Embed Size (px)

Citation preview

Ž .Research Policy 30 2001 535–588www.elsevier.nlrlocatereconbase

The dynamics of technological innovation: the case of thepharmaceutical industry

Basil Achilladelis a,), Nicholas Antonakis b

a 39, Ionias Street, Kifissia, Athens 14563, Greeceb Ministry of DeÕelopment and UniÕersity of Athens, Athens Greece

Received 9 April 1999; received in revised form 7 October 1999; accepted 18 January 2000

Abstract

Ž .This is an empirical and historical study of the dynamics of technological innovation TI in the pharmaceutical industryfrom its establishment at the beginning of the 19th century to 1990. It is based on the identification and evaluation of the

Ž .originality and commercial significance of 1736 product innovations new medicines commercialized between 1800 and1990, and on company economic data for the period 1950–1990. The study is presented in the framework of establishedmacroeconomic theory of technical change.

Ž .Applying both empirical and historical evidence, the study: a identifies the technological, social and economic drivingŽ . Ž .forces for TI; b examines the relation between originality and market performance of medicinal innovations; c studies the

Žmechanisms of the diffusion of medicinal technologies that led to the formation of five successive generations of drugs long. Ž .waves ; d describes the structural changes forced on the pharmaceutical industry by the introduction and development of

Ž .each successive generation of drugs; e provides evidence of the concentration of the innovative segment of thepharmaceutical industry among few large companies, which sustained high levels of growth and R&D expenditures bymeans of inhouse innovation, technological and therapeutic market specialization, and mergers and acquisitions of

Ž .companies within and outside the pharmaceutical industry; and f shows that the localization of the innovative segment ofthe pharmaceutical industry in the USA, UK, Germany, Switzerland and France was caused by the influence of nationalenvironments on the intensities of the driving forces for TI. q 2001 Elsevier Science B.V. All rights reserved.

Keywords: Dynamics of technological innovation; Pharmaceutical industry; Long waves of technical change

1. Introduction

Ž .Technological innovation TI is a dynamic pro-cess, perhaps the most dynamic of all industrial

Ž .activities. Schumpeter 1943 with his Agales of cre-ative destructionB gave a vivid description of theeffects of the introduction and diffusion of major

) Corresponding author. Tel.: q30-1-800-01-52; fax: q30-1-800-01-52.

technological discoveries and inventions in industryand the world economy.

Schumpeter’s seminal theory was further elabo-rated at the macroeconomic level by many authorsŽ . Že.g., Freeman, 1996 , notably Rosenberg 1969,

. Ž . Ž .1976 , Nelson and Winter 1977 , Dosi 1982 , Free-Ž .man and Perez 1988 , who, by incorporating Kon-

Ž .dratiev’s 1925 theory of Along wavesB in theŽ .world economy and Kuhn’s 1962 theory of scien-

tific revolutions, introduced the concepts of Atechno-

0048-7333r01r$ - see front matter q 2001 Elsevier Science B.V. All rights reserved.Ž .PII: S0048-7333 00 00093-7

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588536

logical imperativesB or Atechnological paradigmsBŽ .TPs , which initiate Atechnological trajectoriesBŽ .TTs whose pathways determine the fluctuating ratesof technical change. TT were, in turn, found tocluster together forming Atechnology systemsB andAtechno-economic paradigmsB which, by spreadingacross numerous industrial and service sectors, causethe formation and succession of Along wavesB in theworld economy.

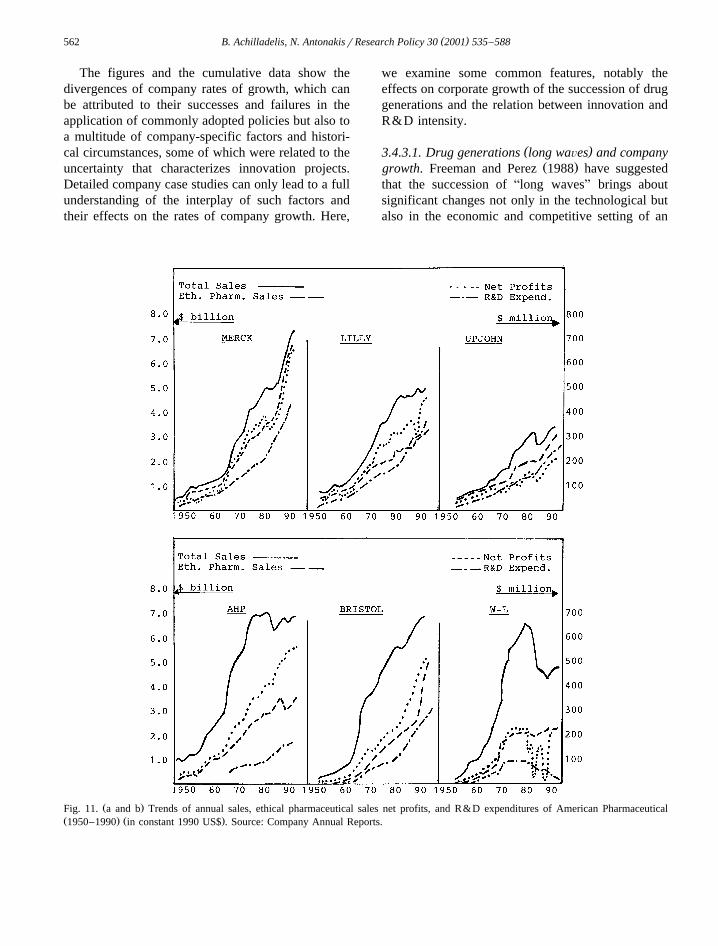

These concepts provided an extremely usefulframework for the study of TI, which offered anumber of plausible macroeconomic interpretationsregarding the fluctuations of the rates of technicalchange, the diffusion of technologies and their inter-actions with the economy. Less attention was, how-ever, addressed at the microeconomic aspects oftechnological advance, notably the dynamics of TI atthe level of innovating institutions where they arefirst expressed and can be more accurately detectedand evaluated. Indeed, the dynamism of TI is ex-pressed in more subtle ways before it integrates intoAtechno-economic paradigmsB and Along wavesB.For example, TI acts as a catalyst in the interactionof science and technology accelerating their other-wise arduous advance, in the technological develop-ment and market expansion of industrial sectors, inthe research intensity, technological specializationand business performance of industrial companies,and in the competitive advantage of national indus-tries.

The mechanisms by which TI exerts such influ-ence can be identified and evaluated by studies ofthe technological and business histories of research-intensive industrial sectors. Long-term sectoral stud-ies of TI offer the advantage of a homogeneousscientific, technological and commercial frameworkwhich allows for the study of the rates of technicalchange and for comparisons in science, technologyand business among historical periods, companiesand countries. The use of technology inputroutputindicators is essential because they provide quantita-tive evidence for or against any proposed hypothesis.

This is a study of the dynamics of TI in thepharmaceutical industry from its establishment at thebeginning of the 19th century to 1990. The pharma-ceutical industry is a relatively small research-inten-sive industry that showed a consistently strong inno-vative record throughout its 200-year-long history.

From its establishment to this day, it has maintaineda close and fruitful two-way relation with academicresearch institutions in chemistry, pharmacology, thelife sciences and medicine. The succession of tech-nologies did not create waves but only ripples ofcreative destruction because leading companies wereflexible enough to adapt to the exigencies of the newregimes and even to prosper from them. A thrivingand extremely profitable business was created withsome of its innovations becoming household namesfor nearly a century and others having deeply af-fected the nature, structure and morals of our society.Indeed, in this latter aspect, there is no other industrythat had a comparable effect.

The study is presented in the following threesections.

Section 2 describes the sources and assesses thedata used in the study.

Section 3 presents an empirical study of the dy-namics of TI in the pharmaceutical industry in theframework of established theory of technical change.

Ž .a DriÕing forces of TI. TI involves scientificrtechnological and commercial uncertainties and hencethe acceptance of financial risks on the part of publicand private innovating institutions. It is, therefore,essential to identify the scientific, technological, so-cial and economic forces that have compelled thepharmaceutical industry throughout its long historyto discover, develop and commercialize newmedicines.

Ž . ( )b Dynamic effects of radical innoÕations RIs .Highly original innovations cause the establishmentof new industrial sectors or subsectors and contributeto the diffusion of technology. The pharmaceuticalindustry is not an exception to this rule. In ouranalysis, we examine the technological and commer-cial characteristics of RIs, which impart to them theirdynamic properties, and investigate the companies’justifications in accepting the higher risks associatedwith their development and commercialization.

Ž .c Diffusion of innoÕation. The 200-year-longinnovation history of the pharmaceutical industry isunique in manufacturing. To identify the dynamicsand mechanisms by which it maintained a nearlycontinuous drive for innovation over such a longperiod, we examine the patterns of distribution over

Ž .time of radical and incremental innovations IIs bytherapeutic sector; we identify the characteristics of

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 537

innovations that served as TPs and of the TTs theygenerated; and we find that the clustering of TPs andtrajectories gave rise to five successive generationsof pharmaceuticals that have kept alive the industry’sdrive for innovation.

Ž .d The innoÕatiÕe performance of pharmaceuti-cal companies. Our innovation data show that 30companies introduced more than 70% of all theinnovations of our sample. Most of these companiesstayed in business for about a century despite therevolutionary changes of the competitive environ-ment of the pharmaceutical industry caused by theintroduction of successive generations of technology.We examine the patterns of growth of some of thesecompanies, their innovation records, and the strate-gies they adopted to ensure growth including techno-logical and market specialization, mergers and acqui-sitions and R&D intensity.

Ž .e The geography of innoÕation. Despite theuniversal need for medicines, our data show a strongconcentration of the innovative segment of the phar-maceutical industry in five countries, namely theUSA, Germany, Switzerland, the UK and France.We examine the causes of this concentration and inparticular the influence of national policies on theintensities of the driving forces of TI.

Section 4 presents an interpretation of the historyof innovation in the pharmaceutical industry fromthe beginning of the 19th century to 1990 based onthe findings and analysis of the previous section.

2. Sources, evaluation and interpretation of data

2.1. InnoÕation counts

The study is primarily based on the identificationand evaluation of product innovations of the pharma-ceutical industry, which were commercialized from

Ž .about 1800 to 1990. Product innovations new drugsŽ .that are included are new chemical entities NCEs ,

i.e., they differ in chemical composition and struc-ture. Mixtures and diverse formulations of NCEs are

Žnot included. From previous studies Achilladelis et.al., 1987; Achilladelis, 1993 , we came to understand

that the identification of all the innovations of anindustrial sector or subsector is essential if we are toarrive to useful conclusions about the dynamics of

TI. To this end, we identified all the innovationsŽ .1736 of 16 subsectors of the pharmaceutical indus-

Žtry described in Martindale’s Pharmacopoeia Re-.ynolds, 1989 , which account for about 80% of all

Ž .subsectors Table 1 . The chemical structure andcomposition of each drug were obtained from the

ŽUSAN and USP Dictionary of Drug Names Fleeger,.1994 ; tradenames, innovating companies and years

of commercialization were obtained by crosscheck-ing the above references with the World’s Pharma-

Ž .ceutical Directory Anon, 1991 . To ensure againstomissions of significant drugs, we cross-checked ourlists with those of the USA Food and Drug Admi-

Ž .nistration’s FDA Center for Drug Evaluation andŽResearch U.S. Department of Health and Human

.Services, 1989 ; with the American Medical Associa-Ž .tion’s 1980 AAMA Drug EvaluationsB; and with

Ž .Sneader’s 1996 book ADrug Prototypes and theirExploitationB, which describes about 1300 drugs.Thus, although there must be some omissions, ourdata base is adequate for the purposes of our re-search and analysis.

