Embed Size (px)

DESCRIPTION

The Doom of Offshore Tax Planning?. Moderators: Diego Salto & Peter Utterström Panel: Michael Burns, Thijs Clement, Stephan Neidhardt, Michael Silva. AGENDA. 1. Introduction - Diego Salto/Peter Utterström 2. Model use historically - the practioner’s view! Thijs Clement - PowerPoint PPT Presentation

Citation preview

The Doom of Offshore Tax

Planning?

Moderators: Diego Salto & Peter UtterströmPanel: Michael Burns, Thijs Clement, Stephan Neidhardt, Michael Silva

AGENDA

1. Introduction - Diego Salto/Peter Utterström 2. Model use historically - the practioner’s

view! Thijs Clement3. The Obama Tax Bill and transparency -

Michael A. Silva 4. The OECD/G20 view on transparency -

Stephan Neidhardt 5. The Offshore Perspective - Michael Burns 6. Future outlook – restrictions, tools etc.7. Discussion

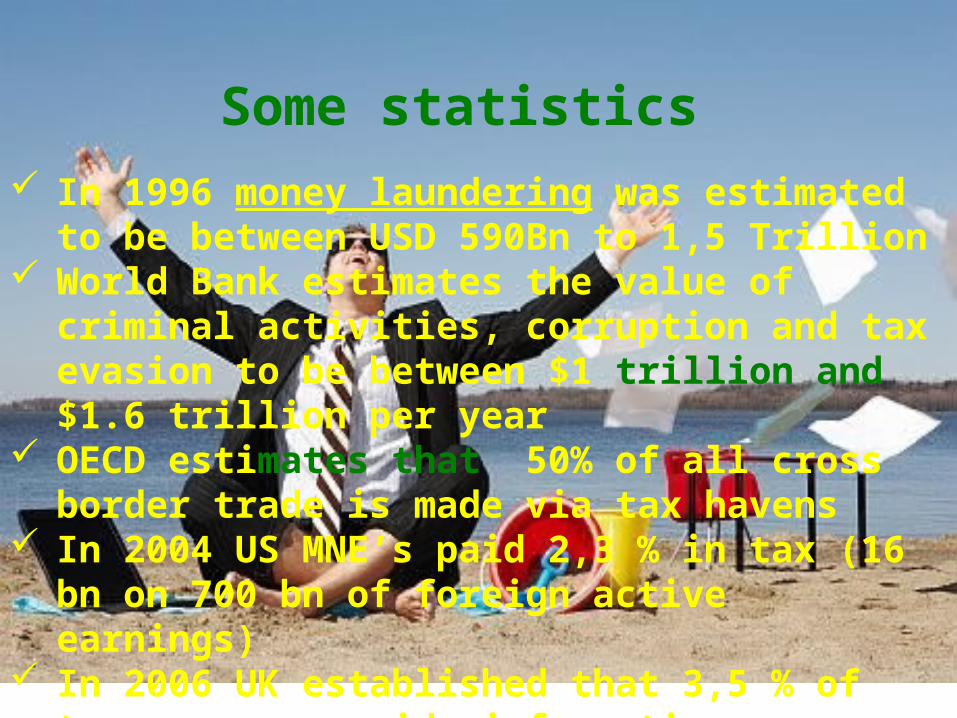

In 1996 money laundering was estimated to be between USD 590Bn to 1,5 Trillion

World Bank estimates the value of criminal activities, corruption and tax evasion to be between $1 trillion and $1.6 trillion per year

OECD estimates that 50% of all cross border trade is made via tax havens

In 2004 US MNE’s paid 2,3 % in tax (16 bn on 700 bn of foreign active earnings)

In 2006 UK established that 3,5 % of tax payers provide information re offshore accounts.

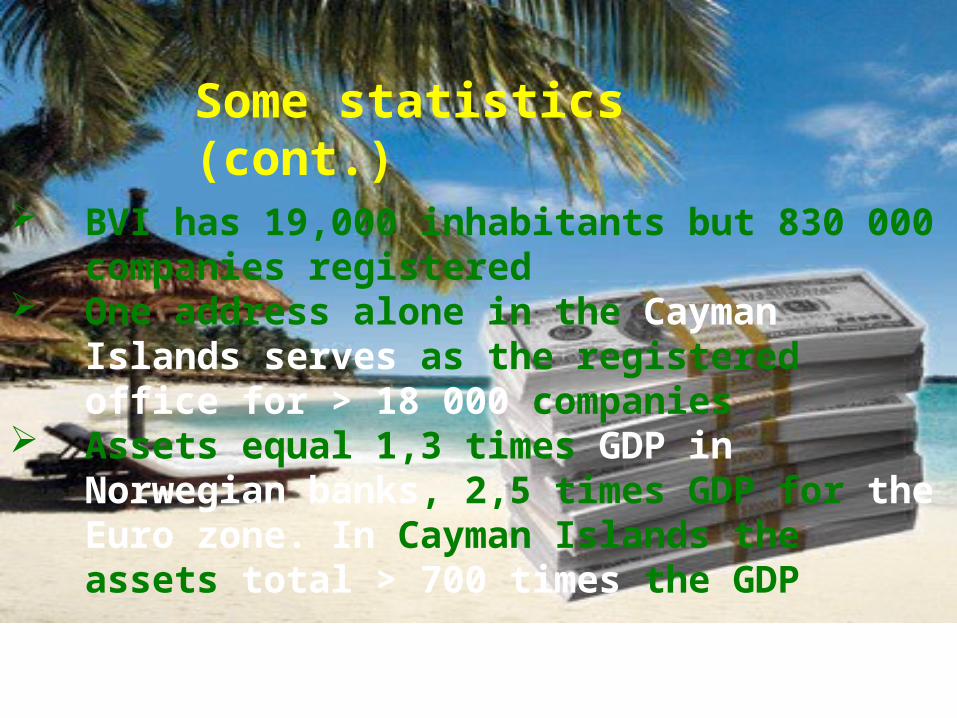

Some statistics

Some statistics (cont.)

