Embed Size (px)

Citation preview

The Federal Estate Tax Return: Dealing with Portability and other Preparation Pointers

Philadelphia Bar Association’s Probate & Trust Section’s Tax Committee

May 21, 2013

Robert M. Maxwell, Esq. Direct: 215-419-6914

Director of Estate Tax, Managing Director Facsimilie: 215-640-3753

The Glenmede Trust Company, N.A.

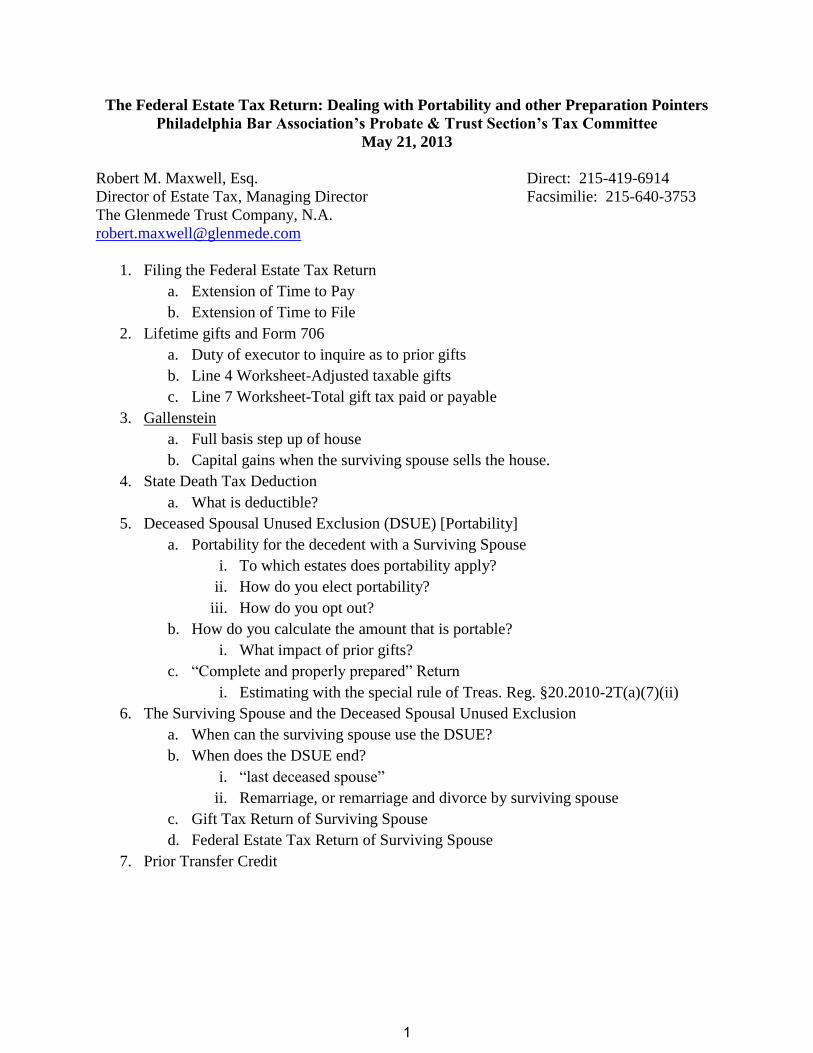

1. Filing the Federal Estate Tax Return

a. Extension of Time to Pay

b. Extension of Time to File

2. Lifetime gifts and Form 706

a. Duty of executor to inquire as to prior gifts

b. Line 4 Worksheet-Adjusted taxable gifts

c. Line 7 Worksheet-Total gift tax paid or payable

3. Gallenstein

a. Full basis step up of house

b. Capital gains when the surviving spouse sells the house.

4. State Death Tax Deduction

a. What is deductible?

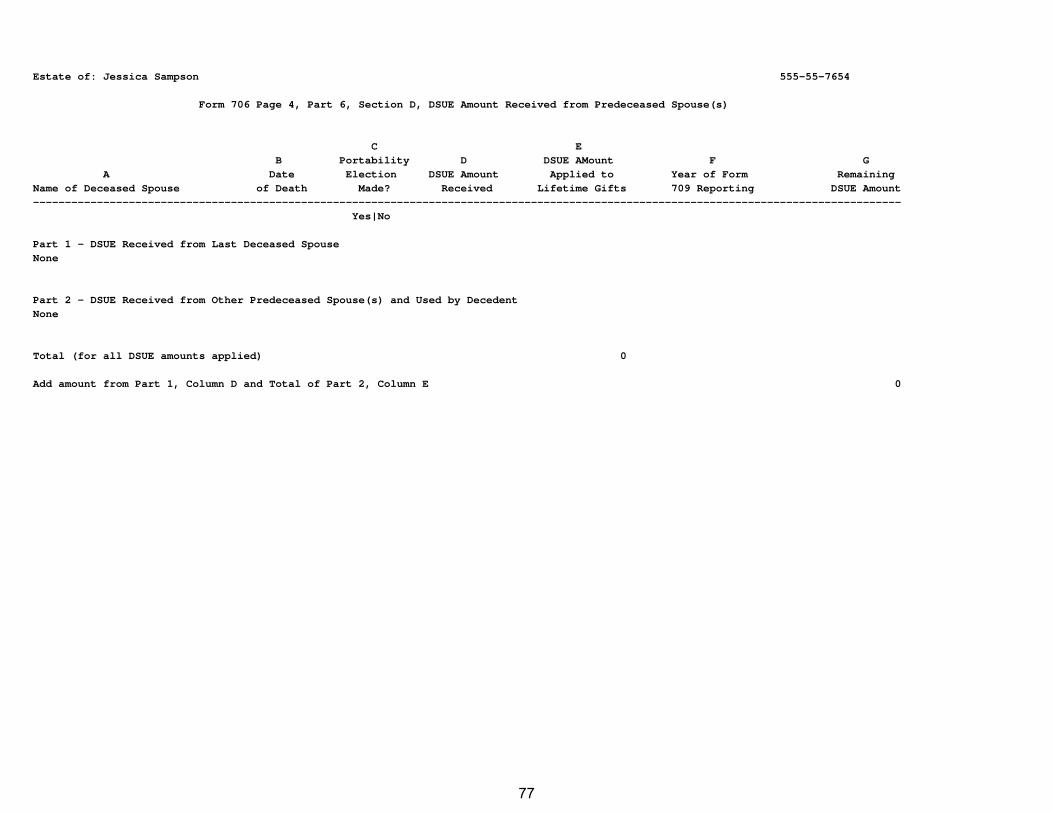

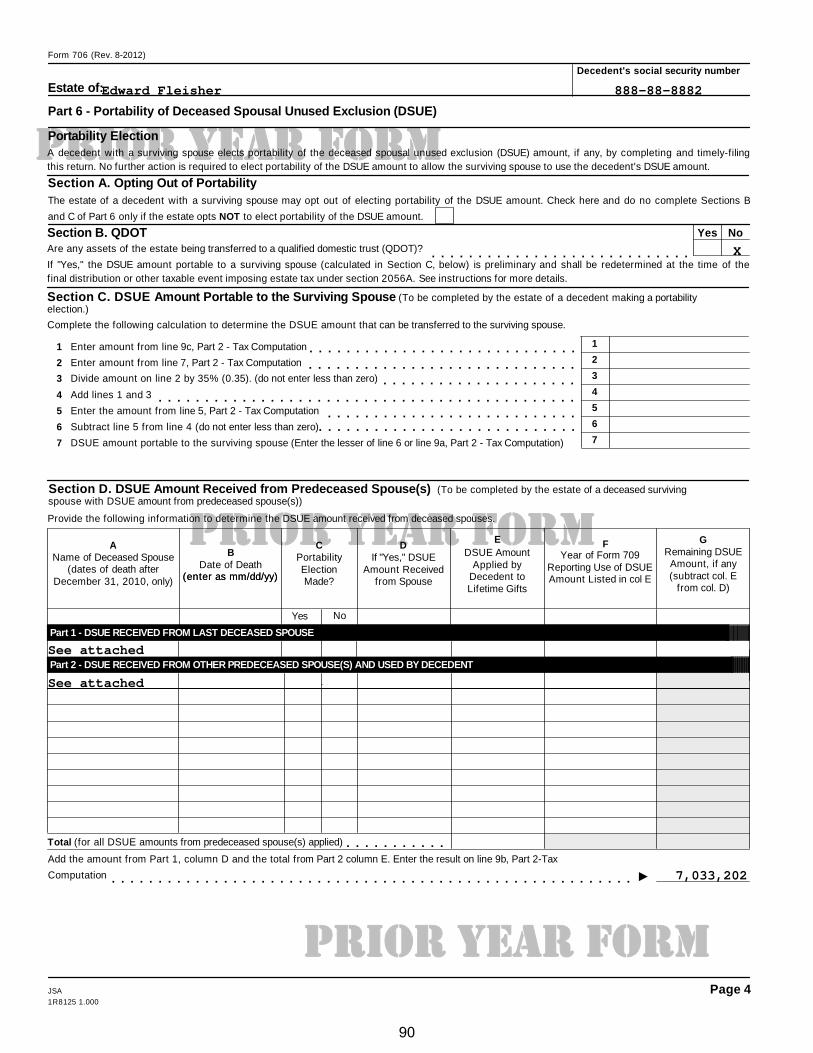

5. Deceased Spousal Unused Exclusion (DSUE) [Portability]

a. Portability for the decedent with a Surviving Spouse

i. To which estates does portability apply?

ii. How do you elect portability?

iii. How do you opt out?

b. How do you calculate the amount that is portable?

i. What impact of prior gifts?

c. “Complete and properly prepared” Return

i. Estimating with the special rule of Treas. Reg. §20.2010-2T(a)(7)(ii)

6. The Surviving Spouse and the Deceased Spousal Unused Exclusion

a. When can the surviving spouse use the DSUE?

b. When does the DSUE end?

i. “last deceased spouse”

ii. Remarriage, or remarriage and divorce by surviving spouse

c. Gift Tax Return of Surviving Spouse

d. Federal Estate Tax Return of Surviving Spouse

7. Prior Transfer Credit

1

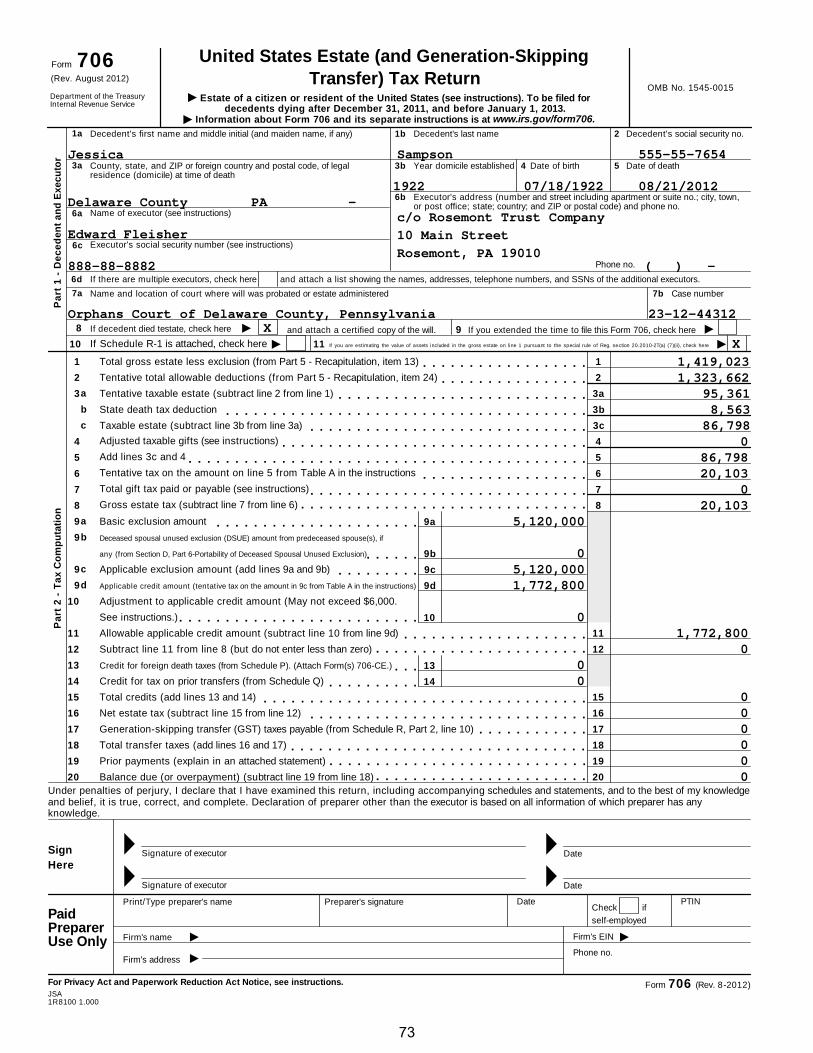

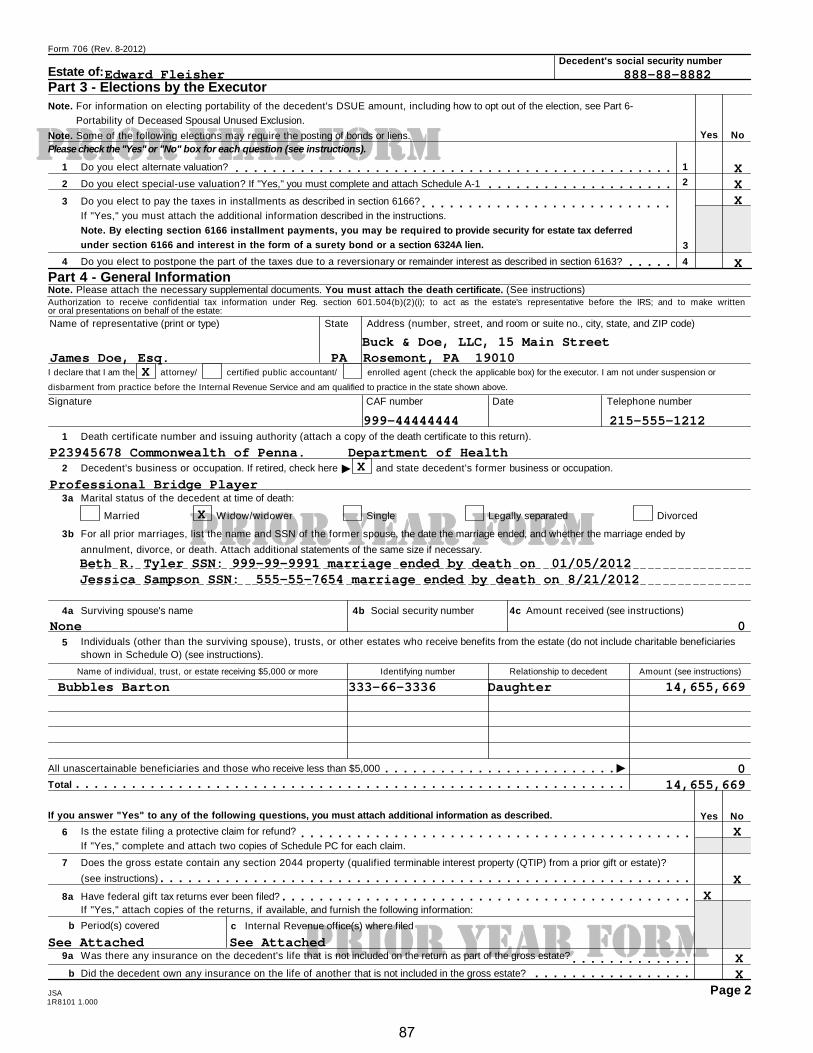

TIMELINE OF EVENTS – Beth R. Tyler, Edward Fleisher, Jessica Sampson

12/31/1969 Beth R. Tyler marries Edward Fleisher

01/01/1972 Beth and Edward buy 23 Lowry’s Lane, Rosemont, PA

-Beth pays all consideration

-House titled as tenants-by-the-entireties

02/02/2002 Beth gives $1,511,000 to Michelle Jackson (her sister)

-Annual gift tax exclusion is $11,000

-Gift tax due when lifetime taxable gifts exceed $1,000,000

04/15/2002 Beth files a 2002 Gift Tax Return

-Pays $210,000 of Gift Tax

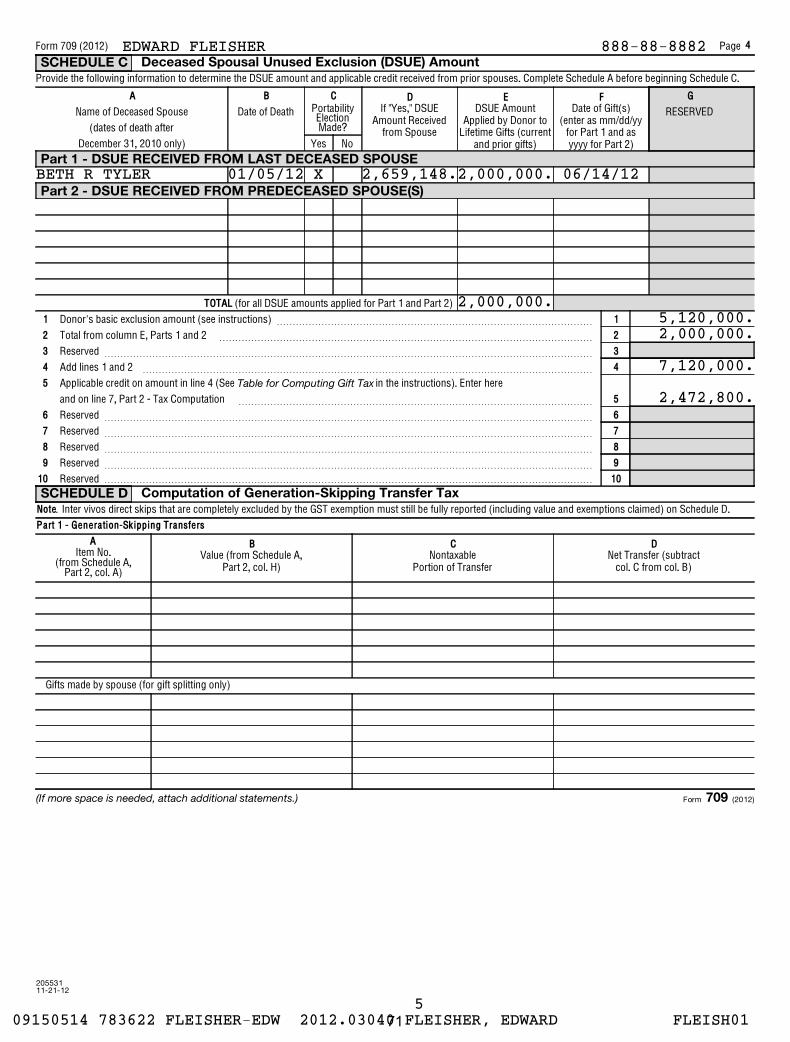

01/05/2012 Beth dies

-Surviving spouse: Edward Fleisher

-Executor: Edward Fleisher

-Federal Estate Tax Return due 10/05/2012 – extended to 4/05/2013

-PA Inheritance Tax Return due 10/05/2012 – extended to 4/05/2013

-“Gross estate” plus “adjusted taxable gifts” are less than $5,120,000

Federal filing requirement.

