Embed Size (px)

Citation preview

The Federal Reserve and Monetary Policy

Chapter 14

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

14-2

Learning Objectives

1. Understand the organization of the Federal Reserve System.

2. Explain reserve requirements.

3. Apply the deposit expansion multiplier.

4. Explain the creation and destruction of money.

5. List and apply the tools of monetary policy.

6. Discuss the Fed’s effectiveness in fighting inflation and recession.

7. Examine the Banking Act of 1980 and 1999.

8. List and discuss monetary policy lags.

9. Summarize the housing bubble and the subprime mortgage crisis.

10. Explain how a normally functioning financial system was restored.

11. Discuss whether “Ben Bernanke should have been reappointed to a second term.

After this chapter you should be able to:

14-3

Early U.S. central banks lapsed due to political differences over direction of U.S. economy:

• First United States Bank [1791–1811]• Second United States Bank [1816–1836]

Central bank protects banking system from panics:• Panic is “run on bank” leading to depletion of reserves.

The Federal Reserve Act of 1913 created the Federal Reserve System:

• Legislation was response to Panic of 1907.• Federal Reserve and its District Banks created to act as

“lender of last resort” if bank’s reserves run low.

Fed is a quasi public-private enterprise.

The Federal Reserve System

14-4

Five Main Jobs of Federal Reserve

1. Conduct monetary policy: control the rate of growth of the money supply to foster macroeconomic stability

2. Serve as lender of last resort to commercial banks, savings banks, savings and loan associations, and credit unions

3. Issue currency (“Federal Reserve Note”)

4. Provide banking services to the U.S. government

5. Supervise and regulate our financial institutions

14-5

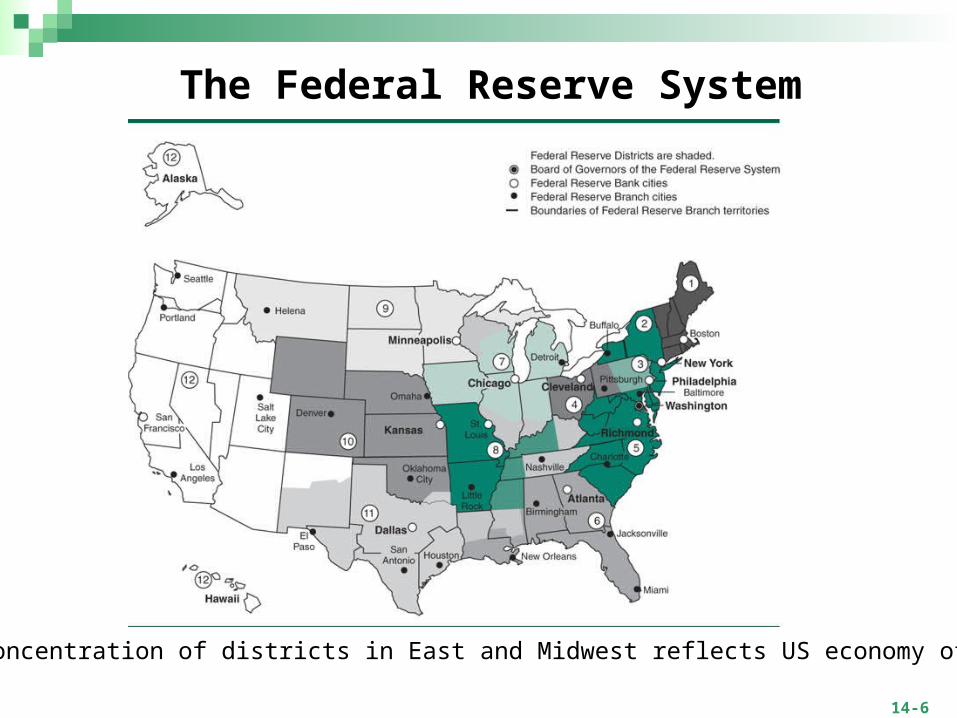

Structure of the Federal Reserve (“Fed”)

12 Federal Reserve District Banks, owned by the several hundred member banks in that district (private).

• Commercial banks own stock in Fed District Banks.• Each bank issues currency. (Look at your dollar bills!)

Federal Reserve Board of Governors in Washington, D.C. (public)

• Seven members, nominated by President and confirmed by Senate, serve one 14-year, non-renewable term.

Chair of the Board of Governors (public) • Chair, nominated by President and confirmed by Senate,

serves four-year, renewable terms. • Current Chair is Ben Bernanke (former Princeton economist). • Former Chair, Alan Greenspan, served 1987-2006.

14-6

The Federal Reserve System

Concentration of districts in East and Midwest reflects US economy of 1913.

14-7

Independence of the Board of Governors System was designed to limit political influence on Fed

policy makers. • One vacancy occurs every other year.• There are only two appointees during each presidential term,

unless Governors retire early. • Once appointed for 14 years, Fed Governors are not

answerable to elected officials. Is political independence good or bad?

• Pro: It allows Governors to follow unpopular policies they believe are in the best economic interest of the nation.

• Con: Critics argue they have too much power for unelected officials.

Political independence makes it easier for the Fed to fight inflation than it is for Congress and the President to use fiscal policy.