2.1.1. Process innoÕationsAlthough extremely important, we have not in-

cluded them because, with few notable exceptions,they are hard to identify and evaluate with certainty.Most of them are used for the manufacture of one ora few products so that the study of product innova-tions covers indirectly processing as well. Further-more, process innovations are seldom commercial-ized because companies seldom license their pro-cesses unless they license the corresponding product.

2.2. EÕaluation of innoÕations

2.2.1. OriginalityThe evaluation of the originality of innovations

was based on their chemical composition, therapeuticaction and effectiveness, timing of their commercial-ization and the extent to which they were imitated.

2.2.2. Market performanceThe measurement of commercial success of phar-

maceutical innovations is easier than it is in othersectors of manufacturing because of governmentalagencies’ reports on the subject, particularly sincethe 1970s when annual reports of the International

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588538

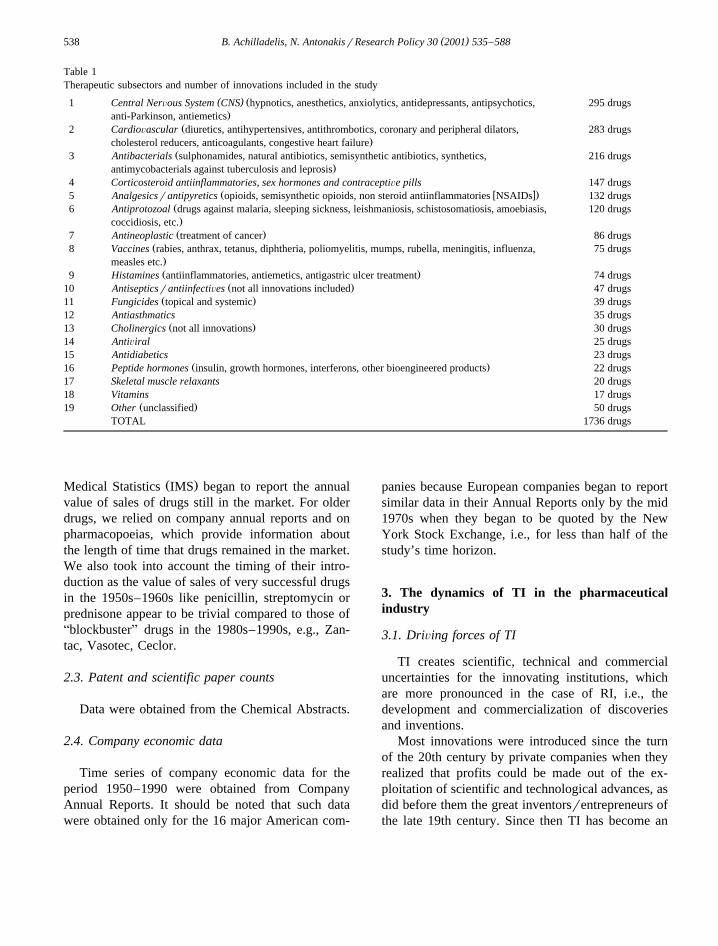

Table 1Therapeutic subsectors and number of innovations included in the study

( ) Ž1 Central NerÕous System CNS hypnotics, anesthetics, anxiolytics, antidepressants, antipsychotics, 295 drugs.anti-Parkinson, antiemetics

Ž2 CardioÕascular diuretics, antihypertensives, antithrombotics, coronary and peripheral dilators, 283 drugs.cholesterol reducers, anticoagulants, congestive heart failure

Ž3 Antibacterials sulphonamides, natural antibiotics, semisynthetic antibiotics, synthetics, 216 drugs.antimycobacterials against tuberculosis and leprosis

4 Corticosteroid antiinflammatories, sex hormones and contraceptiÕe pills 147 drugsŽ w x.5 Analgesicsrantipyretics opioids, semisynthetic opioids, non steroid antiinflammatories NSAIDs 132 drugs

Ž6 Antiprotozoal drugs against malaria, sleeping sickness, leishmaniosis, schistosomatiosis, amoebiasis, 120 drugs.coccidiosis, etc.Ž .7 Antineoplastic treatment of cancer 86 drugs

Ž8 Vaccines rabies, anthrax, tetanus, diphtheria, poliomyelitis, mumps, rubella, meningitis, influenza, 75 drugs.measles etc.Ž .9 Histamines antiinflammatories, antiemetics, antigastric ulcer treatment 74 drugs

Ž .10 AntisepticsrantiinfectiÕes not all innovations included 47 drugsŽ .11 Fungicides topical and systemic 39 drugs

12 Antiasthmatics 35 drugsŽ .13 Cholinergics not all innovations 30 drugs

14 AntiÕiral 25 drugs15 Antidiabetics 23 drugs

Ž .16 Peptide hormones insulin, growth hormones, interferons, other bioengineered products 22 drugs17 Skeletal muscle relaxants 20 drugs18 Vitamins 17 drugs

Ž .19 Other unclassified 50 drugsTOTAL 1736 drugs

Ž .Medical Statistics IMS began to report the annualvalue of sales of drugs still in the market. For olderdrugs, we relied on company annual reports and onpharmacopoeias, which provide information aboutthe length of time that drugs remained in the market.We also took into account the timing of their intro-duction as the value of sales of very successful drugsin the 1950s–1960s like penicillin, streptomycin orprednisone appear to be trivial compared to those ofAblockbusterB drugs in the 1980s–1990s, e.g., Zan-tac, Vasotec, Ceclor.

2.3. Patent and scientific paper counts

Data were obtained from the Chemical Abstracts.

2.4. Company economic data

Time series of company economic data for theperiod 1950–1990 were obtained from CompanyAnnual Reports. It should be noted that such datawere obtained only for the 16 major American com-

panies because European companies began to reportsimilar data in their Annual Reports only by the mid1970s when they began to be quoted by the NewYork Stock Exchange, i.e., for less than half of thestudy’s time horizon.

3. The dynamics of TI in the pharmaceuticalindustry

3.1. DriÕing forces of TI

TI creates scientific, technical and commercialuncertainties for the innovating institutions, whichare more pronounced in the case of RI, i.e., thedevelopment and commercialization of discoveriesand inventions.

Most innovations were introduced since the turnof the 20th century by private companies when theyrealized that profits could be made out of the ex-ploitation of scientific and technological advances, asdid before them the great inventorsrentrepreneurs ofthe late 19th century. Since then TI has become an

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 539

essential activity for companies in research-intensivesectors. The acceptance of financial risks associatedwith TI on the part of companies indicates that thereare social and economic forces which compel themto innovate.

However, TIs were also introduced in socialistcountries or when the capitalist system was stillyoung and research-intensive companies did not ex-ist, as was the case of the pharmaceutical industryfor most of the 19th century. Forces of a less capital-istic nature acted upon individual scientists, engi-neers, physicians and on institutions, such as univer-sities, hospitals, public or private, not for profithealth-care organizations, which discovered and de-veloped new medicines and made them available tothe public. These forces were effective because oftheir relation to AnoncommercialB characteristics ofTI, namely its dependence on scientific advance,creative individuals and the recognition of societalneeds rather than on market demand, commercialcompetition and profit.

Sciencertechnology ApushB and market ApullBwere considered the main driving forces for TI andmany scholars have argued in favor of one or the

Žother Schmookler, 1976; Mowery and Rosenberg,.1979; Walsh, 1984 . For economists, in particular,

this concept accommodated the treatment of all eco-nomic parameters under Amarket demandB leavingAsciencertechnologyB as an externality. Because ofthe complexity of the process of TI, this concept hasa weak explanatory power regarding the interpreta-tion of historical facts and is inadequate for thesupport of a theory of the dynamics of TI. Theseshortcomings were realized and authors of morerecent studies found it necessary to introduce a mul-titude of more specific factors to account for differ-ences and fluctuations over time of the innovationrecord of industrial sectors, companies and countriesŽ .Dosi et al., 1988; Mokyr, 1990; Porter, 1990 .

To identify the driving forces that impel compa-nies and other institutions to innovate, we havereviewed numerous case studies and applied thefindings of two empirical studies that were con-ducted with the participation of researchers, inven-tors, managers and many research-intensive compa-nies: Project ASAPPHOB examined the factors thatare associated with success and failure in industrial

Ž .innovation Freeman et al., 1971, 1972 and project

AInnovation and the firm in the chemical industryBstudied the dynamics of TI including the forces that

Ž .drive innovation Achilladelis et al., 1982, 1990 .Seven driving forces were identified and defined

as follows:

v ŽScientific and technological adÕances external.to the innovating institution ;

v Ž .Raw materials availability or scarcity ;v ŽMarket demand evaluated by companies prior

to the decision to proceed with the development.of an innovation ;

v ŽCompetition response to scientificrtechnicalrcommercial advances made by competing com-

.panies ;v ŽSocietal needs which could not be evaluated in

terms of market demand prior to the decision to.proceed with the development of an innovation ;

v ŽGoÕernment legislation legislation that affectsR&D and the competitive setting of an indus-

.trial sector ;v Company scientific, technological and market

Žspecialization a company has introduced in thepast innovations based on related science, tech-

.nology and markets .

These driving forces are not independent fromeach other but their effects on TI are distinct asare the responses to them by innovating institutions.The first six are AenvironmentalB in character, i.e.,they affect all research-intensive companies of oneor a number of industries. Indeed, they were im-

Ž .plicitly identified by Landes 1970 in AUnboundPrometheusB as factors responsible for technicalchange since the Industrial Revolution. The seventhis company-specific and exerts a strong influence ona company’s innovation record over long periods oftime.

