Embed Size (px)

Citation preview

599

The Financial Asset and Liability in Japanese Household Statistics*

Saeko MaedaThe Economic and Social Research Institute, the Cabinet Office.

AbstractThis paper examines the possible differences exist among each survey data of household

assets and liabilities in Japan, comparing the most representative statistics. There are differ-ences between individual statistical surveys in the distributions of financial assets and liabil-ities and on an average basis.

The differences could be made by differences in the characteristics of sample house-holds and in the questionnaire format. The fact that the averages of total financial assets in a survey are small relative to those in other statistics may be not only because of the attributes of samples such as the age of the household head but also because of the questionnaire de-signed so as to ask about the total amount of financial assets without a breakdown by asset type, a fact which may have led to understatement of the asset amounts. Meanwhile, what is notable about one survey is that the proportion of households which replied that they did not own financial assets has been markedly large in recent years compared with other surveys.

Moreover, comparison of statistical surveys with figures obtained from macroeconomic statistics shows that the survey figures are smaller than the estimates based on macroeco-nomic statistics. Of this gap, only 25% in the case of assets and only 40% in the case of debts was explicitly explainable due to the concept and definition of the statistics.

When analyzing assets and debts using statistical survey data, it is necessary to pay at-tention to the characteristics of individual surveys and the differences in the coverage of each statistics including the difference in definition from macro statistics.

Keywords: household, financial asset, liability JEL Classification: D14, D31, E21

I. Financial Asset and Liability of Japanese Household

It is possible that assets and liabilities in a family account affect household consumption behavior as well as the flow income such as wages. Financial assets create property income receivables like the interest and dividends, and liabilities make property income payables. These property incomes increase and decrease current disposable income directly. Beyond * In this paper, public values are basically used for the comparison, while based on the common definition, the answer data are also estimated. NSFIES and FIES from Ministry of Internal affairs, CSLC from Ministry of Health and Living Welfare were provided under the article 33 of Statistic Law. And then, CCFSI have allowed me to use the data of their public opinion surveys. I greatly appreciate the cooperation of the ministries and the committee. Furthermore Dr. Takashi Unayama (Senior Research Fellow of PFI) and Mr. Shunji Tada (Researcher of PFI) supported me in making this paper. Dr. Hamada and Dr. Hori (ESRI) provide the invaluable comments. This paper presents the personal opinion of author only, but does display the statements of the institute to which she belongs.

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 599 2015/09/03 13:19:01

these direct effects on the income flow, assets and debts can be a kind of safety net or risk for the households and have an implicit effect on consumption and saving behavior. Given the declining the working population ratio amidst the aging society, these asset effects be-come bigger factors on the economic activities than before. However, it is quite difficult to grasp the assets and liabilities of each household and no survey conducted by the govern-ment agencies can give an accurate picture of these situation in Japan.

This paper examines the differences in the scopes, outcomes and definitions among vari-ous statistics focusing on household asset and debts, mutually comparing these data.

The following section introduces the contents of survey statistics that investigate the household assets and liabilities in Japan. Section III checks trends of average values and dis-tributions of these surveys. I focus on question forms and styles as triggers for the differenc-es among surveys in section IV. The last part adds comparison survey data to macro statis-tics data in concepts and scope.

II. Surveys on Financial assets and liabilities

In this paper, four survey statistics are compared: the National Survey of Family Income and Expenditure (NSFIE, conducted by the Statistics Bureau, Ministry of Internal Affairs and Communications), the Family income and Expenditure Survey (FIES, conducted by the Statistics Bureau, Ministry of Internal Affairs and Communications), the Comprehensive Survey of Living Conditions (CSLC, conducted by Ministry of Health and Life Welfare) and the “Public opinion survey on household financial behavior” (conducted by The Central Council for Financial Services Information). Table 1 shows the characteristics of these sur-vey statistics in contents, form, timing and so on.

II-1. National Survey of Family Income and Expenditure (NSFIE)

The survey has conducted every 5 years by the Statistics Bureau of the Ministry of Inter-nal Affairs and Communications since 1959, aiming at providing comprehensive data on in-come and expenditure of households. The survey runs for 3 months from September to No-vember in the survey year1. NSFIE inquires about the financial assets2 and liabilities at the end of November.

The questionnaires ask items concerning financial assets and liabilities. There are many items in financial assets; balances of deposits (postal deposits, bank deposits, etc.), premi-ums paid for life and damage insurance, current values of stocks, trusts, and shares, and the others (including deposits at a company). In liabilities there are three items: “liability for purchase of houses and/or land”, “liability other than purchase of houses and/or land” and “monthly or yearly installments”.

1 Single family participates for two months only (from October to November).2 Financial assets are named “savings” in the questionnaire.

600 S Maeda / Public Policy Review

CW6_A6335D06.indd 600 2015/09/03 13:19:01

601

NSFIE reports financial assets as net financial assets which are derived by subtracting the amount of liabilities from that of financial assets. The survey also evaluates the real asset values from the houses and/or land, and durable goods in both gross and net values, consid-ering depreciation. Moreover the surveys reports net assets by subtracting the amount of lia-bilities from gross assets (sum of real assets and gross financial assets)3. This paper defines

注1. Approximately 40 thousand households 2. Enumerators method had employed by 2003 3. See Table A4

Table 1The comparison of the surveys for household assets and liabilities

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 601 2015/09/03 13:19:02

the gross financial assets as “financial assets” for comparison with other surveys.NSFIE includes “those kept by household head and household members” and “those

used for individual business purpose” in assets and liabilities, but excludes “those kept by persons sharing living expenses and live-in employees”, “cash stored at home” and “money lent to acquaintances”, etc.

Most of the asset items in NSFIE are consistent with those in the macro statistics ac-count. However there are some differences between NSFIE and the macro statistics in their definitions and categories. (Table A1)

II-2. Family Income and Expenditure Survey: Pieces of Savings and liabilities (FIES) and Family Saving Survey (FSS)

Family Income and Expenditure Survey (hereafter FIES) has been conducted since 1953, aiming at providing comprehensive data on income and expenditure of households. Until the January 2001 survey, the Family Saving Survey (hereafter FSS) had been imple-mented as supplement of the FIES. FIES added the piece of “savings and liabilities”, and then FSS was incorporated into the FIES in 2002

Formerly FSS was implemented on every January and asked the assets and liabilities at the end of the previous year (the end of December). Around half of the FSS sample was drawn from the two-or-more-person households sample of FIES in January of the survey year (approximately 3,000 households) and half was drawn from the previous year’s FSS sample (approximately 3,000 households). FSS had around 6,000 respondents. After inte-gration of FSS to the FIES, all two-or-more-person households of FIES were requested to fill in the schedule of “savings and liabilities” on the 1st day of 3rd month of a survey4.