14-8

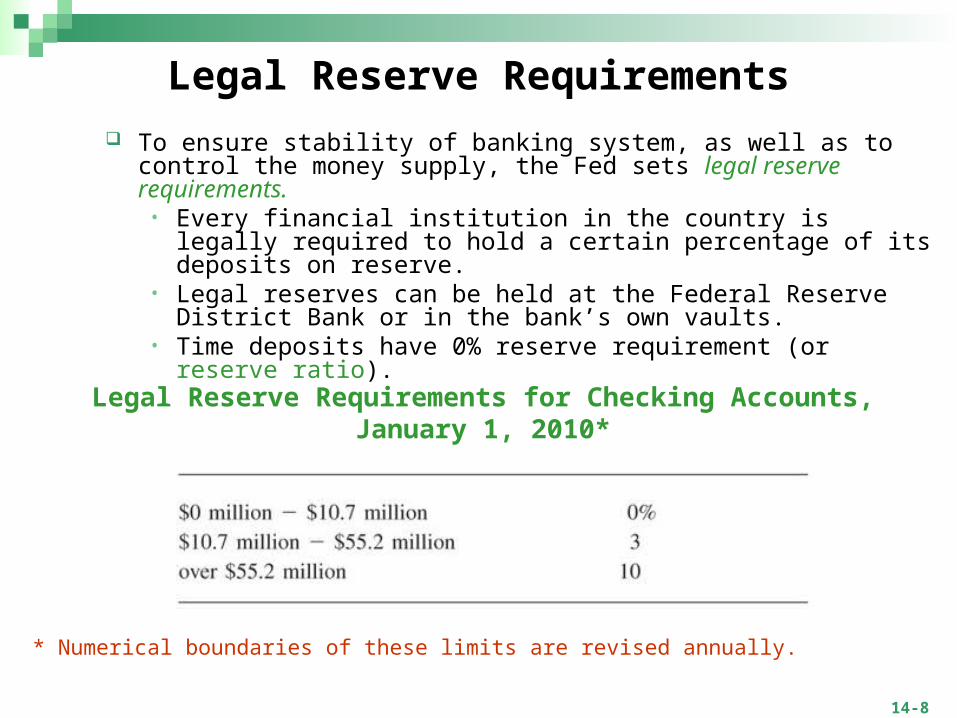

Legal Reserve Requirements

To ensure stability of banking system, as well as to control the money supply, the Fed sets legal reserve requirements.

• Every financial institution in the country is legally required to hold a certain percentage of its deposits on reserve.

• Legal reserves can be held at the Federal Reserve District Bank or in the bank’s own vaults.

• Time deposits have 0% reserve requirement (or reserve ratio).

Legal Reserve Requirements for Checking Accounts, January 1, 2010*

* Numerical boundaries of these limits are revised annually.

14-9

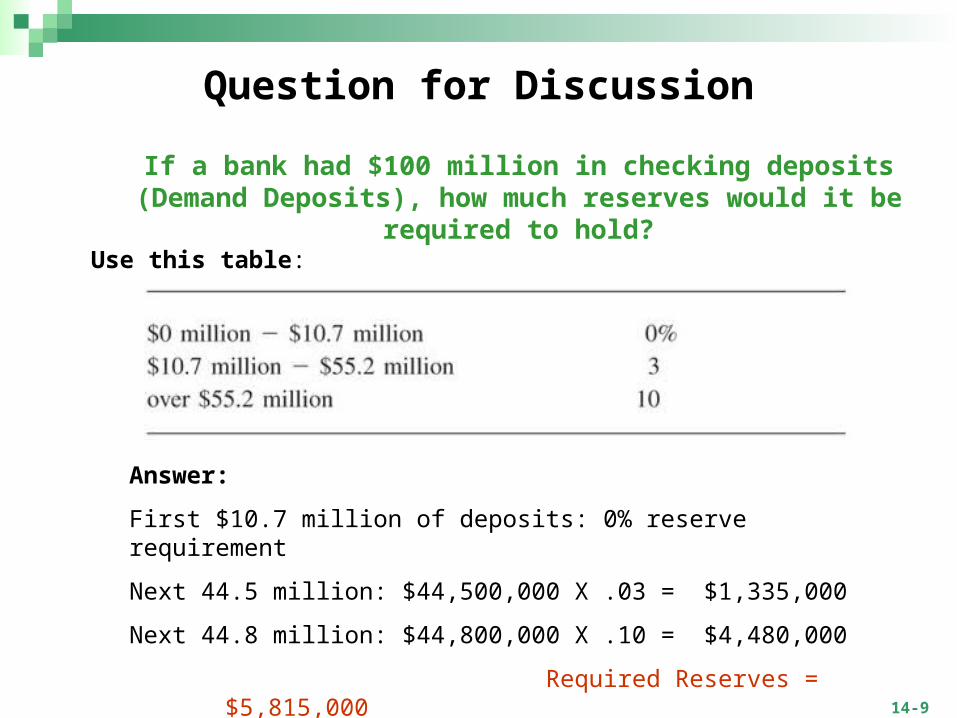

If a bank had $100 million in checking deposits (Demand Deposits), how much reserves would it be required to hold?

Answer:

First $10.7 million of deposits: 0% reserve requirement

Next 44.5 million: $44,500,000 X .03 = $1,335,000

Next 44.8 million: $44,800,000 X .10 = $4,480,000

Required Reserves = $5,815,000

Question for Discussion

Use this table:

14-10

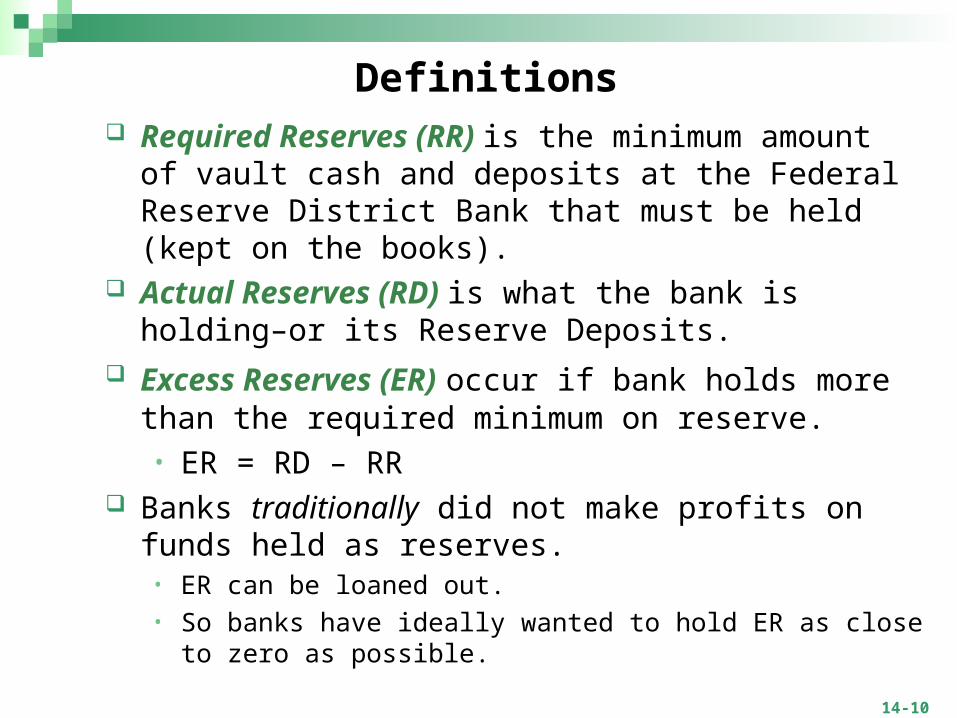

Definitions Required Reserves (RR) is the minimum amount of

vault cash and deposits at the Federal Reserve District Bank that must be held (kept on the books).

Actual Reserves (RD) is what the bank is holding–or its Reserve Deposits.

Excess Reserves (ER) occur if bank holds more than the required minimum on reserve.• ER = RD – RR

Banks traditionally did not make profits on funds held as reserves.

• ER can be loaned out. • So banks have ideally wanted to hold ER as close to zero as

possible.

14-11

What Happens if the Bank is Short?

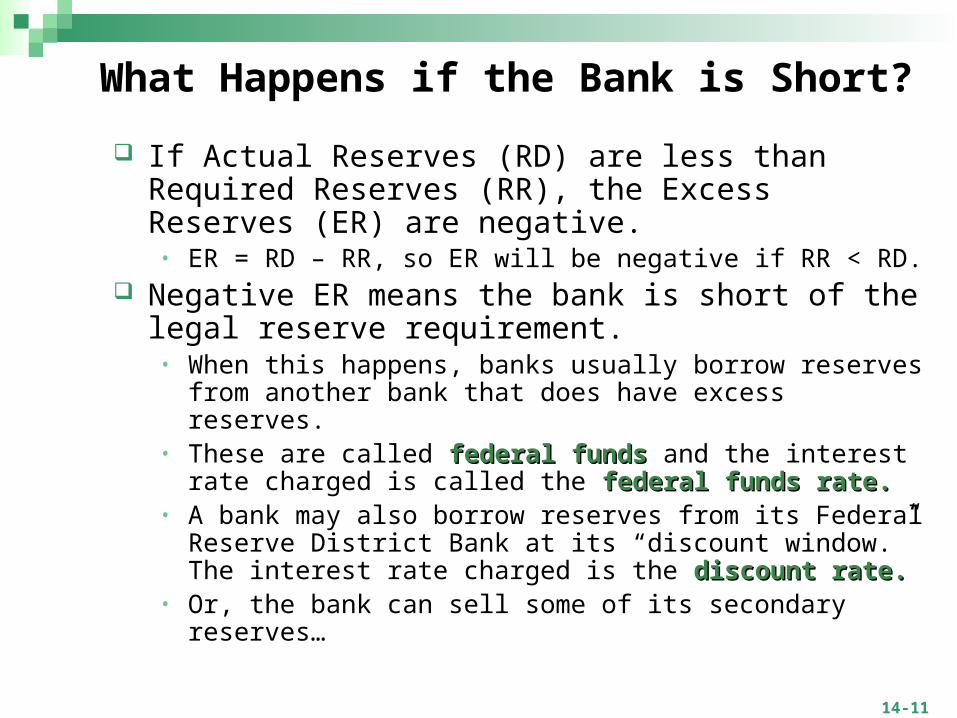

If Actual Reserves (RD) are less than Required Reserves (RR), the Excess Reserves (ER) are negative.

• ER = RD – RR, so ER will be negative if RR < RD. Negative ER means the bank is short of the legal

reserve requirement. • When this happens, banks usually borrow reserves from

another bank that does have excess reserves. • These are called federal fundsfederal funds and the interest rate charged

is called the federal funds rate.federal funds rate.• A bank may also borrow reserves from its Federal Reserve

District Bank at its “discount window.” The interest rate charged is the discount rate.discount rate.

• Or, the bank can sell some of its secondary reserves…

14-12

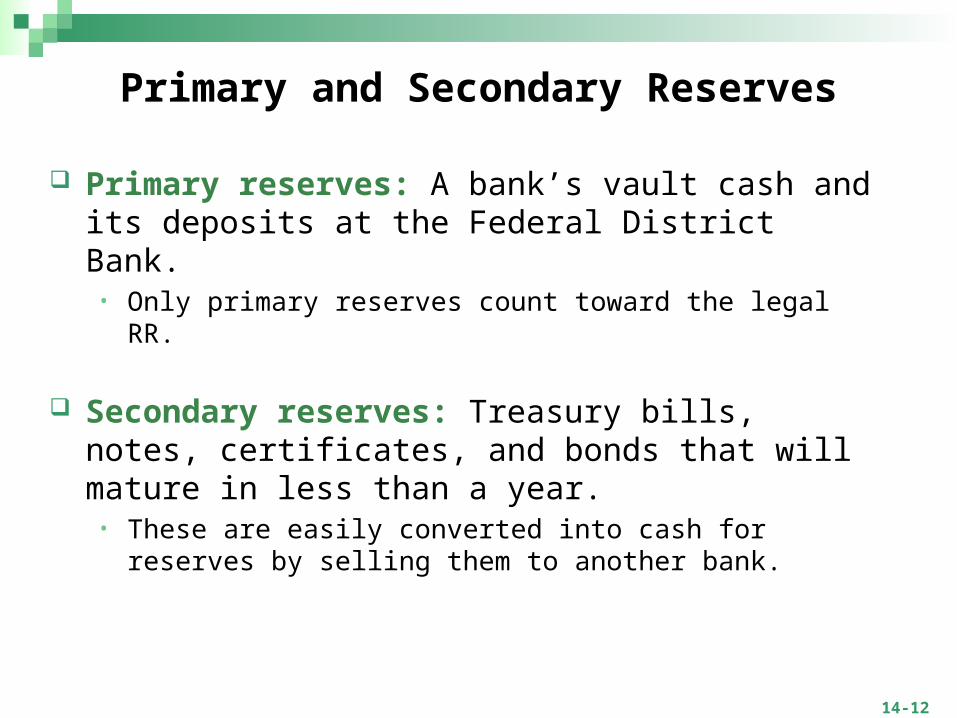

Primary reserves: A bank’s vault cash and its deposits at the Federal District Bank.

