Embed Size (px)

Citation preview

The Economy and External Environment

10th Annual Georgia Idea Institute

August 19, 2015Bill Hampel, Chief Policy Officer

Credit Union National Association

Starting questions:

• Equity markets• Exempt employee changes• Rates• Oil industry impact• NIM• China devaluation• Bubbles?• Euro• Puetro Rico

Economic Summary

• Beginning the seventh year of recovery.• First quarter slowdowns “normal”?• Job market improving, but still significant

slack.• Inflation outlook moderate. • Economy now in a sustained recovery:

escape velocity.• External risks not life threatening.

Gross Domestic Product Quarterly Changes at Annual Rates, Real

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

-10

-8

-6

-4

-2

0

2

4

6

8

10

Great RecessionOf 2008 - 2009

2.4% since 2009 III

2001 Recession

Gross Domestic Product Quarterly Changes at Annual Rates, Real

REVISED JULY 30

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

-10

-8

-6

-4

-2

0

2

4

6

8

10

Great RecessionOf 2008 - 2009

2001 Recession

2.2% since 2009 III

Household Finances• Recovered:

– Debt payments low– Stock market recovered– Home prices rising

• But still room for further improvement:– Debt outstanding still relatively high– Home prices still off peak

• Improved ability to spend, willingness finally catching up?

• Demand backlogs

Household Debt OutstandingTo Annual Disposable Income

1959196219651968197219751978198119851988199119941998200120042007201120140%

20%

40%

60%

80%

100%

120%

140%

Mortgage

123%

Consumer

96%

Latest: 2015 QI

Household Debt Service RatioMonthly Payments to Disposable Income

1980 1982 1984 1986 1989 1991 1993 1995 1998 2000 2002 2004 2007 2009 2011 20130

2

4

6

8

10

12

14

Mortgage

Consumer

Percent

Latest: 2015 QI

US Home PricesCase-Schiller National Index, Jan 2000 = 100

1975197719801983198619891992199419972000200320062009201120140

20

40

60

80

100

120

140

160

180

200

US Home vs.Stock PricesCase-Schiller National Index, S&P 500

197519781981198419871990199319961999200220052008201120140

20

40

60

80

100

120

140

160

180

200

-200

300

800

1300

1800

2300

Case Schiller S&P 500

Household Net Worth

2006

2006

2007

2007

2008

2008

2009

2009

2010

2010

2011

2011

2012

2012

2013

2013

2014

2014

2015

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

Annual Light Vehicle SalesMillions

Annual Light Vehicle SalesMillions

Annual Light Vehicle SalesMillions

Annual Light Vehicle SalesMillions

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2014

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Annual Light Vehicle SalesMillions

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Non-Farm PayrollsMonthly Changes SA, to June 2015

06 07 08 09 10 11 12 13 14 15-1000

-800

-600

-400

-200

0

200

400

600

8.7 million jobs lost

12.1 million jobs gainedNet Gain: 3.4 million

Job Loss and Recovery: Four Recessions Since 1980

Scaled to 2008 Employment of 138 million

Great Recession

Job Losses in Recession

8.7 million

Job Gains First Five Years

12.1 million

Net Change Five Yrs into Recovery

PLUS3.4 million

Job Loss and Recovery: Four Recessions Since 1980

Scaled to 2008 Employment of 138 million

Great Recession

Average of Three Previous Recessions

Job Losses in Recession

8.7 million 3.0 million

Job Gains First Five Years

12.1 million 14.0 million

Net Change Five Yrs into Recovery

PLUS3.4 million

PLUS11 million

Job Loss and Recovery: Four Recessions Since 1980

Scaled to 2008 Employment of 138 million

Great Recession

Average of Three Previous Recessions Difference

Job Losses in Recession

8.7 million 3.0 million 5.7 million

Job Gains First Five Years

12.1 million 14.0 million -1.9 million

Net Change Five Yrs into Recovery

PLUS3.4 million

PLUS11 million

BEHIND7.6 million

Unemployment Rates and RecessionsPercent of the Labor Force

80 85 90 95 00 05 10 1502468

101214161820

Recessions Top Line Rate U6 Rate

Broadest Measure 10.4%Down from 17.4%, Oct 2009

Narrow Measure 5.3%Down from 10.1%

Consumer Confidence? Conference Board

05 06 07 08 09 10 11 12 13 14 150

20

40

60

80

100

120

Consumer Price Inflation1970 to Present, Annual Rates

70 73 76 79 82 85 88 91 94 97 00 03 06 09 12 15 16F

-2

0

2

4

6

8

10

12

14

16

12 Months to June

Top Line = 0.2%Core = 1.8%

Interest Rate Outlook

Interest Rates1988 to Present

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 150

2

4

6

8

10

12

Fed Funds10-yr Treas

Waiting on the Fed• The Fed has lost its patience.• But we exist in international financial

markets.• Fed Funds Rate Move:

– September, October?– Speed and frequency

• Longer-term rates.• Liquidity vs. NEV or Net Interest Income

Interest Rates1988 to Present

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 150

1

2

3

4

5

6

7

8

9

10

10-yr Treas

Treasury Yield Curves

3 mth 1 Yr 3 Yrs 5 Yrs 7 Yrs 9 Yrs 10 Yrs0.00

0.50

1.00

1.50

2.00

2.50

3.00

April 2013 April 2014 July 2015

Treasury Yield Curves

3 mth 1 Yr 3 Yrs 5 Yrs 7 Yrs 9 Yrs 10 Yrs0

1

2

3

4

5

6

July 2015 Dec 2016 ? June 2017 ?