FIES investigate the amount of financial assets (”amount of savings” in questionnaire) , amount of liabilities and these items under the same definition of NSFIE. FSS surveyed more detailed categories of financial assets than FIES (see TableA2).

II-3. Comprehensive Survey of Living Conditions (CSLC)

Comprehensive Survey of Living Conditions (hereafter CSLC), conducted by the Minis-try of Health, Labour and Welfare, aims to investigate matters of health, medical care, wel-fare, pensions and income, etc. The survey has questions about financial assets and liabilities every 3 years5 in July. The participants are requested to answer the total of financial assets 3 The survey has focused on the savings and liabilities since 1969. Expanding the item of the questionnaire to the information of dwellings and/or land of the residence (total floor and land area space, time of construction, etc.) in 1974, we can estimate the real assets since then. And also the statistics bureau has estimated the real asset values including dwelling and land other than present place of residence since 1989.4 Last FSS looked into the value of 2000’s end, FIES (January 2002) investigated the amount of assets and liabilities as of 1st January 2002. There seemed to be the blank between 2000 and 2002 on the chart1 and 2. Here as I considered the FSS value at the end of year to be equal to that at the beginning of next year, there is no blank between FSS and FIES. In “Regarding the comparison of time-series data FIES and FSS”(http://www.stat.go.jp/data/sav/4.htm in Japanese), annual values in FIES annual report are the average of 12 months of savings and liabilities, we cannot simply compare the FSS value at the end of the year. In this paper, the values of each January are calculated by individual micro-data of FIES.

602 S Maeda / Public Policy Review

CW6_A6335D06.indd 602 2015/09/03 13:19:02

603

and liabilities at the end of the June6.Until 1998, the survey had asked only class values of the “amount of savings” and

“amount of liabilities”. The amount of savings corresponds the sum of items; banking ac-counts, accumulative insurance fees such as life insurance, stocks and shares, securities, other deposits (property accumulation savings and deposits at companies, etc.),”the amount of liabilities” in this survey corresponds to liabilities. In the survey in 2001 the survey changes the question to ask about the values of “amount of savings” and “amount of liabili-ties”. (TableA3)

II-4. The Surveys by the Central Council for Financial Services Information (CCFSI)

The Central Council for Financial Services Information has conducted the public opin-ion survey every year since 1953. The survey investigates such household financial behavior as savings and loan planning and so on to provide the information for the public relations of financial activities. The council has modified the methods, questions and name of survey7 as it has been carried out. (See in detail Table A4).The survey in 2013 targeted 8,000 two-or-more person households (approximately 4,000 responded) and 2,500 one-person house-holds.

The survey checks the possessions of any financial assets and the values of each items of financial assets. The categories are similar to the ones in NSFIE and FIES; the insurance itemized in life insurance, damage insurance and private pension insurance, the financial trusts, stock and shares investment trust, property accumulation savings, etc. On the other hand, some differences can be pointed out. The survey includes neither the funds for busi-ness nor the banking account for the salary payment or credit expenditure in the financial assets, while NSFIE and FIES does. There are also some different classifications in “stock and shares” and “trust”. The survey distinguishes currency holdings from items of financial asset.

Regarding liabilities, every year the survey has questions of the “amount of liabilities”. Some years checked housing loans, education loans, and general purpose loans also.

5 CSLS has two types of surveys; small and large-scale surveys. The large-scale one is implemented every 3 years. The ques-tions related to the assets and liabilities are contained in the complicated survey. The small one is run every interim year.6 The income questionnaire is also implemented in July. Until 1986 the survey has been implemented in October to investigate the conditions at the end of September.7 CCFSI changed their survey’s name four times before. The survey was started as ”Public opinion survey on Savings” in 1973, and changed the name to “Public opinion survey on savings and consumption” in 1992, “Public opinion survey on household financial assets and liabilities” in 2001,” and “Public opinion survey on household financial behavior” in 2007. The survey series have gone through a change of not only the names but also the question items, definitions and samples. The sur-vey came to cover the one-person households in 2003. The series of these surveys is called “CCFSI” in this paper.

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 603 2015/09/03 13:19:02

III Values of Financial Assets and Liabilities

III-1. Average value

Chart1 shows the average values of financial asset amount per a family in the above four surveys since 1984, employing the data of two-or-more family size.

I can explain the similar trends in any survey other than CSLC. After a fairly sizable in-crease in 1980, it shows a gentle slope by the first half of the 2000s and then remains stable. Only CSLC leveled off between 1992 and 1997 when other surveys’ data had presented up-per trends.

The average values of assets in 1989 and 2004, when all 4 surveys are carried out, are compared in Table 2. The values of FIES are at the highest levels in both years, about 300 thousand yen in 1989 and 1.4 million yen in 2004 higher than NFIES’s. CSLC’s values are quite low. It is around 60% in 19898, 90% in 2004 of NFIES’s.

Chart 2 presents changes of liabilities in the same way as that of the financial assets. The values of any surveys increased until 2000, and remained at the same levels (approximately

8 As CSLC asks the value of class of asset until 2001, the annual average value until 2001 is calculated by the median of value class in this paper. The median of the top class takes into account the trend that the wider the range of the class the higher the class. The average values are since 2004 are based on public information.

Chart 1Amount of financial assets per household (million yen)

*1. FIES line since 2002 is jointed FSS line (by 2001). 2. The values of CSLC until 1998 are the average of median scores of classes. 3. The values of CCFSIs are the averages of the asset holding households only. 4. Values at interim years of NSFIE and CSLC are complemented by linear interpola-

tion.

604 S Maeda / Public Policy Review

CW6_A6335D06.indd 604 2015/09/03 13:19:02

605

5 million yen of liabilities per household) or slightly decreased recently. The levels and tran-sitions of all surveys are similar.