-Federal Estate Tax Return filed for portability.

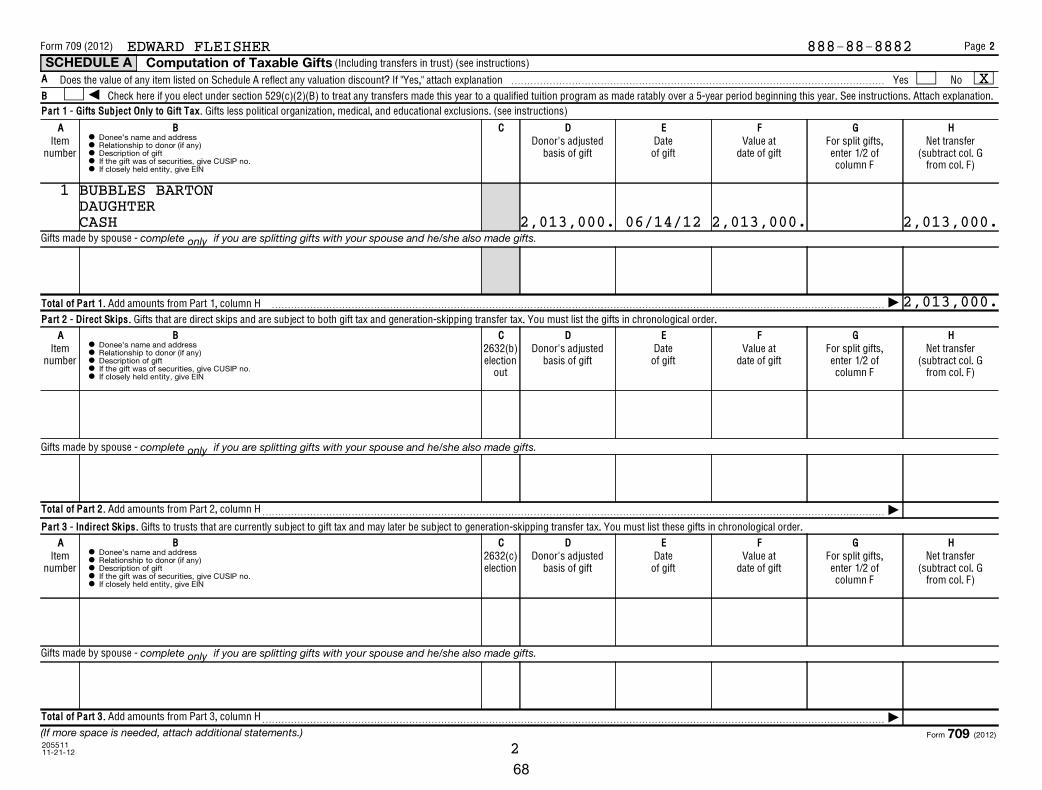

$2,659,148 is the Deceased Spousal Unused Exclusion (DSUE)

portable to Edward Fleisher for gift and estate tax purposes.

05/02/2012 Edward Fleisher marries Jessica Sampson

06/14/2012 Edward gives $2,013,000 to Bubbles Barton (his daughter)

-Annual gift tax exclusion is $13,000

8/21/2012 Jessica Sampson dies

-Federal Estate Tax Return due 5/21/2013

-PA Inheritance Tax Return due 5/21/2013

02/02/2013 Edward Fleisher dies

-Federal Estate Tax Return due 11/2/2013

-PA Inheritance Tax Return due 11/2/2013

2

I. THE FEDERAL ESTATE TAX RETURN-GENERAL FILING INFORMATION

A. WHICH ESTATES MUST FILE A RETURN

1. Gross estate requirement—The executor must file a federal estate tax

return if the gross estate, plus adjusted taxable gifts and specific exemption is

more than the amount shown below:

a) 2011 deaths-$5,000,000

b) 2012 deaths-$5,120,000

c) 2013 deaths-$5,250,000 (top rate increases to 40%)

2. Portability election—The executor must a file a federal estate tax return

(regardless of the size of the gross estate), if the executor wants to elect to permit

the decedent’s surviving spouse to use the decedent’s unused exclusion amount.

a) The 2012 Tax Relief Act (passed January 1, 2013) made the

portability provisions permanent. (Under the 2010 Tax Relief Act, the

portability provisions only applied to 2011 and 2012 decedents.).

3. Unified Credit Against Estate Tax

a) A credit of the applicable credit amount shall be allowed to the

estate of every decedent against the federal estate tax. I.R.C. § 2010(a)

b) The “applicable credit amount” is the amount of the tentative tax

which would be determined on the “applicable exclusion amount”. I.R.C.

§ 2010(c)(1)

c) The “applicable exclusion amount” is the sum of:

(1) The “basic exclusion amount” ($5,000,000 for 2011 deaths;

$5,120,000 for 2012 deaths, $5,250,000 for 2013 deaths), AND

(2) In the case of a “surviving spouse”, the “deceased spousal

unused exclusion amount”. I.R.C. §2010(c)(2)

(3) The “deceased spousal unused exclusion amount” is the

lesser of:

(a) The “basic exclusion amount” ($5,000,000 for 2011

deaths; $5,120,000 for 2012 deaths; $5,250,000 for 2013

deaths), OR

3

(b) The excess of:

(i) The applicable exclusion amount of the last

such deceased spouse of such surviving spouse,

over

(ii) The amount with respect to which the

tentative tax is determined on the estate of such

deceased spouse. I.R.C. §2010(c)(4)

d) Prior Gift Tax Paid-For purposes of the Deceased Spousal Unused

Exclusion Amount calculation, the amount of adjusted taxable gifts is

reduced by the amount of gifts on which gift tax was paid. Treas. Reg.

§20.2010-2T(c)(2)

4. Portability Election

a) A “deceased spousal unused exclusion amount” [“DSUE”] may

only be taken into account by a surviving spouse if the executor of the

deceased spouse:

(1) Timely files (including extensions) a federal estate tax

return on which the amount is computed; and

(2) Makes an election on the federal estate tax return. I.R.C.

§2010(c)(5)(A)

b) The election is irrevocable. I.R.C. §2010(c)(5)(A)

(1) A portability election can be superseded by a subsequently

filed return, provided that return is filed by the due date of the

return. Treas. Reg. §20.2010-2T(a)(4)

c) Deemed election—Upon timely filing of a complete and properly-

prepared estate tax return, the executor will have elected portability of the

DSUE amount unless the executor chooses not to elect portability. Treas.

Reg. §20.2010-2T(a)(2)

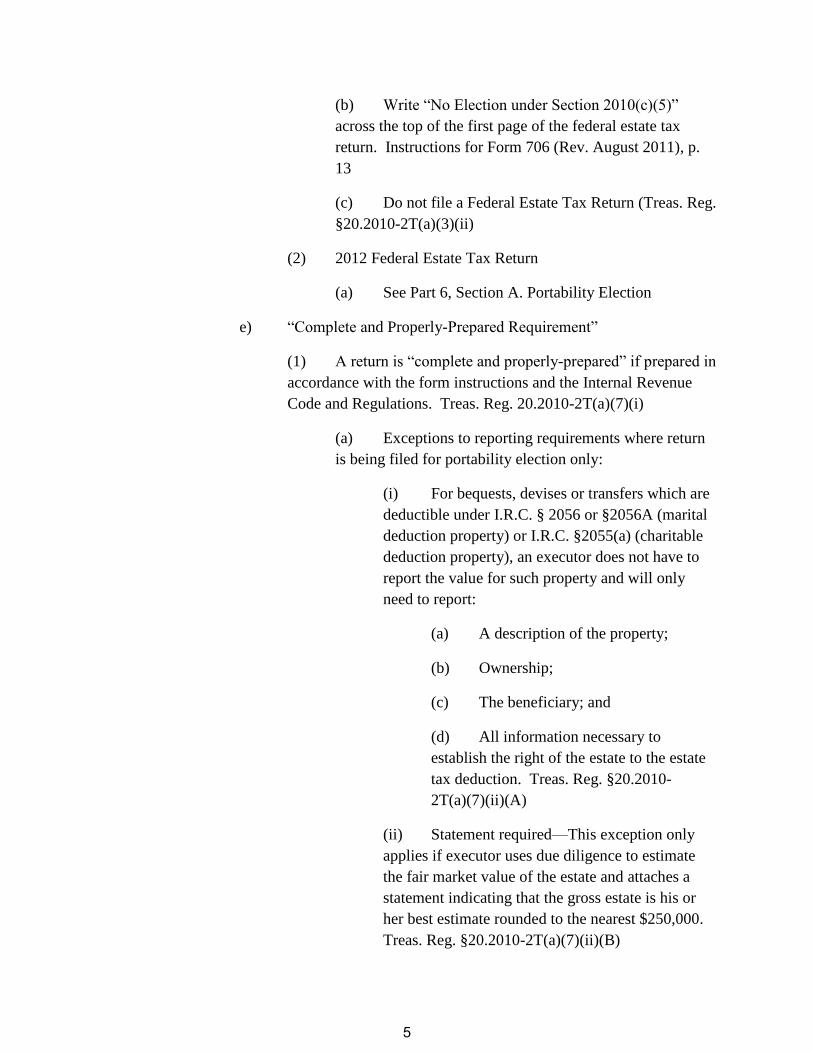

d) Ways to not make the Portability Election

(1) 2011 Federal Estate Tax Form

(a) Statement-Attach a statement to the return

indicating that the estate is not making the election under

2010(c)(5); Treas. Reg. §20.2010-2T(a)(3)(i)

4

(b) Write “No Election under Section 2010(c)(5)”

across the top of the first page of the federal estate tax

return. Instructions for Form 706 (Rev. August 2011), p.

13

(c) Do not file a Federal Estate Tax Return (Treas. Reg.

§20.2010-2T(a)(3)(ii)

(2) 2012 Federal Estate Tax Return

(a) See Part 6, Section A. Portability Election

e) “Complete and Properly-Prepared Requirement”

(1) A return is “complete and properly-prepared” if prepared in

accordance with the form instructions and the Internal Revenue

Code and Regulations. Treas. Reg. 20.2010-2T(a)(7)(i)

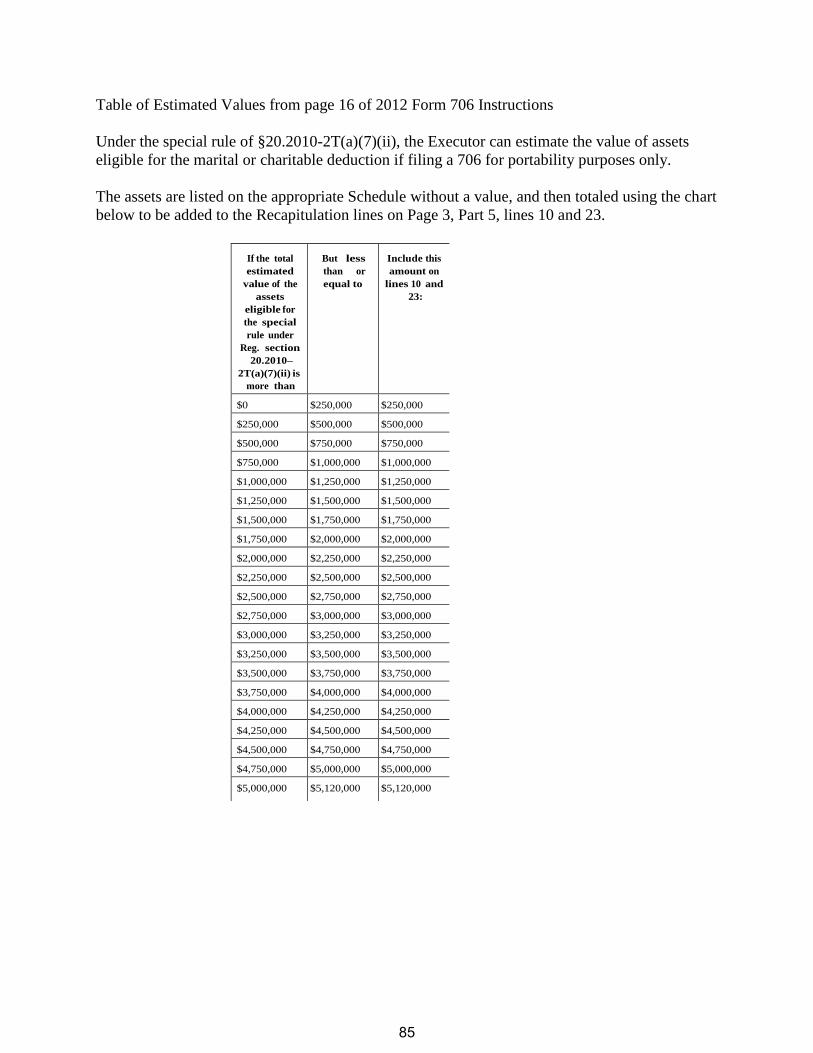

(a) Exceptions to reporting requirements where return

is being filed for portability election only:

(i) For bequests, devises or transfers which are

deductible under I.R.C. § 2056 or §2056A (marital

deduction property) or I.R.C. §2055(a) (charitable

deduction property), an executor does not have to

report the value for such property and will only

need to report:

(a) A description of the property;

(b) Ownership;

(c) The beneficiary; and

(d) All information necessary to

establish the right of the estate to the estate

tax deduction. Treas. Reg. §20.2010-

2T(a)(7)(ii)(A)

(ii) Statement required—This exception only

applies if executor uses due diligence to estimate

the fair market value of the estate and attaches a

statement indicating that the gross estate is his or

her best estimate rounded to the nearest $250,000.

Treas. Reg. §20.2010-2T(a)(7)(ii)(B)

5

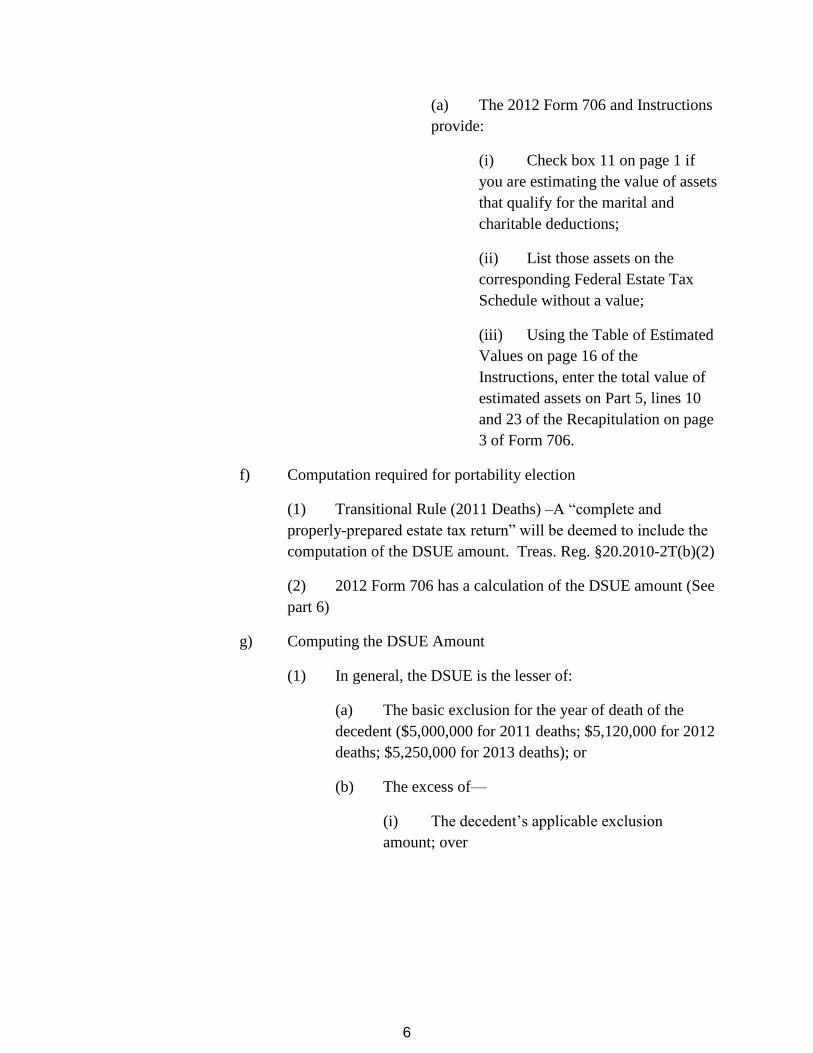

(a) The 2012 Form 706 and Instructions

provide:

(i) Check box 11 on page 1 if

you are estimating the value of assets

that qualify for the marital and

charitable deductions;

(ii) List those assets on the

corresponding Federal Estate Tax

Schedule without a value;

(iii) Using the Table of Estimated

Values on page 16 of the

Instructions, enter the total value of

estimated assets on Part 5, lines 10

and 23 of the Recapitulation on page

3 of Form 706.

f) Computation required for portability election

(1) Transitional Rule (2011 Deaths) –A “complete and

properly-prepared estate tax return” will be deemed to include the

computation of the DSUE amount. Treas. Reg. §20.2010-2T(b)(2)

(2) 2012 Form 706 has a calculation of the DSUE amount (See

part 6)

g) Computing the DSUE Amount

(1) In general, the DSUE is the lesser of:

(a) The basic exclusion for the year of death of the

decedent ($5,000,000 for 2011 deaths; $5,120,000 for 2012

deaths; $5,250,000 for 2013 deaths); or

(b) The excess of—

(i) The decedent’s applicable exclusion

amount; over

6

(ii) The sum of the amount of the taxable estate

and the amount of the adjusted taxable gifts of the

decedent, which is the amount on which the

tentative tax on the decedent’s estate is determined.

