Embed Size (px)

Citation preview

The effect of the board structureon earnings management:evidence from Portugal

Sandra Maria Geraldes AlvesSchool of Accountancy and Administration, University of Aveiro,

Aveiro, Portugal

Abstract

Purpose – This study aims to extend previous research by examining empirically how boardstructure affects the magnitude of earnings management for companies listed in Portugal. Inparticular, the paper focuses on the main characteristics of the board structure that are highlighted bythe Portuguese Securities Market Supervisory Authority recommendations, i.e. board size, boardcomposition and board’s monitoring committees.

Design/methodology/approach – The OLS regression model is used to examine the effect of theboard structure on earnings management for a sample of 34 non-financial listed Portuguese companiesfor the years 2002 to 2007.

Findings – The results support the predicted non-linear relationship between board size andearnings management. It is also found that discretionary accruals are negatively related to boardcomposition. However, no evidence is found that the existence of an audit committee affects the levelsof earnings management.

Practical implications – The findings based on this study provide useful information forregulators in other countries. The results also provide useful information for investors in evaluatingthe impact of board structure on earnings quality, especially under concentrated ownership.

Originality/value – The major contribution of the current study is that, in contrast to similarstudies, it does not assume that the two views on how board size associates with firms’ earningsmanagement behaviour are mutually exclusive. In addition, this paper is the first empirical study toinvestigate the effect of the board structure on earnings management in Portugal.

Keywords Board structure, Earnings management, Discretionary accruals, Boards of directors,Earnings

Paper type Research paper

1. IntroductionBoards of directors are an important part of the firm’s structure. The board providesthe link between the providers of capital (shareholders) and those who use that capitalto create value (managers). Boards of directors are also responsible for monitoring thequality of the information contained in financial reports. In this vein, Portuguesecompany law establishes that boards of directors have the responsibility to monitor thefirm’s accounting system and financial statements. Board monitoring of the financialreports is important because managers often have self-interested incentives to manageearnings, potentially misleading shareholders.

In fact, the board of directors is an important internal control mechanism designedto monitor the actions of top management. It is considered that, mainly, the boardcomposition, the board size and the structure and composition of the board’smonitoring committees are important characteristics that affect the effectiveness of the

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1985-2517.htm

Board structureand earningsmanagement

141

Journal of Financial Reporting& Accounting

Vol. 9 No. 2, 2011pp. 141-160

q Emerald Group Publishing Limited1985-2517

DOI 10.1108/19852511111173103

board in monitoring management (Fama, 1980; Fama and Jensen, 1983; Jensen, 1993;Klein, 1998). The Portuguese Securities Market Supervisory Authority (Comissao deMercado de Valores Mobiliarios; henceforth “CMVM”, the Portuguese equivalent of theSecurities and Exchange Commission, or SEC) has adopted the recommendations thatboard members must be of a plural nature, that the board of directors should include asufficient number of non-executive directors (in addition, the non-executive membersof the board of directors must include a sufficient number of independent members)and that the board of directors should create internal control committees. Theserecommendations suggest that the Portuguese stock market regulator also concursthat board size, board composition and board’s monitoring committees are effectivecorporate governance techniques (Comissao de Mercado de Valores Mobiliarios, 1999).

Fama (1980) and Fama and Jensen (1983) suggested that boards dominated bynon-executives and independent directors are arguably in a better position to monitorand control managers. Independent directors of management have the ability towithstand pressure from the firm to manipulate earnings and are better able to monitorthe earnings process. Fama and Jensen (1983) posit that the superior monitoring abilityof independent directors can be attributed to their respective incentives to maintaintheir reputations in the external labour market.

Board size is also considered as an important characteristic that affects theeffectiveness of the board in monitoring management ( Jensen, 1993). The higher thenumber of members on the board, the greater the monitoring activity of management(Loderer and Peyer, 2002). However, according to Jensen (1993) large boards result inless effective coordination, communication and decision-making, and are more likely tobe controlled by the manager.

The existing literature also suggests that the structure and composition of theboard’s monitoring committees are a value-relevant attribute of corporate boards(Peasnell et al., 2000, 2006; Xie et al., 2003). In this vein, Klein (1998) finds that thestructure of the accounting and finance committees does impact firm performance.

The board of directors and its structure appear to be an effective corporategovernance mechanism to decrease agency problems, and hence to reduce earningsmanagement. Several research studies have found that board structure has an impacton corporate financial reporting choices, including earnings management (Beasley,1996; Dechow et al., 1996; Pope et al., 1998; Peasnell et al., 2000, 2005, 2006; Chtourouet al., 2001; Benkel et al., 2006; Chen et al., 2006, 2007; Cornett et al., 2008; Kim and Yoon,2008; Banderlipe, 2009; Jaggi et al., 2009). For example, Beasley (1996) found that infirms with more outside directors, the occurrence of financial statement fraud is lesslikely for a sample of US firms. Pope et al. (1998), using UK data, tested an empiricalassociation between board composition and earnings management. They hypothesizedthat boards comprised of more outside members would constrain earningsmanagement activity. They found a significant negative association betweenincome-increasing accruals and the proportion of outside board members. For asample of UK firms, Peasnell et al. (2005) found that the likelihood of managers makingincome-increasing abnormal accruals to avoid reporting losses and earningsreductions is negatively related to the proportion of outsiders on the board. UsingUS data, Dechow et al. (1996) found that board size is larger for firms engaging inearnings management than for those not engaging in earnings management, while Xieet al. (2003) found that a larger board is associated with lower levels of discretionary

JFRA9,2

142

current accruals. Bedard et al. (2004) find that aggressive earnings management isnegatively associated with the financial and governance expertise of audit committeemembers for a sample of US firms.

This study extends previous research by examining empirically how boardstructure affects the magnitude of earnings management for companies listed inPortugal. Specifically, we focus on the main characteristics of the board structure thatare highlighted by the CMVM’s recommendations: board size, board composition andthe board’s monitoring committees. The major contribution of the current study is thatin contrast to similar studies, it does not assume that the two views on how board sizeis associated with firms’ earnings management behaviour are mutually exclusive. Italso contributes to the literature by extending the research into the effects of boardstructure on portfolio firms’ earnings management beyond the US and the UKenvironments (e.g. Beasley, 1996; Dechow et al., 1996; Klein, 2002; Pope et al., 1998;Peasnell et al., 2000, 2005, 2006). Furthermore, this paper represents the first knownstudy examining the association between board structure and accruals management inPortugal, where companies’ boards are commonly organized in a single-tier structure.Portuguese listed firms have a wide variety of board structures and compositions. Inaddition, Portuguese capital markets (Euronext Lisbon) present a unique case in thestudy of the corporate board, because ownership in Portuguese listed firms is highlyconcentrated, in contrast with ownership in US and UK listed firms, which is widelydiffused (Shleifer and Vishny, 1997; Silva et al., 2006). Thus, Portuguese boards operatein a unique jurisdiction where public equity markets are highly concentrated.

Since high ownership concentration is a norm rather than an exception around theworld (La Porta et al., 1999), our study of Portuguese boards should be of generalinterest. In fact, these features can affect the board’s effectiveness in monitoringearnings management activity. In firms with a concentrated owner, there is a realdanger that controlling shareholders may expropriate minority shareholders. In fact,“the majority controlling shareholders may use earnings management to camouflagethe reported earnings and hide expropriation from minority shareholders” ( Jaggi et al.,2009, p. 286).

Finally, our findings can provide useful information for both regulators andshareholders, mainly whether the recommended governance practices related to boardstructures mitigate earnings management and enhance earnings quality, especially infirms with highly concentrated equity ownership.

