Embed Size (px)

Citation preview

This article was downloaded by: [Tulane University]On: 28 September 2014, At: 12:26Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House,37-41 Mortimer Street, London W1T 3JH, UK

Asia Pacific Business ReviewPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/fapb20

The Expected Roles of Business Angels in Seed/EarlyStage University Spin-offs in Japan: Can BusinessAngels act as Saviours?MASANOBU TSUKAGOSHI aa incTANK Japan Inc./Research Center for Advanced Science and Technology, University ofTokyo , JapanPublished online: 23 Jun 2008.

To cite this article: MASANOBU TSUKAGOSHI (2008) The Expected Roles of Business Angels in Seed/Early StageUniversity Spin-offs in Japan: Can Business Angels act as Saviours?, Asia Pacific Business Review, 14:3, 425-442, DOI:10.1080/13602380802116864

To link to this article: http://dx.doi.org/10.1080/13602380802116864

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of theContent. Any opinions and views expressed in this publication are the opinions and views of the authors, andare not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon andshould be independently verified with primary sources of information. Taylor and Francis shall not be liable forany losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use ofthe Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

The Expected Roles of Business Angelsin Seed/Early Stage University Spin-offsin Japan: Can Business Angels actas Saviours?

MASANOBU TSUKAGOSHIincTANK Japan Inc./Research Center for Advanced Science and Technology, University of Tokyo,

Japan

ABSTRACT University Spin-offs (USOs) have increasingly been sought after as a means ofinnovation breakthrough in Japanese academic society. To support their success, various financingoptions have been provided in their seed/early stages from institutional venture capital, governmentsand corporations. Non-financial support, however, is often limited in their early development stagewhen such support is most critical. This study reveals a ‘gap’ between the needs of Japanese USOsfor non-financial support and the capacity of existing investors to supply such support. It argues thatbusiness angels in Japan, possessing similar characteristics and investment profiles to those in theUSA, could play a critical role in filling such a gap and so better direct Japanese USOs to success.This paper concludes with the suggestion that an organizational approach towards matchinguniversities and business angels is appropriate in the still traditional Japanese society.

KEY WORDS: business angels, Japan, non-financial support, seed/early stage ventures, universityspin-offs (USOs), venture capital (VC)

Introduction

In recent years, university spin-offs (USOs) have been regarded by Japaneseacademia as a vital innovation engine. The commercialization of academicresearch activities has become an integral part of a once-distanced ‘ivory tower’tradition, in both academic and financial terms. In the main, this shift has occurredbecause of recent university reforms, such as the privatization of national andpublic universities in Japan. According to the Ministry of Economy, Tradeand Industry (METI), USOs are expected to be a means of realizing continuousand subversive innovations from intellectual seeds generated by Japaneseuniversities. The Japanese government has promulgated various regulations,grants and infrastructure projects to support USOs as part of a general policy offostering academic innovation and, consequently, of revitalizing the stagnantJapanese economy.

1360-2381 Print/1743-792X Online/08/030425-18 q 2008 Taylor & FrancisDOI: 10.1080/13602380802116864

Correspondence Address: Masanobu Tsukagoshi, Managing General Partner, incTANK Japan Inc., B-207,

Center for Collaborative Research Building, The University of Tokyo, 4-6-1, Komaba, Meguro-ku, Tokyo

153-8904, Japan. Email: [email protected]

Asia Pacific Business ReviewVol. 14, No. 3, 425–442, July 2008

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

As these new ventures mature beyond the university laboratory and enter thereal world of commercialization, the true test of their economic viability comesinto view. One challenge faced by these new ventures emerging from anenvironment that has traditionally been insulated from the winds of commercialinterests is to amass an operational team and attract the financing in order to grow.In other countries, most notably the United States, business angels have played acritical role at this stage – providing strategic advice, valuable networkingintroductions and early funding. In Japan, where the venture start-up communityis relatively new, the role and effectiveness of angels in general – and insupporting USOs in particular – remains unclear.This study explores more closely the environmental factors surrounding the

USO community in Japan. It then outlines the characteristics and roles of businessangels in the United States – arguably the most established of informal venturecapital communities. The supply and demand of various financial andnon-financial supports in Japan are examined, including the present activity ofJapanese business angels. The existence of a gap between various non-financialneeds of the USOs in Japan and the lack of non-financial value-added supportcommonly available to them is then analysed. Finally, there is a discussion of thepossibility of Japanese business angels acting as a ‘synergistic plug’ designedto fill the gap between need and support and thus direct Japanese USOs moreeffectively to success.

Research Questions and Proposition

The overarching objective of this study is to clarify the potential roles thatbusiness angels can play in support of Japanese USOs in the Japanese venturecapital (VC) community generally and in support of Japanese university spin-offs(USOs) in particular. Towards this objective, this essay addresses the followingresearch questions:

. What is the current role of business angels in the Japanese VC community?

. What is the current role of business angels in support of Japanese USOs?

. How might this role be developed in future and to the benefit of bothparties in seed/early stage USO ventures – above all, in respect ofaddressing the non-financial/management support needs of USOs?

Overall, this study explores and analyzes the proposition that, in Japan, a gapexists between the non-financial needs of USOs and the availability of such non-financial support to these USOs. It furthermore explores the potential of Japanesebusiness angels to act as a ‘synergistic plug’ in order to fill or bridge this gap.Details of this analysis are presented below.

Context: The Current and Emerging Role of Business Angels in Japan

The purpose of this initial contextualizing discussion is to define some of the keyterms relevant to our analysis and to outline some of the policy changes relevantto defining the role and scope of business angels in respect of Japanese USOs.

426 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

Defining USOs

University ventures, most narrowly defined, are incorporated entities formed tocommercialize intellectual property rights, new technologies and/or businessmodels that emerge from university research activities. In the context of thiscurrent study, a broader definition of a USO is adopted to include ventures thatcollaborated with university research initiatives, utilized university facilities(including incubation centres), or otherwise in-licensed technologies from auniversity (METI, 2006a).