Treas. Reg. §20.2010-2T(c)(1)

h) Use of DSUE by surviving spouse

(1) The DSUE of the “last deceased spouse” can be used by the

surviving spouse for transfers made after the decedents death (for

gifts and on the surviving spouse’s federal estate tax return)

provided the portability election is made. Treas. Reg §20.2010-

3T(c) and Treas. Reg. §20.2505-2T(d)

(2) If a surviving spouse makes a taxable gift, the DSUE is

applied first before the surviving spouse’s own basic exclusion

amount. Treas. Reg. §25.2505-2T(b).

(3) The term “last deceased spouse” means the most recently

deceased individual who, at that individual’s death after December

31, 2010, was married to the surviving spouse. Treas. Reg.

§25.2010-1T(d)(5)

(4) If the surviving spouse remarries, or remarries and then

gets divorced, the identity of the last deceased spouse remains

unchanged for gifts made by the surviving spouse, or on the

surviving spouse’s federal estate tax return. Treas. Reg. §25.2010-

3T(a)(3); Treas. Reg. §25.2505-2T(a)(3).

(5) With multiple deceased spouses, the special rule is that the

DSUE amount available is the DSUE of the surviving spouse’s last

deceased spouse and the DSUE amount of each other deceased

spouse that was applied to taxable gifts made by the surviving

spouse. Treas. Reg. §25.2010-3T(b) and Treas. Reg. §25.2505-

2T(c)

7

B. WHEN TO FILE A FEDERAL ESTATE TAX RETURN

1. The Federal Estate Tax Return is due within nine months of the decedent’s

death. I.R.C. §6075(a)

2. Extensions in general

a) File Form 4768, Application for Extension of Time to File a

Return and/or Pay U.S. Estate (and Generation-Skipping Transfer) Taxes

3. Extension of Time to File Form 706 (I.R.C. §6081)

a) An automatic 6-month extension is allowed if you file form 4768

and check the box.

4. Extension of Time to Pay (Section §6161)

a) Extension may not exceed 12 months.

b) Attach a written statement showing why it is impossible or

impractical to pay the full amount of the tax.

(1) Examples of reasonable cause from Treas. Reg. §20.6161-1

(a) Assets needed to pay the tax are located in several

jurisdictions and not immediately subject to control of

executor.

(b) Estate is substantially comprised of rights to receive

future payments such as annuities, receivables or royalties.

(c) Estate consists of a claim which cannot be collected

without litigation.

c) Even in an estate where you estimate no federal estate tax will be

due, request an extension to pay in case you decide to pay estate tax when

the final return is completed.

5. Reasons to extend a federal estate tax return.

a) Executor is missing information on assets or deductions.

b) Executor is missing a valuation of an asset.

c) A substantial asset is listed for sale (such as a house).

8

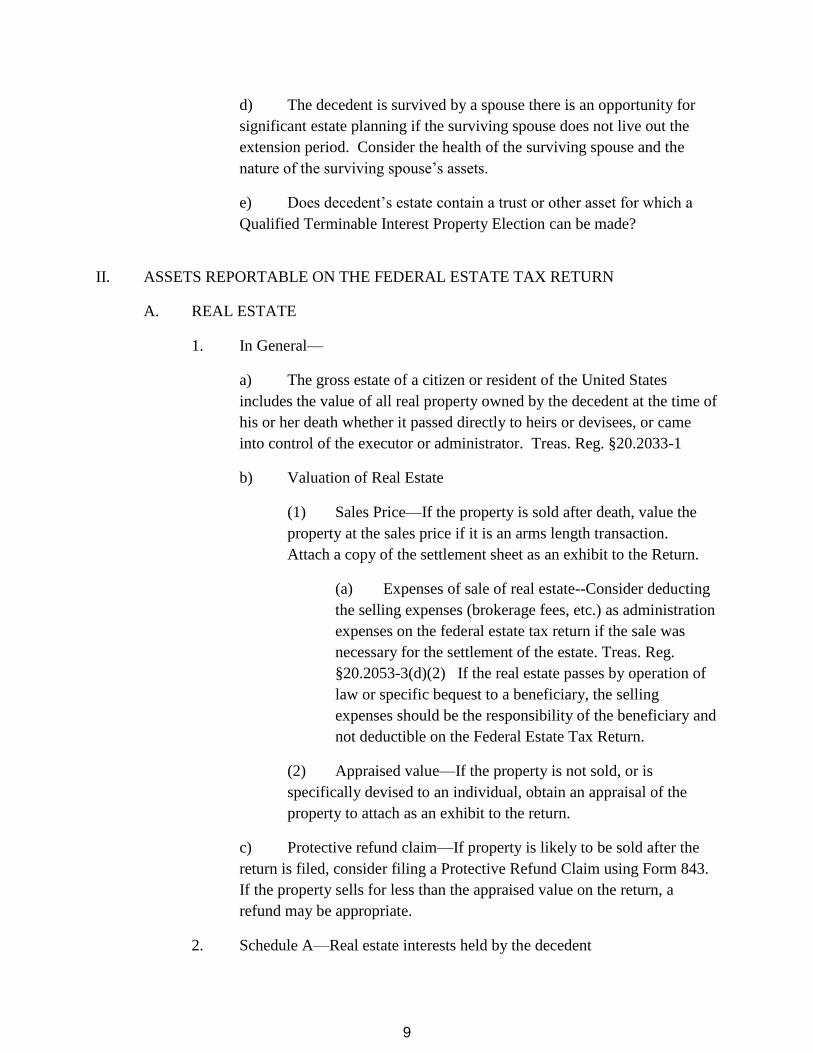

d) The decedent is survived by a spouse there is an opportunity for

significant estate planning if the surviving spouse does not live out the

extension period. Consider the health of the surviving spouse and the

nature of the surviving spouse’s assets.

e) Does decedent’s estate contain a trust or other asset for which a

Qualified Terminable Interest Property Election can be made?

II. ASSETS REPORTABLE ON THE FEDERAL ESTATE TAX RETURN

A. REAL ESTATE

1. In General—

a) The gross estate of a citizen or resident of the United States

includes the value of all real property owned by the decedent at the time of

his or her death whether it passed directly to heirs or devisees, or came

into control of the executor or administrator. Treas. Reg. §20.2033-1

b) Valuation of Real Estate

(1) Sales Price—If the property is sold after death, value the

property at the sales price if it is an arms length transaction.

Attach a copy of the settlement sheet as an exhibit to the Return.

(a) Expenses of sale of real estate--Consider deducting

the selling expenses (brokerage fees, etc.) as administration

expenses on the federal estate tax return if the sale was

necessary for the settlement of the estate. Treas. Reg.

§20.2053-3(d)(2) If the real estate passes by operation of

law or specific bequest to a beneficiary, the selling

expenses should be the responsibility of the beneficiary and

not deductible on the Federal Estate Tax Return.

(2) Appraised value—If the property is not sold, or is

specifically devised to an individual, obtain an appraisal of the

property to attach as an exhibit to the return.

c) Protective refund claim—If property is likely to be sold after the

return is filed, consider filing a Protective Refund Claim using Form 843.

If the property sells for less than the appraised value on the return, a

refund may be appropriate.

2. Schedule A—Real estate interests held by the decedent

9

a) Schedule A Items include:

(1) Land, improvements and fixtures held solely in the name of

the decedent.

(2) Condominium interests

(3) The decedent’s tenants in common interest in real property.

(4) Real property that the decedent contracted to purchase

before his or her death. (Deduct any unpaid purchase monies on

Schedule K as a debt).

b) Discounts—If the decedent owned an undivided fractional interest

in property, the appraiser may give a discount attributable to the lower

price a willing buyer would pay to purchase a fractional interest in real

estate. See Estate of Bonner Sr. v. U.S., 84 F3d 196 (5th

Cir. June 4, 1996)

in which the court held that the estate was entitled to a discount of

fractional interest discount in real estate and a boat.

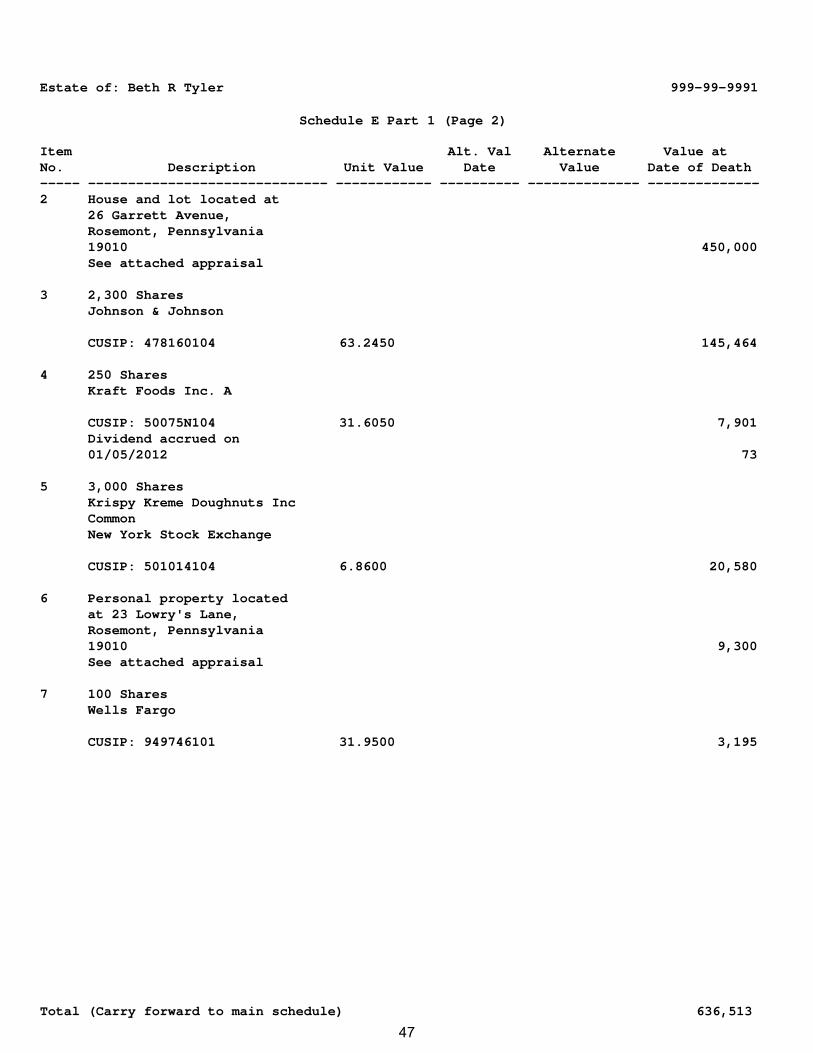

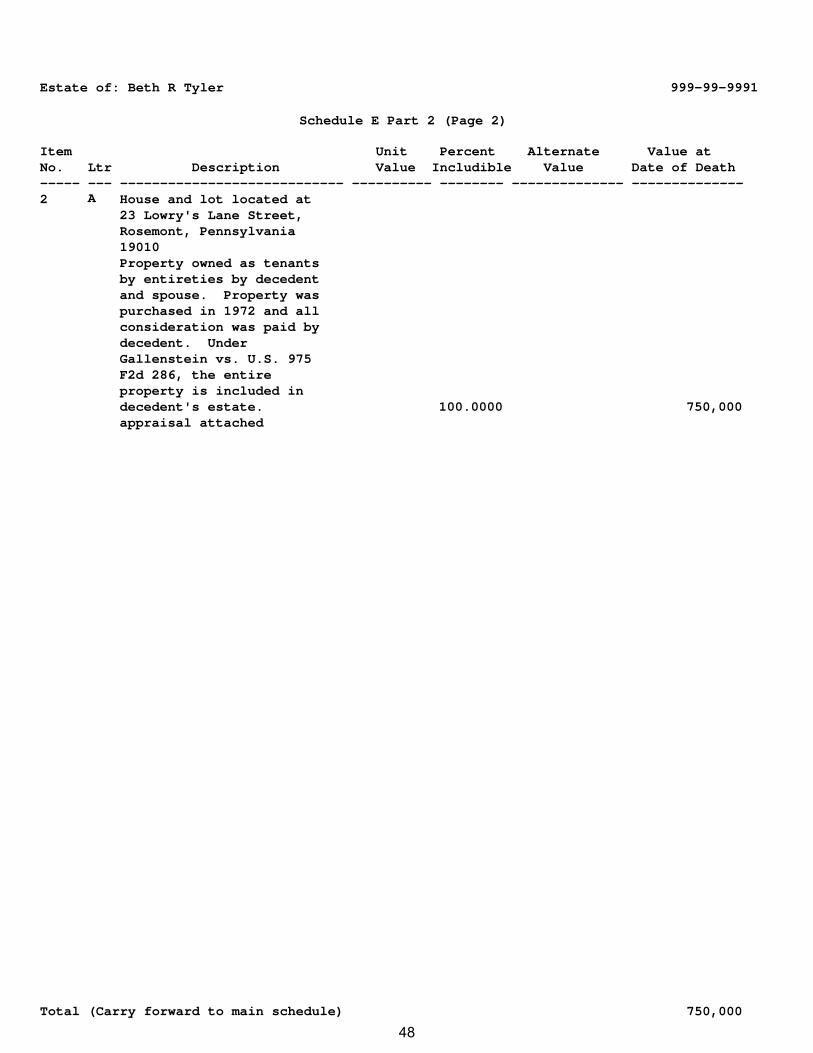

3. Schedule E – Jointly held real estate

a) Property held by husband as wife as tenants by the entireties

property, or joint tenants with rights of survivorship is considered a

“qualified joint interest” under I.R.C. §2040(b)(2)

b) The full value of such property is listed on Schedule E, Part 1.

c) Only one half of the full value of the property is included in the

decedent’s gross estate. I.R.C. §2042(b)(1)

(1) Subsequent sale of real estate by surviving spouse: The

basis of the real estate will only receive one-half step up in basis.

(a) EXAMPLE: Husband and wife buy real estate in

1980 for $30,000. Husband dies and the date of death

value of the entire property is $450,000. Surviving

spouse’s basis in real estate is $15,000 (one-half of original

purchase price) plus $225,000 (one-half entitled to step up

in basis due to death). Total basis is $240,000. If the

spouse later sells the property for $600,000, the spouse’s

gain is $360,000 ($600,000 selling price less basis of

$240,000).

10

(i) An individual can exclude $250,000 of gain

from sale of principal residence under I.R.C.

§121(b)(1) if certain requirements are met.

(ii) Husband and wife can exclude $500,000 of

gain from sale of principal residence under I.R.C.

§121(b)(2) if certain requirements are met.

(iii) Surviving spouse can exclude $500,000 of

gain if house is sold within two years of death of

first spouse and certain requirements are met.

I.R.C. §121(b)(4)

d) EXCEPTION: Step up in basis/Gallenstein Rule—If husband and

wife bought real estate prior to 1977 as entireties or survivorship property,

and one spouse contributed all consideration to the property, a step up of

the entire value of the real estate may be allowed when the contributing

spouse dies. See Gallenstein v. U.S., 975 F2d 286 (6th

Cir. 09/16/1992)

4. Real Estate held in Partnerships, or Sole Proprietorships

a) Report as part of the value of the partnership or proprietorship on

Schedule F.

5. Real Estate held in Trusts

a) Report as part of the Trust valuation if the Trust is reportable on

Schedule G.

b) If the real estate is held in a trust over which the Decedent had a

power of appointment, report on Schedule H.

B. STOCKS AND BONDS

1. In general—

2. Publicly traded stocks and bonds:

a) For publicly traded stocks and bonds, the fair market value is the

mean between the highest and lowest selling prices quoted on the

valuation date. Treas. Reg. §20.2031-2

(1) For stocks provide

(a) Number of shares;

11

(b) Whether common or preferred;

(c) Issue;

(d) Par value where needed for identification;

(e) Price per share – the price per share is the mean

value of the high and low on the date of death;

(f) Exact name of corporation;

(g) Principal exchange upon which sold if listed on an

exchange; and

(h) Nine-digit CUSIP number;

(2) Dividends: List dividends that have not been collected at

death and are payable to the decedent or the estate because the

decedent was a stockholder of record on the date of death.

b) For bonds provide:

(1) Quantity and denomination;

(2) Name of obligor;

(3) Date of maturity;

(4) Interest rate;

(5) Interest due date;

(6) Principal exchange, if listed on an exchange, and

(7) Nine-digit CUSIP number.

(8) Interest: Include accrued to date of death.

3. For closely held stock, attach the following to the return:

a) Copies of complete financial and other data used to determine

value, including balance sheets and statements of the net earnings or

operating results and dividends paid for each of the 5 years immediately

before the valuation date. (Tax returns).

b) Valuation from appraiser or methodology used to calculate value.

4. Reporting of stocks and bonds

12

a) If stocks and bonds are held in the decedent’s name alone, report

on Schedule B.

b) If stocks and bonds are held as tenants by the entireties or with

rights of survivorship by husband and wife, report on Schedule E, Part 1—

Qualified Joint Interests—Interest held by the Decedent and His or Her

spouse as the Only Joint Tenants.

c) If stocks and bonds are held jointly with someone other than a

surviving spouse, report on Schedule E, Part 2—All Other Joint Interests.

d) If stocks and bonds are held in a partnership, report as part of the

partnership valuation on Schedule F.

e) If stocks and bonds are held as part of a trust, report as part of the

trust valuation on Schedule F (Other Miscellaneous Property), Schedule G

(Transfers During Decedent’s life), or Schedule H (Power of

Appointment).

f) If stocks and bonds are held in a Payable on Death Account or a

Transfer on Death Account or form, list on Schedule G.

g) If stocks and bonds are held as part of an Individual Retirement

Account, report as part of the IRA valuation on Schedule I-Annuities.

