Embed Size (px)

Citation preview

PolicyAnalysisSeptember 10, 2014 | Number 756

EXECUTIVE SUMMARY

Daniel Ikenson is director of the Cato Institute’s Herbert A. Stiefel Center for Trade Policy Studies.

The Export-Import Bank and Its VictimsWhich Industries and States Bear the Brunt?By Daniel Ikenson

The charter of the Export-Import Bank of the United States is set to expire on Sep-tember 30. Proponents of reauthorization claim that by increasing exports and jobs, Ex-Im benefits the U.S. economy. But in

that advocacy, the benefits are exaggerated and the costs totally ignored.

The Bank’s skeptics speak of the opportunity costs that arise when government attempts to allocate resourc-es according to nonmarket criteria. They also note that subsidies provided for the benefit of one exporter put competing firms at an artificial disadvantage. In addition to these opportunity and intra-industry costs, there is a third set of significant costs that are too often forgotten: the downstream industry cost.

Using official input-output tables and seven years of Export-Import Bank transactions records, this analysis estimates the downstream costs of Ex-Im subsidies that are inflicted on manufacturing firms in every industry across every U.S. state. These victims populate 189 of 237 manufacturing sub-industries and all 21 broad manufac-turing industry categories identified under the North

American Industry Classification System, and they incurred a net cost of $2.8 billion per year or $14.7 million per sub-industry per year as a result of Ex-Im policies.

Among the specific sub-industry victims bearing the largest costs are U.S. manufacturers of motor vehicle bodies; computer storage devices; and, photographic and photocopying equipment. The 5 broad manufacturing industries incurring the greatest net costs are producers of electrical equipment, appliances and components; fur-niture; food; nonmetallic mineral products; and, chemi-cals. These 5 most ill-affected manufacturing industries account for 50 percent or more of manufacturing GDP in 7 U.S. states, and the 10 largest victims account for two-thirds or more of manufacturing GDP in 22 states.

In their efforts to win reauthorization from Congress, supporters of the Export-Import Bank rely on exagger-ated claims about the Bank’s benefits, while ignoring its costs. Ex-Im policies reward some companies (in the short run) and penalize many others in the process. These kinds of data are often obscured or ignored, but they are essen-tial to any informed judgments about the propriety and efficacy of the Export-Import Bank.

2

“The main purpose of this analysis is to expose the unseen costs, explain that collateral damage must be taken into account when considering the net effects of the Export-Import Bank, and show which industries and states bear the brunt of those costs.”

INTRODUCTION

The Export-Import Bank of the United States is a government-run export credit agen-cy, which provides special financing arrange-ments to facilitate sales between certain U.S. companies and foreign customers. For several months, Washington has been embroiled in a debate over whether to reauthorize the Bank’s charter, which will otherwise expire on Sep-tember 30.

Reauthorization advocates contend that Ex-Im fills a void left by private sector lenders unwilling to finance certain riskier transac-tions and, by doing so, contributes important-ly to U.S. export and job growth. Moreover, rather than burdening taxpayers, the Bank generates profits for the Treasury, helps small businesses succeed abroad, encourages ex-ports of “green” goods, contributes to devel-opment in sub-Saharan Africa, and helps “level the playing field” for U.S. companies compet-ing in export markets with foreign companies supported by their own governments’ gener-ous export financing programs. So what’s not to like about Ex-Im?

First, by dismissing the risk assessments of private-sector, profit-maximizing financial firms and making lending decisions based on nonmarket criteria to pursue often opaque, po-litical objectives, Ex-Im misallocates resources and puts taxpayer dollars at risk. That Ex-Im is currently self-financing and generating rev-enues is entirely beside the point. Ex-Im’s revenue stream depends on whether foreign borrowers are willing and able to service their loans, which is a function of global economic conditions beyond the control of Ex-Im. Given the large concentration of aircraft loans in its portfolio, for example, Ex-Im is heavily ex-posed to the consequences of a decline in de-mand for air travel. Recall that Fannie Mae and Freddie Mac also showed book profits for years until the housing market suddenly crashed and taxpayers were left holding the bag.

Second, even if taxpayers had tolerance for such risk taking, the claim that Ex-Im ex-ists to help small businesses is belied by the

fact that most of Ex-Im’s loan portfolio value is concentrated among a handful of large U.S. companies. In 2013 roughly 75 percent of the value of Ex-Im loans, guarantees, and insur-ance were granted on behalf of 10 large compa-nies, including Boeing, General Electric, Dow Chemical, Bechtel, and Caterpillar.1

Third, the notion that because Beijing, Brasilia, and Brussels subsidize their exporters Washington must, too, is a rationalization that sweeps under the rug the fact that there are dozens of criteria that feed into the ultimate purchasing decision, including product quality, price, producer’s reputation, local investment and employment opportunities created by the sale, warranties, after-market servicing, and the extent to which the transaction contrib-utes toward building a long-term relationship between buyer and seller. To say that U.S. ex-porters need assistance with financing to “lev-el the playing field” suggests that they lack ad-vantages among the multitude of factors that inform the purchasing decision. Moreover, if the offer of cheap financing is the determin-ing factor in these international transactions, what is to stop a growing number of inefficient low-quality producers from contesting these markets with ever-increasing subsidies from their own governments? U.S. companies and the taxpayers that would support them would be better off not competing for these markets if the key to winning foreign customers is par-ticipating in an endless subsidies race.

Fourth, by trying to “level the playing field” with foreign companies backed by their own governments, Ex-Im “unlevels” the playing field for many more U.S. companies compet-ing at home and abroad. This adverse effect has been ignored, downplayed, or mischarac-terized, but the collateral damage is substan-tial and should be a central part of the story.

At the risk of giving short shrift to the mul-titude of other legitimate objections to Ex-Im and its operations—many of which have been described and well-documented by current and former policy scholars2—the main pur-pose of this analysis is to expose the unseen costs, explain that collateral damage must be

3

“While Ex-Im financing reduces the cost of doing business for the lucky U.S. exporter and reduces the cost of capital for his foreign customer, it hurts U.S. competitors of the U.S. exporter, as well as U.S. competitors of his foreign customer by putting them at relative cost disadvantag-es.”

taken into account when considering the net effects of the Export-Import Bank, and show which industries and states bear the brunt of those costs. After all is laid bare and a full and proper accounting is taken, it will be clear that Ex-Im’s policies impose significant costs on manufacturing firms across every industry and in every U.S. state.

THE COSTS OF EX-IM FINANCING

When the Export-Import Bank provides financing to a U.S. company’s foreign customer on terms more favorable than he can secure elsewhere, it may be facilitating a transaction that would not otherwise occur. That is the ba-sis for Ex-Im’s claim that it helps the U.S. econ-omy by increasing exports and “supporting” jobs.3 But that claim is questionable because those resources might have created more value or more jobs if deployed in the private sector instead. If that were the case, Ex-Im’s transac-tion imposes a net loss on the economy.

But suppose it could be demonstrated that Ex-Im transactions grow the economy larger or create more jobs than if those resources had been deployed in the private sector instead. Would Ex-Im then be correct in its claim? Not necessarily. Further analysis is required.

Ex-Im financing helps two sets of compa-nies (in the short-run): U.S. firms whose export prices are subsidized by below market rate fi-nancing and the foreign firms who purchase those subsidized exports. It stands to reason, then, that those same transactions might im-pose costs on two different sets of companies: competing U.S. firms in the same industry who do not get Ex-Im backing, and U.S. firms in downstream industries, whose foreign compe-tition is now benefitting from reduced capital costs courtesy of U.S. government subsidies. While Ex-Im financing reduces the cost of doing business for the lucky U.S. exporter and reduces the cost of capital for his foreign cus-tomer, it hurts U.S. competitors of the U.S. exporter, as well as U.S. competitors of his for-eign customer by putting them at relative cost disadvantages.

These effects are neither theoretical nor difficult to comprehend. Yet proponents of Ex-Im reauthorization rarely acknowledge, let alone concede, that these are real costs perti-nent to any legitimate net benefits calculation. Instead, they speak only of the gross benefits of export subsidies, which they consider to be the value of exports supported by their autho-rizations.4

But there are at least three sets of costs that are essential to determining the net benefits of Ex-Im: (1) the “Opportunity Cost,” repre-sented by the export growth that would have obtained had Ex-Im’s resources been deployed in the private sector; (2) the “Intra-Industry Cost,” represented by the relative cost disad-vantage imposed on the other U.S. firms in the same industry (the domestic competitors) as a result of Ex-Im’s subsidies to a particular firm in the industry, and; (3) the “Downstream In-dustry Cost,” represented by the relative cost disadvantage imposed on the U.S. competitors of the subsidized foreign customer.

The Opportunity Cost is difficult to esti-mate. The “what-would-have-happened” coun-terfactual requires a variety of assumptions about average economic variables and their relationships, each with its own probability of occurrence. The assumptions necessary to generate such an estimate would significantly influence its value. For the sake of not bogging down the analysis in such detail or with con-testable assumptions, suffice it to recognize that opportunity costs exist. Indeed, oppor-tunity costs always exist when there are fore-gone alternatives to the path chosen. But for the sake of argument and the purpose of this study, assume that the overall opportunity cost of Ex-Im is $0. In other words, there will be no attempt here to quantify the opportunity cost of Ex-Im.

The Intra-Industry Cost is somewhat eas-ier to calculate, in theory. If Ex-Im provides a $50 million loan to a foreign farm equipment manufacturer to purchase steel from U.S. Steel Corporation, the transaction may benefit U.S. Steel, but it hurts competitors like Nucor, Steel Dynamics, AK Steel, and dozens of other

4

“Ex-Im helps some U.S. companies increase their exports sales. But it hinders other U.S. companies’ efforts to compete at home and abroad.”

steel firms operating in the United States and competing for the same customers at home and abroad. The $50 million subsidy to U.S. Steel is a cost to the other firms in the industry, who can attribute a $50 million revenue gap between them (aggregated) and U.S. steel to a government intervention that picked a win-ner and made them, relatively speaking, losers. The $50 million “benefit” for U.S. Steel is a $50 million cost to the other steel firms. But the distortion is then compounded when taking into consideration the dynamics that would have played out had the best firm—the one offering the most value for the best price—se-cured that export deal instead. Reaching rev-enue targets, raising capital, and moving down the production cost curve to generate lower unit costs all become more difficult to achieve on account of the original intervention, ampli-fying the adverse impact on other firms in the industry. When government intervenes with subsidies that tilt the playing field in favor of a particular firm, it simultaneously penalizes the other firms in the industry and changes the competitive industry dynamics going forward.