Defining Business Angels

While identifying a USO is relatively clear, identifying a ‘business angel’ is not sostraightforward. Some individuals may merely supply funding, while others mayprovide advice or networking introductions – for equity, for profit, or for free.In this current study the definition of ‘business angels’ is limited to that ofvalue-adding individual investors who provide risk capital directly to newventures in which they have no family connection, and contribute theircommercial skills, entrepreneurial experience, business know-how and contactsthrough a variety of hands-on roles (Mason & Harrison, 1995). These informalventure capital (VC) investors play a vital role in supporting, both financially andnon-financially, seed/early stage start-up developments. Nevertheless, and despitetheir relative importance, few sources of collective information on business angelsare available in Japan owing (mainly) to their relative anonymity.Compared to the role of business angels in the USA there has (hitherto) been

little data on – and even less analysis of – the Japanese business angelcommunity. However, their existence and potential impact was suggested in a2002 survey by the Organization for Small and Medium Enterprises and RegionalInnovation in Japan (SMRJ), whose report defines business angels as ‘privateindividuals who provide entrepreneurs and early-stage businesses with bothfinancial support, through capital investments, and various non-financial supportsfor business growth’ (SMRJ, 2002a: 3). The SMRJ reached this definition afterstudying known definitions of business angels, including that offered by Harrisonand Mason (1995; as cited above). Hence, combined reference to such sourcesshould provide the analysis here with comparable data on investor characteristicsand investment profiles in order to assess subsequently the potential future role ofbusiness angels in Japan.

Recent Policy Developments in Respect of USOs in Japan

The Japanese government has been working hard to support both USOs andpromote the business angel community. The execution of the Science andTechnology Basic Plan (First Phase) in fiscal year (FY) 1996 is often recognizedas the beginning of policy developments for the recent university-industrycollaboration in Japan. Between FY1996 and FY2000 this plan dedicated17 trillion yen towards promoting university-industry collaborations, some ofwhich resulted in USOs. METI and the Ministry of Education, Culture, Sports,

Business Angels in Seed/Early Stage University Spin-offs in Japan 427

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

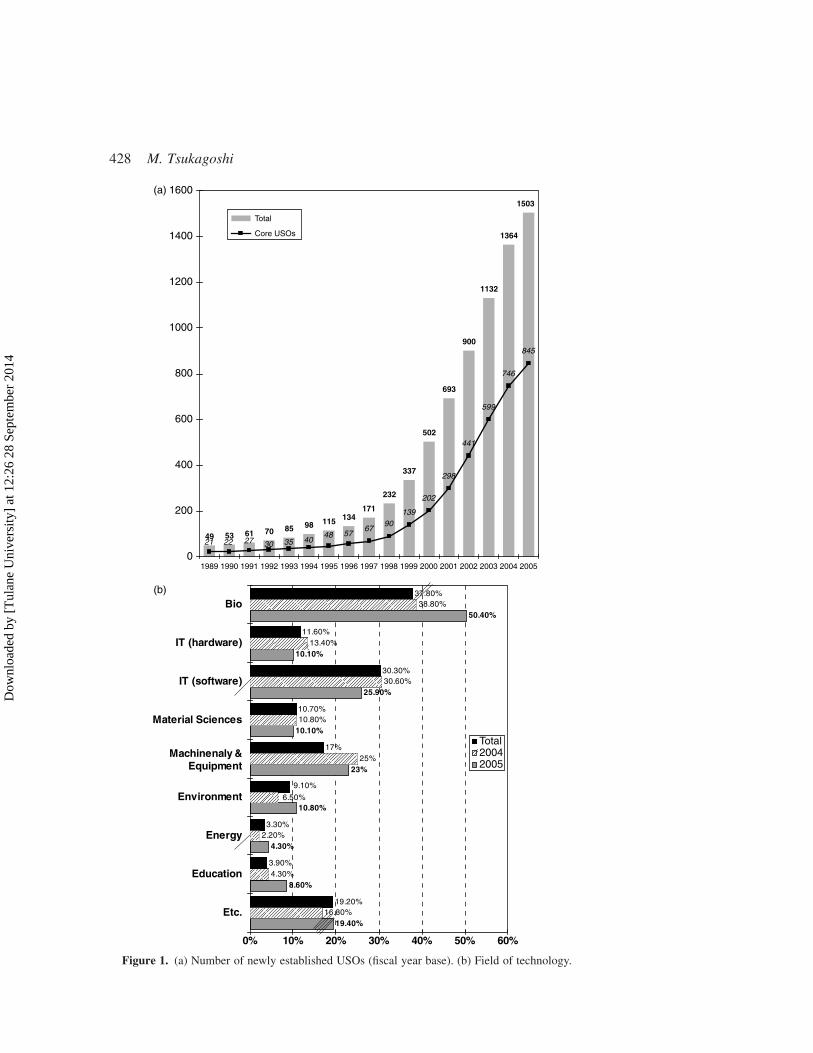

Figure 1. (a) Number of newly established USOs (fiscal year base). (b) Field of technology.

428 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

Science and Technology (MEXT) executed various regulatory efforts and grantprogrammes in support of USOs emerging from these efforts, such as apre-venture grant programme under MEXTand technology licensing office (TLO)support programmes under SMRJ/METI.1

The second phase of the Science and Technology Basic Plan started in 2001with a budget reaching 24 trillion yen through to FY2005. In the same year, thethen economic minister Hiranuma introduced his target of establishing 1,000USOs by FY2004, known as the ‘Hiranuma Plan’. To further promoteindustry-academic collaboration, along with revitalizing the stagnant Japaneseeconomy, METI executed the Industrial Cluster Plan in FY2001, followed bythe Intellectual Cluster Plan (produced by MEXT) in FY2002. The Japanesegovernment released the Intellectual Property Basic Law in FY2002 to fosternew measures and incentive programmes in intellectual property (IP)developments – a policy shift outlined by Taplin in this current collection.This change of law in respect of IP was followed by the privatization ofnational and public universities in FY2004, thus further accelerating theestablishment of USOs in Japan.2

According to METI, USOs in Japan have totalled 1,503 companies inFY2005, of which core USOs have amounted to 845. Ever since establishinguniversity technology licensing offices from 1998, the number of newlyestablished USOs has dramatically increased at a rate of more than 200 start-upsper year (see Figure 1).It is estimated that the total economic impact of Japanese USOs will reach