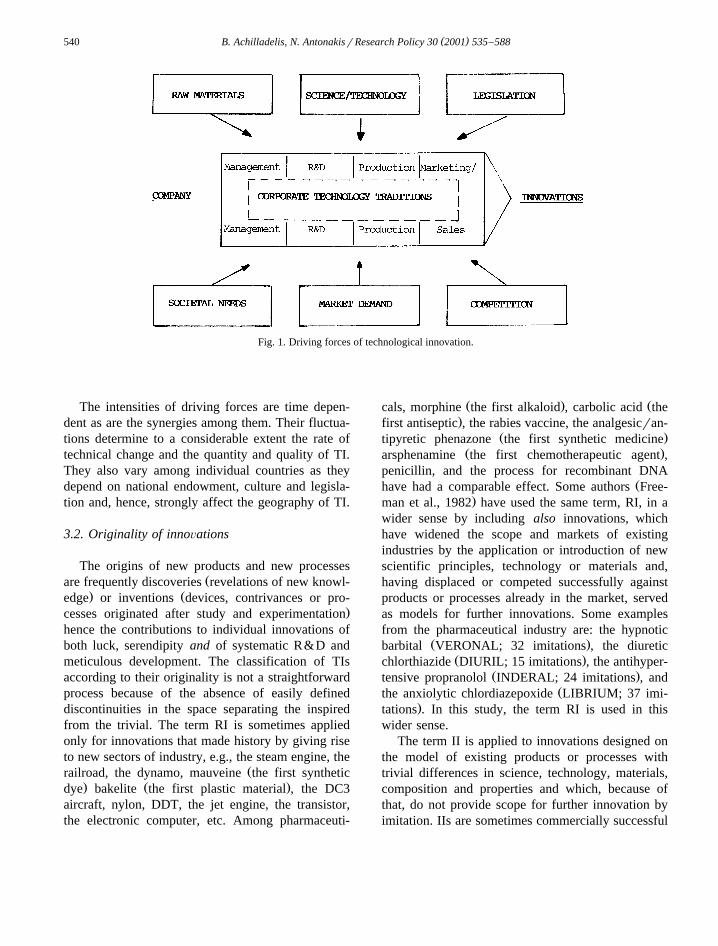

Under the influence of the AenvironmentalB forces,companies in research-intensive sectors developedinhouse capabilities to increase their sensitivity andability to respond to them: R&D departments forsciencertechnology advances and new raw materi-als; marketingrsales departments for market demandand competition; legal and patent departments forgovernment legislation. Fig. 1 shows in a schematicway the interactions between driving forces and in-novating companies.

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588540

Fig. 1. Driving forces of technological innovation.

The intensities of driving forces are time depen-dent as are the synergies among them. Their fluctua-tions determine to a considerable extent the rate oftechnical change and the quantity and quality of TI.They also vary among individual countries as theydepend on national endowment, culture and legisla-tion and, hence, strongly affect the geography of TI.

3.2. Originality of innoÕations

The origins of new products and new processesŽare frequently discoveries revelations of new knowl-

. Žedge or inventions devices, contrivances or pro-.cesses originated after study and experimentation

hence the contributions to individual innovations ofboth luck, serendipity and of systematic R&D andmeticulous development. The classification of TIsaccording to their originality is not a straightforwardprocess because of the absence of easily defineddiscontinuities in the space separating the inspiredfrom the trivial. The term RI is sometimes appliedonly for innovations that made history by giving riseto new sectors of industry, e.g., the steam engine, the

Žrailroad, the dynamo, mauveine the first synthetic. Ž .dye bakelite the first plastic material , the DC3

aircraft, nylon, DDT, the jet engine, the transistor,the electronic computer, etc. Among pharmaceuti-

Ž . Žcals, morphine the first alkaloid , carbolic acid the.first antiseptic , the rabies vaccine, the analgesicran-

Ž .tipyretic phenazone the first synthetic medicineŽ .arsphenamine the first chemotherapeutic agent ,

penicillin, and the process for recombinant DNAŽhave had a comparable effect. Some authors Free-

.man et al., 1982 have used the same term, RI, in awider sense by including also innovations, whichhave widened the scope and markets of existingindustries by the application or introduction of newscientific principles, technology or materials and,having displaced or competed successfully againstproducts or processes already in the market, servedas models for further innovations. Some examplesfrom the pharmaceutical industry are: the hypnotic

Ž .barbital VERONAL; 32 imitations , the diureticŽ .chlorthiazide DIURIL; 15 imitations , the antihyper-

Ž .tensive propranolol INDERAL; 24 imitations , andŽthe anxiolytic chlordiazepoxide LIBRIUM; 37 imi-

.tations . In this study, the term RI is used in thiswider sense.

The term II is applied to innovations designed onthe model of existing products or processes withtrivial differences in science, technology, materials,composition and properties and which, because ofthat, do not provide scope for further innovation byimitation. IIs are sometimes commercially successful

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 541

and are the vehicle par excellence for the diffusionof technologies among companies and countries.

3.3. The dynamic effects of RI

RIs play a capital role in the advances of bothscience and technology, in the establishment andgrowth of industrial sectors, in the diffusion of tech-nology, and in the technological and scientific com-petencies and market specialization of companies.

3.3.1. RI and the adÕance of science and technologyScience advances following its own mechanisms,

dynamics and pace, which are determined, on onehand, by the curiosity of scientists, the strength oftheir intellect, their ability to design and performexperiments, the precision of their observations, thedepth, scope and interpretative power of their theo-ries and, on the other hand, by the excellence ofacademic institutions and research schools, the qual-ity of their leadership, the financial support providedby the public and private sectors and the prestige thatacademic and research communities enjoy on thepart of society and the public at large.

Until the middle of the 18th century, scientists,with the exception of mathematicians, studied naturalphenomena and classified mineral, plant and animalspecies. When inventors began to transform theproperties of materials by chemical and physicalmethods and to introduce new forms of energy,scientists extended the scope of their interests to thestudy of man made phenomena as well. Science andtechnology were—and remain since—inexorablylinked together so that apart of its traditional mecha-nisms, scientific advance is also influenced by socialand economic forces.

The strongest links between science and technol-ogy were forged by RIs—commercializations of in-ventions and discoveries—introduced when the sci-entific knowledge on which they depended was onlypartially understood. Such RIs resulted frequently bytrial-and-error experimentation, by luck or serendip-ity and attracted the curiosity of scientists and engi-neers, who strived to discover the missing scientificprinciples that were responsible for the properties ofthe new products and the mechanisms of the newprocesses. Their efforts to that end led to the advanceof both science and technology and, in some in-stances, even to the creation of new scientific disci-

plines, e.g., the steam engine and thermodynamics,mauveine and synthetic organic chemistry, the tran-sistor and solid state physics. In the pharmaceuticalindustry, morphine and pharmacology, the rabiesvaccine and bacteriology, arsphenamine and chemo-therapy, and the process for recombinant DNA andbiotechnology are such examples.

For most of the 19th century, and even today,academic researchers who made such discoveries lefttheir development to others and pursued their aca-demic careers, as were, for example, the physiciansand academics who discovered the first anaesthetics,hypnotics and antiseptics. However, some amongthem with business acumen recognized the commer-cial opportunities created by their discoveries andinventions and established companies to develop theircommercial applications. Some of these en-trepreneurial companies became the first R&D-intensive companies and led to the orientation of asignificant segment of academic research towardssubjects related to technology. Examples: W. Perkinin the dyestuffs industry; J. Lawes in the fertilizerindustry; Th. Edison and A.G. Bell in the telecom-munications industry; and, in the pharmaceutical in-

Ž .dustry, P.J. Pelletier and J. Caventou quinine , G.Ž . Ž .Merck alkaloids , E.R. Squibb ether , R. Marker

Ž . Ž .corticosteroids , H. Boyer bioengineering .With the growth of capitalist economies in the

second half of the 19th century, companies that madeprofits from the development and commercializationof academic discoveries and inventions became in-terested in improving and standardizing the qualityof their products, in expanding their markets byintroducing new products, in ameliorating the yields,minimizing the operational costs and eliminatinglosses and accidents when running their processes.All this called for a better understanding of thescientific principles on which their innovations andoperations depended, hence the work undertaken inacademia out of curiosity and scientific interest wasof commercial interest for entrepreneurs and manu-facturers. These common interests caused the forgingof relations between academic researchers and indus-trialists as the latter, encouraged by the profits madefrom such RIs, did not hesitate to back their interestwith money. They began by employing leading aca-demic scientists and engineers as consultants but, asthe urgency for industrial results could not be met by

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588542

the normal pace of academic advance, they began tofund research projects in universities and polytech-nics, and ended by organizing inhouse R&D labora-tories that were frequently directed by universityprofessors and staffed by well-trained scientists andengineers. These activities created synergies betweenacademic and industrial interests, which had orientat-ing and accelerating effects in the direction andadvance of both science and technology.

The archetypal example of academia–industry co-operation is that of the German chemical companiesŽ .Beer, 1959 , which became R&D-intensive to de-velop synthetic dyes since the 1860s and whichapplied their expertise in synthetic organic chemistryfor the discovery and manufacture of drugs in the1880s. The pharmaceutical divisions of Bayer andHoechst were the first AmodernB pharmaceuticalcompanies and, by being adopted as models byEuropean and American manufacturing apothecaries,they helped shape the structure and practices of the

Žpharmaceutical industry Baumler, 1968; Verg, 1988;.Lesch, 1993 .

Apart from the commercialization of intra- andextra-mural discoveries and inventions, research-in-tensive companies play a leading role in the diffu-sion of technologies by the introduction of IIs. Incontrast to RIs, which require contributions fromleading scientists and engineers who work at theforefront of their disciplines, the science and technol-ogy of IIs follows the advancing frontier of therelevant disciplines at best by a margin equal to thelead time of the RI, which was the adopted modelbut usually by much longer intervals so that leadingresearchers are not keen in stepping back to developIIs. This task is, however, important for researchteams in industrial laboratories, which have eitherintroduced the original RI and want to strengthentheir position by exploiting their own leads or bycompetitors who strive to get a foot in a promisingmarket. In some instances, IIs prove superior to theoriginal models and become very successful com-mercially. For example, among AblockbusterB drugs,Glaxo’s anti-gastric ulcer ZANTAC was made on

Ž .the model of Smith, Kline and French’s SKFTAGAMET, and Merck’s antihypertensive VA-SOTEC on that of Squibb’s CAPOTEN.

Lastly, a discovery, which is not commercializedor does not succeed in the marketplace, may be

scientifically or therapeutically interesting but failsto gain the financial support from industry and tocreate competition among companies. Progress insuch cases follows the pace of scientific advanceuntil this or an improved RI gets the nod from themarket. Such was the case of penicillin between itsdiscovery in 1928 and the realization that it was an

Žeffective antibacterial for humans in 1941 Hare,.1970 .

3.3.2. RI and market performanceThe relation between originality and commercial

performance of innovations is one of the most impor-tant aspects of the dynamics of TI. Only a strongpositive relation of originality to profitability couldkeep open the channels of communication and coop-eration between centers of academic excellence andindustrial laboratories and the employment of out-standing scientists and engineers by industry. If thisrelation did not exist, the interaction of academic andindustrial research would have been haphazard andconsequential. A linear relation between science andtechnology would have, most probably, ensued, eachsystem obeying its own dynamics and pace withhardly any acceleration caused by the synergies ofinteraction.

Apart from these macroeconomic aspects, the re-lation between originality and market success is amajor concern for company R&D managers whofrequently have to ponder over whether to proceedwith the development of inhouse expertise, buildnetworks of cooperation with academic leaders andface the technological and financial uncertainties of aproject aiming at an RI rather than follow a competi-tor’s lead hoping that with a relatively modest in-vestment in men and means, an improvement to anexisting process or product may turn out to be moreprofitable.

