Embed Size (px)

Citation preview

THE DETERMINATION PROCESS OF INDUSTRIAL PRICES IN U.S.:

A Post Keynesian Approach

GYUN CHEOL GU1

September 1, 2009

Abstract This study investigates the pricing behavior of the U.S. manufacturing industry

by using Johansen’s cointegration method. It demonstrates that industrial prices, investment,

money wage and productivity were cointegrated in the four industries significantly and

meaningfully. In light of their competition environments and market structures compared with

those of the other industries, the empirical results in U.S. are shown to be not inconsistent with a

Post Keynesian theory.

Keywords Price determination, U.S. manufacturing industry, Post Keynesian Model

JEL Classification L11, L60

1 The author is a PhD student in Department of Economics at the University of Missouri at Kansas City. E-mail address is [email protected]. The author wishes to thank Professor Lee and Professor Eaton for a number of suggestions that have helped to significantly improve this paper. All errors remain the author’s own.

2

I. INTRODUCTION

The neoclassical price theory is predicated on unrealistic hypotheses concerning behaviors of

consumer and firm, and technology. To begin with, it needs to make a consumer keep the

transitive property which is fundamental to the whole consumer theory, and assume that each

consumer has a specific form of utility function to aggregate across consumer demand curves for

market demand curve. In addition, the neoclassical microeconomic theory requires that firm’s

marginal cost curve be increasing, which can allow for profit maximization under perfect

competition market condition (Lee and Keen 2004). Even in the neoclassical monopoly model, it

needs to maintain the assumptions on consumer behaviors in order to attain the elasticity of

demand as well as market demand function, which means that the relatively realistic monopoly

model cannot avoid the same critiques, either.

The neoclassical theory has been accused by heterodox theorists of being at odds with

real-world observations. Heterodox microeconomists argue that a completely different approach

to pricing theory is needed, which is supposed to be predicated on realistic understandings of the

nature of decision-making by an enterprise, in particular, run in an oligopolistic market

environment characterized by mutual interdependence. One of them is cost-markup pricing model,

which is extended to incorporate firm’s economic activities by Eichner and Moss. In light of the

theory, I shall show how well the Post Keynesian framework can explain the real world by

empirical study using cointegrating vectors and vector error correction model.

The organization of the paper is as follows. In Section II, we review Eichner-version of

Post Keynesian theory critically and discuss particular theoretical issues on a theory of enterprise

pricing. Section III investigates previous empirical studies and their limitations as a starting point.

Section IV provides econometric methodology and empirical results consistent with the theory.

Section V discusses the findings and suggests some possible reasons for the behaviors of the main

3

economic variables. Section VI deals with the transformation of US economy and the slowdown

of accumulation. Lastly, Section VII concludes.

II. POST KEYNESIAN THEORY OF INDUSTRIAL PRICING

The most basic motivation of business enterprise is survival, which is for the reproduction and

continuation of it. Business enterprise must grow in order to survive under the context of

imperfect competition, more specifically in oligopolistic market characterized by mutual

interdependence2 (Eichner 1976 and Lavoie 1992). This interdependence forces the business

enterprise to make a strategic decision about its investment and thus prices. Most of the Post

Keynesian theories of industrial pricing are predicated upon realistic assumptions reflecting

actual conditions in oligopolistic industries and applying to the prevailing type of enterprises in

most industries.

For a better understanding of how prices are set under oligopoly it is necessary to

examine the conditions impinging upon the industry at large as well as the individual firm over

the long run. Analyzing the oligopolistic industry is tantamount to dealing with the strategic

behaviors of the involved players, in particular, the megacorp-price leader as the surrogate for its

fellow oligopolists in the industry since the common interest among them is to avoid price

competition that would be destructive to all its members. Furthermore, the analysis needs to shed

light on the mechanism through which the industry price set by the leader is acceptable to other

oligopolists in the same industry.

Eichner (1976) provides a pricing formula for oligopoly which is a refined version of

cost-plus approach. Under this formula, the ‘plus’ added to variable and fixed costs is called the

2 What the interdependence means is that no single member of the industry can expect to take action without evoking a response from the other firms which are its rivals.

4

corporate levy, which is required by the megacorp to finance its planned investment expenditures3.

Price should be changed reflecting a change in any of the pricing formula’ components, and thus

assuming variable and fixed costs remain constant the change in price should be a result of a

change in the required corporate levy, which reflects the megacorp’s cost of internally generated

investment funding. Therefore, “the pricing decision in an oligopolistic industry is intimately

bound up with the capital accumulation process” (Eichner 1976, p.56). This linking of the price

level to the industry’s investment program is the most important feature of the Eichner’s

microeconomic model.

In this model, the megacorp price leader can alter intertemporal revenue flow by using

the price variable, which means that it can increase the margin above costs in order to obtain

more internally generated investment funds because of the existence of collective monopolistic

rent. Eichner (1976, p.56) suggests that the real cost is what constrains the price leader from

increasing the industry price level and securing additional internal investment funds. The cost

derives from the substitution effect, the entry factor and the possibility of meaningful government

intervention. Besides the internally generated funds for investment, the oligopolists can obtain

additional investment funds externally by issuing either fixed-interest obligations or equity shares

at the ‘permanent’ interest rate without being significantly affected by current money market

conditions. The extent to which a particular type of expenditure leads to a relatively high increase

in the total corporate levy realized hinges on the marginal efficiency of investment. There are four

types of investment expenditures, each of which can be supposed to promote the growth of the

internally generated funds over time. They can be categorized as follows: (a) the purchase of new

plant and equipment, (b) the differentiation of the industry’s product more sharply, (c) the

erection of higher barriers to entry, or (d) the creation of a more favorable public image. The

overall marginal efficiency of investment schedule provides the price leader’s total demand for

3 It is interchangeable with such terms as discretionary income, internally generated funds, and individual megacorp savings.

