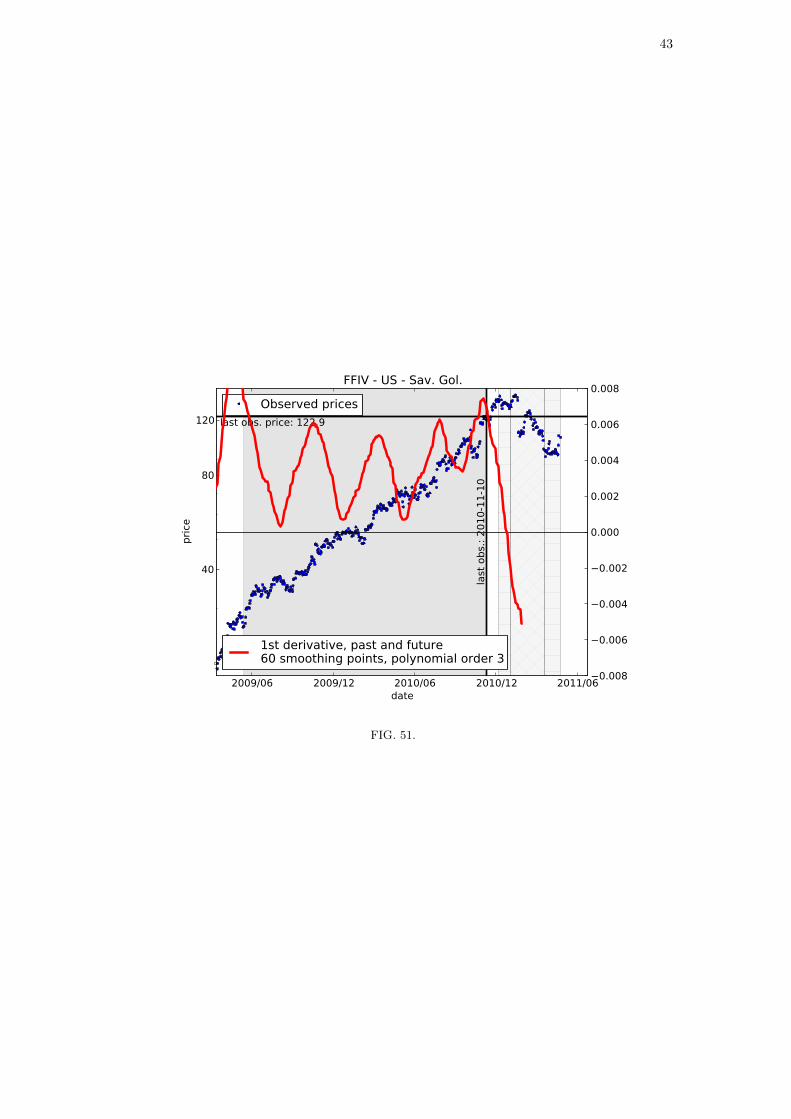

3. F5 NETWORKS

H1/H2: 1/1

2009/06 2009/12 2010/06 2010/12 2011/06date

40

80

120pr

ice

last obs. price: 122.9

last

obs

.: 20

10-1

1-10

dd1 (before t2): 20% / 14 daysdd2 (in quantiles): 45% / 67 days

dd3 (after quantiles): 0.0% / 0 daysdd2 / dd1 = 2.2dd2 / dd3 = 0.0

FFIV - US - drawdown

Observed prices

FIG. 49.

2009/06 2009/12 2010/06 2010/12 2011/06date

40

80

120

pric

e

last obs. price: 122.9

last

obs

.: 20

10-1

1-10

FFIV - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 50.

43

2009/06 2009/12 2010/06 2010/12 2011/06date

40

80

120

pric

e

last obs. price: 122.9

last

obs

.: 20

10-1

1-10

FFIV - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 51.

