Embed Size (px)

Citation preview

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

ISSN (Print): 0976-7185; ISSN (Online): 2349-2325 DOI: 10.16962/EAPJFRM/6_3_2

www.elkjournals.com Volume 6 Issue 3, 21-34

21

The Effects of Monetary and Fiscal Policies on Economic Growth in

Bangladesh

Soeb MD. Shoayeb Noman

Senior Lecturer,

School of Business,

Uttara University

MD. Mohsan Khudri

Assistant Professor,

School of Business,

Uttara University

ABSTRACT

Keywords: Economic growth, Fiscal policy, Monetary policy, Trend analysis, Multiple Linear Regression analysis

1. Introduction

Good governance can be determined by the

good political and economic condition of a

country. It is also a part of good human

affairs and the material resources of local

and central government level. Thus the

economic and political structure depends on

each other. The culture of governance is so

much complex as it can change the

economic, political and social aspects of a

country.

The Bangladesh Bank, in

consultation with Finance Ministry,

conducts monetary policy for the nation, and

it has the ability to control the circulation of

money and costs of borrowing money,

known as interest. The Bangladesh Bank

sets the interest rate at which banks borrow

money from them. When the Bangladesh

Bank reduces interest rates, they make it

cheaper for banks to access to money, which

in turn makes banks more likely to give loan

to businesses and consumers.

The study deals with the impact of fiscal and monetary policies on economic growth in Bangladesh. The

data were collected on annual scale from the period of 1979-80 to 2012-13. The study employed line diagram,

correlation matrix, multiple linear regression models and trend analysis on fiscal (i.e., government revenue and

expenditure) and monetary variables (i.e., exchange rate, interest rate, inflation, broad money, and narrow

money). The major objectives of this study are to evaluate the trends in policy variables and examine the impact of

fiscal and monetary instruments on economic growth (RGDP). This study also attempts to make recommendations

based on the research findings. In accordance with the findings narrow money, broad money, exchange rate,

government revenue and expenditure have positive correlation with RGDP indicating that the unit increase in the

abovementioned variables will lead to the unit increase in RGDP. On the contrary, inflation rate and interest rate

on deposit have negative impact on RGDP. The results further revealed that there has been fluctuation in the trend

of interest rate and inflation rate throughout the observed period and a drastic fall has occurred in narrow money

between year 1999-00 and 2001-02. The upward trends have been observed in broad money, exchange rate,

government revenue and expenditure. The results also showed that more than 75% of the total variation of

dependent variable of each model (i.e., model 1, model 2, model 3 and model 4) used in this study is explained by

the explanatory variables of the given model. The study concluded that exchange rate, interest rate, inflation rate,

government revenue and government expenditure are significant variables that affect economic growth in

Bangladesh.

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

22

Our business's ability to borrow or

establish a line of credit can be largely

affected by how expensive or cheap it is for

banks to get money. The primary thing the

central bank of Bangladesh controls is the

interest rate for banks on borrowing money.

Not surprisingly, banks turnaround and pass

the savings or cost to their borrowers. When

the real interest rate is set low for banks,

commercial as well as consumer interest

rates also tend to decrease, making loans

more affordable.

Interest rates and the value of Taka

per dollar have a distinct relationship. When

the Bangladesh Bank makes the cost of

borrowing cheaper, more money starts

flowing in the economy. The more Taka that

are out there, the less each one is worth. The

value of Taka drops. Often, when the

Bangladesh Bank drops interest rates, it

intends to lower the taka's value in order to

make Bangladesh’s goods more affordable,

and therefore, increase Bangladesh’s

exports, which can foster growth in business

and jobs.

During the period of low interest

rates and increased money flowing through

the economy, inflation can occur if

economic production and employment do

not increase. Stagnant business, despite

increased cash, means that more money is

chasing fewer goods and prices rise. One of

the goals of monetary policy is to prevent

excessive inflation while fostering economic

growth.

On the other hand, the central

government, with the help of local

government, conducts the fiscal policy for

the country. As the fiscal policy has two

parts of revenue collection and expenditure,

it largely depends on the political decision

making. Fiscal policy is the most powerful

instruments that the government has to

stabilize the developing economy like

Bangladesh. When the economy is sluggish,

the government may cut taxes, leaving

taxpayer with extra cash to spend and

thereby increasing levels of consumption.

