Embed Size (px)

Citation preview

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 1/11

The demand chain as anintegral component of the value chain

David Walters and Mark Rainbird

The authors

David Walters is Professor andMark Rainbird is ResearchFellow, both at the Sydney Graduate School of Management,

Sydney, Australia.

Keywords

Value chain, Supply and demand, Supply chain management

Abstract

The term “value chain” encompasses a variety of ideas andconcepts. This paper identies two major themes: a “macro”perspective of how markets operate and, at the other extreme, aprocess-driven “micro” view of the individual rm itself.Focusing on the latter in particular, it seems that corporateemphasis is increasingly efciency based with the primeobjective the reduction of costs. The recent difcultiesexperienced by McDonald’s, Sainsbury and Marks & Spencermay be due in part to a single-minded focus on supply-chainmanagement. Instead it is argued that a rm is best placed tocreate value and exploit market opportunities when there is aneffective combination of supply-chain capabilities and demand-chain effectiveness to maximise the organisation’s overall valuechain. These issues are explored using practical examples fromthe retail and fast food industries. Questions whether traditionalviews of marketing are broad enough or whether, just as thelogistics manager reinvented himself as the supply-chainmanager and the new corporate hero, the marketingprofessional needs to reinvent himself as the demand-chainmanager.

Electronic access

The Emerald Research Register for this journal isavailable atwww.emeraldinsight.com/researchregister

The current issue and full text archive of this journal isavailable atwww.emeraldinsight.com/0736-3761.htm

The notion of value chains probably has its originswith Michael Porter, almost 20 years ago (Porter,1985). Simplistically, Porter proposed the value-chain concept as a means of identifying each of thebusiness actions or stages that transformed inputsinto outputs.

Since that time quite a literature has developedaround value chains and related topics. Indeed theunderlying analogy is a powerful one – the overallcreation of value in a business environment beingsimilar to the inter-joined links in a chain – eachlink interdependent on the other for the strength of the chain as a whole, but each a distinct stage in itsown right. The strength of the chain is dependenton the strength of each of the links. If one breaksthen the chain as a whole collapses. This makescommonsense. If an oil renery stops production,the value chain linking an oil well to a car’s fueltank breaks down.

Conversely, improving the strength orperformance of one link may well improve theperformance of the whole chain. Simplisticallythen, managers should be asking themselves:. What does my link do?. Where does it t in the overall chain?. Can I improve the strength of my link and to

what effect?. How do I interact with other links and how

does the chain work as whole?

Traditionally, this might have lead to pursuingvertical integration strategies – shortening thechain and owning all the links – the twentieth-century oil companies being classic examples(Drucker, 2001).

The traditional view has been that at the end of the chain is the customer and that the better thechain is at servicing this customer the more valuewill be created. At its simplest then,understanding what each link does and how wellit lls its role in the chain provides a vehicle forunderstanding each process or link, its strengthsand weaknesses and how the chain might best berecast to maximise competitive positioning andtherefore value.

This view of the value chain, however, has itslimitations. To assume that the chain itself is a neatset of synchronous links is too simplistic. Thebusiness world is not that static and there is in factwhat Hagel and Singer (1999) refer to as aconstant “bundling and bundling” of processesand links so that a static view of a simple, stablechain needs to accommodate a more dynamicmodel.

Indeed, it seems that the development of value-chain thinking and value-chain management hasnot realised its full potential. One of the principalreasons is terminology. Some quite simple butpowerful ideas have become lost and confused in

Journal of Consumer MarketingVolume 21 · Number 7 · 2004 · pp. 465-475q Emerald Group Publishing Limited · ISSN 0736-3761DOI 10.1108/07363760410568680

465

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 2/11

the absence of some agreed denitions of basicconcepts. Even a cursory review of the literatureshows the words “value chains” used in variouscontexts to mean quite different things – from asimple substitute for “supply chain”, to adescription of work processes to a strategic marketframework

Strategies and business models: a macroand a micro view

Magretta (2002) illustrates very well thedistinction between a rms business model – whatthe rm does and how it does it – and its strategies – where it positions itself in the marketplace. Usingthe example of Wal-Mart, she points out that theunderlying business model of that company is thatof a supermarket, which it has done very well,

pioneering many supply-chain efciencies. On theother hand, what distinguished Wal-Mart, at leastin its early years, was its strategy of putting itsstores in regional areas in the USA rather than inthe large towns and cities.

In this sense the notion of value chains operatesat two levels. The rst is the strategic level, wherevalue-chain analysis is a means of charting where arm sits in the market and how it should positionitself. This is what might be termed the “macroview”. This macro view is a means of analysingwhat key industry drivers are and where the rmsits. It is a perspective that is driven by theoverarching notions of creating “customer value”.Traditionally, this has been driven by strategicpositioning in the marketplace, exploiting what hasbeen termed “prot pools” in various industries(Gadiesh and Gilbert, 1998).