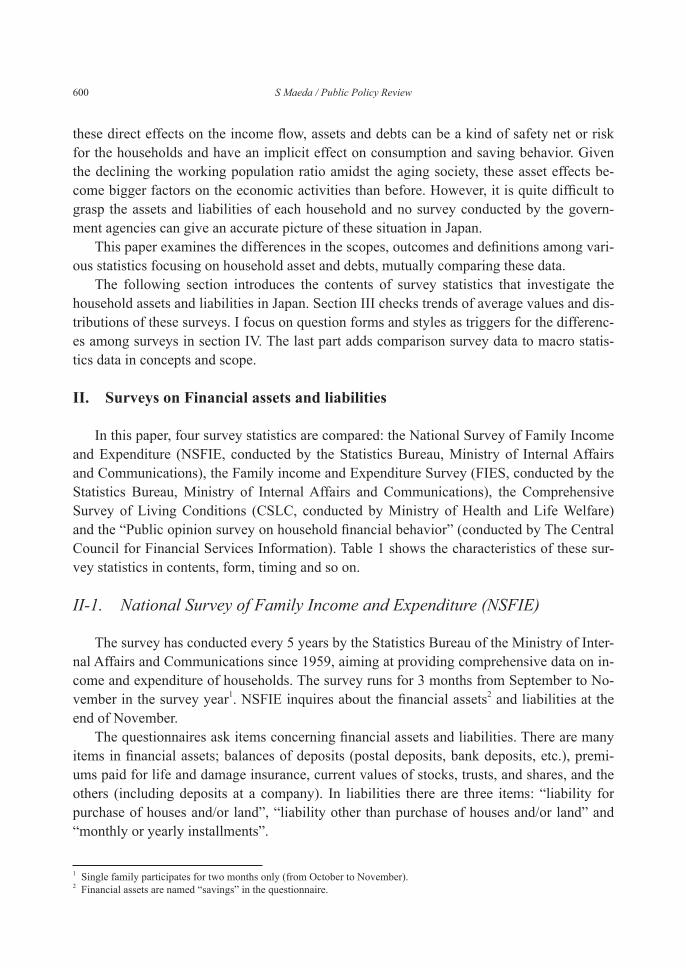

III-2. Distributions

Chart 3 shows the distributions of the assets in 2004 when all four surveys were imple-mented. Box chart (Chart 3(1) ) shows the median, mean, the boundaries of 25% and 75% tile in each survey. FIES ranks higher in each value than any other survey. The second is NSFIE, and CSLS follows. CCFSI values have considerable distance from other surveys.

Chart 3(2) shows frequency distributions of four surveys by financial assets classes. These classes are adjusted to those of the CSLC report. NSFIE and FIES distribution forms are similar. In both surveys, there are around 5% of the “1-5 million yen” class, 10% to 15% in the “500-15 million yen” class, around 8% of “15 - 20 million yen” and around 10% of the “30 million yen or more” . The share of households that answered no-financial assets

Table 2Assets per household (1989, 2004/ thousand yen)

*CCFSI basically shows average of only asset holders , the values in parentheses the average with non-holders’

Chart 2Amount of Liabilities per household (million yen)

*1. FIES line since 2002 is jointed FSS line (by 2001). 2. The value of CSLC until 1998 is the average of median scores of classes.

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 605 2015/09/03 13:19:02

Chart 3Distributions of financial assets (2004)

*made from the micro-data of each survey. two-or-more person households

606 S Maeda / Public Policy Review

CW6_A6335D06.indd 606 2015/09/03 13:19:03

607

(savings) in NSFIE is higher than that of FIES9.Regarding CSLC and CCFSI, these distributions are quite different from the above two

surveys’ distributions in their forms. The biggest difference is in the shares of “5 million yen or less” and “zero” classes. That the shares of CSLC and CCFSI are much higher10 and that 26% (more than one quarter) of CCFSI households answered “non-financial asset” deserves special mention. The high rate causes the lower average financial assets of CCFSI11.

Chart 4 shows the distributions of liabilities in the same forms as Chart 3. As the shares of no-liabilities households occupy 50-60% in any surveys, median values of all surveys are zero in Chart 4(1). Each proportion of households that answer no liabilities (or the sum of liabilities is zero) is around 55% of NSFIE and FIES, 65% of CSLC, 60% of CCFSI. Aver-age values of liabilities are calculated at around 5 million yen. When excluding the no liabil-ity households, average values are placed between 11 -13 million yen.

Chart 4 (2) shows the frequency distributions of the sum of liabilities. The frequency rate of “15-30 million yen” class is the highest among all four surveys. There are no big gaps in the liability data. Only in the less than 0.5 million class, CSLC and CCFSI’s rates are much smaller than NSFIE’s and FIES’s. CSLC and CCFSI could not cover a part of monthly loans and relatively small liabilities.

IV. What does cause the differences?

There are the bigger differences in financial assets among the survey data, according to both the level of the average and the forms of distributions. What would cause the differenc-es? This section examines the two possible contributing factors; sample bias and question-naire forms. There might be a difference caused by sample bias, because each survey em-ploys its ownsampling method. I also doubt that inquiry distinctions can vary the response.

