Embed Size (px)

Citation preview

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

1 www.globalbizresearch.org

The Determinants of Foreign Direct Investment (FDI) in Singapore

Holy Pondicherry,

Faculty of Economics,

Universitas Pelita Harapan,

Tangerang, Indonesia.

E-mail: [email protected]

Pauline Henriette P. Tan,

Faculty of Economics,

Universitas Pelita Harapan, Indonesia.

E-mail: [email protected]

___________________________________________________________________________

Abstract

For the past few years, foreign direct investment (FDI) has become the indicator to economic

growth, especially in emerging economies. Nonetheless, statistics have shown that Singapore

has been receiving 50% of the total FDI inflows coming to Southeast Asia each year. As a small

yet developed country, this fact has raised a big question mark and led to many discussions on

FDI determinants in Singapore. This research used an autoregressive distributed-lag

regression (ARDL) model on 25-year quarterly data for the period of 1990-2014 to find the

empirical evidence of some economic determinants toward FDI inflows in Singapore. This

research used interest rate as the proxy of local government's monetary policy, GDP as the

proxy of country's market size, and trade openness as the proxy of economic liberalization. The

use of ARDL estimation is caused by the stationarity statuses of variables. The results shown

that interest rate has no significance - yet positively affect the FDI inflows, while GDP and

trade openness have positive significant impact toward the FDI inflows. Thus, this research

accepted the alternative hypotheses of the relationship’s existence between FDI inflows and

interest rate, GDP, and trade openness. This research has provided better understanding on

the nature of FDI in Singapore and its correlation with economic factors and helped foreign

investors to make investment decision.

___________________________________________________________________________

Key Words: determinants of FDI, Singapore, foreign direct investment, FDI, interest rate,

gross domestic product, GDP, trade openness, trade liberalization, ARDL time-series

econometrics

JEL Classification: C 19, G13, G 14

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

2 www.globalbizresearch.org

1. Introduction

1.1 Background

Foreign direct investment has been the measurement of one economy’s economic growth

and economic openness, as it promotes the ability to receive other country’s participation in its

economy (Organisation for Economic Cooperation and Development, 2002). The developed

countries had been the main recipients of FDI, but studies have shown that for the past decade,

developing countries has been receiving more than the developed ones (Hansen, 1939).

Southeast Asia consists of a lot of developing countries that have been receiving lots of FDI

inflows and growing in its economy. Interestingly, Singapore – as the only developed economy

amongst the other emerging economies – has been holding roughly 50% of Southeast Asia’s

FDI inflows’ share since 1979 (United Nations, 2015). Referring to the fact that developing

countries receive more that developed countries, Singapore is an exception. For the past 25

years, its FDI has been focused on particular sectors, which are in financial and insurance,

wholesale and retail trade, manufacturing, professional and administrative, and transportation

and storage sectors (Central Intelligence Agency, 2016). There are a lot of determinants of FDI

and the magnitude of each determinant might influence the FDI inflows differently, depending

on the condition of the host country (United Nations Conference on Trade and Development,

2009).

1.2 Problem Statement and Objective

This research assumes that the FDI inflows coming into the developing countries should be

larger than the inflows coming into the developed counties. In contrast, as a developed country,

Singapore has been receiving more FDI inflows compared to the other developing countries in

Southeast Asia. This has raised big and arguable questions of how and why Singapore is very

attractive compared to all other emerging countries in Southeast Asia. The objective of this

research is to identify which determinants that play as major driver of high FDI inflows in

Singapore. It is expected to help foreign investors to obtain better understanding in the nature

of FDI and help the investment decision. The study is conducted to find the relationship

between FDI inflows and some economic determinants in Singapore. The economic

determinants that are taken as the independent variables are interest rate, GDP, and trade

openness.

2. Theoretical Background

2.1 Theoretical Framework

FDI is a real direct investment in equity capital in which the foreign investor retains control

over its capital and management. A 10-percent or more ownership is required to be considered

as a withholding status in the investment (Daniels, Radebaugh, & Sullivan, 2013). As the global

economic activities emerged, international trade and investment have contributed and played a

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

3 www.globalbizresearch.org

major role in global economy. The impact of the international trade and investment have come

from a comparative advantage theory proposed by David Ricardo and later followed by

Hecksher and Ohlin on factor abundant theory. A country should produce and export goods that

are using its relatively abundant-factors, while on the other hand import goods that are using its

relatively scarce-factors in its country (Pugel, 2015). This trading activity expanded to a foreign

investment, which is classified into two categories; international portfolio investment (IPI) and

FDI. In IPI, the foreign investor does not retain any direct control toward the business, while

FDI has control over its management and decision-making. There are a lot of motives underlie

behind the investment decision. The main motive is to earn more profits out of the business,

either by maximizing revenues or minimizing costs. Incentives such as higher growth rates and

returns in a country, lower prices for factors of production and transportation, strong

infrastructure, and lower taxes attract more foreign investors (Salvatore, 1995). Also,

multinational corporations (MNCs) claimed that the reason they existed is to pursue global

strategy. MNCs gain new market access abroad and obtain economies of scale and scope

(Daniels, Radebaugh, & Sullivan, 2013). These various motives are summarized into five main

drivers by Hymer in 1976. The five main drivers are the access of patented non-existent

technology, learning the ‘know-how’ or the management skills, obtaining economies of scale,

learning certain marketing capabilities and strategies, and owning certain brand reputation and

equity (Eiteman, Stonehill, & Moffett, 2013).

Many researchers all over the world have tried to explain the theory of FDI and came up

with different concepts of FDI. The oldest theory was proposed by Raymond Vernon in 1966

and called as the production cycle theory. He proposed that there are four stages of production,

which are innovation, growth, maturity, and decline. FDI occurs in growth phase to maintain

the market share abroad (Vernon, 1966). Another theory tries to explain FDI in different types

of market. In a perfect market, FDI is claimed to never happen because of its perfectly

competitive characteristics. The characteristics are large number of sellers and buyers

participated in the market, symmetrical knowledge, homogeneous product, no government

intervention, and all parties are both price takers and price setters. With equal opportunities and

rate of returns, no investors would like to invest in the economy (Kindleberger, 1969). In

contrary, in an imperfect market, where monopoly and oligopoly could exist, FDI is very likely

to happen (Nayak & Choudhury, 2014). In 1993, John Harry Dunning postulated an eclectic

theory called the OLI Paradigm. Ownership-specific advantages come from the ownership of

limited natural resources, patents, trademarks, and technology of innovation. Location-specific

advantages come from the economic factors of production and transportation, political factors

of common and specific policies regarding FDI, and social factors of distance between home

and host country. Internalization-specific advantage come from the execution of transactions

within the organization (Dunning, 1993).

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

4 www.globalbizresearch.org

Based on the various motives and concepts, three economic variables are suspected to be

the determinants of FDI in Singapore, which are interest rate, GDP, and trade openness. First,

the relationship between interest rate and FDI is explained in the theory of loanable funds

market and basic investment theory. According to the loanable funds theory, if the government

increases the interest rate, more people will invest to get higher returns which makes the supply

of loanable funds increases. Higher interest rate increases supply of loans. In investment theory,

when there is no risk and barriers of capital movement, investors will move the funds from

countries with lower interest rates to countries with higher interest rates. The higher the interest

rates, the higher the FDI inflows coming into the country (Parkin, 2014). Second, the

relationship between GDP and FDI inflows is also positive. As GDP catches the ability of a

country to produce goods as a whole, it perceives the ability of a country to consume goods as

well. The higher the GDP, the bigger the market size and ability to produce, purchase, and

consume, the more attractive a country to investors. FDI that seeks new market to expand its

business will see this variable to be highly attractive to its investing decision (Chawla & Rohra,

2015). Third, the relationship between trade openness and FDI inflows exists as the

international trade between countries emerged. The higher the trade volume of the host country,

the more liberalized its economy to outside participation, the easier foreign investors to

penetrate the market. Furthermore, the more active the host country is engaged in free trade

agreements or partnership, the more likely foreign investors to make business in the country. It

enhances both exports and imports of goods, and firms that run its business can sell its goods

to the host country’s free trade partners, which widen the market scope of its business.

Therefore, the more open a country to trade and investment, the higher the FDI inflows coming

into the country (United Nations Conference on Trade and Development, 1999).

2.2 Literature Review

A research by Eicher, Helfman, and Lenkoski in 2012 proved that some determinants of FDI

are actually not affecting the behavior of FDI although it has been proven for a long time ago.

The research was conducted in 36 OECD countries. They deducted that these behaviors or

characteristics may have changed as time goes by. Then they concluded that among many

determinants of FDI, only few turned out to be significant in their research. These determinants

are from the perspective of the host country, which are: the currency union used; preferential

trade agreement (PTA) membership (to measure the openness and the partnership of trade and

investments); market size; tax rates; productivity rate; and economic growth, which measured

by the GDP growth (Eicher, Helfman, & Lenkoski, 2012). Another study proved that the

determinants of FDI inflows are trade openness and exchange rates. The researcher found that

other economic variables, such as inflation, GDP, and interest rate were insignificant to be

called as the determinants of FDI inflows (Faroh & Shen, 2015). In another study, it was proven

that the exchange rates, trade openness, and inflation significantly affect the FDI inflows

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

5 www.globalbizresearch.org

(Kizilkaya, Ucler, & Ay, 2015). Other study has shown that trade openness, investment climate

(the previous or past behavior of the FDI), and political factor (in this research the researchers

used democracy as the measurement) are the determinants of FDI. Other variables, such as the

market size, potential growth, policy distortions (measured by exchange rate) have no impact

to FDI inflows (Nyarko, Nketiah-Amponsah, & Barnor, 2011). A Japanese researcher

conducted a study in India and proved that FDI in India is related positively with its GDP and

other market size variables, service sector variables, and infrastructure measured by telephone

lines per population (Tsuchiya, 2015). In one of Routledge’s publication, Handbook of

Southeast Asian Economics, the research shown that the economic stability and geographical

factors of the host country has been playing as major factors of FDI inflows. The economic

stability refers to the economic risk, such as exchange rates fluctuations and inflation (Sjoholm,

2015). In addition, another research proved that the main determinants of FDI inflows are the

market size and supportive infrastructure of the host country (Rehman, Ilyas, Alam, & Akram,

2011). A research was once conducted towards Association of Southeast Asian Nations

(ASEAN) top five countries, which are Indonesia, Malaysia, Singapore, the Philippines, and

Thailand. The research found that exchange rates, interest rates and GDP have significant

impact on FDI inflows in Thailand, Malaysia, and Indonesia. Inflation significantly affected

the FDI inflows in Thailand, Indonesia, and Singapore (Siddiqui & Aumeboonsuke, 2014).

2.3 Hypotheses

H0: There is no relationship between economic variable and FDI inflows

H1: There is a positive relationship between interest rate and FDI inflows

H2: There is a positive relationship between GDP and FDI inflows

H3: There is a positive relationship between trade openness and FDI inflows

3. Methodology

3.1 Data

The research used a set of time-series quarterly data from 1990 to 2014. The data for FDI

inflows are converted from yearly data to quarterly data using quadratic average-matched

technique, considering that FDI inflows data are reported annually (EViews, 2016). The

population of the data is Singapore, where the unit analysis is the country itself. This research

was using economic secondary data that were previously collected by professional

organizations and local government. The resources include: The World Bank Development,

International Monetary Fund (IMF), Department of Statistics Singapore, World Fact Book CIA,

and United Nations Conference on Trade and Development Statistics. The data for FDI inflows

are taken from The World Bank Development; the data for interest rates are taken from IMF;

and the data for GDP and trade openness are taken from Department of Statistics Singapore.

The functional form for both FDI inflows and GDP are changed into logarithmic form. The

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

6 www.globalbizresearch.org

logarithmic form used is the natural log, which means log to the base of e, where e equals to

2.718. For all hypothesis testing, this research used 5% level of significance as the critical value

of rejection area. Diagnostic tests are performed with econometrics method by using EViews.

3.2 Empirical Model

The model for FDI inflows in Singapore is formulated from the three independent variables

of interest rate, GDP, and trade openness. The mathematical function is shown as follows:

FDI = ƒ (IR, GDP, TO)

After several econometrics treatment for data analysis, the model is transformed into an

autoregressive distributed lag (ARDL) model, where the dependent variable’s lagged values

are accounted in the model as additional regressors. The model is shown below:

LFDIt = β0 + β1LFDIt-1 + β2LFDIt-2 + β3LFDIt-3 + β4IRt + β5LGDPt + β6TOt + εt

where t-1 is variable’s lagged value by one period, t-2 is variable’s lagged value by two period,

and t-3 is variable’s lagged value by three period. The lag length was determined automatically

by Akaike Information Criterion (AIC).

Foreign Direct Investment (FDI) – the data used for FDI inflows are interpolated from

yearly data to quarterly data. Due to the reason of large amount of its value compared to interest

rate and trade openness, the data are transformed into its logarithmic value. Denoted as LFDI,

the FDI net inflows are measured in constant 2010 US dollar (USD).

Interest Rate (IR) – the variable is used as a proxy of government’s effort to attract FDI.

Higher interest rates lead to higher attraction of foreign investors to invest in the country. Since

a higher rate will lead to higher returns for investment, which increases the FDI inflows, the

relation is expected to be positive. Denoted as IR, the interest rate used in the research is the

real interest rate of lending money and measured in percentage.

Gross Domestic Product (GDP) – the variable is used as a proxy of market size and

economic growth of the country. Increasing FDI flows to countries with increasing GDP leads

to an increase in the economic activity. Growth rates are positively related to foreign capital

stocks. Therefore, the expected relationship is positive. Denoted as LGDP, the type of GDP

used in this research is the constant GDP measured in constant 2010 SGD. Again, note that the

use logarithmic function is to lessen the distance between the large values and small values.

Trade Openness (TO) - the variable is used as a proxy of liberalization or openness to

factors coming from outside the country. The openness to trade enhances the attraction of

foreign investors to invest in the country. Foreign firms that operate its business in the country

could freely sell their goods and services to other countries. It means broader target market is

becoming accessible to foreign firms. Also, the more membership of bilateral agreements or

regional FTAs that a country engaged in, the wider the access of other countries to the traded

goods and services. Denoted as TO, trade openness is calculated as the percentage of net trade

volume (net trade = exports – imports) divided by the real or constant GDP (Faroh & Shen,

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

7 www.globalbizresearch.org

2015). The data for GDP used is the same data used for variable LGDP. The data for net trade

volume used are taken from its constant value.

3.3 Data Analysis

There are seven types of diagnostic test, which are: test for structural break; test for data

stationarity; ARDL estimation; test for optimum lag length; test for heteroscedasticity; test for

autocorrelation; and test for long-run relationship (Gujarati, 2003).

1. Structural Break: a set of time-series data that has a long-time period tend to have a structural

change in between. The structural break test is used to test the stability of parameters overtime

to determine point of break. The test conducted is multiple breakpoint test that uses Schwarz

Information Criterion (SIC).

2. Stationarity: stationarity is one unique characteristic of time-series dataset. The test is

performed to avoid indication of spurious regression and estimation. Sometimes the data should

involve differencing or detrending technique (I(1)). Augmented Dickey-Fuller (ADF) multiple

breakpoint unit root test is performed to test the stationarity. This test measures the stationarity

of data in multiple breakpoints exist. All data in all breakpoints should be stationary either in

level I(0) or I(1) (EViews, 2016).

3. ARDL Estimation: the ARDL estimation technique is used because the level of stationarity

of the model is a combination between I(0) and I(1). The inclusion of lagged values is

considered necessary because some economic variables need time to show its impact toward

other variables. The regression result is used as a short-run estimation.

4. Optimum Lag Length: as the result of inclusion of lagged values, the model needs to establish

the optimum lag length. The model selection criterion is used to choose the best number of lag

length. This research used Akaike Information Criterion (AIC) because it has the least harsh

penalty or error. The lower the AIC, the better the model.

5. Heteroscedasticity: heteroscedasticity is a phenomenon where the spread of variance is not

equal over time. The presence of heteroscedasticity could increase standard errors and increase

bias of the research. Due to the presence of lagged values, this research used autoregressive

conditional heteroscedasticity (ARCH) test. It accounts the unequal weight of observations and

increase preciseness (Engle, GARCH 101: The Use of ARCH/GARCH Models in Applied

Econometrics, 2001).

6. Autocorrelation: autocorrelation is the relationship exist in the residual members of series of

observation. It shows a systematic pattern within residuals that should not be existed. The

presence of autocorrelation increase bias and mislead the research. The research used Breusch-

Godfrey / Lagrange Multiplier (BG / LM) test. It needs a pre-specified lag length that was

obtained in optimum lag length test (Gujarati, 2003).

7. Long-Run Relationship: an ARDL model estimates the dynamic relationship between

variables. It is possible to transform the model into a long-run form even if the model has

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

8 www.globalbizresearch.org

different level of integration (cointegration). To test the existence of long-run relationship of

an ARDL model, bounds test is conducted. If long-run relationship exists, it should proceed to

long-run estimation (Engle & Granger, Co-Integration and Error Correction: Representation,

Estimation, and Testing, 1987).

4. Results and Discussion

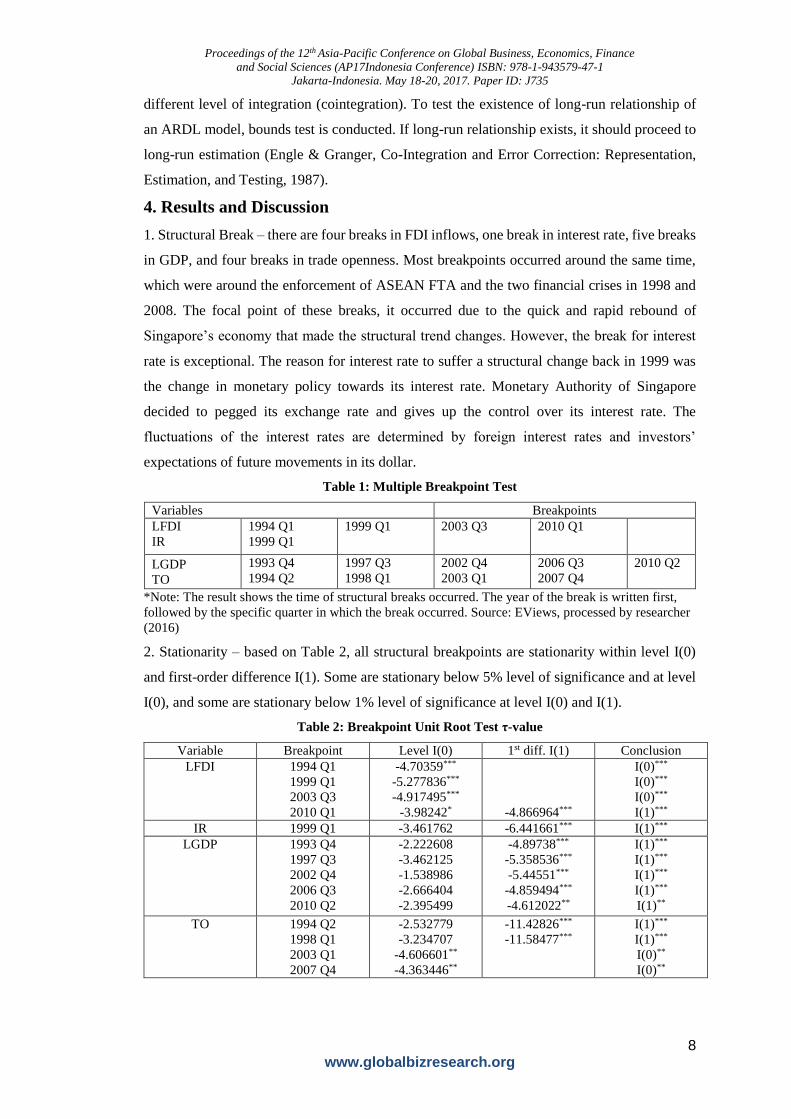

1. Structural Break – there are four breaks in FDI inflows, one break in interest rate, five breaks

in GDP, and four breaks in trade openness. Most breakpoints occurred around the same time,

which were around the enforcement of ASEAN FTA and the two financial crises in 1998 and

2008. The focal point of these breaks, it occurred due to the quick and rapid rebound of

Singapore’s economy that made the structural trend changes. However, the break for interest

rate is exceptional. The reason for interest rate to suffer a structural change back in 1999 was

the change in monetary policy towards its interest rate. Monetary Authority of Singapore

decided to pegged its exchange rate and gives up the control over its interest rate. The

fluctuations of the interest rates are determined by foreign interest rates and investors’

expectations of future movements in its dollar.

Table 1: Multiple Breakpoint Test

Variables Breakpoints

LFDI

IR

1994 Q1

1999 Q1

1999 Q1 2003 Q3 2010 Q1

LGDP

TO

1993 Q4

1994 Q2

1997 Q3

1998 Q1

2002 Q4

2003 Q1

2006 Q3

2007 Q4

2010 Q2

*Note: The result shows the time of structural breaks occurred. The year of the break is written first,

followed by the specific quarter in which the break occurred. Source: EViews, processed by researcher

(2016)

2. Stationarity – based on Table 2, all structural breakpoints are stationarity within level I(0)

and first-order difference I(1). Some are stationary below 5% level of significance and at level

I(0), and some are stationary below 1% level of significance at level I(0) and I(1).

Table 2: Breakpoint Unit Root Test τ-value

Variable Breakpoint Level I(0) 1st diff. I(1) Conclusion

LFDI 1994 Q1

1999 Q1

2003 Q3

2010 Q1

-4.70359***

-5.277836***

-4.917495***

-3.98242* -4.866964***

I(0)***

I(0)***

I(0)***

I(1)***

IR 1999 Q1 -3.461762 -6.441661*** I(1)***

LGDP 1993 Q4

1997 Q3

2002 Q4

2006 Q3

2010 Q2

-2.222608

-3.462125

-1.538986

-2.666404

-2.395499

-4.89738***

-5.358536***

-5.44551***

-4.859494***

-4.612022**

I(1)***

I(1)***

I(1)***

I(1)***

I(1)**

TO 1994 Q2

1998 Q1

2003 Q1

2007 Q4

-2.532779

-3.234707

-4.606601**

-4.363446**

-11.42826***

-11.58477***

I(1)***

I(1)***

I(0)**

I(0)**

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

9 www.globalbizresearch.org

*Note: Table 4.3 summarizes the τ-value for each stationarity, followed with * indicator. The indicator

shows that the computed τ-value exceeds the critical τ-value. ***, **, * are 1%, 5% and 10% respectively.

Source: EViews, processed by researcher (2016)

3. ARDL Estimation – Table 3 shows the components of the model with its variables’

coefficients and probability. Based on the result, the lagged values are applied only to the

dependent variable, LFDI, with the lag of three time periods. The three independent variables,

IR, LGDP, and TO, have no lagged values. The Probability of t-statistic column shows that in

this ARDL estimation, interest rate is highly insignificant to the model. The second lagged

value of FDI is nearly significant at 10% level of significance. The rest of the regressors are

significant below 5% and 1%. First, in the short run, the lagged values of FDI inflows give

significant contribution toward the current FDI inflows. It shows that the decision of current

investment is affected by the past behavior of previous investment. Second, interest rate barely

affects FDI inflows, with coefficient of 0.0206 and insignificant probability of 0.5667. Third,

GDP and trade openness are proved to affect FDI inflows significantly, where GDP has a

coefficient of 0.4439 and probability of nearly 0, and trade openness with coefficient of 0.4351

and probability of 0.03980. As the explanation of structural breaks existence explain how the

change in trade affected the economic growth and its GDP, it also explains how GDP and trade

openness is closely related to the growth of foreign investment. The adjusted R2 is 0.9593,

which suggest that the variability in the dependent variable is explained 95.93% by the

variability of its regressors. The Durbin-Watson statistic is 2.0435, which suggest that the

model contains no serial correlation between disturbances.

Table 3: ARDL Estimation

Variables Coefficient t-statistic Probability of t-statistic

LFDI (-1) 1.178535 11.45765 0.00000***

LFDI (-2) -0.258412 -1.623832 0.10790

LFDI (-3) -0.252095 -2.474089 0.01520**

IR 0.020617 0.575043 0.56670

LGDP 0.443864 4.309043 0.00000***

TO 0.43514 2.085559 0.03980**

C -3.552466 -1.992763 0.04930**

�̅�2 = 0.959268 Prob. (F-stat) = 0.000 Durbin-Watson stat = 2.043463

*Note: ***, **, * are 1%, 5% and 10% respectively. Source: EViews, processed by researcher (2016)

4. Optimum Lag Length – The maximum lag length inserted was 4 lags for both dependent and

independent variables. The result shows the 20 best model with lowest AIC values. As seen in

Figure 1, the lowest AIC value shows that the optimum lag length is ARDL(3,0,0,0). It means

that the dependent variable has 3 lags, and the three independent variables have 0 lag. With

AIC value of -0.5954, the optimum lag length is 3 lags for LFDI and 0 lag for IR, LGDP, and

TO.

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

10 www.globalbizresearch.org

Figure 1: AIC Criteria Graph

Source: EViews, processed by researcher (2016)

5. Heteroscedasticity – Table 4 shows that the probability of ARCH value has failed to reject

the null hypothesis. With the computed χ2 value (ARCH value) of 2.03263 and its probability

of 0.5657, the value is not statistically significant to reject the null hypothesis. Thus, the null

hypothesis is failed to reject. In other words, the ARCH components are not present and the

model is homoscedastic.

Table 4: Summary of Heteroscedasticity and Autocorrelation Test

Test Lag order χ2 Probability of χ2 Result

ARCH 3 2.03263 0.5657 Fail to reject H0

BG / LM 3 3.448664 0.3275 Fail to reject H0

Source: EViews, processed by researcher (2016)

6. Autocorrelation – Table 4 shows that the probability of BG-value has failed to reject the null

hypothesis. With the number of lag order of 3, which were specified using the AIC, the

computed χ2 value (BG-value) of 3.448664, and its probability of 0.3275, the value is not

statistically significant to reject the null hypothesis. Thus, the null hypothesis is failed to reject.

In other words, there is no serial correlation up to lag order 3.

Table 5: ARDL Bounds Test for Cointegration

Test Statistic Value Relationship

F-statistic 8.944848*** Long-run

Critical Value I(0) / Lower Bound I(1) / Upper Bound

10% 2.72 3.77

5% 3.23 4.35

2.5% 3.69 4.89

1% 4.29 5.61

Source: EViews, processed by researcher (2016)

Table 6: ARDL Cointegrating and Long-Run Form

Cointegrating Form

Variables Coefficient t-statistic Probability of t-

statistic

D(LFDI (-1)) 0.510507 5.69899 0.0000***

D(LFDI (-2)) 0.252095 2.474089 0.0152**

D(IR) 0.020617 0.575043 0.5667

D(LGDP) 0.443864 4.309043 0.0000***

TO 0.43514 2.085559 0.0398**

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

11 www.globalbizresearch.org

CointEq (-1) -0.331972 -5.966825 0.0000***

Long-Run Coefficient

Variables Coefficient t-statistic Probability of t-

statistic

IR 0.062105 0.591119 0.5559

LGDP 1.337053 7.298841 0.0000***

TO 1.310774 2.182625 0.0317**

C -10.701107 -2.249445 0.0269**

Cointegration Equation = LFDI – (0.0621 IR + 1.3371 LGDP + 1.3108 TO – 10.7011)

Note: ***, **, * are 1%, 5% and 10% respectively. The upper part of Table 4.7 presents the cointegrating

form of dependent variable and independent variables. The lower part presents the coefficient that forms

a long-run relationship. Source: EViews, processed by researcher (2016)

7. Long-Run Relationship – based on Table 5, the result has shown that there is level and long-

run relationship between dependent and independent variables. With the computed F-statistic

of 8.944848 and the probability of F-statistic is smaller than 0.01, it passes both lower and upper

bound of 1% level of significance. Table 6 has the focus of regressor CointEq (-1). This variable

represents the error-correction coefficient. The coefficient should be significant below 5% level

of significance and negative in value to be said that cointegration exists. With the value of error-

correction coefficient of -0.331972 and its probability of t-statistic of 0.0000, the coefficient is

highly significant. The lower part of Table 6 presents the coefficient of the long-run relationship

between FDI inflows, interest rate, GDP, and trade openness. Interest rate is not statistically

significant, while GDP and trade openness are still statistically significant in the long-run. The

cointegration equation is presented at the very bottom of the table. Although interest rate’s

coefficient increases by 310% from the short-run ARDL estimation, the probability of t-statistic

shows that both in long-run and short run, the FDI inflows is not affected by the interest rate.

In contrast, GDP and trade openness impact Singapore’s FDI inflows significantly. Both

coefficient show that if 1 unit change in each variable changes FDI inflows for around 0.44

unit, which is considered to be high. This could be explained by the fact that Singapore has

been attracting its investor with other measures that include GDP and trade openness. The three

variables’ significance toward FDI inflows are explained together in one discussion as follows:

a. Singapore has been attracting its foreign investors with tax incentives. Low corporate

tax, tax exemptions for all foreign-sourced income in several industries, enhance more tax

incentives specifically for firms operating in financial services and other industries that it tries

to grow, extend the maximum incentive duration for pioneer that has its business activities in

Singapore, engaged in double taxation treaties (DTTs) with more than 70 countries, tax

dividend of 0%, and the highest tax applied to the income is only 17% (World Trade

Organization, 2008). Therefore, interest rates are no longer important in foreign investors eyes,

for its tax incentives has saved them a lot of money. The yield that was expected from the

interest rates are offsetted by the fact that Singapore has been very active in trading.

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

12 www.globalbizresearch.org

b. Singapore has been engaging itself into many bilateral and regional FTAs. Trade

relations is one of the motives in explaining FDI (Salvatore, 1995). By engaging in many FTAs,

Singapore increases its openness, both trade and investment sectors, therefore enlarging the

connections for trading and investing partners. By investing in Singapore that increases its trade

volume over time, it is expected that the firms operating inside the country will be able to access

new market abroad through trading.

c. The increase in trading volume increases the country’s GDP. Higher GDP leads to

higher economic growth of the country. From the previous explanation, it could be seen that

the economic growth is significantly affect the decision of FDI inflows. Higher economic

growth implies higher contribution and economically active in the global market, higher

consumption, and greater market size and spending. Therefore, investors are expecting more

revenue from businesses in Singapore (World Trade Organization, 2008).

d. Singapore liberalized the financial and legal sectors to enhance the growth in its

economy. It planned to turn the city into a financial hub, where Singapore is a focal point for

the financial services industry. It has becoming the home for financial services, especially in

finance (banks) and insurance sector (World Trade Organization, 2008).

5. Conclusions and Recommendations

5.1 Conclusion

The research studied the relationship of FDI inflows and some of its economic determinants

in Singapore. The purpose is to establish the relationship and magnitude of interest rate, GDP,

and trade openness toward the FDI inflows. The findings have shown that interest rate has no

significant impact toward FDI inflows in Singapore for both short-term and long-term. It does

have a positive impact toward FDI inflows, but the significance is nowhere to be found. This

result has been found to be in contrast with any other previous literatures which stated that

interest rate has a positive significant influence toward FDI inflows in other countries. As the

interest rates in Singapore have gone only minor fluctuations over time, the FDI inflows kept

increasing and reached its peak disregarding the growth of interest rates. In addition, the usage

of secondary data could increase the possibility of variable’s insignificance. It frequently

contains numbers of errors due to erroneous transcription and faulty rounding-offs, making it

less dependable for the research accuracy. Nonetheless, the result supported H1 with minor

importance in impacting FDI inflows to change. Also, the findings have shown that both GDP

and trade openness have significant impact toward FDI inflows in short-term and long-term.

Both have shown positive relationship with FDI inflows for around the same magnitude. These

results correspond with other previous literatures which stated that GDP and trade openness

enhance FDI inflows in a country. The FDI inflows kept increasing in accordance of its market

size and trade liberalization’s growth. The result supported both H2 and H3, which stated that

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

13 www.globalbizresearch.org

GDP and trade openness have positive impact toward the FDI inflows in Singapore. Thus, the

research has answered the research questions where interest rate insignificantly impacted the

FDI inflows, while GDP and trade openness significantly impacted the FDI inflows in

Singapore.

5.2 Research Limitation

The limitation of this research is data availability. The availability for all variables are vary.

The quarterly data of FDI inflows were not available and needed to be interpolated. If the

research could use the real quarterly data for FDI inflows, it could decrease the standard errors

and increase precision of estimation.

5.3 Future Research Recommendation

Hence, this research has a suggestion for the future research. Due to its unique economic

conditions, there should be more studies conducted about particular sectors of FDI in

Singapore, especially in financial & insurance sector and manufacturing sector. Investment

decisions may vary according to the nature of each sector. Financial & insurance sector and

manufacturing sector have been holding 50% and 15% of Singapore’s FDI inflows shares

respectively. Moreover, the manufacturing sector is now growing its share in Singapore.

References

Central Intelligence Agency, 2016. World FactBook CIA. [Online]

Available at: https://www.cia.gov/library/publications/the-world-factbook/rankorder/2198rank.html

[Accessed 27 August 2016].

Chawla, K. & Rohra, N., 2015. Determinants of FDI: A Literature Review. The International Journal

of Business & Management, pp. 227-250.

Daniels, J. D., Radebaugh, L. H. & Sullivan, D. P., 2013. Globalization and International Business. In:

International Business: Environment and Operations. Harlow: Pearson Education, pp. 45-87.

Dunning, J. H., 1993. Global Strategy and the Theory of International Production. In: The

Globalization of Business: The Challenge of the 1990s. London: Routledge Revivals, pp. 78-97.

EViews, 2016. EViews Help. [Online]

Available at: http://www.eviews.com/help/helpintro.html

EViews, 2016. EViews Tutorial: Frequency Conversion Part A. [Online]

Available at: http://www.eviews.com/Learning/freqconv_a.html

Eicher, T. S., Helfman, L. & Lenkoski, A., 2012. Robust FDI Determinants: Bayesian Model -

Averaging in the Presence of Selection Bias. Journal of Macroeconomics, pp. 637-651.

Eiteman, D. K., Stonehill, A. I. & Moffett, M. H., 2013. Foreign Direct Investment: Return and Risks.

In: Multinational Business Finance. Harlow: Pearson Education, pp. 482-509.

Engle, R. F., 2001. GARCH 101: The Use of ARCH/GARCH Models in Applied Econometrics. The

Journal of Economic Perspectives, pp. 157-168.

Engle, R. F. & Granger, C. W. J., 1987. Co-Integration and Error Correction: Representation,

Estimation, and Testing. Econometrica, pp. 251-276.

Faroh, A. & Shen, H., 2015. Impact of Interest Rates on Foreign Direct Investment: Case Study Sierra

Leone Economy. International Journal of Business Management and Economic Research (IJBMER),

pp. 124-132.

Gujarati, D. N., 2003. Basic Econometrics, Fourth Edition. New York: Mc-Graw Hill.

Proceedings of the 12th Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP17Indonesia Conference) ISBN: 978-1-943579-47-1

Jakarta-Indonesia. May 18-20, 2017. Paper ID: J735

14 www.globalbizresearch.org

Hansen, A. H., 1939. Economic Progress and Declining Population Growth. The American Economic

Review, pp. 1-15.

Kindleberger, C. P., 1969. American Business Abroad: Six Lectures on Direct Investment. New

Haven(CT): Yale University Press.

Kizilkaya, O., Ucler, G. & Ay, A., 2015. The Interaction between Exchange Rate and Foreign Direct

Investments: Evidence from Turkey. Journal of Business and Economics, pp. 337-347.

Nayak, D. & Choudhury, R. N., 2014. A Selective Review of Foreign Direct Investment Theories,

Bangkok: Asia - Pacific Research and Training Network on Trade.

Nyarko, P. A., Nketiah-Amponsah, E. & Barnor, C., 2011. Effects of Exchange Rate Regimes on FDI

Inflows in Ghana. International Journal of Economics and Finance, pp. 277-286.

Organisation for Economic Cooperation and Development, 2002. Foreign Direct Investment for

Development: Maximising Benefits, Minimising Costs, France: OECD Publications Service.

Parkin, M., 2014. Monetary Policy. In: Economics, Eleventh Edition. Harlow: Pearson Education

Limited, pp. 753-778.

Pugel, T. A., 2015. Why Everybody Trades: Comparative Advantage. In: International Economics.

New York: McGraw-Hill, pp. 31-46.

Rehman, A., Ilyas, M., Alam, H. M. & Akram, M., 2011. The Impact of Infrastructure on Foreign

Direct Investment: The Case of Pakistan. International Journal of Business and Management, pp. 268-

276.

Salvatore, D., 1995. International Resource Movements and Multinational Corporations. In:

International Economics. Englewood Cliffs: Prentice Hall, pp. 367-395.

Siddiqui, H. A. A. & Aumeboonsuke, V., 2014. Role of Interest Rate in Attracting the FDI: Study on

ASEAN 5 Economy. International Journal of Technical Research and Applications, pp. 59-70.

Sjoholm, F., 2015. Foreign Direct Investment in Southeast Asia. s.l., Routledge, pp. 1-36.

Tsuchiya, Y., 2015. Determinants of Foreign Direct Investment in India: Region Sector Wise Analysis,

Tokyo: Tokyo University of Foreign Studies.

United Nations Conference on Trade and Development, 1999. Foreign Direct Investment, Trade and

Development: Policy Issues. In: Foreign Direct Investment and Development. Geneva: United Nations

Publication, pp. 45-52.

United Nations Conference on Trade and Development, 2009. Host Country Determinants of FDI. In:

The Role of International Investment Agreements in Attracting Foreign Direct Investment to

Developing Countries. New York; Geneva: United Nations Publication, pp. 5-28.

United Nations, 2015. Foreign direct investment: Inward and Outward flows and stock, annual, 1980-

2014. [Online]

Available at: http://unctadstat.unctad.org/wds/TableViewer/tableView.aspx

Vernon, R., 1966. International Investment and International Trade in The Product Cycle. Quarterly

Journal of Economics, pp. 190-207.

World Trade Organization, 2008. [Online]

Available at: https://www.wto.org/english/tratop_e/tpr_e/s202-01_e.doc