Embed Size (px)

Citation preview

The economics of gas and coal-fired

plants – signs of market failure?

Graham Weale - Chief Economist, RWE AG

Markus Roth - RWE Generation SE

IEA Electricity Supply Security Conference 1st October 2013

Forward Looking Statement

Projections of revenues, income, earnings per share, capital expenditures, dividends, capital structure or other financial items,

Statements of plans or objectives for future operations or of future competitive position,

Expectations of future economic performance; and

Statements of assumptions underlying several of the foregoing types of statements are forward-looking statements.

Also words such as “anticipate”, “believe”, “estimate”, “intend”, “may”, “will”, “expect”, “plan”, “project” “should” and similar expressions are

intended to identify forward-looking statements.

The forward-looking statements reflect the judgment of RWE's management based on factors currently known to it. No assurances can be

given that these forward-looking statements will prove accurate and correct, or that anticipated, projected future results will be achieved. All

forward-looking statements are subject to various risks and uncertainties that could cause actual results to differ materially from expectations.

Such risks and uncertainties include, but are not limited to, changes in general economic and social environment, business, political and legal

conditions, fluctuating currency exchange rates and interest rates, price and sales risks associated with a market environment in the throes of

deregulation and subject to intense competition, changes in the price and availability of raw materials, risks associated with energy trading

(e.g. risks of loss in the case of unexpected, extreme market price fluctuations and credit risks resulting in the event that trading partners do not

meet their contractual obligations), actions by competitors, application of new or changed accounting standards or other government agency

regulations, changes in, or the failure to comply with, laws or regulations, particularly those affecting the environment and water quality (e.g.

introduction of a price regulation system for the use of power grid, creating a regulation agency for electricity and gas or introduction of trading

in greenhouse gas emissions), changing governmental policies and regulatory actions with respect to the acquisition, disposal, depreciation

and amortisation of assets and facilities, operation and construction of plant facilities, production disruption or interruption due to accidents or

other unforeseen events, delays in the construction of facilities, the inability to obtain or to obtain on acceptable terms necessary regulatory

approvals regarding future transactions, the inability to integrate successfully new companies within the RWE Group to realise synergies from

such integration and finally potential liability for remedial actions under existing or future environmental regulations and potential liability

resulting from pending or future litigation. Any forward-looking statement speaks only as of the date on which it is made. RWE neither intends

to nor assumes any obligationto update these forward-looking statements. For additional information regarding risks, investors are referred to

RWE’s latest annual report and to other most recent reports filed with Frankfurt Stock Exchange and to all additional information published on

RWE’s Internet Web site.

This presentation contains certain forward-looking statements within the meaning of the US federal securities laws.

Especially all of the following statements

Page 2 RWE AG – CEA : Weale IEA Conference 01.10.2013

Page 3 RWE AG – CEA : Weale IEA Conference 01.10.2013

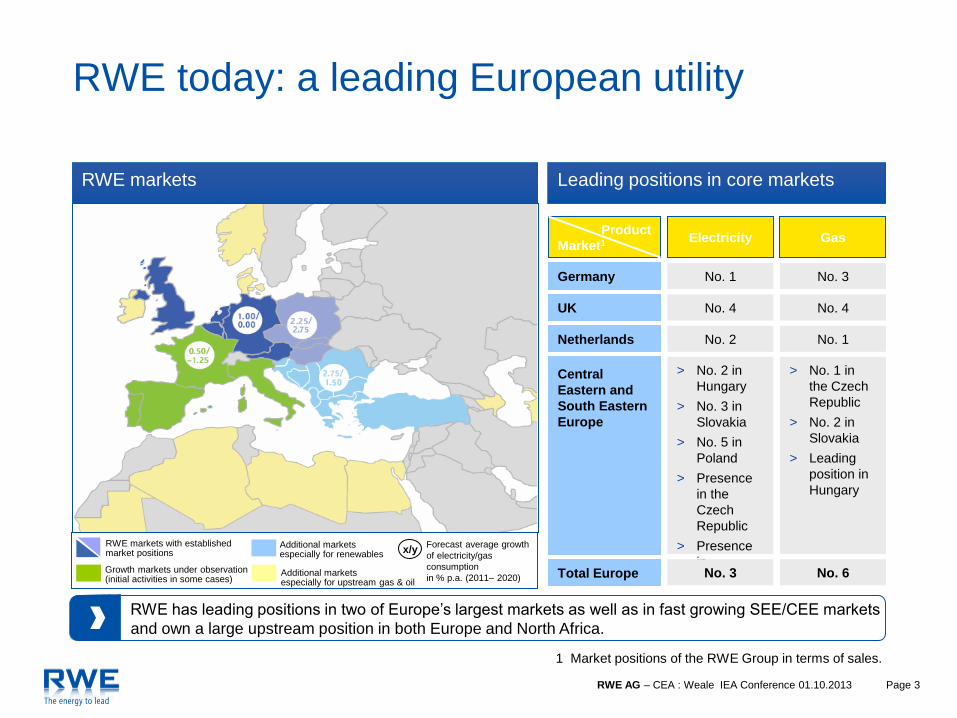

RWE today: a leading European utility

1 Market positions of the RWE Group in terms of sales.

RWE markets Leading positions in core markets

RWE has leading positions in two of Europe’s largest markets as well as in fast growing SEE/CEE markets

and own a large upstream position in both Europe and North Africa.