• Only primary reserves count toward the legal RR.

Secondary reserves: Treasury bills, notes, certificates, and bonds that will mature in less than a year.

• These are easily converted into cash for reserves by selling them to another bank.

Primary and Secondary Reserves

14-13

Reserve Requirements and the Deposit Expansion Multiplier

New money injected into the economy will have a multiplied effect on the macroeconomy (real GDP).

• Remember: Banks, like goldsmiths, create money when they make loans.

• If the reserve requirement is low, the bank has to keep less in their vaults (or with the Fed) and can lend out more money.

• If the reserve requirement is high, the bank has to keep more in their vaults (or with the Fed) and can lend out less money.

The reserve requirement affects the size of the deposit expansion multiplier.

• Let’s look at an example of the deposit expansion process…

14-14

Example of Deposit Expansion

Assume a 10% reserve ratio. Someone deposits $100,000 in a bank.

• The bank must keep $10,000 as RR (10% x 100,000).• It can lend out $90,000.

The company with the $90,000 loan writes a check to spend it. This is deposited in another bank.

• This bank must keep $9,000 in reserves to cover the new deposit—by borrowing cash or selling secondary reserves.

• But the second bank can lend out $81,000 ($90,000 – $9,000).

This $81,000 becomes a deposit in another bank, and the process continues.

14-15

Hypothetical Deposit Expansion with 10 Percent Reserve Requirement

If the process continued, there would be $100,000 in deposits credited tovarious bank accounts, backed by $100,000 in reserves.

14-16

Calculating the Deposit Expansion Multiplier(DEM)

DEM = 1

Reserve Ratio

Example: Assume a RR of 10%:

DEM =1

.10

= 10

14-17

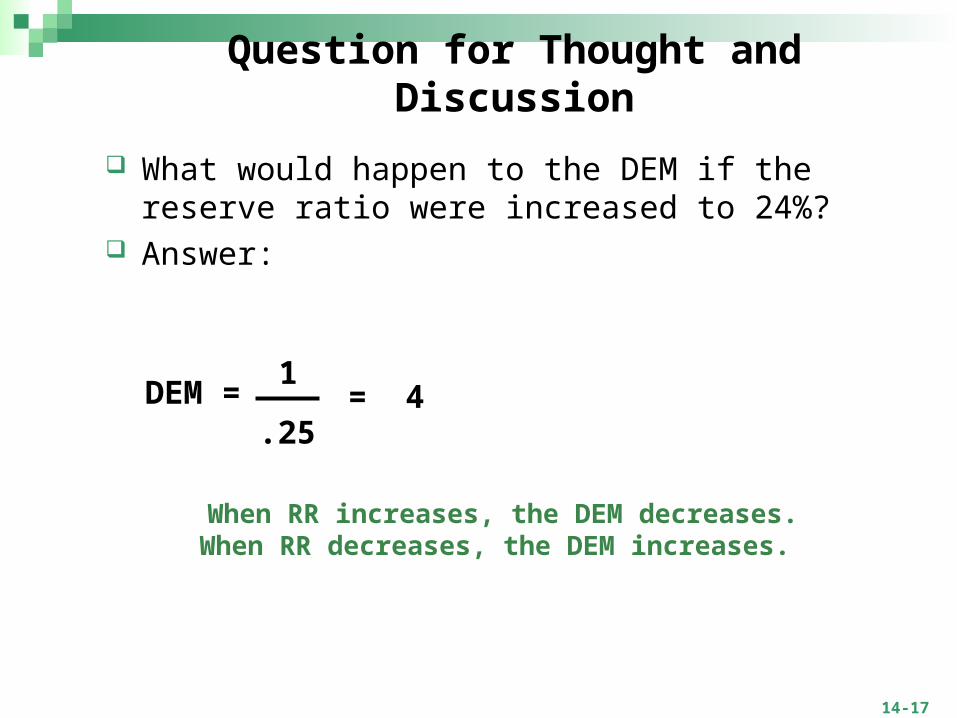

Question for Thought and Discussion

What would happen to the DEM if the reserve ratio were increased to 24%?

Answer:

DEM = 1

.25= 4

When RR increases, the DEM decreases.When RR decreases, the DEM increases.

14-18

Modifications of the DEM

The real DEM is lower than if it were based solely on the reserve ratio.

Three modifications:1. Some people will keep part of their loans in cash, rather than

depositing them in a checking account.2. Banks may carry excess reserves, to avoid getting caught

short.3. There are leakages of dollars to foreign countries, due to our

trade imbalance.

14-19

How Money Moves: Cash, Checks, and Electronic Money

About 90 percent of total payments in dollars worldwide are made electronically rather than with cash.

In 2004 Congress passed the Check Clearing Act of the 21st Century (“Check 21”).

• Law intended to facilitate electronic check processing. • How? Let’s look at the check clearing process.