44

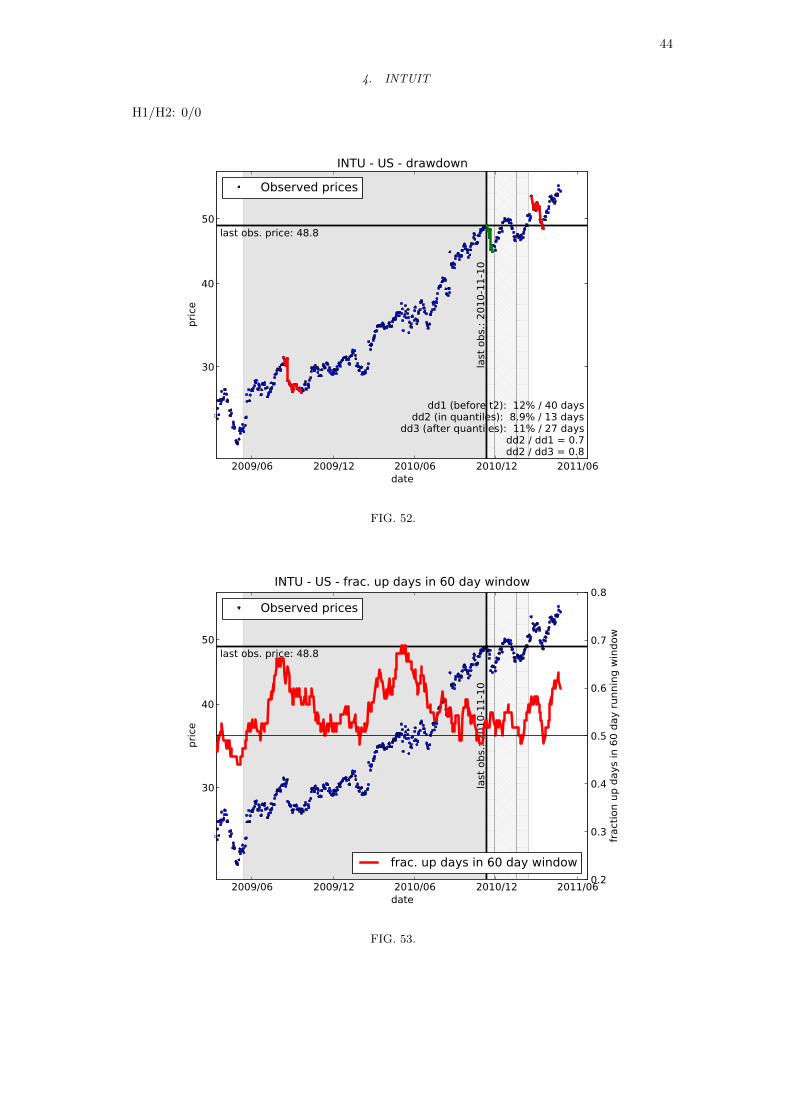

4. INTUIT

H1/H2: 0/0

2009/06 2009/12 2010/06 2010/12 2011/06date

30

40

50

pric

e

last obs. price: 48.8

last

obs

.: 20

10-1

1-10

dd1 (before t2): 12% / 40 daysdd2 (in quantiles): 8.9% / 13 days

dd3 (after quantiles): 11% / 27 daysdd2 / dd1 = 0.7dd2 / dd3 = 0.8

INTU - US - drawdown

Observed prices

FIG. 52.

2009/06 2009/12 2010/06 2010/12 2011/06date

30

40

50

pric

e

last obs. price: 48.8

last

obs

.: 20

10-1

1-10

INTU - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 53.

45

2009/06 2009/12 2010/06 2010/12 2011/06date

30

40

50

pric

e

last obs. price: 48.8

last

obs

.: 20

10-1

1-10

INTU - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 54.