Gas Electricity Market1

Product

Germany No. 1 No. 3

UK No. 4 No. 4

> No. 2 in

Hungary

> No. 3 in

Slovakia

> No. 5 in

Poland

> Presence

in the

Czech

Republic

> Presence

in

Turkey

> No. 1 in

the Czech

Republic

> No. 2 in

Slovakia

> Leading

position in

Hungary

Central

Eastern and

South Eastern

Europe

Total Europe No. 3 No. 6

Netherlands No. 2 No. 1

x/y RWE markets with established market positions

Growth markets under observation (initial activities in some cases)

Additional markets especially for renewables

Additional markets especially for upstream gas & oil

Forecast average growth

of electricity/gas

consumption

in % p.a. (2011– 2020)

Page 4 RWE AG – CEA : Weale IEA Conference 01.10.2013

Agenda

1. Definition and determinants of „economics“ and key input

parameters

2. Power prices set through merit-order curve

3. Performance of plants and cost recovery

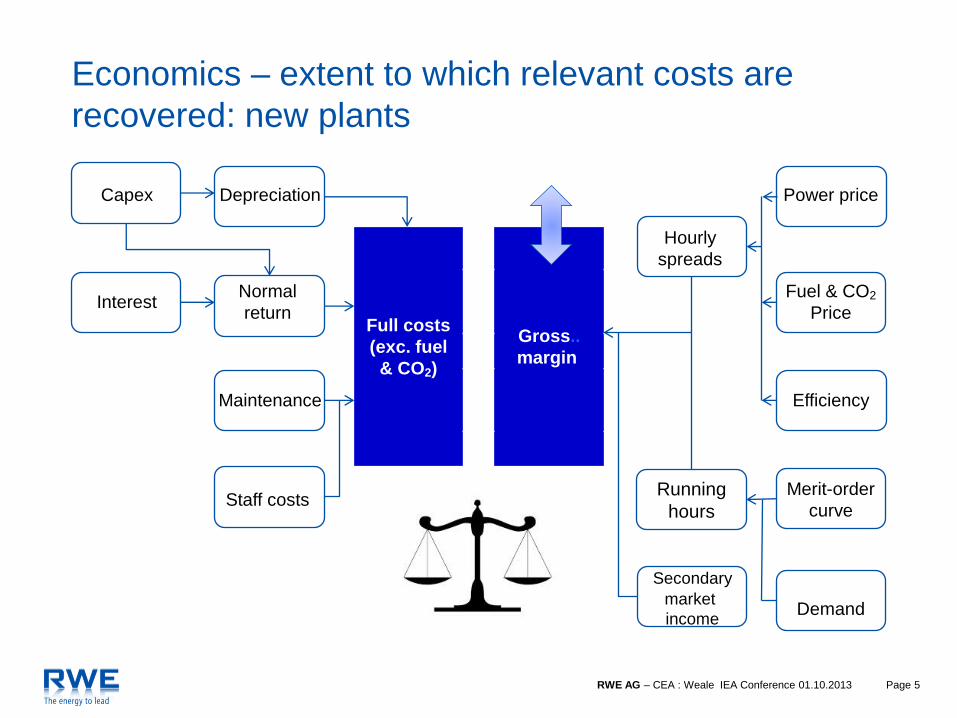

Page 5 RWE AG – CEA : Weale IEA Conference 01.10.2013

Capex Depreciation Power price

Full costs

(exc. fuel

& CO2)

Gross..

margin

Hourly

spreads

Interest Normal

return

Fuel & CO2

Price

Maintenance Efficiency

Staff costs Merit-order

curve

Secondary

market

income

Demand

Economics – extent to which relevant costs are

recovered: new plants

Running

hours

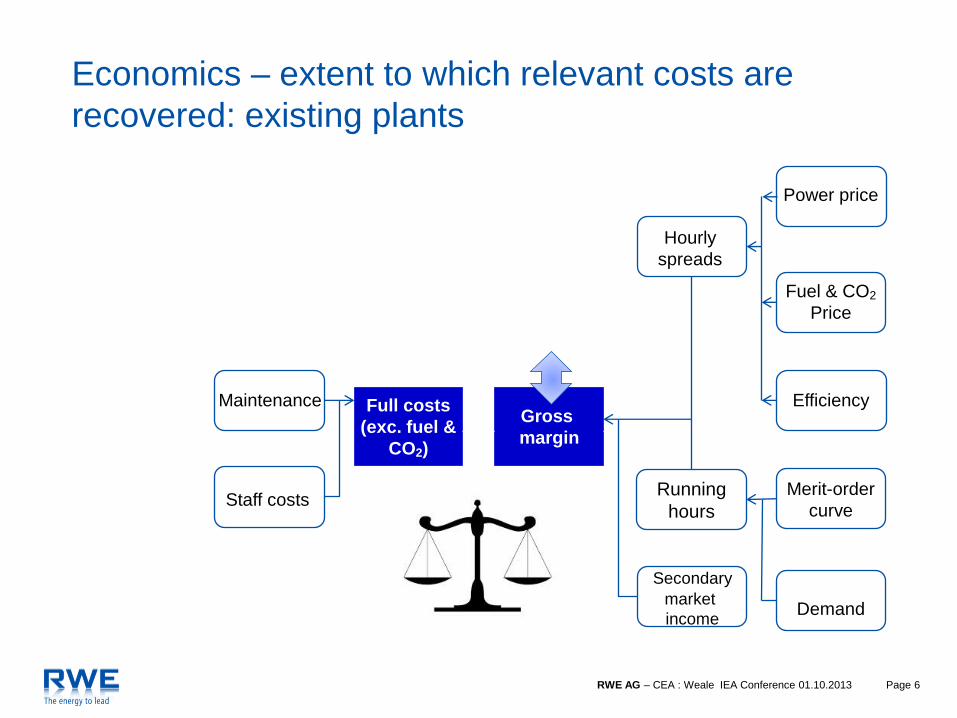

Page 6 RWE AG – CEA : Weale IEA Conference 01.10.2013

Depreciation Power price

Full costs

(exc. fuel &

CO2)

Hourly

spreads

Interest Normal

return

Fuel & CO2

Price

Maintenance Efficiency Full costs

(exc. fuel &

CO2)

Gross.