These “prot pools”, however, shift. The classicexample is the automotive industry where marginsare no longer driven solely by making the car, butselling it, and more importantly nancing that sale.Additional “prot pools” have been added such ascar rentals and in some instances recoveryinsurance.

These shifts are illustrative of what has beentermed the emergence of the “new economy”. Insome ways this is an unfortunate term, withovertones of dot.com excess. In its broadest sense,however, the new economy is about a series of changes to the economic landscape, drivenpartially by technology, but also by differentexpectations of the market participants. One of theconsequences of this “new economy” is that valueis no longer necessarily created by simply owningas many of the links in the value chain as possible – the traditional strategy of vertical integration.Instead what has been termed “virtual” integrationassumes a new importance. It is argued that it is no

longer an imperative to necessarily own the meansthe production, but instead simply to have accessto them in an effective manner (Normann, 2001;Hagel, 2002). Indeed the less resources the rmhas tied up, the less capital intensive it is, the morelikely it is to achieve adequate returns on thoseassets. Firms then are increasingly specialising intheir competencies and forming alliances ornetworks or clusters to ll in the other parts of thevalue chain and amplify their own contribution. Atits simplest this is seen in successful using of outsourcing of manufacture by Nike, Dell andothers.

The second “micro” level perspective of thevalue chain is the aggregate of actual processes thatare occurring within the rm itself. This iscommonly labelled “operational management”,but should not be limited to just thinking aboutsupply chains and logistics. Operationsmanagement in the true sense encompasses all

those processes that a rm undertakes – frommanaging its people, to building its products andservices, to selling those products. The outcome of operational management should be theachievement of the rm’s dened value objectives.This is fundamentally a process-driven view of therm.

It is suggested that the real potential strength of value-chain analysis lies not just in understandingthe micro and macro issues better, which ithopefully does, but in understanding thesynthesis of the two. Strategic marketopportunities are useless in the absence of

operational processes to capitalise on them.Conversely, excellent operations do not producevalue if they are not attuned to the market bymaximising customer value. The true creation of value in its broadest sense comes from havingboth halves of the equation working effectivelyand in unison.

This paper, however, focuses on just one part of that equation – the “micro” perspective, and seeksto illustrate how the adoption of a process-driven“chain” approach has raised questions about thetraditional role and function of marketing in therm.

The supply-chain manager as the newcorporate hero

The notion of the supply-chain manager as thenew corporate hero, championing reduced costs,improving efciencies and rewarding customerswith reduced prices, seems somewhat incongruousto those brought up on the notion that marketingwas the dominant corporate philosophy. Indeed atleast one generation of business students and

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

466

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 3/11

practitioners were taught that it was marketing thatwas responsible for inculcating customer valuesinto the organisation and that this was the ultimatemeans of fostering competitive advantage. Even acursory glance at today’s nancial pages, however,suggests that instead it is rms that consistentlyand persistently manage their cost structures thatare seen as the over-achievers

A number of potential dangers arise from thisnew supply-chain dominance of corporatethinking. Not the least is that supply-chainefciency is mistaken for effectiveness, with undueshort-term emphasis on cost reduction at theexpense of contribution to broader gaols. Inparticular, customer needs may ultimately be seenin simplistic terms revolving simply aroundreduced price as a major determinant of satisfaction.

This may, at least partially, reect a failure bymarketing as a discipline to provide the coherence

to corporate organisation, operations andobjectives that its proponents have claimed. Inresponse this paper proposes a broaderperspective, based on the notion of the demandchain, which encompasses a more holistic view of all of those processes in the rm that do, or should,respond to the customer.

Supply chains: too much emphasis onefciency?

The notion that organisations have supply chainsthat require active management to maximiseefciency is well recognised. Indeed from beingan unfashionable backwater of managementtheory and practice, supply-chain managementhas asserted considerable inuence onoperational and strategic thinking. Its inuence inretailing is a good example of how the supply-chain manager has become the new dominantforce in driving corporate efciencies andprotability.

Waller (1998) discusses “customer-driven”logistics as an increasingly accepted concept; “ . . .as businesses begin to understand that their futureexistence depends upon the loyalty of the end usersof their products”. In particular, he noted that“For retailers, it has been their focus on the supplychain back into suppliers that has provided themechanism for value-chain visibility and control asa formula for generating effective end-deliveredcost and consumer satisfaction”. He cites Marks &Spencer in the UK as having “long been regardedas leaders in this”.

Similarly, in Australia, two dominant retailinggroups, Woolworths and Coles have made “everyday low prices” their primary offer to customers,

an offer driven by and rooted in supply-chainefciency strategies. Woolworths “project refresh”supply-chain-driven strategy has markedlyincreased the return on sale ratio. Cumulative costsavings has resulted in excess of A$1 billion over aperiod of four years. This has seen the companydominate its sector and produce consistentincrease in shareholder value, at least in terms of share price. It is interesting that the company hasreinvested much of this surplus in lower sellingprices (Moullakis, 2003). This reects the notionthat an effective supply chain will ensure adequatecustomer satisfaction through reducing costs andtherefore prices.