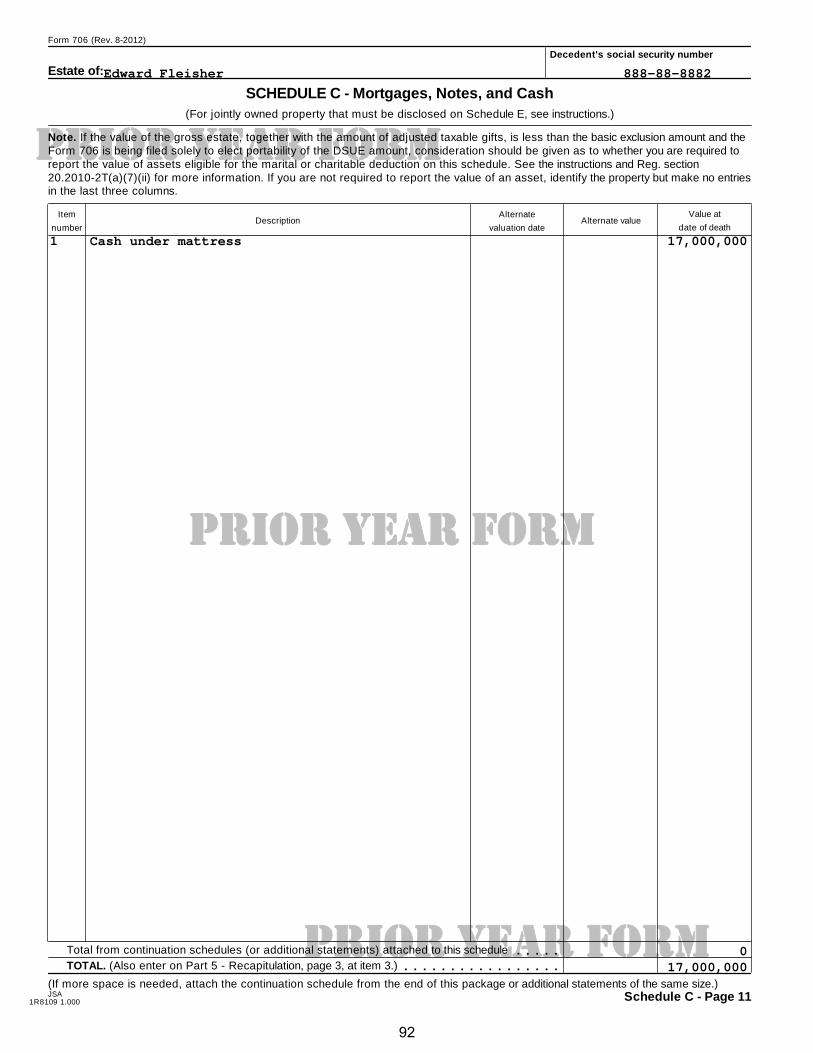

C. MORTGAGES, NOTES, AND CASH

1. Mortgages payable to the decedent at the time of death:

a) For mortgages and notes, provide the following:

(1) Face value,

(2) Unpaid balance,

(3) Date of mortgage or note,

(4) Name of maker,

(5) Property mortgaged,

(6) Date of maturity,

(7) Interest rate, and

(8) Interest date.

13

b) For contracts by the decedent to sell land report:

(1) Name of purchaser,

(2) Contract date,

(3) Property description,

(4) Sale price,

(5) Initial payment,

(6) Amounts of installment payment,

(7) Unpaid balance of principal, and

(8) Interest rate.

c) For miscellaneous cash items, report:

(1) Insurance refunds,

(2) Subscription refunds,

(3) Cash, coins.

d) For bank and money market accounts, report:

(1) Name and address of each financial organization,

(2) Amount in each account,

(3) Account number,

(4) Nature of account—checking, savings, time deposit, etc.,

and

(5) Unpaid interest accrued from date of last interest payment

to the date of death.

(6) Bank date of death letters—attach bank date of death

balance letters to return as an exhibit.

(7) Jointly held accounts held between decedent and non-

spouse

14

(a) The full value of jointly owned property held with

anyone other than the spouse must be included on Schedule

E, Part 2.—All Other Joint Interests, unless:

(i) the executor can show that a part of the

property originally belonged to the other tenant and

was never received by the decedent for less than

adequate and full consideration, or

(ii) unless the executor can demonstrate that any

of the property was acquired with consideration

originally belonging to the surviving joint tenant.

I.R.C. §2040(a)

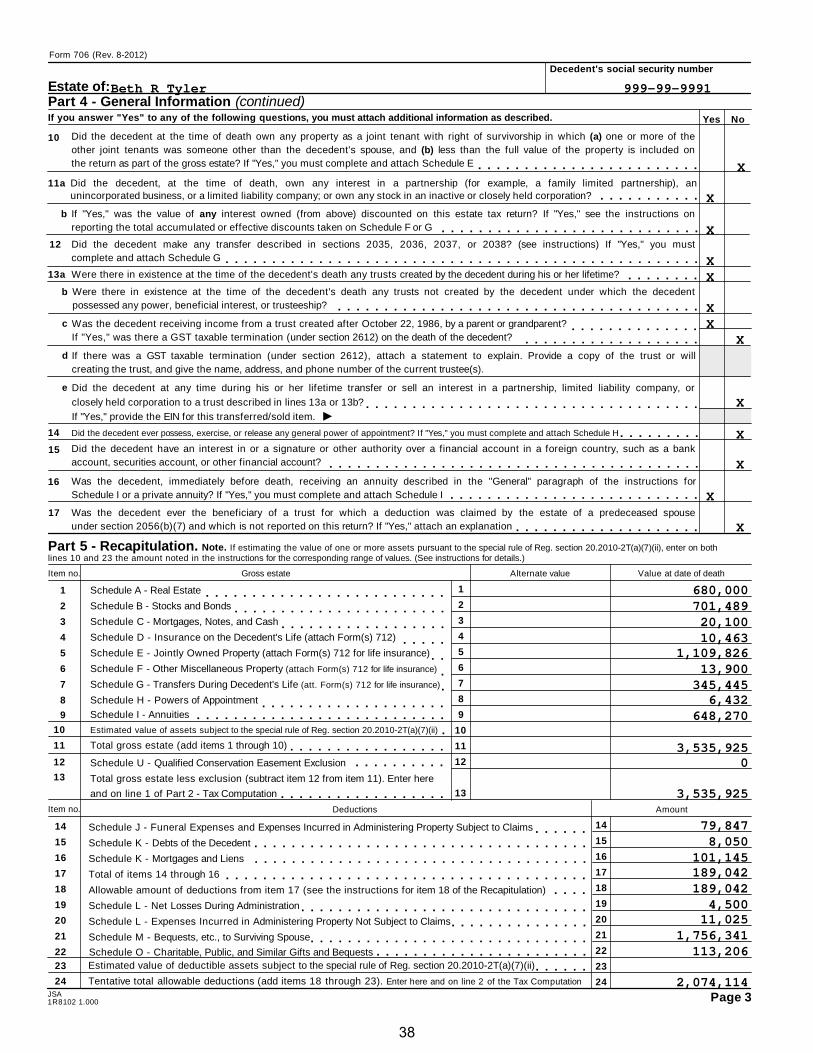

(b) Note Question 10 on Part 4, Page 3 of Form 706:

Did the decedent at the time of death own any property as a

joint tenant with right of survivorship in which (a) one or

more of the other joint tenants was someone other than the

decedent’s spouse, and (b) less than the full value of the

property is included on the return as part of the gross

estate?

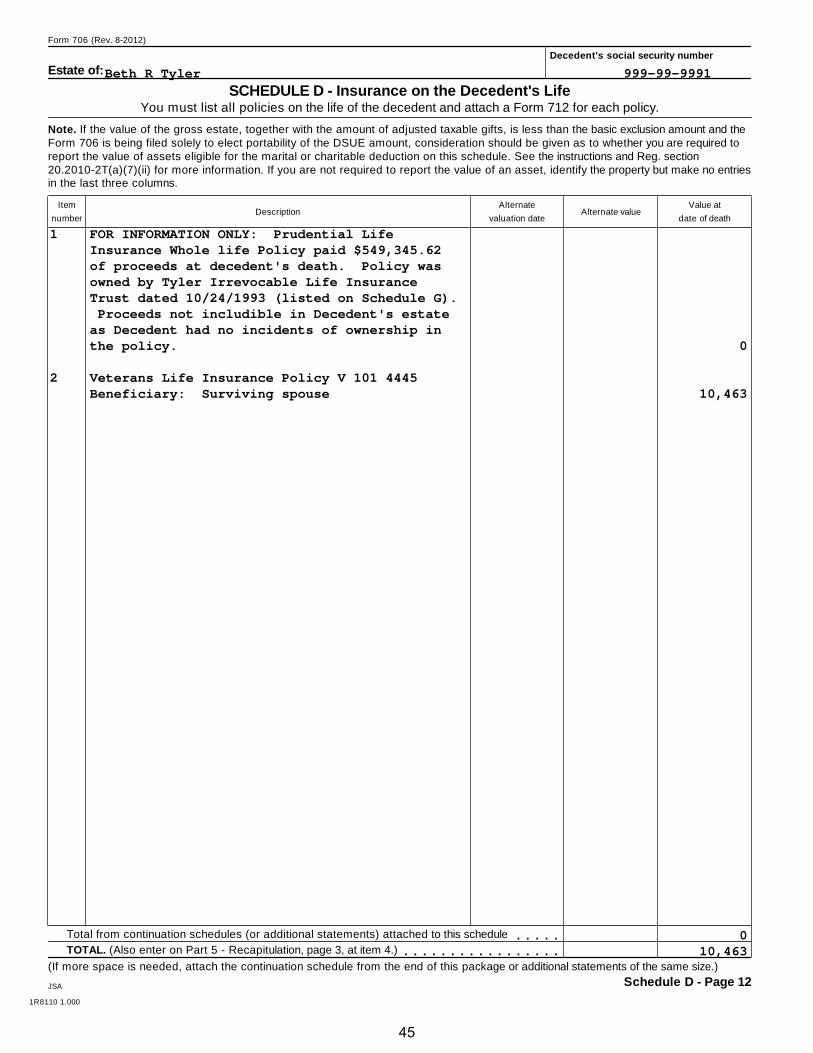

D. LIFE INSURANCE REPORTABLE ON SCHEDULE D:

1. Proceeds of life insurance in which the decedent had any “incidents of

ownership” whether payable to the estate or other beneficiaries are included on

Schedule D. I.R.C. §2042

2. Incidents of ownership

a) The right of the insured or estate to its economic benefits;

b) The power to change the beneficiary;

c) The power to surrender or cancel the policy;

d) The power to assign the policy or revoke an assignment;

e) The power to pledge the policy for a loan;

f) The power to obtain form the insurer a loan against the surrender

value of the policy; and

g) A reversionary interest if the value of the reversionary interest was

more than 5% of the value of the policy.

15

3. Describe the policy by listing:

a) The name of the insurance company, and

b) The number of the policy.

4. Report the proceeds paid in one lump sum and attach Form 712 obtained

from the insurance company.

5. Life Insurance on the Decedent’s life which decedent had no “incidents of

ownership” should be listed “FOR INFORMATION ONLY” on Schedule D.

Examples would be life insurance owned by a Life Insurance Trust or a Business.

a) Note question 9a on Part 4, Page 2 of Form 706: Was there any

insurance on the decedent’s life that is not included on the return as part of

the gross estate?

6. Life Insurance owned by the Decedent on others should be listed on

Schedule F.

a) Form 712 should be attached to the return.

b) Note question 9b on Part 4, Page 2 of Form 706: Did the decedent

own any insurance on the life of another that is not included in the gross

estate?

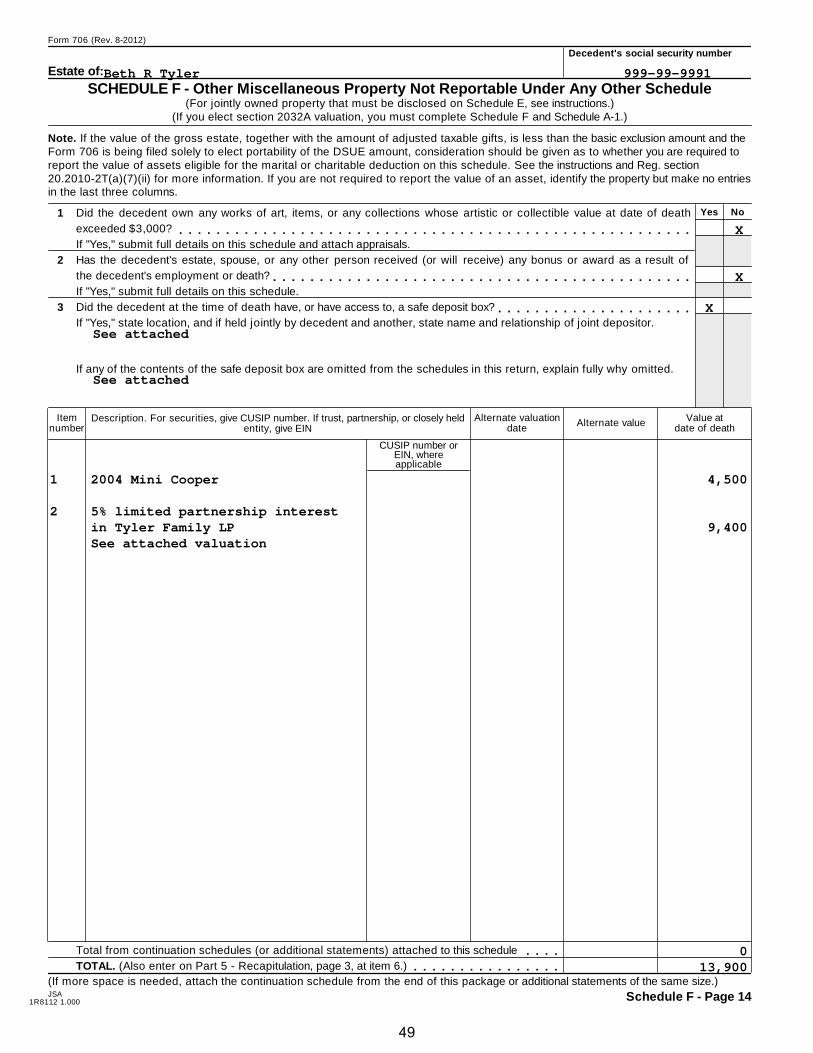

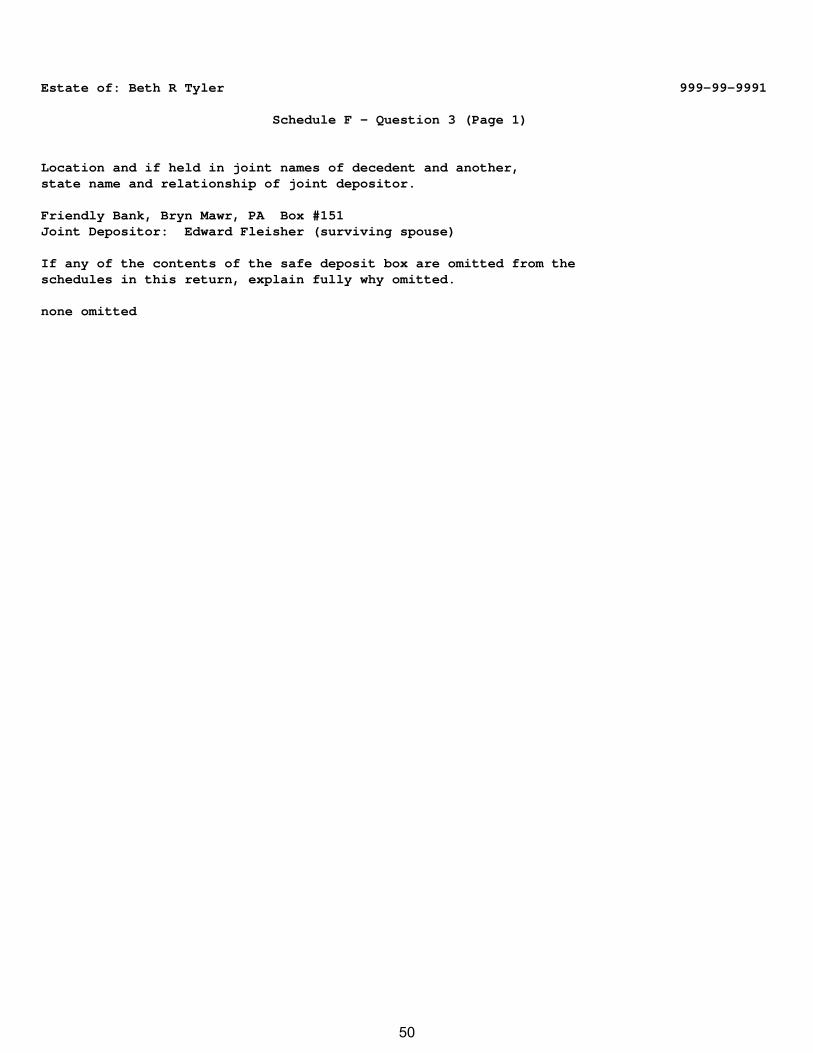

E. MISCELLANEOUS PROPERTY REPORTABLE ON SCHEDULE F

1. Business interests and partnerships

a) Provide statement of assets and liabilities for the valuation date and

for the 5 years before the valuation date.

b) Attach statements of net earnings for the same 5 years (tax returns

of partnership, Limited Liability Company, or S corporation).

c) Provide EIN (Employer Identification Number) of entity.

d) Provide valuation of entity.

e) Note question 11a on Part 4, Page 3 of Form 706: Did the

decedent, at the time of death, own any interest in a partnership (for

example, a family limited partnership), an unincorporated business, or a

limited liability company; or own any stock in an inactive or closely held

corporation?

16

f) VALUATION DISCOUNTS FOR BUSINESSES OR

PARTNERSHIPS:

(1) Note question 11b on Part 4, Page 3 of Form 706: If “Yes”

was the value of any interest owned (from above-see 10a)

discounted on this estate tax return? If “Yes,” the instructions

require that the executor attach a statement that identifies the

business entity on Schedule F and the discounts taken.

(2) Possible discounts

(a) Lack of control

(b) Lack of marketability

2. Insurance on the life of another (attach Form 712 showing the value)

3. If decedent was a surviving spouse, they may have been the beneficiary of

a qualified terminable interest property (QTIP) trust established by the first

spouse to die. The value of the trust assets is reportable on Schedule F. I.R.C.

§2044 Property

4. Rights

5. Royalties

6. Leaseholds

7. Judgments

8. Reversionary or remainder interests

9. Household goods and personal effects, including wearing apparel

a) For assets specifically bequeathed to individuals:

(1) Report sale value if sold at an arms length transaction (at

auction or for appraised value).

(2) Report appraised value if not sold.

b) For assets that are left to residue of the estate:

(1) Report sale value net of auctioneer or sale commissions or

deduct selling expenses as administrative expenses.

