Embed Size (px)

Citation preview

The Digital Operator How do operators transform to a full Service Strategy

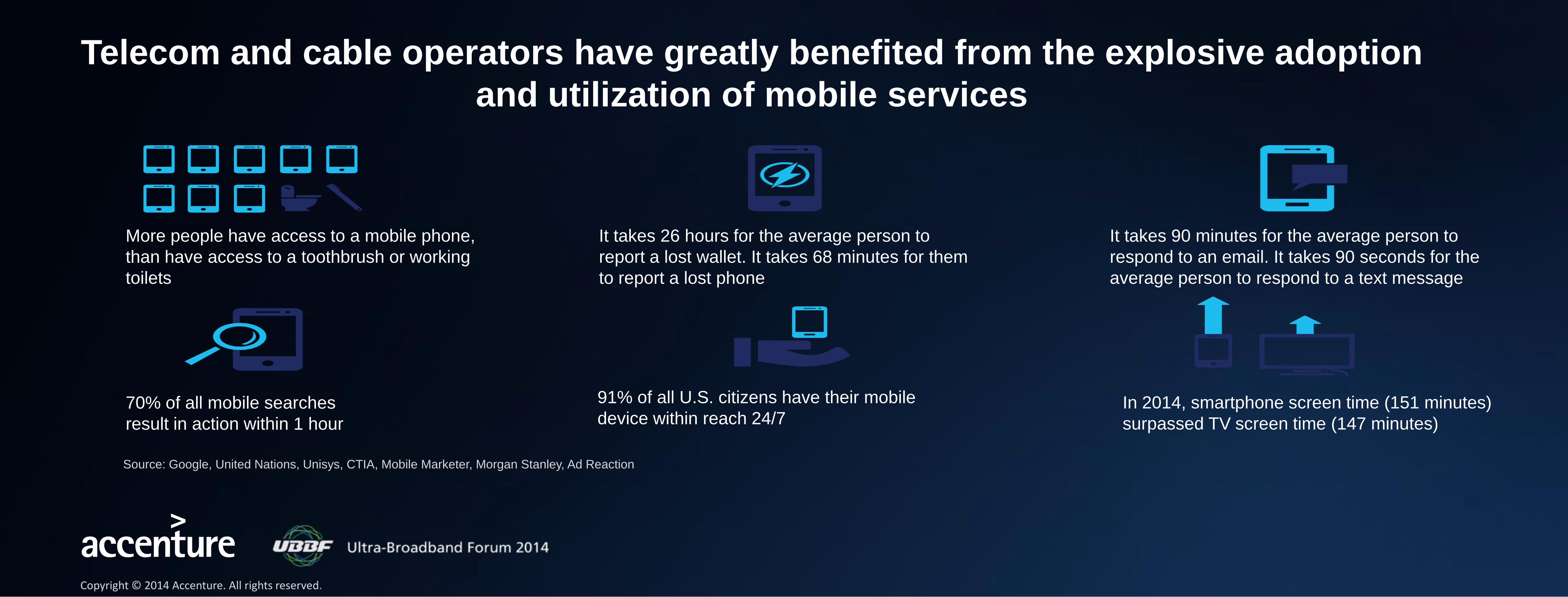

Telecom and cable operators have greatly benefited from the explosive adoption

and utilization of mobile services

More people have access to a mobile phone,

than have access to a toothbrush or working

toilets

It takes 26 hours for the average person to

report a lost wallet. It takes 68 minutes for them

to report a lost phone

It takes 90 minutes for the average person to

respond to an email. It takes 90 seconds for the

average person to respond to a text message

70% of all mobile searches

result in action within 1 hour

91% of all U.S. citizens have their mobile

device within reach 24/7 In 2014, smartphone screen time (151 minutes)

surpassed TV screen time (147 minutes)

Source: Google, United Nations, Unisys, CTIA, Mobile Marketer, Morgan Stanley, Ad Reaction

Copyright © 2014 Accenture. All rights reserved.