14-20

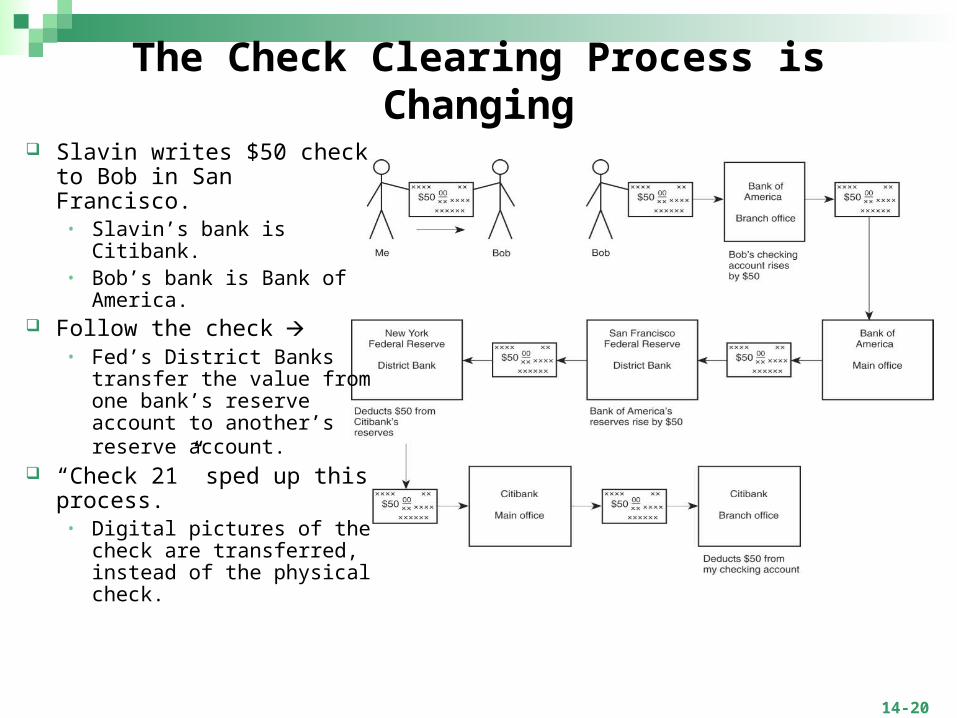

The Check Clearing Process is Changing

Slavin writes $50 check to Bob in San Francisco.

• Slavin’s bank is Citibank.• Bob’s bank is Bank of

America. Follow the check

• Fed’s District Banks transfer the value from one bank’s reserve account to another’s reserve account.

“Check 21” sped up this process.

• Digital pictures of the check are transferred, instead of the physical check.

14-21

Increasingly, money is changing hands electronically. • Example: When you use your debit card the amount is

deducted within seconds after the card is swiped. • Example: PayPal accounts facilitate paperless transfers.

About $1.4 trillion a day is transferred electronically.• About one-third of these transfers are carried out by the

Federal Reserve’s electronic network.• About two-thirds are done by the Clearing House Interbank

Payment System (CHIPS) which is owned by 10 big New York Banks.

Electronic Transfers

14-22

Tools of Monetary Policy The most important job of the Fed is to control the rate

of growth of the money supply. How? The Fed controls the money supply by using 3

monetary policy tools: 1. Open market operations: buying and selling government

securities to financial institutions. Open market operations have been the most commonly

used monetary policy tool.

2. Discount rate and federal funds rate: key interest rates that affect other interest rates.

3. Reserve requirements: changing the reserve ratio.

In response to the financial crisis, the Fed has developed new tools.

• Paying interest on reserve deposits to control rate of bank lending during recovery.

14-23

How Open-Market Operations Work

Remember: When the federal government runs a budget deficit (fiscal policy), the Treasury borrows money from the public:

• Treasury issues U.S. government securities, including Treasury bills, notes, certificates, and bonds.

• The total value of all outstanding U.S. government securities (our national debt) is about $6.0 trillion.

These securities can be resold in secondary financial markets.

• The Fed and other financial institutions buy and sell these chunks of the national debt.

• The Fed is constantly buying or selling Treasury bonds in open (secondary) markets.

14-24

Scenario #1: Increasing the Money Supply

To increase the money supply, the Fed buys bonds from banks and other financial institutions.

Follow the money: • The banks get money in exchange for some of the bonds in

their portfolios. • This money is put into circulation and increases the banks’

demand deposits.• Because of the DEM, there is a multiplied increase in the

money supply.

How does the Fed get the banks to sell?• It makes an offer they can’t refuse! • Price of bonds is pushed up.

14-25

Scenario #2: Decreasing the Money Supply

To decrease the money supply, the Fed sells bonds to banks and other financial institutions.

Follow the money: • The Fed gets money in exchange for some of the bonds in

their portfolios. • This money is taken out of circulation by the Fed.• Because of the DEM, there is a multiplied decrease in the

money supply.

How does the Fed get the banks to buy?• It makes an offer they can’t refuse! • The price of bonds is pushed down.