Using discretionary accruals as a proxy for earnings management, the resultssupport the predicted non-linear relationship between board size and earningsmanagement for a sample of 34 non-financial listed Portuguese firms in the years from2002 to 2007. We also find that discretionary accruals are negatively related to boardcomposition. However, we find no evidence that the existence of an audit committeeaffects the levels of earnings management. Overall, the results suggest that boardstructure can mitigate earnings management.

The remainder of the paper is organized as follows. In section 2, we give a briefoverview of the CMVM recommendations for board structures. A literature review andthe development of testable hypotheses are presented in section 3. Section 4 describesthe variable measurement and research design, while section 5 reports the main resultsand the results of sensitivity analysis. Section 6 summarises and concludes this paper.

Board structureand earningsmanagement

143

1.1 CMVM recommendations for board structuresTo alleviate shareholder/manager and controlling-shareholder/minority-shareholderagency conflicts, several countries have made efforts to create a legal and regulatoryframework in order to ensure that public companies adopt good governanceprocedures.

Portugal has placed an emphasis on corporate governance procedures for a numberof years. The existing legal framework is spanned in numerous provisions of thePortuguese Companies Code, the Portuguese Securities Code and in severalrecommendation documents and regulations issued by the CMVM.

The significant governance initiative may date back to October 1999, when theCMVM issued a set of 17 voluntary corporate governance best practices (CMVMRegulation No. 7) and required Portuguese listed companies to disclose annually theircorporate governance practices, and compare their practices to the 17 best practicesrecommendations on different subjects regarding corporate governance. Theserecommendations, in accordance with CMVM Regulation No. 7, were implemented on acomply-or-explain basis in 2001 (these recommendations have been revised andupdated regularly). They were classified by CMVM Regulation No. 7 into five distinctgroups:

(1) recommendations regarding the disclosure of information;

(2) recommendations regarding voting and shareholder representation;

(3) a set of recommendations on the adoption of certain society rules;

(4) recommendations on the structure and functioning of the board of directors; and

(5) recommendations for institutional investors (Alves and Mendes, 2001).

In relation to the structure and role of the board of directors the CMVM’srecommendations (CMVM Regulation 10/1999 as amended by CMVM Regulation7/2001, CMVM Regulation 11/2003, CMVM Regulation 10/2005 and CMVM Regulation3/2006) incorporate six recommendations. The first recommendation considers thatboard members must be of a plural nature and the board itself must carry out aneffective guidance in the management of the company, their directors and managers. Inaddition, the board of directors should include a sufficient number of non-executivedirectors, whose role is continuously to monitor and assess the management of thecompany by the executive members of the board. The second recommendationestablishes that the non-executive members of the board of directors must include asufficient number of independent members. When there is only one non-executivedirector, he/she must also be independent. The third recommendation determines thatthe board of directors should create internal control committees, with the power toassess the corporate structure and its governance. The fourth recommendationestablishes that the remuneration of members of the board of directors should bestructured in such a way as to permit the interests of board members to be in line withthose of the company, and should be disclosed annually in individual terms.Additionally, a proposal should be submitted to the general meeting with regard to theapproval of plans for the allotment of shares, and/or options to purchase shares orbased on variations in share prices, to members of the board of directors and/oremployees. The fifth recommendation establishes that the members of theremuneration committee or equivalent should be independent as regards the

JFRA9,2

144

members of the board of directors. Finally, the sixth recommendation determines that aproposal should be submitted to the general meeting with regard to the approval ofplans for the allotment of shares, and/or options to purchase shares or based onvariations in share prices, to members of the board of directors and/or employees.

These recommendations suggest that CMVM regulator concurs mainly that boardsize, board composition and board’s monitoring committees are importantcharacteristics that affect the effectiveness of the board in monitoring management.

2. Literature review and testable hypothesesAccording to agency theory, separation of ownership and control leads to a divergenceof interests between managers and shareholders ( Jensen and Meckling, 1976), and thusmonitoring managerial decisions becomes essential for boards of directors to assurethat shareholders’ interests are protected (Fama and Jensen, 1983) and to ensurereliable and complete financial reporting. The role of the board of directors is tomonitor and discipline a firm’s management, thereby ensuring that managers pursuethe interests of shareholders ( Jensen and Meckling, 1976). Thus, the board of directorsplays an important oversight role in controlling the quality and reliability of financialreporting (Beasley, 1996; Dechow et al., 1996; Cohen et al., 2002). Board monitoring ofthe financial reports is important because managers often have self-interestedincentives to manage earnings, potentially misleading shareholders.

Similar to most European countries, Portuguese board structure is characterised bythe existence of a single-tier structure, without a separate supervising board. Theboard of directors of the firm includes the chief executive officer (CEO) and a varyingnumber of other board members that can be either executive or non-executive. Eachexecutive board member oversees different functional areas of the firm (finance,marketing, human resources, strategy, etc.). In the single-tier system, non-executiveboard members have an assigned role of monitoring management, filling the gapbetween uninformed shareholders and fully informed executive managers.

Based on previous research on the association between board structure andearnings management, and taking into account the specificities of the Portuguesecontext, in this section we develop the hypotheses that are tested in the empiricalanalysis. We focus on the main characteristics of the board structure that arehighlighted by the CMVM’s recommendations – i.e. board size, board composition andboard’s monitoring committees.

2.1 Board size and earnings managementAccording to Jensen (1993) board size is related to board effectiveness. In reality, boardsize can affect boards’ functions and, potentially, firm performance. The greater thenumber of members on the board, the greater the monitoring activity of management.Additionally, “a larger board could bring together specialists from various functionalareas and therefore contribute to higher firm value” (Loderer and Peyer, 2002, p. 182). Ifa large board size is a signal of board effectiveness, then the higher the number ofmembers on the board, the lower should be the likelihood of managers to manageearnings. Eisenberg et al. (1998), Ebrahim (2007) and Xie et al. (2003) find that largerboards are associated with lower levels of discretionary accruals.

However, large boards can be controlled more easily by managers, which reduce themonitoring efficiency of the boards. Also, a larger board would introduce problems of

Board structureand earningsmanagement

145

communication and coordination, as well as of decision-making ( Jensen, 1993;Eisenberg et al., 1998; Forbes and Milliken, 1999). Thus, “when boards become too big,agency problems (e.g. director free-riding) increase and the board becomes moresymbolic and neglects its monitoring and control duties” (Beiner et al., 2004, p. 328).Yermack (1996) and Eisenberg et al. (1998) provide evidence that firm performance isnegatively related to board size. This suggests that smaller boards can be moreeffective than larger boards. Consequently, small boards might be more effective inmonitoring managerial behaviour. Corroborating this argument, Kao and Chen (2004),Abdul Rahman and Mohamad Ali (2006) and Jaggi and Leung (2007) find that boardsize is positively related to earnings management.

Taking the above opposing arguments into account, we expect a non-linearrelationship between board size and earnings management. With respect to a board’seffectiveness to monitor the financial reporting process, in a smaller board each boardmember will be more able to take personal responsibility for the board’s monitoring ofthe financial statements, and consequently to monitor earnings management activity.In contrast, as board size increases, it may become difficult after a certain point(optimal size) for boards to monitor managerial behaviour and, consequently, to limitearnings management. In larger boards the responsibility of monitoring managementis diffused, leading to great dilution on each member personally. Therefore, neitherargument by itself is likely to explain satisfactorily the relationship between board sizeand earnings management. Instead, we suggest that both arguments can coexist. Thus,we propose a “U”-shaped relationship between board size and earnings management,with an optimal board size existing midway. Below this optimal or the most efficientsize, there is a negative relationship between board size and earnings managementfollowed by a positive relationship.