5

investment funds. Since the price leader enjoys a cost advantage, the other firms in the industry

will accept the price leader’s choice of price change and thus the change in price will then prevail

until at least the next pricing period.

However, according to Moss (1981), the problem with Eichner’s theory is that it is

applicable only to oligopolistic markets where a price leader has undisputable power to constrain

its peers from deviating from the price set by the leader. Moss (1981, p 162) argues that the price

leader must have some sort of market power4 to ensure that competitors follow its pricing

decisions, and then suggests markets to which the Eichner pricing theory is applicable as follows:

[T]he Eicher-Wood price theory applies to what were called ‘fixprice’ markets by Hicks

(1965) but not to those which he called ‘flexprice’markets. For in fixprice markets, prices

do not adjust in the short run to eliminate excess supplies and demands, while in flexprice

markets they do. Thus, the conditions in which Eichner-Wood price theory can be applid

are the same conditions that give rise to fixprice markets. The conditions in which

Eichner-Wood price theory cannot be applied are the same conditions that give rise to

flexprice markets.5

In the fixprice market fluctuations in stockholdings, queue lengths and production rates

resolve discrepancies between supplies and demands, whereas in the flexprice market such

difference are settled by such price coordination as neoclassical theory hinges on. This

differentiation of fixprice from flexprice market is just necessary condition for specifying the

applicability of Eichner’s theory.

4 Moss (1981) identifies market power with the ability systematically to eliminate the positive net cash flows of competitors, suppliers and/or customers in so far as that cash flow derives from, or depends upon, activities in the markets in which the holder of market power trades. 5 S. Moss, An Economic Theory of Business Strategy, 1981, p. 191

6

III. PREVISOUS EMPIRICAL STUDIES AND LIMITATIONS

Sen and Vaidya (1995) test the validity of the Post Keynesian model in India using methods of

cointegration, and demonstrated that industrial prices, the interest rate, investment, money wages,

and productivity were cointegrated. Using error correction models, they trace the short-run

dynamics of these five variables and argue that the empirical results are consistent with the Post

Keynesian theory. Cin (2005) investigates the pricing behavior of the subsectors of the Turkish

private manufacturing industry by using Johansen’s cointegration analysis. Cin argues that it is

found that prices, demand and unit wage cost demonstrate cointegration relations in 14 out of 16

subsectors in accordance with the expectation of the theory. Cin considers output in an industry as

a proxy for demand pressure. The output, however, includes foreign demand, which is

inconsistent with domestic wholesale price indices used as the dependent variable.

Bloch and Olive (1996) argues that the implication of fixed mark-up pricing that the rate

of change in domestic manufacturing prices is equal to the rate of change of unit production costs

receives qualified support from their empirical results for explaining pricing in Australian

manufacturing. Moreover, the pricing equation based on a fixed mark-up is found to provide the

most reasonable explanation of pricing behaviour for industries in which either the intensity of

domestic competition is high or there is little exposure to foreign competition.

Atesoglu (1997) provides a Post Keynesian explanation of U.S. inflation. The emphasis

of the modeling approach in explaining inflation is on the growth rate of wages relative to the

growth rate of labor productivity, i.e. the wage-cost markup model. Atesoglu (2000) finds a

positive cointegration relationship between income and autonomous expenditures, employment

and autonomous expenditures in wage units, inflation and rate of growth in unit labor costs, and

the money supply and autonomous expenditures. Atesoglu also argues that these results provide

rigorous empirical support for the Post Keynesian, demand-oriented explanation of income and

employment, the wage-cost model of inflation, and the endogeneity of the money supply thesis.

7

Two of the papers utilize highly aggregated variables for wage rate, productivity and inflation as

a whole. Indeed, there have been little studies on the price determination process by industrial

level in U.S.

IV. ECONOMETRIC METHODS AND EMPRICAL FINDINGS

Economic Model

According to Eichner (1976), there is a long-run relationship between industrial prices,

investment, money wages, and productivity. A rise in industrial prices can occur when firms

increase markups in order to generate internal funds for planned investment. Also, industrial

prices can rise when workers’ compensation increases more than productivity improvement. The

Wage-Cost Markup (WCM) provides a Post Keynesian functional framework which has been

discussed in the previous section:

, where P is the price index of a manufacturing industry, K is the profit markup, W is the

money wage per worker, and Z is labor productivity in the industrial sector.

The markup is assumed to be an increasing function of investment. The markup can be

affected by the wage and productivity since a firm would absorb a part of the increase in money

wages by reducing the markup; and the firm also has a strong incentive to maintain productivity

gains without price reductions (Sen and Vaidya 1995). That is, a part of the gains would be

retained for a higher corporate levy. Considering these factors, a general formulation of the

markup and the implied price equation would be as follows:

8

, where a2, a3 > 0.

Substituting equation (2) into K in (1) and taking log of both sides give us

Equation (3) is the equation to be estimated by MLE in VECM (Vector Error Correction Model).

The equation represents the long-run relationship between industrial price, investment, money

wage and labor productivity. The actual price may be greater or less than the price shown in the

equation.

It should be noted that the rate of interest is excluded from the determinants of the

markup, which has real effects on the result of Sen and Vaidya (1995). Most evidence shows that

the demand for credit are inelastic (or at times even perversely positive) with respect to the

general level of interest rates; and in a downturn, the expected returns to investment fall farther

and faster than market interest rates can be brought down (Wray 2004). Corbett and Jenkinson

(1997) investigates how physical investment has been funded in four countries over the period

1970 to 1994 and reports that Germany, UK and US are predominantly internally financed and

Japan has shown relatively higher level of bank finance as the second big part of investment fund,

of which the contribution has continued to fall. Moreover, Fazzari (1993) also argues that there is

no credible evidence that a negative relation between interest rate and the amount of investment.