margin

Staff costs Merit-order

curve

Secondary

market

income

Demand

Economics – extent to which relevant costs are

recovered: existing plants

Running

hours

Page 7 RWE AG – CEA : Weale IEA Conference 01.10.2013

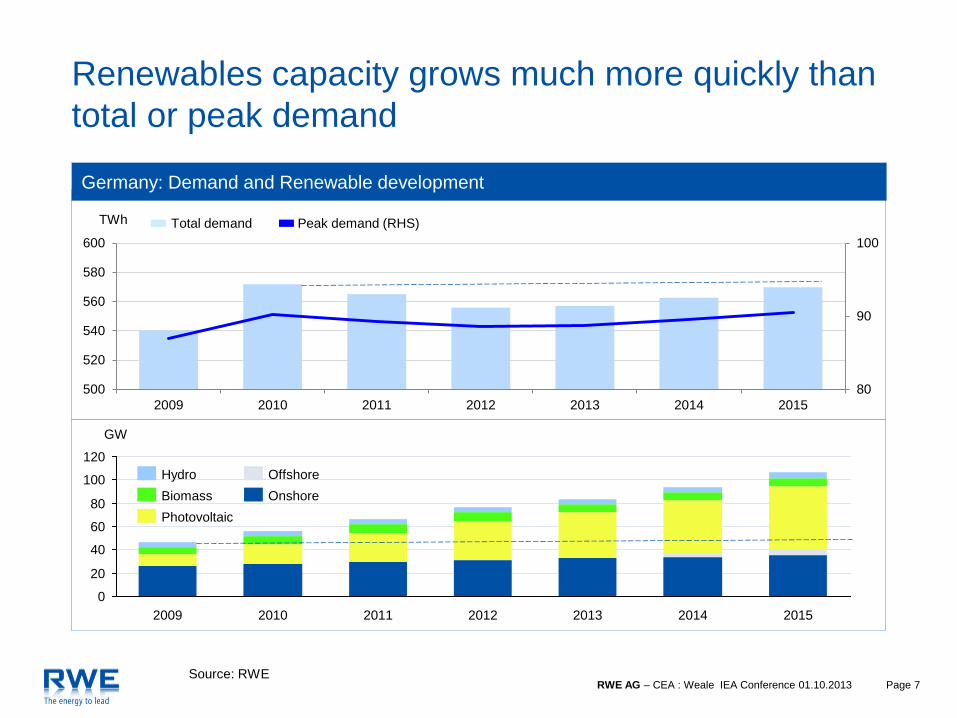

Renewables capacity grows much more quickly than

total or peak demand

80

90

100

500

520

540

560

580

600

2009 2010 2011 2012 2013 2014 2015

Total demand Peak demand (RHS)

GW Germany: Demand and Renewable development

TWh

2010 2011 2012 2013 2014 2015 2009

120

100

80

60

40

20

0

GW

Hydro

Biomass

Photovoltaic

Offshore

Onshore

Source: RWE

Page 8 RWE AG – CEA : Weale IEA Conference 01.10.2013

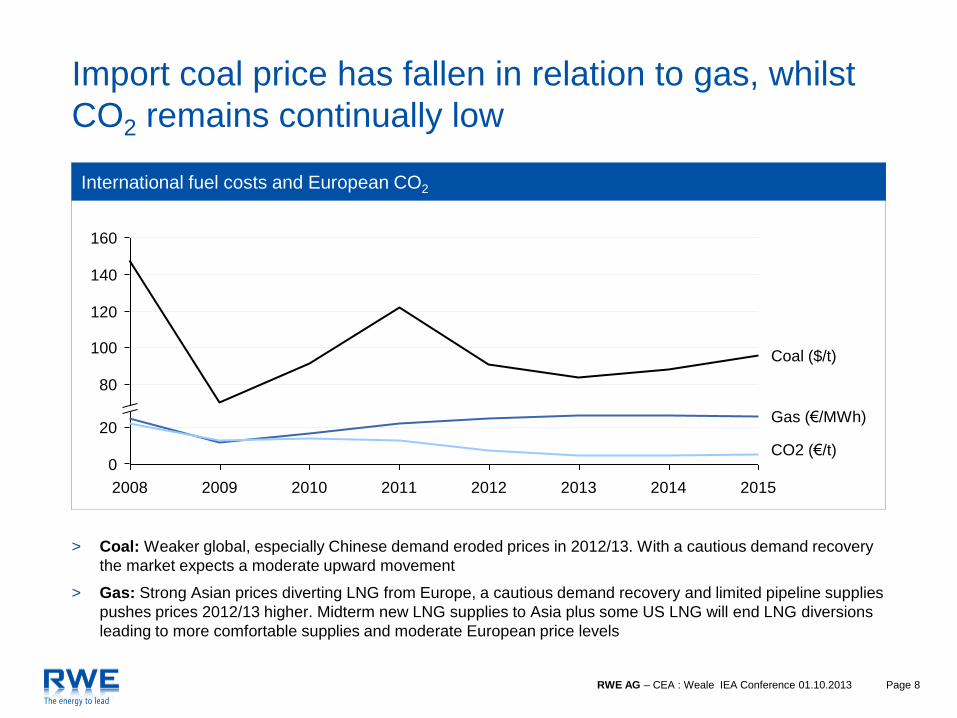

Import coal price has fallen in relation to gas, whilst

CO2 remains continually low

> Coal: Weaker global, especially Chinese demand eroded prices in 2012/13. With a cautious demand recovery

the market expects a moderate upward movement

> Gas: Strong Asian prices diverting LNG from Europe, a cautious demand recovery and limited pipeline supplies

pushes prices 2012/13 higher. Midterm new LNG supplies to Asia plus some US LNG will end LNG diversions

leading to more comfortable supplies and moderate European price levels

2008 2009 2010 2011 2012 2013 2014 2015

120

80

140

160

0

100

20

Coal ($/t)

Gas (€/MWh)

CO2 (€/t)