IV-1. Sample: Difference in the age of the household heads

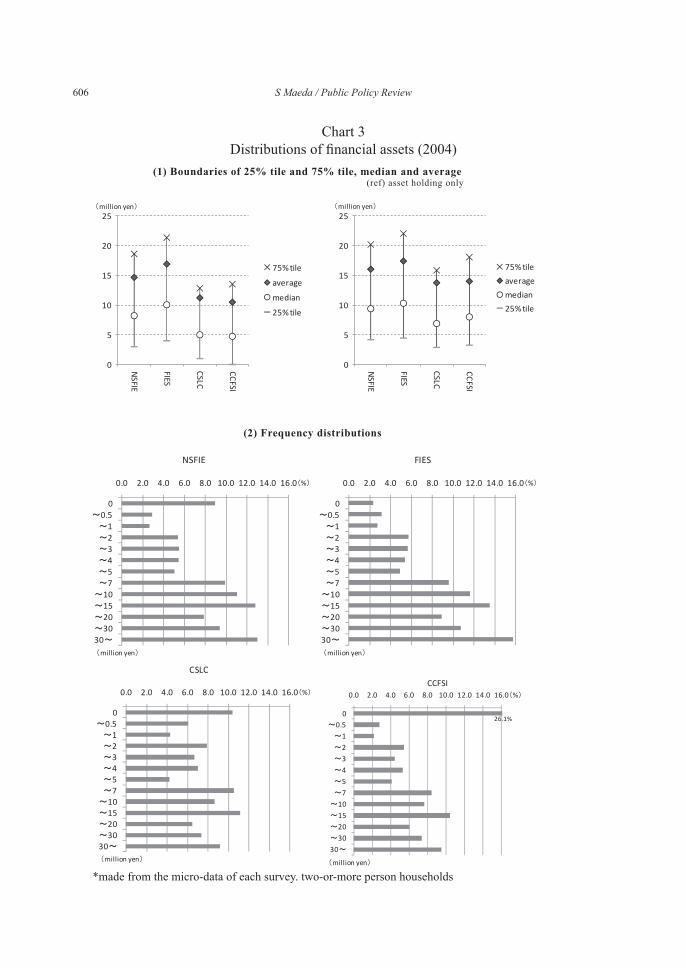

IV-1-1. The age of the head of householdChart 5 shows the proportions by the age-groups of household heads of four targeted

surveys and national census in 2010. The amount of financial assets would be affected by the age of the household head. The aged households tend to have more chance of having in-heritance assets than the younger households. Households with heads over 60 have a high probability of increasing financial assets by receiving retirement fees. All survey data actu-

9 The share of households without financial assets listed in FIES (since 2002) tends to be higher by around 1% than that of FSS (before 2000), and then it has seemed to be increasing.10 In CSLC, the ratio of those answered without assets (savings) has decreased to beneath 10% since 2000, while it had been 10-13% during 1986 to 1998. CCFSIs’ ratio, from 5% to 10% until 2000, had climbed to over 20% since 2000 and increased continuously. The values are observed, paying attention to a question structure change during the 2007’s survey.11 Suzuki (2009) reported the ratio of “no assets” in the CCFSI could be changed. He pointed out the possibility that the ratio, 21.8% in the 2003 survey, would be 14.5% when excluding the households with inconsistent answers, and then would be 4.5% when applying the strict definition.

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 607 2015/09/03 13:19:03

Chart 4Distributions of liabilities (2004)

*made from the micro-data of each survey. two-or-more person households

608 S Maeda / Public Policy Review

CW6_A6335D06.indd 608 2015/09/03 13:19:03

609

ally show a higher amount of assets in the higher ages of household heads. Suppose a survey including many households with aged heads (with the possibility to

possess much more assets) could show higher average assets and liabilities. The share of “30s or less” in all of four surveys are smaller than that of the national census12. In CSLC, “30-40s” are especially small, and “60s or more” are bigger. In CCFSI, the share of “50s” is comparatively large. The age distributions of NSFIE and FIES are close to that of the na-tional census.

CSLC should show higher financial asset averages because the survey has a larger pro-portion of aged household heads which should mean bigger financial assets. However CSLC average is actually lower than any other administrative surveys according to the comparison in the previous section. CSLC’s values of financial assets may be smaller than those of the other surveys even in aged households.

IV-1-2. The amount of financial assets by the age-class of the household headChart 6 is the box chart that shows the values of 10%, 25%, 75% and 90% tile, median

and average in sum of financial assets by age classes of households’ heads. There are three age classes, “30-40s”, “50s” and “60s”, in the graph.

There are not big differences among the values of all surveys in the class of “30-40s”. The differences between surveys become clarified in “50s” or “60s”. The highest is the FIES in any boundaries. NSFIE is a close second based on averages. CSLC is quite low compared to these two surveys. Thus CSLC reports the lowest level of asset amount by age classes among the surveys targeted in this paper.

12 In this data, the household head is not the person earning the substantial income of the household. The definition is different from that of the national census.

Chart 5Age-classes of household heads (2004)

*two-or-more household.

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 609 2015/09/03 13:19:03

IV-2. Characteristics of outcomes and methods of surveys

IV-2-1. Effect of the breakdownBias may be sited as a cause of a small CSLS value. Some CSLC characteristics except

age might drive the omission of reports by household. Respondents usually copy the values on available records to the schedules of surveys, and fulfill the questionnaires based on their own memories. Survey accuracy would require a design to prevent omission of report. It is possible smaller categories of assets reduce underclaims or omissions of report. If the assets are fractionized on more detailed categories, respondents must check the information item by items to fulfill their questionnaires. For example, when the respondents answer the bal-ance of banking accounts only, they are probably ready to check their account books. How-ever, if they answer the total of the assets, they might forget summing up financial commod-ities that they do not ordinarily recognize as ”financial assets (savings in questionnaires of the surveys)”; trusts and money trusts, insurance fees paid-in and so on.

In order to check whether the differences in question structures cause differences of sur-veys outcomes or not, it is necessary to compare plural surveys with similar scopes of sam-ples. I picked up FIES in 2002 and FSS in 2001. FSS did not have exactly the same question items but had the same sampling procedure of FIES.

When the FSS was integrated into FIES, two points were changed in the question struc-ture. One is the question of possession of assets or liabilities. FIES ask the values of asset or

Chart 6Distribution of Financial Assets By age classes of household heads (2004)

*made from the micro-data of each survey. two-or-more person households

610 S Maeda / Public Policy Review

CW6_A6335D06.indd 610 2015/09/03 13:19:03

611

liability items directly. FSS asks the value after checking the possession of each asset. An-other is the categories of the assets. The FSS itemized the assets in more detail than FIES (See Table A2). FSS itemized deposits of banking accounts into the bank accounts and trust associations, and insurance into the postal, life and damage insurance. FSS also divided the “stock and shares”, “open-end trusts”, “bonds” and “bond trust” in securities. Participants of FIES are requested to fill the values summed up in these two or three contents.