Fazzari offers evidence that policies aimed at stimulating private sector investment through

interest rate reductions are, at best, misguided because of the nebulous effect of interest rates on

investment. Now that there is little evidence of relations between interest rate and private

investment, it can be ignored that interest rate can affect the size of markup through planning to

finance investment with borrowed funds from financial sector.

9

Data Source and Industries

Our data sample period runs from 1987 to 2006 annually and contains a total of 20 observations

for each industry. All data are taken from OECD STAN database. The STAN database for

industrial analysis includes annual measures of output, labor input, investment and international

trade. STAN is primarily based on member countries' annual National Accounts by activity tables

and uses data from other sources, such as national industrial surveys/censuses, to estimate any

missing detail. The current version of STAN is based on the International Standard Industrial

Classification of all Economic Activities, Revision 3 (ISIC Rev.3) and covers all activities

(including services).

The industry levels were chosen as specifically as possible according to the availability.

These industries are 15, 17, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 34, and 35 defined as follows:

15: FOOD PRODUCTS AND BEVERAGES 17: TEXTILES, TEXTILE PRODUCTS, LEATHER AND FOOTWEAR 20: WOOD AND PRODUCTS OF WOOD AND CORK 21: PULP, PAPER AND PAPER PRODUCTS 22: PRINTING AND PUBLISHING 23: COKE, REFINED PETROLEUM PRODUCTS AND NUCLEAR FUEL 24: CHEMICALS AND CHEMICAL PRODUCTS 25: RUBBER AND PLASTICS PRODUCTS 26: OTHER NON-METALLIC MINERAL PRODUCTS 27: BASIC METALS 28: FABRICATED METAL PRODUCTS, except machinery and equipment 29: MACHINERY AND EQUIPMENT, N.E.C 34: MOTOR VEHICLES, TRAILERS AND SEMI-TRAILERS 35: OTHER TRANSPORT EQUIPMENT

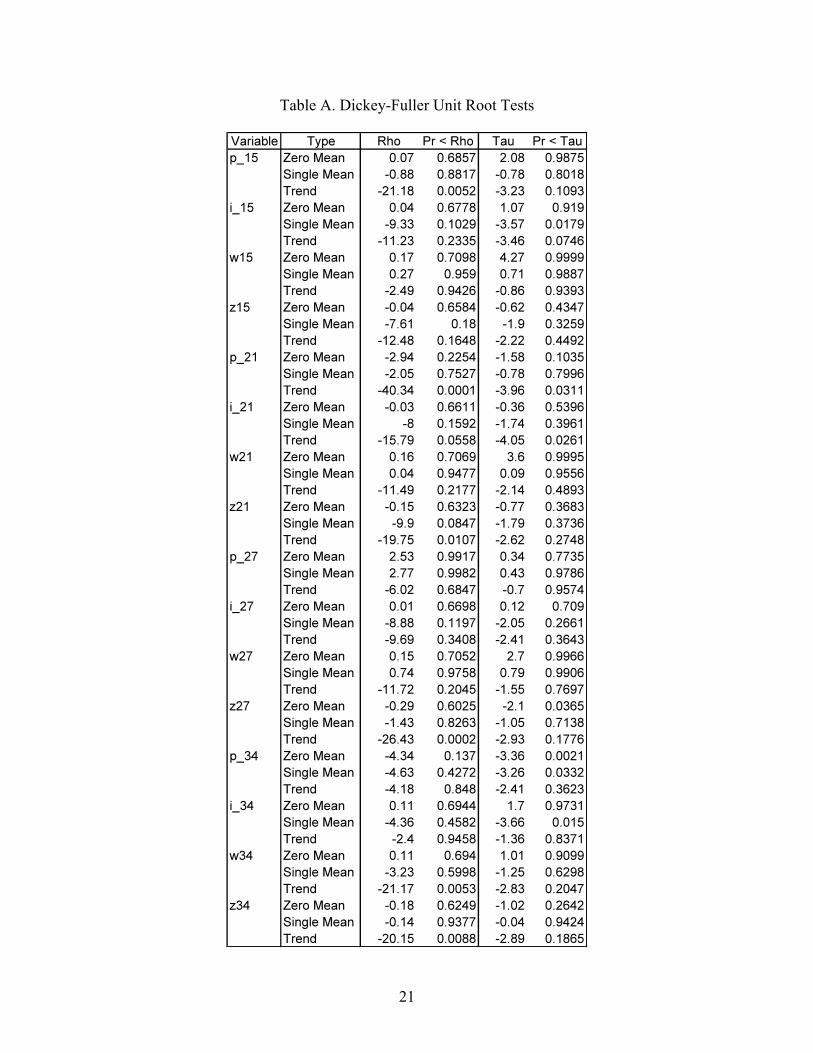

Unit Root Tests

The unit root tests are calculated and reported in the appendix. Dickey-Fuller (DF) unit root test,

Augmented Dickey-Fuller (ADF) test and Phillips and Perron (PP) test are investigated. Trend is

included, as these series contain clear trend, and lag lengths are chosen according to Akaike

information criterion (AIC). Accordingly, all the variables are integrated of order 1, i.e. I(1) in

10

accord with the usual expectation that many macroeconomic time series are non-stationary. The

results are shown in Table A on the appendix.