BVI has 19,000 inhabitants but 830 000 companies registered

One address alone in the Cayman Islands serves as the registered office for > 18 000 companies

Assets equal 1,3 times GDP in Norwegian banks, 2,5 times GDP for the Euro zone. In Cayman Islands the assets total > 700 times the GDP

Convenient knowledge:

CFC – Controlled Foreign CorporationDTT – Double Tax TreatyFBAR – Foreign Bank Account Report (US)LOB – Limitation of Benefits QI – Qualified IntermediaryTax Haven - ?TIEA – Tax Information Exchange AgreementsWhite, Grey, Black List – CFC-related lists

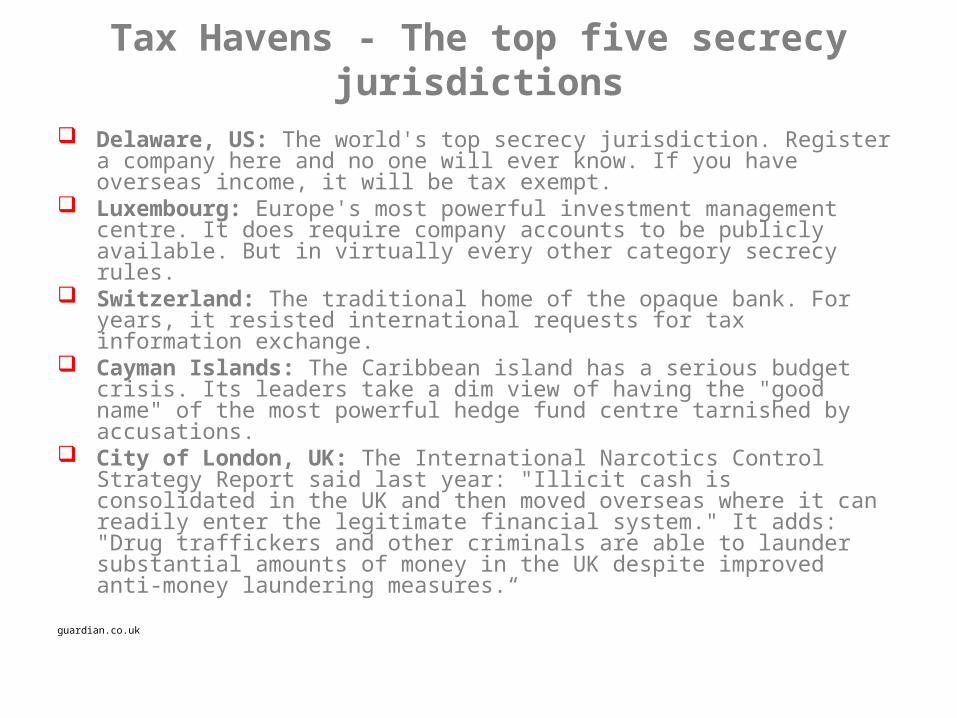

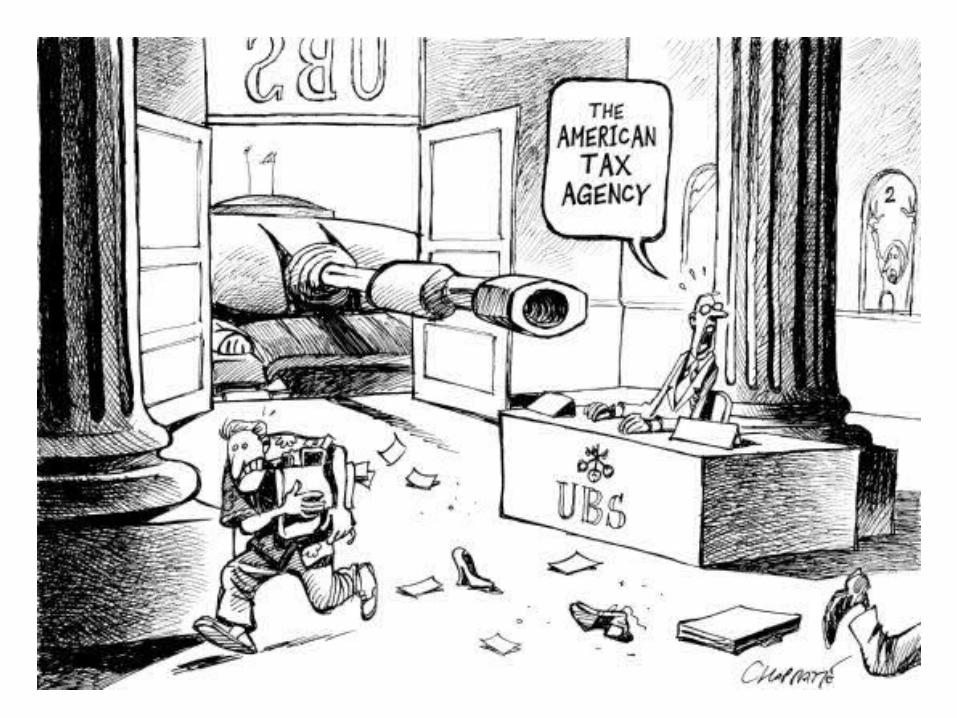

Tax Havens - The top five secrecy jurisdictions

Delaware, US: The world's top secrecy jurisdiction. Register a company here and no one will ever know. If you have overseas income, it will be tax exempt.

Luxembourg: Europe's most powerful investment management centre. It does require company accounts to be publicly available. But in virtually every other category secrecy rules.

Switzerland: The traditional home of the opaque bank. For years, it resisted international requests for tax information exchange.

Cayman Islands: The Caribbean island has a serious budget crisis. Its leaders take a dim view of having the "good name" of the most powerful hedge fund centre tarnished by accusations.

City of London, UK: The International Narcotics Control Strategy Report said last year: "Illicit cash is consolidated in the UK and then moved overseas where it can readily enter the legitimate financial system." It adds: "Drug traffickers and other criminals are able to launder substantial amounts of money in the UK despite improved anti-money laundering measures.“

guardian.co.uk

With this – will tax havens have a future?

Having said all this ---

…. The historical model transaction and its use - the practioner’s view!