As the fiscal policy has always been

conducted by the central government, it is

central to health of any economy. As the

fiscal policy changes the tax lows and

government expenditures, it can affect

citizens, corporations and business climates

through disposable income. In this regard,

the interrelationship between public

spending and private sector performance is

of prime importance (Ekpo, 2003).

Governments use fiscal policy to

influence the level of aggregate demand in

the economy, in an effort to achieve

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

23

economic objectives of price stability, full

employment, and economic growth.

Government expenditure in recent years has

increased tremendously in attempt to solve

budgetary problems and also accelerate

economic growth.

Traditionally, the economists make

controversy among them about the impact of

fiscal and monetary policy. But the modern

economists believe that both policies have

impact on economic stabilization. On the

other way we can state that both policies

should be implemented simultaneously as

one can complement each other. If the

economy remains below the full

employment level in case of Bangladesh,

both the monetary and fiscal policy can

stimulate economic growth by invigorating

both nominal and real GDP.

The official goals usually include

relatively stable prices and low

unemployment. It is referred to as either

being expansionary or contractionary, where

an expansionary policy increases the total

supply of money in the economy more

rapidly than usual, and contractionary policy

expands the money supply more slowly than

usual or even shrinks it. Expansionary

policy is traditionally used to try to combat

unemployment in a recession by lowering

interest rates in the hope that easy credit will

entice businesses into expanding.

Contractionary policy is intended to slow

inflation in hopes of avoiding the resulting

distortions and deterioration of asset values.

2. Objectives of the Study

There is consensus view of opinion in

literatures as regards impact of fiscal and

monetary policies on economic growth in

developed and developing countries of the

world. In Bangladesh, there is still lack of

empirical studies about the effectiveness of

the fiscal and monetary policies. The main

purpose of this study is to test empirically

the effectiveness of macroeconomic policy

tools. The monetarists believe that the fiscal

policy is ineffective and another group

believes that monetary policy is ineffective

in any economy. The general objective of

the study is to examine the impact of fiscal

and monetary policies on economic growth

in Bangladesh.

Specific objectives of this study are

to determine the trend in monetary

and fiscal instrument over the years

(1979-80 to 2011-12);

to examine the impact of monetary

and fiscal policies on gross domestic

product being a proxy for economic

growth in Bangladesh; and

to make recommendations based on

research findings to enhance

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

24

economic growth and development

in Bangladesh.

3. Statement of Hypothesis

Ho: Fiscal and monetary policies have no

impact on economic growth of Bangladesh.

H1: Fiscal and monetary policy have a

significant impact on the economy of

Bangladesh.

4. Significance of the Study

The study is very relevant as it will

empirically show the impact of fiscal and

monetary policies on economic growth in

Bangladesh. However it is important to

study the effect of the two policies to ensure

the growth of real gross domestic product

(RGDP). Thus, the purpose of this study is

to fill the gap by testing the effectiveness of

two policy variables on RGDP in the case of

less developed country like Bangladesh.

This will also help the government to

establish policy mix to boost economic

growth and development.

5. Empirical Review

Monetary policy and fiscal policy are two

policy variables that are often used to

accelerate the economic growth. According

to the need of the central government,

Bangladesh Bank conducts monetary policy

to control money supply and the rate of

interest. Under the Financial Sector Reform

Programs (FSRP) in 1990s the legal,

institutional and policy frameworks have

been changed significantly (Bangladesh

Bank, 2009).

Ahmed and Islam (2004) mentioned

about the changes in the financial system of

Bangladesh under the reforms programs.

This reform ensures that Bangladesh Bank

can use both the market based instruments

and direct instruments to conduct monetary

policy and achieve their goal of stable price

and control financial intermediaries.

Therefore, with a view to making and

implementing smooth monetary policy the

central bank need to understand the distinct

active channels of monetary transmission

mechanisms in the economy of Bangladesh

(Ahmed and Islam, 2004).