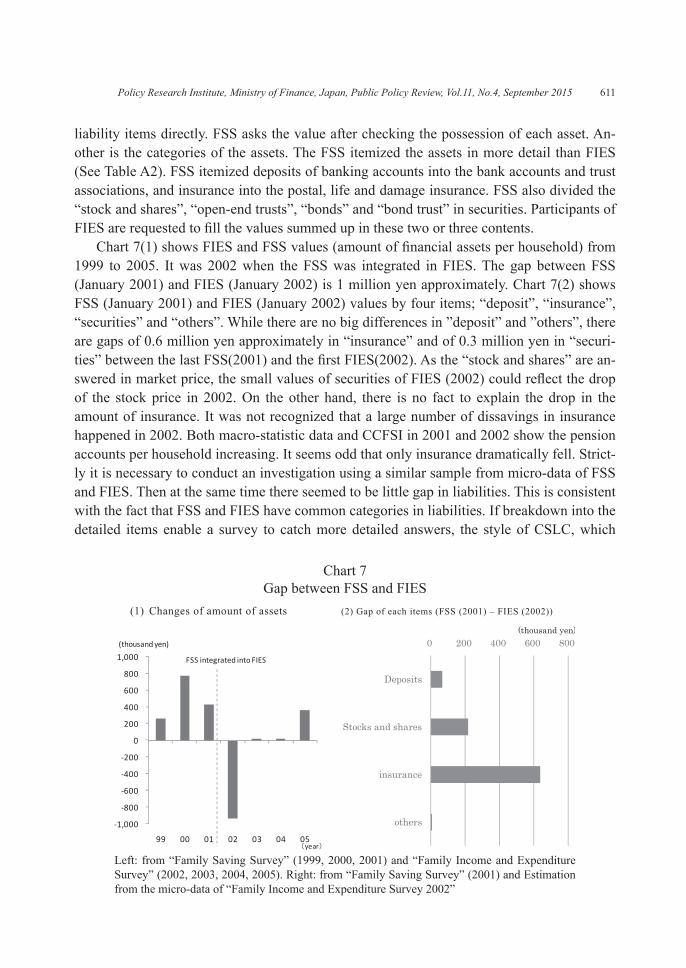

Chart 7(1) shows FIES and FSS values (amount of financial assets per household) from 1999 to 2005. It was 2002 when the FSS was integrated in FIES. The gap between FSS (January 2001) and FIES (January 2002) is 1 million yen approximately. Chart 7(2) shows FSS (January 2001) and FIES (January 2002) values by four items; “deposit”, “insurance”, “securities” and “others”. While there are no big differences in ”deposit” and ”others”, there are gaps of 0.6 million yen approximately in “insurance” and of 0.3 million yen in “securi-ties” between the last FSS(2001) and the first FIES(2002). As the “stock and shares” are an-swered in market price, the small values of securities of FIES (2002) could reflect the drop of the stock price in 2002. On the other hand, there is no fact to explain the drop in the amount of insurance. It was not recognized that a large number of dissavings in insurance happened in 2002. Both macro-statistic data and CCFSI in 2001 and 2002 show the pension accounts per household increasing. It seems odd that only insurance dramatically fell. Strict-ly it is necessary to conduct an investigation using a similar sample from micro-data of FSS and FIES. Then at the same time there seemed to be little gap in liabilities. This is consistent with the fact that FSS and FIES have common categories in liabilities. If breakdown into the detailed items enable a survey to catch more detailed answers, the style of CSLC, which

Chart 7Gap between FSS and FIES

Left: from “Family Saving Survey” (1999, 2000, 2001) and “Family Income and Expenditure Survey” (2002, 2003, 2004, 2005). Right: from “Family Saving Survey” (2001) and Estimation from the micro-data of “Family Income and Expenditure Survey 2002”

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 611 2015/09/03 13:19:04

asks only the sum of assets and liability, would tend to encourage omissions and the result would be smaller13.

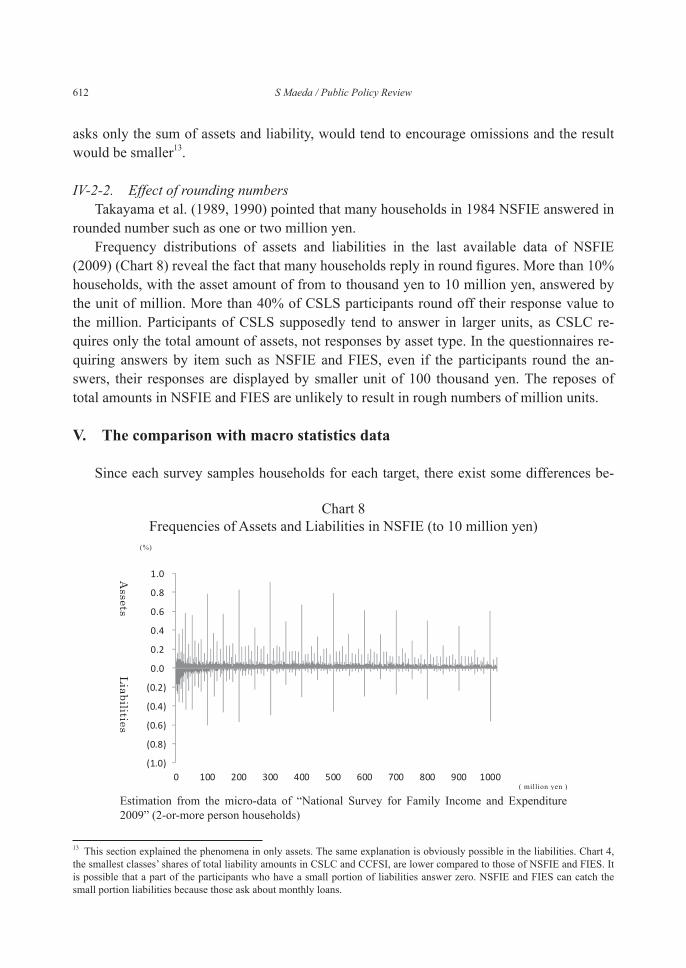

IV-2-2. Effect of rounding numbersTakayama et al. (1989, 1990) pointed that many households in 1984 NSFIE answered in

rounded number such as one or two million yen. Frequency distributions of assets and liabilities in the last available data of NSFIE

(2009) (Chart 8) reveal the fact that many households reply in round figures. More than 10% households, with the asset amount of from to thousand yen to 10 million yen, answered by the unit of million. More than 40% of CSLS participants round off their response value to the million. Participants of CSLS supposedly tend to answer in larger units, as CSLC re-quires only the total amount of assets, not responses by asset type. In the questionnaires re-quiring answers by item such as NSFIE and FIES, even if the participants round the an-swers, their responses are displayed by smaller unit of 100 thousand yen. The reposes of total amounts in NSFIE and FIES are unlikely to result in rough numbers of million units.

