Embed Size (px)

Citation preview

BHP Petroleum

The Effects of Increasing Demand on

the Dynamics of the Gas Business

Seapex Presentation

Singapore

February 1997

BHP Petroleum

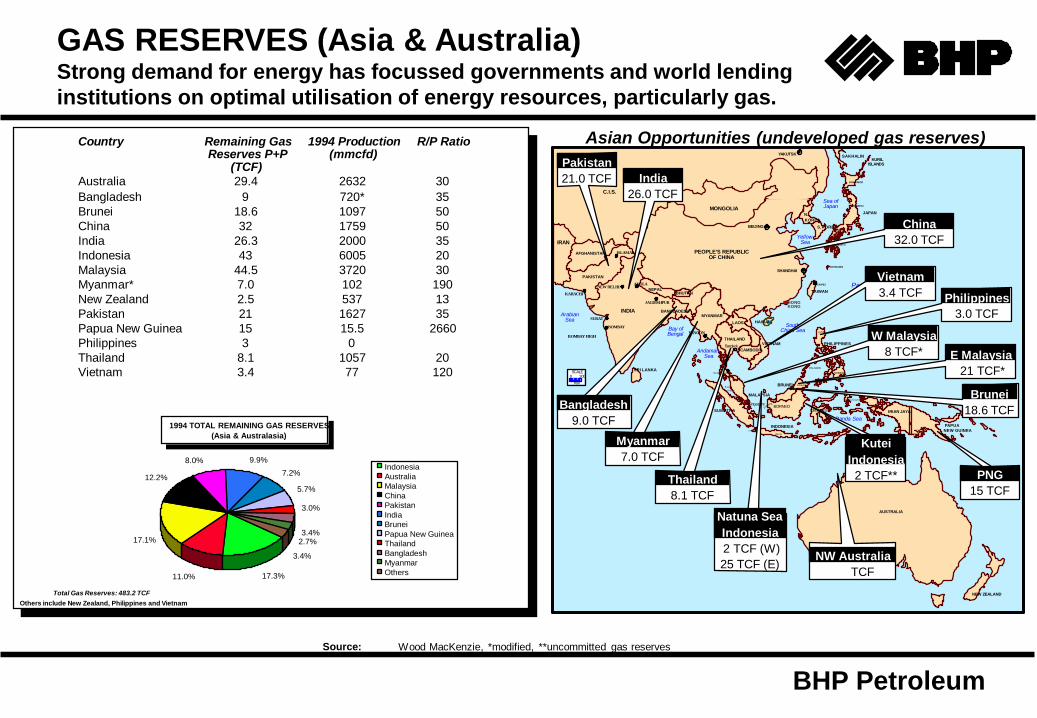

GAS RESERVES (Asia & Australia)Strong demand for energy has focussed governments and world lending

institutions on optimal utilisation of energy resources, particularly gas.

Source: Wood MacKenzie, *modified, **uncommitted gas reserves

Country Remaining Gas Reserves P+P

(TCF)

1994 Production (mmcfd)

R/P Ratio

Australia 29.4 2632 30

Bangladesh 9 720* 35

Brunei 18.6 1097 50

China 32 1759 50

India 26.3 2000 35

Indonesia 43 6005 20

Malaysia 44.5 3720 30

Myanmar* 7.0 102 190

New Zealand 2.5 537 13

Pakistan 21 1627 35

Papua New Guinea 15 15.5 2660

Philippines 3 0

Thailand 8.1 1057 20

Vietnam 3.4 77 120

1994 TOTAL REMAINING GAS RESERVES

(Asia & Australasia)

Total Gas Reserves: 483.2 TCF

Others include New Zealand, Philippines and Vietnam

Asian Opportunities (undeveloped gas reserves)

LUZON

PALAWAN

MINDANAO

M A NILA

SUMATRABORNEO

SABAH

CELEBES

MOLUCCAS

PAPUA

SRI LANKA

PHILIPPINES

NEW GUINEA

JAPANN.

S.

SCALE0 300

KM

KOREA

KOREA

SAKHALIN

HOKKAIDO

HONSHU

KYUSHU

SHIKOKU

KURILISLANDS

HAINAN

TAIWAN

HONGKONG

Singapore

Segam at

Kuala

Lumpur

Su rat Thani

Bangkok

TAIPEI

OKINAWA

J A K A R TA

YANGON

ISLAMABAD

KARACHI

BEIJING

YAKUTSK

SHANGHAI

BOMBAY HIGH

BOMBAY

SURAT

JAGDISHPUR

NEW DELHIANOLA

Sea ofJapan

Yellow Sea

Pacific Ocean

SouthChina Sea

Banda Sea

Arafura Sea

AndamanSea

Bay ofBengal

ArabianSea

C.I.S.

MONGOLIA

PEOPLE'S REPUBLICOF CHINA

IRAN

AFGHANISTAN

PAKISTAN

INDIA

NEPALBHUTAN

BANGLADESHMYANMAR

LAOS

THAILAND

CAMBODIA

VIETNAM

BRUNEI

MALAYSIA

INDONESIA

IRIAN JAYA

AUSTRALIA

NEW ZEALAND

Bangladesh

9.0 TCF

Myanmar

7.0 TCF

Thailand

8.1 TCF

PNG

15 TCF

E Malaysia

21 TCF*

W Malaysia

8 TCF*

Philippines

3.0 TCF

Brunei

18.6 TCF

Vietnam

3.4 TCF

Natuna Sea

Indonesia

2 TCF (W)

25 TCF (E)

Kutei

Indonesia

2 TCF**

NW Australia

TCF

China

32.0 TCF

India

26.0 TCF

Pakistan

21.0 TCF

17.3%11.0%

17.1%

12.2%

8.0% 9.9%

7.2%

5.7%

3.0%

3.4%2.7%

3.4%

Indonesia

Australia

Malaysia

China

Pakistan

India

Brunei

Papua New Guinea

Thailand

Bangladesh

Myanmar

Others

BHP Petroleum

GAS PRICINGStrong demand, and high value and prices for gas in power generation,

means that regional pricing depends primarily on proximity to power

demand markets.

LUZON

PALAWAN

MINDANAO

MANILA

BORNEO

SABAH

CELEBES

MOLUCCAS

SCALE0 300

KM

HOKKAIDO

HONSHU

KYUSHU

SHIKOKU

KURILISLANDS

Singapore

Segam at

Ku ala

Lumpur

Surat Thani

Bangkok

TAIPEI

OKINAWA

JAKARTA

YANGON

ISLAMABAD

KARACHI

BEIJING

YAKUTSK

SHANGHAI

BOMBAYHIGH

BOMBAY

SURAT

JAGDISHPUR

NEWDELHIANOLA

Sea ofJapan

Yellow Sea

Pacific Ocean

SouthChina Sea

Banda Sea

Arafura Sea

AndamanSea

Bay ofBengal

ArabianSea

C.I.S.

MONGOLIA

PEOPLE'S REPUBLICOF CHINA

IRAN

AFGHANISTAN

PAKISTAN

INDIA

NEPALBHUTAN

BANGLADESHMYANMAR

LAOS

THAILAND

CAMBODIA

VIETNAM

BRUNEI

MALAYSIA

INDONESIA

IRIAN JAYA

AUSTRALIA

NEW ZEALAND

Undeveloped resources without markets

Gas demand centres

Indicative market price *

(US$/GJ)

$3.80

$3.80

$3.80

$3.00

$3.00

$1.30

$1.50

SUMATRA

PAPUA

SRILANKA

PHILIPPINES

NEWGUINEA

JAPANN.