Every Ex-Im transaction touted for boost-ing U.S. exports creates victims within the same U.S. industry. Without Ex-Im’s interven-tion, Nucor might have been able to win that foreign farm equipment producer’s business, which is a prospect that undermines the prem-ise that Ex-Im boosts exports at all and rein-forces the point that it merely shifts resources around without creating value, and possibly destroys it. What is given to U.S. steel is taken from Nucor and the other firms, among whom may be the more efficient producers. Consid-ering only the intra-industry costs there is a strong case to be made that the net benefits of Ex-Im are at best $0.

But, again, for the sake of argument and the purpose of this paper, assume that the ben-efits do equal the amount of Ex-Im subsidies and that these transactions impose no costs on other firms in the industry. In other words, assume the intra-industry costs also equal $0.

The Downstream Industry costs are those imposed by the transaction on the U.S. compa-

nies that compete with the foreign customer. When a foreign farm machinery producer purchases steel on credit at subsidized interest rates, it obtains an advantage over its competi-tors—including its U.S. competitors. So, when that subsidized rate comes courtesy of a U.S. government program committed to increas-ing U.S. exports, it only seems reasonable to consider the effects on firms in downstream U.S. industries before claiming success. Has the subsidy to the foreign farm machinery producer made John Deere, Caterpillar, New Holland, or other U.S. farm machinery pro-ducers less competitive? Has it hurt their bot-tom lines?

To give a live example, Delta Airlines has been vocal in its objection to Ex-Im-facilitat-ed sales of Boeing jetliners to foreign carriers, such as Air India. Delta rightly complains that the U.S. government, as a matter of policy, is subsidizing Delta’s foreign competition by re-ducing Air India’s cost of capital. That cost re-duction enables Air India to offer lower prices in its bid to compete for passengers, which has a direct impact on Delta’s bottom line. This is a legitimate concern and it is not limited to this example.

Consider the generic case. A U.S. supplier sells to both U.S. and foreign customers. Those customers compete in the same downstream industry in the U.S. and foreign markets. Ex-Im is happy to provide financing to facilitate the sale, as its mission is to increase exports and create jobs. The U.S. supplier is thrilled that Ex-Im is providing his foreign customer with cheap credit because it spares him from having to offer a lower price or from sweeten-ing the deal in some other way to win the busi-ness. The foreign customer is happy to accept the advantageous financing for a variety of reasons, among which is the fact that his capi-tal costs are now lower relative to what they would have been and relative to the costs of his competitors—including his U.S. competitors, who are now on the outside looking in.

Ex-Im helps some U.S. companies increase their exports sales. But it hinders other U.S. companies’ efforts to compete at home and

5

“Supporters tend only to speak of the benefits of Ex-Im activities, as if there were no opportunity costs, intra-industry costs, or downstream industry costs.”

abroad. Moreover, by subsidizing export sales, Ex-Im artificially diverts domestic supply, pos-sibly causing U.S. prices to rise and rendering U.S. customers less important to their U.S. suppliers. Especially in industries where there are few producers, numerous customers, and limited substitute products, Ex-Im disrupts the relationships between U.S. buyers and U.S. sellers by infusing the latter with greater mar-ket power and leverage.

Delta was able to connect the dots. Other companies have, too. But most of the time, the downstream U.S. companies are unwitting victims of this gradual and silent cost-shifting.

UPSTREAM BENEFITS AND DOWNSTREAM COSTS

Supporters tend only to speak of the ben-efits of Ex-Im activities, as if there were no op-portunity costs, intra-industry costs, or down-stream industry costs. But those costs exist and they need to be taken into consideration as part of a net benefit analysis, where:

Net Benefit = Gross Benefit – Opportunity Cost – Intra-Industry Cost – Downstream Industry Cost

While it is intuitive that the full costs of Ex-Im include the opportunity costs and intra-industry costs, as explained earlier, their esti-mation requires making certain assumptions and assigning probabilities that are contest-able and that would detract from the thrust of this analysis. Suffice it to recognize that these costs are real, but go uncaptured in the follow-ing analysis. By setting those costs to zero, the equation becomes:

Net Benefit = Gross Benefit – Downstream Industry Cost

To estimate benefits, Export-Import Bank transaction data for the period 2007–2013—compiled from annual reports—were obtained from the Ex-Im website.5 Based on the infor-mation in the product description field, each

record was assigned a six-digit North Ameri-can Industry Classification System (NAICS) code. The NAICS is “the standard used by Federal statistical agencies in classifying busi-ness establishments for the purpose of col-lecting, analyzing, and publishing statistical data related to the U.S. business economy.”6 A six-digit NAICS code identifies an industry at the most detailed level of specificity, while a three-digit code reflects the aggregated in-dustry classification. For example, NAICS 336111 represents “Automobile Manufactur-ing,” which is a subset of NAICS 33611 (“Auto-mobile and Light Duty Motor Vehicle Manu-facturing”), which is a subset of NAICS 3361 (“Motor Vehicle Manufacturing”), which is a subset of NAICS 336, representing the broad-er Transportation Equipment Manufacturing industry. All NAICS codes that begin with the numbers 31–33 represent industries within the manufacturing sector. At the three-digit level, there are 21 official manufacturing industries in the United States. At the six-digit level, there are 237 individual manufacturing sector sub-industries.7

The following summary statistics derive from these data:

■ Ex-Im authorized $167.8 billion over 24,366 transactions during the seven-year period, which comes to about $24 billion per year and $6.9 million per transaction;

■ Manufactured exports accounted for $107.1 billion and 14,101 transactions for an average of about $15 billion per year and $7.6 million per transaction;

■ Aircraft accounted for nearly $57 bil-lion of the manufacturing total, which was spread over 722 authorizations, the average value of which was about $80 million—more than 10 times the value of the average manufacturing sector trans-action;

■ Producers in all 21 broad manufacturing industries (3-digit NAICS) received sub-sidies;

■ Producers in 225 of 237 manufacturing

6

“Among the most prominent issues in trade policy in recent years has been concern about globally in-terdependent supply chains and how policy is used to extract advantages for some and impose costs on other segments of the supply chain.”

sub-industries (6-digit NAICS) received subsidies.

While aircraft manufacturers (NAICS 336411)—Boeing, primarily—received $57 bil-lion over the seven-year period, additional subsidies, to the tune of almost $50 billion, were provided to exporters in all 21 broad U.S. manufacturing industries from food, textiles, and wood products to machinery, computers, and transportation equipment.

At the six-digit level of specificity, manu-facturers in 225 of 236 industries partook of the $50 billion in non-aircraft manufacturing largesse.8 The range of subsidies spans from $0 (for 11 industries receiving no benefits) to $5.2 billion (for “turbine and turbine generator set units”). The median value was $39.9 million and the mean (skewed far to the right by bil-lion dollar-plus subsidies to 11 industries) was $213.9 million.

Although subsidies like these have been shown to weaken firms over time by reducing their incentive to be efficient and competitive, this analysis assumes that the subsidy amounts authorized are approximations of the “ben-efits” of Ex-Im.9 The analysis takes as given the claim that the value of Ex-Im’s authorizations are benefits that translate dollar-for-dollar into U.S. exports that would not have materialized in the absence of Ex-Im support. In other words, the analysis accepts the rationale for Ex-Im’s existence put forth in its marketing mate-rials, so as to focus on one major oversight.

Consider the impact on firms in down-stream industries. As already described, when companies are given artificial incentives to ex-port, industries downstream to the subsidized exporters bear a cost. Domestic supply is di-verted, more market power is bestowed upon upstream suppliers, and foreign competitors’ capital costs are reduced, giving them an ad-vantage over U.S. firms.

These effects are not merely theoretical. Among the most prominent issues in trade policy in recent years has been concern about globally interdependent supply chains and how policy is used to extract advantages for

some and impose costs on other segments of the supply chain. In recent years, the U.S. gov-ernment brought disputes to the World Trade Organization in hopes of ending Chinese export restrictions on certain raw materials and “rare earth” elements. In both cases, the adverse economic impacts of the restrictions on downstream U.S. industries were the main reasons for pursuing dispute resolution. Then-U.S. Trade Representative Ron Kirk had the following to say about the matter:

China maintains a number of measures that restrain exports of raw material in-puts for which it is the top, or near top, world producer. These measures skew the playing field against the United States and other countries by creating substantial competitive benefits for downstream Chinese producers that use the inputs in the production and export of numerous processed steel, aluminum and chemical products and a wide range of further processed products.10

Policymakers are aware that restrictions on access to crucial intermediate goods raise pro-duction costs for industry. Some have worked to remove unnecessary impediments. Tradi-tionally, the Miscellaneous Tariff Bill has been a legislative vehicle for removing nuisance tar-iffs on industrial inputs.11 Upon signing the last MTB into law, President Obama said:

To make their products, manufactur-ers—some of whom are represented here today—often have to import cer-tain materials from other countries and pay tariffs on those materials. This leg-islation will reduce or eliminate some of those tariffs, which will significantly lower costs for American companies across the manufacturing landscape—from cars to chemicals; medical devices to sporting goods. And that will boost output, support good jobs here at home, and lower prices for American consum-ers.12

7

“Trade restrictions that impede domestic producers’ access to inputs put them at a cost disadvantage vis-à-vis foreign com-petitors with better access. Likewise, export subsidies—by encouraging exports—have the same deleterious effects on domestic downstream industries.”

Ready access to imported intermediate goods is paramount to manufacturing success in our globalized economy. Over the past five years, “industrial supplies and materials” and “capital goods except automotive” accounted for an average of 55 percent of goods imports.13 These are the purchases of U.S. downstream industries. Trade restrictions that impede do-mestic producers’ access to inputs put them at a cost disadvantage vis-à-vis foreign competi-tors with better access. Likewise, export subsi-dies—by encouraging exports—have the same deleterious effects on domestic downstream industries. These costs are real and there is no ignoring them in any legitimate analysis of the effect of Ex-Im’s policies.

ANALYSIS METHODOLOGY

Returning to the fictitious example of steel sales to foreign farm equipment producers, the $50 million loan to the foreign customer would be counted as a $50 million benefit to the U.S. economy, according to Ex-Im’s methodology. In reality, the benefit accrues to U.S. Steel Corpo-ration—not the broader economy—and some percentage of that $50 million is a cost borne by U.S. farm equipment producers.

What percentage? That depends on steel’s relative importance as an input in the produc-tion of farm equipment. If steel accounts for 90 percent of the cost of all intermediate inputs used in farm equipment manufacturing, then $45 million would be the cost borne by that in-dustry (0.9 x $50 million). If steel accounts for only 10 percent of the value of all intermediate inputs used to manufacture farm equipment, then $5 million would be the cost to the indus-try (0.1 x $50 million). Weighting is necessary because the extent of the cost inflicted on the downstream U.S industry depends on the im-portance of the intermediate good being sub-sidized to the production of the downstream product. If steel only accounts for 10 percent of all input costs, then subsidized steel sales to foreign companies have a smaller competitive impact on U.S. firms than if steel accounted for a larger share of the input costs.