Thijs Clement, Van Doorne

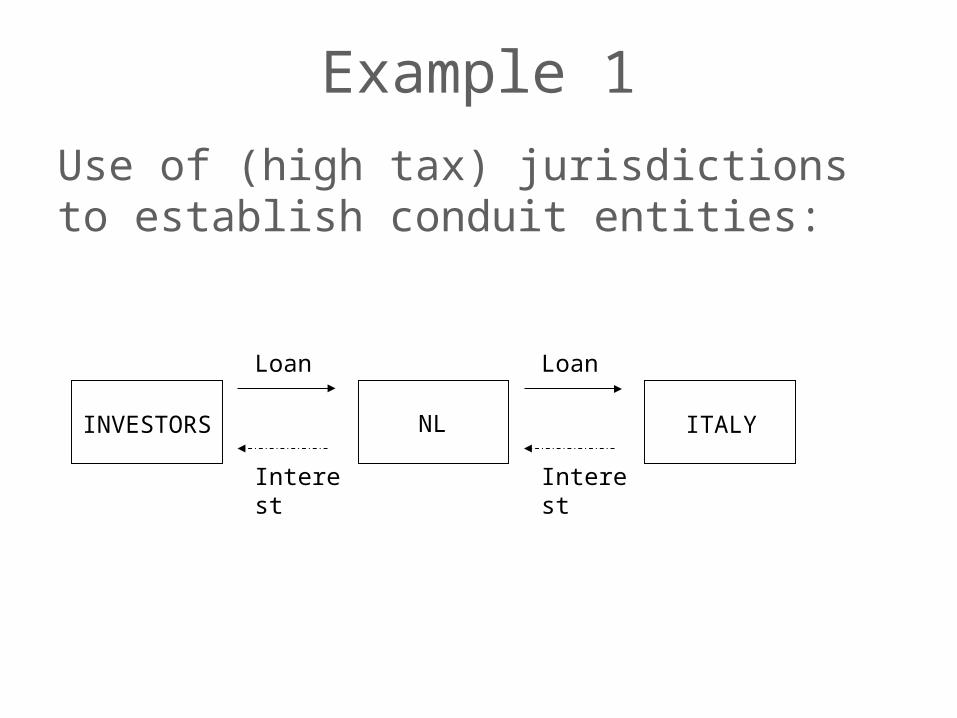

Example 1

Use of (high tax) jurisdictions to establish conduit entities:

Loan Loan

Interest Interest

NLINVESTORS ITALY

Discussion

Transfer pricing Treaty application Limitation on Benefits ? Concept of Beneficial Ownership

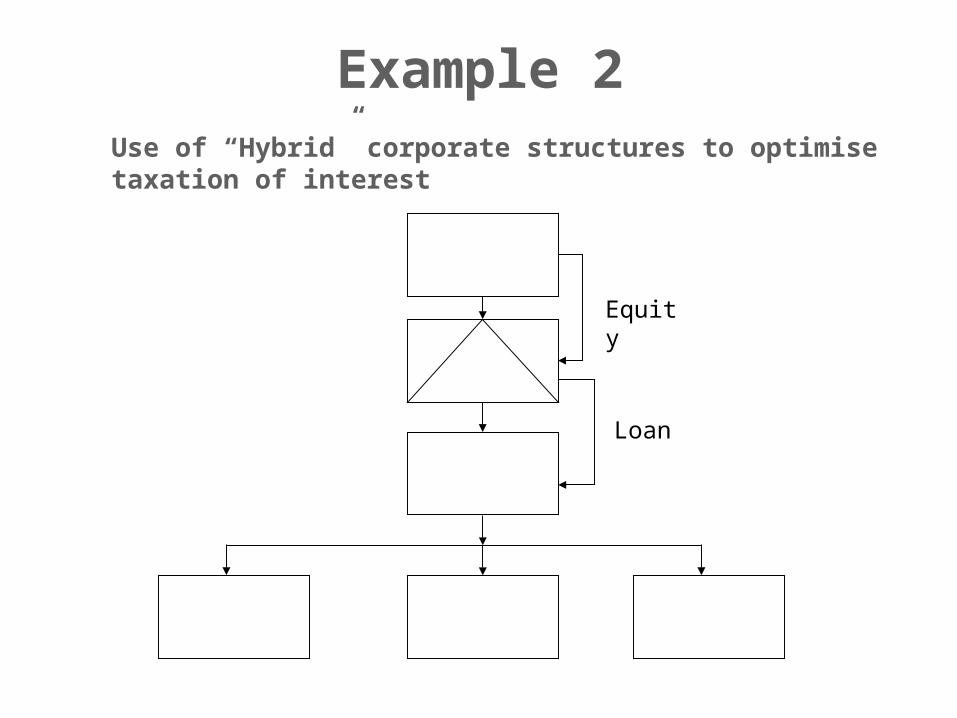

Example 2Use of “Hybrid” corporate structures to optimise taxation of interest

Equity

Loan

Discussion

Qualification legal entities in multiple jurisdictions

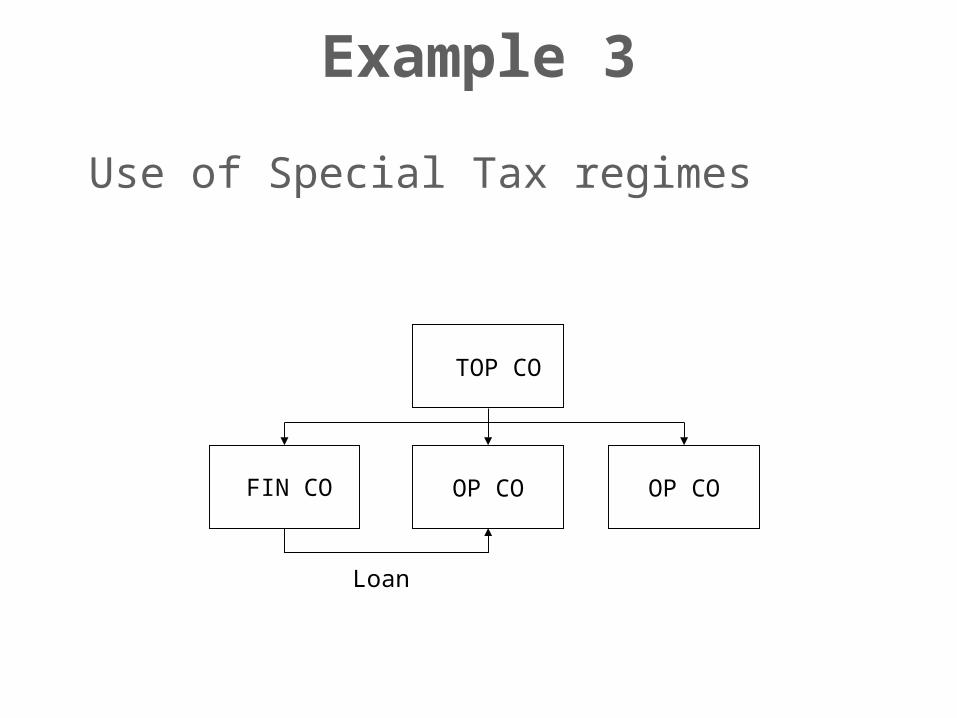

Example 3

Use of Special Tax regimes

OP CO

TOP CO

FIN CO OP CO

Loan

Discussion

Jurisdiction of establishment of FinCo Tax Haven/Non Tax Haven

What Threats do U.S. and OECD Reforms Pose to Global Foreign Direct Investments?