S.

KOREA

KOREA

SAKHALIN

HAINAN

TAIWAN

HONGKONG

$3.00

$2.50

$2.20

$3.80

$1.50$2.50

* for end user

$1.50

$3.10

$2.60

$2.00

$0.50* For the Middle East:

Strong rates of economic growth

Developing countries on the threshold of industrialisation

Fast rising demand for electrical power (i.e. widening

capacity shortfalls)

Environmental constraints

Gas fired power generation capacity expansion

(i.e. GTCC technology)

short construction lead time

higher generation efficiency

lower emissions (i.e. as against coal)

Co-generation

Strong demand for gas into power generation

Relatively high gas price ~ US$2.00/Mcf upwards cf urea

feedstock

High intrinsic value as a result of competing fuel prices

BHP Petroleum

INDONESIAGas in Indonesia has been primarily developed for the export market to East

Asia. The large gas resource base will continue to permit an export focus.

INDONESIA GAS MARKET(Supply/Demand Balance)

TIMOR

BUTON

Alor

Tali AbuJambi

Bandung

Bandar Lampung

JAKARTA

Lhok Seumawe

Medan

Padang

Bengkulu

Palembang

Pontianak

Banjarmasin

Semarang

Yogyakarta

Banda Aceh

Manado

Palu

Kendari

Denpasar

Kupang

Mataram

BRUNEI PHILIPPINES

MALAYSIASINGAPORE

MALAYSIA

THAILAND

Flores

Sumba

Bangka

SOUTH CHINA SEA

INDIAN

OCEAN

CELEBES

SEA

JAVA SEA

FLORES SEA

Simeulue

Nias

Siberut

Togian

Ujungpandang

Sumbawa

Belitung

JAVA

KALIMANTAN

Palangkaraya

SULAWESI

Samarinda

0 km 600

Bali

SUMATRA

Natuna

Lombok

KangeanMaduraSurabaya

120100

5

0

5

120°100°

C. Sumatra0.5 Bt provenBrown coal

S. Sumatra1.8 Bt provenBrown coal

Arunsoon to decline

6 TCF

1 TCF

2 TCF 25 TCF

1.1 TCF0.4 TCF

Natuna potential LNGHigh CO2

1.8 TCF

1 TCF

0.5 TCF0.3 TCF

1.5 TCF

0.5 TCF

2 Bt Black coal

10 TCF

E. Kalimantan6 trains plus 22 TCF uncommitted

Indonesia has significant gas reserves located primarily in remote areas.

Largest reserves are located in North Sumatra and East Kalimantan with gas used mostly for LNG plants.

Natuna will be developed initially as an LNG project.

Currently over half the gas produced in Indonesia is liquefied into LNG, and further investments in gas export infrastructure at

East Kalimantan and Natuna are planned.

Java's industrialisation and energy demand growth is generating strong domestic gas demand

Demand projection as per Pertamina forecast

Supply projecction as per Wood MacKenzie

East Kalimantan North Sumatra South Sumatra Java Other Fields

0

2000

4000

6000

8000

93 94 95 96 97 98 99 2000 2001 2002 2003 2004

YEAR

Ga

s R

eq

uir

em

en

ts (

mm

cfd

)

LNG Capacity Feedstock Power Generation City Gas & CNG Industry

BHP Petroleum

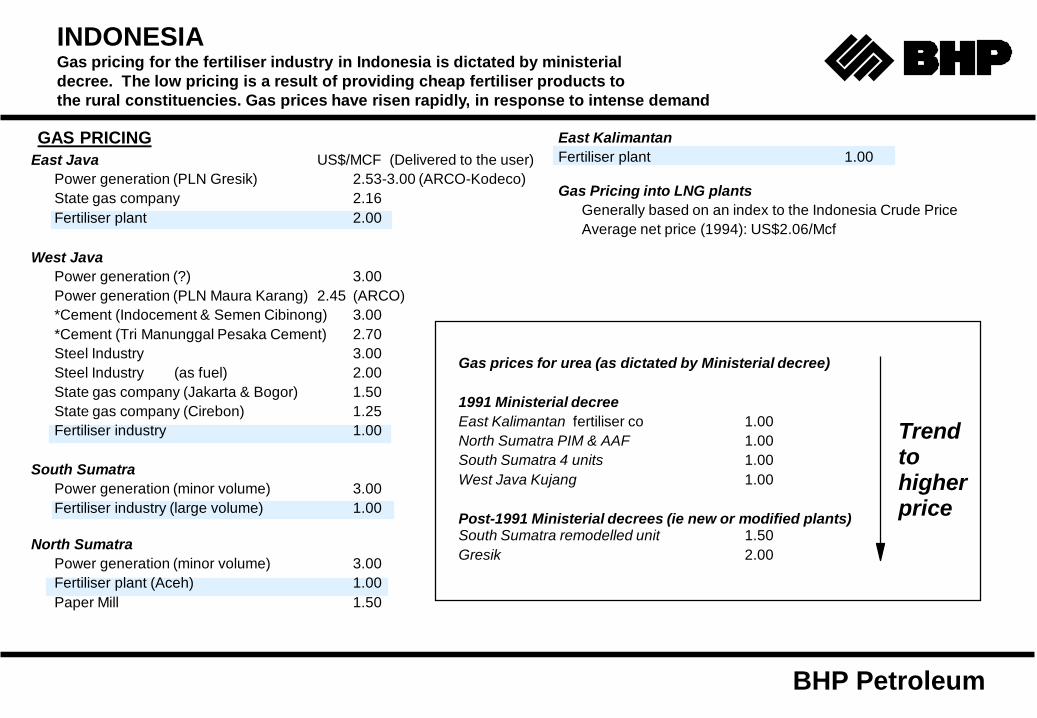

INDONESIAGas pricing for the fertiliser industry in Indonesia is dictated by ministerial

decree. The low pricing is a result of providing cheap fertiliser products to

the rural constituencies. Gas prices have risen rapidly, in response to intense demand

GAS PRICING East Kalimantan

Fertiliser plant 1.00

Gas Pricing into LNG plants

Generally based on an index to the Indonesia Crude Price

Average net price (1994): US$2.06/Mcf

East Java US$/MCF (Delivered to the user)

Power generation (PLN Gresik) 2.53-3.00 (ARCO-Kodeco)

State gas company 2.16

Fertiliser plant 2.00

West Java

Power generation (?) 3.00

Power generation (PLN Maura Karang) 2.45 (ARCO)

*Cement (Indocement & Semen Cibinong) 3.00

*Cement (Tri Manunggal Pesaka Cement) 2.70

Steel Industry 3.00

Steel Industry (as fuel) 2.00

State gas company (Jakarta & Bogor) 1.50

State gas company (Cirebon) 1.25

Fertiliser industry 1.00

South Sumatra

Power generation (minor volume) 3.00

Fertiliser industry (large volume) 1.00

North Sumatra

Power generation (minor volume) 3.00

Fertiliser plant (Aceh) 1.00

Paper Mill 1.50

Gas prices for urea (as dictated by Ministerial decree)

1991 Ministerial decree

East Kalimantan fertiliser co 1.00

North Sumatra PIM & AAF 1.00

South Sumatra 4 units 1.00

West Java Kujang 1.00

Post-1991 Ministerial decrees (ie new or modified plants)South Sumatra remodelled unit 1.50

Gresik 2.00

Trend to higher price

BHP Petroleum

THAILANDThailand's gas supply is heavily committed to power generation expansion

plans. Domestic ammonia/urea production is not likely to occur.