364.2 billion yen, providing 25,858 new jobs (METI, 2006a). The most popularfield of technology among USOs is biotechnology (50.4 per cent), followedby information technology (IT)/software (25.9 per cent), machinery andequipment (23.0 per cent), IT/hardware (10.1 per cent) and material science(10.1 per cent). As suggested in Figure 1, non-technology related USOs infields such as education and consulting accounted for 19.4 per cent of start-ups(METI, 2006a: 4–10).The number of universities with USOs increased from 231 in FY2004 to 248 in

FY2005, with a noticeable increase in liberal arts schools (METI, 2006a: 11–22).The top five universities in terms of cumulative number of USOs are theUniversity of Tokyo (92 USOs), Waseda University (75 USOs), Osaka University(71 USOs), Kyoto University (59 USOs) and Tsukuba University (57 USOs).Owing to the greater number of existing universities in large prefectures, Tokyo,Osaka, Kanagawa, Kyoto and Fukuoka are the top five prefectures in terms of thecumulative number of USOs. In 2005, non-central regions such as Chubu,Chugoku, Shikoku and Kyushu indicated a noticeable increase in the number ofUSO establishments over the national average. As of March 2005, 16 USOs filedfor an initial public offering (IPO), of which ten firms were biotech-related(METI, 2006a:24). According to a recent METI survey, 50.9 per cent were R&Dand seed/early-stages ventures, and over 70 per cent of the start-ups were stillrunning at a loss on an annual basis (METI, 2006a: 27–28).Although the FY2006 survey results (compared to similar data from FY2005)

have shown either progress or improvement in 33.8 per cent of the overall USOcases surveyed, around 66 per cent of these ventures reported no progress, or even

Business Angels in Seed/Early Stage University Spin-offs in Japan 429

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

a deterioration in their business operations. This suggests that there is room forimprovement in expediting the commercialization process of their technologies(METI, 2006a: 29–30). In order to achieve a newly set target to make 100 USOspublicly owned by FY2010, the Japanese government has started examiningrequired improvements and policy measures to meet this target.

The ‘Angel Tax’ Measure

To foster private investments in venture businesses, the Japanese governmentintroduced a tax incentive measure in 1997. The so-called ‘Angel Tax Treatment’allowed a three-year carry-forward period on capital losses generated by investingin pre-registered qualified venture businesses. After amending the measure a fewtimes since introduction in order to fit the investment climate more precisely, thegovernment has recently disclosed the expansion of tax measures to extend thecarry-forward to March 2009, and widen the subject of qualified businesses fromtechnology-oriented to business model-driven ventures.

The Emerging Significance of Business Angels

The type of government tax incentives for investment outlined here together withthe increasing popularity of USOs suggests that a thriving business angelcommunity would play a value-adding role in guiding Japanese USOs on the pathto business success. However, what approach should the Japanese business angelcommunity adopt? One option is to adapt from approaches established by businessangels in the United States.

A Business Angels Model: Informal Venture Capital in the USA

The US business angel community is a well-defined informal VC market andrepresents the most established model for this field of investment activity.According to a recent survey taken by Center for Venture Research at theUniversity of New Hampshire, the US angel investor market grew steadily in 2006to US$25.6 billion, an increase of 10.6 per cent over 2005 and representingsustainable growth (Sohl, 2007). Takahashi (2000) has suggested that one out offour to five start-ups in the USA receive the support of business angels.Indeed, it appears that an informal VC market has played a major role in

filling the equity gap that exists for seed/early stage ventures (Harrison &Mason, 1992). A typical investment size of this equity gap ranges between50,000 and 500,000 US dollars, the most popular segment for business angels(Yokota, 2004). Although this investment segment was shared by classic orhands-on venture capitalists – as it is still is, to a significant extent – the recentshift of investment focus to later stages by the overall VC community createdsuch an equity gap. Over the past decade, VC funds in the USA have grown inboth investment size and number of managing partners. As VC funds becomemore institutionalized, so their investment focus has shifted to later stagedevelopment in order to shorten their investment horizon and to capture gainsearly – a trend outlined by Ibata-Arens in this current collection. In fact, the

430 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

average investment size per deal by VC funds in the USA increased from US$2.3million in 1987 to US$4.7 million in 1997, and recently to US$7.5 million in2006 (Oh, 2001; note 1).According to Harrison et al. (1997), a typical US business angel is a male in

his late 40s, who has postgraduate qualifications and has relevant businessexperience. Business angels not only often invest money but also supplyexperience-based skills and business know-how. It is common to see a businessangel on the board of directors, and unofficially offering consulting services.On occasion, an active angel investor might work full-time or part-time for thecompanies he invests in (Harrison et al., 1997). To paraphrase from Mason &Harrison (1995), the opportunity to be involved in an entrepreneurial venture isa significant motivating factor for US-based angels when deciding on informalventure capital investments, as well as a means of protecting their investment.Business angels seldom fund start-ups to exit. At some strategic point, theypass on the development task to venture capitalists (VCs). According to asurvey conducted by George Washington University (cited in Akah & Stanco,2005), 94 per cent of VCs responded that angels are beneficial to the ventureindustry.Of course, not all informal investors are quality angels. Some unfortunately do

not possess the required set of skills to support start-ups properly. These businessangels may be transformed into vultures or devils – offering improper advice,distracting the core team, or taking over the investment venture. However, oneshould assume that most are inherently interested in nurturing the growth of theirinvested entrepreneurs and venture business. One can conclude that this active andinformal venture capital market is an indispensable factor in the vitalentrepreneurial economy in the US (Oh, 2000).

Analysis: Framework

Against the background of environmental factors outlined thus far in this study,there now follows an examination of the investment trends and styles in respectof Japanese institutional venture capital – as indicated above, one of the criticalfinancing sources for USOs, followed by other financing sources such asgovernments and corporations. In this section, there is an analysis of whethernon-financial value-added support properly exists in the context of seed/early-stage venture development. There is also a discussion of the current role of businessangels in Japan in order to assess the effectiveness of their activities. The study thenexamines the existence of a gap between supply and demand of non-financialsupport and considers the potential of Japanese business angels to bridge this gap.