Ideally, this approach to calculating the benefits and downstream costs would be pos-sible. But customer names in the Ex-Im da-tabase are often missing or cryptic and the records lack information about the buyer’s industry. Thus, it would be difficult to discern the name of U.S. Steel’s foreign customer (in the fictitious example) using the Ex-Im data-base and even more difficult to ascertain that the customer is in the farm equipment manu-facturing industry. Moreover, U.S. farm equip-ment manufacturers would not be the only victims in this transaction. They are most ad-versely affected because their foreign compe-tition is being directly subsidized by U.S. tax-payers, but other U.S. industries that consume steel are adversely affected by the supply diver-sion and its impact on the balance of market power between them and their steel suppliers.

These impediments necessitate a different approach. Fairly precise calculations of the benefits of Ex-Im by industry can be culled directly from the transactions database. Al-though the name of the exporter or supplier is frequently missing, product descriptions (and thus NAICS product codes) are available for 23,606 of 24,366 transactions. And the real costs of Ex-Im’s subsidies can be estimated us-ing input-output tables in conjunction with the Ex-Im transactions database. On its web-site, the Bureau of Economic Analysis main-tains a set of input-output tables that map the relationships between industries throughout the U.S. economy. Among the information that can be discerned from those tables are the disposition of output from any and all in-dustries and the input use requirements of any and all industries.14

The first observation about the BEA 2007 I-O Use Table is that 45 percent of the value of all U.S. economic output is consumed as in-puts in the production of other industries.15 The interdependence of industries is even more striking with respect to manufacturing output, of which 55 percent is consumed as inputs in the production of other industries.16 The I-O table also reveals how many indus-tries’ output each industry requires as inputs

8

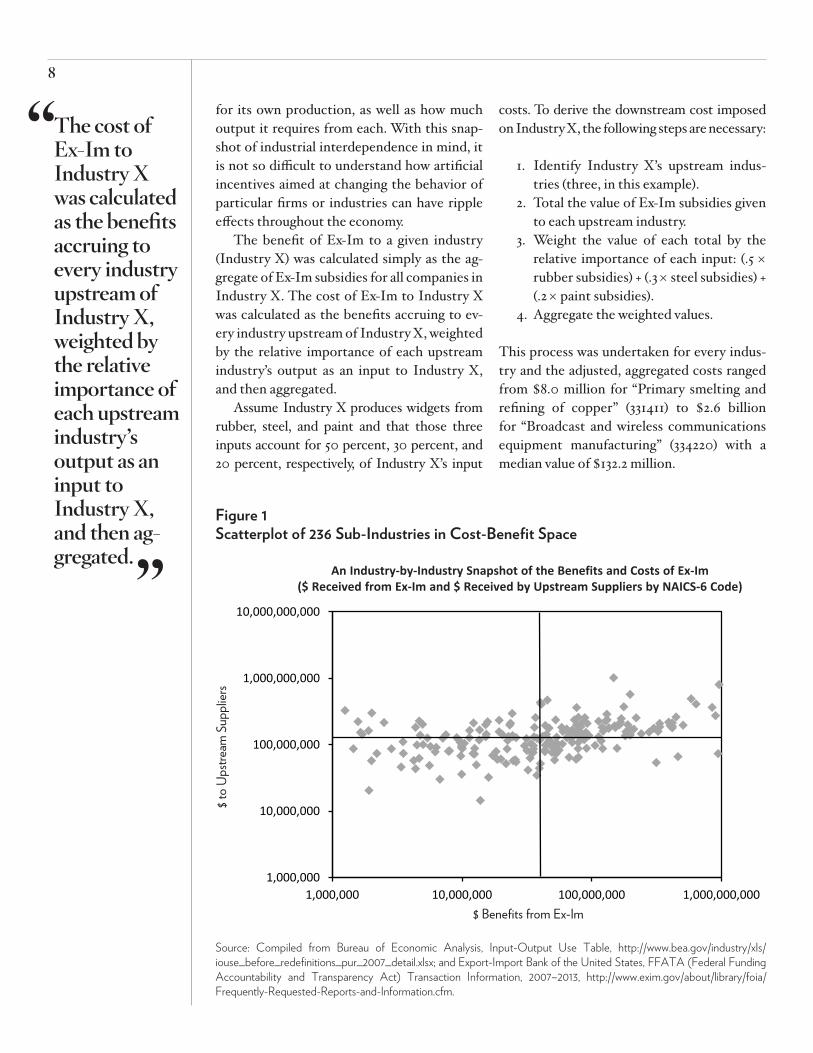

“The cost of Ex-Im to Industry X was calculated as the benefits accruing to every industry upstream of Industry X, weighted by the relative importance of each upstream industry’s output as an input to Industry X, and then ag-gregated.”

for its own production, as well as how much output it requires from each. With this snap-shot of industrial interdependence in mind, it is not so difficult to understand how artificial incentives aimed at changing the behavior of particular firms or industries can have ripple effects throughout the economy.

The benefit of Ex-Im to a given industry (Industry X) was calculated simply as the ag-gregate of Ex-Im subsidies for all companies in Industry X. The cost of Ex-Im to Industry X was calculated as the benefits accruing to ev-ery industry upstream of Industry X, weighted by the relative importance of each upstream industry’s output as an input to Industry X, and then aggregated.

Assume Industry X produces widgets from rubber, steel, and paint and that those three inputs account for 50 percent, 30 percent, and 20 percent, respectively, of Industry X’s input

costs. To derive the downstream cost imposed on Industry X, the following steps are necessary:

1. Identify Industry X’s upstream indus-tries (three, in this example).

2. Total the value of Ex-Im subsidies given to each upstream industry.

3. Weight the value of each total by the relative importance of each input: (.5 × rubber subsidies) + (.3 × steel subsidies) + (.2 × paint subsidies).

4. Aggregate the weighted values.

This process was undertaken for every indus-try and the adjusted, aggregated costs ranged from $8.0 million for “Primary smelting and refining of copper” (331411) to $2.6 billion for “Broadcast and wireless communications equipment manufacturing” (334220) with a median value of $132.2 million.

1,000,000

10,000,000

100,000,000

1,000,000,000

10,000,000,000

1,000,000 10,000,000 100,000,000 1,000,000,000

Figure 1Scatterplot of 236 Sub-Industries in Cost-Benefit Space

$ to

Upstr

eam

Sup

plier

s

$ Benefits from Ex-Im

An Industry-by-Industry Snapshot of the Benefits and Costs of Ex-Im($ Received from Ex-Im and $ Received by Upstream Suppliers by NAICS-6 Code)

Source: Compiled from Bureau of Economic Analysis, Input-Output Use Table, http://www.bea.gov/industry/xls/iouse_before_redefinitions_pur_2007_detail.xlsx; and Export-Import Bank of the United States, FFATA (Federal Funding Accountability and Transparency Act) Transaction Information, 2007–2013, http://www.exim.gov/about/library/foia/Frequently-Requested-Reports-and-Information.cfm.

9

“Using this conservative approach to estimating the often ignored costs of Ex-Im’s subsidies, 189 of the 236 non-aircraft U.S manufac-turing indus-tries can be characterized as victims.”

IDENTIFYING THE VICTIMS

Plotting these costs on the vertical axis and combining with the benefits on the horizontal axis, the scatterplot tells the first part of the story (see Figure 1).

First note that the axes are in logarithmic scales because otherwise the wide range of values for both metrics would have stretched both axes to the point of obscuring the details. Values on the X-axis represent benefits (dollar authorizations from Ex-Im) to each industry and values of the Y-axis represent costs (ad-justed, aggregated benefits to each industry’s upstream supplier industries).

The quadrants are formed by the intersec-tion of the lines drawn at the median values of each metric. Accordingly, the top-right and bottom-right quadrants are populated by in-dustries that received above-median benefits and the top-left and bottom-left quadrants show industries that received below-median benefits. Likewise, the top-left and top-right quadrants contain industries that incurred above-median costs and the lower-left and lower-right quadrants are populated by indus-tries that incurred below-median costs.

With that in mind, the 36 industries repre-sented by dots in the bottom-right quadrant are those industries that received above-medi-an benefits and incurred below-median costs. One might expect to find the “winners” of Ex-Im’s policies concentrated in this most de-sirable quadrant. The 82 industries in the top-right quadrant are those that received above-median benefits and incurred above-median costs. The 82 industries in the bottom-left re-ceived below-median benefits and incurred below-median costs. And the 36 industries in the top-left received below-median benefits and incurred above-median costs, which by most definitions would constitute the “vic-tims” of Ex-Im’s policies.

Indeed, each of the 36 industries in the top left quadrant is an Ex-Im victim, which is de-fined as an industry with negative “net” benefits (where benefit minus cost is less than $0). But the other quadrants are also heavily populated

by industries with negative net benefits. Even though their benefits were above the median benefit and their costs were below the median cost, 24 of the 36 industries in the bottom-right quadrant incurred costs in excess of benefits; 48 of 82 in the top right quadrant had negative net benefits; and the same is true of 81 of the 82 industries in the bottom left quadrant. Using this conservative approach to estimating the often ignored costs of Ex-Im’s subsidies, 189 of the 236 non-aircraft U.S manufacturing indus-tries can be characterized as victims.