There was much anecdotal information butscarcely any statistical evidence for the relation be-tween originality and market performance of innova-tions. To this end, we have carried out three studieson subsectors of the chemical and the pharmaceutical

Žindustries organic chemical intermediates, pesticides.and antibacterial medicines for each of which we

have identified all the innovations introducedŽthroughout their history Achilladelis, 1993;.Achilladelis et al., 1987, 1990 . We repeated this

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 543

Table 2The relation between originality and commercial performance ofinnovations

M OR

1 2 3 Total

PesticidesŽ . Ž . Ž . Ž .A 40% 36% 24% 100%34 31 21 85Ž . Ž . Ž . Ž .37% 22% 5% 13%Ž . Ž . Ž . Ž .B 17% 39% 44% 100%18 42 48 105Ž . Ž . Ž . Ž .20% 30% 12% 17%Ž . Ž . Ž . Ž .C 9% 15% 76% 100%39 68 338 445Ž . Ž . Ž . Ž .43% 48% 83% 70%

Ž .Total 100%89 140 405 634Ž . Ž . Ž . Ž .14% 22% 64% 100%

Organic intermediatesŽ . Ž . Ž . Ž .A 66% 28% 6% 100%118 50 11 179Ž . Ž . Ž . Ž .70% 25% 2% 22%Ž . Ž . Ž . Ž .B 18% 53% 29% 100%31 90 50 171Ž . Ž . Ž . Ž .19% 45% 11% 12%Ž . Ž . Ž . Ž .C 4% 12% 84% 100%20 58 393 471Ž . Ž . Ž . Ž .12% 30% 87% 57%Ž . Ž . Ž . Ž .Total 21% 24% 55% 100%169 198 454 821Ž . Ž . Ž . Ž .100% 100% 100% 100%

AntibacterialsŽ . Ž . Ž . Ž .A 61% 18% 21% 100%27 8 9 44Ž . Ž . Ž . Ž .64% 25% 7% 21%Ž . Ž . Ž . Ž .B 22% 28% 50% 100%8 10 18 36Ž . Ž . Ž . Ž .19% 31% 14% 18%Ž . Ž . Ž . Ž .C 6% 11% 83% 100%7 14 103 124Ž . Ž . Ž . Ž .17% 44% 79% 61%Ž . Ž . Ž . Ž .Total 20% 16% 64% 100%42 32 130 204Ž . Ž . Ž . Ž .100% 100% 100% 100%

CorticosteroidsŽ . Ž . Ž . Ž .A 56% 23% 21% 100%29 12 11 52Ž . Ž . Ž . Ž .66% 27% 15% 32%Ž . Ž . Ž . Ž .B 25% 41% 34% 100%8 13 11 32Ž . Ž . Ž . Ž .18% 30% 15% 20%Ž . Ž . Ž . Ž .C 9% 24% 67% 100%7 19 52 78Ž . Ž . Ž . Ž .16% 43% 70% 48%

Ž .Table 2 continued

M OR

1 2 3 Total

Ž . Ž . Ž . Ž .Total 27% 27% 46% 100%44 44 74 162Ž . Ž . Ž . Ž .14% 22% 64% 100%

CardioÕascularŽ . Ž . Ž . Ž .A 57% 17% 26% 100%40 12 18 70Ž . Ž . Ž . Ž .59% 20% 12% 26%Ž . Ž . Ž . Ž .B 23% 36% 42% 100%12 19 22 53Ž . Ž . Ž . Ž .18% 31% 16% 19%Ž . Ž . Ž . Ž .C 10% 20% 70% 100%16 30 105 151Ž . Ž . Ž . Ž .24% 49% 72% 55%Ž . Ž . Ž . Ž .Total 25% 22% 53% 100%68 61 145 274Ž . Ž . Ž . Ž .100% 100% 100% 100%

Central nerÕous systemŽ . Ž . Ž . Ž .A 43% 32% 25% 100%27 20 16 63Ž . Ž . Ž . Ž .59% 27% 13% 26%Ž . Ž . Ž . Ž .B 19% 40% 40% 100%9 19 19 47Ž . Ž . Ž . Ž .20% 26% 15% 19%Ž . Ž . Ž . Ž .C 7% 25% 67% 100%10 34 90 134Ž . Ž . Ž . Ž .21% 47% 72% 55%Ž . Ž . Ž . Ž .Total 19% 30% 15% 100%46 73 125 244Ž . Ž . Ž . Ž .100% 100% 100% 100%

OR: originality ranking:1 s radical; 2 s intermediate; 3 sincremental.M: market ranking: Asbig market success; Bsaverage; Csunsuccessful.The figure in bold characters indicates the number of productsclassified in each originalityrmarket rank. The upper percentage

Ž .figure refers to the horizontal row same market classification .ŽThe lower percentage figure refers to the vertical row same

.originality classification .

exercise for three subsectors of the pharmaceuticalindustry: corticosteroids, cardiovascular and CNSdrugs. Each innovation was then evaluated with thehelp of academic researchers and industrial managersin terms of originality and market performance on a

Ž . Ž . Ž .three level scale: RI 1 , intermediate 2 , and II 3 ;Ž . Ž .commercially successful A , intermediate B and

Ž .modest or failure C . The data are presented inTable 2. They show a statistically significant positive

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588544

relation of originality with commercial success, andof triviality with modest market performance or fail-ure. RIs, which represent about 20% of the innova-tions of each subsector, appear to have a greaterchance to succeed commercially: about 60% of themwere market successes and only 10% were modestmarket performers or failures. On the other hand, IIs,which represent about 60% of all innovations, wereusually commercially unsuccessful: about 70% ofthem were poor market performers and only 10–15%were commercially successful.

This relation lies at the heart of the dynamicfunction of RI in a capitalist economy as companiesleading in science and technology have a betterchance to be rewarded for their commitment.

3.3.3. The diffusion of technology: RI, TPs and TTsThe hypotheses proposed by Rosenberg, Nelson

and Winter, and Dosi about TPs and TTs offered anumber of plausible mechanisms regarding the ad-vance and diffusion of technologies and their interac-tions with the economy. The scarcity, however, ofquantitative empirical evidence led to a proliferationof related hypotheses regarding the microeconomicmechanisms by which science and technology ad-vance under a multitude of economic and marketconditions and on how the accelerating synergies andthe decelerating bottlenecks, which characterize thedynamics of TI, form and exert their influence.

To a great extent, the scarcity of empirical quanti-tative evidence was due to the lack of appropriatetechnology output indicators, which are indispens-able for the systematic testing of the proposed micro-and macro-economic hypotheses of technical change.The study of the technological and business history

Ž .of an industrial sector or subsector , the identifica-tion of all its innovations, the evaluation of theiroriginality and commercial success and their distri-bution over time offer an extremely useful tool forthat purpose. They provide a precise description ofthe rate of technical change, of the volume andquality of innovation of an industrial sector, andallow for comparisons of the innovation record, tim-ing, period of commitment and commercial perfor-mance of individual companies and countries.

A TP, defined as a model for the solution ofŽ .related technological problems Dosi, 1982 , was, in

most cases in the pharmaceutical industry, either aŽ .commercially successful radical innovation RIrMS ,

which was introduced when the scientific and medi-cal principles on which it depended were not com-pletely elucidated and offered a robust and versatilemodel for imitation, or a radical process innovation,which made possible the discovery or developmentof numerous drugs in one or more therapeutic cate-gories. Examples of the first case include: cortisoneŽ .CORTONE, Merck, 1948 in corticosteroids, barbi-

Ž .tal VERONAL, Bayer, 1903 in barbiturate hyp-notics; propranolol, the first beta adrenergic blockerŽ .INDERAL, ICI, 1964 in antihypertensives; chlor-

Ž .promazine LARGACTIL, Rhone Poulenc, 1952 inˆŽtranquilizers; chlordiazepoxide LIBRIUM, Roche,

. Ž1960 , in anxiolytics. For more examples, see Table.3 . Examples of the second case include: the chemi-

cal processes for the isolation and purification ofalkaloids, which led to the development of manydrugs for a score of therapeutic uses, such as mor-phine, quinine, papaverine, codeine, noscapine, etc.;the process of screening soil samples for the identifi-cation of fungal metabolites with antibacterial prop-erties and the process of deep aerobic fermentation,which made possible the industrial production ofpenicillin and the discovery of a score of antibiotics,such as streptomycin, tetracycline, chloramphenicol,erythromycin, etc., which have nothing in commonin terms of structure or composition. Fermentationprocesses for the production of 6-aminopenicillanicacid and 7-aminocephalosporanic acid made possiblethe manufacture of a wide range of semisyntheticpenicillins and cephalosporins. The processes forrecombinant DNA and cell fusion opened the bio-technology era for the pharmaceutical industry andled to biosynthetic proteins, such as human insulinand growth hormone, antineoplastic drugs and diag-nostics.

It should be noted that there are many commer-cially successful RIs that cannot be imitated fortechnological reasons as was the case of vitamins,centrally acting antihypertensives, e.g., methyl DOPAŽ . ŽALDOMET, Merck, 1961 , clonidine CATA-

.PRESS, Boehringer, 1966 , and antineoplastic drugs,Ž .e.g., tamoxifen NOLVADEX, ICI, 1971 and cis-

Ž .platin PLATINOL, Bristol, 1978 . Thus, the tech-nology of an industrial sector or subsector advancesby both paradigms and by innovations unrelated to

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 545

Table 3Ž .Generations, clusters of technologies, and radical innovations in the pharmaceutical industry 1800–1995

Generations Technologies First radical Year Company Countryinnovations

Ž .First 1 Alkaloids Morphine 1806 – GEŽ .1802–1880 Quinine 1820 – FR

Ž .2 Organic chemicals Ether 1842 – USAŽ .Second 1 AnalgesicsrAntipyretics Phenazone ANTIPYRIN 1884 HOECHST GE

Ž .1880–1930 Acetanilide ANTIFEBRIN 1886 KALLE GEŽ .2 Hypnotics Sulfonmethane SULFONAL 1888 BAYER GE

Barbital VERONAL 1903 BAYER GEŽ .3 Biologicals Anthrax vaccine 1881 – FR

Diphtheria serum 1890 HOECHST GEŽ .4 Local anesthetics Cocaine 1860 – GErAUS

Orthocaine ORTHOFORM 1896 HOECHST GEŽ .5 Antiprotozoal Arsphenamine SALVARSAN 1911 HOECHST GEŽ .Third 1 Vitamins Ergosterol PRO-VITAMIN D 1927 – GE

Ž .1930–1960 Retinol VITAMIN A 1931 ROCHE SWAscorbic acid VITAMIN C 1934 ROCHE SW

Ž .2 Sex hormones Estrone – 1931 PARKE-DAVIS, USrGESCHERING

Testosterone – 1935 PARKE-DAVIS, USrGErSCHERING, NErSWORGANON

Ž .3 Sulphonamides Sulphamido- PRONTOSIL 1935 BAYER GEchrysoidine

Ž .4 Antihistamines Phenbenzamine ANTEGRAN 1942 RHONE FRŽ .5 Antibiotics Penicillin PENALEN 1943 MERCK, PFIZER USŽ .6 Corticosteroids Cortisone CORTONE 1948 MERCK USŽ .Fourth 1 Antihypertensiverdiuretics Chlorothiazide DIURIL 1958 MERCK US