It is widely accepted that the main

objective of monetary policy is to make the

price of an economy stable. Nowadays, the

central bank like Banco de Mexico has

changed their monetary policy objectives, by

setting price stability as their main goal

targeting low-level inflation (Banco de

Mexico, 2012). In a market economy, no

one can set the market price directly because

it has been determined by the market

mechanism of demand and supply. But the

central bank can influence the price-

determination process by using the monetary

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

25

policy and thus accomplish its inflation

target (Banco de Mexico, 2012).

Most empirical analyses are limited

to simple linear regressions of growth on

government revenues and expenditures.

Although the extensive variety of possible

theoretical relationships among government

revenues (taxation and other sources),

expenditures, and economic growth. Many

researchers performed a systematic

comparative analysis (both theoretically and

empirically) of the various economic

insights (fiscal policy, investments and

economic growth, etc) that were currently

available. Based on empirical experiments,

they indicated directions for future empirical

research that may enrich our knowledge on

the complex relationship between fiscal

policies and economic growth (Brons et al.,

1999).

Baum and Koester (2011) analyzed

quarterly German data from 1976 to 2009 by

threshold SVAR, expanding the SVAR

approach developed by Blanchard and

Perotti (2002). The threshold model gave

new idea about the impacts of fiscal shocks

on economic stability. Changing the time,

size and direction of the shocks may alter

the impacts of shocks. When there is

negative output gap the fiscal spending

multipliers are more effective than when

there is positive output gap. But

discretionary revenue policies have

generally more limited impacts on fiscal

shocks (Baum and Koester, 2011).

6. Methodology

The area of study is Bangladesh. The

sources of data were mainly from secondary

sources. We collected data from two

sources: (1) Monthly Economic Trend

published by Bangladesh Bank and (2)

Economy watch

(www.economywatch.com). Time series

data spinning from 1979-80 to 2012-13 were

gathered on seven independent variables

namely exchange rate, interest rate on

deposit, inflation rate, broad money, narrow

money, government revenue and

government expenditure and one dependent

variable which is gross domestic product.

6.1. Analytical Techniques

Different types of descriptive and inferential

statistical techniques adopted in this study

are narrated below:

6.1.1. Trend Analysis

This involves using line diagrams to show

the trends in all macro-economic variables,

i.e., exchange rate, interest rate, inflation

rate, narrow money, broad money,

government revenue, and government

expenditure). This technique fits a trend line

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

26

to a series of historical data points and

projects the line into the future for medium

to long-range forecasts. The method we

have applied here is the least squares

method which results in a straight line that

minimizes the sum of the squares of the

vertical differences or deviations from the

line to each of the actual observations. The

trend equation can be expressed as follows:

ŷ𝑡 = 𝑎 + 𝑏𝑥 (1)

Where, ŷ is a computed value of the variable

to be predicted (i.e., dependent variable) and

x is the independent variable (which in this

case is time).

a = y-axis intercept

b = slope of the trend line (i.e., the rate of

change in y for given change in x)

x = time (i.e., the independent variable)

6.1.2. Correlation Coefficient

With a view to identifying the linear

relationship between macroeconomic

variables, we have used the following

formula:

rxy = ∑ (xi−x)(yi−y)n

i=1

(n−1)sxsy=

∑ (xi−x)(yi−y)n

i=1

√∑ (xi−x)2 ∑ (yi−y)2ni=1

ni=1

(2)

6.1.3. Model specification

Our empirical model has been specified in

the following manner:

𝑦𝑡 = 𝑓 (𝑀𝑃𝑡 , 𝐹𝑃𝑡) (3)

Where, Y is a measure of economic activity

in which Gross Domestic Product (GDP) is

employed as a proxy, MP and FP are

measures of monetary and fiscal actions of

the government respectively.

