Embed Size (px)

Citation preview

The Double Edged Sword of Participant Loans Sunday, April 28, 2013

Kimberly B. Martin, APA, CPC, QPA, Director

of Education, National Institute of Pension

Administrators

What We Will Cover…

• Participants with multiple loans

• Refinancing participant loans

• Handling LOA and part-time employees

• Managing loan offsets and deemed distributions

• EPCRS correction methods for participant loans

Tax Rules Relating to Participant Loans

• Amount limitation

• Lesser of $50,000 or 50% of VAB §72(p)(2)(A)

• 5-year repayment period

• Home loan exception §72(p)(2)(B)

• Level amortization

• Payments at least quarterly §72(p)(2)(C)

Participant loans are taxable distributions unless the

requirements of IRC §72(p) are met:

Multiple Plan Loans

• Verify plan provisions.

• Can a participant have more than one outstanding loan?

• Check the plan document and any separate loan policy.

• It’s an operational failure if the terms of the plan are not followed.

• Calculate the maximum amount under IRC §72(p)(2)(A).

• If multiple plan loans are permitted under the plan, special

adjustments must be made when determining the maximum

amount for additional loans.

• IRC §72(p)(2)(A) permits plan loans as long as all of a

participant’s loans combined do not exceed the maximum loan

amount.

• If a loan exceeds the maximum amount, the excess is taxable

(deemed distribution).

Impact of Multiple Plan Loans on Amount Limitation

• Maximum loan amount.

• The new loan plus the outstanding balance of all of the

participant’s other loans cannot exceed the lesser of:

• 50% of the participant’s vested account balance, or

• $50,000 less adjustment.

• $50,000 limit adjustment

• The $50,000 limit takes into account loans during the last 12 months.

• Adjustment = participant’s highest outstanding balance of all loans

during the 12-month period ending on the day before the new loan,

less the outstanding balance of the participant’s loans on the day of

the new loan.

• This special 12-month rule inherently limits the number of loans that

can be made for larger borrowings.

• Adjustment doesn’t apply to the 50% of VAB limit.

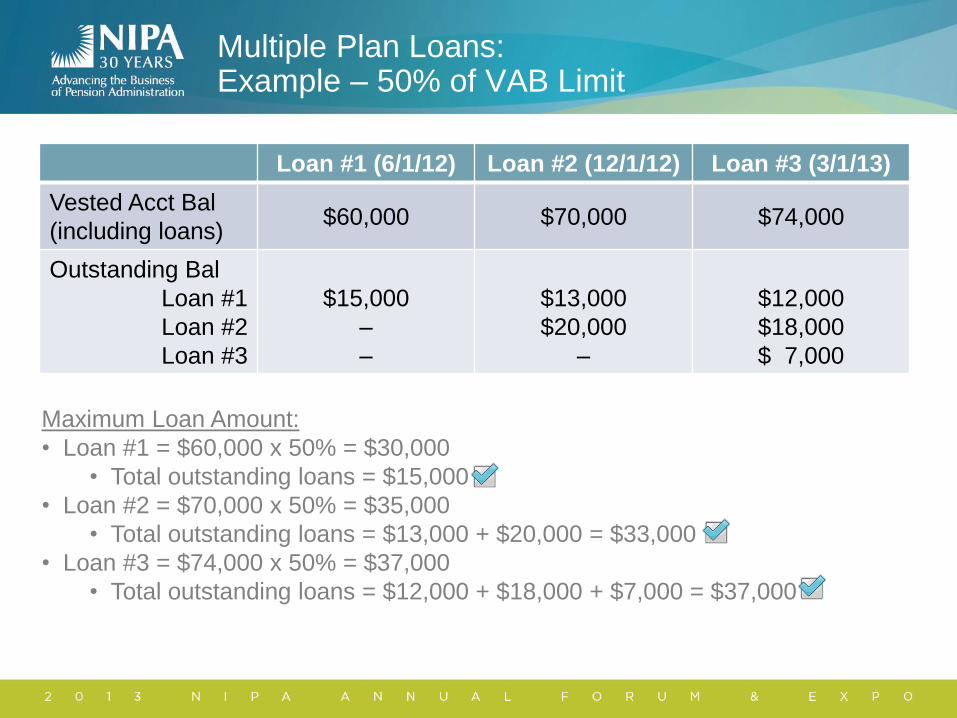

Multiple Plan Loans: Example – 50% of VAB Limit

Loan #1 (6/1/12) Loan #2 (12/1/12) Loan #3 (3/1/13)

Vested Acct Bal

(including loans) $60,000 $70,000 $74,000

Outstanding Bal

Loan #1

Loan #2

Loan #3

$15,000

–

–

$13,000

$20,000

–

$12,000

$18,000

$ 7,000

Maximum Loan Amount:

• Loan #1 = $60,000 x 50% = $30,000

• Total outstanding loans = $15,000

• Loan #2 = $70,000 x 50% = $35,000

• Total outstanding loans = $13,000 + $20,000 = $33,000

• Loan #3 = $74,000 x 50% = $37,000

• Total outstanding loans = $12,000 + $18,000 + $7,000 = $37,000

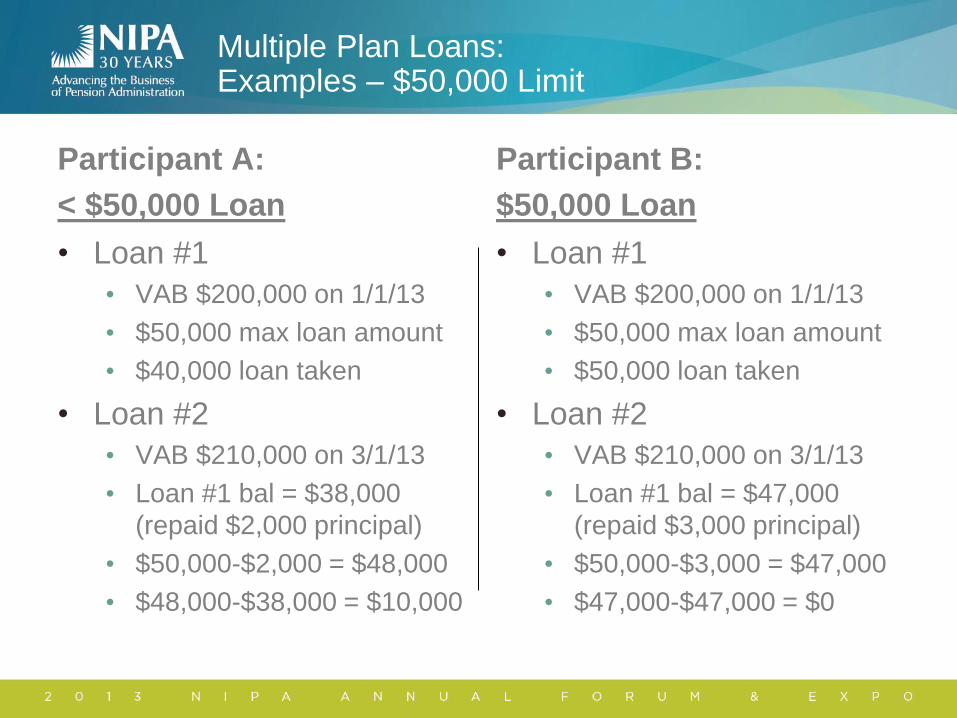

Multiple Plan Loans: Examples – $50,000 Limit

Participant A:

< $50,000 Loan

• Loan #1

• VAB $200,000 on 1/1/13

• $50,000 max loan amount

• $40,000 loan taken

• Loan #2

• VAB $210,000 on 3/1/13

• Loan #1 bal = $38,000

(repaid $2,000 principal)