10. Livestock

17

11. Farm machinery

12. Automobiles.

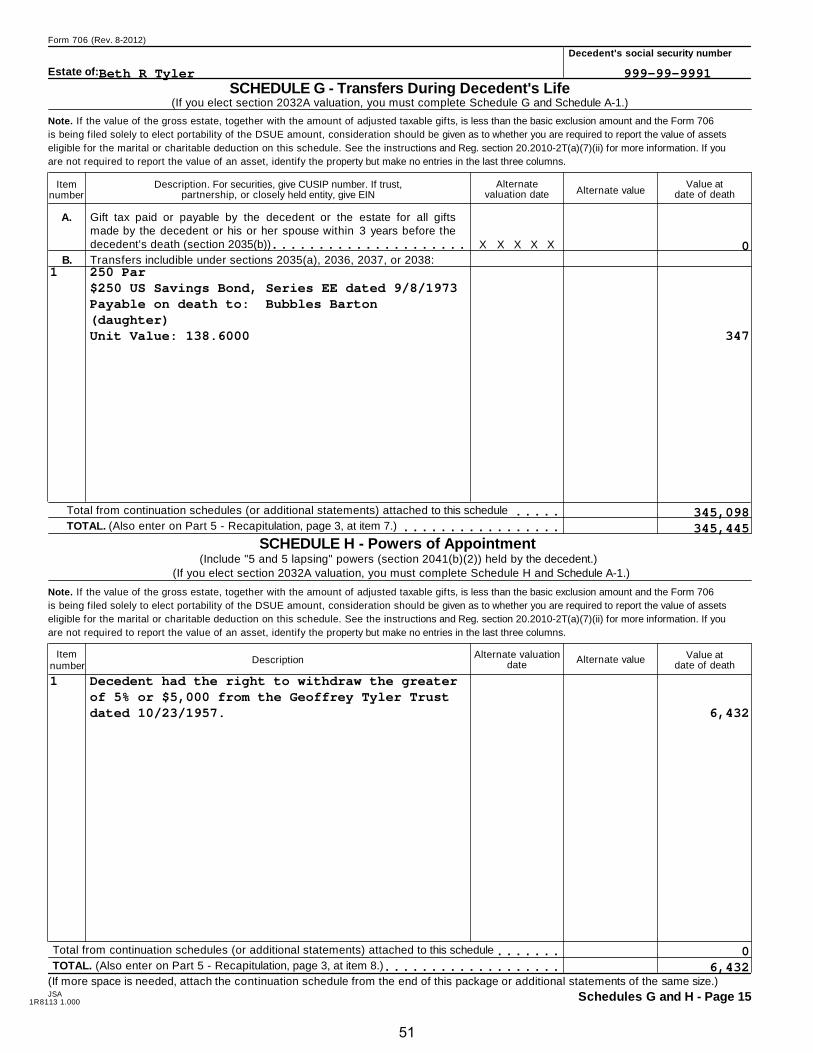

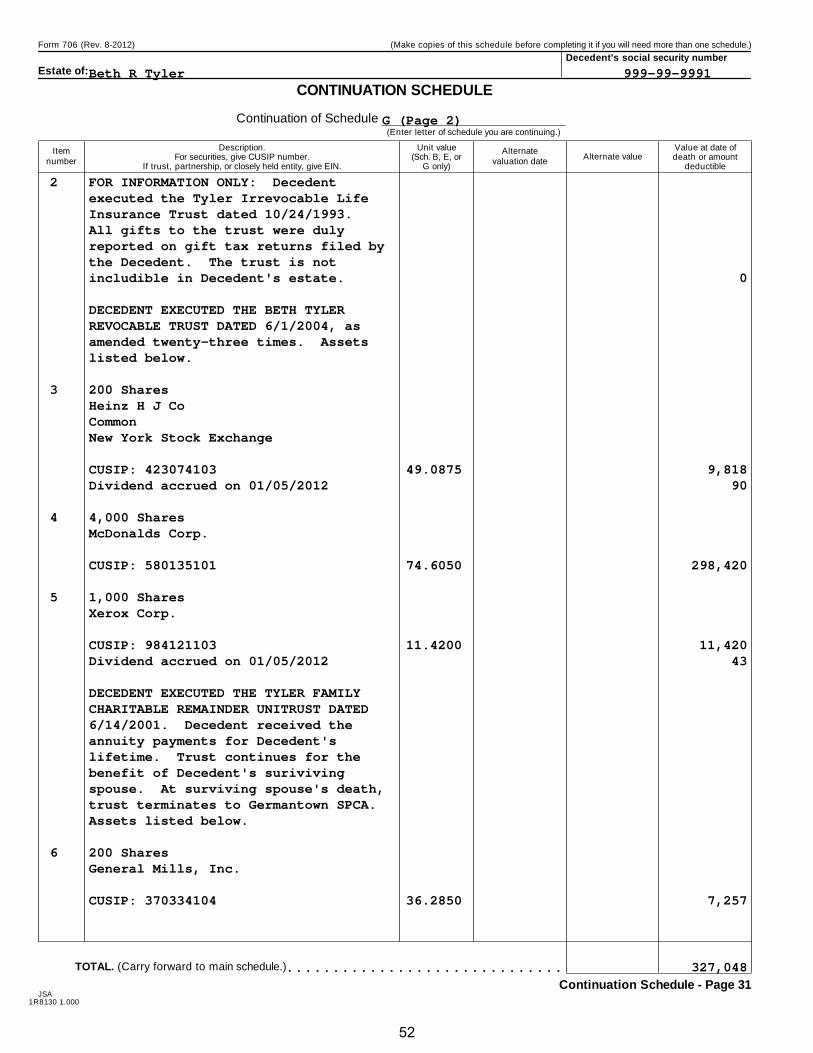

F. TRANSFERS DURING THE DECEDENT’S LIFE—Schedule G

1. Gift taxes paid by the decedent or the estate on gifts made by the decedent

or the decedent’s spouse within 3 years of death are included in the gross estate.

I.R.C. §2035(b)

2. Transfers made within 3 years of death that would have been included

under I.R.C. §2036, §2037, §2038, or I.R.C. §2042 had the decedent retained the

interest in the property are included in the gross estate. I.R.C. §2035(a).

a) Example: Where the decedent transfers ownership of a life

insurance policy to another within three years of death, the policy

proceeds are included in the decedent’s estate because the proceeds would

have been included in decedent’s estate under I.R.C. §2042 had the

decedent retained ownership of the policy.

3. Transfers by the decedent in which the decedent retained an interest in the

property are included in the gross estate. I.R.C. §2036

a) If the decedent transferred property to a trust and retained an

income, annuity or unitrust interest in the trust for decedent’s life, or for a

period that does not end before decedent’s death, the value of the trust is

included in the gross estate. I.R.C. §2036(a)

4. Transfers taking effect at death are included in the decedent’s gross estate.

I.R.C. §2037

5. Revocable transfers are included in the decedent’s gross estate. I.R.C.

§2038.

a) If the decedent had to right to change, alter, amend, revoke or

terminate the enjoyment of the property, the property is included in the

decedent’s gross estate.

b) A Revocable Trust or Totten Trust are revocable transfers included

in the decedent’s gross estate under I.R.C. §2038.

G. POWERS OF APPOINTMENT—SCHEDULE H

1. A “general power of appointment” is included in the decedent’s gross

estate. I.R.C. §2041

18

a) A “general power of appointment” is a power held by the decedent

exercisable in favor of the decedent, his estate, his creditors, or the

creditors of his estate. I.R.C. §2041(b)

b) The right to withdraw the greater of five percent or $5,000 from a

trust is a general power which is included in the decedent’s estate to the

extent the power was not exercised by the decedent. I.R.C. §2041(b)

H. ANNUITIES—SCHEDULE I

1. Annuities, pension plans, individual retirement arrangements, purchased

commercial annuities and private annuities owned by the decedent are included in

the decedent’s gross estate. I.R.C.§ 2039

a) The annuity or payment must be receivable by the beneficiary

following the death of the decedent.

b) The annuity is under a contract or agreement entered into after

March 3, 1931.

c) The annuity was payable to the decedent, for the decedent’s life or

for a period that did not end before the decedent’s death.

III. FEDERAL ESTATE TAX DEDUCTIONS

A. In General—For federal estate tax purposes, the value of the taxable estate shall

be determined by deducting from the value of the gross estate such amounts

1. For funeral expenses,

2. For administration expenses,

3. For claims against the estate, and

4. For unpaid mortgages on, or any indebtedness in respect of, property

where the value of the decedent’s interest therein, undiminished by such mortgage

or indebtedness, is included in the value of the gross estate, as are allowable under

the laws of the jurisdiction, whether within or without the united states, under

which the estate is being administered.

B. FUNERAL EXPENSES—SCHEDULE J

1. Funeral expenses are only deductible on Form 706.

19

2. Funeral expenses that (a) are actually expended, (b) are properly allowable

out of property subject to claims (probate assets), and (c) satisfy the requirements

of Treas. Reg. §20.2053-1(c) are deductible on Form 706. Treas. Reg. §20.2053-

2

3. Funeral expenses should be reduced by reimbursements such as Social

Security or Veterans Administration benefits.

4. Examples of expenses:

a) Casket

b) Tombstone, monument, mausoleum, burial lot, vault and future

care

c) Undertaker’s Fee

d) Flowers provided by the estate

e) Food for mourners

f) Clothing purchased for burial

g) Cost of transportation of the person bringing the body to the place

of burial. Treas. Reg. §20.2053-2

h) Transportation of one person to and from the burial site for stone

setting

i) Obituary cost

j) Printing and mailing acknowledgment cards

k) Honoraria for rabbi, minister, organist, cantor, etc.

C. ADMINISTRATION EXPENSES—SCHEDULE J

1. In General

a) Treas. Reg. §20.2053-3(a) provides that the deduction for

“administration expenses” is limited to such expenses as are actually and

necessarily incurred in the administration of the decedent’s estate; that is,

in the collection of assets, payment of debts, and distribution of property

to the persons entitled to it. Expenditures not essential to the proper

settlement of the estate, but incurred for the individual benefit of the heirs

may not be taken as deductions.

20

b) Estate Tax versus Income Tax Deduction

(1) Administrative expenses under I.R.C. §2053 or §2054 can

be claimed either as (i) deductions from the decedent’s gross estate

for federal estate tax purposes under I.R.C. §2053, or (ii) as

deductions in computing the taxable income of the estate or as an

offset against the sales price of property in determining gain or

loss. I.R.C. §642(g) Administrative expenses cannot be taken on

both returns.

(2) An estate may claim the administration expenses as income

tax deductions if it files, in duplicate, a statement with the Internal

Revenue Service waiving its right to claim them as estate tax

deductions. Treas. Reg. §1.642(g)-1

(3) Exception to Disallowance of Double Deductions: Taxes,

interest, business expenses, and other items accrued at date of

death are deductible from the gross estate under I.R.C. §2053(a)(3)

as claims against the estate are also deductible from gross income

under I.R.C. §692(b) as deductions in respect of a decedent for

income tax purposes. Treas. Reg. §1.642(g)-2

(4) Portability—Administrative expenses deducted on the

federal estate tax return will increase the amount of the “deceased

spousal unused exclusion amount” that can shield a surviving

spouse’s estate from estate tax, but the deductions cannot then be

used as income tax deductions on the fiduciary income tax return

of the estate.

c) Protective Claim for Refund Treas. Reg. 20.2053-1(d)(5)(i)

(1) A protective claim for refund may be filed to preserve the

estate’s right to claim a refund by reason of claims or expenses that

are not paid or do not otherwise meet the section 2053

deductibility requirements. Treas. Reg. 20.2053-1(d)(5)(1)

(a) Rev. Proc 2011-48 (10/14/11) sets forth the

procedure for a “2053 Protective Claim for Refund”

(i) Time period for filing: The later of 3 years

of return filing, or 2 years from tax payment.

(ii) Requirements of claim: Set forth grounds

and facts for refund under penalties of Perjury.

21

(iii) How to File “2053 Protective Claim for

Refund”:

(a) For deaths on or after January 1,

2012: Schedule PC or Form 843

(iv) Notification for Consideration—The

executor must notify the IRS that the issue is

resolved for the IRS to consider the Protective

Claim for Refund.:

(a) For deaths on or after January 1,

2012: Supplemental Form 706, or Form 843

(b) See Schedule PC attached to 2012 Form 706—

Protective Claim for Refund.

d) TYPES OF ADMINISTRATION EXPENSES

(1) Executor’s Commisions—Under Treas. Reg. §20.2053-

3(b)(1), a deduction is allowed for commissions in accordance with

the usually accepted standards and practice of allowing such an

amount in estates of similar size and character in the jurisdiction in

which the estate is being administered.

(2) Attorney’s Fees—Under Treas. Reg. §20.2053-3(c)(1)

attorney fees may not exceed a reasonable remuneration for the

services rendered, taking into account the size and character of the

estate, the law and practice in the jurisdiction in which the estate is

being administered, and the skill and expertise of the attorney.

(3) A deduction is allowed for attorney and executor fees not

paid at the time of filing of the return provided the amount is

ascertainable with reasonable certainty and will be paid. Treas.

Reg. §20.2053-1(d)(4)

(4) Miscellaneous administration expenses include:

(a) Court costs,

(b) Probate fees,

(c) Surrogate’s fees,

(d) Accountants’ fees

22

(e) Appraisers’ fees

(f) Expenses to preserve and distribute estate assets

including storing property of the estate.

(g) Expenses of sale of property such as real estate or

personal property if the sale is necessary to pay the

decedent’s debts, expenses of administration, or taxes, to

preserve the estate, or to effect distribution. Treas. Reg.

§20.2053-3(d)(2)

D. DEBTS OF DECEDENT AND MORTGAGES AND LIENS—SCHEDULE K

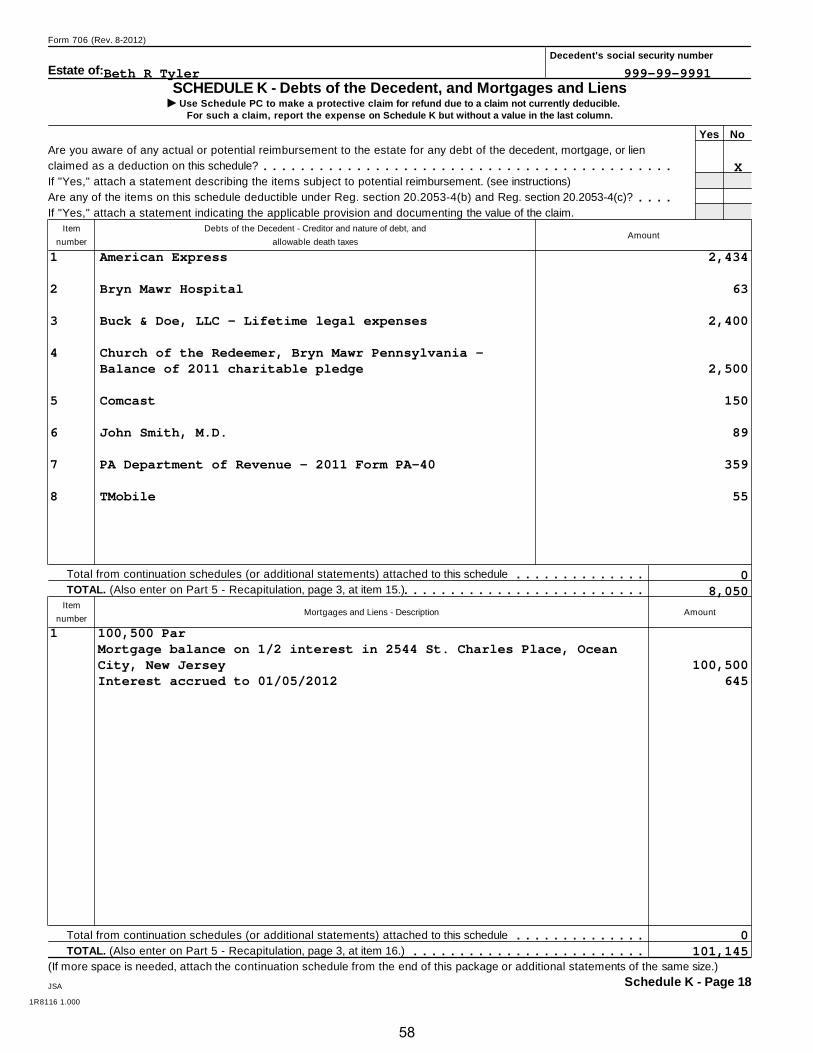

1. Personal liabilities imposed by law, or arising out of contracts or torts,

which exist at the time of decedent’s death which are bona fide enforceable

claims that are actually paid by the estate, or are unpaid but are ascertainable are

listed on Schedule K. Treas. Reg.§ 20.2053-4

2. Unpaid income taxes are allowable debts under Treas. Reg. §20.2053-6(f)

3. Unpaid gift taxes are allowable debts under Treas. Reg. §20-2053-6(d)

4. Medical care expenses paid by the estate within one year beginning with

the day after death can be taken as I.R.C. §2053 federal estate tax deductions, or

as I.R.C. §213(c) income tax deductions on the Decedent’s final income tax

return, but not both.

a) In order to take the income tax deduction, a statement must be filed

with the income tax return that the amount has not been allowed as a

I.R.C. §2053 deduction and waiving the right to having the deduction be

allowed as an estate tax deduction. I.R.C. §213(c)(2)

b) 7.5% adjusted gross income limit—An estate tax deduction is not

allowed for that portion of medical expenses disallowed by the 7.5% AGI

income tax limitation. Rev. Rul. 77-357, 1977-2, CB 328

5. An unpaid charitable pledge may be deductible on the federal estate tax

return under Treas. Reg. §20.2053-5 if:

a) The liability was contracted bona fide and for adequate and full

consideration in cash or its equivalent, or

b) It would be allowed as a charitable deduction under I.R.C. §2055.

23

6. Property taxes are not deductible unless accrued before the decedent’s

death. Treas. Reg. §20.2053-6(b)

E. MORTGAGES AND LIENS—SCHEDULE K

1. Unpaid mortgages, including interest which accrued to decedent’s death

are deductions listed on Schedule K. Treas. Reg. §20.2053-7

F. NET LOSSES DURING ADMINSTRATION—SCHEDULE L

1. A deduction is allowed on Schedule L for losses due to casualties

occurring during the settlement of the decedent’s estate including losses from

fires, storms, shipwrecks and theft. I.R.C. §2054

2. The deduction may be made, in the alternative, on the estate’s fiduciary

income tax return if the estate has waived its right to take a deduction for such

loss. I.R.C. §642(g)

3. Amounts recovered by insurance reduce the deduction. Treas. Reg.

§20.2054-1

G. EXPENSES INCURRED IN ADMINISTERING PROPERTY NOT SUBJECT

TO CLAIMS—SCHEDULE L

1. Expenses incurred in administering property in a decedent’s gross estate,

but not subject to claims may be allowed as deductions. Treas. Reg. §20.2053-8

2. Examples of such expenses include:

a) Expenses incurred in administering a Revocable Trust established

by the decedent during his or her lifetime such as attorney and trustee fees.

b) Expenses and costs incurred in connection with the collection,

valuation and distribution of non-probate assets.