It is suggested, however, that a downstream-orientated supply-chain strategy focused on costreduction only, has a number of inherentlimitations. The rst is that in oligopolistic orsemi-oligopolistic environments like theAustralian and UK supermarkets, the supply-chain systems and relationships, are often farfrom two-way, mutual agreements. The rationaleis based on increased volumes creating leverageover suppliers resulting in increased procurementmargins, lower prices at the point of sale andultimately dominant market share driving greaterprotability for the retailer. Many of the smallerspecialist chains are being absorbed in the rush toacquire outlets and the result is a merging of market segments.

This has had a signicant effect has been on thesupply-chain “partners”. Though poormanagement responses have no doubt played apart, the volume-driven strategy of the majorretailers has had a signicant impact on bothsmall suppliers who are at risk of beingmarginalised, and on the larger companies aswell. For example the largest Australian wineproducer, Southcorp, found that within 12months supermarket sales had risen from 29 percent to 42 per cent of its business with asignicant decline in protability

In Australia both the major retailing groups(Woolworth and Coles) recently gave furtherdemonstrations of “retailer power” in alcohol andpetroleum retailing by acquiring independent

wine, spirits and beer operators and throughmarketing arrangements with major oilcompanies. In both product-markets there isconcern that the remaining independents willhave considerable difculties in competing asconsumer pricing deals dominate these markets.This lack of equity in supply-chain relationshipsmay ultimately invite government and legislativeresponses and this has recently been agged in theAustralian retail liquor market. Perhaps, moreimportantly, it may be inadvertently introducingan inherent fragility into the dominant partners

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

467

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 4/11

supply chain that may not be even in its own long-term interests. This is not only in terms of theviability and stability of its suppliers, but may leadto compromises in product quality and choicethat will reect on its own brand and marketpositioning.

The second and perhaps most importantlimitation of a purely mechanistic supply-chainapproach entirely driven by cost efciency is loss of customer focus. Indeed, the notion that aneffective supply chain alone will ensure adequatecustomer satisfaction through reducing costs andtherefore prices is not necessarily an adequatemodel by itself. Sainsbury (the UK formermarket leader in food retailing) noted in the late1990s in an annual report the positive impact onoverall protability of its increased logisticsproductivity and saw this as a key corporatestrategy. This reected a business modeldominated by a downstream oriented supplychain, assuming a relatively “steady state” amongstits customers. The problems that Marks &Spencer, and to a degree Sainsbury, experiencedduring the 1990s were not because theymismanaged the operational effectiveness of thebusiness, but rather because they missed the shiftin customer expectations and did not appear torespond to those expectations.

Towards an alternative model: theemergence of the demand chain as aconcept

As a discipline supply-chain management rstappeared in the literature in the mid-1980s, but asCooper et al. (1997) suggest, it is based uponfundamental assumptions emanating frommanaging organisational operations, which in turncan be traced back to channels and systemsintegration research in the 1960s and morerecently work on information management andinventory control. Supply-chain management wasdened by members of The International Centrefor Competitive Excellence (1994, cited in Cooper

et al. , 1997) as:Supply-chain management is the integration of business processes from end-user through originalsuppliers that provide products, services andinformation and add value for customers.

Important from the point of view of this discussionis the direction in which supply-chain planningand coordination is seen to “travel”. Initially thecommon view held was that it simply covered theow of goods from supplier throughmanufacturing and distribution to the end user(Keith and Webber, 1982, cited in Christopher,

1992). This was followed by a series of stepsseeking to somehow incorporate the customer intothe model.

Christopher (1998) for example adds aninteresting dimension to the supply-chainperspective noting that:

It could be argued that it [supply-chainmanagement] should be termed “demand-chainmanagement” to reect the fact that the chainshould be driven by the market, not by suppliers.Equally the word “chain” should be replaced by“network” since there will normally be multiplesuppliers and, indeed, suppliers to suppliers as wellas multiple customers and customers’ customers tobe included in the total system.

Langabeer and Rose (2001) take the argument astep further by looking at the demand chain as anentity in its own right making an interestingdifferentiation between the supply chain and thedemand chain and between demand managementand demand-chain management. They dene thedemand chain as:

The complex web of business processes andactivities that help rms understand, manage, andultimately create consumer demand.

They emphasise the point that demand-chainmanagement attempts to analyse and understandoverall demand for markets within the rm’scurrent and potential product range. Supplychains, by contrast emphasise the efciencies inthe production and logistics processes, while thedemand chain emphasises effectiveness in thebusiness. A very useful point in their argument isthat demand-chain analysis and managementhelps to improve an organisation’s processes byaligning the organisation around a common plan,improves coordination within the supply chain byusing forecasts and plans, and exploits thecommercial processes by understanding consumerdemand and by selecting those markets that bestmeet an organisations, owned and/or “leased”,skills and resources.