46

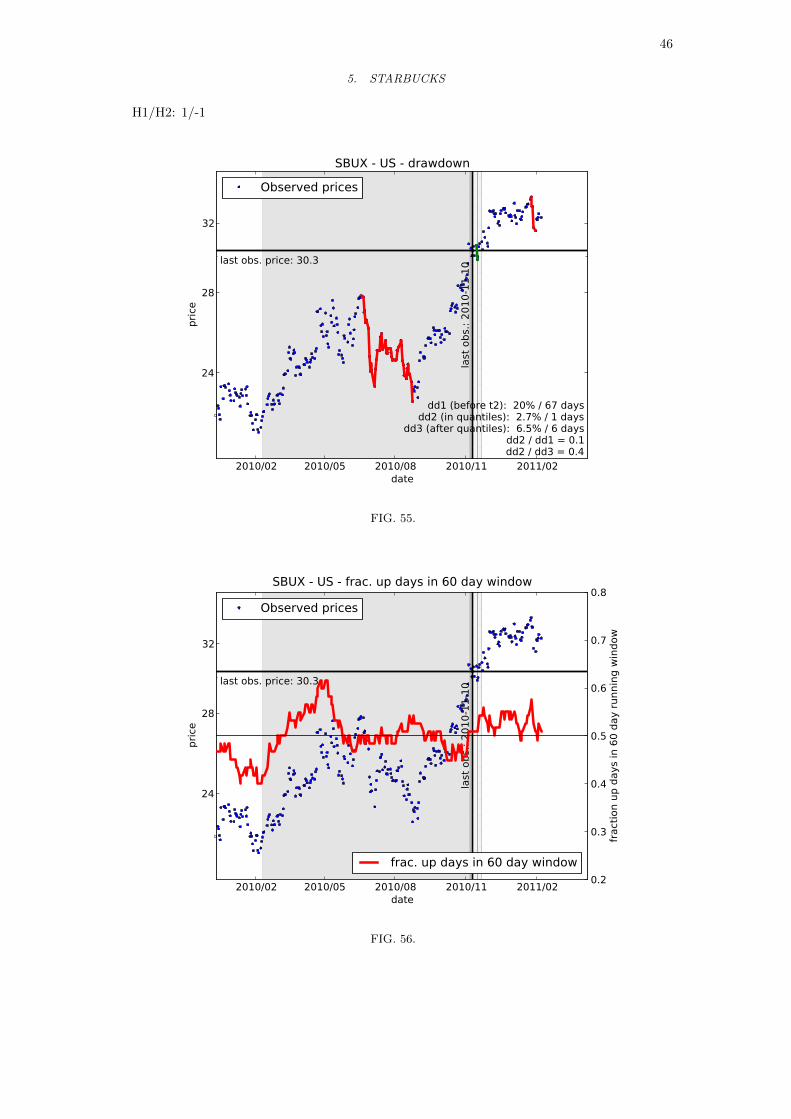

5. STARBUCKS

H1/H2: 1/-1

2010/02 2010/05 2010/08 2010/11 2011/02date

24

28

32

pric

e

last obs. price: 30.3

last

obs

.: 20

10-1

1-10

dd1 (before t2): 20% / 67 daysdd2 (in quantiles): 2.7% / 1 days

dd3 (after quantiles): 6.5% / 6 daysdd2 / dd1 = 0.1dd2 / dd3 = 0.4

SBUX - US - drawdown

Observed prices

FIG. 55.

2010/02 2010/05 2010/08 2010/11 2011/02date

24

28

32

pric

e

last obs. price: 30.3

last

obs

.: 20

10-1

1-10

SBUX - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 56.

47

2010/02 2010/05 2010/08 2010/11 2011/02date

24

28

32

pric

e

last obs. price: 30.3la

st o

bs.:

2010

-11-

10

SBUX - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 57.