Analysis 1: Investment Stages and Styles of Venture Capitalists (VCs)in Japan as a Major Financing Source for USOs

Success in seed/early stage investments often requires more than just money.Hands-on VCs, also known as ‘classic’ VCs, provide their portfolio companies withvarious non-financial support, ranging from business planning to businessdevelopment. These VCs often play an active role on the Board of Directors and

Business Angels in Seed/Early Stage University Spin-offs in Japan 431

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

so navigate their portfolio companies to contain downside risk while adding value totheir investment. In the USA, hands-on VCs act both as a riskmoney provider and asan interest-sharing partner, who provide various types of managerial support.As Kirihata (2003) points out, of the managerial support provided by VCs the mostimportant functions include utilizing personal networks and managing externalrelationships – such as supplying temporary help, expanding human networks andproviding informative networking opportunities. In short, hands-on VCs seek toincrease the corporate value of portfolio businesses through providing acomprehensive range of managerial support in their role as investors and/or partners.Japanese VCs are generally viewed as passive investors, more comfortable with

later stage investments. In large part, their activities are influenced by the sourceof limited partner funding. As of 1999, 54 per cent of the overall financing sourcefor Japanese VCs was corporations, followed by banks at 18 per cent andinsurance companies at 17 per cent (SMRJ, 2002b: 23–26). During the sameperiod, the most popular investment stage for Japanese VCs was expansion at50 per cent, followed by mezzanine (between expansion and buy-outs/IPO) at19 per cent, with start-ups comprising only 15 per cent. Thus, Japanese VCs haveappeared to prefer the later stages of investment.In recent years, however, Japanese VCs have started looking more to earlier

stage investing. There is anecdotal evidence, to support the view that a growingnumber of Japanese firms are focusing (and perhaps more aggressively) at newventure start-ups, including USOs. A recent survey by the Venture EnterpriseCenter (VEC) supports this view. During FY2005, the 105 VC respondentssurveyed invested 196.8 billion yen into 2,759 companies, of which 48.7 per centhad been incorporated less than five years prior to the investment (VEC, 2006:2–3). Although the survey does not capture the entire VC industry in Japan, thefigures cited are believed to be illustrative of an overall trend.Japanese VCs have now started forming new funds with a focus – or at least a

scope – that includes USOs as a target. As of FY2006, 55 venture funds totalling84.9 billion yen received matching funds under the METI investment programmefor fostering new business exploitation. Of these, nine funds totalling 17.5 billionyen specifically target the USO sector. Although no aggregate data is available,there are other new VC funds targeting USOs that have not sought matching fundsfrom the central government, some of which focus on regional opportunities.According to METI (2006b), Japanese VCs were ranked as the top source forfinancing current USOs, investing 397 million yen per company on average at theseed/early R&D stage – a level of investment followed by private corporationswith 283 million yen and government grants of 96 million yen. Although thisanalysis alone cannot confirm ample funds to fill in the entire equity gap in theseed/early investment stage, Japanese VCs appear increasingly willing to fundUSOs at an early stage.

The Current Profile of Japanese VCs

Against the background of these apparent trends describing investment interestamong established VCs, is there still a role for the Japanese business angel? As willbe argued subsequently, just because VCs have started to focus more on early stage

432 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

investments does not mean that new USOs can expect to receive high-risk fundingas well as critical business advice from these investors. Indeed, I argue fromexperience that the business angel remains an important element of the ventureeven after the professional investor places a bet.Unlike in the USAwhere private VCs dominate, themajority of Japanese VCs are

subsidiaries of either financial institutions or large corporations: as outlined in ourdiscussion above, the investment style of Japanese VCs differs markedly from thatof their US counterparts. Individual venture capitalists working for Japanese VCfirms are often referred to as salaryman venture capitalists, since many of them areeither visiting or temporarily transferred personnel from a parent company. Drawingon VEC (2006) data, it appears that although 32 per cent of the individual capitalistsin financial institution-related VCs and 67 per cent of those in corporate VCs claimover 20 years of previous professional experience, their VC experience is relativelylimited, in fact. Of those VCs managing venture money, 62 per cent have less thanfive years experience in the VC space while 20 per cent have between five and tenyears’ experience. The most common function while working at a VCfirm/subsidiary was deal analysis and execution at (87 per cent), followed by duediligence and planning at 83 per cent. Contradicting a common view that JapaneseVCs often do not provide hands-on support, 72 per cent of those surveyed claimed tohave experience in managerial support (VEC, 2006: 71–74).Turning our eyes to actual investments by Japanese VCs, nearly 90 per cent of

those surveyed stated that they provide managerial support to their portfoliocompanies. However, only 58 per cent are dispatched as directors while 53 per centprovide financial and administrative support. This is surprisingly low in light of theincreasing levels of investment in early stage companies, and the fact that many VCsthemselves are related to financial institutions. It is significant that nearly 80 per centof the VCs who recognized the need of managerial support could not provide suchsupport due to a lack of proper human resources (VEC, 2006: 77–78). One possibleexplanation for this shortfall in support lies in the relatively short length of individualservice in a corporate VC structure, for acquiring relevant managerial capabilityoften requires years of professional VC experience and hands-on know-how.To summarize this first section of analysis, the above data reveals that the

understanding of ‘hands-on support’ among venture capitalists in Japan is limitedby their rather passive investment culture. This suggests that their seed/early stageinvestments are likely to receive only limited non-financial support. Althoughthere are signs of quality hands-on VCs in Japan, their availability and numberrelative to the overall VC industry is limited (Jinza, 2005). Most VCs in Japanadopt a less individual approach and more organizational approach to investment,which perhaps is in agreement with the established investment style of theJapanese VC community. It can be argued that this organizational approach toinvestment might be of limited value to seed/early stage investments.