Credit Union Outlook Through 2015

• Weak savings and asset growth– Low interest rates– Consumer spending growth

• Strengthening loan growth– Household de-leveraging slowing– Improving confidence, building backlogs

• Loan delinquencies and losses about back to normal

• Mixed outlook for net income– See below

• Rising net worth ratios

Credit Union Loan GrowthAnnual Percent Change

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16F

-10

-5

0

5

10

15

20

25

30

U.S. GA

Credit Union DelinquencyDollars Delinquent as Percent of Total Portfolio

84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16F

0

0.5

1

1.5

2

2.5

Net Loan Charge-0ffsTotal Portfolio

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15F

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Credit Union Savings GrowthAnnualized Percent Change

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16F

-5

0

5

10

15

20

25

Credit Union Net IncomeTo Average Assets

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16F

-20

0

20

40

60

80

100

120

140

160

Net Capital to Assets

83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 15F

0

2

4

6

8

10

12

14

16

U.S. New Jersey PCA Well Cap'd PCA Adequate

What’s Driving Earnings?POSITIVES:• Lower provision expenses• Finished stabilization assessments

NEGATIVE, for a while longer:• Net Interest Income

EVAPORATING• Mortgage refinance revenue

AT LONG-TERM RISK• Debit interchange revenue• Overdraft revenue

39

What’s Driving Earnings?POSITIVES:• Lower provision expenses• Finished stabilization assessments

NEGATIVE, for a while longer:• Net Interest Income

EVAPORATING• Mortgage refinance revenue

AT LONG-TERM RISK• Debit interchange revenue• Overdraft revenue

Corporate Stabilization AssessmentsBasis Points of Insured Shares

Corporate Stabilization AssessmentsBasis Points of Insured Shares

?

What’s Driving Earnings?POSITIVES:• Lower provision expenses• Finished stabilization assessments

NEGATIVE, for a while longer:• Net Interest Income

EVAPORATING• Mortgage refinance revenue

AT LONG-TERM RISK• Debit interchange revenue• Overdraft revenue

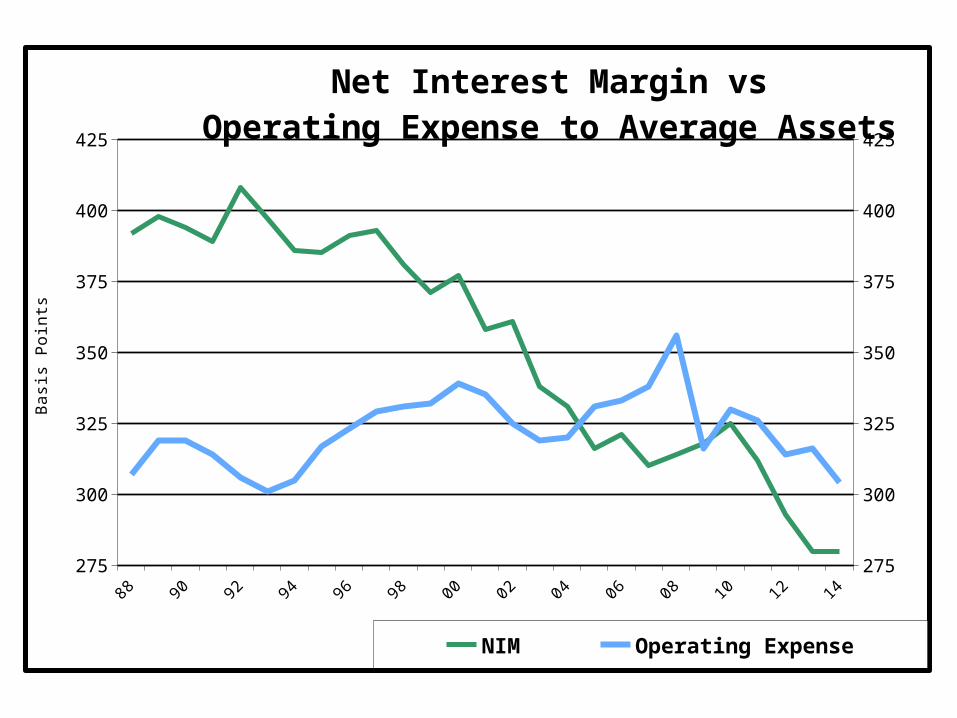

275

300

325

350

375

400

425

275

300

325

350

375

400

425

Net Interest Margin vsOperating Expense to Average Assets

NIM Operating Expense

Bas

is P

oint

s

Credit Union Net Interest Income

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

I0

50

100

150

200

250

300

350

400

450

284

What’s Driving Earnings?POSITIVES:• Lower provision expenses• Finished stabilization assessments

NEGATIVE, for a while longer:• Net Interest Income

EVAPORATING• Mortgage refinance revenue

AT LONG-TERM RISK• Debit interchange revenue• Overdraft revenue

Mortgage Refinancing

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 150

1

2

3

4

5

6

7

8

9

10

10-yr Treas

What’s Driving Earnings?POSITIVES:• Lower provision expenses• Finished stabilization assessments

NEGATIVE, for a while longer:• Net Interest Income

EVAPORATING• Mortgage refinance revenue

AT LONG-TERM RISK• Debit interchange revenue• Overdraft revenue

Performance Varies by Size

LT $50 $50 - $200 $200 - $500 $500 - $1B GR $1 B

-20

0

20

40

60

80

100

120

19

47

64

81

99

-1

38

1319

2014 ROA Mbr Growth Since 2011

49