14-26

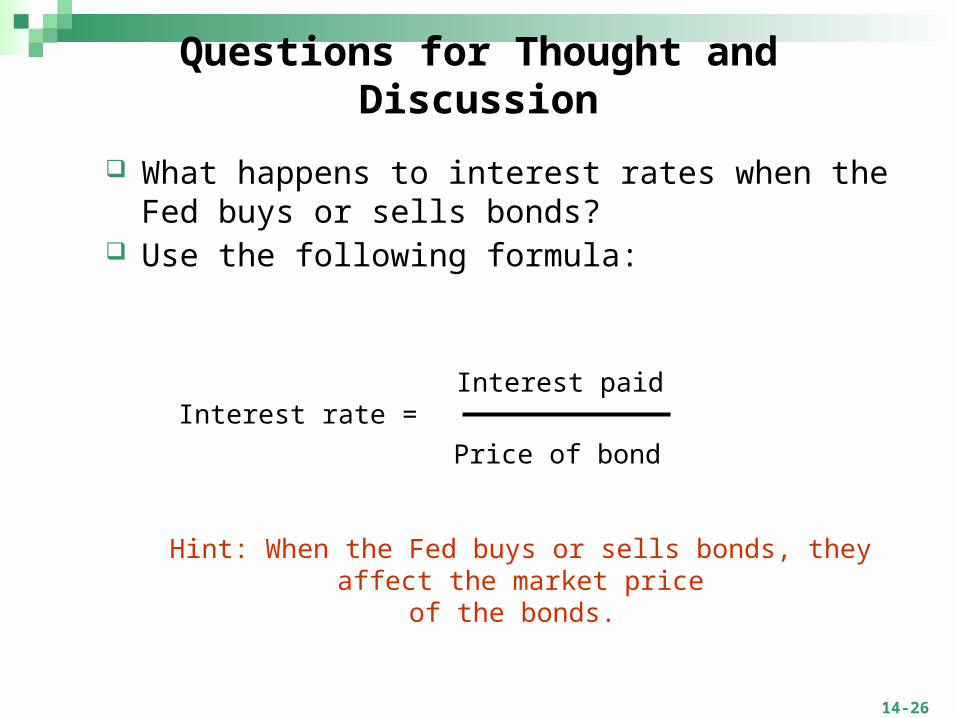

Questions for Thought and Discussion

What happens to interest rates when the Fed buys or sells bonds?

Use the following formula:

Interest rate =Interest paid

Price of bond

Hint: When the Fed buys or sells bonds, they affect the market priceof the bonds.

14-27

Impact of Increasing the Money Supply

Increasing the money supply leads to a decrease in interest rates.

During a recession, lower interest rates may encourage businesses to increase Investment and households to increase Consumption.

If C and I increase, the fiscal policy multiplier will lead to a greater increase in real GDP.

14-28

Impact of Decreasing the Money Supply

Decreasing the money supply leads to an increase in interest rates.

During inflation, higher interest rates may discourage business Investment and household Consumption.

If C and I decrease, the fiscal policy multiplier will lead to a greater decrease in real GDP, but it will also bring down the price level.

14-29

Federal Open-Market Committee

Open market operations are directed by the FOMC.

• FOMC consists of 8 permanent members – the Board of Governors and the president of the New York Federal Reserve District Bank.

• The other four positions rotate among the presidents of the other 11 Federal Reserve District Banks.

FOMC meets about every six weeks.• To fight recessions, the FOMC buys securities, increasing the

rate of growth of the money supply.• To fight inflation, the FOMC sells securities, decreasing the

rate of growth of the money supply.

14-30

Questions for Thought and Discussion

Suppose the Fed buys $200 million of securities and the deposit expansion multiplier (DEM) is 5. By how much could our money supply increase?

• ER x DEM = Potential increase in Money Supply• $200 million x 5 = $1,000,000,000 (or $1 billion)

Why is the answer only a “potential” increase in the money supply? Why is the actual increase probably less?

14-31

Discount rate is the interest rate paid by member banks when they borrow reserve deposits (RD) at their Federal Reserve District Bank.

Federal funds rate is the interest rate banks charge each other for borrowing reserve deposits (RD) from each other.

• Federal funds rate is higher than the discount rate. Lowering interest rates is expansionary response to

recession. Raising interest rates is contractionary response to

inflation.

Monetary Policy Tool #2: Key Interest Rates

14-32

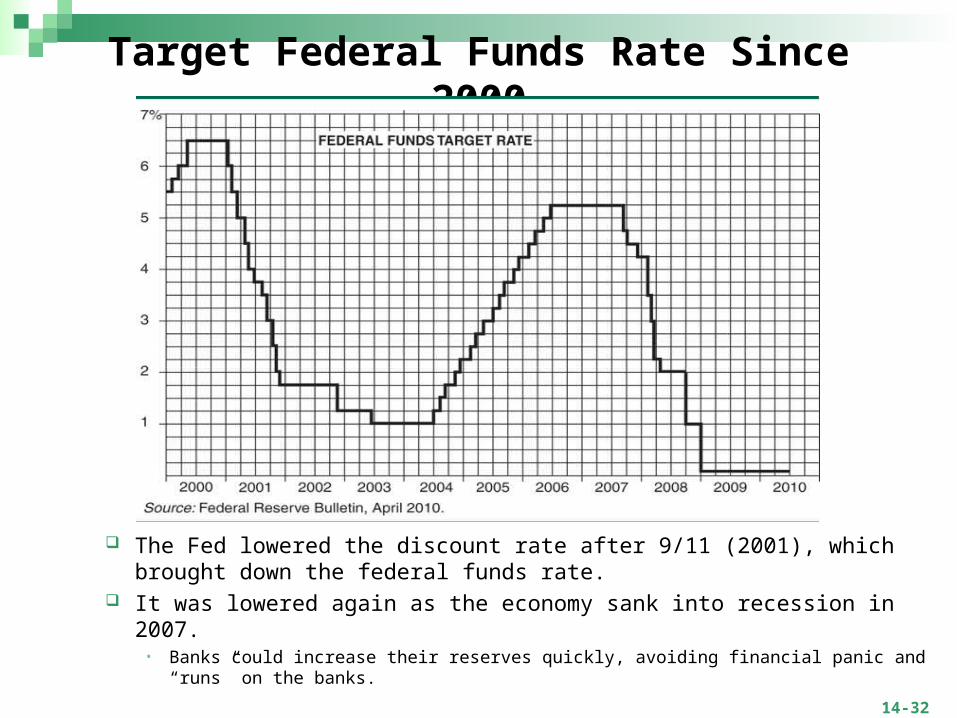

Target Federal Funds Rate Since 2000

The Fed lowered the discount rate after 9/11 (2001), which brought down the federal funds rate.

It was lowered again as the economy sank into recession in 2007.• Banks could increase their reserves quickly, avoiding financial panic and “runs”

on the banks.

14-33

Monetary Policy Tool #3: Changing Reserve Requirements

The Federal Reserve Board has the power to change reserve requirements within the legal limits of 8 and 14 percent for checkable deposits.