Analysis 2: Government Grants and Private Corporations as Sources of R&DFunding and Knowledge Supporting USO Development

The Japanese government is intent on increasing the number of new USOs. Thisobjective has become a critical element of university reforms, as outlined

Business Angels in Seed/Early Stage University Spin-offs in Japan 433

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

subsequently by Debroux in this current collection. To illustrate: METI alone hasconsistently built a sizeable budget specifically related to USOs over the past fewyears – 43.4 billion yen in FY2003, 45.1 billion yen in FY2004, 50.9 billion yenin FY2005, and 52.8 billion yen in FY2006. These budgets have been applied tovarious programmes from R&D grants to human resources (HR) development(METI, 2003, METI, 2005). In addition, MEXT budgeted 27.5 billion yen inFY2004 and 29.4 billion yen in FY2005 for university-industry collaborationactivities, some of which were USO-related. The METI figures alone suggest thatan average sum of approximately 34 million yen was available for each of 1,503USOs counted in FY2005. Though generalized here, this funding availability issignificant given that more than half of these USOs are still at their seed/earlyR&D stages.Furthermore, a comparative study of entrepreneurship in Japan and the USA’s

Silicon Valley also suggested that Japanese venture businesses enjoyed betteraccess to diverse funding sources, particularly bank loans and governmentfinancing (Suzuki, et al., 2002). As there are other public financing sources such asregional governments are also available, Japanese USOs seem to have variousmeans to obtain financing beyond VCs and business angels.In addition, the recent and protracted economic stagnation in Japan has forced

many large corporations to streamline their internal R&D management. As aconsequence, large corporations have been outsourcing some R&D processesto university laboratories and consistently building up collaboratively fundedresearch with universities. To illustrate: the MEXT homepage tells us thatJapanese universities received approximately 21.6 billion yen in FY2003 and26.4 billion yen in FY2004 from private corporations.3 Although this corporatefunding primarily targets collaborative R&D, such activities sometimes resultin establishing USOs, as the study by Debroux (in this current collection)illustrates. Furthermore, these R&D collaborations can act as a wellspring ofexperiences and knowledge in the university laboratories for future technologycommercialization and thus sustain an on-the-job habitat for future technologyentrepreneurs.

Analysis 3: Characteristics and Activities of Japanese Business Angels

There is a popular view that the business angel community is less developed inJapan than in other developed nations. Harada & Kutsuna (2002) reasoned that inJapan:

1) there is a relatively smaller percentage of business professionalswealthy enough to become business angels;

2) few people succeed as entrepreneurs;3) there is a less-than-functional market in respect of providing a reliable

and efficient risk-and-return structure from seed to IPO;4) there are insufficient tax incentives for business angel activities; and5) the matching system between entrepreneurs and business angels is less

developed.

434 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

The Current Profile of Japanese Business Angels

Although the business angel community as a whole might be relativelyunderdeveloped, SMRJ recently reported a potential of Japanese business angelsas a vital supporter in the seed/early stage venture development. This survey(SMRJ, 2002a) covered both business angels (73 respondents) and venturebusinesses (160 respondents) and revealed that the typical profile of a Japanesebusiness angel is male (85 per cent), 56 years old, and holding a bachelor’s degreeor better (70 per cent), with 10 per cent holding advanced degrees. The mostpopular fields of expertise of Japanese business angels are management andeconomics, followed by science and engineering – a ranking that is opposite thatof US business angels (see discussion above). The historically lower pay scale andenduring lifetime employment system of Japanese corporate engineers mightexplain this contrast.The SMRJ (2002a) report further states that the start-up experience of Japanese

business angels was noticeably lower than that of their foreign counterparts:51 per cent of those surveyed were experienced entrepreneurs, of which 30 per centhad experienced an IPO. To compare: 83 per cent of US business angels and75 per cent of Canadian business angels were experienced entrepreneurs. About60 per cent and 15 per cent of Japanese business angels still hold president/chiefexecutive officer (CEO) and chairman positions, respectively. 67 per cent of thesebusiness angels still work in a corporation, with 8 per cent of them being retired.Although the the dominant male figure is similar in Japan and in the USA,becoming a business angel in Japan appears to require more time – possibly toaccumulate sufficient wealth and experience. This supposition is supported by theolder average age (about 10 years) of Japanese angels in comparison with their UScounterparts.Although some differences can be seen in the general profiles of business angels

in Japan and in the USA, their economic figures are comparable. Japanesebusiness angels earn on average 18.6 million yen per annum and have an averagenet worth of 390 million yen. Although these figures are higher than those of USangels, factoring higher income tax in Japan and real estate inclusion in theJapanese net worth would make the average financial position of Japanesebusiness angels comparable to that of US angels (SMRJ, 2002a). The SMRJ reportalso points out how Japanese business angels invest on average about 13.4 per centof their net worth, which is lower than the average figures for angels in otherdeveloped nations. The report further notes that the inclusion of real estate in networth might be a reason for this difference.In terms of geographical distribution, the majority of Japanese angels in the

survey are located in the metropolitan Tokyo area (40 per cent), followed byOsaka Prefecture (8.3 per cent) and Kanagawa Prefecture (6.3 per cent). Althoughit may be premature to conclude firmly, the SMRJ survey suggests a potentialnation-wide availability of business angels in Japan given that one-third ofrespondents live in non-prime regions. This is significant – and encouraging,since many recent USOs have been established in non-central regions.In terms of investment decision making, Japanese business angels rated

(at 52 per cent) the personal integrity, skills and capability of the entrepreneur

Business Angels in Seed/Early Stage University Spin-offs in Japan 435

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

as the highest investment factors, followed by the business growth potential at50 per cent. In terms of motivating factors, 53 per cent of Japanese business angelsecho their US counterparts by citing ‘wanting to enjoy the growth process ofcompanies’ as the prime reason to decide on actual investment. Also noted werethe expected investment return at 44.4 per cent and the social contribution level at33.3 per cent. This trend fits potentially well to support well-funded USOs inJapan since business angels may have lesser opportunities to actually invest inthe USOs.Unsurprisingly, perhaps, 37.3 per cent of Japanese business angels becoming

actively involved with their invested companies reported that wanting to enjoy thegrowth process was their main reason to get involved, followed by expectinginvestment returns (at 28.4 per cent). These active business angels seem to providevarious non-financial support to the invested start-ups, such as:

. Advising on management strategy (ranks the highest, at 19.5 per cent).

. Monitoring management activity (14.3 per cent).

. Encouraging entrepreneurial activity (13 per cent).

. Advising on marketing (10.4 per cent).