• $50,000-$2,000 = $48,000

• $48,000-$38,000 = $10,000

Participant B:

$50,000 Loan

• Loan #1

• VAB $200,000 on 1/1/13

• $50,000 max loan amount

• $50,000 loan taken

• Loan #2

• VAB $210,000 on 3/1/13

• Loan #1 bal = $47,000

(repaid $3,000 principal)

• $50,000-$3,000 = $47,000

• $47,000-$47,000 = $0

Multiple Plan Loans: Example – $50,000 Limit

Loan #1 (6/1/12) Loan #2 (12/1/12) Loan #3 (3/1/13)

Vested Acct Bal

(including loans) $100,000+ $100,000+ $100,000+

Outstanding Bal

Loan #1

Loan #2

Loan #3

$25,000

–

–

$23,000

$24,000

–

$22,000

$23,000

$ 3,000

Maximum Loan Amount:

• Loan #1 = $50,000 – $0 = $50,000

• Total outstanding loans = $25,000

• Loan #2 = $50,000 – ($25,000 – $23,000) = $48,000

• Total outstanding loans = $23,000 + $24,000 = $47,000

• Loan #3 = $50,000 – ($47,000 – $45,000) = $48,000

• Total outstanding loans = $22,000 + $23,000 + $3,000 = $48,000

Total Loans:

• $25,000 + $24,000 + $3,000 = $52,000!

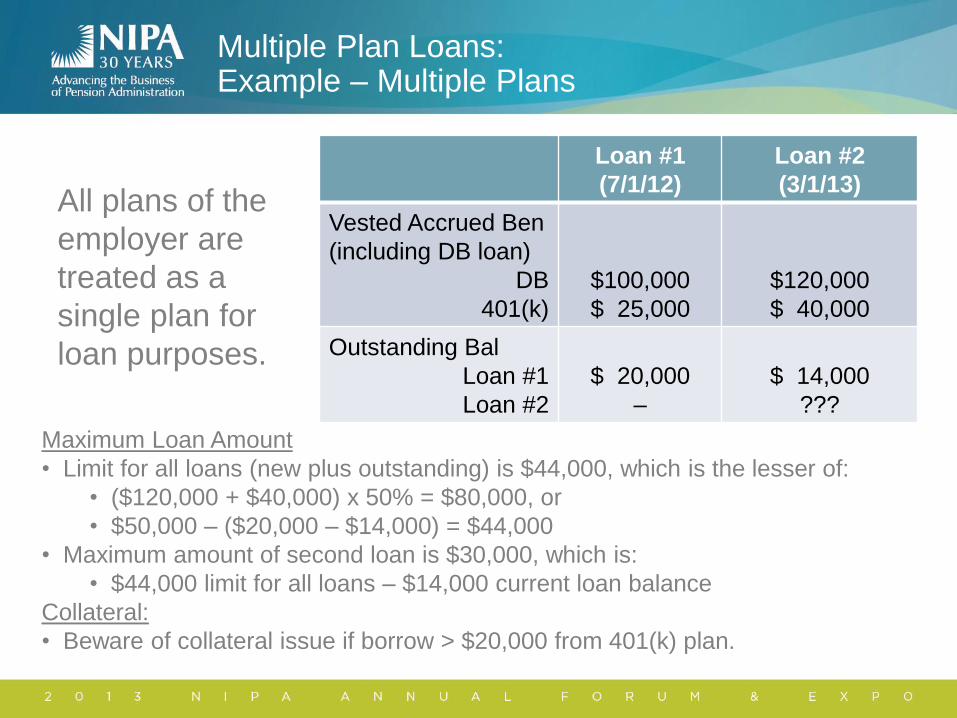

Multiple Plan Loans: Example – Multiple Plans

Loan #1

(7/1/12)

Loan #2

(3/1/13)

Vested Accrued Ben

(including DB loan)

DB

401(k)

$100,000

$ 25,000

$120,000

$ 40,000

Outstanding Bal

Loan #1

Loan #2

$ 20,000

–

$ 14,000

???

Maximum Loan Amount

• Limit for all loans (new plus outstanding) is $44,000, which is the lesser of:

• ($120,000 + $40,000) x 50% = $80,000, or

• $50,000 – ($20,000 – $14,000) = $44,000

• Maximum amount of second loan is $30,000, which is:

• $44,000 limit for all loans – $14,000 current loan balance

Collateral:

• Beware of collateral issue if borrow > $20,000 from 401(k) plan.

All plans of the

employer are

treated as a

single plan for

loan purposes.

Refinancing

• What is it?

• Refinancing is a transaction in which one loan replaces another

loan.

• The loan that is replaced is treated as repaid.

• The refinanced loan is treated as a new loan.

• Interest rate and loan limit must be re-determined.

• Optional provision – Check document and/or loan policy.

• Why do it?

• Extend amortization period (3-yr term to 5-yr term).

• Borrow additional funds (circumvents one loan limit).

• Renegotiate to a lower interest rate.

• Change payment frequency.

Impact of Loan Refinancing on Amount Limitation

• Any loan resulting from refinancing must still meet the

requirements of IRC §72(p).

• Caution: The loan amount considered outstanding may be

affected by the refinancing transaction.

• Which loans are treated as outstanding depends upon the payoff

date of the replaced loan under the terms of the replacement

loan.

• Huh?

• Terms to understand

• Replaced loan = original loan that is replaced

• Replacement loan = new, refinanced loan

• Latest permissible term (LPT) = latest payoff date permitted (5

years from date of original loan)

Impact of Loan Refinancing on Amount Limitation

• Amount limitation recap:

• A new loan plus the outstanding balance of all other loans cannot

exceed the lesser of 50% of VAB or $50,000 as adjusted.

• The outstanding loan balance in a refinance transaction

depends upon the replacement loan payoff date.

• If replacement loan term ends on or before LPT of replaced loan:

• Only the replacement loan is considered outstanding.

• If replacement loan term ends after LPT of replaced loan:

• Both the replacement loan and the replaced loan are considered

outstanding.

• This could cause the maximum loan amount to be exceeded,

resulting in a taxable loan (deemed distribution).

Loan Refinancing: Example – Facts

• A participant loan of $30,000 is made on 1/1/2012.

• Payments are $449 twice a month for 3 years (due 12/31/2014)

using a 5% interest rate.

• Loan is refinanced on 1/1/2013.

• VAB is $150,000.

• Replaced loan balance is $20,944.

• Replacement loan is $25,000.

• $20,944 original loan is considered repaid.

• $4,056 additional funds are disbursed to participant.

• 5% interest is determined to still be a commercially reasonable

interest rate.

• The LPT of the replaced loan is 12/31/2016.

Loan Refinancing: Example – Term Ends On Or Before LPT

• Option #1 – Payoff by end of replaced loan term

• Replacement loan payments are $548 twice a month for 2 years

(due 12/31/2014 – before the LPT of the replaced loan).

• Amount limitation = $50,000 – ($30,000 - $20,944) = $40,944

• Since the due date for the replacement loan is the same as the

replaced loan, only the $25,000 replacement loan is outstanding.

→ Replacement loan satisfies the amount limitation of 72(p)(2)(A).

• Option #2 – Payoff by end of LPT of replaced loan

• Replacement loan payments are $288 twice a month for 4 years

(due 12/31/2016 – the LPT of the replaced loan).

• Amount limitation = $50,000 – ($30,000 - $20,944) = $40,944

• Since the due date for the replacement loan ends on the LPT of the

replaced loan, only the $25,000 replacement loan is outstanding.

→ Replacement loan satisfies the amount limitation of 72(p)(2)(A).

Loan Refinancing: Example – Term Ends After LPT

• Option #3 – Payoff after LPT of replaced loan

• Replacement loan payments are $236 twice a month for 5 years

(due 12/31/2017).