Ž . Ž .1960–1980 2 Antihypertensive B-blockers Propranolol INDERAL 1964 ICI UKŽ .3 CNS drugs Chlorpromazine LARGACTIL 1952 RHONE FRŽ .4 Tranquilizers Haloperidol HALDOL 1958 JANSSEN BEŽ .5 Antidepressants Imipramine TOFRANIL 1959 GEIGY SWŽ .6 Anxiolytics Chlordiazepoxide LIBRIUM 1960 ROCHE SWŽ .7 Semisynthetic antibiotics Phenethicillin BROXIL 1959 BEECHAM UK

Cephalothin KEFLIN 1964 LILLY USCephaloridine CEPORIN 1964 GLAXO UK

Ž .8 Non-steroid antiinflammatory Phenyl butazone BUTAZOLIDIN 1952 GEIGY SWŽ .drugs NSAIDS Ibuprofen BRUFEN 1964 BOOTS UK

Indomethacin INDOCID 1964 MERCK USŽ .9 Oral contraceptives Mestranolr ENOVID 1961 SEARLE US

norethynodrelŽ .Fifth 1 Calcium ion channel antagonists Nifedipine ADALAT 1974 BAYER GE

Ž . Ž .1980–1993 2 ACE inhibitors Captopril CAPOTEN 1977 SQUIBB USŽ .3 Hypolipidemics Lovastatin MEVACOR 1987 MERCK USŽ .4 Serotonin inhibitors Methysergide SANSERT 1962 SANDOZ SWŽ .5 Anti-Parkinson Carbidopa SINEMET 1967 MERCK US

Bromocryptine PARLODEL 1978 SANDOZ SWŽ .6 Anti-nausea Domperidone MOTILIUM 1979 JANSSEN BEŽ .7 Gastric and duodenal ulcers Cimetidine TAGAMET 1976 SKF USŽ .8 Antiviral Acyclovir ZOVIRAX 1982 WELLCOME UKŽ .9 Biotechnology Human insulin HUMULIN 1983 GENENTECHr US

LILLYSomatrem PROTROPIN 1985 GENENTECH US

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588546

them. The greater the contribution of paradigms, theŽfaster the advance e.g., in the case of CNS drugs,

.antihistamines and corticosteroids because the pres-ence of versatile models for imitation reduces thedependence of innovating firms on further discover-ies, inventions or advances in academic science,which are less predictable and more difficult to comeŽe.g., antihypertensives up to the late 1950s and of

.antineoplastic drugs .TTs, defined as the patterns of problem solving

Žactivities, i.e., of progress based on a TP Dosi,.1982 , describe the rate of diffusion of technologies.

They are initiated by a commercially successful radi-Ž .cal innovation RIrMS , which is followed by many

other RIs and IIs. Robustness and versatility of theoriginal RIrMS, the size of the market and thenumber of competing companies determine the ex-tent to which the model will be imitated, i.e., thestrength and time span of the TT.

The distribution of innovations over time providesan accurate profile of a TT because the totality ofinnovations introduced up to any moment in timerepresents the progress of a technology made thatfar. Even the stock of academic research and of tacit

knowledge accumulated by researchers and compa-nies is embodied in the innovations, while this is notthe case when using other R&D output indicators,such as scientific papers or patents.

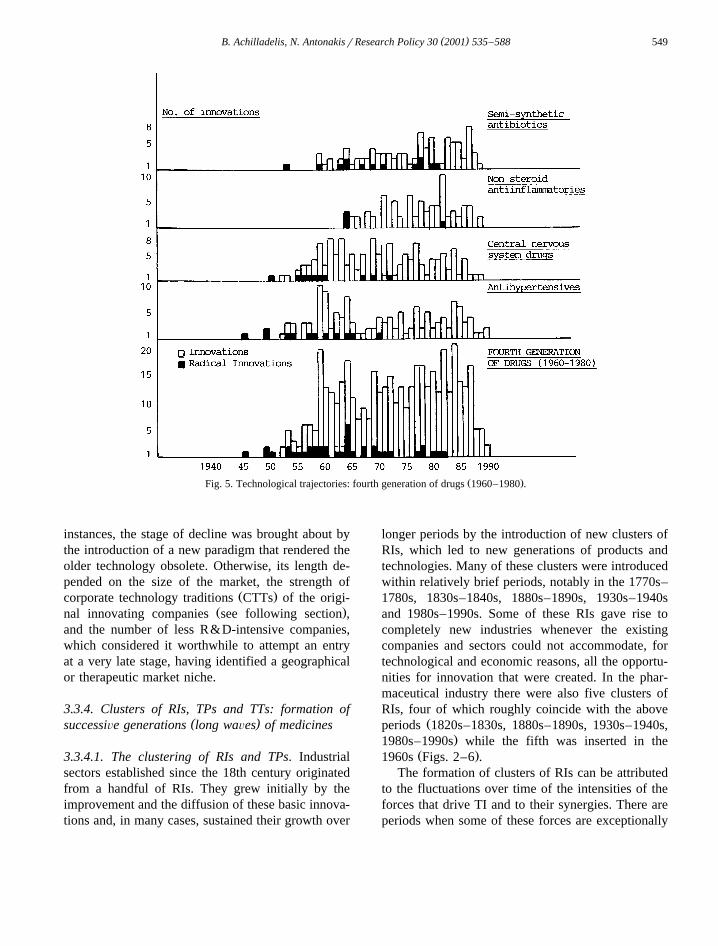

Figs. 2–6 present the most important TTs of thepharmaceutical industry traced by the distributionover time of the RIs and IIs related to each TP. Theyare arranged chronologically in the order of the fiveconsecutive generations of drugs, which are profiledby integrating the corresponding TTs. Fig. 7 showsthe overlap of the last three generations of drugsŽ .1930–1990 . Lastly, Fig. 8 shows the distributionover time of all RIs and IIs whether they belong toTTs or not. All TTs are roughly bell-shaped butshow important differences among them caused bythe changing intensities of the driving forces. Forexample, the time span varies from nearly 80 yearsfor the TTs of the first two generations to about 50years for the TTs of the next two generations, whilethose of the last generation have not yet run their fullcourse. However, even among contemporary TTs,some have a shorter span either because of very fastdiffusion of the technology due to inadequate patentprotection, e.g., antihistamines and corticosteroids,

Ž .Fig. 2. Technological trajectories: first generation of drugs 1820–1880 .

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 547

Ž .Fig. 3. Technological trajectories: second generation of drugs 1880–1930 .

or because a new paradigm rendered the technologyobsolete, e.g., corticosteroids.

TTs are divided into four rather distinct stages:Ž .a The stage of youth, shown by the early, nearly

flat part of the curve, was usually of short durationand was characterized by a few, mostly radical,innovations. Unless the new technology addressed apreviously untreatable disease, e.g., Salvarsan forsyphilis, market demand was usually weak at thatstage because of the familiarity of the medical pro-fession with drugs already in the market, e.g., thecase of penicillin in 1942 following the introduction

Ž .of antibacterial sulphonamides 1935 . Pharmaceuti-cal companies were, however, aware of both thesocietal need and the potential of a therapeuticmarket from national and worldwide health statistics.The stage of youth ended by the introduction of a

Ž .commercially successful radical innovation RIrMS ,which triggered the process of imitation by the inno-vating company and its competitors.

Ž .b The stage of growth is represented by thesharply rising part of the bell-shaped curve. It is

characterized by a sharp increase in the number ofinnovating companies and innovations many of whichare RIs because TPs were usually sufficiently versa-tile to offer opportunities for radical departures, notonly for IIs. Many of them were also commerciallysuccessful because the markets were rapidly expand-ing. Competing companies tried to improve the ther-apeutic effectiveness of the original drug, to elimi-nate side effects, to develop better manufacturingprocesses and to circumvent patent barriers. Most

Ž .RIs and market successful drugs MSs of a TT wereintroduced at that stage and the technology expandedalong unexpected directions hardly envisaged by theoriginal innovators. The strength of the stage ofgrowth determined to a considerable extent the lengthof the span of the TT, the size and diversity of themarkets and the leading companies of the sector.

Whenever patent protection was particularly ef-fective andror when only few companies could takeadvantage of the opportunities opened by the TPbecause of low R&D intensity in the industry as a

Ž .whole 1820–1920 , the stage of growth spread over

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588548

Ž .Fig. 4. Technological trajectories: third generation of drugs 1930–1960 .

decades rather than years. Thus, the stages of matu-rity and decline of the second generation of drugswas located in the 1940s and beyond, i.e., whencompetition sharpened by the entry of many R&D-intensive companies. On the contrary, the span of theTTs of the third and fourth generations was muchshorter because of the presence at the time of theirintroduction of many R&D-intensive companiesŽ .Section 4 .

Ž .c The stage of maturity is represented by therather flat segment of the TT during which thenumber of innovations introduced annually reachesand passes its peak. Most innovations were incre-mental as the potential of the technology was by thenlargely exhausted. The numerous IIs represent theefforts of latecomer, less expert, companies, whichstrived to gain entry in a vigorous market which bythen was reaching its peak. Depending on the size ofthe market, some of these IIs became commerciallysuccessful. In many cases, the patents of the originalinnovations expired at that stage facilitating the entry

of less expert companies as shown by the vigor ofthe Abandwagon effectB, i.e., the number of compa-nies entering the market with an own innovationŽ .Fig. 9 . The length of this stage depends primarilyon the size of the market which, as the technology isby then unable to create new radical departures,provides the only initiative for companies already inthe market to pursue their R&D and innovation inthat area, or for newcomers to attempt an entry inthat market despite the established position of theearly innovators. The modest commercial perfor-

Ž .mance of IIs Table 2 can be attributed to theirlaunching at the later stages of TTs when the leadingdrugs were well established in the market and weredifficult to dislocate by newer products most ofwhich did not offer substantial therapeutic advan-tages.

Ž .d The stage of decline is represented by the tailsegment of the bell-shaped curve and is character-ized by a drastic reduction in the number of innova-tions and the absence of both RIs and MSs. In many

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 549

Ž .Fig. 5. Technological trajectories: fourth generation of drugs 1960–1980 .

instances, the stage of decline was brought about bythe introduction of a new paradigm that rendered theolder technology obsolete. Otherwise, its length de-pended on the size of the market, the strength of

Ž .corporate technology traditions CTTs of the origi-Ž .nal innovating companies see following section ,

and the number of less R&D-intensive companies,which considered it worthwhile to attempt an entryat a very late stage, having identified a geographicalor therapeutic market niche.

3.3.4. Clusters of RIs, TPs and TTs: formation of( )successiÕe generations long waÕes of medicines

3.3.4.1. The clustering of RIs and TPs. Industrialsectors established since the 18th century originatedfrom a handful of RIs. They grew initially by theimprovement and the diffusion of these basic innova-tions and, in many cases, sustained their growth over

longer periods by the introduction of new clusters ofRIs, which led to new generations of products andtechnologies. Many of these clusters were introducedwithin relatively brief periods, notably in the 1770s–1780s, 1830s–1840s, 1880s–1890s, 1930s–1940sand 1980s–1990s. Some of these RIs gave rise tocompletely new industries whenever the existingcompanies and sectors could not accommodate, fortechnological and economic reasons, all the opportu-nities for innovation that were created. In the phar-maceutical industry there were also five clusters ofRIs, four of which roughly coincide with the above

Žperiods 1820s–1830s, 1880s–1890s, 1930s–1940s,.1980s–1990s while the fifth was inserted in the

Ž .1960s Figs. 2–6 .The formation of clusters of RIs can be attributed

to the fluctuations over time of the intensities of theforces that drive TI and to their synergies. There areperiods when some of these forces are exceptionally

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588550

strong and exert powerful pressures on innovatinginstitutions causing the introduction of numerous RIssome of which have the qualities—robustness, versa-tility, commercial appeal—which lead to the initia-tion of TTs. Among driving forces, those whichshow abrupt changes in intensity are: scientificrtechnological advance, new materials and govern-ment legislation.