However, digital is enabling new entrants to disrupt services traditionally

monetized by operators Traditional Operator Offerings Disruptors

Text Messaging

Voice Calling

Data Connectivity

Yellow Pages

Maps & dedicated GPS devices

Television

Location Based Services

Yet, only a few Operators have set up their organizations and capabilities to effectively capitalize digital services

Copyright © 2014 Accenture. All rights reserved.

Our recent consumer survey demonstrated a global demand for digital companies

as alternatives to operators “If the following services were available from all of these providers, which providers would you consider using for each service?”

(if it were available)

Broadband Phone Calls Pay TV VoD Catch Up TV Broadband Phone Calls Messaging

In The Home Mobile

35%

29%

23% 27%

24%

32%

24% 26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Apple

Microsoft

Amazon

Samsung

Copyright © 2014 Accenture. All rights reserved.

Source: Accenture Digital Consumer Survey 2014

Not surprisingly, digital frontrunners are outperforming traditional operators

Serve Efficiently:

-29%

17% 21%

Telecom S&P 500 Technology

Sector Performance (Jul 30, 2013 – Jul 29, 2014)

Scale Rapidly:

Alter Economics:

64 billion messages per day, across

465 million users

Expanded from 50,000 users to 17

million in 9 months

Able to offers Maps for free to nearly

60M users a month

Source: Google Finance Analysis, WhatsApp, Amazon, comScore/Mashable

Note: Based on domestic equities and ADRs listed in US. 786

companies within Technology sector, including Apple, Microsoft,

Amazon and Google. 109 companies within Telecommunications

Services sector, including AT&T, CenturyLink, Verizon, Comcast.

Copyright © 2014 Accenture. All rights reserved.

New

Class of

Competitors

Six major digital trends are having an impact on operators.

1 2 3 4 5 6

Living Services

Wave

Shared

Customer

Competition

at the

Network Edge

The Great

Unbundling The New Scale

Copyright © 2014 Accenture. All rights reserved.

New Class of Competitors

PC

Tab

let

Ph

on

e

TV

Devic

e

s

Ap

ps

Bro

ws

er

OS

HW

Desig

n

Se

mi

IP

Me

dia

Ma

pp

i

ng

Se

arc

h

Sto

rag

e /

Ho

sti

n

g

Ma

rket

pla

ce

Ap

p

Dev

Clo

ud

Dev

Vo

ice /

Ms

g

Data

Care

Data

Acce

s

s

Se

rvic

es

Devices Platforms Cloud Services Dev Operators Services

20

08

20

10

2

01

4

Copyright © 2014 Accenture. All rights reserved.