So, we test the following hypothesis:

H1. Board size negatively influences the earnings management at smaller sizesfollowed by a positive influence at larger sizes.

2.2 Board composition and earnings managementThe board of directors is an important internal control mechanism designed to monitorthe actions of top management, and possibly the use of accruals to manage earnings.Fama (1980) and Fama and Jensen (1983) suggest that the effectiveness of the board isa function of the composition of the board. They argue that the inclusion ofnon-executive members enhances internal control through the corporate board. In fact,although all board members are supposed to work to increase shareholders’ wealth,agency theory argues that non-executive directors (NEDs), because of theirindependence and specialised expertise, are a particularly powerful monitoringdevice of executive directors’ actions (who are assumed to be opportunistic agents)(Rediker and Seth, 1995). NEDs are potentially effective since “outside directors haveincentives to develop reputations as experts in decision control” (Fama and Jensen,1983, p. 315). The board can be seen as an instrument by which managers control othermanagers. As described by Fama (1980, p. 293), “if there is competition among the topmanagers themselves (all want to be the boss of bosses), then perhaps they are the bestones to control the board of directors”. Research generally supports the view thatNEDs are important for both monitoring management and providing relevantcomplementary knowledge (Booth et al., 2002).

JFRA9,2

146

Board composition appears to be an effective corporate governance mechanism toreduce agency problems and increase earnings quality. Several research studies haveexamined the effect of board composition on constraining opportunistic earningsmanagement activity. The evidence indicates consistently that boards comprised ofmore outside members will constrain earnings management activity (Klein, 2002;Peasnell et al., 2000, 2005, 2006; Benkel et al., 2006; Benkraiem, 2009). For example,Beasley (1996), Dechow et al. (1996) and Uzun et al. (2004) examined US firms identifiedas having been engaged in financial statement fraud. They reported that the proportionof independent directors of the board is inversely related to the likelihood of financialstatement fraud. Klein (2002), using US data, found a significant negative associationbetween the magnitude of abnormal accruals and the percentage of outside directors onthe board. Pope et al. (1998) tested an empirical association between board compositionand earnings management for a sample of UK firms. They hypothesised that boardscomprised of more outside members would constrain earnings management activity.They find a significant negative association between income-increasing accruals andthe proportion of outside board members. Using a sample of UK firms, Peasnell et al.(2000) examine the effect of the Cadbury Committee Report of 1992 on the relationshipbetween board composition and earnings management. While they find no evidence ofassociation between board composition and earnings management during thepre-Cadbury period, they report a significant negative association betweenincome-increasing accruals and the proportion of outside board members in thepost-Cadbury period. Recently, Peasnell et al. (2006) also find that the greater theproportion of outside directors on the board, the smaller is the magnitude of abnormalaccruals.

Portuguese listed firms’ boards are commonly organised in a single-tier structure. Inthis single-tier system, non-executive board members’ prescribed role is to protectshareholders’ interests in key decisions of the firm. As referred previously, CMVM’srecommendations also suggest the inclusion of non-executive directors on the board forthe supervision, control, and evaluation of executive directors. Therefore,non-executive directors are expected to monitor the financial information elaborationprocess by constraining executive’s attempts to earnings management. Thus, we testthe following hypothesis:

H2. The proportion of non-executive directors on the board is negatively related toearnings management.

2.3 Board’s monitoring committee and earnings managementThe CMVM’s regulation recommends the creation of internal control committees withthe power to assess the corporate structure and its governance. Among the specificcommittees (e.g. strategy committee, corporate governance committee, accounting andfinance committee, audit committee and compensation committee) that can be createdwithin boards of directors, the audit committee has been considered as having a veryimportant role within the governance structure. An audit committee plays animportant monitoring role to ensure that the financial information is analysed byexternal auditors that are independent, competent and qualified according to thestrictest international standards, and that the released information reflects the actualsituation of the firm. Therefore, if an audit committee is important to assure the qualityof financial reporting and corporate accountability (Carcello and Neal, 2000), then “an

Board structureand earningsmanagement

147

active, well-functioning, and well-structured audit committee may be able to preventearnings management” (Xie et al., 2003, p. 299). Dechow et al. (1996), Klein (2002), Xieet al. (2003), Bedard et al. (2004), Benkel et al. (2006) and Saleh et al. (2007) foundevidence that an audit committee is associated with a reduced level of discretionaryaccruals.

Based on CMVM’s recommendation and previous research our third hypothesis isthe following:

H3. The existence of an audit committee is negatively related to earningsmanagement.

3. Variable measurement and research design3.1 Measuring board structureAs referred previously, to analyse whether a firm’s board structure provides effectivemonitoring of earnings management, we focus on the main characteristics of the boardstructure that are highlighted by the CMVM’s recommendations: board size, boardcomposition and board’s monitoring committees. Board size (Bsize) is the number ofmembers on the board. Board composition (Bcomp) is calculated by dividing thenumber of non-executive directors by the total number of board members. Auditcommittee (Audit) is measured as an indicator variable, taking the value of 1 when thefirm has an audit committee and 0 otherwise.

3.2 Measuring earnings managementFollowing standard accounting literature, we use discretionary accruals as a proxy forearnings management. Discretionary accruals are estimated using the cross sectionalvariation of the modified Jones model proposed by Dechow et al. (1995), which iscommonly used by most of earnings management research (Warfield et al., 1995;Peasnell et al., 2005; Frankel et al., 2002; Haw et al., 2004; Abdul Rahman and MohamadAli, 2006; Liu and Lu, 2007; Cornett et al., 2008; Kim and Yoon, 2008; Ahn and Choi,2009).

The modified Jones model consists of regressing total accruals (TACC) on threevariables:

(1) the change in revenues (DRev);

(2) the change in receivables (DRec); and

(3) the level of gross property, plant and equipment (PPE).

All variables and the intercept are divided by lagged total assets in order to avoidproblems of heteroscedasticity. Non-discretionary accruals (NDACC) are thepredictions from the ordinary least squares (OLS) estimation of model (1), whilediscretionary accruals (DACC) are the residuals.

The modified Jones model is as follows:

TACCit

TAit21¼ a1

1

TAit21

� �þ a2

DRevit 2 DRecitTAit21

� �þ a3

PPEit

TAit21

� �þ 1it; ð1Þ

where TACC is the total accruals in year t, calculated as the difference between netincome and operating cash flows; TA is the total assets at the beginning of year t; DRev

JFRA9,2

148

is the change in revenues; DRec is the change in accounts receivable; PPE is the grossproperty, plant and equipment; and i and t are firm and year indexes.

3.3 Control variablesGiven that board size, board composition and the existence of an audit committee arenot the sole factors affecting earnings management, several control variables areintroduced to isolate other contracting incentives that may influence managers’accounting choices. Previous studies suggest that stock options (Options), firm size(Size), leverage (Lev) and managerial ownership (Managerial) are associated withearnings management (Banderlipe, 2009; Peasnell et al., 2000; Jiang et al., 2008; DeFondand Jiambalvo, 1994; Klein, 2002; Warfield et al., 1995; Xie et al., 2003). Additionally, asownership of Portuguese listed firms is highly concentrated, we also include theownership concentration (Concentration) variable to control for the potential effect ofownership concentration on earnings management.

3.3.1 Stock options (Options). Stock options potentially motivate managers tomaximize the firm value given that part of his remuneration will be dependent on theevolution of the share prices. However, stock options may induce executives to engagein earnings management. Bergstresser and Philippon (2006), Cornett et al. (2008) andKuang (2008) find evidence that managers are more likely to engage in earningsmanagement when they hold stock options. Bartov and Mohanram (2004) find thattop-level executives use private information about inflated earnings to timeabnormally large stock option exercises. The Stock options variable takes a value of1 if the managers hold stock options and 0 otherwise.