This introduces the notion that an effectiveapproach to demand-chain management rstrequires the organisation to understand its currentand potential markets and second to identify theessential (or core) processes and capabilities thatare required for success. They offer a usefulcomparison of the two approaches:(1) Supply chain:

. efciency focus (cost per item);

. processes are focused on execution;

. cost is the key driver;

. short term oriented, within the immediateand controllable future;

. typically the domain of tacticalmanufacturing and logistics personnel;

. focuses on immediate resource andcapacity constraints; and

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

468

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 5/11

. historical focus on manufacturing planningand controls.

(2) Demand chain:. effectiveness focus; product-market t;. processes are focused more on planning;. revenue is the key driver;. long-term oriented, within the next

planning cycles;. typically, the domain of marketing, sales

and strategic supply-chain managers;. focuses on long term capabilities, not short

term constraints; and. historical focus on marketing and supply-

chain alignment (Langabeer and Rose,2001).

The authors go on to propose a demand strategycomprising a supply-chain strategy (focusing onmanufacturing, distribution and networkoptimisation), customer strategy (customers andmarkets), a product and brand strategy (focusingon key product requirements and customisationneeds), and a sales and marketing strategy(creating awareness and demand). They suggestthat these, when coordinated, create a demandstrategy that may be expressed as:

The direction that a rm pursues to attract andretain desirable customers and improve its productpositioning in protable markets.

They expand the argument with a modeldescribing demand-chain management in somedetail as a:

Focus on creating demand strategy (what isoptimal for each product-market?) and manage theentire organisation to meet this demand.

This model, however, remains essentially amarketing-driven one that is emphasising customerrelationship management and ensuring that thesupply chain reects this concern. In this sense itretains a predominant place for demand strategythat inuences and by inference guides the supply-chain activities. As will be argued below grafting thesupply chain onto a dominant demand perspective,or in contrast seeking to somehow introduce thecustomer into the supply chain, both fail toaccommodate what are two quite distinct and basiccomponents of the rms overall value chain.

Despite this, the identication of the demandchain as a separate entity is a signicantcontribution to the debate and to ourunderstanding of this area.

The demand chain as a distinct entity

How then should we view this broader notion of the demand chain? Possibly a rst step is to

reinforce that both supply-chain managementand demand-chain management are aboutprocess management. Hammer (2001) arguesthat as businesses become accustomed to thecustomer economy ‘process thinking’ becomesessential:

In order to achieve the performance levels thatcustomers now demand, businesses must organiseand manage themselves around the axis of process;moreover, they must apply the discipline of processeven to the most creative and heretofore mostchaotic aspects of their operations.

Just as the industry level macro value chain isdynamic, so too is its replicant within the rm.Different processes do not necessarily work intandem and may often conict. Production doesnot always produce what sales wants to sell andR&D does not always formulate what marketingsays the customer wants.

Interestingly, Butler et al. (1997) note what

they call “interaction costs”, namely “the moneyand time that are expended whenever people andcompanies exchange goods, services and ideas . . .In a very real sense, interaction costs are thefriction in the economy”. This same notion canbe applied at the micro level of the rm. A rm’svalue chain is not a smooth synchronous link – its has its own friction and its own interactioncosts.

Hagel and Singer’s (1999) description then of “unbundling and rebundling” of organisationalstructures as a means to adapt to new marketdemands is a useful one. It is suggested that in factthere is, or at least should be, a constantrealignment of core processes going on within anyrm on a day-to-day basis as it interacts with itsenvironment. Such constant realignments shouldnot be seen as a sign of instability or as a negativeforce, but rather the ability to manage them pro-actively optimises the ability to create value,particularly the more dynamic the rmsenvironment.

The second step is to re-validate the notion of the demand chain as a separate entity from thesupply chain. It is not an adjunct to the supplychain, nor is it simply another re-statement of themarketing concept. Marketing is a philosophy,stressing the customer centric goals of anorganisation. The demand chain is a practicaldescription and analysis encompassing all thoseprocesses within the rm that adopt and apply thatphilosophy. In this sense the demand chain shouldnot be seen as the sole domain of the rmsmarketing department. It should be thought of ascross-disciplinary, encompassing all thoseprocesses which contribute to orientating the rmsactivities to the needs and requirements of thecustomers. This potentially incorporates a range of processes like production planning that would not

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

469

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 6/11

be traditionally associated with direct customerinterface

The third step is a recognition that thesenotions of demand and supply while distinct alsooverlap and interact and should be seen asconstituent, but independent elements of what hasbeen termed the rm’s value chain. It is also worthnoting that having both competent and workablesupply and demand chains are competitivenecessities. The best factory in the world is uselessif it is producing the wrong product. The bestinnovation is worthless if it cannot beimplemented. Competitive advantage can,however, be spawned by excellence in eithersupply-chain processes or demand-chain activities,or of course preferably both.

