Embed Size (px)

Citation preview

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 1/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

The Determinants o

Emmanuel

School of Busin

ananeemmanuel@yah

ABSTRACT

In support of the recent U.S eviden

varying and the conditional variance premium implicit in the U.S. econom

as a determinant of the term premium

Keywords: Term Premium, Yield Sp

1.0 INTRODUCTION

The uncertainties associated with t

researchers and practitioners. Unders

certain areas in the economy like th

public debt, formation of expectatio

securities, interest rate derivatives val

The term structure of interest rate

compensation for being exposed to

Merton,1983, explains that( Lee San

respect to how they are hedged aga

macroeconomic state variables to unc

the state variables also changes over t

Research conducted by Shiller (1979)

time-varying risk premium of the ter

unemployment rates, yield spreads a

of excess returns aid the explanationstudies are; Engle 1982; Engle, Lillie

like Breden 1986;Campbell 1986,19

realized that the expectations hypothe

varying. Investors require risk premiu

risk premium may reduce the numbe

of a bank and financial companies.

calculate a correct risk premium for b

Interest rates are very volatile and

Merton’s model, the model of Vasi

unting 847 (Online)

181

the Term Premium in the Ter

Interest Rates Anane1, Eugene Okyere-Kwakye2 Twum Amankwaa

ss Administration, All Nations University College (A

P.O. Box KF1908. Koforidua, Ghana.

oo.co.uk , [email protected], twumas122

e, the Garch methodology reveals in two fold that,

s of the yield spread, money supply and the exchany. However the impact of the conditional variance of

is felt only for longer maturity bonds.

ead, Money Supply, Exchange Rate, Industrial Produ

e term structure of interest rates have gained m

tanding how yields changes with time as well as it

e conduct of monetary policy, and investment secto

s about real economy activity and inflation, risk ma

ations.

takes into account the risk premium that are r

different sources of macroeconomic risk. The CA

-Sub, May 1995) risk premium are the prices of ris

nst the shocks related to some state variables in th

ertainties makes it varies over time and therefore the p

me. Consequently, the risk premium on assets in gen

; Pesando (1975); Mankiw and Summers(1984); Nel

structure of interest rates paid attention to the firs

d the level of interest rates. Studies nowadays emplo

f the intuition relating to the rejection of the expectatiand Robbins 1987; Engle, Ng and Rothschild 1990;

87 directed their minds to the equilibrium asset pr

sis have failed and the term premium in the term struc

m for the risk that they take in investing in securities

of investors and overstating the risk premium may l

esearching into the macroeconomic determinants of

oth investors and firms.

unpredictable despite various economic models in

ek, Ho and Lee, Hull and White, Black Derman

www.iiste.org

Structure of

3

NUC),

yahoo.com

the term premium is time

e rate determines the termindustrial production index

ction Index.

ch attention by academic

volatility is necessary for

s such as the financing of

nagement of a portfolio of

equired by investors as a

M in finance congrats to

built in assets priced with

e economy. Subject of the

rices of risk that depend on

ral, varies over time, too.

on (1970) to determine the

moments of variables i.e.,

y the conditional variances

on theory. Example of suchand Lee 1995. researchers

icing models because they

ture of interest rates is time

like bond. Understating the

ead to a collapse and a loss

he term structure will help

luding Heath, Jarrow and

and Toy(BDT),and Black-

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 2/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

Karasinki. The macroeconomic vari

prediction.

There has been a lot of research o

researchers neglect the effect on the

necessary to see the combined effect

the term structure of Interest rates.

1.6 OVERVIEW OF THE UNITE

THE UNITED STATE MONEY M

The U.S. has the world largest GDP

private firms make the majority of

economy maintains a high capita GD

of research and development investactivity, attempting to maintain stea

government uses powerful tools to f

fiscal policy or managing the money

slowing down or speeding up the e

( Source-Wikipedia-the free encyclop

The U.S. bond market is the largest

sector, agency sector, municipal sec

treasury sector is made up of securit

included in these securities. The tre

interest rate in all parts of the world.

issued by the treasury department. ThIn effect, interest rates on the treasur

Finally because the treasury departme

concern, it is regarded as the most act

of the fixed income market, which

Individual investors mostly do not g

However, small investors resort to m

pool the resources of most investors a

of treasury bills, certificate of depo

federal funds, broker’s calls, the libo

money market instruments. Treasury

order to raise money. What investors

maturity, the bill holder gets from t

calculated as the difference between

initial maturities with which t-bills a

which does not contain much risk. Tr

government securities dealer. A dis

instrument is that the income earned

sell in minimum denominations of

denomination of $100000.

Source: Frank J. Fabozzi. Bond mar

fixed income securities. Seventh editi

unting 847 (Online)

182

bles that causes such changes should be investigate

the effect of monetary policy and yield spread o

conditional variance of excess return on the term st

of monetary policy, yield spread and the conditional

D STATES ECONOMY, THE UNITED STATE

RKET.

around $13.21 trillion and has a mixed economy w

microeconomic decisions while being regulated by

, a reasonably high GDP growth rate, a low unemplo

ent. The federal government attempt to guide thedy growth, high level of employment and price st

rward a growth and stability agenda. Adjusting spe

supply and controlling the use of credit through m

conomy’s rate of growth, which affect the level of

edia).

ond market in the world. It is divided into six sector

tor, corporate sector, asset-backed securities sector,

es that are issued by the U.S. government. Treasur

asury sector being the largest issuer of securities i

he government of the United States with credit and

is makes market participants around the world see thy securities serve as the benchmark interest rates in

nt issues the largest size of securities as far as the tre

ive and the most liquid in the world. The united state

consists of very short-term debt securities that are

t access to most of these securities because they tr

oney market funds. The way in which money marke

nd buy many money market securities on their behalf.

sit, commercial papers, bankers acceptances, Eurod

r market. The united state treasury bills are the mos

ills are seen as a form of borrowing. The governme

do is that they purchase bills at a discount from the m

e government a value same as the face value of t

the purchase price and the ultimate maturity value.

re issued-bills are converted to cash with ease and

easury bills can be bought directly, at auction, or on t

inguishing feature that distinguishes Treasury bill

on treasury bills is exempt from all state and local ta

10000, unlike most other money market instrume

et analysis and strategies. Sixth edition and Frank J.

n

www.iiste.org

d in order to get a correct

the term structure. Most

ucture. It is therefore very

ariance of excess return on

BOND MARKET AND

ere corporations and other

the government. The U.S.

ment rate, and a high level

overall pace of economic bility. At its disposal, the

ding and tax rates through

netary policy. This end up

prices and unemployment

s namely, the U.S. treasury

and mortgage sector. The

bills, notes and bonds are

the world determines the

ull faith supports securities

m as having no credit risk.he United States economy.

sury market in the world is

money market is a division

marketable in high sense.

de in large denominations.

t funds operate is that they

. The money market consist

ollars, repos and reserves,

marketable security of all

t sells bills to the public in

aturity value stated. During

e bill. Investors earning is

28, 91, or182 days are the

re sold at low action cost,

e secondary market from a

from other money market

es. Moreover treasury bills

ts which sell in minimum

Fabozzi. The handbook of

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 3/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

1.7 MACROECONOMIC VARIAB

The purpose of this research is to istructure of interest rates in the unite

likely factors to posses the power of

with previous research such as Camp

David M. Lillien, and Russel P. Rob

Rothschild 1990; and Lee 1995. Empi

structure of interest rates and partly h

TERM STRUCTURE

The term structure of interest rates

function that relates the interest rate

until the maturity date. Exploring thefor the pattern and determines what i

relationship that exists between short

term interest rates as a lever on the r

operations, which help influence the r

different behavioral hypothesis about

INDUSTRIAL PRODUCTION IN

The Industrial Production Index is an

percentage of real output with base y

with the weights based on annual e

construction, accounts for the bulk production index is the most import

frequency the difficulties of industri

index helps to identify the turning

production index is one of the most i

production index for the United Stat

database.

MONEYSUPPLY

In financial economics, monetary ag

in bank accounts in the hands of the

serving as securities. The relationshipmoney. The two are related inversely,

equals the quantity of money demand

money market equilibrium. The mark

Supply and demand give rise to a pri

sum of long-term interest rate or free

The Federal Reserve manipulates the

of monetary aggregates is to take int

financial accounts and all printed-pap

unting 847 (Online)

183

LES SELECTION AND DESCRIPTION

entify the macroeconomic variables that are signifid state economy. Four macroeconomic variables hav

xplaining the term structure of interest rates. This h

ell (1995), Shiller (1990); Melano (1988) Laurence J

ins 1987; Walid Hejazi, Huiwen lai and Xian Yan (

rical literatures have shown that these variables have

ve unique association with the United States econom

escribes how a bonds yield changes as the bonds

o the term. The term of a debt instrument with a fix

pattern of interest rate for different term assets identiformation may be derived from the term structure of i

rates and long rates is that most central banks at a ce

eal economy. Monetary authorities accomplish this b

ate of inflation. Behavior of interest rates and bond pr

market participants and market efficiency.

EX

economic indicator, which measures real production

ear currently at 2002. Production indexes are comput

stimates of value added. This index, along with o

f the variation in national output over the durationant business indicators in the short term, which aim

al production during the long period. Monthly surv

points in economic development at an early stage;

portant measures of economic activity. Below repre

s data between the periods January 1921 to July 20

regates or money supply or money stock is the quan

on-bank public available within the economy to buy

between the rate of interest and money is that the rasuch that, a rise in money supply decreases interest r

ed with the quantity of money supply, the economy i

et of money demand utilizes the tools of analysis that

e known as equilibrium price. A price is said to be in

market and the quantity of available real money bala

Short-term interest rates artificially. An accurate way

o account of all-electronic, credit-based deposit bala

er and minted coins.

www.iiste.org

antly influencing the termintuitively been chosen as

s mainly been done in line

ay Mauer, Robert F. Engle,

Feb 2000) ; Engle, Ng and

a relationship with the term

.

aturity changes. It gives a

d maturity date is the time

fies the factors that accountnterest rates. An interesting

rtain times influence short-

y engaging in open market

ces are necessary in testing

output. It is expressed as a

ed mainly as fisher indexes

her industrial indexes and

of the business cycle. Thes to measure at a monthly

y on industrial production

also the timely industrial

sent the graph of industrial

7 taken from st. Louis fed

tity of currency and money

items, render services, and

te of interest is the price of ates. When the interest rate

s said to be operating at the

are similar to other markets.

equilibrium price when the

ces the demand for money.

for calculating the concept

ces in banks accounts and

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 4/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

EXCHANGE RATE

In financial economics, exchange ratconcern. A typical case is an exchan

means that GBP 123 has a value equ

show that, around 2 trillion USD val

market is termed as the Spot exchan

delivery and payment on a certain fut

for international trade. The dollar-po

importing raw materials and other i

hence the amount of interest paid, thu

have given its explanatory power on t

YIELD SPREAD

Yield spread is the differences in yiel

credit rating, and interest rate change

on two different investments, usually

the percentage return on investment

financial instrument A minus in a y

offered by each of the instruments.

maturities, credit ratings and risk. On

indicates the risk premium that an i

product. When yield spreads between

more risk of default on lower grade b

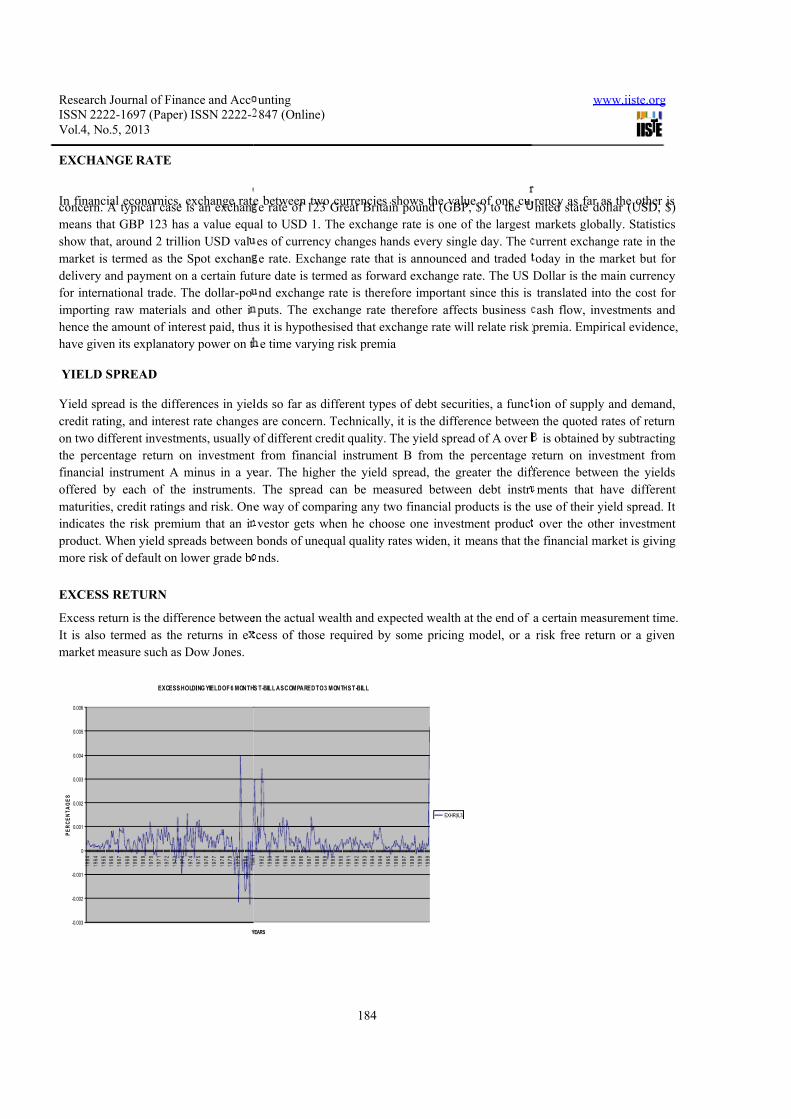

EXCESS RETURN

Excess return is the difference betwee

It is also termed as the returns in e

market measure such as Dow Jones.

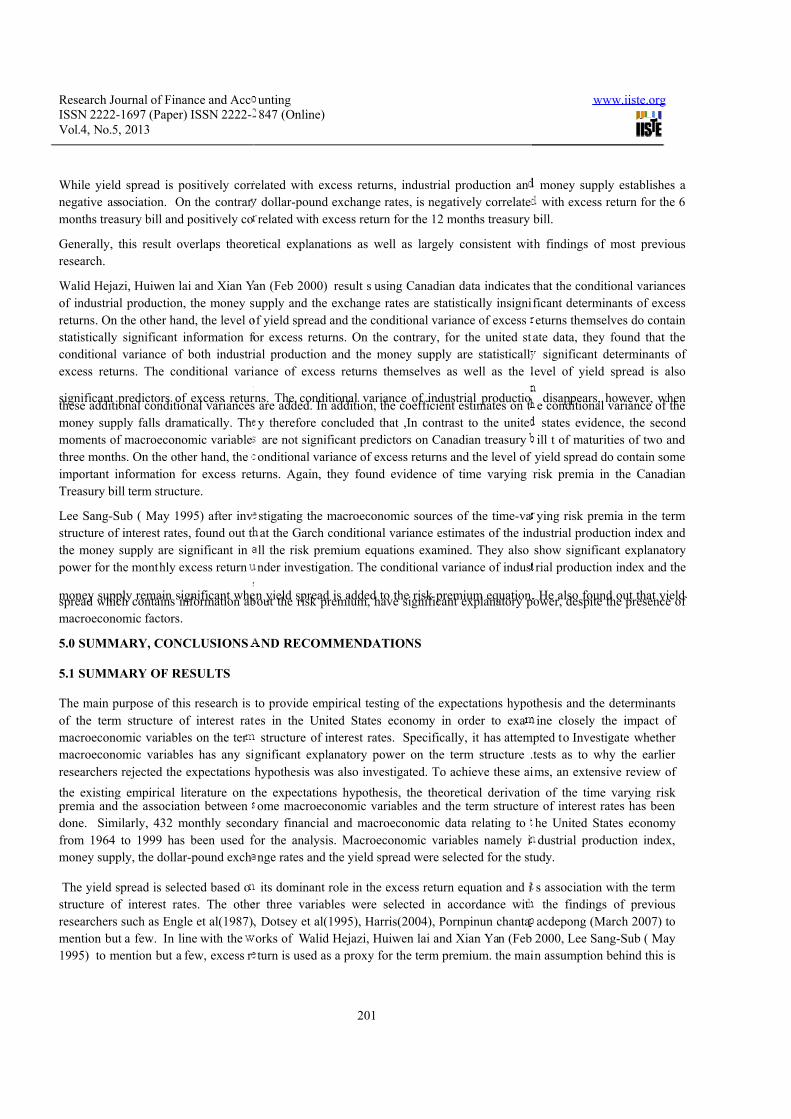

EXCESS HOLDING YIELD OF 6 MONTH I I

-0.003

-0.002

-0.001

0

0.001

0.002

0.003

0.004

0.005

0.006

1

9

6

4

1

9

6

4

1

9

6

5

1

9

6

6

1

9

6

7

1

9

6

8

1

9

6

9

1

9

6

9

1

9

7

0

1

9

7

1

1

9

7

2

1

9

7

3

1

9

7

4

1

9

7

4

1

9

7

5

1

9

7

6

1

9

7

7

1

9

7

8

1

9

7

9

1

9

7

9

1

9

8

0

Y

P E R C E N T A G

E S

unting 847 (Online)

184

e between two currencies shows the value of one cue rate of 123 Great Britain pound (GBP, $) to the

al to USD 1. The exchange rate is one of the largest

es of currency changes hands every single day. The

e rate. Exchange rate that is announced and traded

ure date is termed as forward exchange rate. The US

nd exchange rate is therefore important since this is

puts. The exchange rate therefore affects business

s it is hypothesised that exchange rate will relate risk

e time varying risk premia

ds so far as different types of debt securities, a func

s are concern. Technically, it is the difference betwee

of different credit quality. The yield spread of A over

from financial instrument B from the percentage

ear. The higher the yield spread, the greater the dif

The spread can be measured between debt instr

e way of comparing any two financial products is the

vestor gets when he choose one investment produc

bonds of unequal quality rates widen, it means that th

nds.

n the actual wealth and expected wealth at the end of

cess of those required by some pricing model, or a

I I S T-BILL AS COMPARED TO 3 MONTHS T-BILL

1

9

8

2

1

9

8

3

1

9

8

4

1

9

8

4

1

9

8

5

1

9

8

6

1

9

8

7

1

9

8

8

1

9

8

9

1

9

8

9

1

9

9

0

1

9

9

1

1

9

9

2

1

9

9

3

1

9

9

4

1

9

9

4

1

9

9

5

1

9

9

6

1

9

9

7

1

9

9

8

1

9

9

9

1

9

9

9

EARS

EXHR(6,3)

www.iiste.org

rency as far as the other isnited state dollar (USD, $)

markets globally. Statistics

urrent exchange rate in the

oday in the market but for

Dollar is the main currency

translated into the cost for

ash flow, investments and

premia. Empirical evidence,

ion of supply and demand,

n the quoted rates of return

is obtained by subtracting

return on investment from

ference between the yields

ments that have different

use of their yield spread. It

over the other investment

e financial market is giving

a certain measurement time.

risk free return or a given

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 5/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

2.0 THEORETHICAL FRAMEW

2.1 THE EXPECTATIONS THEO

Assuming that by the principle of ri

what their maturity, the expected one

and would be equal to the known saf

the risk premium is zero for all mat

pure expectation hypothesis in that th

all information at time t whereas thethere is uncertainty related to the retu

to depend on some form of reward fo

The basic assumptions, which constit

1. The term premium is constant over

2. The term premium is

A combination of the expectation h

gives a variance inequality such that

be greater than or equal to the one p

return should be the same for differen

The theory concerning the expectatio

(1995), Shiller (1990); Melano (198

explains that agents that hold ration

attributed to two reasons. Either time

errors, which appear biased when vi

line with this study. Researchers like

used Canadian government Treasur

researchers for the expectation theory

and Hardouvelis (1994), Gerlach and

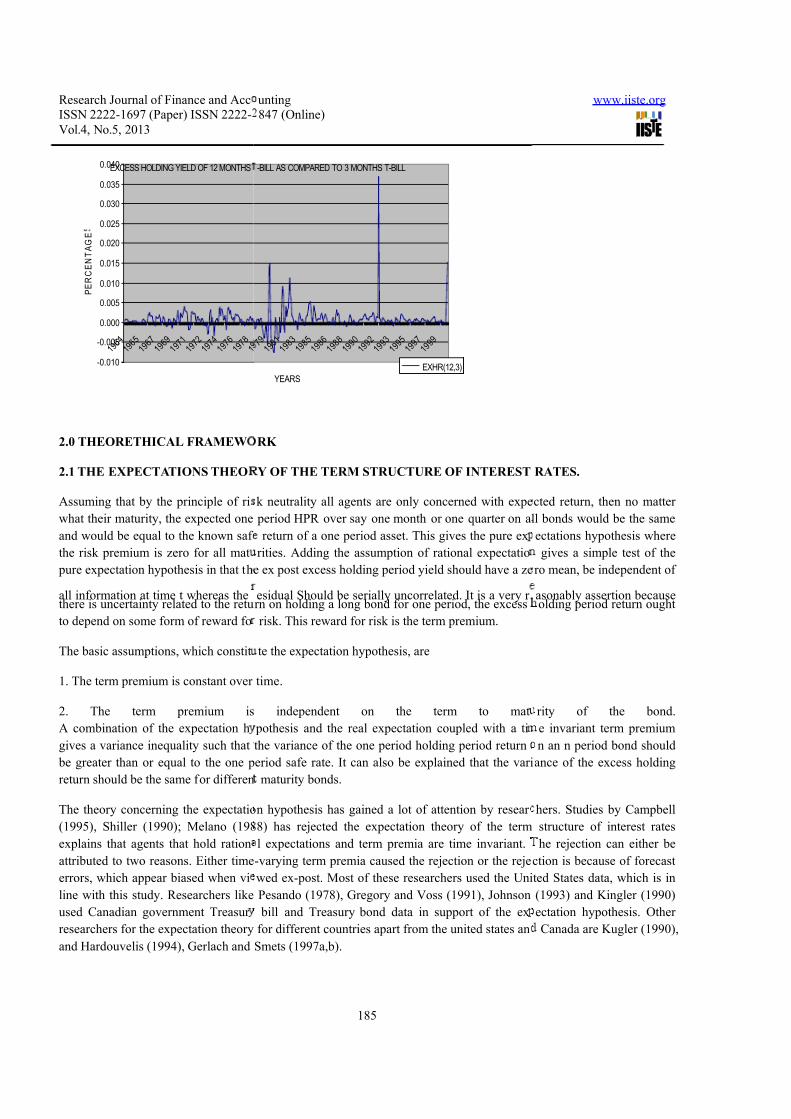

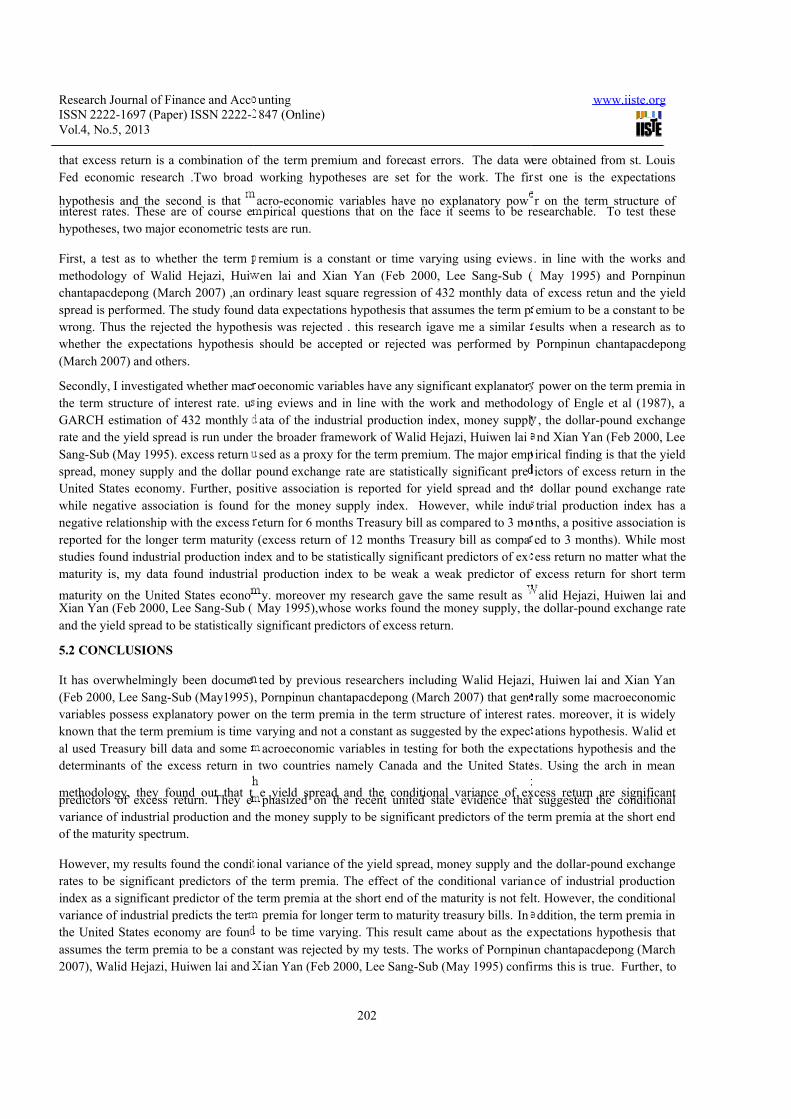

EXCESS HOLDING YIELD OF 12 MONTHS

-0.010

-0.005

0.000

0.005

0.010

0.015

0.020

0.025

0.030

0.035

0.040

1 9 6 4

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1

P E R C E N T A G

E

unting 847 (Online)

185

RK

Y OF THE TERM STRUCTURE OF INTEREST

k neutrality all agents are only concerned with expe

period HPR over say one month or one quarter on al

return of a one period asset. This gives the pure ex

rities. Adding the assumption of rational expectatio

e ex post excess holding period yield should have a ze

esidual Should be serially uncorrelated. It is a very r rn on holding a long bond for one period, the excess

risk. This reward for risk is the term premium.

te the expectation hypothesis, are

time.

independent on the term to mat

pothesis and the real expectation coupled with a ti

the variance of the one period holding period return

eriod safe rate. It can also be explained that the vari

maturity bonds.

n hypothesis has gained a lot of attention by resear

8) has rejected the expectation theory of the term

l expectations and term premia are time invariant.

-varying term premia caused the rejection or the reje

wed ex-post. Most of these researchers used the Uni

Pesando (1978), Gregory and Voss (1991), Johnson

bill and Treasury bond data in support of the ex

for different countries apart from the united states an

Smets (1997a,b).

-BILL AS COMPARED TO 3 MONTHS T-BILL

7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

YEARS

EXHR(12,3)

www.iiste.org

RATES.

cted return, then no matter

l bonds would be the same

ectations hypothesis where

gives a simple test of the

ro mean, be independent of

asonably assertion becauseolding period return ought

rity of the bond.

e invariant term premium

n an n period bond should

ance of the excess holding

hers. Studies by Campbell

structure of interest rates

he rejection can either be

ction is because of forecast

ted States data, which is in

(1993) and Kingler (1990)

ectation hypothesis. Other

Canada are Kugler (1990),

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 6/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

Pesando (1978) identified that the ch

when he used quarterly interest rate d

Gregory and Voss (1991) using quart

like forward premium, the premium o

Johnson (1993) identified that when

well as the spread between internatio

Canadian and the united states treasu

conclusion when he used Canadian a

1971 to 1988.He further argued that

far as Canada and the united states ar

The arguments raised above calls for

time varying risk premia.

Walid Hejazi, Huiwen lai and Xian Y

The long-term rate say K period can

plus a premium. Then mathematically

k

t

k

i

it t

k

t Y E k

Y θ += ∑−

=

+

1

0

11

...................

Where

k

t Y Represent the yield to maturity o

t E Represent the markets expectatio

k

t θ Represent the expected excess re

premium component.

∑−

=

+

1

0

11 k

i

it t Y E k

Represent the expectati

So far as the expectation hypothesis i

t. Assumek

t H 1+ is the investors reali

that begins with time t, in excess of th

11

11 )1( t

k

t

k

t

k

t Y Y k kY H −−−=−

++ …

This linearization is appropriate for di

For pure discount bonds, the time-var

unting 847 (Online)

186

nges in Canadian long-term interest rates are well ap

ata on Government of Canada long -maturity bonds fr

rly priced data between 1961 and 1988 explained th

n three and six months Canadian treasury bills can be

both the spread between the Canadian long-term an

al yields are used, the significant difference that exis

ry bonds of maturity two, ten and twenty years are p

d the united states treasury bills of maturity two, ten

is evidence suggest that there is no equalization in th

concerned.

an equation for testing the expectation hypothesis i

n (Feb 2000) deduced an equation for performing suc

always be written as an average of expected future

the yield for pure discount bond purchased at time t c

.... (1)

a K period pure discount bond.

conditional upon information available at time t.

urn on holding a long bond relative to rolling over sh

n component. This serves as the rolling premium.

s concern the rolling premia vary with the maturity k

zed one period excess return when he holds a k peri

at to holding a one period bond. Expression this in an

............. (2)

scount bond (shiller 1979, 1990; or shiller, Campbell,

ing expected excess return is defined as

www.iiste.org

roximated by a martingale

om 1961 to the period 1976.

t using current information

predicted.

short-term interest rate as

t between excess returns on

redictable. He came to this

and twelve over the period

e long term bond returns so

searching for evidence of

h task. According to them,

short rates says one period

an be written as

ort bond. This serves as the

but does not vary with time

od bond for a single period

equation gives

and schoenholtz 1983).

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 7/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

1 )1( t

k

t

k

t t

k

t Y E k kY H E −−==+

φ

Equation (3) is the term premium.

Term premium are observed i

)[1( 1

1

11 +

−

++ −−−=k

t t

k

t

k

t

k

t Y E Y k H φ

plus a single period forecast error. A

the long-term interest rate is containe

spread. Mathematically,

10

1

1 ())(1( −

+ +=−−k

t

k

t

k

t Y bbY Y k

k

t ob φ −= 11 =b

Rearranging gives

1

1

11 )(++

+−+= t t

k

t o

k

t eY Y aa H

Where=

+1t ek

t

k

t Y k −−−−

+

1

1)(1(φ

According to the expectation hypothe

Equation (6) is use in the testing of th

can be seen clearly how equation (6)

ex-ante that forecast errors are orthog

serves as an indicative of time-varyin

2.2 THE ECONOMIC THEORY

VARIABLES AND THE TERM ST

The theory as to what determines th

economists. whiles some think mon

others think industrial production ind

interest rates. However recent studi

determines the term structure of inter have some link with the term structu

using different methods which includ

ARCH in mean or the GARCH appro

Walid Hejazi, Huiwen lai and Xian

Canadian T-bill term structure of inte

on Canadian treasury bills with one to

state treasury-bill during the same ti

conditional variances of industrial pr

determinants of excess returns. On t

unting 847 (Online)

187

11

1 t

k R−−

+ … (3) = TERM PREMIUM

the presence of forecast errors. A typical

]1

........... (4) Where excess return is decomposed int

cording to the expectation hypothesis, the markets be

in the spread between the long K period yield and th

1

1) ++ t t uY ………………….. (5)

…………………….. (6)

o

k

t t a R E −−

+

1

1

sisk

oa φ =and

01 =a

e expectation hypothesis in searching for evidence of

an be split into premium component and forecast erro

onal to available information, Estimated values of 1a

risk premia.

N THE ASSOCIATION BETWEEN INDIVIDU

RUCTURE OF INTEREST RATES.

term structure of interest rates has been of differen

tary aggregates is a strong determinant of the term

ex, yield spread, excess returns have a strong linkag

es are of the view that all the macroeconomic i

est rates. Another school of thought is of the view thre of interest rates. This has been tested by different

the Value at Risk approach, the linear regression app

ach.

Yan (Feb 2000) examined the determinants of the t

rest rates. They used monthly data over the period J

three months to maturity. In order to enhance their a

e periods for comparison. Their result s using Cana

oduction, the money supply and the exchange rates a

e other hand, the level of yield spread and the con

www.iiste.org

case is the equation

o a sum of a term premium

st forecast of the change in

e short period yield or yield

ime varying risk premia. It

r component. Assuming

that are not equal to zero

L MACROECONOMIC

t views by researchers and

structure of interest rates,

with the term structure of

dicators mentioned above

at microeconomic variableseconomist and researchers

roach and the Engle (1982)

erm premia implicit in the

ly 1960 to December 1995

alysis, they used the united

dian data indicates that the

re statistically insignificant

ditional variance of excess

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 8/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

returns themselves do contain statisti

state data, they found that the conditi

significant determinants of excess retyield spread is also significant pre

disappears, however, when these ad

conditional variance of the money su

in the Canadian term structure are re

and surprisingly, they saw a statistic

supply and the term premia implicit i

the united states evidence, the second

treasury bill t of maturities of two an

the level of yield spread do contain s

varying risk premia in the Canadian

macro economy as measured by their

insisted that there is important link b

and therefore the determinants of the

Lee Sang-Sub ( May 1995) investi

structure of interest rates, based upo

advance constraint using monthly un

advance constraint combined with ge

the model derives the risk premium

nominal term structure depending on

money supply, measured by their con

and the money supply are important s

He also found out that the Garch co

supply are significant in all the risk p

the monthly excess return under inve

supply remain significant when yield

which contains information about t

macroeconomic factors.

Paul Boothe (August 1991) used co

evaluate a model of the term structur

with the hypothesis of high or perfe

States assets of comparable maturity.

and long interest rates, which was co

Carlos Del Castillo and Jean- Franco

2000 tested a theoretical model expla

degree of risk aversion and the deg

variance of consumption growth. Th

significant in an econometric equatio

Laurence Jay Mauer using six month

commercial bank maturity behavior t

hypothesis, which stresses the impo

structure of interest rates; again to a

unting 847 (Online)

188

cally significant information for excess returns. On

nal variance of both industrial production and the m

rns. The conditional variance of excess returns themsdictors of excess returns. The conditional varianc

itional conditional variances are added. Also, the c

ply falls dramatically. They pursue the possibility tha

lated to the conditional variances of the united state

lly significant link between the conditional variance

the Canadian t-bill term structure. They therefore c

moments of macroeconomic variables are not signifi

three months. On the other hand the conditional va

me important information for excess returns. Althou

reasury bill term structure, these premia are not relate

conditional variance of industrial production and the

etween the U.S. money supply and the Canadian ter

erm structure of interest rates of the two countries are

ated the macroeconomic sources of the time-varyi

n a monetary general equilibrium model of the ter

ted states term structure data for one to six months

eral time series representations of the relevant macro

expression that succinctly describes the relationship

the uncertainties related to the macroeconomic forci

ditional variance-covariance_s. Lee found out that un

ources of time-varying risk premia in the nominal ter

nditional variance estimates of the industrial produ

emium equations examined and they also show signif

stigation. The conditional variance of industrial prod

spread is added to the risk premium equation. He also

e risk premium, have significant explanatory pow

integration tests and two different sets of Canadian

of interest rates in an open economy. He found out t

t substitutability or uncovered interest parity betwee

However, he found mixed support for the hypothesi

trary to the findings of Engle and Granger and Camp

is Fillion (October 2002) using three months forwar

ining the term premium. They found out that, the ter

ee of persistence in consumption growth and on o

y found out that, the conditional variance of consum

of excess returns.

s maturity class and seven to twelve month maturity

owards the term structure of interest rates. His aim w

rtance of expectations of future yields as a deter

so verify the liquidity hypothesis, which emphasize

www.iiste.org

the contrary, for the united

ney supply are statistically

elves as well as the level of e of industrial production

oefficient estimates on the

t the term premium implicit

s macroeconomic variables

of the united states money

ncluded that ,In contrast to

ant predictors on Canadian

iance of excess returns and

h there is evidence of time

d to the uncertainties in the

money supply. They again

structure of interest rates

different.

g risk premia in the term

structure with a cash in

treasury bill with a cash in

economic forcing variables,

between risk premia in the

g variables, output and the

certainties related to output

structure of interest rates.

tion index and the money

icant explanatory power for

ction index and the money

found out that yield spread

r, despite the presence of

nd the united state data to

at the data were consistent

n Canadian and the United

s of co integration of short

ell and Shiller.

interest rate from 1960 to

premium depends on the

e variable, the conditional

ption growth is statistically

class analyzed the effect of

as to verify the expectation

inant of the present term

s the greater moneyness of

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 9/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

short-term debt as opposed to long-te

that both the liquidity and expectation

Arturo Estrella and Frederic S. Mis

monetary policy instruments and to s

results show that monetary policy is

only determinant. In addition, they fo

Rodrigo Sekkel and Denisard Alv

macroeconomic shocks on the dynam

policy shocks flattens the term stru

Nevertheless, they found that monet

dynamics of the term structure than

importance of the standard macroec

structure of Brazil.

2.3 THE THEORETICAL DERIV

A methodology by Engle et al (198

methodology, the conditional varianc

model using 3-month and 6-month

concluded that that risk premia vary s

research, I generate measures of the

months treasury bill over 3 months a

I used monthly observation as done

Xian Yan (Feb 2000). This is in repl

standard deviation of the error term ia micro-founded model with risk-aver

Below is a generalization of the work

to determine the time varying risk

decompose the excess holding yield i

t t t E ε µ +=………………………

Where t E =excess holding yield on

t µ =risk premium or the exp

long-term asset. This parameter is no

t ε

=difference between the e

This signifies that the expected exces

Expressing the risk premium in an eq

t t hu δ β +=……………………..

unting 847 (Online)

189

m debt. After their estimation and analyses, they fou

theories are consistent with the data.

kin (1995) examined the relationship of the term s

bsequent real activity and inflation in both Europe a

an important determinant of the term structure sprea

nd a significant predictive power for both real activit

s using near-VaR estimation identified the effect

ics of the Brazilian term structure of interest rates. T

ture of interest rates, which is similar to that of t

ary policy shocks in brazil appear to explain a sig

in the united states of America. Furthermore, the

onomic variables, such as Gross domestic product

TION OF THE TIME VARYING RISK PREMIA

) known as the Arch -M model is use to determin

e of excess return determines the current risk premi

U.S. Treasury bill rate between 1960 to 1984.The

ystematically over time with agents perception of un

term premium by estimating the Arch-M model of

d 12 months bill over 3 months treasury bill betwee

y Pornpinun chantapacdepong (March 2007) and W

icates Engle et al (1982) methodology, which incorp

the mean equation of the excess holding yield.This, ise agents.

s of Pornpinun chantapacdepong (March 2007)

remia using the Arch-M model proposed by Engl

to

………................. (7)

6 months Treasury bill over the 3 months Treasury bil

ected return that the risk averse investor would expe

-static.

ante and ex post rate of return which cannot be fore

return from holding the longer-term asset is just equa

ation gives

8) ’ 0>δ

www.iiste.org

d at microeconomic levels

ructure of interest rates to

nd the United States. Their

d, but is unlikely to be the

and inflation.

of monetary policy and

ey found out that monetary

e United States economy.

ificant larger share of the

e was an evidence of the

and inflation on the term

.

the risk premium. In this

m.. Engle et al tested their

y used quarterly data and

erlying uncertainty. In this

xcess holding return for 6

the period 1964 and 1999.

lid Hejazi, Huiwen lai and

orates expected conditional

ncorporates in pattern from

showing how

et al. The first step is to

.

t for holding such a riskier

asted in an efficient market.

l to the risk premium.

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 10/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

Where t h =conditional standard devia

0>δ = the coefficient of th

The assumption behind is that the ris

unforecastable shocks ( t ε ).

2

t h =The conditional varianc

investors.

)(2

t t Var h ε =For all avail

A point of interest is that this model

variance2

t h .The main reason is that

in the mean. Researchers including

same specification.

According to Engle,et al (1987), it

innovations,2

t ε .The conditional varia

2

10

2

t it wh ε α α +=………………

This means that the variance of the

squared innovations, where iw Repr

every year I have 12 months and 13

the mean.

Pornpinun chantapacdepong (March

where 78

113 −=iw

And 11−=i

He noticed the declining weight sche

terms. The equation is therefore

2

2

11

2

78

11

78

12−−+++= t t ot h ε ε α α

The above equation including the one

)( t H E Depends on the conditional

unting 847 (Online)

190

tion of the unforecastable shocks t ε to the excess ret

relative risk aversion.

k premium is an increasing function of the condition

e of the error term and is a function of the informa

ble information.

takes the mean as a linear function of the standard

it is assumed that changes in the variance are reflect

omowitz and Hakko (1985), Engle, Wooldridge and

is assumed that the conditional variance is a wei

nce follows an ARCH(P) process below.

……………………… (9)

error term depends on the intercept oα and the w

esent the weighting parameters. I used monthly obs

ags on the assumption that the past years informatio

2007) Discounted the older information using a linear

.

e on lag structure aids in coping with the co linearit

2

1278

1......................

−+ t ε

………………………

s earlier analyzed concludes that the conditional mean

tandard deviation of the unforecastable error term.

www.iiste.org

rn on the long-term asset.

al standard deviation of the

tion set that is available to

deviation t h

Instead of the

ed less than proportionality

Bollerslex (1988) used the

hted sum of past squared

ighted average of the past

ervations. This means that

n is essential for predicting

ly declining weight scheme

y of past square innovation

… (10)

of the excess holding yield

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 11/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

t t t H E µ =−1 indicates that the ris

returns. On the assumption that the va

HYPOTHESIS

The following hypothesis are stated a

H1: The risk premia in the nominal te

related to the macroeconomic fo

measured by their conditional va

H2: The term premia implicit in the u

H3: The Garch conditional variance e

are significant in all the risk pre

power for the monthly excess ret

3.0 METHODOLOGY

This section presents the methods tha

all scientific work has to be replicabl

how the study is carried out, Hussey

Summers 1984; Nelson 1970 used fis

1987; Walid Hejazi, Huiwen lai andtaken into consideration, in the deter

this research, single equation regressi

on the first moment determinants of t

determinants of the time varying risk

independent variable are taken into c

is a sum of a term premium, and a s

expectation hypothesis in my single e

3.1 Sources of Data

Data for the study were mainly obta

industrial production index, U.S dollmonths and 12 months Treasury bills

data were collected from the st. Loui

using 432 monthly observations.

3.2 EXCESS RETURN GENERAT

Before generating risk premia, it is us

the assumption that excess return is d

excess holding yield return for holdi

months treasury bills as well as the e

return from holding consecutive 3-m

unting 847 (Online)

191

premium is an increasing function of the condition

riation of return measures riskiness.

ter the discussions above:

rm structure depends on the uncertainties

cing variables, output and the money supply

riance-covariances.

.s. term structure are time varying.

stimates of the industrial production index and M1

ium equations and show significant explanatory

rn.

t were used to collect and analyse data for this resea

e and this can be done only if the researcher gives a

and Hussey, 1997a. Researchers like shiller 1979;

t moments of variables, Robert F. Engle, David M. L

ian Yan (Feb 2000) used second moment where theination of the time-varying risk premia of the term s

on is used in testing for the expectation hypothesis. T

e term structure of interest rates. ARCH Model was

premia where the conditional variances of both the

nsideration. This helps identify the significant predic

ingle period forecast errors. It also explains the mai

quation regression test.

ined from secondary sources. Monthly macroecono

ar- G.B pound sterling exchange rate, money supply.were used in the calculation of the yield spread and th

s Fed economic research. The study covers the perio

ON AND DESCRIPTION

eful to explain in twofold how the properties of the e

ecomposed into a sum of a term premium plus a sing

ng a 6-month treasury bill compared to the return f

xcess holding yield return for holding a 12-month tr

onths treasury bills are calculated. The risk premia o

www.iiste.org

al standard deviation of the

ch. The significance is that

laid down procedure as to

esando 1975; Mankiw and

llien, and Russel P. Robins

ir conditional variances aretructure of interest rates. In

his in other words focussed

used in the second moment

dependent variable and the

ors of excess return, which

reason why I rejected the

mic data collected include,

Spot rates on 3 months, 6e excess holding return. All

d of Jan 1964 to Dec 1999

cess return was obtain. On

le period forecast error, the

om holding consecutive 3-

asury bill compared to the

f the excess holding yields

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 12/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

was generated as a result of the vola

(1987) where he used the treasury bill

the same methodology but he represtreasury bills are zero coupon bills w

par value to create a positive yield

procedure as done by Engle et al(19

in constructing the excess holding yie

)1(]1

2)^1([

1

3,6

t

t

t

t r r

R H +−

+

+=

+

This is approximated as

t t t t r r R H −−= +1

3,6

2

Where; the unit of time t stands for ev

t RIs the yield on a 6 month t

t r Is the yield on the 3 month

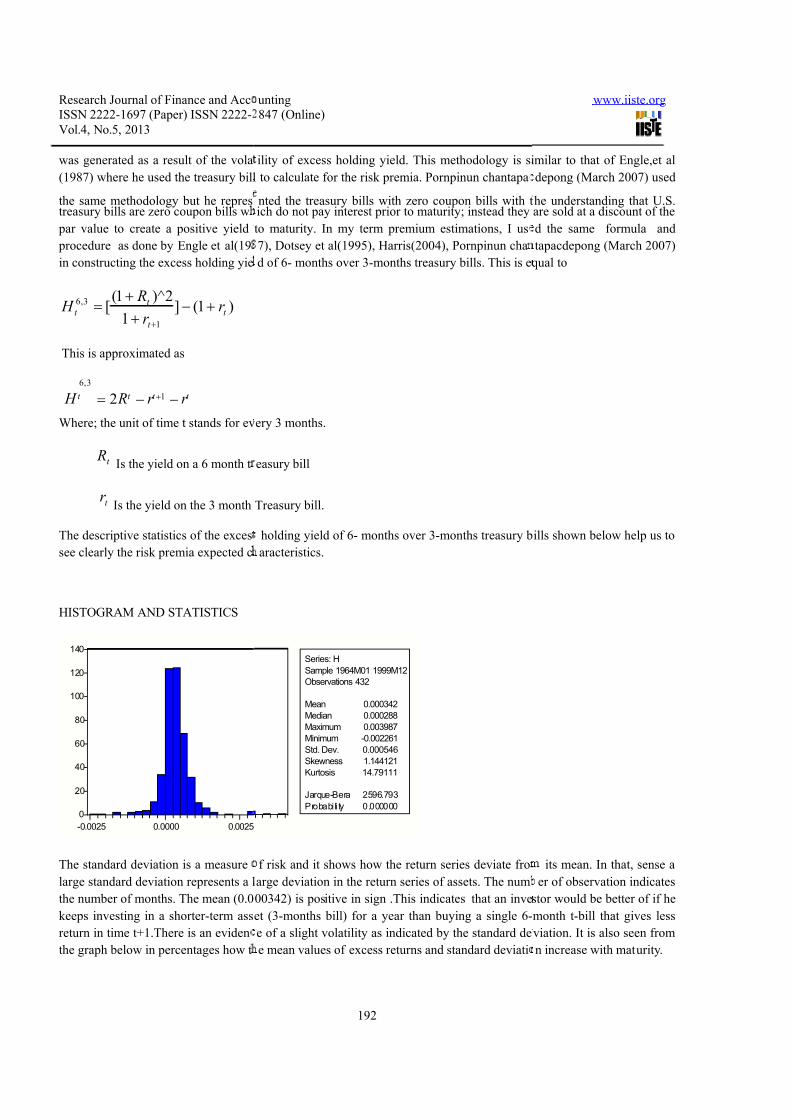

The descriptive statistics of the exces

see clearly the risk premia expected c

HISTOGRAM AND STATISTICS

The standard deviation is a measure

large standard deviation represents a l

the number of months. The mean (0.0

keeps investing in a shorter-term ass

return in time t+1.There is an eviden

the graph below in percentages how t

0

20

40

60

80

100

120

140

-0.0025 0.0000 0.0025

unting 847 (Online)

192

ility of excess holding yield. This methodology is si

to calculate for the risk premia. Pornpinun chantapa

nted the treasury bills with zero coupon bills with tich do not pay interest prior to maturity; instead they

to maturity. In my term premium estimations, I us

7), Dotsey et al(1995), Harris(2004), Pornpinun cha

d of 6- months over 3-months treasury bills. This is e

ery 3 months.

easury bill

Treasury bill.

holding yield of 6- months over 3-months treasury b

aracteristics.

f risk and it shows how the return series deviate fro

arge deviation in the return series of assets. The num

00342) is positive in sign .This indicates that an inve

et (3-months bill) for a year than buying a single 6-

e of a slight volatility as indicated by the standard de

e mean values of excess returns and standard deviati

Series: H

Sample 1964M01 1999M12

Observations 432

Mean 0.000342

Median 0.000288

Maximum 0.003987

Minimum -0.002261

Std. Dev. 0.000546

Skewness 1.144121

Kurtosis 14.79111

Jarque-Bera 2596.793

Probability 0.000000

www.iiste.org

milar to that of Engle,et al

depong (March 2007) used

he understanding that U.S.are sold at a discount of the

d the same formula and

tapacdepong (March 2007)

qual to

ills shown below help us to

its mean. In that, sense a

er of observation indicates

stor would be better of if he

month t-bill that gives less

viation. It is also seen from

n increase with maturity.

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 13/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

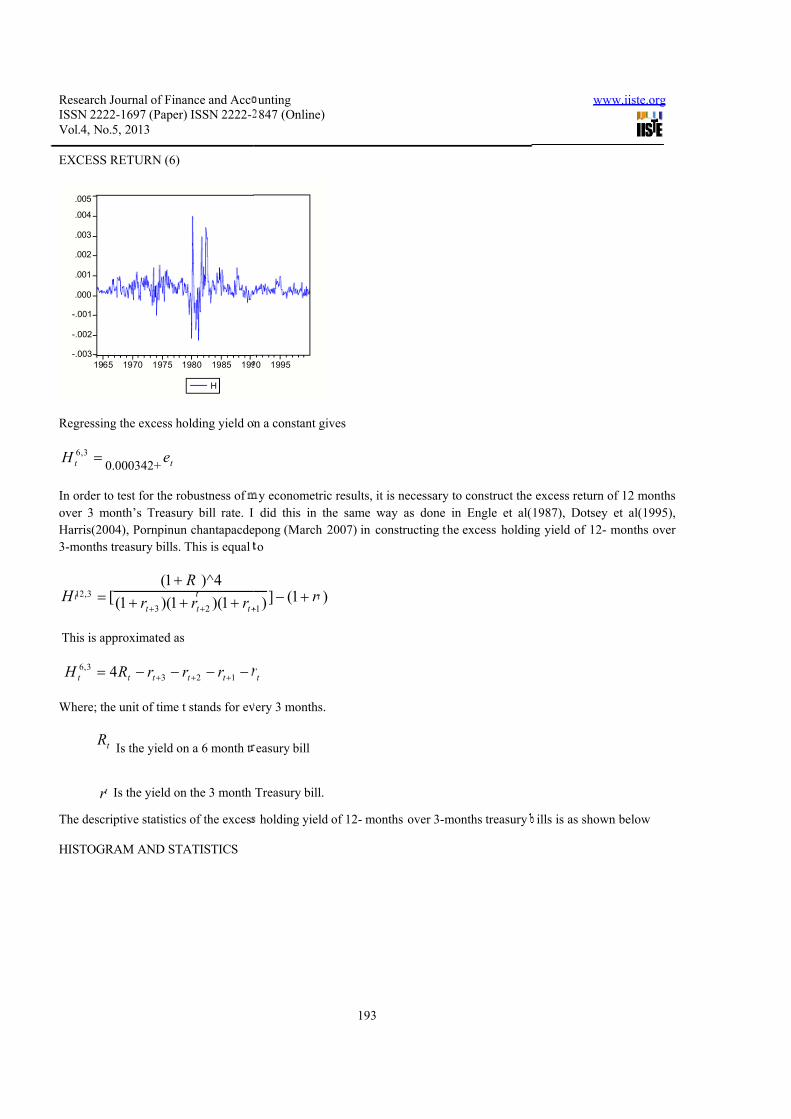

EXCESS RETURN (6)

Regressing the excess holding yield o

=3,6

t H 0.000342+ t e

In order to test for the robustness of

over 3 month’s Treasury bill rate. I

Harris(2004), Pornpinun chantapacde

3-months treasury bills. This is equal

1)(1)(1(

4)^1([

23

3,12

t t t

t t r r r

R H +++

+

=+++

This is approximated as

t t t t t r r r R H −−−−=+++ 123

3,6 4

Where; the unit of time t stands for ev

t RIs the yield on a 6 month t

t r Is the yield on the 3 month

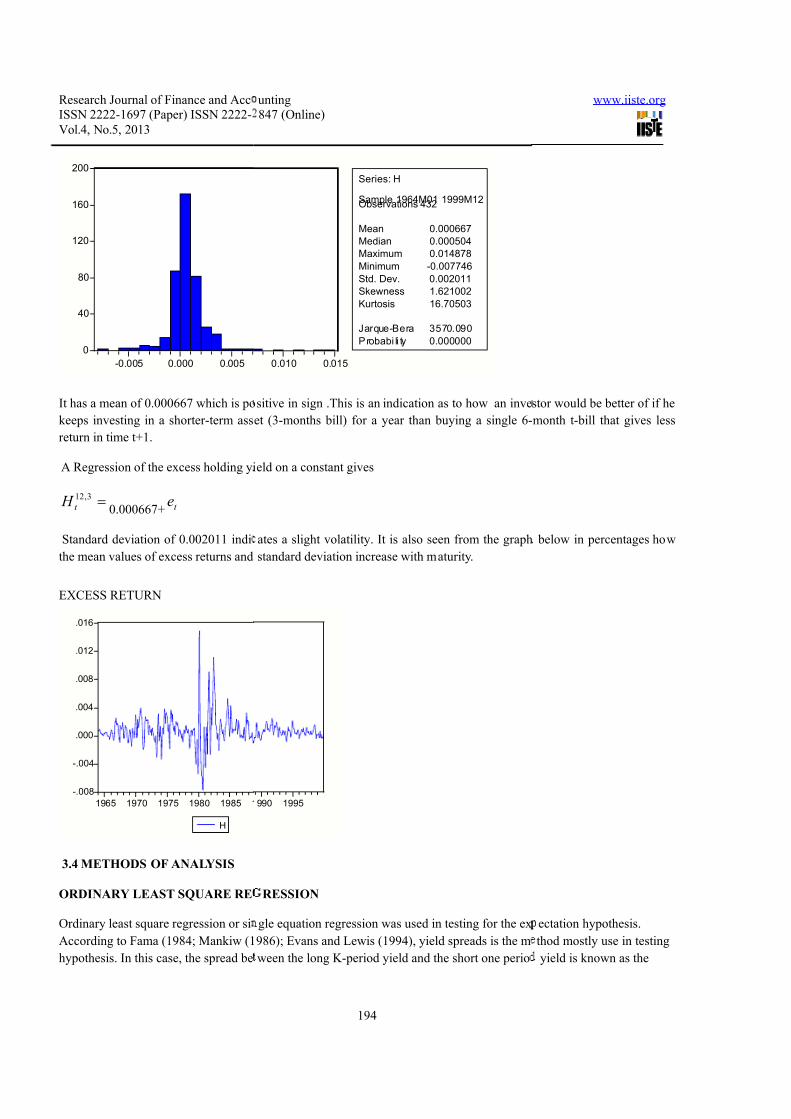

The descriptive statistics of the exces

HISTOGRAM AND STATISTICS

-.003

-.002

-.001

.000

.001

.002

.003

.004

.005

1965 1970 1975 1980 1985 199

H

unting 847 (Online)

193

n a constant gives

y econometric results, it is necessary to construct the

did this in the same way as done in Engle et al(

pong (March 2007) in constructing the excess holdin

o

)1(])1

t r +−

t

ery 3 months.

easury bill

Treasury bill.

holding yield of 12- months over 3-months treasury

0 1995

www.iiste.org

excess return of 12 months

1987), Dotsey et al(1995),

g yield of 12- months over

ills is as shown below

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 14/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

It has a mean of 0.000667 which is po

keeps investing in a shorter-term ass

return in time t+1.

A Regression of the excess holding yi

=3,12

t H 0.000667+ t e

Standard deviation of 0.002011 indi

the mean values of excess returns and

EXCESS RETURN

3.4 METHODS OF ANALYSIS

ORDINARY LEAST SQUARE RE

Ordinary least square regression or si

According to Fama (1984; Mankiw (1

hypothesis. In this case, the spread be

0

40

80

120

160

200

-0.005 0.000 0.005

-.008

-.004

.000

.004

.008

.012

.016

1965 1970 1975 1980 1985 1

H

unting 847 (Online)

194

sitive in sign .This is an indication as to how an inve

et (3-months bill) for a year than buying a single 6-

eld on a constant gives

ates a slight volatility. It is also seen from the graph

standard deviation increase with maturity.

RESSION

gle equation regression was used in testing for the ex

986); Evans and Lewis (1994), yield spreads is the m

ween the long K-period yield and the short one perio

0.010 0.015

Series: H

Sample 1964M01 1999M12Observations 432

Mean 0.000667

Median 0.000504

Maximum 0.014878

Minimum -0.007746

Std. Dev. 0.002011

Skewness 1.621002

Kurtosis 16.70503

Jarque-Bera 3570.090

Probabi li ty 0.000000

990 1995

www.iiste.org

stor would be better of if he

month t-bill that gives less

below in percentages how

ectation hypothesis.

thod mostly use in testing

yield is known as the

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 15/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

yield spread, contains the markets bes

gives equation (6)

1

1

11 )(++

+−+= t t

k

t o

k

t eY Y aa H

For reasons attributed to Eviews com

11 +++= t o eYS aa H

Where oa and 1a are constant coeffi

According to the expectation hypothe

The expectations hypothesis assumes

THE GARCH AND THE ARCH I

Unlike the above methodology that

methodology that assumes the term p

autoregressive conditional heterosked

current error term to be a function of

to the square of a previous period's er

varying volatility clustering, i.e. per

assumed for the error variance, theBollerslev(1986)) model. The GAR

equation.

In replication of the works of Walid

the term premia. Excess return is expr

2

,1

2

,11 +++++= t y yst ysO

k

t B B B H σ σ

Where

y=log of industrial production index

m=log of money supply

ex=log of the dollar-pound exchange

ys= yield spread

H=excess return

O B=constant term

unting 847 (Online)

195

t forecast of the change in the long term interest rate.

atibility and simplicity, I rewrite the equation above

ients and YS= yield spread and H=excess return

sisk

oa φ =and

01 =a.

the term premium to be a constant term.

MEAN MODEL OF THE TERM PREMIA.

assumes the term premium to be a constant, Engle

remium to be time varying instead of being a consta

asticity (ARCH, Engle (1982)) model takes into consi

the variances of the previous period’s error terms. A

or. It is employed commonly in modelling financial ti

iods of swings followed by periods of relative cal

odel is a generalized autoregressive conditional hH-in-mean (GARCH-M) model adds a heterosked

ejazi, Huiwen lai and Xian Yan (Feb 2000), I used

essed as a linear function in the form

1

2

,1

2

,1 ++++++ t ext exmt m B B µ σ σ

ate

www.iiste.org

riting and Rearranging

s

et al proposed the Garch

nt. In Financial economics,

deration the variance of the

CH links the error variance

me series that exhibit time-

.If an ARMA model is

teroskedasticity (GARCH,sticity term into the mean

the Arch in mean model of

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 16/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

By=coefficient on the conditional va

Bm=coefficient on the conditional v

Bys=coefficient on the level of yiel

Bex=coefficient on the conditional v

2

,1,1

2

,1 , ext mt yt and +++

σ σ σ , the cond

respectively.

Moreover, the conditional variances

2

,2

2

,1

2

,1 H t H t o H t aeaa σ σ ++=+

2

,2

2

,1

2

,1 yt yt o yt bebb σ σ ++=+

2

,2

2

,1

2

,1 mt mt omt cecc σ σ ++=+

2

,2

2

,1

2

,1 ext ext oext bed d σ σ ++=+

mt ext yt eee ,,, ,,Denotes serially unco

respectively. During this estimation,

regressions. It is known as multivari

into account the real and the monetar

conditional variances of industrial pro

4.0 ANALYSES, INTERPRETATI

4.1 TESTING THE EXPECTATIO

OLS regression test using the equatio

11 +++= t o eYS aa H

To test for

Appendices 1 and 2, together with Ta

and the constant on excess return for

months Treasury bill

unting 847 (Online)

196

riance of the industrial production index.

ariance of the money supply

spread

ariance of exchange rate

itional variances of industrial production, money

ere modeled as described below.

rrelated innovations in industrial production, excha

the conditional variance are estimated simultaneou

te Arch in mean estimation. One merit of this mod

sides of the economy and therefore allows excess ret

duction and the money supply.

N AND DISCUSSION OF EMPIRICAL RESULT

HYPOTHESIS

n below

y expectations hypothesis

les 1 show the OLS E-VIEWS and Tabulated output

oth the 6 months and the 12 months Treasury bill eac

www.iiste.org

upply, and exchange rate

ge rate and money supply

sly with the excess return

l estimation is that it takes

urns to be dependent on the

S.

f the effect of yield spread

h compared with the 3

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 17/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

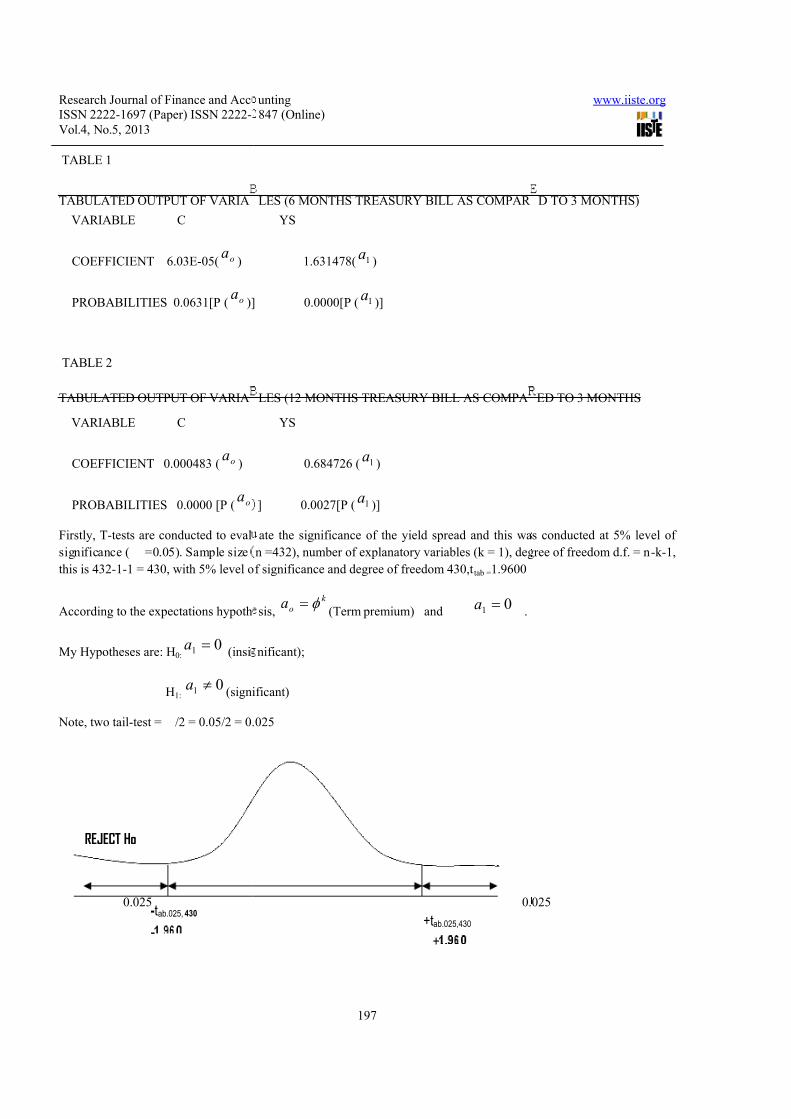

TABLE 1

TABULATED OUTPUT OF VARIA

VARIABLE C

COEFFICIENT 6.03E-05( oa )

PROBABILITIES 0.0631[P ( oa )]

TABLE 2

TABULATED OUTPUT OF VARIA

VARIABLE C

COEFFICIENT 0.000483 ( oa )

PROBABILITIES 0.0000 [P ( oa

Firstly, T-tests are conducted to eval

significance ( =0.05). Sample size

this is 432-1-1 = 430, with 5% level o

According to the expectations hypoth

My Hypotheses are: H0:01 =a

(insi

H1:01 ≠a

(signi

Note, two tail-test = /2 = 0.05/2 = 0.

0.025

REJECT Ho

-tab.025, 430

-

unting 847 (Online)

197

LES (6 MONTHS TREASURY BILL AS COMPAR

YS

1.631478( 1a )

0.0000[P ( 1a )]

LES (12 MONTHS TREASURY BILL AS COMPA

YS

0.684726 ( 1a )

] 0.0027[P ( 1a )]

ate the significance of the yield spread and this wa

n =432), number of explanatory variables (k = 1), deg

f significance and degree of freedom 430,t tab =1.9600

sis,k

oa φ =(Term premium) and

01 =a.

nificant);

ficant)

025

0.

+tab.025,430

+

www.iiste.org

D TO 3 MONTHS)

ED TO 3 MONTHS

s conducted at 5% level of

ree of freedom d.f. = n-k-1,

025

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 18/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

The t-distribution above provides u

significant in determining stock retu

explanatory variable. In general, th

accepted, this means that01 =a

a

following table and the analysis belo

A very simple way of doing this is by

spread. The principle we apply here i

denote probability.

From our eviews results

P ( 1a ) for the 6 months bill =0.0000

We therefore reject the null hypothesi

Similarly, for the 12 months bill P (a

Therefore, the null hypothesis 1a

hypothesis. . Another point of interest

also assumed that all my forecast erro

are time varying.

Although my2

R indicates that onlychanges in the excess holding return

of the expectations hypothesis obtain

(1990); Melano (1988) whose works

joint hypothesis that agents that hold

basis of either or both of these two r

because of of forecast errors, which a

2000),), Gregory and Voss (1991),

expectations hypothesis. The conditi

months Treasury bill each compared

significant predictors of excess return

the sign and the statistically significato my results, when there is an inc

increase in the yield. There is an evid

embedded in the ols results output

compared to 3 months treasury bill a

that the2 R statistics of the test incr

volatility associated with the excess r

4.2 THE MACROECONOMIC DE

unting 847 (Online)

198

s with a useful tool in making decision whether t

ns or not at the 5% level of significance and acco

e explanatory variable is said to be insignificant

d it is significant when the null hypothesis is rej

explain the decision rule for rejecting the expectatio

using the probabilities from the eviews output of bot

s that if the probability is less than .005 (5%), we rej

0.05

s that01 =a

1 ) =0.0027p 0.05

0is rejected. This in effect shows that I have

is that as we can see my 1a estimates significantly a

rs are orthogonal within the sample. This brings an ev

25.7 % and 20.6% respectively for my six monthf my data has been explained by the yield spread an

ed similar results when the research was conducted b

rejected the expectation theory of the term structure

rational expectations and term premia are time invari

easons. Either time-varying term premia caused the

ppear biased when viewed ex post. Walid Hejazi, Hu

Johnson (1993) and Kingler (1990) also had a si

nal variance of the yield spread in both the 6 mont

to the 3 months treasury bill are positive and can als

in the united state economy. I further reject the expec

ce of the yield spread. The expectations hypothesis iease in yield, investors of long-term treasury bills

ence of serial correlation in the residuals as explaine

at the appendix for my 6 months compared to 3

t the appendix. Moreover comparing the2 R of the t

eases as the term to maturity increases. The explan

turns increases variably with the term to maturity.

TERMINANTS OF THE TERM STRUCTURE.

www.iiste.org

he explanatory variable is

ding to the t-values of the

hen the null hypothesis is

ected that is01 ≠a

. The

s hypothesis.

h the constant and the yield

ct the null hypothesis. let p

rejected the expectations

e not equal to zero and it is

idence that the term premia

and my 12 months of thethe constant, my rejection

y Campbell (1995), Shiller

of interest rates which is a

ant. They rejected it on the

rejection or the rejection is

wen lai and Xian Yan (Feb

ilar results in testing the

s Treasury bill and the 12

o be viewed statistically as

tations hypothesis based on

s wrong because Accordingget a capital gain plus the

by my Durbin Watson test

onths and my 12 months

wo sets of results indicates

tion is that the risk or the

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 19/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

On the assumption that the term pr

variables were factored into the exce

came about is the one described belo

2

,1

2

,11 +++++= t y yst ysO

k

t B B B H σ σ

Running the garch equation with the

results on the next page.

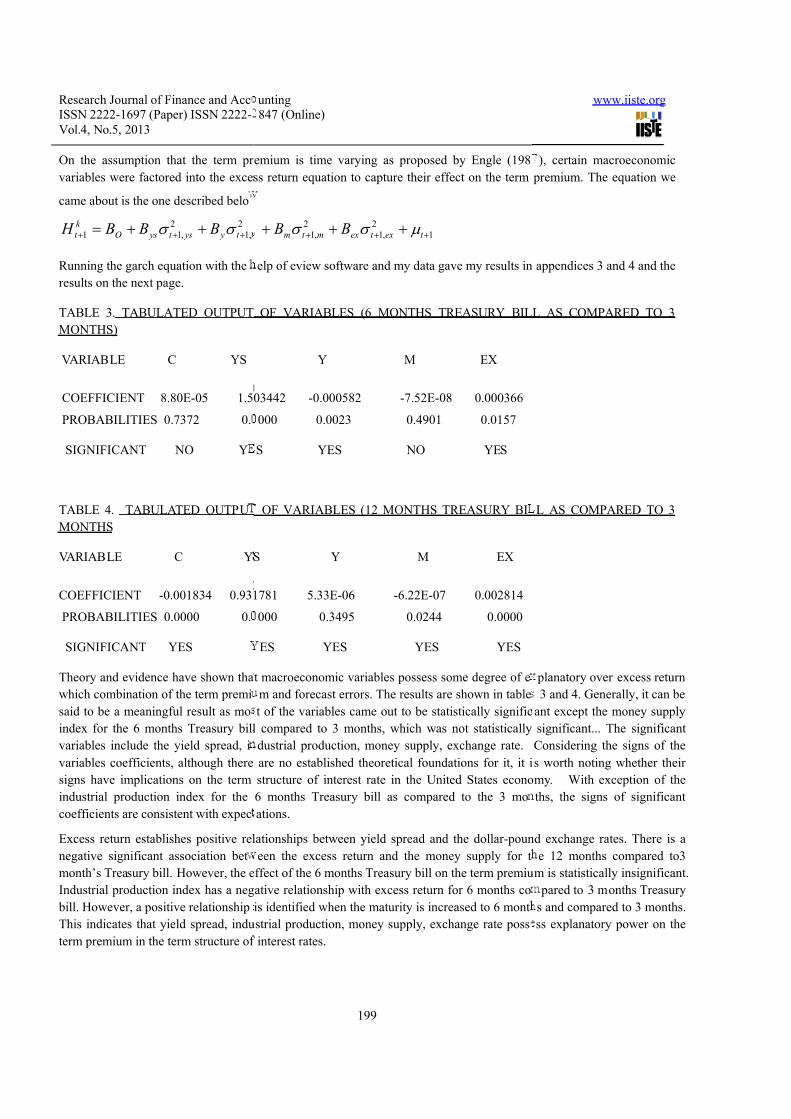

TABLE 3. TABULATED OUTPUT

MONTHS)

VARIABLE C YS

COEFFICIENT 8.80E-05 1.5

PROBABILITIES 0.7372 0.

SIGNIFICANT NO Y

TABLE 4. TABULATED OUTPU

MONTHS

VARIABLE C Y

COEFFICIENT -0.001834 0.93

PROBABILITIES 0.0000 0.

SIGNIFICANT YES

Theory and evidence have shown tha

which combination of the term premi

said to be a meaningful result as mo

index for the 6 months Treasury bill

variables include the yield spread, i

variables coefficients, although there

signs have implications on the term

industrial production index for the

coefficients are consistent with expec

Excess return establishes positive rel

negative significant association bet

month’s Treasury bill. However, the e

Industrial production index has a neg

bill. However, a positive relationship

This indicates that yield spread, indu

term premium in the term structure of

unting 847 (Online)

199

emium is time varying as proposed by Engle (198

ss return equation to capture their effect on the term

1

2

,1

2

,1 ++++++ t ext exmt m B B µ σ σ

elp of eview software and my data gave my results in

OF VARIABLES (6 MONTHS TREASURY BIL

Y M EX

03442 -0.000582 -7.52E-08 0.000366

000 0.0023 0.4901 0.0157

S YES NO YES

OF VARIABLES (12 MONTHS TREASURY BI

S Y M EX

1781 5.33E-06 -6.22E-07 0.002814

000 0.3495 0.0244 0.0000

ES YES YES YES

t macroeconomic variables possess some degree of e

m and forecast errors. The results are shown in table

t of the variables came out to be statistically signific

compared to 3 months, which was not statistically

dustrial production, money supply, exchange rate.

are no established theoretical foundations for it, it i

structure of interest rate in the United States econo

6 months Treasury bill as compared to the 3 mo

ations.

ationships between yield spread and the dollar-poun

een the excess return and the money supply for t

ffect of the 6 months Treasury bill on the term premiu

ative relationship with excess return for 6 months co

is identified when the maturity is increased to 6 mont

strial production, money supply, exchange rate poss

interest rates.

www.iiste.org

), certain macroeconomic

premium. The equation we

appendices 3 and 4 and the

L AS COMPARED TO 3

L AS COMPARED TO 3

planatory over excess return

3 and 4. Generally, it can be

ant except the money supply

significant... The significant

Considering the signs of the

s worth noting whether their

my. With exception of the

ths, the signs of significant

d exchange rates. There is a

e 12 months compared to3

m is statistically insignificant.

pared to 3 months Treasury

s and compared to 3 months.

ss explanatory power on the

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 20/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

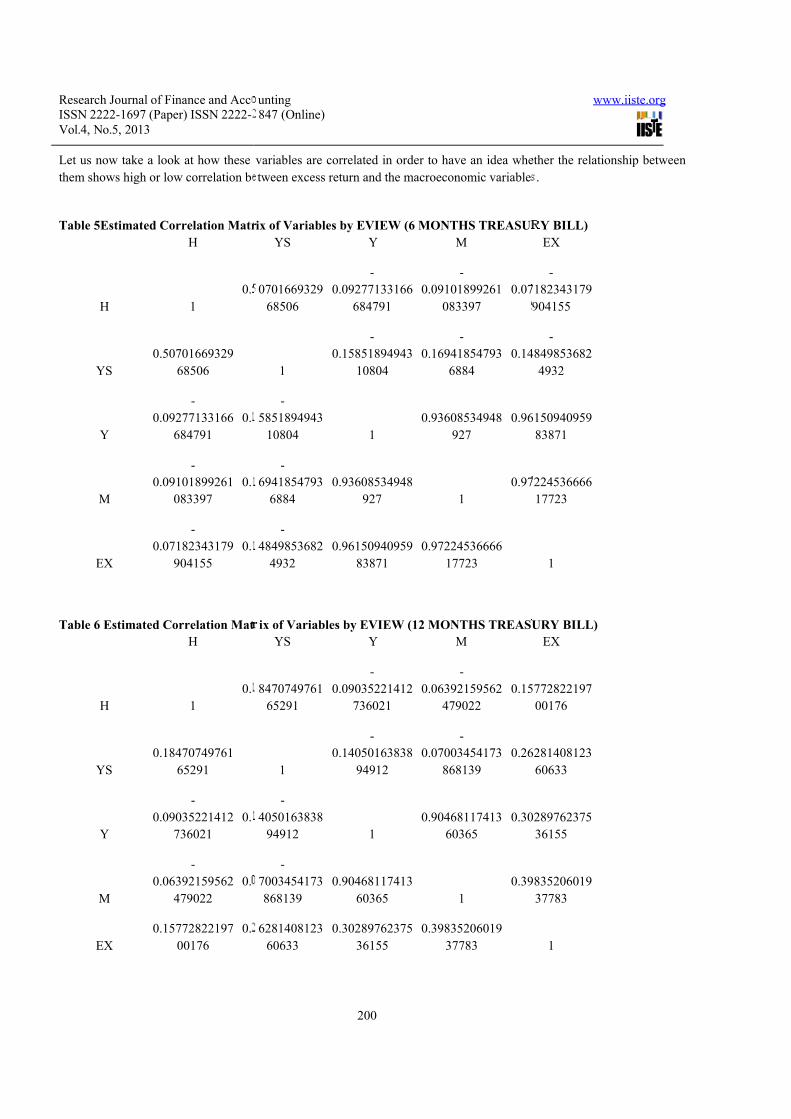

Let us now take a look at how these

them shows high or low correlation b

Table 5Estimated Correlation Matr

H

H 1

0.

YS

0.50701669329

68506

Y

-

0.09277133166

684791

0.

M

-

0.09101899261

083397

0.

EX

-

0.07182343179

904155

0.

Table 6 Estimated Correlation Mat

H

H 1

0.

YS

0.18470749761

65291

Y

-

0.09035221412

736021

0.

M

-

0.06392159562

479022

0.

EX

0.15772822197

00176

0.

unting 847 (Online)

200

variables are correlated in order to have an idea whe

tween excess return and the macroeconomic variable

ix of Variables by EVIEW (6 MONTHS TREASU

YS Y M

0701669329

68506

-

0.09277133166

684791

-

0.09101899261

083397

0.07

1

-

0.15851894943

10804

-

0.16941854793

6884

0.14

-

5851894943

10804 1

0.93608534948

927

0.96

-

6941854793

6884

0.93608534948

927 1

0.97

-

4849853682

4932

0.96150940959

83871

0.97224536666

17723

ix of Variables by EVIEW (12 MONTHS TREAS

YS Y M

8470749761

65291

-

0.09035221412

736021

-

0.06392159562

479022

0.15

1

-

0.14050163838

94912

-

0.07003454173

868139

0.26

-

4050163838

94912 1

0.90468117413

60365

0.30

-

7003454173

868139

0.90468117413

60365 1

0.39

6281408123

60633

0.30289762375

36155

0.39835206019

37783

www.iiste.org

ther the relationship between

.

Y BILL)

EX

-

182343179

904155

-

849853682

4932

150940959

83871

224536666

17723

1

URY BILL)

EX

772822197

00176

281408123

60633

289762375

36155

835206019

37783

1

7/30/2019 The Determinants of the Term Premium in the Term Structure of Interest Rates

http://slidepdf.com/reader/full/the-determinants-of-the-term-premium-in-the-term-structure-of-interest-rates 21/25

Research Journal of Finance and AccISSN 2222-1697 (Paper) ISSN 2222-Vol.4, No.5, 2013

While yield spread is positively corr

negative association. On the contrar

months treasury bill and positively co

Generally, this result overlaps theor

research.

Walid Hejazi, Huiwen lai and Xian Y

of industrial production, the money s

returns. On the other hand, the level o

statistically significant information f

conditional variance of both industri

excess returns. The conditional vari

significant predictors of excess retur these additional conditional variances

money supply falls dramatically. Th

moments of macroeconomic variable

three months. On the other hand, the

important information for excess ret

Treasury bill term structure.

Lee Sang-Sub ( May 1995) after inv

structure of interest rates, found out t

the money supply are significant in

power for the monthly excess return

money supply remain significant whespread which contains information ab

macroeconomic factors.

5.0 SUMMARY, CONCLUSIONS

5.1 SUMMARY OF RESULTS

The main purpose of this research is

of the term structure of interest rat

macroeconomic variables on the ter

macroeconomic variables has any si

researchers rejected the expectations

the existing empirical literature on t premia and the association between

done. Similarly, 432 monthly secon

from 1964 to 1999 has been used f

money supply, the dollar-pound exch

The yield spread is selected based o

structure of interest rates. The othe

researchers such as Engle et al(1987),

mention but a few. In line with the

1995) to mention but a few, excess r

unting 847 (Online)

201

elated with excess returns, industrial production an

dollar-pound exchange rates, is negatively correlate

related with excess return for the 12 months treasury

etical explanations as well as largely consistent wit

an (Feb 2000) result s using Canadian data indicates

upply and the exchange rates are statistically insigni

f yield spread and the conditional variance of excess

or excess returns. On the contrary, for the united st

al production and the money supply are statisticall

ance of excess returns themselves as well as the l

ns. The conditional variance of industrial productioare added. In addition, the coefficient estimates on t

y therefore concluded that ,In contrast to the unite

are not significant predictors on Canadian treasury

onditional variance of excess returns and the level of

urns. Again, they found evidence of time varying

stigating the macroeconomic sources of the time-va

at the Garch conditional variance estimates of the in

ll the risk premium equations examined. They also

nder investigation. The conditional variance of indus

n yield spread is added to the risk premium equation.out the risk premium, have significant explanatory p

ND RECOMMENDATIONS

to provide empirical testing of the expectations hypo

es in the United States economy in order to exa

structure of interest rates. Specifically, it has attem

gnificant explanatory power on the term structure .

hypothesis was also investigated. To achieve these ai

he expectations hypothesis, the theoretical derivatioome macroeconomic variables and the term structur

dary financial and macroeconomic data relating to

or the analysis. Macroeconomic variables namely i

nge rates and the yield spread were selected for the st

its dominant role in the excess return equation and i

r three variables were selected in accordance wit

Dotsey et al(1995), Harris(2004), Pornpinun chanta

orks of Walid Hejazi, Huiwen lai and Xian Yan (Feb

turn is used as a proxy for the term premium. the mai

www.iiste.org

money supply establishes a

with excess return for the 6

bill.

h findings of most previous

that the conditional variances

ficant determinants of excess

eturns themselves do contain

ate data, they found that the

significant determinants of

evel of yield spread is also

disappears, however, whene conditional variance of the

states evidence, the second

ill t of maturities of two and

yield spread do contain some

risk premia in the Canadian

ying risk premia in the term

dustrial production index and

show significant explanatory

rial production index and the

. He also found out that yieldower, despite the presence of

thesis and the determinants

ine closely the impact of

pted to Investigate whether

tests as to why the earlier

ms, an extensive review of

n of the time varying risk e of interest rates has been

he United States economy

dustrial production index,

udy.

s association with the term

the findings of previous

acdepong (March 2007) to