• Changing reserve requirements is the ultimate weapon and is rarely used (about once per decade).

To combat recession, Fed lowers required reserve ratio to create more excess reserves.

• Example: Lowered from 12% to 10% in 1992.

To combat inflation, Fed would increase required reserve ratio.

• Banks would have to scramble to increase reserves.

14-34

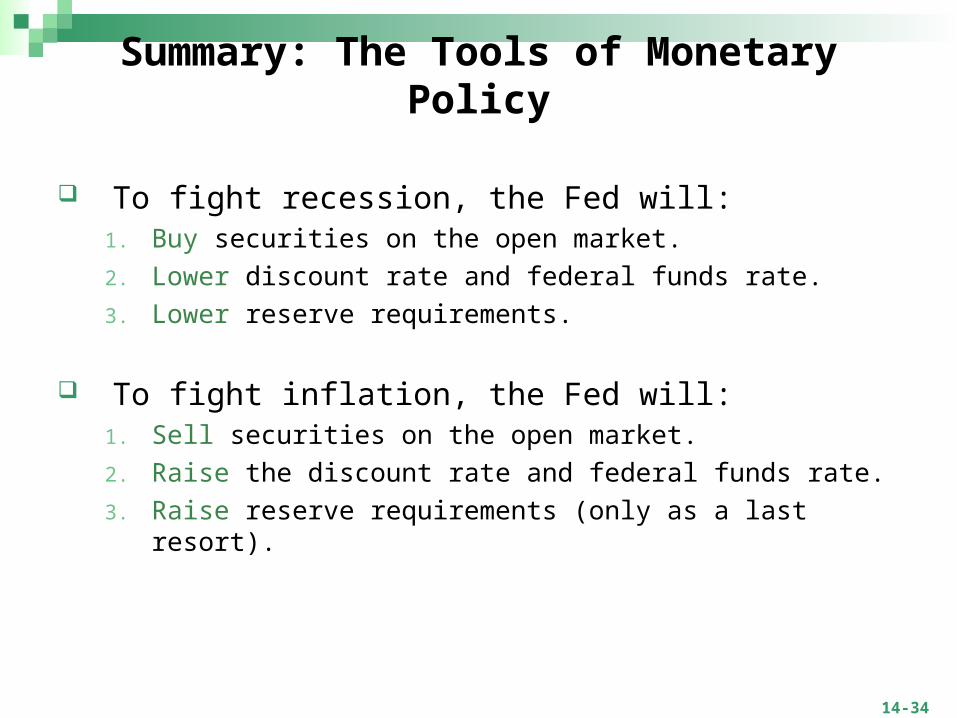

Summary: The Tools of Monetary Policy

To fight recession, the Fed will:1. Buy securities on the open market.

2. Lower discount rate and federal funds rate.

3. Lower reserve requirements.

To fight inflation, the Fed will:1. Sell securities on the open market.

2. Raise the discount rate and federal funds rate.

3. Raise reserve requirements (only as a last resort).

14-35

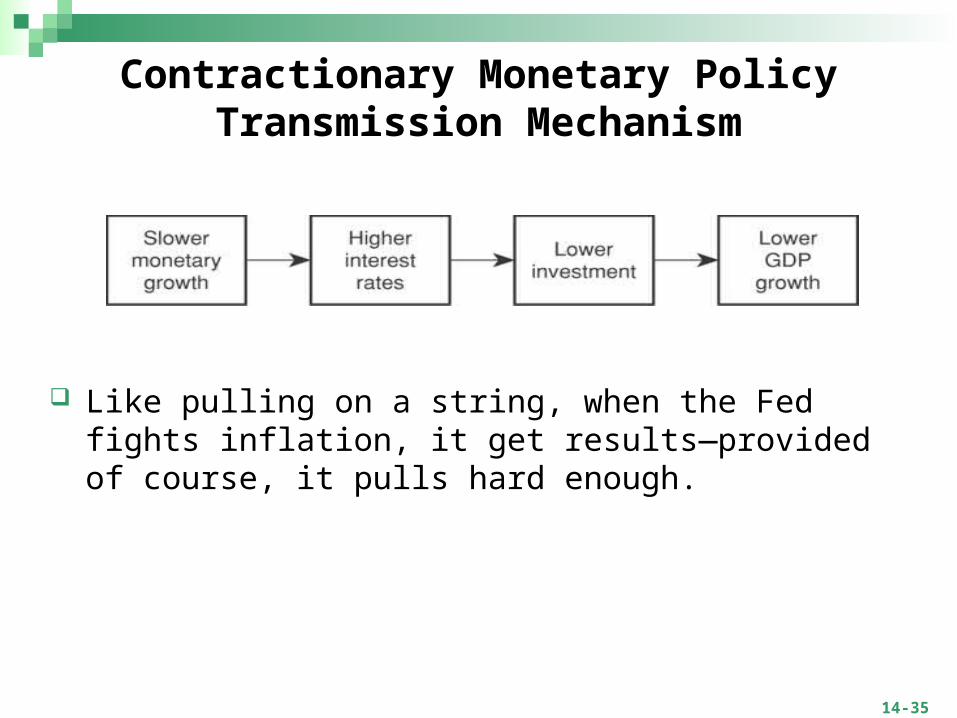

Contractionary Monetary Policy Transmission Mechanism

Like pulling on a string, when the Fed fights inflation, it get results—provided of course, it pulls hard enough.