Gas reserves are mainly concentrated offshore in the Gulf of Thailand (i.e. 7 TCF)

Expanding infrastructure

capacity debottlenecking.

links with Myanmar and Malaysia

PTT has a contract for 525 mmcfd of gas from the Yadana offshore gasfield starting from 1998

The power generation sector will continue to dominate gas demand (i.e. EGAT plans to double gas-fired capacity over the next 10 years).

Industrialisation in the country is driving a high growth rate in electricity consumption.Gas use in the residential and industrial sectors will grow as the pipeline network is expanded (i.e. Bangkok ring).Local gas supply is constrained.Pipeline imports from Myanmar and Malaysia represents the best option for incremental gas supply.Potential LNG buyer.

ANDAMAN SEA

MYANMAR

THAILAND

LAOS

CAMBODIA

VIETNAM

MALAYSIA

INDONESIA

BASIR GUDANG

SEGAMAT

KUALA

LUMPUR

BANGKOK

Khonkaen

Rayong

SONG KHLA

PRAI

ARUN

KhanchanaburiYadana

ERAWAN

COMPLEX

BONGKOT

BEKOK

DUYONG

SOTONG

NAMPHONG

JOINT DEVELOPMENT AREA

KERTEH

(THAILAND-MALAYSIA)

Kang Koi

Ta Luang

Yetagun

Bang Pa -in

Ratchburi Bangpakong

Platong

Khanom

Krabi

Natural gas field

Natural gas demand location

Existing pipeline

Future pipeline

LNG

LNG (possibility)

THAILAND NATURAL GAS MARKET(Supply/Demand Balance)

* Assumes all IPP generating capacity to be gas fired (ie LNG) IPP to build a total at 10600 MW by 2006

Demand projections as per PTT forecast and EGAT generation energy plan

Supply projections as per Wood MacKenzie

1st Contract (Unocal) 2nd Contract (Unocal) 3rd Contract (Unocal) Pailin (Unocal)

Sikirit (Shell) Nam Phong (Esso) Bongkot (Total) Yadana (Total)

Yetagun (Texaco) JDA

0

1000

2000

3000

4000

90 91 92 93 94 95 96 97 98 99 2000 2001 2002 2003 2004 2005

YEAR

Ga

s R

eq

uir

em

en

ts (

mm

cfd

)

Feedstock Industry Bangkok Ring EGAT (Energy Plan) IPP

BHP Petroleum

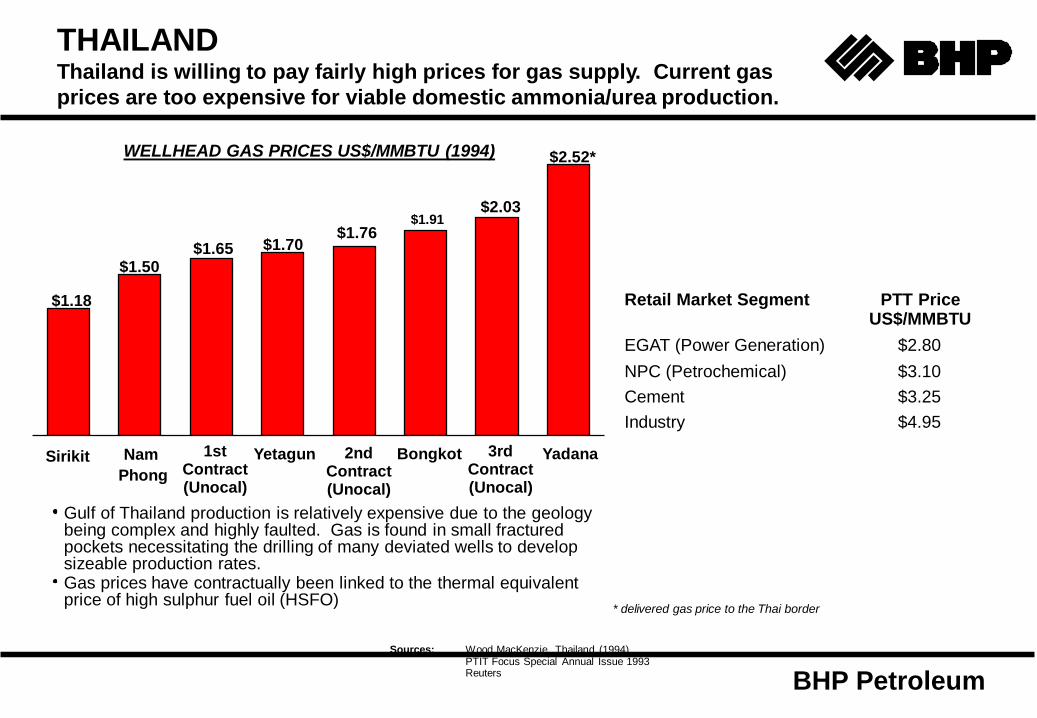

THAILANDThailand is willing to pay fairly high prices for gas supply. Current gas

prices are too expensive for viable domestic ammonia/urea production.

Retail Market Segment PTT Price US$/MMBTU

EGAT (Power Generation) $2.80

NPC (Petrochemical) $3.10

Cement $3.25

Industry $4.95

Gulf of Thailand production is relatively expensive due to the geology being complex and highly faulted. Gas is found in small fractured pockets necessitating the drilling of many deviated wells to develop sizeable production rates.Gas prices have contractually been linked to the thermal equivalent price of high sulphur fuel oil (HSFO)

* delivered gas price to the Thai border

Sources: Wood MacKenzie, Thailand (1994)PTIT Focus Special Annual Issue 1993Reuters

WELLHEAD GAS PRICES US$/MMBTU (1994)

Sirikit Nam

Phong

1st Contract (Unocal)

Yetagun 2nd Contract (Unocal)

Bongkot 3rd Contract (Unocal)