Exchange Rate, interest Rate,

inflation, narrow money (M1) and broad

money (M2) are employed as proxies for

monetary policy variables while the fiscal

variables are government revenue and

government expenditure. The subscript (t)

means time period. The models are

explicitly specified as:

Model 1

RGDP = β0+ β1M1+ β2M2+β3ER+ β4INT+

β5INF (4)

Model 2

RGDP = α0+ α1GREV+ α2GEXP (5)

Model 3

RGDP = γ0 + γ1M1 + γ2M2 + γ3ER + γ4INT +

γ5INF + γ6GREV + γ7GEXP + Et (6)

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

27

Model 4

RGDP = τ0 + τ1ΣMV + τ2ΣFV (7)

Where,

Et = Error term

β0 β1 β2 β3 β4 and β5 are the coefficients of

the independent variable

RGDP = Real gross domestic product

(billion)

M1 = Narrow money supply (million)

M2 = Broad money supply (million)

ER = Exchange Rate (against USD) (Period

average)

INT = Interest rate (%) (Weighted average)

INF = Inflation rate (%) (Period average)

GREV = Government revenue (billion)

GEXP = Government expenditure (billion)

ΣMV = Sum of all monetary variables

ΣFV = Sum of all fiscal variables

The model was estimated using

Ordinary Least Square techniques (OLS). It

was subjected to a dynamic estimation using

the lag structure of the variables. There will

be determination of the existence of

substantial co-movements among time series

variables. The reason for this is that when

the dependent and independent variables

have unit roots, traditional estimation

method, using observations on levels of

those variables would likely find a

statistically significant relationship even

when meaningful “economic” linkage is

absent (Akinlo and Odusola, 2003).

7. Results and Discussions

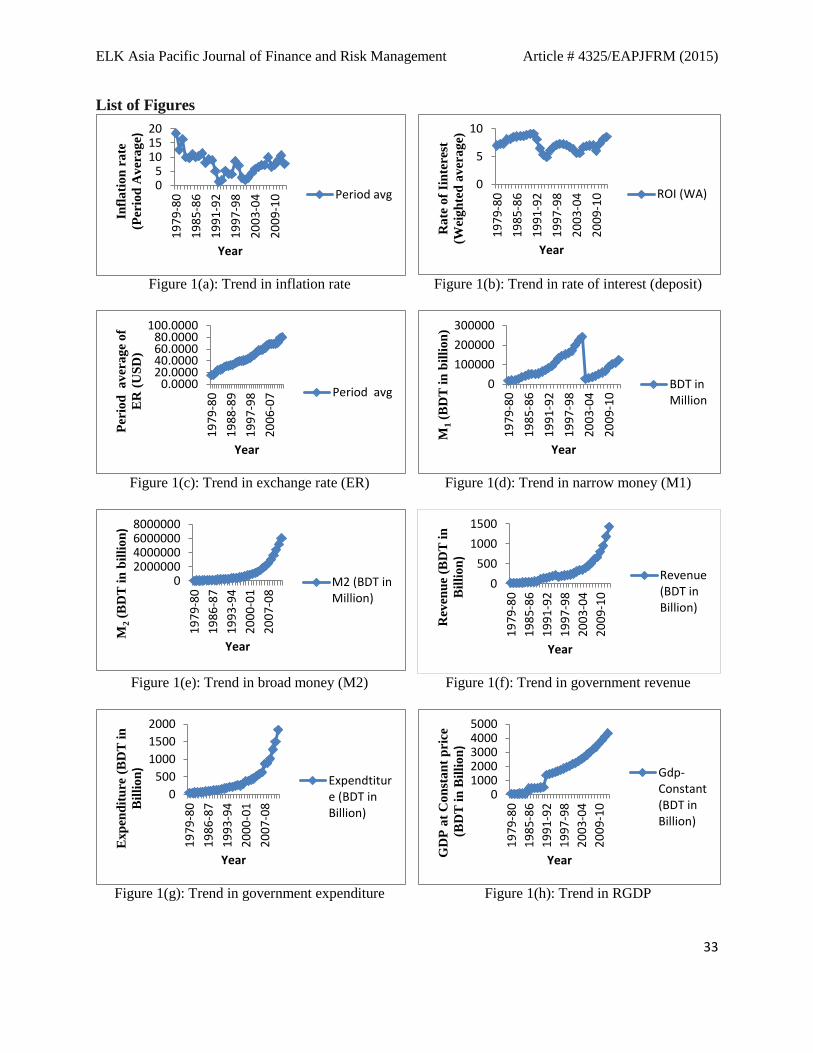

7.1. Trend Analysis

Figure 1(a) shows the inflationary trend. In

1979-80, the inflation rate was very high,

after 1983-84 it remains stable then tends to

fall in mid 1990s. It increased in 1999-2000

and fell back in 2001-02; it rose steadily

after 2001-02.