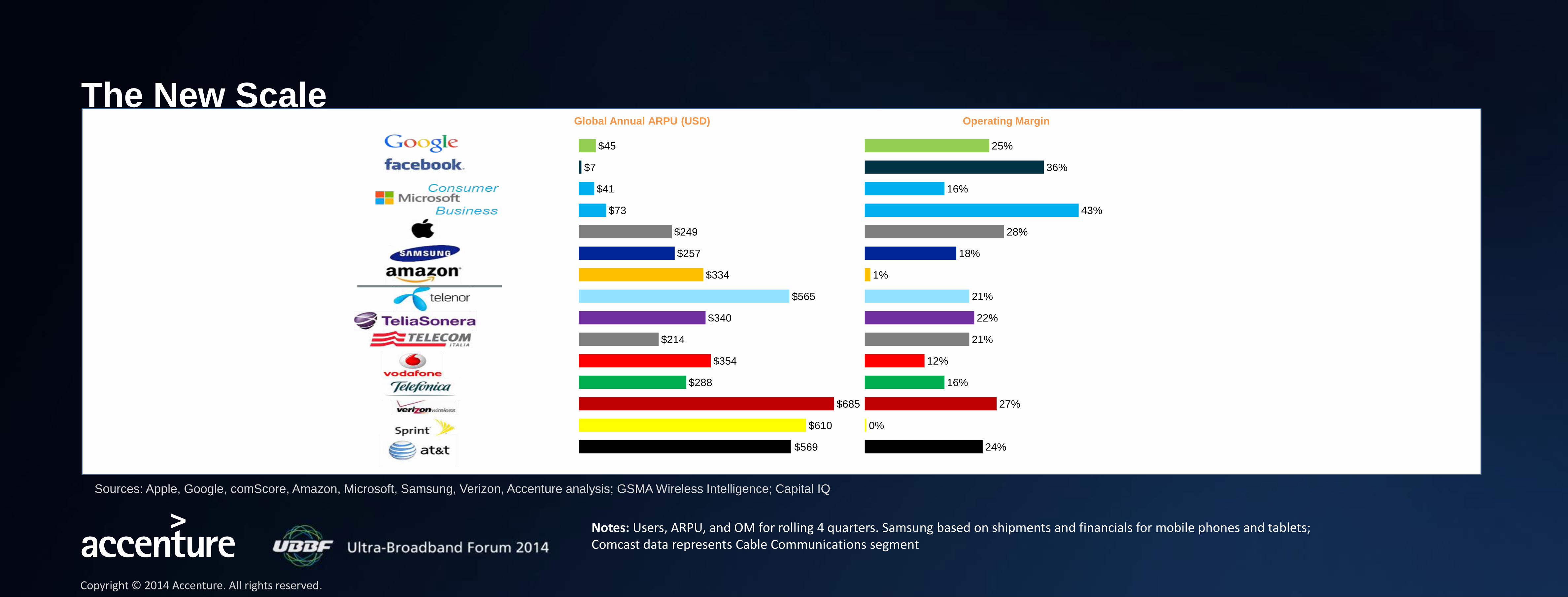

The New Scale

Sources: Apple, Google, comScore, Amazon, Microsoft, Samsung, Verizon, Accenture analysis; GSMA Wireless Intelligence; Capital IQ

Copyright © 2014 Accenture. All rights reserved.

$569

$610

$685

$288

$354

$214

$340

$565

$334

$257

$249

$73

$41

$7

$45

24%

0%

27%

16%

12%

21%

22%

21%

1%

18%

28%

43%

16%

36%

25%

Global Annual ARPU (USD) Operating Margin

Notes: Users, ARPU, and OM for rolling 4 quarters. Samsung based on shipments and financials for mobile phones and tablets; Comcast data represents Cable Communications segment