3.3.2 Firm size (Size). Positive accounting theory suggests that managers of largefirms are more likely to exploit latitude in accounting to reduce political costs (Wattsand Zimmerman, 1978). Therefore, large firms are more likely to chooseincome-decreasing earnings management in order to reduce the probability ofadverse impact from political exposure (the size hypothesis). In this vein, Peasnell et al.(2000), Jiang et al. (2008) and Banderlipe (2009) find that larger firms are associatedwith lower absolute discretionary accruals. On the other hand, large firms are likely tobe under closer scrutiny by analysts than small firms. This scrutiny may reducemanagers’ opportunities to exercise their accounting discretion (Koh, 2003). Inaddition, large firms face more pressures than small firms to meet or beat the analysts’expectations (Barton and Simko, 2002). Chung et al. (2002) and Chen et al. (2007) findthat larger firms are associated with higher absolute discretionary accruals. Size iscalculated as the logarithm of market value of equity.

3.3.3 Leverage (Lev). Because higher debt levels increase the risk of violating debtcovenants, managers may be motivated to manipulate earnings to comply with debtcovenants (DeFond and Jiambalvo, 1994; Ali et al., 2008; Jiang et al., 2008). However,monitoring by external lenders reduces the opportunities to manipulate earnings (Parkand Shin, 2004). Chung et al. (2002) and Park and Shin (2004) find a negativerelationship between leverage and earnings management. Lev variable is calculated asthe ratio between the book value of all liabilities and the total assets of the firm.

3.3.4 Managerial ownership (Managerial). The alignment of interest hypothesissuggests that larger levels of ownership by the executive directors on the board maydecrease the likelihood of earnings management as share ownership should createincentive alignment with external shareholders. Warfield et al. (1995), Ali et al. (2008)

Board structureand earningsmanagement

149

and Banderlipe (2009) document a negative association between managerial ownershipand the absolute value of discretionary accruals. Managerial is measured as theproportion of the company’s shares directly or indirectly owned by the manager.

3.3.5 Ownership concentration (Concentration). Large shareholders are expected tomonitor managerial behaviour actions effectively, which reduce the scope ofmanagerial opportunism to engage in earnings management (Dechow et al., 1996). Inthis vein, Ali et al. (2008) find that ownership concentration reduces the managers’discretionary behaviour. However, large shareholders may intervene in the firm’smanagement, and may encourage managers to engage in earnings management tomaximise their private benefits ( Jaggi and Tsui, 2007). Choi et al. (2004) and Kim andYoon (2008) document that earnings management is positively related with ownershipconcentration. The Concentration variable is the proportion of stocks owned byshareholders who own at least 2 per cent of the common stock of the company.Portuguese listed firms need to disclose the ownership levels of shareholdings inexcess of 2 per cent.

3.4 Regression modelThis study predicts a non-linear relationship between board size and earningsmanagement. Following a quadratic function specification, Bsize and Bsize2 (thesquare value of Bsize) are introduced to capture the predicted non-linear relation. Thisstudy uses the following OLS regression model to assess the association between boardstructure and earnings management:

DACCit ¼ b0 þ b1ðBSizeitÞ þ b2ðBsize2itÞ þ b3ðBCompitÞ þ b4ðAudititÞ

þ b5ðOptionsitÞ þ b6ðSizeitÞ þ b7ðLevitÞ þ b8ðManagerialitÞ

þ b9ðConcentrationitÞ þ 1it;

ð2Þ

where Bsizeit is the number of members on the board of firm i for period t; BSize2it is the

square of the number of members on the board of firm i for period t; Bcompit is the ratiobetween the number of non-executive directors and the total number of board membersof firm i for period t; Auditit is a dummy variable taking a value 1 if firm i has an auditcommittee for period t and 0 otherwise; Optionsit is a dummy variable taking a value of1 if the managers of firm i hold stock options for period t, and 0 otherwise; Sizeit is thelogarithm of market value of equity of firm i for period t; Levit is the ratio between thebook value of all liabilities and the total assets of firm i for period t; Managerialit is theproportion of the company’s shares directly or indirectly owned by the manager of firmi for period t; Concentrationit is the proportion of stocks owned by shareholders whoown at least 2 per cent of the common stock of firm i for period t; 1it is a residual term offirm i for period t; b0 is a constant; and b1 to b9 are the coefficients.

3.5 Sample selectionThe initial sample includes all companies whose stocks are listed in the main market inEuronext Lisbon. A total of 52, 50, 48, 51, 51 and 51 companies were listed at the yearend of 2002, 2003, 2004, 2005, 2006 and 2007, respectively (303 firm-year observationsin total). We selected 2002 as the starting period because data on board structure werenot available before then.

JFRA9,2

150

Foreign companies (two in each of the six years, 12 in total) are excluded.Companies not having shares listed in the previous year and companies whose shareswere de-listed in the following year are also excluded (eight, six, four, seven, eight andeight firms in 2002, 2003, 2004, 2005, 2006 and 2007, respectively). Companies withmissing data (one in each of the first four years) are also excluded. As a result, the finalsample size is 34 non-financial companies per year, and thus 204 observations in total.This reduced number of observations may influence some results. Nevertheless, thislimitation is an immediate consequence of the small size of the Portuguese stockmarket.

Information on board size, board composition, audit committee, stock options,leverage, managerial ownership, ownership concentration, total assets, revenues, grossproperty, plant and equipment, receivables and net income were collected from annualreports and corporate governance report. Both annual report and corporate governancereports were available on-line (see www.cmvm.pt). We obtained stock price data fromEuronext Lisbon, which allowed us to measure the variable firm size.

4. Results and discussion4.1 Descriptive statisticsTable I presents the sample descriptive statistics for the explanatory variables used inthis research. Board size (Bsize) is comprised of approximately eight members (with amedian of seven members). Because the minimum number of members on the board isthree but the maximum number of members is 23, large differences exist acrossdifferent firms for this variable. About 36 per cent (with a median of 40 per cent) of themembers of the board are non-executive directors (Bcomp), with a minimum of 0.0 percent and a maximum of 100 per cent, suggesting that there is a large difference acrossdifferent firms for this variable too. Analysis of Table I also shows that about 28 percent of companies have an audit committee (Audit). Therefore, descriptive statistics forthe Bsize, Bcomp and Audit variables suggest that Portuguese listed firms have a widevariety of board structures and compositions.