Michael A. SilvaInternational Tax Partner Hunton & Williams LLP

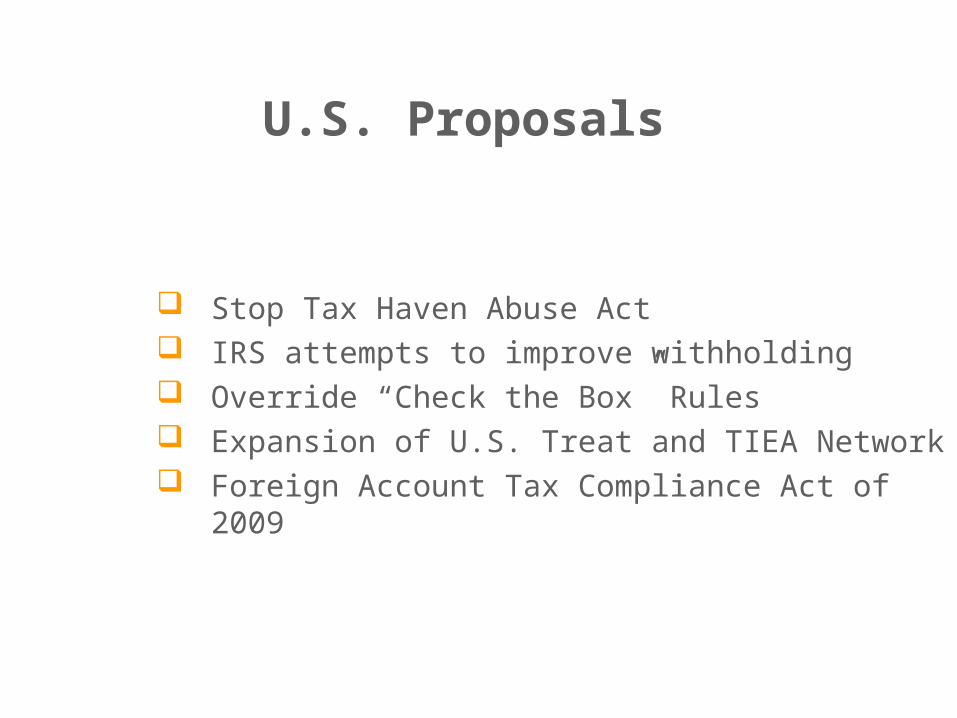

Stop Tax Haven Abuse Act IRS attempts to improve withholding Override “Check the Box” Rules Expansion of U.S. Treat and TIEA Network Foreign Account Tax Compliance Act of 2009

U.S. Proposals

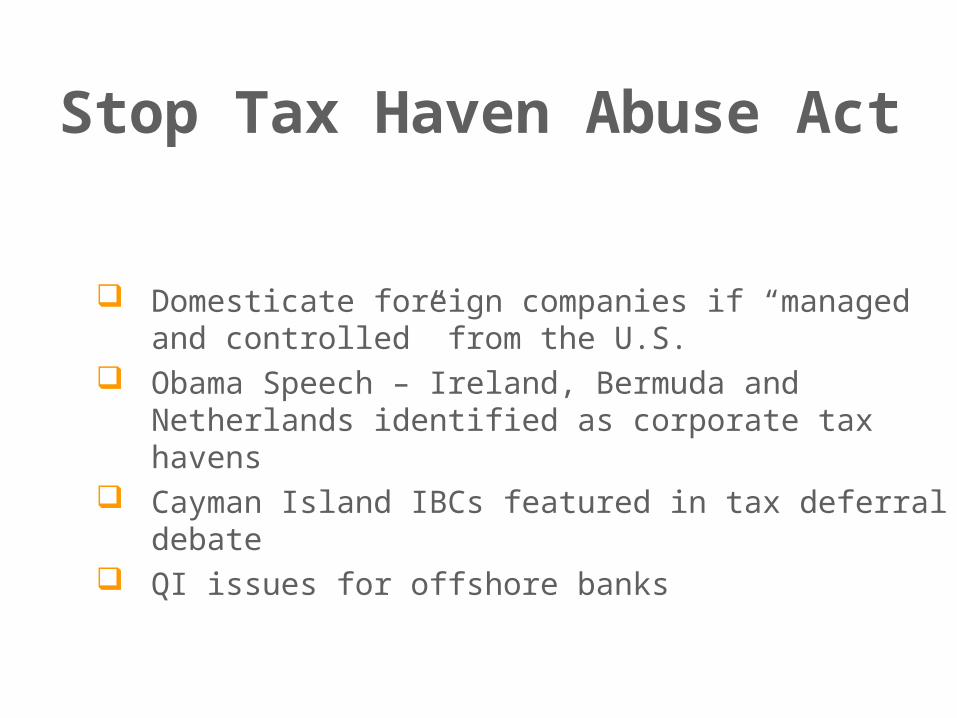

Domesticate foreign companies if “managed and controlled” from the U.S.

Obama Speech – Ireland, Bermuda and Netherlands identified as corporate tax havens

Cayman Island IBCs featured in tax deferral debate QI issues for offshore banks

Stop Tax Haven Abuse Act

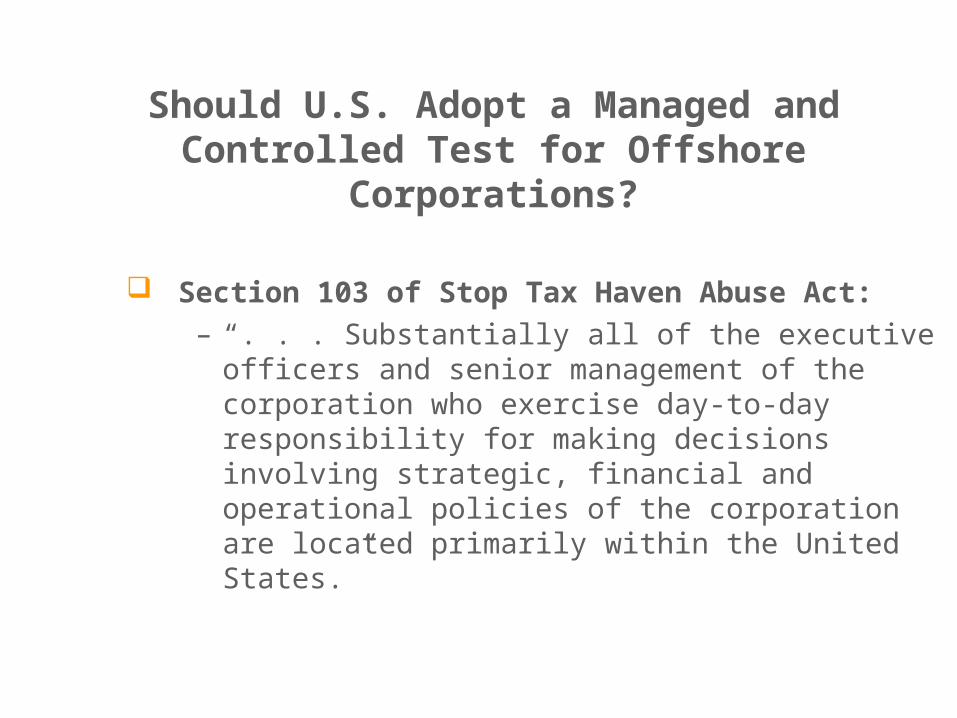

Section 103 of Stop Tax Haven Abuse Act:– “. . . Substantially all of the executive officers and