Figure 1(b) shows the movement of

interest rate over the period 1979-80 to

2012-13. Over the period the interest rate

remains between 4% and 9%. In 1991-92 it

was high and dropped to 4% in 1995-96.

After 2009-10 it rose gradually till 2012-13.

We all know that there is a direct

relationship between interest rate and saving

and an inverse relationship between

investment and interest rate; which may be

the cause of such stable fluctuations.

Figure 1(c) shows trend in Exchange

rate of Bangladeshi taka to US dollar. We

can clearly see from the figure that the

exchange rate increases steadily over time

starting from 15 taka per USD in 1979-80 to

78 taka per USD in 2012-13. One of the

probable reasons behind this may be the

government is trying to control the exchange

rate to boost up the confidence of the

exporters in Bangladesh.

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

28

Figure 1(d) shows that there has been

a continuous increase in the supply of

currency with non-bank and demand deposit

between the periods of 1979-80 and 2012-13

except in 2001-02 when the supply of

money had been reduced sharply by the

government. The reason for sharp decline

may be controlling the inflationary pressure.

Figure 1(e) shows that amount of

money and liquidity in the economy

continues to increase from 1979-80 to 2012-

13. Figure 1(f) shows that government

revenue continues to increase from 1979-80

till 2012-13. Figure 1(g) shows that the

government expenditure continues to

increase from 1979-80 to 2012-13. Figure

1(h) shows that although there are larger

hikes in 1985-86 and 1991-92 but the

growth in RGDP remains stable from 1979-

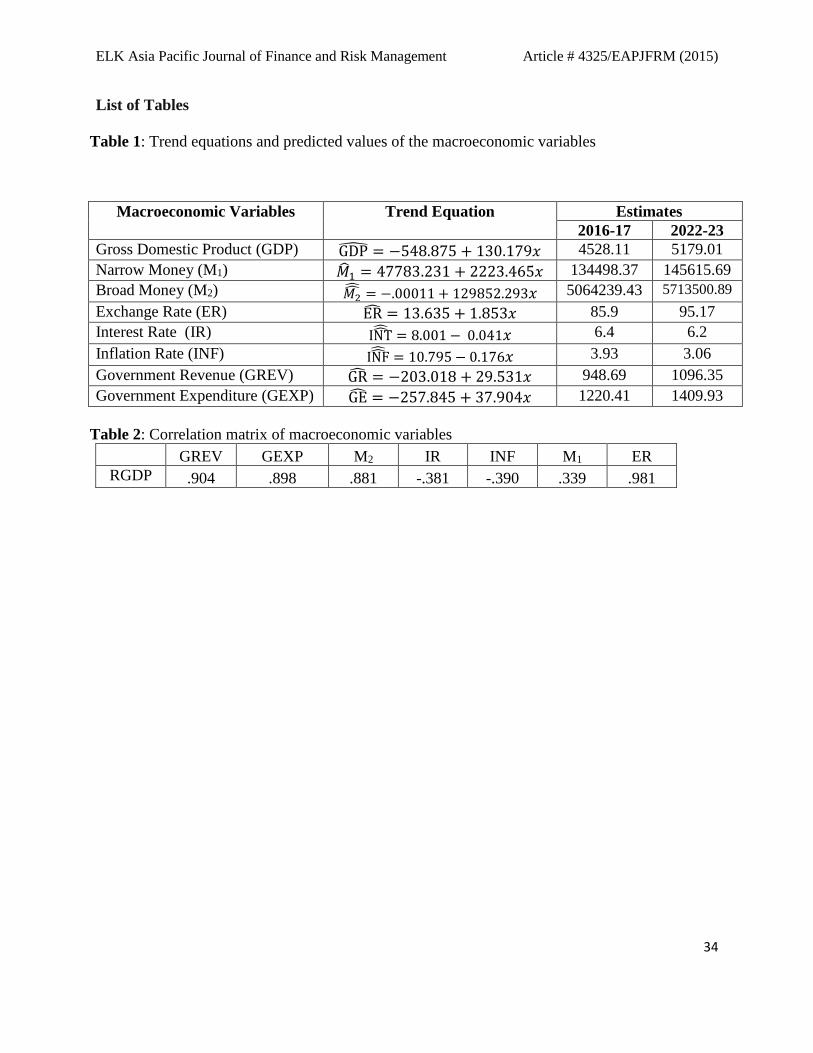

80 to 2012-13. The projected figures of all

the macroeconomic variables have been

showed in two phases, namely 5 years

(2016-17) and ten years (2022-23). All the

estimates except for inflation rate and

interest rate on deposit are showing

significant upward trend (Insert Table 1

here)

7.2. Correlation Matrix

This shows the linear relationship between

RGDP and other variables (i.e., exchange

rate, interest rate, inflation, M1, M2,

government revenue and government

expenditure).

(Insert Table 2 here)

The results of Table 2 disclose that RGDP

has strong positive correlation with GREV,

GEXP, M2 and ER which refer to strong

influence of each of the aforementioned

variables on RGDP. On the contrary, there

exists a weak negative correlation between

RGDP and IR. The thing goes same between

RGDP and INF. These indicate both of these

variables have negative impact on RGDP. In

addition, it is found that the linear

relationship between RGDP and M1 is weak