• Loan limit = $50,000 – ($30,000 - $20,944) = $40,944

• Since the due date for the replacement loan ends after the LPT of

the replaced loan, both the replacement loan and the replaced loan

are outstanding.

• Total outstanding loans = $25,000 + $20,944 = $45,944

→ Outstanding loans exceed the amount limitation of 72(p)(2)(A).

→ Replacement loan does not satisfy the amount limitation.

→ $5,000 taxable loan on 1/1/13 (deemed distribution).

• To satisfy §72(p) and avoid taxation, a $20,000 replacement loan

with level amortization over 5 years could be made.

Loan Refinancing: Example – Term Ends After LPT

• Option #4 – Combination Payoff Method

• Replacement loan treated as two separately amortized loans –

the original loan with payments of $449 twice a month until

12/31/14, plus the additional funds of $4,056 with payments of

$38 twice a month until 12/31/2017:

• Payments of $487 twice a month in 2013 and 2014, and

• Payments of $38 twice a month in 2015, 2016 and 2017.

• Loan limit = $50,000 – ($30,000 - $20,944) = $40,944

• Since the replacement loan is repaid by it’s LPT and the replaced

loan is repaid by it’s LPT, only the $25,000 replacement loan is

outstanding.

→ Replacement loan satisfies the amount limitation of 72(p)(2)(A).

• Note: If multiple plan loans are allowed, the plan could make a

separate loan of $4,056 with the same results.

Exceptions to Repayment Rules

• Loan Repayment Terms Under §72(p)(2)(B)&(C)

• The participant must repay the loan within 5 years from the date

of the loan, unless the loan is used to purchase the participant’s

main home.

• The terms of the loan must require the participant to make level

amortized repayments at least quarterly.

• Substantially equal payments of principal and interest.

• Missed payments violate the amortization requirement, resulting

in a deemed distribution of the entire outstanding balance.

• Exceptions:

• The suspension of payments is permitted in the event of:

• Leave of absence (LOA), or

• Military service

Leave of Absence Exception

• Leave of Absence (LOA)

• A plan may permit a participant to suspend repayments for up to

a year while on a LOA.

• LOA must be without pay or with a level of pay that is insufficient to

make the loan payment.

• Interest continues to accrue during the suspension.

• The loan’s maximum repayment period cannot be extended.

• Upon return from a LOA (or after one year, if earlier), the participant

must make additional payments on the loan to ensure it is repaid

within the 5-year period by either:

• Increasing the payment amounts owed over the remaining period of the

loan, or

• Keeping the payment amounts the same, but making a lump-sum

payment for the missed installments that occurred during the leave of

absence.

• Loan repayment includes the accrued interest.

Leave of Absence: Example – 5-Year Loan Term

• Facts:

• Joe receives a $20,000 loan on 3/1/2012.

• The loan term requires 60 monthly payments of $377.

• The loan maturity date is 2/28/2017.

• Joe begins a 12-month LOA on 9/1/2012.

• As of 9/1/2012, six loan payments have been made.

• Twelve loan payments are suspended during the LOA.

• Joe returns from his leave on 9/1/2013.

• When Joe’s leave ends, what are his repayment options?

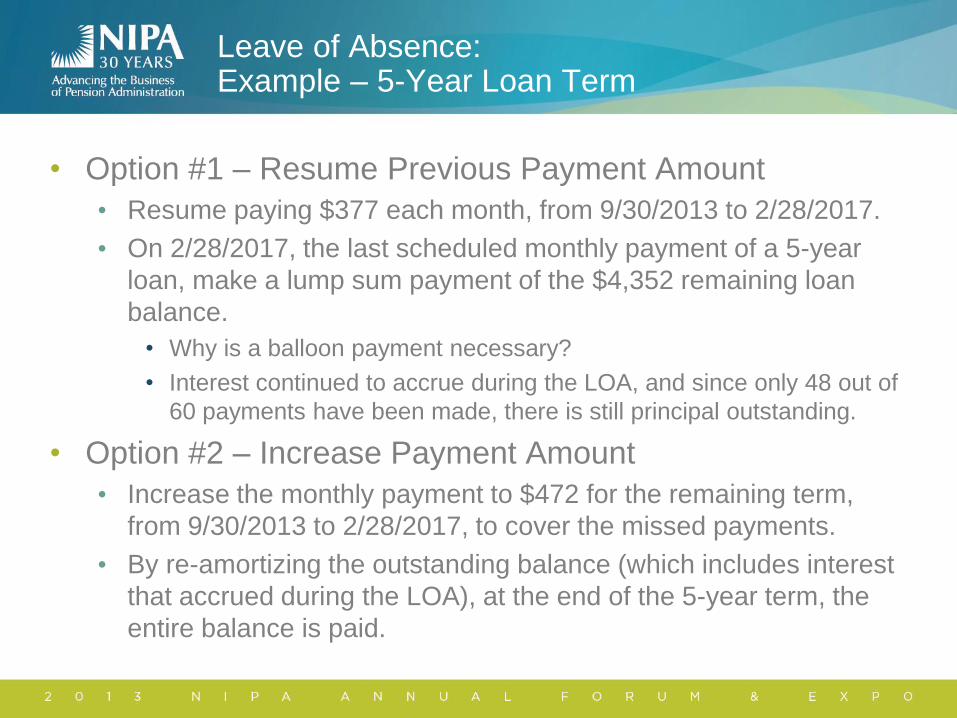

Leave of Absence: Example – 5-Year Loan Term

• Option #1 – Resume Previous Payment Amount

• Resume paying $377 each month, from 9/30/2013 to 2/28/2017.

• On 2/28/2017, the last scheduled monthly payment of a 5-year

loan, make a lump sum payment of the $4,352 remaining loan

balance.

• Why is a balloon payment necessary?

• Interest continued to accrue during the LOA, and since only 48 out of

60 payments have been made, there is still principal outstanding.

• Option #2 – Increase Payment Amount

• Increase the monthly payment to $472 for the remaining term,

from 9/30/2013 to 2/28/2017, to cover the missed payments.

• By re-amortizing the outstanding balance (which includes interest

that accrued during the LOA), at the end of the 5-year term, the

entire balance is paid.

Leave of Absence: Example – 5-Year and 3-Year Loan Terms

• Option #3 – Refinance

• Joe may be able to start a new 5-year term with a replacement

loan.

• Option #4 – Extend Term of Loan (if < 5 years)

• If Joe’s $20,000 loan on 3/1/2012 actually had a 3-year term with

monthly payments of $599, after his LOA the plan could add 12

months (his leave period) to the end of his 3-year loan term.

• Joe could then continue making monthly payments of $599 until

2/28/2016 instead of 2/28/2015.

• Joe’s payment on 2/28/2016 must also include a balloon payment

of the unpaid loan balance due to his failure to pay interest on the

loan during the LOA.

Military Service Exception

• A plan may suspend loan payments for more than one

year for an employee performing military service.

• Payments are suspended for the entire period during which an

employee is performing military service.

• The loan repayment period is extended for the period of

military service.

• The employee must repay the loan within five years from the date

of the loan, plus the period of military service.

• Example: A participant takes out a 5-year loan on 1/1/2012. If he

suspends payments during a 1-year LOA in 2013, he must still

repay the loan by the end of the original 5-year term: 12/31/2016.

However, if he takes a 1-year LOA to serve in the military, he

does not have to finish paying off the loan until 12/31/2017.

Military Service Exception

• Upon return from military service, repayments must

resume.

• The loan, which includes interest that accrued during the military

service suspension period, is repaid by either:

• Increasing the payment amounts owed over the remaining period of

the loan (as extended), or

• Keeping the payment amounts the same, but making a lump-sum

payment for the accrued interest and outstanding principal.