3.3.4.2. Scientific adÕance. For the pharmaceuticalindustry that thrived on a two-way vigorous relationwith chemistry, the life sciences and medicine, scien-tific advance was the major driving force for all five

Ž .clusters Section 4 . Science and technology advanceby quantum jumps, which are followed by periods ofless adventurous steps along the established path-ways. Such discontinuities are not caused only by thescientific revolutions of historical dimensions de-

Ž .scribed by Kuhn 1962 but also by the gradualaccumulation of knowledge, which at certain mo-ments in time makes possible the understanding of agroup of previously incomprehensible phenomena,by the introduction of novel scientific instruments

that make possible the observation and study of agroup of natural and man made phenomena, and bythe interaction and cross-fertilization of disciplines,which open new horizons for study and interpreta-tion. TPs are closely associated with the advancingfrontier of scientific disciplines so that periods ofrevolutionary advance create opportunities for moreTPs than do periods of evolutionary advance.

Raw materials are, perhaps, the most obviousdriving force that cause clustering of RIs: cottonŽ . Ž .1770s , coal and cheap steel 1830s , coal tarŽ . Ž .1880s , oil and petrochemicals 1930s , have allcreated clusters of TPs and new R&D-intensiveindustries. In the case of the pharmaceutical industry,

Ž .tropical medicinal plants 1820s and coal tar derivedŽ .organic chemicals 1880s have contributed to the

corresponding clusters of TPs.GoÕernment legislation has led to clustering of

RIs particularly when it was related to armed con-flicts or the preparation for war but in the case of thepharmaceutical industry, because of its relevance topublic health, it contributed also during peacetime.The establishment of public medical research labora-

Ž .Fig. 6. Technological trajectories: fifth generation of drugs 1980–1993 .

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 551

Ž .Fig. 7. Overlap of successive Along wavesB third, fourth, and fifth generations of drugs up to 1990 .

Ž .tories 1880s , funding of the wartime projects forŽ .penicillin, malaria, and corticosteroids 1940s , the

Ž .patenting of drugs Germany, 1880s , of naturalŽ .antibiotics USA, 1940s and of bioengineered pro-

Ž .teins USA, 1980s have all contributed to the clus-tering of RIs and TPs.

3.3.4.3. The clustering of TTs: successiÕe genera-( )tions A long waÕesB in the pharmaceutical indus-

try. The trajectories that technologies follow beyondtheir stage of youth are determined by the qualitiesof the TPs, the inherent properties of each technol-ogy and by the driving forces for TI, which exert

ŽFig. 8. Distribution of innovations, radical innovations, and innovations related to technological trajectories over time 3-year moving.average .

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588552

Fig. 9. ABandwagon effectB: technological trajectories and first entry of companies by an own innovation.

their influence throughout their span, in particular,by market demand and competition which becomeincreasingly important at the later stages of the TTs.Thus, many of the technologies that are launchedwithin brief periods are likely to follow paralleldiffusion patterns, i.e., TTs cluster together through-out their span, because innovating institutions areexposed to the influence of a homogeneous commer-cial and competitive environment, or, in other words,

Ž .to driving forces of similar intensities Figs. 2–7 .Whenever such a cluster of TTs is formed within

a particular industry, it dominates its technologicaland commercial development. The coincidence oftheir stages of growth and maturity creates waves ofradical and particularly of IIs, a fast growth ofmarket demand, a powerful Abandwagon effectB andthe industry as a whole expands and flourishes.When they reach the stage of decline, they followone of two alternative pathways depending on the

rate of advance of the scientific disciplines and thetechnologies on which the industry depends: either anew cluster of RIs is introduced and the industry isregenerated by riding a new wave of innovation andcommercial expansion, or it becomes a technologi-cally mature sector with declining profitability andan oligopolistic market due to the dropping out ofmany companies and the merger of the rest into fewlarge, less R&D-intensive companies.

There was considerable overlap between succes-Ž .sive clusters of TTs Fig. 7 and substantial depen-

dence of the more recent TTs on their predecessorsbecause of the cumulative character of scientific andtechnological knowledge and of the common mar-kets they addressed. However, the clustering of RIsand TTs and the formation of successive generationsof drugs is clearly documented by the patterns ofdistribution of innovations, the identification of thescientific and technological advances that caused the

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 553

emergence of the newer and the obsolescence of theolder technologies, and by significant changes in thecompetitive environment of the pharmaceutical in-dustry that were associated with the successions of

Ž .generations Section 4 . These characteristics and thecoincidence in the timing of introduction of four outof the five generations of drugs with those of theAlong wavesB of world economic growth indicatethat the pharmaceutical industry has followed thegeneral pattern of economic development as de-scribed by macroeconomic theory but showed anexceptional flexibility and adaptability, which en-sured its survival as one of the most innovative andprofitable businesses.

As in the case of Along wavesB, the transitionfrom generation to generation required considerableskills and ingenuity on the part of individual pharma-ceutical companies that were forced to drop tradi-tional products, technologies and markets to developnew ones and adapt to new competitive settings.Those companies that failed to make these adjust-ments lost their competitive edge and either mergedwith or were acquired by their more successful com-petitors.

3.4. The pharmaceutical firm as innoÕating institu-( )tion Corporate Technology Traditions CTTs

3.4.1. Corporate technology traditionsA common characteristic of companies in R&D-

intensive industries is that they tend to specialize infew technologies on which they rely for the develop-

Ž .ment of their new products. Pavitt 1984 attributedthis phenomenon to a process of knowledge accumu-lation in industrial firms: A.industrial firms cannotand do not identify and evaluate all innovation possi-bilities indifferently, but are constrained in theirsearch by their existing knowledge and skills toclosely related zonesB. We propose that the synergiesof the driving forces of TI, and the dynamic effectsof RIs and TTs provide a plausible explanation ofhow and why this happens.

External driving forces are effective only to theextent that they generate internal forces within theinstitutions that foster innovation: private companiesfirst and foremost and then academic institutions,government research laboratories, public and privatenot for profit research institutions. The research-in-

tensive pharmaceutical firm is the most effectiveagency for TI because it is sensitive and able torespond to the stimuli of all the driving forces; it isespecially sensitive to market demand and competi-

Ž .tion Fig. 1 .Research-intensive companies respond to external

stimuli by the investment of capital for the develop-ment of new products and processes in anticipationof sizable returns from their commercialization.Making profit is the Araison d’ etreB of a capitalistˆenterprise so that however strong the external stimuliand the conviction of company managers that R&Dand innovation are essential for survival in the com-petitive setting of an R&D-intensive industry, theywill not support for long—and may eventually re-treat from the sector—unless the company’s cashflow can provide for the required investments. Com-pany R&D budgets are not determined by expecta-

Ž .tions but by the size of cash flow Section 3.4.3 .As shown in Table 2, RIs are more frequently

commercially successful than IIs and, hence, moreprofitable, so that innovating companies can spendmore on further R&D to perpetuate their advantagethan competitors who introduce IIs. However, theintroduction of an RI has another important conse-quence: although it is a company’s response to thestimulus of external driving forces, once launched, itintensifies rather than satisfies them. It has beenargued earlier that the introduction of a commer-

Ž .cially successful radical innovation RIrMS exertsan orientating effect on scientific or technologicaladvance, strengthens market demand and sharpenscompetition. Thus, the innovating company findsitself under stronger pressure to pursue R&D andinnovation in the same technology and market afterrather than before the introduction of the RI. This isan important, but not the only, reason that leadsresearch-intensive companies to specialize in sci-ence, technology and markets.

Apart from intensifying the AenvironmentalB driv-ing forces, RIrMSs when introduced at the earlystages of a TT, create a powerful internal drivingforce within innovating companies, which stronglyinfluences their subsequent R&D, innovation andmarkets. We have called this driving force a ACTTBŽ .Achilladelis, 1973; Achilladelis et al., 1987, 1990and defined it as AA company’s specialization in atechnology, its underlying science and the markets of

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588554

the products derived from it, achieved by an earlycommercially successful RI and followed by theconcentration of its resources, the specialization ofits staff and the introduction of many technologicallyrelated innovations over a very long period of timeranging from 20 to 40 yearsB.

The strong, post innovation, commitment to moreR&D leads, on one hand, to the concentration of thecompany’s finite R&D resources on one or a fewareas depending on its R&D budget and creativity atthat time and, on the other hand, to an accumulationof knowledge and experience, including markets andmarketing. This expertise creates opportunities forthe improvement of the original innovation by IIsand even by further RIs.

This drive for further innovation is caused by theemergence of the following strong corporate forces.

3.4.1.1. Scientific leadership. The underlying scienceof an RIrMS introduced at an early stage of a TT isusually close to the advancing frontier of the relevantscientific disciplines so that company researchers,encouraged by their success and the availability offunds, deepen and widen their knowledge and, inmany instances, come to be recognized by theiracademic and industrial peers as authorities in theirdisciplines. This distinction is appreciated by bothresearchers and managers who project it as proof ofthe company’s technological leadership and are ea-ger to nurse and to maintain it for as long as it ispossible.

3.4.1.2. Influence on top management. Innovatorsand managers associated with an original and lucra-tive innovation are usually promoted to positions ofinfluence from which they steer the company’s inno-vative efforts towards technologies and markets withwhich they are most familiar.

3.4.1.3. Time lag. As R&D begins on average 8–10years before commercialization of an RI, companiesare eager to consolidate their position by introducingIIs with improved properties before their competitorscover that lag and become able to compete.

3.4.1.4. Familiarity with markets. Early commercial-ization of an RI requires the opening of a new or thedevelopment of an existing market, which lead to

specialization of company marketingrsales depart-ments, a feature particularly important in the phar-maceutical industry whose markets are global andthe investments required for that purpose immense.Feedback from users and the medical professionleads to market expansion by the design of IIs withimproved properties.

3.4.1.5. Economies of size and scope. Cash flowcreated by an RIrMS leads to further investments inR&D, manufacturing capacity and marketingrsales,which create economies of size and scope. Theselection of subsequent R&D projects whose costcan be cut by sharing accumulated knowledge, re-search facilities and marketing networks, becomeseasier and leads, in turn, to further specializationŽ .Henderson and Cockburn, 1996 .

3.4.1.6. The A inÕented hereB syndrome. Companiesshow a strong tendency to pursue their own leadsrather than those of their competitors. This is fre-quently the case of very innovative firms.