in positive direction.

7.3. Multiple Linear Regression Models

7.3.1. RGDP and Monetary Instruments

The result reveals that there is inverse

relationship between economic growth and

interest rate & inflation, whereas there is a

positive relationship between economic

growth and other variables (exchange rate,

M1 and M2). Thus, exchange rate, M1, M2,

growth will increase RGDP while holding

interest rate and inflation constant, but the

reverse is the case for interest rate &

inflation, when exchange rate, M1 and M2

are held constant. The t-statistics show the

significant relationship between RGDP and

the estimated macroeconomic variables. R-

square value shows that 79% of total

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

29

variation in GDP is being explained by the

explanatory variables. F-statistics value of

739.519. Only exchange rate and interest

rate are showing significant on the GDP.

Summary of regression results:

Model 1

RGDP = 483.768 + 0.001M1+ 0.000M2+ 45.896ER – 175.615INT – 2.130INF (8)

(1.689) (2.587) (6.491) (12.321) (-6.885) (-0.200)

R-square = 0.79 (79.0%)

F-statistic = 739.519 (Significant at 0.000)

D.W= 1.518

Figures in parentheses are values of t-statistic

7.3.2. RGDP and Fiscal Policy

The result shows the positive relationship

between economic growth and Government

revenue and a negative relationship between

economic growth and government

expenditure. The co-efficient of

determination, R-square reveals that 82% of

the variations in RGDP are being explained

by government revenue and government

expenditure. The f-statistics also shows that

the model is statistically significant.

However, the model also revealed positive

serial correlation as shown in the value of

Durbin Watson test of 0.202.

Summary of regression results:

Model 2

RGDP = 643.595 + 5.936GREV – 1.916GEXP (9)

(4.778) (1.509) (-0.630)

R-square = 0.82 (82.0%)

F-statistic = 70.705 (Significant at 0.000)

D.W=0.202

7.3.3. RGDP, Monetary and Fiscal

Policies

This model examined the relationship

between GDP and the fiscal and monetary

policies in Bangladesh. The result shows

that M1, M2, ER, revenue and expenditure

have positive relation with RGDP, while

other variables (INF and INT) have negative

relationship with GDP. The R-square shows

that 76% of the variation in GDP is ascribed

to joint consideration of all variables of the

two sectors. The F-statistic indicates that the

specified model is significant. The series

possess a level of positive autocorrelation as

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

30

the Durbin Watson test shows that the value

is approximately 1.486, which is less than 2.