• During the military leave period, interest may be capped at 6% if

requested by the participant.

• Example: A participant has a loan with an interest rate of 8%. The

participant goes on military leave for two years. During the two-year

period of military service, interest continues to accrue, but at a

reduced rate of 6%. When the participant's military service ends and

he resumes employment, the loan will be re-amortized at the original

8% interest rate.

Military Service: Example

• Facts:

• Joe receives a $20,000 loan on 3/1/2012.

• The loan term requires 60 monthly payments of $377.

• The loan maturity date is 2/28/2017.

• Joe begins a 24-month period of military service on 9/1/2012.

• As of 9/1/2012, six loan payments have been made.

• Twenty-four loan payments are suspended during the military

service period.

• Joe returns from military service on 9/1/2014.

• When Joe resumes his employment, what are his

repayment options?

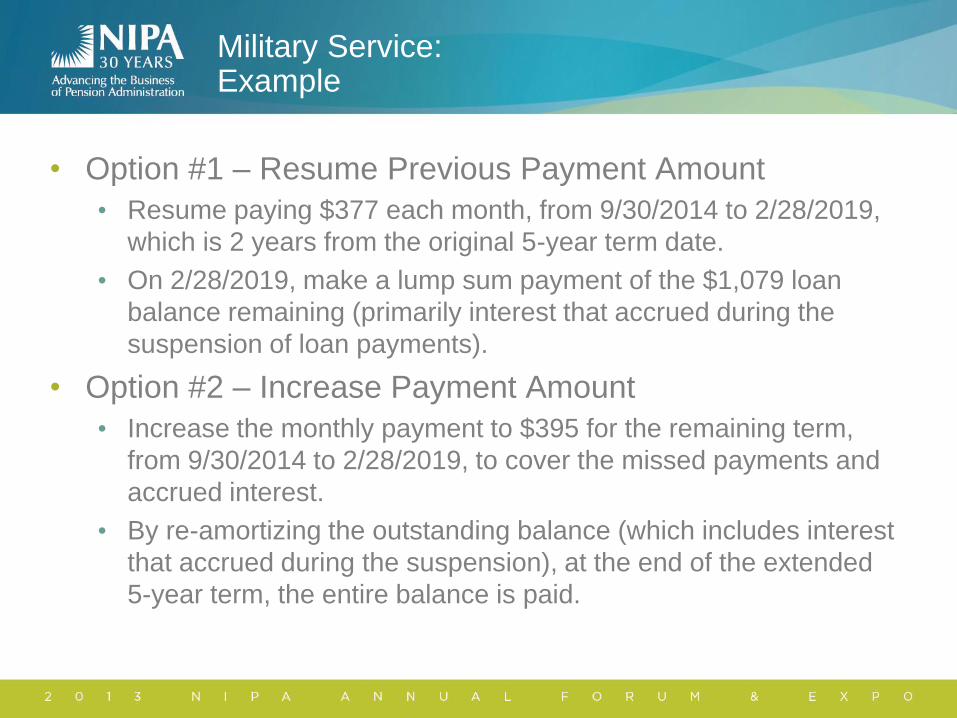

Military Service: Example

• Option #1 – Resume Previous Payment Amount

• Resume paying $377 each month, from 9/30/2014 to 2/28/2019,

which is 2 years from the original 5-year term date.

• On 2/28/2019, make a lump sum payment of the $1,079 loan

balance remaining (primarily interest that accrued during the

suspension of loan payments).

• Option #2 – Increase Payment Amount

• Increase the monthly payment to $395 for the remaining term,

from 9/30/2014 to 2/28/2019, to cover the missed payments and

accrued interest.

• By re-amortizing the outstanding balance (which includes interest

that accrued during the suspension), at the end of the extended

5-year term, the entire balance is paid.

Part-Time Employees

• Part-time employees may be eligible to participate in a

qualified plan.

• Period of service eligibility requirement (such as 3 months)

• Work 20+ hours per week (20 hours x 52 weeks = 1,040 hours)

• Participant Loan Repayment Issue

• A plan may require participants to make loan payments through

payroll withholding.

• A part-time employee’s hours may fluctuate so that at times the

level of pay is insufficient to make the full loan payment via

payroll withholding.

• Seasonal employees who have become plan participants could

also have difficulty making loan repayments via payroll

withholding during the “off” season when they are not working

(and not paid).

Loan Failures → Deemed Distributions

Failure to satisfy the amount limitation

Deemed distribution of the excess loan

amount

At the time the loan is made

Failure to satisfy the repayment period

Deemed distribution of the entire loan

amount

At the time the loan is made

Failure to satisfy level amortization

Deemed distribution of the entire loan

amount

At the time the loan is made or

upon default

Failure to satisfy an enforceable agreement

Deemed distribution of the

entire loan amount

At the time the loan is made

Deemed Distribution: Examples

• Amount Limitation

• A participant with a VAB of $200,000 receives an $80,000 loan

repayable in level monthly installments over 5 years.

• The participant has a deemed distribution of $30,000 – the excess of

$80,000 over the $50,000 limit – at the time the loan is made.

• Repayment Period

• A participant with a VAB of $70,000 receives a $20,000 non-

home loan repayable in level quarterly installments over 7 years.

• The participant has a deemed distribution of $20,000 at the time the

loan is made.

• Level Installments

• A participant with a VAB of $120,000 receives a $50,000 loan

repayable in annual installments over 4 years.

• The participant has a deemed distribution of $50,000 at the time the

loan is made.

Deemed Distribution: Examples

• Legally Enforceable Agreement

• A participant with a VAB of $100,000 receives an $40,000 loan

repayable in level monthly installments over 5 years. There is no

agreement which demonstrates compliance with IRC §72(p).

• The participant has a deemed distribution of $40,000 at the time the

loan is made.

• Loan Default

• A participant with a VAB of $40,000 receives a $20,000 loan on

2/1/2012, repayable in level bi-weekly installments over 5 years.

After making payments through 1/30/2013, the participant fails to

make any additional payments.

• The participant has a deemed distribution of the outstanding loan

balance at the time the loan defaults.

What is a Deemed Distribution?

• Taxable Distribution of a Loan Failure

• When a loan fails to satisfy the plan loan rules with respect to

amount, duration, repayment terms and enforceable agreement,

the loan is treated as a taxable distribution from the plan.

• The amount deemed to be distributed is included in the participant’s

gross income and may be subject to the 10% early distribution tax.

• But is it an Actual Distribution?

• A deemed distribution is a distribution for tax purposes only.

• It is not treated as an actual distribution for qualification purposes.

• Therefore, the deemed distribution does not violate any restrictions

on in-service distributions applicable to certain plans (pension plan,

401(k) plan).

• A deemed distribution occurs before a participant is eligible for a

distribution, but because it is “deemed,” the plan is not disqualified.

Impact of a Deemed Distribution

• Obligation To Repay → Maintain Loan On Books

• Because an actual distribution has not occurred, there is still an

obligation to repay the loan – even though it’s been taxed.

• The participant’s account balance continues to reflect the loan.

• Interest on the outstanding loan balance continues to accrue.

• The loan remains as part of the participant’s account balance until a

distributable event occurs.

• Maintaining the loan complicates recordkeeping.

• Top Heavy Rules

• As part of the participant’s account balance, the loan is taken into

account when calculating the top heavy ratio.

• Coverage and Nondiscrimination Testing

• The loan is included in certain coverage and nondiscrimination

tests that consider accumulated accrued benefits.

Impact of a Deemed Distribution

• RMD Rules

• The deemed distribution does not count toward satisfying RMDs.

• Future Loans

• The loan plus accrued interest count as an outstanding loan for

determining the maximum amount under the 50%/$50,000 limit.