48

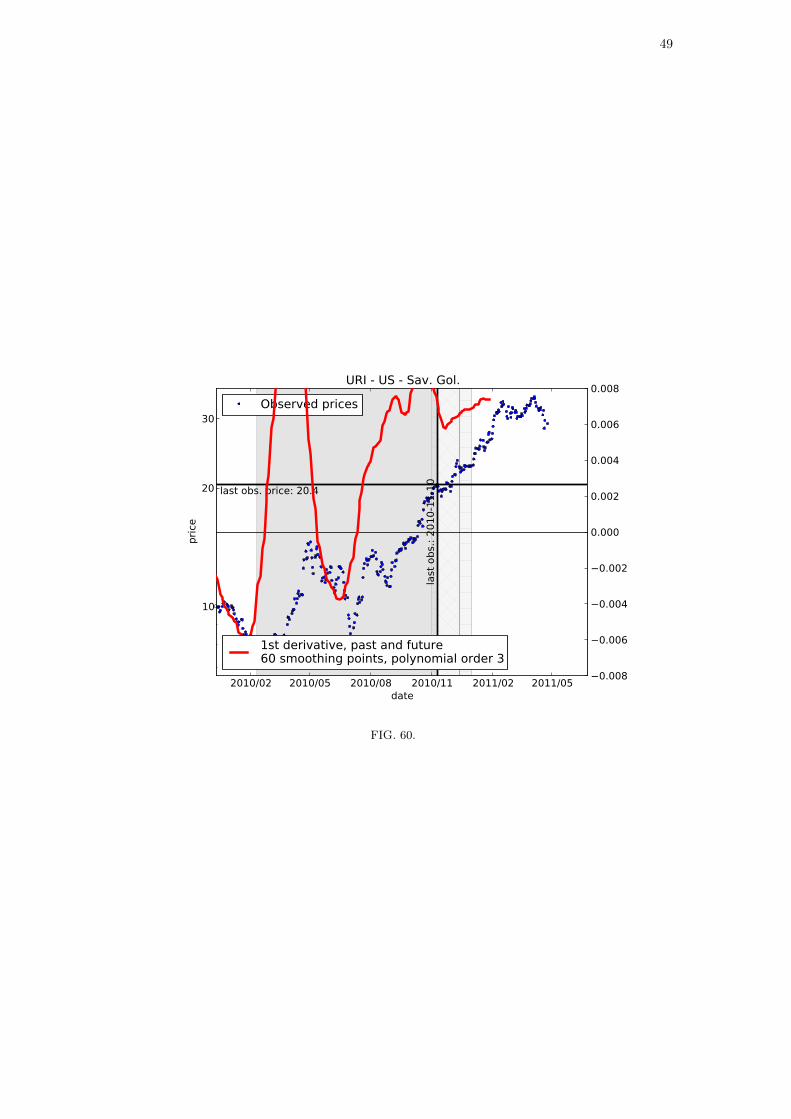

6. UNITED RENTALS INC

H1/H2: 1/-1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

10

20

30pr

ice

last obs. price: 20.4

last

obs

.: 20

10-1

1-10

dd1 (before t2): 56% / 64 daysdd2 (in quantiles): 6.9% / 5 days

dd3 (after quantiles): 18% / 15 daysdd2 / dd1 = 0.1dd2 / dd3 = 0.4

URI - US - drawdown

Observed prices

FIG. 58.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

10

20

30

pric

e

last obs. price: 20.4

last

obs

.: 20

10-1

1-10

URI - US - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 59.

49

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

10

20

30

pric

e

last obs. price: 20.4

last

obs

.: 20

10-1

1-10

URI - US - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 60.

50

C. H1 & H2 Commodities

1. Copper future (USD)

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

3.2

4.0

4.8

pric

e

last obs. price: 4.0

last

obs

.: 20

10-1

1-10

dd1 (before t2): 27% / 63 daysdd2 (in quantiles): 8.8% / 14 days

dd3 (after quantiles): 11% / 29 daysdd2 / dd1 = 0.3dd2 / dd3 = 0.8

Copper future - USD - drawdown

Observed prices

FIG. 61.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

3.2

4.0

4.8

pric

e

last obs. price: 4.0

last

obs

.: 20

10-1

1-10

Copper future - USD - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 62.

51

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

3.2

4.0

4.8

pric

e

last obs. price: 4.0

last

obs

.: 20

10-1

1-10

Copper future - USD - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 63.

52

2. Corn future (CHF)

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

4.5

6.0

pric

e

last obs. price: 5.5

last

obs

.: 20

10-1

1-10

dd1 (before t2): 20% / 33 daysdd2 (in quantiles): 10.0% / 14 days

dd3 (after quantiles): 20% / 33 daysdd2 / dd1 = 0.5dd2 / dd3 = 0.5

Corn future - CHF - drawdown

Observed prices

FIG. 64.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

4.5

6.0

pric

e

last obs. price: 5.5

last

obs

.: 20

10-1

1-10

Corn future - CHF - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 65.

53

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

4.5

6.0

pric

e

last obs. price: 5.5

last

obs

.: 20

10-1

1-10

Corn future - CHF - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 66.

54

3. Cotton future (USD)

H1/H2: 1/1

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1.0

1.5

2.0pr

ice

last obs. price: 1.5

last

obs

.: 20

10-1

1-10

dd1 (before t2): 9.3% / 17 daysdd2 (in quantiles): 8.6% / 6 days

dd3 (after quantiles): 20% / 8 daysdd2 / dd1 = 0.9dd2 / dd3 = 0.4

Cotton future - USD - drawdown

Observed prices

FIG. 67.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1.0

1.5

2.0

pric

e

last obs. price: 1.5

last

obs

.: 20

10-1

1-10

Cotton future - USD - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 68.