V. The comparison with macro statistics data

Since each survey samples households for each target, there exist some differences be-

13 This section explained the phenomena in only assets. The same explanation is obviously possible in the liabilities. Chart 4, the smallest classes’ shares of total liability amounts in CSLC and CCFSI, are lower compared to those of NSFIE and FIES. It is possible that a part of the participants who have a small portion of liabilities answer zero. NSFIE and FIES can catch the small portion liabilities because those ask about monthly loans.

Chart 8Frequencies of Assets and Liabilities in NSFIE (to 10 million yen)

Estimation from the micro-data of “National Survey for Family Income and Expenditure 2009” (2-or-more person households)

612 S Maeda / Public Policy Review

CW6_A6335D06.indd 612 2015/09/03 13:19:04

613

tween survey data and the macro statistics data which cover the entire nation. For correct understanding of the analysis using these survey data, it would be useful to recognize the differences of both types of data14.

This section checks recent trends of macro statistics data and examines the difference between macro statistic data and survey data in their definitions. The NSFIE data is em-ployed as survey data to compare with the macro statistic data. This is because the NSFIE has the largest sample size of the household surveys by the government and covers the one person households.

V-1. Assets and liabilities in SNA and FFA

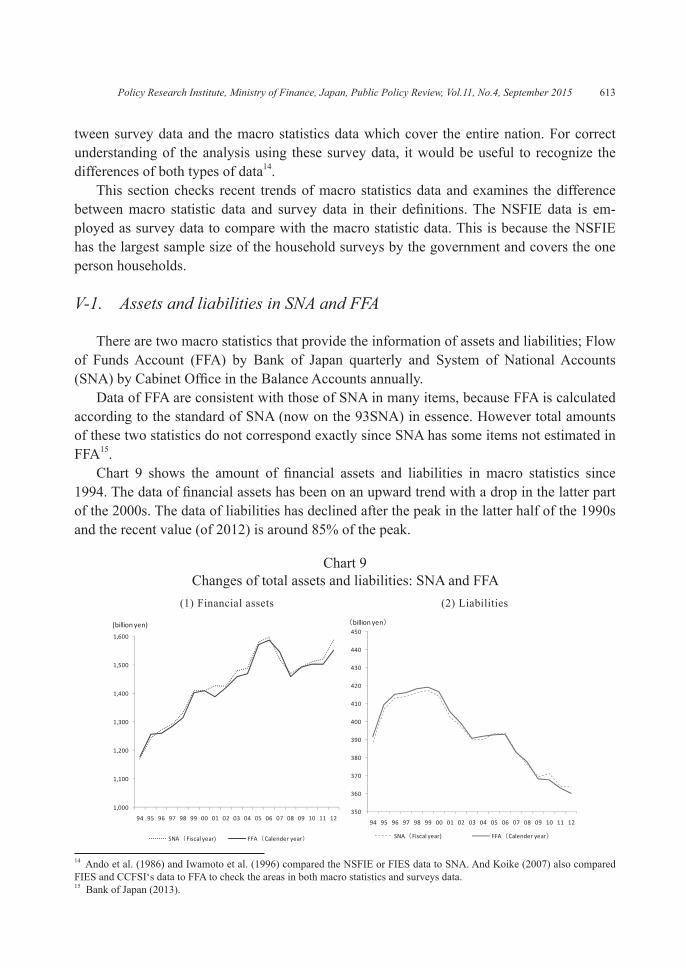

There are two macro statistics that provide the information of assets and liabilities; Flow of Funds Account (FFA) by Bank of Japan quarterly and System of National Accounts (SNA) by Cabinet Office in the Balance Accounts annually.

Data of FFA are consistent with those of SNA in many items, because FFA is calculated according to the standard of SNA (now on the 93SNA) in essence. However total amounts of these two statistics do not correspond exactly since SNA has some items not estimated in FFA15.

Chart 9 shows the amount of financial assets and liabilities in macro statistics since 1994. The data of financial assets has been on an upward trend with a drop in the latter part of the 2000s. The data of liabilities has declined after the peak in the latter half of the 1990s and the recent value (of 2012) is around 85% of the peak.

Chart 9Changes of total assets and liabilities: SNA and FFA

14 Ando et al. (1986) and Iwamoto et al. (1996) compared the NSFIE or FIES data to SNA. And Koike (2007) also compared FIES and CCFSI‘s data to FFA to check the areas in both macro statistics and surveys data.15 Bank of Japan (2013).