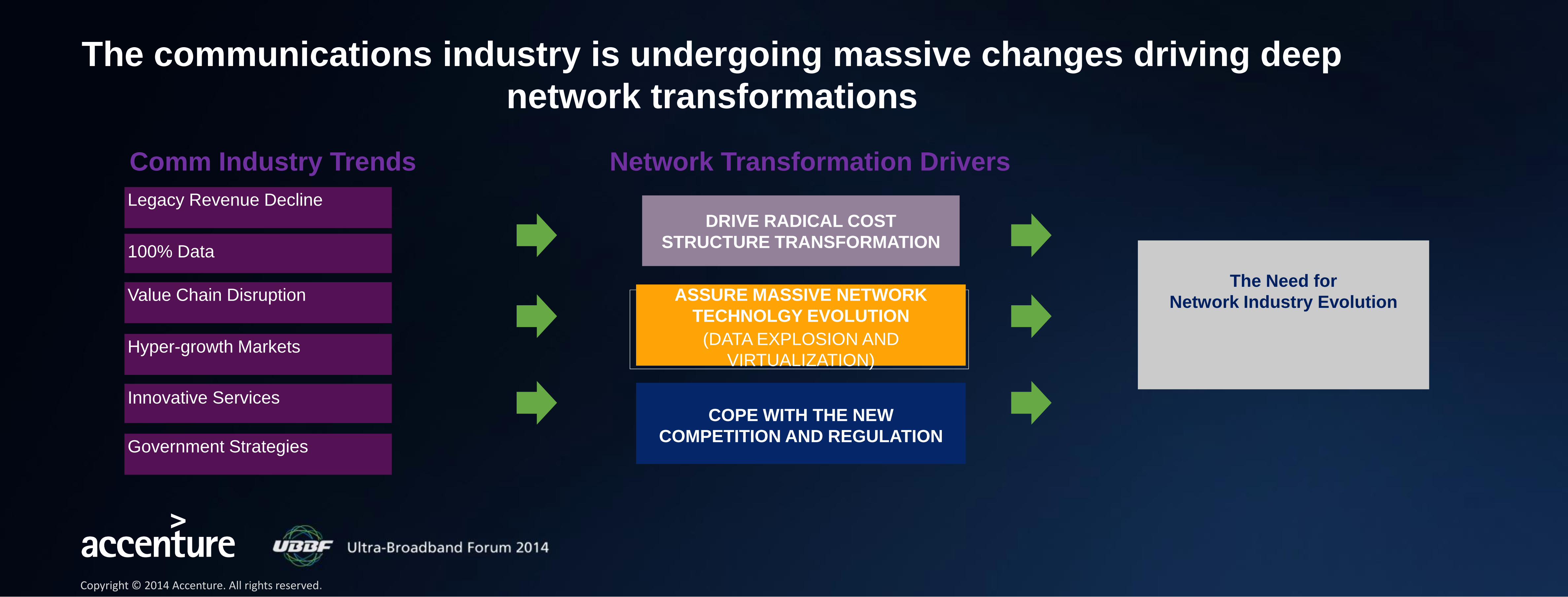

The communications industry is undergoing massive changes driving deep

network transformations

Legacy Revenue Decline

100% Data

Value Chain Disruption

Hyper-growth Markets

Innovative Services

Government Strategies

Comm Industry Trends Network Transformation Drivers

The Need for

Network Industry Evolution

DRIVE RADICAL COST

STRUCTURE TRANSFORMATION

ASSURE MASSIVE NETWORK

TECHNOLGY EVOLUTION

(DATA EXPLOSION AND

VIRTUALIZATION)

COPE WITH THE NEW

COMPETITION AND REGULATION

Copyright © 2014 Accenture. All rights reserved.