The resultant of these forces is the establishmentof CTTs that acquire their own momentum so thatover periods ranging from 20 to 40 years, a dispro-portionate number of innovations result from thesame technology. Although the originality of allthese innovations cannot be high, some are commer-cially successful and help perpetuate the CTT.

The study of innovations in subsectors of thepharmaceutical industry shows that leading compa-nies in each one of them have all introduced RIrMSat the early stages of the corresponding TTs andhave created long lasting CTTs by which they gained

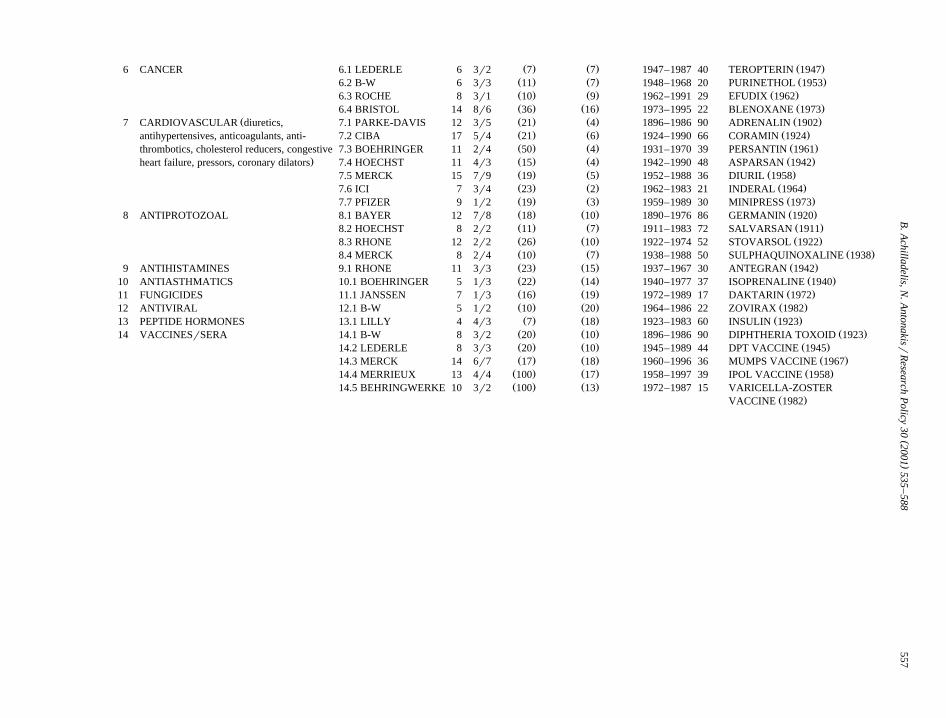

Ž .important competitive advantages Tables 4, 5 . Table5 lists all the CTTs that we identified in the thera-peutic sectors reviewed in this paper.

3.4.2. CTTs, TTs and the A riding B of A long waÕesBMany innovations of a CTT belong to a particular

TT and it may be said that they represent that part ofthe TT, which was appropriated by a particularcompany. The strength of this relation is manifestedby the fact that although companies innovate insuccessive TTs within a therapeutic market, theyseldom introduce the TP that launches the newerTTs. The blurred sensitivity of companies with CTTs

()

B.A

chilladelis,N.A

ntonakisrR

esearchP

olicy30

2001535

–588

555

Table 4Ž . w Ž . Ž . Ž .xTop innovating companies 1880–1992 innovations, radical innovations RIs , market successes MSs and the contribution of corporate technology traditions CTTs

No. Company Country 1880–1930 1930–1960 1960–1980 1980–1992 Total CTTs

No Innvs RI MS No Innvs RI MS No Innvs RI MS No Innvs RI MS No Innvs RI MS No of Innvs of % of totalCTTs CTTs Innvs

Ž .1 CIBA-GEIGY SW 2 0 2 48 19 14 23 8 8 9 1 1 82 28 25 5 61 74Ž .2 ROCHE SW 3 0 1 30 12 8 25 4 7 24 4 4 82 20 20 5 50 61Ž .3 MERCK US – – – 33 17 18 30 14 15 16 7 10 79 38 43 7 60 75Ž .4 HOECHST GE 19 8 8 12 3 5 24 4 6 18 2 2 73 17 21 3 31 42Ž .5 BAYER GE 25 11 11 19 6 11 16 6 4 6 2 1 66 25 27 3 39 60Ž .6 LILLY US 5 4 4 15 8 6 28 8 10 10 5 4 58 25 24 2 18 31Ž .7 PARKE DAVIS US 6 3 3 21 6 7 22 3 6 8 0 2 57 12 18 1 12 21

a Ž .8 B-W UK 8 3 3 20 8 6 9 3 3 14 2 2 51 16 14 3 19 38Ž .9 PFIZER US – – – 18 4 7 22 5 7 7 3 1 47 12 15 2 24 51Ž .10 RHONErM&B FR 3 1 1 27 11 10 14 2 0 2 0 0 46 14 11 2 23 50Ž .11 UPJOHN US – – – 19 5 5 18 5 4 7 3 1 44 13 10 1 14 32Ž .12 JANSSEN BE – – – 4 1 1 28 4 5 12 0 3 44 5 9 3 34 77Ž .13 LEDERLE US – – – 27 14 12 11 1 2 3 0 1 41 15 15 3 26 63Ž .14 BRISTOL US – – – 7 2 1 19 6 4 13 2 3 39 10 8 2 29 74Ž .15 SANDOZ SW 1 1 1 8 2 0 17 1 2 12 3 4 38 7 7 1 13 34Ž .16 ABBOTT US 8 0 2 12 3 3 13 6 0 3 0 0 36 9 5 1 14 39

17 STERLING US – – – 13 0 4 15 1 3 6 0 0 34 1 7 – – –18 SCHERING US – – – 14 4 8 9 2 2 10 3 0 33 9 10 – – –

Ž .19 GLAXO UK – – – 11 3 2 13 4 4 8 2 4 32 9 10 1 8 25b20 AHP US – – – 9 0 1 15 0 3 7 1 1 31 1 5 – – –

c Ž .21 ICI UK – – – 13 3 4 12 6 4 5 0 2 30 9 10 1 7 23d22 SKF US – – – 13 3 9 14 3 4 1 0 0 28 6 13 – – –

23 SQUIBB US – – – 13 6 7 9 4 3 4 2 2 26 12 12 – – –Ž .24 SCHERING AG GE 4 4 0 10 7 4 11 0 0 1 1 0 26 12 4 1 16 61

25 MERRELL-DOW US – – – 9 0 0 8 1 0 6 1 1 23 2 1 – – –Ž .26 BOEHRINGER GE 1 0 – 6 1 2 13 2 6 2 0 0 22 3 8 2 16 73Ž .27 SYNTEX US – – – 8 3 2 8 0 4 6 0 0 22 3 6 1 16 72Ž .28 BEECHAM UK – – – 2 1 0 11 2 2 8 2 1 21 5 3 1 15 71Ž .29 SEARLE US – – – 8 3 4 8 1 4 1 0 0 17 4 8 1 9 53Ž .30 ORGANON NE – – – 6 3 3 7 0 1 1 0 0 14 3 4 1 11 78

a Burroughs-Wellcome.bAmerican Home Products.c Imperial Chemical Industries, Zeneca since the 1980s.dSmith Kline French.

()

B.A

chilladelis,N.A

ntonakisrR

esearchP

olicy30

2001535

–588

556

Table 5Ž .Corporate technology traditions CTTs by therapeutic sector

No. Sector Company Innovations Commitment First RIrMS

No. RIrMS % of company % of sector Period Yearsinnovations innovations

Ž . Ž . Ž .1 ANALGESICSrANTIPYRETICS 1.1 HOECHST 12 3r5 16 9 1882–1981 99 ANTIPYRIN 1884Ž . Ž . Ž .1.2 MERCK 6 2r5 7 4.5 1945–1979 34 MYOCRISIN 1945Ž . Ž . Ž .1.3 CIBA 6 1r1 7 4.5 1950–1976 26 BUTAZOLIDIN 1952Ž . Ž . Ž .1.4 ROCHE 8 1r1 10 6 1946–1982 36 DROMORAN 1946Ž . Ž . Ž .1.5 JANSSEN 7 1r2 16 5 1958–1984 26 PALFIUM 1958

Ž Ž . Ž . Ž .2 ANTIBACTERIALS Sulphonamides, 2.1 BAYER 11 4r5 16 5 1935–1985 50 PRONTOSIL 1935. Ž . Ž . Ž .Antibiotics, Synthetics 2.2 MERCK 13 9r5 16 6 1939–1986 47 PENICILLIN 1943

Ž . Ž . Ž .2.3 LEDERLE 12 4r5 30 6 1940–1987 47 AUREOMYCIN 1948Ž . Ž . Ž .2.4 PFIZER 15 5r6 32 7 1943–1986 43 PENICILLIN 1943Ž . Ž . Ž .2.5 LILLY 14 8r7 24 7 1952–1983 31 ILOTICIN 1952Ž . Ž . Ž .2.6 GLAXO 8 4r5 25 4 1955–1987 32 SEPORAN 1964Ž . Ž . Ž .2.7 BRISTOL 15 2r1 38 7 1956–1987 31 TETREX 1956Ž . Ž . Ž .2.8 BEECHAM 15 4r3 70 7 1959–1985 26 BROXIL 1959Ž . Ž . Ž .3 VITAMINS 3.1 ROCHE 5 4r4 5 35 1934–1978 44 VITAMIN C 1934Ž . Ž . Ž .3.2 MERCK 4 4r4 5 25 1937–1949 12 VITAMIN B1 1937Ž . Ž . Ž .4 SEX HORMONESrCORTICOSTEROIDS 4.1 CIBA 14 8r4 17 10 1934–1973 39 PROGESTERONE 1934Ž . Ž . Ž .4.2 SCHERING AG 16 7r4 61 11 1931–1977 46 PROGYNON 1931Ž . Ž . Ž .4.3 ORGANON 11 3r4 78 8 1920–1975 55 OVARIAN EXTRACT 1920Ž . Ž .4.4 SYNTEX 16 3r5 73 11 1944–1981 37 PROGESTERONE FROM

Ž .DIOSGENIN 1944Ž . Ž . Ž .4.5 SEARLE 9 3r5 53 6 1951–1965 14 NILEVAR 1955Ž . Ž .4.6 UPJOHN 14 3r4 32 10 1935–1979 44 CORTISONE FROM

Ž .PROGESTERONE 1952Ž Ž . Ž . Ž .5 CNS MEDICINES anesthetics, hypnotics, 5.1 BAYER 13 3r5 20 4 1888–1996 78 SULPHONAL 1888

Ž . Ž . Ž .antidepressants, anxiolytics, neuroleptics, 5.2 ABBOTT 14 1r3 40 5 1922–1977 55 NEONAL 1922. Ž . Ž . Ž .anti-Parkinson, antiemetics 5.3 CIBA-GEIGY 11 5r4 13 4 1945–1977 32 RESERPINE 1953