In more simple terms a rm will create valuewhen what the customer demands can be broughtinto synchronisation with what the rm cansupply, minimising friction and internalinteraction costs and maximising the dynamicforces of the interaction. Where they are notsynchronised, value will either not be realised oractually destroyed. This may sound simple, but thereality of complex organisations is such that thisprocess fusion is in fact problematic and representsthe key tactical task for management on a day-to-day basis.

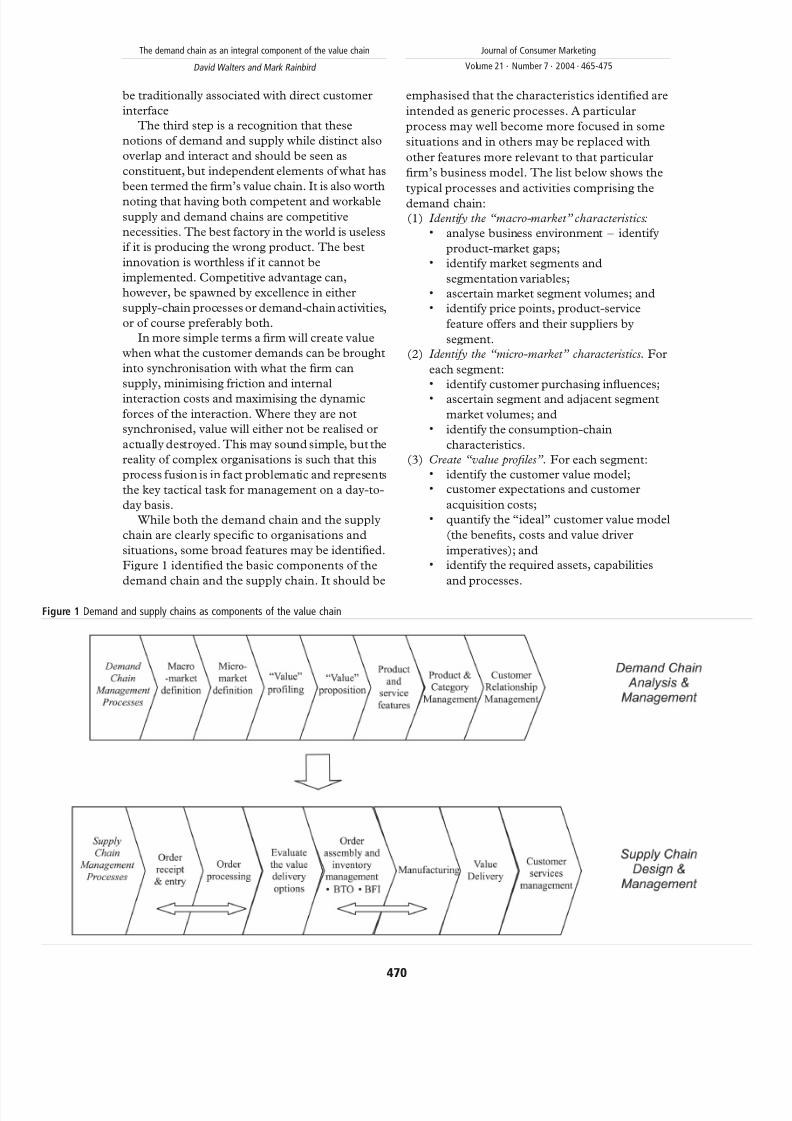

While both the demand chain and the supplychain are clearly specic to organisations andsituations, some broad features may be identied.Figure 1 identied the basic components of thedemand chain and the supply chain. It should be

emphasised that the characteristics identied areintended as generic processes. A particularprocess may well become more focused in somesituations and in others may be replaced withother features more relevant to that particularrm’s business model. The list below shows thetypical processes and activities comprising thedemand chain:(1) Identify the “macro-market” characteristics:

. analyse business environment – identifyproduct-market gaps;

. identify market segments andsegmentation variables;

. ascertain market segment volumes; and

. identify price points, product-servicefeature offers and their suppliers bysegment.

(2) Identify the “micro-market” characteristics. Foreach segment:. identify customer purchasing inuences;. ascertain segment and adjacent segment

market volumes; and. identify the consumption-chain

characteristics.(3) Create “value proles”. For each segment:

. identify the customer value model;

. customer expectations and customeracquisition costs;

. quantify the “ideal” customer value model(the benets, costs and value driverimperatives); and

. identify the required assets, capabilitiesand processes.

Figure 1 Demand and supply chains as components of the value chain

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

470

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 7/11

(4) Establish alternative value propositions. Reviewthe customer value models, identifying:. customer expectations;. relative competitive positioning: product-

service comparisons (range, quality,services, price, etc.);

. relative costs; and

. the role that can be played by partner/complementor organizations (within oroutwith the demand and/or supply chain).