The top position that these business angels actually held was as unofficialadviser (at 32.7 per cent). A directorship position was ranked third (at 21 per cent).Although different degrees of relationship become apparent from the SMRJsurvey, around 30 per cent and 50 per cent respectively expressed their proactiveinterests in future investment opportunities.In apparent contrast, business angels in other nations such as the USA and the

UK have a mixture of financial and non-financial motives, with the prospectof financial gain as the single most important factor (Tashiro, 1999). Tashiro,using a separate survey, confirmed our assessment that financial gain is a minorreason for investment by Japanese business angels. As the informal venture capitalmarket in Japan builds experience and success stories, Japanese business angelsmay become more financially oriented and thus more in balance with their non-financial motives. In general, however, it can be concluded that business angels inJapan as elsewhere share similar characteristics and interests in nurturing thedevelopment of their start-ups.

Analysis 4: The Needs and Challenges of USOs in Japan

There are many challenges in the different stages of a venture’s growth.Metaphors such as ‘The valley of death’ or ‘Darwinian Sea’ are often used todepict such challenges. Although these challenges exist, enactment of the TLOAct, regulatory relaxation of employing professors and researchers, develop-ments of start-up incubation facilities, privatization of national and publicuniversities, along with increasing awareness within academic personnel, haveall contributed to an increase in the number of USOs established in recent years(METI, 2006b:11). It appears that approximately 33 per cent of the USOssurveyed had not exercised, or appeared not to know about, market research.This suggests a tendency towards technology driven approaches to businessdevelopment, although 52.9 per cent of the USOs surveyed have an IPO as

436 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

their exit strategy (METI, 2006a: 31–32). As for funding in the seed/early-stage development, the most popular approach was to utilize their initialcapital, funded internally and/or externally, and national/regional-governmentgrants. Utilizing initial capital to weather the storm is not unusual for start-upsand is, in fact, often encouraged. Accessing government sources is alsounsurprising since (as suggested earlier) ample public financing options areavailable for Japanese USOs. Given that more than half of the USOs inFY2005 were still at the seed/early R&D stages, the study will now look atvarious managerial challenges that these USOs are facing.

The Profile of Seed/Early-Stage USOs: HR Issues

Although recently relaxed, the legal process to establish a company is still atime-consuming administrative task in Japan. However, it is nothing comparedto developing and growing the company thereafter. One METI report (2006b)highlighted three major challenges that current USOs faced: securing andnurturing human capital, fund raising, and finding new markets. In thisparticular report, the single most obstructive factor was the HR issue frominception to current stages. As most USOs in Japan are technology/research-driven, it was not surprising to note that 25% of their current CEOs wereprofessors (14.8 per cent) and students/researchers (9.4 per cent), especially atseed/early stages. But this management structure is not without its concerns, asthese CEOs have little or no business experience. 19.1 per cent of USOs havechanged their CEO at least once since inception, of which 59.1 per centreasoned that their development stage had changed. However, this admissiondoes not necessarily mean that those USOs actually have found business savvymanagers. In fact, only 9.9 per cent responded that they had found moreappropriate individuals from the private sector, which indicates continuingdifficulty in attracting quality executives.Many USOs also seek individuals with a higher academic degree to oversee

both R&D functions and business development. The most expected functionfor such individuals was business planning at 53.3 per cent, followed by newmarket development and fund raising at 44.3 per cent. The Chief TechnologyOfficer (CTO) function was ranked the lowest at 18.9 per cent. These resultscan be explained perhaps by reference to 1) the technical nature of coretechnology requires such understanding even for business managers, and 2) thecurrent CEOs being the likely inventors of the core technology and alreadyacting CTOs. It can also be inferred from this result that the professor/re-searcher CEOs are in need of smart ‘all-rounders’ to fill in for labour-intensiveR&D processes and business functions requiring relatively less experience,given the general lack of resources to hire personnel.Also noted was the success rate to secure personnel. The rate for obtaining

business managers for new market development was the lowest at 50.5 per cent,followed by management executives at 59.2 per cent. Unsurprisingly, perhaps,attracting R&D personnel was the most successful at 70.7 per cent, probably owingto their proximity to academic researchers and students. Their associateduniversity and/or friends were the most popular route to seek human resources,

Business Angels in Seed/Early Stage University Spin-offs in Japan 437

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

ranking at around 70 per cent. However, it can be argued that business savvymanagers and managerial executives are to be found elsewhere. Correspondingly,beyond the expected close networks, using VCs as a referral route ranks at only1.9 per cent to 9.0 per cent and, with a success rate of 33.3 per cent to 66.7 per cent,the conclusion might be which that VCs are not necessarily an assured source ofhuman capital.

Linking HR to VC Funding

However, and as mentioned earlier, the VC community remains the primaryfunding source for seed and early stage USOs, followed by private corporationsand government grants. However, the most popular funding source seems to lackan appropriate level of non-financial support, as evinced in the HR difficultiesoutlined above. The METI survey in particular revealed the dissatisfaction thatmany funded USOs had with their VC support. Although many were still at earlyR&D stages, 22.8 per cent of USOs only received financing from VCs.The remainder received some sort of non-financial support, but of a relativelypassive nature, such as advice on business planning. It is inevitable that, as a profitentity, VCs need to balance their non-financial involvement (a time factor) relativeto actual investment size. Consequently, a small early-stage USO cannot expectmuch attention relative to much larger investments. However, the analysisdeveloped here raises concerns about the success probability of those USOsinvested in, especially during their early stages when such support is most critical.Ultimately, VCs themselves will need to cover the possible investment loss if theirinvested USOs fail, unless some improvement measures – internally and/orexternally – are taken.