14-36

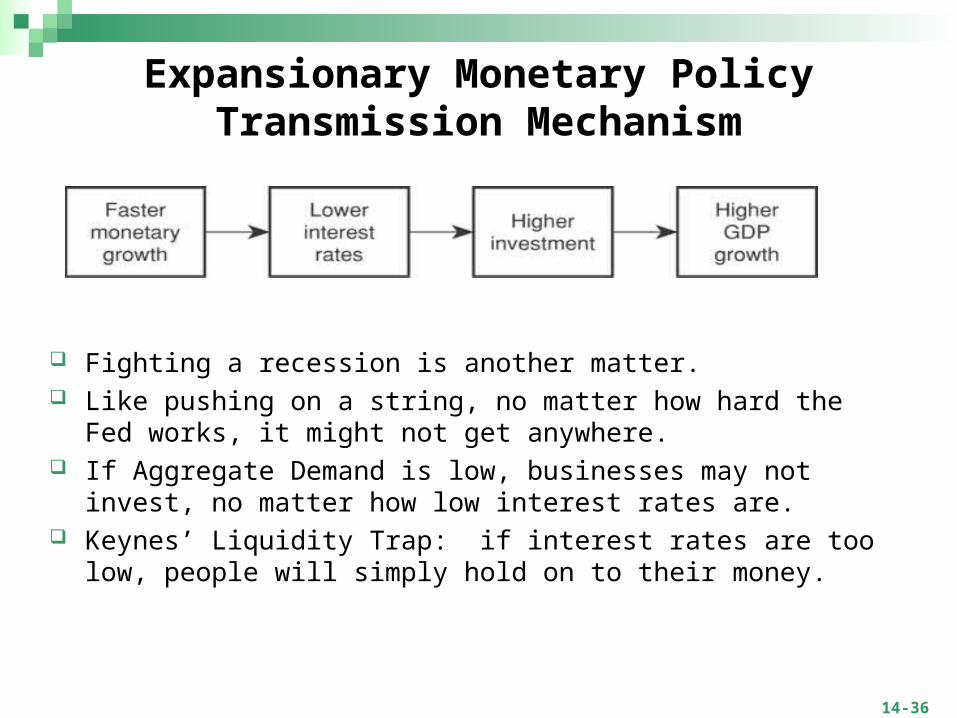

Expansionary Monetary Policy Transmission Mechanism

Fighting a recession is another matter. Like pushing on a string, no matter how hard the Fed works, it might

not get anywhere. If Aggregate Demand is low, businesses may not invest, no matter

how low interest rates are. Keynes’ Liquidity Trap: if interest rates are too low, people will

simply hold on to their money.

14-37

The Depository Institutions Deregulation and Monetary Control Act of 1980:

1. All depository institutions are now subject to the Fed’s legal reserve requirements.

2. All depository institutions are now legally authorized to issue checking deposits that may be interest bearing.

3. All depository institutions now enjoy all the advantages that only Federal Reserve member banks formerly enjoyed –including check clearing and borrowing from the Fed (discounting).

The Banking Act of 1999 allows banks, securities firms and insurances companies to merge and sell each other’s products.

• Repealed Glass-Steagall Act of 1933.• It was a major contributory factor to the financial crisis of

2008.

New Banking Regulations

14-38

Monetary Policy Lags

Monetary policy has the same three lags as fiscal policy:• Recognition lag• Decision lag• Impact lag

The first two lags may be shorter because of consolidated power of Fed’s Board of Governors.

But the impact lag may be longer.

14-39

Roots of The Housing Bubble After 9/11 attack and dot-com bubble burst, Fed dramatically

lowered interest rates to combat recession.• Lower interest rates contributed to new bubble in housing market.

Low interest rates made buying, flipping, and refinancing cheap.• Banking deregulation led to creating of new financial “instruments” for

sale, including mortgage securities. These “collateralized debt obligations” (CDOs) bundled mortgages into

a pool that earned income as mortgages were paid. Because mortgage lenders were selling mortgages to investment

banks for securities, they had less stake in whether borrowers could actually afford their mortgage.

Lenders assumed house values would keep rising, minimizing the risk since houses were collateral.

• Subprime mortgage market and speculative bubble boomed.

14-40

Financial Crisis of 2008

Subprime borrowers began to default on their mortgages.

• This led to an increase in the supply of houses, pushing down housing values.

• Borrowers found themselves “under water,” meaning their homes were worth less than their mortgages.

Banks, insurance companies, hedge funds, and other investors who owned large amounts of CDOs now owned paper of undetermined value (“toxic assets”).

• Many of the losers were “shadow banks,” financial intermediaries that were not regulated banks.

• Due to deregulation, there was little oversight as these institutions became indebted.

14-41

Financial Meltdown and the Great Recession

Two inter-related problems in Fall 2008: financial system meltdown and severe recession.

• The financial crisis began to affect “Main Street. ” • Lending of all kinds froze up contributing to a credit crisis. • Consumers spending fell as home values plunged. • Unemployment rose. • Millions of homeowners, not only subprime borrowers, faced

foreclosures.

14-42

Restoring the Financial System

TARP (Toxic Asset Relief Program) Bailout:• Congress and President Bush authorized U.S. Treasury to purchase

CDOs and other securities from banks and financial intermediaries. • TARP also authorized Treasury to purchase stock in these

companies. • Initially authorized $7 billion, in two $350 billion installments, with little

oversight.

Three criticisms:• Money not used to help homeowners avoid foreclosures.• Banks not required to use funds to increase lending.• No prohibition to pay huge executive bonuses.

Good news: Far less than $700 billion was spent and Treasury was paid back much of the funds.

14-43

Stopping Mortgage Foreclosures

By early 2009, 1 out of 11 homes was in foreclosure. • Typically such homes become run down or even vandalized.• This lowers property values of surrounding homes, driving down

housing prices.

February 2009, President Obama passed a $275 billion plan to help homeowners refinance their mortgages or avert foreclosure:

1. Provides incentives to lenders to change the terms of the loan to make them more affordable.

2. Help homeowners who were current in their payments refinance at lower interest rates.

3. Provide Fannie Mae and Freddie Mac with funds for mortgages.

14-44

Questions for Thought and Discussion

How is having foreclosed homes in your neighborhood an example of a negative externality?

What is the difference between the TARP Bailout and the Economic Stimulus Package described in the last chapter?

Why is there a “credit crisis?” How does the credit crisis affect consumers and businesses?

Should Congress have passed the TARP Bailout? • Why or why not?