(5) Develop product-service options:. determine the unique/exclusive value

drivers that are important to targetcustomers;

. forecast the potential revenues;

. cost the options;

. establish cost structures and the asset“ownership” and funding implications;

. identify the risk/return proles;

. project the long-term economic free cash

ows; and. estimate the potential for sustainable

competitive advantage of the productservice options.

(6) Evaluate the value delivery options. Identify theoptimal value-chain structure:. the role that can be played by partner/

complementor organisations;. compare the “returns” to shareholders and

stakeholders as well as to end-usercustomers;

. consider the implications of alternatives forasset, capability and process leverage; and

. consider the implications of these on theeffectiveness and efciency of the controlof the value delivery process.

(7) Product and category management. A review of the product range to determine current andfuture product and category proles:. revenues, costs, contribution and cash

ow;. share of market, share of market value;. competitor analysis on like for like basis

(markets, segments, customers);. gap analysis; and. investment requirements; risks, cash ow

forecast.(8) “Service” the value: customer relationship

management. Service support levels andinfrastructure comprising:. service intermediaries, roles, tasks and

location;. technical support, installation, operation

and maintenance;. presale liaison;. information and advice;. design services;. transactions systems;. ordering systems;

. payment options;

. nancing;

. post-transactions services;

. maintenance;

. installation;

. training;

. operations;

. warranty operations;

. product/service liability commitments;

. product-recall programmes; and

. customer loyalty programmes.

The following list the typical processes andactivities comprising the supply chain:(1) Order receipt and entry:

. order acknowledgement;

. credit checks;

. inventory availability;

. manufacturing instructions; and

. price and discount extensions.(2) Order processing:

. order administration (generate invoice,generate picking documents, schedulinginformation);

. determine and report order status;

. create distribution documentation; and

. manage order location communications.(3) Evaluate the value delivery options:

. identify the optimal value-chain structure;

. compare the “returns” to shareholders andstakeholders as well as to end-user customers;

. consider the implications of alternatives forasset, capability and process leverage; and

. consider the implications of these on theeffectiveness and efciency of the controlof the value delivery process.

(4) Order assembly:. liaison with manufacturing;. order picking;. packing; and. unitisation.

(5) Inventory management:. replenishment policies based upon

demand forecasts and collaborativeagreements;

. cycle stock and safety stock responsepolicies by customer segments and productcategories;

. key customer response policies; and

. product liability/return procedures.(6) Manufacturing:

. process selection;

. capacity management;

. materials requirement planning andmanagement;

. quality control;

. cost management; and

. supplier/partner liaison.

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

471

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 8/11

(7) Order transportation. Order deliverymanagement that meets customers’ serviceexpectations. Selection of:. mode;. frequency; and. reliability.

(8) Customer services management. Themanagement of; time, dependability,communications and convenience byproviding:. product availability;. agreed OCT;. exibility; and. relevant and timely information.

This notion of the demand chain suggests thatmarketing in its narrowest sense loses a lot of itsrelevance and just as the old logistics manager hasreinvented himself as the new supply-chaincorporate hero, so perhaps the marketing managerneeds to take a broader perspective of the rm as awhole and reinvent himself as the demand-chainmanager.

An example: McDonald’s Corporation

Leaving to one side whatever views one may haveon the merits of its products, the growth of McDonald’s Corporation over the last fourdecades from a hamburger stand to a majorinternational corporation has been impressive.

However, McDonald’s in 2003 reported aquarterly loss amidst wide-scale discontentamongst franchisees and a plunging share price atten year lows. What went wrong?

In many respects McDonald’s was one of thepioneers of both efcient and effective supply-chain management and of marrying these withtraditional marketing techniques, fostering a wholenew category of food retailing. McDonald’sdelivered new levels of product consistencythrough standardised menus and strict suppliercontrols. It maximised the impact of its deliverypoints by developing and applying demographicresearch to its store placement. It maximisedthroughput and asset and inventory utilisation byfocusing on speed of production and deliverythrough new standards of staff training and processcontrol. It deployed economies of scale andbargaining power to deliver affordable products.By fostering the concept of franchisingMcDonald’s in effect not only outsourced theactual production and delivery of its products, butalso outsourced operational risk by putting theonus to raise and manage working capital on thefranchisee. These were not the innovations of acompany in the new millennium, but of the 1970s

and 1980s. In this sense McDonald’s was abusiness orchestrator (Hagel, 2002), long beforethat term was coined.