H. BEQUESTS, ETC. TO A SURVIVING SPOUSE—SCHEDULE M

1. A marital deduction is allowed for any property interest which passes to

the surviving spouse, but only to the extent that the interest is included in the

gross estate. I.R.C. §2056(a)

2. The value of the marital deduction is reduced by any estate, succession,

legacy, or inheritance taxes paid out of such property. I.R.C. §2056(b)(4)

3. Items passing to surviving spouse outright or by operation of law:

24

a) Bequests and devises I.R.C. §2056(c)(1)

b) Items inherited by surviving spouse I.R.C. §2056(c)(2)

c) Dower or curtesy interests I.R.C. §2056(c)(3)

d) Interest transferred to spouse at any time I.R.C. §2053(c)(4)

e) Jointly held property with right of survivorship. §2056(c)(5)

f) Property over which decedent had power of appointment or which

was appointed to spouse, or passes to spouse in default of appointment

I.R.C. §2056(c)(6)

4. Trusts for which the marital deduction may be allowed

a) Life estate with power of appointment in surviving spouse—If the

surviving spouse (a) is the only beneficiary during his or her life, (b)

receives all income for life, and (c) has a general power of appointment,

the trust will qualify for the marital deduction under I.R.C. §2056(b)(5)

b) Charitable remainder trusts where spouse is only lifetime

beneficiary

(1) Marital Deduction: allowed for spouse’s interest. I.R.C.

§2056(b)(8)

(2) Charitable Deduction: allowed for charitable remainder.

§2055

c) QTIP (Qualified Terminable Interest Property) Trusts I.R.C.

§2056(b)(7)

(1) Requirements:

(a) Property must pass from decedent;

(b) Surviving spouse must have a “qualifying income

interest for life”:

(i) Surviving spouse must be entitled to all

income and be the only beneficiary during his or her

lifetime.

(ii) QTIP election made on the Federal Estate

Tax Return. I.R.C. §2056(b)(7)(B)

25

I. CHARITABLE, PUBLIC, AND SIMILAR GIFTS AND BEQUESTS—

SCHEDULE O

1. I.R.C. §2055 allows for a deduction from the gross estate of the amount of

all bequests, legacies, devises, or transfers to the following entities:

a) The United States, any State, any political division of a state, or the

District of Columbia for exclusively public purposes.

b) Religious, charitable, scientific, literary, or educational

corporations or associations.

c) Trusts or trustees, or fraternal societies for religious, charitable,

scientific, literary, or educational purposes, or for prevention of cruelty to

children or animals.

d) Veterans’ organizations.

2. Charitable Remainder Trusts—Under I.R.C. §2055(e)(2)(A), no charitable

deduction is allowed for a remainder interest which will pass to charity unless the

interest is in the form of a:

a) A “charitable remainder annuity trust”

b) A “charitable remainder trust” I.R.C. §664

c) A “pooled income fund” is in the form of a “charitable remainder a

charitable remainder interest unless I.R.C. §642(c)(5)

3. Payment of death taxes—The amount of the charitable deduction is

reduced by any estate, succession, legacy, or inheritance taxes required to be paid

out of the bequest by the terms of the will or local law. I.R.C. §2055(c)

26

IV. DEDUCTION FOR STATE DEATH TAXES I.R.C. §2058 for Decedents dying after

January 1, 2005—

A. I.R.C. §2058(a) Allowance of deduction. For purposes of the tax imposed by

section 2001 (Federal Estate Tax), the value of the taxable estate shall be determined by

deducting from the value of the gross estate the amount of any estate, inheritance, legacy,

or succession taxes actually paid to any State or the District of Columbia, in respect of

any property included in the gross estate (not including any such taxes paid with respect

to the estate of a person other than the decedent).

B. “Actually paid” Requirement

1. The state death taxes must be actually paid within the Period of

Limitations. I.R.C. §2058(b)

2. Pennsylvania’s 5% discount on inheritance tax paid within three months of

death is not “actually paid”.

C. “In respect of any property included in the gross estate”

1. The deduction should not be allowed for items subject to Pennsylvania

inheritance tax that are not included in the federal gross estate:

a) Gifts within one year of death—A gift made within one year of

death is subject to Pennsylvania Inheritance Tax, but may not be included

in the federal gross estate.

b) Sole use trusts—At the death of the first spouse to die, the

Executor can defer the Pennsylvania inheritance tax on a “sole use trust”

for the surviving spouse’s benefit until the death of the surviving spouse.

When the surviving spouse dies, the trust may not be included in the

surviving spouse’s federal gross estate depending upon the terms of the

trust, and the elections made by the executors of the first spouse to die.

D. IRS Form 706 for 2012

1. Report state death tax deduction on page 1, line 3b

2. File with return:

a) Certificate from state showing:

(1) Total amount of tax imposed;

(2) Amount of discount allowed;

27

(3) Amount of penalties and interest imposed or charged;

(4) Total amount actually paid in cash; and

(5) Date of payment.

V. GIFT TAX RETURNS FILED BY THE DECEDENT

A. Calculation of Federal Estate Tax—Impact of Taxable Gifts

1. The federal estate tax is calculated by calculating a “tentative tax” and

then applying various credits.

a) The “tentative tax” is calculated on the sum of the “taxable estate”

and “adjusted taxable gifts” over “the aggregate amount of tax which

would have been payable under chapter 12 with respect to gifts made by

the decedent after December 31, 1976” as if the tax rate in effect at the

decedent’s death is used to calculate the gift tax and credit against such tax

[“Total gift tax paid or payable with respect to gifts made by the decedent

after December 31, 1976”]. I.R.C. §2001(b)

b) The “taxable estate” is the “gross estate” on page 1, line 1, less

“total allowable deductions” on line 2, less the “State death tax deduction”

on line 3b.

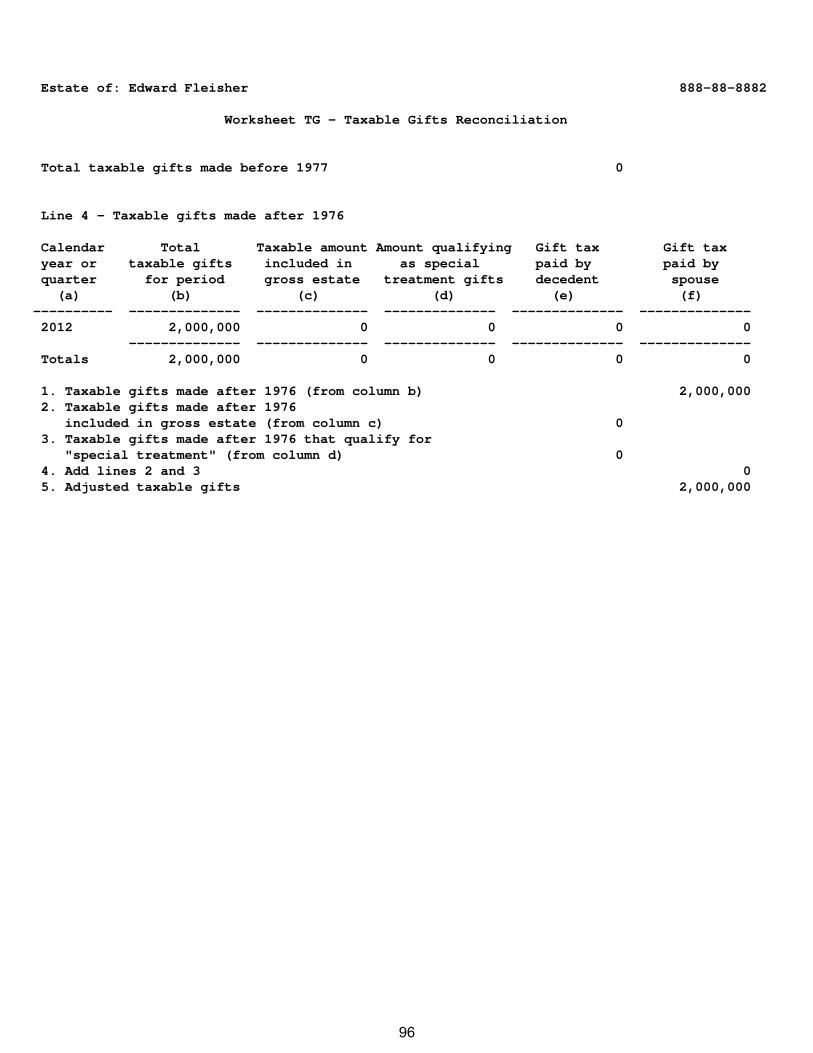

c) “Adjusted taxable gifts” are calculated using Worksheet TG—

Taxable Gift Reconciliation.

d) The “Total gift tax paid or payable with respect to gifts made by

the decedent after December 31, 1976” is calculated using the Line 7

Worksheet.

B. Copies of all gift tax returns filed by the Decedent must be filed with the 706.

The executor will need copies of all gift tax returns to complete the Line 4 and Line 7

Worksheets.

C. “Adjusted taxable gifts”—Line 4 of page 1 of the return.

1. Worksheet TG—Taxable Gift Reconciliation

a) The executor needs copies of all of the decedent’s gift tax returns

(Forms 709) to complete Worksheet TG—Taxable Gifts Reconciliation.

b) If any Gift Tax Returns were audited by the IRS, the executor

should use amounts that were finally determined as a result of the audit.

28

c) The executor must make reasonable effort as to the existence of

any gifts in excess of the annual exclusion made by the decedent for which

no Forms 709 were filed (Instructions for Form 706 (Rev. August 2012),

page 6). Any unreported gifts should be listed in column b of Worksheet

TG.

(1) Reasonable Effort—

(a) Review statements for banks, trusts and other

accounts from which decedent could have made gifts.

(b) Review cancelled checks and bank statements.

(c) Keep copies of such records in case Federal Estate

Tax Return is audited as auditor may review the statements

for gifts.

(2) Annual gift tax exclusion amounts:

(a) 1977-1981 -- $3,000 per donee

(b) 1981-2011 -- $10,000 per donee

(c) 2002-2005 -- $11,000 per donee

(d) 2006-2008 -- $12,000 per donee

(e) 2009 to 2012 -- $13,000 per donee

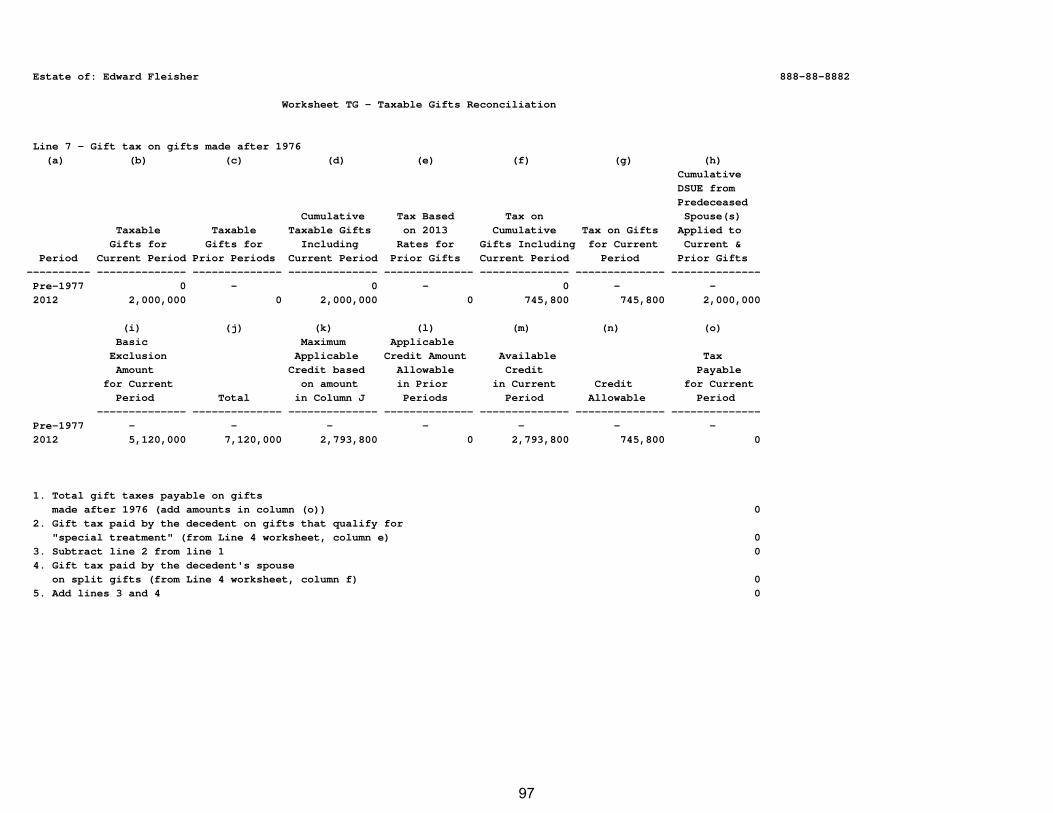

D. Line 7 Worksheet—

1. The executor must carefully follow the instructions of the Line 7

Worksheet.

2. Line 7 is NOT simply the total of all gift tax paid by the decedent during

his or her lifetime.

3. The Line 7 worksheet forces the executor to recalculate the gift tax as if

the tax rate in effect at the decedent’s death is used to calculate the gift tax and

credit against such tax. I.R.C. §2001(g)

E. Example—Emma Alden Form 706

29

1. In 1996, Emma Alden made a cash gift of $2,012,000 to her son, Edward

Alden. The annual gift tax exclusion for 1996 was $12,000. Emma filed 1996

Form 709 reporting a taxable gift of $2,000,000 ($2,012,000 less the annual gift

tax exclusion of $12,000) and paid gift tax of $588,000.

2. Line 4 Worksheet -- $2,000,000 of adjusted taxable gifts are added to Line

4, page 1.

3. Line 7 Worksheet – Even though Emma paid $588,000 of gift tax when

she made the 1996 gift, the Line 7 Worksheet only allows $490,000 on line 7

“Total gift tax paid or payable with respect to gifts made by the decedent after

December 31, 1976”.

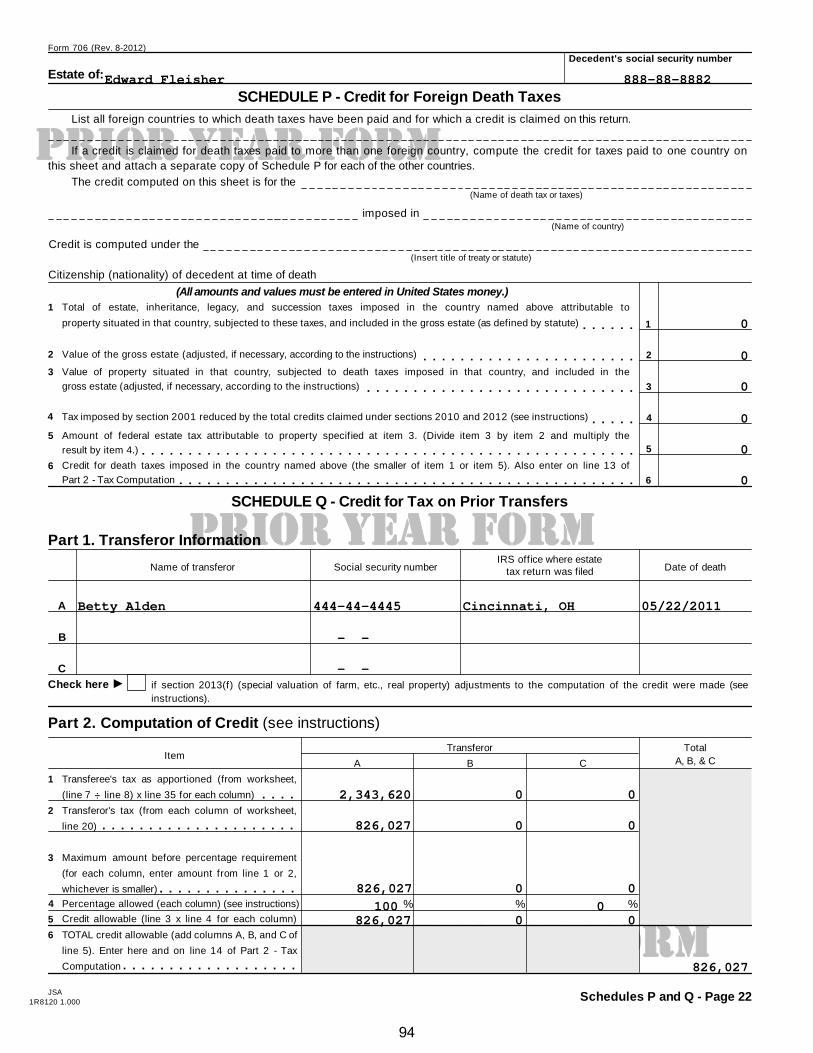

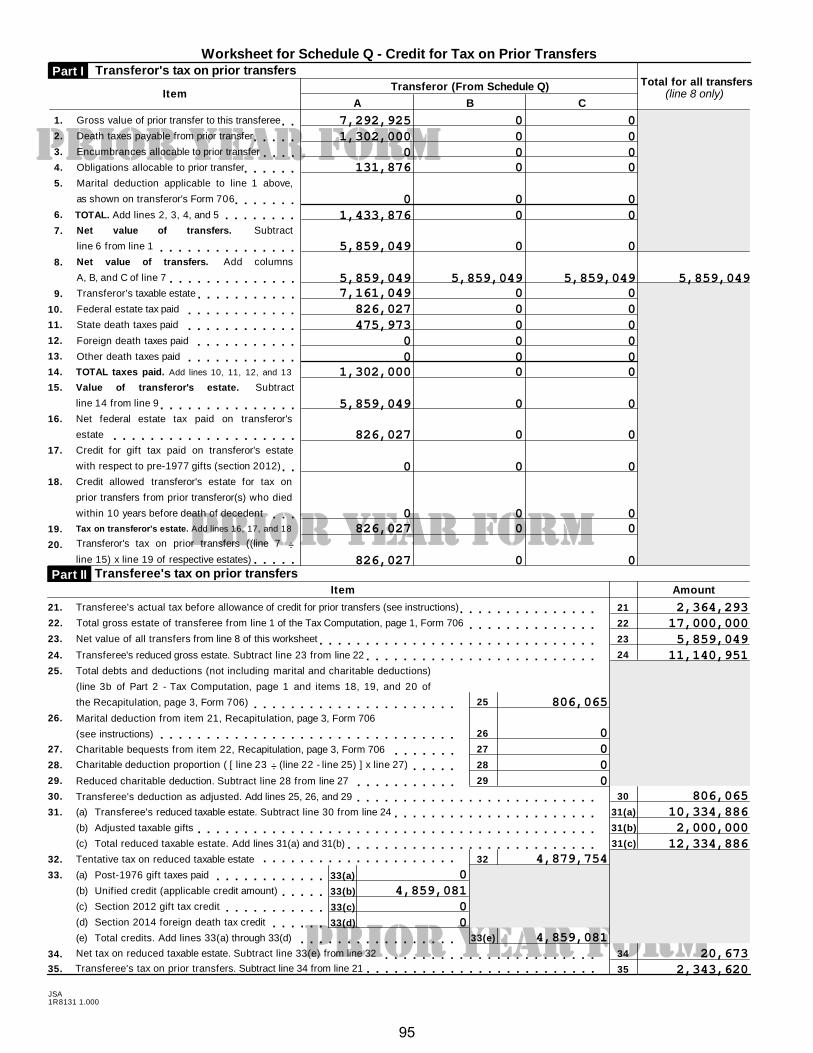

VI. PRIOR TRANSFER CREDIT—SCHEDULE Q

A. A credit against the federal estate tax is allowed for the amount of federal estate

tax paid with respect to the transfer of property to the decedent by or from a person

(“transferor”) who died within 10 years before, or within 2 years after the decedent’s

death. I.R.C. §2013

B. There is no requirement that the property be identified in the estate of the

transferee or that it exist on the date of the transferee’s death.