Yadana

$1.18

$1.50$1.65 $1.70

$1.76$1.91

$2.03

$2.52*

BHP Petroleum

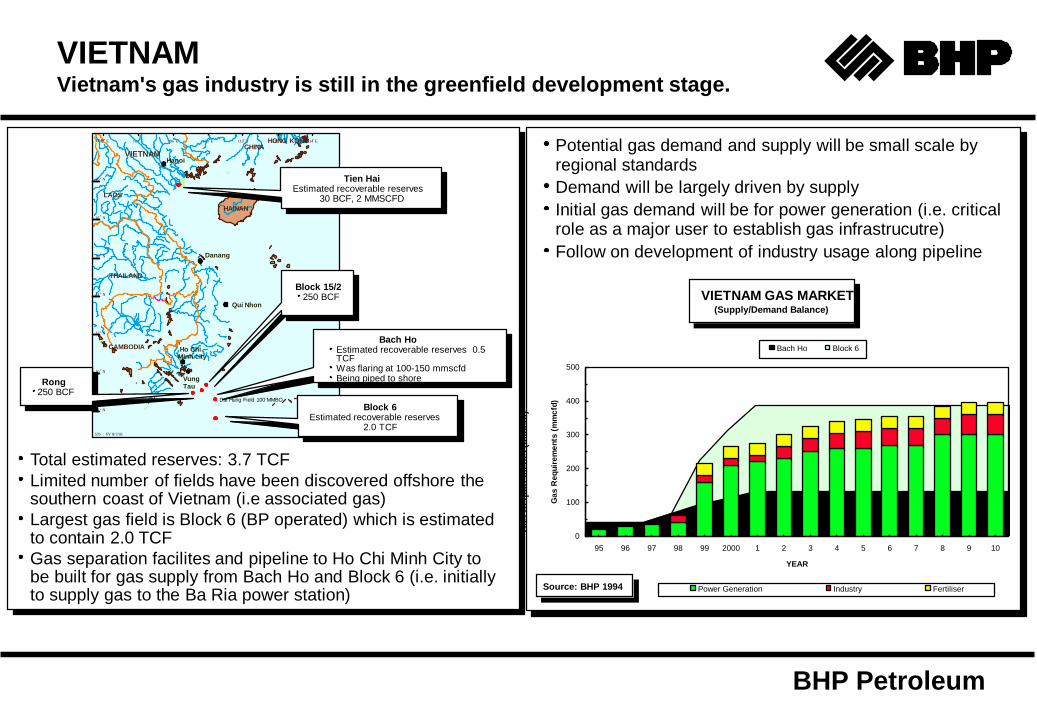

VIETNAMVietnam's gas industry is still in the greenfield development stage.

VIETNAM GAS MARKET(Supply/Demand Balance)

Source: BHP 1994

Gas R

eq

uir

em

en

ts (

mm

cfd

)

Total estimated reserves: 3.7 TCF

Limited number of fields have been discovered offshore the southern coast of Vietnam (i.e associated gas)

Largest gas field is Block 6 (BP operated) which is estimated to contain 2.0 TCF

Gas separation facilites and pipeline to Ho Chi Minh City to be built for gas supply from Bach Ho and Block 6 (i.e. initially to supply gas to the Ba Ria power station)

Potential gas demand and supply will be small scale by regional standards

Demand will be largely driven by supply

Initial gas demand will be for power generation (i.e. critical role as a major user to establish gas infrastrucutre)

Follow on development of industry usage along pipeline

57b VV 8/7/93

102 E 104 E 106 E 108 E 110 E 112 E 114 Eo o o o o o o

LAOS

THAILAND

CAMBODIA

CHINA

HAINAN

VIETNAMHanoi

Danang

Qui Nhon

Ho ChiMinh city

8 N

10 N

12 N

14 N

16 N

18 N

20 N

o

o

o

o

o

o

o

o22 N HONG KONG

VungTau

Dai Hung Field 100 MMBO

Tien Hai Estimated recoverable reserves

30 BCF, 2 MMSCFD

Bach Ho Estimated recoverable reserves 0.5 TCFWas flaring at 100-150 mmscfdBeing piped to shore

Block 6Estimated recoverable reserves

2.0 TCF

Block 15/2250 BCF

Rong250 BCF

Bach Ho Block 6

0

100

200

300

400

500

95 96 97 98 99 2000 1 2 3 4 5 6 7 8 9 10

YEAR

Ga

s R

eq

uir

em

en

ts (

mm

cfd

)

Power Generation Industry Fertiliser

BHP Petroleum

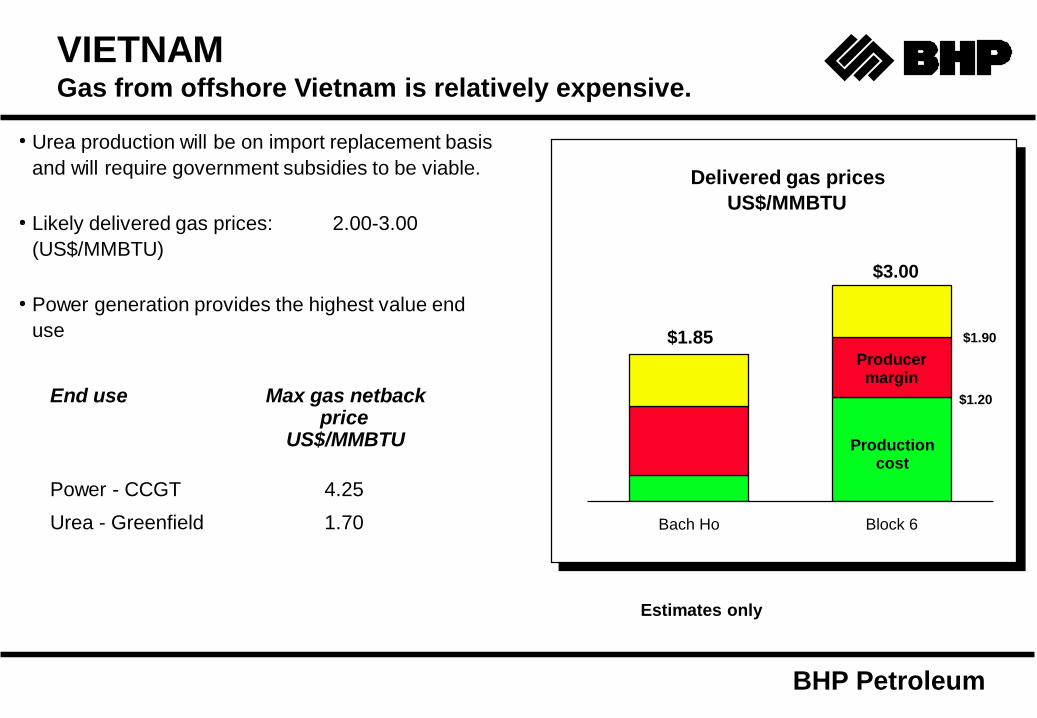

VIETNAMGas from offshore Vietnam is relatively expensive.

Urea production will be on import replacement basis

and will require government subsidies to be viable.

Likely delivered gas prices: 2.00-3.00

(US$/MMBTU)

Power generation provides the highest value end

use

End use Max gas netback price

US$/MMBTU

Power - CCGT 4.25

Urea - Greenfield 1.70

Delivered gas prices

US$/MMBTU

Estimates only

Bach Ho Block 6

$1.85

$3.00

$1.90

$1.20

Producer margin

Production cost

BHP Petroleum

MYAMNARA large proportion of the newly discovered offshore gas has

been allocated for export to Thailand.

Total reserves: 7 TCF.

Gas reserve distribution: 98% offshore 2% onshore.

Declining onshore gas production due to depleting reserves and loss of reservoir pressures.

National oil company lacks the expertise and funds to develop the gas reserves.

Gas potential lies offshore in the Gulf of Martaban where two discoveries (Yadana and Yetagun) have been made. Total reserves 6.9 TCF.

The option of exporting gas to Thailand has been taken in order to earn vital foreign exchange.Alteration of domestic supply constraint dependent upon further exploration success.Only incremental production from the offshore gas fields will be available for domestic use.Power generation to dominate gas demand.Proposed ammonia urea plant in Yangon is dependent upon increasing domestic gas supply.