• If the loan is not repaid after a deemed distribution, the plan must

require that certain conditions be satisfied for all future loans.

• Either:

• Repayments must be made by payroll deduction, or

• The participant must provide additional collateral.

• One of these conditions must be met for the entire term or the

subsequent loan will be treated as a new deemed distribution.

• If a plan has a one loan limit, the participant may be forced to

repay the loan to get a new one.

Loan Default

• A loan default occurs when the loan is not repaid

according to its terms.

• The default results in a deemed distribution at the time of the

default if the participant is not entitled to a distribution

• The participant is taxed on the unpaid loan balance, but still owes

the plan the borrowed funds.

• The unpaid loan balance includes interest that has accrued through

the date of default.

• Payroll Withholding

• To reduce the chances of default, the plan may require active

participants’ loan payments to be made by payroll withholding.

• Check the plan document and loan policy for instructions.

• The plan will specify loan when a loan is in default.

Cure Period

• A plan may provide a period of time to allow the

participant to make up any missed payments and bring

them current.

• Statutory cure period: A plan may provide that a loan is not in

default until the end of the calendar quarter following the quarter

in which the repayment was missed.

• For example, if a participant failed to make the January 31st monthly

payment and any subsequent payments, the loan would be in default

and would be treated as a deemed distribution as of June 30th.

• A plan can provide a shorter cure period, such as 30 or 90 days.

• The loan defaults when the cure period ends.

• Without a cure period, a deemed distribution would occur

if a loan payment is one day late!

• Interest accrues during the cure period.

$$$

Past

Due

Accrued Interest After a Deemed Distribution

• Interest continues to accrue after a deemed distribution.

• Previously-taxed loans continue to be due and payable.

• Consequently, the plan must continue to charge interest on an

outstanding loan until the loan is repaid or offset.

• Failure of the loan to bear a reasonable interest rate would result in a

prohibited transaction.

• To repay the entire loan, the participant must pay the unpaid loan

balance plus the accrued interest.

• Interest accrued after a deemed distribution is not taxable to the

participant.

• Accrued interest must be tracked.

• The outstanding loan (including accrued interest) is considered

outstanding when calculating the maximum loan amount for

future loans.

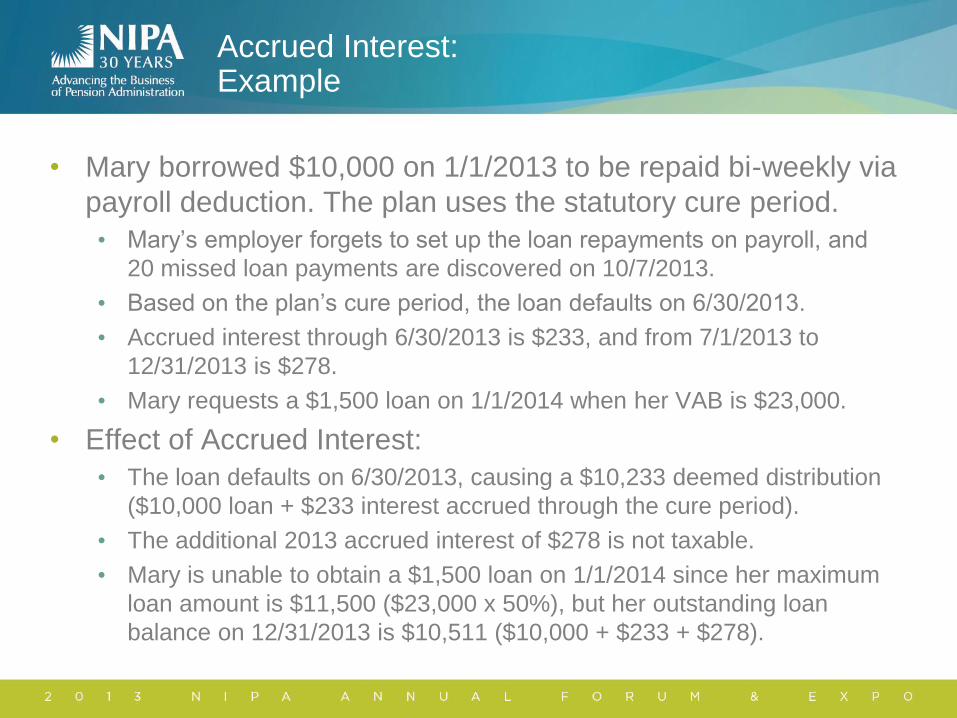

Accrued Interest: Example

• Mary borrowed $10,000 on 1/1/2013 to be repaid bi-weekly via

payroll deduction. The plan uses the statutory cure period.

• Mary’s employer forgets to set up the loan repayments on payroll, and

20 missed loan payments are discovered on 10/7/2013.

• Based on the plan’s cure period, the loan defaults on 6/30/2013.

• Accrued interest through 6/30/2013 is $233, and from 7/1/2013 to

12/31/2013 is $278.

• Mary requests a $1,500 loan on 1/1/2014 when her VAB is $23,000.

• Effect of Accrued Interest:

• The loan defaults on 6/30/2013, causing a $10,233 deemed distribution

($10,000 loan + $233 interest accrued through the cure period).

• The additional 2013 accrued interest of $278 is not taxable.

• Mary is unable to obtain a $1,500 loan on 1/1/2014 since her maximum

loan amount is $11,500 ($23,000 x 50%), but her outstanding loan

balance on 12/31/2013 is $10,511 ($10,000 + $233 + $278).

Taxation of Deemed Distributions

• Amount Taxed

• Default = principal and interest accrued through cure period

• Other failures = see “Loan Failures → Deemed Distribution” slide

• Tax Withholding

• A deemed distribution is not an eligible rollover distribution.

• As such, the distribution is not eligible for rollover.

• The distribution is not subject to the 20% mandatory tax withholding.

• A deemed distribution is subject to the voluntary 10% withholding

rules that apply to nonperiodic distributions.

• However, withholding only occurs only if there is cash or other

property distributed at the same time as the deemed distribution.

• Designated Roth Account

• A deemed distribution of Roth money is treated as a nonqualified

distribution under the Roth rules.

Reporting Deemed Distributions

• Form 1099-R

• Loans that are deemed distributions must be reported on Form

1099-R for the year the deemed distribution occurred.

• Code L designates the distribution as a deemed distribution in

Box 7.

• Code 1 or Code B may also be used in conjunction with Code L.

• Interest that accrues after the deemed distribution is not an

additional loan and is therefore is not reportable on Form 1099-R.

• Form 5500 Series

• A loan that is deemed distributed remains on the books, except

for the Form 5500 financials if the loan is not being repaid.

• The deemed distribution is reported on Form 5500-SF or either

Schedule H or I, but the loan is not included on Schedule G or in

end-of-year assets for the distribution year or subsequent years.