International fuel costs and European CO2

Page 9 RWE AG – CEA : Weale IEA Conference 01.10.2013

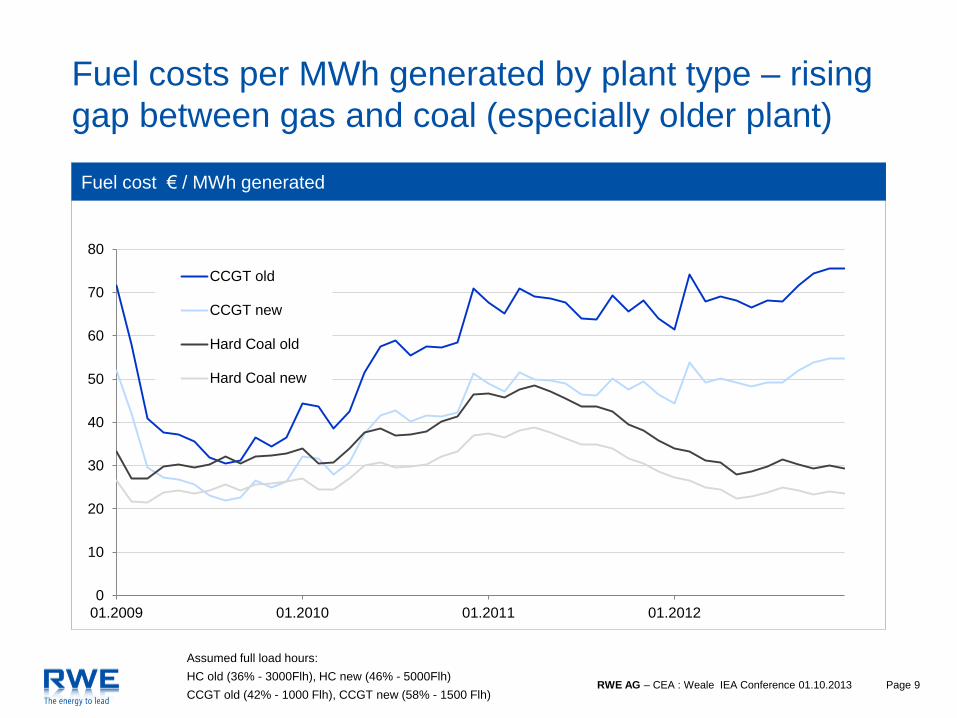

Fuel cost € / MWh generated

0

10

20

30

40

50

60

70

80

01.2009 01.2010 01.2011 01.2012

CCGT old

CCGT new

Hard Coal old

Hard Coal new

Assumed full load hours:

HC old (36% - 3000Flh), HC new (46% - 5000Flh)

CCGT old (42% - 1000 Flh), CCGT new (58% - 1500 Flh)

Fuel costs per MWh generated by plant type – rising

gap between gas and coal (especially older plant)

Page 10 RWE AG – CEA : Weale IEA Conference 01.10.2013

Agenda

1. Definition and determinants of „economics“ and key input

parameters

2. Power prices set through merit-order curve

3. Performance of plants and cost recovery

Page 11 RWE AG – CEA : Weale IEA Conference 01.10.2013

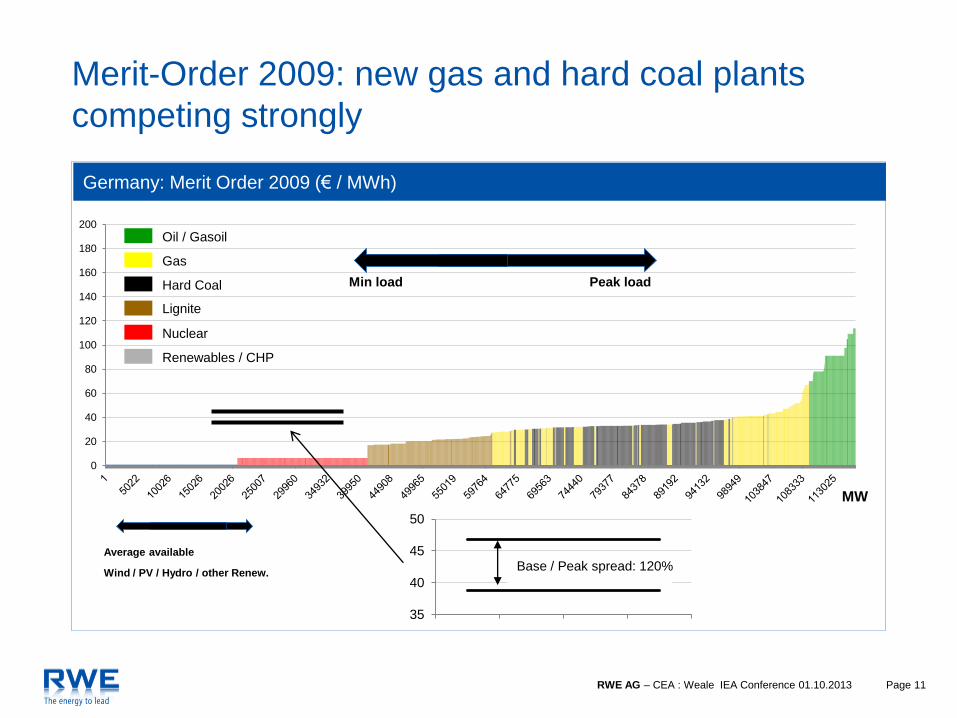

35

40

45

50

Base / Peak spread: 120%

0

20

40

60

80

100

120

140

160

180

200

Peak load Min load

MW

Germany: Merit Order 2009 (€ / MWh)

Average available

Wind / PV / Hydro / other Renew.