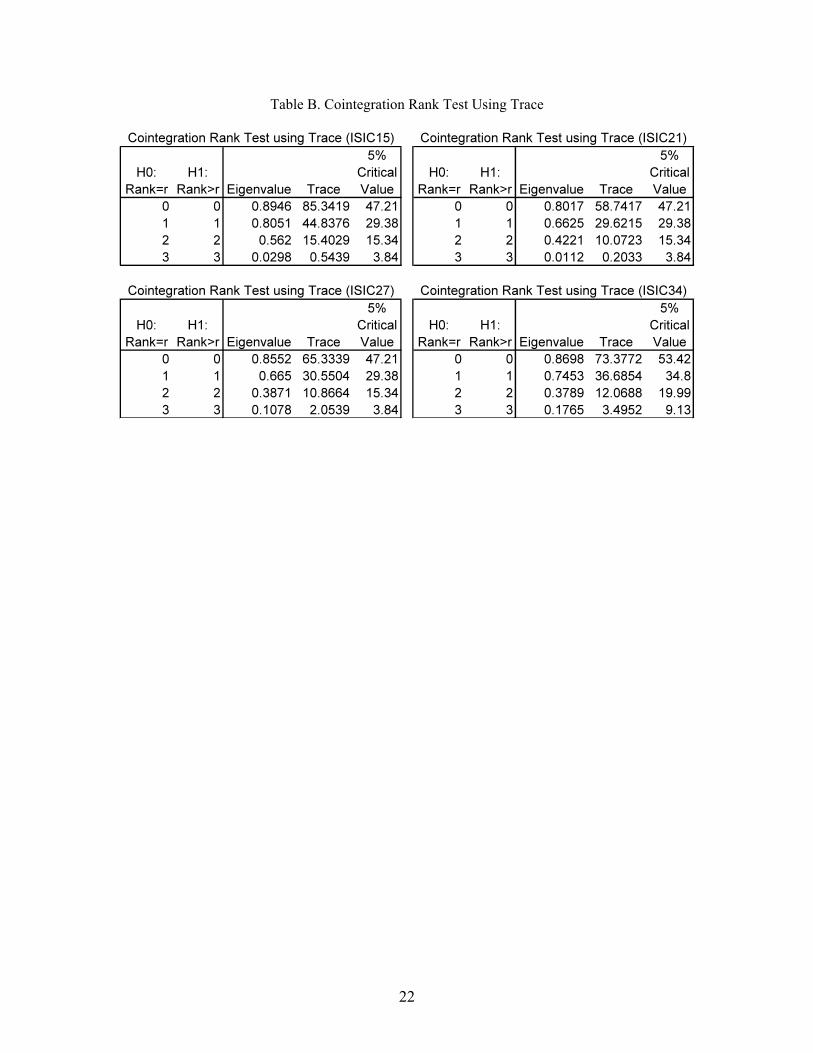

Cointegration Rank Tests

I employ the cointegration rank test developed by Johansen (1988) and Johansen and Juselius

(1990), which allows for the maximum likelihood multivariate cointegration technique.

According to Hansen and Juselius (1995), this method allows for testing various hypotheses more

appropriately than the other methods, even if some variables are I(0).

SAS Varmax procedure provides cointegration rank test using trace with and without

restriction, and also hypothesis test of the restriction. The result from hypothesis test of the

restriction indicates that there is a separate drift and no separate linear trend in the VECM form.

In light of the result as well as the graphs of the variables, the specification of deterministic trends

is determined as follows:

(4)

, where and

, is normalized adjustment parameters and is normalized cointegration coefficients

Johansen cointegration tests are applied for 14 industries of the U.S. manufacturing.

According to maximum eigenvalue and trace statistics, the existence of a long-run relationship

among prices, investment, wage and productivity is found in almost all the industries. Their

11

results of the cointegration tests are shown in Table B of the appendix6. The test statistics present

in Table B indicate that the hypothesis of no integration relationship can be rejected in 5%

significant level. Hence, there is at least one long-run relationship between p, i, w and z.

Moreover, the maximum likelihood estimator of in equation (4) is obtained from the

eigenvectors that correspond to the r largest eigenvalues. The cointegrating vectors are

normalized to coefficient of price variable p, and the long-run relationship can be written as