Implications

Although financial support is naturally on the wish list of most USOs, the analysishere has revealed that financial support seems readily available. Often this isactually provided to Japanese USOs because of the early stage investmentinterests of Japanese VCs in combination with various government policymeasures to support USO development. Financing is important in both seed/earlystages and in later development stages. However, non-financial support can be justas important as monetary support, and especially when the venture business is atits infant stage. It has been seen here that non-financial support is often lacking forseed/early stage USOs in Japan, as opposed to the relatively ample financingoptions. Consequently, it is possible to identify a distortion or ‘gap’ between thesupply and demand equation of non-financial support to USOs.In terms of profile it has also been found that business angels in Japan,

though still underdeveloped as a community, have similar personal traits andinterests in nurturing start-ups as their counterparts in other well-developedinformal VC markets such as the USA. Surveys suggests that proactiveJapanese business angels already exercise their potential in supporting venturestart-ups in both financial and non-financial terms. It is argued here, therefore,that the professional infrastructure required for guiding seed/early stage

438 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

Japanese USOs to success can be improved with more proactive involvementby Japanese business angels.In recent years, Japanese universities have built many venture incubation

centres and USO support programmes. These have been portrayed as a valuabletool with which to transform Japanese academic society to a more dynamic andentrepreneurial one. However, these facilities and programmes are only as strongas their management components (Wolfe et al., 2001). The most critical factor tothe success of start-ups utilizing such programmes is to have personnel who canguide business decisions, provide experienced advice and develop the strengths ofentrepreneurs (Drucker, 1985). I argue that quality business angels are capableto perform this function. However, and despite this possibility, effectivecollaboration between incubators and angels in the Japanese USO ecosystemappears to have been rare. I believe that an invisible hurdle between universitiesand business angels exists, described by reference to the following challenges atboth ends of the spectrum.The old bureaucratic-like management behaviour of universities – to do, or try

to do, everything in-house – is looked upon as one of the causes of current USOineffectiveness. Expressing old management styles continues in many academicinstitutions, probably because the government funds various costly propositionssuch as building a venture laboratory. As a consequence, Japanese universities areless pressured to manage such facilities with a business mindset, and furthermore,are prone to creating a self-contained, ineffective USO support infrastructure. As aresult, fewer effective personnel might be hired or positioned to support USOs.Certainly, functional outsourcing is a low priority in such old-fashioned systems.Along with existed protectionism generated by vested rights and academic pride,the traditional university-style management might have created an invisiblebarrier to outside help.Business angels are also required to be more visible and accessible to university

management. In a recent interview, Mr Keisuke Yawata, Chairman of IAI Japanobserved that Japanese business angels are less organizational and less motivatedto disclose his/her existence.4 A well-known Japanese business angel himself,Mr Yawata further pointed out that Japanese business angels are arguably lessmotivated by financial interests, as in other countries such as the USA – possiblybecause of cultural factors that tend to downplay one’s status and wealth.Although often anonymous and geographically dispersed, business angels do existnationally in Japan and are looking for new opportunities.Matching universities and business angels in Japan therefore seems to require

a separate ‘lubricant’ agent. One possibility is an ‘organizational’ relationshipbetween these two parties. As business angels are inherently individualistic, theyhave less success in opening the door of the traditionally aloof academic world.To compensate for such drawbacks, the aforementioned IAI Japan has beengradually building a possible organizational alliance with some universities in theKanto region. As trust building is the single most critical factor in angel activities,and remains so important in traditional Japanese society, utilizing the collectiveindividual qualifications of angel members may become a powerful tool to bridgethe gap between the two parties.

Business Angels in Seed/Early Stage University Spin-offs in Japan 439

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

A more compelling option for an angel network or organization, perhaps, is toestablish a business alliance with those institutional VCs already investing inUSOs, especially the VCs dealing with problematic USOs. The vested interests ofsuch alliances are much clearer than the earlier option since those VCs want tomaximize investment returns, and angels seek to experience the nurturing processof USOs. The support of promising USOs by Japanese VCs remains essentialto the growth of the USO community as a whole. As most USOs in Japan aretechnology-related and require heterogeneous personnel skills, Japanese VCsmay ultimately perceive such investments as too risky, and will – unless someimprovement measures are taken – turn to later stage investment opportunities.Although such argument is still premature, it is possible that the shifting ofinvestment focus to later stages may occur if the VC industry dynamics in theUSA can be a guide to what may happen in Japan.In their role as potential saviours to USOs in Japan, there should be more

attention given to the potential role of business angels generally, and particularlyas part of an organizational approach to building strategic alliances among earlystage supporters, as remains the norm in traditional Japanese society.

Conclusions

This study is by no means intended to criticize the Japanese VC community intheir current association with USOs, or the Japanese government and universitiesin their efforts to develop policies and measures of university-industrycollaboration. Rather, this paper suggests that both parties have the potential toplay a critical role in fostering a shift in the focus of the Japanese economy fromthe large corporate to the more entrepreneurial. As mentioned above in this study,there are encouraging signs of quality hands-on VCs supporting start-ups in Japan.However, these remain the exception rather than the rule.Japanese policy makers have been proactively supporting innovation, and

promising results can be seen in some universities and research institutions acrossJapan. The factors for a successful venture are varied: quality of entrepreneurs,sound intellectual property portfolio development, the general economicenvironment, and a little bit of luck. All these factors play important roles inthe business success of USOs. It is inevitable that, in the context of humaninteraction and new forms of cooperation, a degree of continuous trial-and-errormust be allowed, enabling parties to find the most appropriate infrastructure andprogrammes for the environment in question. As a consequence, further researchshould look into cultural factors influencing business angel activities and theirperceptions in relation to (relatively speaking) insular academic entrepreneursin Japan.As an early-stage venture capitalist and a humble angel practitioner myself,

I will conclude this study by paraphrasing from the enduringly wise words of PeterDrucker (1985) who, when discussing ‘entrepreneurial management’ remindedus that, in standard institutional contexts, the ‘entrepreneurial’ element of thisprocess is the key to success. However, he reminded us also that, in the venturebusiness, it is ‘management’ that is key.

440 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

Acknowledgements

The author would like to take this opportunity to thank Dr Philippe Debroux, a Professor at Soka University, in

providing him with this opportunity to extend his research efforts. He also would like to extend his appreciation to

Mr Karl Ruping, his old friend and business colleague at incTANK Ventures, and to Mr. Sugiyama, a quality

researcher at the University of Tokyo, who inspired and encouraged him in completing this research.

Notes1 See the website for NVCA (National Venture Capital Association), available at http://www.nvca.org/

ffax.html2 See Nikkei Business (14 November 2005); Cabinet Office, Government of Japan, Office of Intellectual

Property Strategy (2006).3 See the website for the Ministry of Education, Culture, Sports, Science and Technology (MEXT).