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 613 2015/09/03 13:19:04

V-2. Comparison between the survey data and macro statistics data

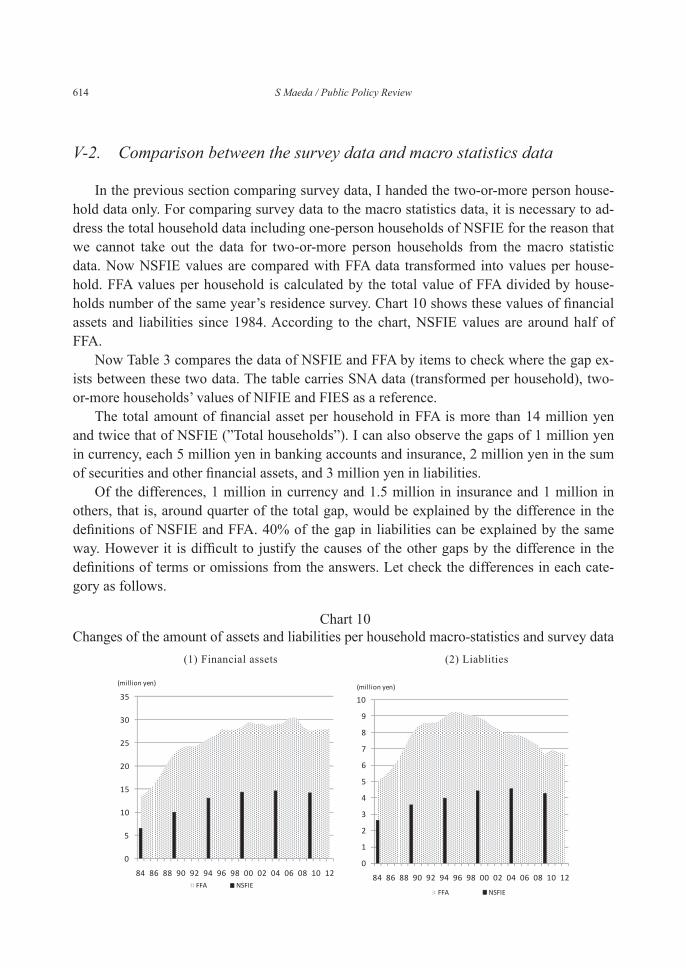

In the previous section comparing survey data, I handed the two-or-more person house-hold data only. For comparing survey data to the macro statistics data, it is necessary to ad-dress the total household data including one-person households of NSFIE for the reason that we cannot take out the data for two-or-more person households from the macro statistic data. Now NSFIE values are compared with FFA data transformed into values per house-hold. FFA values per household is calculated by the total value of FFA divided by house-holds number of the same year’s residence survey. Chart 10 shows these values of financial assets and liabilities since 1984. According to the chart, NSFIE values are around half of FFA.

Now Table 3 compares the data of NSFIE and FFA by items to check where the gap ex-ists between these two data. The table carries SNA data (transformed per household), two-or-more households’ values of NIFIE and FIES as a reference.

The total amount of financial asset per household in FFA is more than 14 million yen and twice that of NSFIE (”Total households”). I can also observe the gaps of 1 million yen in currency, each 5 million yen in banking accounts and insurance, 2 million yen in the sum of securities and other financial assets, and 3 million yen in liabilities.

Of the differences, 1 million in currency and 1.5 million in insurance and 1 million in others, that is, around quarter of the total gap, would be explained by the difference in the definitions of NSFIE and FFA. 40% of the gap in liabilities can be explained by the same way. However it is difficult to justify the causes of the other gaps by the difference in the definitions of terms or omissions from the answers. Let check the differences in each cate-gory as follows.

Chart 10Changes of the amount of assets and liabilities per household macro-statistics and survey data

614 S Maeda / Public Policy Review

CW6_A6335D06.indd 614 2015/09/03 13:19:04

615

V-2-1. Currency, banking accountWhile the currency is contained into the macro statistics, it is not the item of any sur-

veys’ data. NSFIE and FIES, for example, reflect held cash and hoarded money which are not subjects in NSFIE and FIES. The gap is demonstrated by the gap of the definition of mi-cro and macro statistics.

Banking account has the biggest gap between survey data and macro statistics. It may exist for two reasons; incorrect answer and a definition gap in the households between these two kinds of data.

Possible omission of report in the survey data can be explained by the reason in the pre-vious section (IV-2). That is, surveys ask the total balance of deposits rather than by each account book of financial institutions such as banks and credit associations. Suppose a case that a household can have a number of banking accounts. The household head cannot check the all the banking accounts of household given that family members might make new bank-ing accounts. Respondents might answer the rounded value. For the above situation, it would be natural that survey data is smaller than that of macro statistics data.

The difference of these two data is caused by the range of the households. Macro statis-tics data include the private business owners in the households. Household deposit balance in macro statistics data simply refers to deposits made in the name of individuals. That is, the balance would be also contained the business accounts with the name of individuals. Though questionnaires of both NSFIE and FIES explain that the funds and banking balance for private business should be private savings, the answerer can judge to classify the account for business with its own individual name or into the private one or not. The scope of the survey data can be smaller than that of macro statistics data method (the deposit with an in-dividual name sorted into the category of household)

6

Table 3Comparison macro statistics data and survey data Assets and liabilities per household (2009)

16 At the 1st January, 2010

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 615 2015/09/03 13:19:05

V-2-2. Insurance and pensionInsurance and pension of NSFIE is less than 40% of the macro statistics data, it has the

largest gap. In this category, there is a clear difference in the definition. Survey data request the insurance premiums that household paid. On the other hand, macro statistics data in-clude the premiums paid by the companies and a part of the annuity reserves that are calcu-lated by the statistics of insurers. The share of workers’ household is 54% of “Total house-holds”(NSFIE, 2009). If those people go halves with their companies in premiums, 1.5 million yen (30% of the gap) per household can be explained.

V-2-3. SecuritiesThe majority of securities are stock and shares. The stock and shares of survey data (NS-

FIE) seems to be the equivalent level of that of the macro statistics data (FFA). However at-tention should be paid to the difference of the definition in investment trusts in securities be-tween the survey data and macro statistics. While survey data mainly deals with the investment trust as bond trusts, stock and shares, trusts are included in stock and shares, macro statistics data totals stock, shares, money and bond trust as the investment trust. We can see the relation of ‘“stock and shares” in macro statistics “stock and shares”, + “stock and shares”, “trusts” in survey data’ in the comparison of Table3. That means ‘“stock and shares,” in macro statistics’ > ‘“stock and shares” in survey data’17. Unfortunately we cannot recognize the exact extent of the underestimation.

V-2-4. Others (assets)The gaps in the others are primarily explained by the difference of definitions. Macro

statistics data contains deposit money, golf-club memberships, balances of prepaid money, etc., while survey data omit these contents in the survey items. The deposits money in mac-ro statistics data (deposit money and balance of accounts receivable/payable) per household is approximately 900 thousand yen. Including premiums of golf-club memberships, elec-tronic money etc. are estimated at 150 thousand yen (by other survey estimation) per house-hold18. Thus at least 1 million yen of the gap with other assets would be explained by the definition.