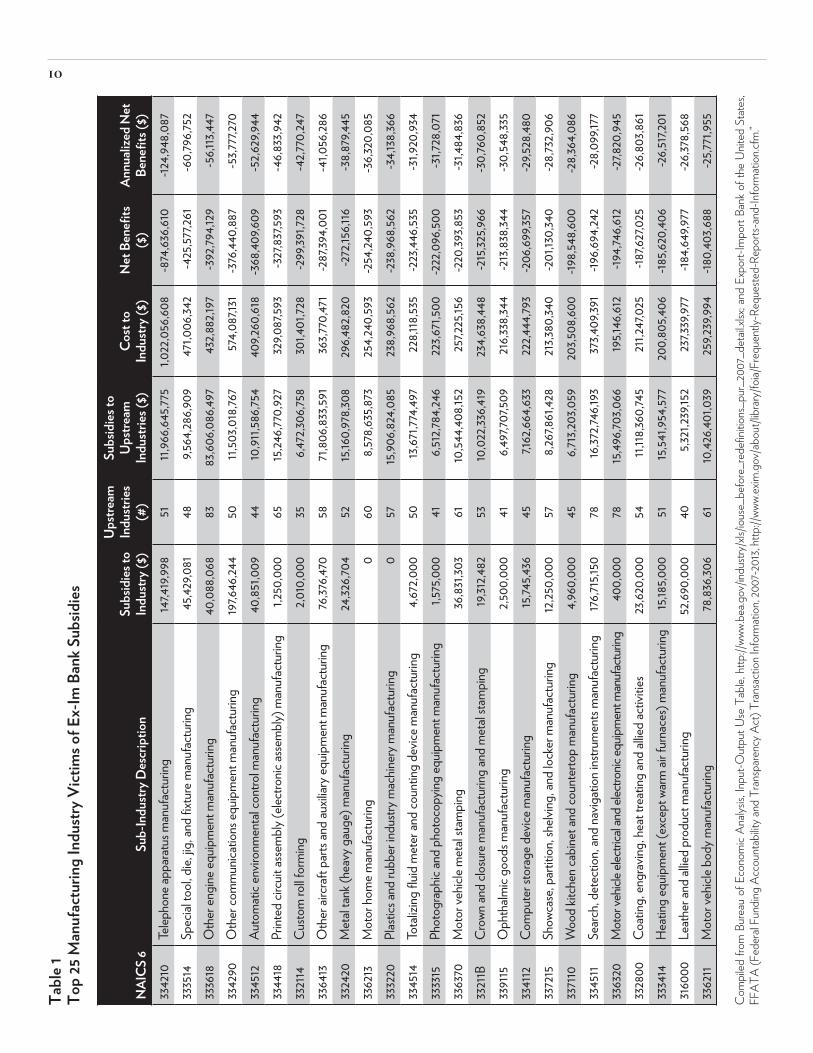

While the appendix contains data for all 236 non-aircraft manufacturing industries plotted in Figure 1, the following table reveals details for the 25 biggest victims (those incur-ring the largest net costs).

It turns out that for nearly every Ex-Im fi-nancing authorization that might advance the fortunes of a single U.S. company, there is at least one U.S. industry—and often dozens or scores of industries—whose firms are adversely impacted because supply is being diverted, market power is being shifted, and the cost of capital is being lowered for their foreign com-petition.

Telephone apparatus manufacturing (NA-ICS 334210), which falls within the comput-ers and electronics industry (NAICS 334), incurred the greatest net cost among all manu-facturers. As shown in the table, companies in the industry received $148 million of ex-port subsidies over the seven-year period. But telephone apparatus manufacturing relies on the output of 51 upstream industries, which received an aggregate total of nearly $12 bil-lion in subsidies over the period. Weighting those subsidies by the relative importance of each industry’s output to the production of telephone apparatus (and then aggregating) generates the cost of Ex-Im to manufactur-ers in this industry. With just over $1 billion in downstream costs, the net benefits of Ex-Im to this industry amount to -$875 million or a cost of $125 million per year.

A total of 189 out of 236 industries populat-ing all of the 21 broad manufacturing industries can be counted among Ex-Im’s victims. The

10Ta

ble 1

Top

25 M

anuf

actu

ring

Indu

stry V

ictim

s of E

x-Im

Ban

k Sub

sidies

NAI

CS 6

Sub-

Indu

stry D

escr

iptio

nSu

bsid

ies to

In

dustr

y ($)

Upstr

eam

In

dustr

ies

(#)

Subs

idies

to

Upstr

eam

In

dustr

ies ($

)Co

st to

In

dustr

y ($)

Net

Ben

efits

($

)An

nuali

zed

Net

Be

nefit

s ($)

3342

10Te

lepho

ne ap

para

tus m

anuf

actu

ring

147,4

19,99

851

11,96

6,645

,775

1,022

,056

,608

-874

,636,6

10-12

4,948

,087

3335

14Sp

ecial

tool,

die,

jig, a

nd fi

xtur

e man

ufac

turin

g45

,429,0

8148

9,564

,286,9

0947

1,006

,342

-425

,577,2

61-6

0,79

6,752

3336

18O

ther

engi

ne eq

uipm

ent m

anuf

actu

ring

40,0

88,0

6883

83,60

6,086

,497

432,8

82,19

7-3

92,79

4,129

-56,1

13,44

733

4290

Oth

er co

mm

unica

tions

equip

men

t man

ufac

turin

g19

7,646

,244

5011,

503,0

18,76

757

4,087

,131

-376

,440,

887

-53,7

77,27

033

4512

Auto

mat

ic en

viron

men

tal c

ontro

l man

ufac

turin

g40

,851,0

0944

10,91

1,586

,754

409,2

60,61

8-3

68,40

9,609

-52,6

29,94

433

4418

ed ci

rcuit

asse

mbl

y (ele

ctro

nic as

sem

bly)

man

ufac

turin

g1,2

50,0

0065

15,24

6,770

,927

329,0

87,59

3-3

27,83

7,593

-46,8

33,94

233

2114

Cus

tom

roll f

orm

ing2,0

10,0

0035

6,472

,306,7

5830

1,401

,728

-299

,391,7

28-4

2,770

,247

3364

13O

ther

airc

raft

parts

and

auxil

iary e

quip

men

t man

ufac

turin

g76

,376,4

7058

71,80

6,833

,591

363,7

70,47

1-2

87,39

4,001

-41,0

56,28

633

2420

Met

al ta

nk (h

eavy

gau

ge) m

anuf

actu

ring

24,32

6,704

5215

,160,

978,3

0829

6,482

,820

-272

,156,1

16-3

8,879

,445

3362

13M

otor

hom

e man

ufac

turin

g0

608,5

78,63

5,873

254,

240,

593

-254

,240,

593

-36,3

20,0

8533

3220

Plas

tics a

nd ru

bber

indu

stry m

achin

ery m

anuf

actu

ring

057

15,90

6,824

,085

238,9

68,56

2-2

38,96

8,562

-34,1

38,36

633

4514

Tota

lizing

fluid

met

er an

d co

untin

g de

vice m

anuf

actu

ring

4,672

,000

5013

,671,7

74,49

722

8,118

,535

-223

,446,5

35-3

1,920

,934

3333

15Ph

otog

raph

ic an

d ph

otoc

opyin

g eq

uipm

ent m

anuf

actu

ring

1,575

,000

416,5

12,78

4,24

622

3,671

,500

-222

,096

,500

-31,7

28,0

7133

6370

Mot

or ve

hicle

met

al sta

mpi

ng36

,831,3

0361

10,54

4,408

,152

257,2

25,15

6-2

20,39

3,853

-31,4

84,83

633

211B

Cro

wn an

d clo

sure

man

ufac

turin

g an

d m

etal

stam

ping

19,31

2,482

5310

,022

,336,4

1923

4,638

,448

-215

,325,9

66-3

0,76

0,85

233

9115

Oph

thalm

ic go

ods m

anuf

actu

ring

2,500

,000

416,4

97,70

7,509

216,3

38,34

4-2

13,83

8,344

-30,

548,3

3533

4112

Com

pute

r sto

rage

dev

ice m

anuf

actu

ring

15,74

5,436

457,1

62,66

4,633

222,4

44,79

3-2

06,69

9,357

-29,5

28,48

033

7215

Show

case

, par

tition

, she

lving

, and

lock

er m

anuf

actu

ring

12,25

0,00

057

8,26

7,861

,428

213,3

80,34

0-2

01,13

0,34

0-2

8,732

,906

3371

10W

ood

kitch

en ca

bine

t and

coun

terto

p m

anuf

actu

ring

4,960

,000

456,7

13,20

3,059

203,5

08,60

0-19

8,548

,600

-28,3

64,0

8633

4511

Sear

ch, d

etec

tion,

and

navig

ation

instr

umen

ts m

anuf

actu

ring

176,7

15,15

078

16,37

2,746

,193

373,4

09,39

1-19

6,694

,242

-28,0

99,17

733

6320

Mot

or ve

hicle

electr

ical a

nd el

ectro

nic eq

uipm

ent m

anuf

actu

ring

400,

000

7815

,496,7

03,0

6619

5,146

,612

-194,7

46,61

2-2

7,820

,945

3328

00C

oatin

g, en

grav

ing, h

eat t

reat

ing an

d all

ied ac

tivitie

s23

,620,

000

5411,

118,36

0,74

521

1,247

,025

-187,6

27,0

25-2

6,803

,861

3334

14He

ating

equip

men

t (ex

cept

war

m ai

r fur

nace

s) m

anuf

actu

ring

15,18

5,000

5115

,541,9

54,57

720

0,80

5,406

-185,6

20,40

6-2

6,517,

201

3160

00Le

athe

r and

allie

d pr

oduc

t man

ufac

turin

g52

,690,

000

405,3

21,23

9,152

237,3

39,97

7-18

4,649

,977

-26,3

78,56

833

6211

Mot

or ve

hicle

body

man

ufac

turin

g78

,836,3

0661

10,42

6,401

,039

259,2

39,99

4-18

0,40

3,688

-25,7

71,95

5

Com

piled

from

Bur

eau

of E

cono

mic

Ana

lysis,

Inpu

t-Out

put U

se T

able,

http

://ww

w.be

a.gov

/indu

stry/

xls/io

use_

befo

re_r

edef

initio

ns_p

ur_2

007_

deta

il.xlsx

; and

Exp

ort-I

mpo

rt Ba

nk o

f the

Unit

ed S

tate

s, FF

ATA

(Fed

eral

Fund

ing A

ccou

ntab

ility a

nd T

rans

pare

ncy A

ct) T

rans

actio

n In

form

atio

n, 20

07-2

013,

http

://ww

w.ex

im.g

ov/a

bout

/libr

ary/

foia/

Freq

uent

ly-Re

ques

ted-

Repo

rts-a

nd-In

form

atio

n.cfm

.”

11

“One would be hard-pressed to find a better example of a policy that produces a few winners at the expense of a multitude of losers.”

annual cost for these 189 victims was an aggre-gated $2.8 billion or $14.7 million per industry. There are hundreds and probably thousands of U.S. companies scattered over these 189 in-dustries that produce in the United States, em-ploy American workers, pay federal, state, and local taxes, and contribute to the social fabric of the communities in which they operate. But they are competitively disadvantaged—victim-ized—by Ex-Im’s provision of subsidies that benefit their foreign competitors and reduce their leverage vis-à-vis their U.S. suppliers. These are the unseen consequences—the col-lateral damage—of Ex-Im’s mission.

Meanwhile, a total of 47 of 236 manufac-turing sub-industries populating 13 of 21 broad manufacturing industries can be counted among Ex-Im’s “winners.” Between 2007 and 2013, gross Ex-Im benefits of $42.8 billion and downstream costs of $13.3 billion accrued to these 47 winners, who realized a net benefit of $29.5 billion or $4.2 billion per year or $89.8 million per sub-industry per year as a result of Ex-Im.