Mean Median Minimum Maximum

Bsize 8.015 7.000 3.000 23.000Bsize2 79.466 49.000 9.000 529.000Bcomp 0.360 0.400 0.000 1.000Audit 0.280 0.000 0 1Options 0.140 0.000 0 1Size 19.085 18.928 14.590 23.517Lev 3.200 1.841 0.176 19.744Managerial 0.056 0.001 0.000 0.606Concentration 0.685 0.723 0.161 0.978

Note: Bsize, the number of members of the board; Bsize2, square of the number of members on theboard; Bcomp, ratio between the number of non-executive directors and the total number of boardmembers; Audit, dummy variable taking a value 1 if the firm has an audit committee and 0 otherwise;Options, dummy variable taking a value 1 if the managers hold stock options and 0 otherwise; Size, thefirm’s size; Lev, the ratio between the book value of all liabilities and the total assets; Managerial, theequity held by managers; Concentration, the proportion of stocks owned by shareholders who own atleast 2 per cent of the common stock

Table I.Summary of descriptive

statistics

Board structureand earningsmanagement

151

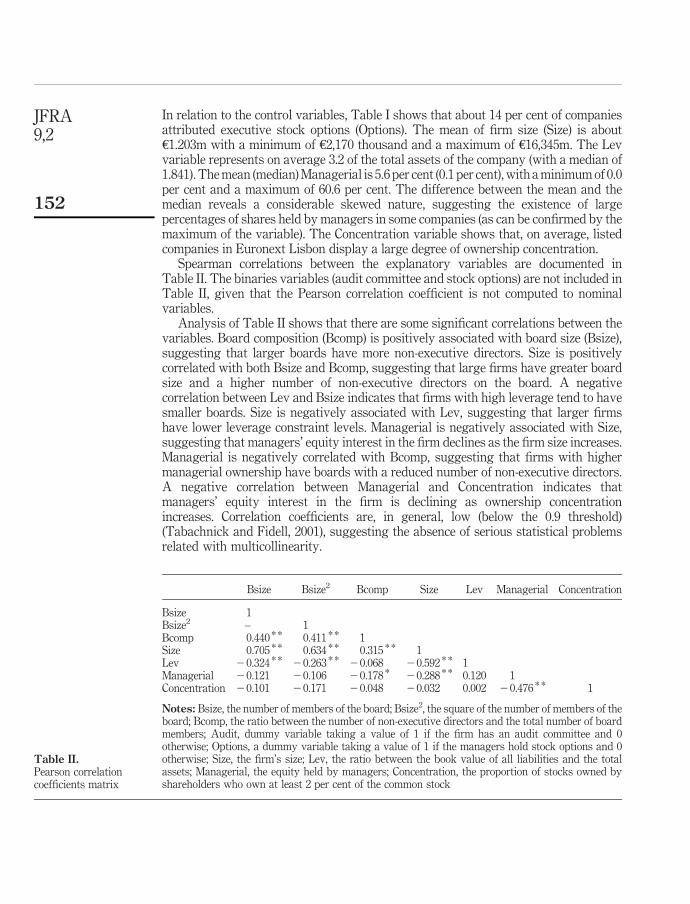

In relation to the control variables, Table I shows that about 14 per cent of companiesattributed executive stock options (Options). The mean of firm size (Size) is aboute1.203m with a minimum of e2,170 thousand and a maximum of e16,345m. The Levvariable represents on average 3.2 of the total assets of the company (with a median of1.841). The mean (median) Managerial is 5.6 per cent (0.1 per cent), with a minimum of 0.0per cent and a maximum of 60.6 per cent. The difference between the mean and themedian reveals a considerable skewed nature, suggesting the existence of largepercentages of shares held by managers in some companies (as can be confirmed by themaximum of the variable). The Concentration variable shows that, on average, listedcompanies in Euronext Lisbon display a large degree of ownership concentration.

Spearman correlations between the explanatory variables are documented inTable II. The binaries variables (audit committee and stock options) are not included inTable II, given that the Pearson correlation coefficient is not computed to nominalvariables.

Analysis of Table II shows that there are some significant correlations between thevariables. Board composition (Bcomp) is positively associated with board size (Bsize),suggesting that larger boards have more non-executive directors. Size is positivelycorrelated with both Bsize and Bcomp, suggesting that large firms have greater boardsize and a higher number of non-executive directors on the board. A negativecorrelation between Lev and Bsize indicates that firms with high leverage tend to havesmaller boards. Size is negatively associated with Lev, suggesting that larger firmshave lower leverage constraint levels. Managerial is negatively associated with Size,suggesting that managers’ equity interest in the firm declines as the firm size increases.Managerial is negatively correlated with Bcomp, suggesting that firms with highermanagerial ownership have boards with a reduced number of non-executive directors.A negative correlation between Managerial and Concentration indicates thatmanagers’ equity interest in the firm is declining as ownership concentrationincreases. Correlation coefficients are, in general, low (below the 0.9 threshold)(Tabachnick and Fidell, 2001), suggesting the absence of serious statistical problemsrelated with multicollinearity.

Bsize Bsize2 Bcomp Size Lev Managerial Concentration

Bsize 1Bsize2 – 1Bcomp 0.440 * * 0.411 * * 1Size 0.705 * * 0.634 * * 0.315 * * 1Lev 20.324 * * 20.263 * * 20.068 20.592 * * 1Managerial 20.121 20.106 20.178 * 20.288 * * 0.120 1Concentration 20.101 20.171 20.048 20.032 0.002 20.476 * * 1

Notes: Bsize, the number of members of the board; Bsize2, the square of the number of members of theboard; Bcomp, the ratio between the number of non-executive directors and the total number of boardmembers; Audit, dummy variable taking a value of 1 if the firm has an audit committee and 0otherwise; Options, a dummy variable taking a value of 1 if the managers hold stock options and 0otherwise; Size, the firm’s size; Lev, the ratio between the book value of all liabilities and the totalassets; Managerial, the equity held by managers; Concentration, the proportion of stocks owned byshareholders who own at least 2 per cent of the common stock

Table II.Pearson correlationcoefficients matrix

JFRA9,2

152

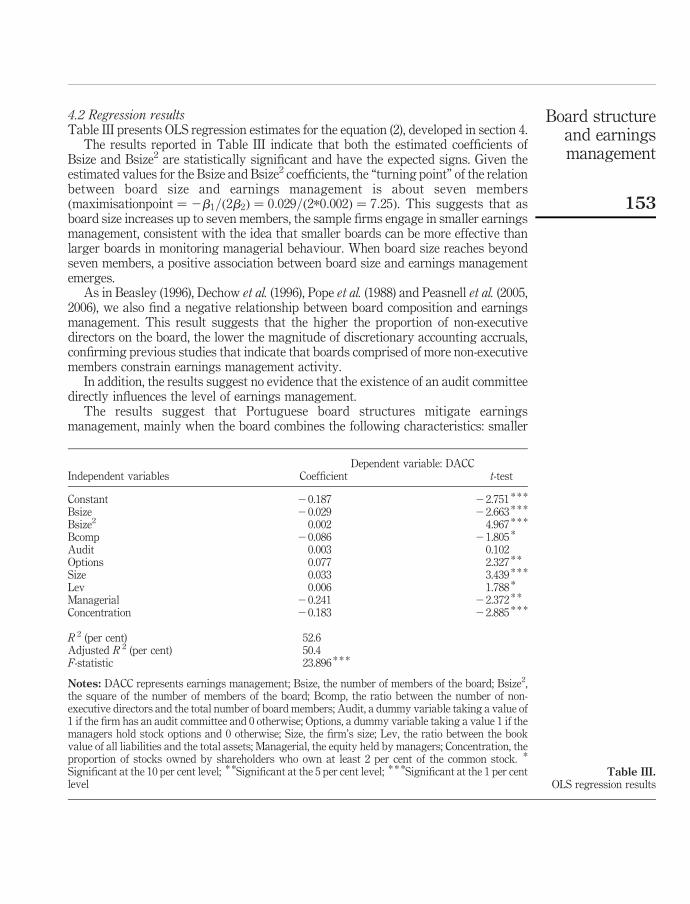

4.2 Regression resultsTable III presents OLS regression estimates for the equation (2), developed in section 4.

The results reported in Table III indicate that both the estimated coefficients ofBsize and Bsize2 are statistically significant and have the expected signs. Given theestimated values for the Bsize and Bsize2 coefficients, the “turning point” of the relationbetween board size and earnings management is about seven membersðmaximisationpoint ¼ 2b1=ð2b2Þ ¼ 0:029=ð2*0:002Þ ¼ 7:25Þ. This suggests that asboard size increases up to seven members, the sample firms engage in smaller earningsmanagement, consistent with the idea that smaller boards can be more effective thanlarger boards in monitoring managerial behaviour. When board size reaches beyondseven members, a positive association between board size and earnings managementemerges.