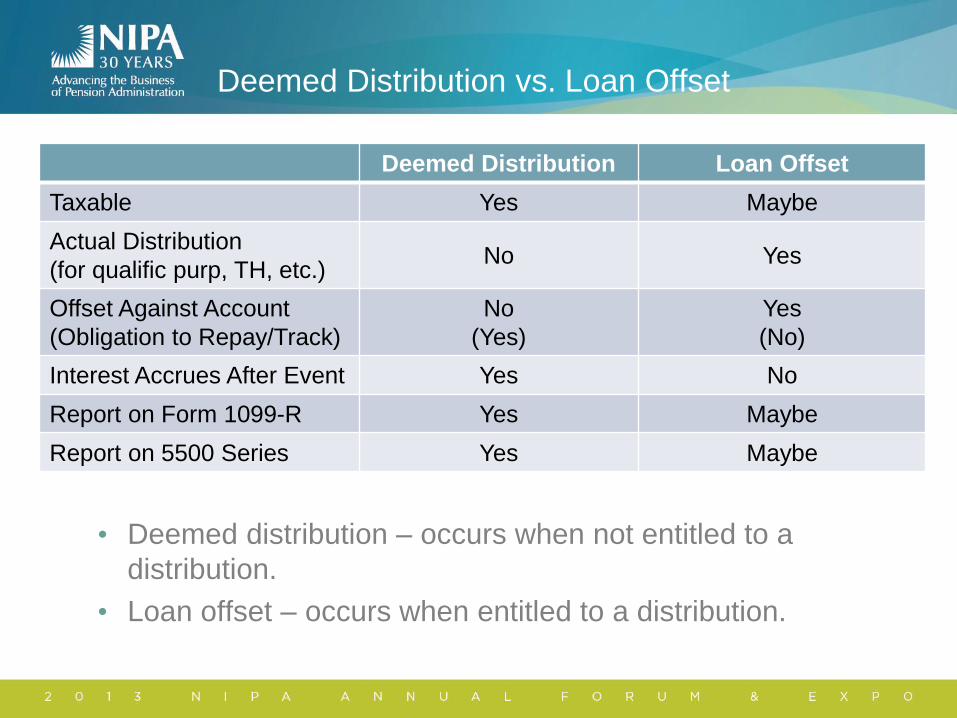

Deemed Distribution vs. Loan Offset

• Deemed distribution – occurs when not entitled to a

distribution.

• Loan offset – occurs when entitled to a distribution.

Deemed Distribution Loan Offset

Taxable Yes Maybe

Actual Distribution

(for qualific purp, TH, etc.) No Yes

Offset Against Account

(Obligation to Repay/Track)

No

(Yes)

Yes

(No)

Interest Accrues After Event Yes No

Report on Form 1099-R Yes Maybe

Report on 5500 Series Yes Maybe

Loan Offset

• Loan Offset is an Actual Distribution.

• May not be a distribution for tax purposes.

• Is treated as a distribution for all other purposes, including

qualification requirements.

• Can offset loan against participant’s account without violating the in-

service distribution restrictions.

• Since the loan is actually distributed, There is no longer an obligation

to repay the loan, so the loan is not maintained in the books

• Is triggered by a distributable event:

• Termination of employment

• Distribution of VAB

• Loan default

• Check plan document and loan policy for timing of loan offset.

• Interest accrues until the loan is offset.

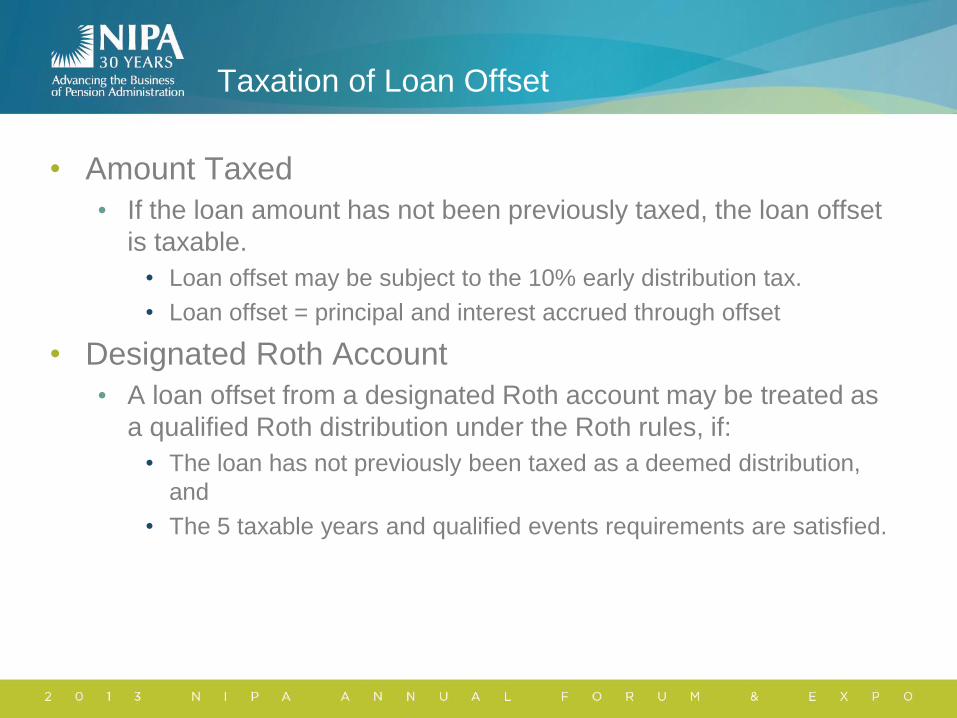

Taxation of Loan Offset

• Amount Taxed

• If the loan amount has not been previously taxed, the loan offset

is taxable.

• Loan offset may be subject to the 10% early distribution tax.

• Loan offset = principal and interest accrued through offset

• Designated Roth Account

• A loan offset from a designated Roth account may be treated as

a qualified Roth distribution under the Roth rules, if:

• The loan has not previously been taxed as a deemed distribution,

and

• The 5 taxable years and qualified events requirements are satisfied.

Taxation of Loan Offset: Examples

• Loan offset upon termination of employment.

• Debra has an outstanding loan of $10,000 in her employer’s plan

and loan payments are current. Debra terminates employment

with a VAB of $30,000 but elects to postpone a distribution. The

plan provides for a loan offset upon termination. Even though

Debra doesn’t receive a distribution, a $10,000 loan offset occurs.

Her taxable distribution is $10,000, and her remaining non-loan

VAB is $20,000.

• Loan offset upon distribution of VAB.

• The plan provides for a loan offset upon distribution of benefits. If

instead Debra has an outstanding loan of $10,000 in her

employer’s plan and loan payments are current. Debra terminates

employment and elects a distribution of her VAB. The actual

amount distributed to Debra is reduced by $10,000 – the loan

offset. However, her taxable distribution is $30,000.

Taxation of Loan Offset

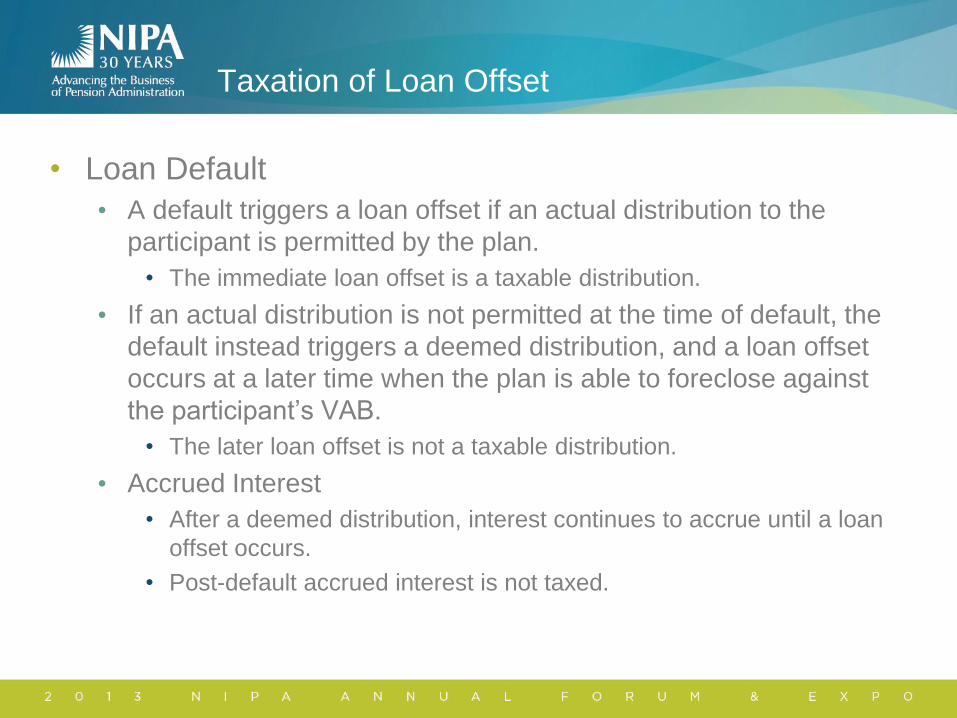

• Loan Default

• A default triggers a loan offset if an actual distribution to the

participant is permitted by the plan.