Summary of regression results:

Model 3

RGDP = 475.871 + 0.001M1 + 0.000M2 + 45.655ER – 175.433INT – 1.757INF + 0.078GREV

+ 0.147GEXP

(1.522) (2.312) (0.811) (11.169) (-6.572) (-0.147) (0.068) (0.133) (10)

R-squared = 0.760 (76.0%)

F-statistic = 380.163 (Significant at 0.000)

D.W = 1.486

7.3.4. RGDP, Sum of Monetary Variables

and Sum of Fiscal Variables

This model examined the relationship

between GDP and the sum of fiscal and

monetary variables in Bangladesh. The

result shows that MV have negative and FV

have positive relation on GDP. The R-

square shows that 83.3% of the variation in

GDP is attributed to joint consideration of

the sum of variables of the two sectors. This

implies that a unit increase in the number of

independent variables will lead to a unit

increase in GDP. While the f-statistics

indicates that the specified model is

statistically significant. The series possess

positive serial correlation (autocorrelation)

as the Durbin Watson test shows that the

value is approximately 0.425, which is less

than 2.

Summary of regression results:

Model 4

RGDP = 381.802 - 0.002ΣMV+ 4.7257ΣFV (11)

(2.023) (-1.922) (2.815)

R-square = 0.833 (83.3%)

F-statistic = 77.185 (Significant at 0.000)

D.W = 0.425

8. Summary of Findings

The study focuses on the impact of

monetary and fiscal policies of Bangladesh.

These have been evaluated by addressing

some critical hypotheses of these

instruments on the economy. The study has

been able to find out that there has been

fluctuation in the trend of policy variables in

Bangladesh considered with reference to the

year 1979-80 to 2012-13. The result of

regression shows that 99.0% of the

variations (model 1) in the dependent

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

31

variable had been explained by the

explanatory variables. In model 2, 82.0% of

the variations in dependent variable were

explained by the explanatory variable while

99.0% of the total variation has been

explained by the explanatory variables

(model 3) and 83.3% of the variations in the

dependent variable of model 4 had been

explained by the explanatory variables as

indicated above. The result further shows

that narrow money, broad money, exchange

rate, and government revenue and

government expenditure have positive

relationship with RGDP which shows that a

unit increase in those variables will lead to a

unit increase in GDP. Inflation and interest

rate have negative impact on GDP, and

significant at 1% probability level. Thus,

these variables contribute to economic

growth.

9. Conclusions

Keynesian economics suggests that

increasing government spending and

decreasing tax rates are the best ways to

stimulate aggregate demand, and decreasing

spending & increasing taxes after the

economic boom begins. Keynesians argue

this method to be used in times of recession

or low economic activity as an essential tool

for building the framework for strong

economic growth and working towards full

employment.

The research study examined the impact of

fiscal and monetary policies on economic

growth of Bangladesh to the period of 1979-

80 to 2012-13. The study concluded that

exchange rate, interest rate, inflation rate,

government revenue and government

expenditure are significant policy variables

that affect economic growth in Bangladesh

(i.e., using Real Gross Domestic Product as

proxy for economic growth). The study

therefore opined and recommends that in

order to put Bangladesh economy on the

path of sustainable growth and development;

the government must put emphasis on its

fiscal and monetary policies with the

cooperation of Bangladesh Bank in order to

enhance the welfare of their citizen.

10. References

[1] Ahmed, S. and Islam, M.E. (2004). The

Monetary transmission Mechanism in

Bangladesh: Bank Lending and

exchange Rate Channels. The

Bangladesh Development Studies, 30

(3&4), 31-87.

[2] Akinlo, A.E. and Odusola, A.T. (2003).

Assessing the impact of Nigeria’s naira

depreciation on output and inflation.

Applied Economics, 35(6), 691-703, doi:

10.1080/0003684032000056823.

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

32

[3] Banco de Mexico (2012). The Effects of

Monetary Policy on the Economy.

[4] Baum, A. and Koester, G.B. (2011). The

impact of fiscal policy on economic

activity over the business cycle –

evidence from a threshold VAR analysis.

Discussion Paper Series 1: Economic

Studies, Deutsche Bundesbank, No 03.

[5] Blanchard, O. and Perotti, R. (2002). An

Empirical Characterization of the

Dynamic Effects of Changes in

Government Spending and Taxes on

Output. Quarterly Journal of Economics

117(4), 1329-1368, doi:

10.1162/003355302320935043.