C. The transfer of the property must have been subjected to federal estate tax in the

estate of the transferor.

D. Where the transferor predeceased the transferee, the credit is reduced by the time

elapsed between dates of death:

1. 100% credit if time elapsed is less than 2 years.

2. 80% credit if time is between 2 years, and less than 4 years.

3. 60% credit if time is between 4 years, and less than 6 years.

4. 40% credit if time is between 6 years, and less than 8 years.

5. 20% credit if time is between 8 years and 10 years.

6. No credit if greater than 10 years.

E. Carefully complete the Schedule Q Worksheet using numbers from the Federal

Estate Tax Return of the Transferor.

30

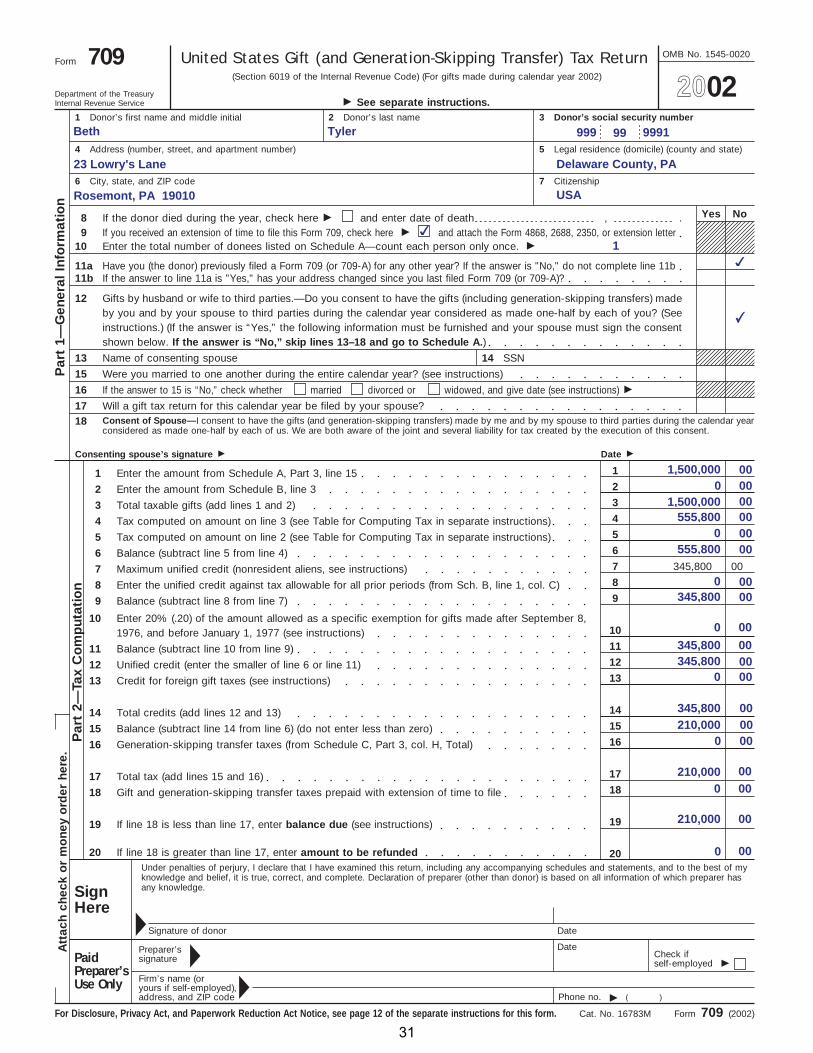

United States Gift (and Generation-Skipping Transfer) Tax ReturnForm 709(Section 6019 of the Internal Revenue Code) (For gifts made during calendar year 2002)

OMB No. 1545-0020

Department of the TreasuryInternal Revenue Service � See separate instructions.

1 2 Donor’s last nameDonor’s first name and middle initial Donor’s social security number3

Address (number, street, and apartment number)4 5 Legal residence (domicile) (county and state)

6 City, state, and ZIP code Citizenship7

NoYesIf the donor died during the year, check here � and enter date of death , .89 If you received an extension of time to file this Form 709, check here � and attach the Form 4868, 2688, 2350, or extension letter

Enter the total number of donees listed on Schedule A—count each person only once. �10

11a Have you (the donor) previously filed a Form 709 (or 709-A) for any other year? If the answer is "No," do not complete line 11b

12 Gifts by husband or wife to third parties.—Do you consent to have the gifts (including generation-skipping transfers) madeby you and by your spouse to third parties during the calendar year considered as made one-half by each of you? (Seeinstructions.) (If the answer is “Yes,” the following information must be furnished and your spouse must sign the consentshown below. If the answer is “No,” skip lines 13–18 and go to Schedule A.)

13 Name of consenting spouse 14 SSN

15 Were you married to one another during the entire calendar year? (see instructions)Par

t 1—

Gen

eral

Inf

orm

atio

n

16 If the answer to 15 is “No,” check whether

Will a gift tax return for this calendar year be filed by your spouse?17Consent of Spouse—I consent to have the gifts (and generation-skipping transfers) made by me and by my spouse to third parties during the calendar yearconsidered as made one-half by each of us. We are both aware of the joint and several liability for tax created by the execution of this consent.

18

Date �Consenting spouse’s signature �

11 Enter the amount from Schedule A, Part 3, line 1522 Enter the amount from Schedule B, line 333 Total taxable gifts (add lines 1 and 2)44 Tax computed on amount on line 3 (see Table for Computing Tax in separate instructions)55 Tax computed on amount on line 2 (see Table for Computing Tax in separate instructions)66 Balance (subtract line 5 from line 4)

345,800 0077 Maximum unified credit (nonresident aliens, see instructions)88 Enter the unified credit against tax allowable for all prior periods (from Sch. B, line 1, col. C)99 Balance (subtract line 8 from line 7)

10 Enter 20% (.20) of the amount allowed as a specific exemption for gifts made after September 8,1976, and before January 1, 1977 (see instructions) 10

1111 Balance (subtract line 10 from line 9)1212 Unified credit (enter the smaller of line 6 or line 11)1313 Credit for foreign gift taxes (see instructions)

1414 Total credits (add lines 12 and 13)15

Par

t 2—

Tax

Co

mp

utat

ion

15 Balance (subtract line 14 from line 6) (do not enter less than zero)1616 Generation-skipping transfer taxes (from Schedule C, Part 3, col. H, Total)

1717 Total tax (add lines 15 and 16)1818 Gift and generation-skipping transfer taxes prepaid with extension of time to file

1919 If line 18 is less than line 17, enter balance due (see instructions)

If line 18 is greater than line 17, enter amount to be refunded 20 20

Att

ach

chec

k o

r m

one

y o

rder

her

e.

Form 709 (2002)For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see page 12 of the separate instructions for this form. Cat. No. 16783M

If the answer to line 11a is "Yes," has your address changed since you last filed Form 709 (or 709-A)?11b

divorced or widowed, and give date (see instructions) �married

Under penalties of perjury, I declare that I have examined this return, including any accompanying schedules and statements, and to the best of myknowledge and belief, it is true, correct, and complete. Declaration of preparer (other than donor) is based on all information of which preparer hasany knowledge.Sign

HereDateSignature of donor

DatePreparer’ssignature Check if

self-employed �PaidPreparer’sUse Only Firm’s name (or

yours if self-employed), address, and ZIP code

�

�

�Phone no. � ( )

2002Beth Tyler 999 99 9991

23 Lowry's Lane Delaware County, PA

Rosemont, PA 19010 USA

✔1

✔

✔

1,500,000 000 00

1,500,000 00555,800 00

0 00555,800 00

0 00345,800 00

0 00345,800 00345,800 00

0 00

345,800 00210,000 00

0 00

210,000 000 00

210,000 00

0 00

31

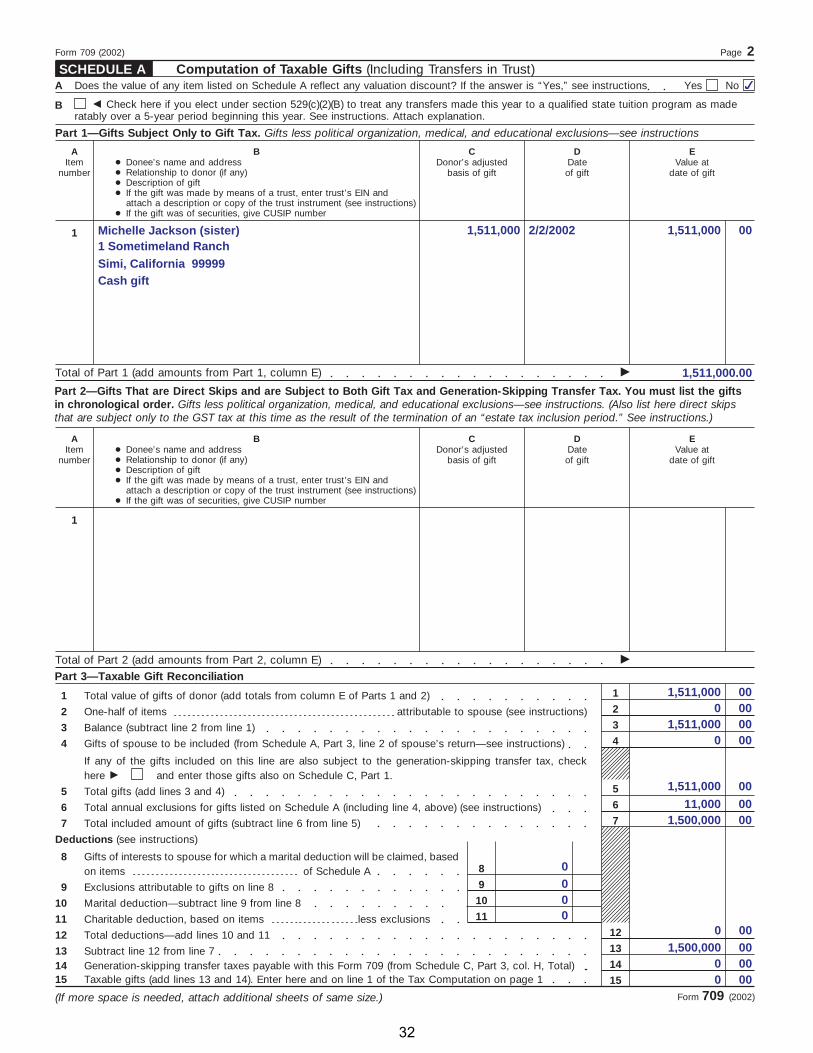

SCHEDULE APage 2Form 709 (2002)

Computation of Taxable Gifts (Including Transfers in Trust)

Part 1—Gifts Subject Only to Gift Tax. Gifts less political organization, medical, and educational exclusions—see instructions

EValue at

date of gift

DDateof gift

CDonor’s adjusted

basis of gift

AItem

number

1

Part 2—Gifts That are Direct Skips and are Subject to Both Gift Tax and Generation-Skipping Transfer Tax. You must list the giftsin chronological order. Gifts less political organization, medical, and educational exclusions—see instructions. (Also list here direct skipsthat are subject only to the GST tax at this time as the result of the termination of an “estate tax inclusion period.” See instructions.)

EValue at

date of gift

DDateof gift

CDonor’s adjusted

basis of gift

AItem

number

1

Part 3—Taxable Gift Reconciliation1Total value of gifts of donor (add totals from column E of Parts 1 and 2)12One-half of items attributable to spouse (see instructions)23Balance (subtract line 2 from line 1)34Gifts of spouse to be included (from Schedule A, Part 3, line 2 of spouse’s return—see instructions)4

If any of the gifts included on this line are also subject to the generation-skipping transfer tax, checkhere � and enter those gifts also on Schedule C, Part 1.

5Total gifts (add lines 3 and 4)56Total annual exclusions for gifts listed on Schedule A (including line 4, above) (see instructions)67Total included amount of gifts (subtract line 6 from line 5)7

Deductions (see instructions)Gifts of interests to spouse for which a marital deduction will be claimed, basedon items of Schedule A

889Exclusions attributable to gifts on line 89

10Marital deduction—subtract line 9 from line 81011Charitable deduction, based on items less exclusions11

12Total deductions—add lines 10 and 111213Subtract line 12 from line 71314Generation-skipping transfer taxes payable with this Form 709 (from Schedule C, Part 3, col. H, Total)14

Taxable gifts (add lines 13 and 14). Enter here and on line 1 of the Tax Computation on page 115 15(If more space is needed, attach additional sheets of same size.)

B

B

● Donee’s name and address● Relationship to donor (if any)● Description of gift● If the gift was made by means of a trust, enter trust’s EIN and

attach a description or copy of the trust instrument (see instructions)● If the gift was of securities, give CUSIP number

● Donee’s name and address● Relationship to donor (if any)● Description of gift● If the gift was made by means of a trust, enter trust’s EIN and

attach a description or copy of the trust instrument (see instructions)● If the gift was of securities, give CUSIP number

Does the value of any item listed on Schedule A reflect any valuation discount? If the answer is “Yes,” see instructions Yes No

Total of Part 1 (add amounts from Part 1, column E) �

Total of Part 2 (add amounts from Part 2, column E) �

� Check here if you elect under section 529(c)(2)(B) to treat any transfers made this year to a qualified state tuition program as maderatably over a 5-year period beginning this year. See instructions. Attach explanation.

B

A

Form 709 (2002)

✔

Michelle Jackson (sister) 1,511,000 2/2/2002 1,511,000 001 Sometimeland RanchSimi, California 99999Cash gift

1,511,000.00

1,511,000 000 00

1,511,000 000 00

1,511,000 0011,000 00

1,500,000 00

0000

0 001,500,000 00

0 000 00

32

SCHEDULE B

SCHEDULE APage 3Form 709 (2002)

Computation of Taxable Gifts (continued)16 Terminable Interest (QTIP) Marital Deduction. (See instructions for line 8 of Schedule A.)

17 Election Out of QTIP Treatment of Annuities� Check here if you elect under section 2523(f)(6) NOT to treat as qualified terminable interest property any joint and survivor annuities that

are reported on Schedule A and would otherwise be treated as qualified terminable interest property under section 2523(f). (See instructions.)Enter the item numbers (from Schedule A) for the annuities for which you are making this election �

Gifts From Prior Periods

DAmount of specificexemption for prior

periods ending beforeJanuary 1, 1977

CAmount of unified

credit against gift taxfor periods after

December 31, 1976

ACalendar year orcalendar quarter(see instructions)

EAmount of

taxable gifts

BInternal Revenue office

where prior return was filed

1Totals for prior periods1

2Amount, if any, by which total specific exemption, line 1, column D, is more than $30,0002Total amount of taxable gifts for prior periods (add amount, column E, line 1, and amount, if any, online 2). (Enter here and on line 2 of the Tax Computation on page 1.)

33

(If more space is needed, attach additional sheets of same size.)

If a trust (or other property) meets the requirements of qualified terminable interest property under section 2523(f), anda. The trust (or other property) is listed on Schedule A, andb. The value of the trust (or other property) is entered in whole or in part as a deduction on line 8, Part 3 of Schedule A,

then the donor shall be deemed to have made an election to have such trust (or other property) treated as qualified terminable interest propertyunder section 2523(f).

If less than the entire value of the trust (or other property) that the donor has included in Part 1 of Schedule A is entered as a deduction online 8, the donor shall be considered to have made an election only as to a fraction of the trust (or other property). The numerator of this fractionis equal to the amount of the trust (or other property) deducted on line 10 of Part 3, Schedule A. The denominator is equal to the total value ofthe trust (or other property) listed in Part 1 of Schedule A.

If you answered “Yes” on line 11a of page 1, Part 1, see the instructions for completing Schedule B. If you answered “No,” skip to the TaxComputation on page 1 (or Schedule C, if applicable).

If you make the QTIP election (see instructions for line 8 of Schedule A), the terminable interest property involved will be included in yourspouse’s gross estate upon his or her death (section 2044). If your spouse disposes (by gift or otherwise) of all or part of the qualifying lifeincome interest, he or she will be considered to have made a transfer of the entire property that is subject to the gift tax (see Transfer of CertainLife Estates on page 4 of the instructions).