• The immediate loan offset is a taxable distribution.

• If an actual distribution is not permitted at the time of default, the

default instead triggers a deemed distribution, and a loan offset

occurs at a later time when the plan is able to foreclose against

the participant’s VAB.

• The later loan offset is not a taxable distribution.

• Accrued Interest

• After a deemed distribution, interest continues to accrue until a loan

offset occurs.

• Post-default accrued interest is not taxed.

Taxation of Loan Offset: Loan Default Example

• Example: Going back to Mary who defaulted on a $10,000 loan…

• Mary’s loan default triggered a $10,233 deemed distribution on

6/30/2013. Additional 2013 accrued interest totaled $278, and

interest of $537 accrued in 2014. Mary terminates on 12/31/2014

with an outstanding loan balance of $11,048. The plan provides

for an immediate loan offset upon termination of employment.

• Consequences of loan offset:

• Mary’s account balance is offset (reduced) by the $11,048 loan

balance on 12/31/2014.

• The loan offset is not taxable in 2014.

• The additional 2013 accrued interest of $278 is not taxable in 2013 or

2014.

• The 2014 accrued interest of $537 is not taxable in 2014.

• Interest no longer accrues after the offset since the loan is no longer

a plan asset.

Taxation of Loan Offset

• Loan Repayments of Deemed Distributions

• If a loan is taxed as a deemed distribution and the participant

repays the loan, the repayment generates basis.

• When a distribution is subsequently made, a portion of the

distribution (the basis) will be tax-free.

• Basis includes interest paid on the outstanding loan.

• Example: Tim receives a $20,000 loan. Before the loan is repaid,

he stops making payments, resulting in a $10,000 deemed

distribution. Over a period of time, Tim repays the loan, with total

payments of $12,500. Tim has basis of $12,500. He later

terminates and is receives a distribution of $50,000. The taxable

portion is $37,500 ($50,000 distribution – $12,500 basis).

Taxation of Loan Offset

• Rollover of Loan Offset

• A loan offset is an eligible rollover distribution.

• A participant can elect to roll over a loan offset.

• The portion of the loan offset not rolled over is subject to the

mandatory 20% tax withholding.

• The automatic rollover rules do not apply to a loan offset.

• Rollover options of a taxable loan offset:

• Cash equivalent of the offset amount may be contributed to a

qualified plan or IRA.

• Must be within 60 days of the offset date.

• Direct rollover of loan note to a qualified plan if not offset.

• Rollover to an IRA, SIMPLE or SEP is not permitted.

• Rollover options of a previously-taxed deemed distribution:

• Cash equivalent contribution within 60 days to an IRA.

• Repay loan and directly roll over to qualified plan.

Taxation of Loan Offset: Example – Rollover

• John is a terminated participant with a $100,000 VAB,

including an outstanding loan of $20,000 that has never been

taxed. The plan provides 30 days from date of termination

before a loan offset occurs. Options include:

• To defer taxation, John can elect a direct rollover of his $100,000

VAB, including the loan (assuming the receiving plan accepts it).

• If the receiving plan will not accept the note, John can repay the

loan and defer taxation through a direct rollover of his entire VAB.

• If the rollover is to an IRA or if the loan offset has occurred, John

can elect a direct rollover of his non-loan VAB and come up with

$20,000 out-of-pocket which he can roll over within 60 days.

• If John is not able to come up with $20,000, he can roll over the

non-loan VAB and be taxed on the $20,000 loan offset.

• John can elect a distribution of all or part of his VAB and be taxed

on the amount distributed, including the $20,000 loan offset.

Taxation of Loan Offsets

• Tax Withholding

• The taxable portion of a loan offset is subject to the mandatory

20% tax withholding.

• The required withholding applies since a loan offset is an eligible

rollover distribution.

• If the loan offset is part of a taxable distribution of cash, the 20%

withholding will apply to the entire taxable distribution – assuming

the cash is sufficient to cover the withholding.

• However, the tax withholding cannot exceed the cash distributed.

• Example: Mary’s loan default triggered a $10,233 deemed

distribution on 6/30/2013. Mary terminates on 12/31/2014 with a

VAB of $30,000, including an $11,048 outstanding loan balance.

Mary elects a lump sum distribution, which triggers a loan offset.

• Mary’s taxable distribution is only $18,952 ($30,000-$11,048). The

$10,233 previously-taxed default and subsequent accrued interest is

not taxed upon offset. Withholding applies to the non-loan $18,952.

Taxation of Loans: Example – Tax Withholding

• John is a terminated participant with a $100,000 VAB, including an

outstanding loan of $20,000 that has never been taxed. Options:

• Direct rollover of entire VAB, including loan: Tax is deferred on the

full $100,000, so no withholding is required.

• Repay loan and roll over entire VAB: Tax is deferred on the full

$100,000, so no withholding is required.

• Incur a loan offset, direct rollover of remaining VAB and indirect

rollover of $20,000 out-of-pocket offset amount: Tax is deferred on

$80,000 direct rollover. No cash is distributed so withholding is not

required on the $20,000 loan offset.

• Incur a loan offset and direct rollover of remaining VAB: Tax is

deferred on $80,000 direct rollover. No cash is distributed so no

withholding is required on the $20,000 taxable loan offset.

• Incur a loan offset and receive a cash distribution of remaining VAB:

Entire $100,000 distribution is taxable for required $20,000 tax

withholding ($100,000 x 20%). Actual cash payment is $60,000

($100,000 VAB – $20,000 offset – $20,000 tax).

Reporting Deemed Distributions

• Form 1099-R

• Taxable loan offsets must be reported on Form 1099-R for the

year the offset occurred.

• Includes when loan defaults and offset occur simultaneously.

• Code L in Box 7 is not used for a loan offset.

• Nontaxable loan offsets, such as loan defaults that occur prior to

offset, are not reported on Form 1099-R.

• Interest that accrues after the deemed distribution is not reportable

on Form 1099-R.

• Form 5500 Series

• A taxable loan offset is reported on Form 5500-SF or either

Schedule H or I as an actual distribution.

• A deemed distribution that is later offset is not reportable as a

distribution on the Form 5500 series for the offset year.

EPCRS: Correcting §72(p) Loan Failure

• Plan Loans under IRC §72(p)

• Loans that satisfy the requirements of IRC §72(p) are exempt

from treatment as taxable distributions.

• Once a loan violates a requirement, there are a few situations in

which the plan administrator can make correction and preserve

the exemption.

• Employee Plans Compliance Resolution System

(EPCRS) – Rev. Proc. 2013-12

• Loans that do not comply with the §72(p) requirements may not

be corrected under the Self-Correction Program (SCP).

• Correction may be made under the Voluntary Correction Program

(VCP) or the Audit Closing Agreement Program (Audit CAP).

EPCRS: Tax Relief Available for Loan Failures

• Relief = Timing of Deemed Distribution

• If a plan loan that fails to satisfy the IRC §72(p) requirements is

properly corrected under EPCRS, the employer may request the

ability to report the loan as a deemed distribution in the year of

correction rather than the year of failure.