In essence, Ex-Im policies amount to a net tax of $2.8 billion per year on 189 sub-indus-tries ($15 million per industry) and a net sub-sidy of $4.2 billion per year to 47 sub-industries ($90 million per industry). For the winners, the downstream costs amount to less than one-third of the benefits received; for the los-ers, who outnumber the winners by a margin of 4-to-1, the costs are more than triple the benefits. One would be hard-pressed to find a better example of a policy that produces a few winners at the expense of a multitude of losers.

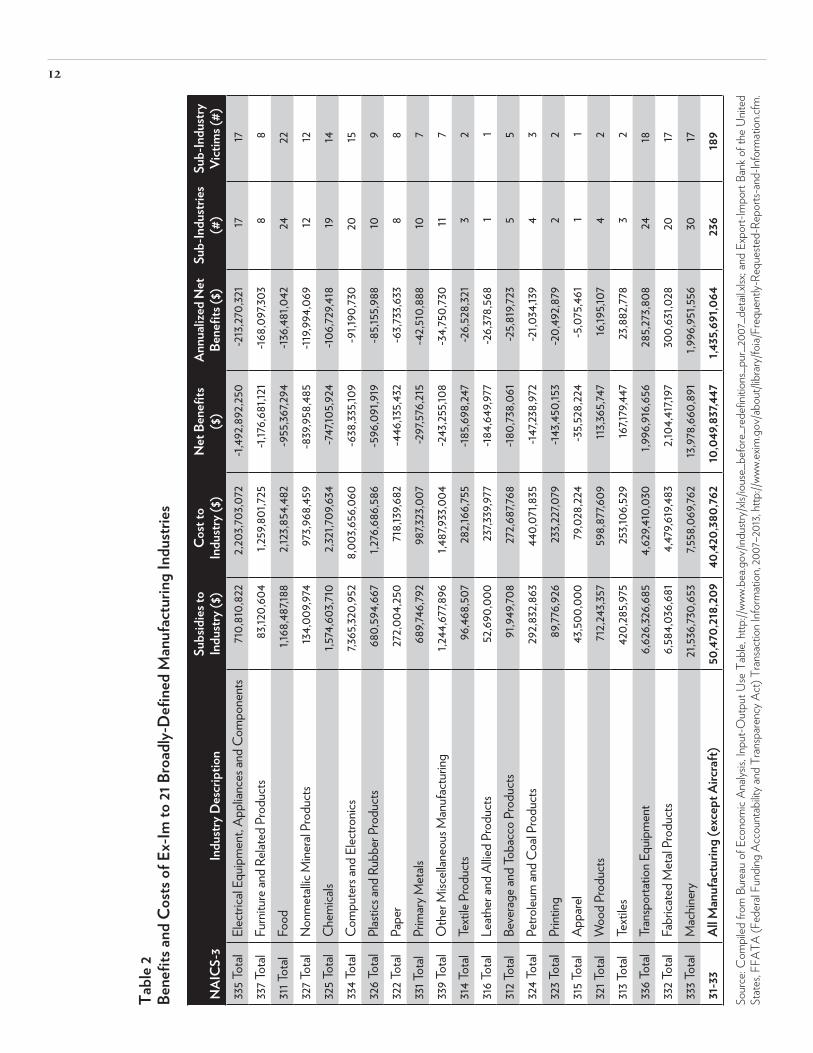

Table 2 presents the results consolidated at the 3-digit NAICS level to provide more of a bird’s-eye view of the benefits received and costs incurred by industry. The data are pre-sented in ascending order of “net benefits” so that the most heavily-burdened industries appear at the top. Sixteen of the 21 broad manufacturing industries experienced costs in excess of benefits over the seven-year period with “Electrical equipment, appliance and components” manufacturers (NAICS 335) in-curring the biggest loss at $1.5 billion. Each of

the 17 sub-industries within NAICS 335 expe-rienced losses over the period.

Eight of the 21 broad manufacturing indus-tries consist only of sub-industries that are Ex-Im victims: Electrical equipment, appliance and components (335); furniture and related products (337); nonmetallic mineral products (327); paper (322); leather and allied products (316); beverage and tobacco products (312); printing (323); and apparel (315).

Of the five broad industries that experi-enced positive net benefits, machinery pro-ducers (NAICS 333) fared best. However, within the machinery industry—as well as within the other “winning” industries—most of the sub-industries experienced losses. Out of 30 machinery sub-industries, 17 experi-enced losses; two-thirds of transportation equipment sub-industries and 85 percent of fabricated metal product sub-industries also incurred net losses.

These figures would all seem to confirm that Ex-Im helps some companies in some in-dustries, but at great cost to industries across the manufacturing spectrum, which is to say Ex-Im amounts to an exercise in “picking win-ners and losers.”

VICTIMS STATE-BY-STATE

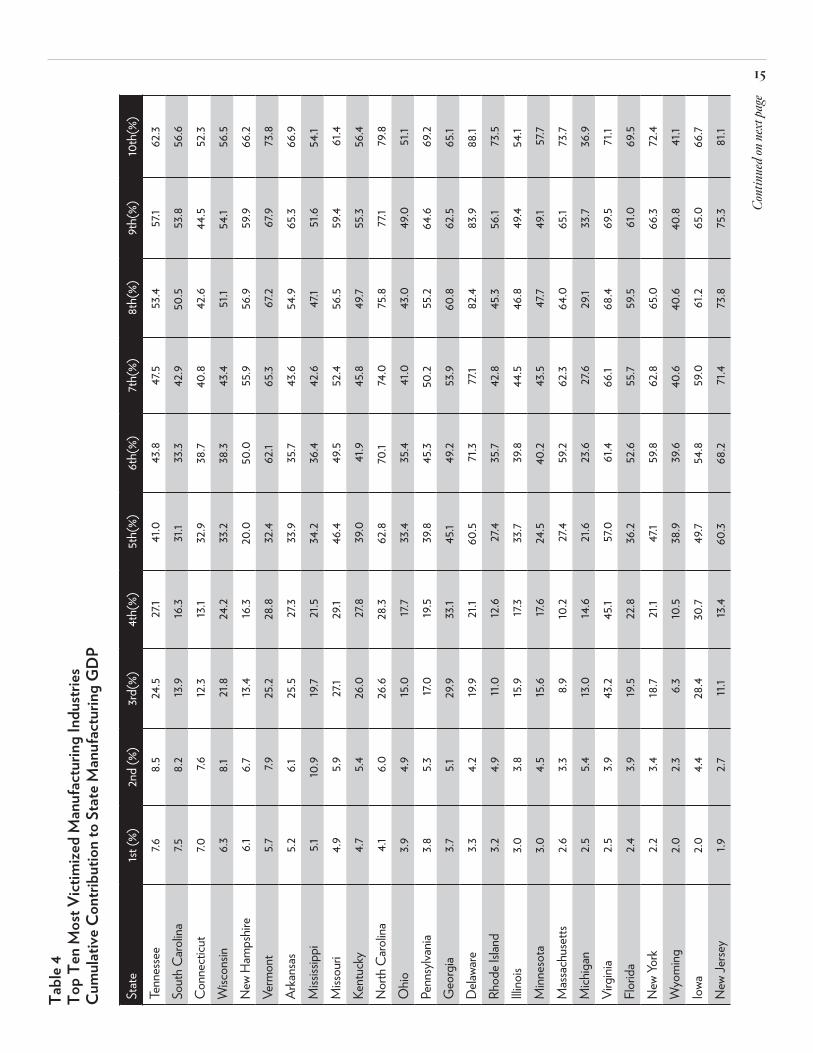

The victims of Ex-Im are scattered across industries and across U.S. states. But every broadly defined industry and every state can count victims among its manufacturing firms. Tables 3 and 4 provide overviews of the manu-facturing victims by state. Table 3 ranks the contribution of the 10 most victimized manu-facturing industries to each state’s manufac-turing GDP. The industry accounting for the most manufacturing GDP in each state is as-signed a value of “1.” The most important man-ufacturing industry was a top-10 victim for 33 states and the first or second most important industry was a top-10 victim in 47 states.

Table 4 presents the cumulative contribu-tion to each state’s manufacturing GDP of the 10 most victimized manufacturing industries. Field “1st” represents the contribution of “Elec-

12

Tabl

e 2Be

nefit

s and

Cos

ts of

Ex-

Im to

21 B

road

ly-D

efin

ed M

anuf

actu

ring

Indu

stries

NAI

CS-3

Indu

stry D

escr

iptio

nSu

bsid

ies to

In

dustr

y ($)

Cost

to

Indu

stry (

$)N

et B

enef

its

($)

Annu

alize

d N

et

Bene

fits (

$)Su

b-In

dustr

ies

(#)

Sub-

Indu

stry

Vict

ims (

#)33

5 Tot

alEl

ectri

cal E

quip

men

t, Ap

plian

ces a

nd C

ompo

nent

s71

0,81

0,82

22,2

03,70

3,072

-1,49

2,892

,250

-213

,270,

321

1717

337 T

otal

Furn

iture

and

Relat

ed P

rodu

cts

83,12

0,60

41,2

59,80

1,725

-1,17

6,681

,121

-168,0

97,30

38

831

1 Tot

alFo

od1,1

68,48

7,188

2,123

,854,4

82-9

55,36

7,294

-136,4

81,0

4224

2232

7 Tot

alN

onm

etall

ic M

inera

l Pro

duct

s13

4,009

,974

973,9

68,45

9-8

39,95

8,485

-119,9

94,0

6912

1232

5 Tot

alC

hem

icals

1,574

,603,7

102,3

21,70

9,634

-747

,105,9

24-10

6,729

,418

1914

334

Tota

lC

ompu

ters

and

Elec

tronic

s7,3

65,32

0,95

28,0

03,65

6,060

-638

,335,1

09-9

1,190

,730

2015

326 T

otal

Plas

tics a

nd R

ubbe

r Pro

duct

s68

0,59

4,667

1,276

,686,5

86-5

96,0

91,91

9-8

5,155

,988

109

322 T

otal

Pape

r27

2,004

,250

718,1

39,68

2-4

46,13

5,432

-63,7

33,63

38

833

1 Tot

alPr

imar

y Met

als68

9,746

,792

987,3

23,0

07-2

97,57

6,215

-42,5

10,88

810

733

9 Tot

alO

ther

Misc

ellan

eous

Man

ufac

turin

g1,2

44,67

7,896

1,487

,933,0

04-2

43,25

5,108

-34,7

50,73

011

731

4 Tot

alTe

xtile

Pro

duct

s96

,468,5

0728

2,166

,755

-185,6

98,24

7-2

6,528

,321

32

316 T

otal

Leat

her a

nd A

llied

Prod

ucts

52,69

0,00

023

7,339

,977

-184,6

49,97

7-2

6,378

,568

11

312 T

otal

Beve

rage

and

Toba

cco

Prod

ucts

91,94

9,708

272,6

87,76

8-18

0,73

8,061

-25,8

19,72

35

532

4 Tot

alPe

troleu

m an

d C

oal P

rodu

cts

292,8

32,86

344

0,07

1,835

-147,2

38,97

2-2

1,034

,139

43

323 T

otal

ing89

,776,9

2623

3,227

,079

-143,4

50,15

3-2

0,49

2,879

22

315 T

otal

Appa

rel

43,50

0,00

079

,028

,224

-35,5

28,22

4-5

,075

,461

11

321 T

otal

Woo

d Pr

oduc

ts71

2,243

,357

598,8

77,60

9113

,365,7

4716

,195,1

074

231

3 Tot

alTe

xtile

s42

0,28

5,975

253,1

06,52

916

7,179

,447

23,88

2,778

32

336 T

otal

Tran

spor

tatio

n Equ

ipm

ent

6,626

,326,6

854,6

29,41

0,03

01,9

96,91

6,656

285,2

73,80

824

1833

2 Tot

alFa

brica

ted

Met

al Pr

oduc

ts6,5

84,0

36,68

14,4

79,61

9,483

2,104

,417,1

9730

0,63

1,028

2017

333 T

otal

Mac

hiner

y21

,536,7

30,65

37,5

58,0

69,76

213

,978,6

60,89

11,9

96,95

1,556

3017

31-3

3Al

l Man

ufac

turin

g (e

xcep

t Airc

raft)