Renewables / CHP

Nuclear

Hard Coal

Gas

Oil / Gasoil

Lignite

Merit-Order 2009: new gas and hard coal plants

competing strongly

Page 12 RWE AG – CEA : Weale IEA Conference 01.10.2013

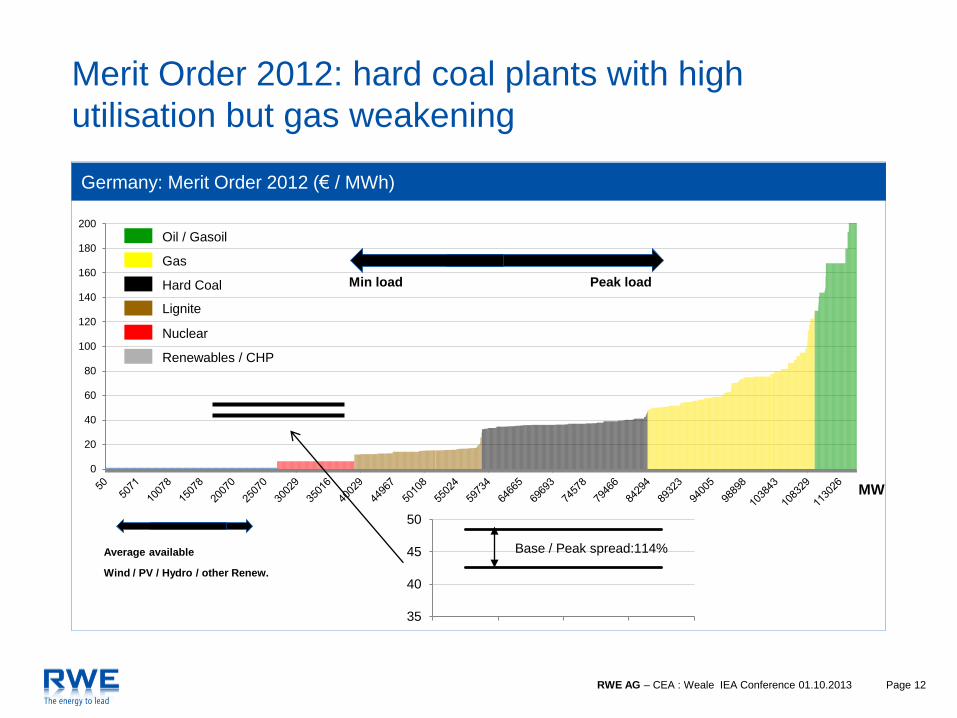

Germany: Merit Order 2012 (€ / MWh)

0

20

40

60

80

100

120

140

160

180

200

Peak load Min load

35

40

45

50

Base / Peak spread:114%

Merit Order 2012: hard coal plants with high

utilisation but gas weakening

Average available

Wind / PV / Hydro / other Renew.

Renewables / CHP

Nuclear

Hard Coal

Gas

Oil / Gasoil

Lignite

MW

Page 13 RWE AG – CEA : Weale IEA Conference 01.10.2013

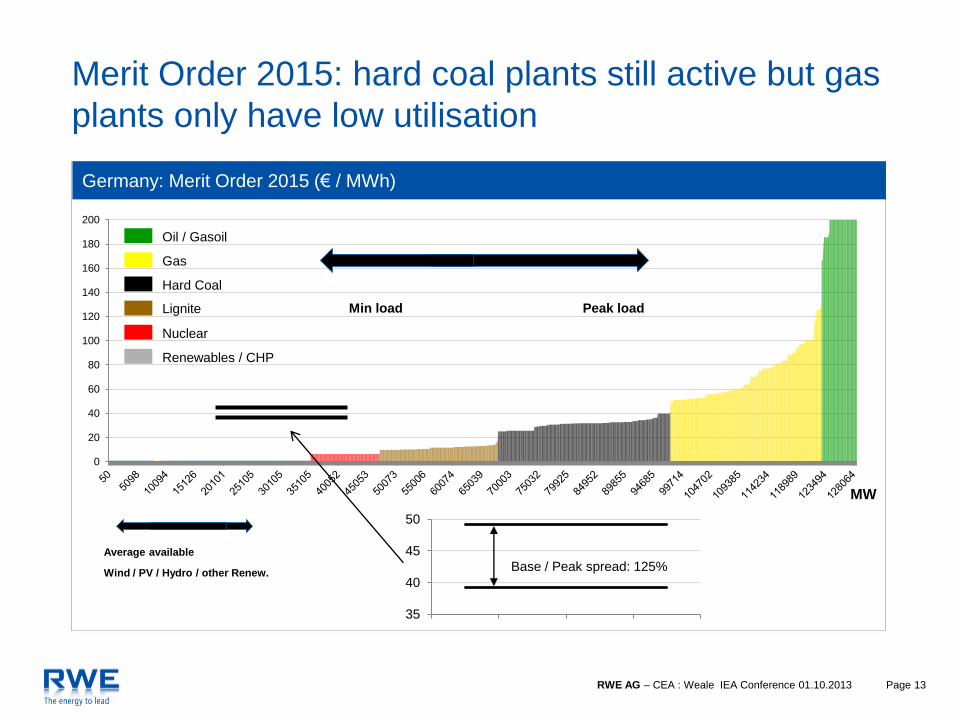

Germany: Merit Order 2015 (€ / MWh)

0

20

40

60

80

100

120

140

160

180

200

MW

35

40

45

50

Base / Peak spread: 125%

Merit Order 2015: hard coal plants still active but gas

plants only have low utilisation

Average available

Wind / PV / Hydro / other Renew.