• Relief = No Deemed Distribution

• Alternatively, the employer may request relief from reporting such

loan as a deemed distribution.

• Generally, for a plan loan to be eligible for relief from income tax

reporting:

• The loan failure must be properly corrected within the maximum

repayment period (generally 5 years), and

• Employer action must have caused the loan failure.

EPCRS: Amount Limitation Exceeded

• Correction

• The participant must repay the excess loan amount plus interest.

• The amount that must be repaid is based on how previous

payments have been applied to the loan, using one of three

alternatives:

• Reduce portion of loan that did not exceed maximum amount limit:

Corrective repayment = excess loan amount plus allocable interest;

• Reduce allocable interest on excess loan amount, with remainder

used to reduce portion of loan which did not exceed maximum

amount limit: Corrective repayment = original excess loan amount; or

• Reduce excess loan and maximum loan amount on pro-rata basis:

Corrective repayment = outstanding balance of excess loan.

• The remaining principal balance of the loan is then re-amortized

over the remaining period of the original loan, but not beyond 5

years from the date of the original loan.

EPCRS: Amount Limitation Exceeded

• Example

• On March 1, 2012, Peter took a $55,000 plan loan with a VAB of

$110,000. Peter received an excess loan of $5,000.

• Correction of the loan amount failure under EPCRS:

• Repay the excess loan amount (including interest)

• Apply prior payments:

• Option #1 – To portion of loan that did not exceed the maximum

amount, in which case the corrective payment is $5,000 plus interest;

• Option #2 – First to the interest on excess amount, and then to portion

of loan that did not exceed the maximum amount, in which case the

corrective payment is $5,000; or

• Option #3 – Pro-rata to reduce the excess loan amount (9.09%) and the

proper loan amount (90.91%), in which case the correction payment is

remaining excess loan balance plus interest.

• Re-amortize remaining balance (after applying prior payments) over

the remaining period of the loan.

EPCRS: Improper Loan Repayment Terms

• Correction

• The remaining principal balance of the loan is re-amortized over

the remaining portion of the maximum 5-year repayment period,

measured from the date of the original loan.

• Example

• Paul took a plan loan of $25,000 on June 1, 2011. The loan

provided a 6-year term.

• The mistake is discovered in 2013, when the outstanding

principal balance on the loan is $16,000.

• To correct the loan failure, the $16,000 outstanding balance is re-

amortized over a period ending not later than May 31, 2016,

reflecting the maximum 5-year repayment period.

EPCRS: Loan Default

• Correction

• Either:

• The participant may repay the missed payments plus accrued

interest in a lump sum payment,

• The loan balance may be re-amortized over the remaining original

term or over a period up to 5 years from the date of the original loan

(if the original term was less than 5 years), or

• A combination of the above methods.

• If the default is due to employer error, the employer should pay

the interest on the unpaid amount.

• The interest is generally determined at a rate equal to the greater of

the plan loan interest rate or the rate of return under the plan.

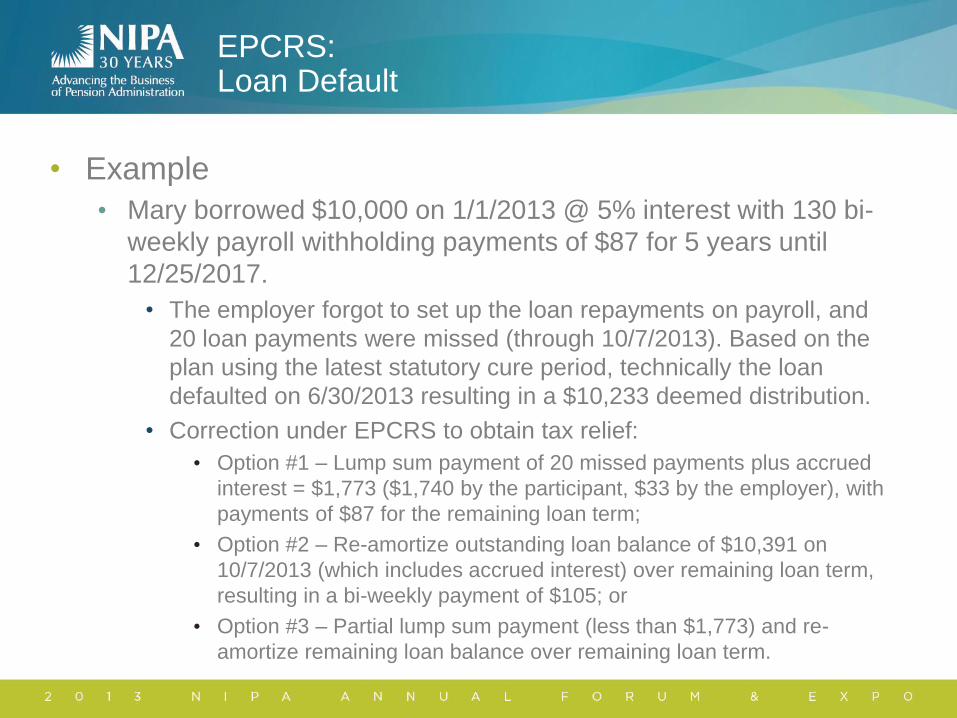

EPCRS: Loan Default

• Example

• Mary borrowed $10,000 on 1/1/2013 @ 5% interest with 130 bi-

weekly payroll withholding payments of $87 for 5 years until

12/25/2017.

• The employer forgot to set up the loan repayments on payroll, and

20 loan payments were missed (through 10/7/2013). Based on the

plan using the latest statutory cure period, technically the loan

defaulted on 6/30/2013 resulting in a $10,233 deemed distribution.

• Correction under EPCRS to obtain tax relief:

• Option #1 – Lump sum payment of 20 missed payments plus accrued

interest = $1,773 ($1,740 by the participant, $33 by the employer), with

payments of $87 for the remaining loan term;

• Option #2 – Re-amortize outstanding loan balance of $10,391 on

10/7/2013 (which includes accrued interest) over remaining loan term,

resulting in a bi-weekly payment of $105; or

• Option #3 – Partial lump sum payment (less than $1,773) and re-

amortize remaining loan balance over remaining loan term.

EPCRS: VCP Submissions

• The VCP compliance fee is reduced by 50% if:

• The submission involves an IRC §72(p)(2) failure;

• No more than 25% of participants are affected by loan errors, and

• The loan failure is the only failure of the submission.

• Coordination with VFCP

• The DOL’s Voluntary Fiduciary Correction Program allows

fiduciaries to correct breaches relating to prohibited transactions

arising from failure to follow the plan’s terms regarding loans.

• Correction under VFCP requires a VCP submission with the IRS.

VCP

VFCP

EPCRS: Audit CAP – Correction on Audit

• Audit CAP is available to correct IRC §72(p)(2) loan

failures found by the IRS in an examination.

• The same correction principles apply to both VCP and

Audit CAP.

• When negotiating the sanction under Audit CAP relating

to loan failures,

• The Maximum Payment Amount will include the tax the IRS could

collect as a result of the loan not being excluded from gross

income under § 72(p)(2), and

• The IRS will take into account the extent to which the failure is a

result solely of action or inaction of the employer or its agents, or

the extent to which failure is a result of the employee’s actions or

inactions.

EPCRS: Correcting Plan Document Loan Failures

• Allowing Plan Loans

• The plan document must provide for participant loans in

order for loans to be issued.

• Plan sponsors should check their plan documents before

allowing participants to borrow money from the plan.

• Correction

• If loans have been issued to participants under a plan that does

not provide for loans, the plan is amended retroactively under

SCP to provide for loans.

• The amendment must satisfy IRC §401(a).

• The plan, as amended, would have satisfied §401(a) and §72(p) had

the amendment been adopted when loans were first made available.