50,47

0,21

8,20

940

,420,

380,

762

10,0

49,8

37,44

71,4

35,6

91,0

6423

618

9

Sour

ce: C

ompi

led fr

om B

urea

u of

Eco

nom

ic A

nalys

is, In

put-O

utpu

t Use

Tab

le, h

ttp://

www.

bea.g

ov/in

dustr

y/xls

/ious

e_be

fore

_red

efini

tions

_pur

_200

7_de

tail.x

lsx; a

nd E

xpor

t-Im

port

Bank

of t

he U

nited

St

ates

, FFA

TA (F

eder

al Fu

nding

Acc

ount

abilit

y and

Tra

nspa

renc

y Act

) Tra

nsac

tion

Info

rmat

ion,

2007

–201

3, ht

tp://

www.

exim

.gov

/abo

ut/li

brar

y/fo

ia/Fr

eque

ntly-

Requ

este

d-Re

ports

-and

-Info

rmat

ion.c

fm.

13Ta

ble 3

Top

Ten

Mos

t Vict

imize

d M

anuf

actu

ring

Indu

stries

(Lef

t to

Righ

t) Ra

nk o

f Con

tribu

tion

to S

tate

Man

ufac

turin

g G

DP

Elec

trica

l Equ

ipm

ent,

Appl

iance

s and

C

ompo

nent

s

Furn

iture

an

d Re

lated

Pr

oduc

ts

Food

, Be

vera

ge,

Toba

cco

Non

met

allic

Mine

ral

Prod

ucts

Che

mica

ls

Com

pute

rs an

d

Elec

tronic

s

Plas

tics a

nd

Rubb

er

Prod

ucts

Pape

rPr

imar

y M

etals

Oth

er

Misc

ellan

eous

M

anuf

actu

ring

33

533

731

1,312

327

325

334

326

322

331

339

Alab

ama

1514

813

210

95

317

Alas

ka17

132

310

78

1816

12Ar

izona

1314

49

31

1015

75

Arka

nsas

817

113

614

52

415

Cali

forn

ia10

164

132

19

1417

5C

olora

do12

142

93

110

1713

4C

onne

cticu

t5

168

142

69

1210

4D

elawa

re8

162

131

34

510

6Fl

orid

a12

152

93

110

816

5G

eorg

ia11

171

122

107

516

13Ha

waii

1610

23

512

917

187

Idah

o12

142

133

17

916

11Illi

nois

1016

314

26

813

117

Indi

ana

1512

714

111

916

45

Iowa

129

110

25

711

815

Kans

as11

152

124

78

1614

13Ke

ntuc

ky8

172

133

119

105

16Lo

uisian

a16

173

92

1410

68

13M

aine

1716

315

46

81

1812

Mar

yland

1614

311

12

413

1210

Mas

sach

uset

ts10

156

122

18

1113

4M

ichig

an10

94

135

127

146

8M

innes

ota

1216

314

71

119

175

Miss

issip

pi10

74

161

156

1211

14M

issou

ri7

171

132

1012

811

14

Cont

inue

d on n

ext p

age

14El

ectri

cal E

quip

men

t, Ap

plian

ces a

nd

Com

pone

nts

Furn

iture

an

d Re

lated

Pr

oduc

ts

Food

, Be

vera

ge,

Toba

cco

Non

met

allic

Mine

ral

Prod

ucts

Che

mica

ls

Com

pute

rs an

d

Elec

tronic

s

Plas

tics a

nd

Rubb

er

Prod

ucts

Pape

rPr

imar

y M

etals

Oth

er

Misc

ellan

eous

M

anuf

actu

ring

Mon

tana

1513

25

79

1219

178

Neb

rask

a14

151

112

87

1310

4N

evad

a14

152

65

47

1310

1N

ew H

amps

hire

618

410

81

716

95

New

Jerse

y12

142

111

38

1013

4N

ew M

exico

1316

37

41

1211

188

New

York

1316

211

13

712

156

Nor

th C

aroli

na5

112

131

36

1215

9N

orth

Dak

ota

1713

24

107

915

1814

Ohio

1016

511

113

814

712

Okla

hom

a14

184

85

76

1112

13O

rego

n15

162

119

112

75

8Pe

nnsy

lvania

1116

213

16

98

410

Rhod

e Isla

nd11

148

152

46

123

1So

uth

Car

olina

717

813

114

36

1112

Sout

h D

akot

a15

93

84

710

1314

1Te

nnes

see

517

212

311

97

108

Texa

s13

166

112

39

1410

12Ut

ah16

126

102

513

111

3Ve

rmon

t5

122

98

110

1317

4Vi

rgini

a9

161

132

75

1017

15W

ashin

gton

1617

212

73

148

119

Wes

t Virg

inia

1516

119

113

717

210

Wisc

onsin

616

213

49

85

1214

Wyo

ming

713

54

211

819

1615

Unite

d St

ates

1316

314

12

1012

119

Sour

ce: C

ompi

led fr

om B

urea

u of E

cono

mic

Ana

lysis,

Inpu

t-Out

put U

se T

able,

http

://ww

w.be

a.gov

/indu

stry/

xls/io

use_

befo

re_r

edef

initio

ns_p

ur_2

007_

deta

il.xlsx

; Exp

ort-I

mpo

rt Ba

nk o

f the

Unit

ed S

tate

s, FF

ATA

(Fed

eral

Fund

ing A

ccou

ntab

ility

and

Tran

spar

ency

Act

) Tra

nsac

tion

Info

rmat

ion,

2007

–201

3, ht

tp://

www.

exim

.gov

/abo

ut/li

brar

y/fo

ia/Fr

eque

ntly-

Requ

este

d-Re

ports

-and

-Info

rmat

ion.c

fm; a

nd

Bure

au o

f Eco

nom

ic A

nalys

is, G

DP

by S

tate

, Man

ufac

turin

g (in

tera

ctive

tabl

e), h

ttp://

www.

bea.g

ov/iT

able/

iTab

le.cf

m?re

qid=

70&s

tep=

1&isu

ri=1&

acrd

n=1#

reqi

d=70

&ste

p=6&

isuri=

1&70

03=9

00&7

004=

nai

cs&7

005=

12&7

001=

1900

&700

2=1&

7090

=70.

Tabl

e 3 Contin

ued

15Ta

ble 4

Top

Ten

Mos

t Vict

imize

d M

anuf

actu

ring

Indu

stries

Cu

mul

ative

Con

tribu

tion

to S

tate

Man

ufac

turin

g G

DP

Stat

e1st

(%)

2nd

(%)

3rd(

%)4t

h(%)

5th(

%)6t

h(%)

7th(

%)8t

h(%)

9th(

%)10

th(%

)Te

nnes

see

7.68.5

24.5

27.1

41.0

43.8

47.5

53.4

57.1

62.3

Sout

h C

aroli

na7.5

8.2

13.9

16.3

31.1

33.3

42.9

50.5

53.8

56.6

Con

nect

icut

7.07.6

12.3

13.1

32.9

38.7

40.8

42.6

44.5

52.3

Wisc

onsin

6.38.1

21.8

24.2

33.2

38.3

43.4

51.1

54.1

56.5

New

Ham

pshir

e6.1

6.713

.416

.320

.050

.055

.956

.959

.966

.2Ve

rmon

t5.7

7.925

.228

.832

.462

.165

.367

.267

.973

.8Ar

kans

as5.2

6.125

.527

.333

.935

.743

.654

.965

.366

.9M

ississ

ippi

5.110

.919

.721

.534

.236

.442

.647

.151

.654

.1M

issou

ri4.9

5.927

.129

.146

.449

.552

.456

.559

.461

.4Ke

ntuc

ky4.7

5.426

.027

.839

.041

.945

.849

.755

.356

.4N

orth

Car

olina

4.16.0

26.6

28.3

62.8

70.1

74.0

75.8

77.1

79.8

Ohio

3.94.9

15.0

17.7

33.4

35.4

41.0

43.0

49.0

51.1

Penn

sylva

nia3.8

5.317.

019

.539

.845

.350

.255

.264

.669

.2G

eorg

ia3.7

5.129

.933

.145

.149

.253

.960

.862

.565

.1D

elawa

re3.3

4.2

19.9

21.1

60.5

71.3

77.1

82.4

83.9

88.1

Rhod

e Isla

nd3.2

4.911.

012

.627

.435

.742

.845

.356

.173

.5Illi

nois

3.03.8

15.9

17.3

33.7

39.8

44.5

46.8

49.4

54.1

Minn

esot

a3.0

4.515

.617.

624

.540

.243

.547

.749

.157

.7M

assa

chus

etts

2.63.3

8.910

.227

.459

.262

.364

.065

.173

.7M

ichig

an2.5

5.413

.014

.621

.623

.627

.629

.133

.736

.9Vi

rgini

a2.5

3.943

.245

.157

.061

.466

.168

.469

.571

.1Fl

orid

a2.4

3.919

.522

.836

.252

.655

.759

.561

.069

.5N

ew Yo

rk2.2

3.418

.721

.147

.159

.862

.865

.066

.372

.4W

yom

ing2.0

2.36.3

10.5

38.9

39.6

40.6

40.6

40.8

41.1

Iowa

2.04.4

28.4

30.7

49.7

54.8

59.0

61.2

65.0

66.7

New

Jerse

y1.9

2.711.