BANGLADESH

THAILAND

BAY

OF

BENGAL

LAOS

GULF

OF

THAILAND

094 00 00E 098 00 00E

12 00 00N

16 00 00N

20 00 00N

24 00 00N

28 00 00N

090 00 00E 102 00 00E

CHINA

AndamanIsland

Dhaka

Yangon

Bangkok

Yadana

0 200km

Mandalay

INDIA

M Y A N M A R

Yetagun

Ayadaw

ChaukChaukChauk

Pyalo

Prome

Apyauk

Payogon

PIPELINES

Existing

Planned

MYANMAR NATURAL GAS MARKET

(Supply/Demand Balance)

Demand profile based on gas users maximum production capacities:

I. Power generation: As per MEPE power development plan with capacity operated @80% cf

II. Methanol capacity: 450 tonnes/dayIII. Urea capacity: (Existing) 1470 tonnes/day

(New additional Yr 2000) 1750 tonnes/dayIV. Cement capacity: 3000 tonnes/dayV. Allowance for paper mill and general industrial use

Onshore (MOGE) Yadana

0

100

200

300

400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

YEAR

Ga

s R

eq

uir

em

en

ts (

mm

cfd

)

Power Gen Urea Cement Methanol Industrial Paper Mill

Supply shortfall

BHP Petroleum

SummaryIn summary, intense pressure on gas demand in Asia is fuelling substantial

gas price increases and restricting use in low value end uses.

Sources: The outlook for Urea, December 1993 (Fertecon)BHPP Analysis

Iran

315,000 T/a capacity

On-line 1995

Iran

570,000 T/a capacity

On-line 2000

Iraq

570,000 T/a capacity

On-line 2000

Saudi Arabia

570,000 T/a capacity

On-line 2000

Bahrain

570,000 T/a capacity

On-line 1997

Qatar

660,000 T/a capacity

On-line 1997

Bangladesh

560,000 T/a capacity

On-line 1995

Bangladesh

330,000 T/a capacity

On-line 1997

Myanmar

570,000 T/a capacity

On-line 2000

Malaysia

495,000 T/a capacity

On-line 1997

Indonesia

462,000 T/a capacity

On-line 1994

Indonesia

572,000 T/a capacity

On-line 1997* Note: Plant capacities are for total urea output at tonnes/annum

* Urea gas feedstock

prices (likely); US$/GJ

$1.50-$2.00

$1.50 plus$1.80

$0.30-$0.80

$0.50-$0.80

$1.10 - $1.50

Location of proposed urea projects and likely gas feedstock prices

$1.50

BHP Petroleum

Asia dominates world urea demand and is responsible for approximately

50% of total world production. Significant regional supply shortfall is

made up from imports from the Middle East and the former Soviet Union.

Regional Surplus/Deficit(1992)

ASIA & OCEANIA UREA MARKET(Supply/Demand Balance)

Total demand growth (post 93): 4.5% pa.

Demand growth is driven by increasing fertiliser usage rates due to agricultural expansion in developing countries with large populations.

A demand shortfall of at least 8 million tonnes per annum is expected to exist in the region throughout the decade.

China and India dominate demand in the region and represent the largest import market segments in the region.

Local urea production in the region is constrained by the availability of low cost indigenous gas supply.

Urea is the most widely used and tested nitrogen fertiliser, particularly in the developing countries.

Imports are mainly from the former Soviet Union & Middle East

China Production India Production SE Asia Production

West Asia Production East Asia Production Oceania Production

Imports

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

88 89 90 91 92 93 94 95 96 97 98

YEAR

Ure

a V

olu

me

(T

on

ne

s)

Mil

lio

ns

China Demand India Demand SE Asia Demand

West Asia Demand East Asia Demand Oceania Demand

-8.0E+6 -6.0E+6 -4.0E+6 -2.0E+6 000.0E+0 2.0E+6

Indonesia

Malaysia

Bangladesh

New

Zealand

North Korea

Pakistan

Taiwan

Myanmar

Japan

South Korea

Australia

Thailand

Vietnam

Philippines

India

China

BHP Petroleum

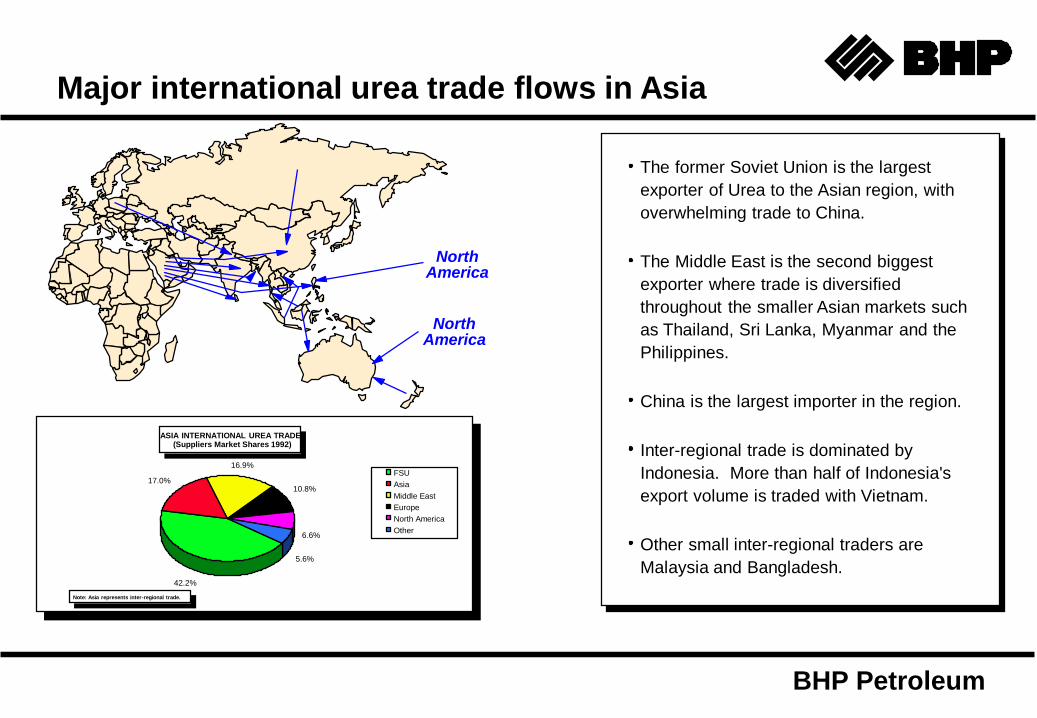

Major international urea trade flows in Asia

The former Soviet Union is the largest

exporter of Urea to the Asian region, with

overwhelming trade to China.

The Middle East is the second biggest

exporter where trade is diversified

throughout the smaller Asian markets such

as Thailand, Sri Lanka, Myanmar and the

Philippines.

China is the largest importer in the region.

Inter-regional trade is dominated by

Indonesia. More than half of Indonesia's

export volume is traded with Vietnam.

Other small inter-regional traders are

Malaysia and Bangladesh.

ASIA INTERNATIONAL UREA TRADE(Suppliers Market Shares 1992)

Note: Asia represents inter-regional trade.