senior management of the corporation who exercise day-to-day responsibility for making decisions involving strategic, financial and operational policies of the corporation are located primarily within the United States.”

Should U.S. Adopt a Managed and Controlled Test for Offshore Corporations?

France-U.S. Protocol New Zealand – U.S. Income Tax Treaty Malta-U.S. Income Tax Treaty

2009 Tax Treaty Network Expansion

The OECD / G20 view

Stephan Neidhardt Walder Wyss & Partners Ltd. Zurich

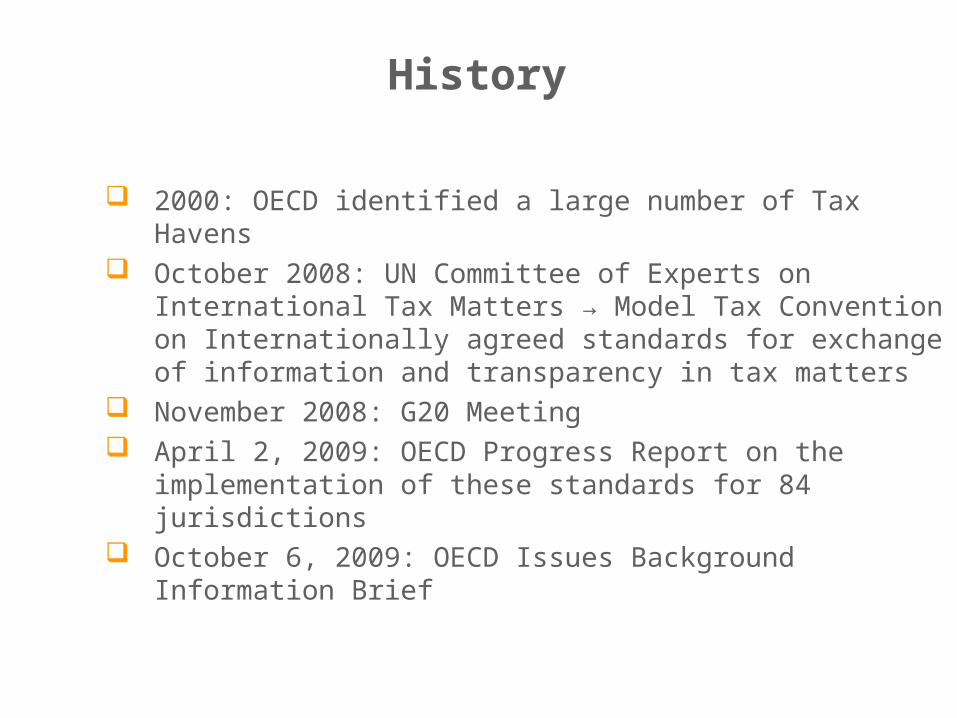

History

2000: OECD identified a large number of Tax Havens October 2008: UN Committee of Experts on

International Tax Matters → Model Tax Convention on Internationally agreed standards for exchange of information and transparency in tax matters

November 2008: G20 Meeting April 2, 2009: OECD Progress Report on the

implementation of these standards for 84 jurisdictions October 6, 2009: OECD Issues Background

Information Brief

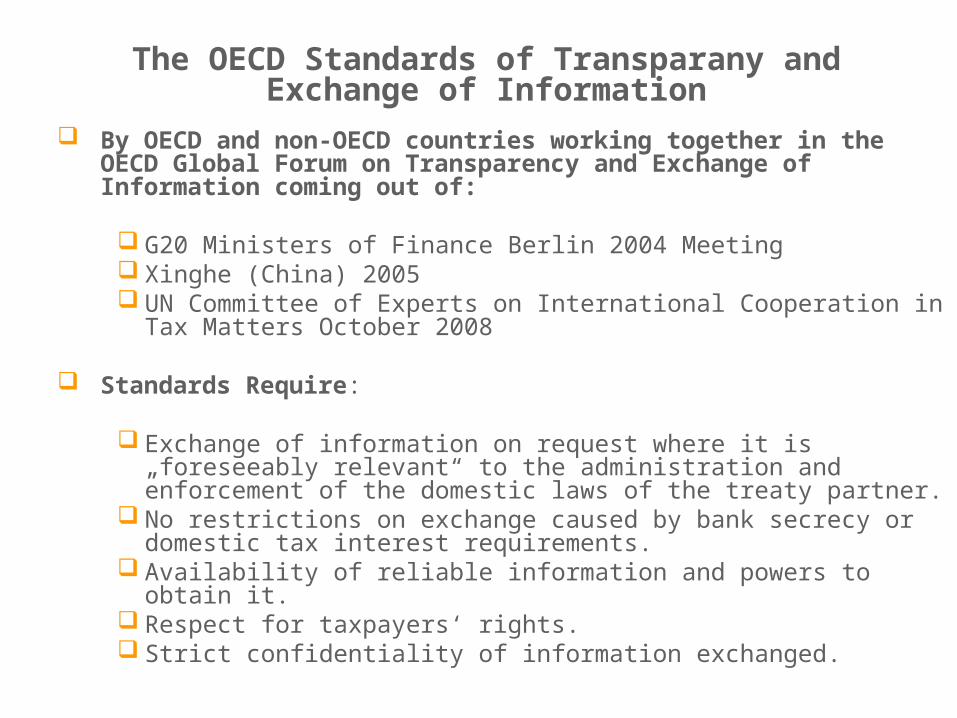

The OECD Standards of Transparany and Exchange of Information

By OECD and non-OECD countries working together in the OECD Global Forum on Transparency and Exchange of Information coming out of:

G20 Ministers of Finance Berlin 2004 Meeting Xinghe (China) 2005 UN Committee of Experts on International Cooperation in Tax

Matters October 2008

Standards Require:

Exchange of information on request where it is „foreseeably relevant“ to the administration and enforcement of the domestic laws of the treaty partner.