As in Beasley (1996), Dechow et al. (1996), Pope et al. (1988) and Peasnell et al. (2005,2006), we also find a negative relationship between board composition and earningsmanagement. This result suggests that the higher the proportion of non-executivedirectors on the board, the lower the magnitude of discretionary accounting accruals,confirming previous studies that indicate that boards comprised of more non-executivemembers constrain earnings management activity.

In addition, the results suggest no evidence that the existence of an audit committeedirectly influences the level of earnings management.

The results suggest that Portuguese board structures mitigate earningsmanagement, mainly when the board combines the following characteristics: smaller

Dependent variable: DACCIndependent variables Coefficient t-test

Constant 20.187 22.751 * * *

Bsize 20.029 22.663 * * *

Bsize2 0.002 4.967 * * *

Bcomp 20.086 21.805 *

Audit 0.003 0.102Options 0.077 2.327 * *

Size 0.033 3.439 * * *

Lev 0.006 1.788 *

Managerial 20.241 22.372 * *

Concentration 20.183 22.885 * * *

R 2 (per cent) 52.6Adjusted R 2 (per cent) 50.4F-statistic 23.896 * * *

Notes: DACC represents earnings management; Bsize, the number of members of the board; Bsize2,the square of the number of members of the board; Bcomp, the ratio between the number of non-executive directors and the total number of board members; Audit, a dummy variable taking a value of1 if the firm has an audit committee and 0 otherwise; Options, a dummy variable taking a value 1 if themanagers hold stock options and 0 otherwise; Size, the firm’s size; Lev, the ratio between the bookvalue of all liabilities and the total assets; Managerial, the equity held by managers; Concentration, theproportion of stocks owned by shareholders who own at least 2 per cent of the common stock. *

Significant at the 10 per cent level; * *Significant at the 5 per cent level; * * *Significant at the 1 per centlevel

Table III.OLS regression results

Board structureand earningsmanagement

153

board size and a board composed of mostly non-executive directors. Therefore,Portuguese boards seem to play a significant role in monitoring earnings managementactivities.

The Portuguese business environment is characterised by concentrated ownership.Therefore, the main agency problem is not the manager-shareholder conflict but ratherthe risk of expropriation by the controlling shareholder at the expense of minorityshareholders. Consequently, in firms with concentrated ownership, the boardeffectiveness can be important because it is difficult for the minority shareholders tocoordinate their monitoring earnings management activities. The results suggest thatin firms with concentrated ownership the board structure may be an importantmechanism to reduce the potential expropriation of minority shareholders throughearnings management.

In conclusion, this study observes that adding more non-executive directors and asmaller board in a firm may improve the governance practices and, consequently, thequality of financial reporting, especially in firms with highly concentrated equityownership.

Regarding the other variables, included as control variables, as in Bergstresser andPhilippon (2006), Cornett et al. (2008) and Kuang (2008), we find a positive relationshipbetween Options and earnings management, suggesting that managers engage inearnings management to maximise their compensations. We find that large firmsengage in more earnings management, similar to the findings in Chung et al. (2002) andChen et al. (2007). Lev is significantly positive providing evidence that an increase inleverage encourages managers to use more accruals to manage earnings to avoid debtcovenant violation, confirming the prediction and results of DeFond and Jiambalvo(1994) and Jiang et al. (2008). Consistent with the alignment of interest hypothesis,Managerial is significantly negatively related to earnings management, suggestingthat the higher managerial ownership, the lower the magnitude of discretionaryaccounting accruals, which confirms the findings of Warfield et al. (1995), Klein (2002),Ali et al. (2008) and Banderlipe (2009). Finally, the results also suggest that earningsmanagement is significantly lower for firms with higher ownership concentration.

4.3 Sensitivity analysesTo ensure the robustness of our results, we performed several sensitivity checks. Thefirst sensitivity analysis tests the impact of using alternative definition for the earningsmanagement variable on regression results. Discretionary accruals are determinedusing the Jones model instead of the modified Jones model. The Jones model consists ofregressing total accruals (TACC) on two variables:

(1) the change in revenues (DRev), which models the normal component of workingcapital accruals; and

(2) the level of gross property, plant and equipment (PPE), included to control forthe non-discretionary component of depreciation and amortisation expense, themain component of long-term accruals.

The specific Jones model is as follows:

TACCit

TAit21¼ a1

1

TAit21

� �þ a2

DRevit

TAit21

� �þ a3

PPEit

TAit21

� �þ 1it;

JFRA9,2

154

where TACC is the total accruals in year t, calculated as the difference between netincome and operating cash flows; TA is the total assets at the beginning of year t; dRevis the change in revenues; PPE is gross property, plant and equipment; and i and t arethe firm and year index.

The results (not reported here) of the regression, using an alternative variable tomeasure earnings management has implications for the board composition (Bcomp)variable, its significance level changing from p , 0:10 to p , 0:05. The other resultsremain unchanged (at coefficient signal and significant level).

The next sensitivity analysis examines the effect of influential observations onresults. Where outliers are found (namely in the variables Managerial, Bsize and Lev), aWinsorization method is used to test the robustness of the results. Extreme values(defined as values that are more than three standard deviations away from the mean)are replaced by values that are exactly three standard deviations away from the mean.The results (not reported here) do not differ from results presented previously inTable III. Thus, the influential observations do not affect the results.

We also examine the effects of cash flows from operations on earnings management.The existing literature indicates that cash flows from operations and discretionaryaccruals are negatively correlated (Dechow et al., 1995; Sloan, 1996). The Cash flowsfrom operations variable is introduced to examine the robustness of the results foundin section 5. The Cash flows from operations variable is the ratio between the operatingcash flows and the total assets of firm i for period t 2 1. The unreported results of thesetests are qualitatively the same as those observed in the earlier section. All theestimated coefficients for Bsize, Bsize2, Bcomp and Audit retain their significance leveland have the same signs. The Cash flows from operations variable is significantlynegatively related to earnings management, which suggests that firms with strongoperating cash flows are less likely to use discretionary accruals to engage in earningsmanagement.

Sloan (1996) finds evidence of a concave relation between firm size and totalaccruals. Thus, equation (2) is re-estimated by including an additional variable, Size2,to examine whether the size affects the relationship between board structure andearnings management. Both Size and Size2 are statistically positive. All the results (notreported) are qualitatively the same as the main findings. Thus, the observed impact ofthe board structure on earnings management is unlikely to be a size effect.

Ding et al. (2007) found evidence of a concave relation between ownershipconcentration and earnings management. Accordingly, equation (2) is re-estimated byincluding the squared Concentration (Concentration2), to examine the possibility thatthe relationship between concentration and earnings management may be non-linear.The results (not reported) are qualitatively the same as the main findings. Thecoefficient of Concentration2 variable is not statistically significant, non-supporting aconcave relationship between ownership concentration and earnings management.

The above analyses indicate that the results of this paper are robust aftercontrolling the impact of using alternative definition for the earnings managementvariable, the effect of influential observations, the effect of cash flows from operations,different specification of the relation between Size and earnings management, anddifferent specification of the relation between Concentration and earningsmanagement.

Board structureand earningsmanagement

155

Overall, the several sensitivity analyses conducted largely corroborate the resultspresented in Table III.