Available at http://www.mext.go.jp/b_menu/houdou/17/06/05062201.htm (in Japanese).4 Interview with Mr Yawata is available at http://www.iai-j.com – a not-for-profit organization affiliated

with International AngelInvestors in the USA).

References

Akah, U. & Stanco, T. (2005) Survey: the relationship between angels and venture capitalists in the venture

industry, unpublished manuscript. Available at http://www.papers.ssrn.com/sol3/Delivery.cfm/SSRN_

ID1093006_code339992.pdf?abstractid¼1093006&mirid¼1 (accessed 20 March 2008).

Cabinet Office, Government of Japan, Office of Intellectual Property Strategy (2006) Chiteki Zaisan Suishin

Keikaku 2006 (Intellectual Property Promotion Plan 2006) (in Japanese).

Drucker, P. (1985) Innovation and Entrepreneurship – Practice and Principles (London: Heinemann).

Harada, N. & Kutsuna, K. (2002) Senzaiteki bijinesu enjeru to siteno chuushou kigyou keieisha (Small and

medium enterprise managers as a potential business angels), Research Institute of National Life Finance

Corporation Japan, Chosa Kiho (Seasonal Research Report), No. 63, p. 2 (in Japanese).

Harrison, R. & Mason, C. (1992) International perspectives on the supply of informal venture capital, Journal of

Business Venturing, 7, pp. 459–475.

Harrison, R., Mason, C. & Nishizawa, A. (1997) Bijinesu Enjeru no Jidai (Original Title: Informal Venture

Capital – Evaluating the Impact of Business Introduction Services) (Tokyo: Toyo Keizai Shinposha)

(in Japanese).

Jinza, Y. (2005) Nihon no Bencha Kyapitaru (Japanese Venture Capital) (Tokyo: First Press) (in Japanese).

Kirihata, T. (2003) Fostering university-launched ventures and venture capitals – required value-adding

capabilities of venture capitalists, Journal of Mitsubishi Research Institute, (42), p. 67.

Mason, C. & Harrison, R. (1995) Closing the regional equity capital gap: the role of informal venture capital,

Small Business Economics, 7, pp. 153–172.

METI (2003) Heisei 16 Nendo Sangakukan Renkei Kanren Yosan Ichiran (FY2004 Budget Table Related to

University-Industry Collaboration) (Tokyo: Ministry of Economy, Trade and Industry) (in Japanese).

METI (2005) Heisei 18 Nendo Sangakukan Renkei Kanren Yosan Ichiran (FY2006 Budget Table Related to

University-Industry Collaboration) (Tokyo: Ministry of Economy, Trade and Industry) (in Japanese).

METI (2006a) Daigaku-hatsu Bencha ni Kansuru Kiso Chousa, (Report on Basic Research of University Spin-

offs) (Tokyo: Ministry of Economy, Trade and Industry) (in Japanese).

METI (2006b) Daigaku-hatsu Bencha no Seichou Shien ni Kansuru Chousa Houkokusho (Research Report on

Growth Support for USOs) (Tokyo: Ministry of Economy, Trade and Industry) (in Japanese).

Oh, S. (2000) Beikoku kigyouka keizai ni okeru bijinesu enjeru no yakuwari (Role of business angels in

entrepreneurial economy in the United States), Sapporo University, Keizai to Keiei, 31(3), p. 49

(in Japanese).

Oh, S. (2001) Beikoku bijinesu enjeru no koudou youshiki – bencha kyapitarisuto tono hikaku (Activity style of

US business angels – comparison to venture capitalist), Sapporo University, Keizai to Keiei, 32(2), p. 120

(in Japanese).

SMRJ (2002a) Bijinesu Enjeru no Jittai Chousa Houkokusho (Fact-finding Report on Business Angels)

(Tokyo: Organisation for Small and Medium Enterprises and Regional Innovation) (in Japanese).

Business Angels in Seed/Early Stage University Spin-offs in Japan 441

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14

SMRJ (2002b) Bencha Kigyou ni kansuru Kokunaigai no Chokusetsu Kinyuu (Toushi) Kankyou Joukyou Chousa

Houkokusho (Report on Domestic and Foreign Direct and Indirect Financing – Investment Environments

for Venture Businesses) (Tokyo: Organisation for Small and Medium Enterprises and Regional Innovation)

(in Japanese).

Sohl, J. (2007) The angel investor market in 2006: the angel market continues steady growth, Center for Venture

Research, University of New Hampshire, Media Relations News, p. 1.

Suzuki, K., Kim, S.-H. & Bae, Z.-T. (2002) Entrepreneurship in Japan and Silicon Valley: a comparative study,

Technovation, 22, pp. 595–606.

Takahashi, T. (2000) Waga Kuni ni okeru Oubeigata Bijinesu Enjeru no Kanousei – Kojin Tousika ga Seichou

Kigyou ni hatasu Yakuwari (Potential of western-style business angels in Japan – role of individual investors

in growing companies), Research Institute of National Life Finance Corporation Japan, Geppo (Monthly

Report), pp. 10–11 (in Japanese).

Tashiro, Y. (1999) Business angels in Japan, Venture Capital, 1(3), p. 271.

VEC (2006) Seisei 17 Nendo Bencha Kyapitaru-tou Toushi Doukou Chousa (FY2005 Venture Capital Investment

Trend Survey) (Tokyo: Incorporated Foundation Venture Enterprise Center)) (in Japanese).

Wolfe, C., Adkins, D. & Sherman, H. (2001) Best Practices in Action – Guidelines for Implementing First-Class

Business Incubation Programs (Athens, OH: National Business Incubation Association).

Yokota, A. (2004) Kansai ni okeru bijinesu enjeru no Kasseika Saku – sougyouki no bencha kigyou shien wo

mezashite (Activation measure of business angels in Kansai Region – aiming at supporting early-stage

venture businesses), Japan Research Review, 3, pp. 68–69 (in Japanese).

442 M. Tsukagoshi

Dow

nloa

ded

by [

Tul

ane

Uni

vers

ity]

at 1

2:26

28

Sept

embe

r 20

14