55

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

1.0

1.5

2.0

pric

e

last obs. price: 1.5

last

obs

.: 20

10-1

1-10

Cotton future - USD - Sav. Gol.

Observed prices

0.008

0.006

0.004

0.002

0.000

0.002

0.004

0.006

0.008

1st derivative, past and future60 smoothing points, polynomial order 3

FIG. 69.

56

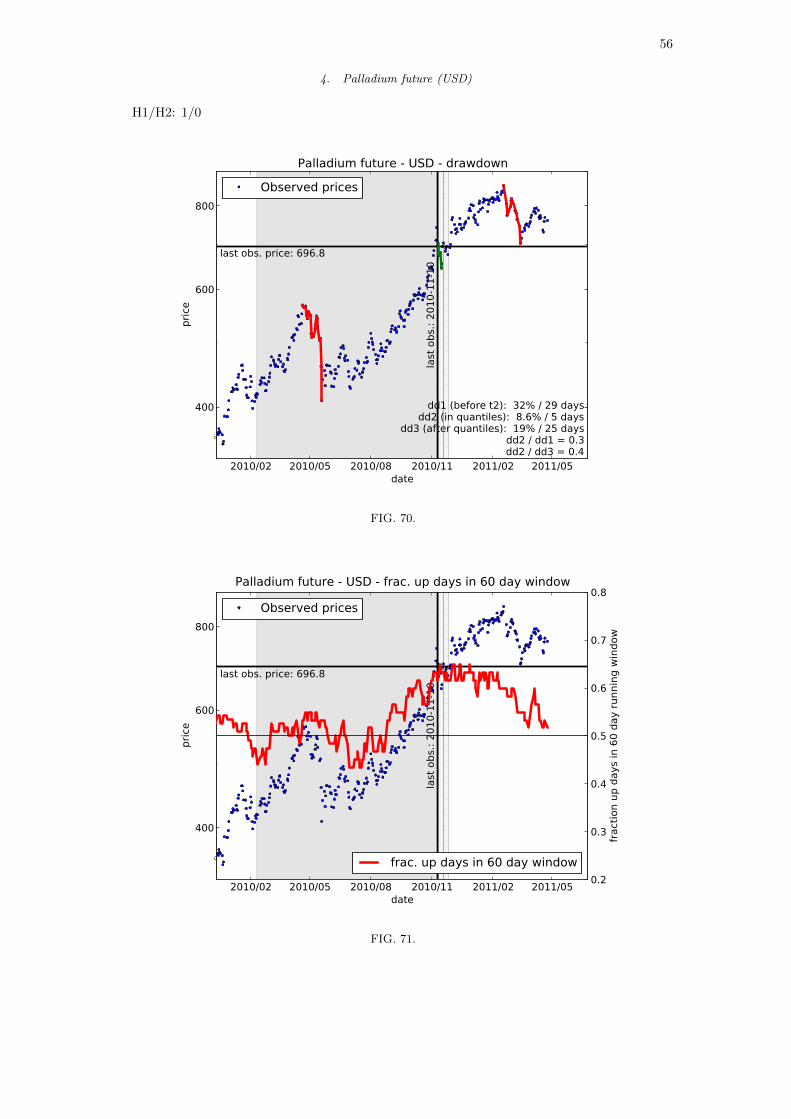

4. Palladium future (USD)

H1/H2: 1/0

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

400

600

800

pric

e

last obs. price: 696.8

last

obs

.: 20

10-1

1-10

dd1 (before t2): 32% / 29 daysdd2 (in quantiles): 8.6% / 5 days

dd3 (after quantiles): 19% / 25 daysdd2 / dd1 = 0.3dd2 / dd3 = 0.4

Palladium future - USD - drawdown

Observed prices

FIG. 70.

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

400

600

800

pric

e

last obs. price: 696.8

last

obs

.: 20

10-1

1-10

Palladium future - USD - frac. up days in 60 day window

Observed prices

0.2

0.3

0.4

0.5

0.6

0.7

0.8fra

ctio

n up

day

s in

60

day

runn

ing

win

dow

frac. up days in 60 day window

FIG. 71.

57

2010/02 2010/05 2010/08 2010/11 2011/02 2011/05date

400

600

800

pric

e

last obs. price: 696.8