5. Summary and conclusionsThe ability of managers to manage reported earnings opportunistically is constrainedby the effectiveness of internal monitoring such as corporate boards. Boards ofdirectors are responsible for monitoring the quality of the information contained infinancial statements, and thus they control the behaviour of managers in order toguarantee that their actions are aligned with the interests of stakeholders.

Therefore, this study investigates whether board structures help constrainmanagement’s opportunistic behaviours. In particular, we focus on the maincharacteristics of the board structure that are highlighted by the Portuguese SecuritiesMarket Supervisory Authority recommendations: board size, board composition andboard’s monitoring committees. Discretionary accruals are used as a proxy for thedegree of earnings management. The data used in the analyses were collected from thePortuguese stock market (Euronext Lisbon) during the period 2002-2007.

The existing literature investigating the associations between board size andearnings management has either implicitly or explicitly assumed that these twocompeting views are mutually exclusive (Eisenberg et al., 1998; Ebrahim, 2007; Kaoand Chen, 2004; Jaggi and Leung, 2007; Abdul Rahman and Mohamad Ali, 2006; Xieet al., 2003). This study departs from that assumption and predicts a non-linearassociation between board size and earnings management.

The results support the predicted non-linear relationship. The predicted negativerelationship between board size and earnings management is observed within thelower region of board size. A positive relationship is found within the higher board sizeregion. We also find that the proportion of non-executive directors on the board isnegatively associated with earnings management. This is consistent with previousstudies, which indicate consistently that boards comprised of more non-executivemembers will constrain earnings management activity. However, results suggest noevidence that the existence of an audit committee directly influences the level ofearnings management.

Moreover, the results also reveal that there is less earnings management when bothmanagerial ownership and ownership concentration are high and that there is moreearnings management when managers hold stock options and when firm size andleverage are high.

The findings of this study make the following contributions. First, the resultsindicate that, on average, both board size and board composition have an impact on thelevels of earnings management in Portuguese listed firms. In particular, this findingsuggests that a smaller board and a board composed of mostly non-executive directorsare positive steps towards improving earnings quality. Second, given the similaritiesbetween Portugal and other countries in Europe (e.g. Denmark, Finland, France,Germany, Italy, Norway and Sweden) in terms of ownership structure (highlyconcentrated), the findings based in this study provide useful information forregulators in these countries. Finally, the findings also provide useful information toinvestors in evaluating the impact of board structure on earnings quality, especiallyunder concentrated ownership.

JFRA9,2

156

References

Abdul Rahman, R. and Mohamad Ali, F.H. (2006), “Board, audit committee, culture and earningsmanagement: Malaysian evidence”, Managerial Auditing Journal, Vol. 21 No. 7,pp. 783-804.

Ahn, S. and Choi, W. (2009), “The role of bank monitoring in corporate governance: evidencefrom borrowers’ earnings management behaviour”, Journal of Banking & Finance, Vol. 33,pp. 425-34.

Ali, S.M., Salleh, N.M. and Hassan, M.S. (2008), “Ownership structure and earnings managementin Malaysian listed companies: the size effect”, Asian Journal of Business and Accounting,Vol. 1 No. 2, pp. 89-116.

Alves, C. and Mendes, V. (2001), “Corporate governance policy and company performance:the case of Portugal”, working paper, University of Porto, Porto.

Banderlipe, M.R.S. (2009), “The impact of selected corporate governance variables in mitigatingearnings management in the Philippines”, DLSU Business & Economics Review, Vol. 19No. 1, pp. 17-27.

Barton, J. and Simko, P. (2002), “The balance sheet as an earnings management constraint”, TheAccounting Review, Vol. 77, Supplement, pp. 1-27.

Bartov, E. and Mohanram, P. (2004), “Private information, earnings manipulations, and executivestock option exercises”, The Accounting Review, Vol. 79 No. 4, pp. 889-920.

Beasley, M. (1996), “An empirical analysis between the board of director composition andfinancial statement fraud”, The Accounting Review, Vol. 71 No. 4, pp. 443-66.

Bedard, J., Chtourou, S.M. and Courteau, L. (2004), “The effect of audit committee expertise,independence, and activity on aggressive earnings management”, Auditing: A Journal ofPractice & Theory, Vol. 23 No. 2, pp. 13-35.

Beiner, S., Drobetz, W., Schmid, F. and Zimmermann, H. (2004), “Is board size an independentcorporate governance mechanism?”, Kyklos, Vol. 57 No. 3, pp. 237-356.

Benkel, M., Mather, P. and Ramsay, A. (2006), “The association between corporate governanceand earnings management: the role of independent directors”, Corporate Ownership& Control, Vol. 3 No. 4, pp. 65-75.

Benkraiem, R. (2009), “Does the presence of independent directors influence accrualsmanagement?”, The Journal of Applied Business Research, Vol. 25 No. 6, pp. 77-86.

Bergstresser, D. and Philippon, T. (2006), “CEO incentives and earnings management”, Journal ofFinancial Economics, Vol. 80, pp. 511-29.

Booth, J.R., Cornett, M.M. and Tehranian, H. (2002), “Boards of directors, ownership, andregulation”, Journal of Banking and Finance, Vol. 26 No. 10, pp. 1973-96.

Carcello, J. and Neal, T. (2000), “Audit committee composition and auditor reporting”, TheAccounting Review, Vol. 75 No. 4, pp. 453-67.

Chen, G., Firth, M., Gao, D. and Rui, O. (2006), “Ownership structure, corporate governance, andfraud: evidence from China”, Journal of Corporate Finance, Vol. 12, pp. 424-48.

Chen, K.Y., Elder, R.J. and Hsieh, Y.-M. (2007), “Corporate governance and earnings management:the implications of corporate governance best-practice principles for Taiwanese listedcompanies”, Journal of Contemporary Accounting & Economics, Vol. 3 No. 2, pp. 73-105.

Choi, J.-H., Jean, K.-A. and Park, J.-I. (2004), “The role of audit committees in decreasing earningsmanagement: Korean evidence”, International Journal of Accounting, Auditing andPerformance Evaluation, Vol. 1 No. 1, pp. 37-60.

Board structureand earningsmanagement

157

Chtourou, S.M., Bedard, J. and Courteau, L. (2001), “Corporate governance and earningsmanagement”, working paper, University of Laval, Laval.

Chung, R., Firth, M. and Kim, J.-B. (2002), “Institutional monitoring and opportunistic earningsmanagement”, Journal of Corporate Finance, Vol. 8, pp. 29-48.

Cohen, J., Krishnamoorthy, G. and Wright, A.M. (2002), “Corporate governance and the auditprocess”, Contemporary Accounting Research, Vol. 19 No. 4, pp. 573-94.

Comissao de Mercado de Valores Mobiliarios (1999), “Recommendations on corporategovernance”, available at: www.cmvm.pt

Cornett, M.M., Marcus, A.J. and Tehraniam, H. (2008), “Corporate governance andpay-for-performance: the impact of earnings management”, Journal of FinancialEconomics, Vol. 87 No. 2, pp. 357-75.

Dechow, P.M., Sloan, R.G. and Sweeney, A.P. (1995), “Detecting earnings management”, TheAccounting Review, Vol. 70 No. 2, pp. 193-225.

Dechow, P.M., Sloan, R.G. and Sweeney, A.P. (1996), “Causes and consequences of earningsmanipulations: an analysis of firms subject to enforcement actions by the SEC”,Contemporary Accounting Research, Vol. 13, pp. 1-36.

DeFond, M.L. and Jiambalvo, J. (1994), “Debt covenant violation and manipulations of accruals”,Journal of Accounting and Economics, Vol. 17, pp. 145-76.