Form 709 (2002)

NONE

33

Form 709 (2002) Page 4

Part 2—GST Exemption Reconciliation (Section 2631) and Section 2652(a)(3) ElectionCheck box � if you are making a section 2652(a)(3) (special QTIP) election (see instructions)Enter the item numbers (from Schedule A) of the gifts for which you are making this election �

1Maximum allowable exemption (see instructions)1

22 Total exemption used for periods before filing this return

33 Exemption available for this return (subtract line 2 from line 1)

44 Exemption claimed on this return (from Part 3, col. C total, below)5 Exemption allocated to transfers not shown on Part 3, below. You must attach a Notice of Allocation. (See

instructions.) 5

6Add lines 4 and 56

77 Exemption available for future transfers (subtract line 6 from line 3)Part 3—Tax Computation

HGeneration-Skipping

Transfer Tax(multiply col. B by col. G)

GApplicable Rate(multiply col. E

by col. F)

FMaximum Estate

Tax Rate

EInclusion Ratio(subtract col. D

from 1.000)

DDivide col. C

by col. B

BNet transfer

(from Schedule C,Part 1, col. F)

CGST Exemption

Allocated

AItem No.

(from ScheduleC, Part 1)

1 50% (.50)23456

Total exemption claimed. Enterhere and on line 4, Part 2,above. May not exceed line 3,Part 2, above

Total generation-skipping transfer tax. Enter here, on line 14 ofSchedule A, Part 3, and on line 16 of the Tax Computation onpage 1

(If more space is needed, attach additional sheets of same size.)

SCHEDULE C Computation of Generation-Skipping Transfer TaxNote: Inter vivos direct skips that are completely excluded by the GST exemption must still be fully reported(including value and exemptions claimed) on Schedule C.

Part 1—Generation-Skipping TransfersF

Net Transfer(subtract col. E

from col. D)

CSplit Gifts

(enter 1⁄2 of col. B)(see instructions)

BValue

(from Schedule A,Part 2, col. E)

AItem No.

(from Schedule A,Part 2, col. A)

ENontaxable

portion of transfer

DSubtract col. C

from col. B

123456

Value includedfrom spouse’s

Form 709

Split gifts fromspouse’s Form 709(enter item number)

If you elected gift splitting and your spousewas required to file a separate Form 709(see the instructions for “Split Gifts”), youmust enter all of the gifts shown onSchedule A, Part 2, of your spouse’s Form709 here. S-In column C, enter the item number of eachgift in the order it appears in column A ofyour spouse’s Schedule A, Part 2. We havepreprinted the prefix “S-” to distinguish yourspouse’s item numbers from your own whenyou complete column A of Schedule C,Part 3.

S-S-S-S-

In column D, for each gift, enter the amountreported in column C, Schedule C, Part 1, ofyour spouse’s Form 709.

S-S-S-

Net transfer(subtract col. E

from col. D)Nontaxable

portion of transfer

50% (.50)50% (.50)50% (.50)50% (.50)50% (.50)50% (.50)50% (.50)50% (.50)50% (.50)

Form 709 (2002)

1,100,000

0

1,100,000

0

0

0

1,100,000

34

United States Estate (and Generation-Skipping706Form

(Rev. August 2012) Transfer) Tax ReturnOMB No. 1545-0015

Department of the TreasuryInternal Revenue Service I Estate of a citizen or resident of the United States (see instructions). To be filed for

decedents dying after December 31, 2011, and before January 1, 2013.Information about Form 706 and its separate instructions is at www.irs.gov/form706.I

1a

3a

6a

6c

7a

Decedent's first name and middle initial (and maiden name, if any) 1b Decedent's last name 2 Decedent's social security no.

County, state, and ZIP or foreign country and postal code, of legalresidence (domicile) at time of death

3b Year domicile established 4 Date of birth 5 Date of death

6b Executor's address (number and street including apartment or suite no.; city, town,or post office; state; country; and ZIP or postal code) and phone no.

Name of executor (see instructions)

Executor's social security number (see instructions)

Phone no.

6d If there are multiple executors, check here and attach a list showing the names, addresses, telephone numbers, and SSNs of the additional executors.

Name and location of court where will was probated or estate administered 7b Case number

Par

t 1 -

Dec

eden

t and

Exe

cuto

r

I I810

If decedent died testate, check here and attach a certified copy of the will. 9 If you extended the time to file this Form 706, check hereI IIf Schedule R-1 is attached, check here If you are estimating the value of assets included in the gross estate on line 1 pursuant to the special rule of Reg. section 20.2010-2T(a) (7)(ii), check here11

123

4567899

99

10

11121314151617181920

Total gross estate less exclusion (from Part 5 - Recapitulation, item 13)

Tentative total allowable deductions (from Part 5 - Recapitulation, item 24)

Tentative taxable estate (subtract line 2 from line 1)

State death tax deduction

Taxable estate (subtract line 3b from line 3a)

12

3a3b3c45678

1112

151617181920

m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m mabc

m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m m m mAdjusted taxable gifts (see instructions) m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mAdd lines 3c and 4

Tentative tax on the amount on line 5 from Table A in the instructionsm m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m

Total gift tax paid or payable (see instructions)

Gross estate tax (subtract line 7 from line 6)m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m

ab

cd

Basic exclusion amount

Deceased spousal unused exclusion (DSUE) amount from predeceased spouse(s), if

any (from Section D, Part 6-Portability of Deceased Spousal Unused Exclusion)

9a

9b9c9d

10

1314

m m m m m m m m m m m m m m m m m m m m m mm m m m m mApplicable exclusion amount (add lines 9a and 9b)

Applicable credit amount (tentative tax on the amount in 9c from Table A in the instructions)

Adjustment to applicable credit amount (May not exceed $6,000.

See instructions.)

Allowable applicable credit amount (subtract line 10 from line 9d)

Subtract line 11 from line 8 (but do not enter less than zero)

Credit for foreign death taxes (from Schedule P). (Attach Form(s) 706-CE.)

Credit for tax on prior transfers (from Schedule Q)

Total credits (add lines 13 and 14)

Net estate tax (subtract line 15 from line 12)

Generation-skipping transfer (GST) taxes payable (from Schedule R, Part 2, line 10)

Total transfer taxes (add lines 16 and 17)

Prior payments (explain in an attached statement)

Balance due (or overpayment) (subtract line 19 from line 18)

m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m

Par

t 2 -

Tax

Com

puta

tion

m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m mm m mm m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m m m m m m mm m m m m m m m m m m m m m m m m m m m m m mUnder penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledgeand belief, it is true, correct, and complete. Declaration of preparer other than the executor is based on all information of which preparer has anyknowledge.

SignHere

M MSignature of executor DateM MSignature of executor Date

Date PTINPrint/Type preparer's name Preparer's signatureCheck if

self-employedPaidPreparerUse Only Firm's EIN

Phone no.I IFirm's name IFirm's address

For Privacy Act and Paperwork Reduction Act Notice, see instructions. Form 706 (Rev. 8-2012)JSA1R8100 1.000

999-99-9991

Delaware County PA1921 09/09/1921 01/05/2012

Tyler

19010-

X XOrphans Court of Delaware County, Pennsylvania 23-12-11111

959 1,460,852

3,535,925 2,074,114 1,461,811

1,500,000 2,960,852 1,017,098 175,000 842,098

5,120,000

0 0 0

0 0

0 0

0 1,772,800

0

0

0 5,120,000 1,772,800

Beth R

Edward Fleisherc/o Rosemont Trust Company10 Main Street

888-88-8882Rosemont, PA 19010

( ) -

35

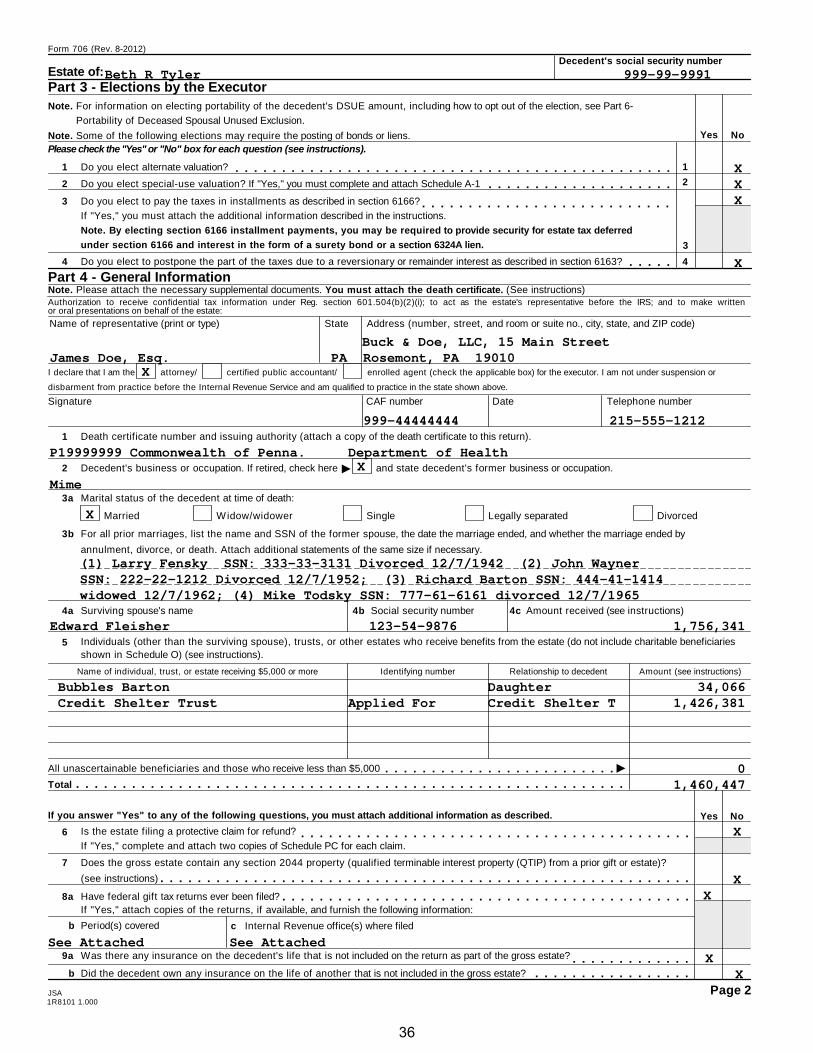

Form 706 (Rev. 8-2012)Decedent's social security number

Estate of:Part 3 - Elections by the ExecutorNote. For information on electing portability of the decedent's DSUE amount, including how to opt out of the election, see Part 6-

Portability of Deceased Spousal Unused Exclusion.

Yes NoNote. Some of the following elections may require the posting of bonds or liens.Please check the "Yes" or "No" box for each question (see instructions).

11 Do you elect alternate valuation? m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m22 Do you elect special-use valuation? If "Yes," you must complete and attach Schedule A-1 m m m m m m m m m m m m m m m m m m m m

3 Do you elect to pay the taxes in installments as described in section 6166?

If "Yes," you must attach the additional information described in the instructions.

Note. By electing section 6166 installment payments, you may be required to provide security for estate tax deferred under section 6166 and interest in the form of a surety bond or a section 6324A lien.

m m m m m m m m m m m m m m m m m m m m m m m m m m m3

4 Do you elect to postpone the part of the taxes due to a reversionary or remainder interest as described in section 6163? 4m m m m mPart 4 - General InformationNote. Please attach the necessary supplemental documents. You must attach the death certificate. (See instructions)Authorization to receive confidential tax information under Reg. section 601.504(b)(2)(i); to act as the estate's representative before the IRS; and to make writtenor oral presentations on behalf of the estate:

Name of representative (print or type) State Address (number, street, and room or suite no., city, state, and ZIP code)

I declare that I am the attorney/ certified public accountant/ enrolled agent (check the applicable box) for the executor. I am not under suspension or

disbarment from practice before the Internal Revenue Service and am qualified to practice in the state shown above.

Signature CAF number Date Telephone number

1 Death certificate number and issuing authority (attach a copy of the death certificate to this return).

I2 Decedent's business or occupation. If retired, check here and state decedent's former business or occupation.

3a Marital status of the decedent at time of death:

Married Widow/widower Single Legally separated Divorced

3b For all prior marriages, list the name and SSN of the former spouse, the date the marriage ended, and whether the marriage ended by

annulment, divorce, or death. Attach additional statements of the same size if necessary.

4a Surviving spouse's name 4b Social security number 4c Amount received (see instructions)

Individuals (other than the surviving spouse), trusts, or other estates who receive benefits from the estate (do not include charitable beneficiaries5shown in Schedule O) (see instructions).

Name of individual, trust, or estate receiving $5,000 or more Identifying number Relationship to decedent Amount (see instructions)

IAll unascertainable beneficiaries and those who receive less than $5,000 m m m m m m m m m m m m m m m m m m m m m m m m mTotal m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m mIf you answer "Yes" to any of the following questions, you must attach additional information as described. Yes No

Is the estate filing a protective claim for refund?

If "Yes," complete and attach two copies of Schedule PC for each claim.6 m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m7 Does the gross estate contain any section 2044 property (qualified terminable interest property (QTIP) from a prior gift or estate)?

(see instructions) m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m8a Have federal gift tax returns ever been filed?

If "Yes," attach copies of the returns, if available, and furnish the following information:m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m

b Period(s) covered c Internal Revenue office(s) where filed

9a Was there any insurance on the decedent's life that is not included on the return as part of the gross estate? m m m m m m m m m m m m mb Did the decedent own any insurance on the life of another that is not included in the gross estate? m m m m m m m m m m m m m m m m m

Page 2JSA1R8101 1.000

X

Beth R Tyler 999-99-9991

XX

X

James Doe, Esq. PABuck & Doe, LLC, 15 Main Street

X

999-44444444 215-555-1212

P19999999 Commonwealth of Penna. Department of HealthX

Mime

X

(1) Larry Fensky SSN: 333-33-3131 Divorced 12/7/1942 (2) John Wayner

Edward Fleisher 123-54-9876

XX

See AttachedSee AttachedX

X

Rosemont, PA 19010

SSN: 222-22-1212 Divorced 12/7/1952; (3) Richard Barton SSN: 444-41-1414

X

widowed 12/7/1962; (4) Mike Todsky SSN: 777-61-6161 divorced 12/7/1965

1,756,341

0 1,460,447

Bubbles Barton Daughter 34,066Credit Shelter Trust Applied For Credit Shelter T 1,426,381

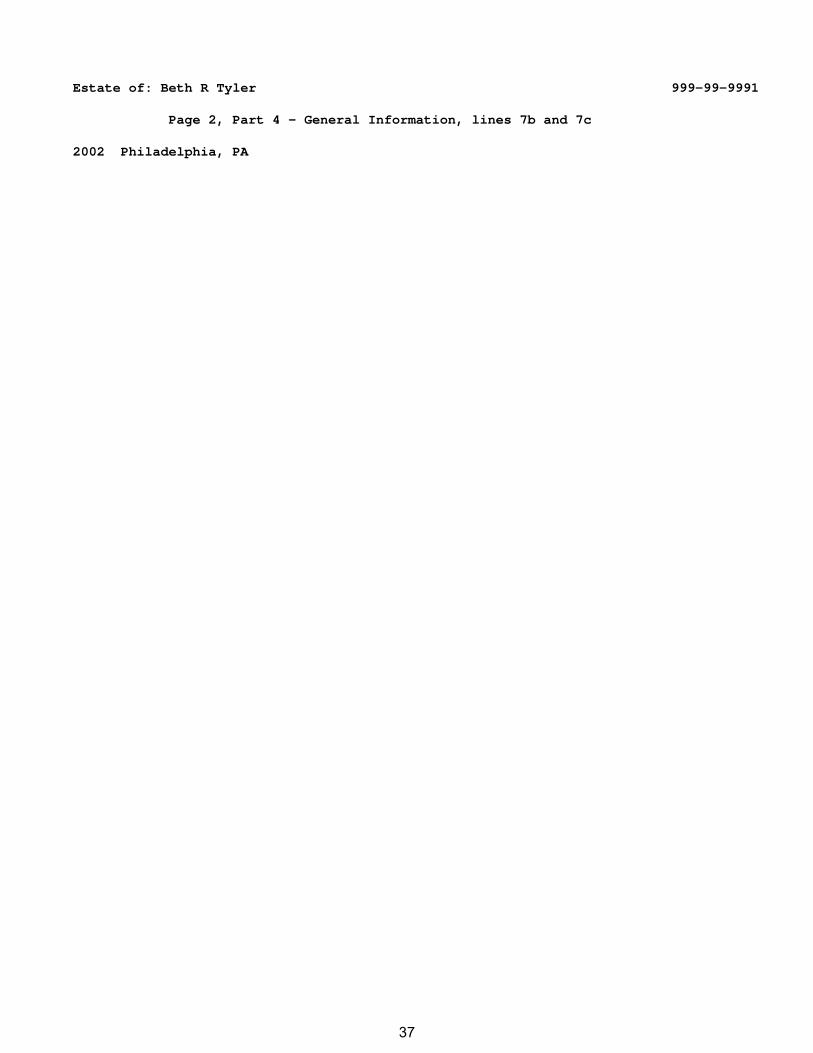

36

Estate of: Beth R Tyler 999-99-9991

Page 2, Part 4 – General Information, lines 7b and 7c

2002 Philadelphia, PA

37

Form 706 (Rev. 8-2012)

Decedent's social security number

Estate of:Part 4 - General Information (continued)If you answer "Yes" to any of the following questions, you must attach additional information as described. Yes No

Did the decedent at the time of death own any property as a joint tenant with right of survivorship in which (a) one or more of theother joint tenants was someone other than the decedent's spouse, and (b) less than the full value of the property is included onthe return as part of the gross estate? If "Yes," you must complete and attach Schedule E

10 m m m m m m m m m m m m m m m m m m m m m m m m11a Did the decedent, at the time of death, own any interest in a partnership (for example, a family limited partnership), an

unincorporated business, or a limited liability company; or own any stock in an inactive or closely held corporation? m m m m m m m m m m mb If "Yes," was the value of any interest owned (from above) discounted on this estate tax return? If "Yes," see the instructions on

reporting the total accumulated or effective discounts taken on Schedule F or G m m m m m m m m m m m m m m m m m m m m m m m m m m m m12 Did the decedent make any transfer described in sections 2035, 2036, 2037, or 2038? (see instructions) If "Yes," you must

complete and attach Schedule G m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m13a Were there in existence at the time of the decedent's death any trusts created by the decedent during his or her lifetime? m m m m m m m m

b Were there in existence at the time of the decedent's death any trusts not created by the decedent under which the decedentpossessed any power, beneficial interest, or trusteeship? m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m m

c Was the decedent receiving income from a trust created after October 22, 1986, by a parent or grandparent?If "Yes," was there a GST taxable termination (under section 2612) on the death of the decedent?