No restrictions on exchange caused by bank secrecy or domestic tax interest requirements.

Availability of reliable information and powers to obtain it. Respect for taxpayers‘ rights. Strict confidentiality of information exchanged.

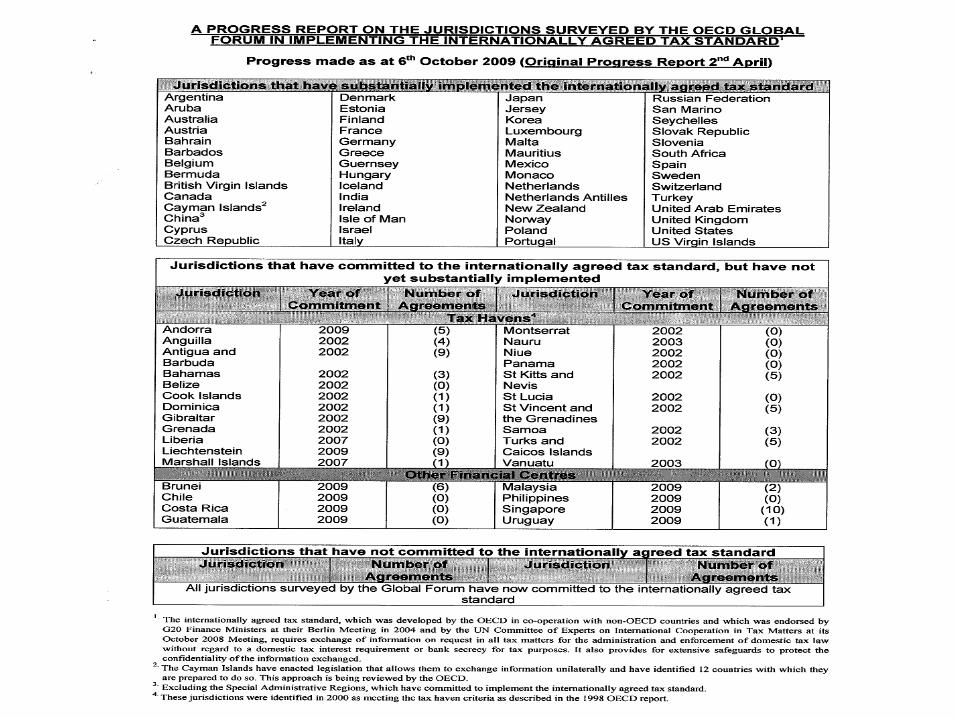

III. The List

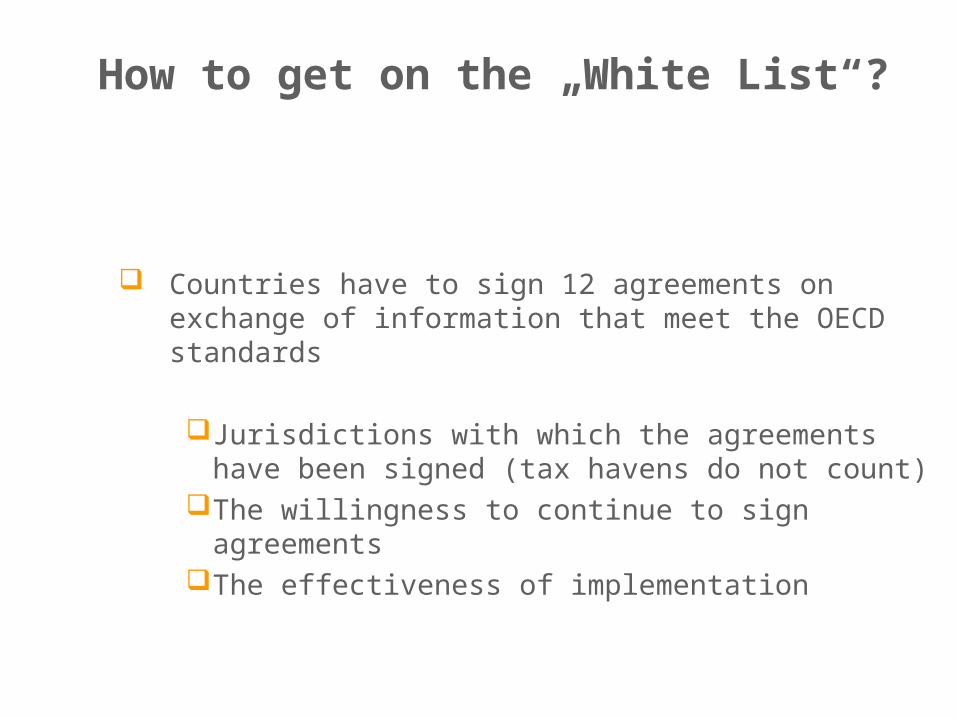

How to get on the „White List“?

Countries have to sign 12 agreements on exchange of information that meet the OECD standards

Jurisdictions with which the agreements have been signed (tax havens do not count)

The willingness to continue to sign agreementsThe effectiveness of implementation

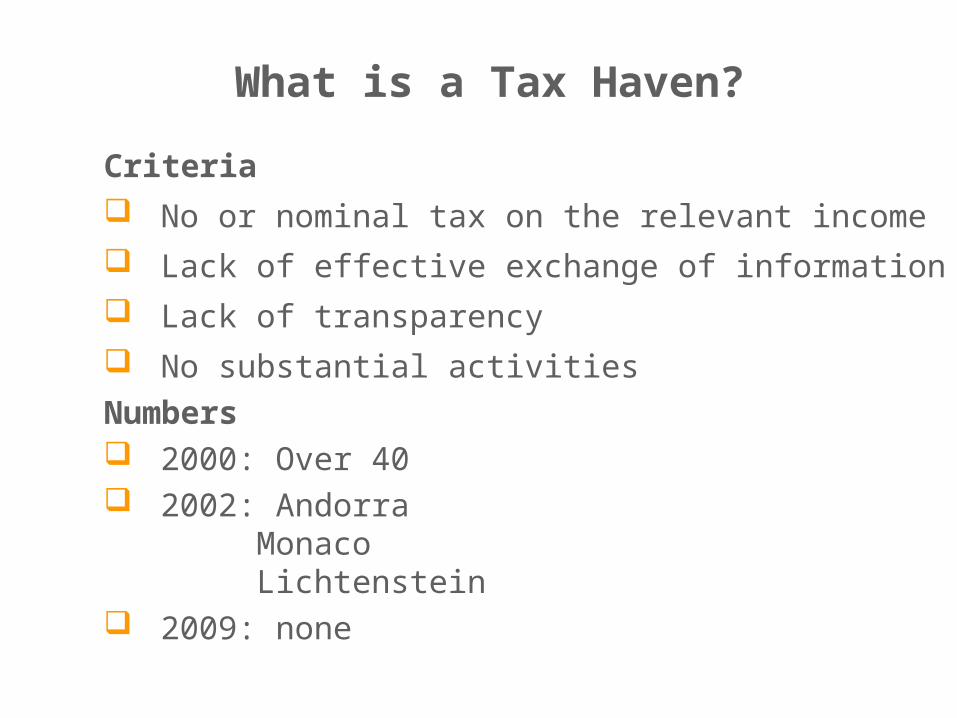

What is a Tax Haven?