113

.460

.368

.271

.473

.875

.381

.1

Cont

inue

d on n

ext p

age

16St

ate

1st (%

)2n

d (%

)3r

d(%)

4th(

%)5t

h(%)

6th(

%)7t

h(%)

8th(

%)9t

h(%)

10th

(%)

Alab

ama

1.83.8

9.611.

624

.027

.331

.439

.050

.752

.2C

olora

do1.7

3.218

.922

.236

.659

.461

.562

.263

.872

.5Ka

nsas

1.72.6

18.3

19.9

30.7

35.5

39.6

40.2

41.1

42.6

Utah

1.54.0

11.0

14.0

27.5

36.8

39.1

41.8

61.4

72.4

Cali

forn

ia1.5

2.412

.413

.631

.758

.960

.862

.062

.969

.5So

uth

Dak

ota

1.54.1

19.0

21.8

33.6

37.3

39.7

41.2

42.7

62.8

Okla

hom

a1.4

1.911.

515

.822

.827

.632

.735

.837

.939

.8Ar

izona

1.42.6

9.712

.019

.951

.753

.954

.959

.765

.6N

evad

a1.4

2.512

.417.

122

.830

.234

.335

.737

.580

.6N

ebra

ska

1.11.9

27.5

28.9

53.0

55.4

59.3

60.4

62.0

71.9

Idah

o1.1

2.025

.626

.734

.475

.677

.979

.980

.581

.6Te

xas

1.11.8

6.98.4

30.6

42.3

44.3

45.3

47.2

48.5

Wes

t Virg

inia

1.02.0

4.68.3

52.4

53.8

58.0

58.7

67.8

71.3

Indi

ana

1.02.5

8.2

9.539

.041

.044

.145

.052

.559

.9M

aryla

nd0.

81.9

15.7

17.6

50.5

70.4

75.0

76.2

77.8

79.8

Was

hingt

on0.

81.4

8.410

.012

.619

.520

.823

.324

.926

.9N

ew M

exico

0.8

1.39.8

12.0

16.5

66.8

67.7

69.0

69.4

71.5

Ore

gon

0.6

1.04.9

5.86.9

84.9

85.7

87.3

89.3

90.6

Main

e0.

51.5

16.6

18.1

27.3

33.8

38.0

53.3

53.7

55.9

Mon

tana

0.4

1.310

.314

.518

.120

.020

.921

.021

.324

.6Ha

waii

0.3

2.133

.939

.243

.445

.046

.847

.147

.150

.2N

orth

Dak

ota

0.3

1.525

.531

.535

.139

.243

.043

.543

.644

.5Lo

uisian

a0.

30.

44.3

5.443

.944

.345

.147

.848

.949

.4Al

aska

0.1

0.5

35.3

38.9

39.5

40.8

41.6

41.6

41.8

42.2

Unite

d St

ates

2.63.8

15.2

17.1

35.3

47.7

51.1

53.7

56.9

61.1

Sour

ce: C

ompi

led fr

om B

urea

u of E

cono

mic

Ana

lysis,

Inpu

t-Out

put U

se T

able.

http

://ww

w.be

a.gov

/indu

stry/

xls/io

use_

befo

re_r

edef

initio

ns_p

ur_2

007_

deta

il.xlsx

; Exp

ort-I

mpo

rt Ba

nk o

f the

Unit

ed S

tate

s, FF

ATA

(Fed

eral

Fund

ing A

ccou

ntab

ility

and

Tran

spar

ency

Act

) Tra

nsac

tion

Info

rmat

ion,

2007

–201

3, ht

tp://

www.

exim

.gov

/abo

ut/li

brar

y/fo

ia/Fr

eque

ntly-

Requ

este

d-Re

ports

-and

-Info

rmat

ion.c

fm; a

nd

Bure

au o

f Eco

nom

ic A

nalys

is, G

DP

by S

tate

, Man

ufac

turin

g (in

tera

ctive

tabl

e), h

ttp://

www.

bea.g

ov/iT

able/

iTab

le.cf

m?re

qid=

70&s

tep=

1&isu

ri=1&

acrd

n=1#

reqi

d=70

&ste

p=6&

isuri=

1&70

03=9

00&7

004=

nai

cs&7

005=

12&7

001=

1900

&700

2=1&

7090

=70.

Tabl

e 4 Contin

ued

17

“If the arguments against reauthoriza-tion were not already persuasive enough, the costs imposed on unwitting downstream U.S. industries by Export-Import Bank subsidies is perhaps the most compelling reason to shut down the Bank.”

trical equipment, appliance and components” manufacturing (NAICS 335)—the biggest vic-tim—to each state’s manufacturing value-add-ed. So for Tennessee, manufacturing industry 335 (the 1st largest victim) accounted for 7.6 per-cent of the state’s manufacturing value added. NAICS 335 accounted for 7.5 percent of South Carolina’s manufacturing value added. Field “2nd” represents the cumulative contribution of the first and second largest victims of Ex-Im—the second largest (with reference to Table 3) being NAICS 337, “Furniture and related products.” Field “3rd” is the cumulative contri-bution of the top three victims to each state’s manufacturing value-added, and so on.

Table 4 is sorted in descending order of “1st” (the largest victim’s contributions to the respective state’s manufacturing value-added). States appearing near the top of the table are likely most ill-affected by the quiet imposi-tions thrust upon their electrical equipment producers in the form of heightened competi-tion at home and abroad from foreign produc-ers benefiting from U.S. taxpayer subsidies.

But to get a better picture of the states that are likely paying the highest price for Ex-Im, look at the “5th” column or the “10th”column, which reveal the cumulative contributions of the top 5 and top 10 biggest victims, respec-tively, to each state’s manufacturing value-added. The top-5 victims cumulatively ac-count for 50 percent of more of manufacturing value-added in seven U.S. states: North Caro-lina (62.8%), Delaware (60.5%), New Jersey (60.3%), Virginia (57.0%), Nebraska (53.0%), West Virginia (52.4%), and Maryland (50.5%). The top 10 victims cumulatively account for two-thirds or more of manufacturing value-added in 22 states.

For 17 U.S. states, the largest manufacturing industry was a top-5 Ex-Im victim. The chemi-cal industry—the fifth largest Ex-Im victim—is the largest manufacturing industry in 11 states. The data reveal countless compelling facts about the costs of Ex-Im and which industries and states bear them.

It is evident from this analysis that al-though Ex-Im’s subsidies may benefit certain

industries and states in the short-run, they ad-versely affect other industries and states. The fact that Table 2 shows positive net benefits, overall, does nothing to mitigate the fact that Ex-Im’s operations essentially rob Peter to pay Paul. In fact, that table shows that for every dollar of subsidies doled out to the winners, $0.80 is imposed as a downstream cost on the victims ($50 billion in benefits vs. $40 billion in adjusted costs), which renders Ex-Im a very inefficient form of industrial policy.

CONCLUSION

In their efforts to win reauthorization from Congress, supporters of the Export-Import Bank rely on exaggerated claims about the Bank’s benefits, while ignoring its costs. Ex-Im pays for itself, the argument goes, as though that claim accounts for the opportunity costs, intra-industry costs, and downstream industry costs.

Realistically, Ex-Im financing helps two sets of companies (in the short-run): U.S. firms whose export prices are subsidized by below-market-rate financing and the foreign firms that purchase those subsidized exports. Those same transactions impose costs on two differ-ent sets of companies: competing U.S. firms in the same industry, who do not get Ex-Im back-ing, and U.S. firms in downstream industries, whose foreign competition is now benefitting from reduced capital costs courtesy of U.S. government subsidies.

The facts are that Ex-Im policies reward some companies and penalize many others in the process. The victims of Ex-Im’s policies populate 189 of 236 non-aircraft manufactur-ing sub-industries and all of the 21 broad man-ufacturing industry categories. The costs are borne in every U.S. state and in many of them the victims are crucial industries. The top-5 victims cumulatively account for 50 percent or more of manufacturing value-added in 7 U.S. states, and the top 10 victims cumulatively ac-count for two-thirds or more of manufactur-ing value-added in 22 states. In 17 U.S. states, the largest manufacturing industry was a top-5 Ex-Im victim.

18

This analysis took into quantitative consid-eration only the downstream costs, leaving the intra-industry and opportunity costs alone. The overall costs of Ex-Im are thus grossly un-derstated. If the arguments against reauthori-

zation were not already persuasive enough, the costs imposed on unwitting downstream U.S. industries by Export-Import Bank subsidies is perhaps the most compelling reason to shut down the Bank.