V-2-5. LiabilitiesLiabilities in macro statistics data include “trade credits” and “accounts payable” which

are not the items in NSFIE. Total of these categories is more than 1 million yen, which can

17 SNA’s stock and shares estimation is larger than those of FFA, as SNA estimates these data including the non-listed stocks. It might be better to compare stocks and shares of the survey (NSFIE) to the SNA, because the survey does not clearly ask the respondents to exclude the non-listed stocks and shares. However, it is difficult for each household to evaluate the market price of the non-listed stocks and shares such as stocks of their own family companies. Survey data seems to exclude the non-listed stock and shares. Then I employ the definition of FAA that excludes the non-listed stocks and shares18 The premium value of golf-club memberships is categorized as durable goods (of real assets) in NSFIE. (0.8 million yen approximately). Now, the other survey in 2009 recently reported that the balance of electrical money is around 100 billion yen by the Bank of Japan (2012)

616 S Maeda / Public Policy Review

CW6_A6335D06.indd 616 2015/09/03 13:19:05

617

explain around 40% of the gap between survey data and macro statistics data.It is difficult to interpret whether the difference of definition creates these gap in “funds

for the business”, the item of macro statistics, or not. According to the direction of NS-FIE,educational loan and the other loan for private business should be included in the total of the liabilities, and liabilities like “loans to companies and governments” in the macro sta-tistics might be covered in the NSFIE. However the survey statistics do not ask the fund or loan for business separately, and thus we cannot check what to extent the participants in-clude the business funds and loans.

VI. Conclusion

In this paper, I examined the points regarding usage of the representative statistics that investigate household assets and liabilities (NSFIE, FIES, CSLC, CCFSI), comparing the surveys with each other and with macro statistics data regarding the consistencies and dif-ferences.

Comparison with the surveys in the average of the financial assets shows that the values of the CSLC and CCFSI’s are significantly lower than the levels of other surveys’. What makes the average of CSLC’s lower than other surveys, is not the difference of the sample, but rather the questions, which inquire only the amount of assets to participants. And then, CCFSI has a big ratio of households who reply that they have no financial assets. This fact causes CCFSI’s average financial assets to be lower. The question styles would be a cause of differences in the survey data, as the question that ask the values summed up withdraws the undervalued or rounded answers.

Moreover, comparing survey data (especially NSFIE) to macro statistics data by the items of financial assets and liabilities, each value of survey data is considerably smaller than those of macro statistics data. While almost 40% of the gap in liabilities could be ex-plained by the difference in the definition (scope of the items) between these two types, it is approximately 25% in assets.

The differences in the scope of the reports and definitions affect the gap among individ-ual surveys and between survey data and macro statistics. It would also be important to un-derstand the differences among the different data in their characteristics and scope when we use these survey data for economic analysis.

References

Ando, Albert・Michiko Yamashita・Junki Murayama (1986), ”Research on Consumption and Saving Behavior from Life Cycle Hypothesis”, Keizai Bunseki 101, pp. 25–139. (Japanese)

Banks of Japan (2005),” Compilation Method of Japan’s Flow of Funds Accounts”Banks of Japan, Payment and Settlement System Department (2012),”Recent Development

in Electronic Money in Japan”, BOJ Report & Research Papers, December 2012

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 617 2015/09/03 13:19:05

Iwamoto, Yasushi・Satoshi Ozaki・Hiroki Maekawa (1996), “Gap on the household saving rate between FIES and SNA (2): regarding consistencies of micro and macro data” (“Kakeichosa to Kokuminkeizaikeisan niokeru kakei chochikuritsu doukou no kairi nitsuite 2”), Ministry of Finance, Financial Review, No. 37. (Japanese)

Koike, Takuji(2007), “Present state and disparities in household assets”, (“Kakei shisan no Genjo to sono Kakusa”), National Diet Library, Reference, November 2007, pp. 67–83. (Japanese)

Ministry of Internal Affairs and Communications, Statistics Bureau (2010), “Outline of the 2009 National Survey for Family Income and Expenditure one-person household”

Suzuki, Wataru (2009), “Who saves nothing? Evidence from Public Opinion Survey on Household Financial Assets and Liabilities” (“Dare ga mutyoiku mushisan kakeika shiteirunoka?”), Gakushuin- University Keizaironju, Vol 46–2, July 2009. (Japanese)

Takayama, Noriyuki・Fumio Funaoka・Fumio Ohtake・Masahiko Sekiguchi・Hiroshi Ueno・Tokiyuki Shibuya (1989), “Assets and saving rates in Japanese households” (”Nihon no kakei shisan to tyotikuritsu”), Keizai Bunseki, No.116, pp. 1–91. (Japanese)

Takayama, Noriyuki・Fumio Funaoka・Fumio Ohtake・Masahiko Sekiguchi・Tokiyuki Shibuya・Dai Ueno・Katsuyuki Kubo (1990) “Intertemporal Comparison in house-holds assets and saving rate”(“Kakeishisan hoyugaku no nenjisuii to kakei chochikurit-su no 2 jitenkan hikaku”), Economic Institute, Economic Planing Agency, Keizai Bun-seki No. 118, pp. 75–121. (Japanese)

618 S Maeda / Public Policy Review

CW6_A6335D06.indd 618 2015/09/03 13:19:05

619

Table A1Definitions of the items in NSFIE and macro statistics data (FFA)

Attention: FFA contains private non-financial assets (non-public stock and shares) into the funds, while the SNA categorizes it as part of the stock and shares.

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 619 2015/09/03 13:19:06

Table A2Differences in items between FSS and FIES

620 S Maeda / Public Policy Review

CW6_A6335D06.indd 620 2015/09/03 13:19:07

621

Table A3Changes in the questions of CSLC

注1. Postal offices until 2007 2. The market prices are designated in 2007 and 2010. 3. The market prices are designated in 2010. 4. Annual report shows 13classes distribution and the average. 5. Underline shows the point of change

Table A4Changes of CCFSI surveys

Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.11, No.4, September 2015

CW6_A6335D06.indd 621 2015/09/03 13:19:08

![Weekly Tallahasseean. (Tallahassee, Florida) 1900-12-27 [p ].ufdcimages.uflib.ufl.edu/UF/00/08/09/51/00025/00197.pdfLIVERFOR CURE Household AIN lillandWlntM-iss Medicitv Japanese tffalkerCmpany](https://img.pdfslide.us/doc/110x75/600699874ce102423d5b33ee/weekly-tallahasseean-tallahassee-florida-1900-12-27-p-liverfor-cure-household.jpg)