Despite the historical excellence of its supplychain, it would be misleading to see McDonald’s asa purely supply-driven operation. Again from anhistorical perspective, the company has excelled inimplementing classical marketing techniques,particularly the “5P’s”. McDonald’s introducednew standards of training and emphasis on its“people” exemplied by the now ubiquitous “frieswith that, sir?”. “Price” has been a consistenttheme, with the affordability of convenience foodincreasing markedly over the last few decades.“Place” has been reected both at the level of individual store placement and at a broader level ina still expanding campaign to open more stores inmore locations in more countries. Indeed, thecompany seems to measure its own performanceby this as much as anything else. “Promotion” has

seen the golden arches, Ronald McDonald and amyriad successful advertising and point-of-salecampaigns successfully targeting various marketsegments, including, in particular, children whereagain it was a pioneer, albeit it has been criticisedfor doing so. Finally, McDonald’s traditional“product” set, including the ubiquitous Big Mac,set new standards for consistency and reliability.Perhaps most importantly this was not just the “5P’s” geared up into a marketing programme, butan effective demand chain that formed an integralpart of the rms overall business model or valuechain.

Overall this was a stunningly successful modelwhere the process fusion between the demands of the emerging fast food market were skilfullycombined with new value-chain capabilities to theextent it is arguable whether McDonald’s createdfast food or the other way around.

In the face, however, of falling prots andinvestor wariness, these were strategies and themesthat seemed to be failing the company. In early2003 a company presentation was described asfollows:

The top team’s wooden presentation on April 7th(2003), liberally doused with marketing cliches andsoundbites about the importance of “people,product, place, price, promotion” and “improvingfocus” only reinforced the impression . . . [thatmanagement] lacks the vision or stomach to makethe necessary changes ( The Economist , 2003).

The reality appears to be that the nature of themarket, or the “macro” value chain McDonald’s isoperating in is changing, at least in its more maturegeographic segments. For example in Australia aBIS Shrapnel (2003) study suggests the averageAustralian is eating out less often, 83 times in 2002compared with 94 occasions in the year 2000.Furthermore, the reasons have changed: “Whereas

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

472

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 9/11

‘convenience’ was the main determinant threeyears ago, the principal reasons now are ‘specialoccasion’, ‘break in routine’ and ‘meeting friends’.The report also identies changing tastes;consumption of hamburgers is down,consumption of takeaway Thai, Sushi, and Indianfoods are increasing, awareness of “healthy eating”clearly growing.

McDonald’s appeared to be aware of this.Comments by Peter Bush (a senior executive) andreported by Shoebridge (2003) suggest that thecompany was at least partially aware of itsproblems:

Our rivals are not just other fast food chains; theyare any other informal eating-out occasion. Forexample, about 6,500 new coffee shops haveopened over the past four years, all competing for ashare of the money people spend on eating awayfrom home.

The real opportunity for McDonald’s is todevelop compelling reasons for people to visit us

more often . . . That means having more relevantmenu variety, and offering menu solutions ratherthan promotional products. There are lots of promotional products on the menu at themoment, but they need to be underpinned bychanges to the core offering. [McDonald’s isseeking to become] more relevant tocontemporary consumer values.

In this changing environment, Bush also indicatedthe rigidity of the McDonald’s operating andsupply-chain systems is not longer a competitiveadvantage but a limiting factor in its response. It isadmitted that the new menu activity “placedstrains on McDonald’s purchasing department,operating systems and restaurant staff”.McDonald’s appeared to be a good example of thelimitations of simply pursuing supply-chainefciency and what might be termed classicalmarketing exploitation techniques in a rapidlychanging environment. In effect, McDonald’s wasresponding to new pressures with a traditionalresponse – lower the price and use cost efcienciesto wear out the competition. This was exempliedby the “dollar deal” campaign apparently targetedat Burger King.

This led some commentators in nancialmarkets to question the on-going viability of thecompany’s business model, calling on it to“manage for cash” rather than growth, liquidatesome of its vast real estate holdings and return thatcash by way of higher dividends. In effect they werecasting doubt on the efcacy of McDonald’s valuechain and the business model supporting it as thefundamental alignment between whatMcDonald’s produces (its supply chain) and whatthe customer wants (its demand chain) seemed tohave faltered.

Clearly disturbed by both the poor results andthe press response McDonald’s reacted. The then

CEO, Jim Cantalupo issued “McDonald’srevitalization plan” (McDonald’s web siteOctober 29, 2003). Since then there has been asteady rise in the company’s protability andshare price, though the later may simply reectwhat McDonald’s calls “Manage for nancialstrength” and which seems a direct reaction tocalls for changes in capital management by“reducing capital spending compared with 2002and using the money remaining after capitalexpenditures to pay down debt and return cash toshareholders”.

The revitalisation plan was still clearlydesigned around the traditional marketingmix of the “5Ps”; people, products, place, priceand promotion, or what Cantalupo announcingthe rst quarters results in 2004 called “thewinning combination of improved service,better tasting and more relevant food, affordablemenu options and extended hours of service”.This has even been followed up with a “acomprehensive balanced lifestyles platformto help address obesity in America andimprove the nation’s overall physicalwell-being”.

If this revitalisation plan were nothing morethan a marketing re-launch one would have toquestion its sustainability in the face of the sort of changes to the “macro” value chain in whichMcDonald’s operates as noted above. There is,however, some evidence of a more fundamentalre-examination of McDonald’s whole demandchain. For example in launching the revitalisationplan it was noted that:

On a broader level we are in the early stages of taking a global, cross functional approach tomenu management. We are creating menumanagement centres around the world that willuse a consistent consumer-driven process todevelop world-class products that leverage oursize and scale.

And, to add emphasis, the company’s new strategiccourse is:

. . .reecting a fundamental change in our approachto growing the business. Previously we emphasizedadding new restaurants. Today, our emphasis is onbuilding sales at existing restaurants.

This too suggests an awareness of the benets of rst understanding the demand chain and thendesigning the supply chain. Indeed it is a clearmove away from the pursuit of economies of scale towards the economies of scope andintegration.

It is too early to tell whether there is a truere-evaluation and realignment of McDonald’sdemand chain and therefore its value chain as awhole, but it provides an illuminating example of the issues.

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

473

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 10/11

Concluding comment

The demand chain then is:An understanding of current and future customerexpectations, market characteristics, and of theavailable response alternatives to meet thesethrough the deployment of operational processes.

In this paper we have suggested and identiedexamples of an emerging qualication forcompetitive advantage – pro-actively managingboth the demand- and supply-chain processes tominimise friction and internal transaction coststhereby enhancing overall value. Where, however,does this t with the rm’s overall strategy?

As noted above, Magretta (2002) makes avaluable distinction between a rm’s businessmodel and its strategy, citing the example of Wal-

Mart who initially adopted a fairly standardsupermarket business model, but prospered byadopting a strategy of building its supermarketsoutside metropolitan areas in rural locations. Thetwo notions of business model and strategy are,however, clearly linked. As Magretta acknowledgesWal-Mart only made their strategy work byimproving on the base business model “throughinnovative practices in areas such as purchasing,logistics and information management”.

It is suggested that constant renement of business models is as important to the success of

the rm as its strategy and that both are critical tothe integrity of the rms overall value chain. Thisimplies a far more important role for operationsmanagement than may have been traditionallyrecognised, and that in this new context themarketing professional needs to very muchconsider himself an “operational manager”. Wesuggest that an important topic for researchconcerns the implementation of the value-chainmodel and its implications for operationsmanagement in the emerging new businessmodels. In Figure 2 we suggest a starting point.The demand-chain and supply-chain processeshave been identied and fused into a value-chain-process model. There are a number of issues thatneed to be researched. These vary from quitesimple issues concerning structure andcommunication through to the more complexissues relating to intra and inter-relationshipmanagement structures and performance planningand control.

References

BIS Shrapnel (2003),Changing Patterns in Australian Consumption , BIS Shrapnel, Sydney.

Butler, P., Hall, T.W., Hanna, A.M., Mendoca, L., Auguste, B.,Manyika, J. and Sahay, A. (1997), “A revolution ininteraction”, The McKinsey Quarterly , No. 1.

Figure 2 Designing and managing the value chain

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

474

8/8/2019 The Demand Chain as an Integral Component of the Value Chain

http://slidepdf.com/reader/full/the-demand-chain-as-an-integral-component-of-the-value-chain 11/11

Christopher, M. (1992),Logistics: The Strategic Issues , Chapmanand Hall, London.

Christopher, M. (1998),Logistics and Supply Chain Management , Financial Times/Prentice-Hall, London.

Cooper, M.C., Lambert, D.M. and Pugh, J.D. (1997), “Supplychain management: more than a new name for logistics”,The International Journal of Logistics Management ,Vol. 8 No. 1.

Drucker, P. (2001), “Will the corporation survive?”,The Economist , 1 November.

(The) Economist (2003), 12 April.Gadiesh, O. and Gilbert, J.L. (1998), “How to map your industry’s

prot pool”,Harvard Business Review , May/June.Hagel, J. III (2002), “Leveraged growth: expanding sales

withoput sacricing prots”,Harvard Business Review ,October.

Hagel, J. III and Singer, M. (1999), “Unbundling thecorporation”,Harvard Business Review , March/April.

Hammer, M. (2001),The Agenda , Crown Publishing Group,New York, NY.

Langabeer, J. and Rose, J. (2001),Creating Demand Driven Supply Chains , Chandos Publishing, Oxford.

Magretta, J. (2002), “Why business models matter”,Harvard Business Review , May.

Moullakis, J. (2003), “Woolworths leads the way on cuttingcosts”, The Australian Financial Review , 11 April.

Normann, R. (2001),Reframing Business , Wiley, Chichester.Porter, M. (1985),Competitive Strategy , The Free Press,

New York, NY.Shoebridge, N. (2003),Business Review Weekly , 7 March.Waller, A. (1998), “The globalisation of business: the role of

supply chain management”,Management Focus , No. 11.

The demand chain as an integral component of the value chain

David Walters and Mark Rainbird

Journal of Consumer Marketing

Volume 21 · Number 7 · 2004 · 465-475

475