NorthAmerica

NorthAmerica

42.2%

17.0%

16.9%

10.8%

6.6%

5.6%

FSU

Asia

Middle East

Europe

North America

Other

BHP Petroleum

Proposed ammonia/urea export-oriented projects

Source: The outlook for Urea, December 1993 (Fertecon)The outlook for Ammonia, December 1993 (Fertecon)Hydrocarbon processing (June 1995)

Facility Capacity

Country Location Company NH3 Urea Production Possible ureaexport surplus

Middle East Iran Bojnurd KhorosanPetrochemical Co

330,000 T/a 315,000 T/a 1995 200,000 T/a

Bharain Sitah Gulf PetrochemicalIndustries

495,000 T/a 570,000 T/a 1997 570,000 T/a

Qatar Umm Said QAFCO 495,000 T/a 660,000 T/a 1997 660,000 T/a

Iran Queshm Island IFFCO/Kribhco 495,000 T/a 660,000 T/a 2000 660,000 T/a

Iraq Khor Al Zubair SEF 330,000 T/a 570,000 T/a 2000 570,000 T/a

Saudi Arabia Al-Jubail Saudi Binladen Group 330,000 T/a 570,000 T/a 2000 570,000 T/a

West Asia Bangladesh Chittagong Karnafuli Fertiliser Co 495,000 T/a 570,000 T/a 1995 100,000 T/a

Bangladesh Fenchuganj Jalalabad Fertiliser Co 190,000 T/a 330,000 T/a 1997 100,000 T/a

Pakistan Port Quesim Farigi Fertilisers 429,000 T/a 462,000 T/a 1998 200,000 T/a

South-East Asia Indonesia Gresik PT Petrokimia Gresik 445,000 T/a 462,000 T/a 1994 300,000 T/a

Indonesia Bontang PT Pupuk Kalimantan 495,000 T/a 572,000 T/a 1997 250,000 T/a

Malaysia Gunan Kedah Petronas 330,000 T/a 495,000 T/a 1998 495,000 T/a

Myanmar Yangon Myanma PetrochemicalEnterprise

330,000 T/a 570,000 T/a 2000 570,000 T/a

BHP Petroleum

INDONESIAUrea Outlook

120°100°

Government policy of urea self-sufficiency (i.e. agriculture efficiency)

Export advantage to Indochina via small shipments to minor ports

Further capacity additions to be limited by increased gas costs due to:

higher value from domestic use (i) power generation

(ii) industry

(i.e. gas supply to java is critical)

alternative export potential for gas as LNG

TIMOR

BUTON

Alor

Tali AbuJambi

Bandung

Bandar Lampung

JAKARTA

Lhok Seumawe

Medan

Padang

Bengkulu

Palembang

Pontianak

Banjarmasin

Semarang

Yogyakarta

Banda Aceh

Manado

Palu

Kendari

Denpasar

Kupang

Mataram

BRUNEI PHILIPPINES

MALAYSIASINGAPORE

MALAYSIA

THAILAND

Flores

Sumba

Bangka

SOUTH CHINA SEA

INDIAN

OCEAN

CELEBES

SEA

JAVA SEA

FLORES SEA

Simeulue

Nias

Siberut

Togian

Ujungpandang

Sumbawa

Belitung

JAVA

KALIMANTAN

Palangkaraya

SULAWESI

Samarinda

0 km 600

Bali

SUMATRA

Natuna

Lombok

KangeanMaduraSurabaya

1201005

0

5

Proposed projects

INDONESIA UREA MARKET

(Production Profile)

INDONESIA UREA MARKET

(Exports)

Source: Urea Outlook 1994 (Fertecon)

0

2,000,000

4,000,000

6,000,000

8,000,000

88 89 90 91 92 93 94 95 96 97 98 99 2000

YEAR

Ure

a V

olu

me

Mil

lio

ns

0

2,000,000

4,000,000

6,000,000

8,000,000

88 89 90 91 92 93 94 95 96 97 98 99 2000

YEAR

Ure

a V

olu

me

Mil

lio

ns

BHP Petroleum

MALAYSIAUrea Outlook

Government has a industry development priority programme (i.e.

launching of Malaysia into the Vision 2020 Industrialisation Era)

Petronas' greenfield urea plant an integral part of the Peninsular Gas

Utilisation Scheme expansion (Phase III)

Export target market of Thailand

Further urea capacity additions not likely for

higher value alternate gas uses (i.e. power generation)

LNG export potential

Thailand

Cambodia

Malaysia

Vietnam

Indonesia

Phnom PenhVung Tau

Kertih

Kuala Lumpur

Singapore

Sarawak

SabahPeninsular Malaysia

Bintulu

Lotong

Proposed project

MALAYSIA UREA MARKET

(Production)

MALAYSIA UREA MARKET

(Import/Export)

Source: Urea Outlook 1994 (Fertecon)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

88 89 90 91 92 93 94 95 96 97 98 99 2000

YEAR

Ure

a V

olu

me

Mil

lio

ns

Production

0

200,000

400,000

600,000

800,000

1,000,000

88 89 90 91 92 93 94 95 96 97 98 99 2000

YEAR

Ure

a V

olu

me

Mil

lio

ns

Import

Export

BHP Petroleum

INDOCHINAUrea Outlook

Rice economy region

Proposed urea production mainly on import replacement basis

Urea projects require government assistance for viability (i.e. low cost

gas position critical)

Export pipeline gas sales to Thailand would provide higher netbacks

and foreign currency savings to the potential urea producing countries

India

Thailand

Myanmar

Bangladesh

Cambodia

Malaysia

China

Vietnam

Laos

Bangkok

Proposed projects

MYANMAR UREA MARKET

VIETNAM UREA MARKET

THAILAND UREA MARKET

Source: Urea Outlook 1994 (Fertecon)

50

100

150

200

250

300

350

88 89 90 91 92 93 94 95 96 97 98 99 2000

Ure

a V

olu

me

Th

ou

sa

nd

s

Production

Consumption

100

200

300

400

500

600

700

88 89 90 91 92 93 94 95 96 97 98 99 2000

Ure

a V

olu

me

Tho

us

an

ds

Consumption

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

88 89 90 91 92 93 94 95 96 97 98 99 2000

Ure

a V

olu

me

Mil

lio

ns

Production

Consumption

BHP PetroleumOctober 1995

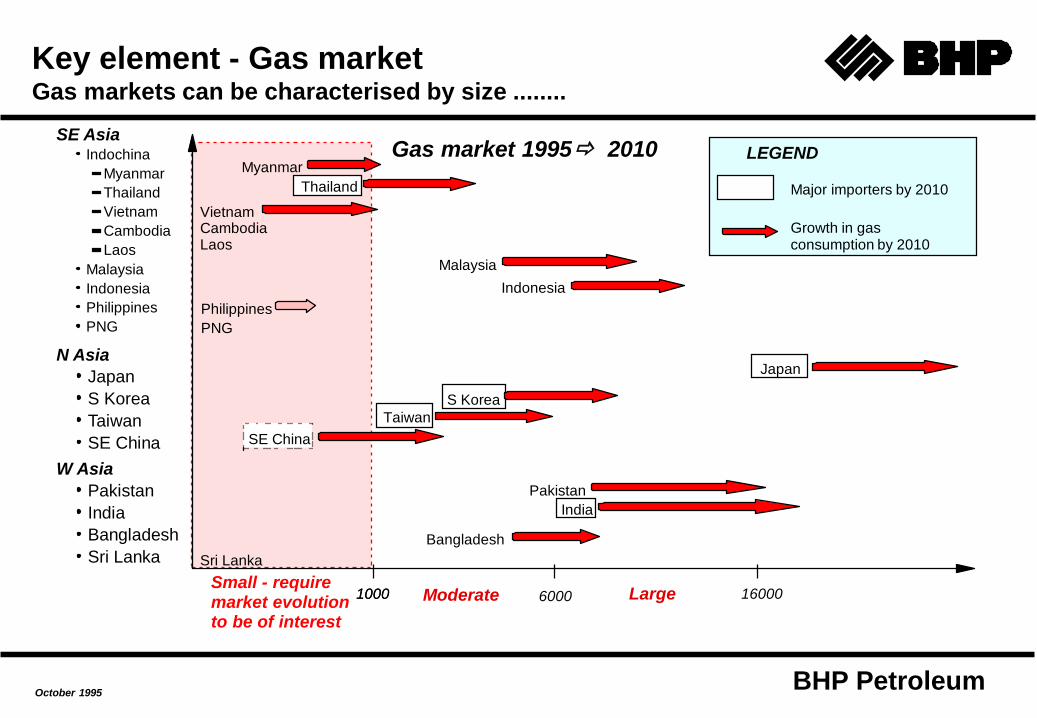

Key element - Gas market Gas markets can be characterised by size ........

SE AsiaIndochina

Myanmar

Thailand

Vietnam

Cambodia

Laos

Malaysia

Indonesia

Philippines

PNG

N Asia

Japan

S Korea

Taiwan

SE China

W Asia

Pakistan

India

Bangladesh

Sri Lanka

Thailand

Philippines

PNG

Indonesia

Japan

Taiwan

SE China

Pakistan

India

Bangladesh

1000

Sri Lanka

6000 160001000

VietnamCambodia Laos

Myanmar

Malaysia

S Korea

Major importers by 2010

Growth in gas consumption by 2010

Small - require market evolution to be of interest

Moderate Large

Gas market 1995 2010 LEGEND

BHP PetroleumOctober 1995

Key element - Gas market Gas markets can be characterised by size ........

SE AsiaIndochina

Myanmar

Thailand

Vietnam

Cambodia

Laos

Malaysia

Indonesia

Philippines

PNG

N Asia

Japan

S Korea

Taiwan

SE China

W Asia

Pakistan

India

Bangladesh

Sri Lanka

Thailand

Philippines

PNG

Indonesia

Japan

Taiwan

SE China

Pakistan

India

Bangladesh

1000

Sri Lanka

6000 160001000

VietnamCambodia Laos

Myanmar

Malaysia

S Korea

Major importers by 2010

Growth in gas consumption by 2010

Small - require market evolution to be of interest

Moderate Large

Gas market 1995 2010 LEGEND

BHP PetroleumOctober 1995

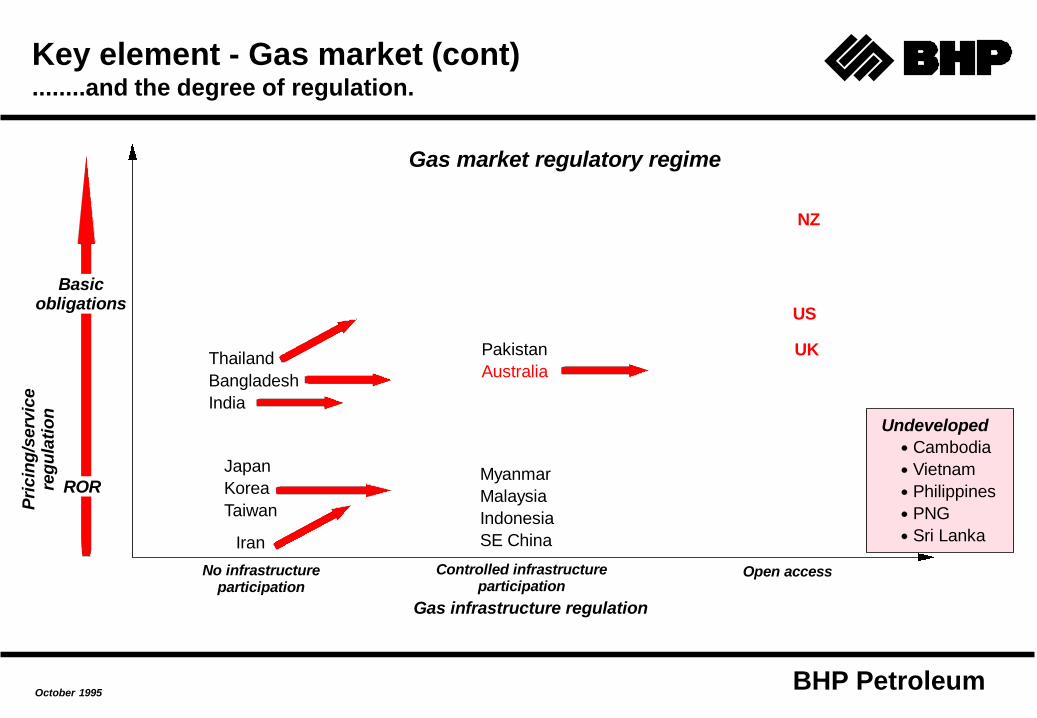

Key element - Gas market (cont)........and the degree of regulation.

Thailand

Bangladesh

India

No infrastructure participation

Controlled infrastructure participation

Open access

Basic obligations

ROR

Pakistan

Australia

Japan

Korea

Taiwan

Myanmar

Malaysia

Indonesia

SE China

NZ

UK

US

Undeveloped

Cambodia

Vietnam

Philippines

PNG

Sri Lanka

Pri

cin

g/s

erv

ice

reg

ula

tio

n

Gas infrastructure regulation

Gas market regulatory regime

Iran

BHP Petroleum

Review - Gas supply business potentialGas supply business potential can be characterised by a country's prospectivity and

fiscal terms. Onerous terms or low prospectivity will preclude BHPP from seeking a

gas supply position in an area.

Myanmar

Vietnam

Thailand

PNG

Pakistan

Bangladesh

SE China

India

Sri Lanka Korea

Philippines

Japan/Taiwan

Malaysia

Indonesia

Iran

Pro

sp

ecti

vit

y

Fiscal terms

High

Low

Onerous Good

cut-off

cu

t-o

ff

Cambodia

BHP Petroleum

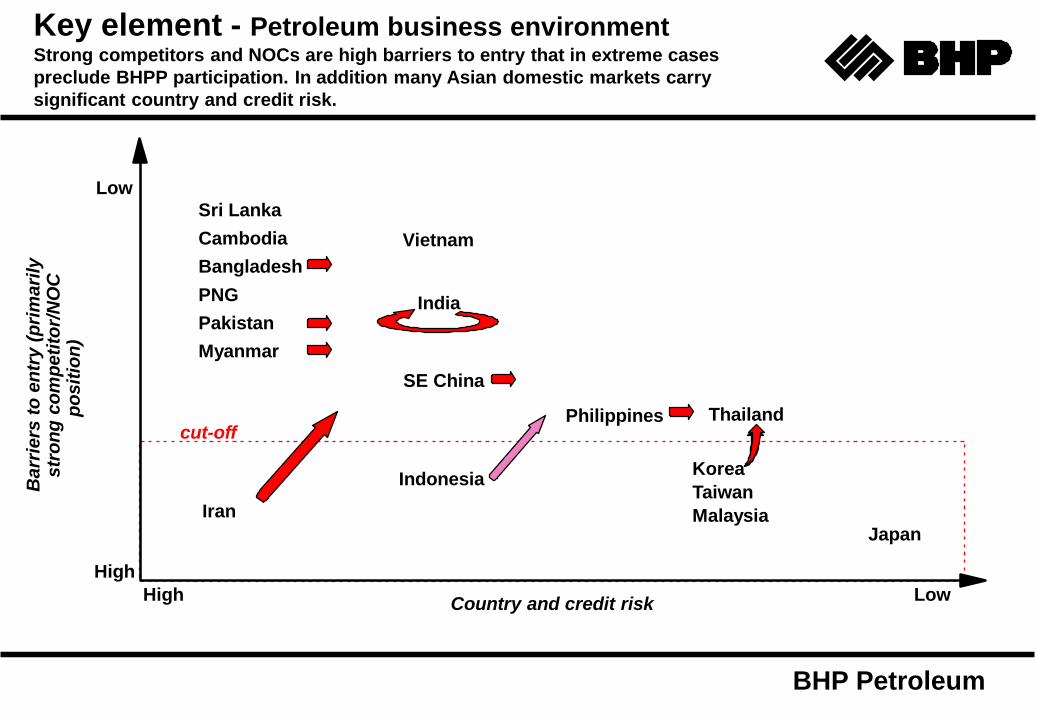

Key element - Petroleum business environmentStrong competitors and NOCs are high barriers to entry that in extreme cases