Ž . Ž . Ž .5.4 ROCHE 24 4r5 30 8 1948–1989 41 MARSILID 1957Ž . Ž . Ž .5.5 SANDOZ 13 2r2 34 4 1952–1992 40 SANSERT 1962Ž . Ž . Ž .5.6 JANSSEN 20 3r3 45 7 1958–1988 30 HALDOL 1958

()

B.A

chilladelis,N.A

ntonakisrR

esearchP

olicy30

2001535

–588

557

Ž . Ž . Ž .6 CANCER 6.1 LEDERLE 6 3r2 7 7 1947–1987 40 TEROPTERIN 1947Ž . Ž . Ž .6.2 B-W 6 3r3 11 7 1948–1968 20 PURINETHOL 1953Ž . Ž . Ž .6.3 ROCHE 8 3r1 10 9 1962–1991 29 EFUDIX 1962Ž . Ž . Ž .6.4 BRISTOL 14 8r6 36 16 1973–1995 22 BLENOXANE 1973

Ž Ž . Ž . Ž .7 CARDIOVASCULAR diuretics, 7.1 PARKE-DAVIS 12 3r5 21 4 1896–1986 90 ADRENALIN 1902Ž . Ž . Ž .antihypertensives, anticoagulants, anti- 7.2 CIBA 17 5r4 21 6 1924–1990 66 CORAMIN 1924Ž . Ž . Ž .thrombotics, cholesterol reducers, congestive 7.3 BOEHRINGER 11 2r4 50 4 1931–1970 39 PERSANTIN 1961

. Ž . Ž . Ž .heart failure, pressors, coronary dilators 7.4 HOECHST 11 4r3 15 4 1942–1990 48 ASPARSAN 1942Ž . Ž . Ž .7.5 MERCK 15 7r9 19 5 1952–1988 36 DIURIL 1958Ž . Ž . Ž .7.6 ICI 7 3r4 23 2 1962–1983 21 INDERAL 1964Ž . Ž . Ž .7.7 PFIZER 9 1r2 19 3 1959–1989 30 MINIPRESS 1973Ž . Ž . Ž .8 ANTIPROTOZOAL 8.1 BAYER 12 7r8 18 10 1890–1976 86 GERMANIN 1920Ž . Ž . Ž .8.2 HOECHST 8 2r2 11 7 1911–1983 72 SALVARSAN 1911Ž . Ž . Ž .8.3 RHONE 12 2r2 26 10 1922–1974 52 STOVARSOL 1922Ž . Ž . Ž .8.4 MERCK 8 2r4 10 7 1938–1988 50 SULPHAQUINOXALINE 1938Ž . Ž . Ž .9 ANTIHISTAMINES 9.1 RHONE 11 3r3 23 15 1937–1967 30 ANTEGRAN 1942Ž . Ž . Ž .10 ANTIASTHMATICS 10.1 BOEHRINGER 5 1r3 22 14 1940–1977 37 ISOPRENALINE 1940Ž . Ž . Ž .11 FUNGICIDES 11.1 JANSSEN 7 1r3 16 19 1972–1989 17 DAKTARIN 1972Ž . Ž . Ž .12 ANTIVIRAL 12.1 B-W 5 1r2 10 20 1964–1986 22 ZOVIRAX 1982Ž . Ž . Ž .13 PEPTIDE HORMONES 13.1 LILLY 4 4r3 7 18 1923–1983 60 INSULIN 1923Ž . Ž . Ž .14 VACCINESrSERA 14.1 B-W 8 3r2 20 10 1896–1986 90 DIPHTHERIA TOXOID 1923Ž . Ž . Ž .14.2 LEDERLE 8 3r3 20 10 1945–1989 44 DPT VACCINE 1945Ž . Ž . Ž .14.3 MERCK 14 6r7 17 18 1960–1996 36 MUMPS VACCINE 1967Ž . Ž . Ž .14.4 MERRIEUX 13 4r4 100 17 1958–1997 39 IPOL VACCINE 1958Ž . Ž .14.5 BEHRINGWERKE 10 3r2 100 13 1972–1987 15 VARICELLA-ZOSTER

Ž .VACCINE 1982

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588558

to the AenvironmentalB driving forces that lead to thenew TT is discerned at the stage of decline of a

technology when most of the companies that intro-duced and profited from it, doggedly pursue their

Fig. 10. Major mergers and acquisitions among pharmaceutical companies.

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588 559

efforts even after it has become obsolete. In theseinstances, the CTT has become so deeply embeddedin the corporate psyche, that acts as a factor oftechnological inertia, blocks its sensitivity to theAenvironmentalB driving forces and undermines thecompany’s technology and market positions. Thus,CTTs contribute to the Schumpeterean destructionassociated with the waves of creativity, wherebycompanies that have thrived from a technology dis-appear with its obsolescence.

The relation between CTTs and TTs raises someintriguing questions regarding the survival of phar-maceutical companies over periods far longer thanindividual Along wavesB. Although many manufac-turing apothecaries and pharmaceutical companieshave folded in the course of the 200-year-long his-tory of the pharmaceutical industry, nearly all oftoday’s large companies were established about acentury ago and this indicates that they overcame thecrises associated with the technologies they have

Ž .championed Fig. 10 .Company histories and innovation records indi-

cate that their ability to Aride the long wavesB wasprimarily due to the fact that they were multiproductcompanies either within or outside the pharmaceuti-cal industry and, accordingly, they did not depend onone but on a number of TTs. As the life span of TTsdiffers even within the same Along waveB, multi-product companies afforded some time for readjust-ment during periods of succession of Along wavesB.

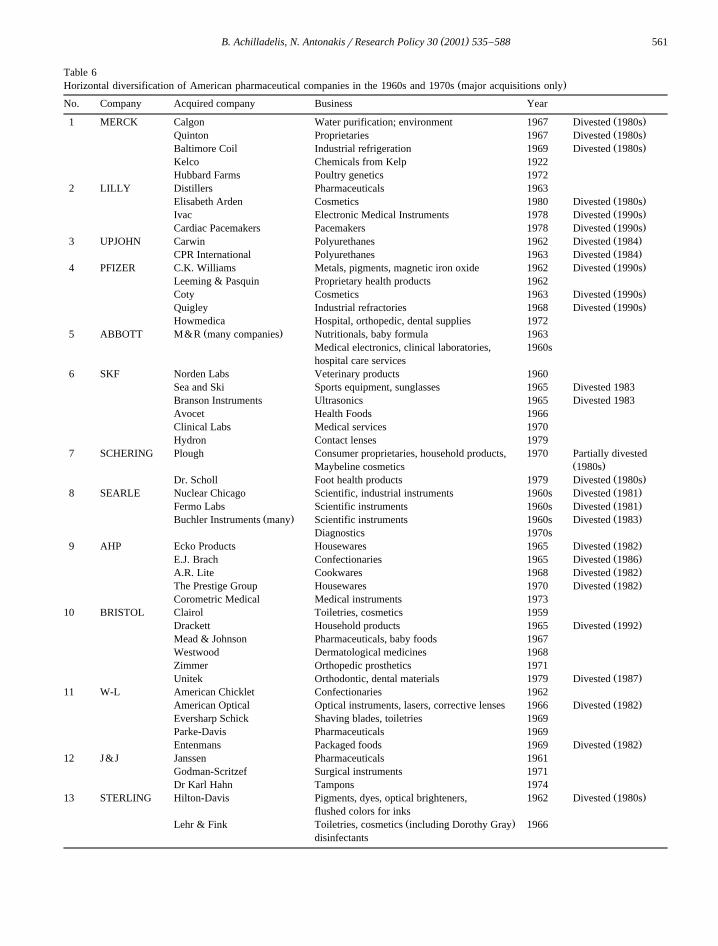

3.4.2.1. Horizontal diÕersification within the phar-maceutical industry. The most research-intensivecompanies developed numerous technologies and

Ž .markets by means of inhouse R&D Tables 4, 5 .However, diversification was also achieved by merg-ers and acquisitions of companies with CTTs intherapeutic markets complementary to their own.Examples: Merck ’s CTT in diuretics originatedfrom its merger with Sharp & Dohme; Bristol’s CTTin antineoplastic drugs originated from its acquisitionof Mead and Johnson; Roche’s entry into bioengi-neering resulted from its cooperation and, later,merger with Genentech. This policy was adopted inthe 1940s–1950s and, particularly, in the 1980s–1990s as shown by the super mergers, which createdglobal companies with a very wide spread of thera-

Ž .peutic markets Fig. 10 .

3.4.2.2. Horizontal diÕersification outside the phar-maceutical industry. Many pharmaceutical compa-nies were established as branches of chemicalrdy-

Žestuffs companies Bayer, Hoechst, Rhone Poulenc,ˆ.Ciba, Geigy, Sandoz, ICI, American Cyanamid and

were from their beginnings members of multiproductcompanies benefiting in periods of turbulence causedby the succession of Along wavesB from cash flowsgenerated by the chemical businesses of the parentcompanies. This was possible until the mid 1970swhen the chemical industry began to decline andcompanies concentrated on high value added chemi-cals and pharmaceuticals. Other pharmaceutical com-panies that began as manufacturing apothecaries—aswas the case of most American companies—hadkept during the interwar and early postwar periodssome businesses in proprietary products, such as

Ž .over-the-counter OTC medicines, toiletries andcosmetics. However, these businesses were modestcompared to chemicals or pharmaceuticals and couldnot extricate them during the slow down that accom-panied the succession of drug generations. Thus, inthe early 1960s, when the pharmaceutical industrycould not attain rates of growth comparable to thoseof many consumer product industries, the Americanpharmaceutical companies diversified by merger and

Ž .acquisition into a host of sectors Table 6 . Most ofthese businesses were less research-intensive andless profitable than pharmaceuticals but they showedvery high rates of growth. The higher turnover thusattained allowed the pharmaceutical companies tosustain, even to increase, their expenditures for R&Dand innovation at a time when they had to overcomeimportant technological barriers. This diversificationhelped the American pharmaceutical companies tosail through the 1960–1980 period at the end ofwhich they divested these acquisitions as the techno-logical and market conditions of the 1980s–1990sguaranteed for the pharmaceutical industry bothgrowth and profits.

3.4.2.3. InnoÕation in successiÕe TTs. Companiesthat have established a CTT in a therapeutic marketseldom introduce the TP that initiates the next TT.The case of Lilly and Pfizer, which were protago-nists in both natural and semisynthetic antibiotics,two successive TTs, is one of the very few excep-tions that prove the rule. Many companies dropped

( )B. Achilladelis, N. AntonakisrResearch Policy 30 2001 535–588560

out of a therapeutic market because they missed theopportunities opened by a new technology. For ex-ample, Bayer and Abbott both with strong CTTsŽ . Ž1890–1940 in CNS depressants barbiturate hyp-

.notics, anticonvulsants missed the post World WarTwo launching of antidepressants, antipsychotics andanxiolytics; Merck, a protagonist in natural antibi-

Ž .otics penicillin, streptomycin missed the opportuni-ties of semisynthetic penicillins and cephalosporins,

Žreturning to them after a lapse of 20 years cefoxitin,.MEFOXIN, 1977 . Also, ICI, which introduced the

Žantihypertensive beta blockers propranolol, IN-.DERAL, 1964 , missed the challenge of ACE in-