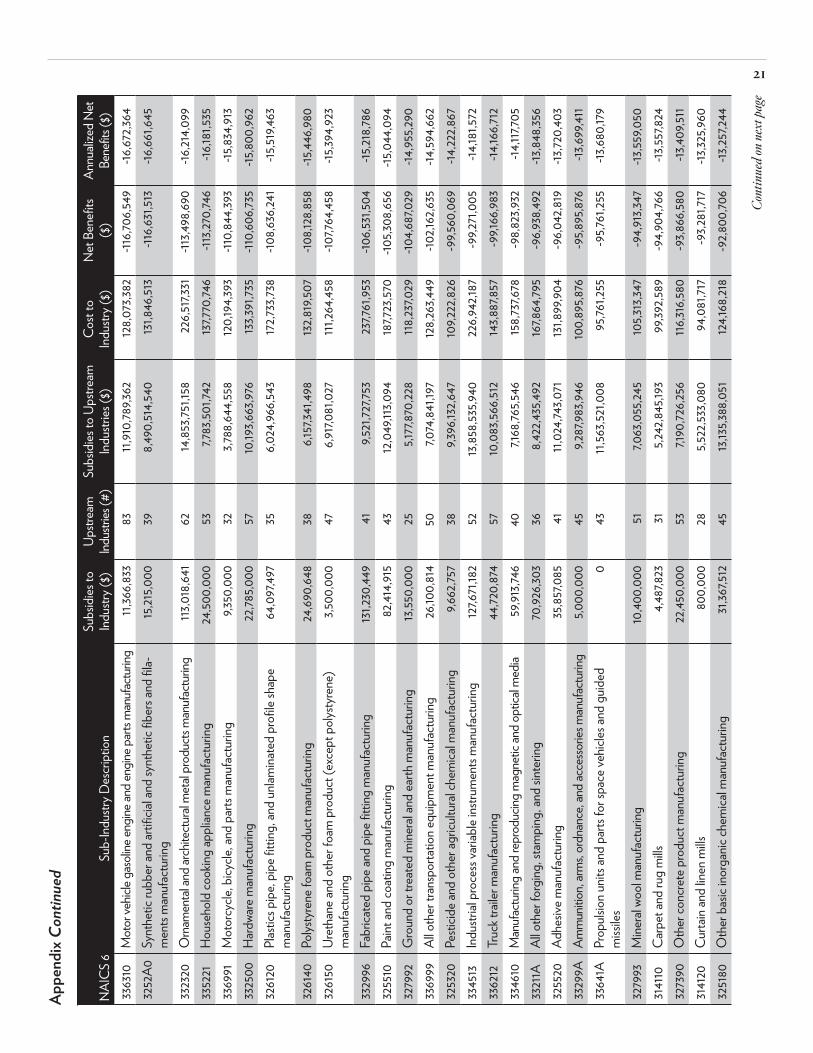

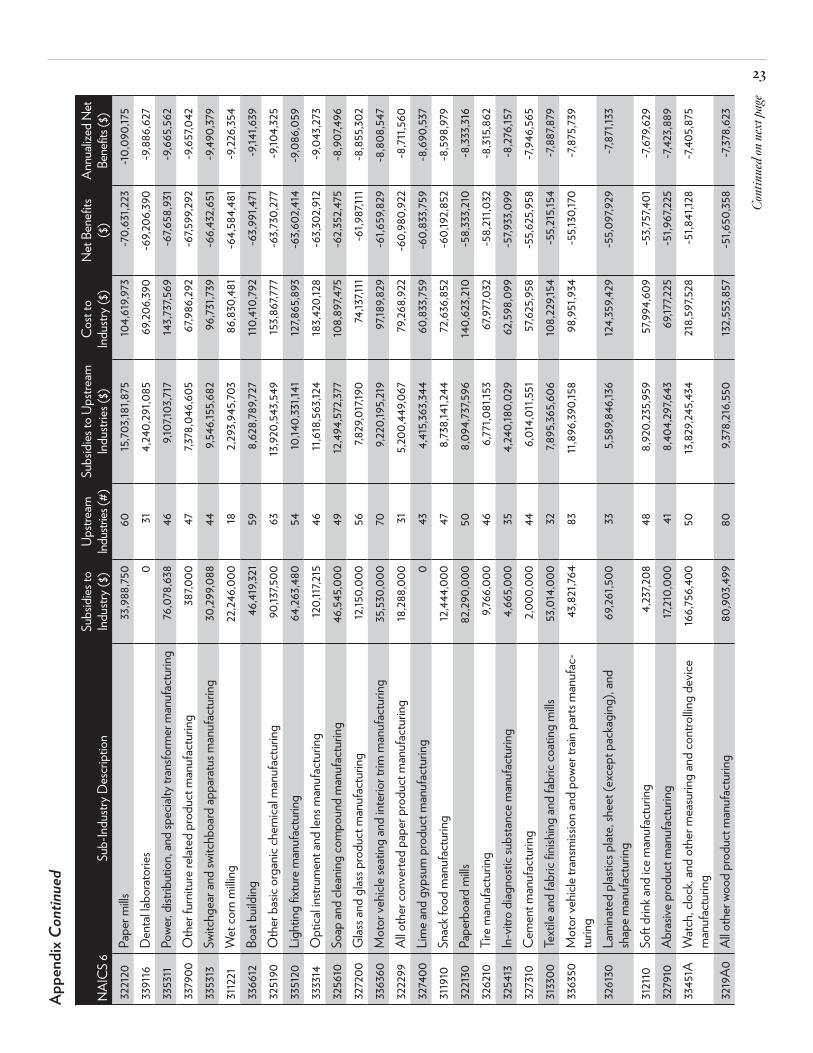

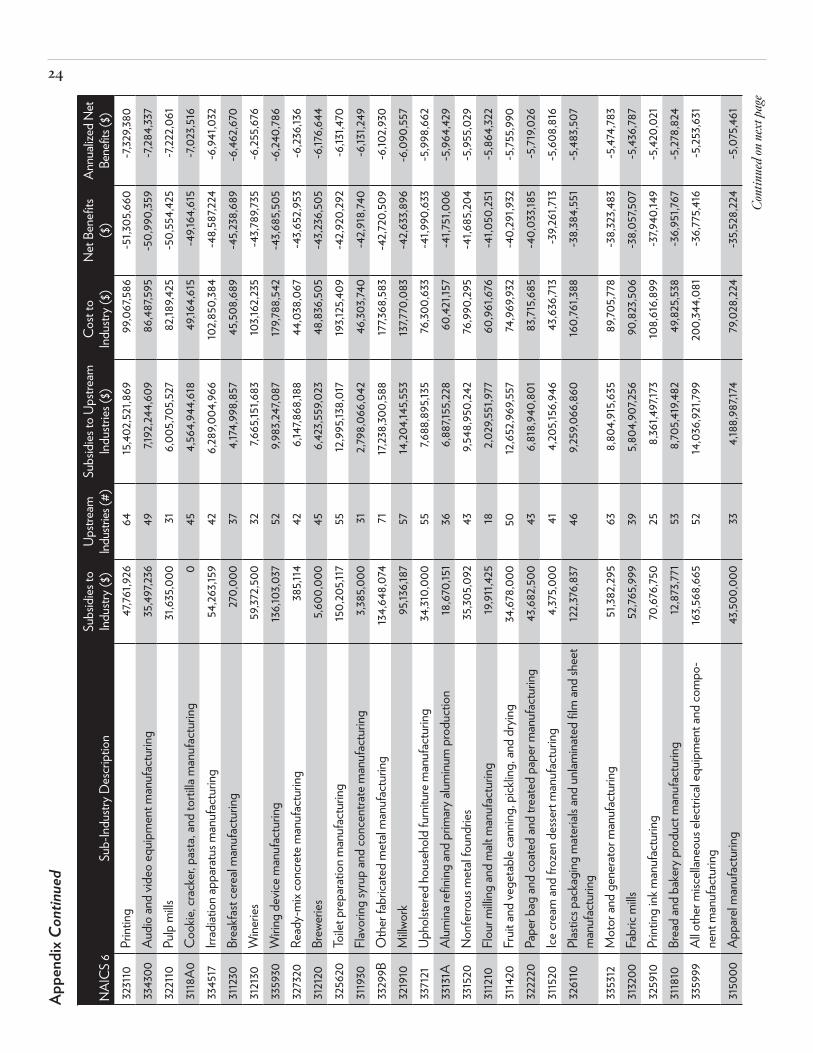

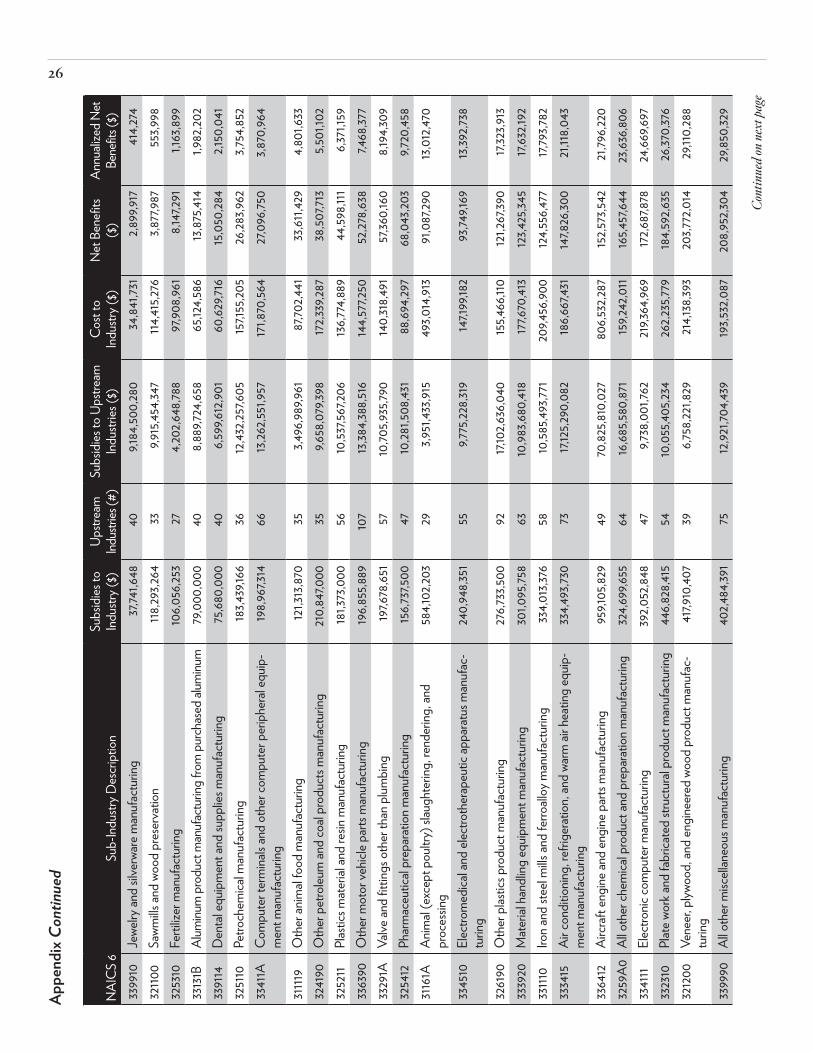

19Ap

pend

ixBe

nefit

s and

Cos

ts of

Ex-

Im to

236

Six-

Dig

it N

AIC

Man

ufac

turin

g Su

b-In

dustr

ies

NAI

CS

6Su

b-In

dustr

y Des

crip

tion

Subs

idies

to

Indu

stry (

$)Up

strea

m

Indus

tries

(#)

Subs

idies

to U

pstre

am

Indu

stries

($)

Cos

t to

In

dustr

y ($)

Net

Ben

efits

($

)An

nuali

zed

Net

Bene

fits (

$)33

4210

Telep

hone

appa

ratu

s man

ufac

turin

g14

7,419

,998

5111,

966,6

45,77

51,0

22,0

56,60

8-8

74,63

6,610

-124,9

48,0

8733

3514

Spec

ial to

ol, d

ie, jig

, and

fixt

ure m

anuf

actu

ring

45,42

9,081

489,5

64,28

6,909

471,0

06,34

2-4

25,57

7,261

-60,

796,7

5233

3618

Oth

er en

gine

equip

men

t man

ufac

turin

g40

,088

,068

8383

,606,0

86,49

743

2,882

,197

-392

,794,1

29-5

6,113

,447

3342

90O

ther

com

mun

icatio

ns eq

uipm

ent m

anuf

actu

ring

197,6

46,24

450

11,50

3,018

,767

574,0

87,13

1-3

76,44

0,88

7-5

3,777

,270

3345

12Au

tom

atic

envir

onm

enta

l con

trol m

anuf

actu

ring

40,85

1,009

4410

,911,5

86,75

440

9,260

,618

-368

,409,6

09-5

2,629

,944

3344

18Pr

inted

circu

it asse

mbly

(elec

tronic

asse

mbly

) man

ufac

turin

g1,2

50,0

0065

15,24

6,770

,927

329,0

87,59

3-3

27,83

7,593

-46,8

33,94

233

2114

Cus