Ding, Y., Zhang, H. and Zhang, J. (2007), “Private vs state ownership and earnings management:evidence from Chinese listed companies”, Corporate Governance, Vol. 15 No. 2, pp. 223-38.

Ebrahim, A. (2007), “Earnings management and board activity: an additional evidence”, Reviewof Accounting and Finance, Vol. 6 No. 1, pp. 42-58.

Eisenberg, T., Sundgren, S. and Wells, M.T. (1998), “Larger board size and decreasing firm valuein small firms”, Journal of Financial Economics, Vol. 48 No. 1, pp. 35-54.

Fama, E.F. (1980), “Agency problems and the theory of the firm”, Journal of Political Economy,Vol. 88 No. 2, pp. 288-307.

Fama, E.F. and Jensen, M.C. (1983), “Separation of ownership and control”, The Journal of Lawand Economics, Vol. 2 No. 26, pp. 301-25.

Forbes, D. and Milliken, F. (1999), “Cognition and corporate governance: understanding boards ofdirectors as strategic decision making groups”, Academy of Management Review, Vol. 24No. 3, pp. 489-505.

Frankel, R.M., Johnson, M.F. and Nelson, K.K. (2002), “The relation between auditors’ fees fornonaudit services and earnings management”, The Accounting Review, Vol. 77,Supplement, pp. 71-105.

Haw, I.M., Hu, B., Hwang, L.S. and Wu, W. (2004), “Ultimate ownership, income management,and legal and extra-legal institutions”, Journal of Accounting Research, Vol. 42 No. 2,pp. 423-62.

Jaggi, B. and Leung, S. (2007), “Impact of family dominance on monitoring of earningsmanagement by audit committees: evidence from Hong Kong”, Journal of InternationalAccounting Auditing & Taxation, Vol. 16 No. 1, pp. 27-50.

Jaggi, B. and Tsui, J. (2007), “Insider trading earnings management and corporate governance:empirical evidence based on Hong Kong firms”, Journal of International FinancialManagement and Accounting, Vol. 18 No. 3, pp. 192-222.

Jaggi, B., Leung, S. and Gul, F. (2009), “Family control, board independence and earningsmanagement: evidence based on Hong Kong firms”, Journal of Accounting and PublicPolicy, Vol. 28, pp. 281-300.

JFRA9,2

158

Jensen, M.C. (1993), “The modern industrial revolution, exit, and the failure of internal controlsystems”, The Journal of Finance, Vol. 3 No. 48, pp. 831-80.

Jensen, M.C. and Meckling, W.H. (1976), “Theory of the firm: managerial behavior, agency andownership structure”, Journal of Financial Economics, Vol. 4 No. 3, pp. 305-60.

Jiang, W., Lee, P. and Anandarajan, A. (2008), “The association between corporate governanceand earnings quality: further evidence using the GOV score”, Advances in Accountingincorporating Advances in International Accounting, Vol. 24, pp. 191-201.

Kao, L. and Chen, A. (2004), “The effects of board characteristics on earnings management”,Corporate Ownership & Control, Vol. 1 No. 3, pp. 96-107.

Klein, A. (1998), “Firm performance and board committee structure”, Journal of Law andEconomics, Vol. 41, pp. 275-303.

Klein, A. (2002), “Audit committee, board of director characteristics, and earnings management”,Journal of Accounting and Economics, Vol. 33 No. 3, pp. 375-400.

Kim, H.J. and Yoon, S.S. (2008), “The impact of corporate governance on earnings management”,Malaysian Accounting Review, Vol. 7 No. 1, pp. 43-59.

Koh, P.-S. (2003), “On the association between institutional ownership and aggressive corporateearnings management in Australia”, The British Accounting Review, Vol. 35, pp. 105-28.

Kuang, Y.F. (2008), “Performance-vested stock options and earnings management”, Journal ofBusiness Finance and Accounting, Vol. 35 Nos 9/10, pp. 1049-78.

La Porta, R., Lopez-de-Silanes, F. and Shleifer, A. (1999), “Corporate ownership around theworld”, Journal of Finance, Vol. 54, pp. 471-517.

Liu, Q. and Lu, Z. (2007), “Corporate governance and earnings management in the Chinese listedcompanies: a tunnelling perspective”, Journal of Corporate Finance, Vol. 13, pp. 881-906.

Loderer, C. and Peyer, U. (2002), “Board overlap, seat accumulation and share prices”, EuropeanFinancial Management, Vol. 8 No. 2, pp. 165-92.

Peasnell, K.V., Pope, P.F. and Young, S. (2000), “Accrual management to meet earnings targets:UK evidence pre- and post-Cadbury”, British Accounting Review, Vol. 32, pp. 415-45.

Peasnell, K.V., Pope, P.F. and Young, S. (2005), “Board monitoring and earnings management: dooutside directors influence abnormal accruals?”, Journal of Business Finance &Accounting,Vol. 32 Nos 7/8, pp. 1311-46.

Peasnell, K., Pope, P. and Young, S. (2006), “Do outside directors limit earnings management?”,Corporate Finance Review, Vol. 10 No. 5, pp. 5-10.

Park, Y.W. and Shin, H.-H. (2004), “Board composition and earnings management in Canada”,Journal of Corporate Finance, Vol. 10, pp. 431-57.

Pope, P.F., Peasnell, K.V. and Young, S. (1998), “Outside directors, board effectiveness, andearnings management”, working paper, Lancaster University, Lancaster.

Rediker, K.J. and Seth, A. (1995), “Boards of directors and substitution effects of alternativegovernance mechanisms”, Strategic Governance Journal, Vol. 16 No. 2, pp. 85-99.

Saleh, N.M., Iskandar, T.M. and Rahmat, M.M. (2007), “Audit committee characteristics andearnings management: evidence from Malaysia”, Asian Review of Accounting, Vol. 15No. 2, pp. 147-63.

Shleifer, A. and Vishny, R.W. (1997), “A survey of corporate governance”, Journal of Finance,Vol. 52 No. 2, pp. 737-83.

Silva, A.S., Vitorino, A., Alves, C.F., Cunha, J.A. and Monteiro, M.A. (2006), Livro Branco sobreCorporate Governance em Portugal (White Book on Corporate Governance in Portugal),Instituto Portugues de Corporate Governance, Lisbon.

Board structureand earningsmanagement

159

Sloan, R.G. (1996), “Do stock prices fully reflect information in accruals and cash flows aboutfuture earnings?”, The Accounting Review, Vol. 71 No. 3, pp. 289-315.

Tabachnick, B.G. and Fidell, L.S. (2001), Using Multivariate Statistics, Allyn and Bacon,New York, NY.

Uzun, H., Szewezyk, S.H. and Varma, R. (2004), “Board composition and corporate fraud”,Financial Analysts Journal, Vol. 60 No. 3, pp. 33-43.

Warfield, T.D., Wild, J.J. and Wild, K.L. (1995), “Managerial ownership accounting choices, andinformativeness of earnings”, Journal of Accounting and Economics, Vol. 20, pp. 61-91.

Watts, R.L. and Zimmerman, J. (1978), “Towards a positive theory of the determination ofaccounting standards”, The Accounting Review, Vol. 53 No. 1, pp. 112-34.

Xie, B., Davidson, W.N. and DaDalt, P.J. (2003), “Earnings management and corporategovernance: the role of the board and the audit committee”, Journal of Corporate Finance,Vol. 9, pp. 295-316.

Yermack, D. (1996), “Higher market valuation of companies with a small board of directors”,Journal of Financial Economics, Vol. 40 No. 2, pp. 185-211.

Corresponding authorSandra Maria Geraldes Alves can be contacted at: [email protected]

JFRA9,2

160

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints