Embed Size (px)

Citation preview

Regional Initiative Concept Paper

Overview of

International Donors' Programs on

Access to Finance for Small and Medium Enterprises

r

September, 2010

Prepared by

January 2012

This publication was produced for review by the United States Agency for International Development. It was prepared for the Partners for Financial Stability (PFS) Project, delivery order number EEM-I-00-07-00005-00 implemented by Deloitte Consulting, LLP

Technical Brief

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe:

Taming the Beast

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 1

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe:

Taming the Beast

Technical Brief

USAID PARTNERS FOR FINANCIAL STABILITY (PFS) PROJECT CONTRACT NUMBER: AID-EEM-I-00-07-00005-00 TASK ORDER NUMBER: AID-OAA-TO-10-00022

DELOITTE CONSULTING, LLP USAID/E&E/ECONOMIC GROWTH/MARKET TRANSITION

January 2012

Author: PFS Advisory Team

DISCLAIMER

The report made possible by the support of the American People through the United States Agency for International Development (USAID). The contents of this report are the sole responsibility of Deloitte Consulting, LLP and do not necessarily reflect the views of USAID or the United States Government.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 2

Table of Contents

EXECUTIVE SUMMARY ......................................................................................................................................1

1. WHY FOREIGN CURRENCY LEADING IS SO PREVALENT ...............................................................................2

Figure 1: High Levels of Foreign Currency Lending in CEE/Eurasia ............................................................ 2

2. THE RISKS OF LENDING IN FOREIGN CURRENCY .........................................................................................4

3. ADDRESSING THE FX LENDING PROBLEM: WILL IT HELP OR HINDER GROWTH AND DEMOCRATIC DEVELOPMENT? – EXPERIENCE FROM FOUR CEE/EURASIAN COUNTRIES ..................................................4

4. TAMING THE BEAST: A MEDIUM TERM CHALLENGE THAT MUST BE ADDRESSED ......................................6

ANNEX OF GRAPHICS ........................................................................................................................................8

Figure 2: CEE/Eurasia Banks’ High Level of Foreign Currency Deposits ..................................................... 8 Figure 3: Currency Volatility in CEE............................................................................................................ 9 Figure 4 – Levels of Non-Performing Loans in CEE .................................................................................... 9 Figure 5: CEE Banks’ Profitability 2007-2010 .......................................................................................... 10 Figure 6 – Economic Growth and Contraction in CEE 2007-2010 ............................................................ 10 Figure 7 – CEE/Eurasia Credit Bubble and Subsequent Credit Crunch ..................................................... 11

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 1

Executive Summary

The high level of bank lending denominated in hard currency (euro, Swiss franc, U.S. dollar) in Central and Eastern Europe (CEE) and Eurasia contributed to the region’s sharp economic downturn that began with the 2008 global financial crisis. During the post-communist transition period in many of the emerging European countries, lending in foreign currencies has been the norm rather than the exception.

Lending in foreign exchange (FX or forex) can appear to be advantageous to borrowers as the interest rates are generally much lower, but these loans carry increased repayment risks for both banks and borrowers. In fact, borrowers with FX loans are, unwittingly, speculating in volatile currency markets.

The FX lending beast has bared its teeth with the sharp depreciation of local currencies in a number of countries since 2008. Financial institutions as well as private businesses and individuals have been badly injured. The region’s banking sectors are weakened with high levels of problem loans, while many businesses and citizens, confronted by increased debt service requirements on loans denominated in foreign currencies, face serious financial hardship.

Problems unleashed with the FX lending binge have reached such high proportions that governments across the region are grappling with measures to lessen the impact. With mortgage foreclosures on the rise and business failures escalating, there is a real risk of political fallout and even democratic backsliding. While today’s headlines point to Hungary as a prominent example of the link between financial / economic instability and democratic backlash, the countries of Southeast Europe and

This Technical Brief is the fifth in a series that addresses financial sector challenges and opportunities in Southeast Europe and Eurasia, specifically the twelve Beneficiary countries of USAID’s Partners for Financial Stability program. The Technical Brief highlights the potential for ongoing fallout from the European debt crisis. The risk from high levels of foreign currency denominated and indexed lending to households and businesses requires more attention and concerted efforts to minimize the impact on businesses and individuals. Borrowing in foreign currency once appeared to be a wise financial decision but is proving to be a hardship and may undermine the progress made in increasing access to finance, promoting private sector growth, expanding the middle class and building credible government institutions.

Origin of the FX Lending Beast in Emerging Europe

As the region transitioned toward market economies, new banking practices and banking systems evolved. Consumers and businesses preferred to save in hard currencies because of underlying skepticism about the long-term viability of “new” local currencies and the prevalence of remittances from relatives abroad. Banks funded their operations in both local and foreign currency, and making loans in local and foreign currency emerged as a reasonable way for banks to manage their FX risk. While lending in foreign currency is prohibited in many advanced countries, in CEE and Eurasia it allowed banking systems to grow and consumers to obtain funds at lower nominal cost since interest rates associated with foreign currencies were much lower.

The underlying risks of FX-lending emerged prominently in 2008-9 as exchange rates moved in favor of the hard currencies. Loan repayments, while stable in the foreign currency, grew in local currency equivalent. Most borrowers, without regular income flows in foreign currency, faced higher loan payments that took larger amounts of their monthly income. Loan defaults and, in some cases, public unrest grew – not because borrowers lost their income or because the economy deteriorated, but because exchange rates shifted.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 2

Ukraine are at particularly high risk of economic contagion and financial instability from the ongoing financial crisis in the European Union1.

This technical brief discusses the prevalence of FX lending in the region and explains the painful downside risks for lenders, borrowers, and the overall economy in terms of credit availability and economic growth. Drawing upon four cases from Ukraine, Hungary, Poland, and Croatia, the paper summarizes the complex mix of policy options that can be employed to try to address the challenge. There is no rapid or single solution. Taming the beast will not be easy, but the stakes are high. With the economic and democratic future of many countries in the region in question, doing nothing is not an appropriate option.

1. Why Foreign Currency Leading is so prevalent

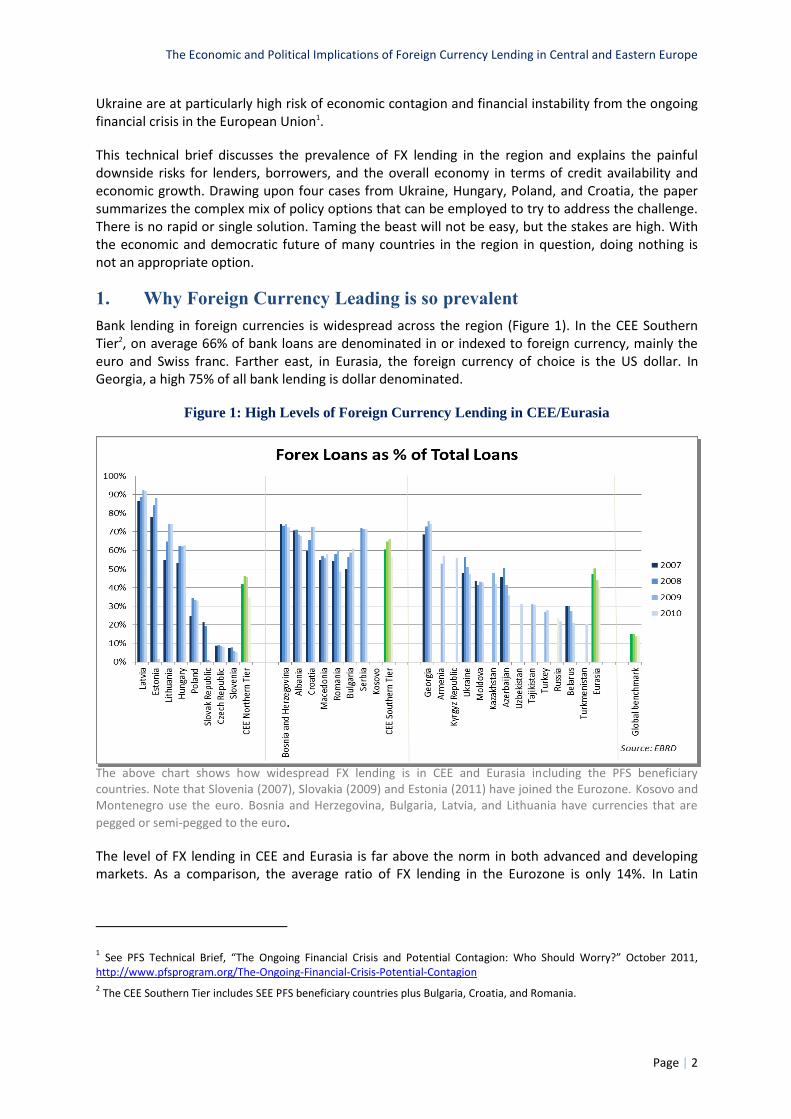

Bank lending in foreign currencies is widespread across the region (Figure 1). In the CEE Southern Tier2, on average 66% of bank loans are denominated in or indexed to foreign currency, mainly the euro and Swiss franc. Farther east, in Eurasia, the foreign currency of choice is the US dollar. In Georgia, a high 75% of all bank lending is dollar denominated.

Figure 1: High Levels of Foreign Currency Lending in CEE/Eurasia

The above chart shows how widespread FX lending is in CEE and Eurasia including the PFS beneficiary countries. Note that Slovenia (2007), Slovakia (2009) and Estonia (2011) have joined the Eurozone. Kosovo and Montenegro use the euro. Bosnia and Herzegovina, Bulgaria, Latvia, and Lithuania have currencies that are

pegged or semi-pegged to the euro.

The level of FX lending in CEE and Eurasia is far above the norm in both advanced and developing markets. As a comparison, the average ratio of FX lending in the Eurozone is only 14%. In Latin

1 See PFS Technical Brief, “The Ongoing Financial Crisis and Potential Contagion: Who Should Worry?” October 2011, http://www.pfsprogram.org/The-Ongoing-Financial-Crisis-Potential-Contagion 2 The CEE Southern Tier includes SEE PFS beneficiary countries plus Bulgaria, Croatia, and Romania.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 3

America, another emerging market region (known for currency crises and bouts of economic instability), FX lending is generally less than 40% of total bank lending3.

There are a number of reasons for the widespread practice of FX lending in the region, including: (1) much lower interest rates on FX loans than on local currency loans; (2) historical use of foreign currency savings to hedge against inflation and other macroeconomic risks; and its impact in terms of (3) the high proportion of bank funding in foreign currency. These reasons are explained below.

Lower Interest Rates on FX Loans Compared to Local Currency Loans

Interest rates on local currency loans across the region are high. Generally, they have not dipped below double digits for most of the transition period4. This reflects a combination of macroeconomic conditions, such as high inflation, as well as the higher lending risks in the region.

Banks are able to offer much lower interest rates on FX loans, which reduce the cost of borrowing and make it possible to borrow more money for the same cost.

Historical use of Foreign Currency Savings to Hedge against Inflation and Other Macroeconomic Risks

Even after 20 years of economic transition since the collapse of communism, macroeconomic uncertainty remains in many of the CEE/Eurasian countries. Inflationary pressures, budget deficits, and current account deficits are high. These weaknesses adversely impact confidence in the local currencies and contribute to exchange rate volatility.

One way businesses and households deal with these uncertainties is to save in foreign currencies which are seen as reliable stores of value. The countries of former Yugoslavia are examples, where the prevalence foreign currency savings is rooted in a long history of macroeconomic instability dating back to hyperinflationary times prior to the transition. Throughout the region, foreign currency savings make up the bulk of banks’ deposit bases (Annex 1 - Figure 2).

High Proportion of Bank Funding in Foreign Currency

To supplement their deposit bases, some CEE and Eurasian banks also borrow from their parent banks or other international financial institutions abroad. These bank borrowings are naturally in foreign rather than the domestic currency. (The amount of money lent by parent banks in the Eurozone to their CEE/Eurasia subsidiaries has dropped significantly since the financial crisis began in 2008.)

With their main sources of funds – deposits and borrowings -- primarily in FX, banks must lend in foreign currency to offset their own exposure to foreign currency risk. Banks do this by “matching” or balancing the amount of foreign currency assets (mainly loans)

3 Canales-Kriljenko, Jorje-Ivan and Coulibaly, Brahima, and Kamil, Herman. “A Tale of Two Regions.” Finance and Development. International Monetary Fund. March 2010. http://www.imf.org/external/pubs/ft/fandd/2010/03/canales.htm 4 Bosnia with a currency pegged to the euro and Belarus are the exceptions. Even Kosovo and Montenegro which use the euro have high interest rates, about 14% and 9% respectively.

How Banks Transfer FX Risk to Borrowers

A lender extends an FX denominated loan to a borrower. When the borrower’s income and savings are in the local currency, the affordability of the scheduled loan payments fluctuates according to changes in exchange rates. A depreciation of the local currency means the borrower must repay more in local currency terms. This increases the likelihood that the borrower will not be able to repay.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 4

and liabilities (deposits and borrowings) they hold. In advanced economies, banks and their clients can hedge FX risk, so the strict matching of banks’ FX assets and liabilities is not required. In developing countries, instruments to hedge against local currency exchange rate movements are not available.

2. The Risks of Lending in Foreign Currency

In this paper, we refer to the practice of lending in FX as a “beast” because the risks are varied, painful and well known from past experience. Following is an overview of the potential risks to banks, businesses, individuals and to economies overall.

Implications for Banks, Businesses and Individuals

When they lend in FX on a large scale, banks expose themselves to the risk of widespread loan defaults when exchange rates move. Losses follow, cutting into banks’ profits and limiting their ability to make new loans. The restricted flow of credit inflicts pain on businesses and households starved of credit.

For those businesses and individuals that borrow in FX and do not have income streams in FX, exchange rate fluctuations can be devastating. Unable to service debts which have ballooned in domestic currency terms, individuals lose their homes and businesses stop growing and lay off employees.

Implications for the Macroeconomy

High levels of FX lending contribute to credit bubbles. The lower interest rates on FX loans allow enterprises and households to borrow larger amounts. Credit expansion helps drive up asset prices. Wide scale deleveraging inevitably occurs when the bubble bursts, resulting in several years of slower economic growth and higher levels of poverty.

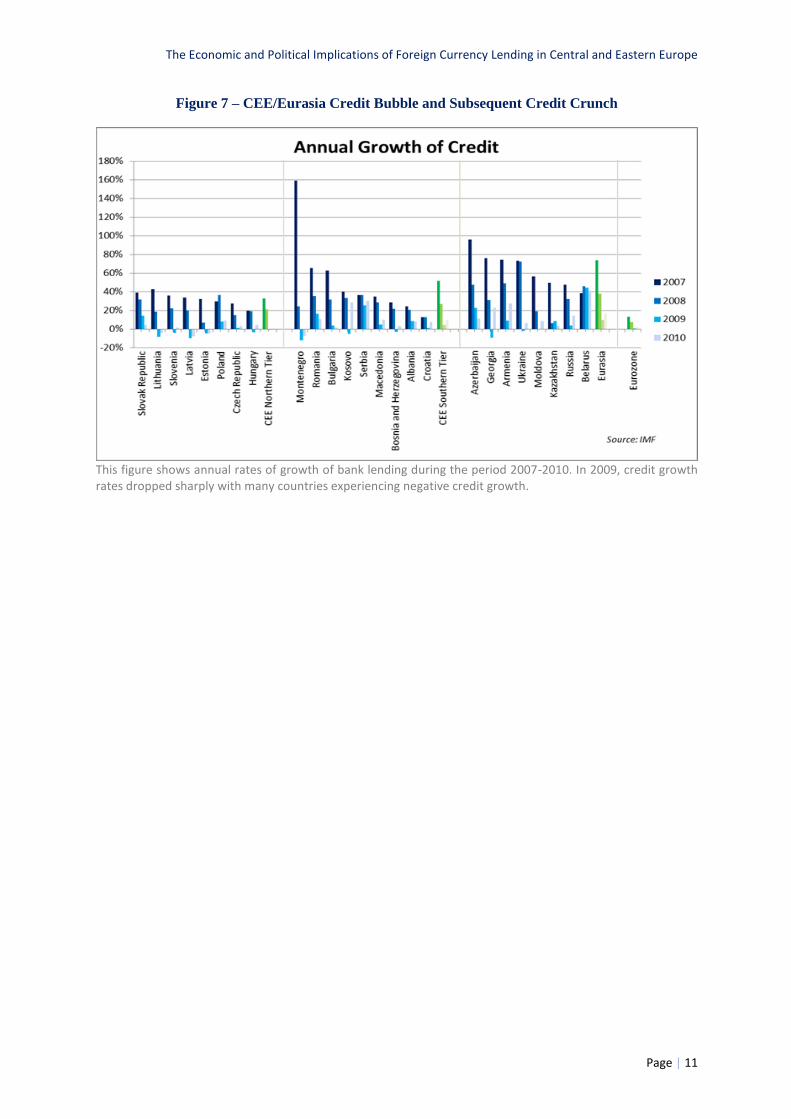

While FX lending was not the only cause of the pre-crisis credit bubble in CEE and Eurasia (Figure 7 – Annual Growth of Credit), it contributed to the bubble and made the region more vulnerable to the external shock brought by the global financial crisis. The immediate impact of the crisis was a credit crunch followed by protracted recessions in many countries across the region in 2009, as central banks increased interest rates to support the local currency and avoid wide scale defaults on FX loans.

3. Addressing the FX Lending Problem: Will it Help or Hinder Growth

and Democratic Development? – Experience from Four

CEE/Eurasian Countries

As financial instability has spread across the region since 2008 and pressure has mounted from distressed borrowers and banks, governments and financial authorities in CEE/Eurasia have undertaken an array of measures to try to address and reduce the risks of FX lending (see Box). In some cases these measures were prompted by populist pressures and demonstrations and were overtly geared to protect consumers and households during a time of rising social tensions.

Worryingly, some of the measures taken to date in the region will relieve political pressure in the short term but raise important longer term concerns about the rule of law. In Hungary, Ukraine, Poland, and Croatia, government decrees in response to populist unrest have negated terms and

FX Lending and Financial Crises

The global financial crisis of 2008 and 2009 exposed fault lines in emerging Europe with the build-up of private debt in foreign currencies. But FX lending is hardly new to crises. Foreign currency risks were catalysts of the financial crises in Asia, Russia and Mexico during the 1990’s. Recently, authorities in Vietnam and Singapore have cautioned financial institutions about lending in foreign currencies.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 5

conditions in legally-binding contracts. While both Hungary and Ukraine have recently banned FX lending to households, Hungary also put a stop to foreclosures and forced banks to assume losses from exchange rate fluctuations on mortgage loans. Likewise, Poland required banks to absorb some of borrowers’ exchange rate losses. Croatia also provided some exchange rate relief for borrowers at the cost of the banks, although officials had tightened restrictions on FX lending earlier in the process.

Some countries in the region have taken another / additional path, recognizing a need to improve consumer disclosures about the risks on FX loans and strengthen consumer protection in other ways in the midst of a widespread outcry from borrowers.

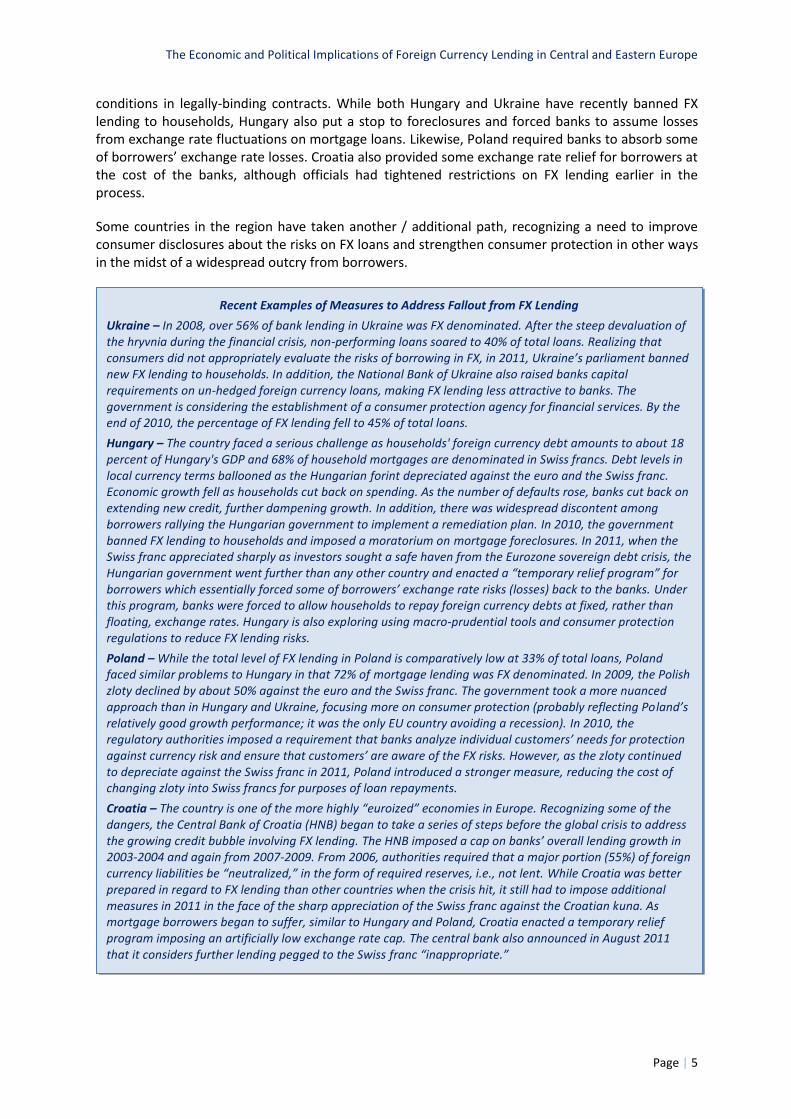

Recent Examples of Measures to Address Fallout from FX Lending

Ukraine – In 2008, over 56% of bank lending in Ukraine was FX denominated. After the steep devaluation of the hryvnia during the financial crisis, non-performing loans soared to 40% of total loans. Realizing that consumers did not appropriately evaluate the risks of borrowing in FX, in 2011, Ukraine’s parliament banned new FX lending to households. In addition, the National Bank of Ukraine also raised banks capital requirements on un-hedged foreign currency loans, making FX lending less attractive to banks. The government is considering the establishment of a consumer protection agency for financial services. By the end of 2010, the percentage of FX lending fell to 45% of total loans.

Hungary – The country faced a serious challenge as households' foreign currency debt amounts to about 18 percent of Hungary's GDP and 68% of household mortgages are denominated in Swiss francs. Debt levels in local currency terms ballooned as the Hungarian forint depreciated against the euro and the Swiss franc. Economic growth fell as households cut back on spending. As the number of defaults rose, banks cut back on extending new credit, further dampening growth. In addition, there was widespread discontent among borrowers rallying the Hungarian government to implement a remediation plan. In 2010, the government banned FX lending to households and imposed a moratorium on mortgage foreclosures. In 2011, when the Swiss franc appreciated sharply as investors sought a safe haven from the Eurozone sovereign debt crisis, the Hungarian government went further than any other country and enacted a “temporary relief program” for borrowers which essentially forced some of borrowers’ exchange rate risks (losses) back to the banks. Under this program, banks were forced to allow households to repay foreign currency debts at fixed, rather than floating, exchange rates. Hungary is also exploring using macro-prudential tools and consumer protection regulations to reduce FX lending risks.

Poland – While the total level of FX lending in Poland is comparatively low at 33% of total loans, Poland faced similar problems to Hungary in that 72% of mortgage lending was FX denominated. In 2009, the Polish zloty declined by about 50% against the euro and the Swiss franc. The government took a more nuanced approach than in Hungary and Ukraine, focusing more on consumer protection (probably reflecting Poland’s relatively good growth performance; it was the only EU country avoiding a recession). In 2010, the regulatory authorities imposed a requirement that banks analyze individual customers’ needs for protection against currency risk and ensure that customers’ are aware of the FX risks. However, as the zloty continued to depreciate against the Swiss franc in 2011, Poland introduced a stronger measure, reducing the cost of changing zloty into Swiss francs for purposes of loan repayments.

Croatia – The country is one of the more highly “euroized” economies in Europe. Recognizing some of the dangers, the Central Bank of Croatia (HNB) began to take a series of steps before the global crisis to address the growing credit bubble involving FX lending. The HNB imposed a cap on banks’ overall lending growth in 2003-2004 and again from 2007-2009. From 2006, authorities required that a major portion (55%) of foreign currency liabilities be “neutralized,” in the form of required reserves, i.e., not lent. While Croatia was better prepared in regard to FX lending than other countries when the crisis hit, it still had to impose additional measures in 2011 in the face of the sharp appreciation of the Swiss franc against the Croatian kuna. As mortgage borrowers began to suffer, similar to Hungary and Poland, Croatia enacted a temporary relief program imposing an artificially low exchange rate cap. The central bank also announced in August 2011 that it considers further lending pegged to the Swiss franc “inappropriate.”

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 6

4. TAMING THE BEAST: A MEDIUM TERM CHALLENGE THAT

MUST BE ADDRESSED

As illustrated by the four case studies in the previous section, there are a number of potential approaches which can be applied to address the problems arising from extensive FX lending. These range from enhancing the attractiveness of the local currency to restricting or discouraging the practice of lending in foreign currency (see Box). While measures that transfer borrowers’ losses to banks may be attractive in the short term, the best solution is a mix of longer term actions and incentives.

Policy Toolbox to Reduce or Address FX Lending

Restricting or discouraging the practice of lending in foreign exchange. These measures range from outright prohibition or regulatory limits on the level of FX lending, to requirements for higher loan loss provisions or risk weights on FX loans for capital adequacy purposes. While, these can generally be effective in reducing FX lending particularly to certain classes of more vulnerable borrowers, such as consumers, an outright prohibition on all FX lending is not advisable. In some countries, there is no alternative, so such a prohibition would restrict the flow of credit to the economy and bring high economic costs. In addition, as the IMF has warned, a ban on FX lending could also encourage shifts to less regulated financial institutions and could have a negative effect on overall financial intermediation. A more market-oriented solution would be to raise the cost of FX lending to unhedged borrowers so that it adequately prices in the risks, by for example requiring banks to hold additional capital. As Croatia’s case illustrated, outright limits on (overall) credit growth appear to have had a beneficial impact on decreasing excessive growth of lending during boom times which lead to harmful credit bubbles.

Reducing banks’ use of FX denominated funding. These measures aim to reduce one of banks’ key reasons for lending in foreign currency. Policy measures can range from outright limits on banks’ use of FX funding sources, to higher liquidity requirements on FX borrowings, to higher deposit insurance premiums on FX deposits. Recent experience from both Latin America and emerging Europe suggests that approaches such as requiring higher liquidity reserves against certain categories of FX denominated liabilities can be effective in curbing FX lending5.

Strengthening banks’ risk management practices with respect to FX lending. Rules can be introduced to require banks to set more conservative loan-to-value or debt service-to-income ratios for foreign currency loans. Romania, Hungary, and Poland all have successfully used such a policy for FX mortgages.

Greater disclosure of risk information to borrowers. While improving disclosure and strengthening financial literacy is important, how effective this can be in reducing demand for FX loans if the cost remains substantially lower, is difficult to assess, unless it is coupled with higher interest rates which reflect the increased risks of FX lending.

Tackling mispricing of risks associated with foreign currency lending. Authorities should require that banks (i) better incorporate these risks in their internal risk pricing and internal capital allocation

5 Canales-Kriljenko, et.al.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 7

models and (ii) hold additional capital, under the Second Pillar of Basel 2, for foreign currency lending to unhedged borrowers6.

Medium-term measures to enhance the attractiveness of borrowing in the local currency. This requires that countries adopt a coherent set of high level macroeconomic (fiscal, monetary and debt management) policies. Credible macroeconomic policies and monetary policy based on inflation targeting rather than exchange rate stability can encourage customers to save in local currency as demonstrated by the Czech Republic, where there are relatively low levels of FX lending even though the banking system is dominated by Eurozone banks. While the impact may only be felt over time, it is important to start putting in place these policies now. In the medium term, it is important that all PFS beneficiary countries improve their macroeconomic institutions and policy framework for both monetary and fiscal policy.

Alleviation of borrowers’ obligations. In response to popular discontent, authorities often introduce measures to benefit borrowers. These typically shift losses from borrowers to banks, which inevitably carries longer term disadvantages in the form of lower lending in the economy.

The IMF and the EBRD are working with monetary authorities in a number of PFS beneficiary countries to develop more flexible exchange rate policies based on inflation targeting rather than exchange rate stability. USAID should actively support these policies through its own programming activities, as they should result in wider exchange rate fluctuations during normal times so that the public and banks better understand the risks of FX lending and thus avoid the practice.

Unfortunately, there is no simple or quick solution. Many of the possible measures involve tampering with the allocation of credit and losses that is ordinarily determined by market forces. Yet, given the stakes – mounting hardship of borrowers and the buildup of social unrest and resentment toward the financial sector – such measures may be warranted. Difficult as it may be, taming the beast is essential to avert financial hardship and democratic backsliding in this strategically important region.

6 ESRB. 2011.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 8

ANNEX OF GRAPHICS

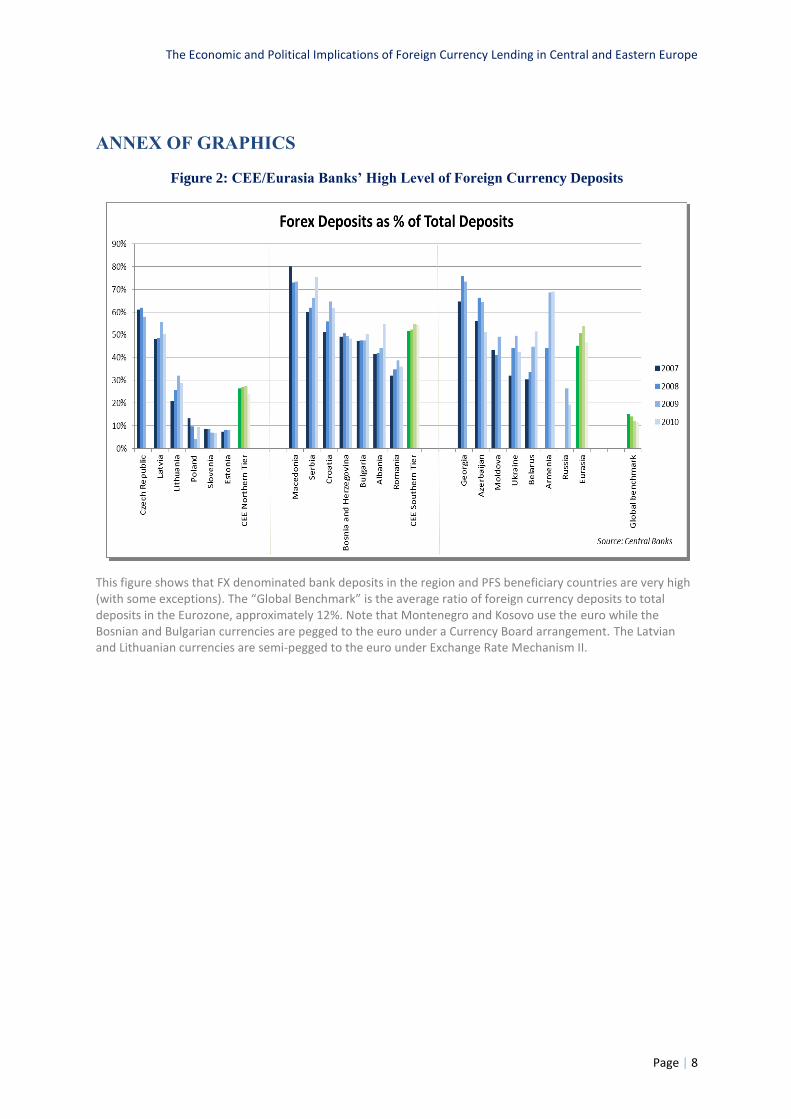

Figure 2: CEE/Eurasia Banks’ High Level of Foreign Currency Deposits

This figure shows that FX denominated bank deposits in the region and PFS beneficiary countries are very high (with some exceptions). The “Global Benchmark” is the average ratio of foreign currency deposits to total deposits in the Eurozone, approximately 12%. Note that Montenegro and Kosovo use the euro while the Bosnian and Bulgarian currencies are pegged to the euro under a Currency Board arrangement. The Latvian and Lithuanian currencies are semi-pegged to the euro under Exchange Rate Mechanism II.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 9

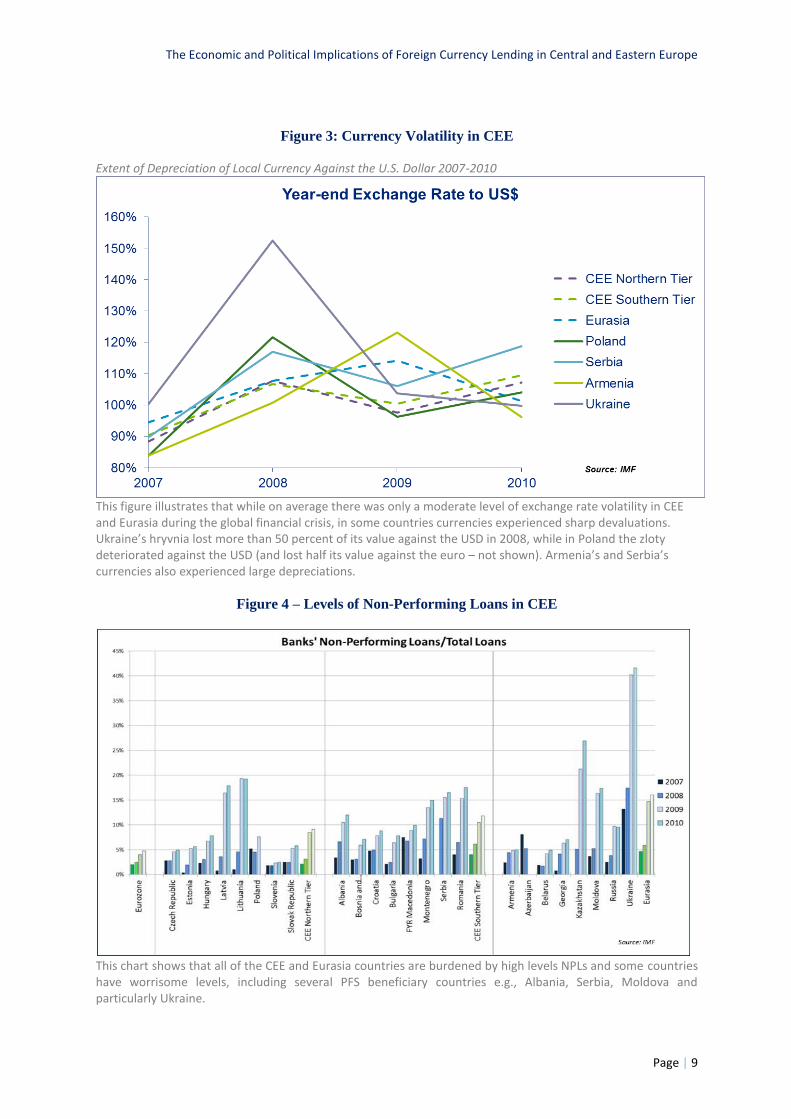

Figure 3: Currency Volatility in CEE

Extent of Depreciation of Local Currency Against the U.S. Dollar 2007-2010

This figure illustrates that while on average there was only a moderate level of exchange rate volatility in CEE and Eurasia during the global financial crisis, in some countries currencies experienced sharp devaluations. Ukraine’s hryvnia lost more than 50 percent of its value against the USD in 2008, while in Poland the zloty deteriorated against the USD (and lost half its value against the euro – not shown). Armenia’s and Serbia’s currencies also experienced large depreciations.

Figure 4 – Levels of Non-Performing Loans in CEE

This chart shows that all of the CEE and Eurasia countries are burdened by high levels NPLs and some countries have worrisome levels, including several PFS beneficiary countries e.g., Albania, Serbia, Moldova and particularly Ukraine.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 10

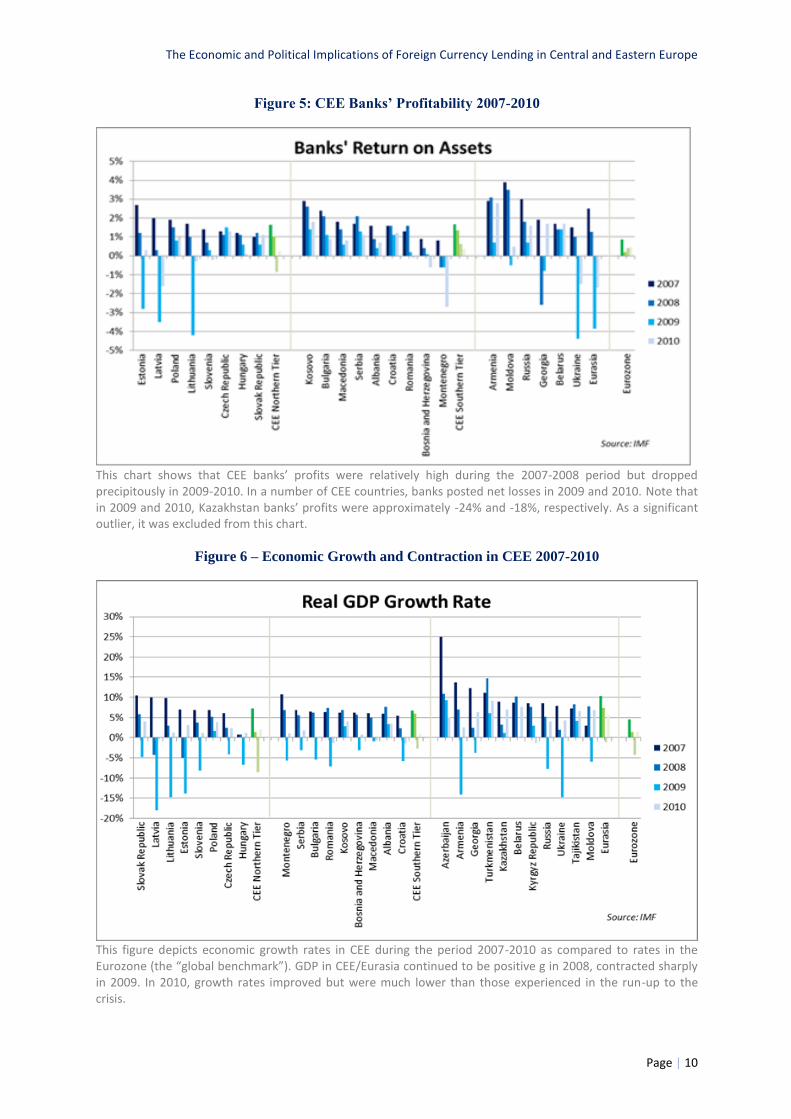

Figure 5: CEE Banks’ Profitability 2007-2010

This chart shows that CEE banks’ profits were relatively high during the 2007-2008 period but dropped precipitously in 2009-2010. In a number of CEE countries, banks posted net losses in 2009 and 2010. Note that in 2009 and 2010, Kazakhstan banks’ profits were approximately -24% and -18%, respectively. As a significant outlier, it was excluded from this chart.

Figure 6 – Economic Growth and Contraction in CEE 2007-2010

This figure depicts economic growth rates in CEE during the period 2007-2010 as compared to rates in the Eurozone (the “global benchmark”). GDP in CEE/Eurasia continued to be positive g in 2008, contracted sharply in 2009. In 2010, growth rates improved but were much lower than those experienced in the run-up to the crisis.

The Economic and Political Implications of Foreign Currency Lending in Central and Eastern Europe

Page | 11

Figure 7 – CEE/Eurasia Credit Bubble and Subsequent Credit Crunch

This figure shows annual rates of growth of bank lending during the period 2007-2010. In 2009, credit growth rates dropped sharply with many countries experiencing negative credit growth.

Partners for Financial Stability (PFS)

1919 N. Lynn Street

Arlington, VA 22209

Phone: +1 571 882 5000

Fax: +1 571 882 5100