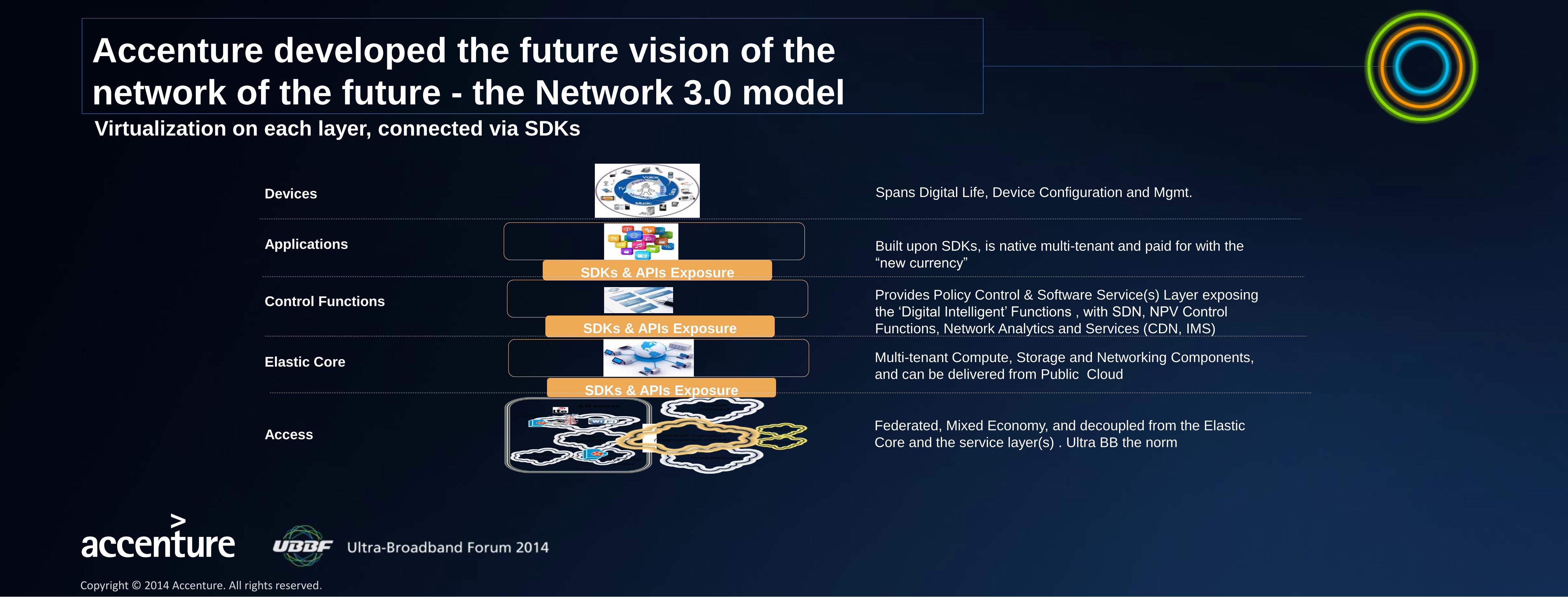

Virtualization on each layer, connected via SDKs

Accenture developed the future vision of the

network of the future - the Network 3.0 model

SDKs & APIs Exposure

SDKs & APIs Exposure

SDKs & APIs Exposure

Spans Digital Life, Device Configuration and Mgmt.

Built upon SDKs, is native multi-tenant and paid for with the

“new currency”

Provides Policy Control & Software Service(s) Layer exposing

the ‘Digital Intelligent’ Functions , with SDN, NPV Control

Functions, Network Analytics and Services (CDN, IMS)

Multi-tenant Compute, Storage and Networking Components,

and can be delivered from Public Cloud

Federated, Mixed Economy, and decoupled from the Elastic

Core and the service layer(s) . Ultra BB the norm

Devices

Applications

Control Functions

Elastic Core

Access

Copyright © 2014 Accenture. All rights reserved.

Accenture will help our Telco and NEP clients leveraging our new Business

Services that will bridge the transformation to the new world

Network Industry Evolution - Technology and Ecosystem Discontinuity

+ New multivendor

integration skills

Complex and

multivendor

environments

(“ALL IP”)

E///

Huawei

Samsung Oracle

ALU

All IP

transformation

Software Network &

Virtualization HW

VIRTUAL

SW Software defined

networks on virtual

environments

(“SDN+NFV”)

+ SW engineering &

integration skills

The new NETWORK SPACE The Old World

Single-Vendor, vertical and closed Silos (“turn key” solutions) Multi-Vendor, horizontal and open Platforms (“multi players” solutions)

…. Nokia

ACCENTURE

Copyright © 2014 Accenture. All rights reserved.

The Network Industry Evolution will be enabled by a fundamental shift in the

market: “THE DIGITAL NETWORK”

Today Target

INFRASTRUCTURE DRIVEN NETWORK

SOFTWARE & INTEGRATION DRIVEN NETWORK

Legacy Sunset

New Digital Network Architecture

Born of the Lean Operating Model

OSS 2.0

IP MIGRATION SERVICES

NETWORK ENGINEERING SERVICES

FIELD FORCE SERVICES

Copyright © 2014 Accenture. All rights reserved.