preclude BHPP participation. In addition many Asian domestic markets carry

significant country and credit risk.

Korea

Taiwan

Malaysia

SE China

Japan

Sri Lanka

Cambodia

Bangladesh

PNG

Pakistan

Myanmar

Vietnam

India

Barr

iers

to

en

try (

pri

mari

ly

str

on

g c

om

peti

tor/

NO

C

po

sit

ion

)

Country and credit risk

Low

High

High Low

cut-off

Indonesia

Philippines Thailand

Iran

BHP Petroleum

Global Gas Production

BHP Petroleum

Global Gas Consumption

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1975

1985

1987

1989

1991

1993

1995

Asia &Australasia

Africa

Middle East

Former SovietUnion

Europe

Sth. & Cen.America

North America

BHP Petroleum

Global Gas Reserves

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1975 1985 1987 1989 1991 1993 1995

Other

Asia &AustralasiaAfrica

Middle East

Former SovietUnionEurope

Sth. & Cen.AmericaNorth America

BHP Petroleum

Asian Gas Reserves

BHP Petroleum

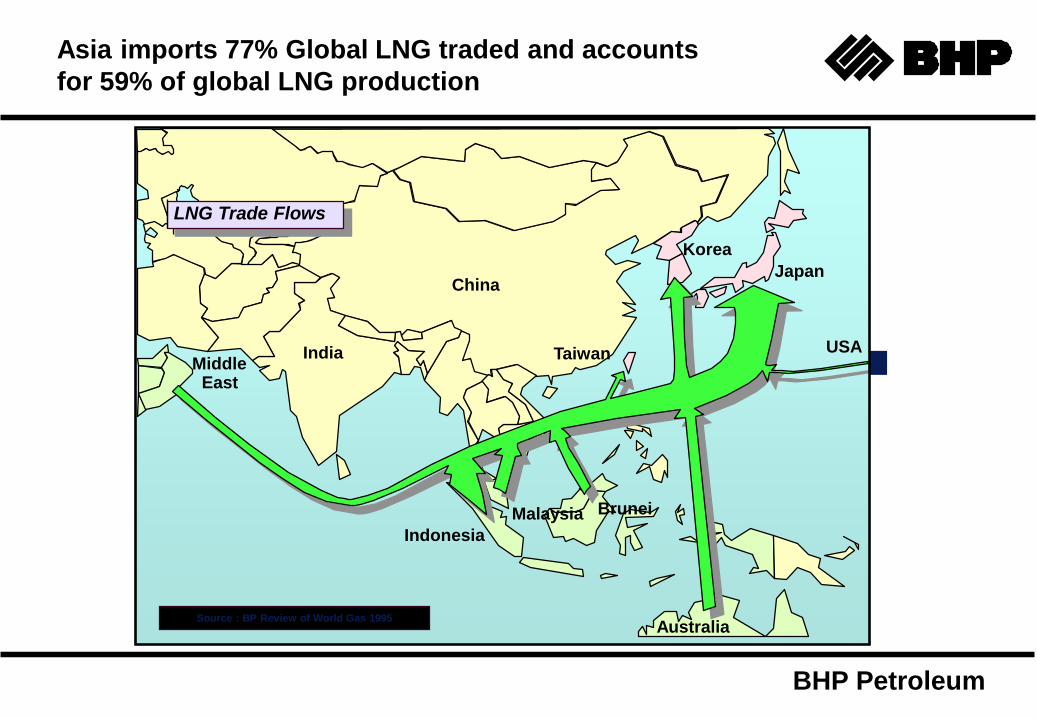

Asia imports 77% Global LNG traded and accounts

for 59% of global LNG production

China

Australia

TaiwanIndia

Japan

Brunei

Middle East

Korea

LNG Trade Flows

Indonesia

Malaysia

USA

Source : BP Review of World Gas 1995

BHP Petroleum

IPP Fuel CostsCurrent pricing favours coal on marginal cost basis

0

1

2

3

4

5

6

7

8

9

Coal Gas

Ge

nera

tio

n c

ost

c/k

Wh

$60/ton

$40/ton

$20/ton

$6/MMBtu

$4/MMBtu

$2/MMBtu

BHP Petroleum

Asian Existing Gas-Fired Power

Generating Capacity by Country

0 10 20 30 40 50

Australia

India

Indonesia

Japan

Malaysia

New Zealand

Pakistan

Singapore

South Korea

Taiwan

Hong Kong

Thailand

MW (Thousands)

Steam Turbine

CC GT

BHP Petroleum

Singapore Gas Demand• Gas demand in the near term will be supply driven

• Malaysia unlikely to supply more gas than its current contract

• Indonesian gas cannot compete with current fuel oil price

• Singapore has ready access to low cost fuel oil supplies

(US$2.40/MMBtu)

• Gas likely to command a slight premium in price - depending,

however, on the country’s commitment to fuel diversity, security

of supply, environmental issues, etc.

• Fuel oil prices have been depressed, and likely to stay that way,

making competition for gas tougher

BHP Petroleum

Malaysia Gas Demand

• Future gas demand in Peninsular Malaysia wil be for power

generation

• Domestic gas demand onshore Peninsular Malaysia can be met

by domestic production until 2010

• Gas supply for PGU Scheme wil double by 2000, mostly

supplied by Exxon

• Gas prices net to suppliers are relatively low due to Petronas’

captive market - unlikely to change in the short/medium term

• Low domestic gas prices make it hard for external sources of

supply to compete

BHP Petroleum

Thailand Gas Demand

• Power sector will be the driving force behind future expansion

of Thailand’s gas market

• Gas will dominate the power generation fuel mix in the near

term, but coal’s position will increase in the medium/longer

term

• A “gas bubble” could emerge in the short/medium term

• In the longer term, as yet uncontracted sources of gas will

compete to supply the Thai gas market

• LNG will not actually be required until around 2010, although

small volumes are likely to be taken from 2005 as a security of

supply measure

BHP Petroleum

Vietnam Gas Demand

• As gas industry is still young, demand is likely to be supply

driven

• Power generation will dominate future gas demand - current

reserve base likely to meet this demand until 2010

• Domestic suppliers still face difficult times in commercialisation

of existing reserves

– Fundamental legislative decisions need to be made

– Gas pricing methodology is still uncertain

– Alternative fuels are subsidised