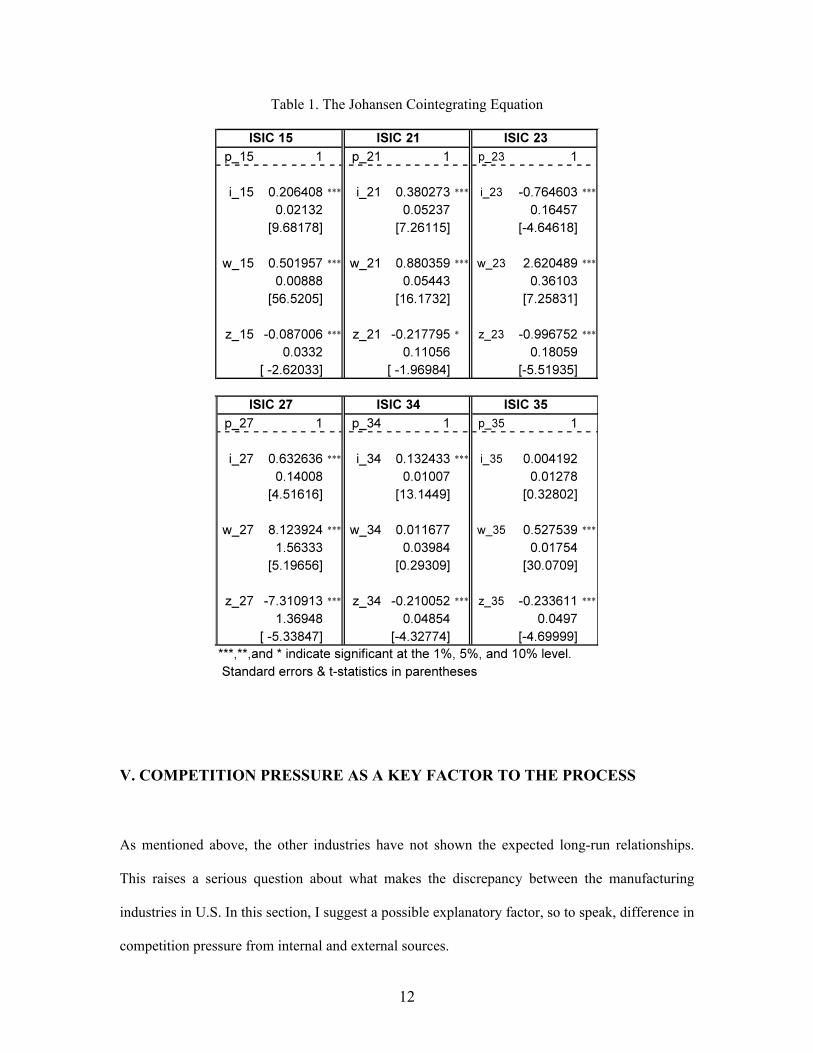

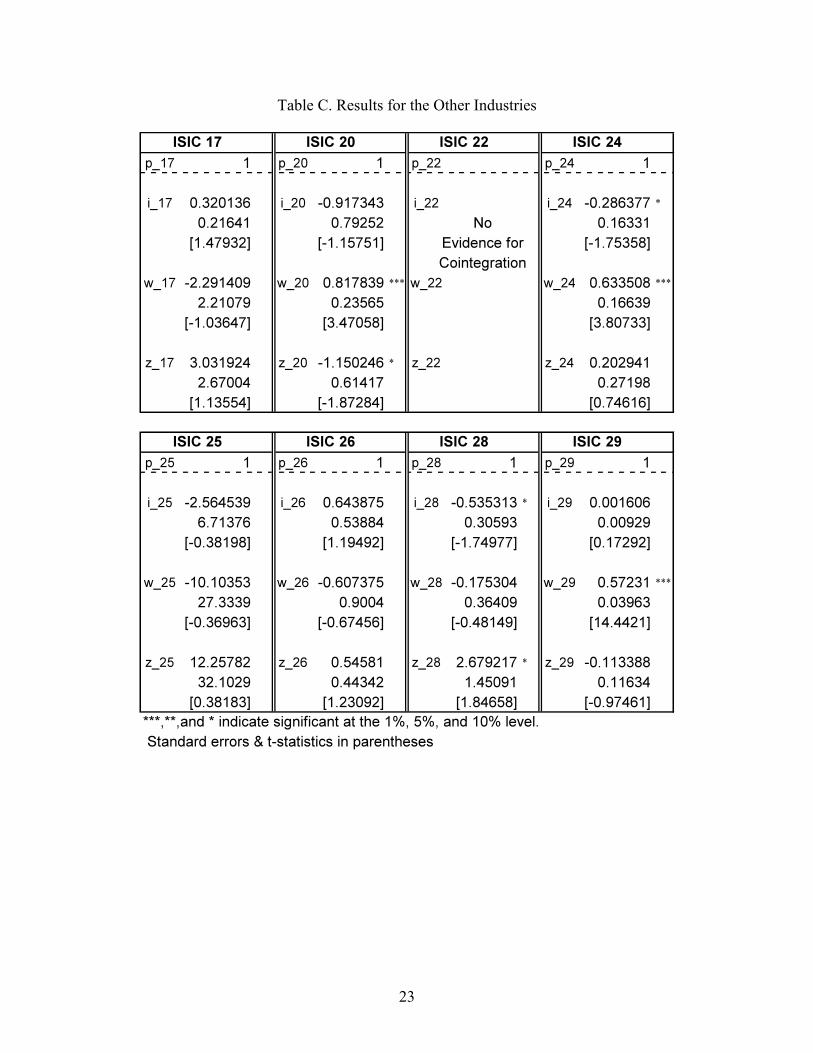

shown in Table 1, which includes the six industries. Each of these industries allows its own

cointegrating vector to have at least two variables significant at 1% level, while the other

industries do not meet this criterion and thus they are reported in table C of the appendix.

Of those industries, only four industries (ISIC 15, 21, 27 and 34) suggest that the

influences of money wage and investment amount on prices are positive and the influences of

labor productivity on prices are negative as expected from the Post Keynesian view. Interestingly,

even if ISIC 23 allows all the variables of its cointegrating vector to be significant at 1% level,

the sign of investment is negative as opposed to the theory. Given that the industry is coke and

refined petroleum products, the result can be ignored since the Eichner model is not applicable to

‘flexprice’ markets which include agriculture and natural resources industries like ISIC 23. In

addition, the industry of ISIC 35 (other transport equipment) follows simple wage markup model

in which investment is not relevant to price determination since the investment variable is not

statistically significant at all.

Moreover, logarithmic values show the responsiveness of prices to other variables. It is

found that the long-run responsiveness of prices to real wage costs (money wage/labor

productivity) is smaller than one, in all the industries except motor vehicles (ISIC 34).

6 It will be shown that only four of them (15, 21, 27, and 34) appear to be in support of the Post Keynesian theory on which the price is an increasing function of money wage and investment amount and also a decreasing function of labor productivity. Accordingly, the table B includes only the results of the four industries.

12

Table 1. The Johansen Cointegrating Equation

V. COMPETITION PRESSURE AS A KEY FACTOR TO THE PROCESS

As mentioned above, the other industries have not shown the expected long-run relationships.

This raises a serious question about what makes the discrepancy between the manufacturing

industries in U.S. In this section, I suggest a possible explanatory factor, so to speak, difference in

competition pressure from internal and external sources.

13

It has been found that the long-run relationships between industrial price, investment,

money wage and labor productivity shown in four industries are exactly in accord with the

expectation of the Post Keynesian pricing theory, whereas others are not following the prediction.

However, it does not imply that the Post Keynesian theory fails to explain the U.S. economy, in

particular the price determining mechanism. Since an enterprise’s market power depends heavily

on relative market competition pressure, the four explainable industries are expected to have

relatively less fierce competition pressure than other 10 industries which have different

coefficients from the expected ones from Post Keynesian vantage point.

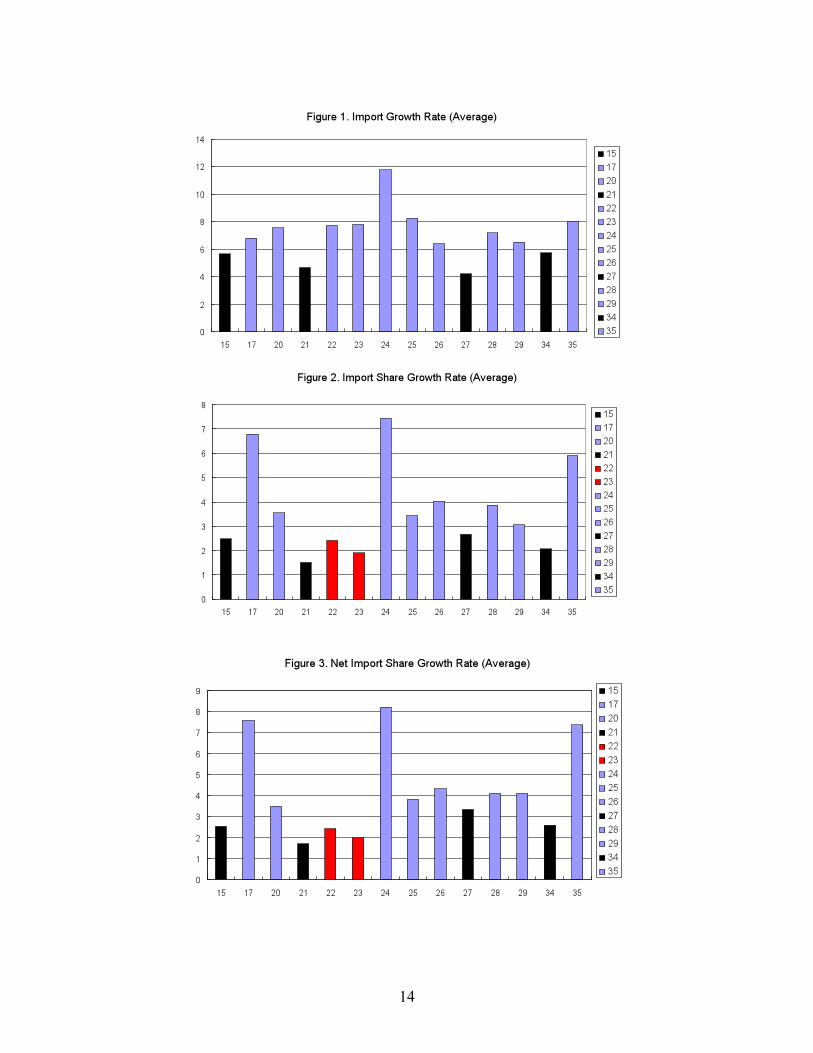

Indeed, figure 1, 2 and 3 show that the four industries have less competition pressure

from outside the country than the others in terms of import growth rate and the growth rate of the

market share of the imported goods as well as the growth rate of the market share of the net

imported goods in their industries.

Nevertheless, the industries 22 and 23 are among the group with less import pressure in

terms of the growth rate of the market share even if they don’t have the expected coefficients. As

discussed above, ISIC 23 (coke and petroleum products) can be ignored where the price change

depends highly on market situations such as demand and supply, shortage from natural disaster

and business cycle. Even so, ISIC 22 (printing and publishing) is left to be explained concerning

the reason why the low external competition does not lead to such high market power that it can

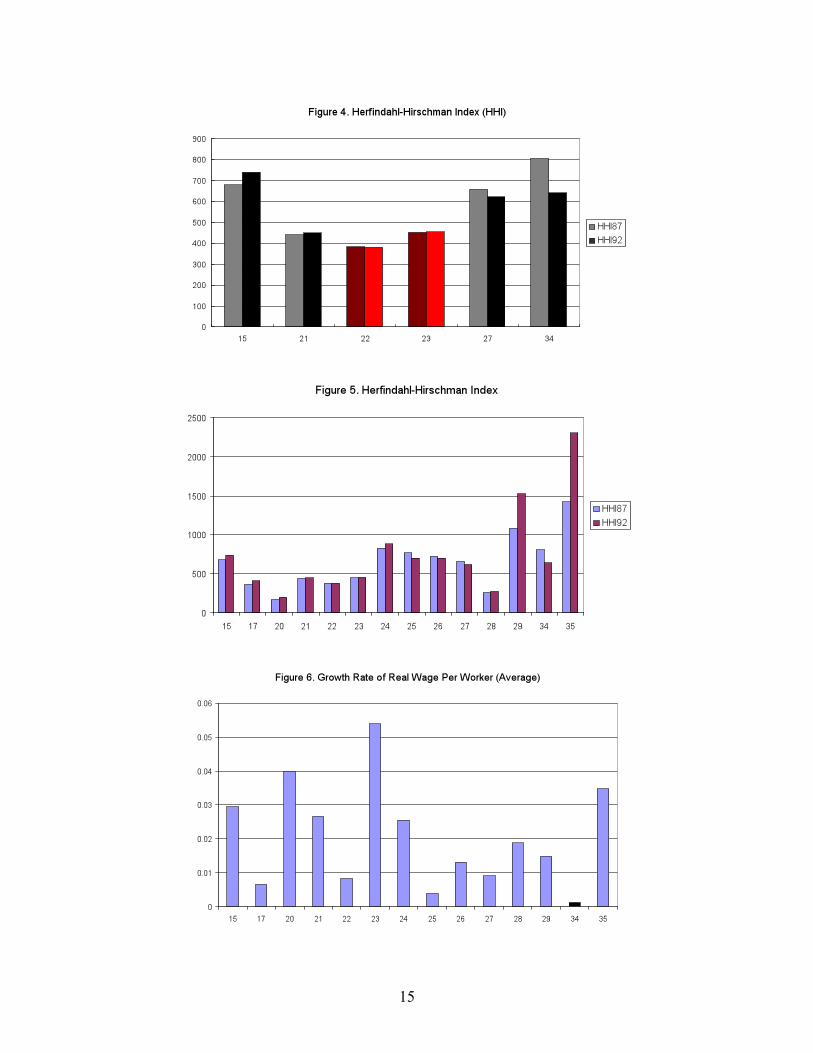

utilize pricing policy to finance its investment. How can it be reconciled with the story? Figure 4

shows Herfindahl-Hirschman Index (HHI) for the six industries with relatively low growth rate of

the market share of the imported goods. Higher HHI generally indicate a higher concentration and

thus a higher market power, whereas lower HHI indicate the opposite. It shows that the firms in

the industries 22 and 23 have fiercer competition pressures from other domestic enterprises in the

same industries than as in industries 15, 21, 27, and 34 to which the theory applies directly.

Hence we come to a conclusion that the question above can be solved by the relative high

competition between domestic firms occupying industries 22 and 23 respectively.

14

15

16

Therefore, it can be said that even if we can not say that every industry in U.S. is fully

explained by the markup model, at least it can be said that the U.S. industries are not

incompatible with the Post Keynesian price theory.

VI. TRANSFORMATION OF CORPORATE STRATEGY

There is a fundamental question left to be asked – what if changes in corporate

governance have been transforming corporate strategy from an orientation towards retention of

corporate earnings and reinvestment in its growth to distribution of the earnings to shareholders

over the past two decades?

Minsky (1993) suggests that money manager capitalism emerged in which the main

business in the financial markets become far removed from the financing of the capital

development of the country; furthermore, the main purpose of those who controlled corporations

was no longer making profits from production and trade but rather to assure that the liabilities of

the corporations were fully priced in the financial market, to give value to stockholders. He

continues to argue:

“The giving of value to stockholders took the form of pledging a very high

proportion of prospective cash flows to satisfy debt liabilities. This prior

commitment of cash meant that there was little in the way of internal finance

left for the capital development of the economy.” (Minsky 1993 p. 112)

Accordingly, Lazonick and O’Sullivan (2000) provide an historical analysis of the rise of

shareholder value as a principle of corporate governance in the United States, tracing the

17

transformation of US corporate strategy from an orientation towards retention of corporate

earnings and reinvestment in corporate growth through the 1970s to one of downsizing of

corporate labour forces and distribution of corporate earnings to shareholders over the past two

decades. In addition, Stockhammer (2004) asserts that power has been shifted to shareholders and

thus reshaped a manager’s priorities, and also offers the empirical link between accumulation and

financialization which is tested using a time series analysis of aggregate non-housing private

investment for the USA, providing evidence of the negative effect of financialization on

accumulation. Indeed, figure 7 shows that the proportion of manufacturing investment out of

grand total of gross fixed capital formation has been continue to fall from almost 20% to 12%

since 1970.

However, it is not clear whether the slowdown of manufacturing accumulation results

from the transformation of US corporate strategy from an orientation towards corporate growth or

not; it could be reflecting the structural transformation of US economy into more intensive

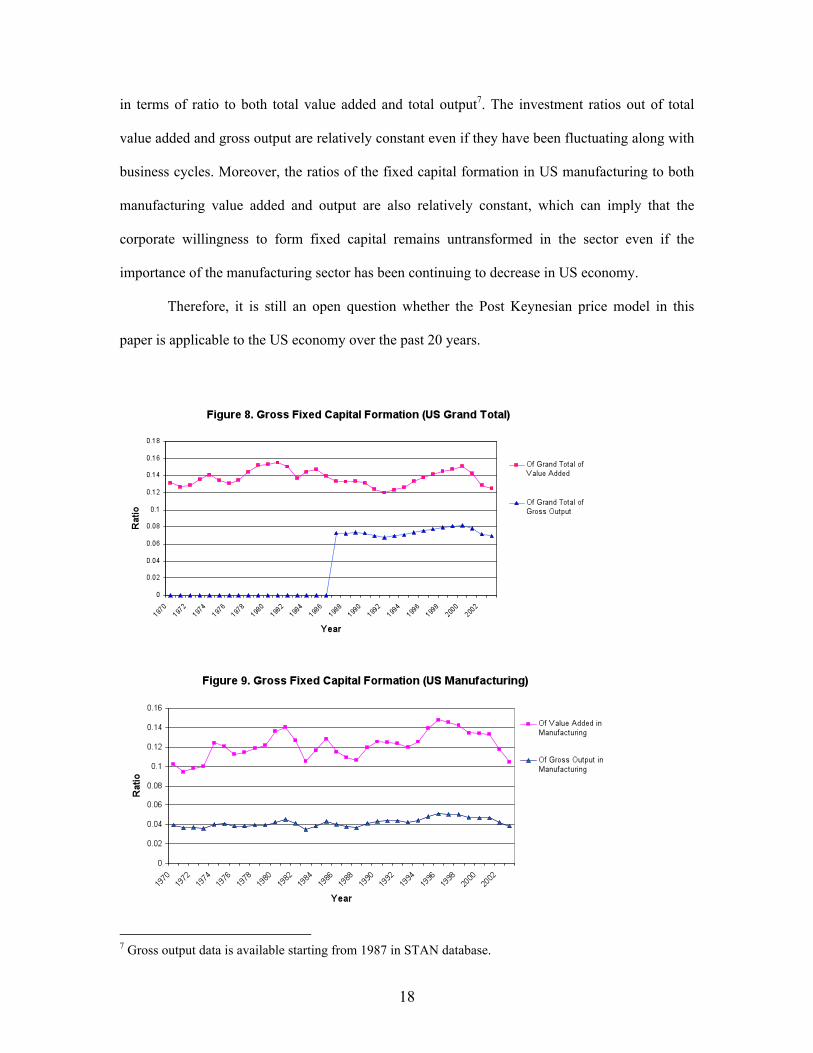

service-based one. Figure 8 indicates the gross fixed capital formation of US economy as a whole

18

in terms of ratio to both total value added and total output7. The investment ratios out of total

value added and gross output are relatively constant even if they have been fluctuating along with

business cycles. Moreover, the ratios of the fixed capital formation in US manufacturing to both

manufacturing value added and output are also relatively constant, which can imply that the

corporate willingness to form fixed capital remains untransformed in the sector even if the

importance of the manufacturing sector has been continuing to decrease in US economy.

Therefore, it is still an open question whether the Post Keynesian price model in this

paper is applicable to the US economy over the past 20 years.

7 Gross output data is available starting from 1987 in STAN database.

19

VII. CONCLUSION

This study investigates the pricing behavior of the U.S. manufacturing industries by using

Johansen’s cointegration method. It demonstrates that industrial prices, investment, money wage

and productivity are cointegrated in the four industries. In other words, they move together in the

long run. The error correction terms shows the short-run dynamics of these four variables. In light

of the market structures, the empirical results of the U.S. manufacturing industries prove to be not

inconsistent with the Post Keynesian price model.

REFERENCES

Atesoglu, H., ”A Post Keynesian Explanation of U.S. Inflation”, Journal of Post Keynesian

Economics, Vol. 19, No. 4, 1997

__________, “Income, Employment, Inflation, and Money in the United States”, Journal of Post

Keynesian Economics, Vol. 22, No. 4, 2000

Bloch and Olive, “Can Simple Rules Explain Pricing Behaviour in Australian Manufacturing”,

Australian Economics Papers, June, 1996

Cin M., “Industrial price determination process in the Turkish private manufacturing industry

between 1980 and 2000: a Keynesian approach”, Journal of Post Keynesian Economics,

Vol. 27, No. 3, 2005

Corbett, J. and T. Jenkinson, “How is Investment Financed? A Study of Germany, Japan, the

United Kingdom and the United States”, Manchester School of Economics and Social

Science, Vol. 65, 1997, p. 69-93

20

Eichner, A., The Megacorp and Oligopoly, Cambridge University Press, 1976

Fazzari, “The Investment-Finance Link, Investment and U.S. Fiscal Policy in the 1990s”,

Public Policy Brief 9, Levy Economics Institute, 1993

Hansen, H. and Juselius, K., CATS in RATS: Co-Integration Analysis of Time Series, Evanston,

1995

Johansen, S., “Statistical Analysis of Co-Integration Vectors”, Journal of Economic Dynamics

and Control, Vol. 12, No.2-3, 1988

________ and Juselius, K., “Maximum Likelihood Estimation with Inference on Co-Integration

with Application to the Demand for Money”, Oxford Bulletin of Economics and Statistics,

Vol. 52, 1990

Lavoie, M., Foundations of Post- Keynesian Economic Analysis, Edward Elgar, 1992

Lazonick and O’Sullivan, “Maximizing shareholder value: a new ideology for corporate

governance”, Economy and Society, Vol. 29, p. 13-35, 2000

Lee and Keen, “The Incoherent Emperor: A Hetetodox Critique of Neoclassical Microeconomic

Theory”, Review of Social Economy, 2004

Minsky, H., “Schumpeter and Finance”, in Market and Institutions in Economic Development

(eds.) Biasco and Roncaglis, 1993

Moss, S., An Economic Theory of Business Strategy, Wiley Blackwell, 1981

Sen, K. and R. Vaidya, “The determination of industrial prices in India: a Post Keynesian

approach”, Journal of Post Keynesian Economics, Vol. 18, No. 1, 1995

Stockhammer, E., “Financialization and the slowdown of accumulation”, Cambridge Journal of

Economics, Vol. 28, p. 719-741, 2004

Wray, L. Randall, “International Aspects of Current Monetary Policy, CFEPS working paper No.

31

21

Table A. Dickey-Fuller Unit Root Tests

22

Table B. Cointegration Rank Test Using Trace

23

Table C. Results for the Other Industries

24

Table D. Error Correction Estimates8

8 From table D, it is clear that the error correction term is significant in most variables for each industry. It implies that those variables adjust in the short run to the disequilibrium. One can interpret the error correction term (CointEq) as a situation where the actual price is greater than the long-run relationship indicates. The situation would happen at a time when firms have market power in the industry that allows them to raise the market price. The firms would try to correct the deviation of actual price from its long-run level in the current period by cutting prices, raising investment or raising money wage. Food products and beverages industry (ISIC15) tends to reduce the next period’s price and increase the next investment. The others are inclined to raise investment or wage bill in the process toward their long-run positions.

25

Table E. Summary Statistics