[6] Brons, M., Groot, H.L.F. and Nijkamp,

P. (1999). Growth Effects of Fiscal

Policies: A Comparative Analysis in a

Multi-Country Context. Tinbergen

Institute Discussion Papers. Number 99-

042/3, June.

[7] Bangladesh Bank (2009). Monetary

Policy Review, October 2005-July 2009.

[8] Ekpo, A. (2003). The Macroeconomic

Policy Framework: Issues and

Challenges. Central Bank of Nigeria 3rd

Annual Monetary Policy Conference

Proceedings on Issues in Fiscal

Management: Implications for Monetary

Policy in Nigeria, Central Bank of

Nigeria Publications, Lagos.

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

33

List of Figures

Figure 1(a): Trend in inflation rate

Figure 1(b): Trend in rate of interest (deposit)

Figure 1(c): Trend in exchange rate (ER)

Figure 1(d): Trend in narrow money (M1)

Figure 1(e): Trend in broad money (M2)

Figure 1(f): Trend in government revenue

Figure 1(g): Trend in government expenditure Figure 1(h): Trend in RGDP

05

101520

19

79

-80

19

85

-86

19

91

-92

19

97

-98

20

03

-04

20

09

-10

Infl

ati

on

ra

te

(Per

iod

Av

era

ge)

Year

Period avg0

5

10

19

79

-80

19

85

-86

19

91

-92

19

97

-98

20

03

-04

20

09

-10

Ra

te o

f Ii

nte

rest

(Wei

gh

ted

av

era

ge)

Year

ROI (WA)

0.000020.000040.000060.000080.0000

100.0000

19

79

-80

19

88

-89

19

97

-98

20

06

-07

Per

iod

a

ver

ag

e o

f

ER

(U

SD

)

Year

Period avg0

100000

200000

300000

19

79

-80

19

85

-86

19

91

-92

19

97

-98

20

03

-04

20

09

-10

M1

(BD

T i

n b

illi

on

)Year

BDT inMillion

02000000400000060000008000000

19

79

-80

19

86

-87

19

93

-94

20

00

-01

20

07

-08

M2

(BD

T i

n b

illi

on)

Year

M2 (BDT inMillion)

0

500

1000

15001

97

9-8

0

19

85

-86

19

91

-92

19

97

-98

20

03

-04

20

09

-10

Rev

enu

e (B

DT

in

Bil

lio

n)

Year

Revenue(BDT inBillion)

0

500

1000

1500

2000

19

79

-80

19

86

-87

19

93

-94

20

00

-01

20

07

-08

Exp

end

itu

re (

BD

T i

n

Bil

lio

n)

Year

Expendtiture (BDT inBillion)

010002000300040005000

19

79

-80

19

85

-86

19

91

-92

19

97

-98

20

03

-04

20

09

-10

GD

P a

t C

on

sta

nt

pri

ce

(BD

T i

n B

illi

on)

Year

Gdp-Constant(BDT inBillion)

ELK Asia Pacific Journal of Finance and Risk Management Article # 4325/EAPJFRM (2015)

34

List of Tables

Table 1: Trend equations and predicted values of the macroeconomic variables

Table 2: Correlation matrix of macroeconomic variables

GREV GEXP M2 IR INF M1 ER

RGDP .904 .898 .881 -.381 -.390 .339 .981

Macroeconomic Variables Trend Equation Estimates

2016-17 2022-23

Gross Domestic Product (GDP) GDP = −548.875 + 130.179𝑥 4528.11 5179.01

Narrow Money (M1) ��1 = 47783.231 + 2223.465𝑥 134498.37 145615.69

Broad Money (M2) 𝑀2 = −.00011 + 129852.293𝑥 5064239.43 5713500.89

Exchange Rate (ER) ER = 13.635 + 1.853𝑥 85.9 95.17

Interest Rate (IR) INT = 8.001 − 0.041𝑥 6.4 6.2

Inflation Rate (INF) INF = 10.795 − 0.176𝑥 3.93 3.06

Government Revenue (GREV) GR = −203.018 + 29.531𝑥 948.69 1096.35

Government Expenditure (GEXP) GE = −257.845 + 37.904𝑥 1220.41 1409.93