Criteria

No or nominal tax on the relevant income

Lack of effective exchange of information

Lack of transparency

No substantial activities

Numbers 2000: Over 40 2002: Andorra

MonacoLichtenstein

2009: none

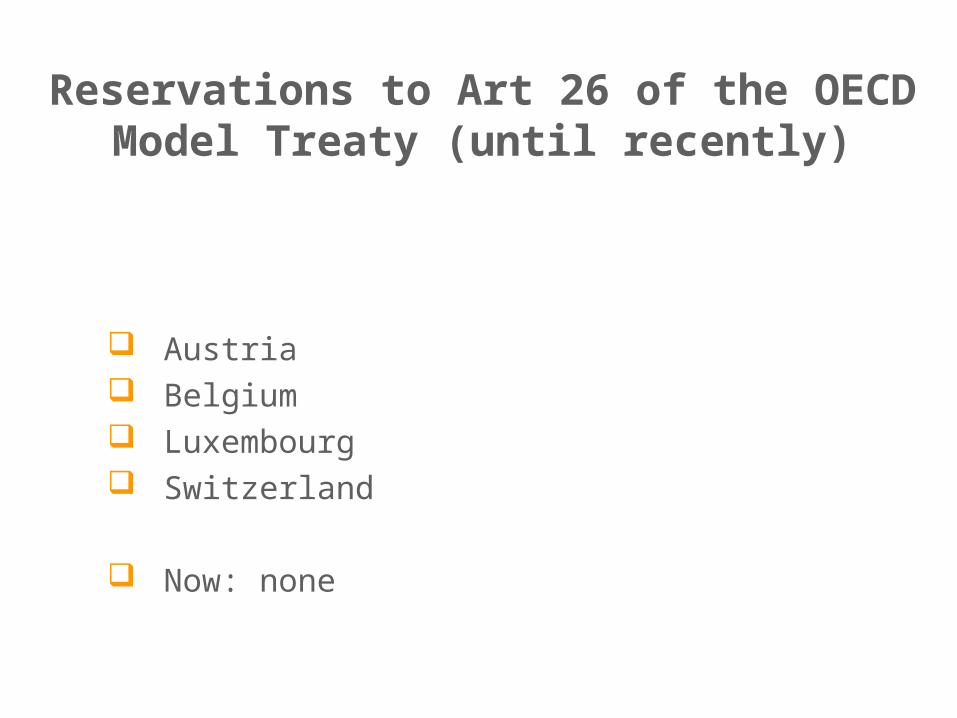

Austria Belgium Luxembourg Switzerland

Now: none

Reservations to Art 26 of the OECD Model Treaty (until recently)

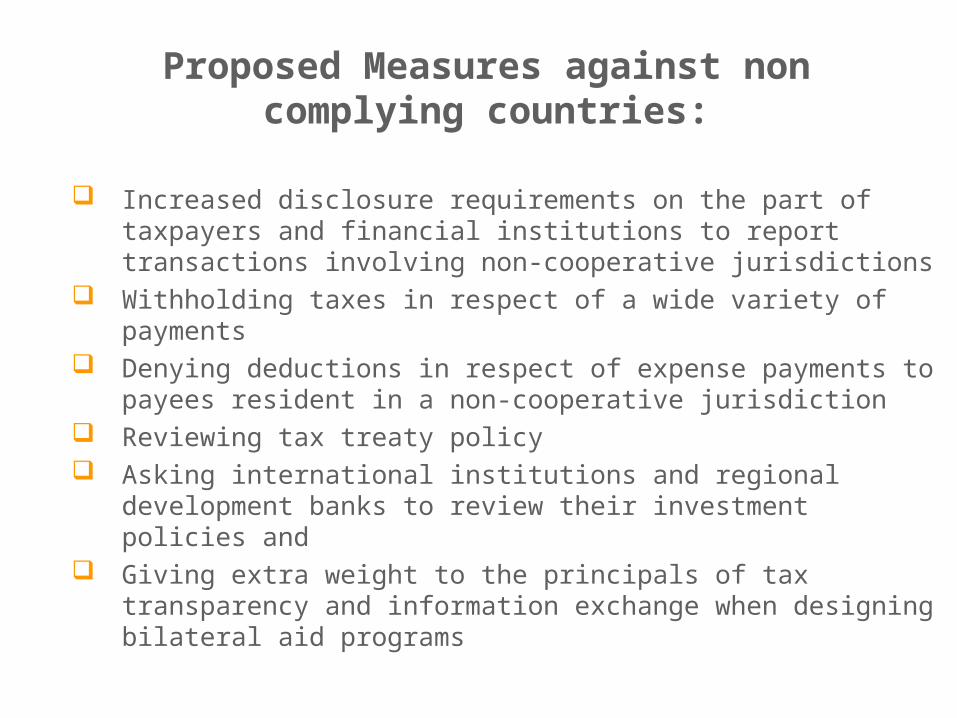

Increased disclosure requirements on the part of taxpayers and financial institutions to report transactions involving non-cooperative jurisdictions

Withholding taxes in respect of a wide variety of payments Denying deductions in respect of expense payments to payees

resident in a non-cooperative jurisdiction Reviewing tax treaty policy Asking international institutions and regional development

banks to review their investment policies and Giving extra weight to the principals of tax transparency and

information exchange when designing bilateral aid programs

Proposed Measures against non complying countries:

Summary

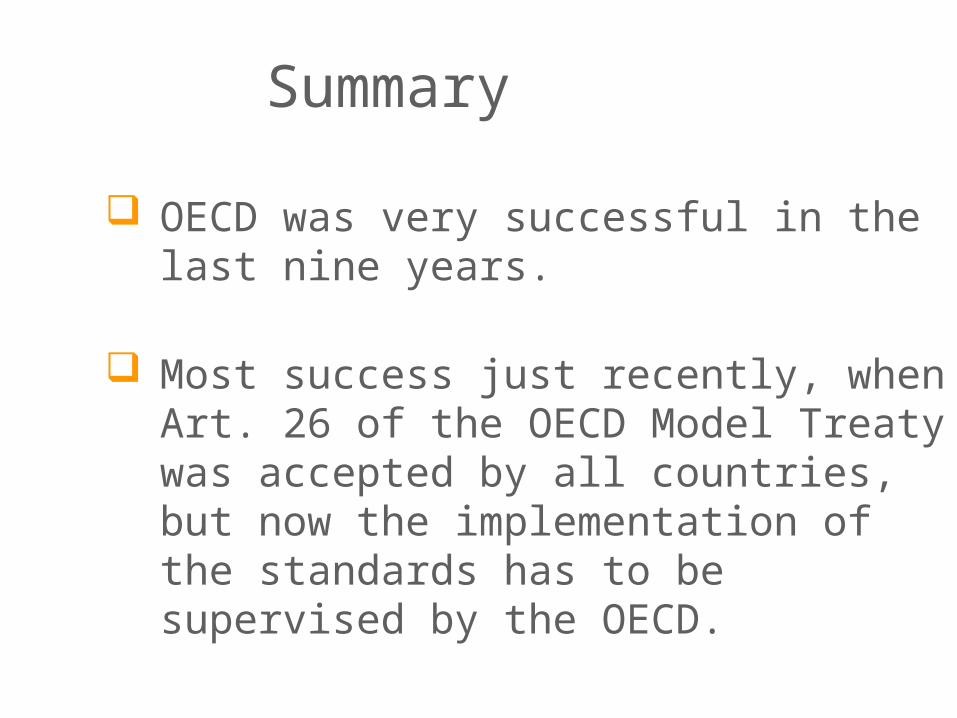

OECD was very successful in the last nine years.

Most success just recently, when Art. 26 of the OECD Model Treaty was accepted by all countries, but now the implementation of the standards has to be supervised by the OECD.

The Offshore Perspective

Michael BurnsAppelby

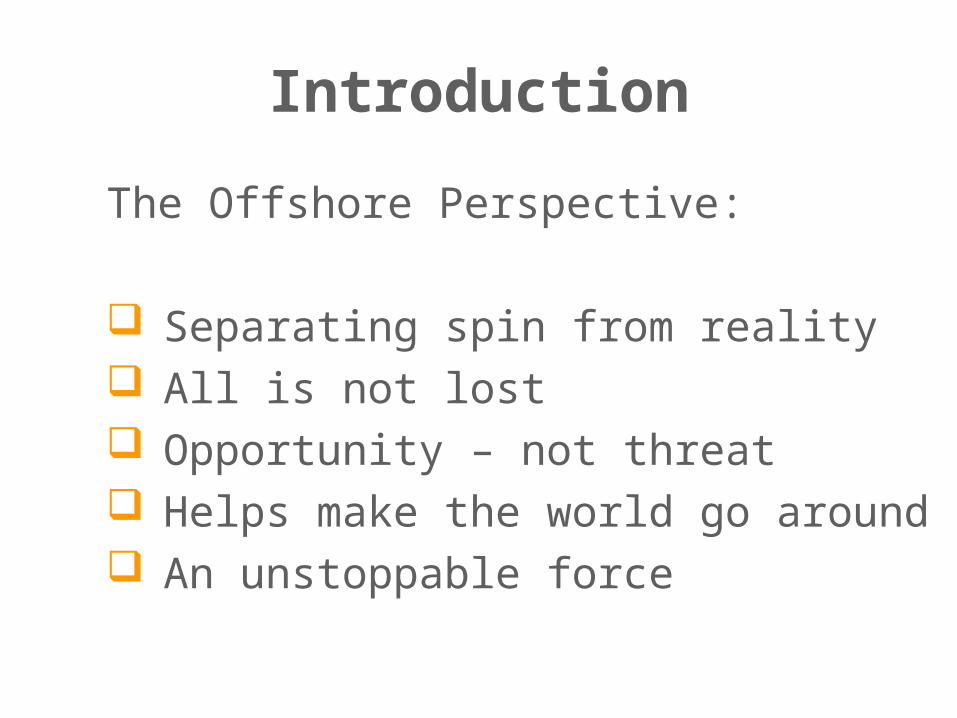

Introduction

The Offshore Perspective:

Separating spin from reality All is not lost Opportunity – not threat Helps make the world go around An unstoppable force

Fact: Tax neutrality, not tax evasion or avoidance

Investors and their advisors choose offshore financial centres (“OFCs”) for tax neutrality, not tax evasion or avoidance

OFC entities provide a tax-neutral platform so that investors from several jurisdictions are not subject to additional layers of foreign taxation to those imposed by their home country.

Investors remain subject to tax in accordance with the codes of their own jurisdictions

Fact: OFC entities required for international business

Global financial system needs legal entities to be formed in a stable jurisdiction on a tax-neutral basis

Multinational companies, investment banks and fund managers are often required to accommodate investors from all over the world

Fact: OFCs to play key role in global economic recovery

Investment funds allow international institutional investors to invest in government and sovereign debt

Provide microfinance loan facilities to small businesses in developing countries often with the help of institutions like the World Bank or other national development aid organizations and agencies

Fact: OFCs to play key role in global economic recovery

Enable syndicates of international banks to make secured loans to finance power and other infrastructure projects in developing countries

Take part in the U.S. government's TARP and related schemes designed to encourage private investors to buy "toxic assets" from banks to help free up their balance sheets to allow them to recommence lending

Summary

OFC’s will continue to survive and will continue to serve the purpose of promoting the efficient deployment of international capital

Continuing future for OFC’s, as long as they comply with internationally accepted standards of transparency

Appleby’s jurisdictions are all on the White list Choice of jurisdiction largely dependent on the

nature of the business to be transacted

With all this …

… what is really the future for tax havens?

The toolbox availabke Accepted use of tax havens Future outlook

DISCUSSION!!Or?

![Finale 2002 - [15-1749H Spiritual Jubilee (SATB).MUS] · SATB Chorus and Piano* Bass Brightly q = 112 1. 6 down by the riv - er-side, doom doom doom doom doom ... We are climb - ing,](https://img.pdfslide.us/doc/110x75/5b2410317f8b9a9a028b5148/finale-2002-15-1749h-spiritual-jubilee-satbmus-satb-chorus-and-piano.jpg)