Renewables / CHP

Nuclear

Hard Coal

Gas

Oil / Gasoil

Lignite Peak load Min load

Page 14 RWE AG – CEA : Weale IEA Conference 01.10.2013

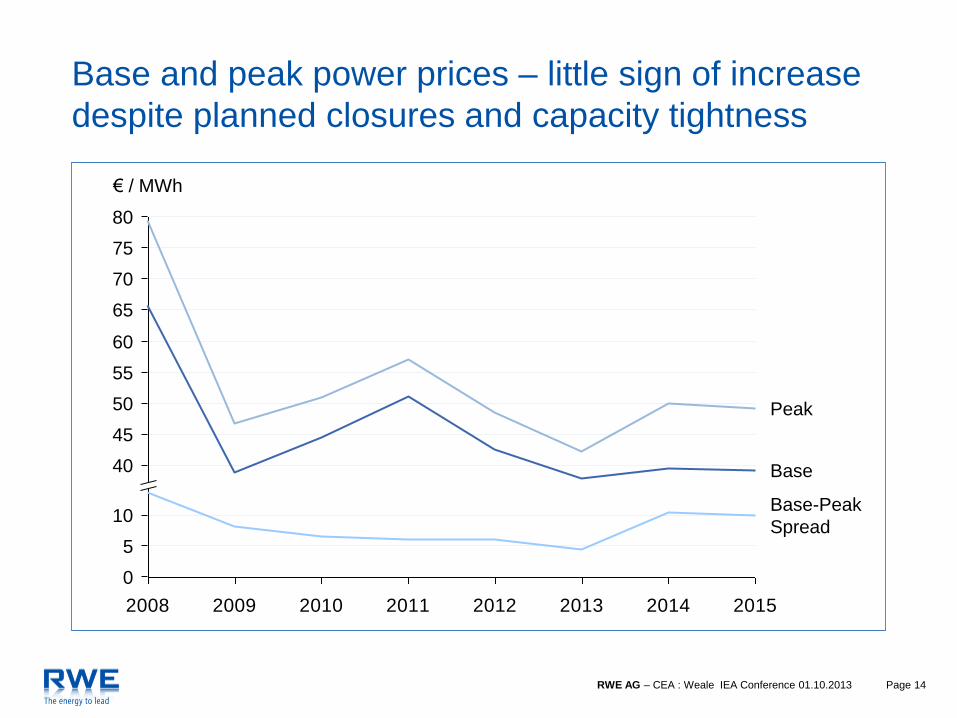

Base and peak power prices – little sign of increase

despite planned closures and capacity tightness

2008 2009 2010 2011 2012 2013 2014 2015

Peak

Base-Peak

Spread

Base

45

10

5

55

75

80

€ / MWh

50

0

65

40

60

70

Page 15 RWE AG – CEA : Weale IEA Conference 01.10.2013

Agenda

1. Definition and determinants of „economics“ and key input

parameters

2. Power prices set through merit-order curve

3. Performance of plants and cost recovery

Page 16 RWE AG – CEA : Weale IEA Conference 01.10.2013

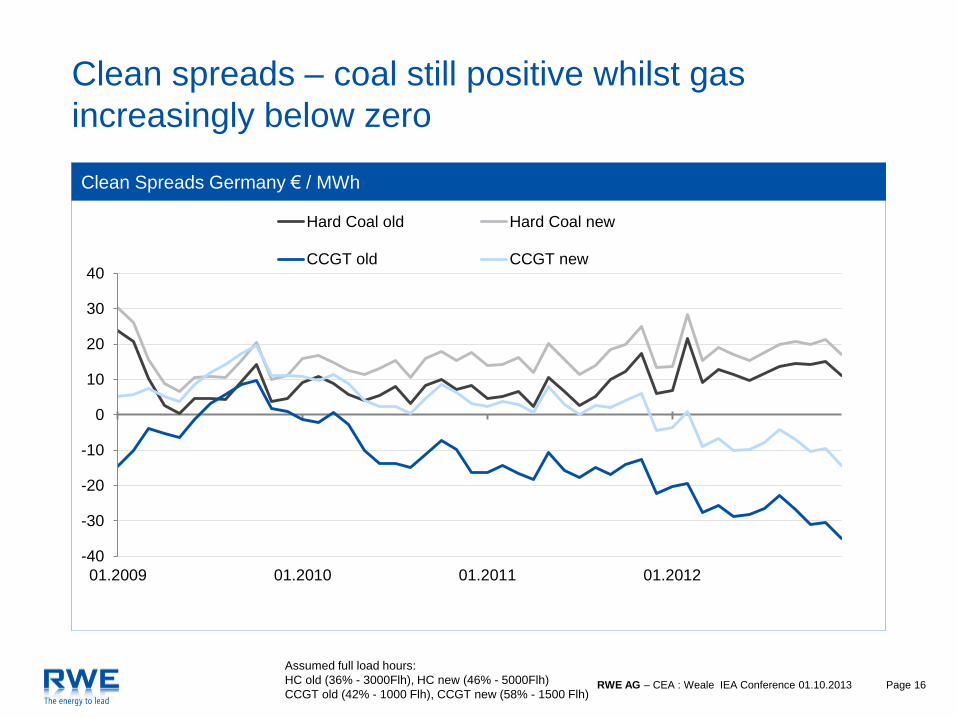

Clean Spreads Germany € / MWh

-40

-30

-20

-10

0

10

20

30

40

01.2009 01.2010 01.2011 01.2012

Hard Coal old Hard Coal new

CCGT old CCGT new

Assumed full load hours:

HC old (36% - 3000Flh), HC new (46% - 5000Flh)

CCGT old (42% - 1000 Flh), CCGT new (58% - 1500 Flh)

Clean spreads – coal still positive whilst gas

increasingly below zero

Page 17 RWE AG – CEA : Weale IEA Conference 01.10.2013

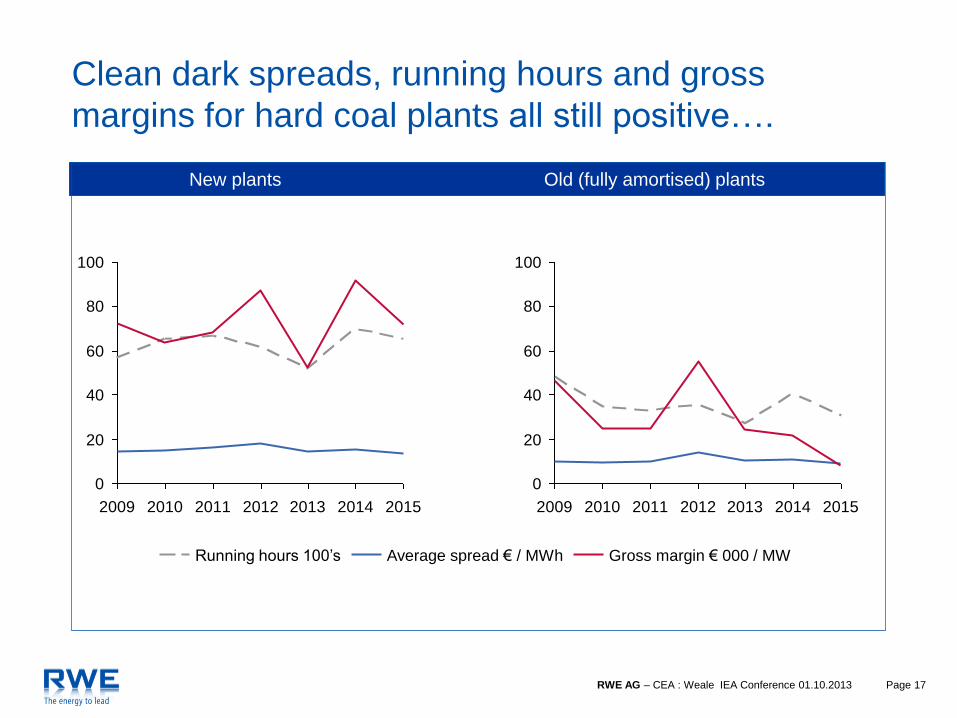

Clean dark spreads, running hours and gross

margins for hard coal plants all still positive….

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014 2015

Gross margin € 000 / MW Average spread € / MWh Running hours 100’s

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014 2015

New plants Old (fully amortised) plants

Page 18 RWE AG – CEA : Weale IEA Conference 01.10.2013

2009 2011 2012 2013 2014

100

150

€ 000 / MW

2010

0

2015

50

2013

0

2015 2010 2012 2011 2009 2014

50

100

150

€ 000 / MW

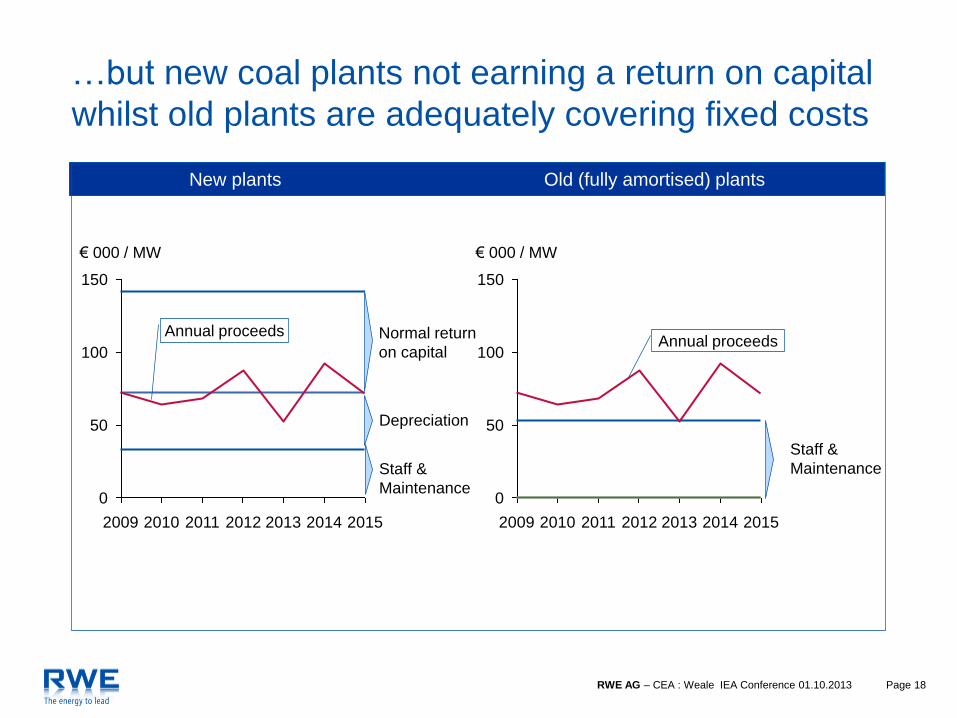

…but new coal plants not earning a return on capital

whilst old plants are adequately covering fixed costs

New plants Old (fully amortised) plants

Normal return

on capital

Depreciation

Staff &

Maintenance

Annual proceeds Annual proceeds

Staff &

Maintenance

Page 19 RWE AG – CEA : Weale IEA Conference 01.10.2013

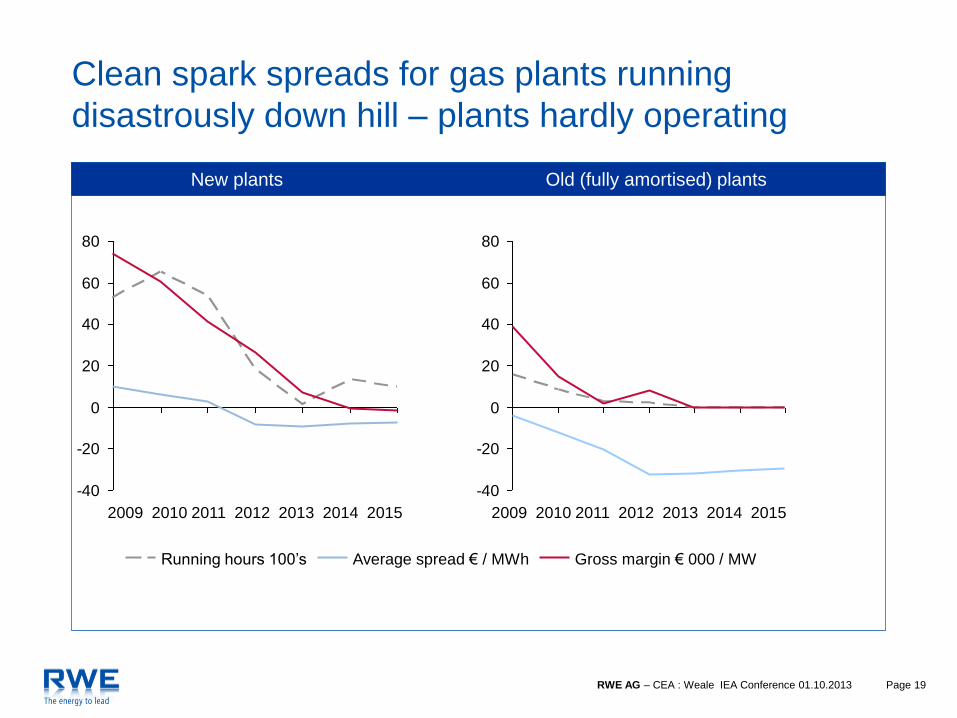

Clean spark spreads for gas plants running

disastrously down hill – plants hardly operating

-40

-20

0

20

40

60

80

Gross margin € 000 / MW Average spread € / MWh Running hours 100’s

New plants Old (fully amortised) plants

-40

-20

0

20

40

60

80

2009 2010 2011 2012 2013 2014 2015 2009 2010 2011 2012 2013 2014 2015

Page 20 RWE AG – CEA : Weale IEA Conference 01.10.2013

€ 000 / MW

2014 2010 2013 2015 2012 2009

0

10

20

30

40

50

60

70

80

90

2011

80

90

30

2013

10

2015

€ 000 / MW

0

2014

20

2012

40

70

60

50

2009 2010 2011

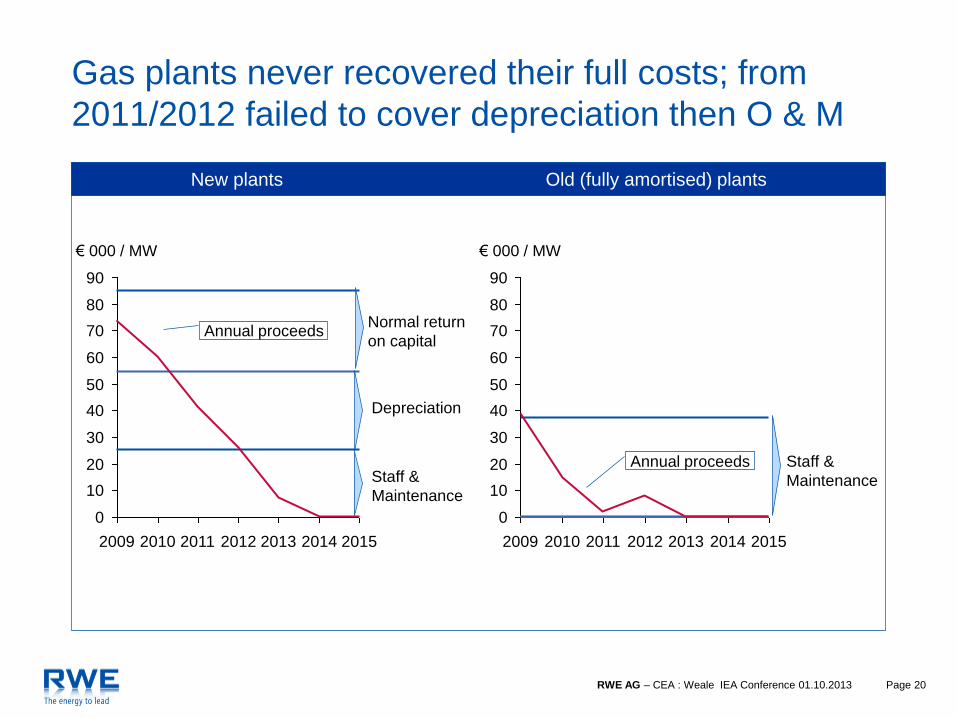

Gas plants never recovered their full costs; from

2011/2012 failed to cover depreciation then O & M

New plants Old (fully amortised) plants

Normal return

on capital

Depreciation

Staff &

Maintenance

Annual proceeds

Annual proceeds Staff &

Maintenance

Page 21 RWE AG – CEA : Weale IEA Conference 01.10.2013

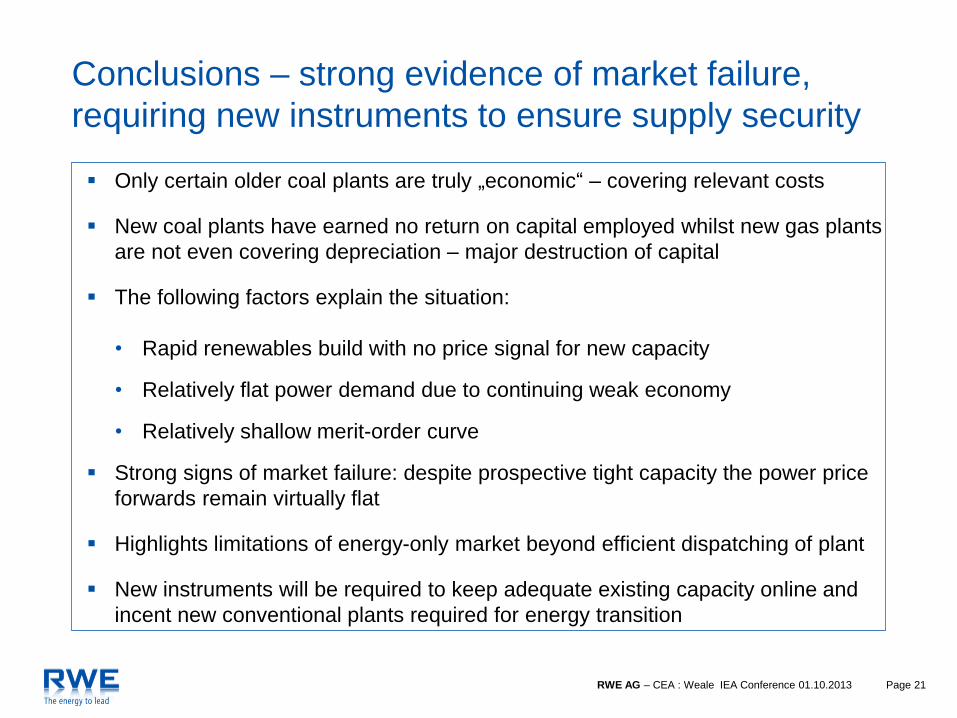

Conclusions – strong evidence of market failure,

requiring new instruments to ensure supply security

Only certain older coal plants are truly „economic“ – covering relevant costs

New coal plants have earned no return on capital employed whilst new gas plants

are not even covering depreciation – major destruction of capital

The following factors explain the situation:

• Rapid renewables build with no price signal for new capacity

• Relatively flat power demand due to continuing weak economy

• Relatively shallow merit-order curve

Strong signs of market failure: despite prospective tight capacity the power price

forwards remain virtually flat

Highlights limitations of energy-only market beyond efficient dispatching of plant

New instruments will be required to keep adequate existing capacity online and

incent new conventional plants required for energy transition

![EXERGY DIAGNOSIS OF COAL FIRED COMBINED … · Exergy Diagnosis of Coal Fired Combined Heat and Power ... in coal fired combined heat and power plant have ... Thermoeconomic [2] analysis](https://img.pdfslide.us/doc/110x75/5b4f746a7f8b9a1b6e8c4949/exergy-diagnosis-of-coal-fired-combined-exergy-diagnosis-of-coal-fired-combined.jpg)