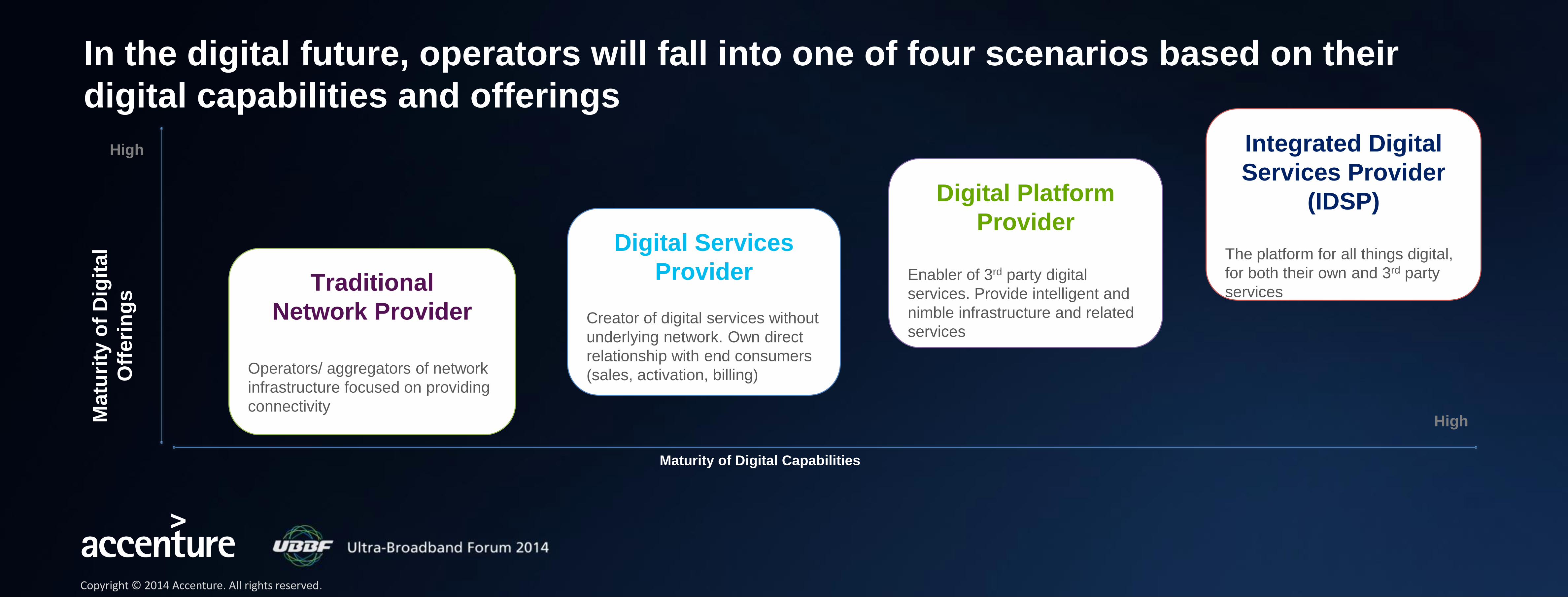

In the digital future, operators will fall into one of four scenarios based on their

digital capabilities and offerings

Digital Services

Provider Creator of digital services without

underlying network. Own direct

relationship with end consumers

(sales, activation, billing)

Integrated Digital

Services Provider

(IDSP)

The platform for all things digital,

for both their own and 3rd party

services

Traditional

Network Provider

Operators/ aggregators of network

infrastructure focused on providing

connectivity

Digital Platform

Provider

Enabler of 3rd party digital

services. Provide intelligent and

nimble infrastructure and related

services

Maturity of Digital Capabilities

High

High

Matu

rity

of

Dig

ital

Off

eri

ng

s

Copyright © 2014 Accenture. All rights reserved.

Our recommendation: Operators must strive to become Integrated Digital Service

Providers (IDSPs)

IDSP: Designed for Digital as a Business

Copyright © 2014 Accenture. All rights reserved.

IDSPs are Operators that are standing up infrastructure capabilities, operations and offerings to pursue digital as a business

Digital Business Operations & Capabilities

Digital Infrastructure Core

Digital Offerings

Becoming an IDSP will enable Operators to offer a new set of services and solutions

One-stop-shop for IT Virtual Interaction Provider Smart City Provider Road Tolling Partner

Digital Home Integrator Home Healthcare Integrator Customized Cloud Provider M2M Enabler Unleashes the full

entertainment experience in

every home

Takes care of your health Builds and maintains your own cloud Unleashes the power & intelligence

of connected machines

Services all your IT needs Enhances virtual interaction

with colleagues and customers

Partners with the government

to realize smart cities Provides secure, fast and

cost effective road tolling

Sample set of scenarios

Copyright © 2014 Accenture. All rights reserved.