Embed Size (px)

Citation preview

The Deficit Reduction Act of 2005:

Hope or Illusion for Increased LTCi Production?

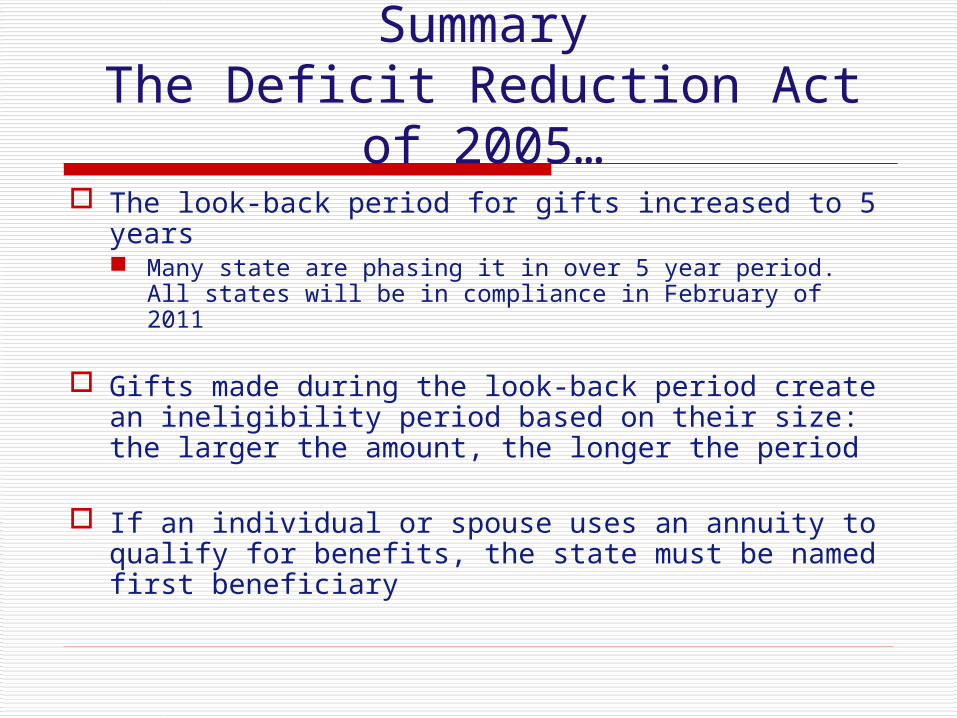

SummaryThe Deficit Reduction Act of 2005… The look-back period for gifts increased to 5 years

Many state are phasing it in over 5 year period. All states will be in compliance in February of 2011

Gifts made during the look-back period create an ineligibility period based on their size: the larger the amount, the longer the period

If an individual or spouse uses an annuity to qualify for benefits, the state must be named first beneficiary

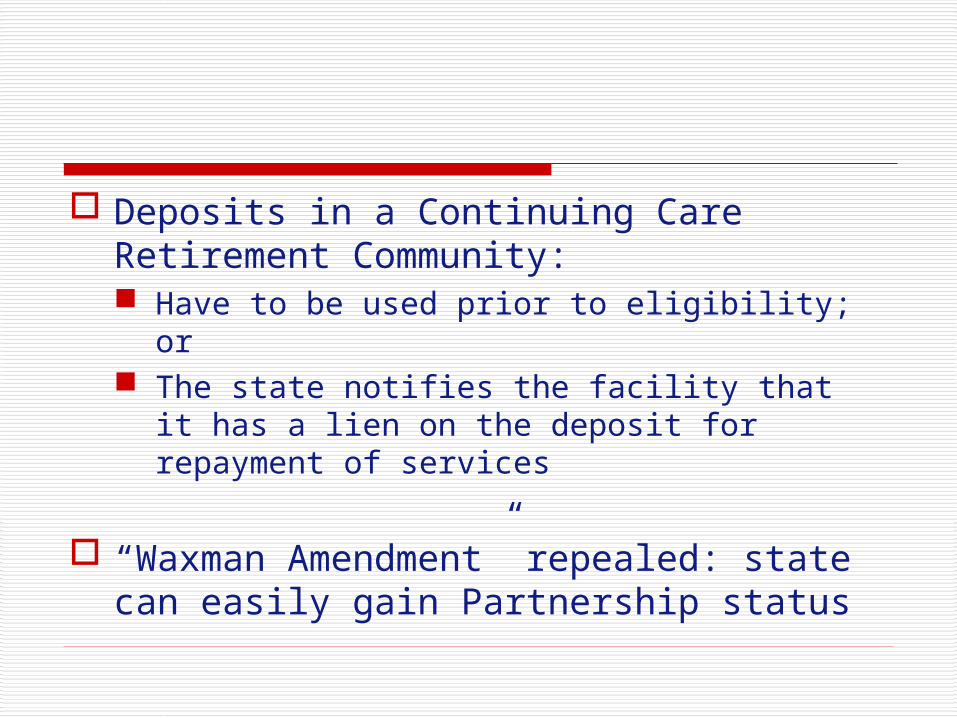

Deposits in a Continuing Care Retirement Community: Have to be used prior to eligibility; or The state notifies the facility that it has a lien

on the deposit for repayment of services

“Waxman Amendment” repealed: state can easily gain Partnership status

5 year look-back period

All states look for disqualifying transfers (gifts). Referred to as the look-back period, it begins on the date of application for Medicaid benefits

Gifts made during this time create a period of ineligibility, based on their amount.

The formula is: The amount divided by your states average monthly

cost of a private pay nursing home room

Example John enters a nursing home on December 25, 2008. He

applies for Medicaid on this date.

He tells Medicaid that he gifted $100,000 to his children on December 25, 2007

His state sets the average monthly cost of care at $5,000

The “penalty” (ineligibility for Medicaid benefits) is 20 months ($100,000 / $5,000)

When does the penalty begin?

For all gifts made after February 8, 2006 (the date president Bush signed the bill) the penalty begins on the date John applies for Medicaid, not the date he made the gift

Going back to the example…

John enters a nursing home on December 25, 2008. He applies for Medicaid on this date. He tells Medicaid that he gifted $100,000 to his children on December 25, 2007

His state sets the average monthly cost of care at $5,000. The “penalty” (ineligibility for Medicaid benefits) is 20 months ($100,000 / $5,000)

The penalty begins December 25, 2008. He must therefore, wait 20 months before Medicaid will start to pay for care

Will this encourage people to buy LTCi?

No, for at least two reasons…1. The majority of people who look to Medicaid

already have a pre-existing condition; they wouldn’t qualify for the policy to begin with

2. Telling a prospect, You know, you’ll have to wait 5 years after giving your money away to qualify for benefits, is also a waste of time. He likely will go back to the attorney who will tell him he can find a way around it

Medicaid now mandates the

state be added as beneficiary…

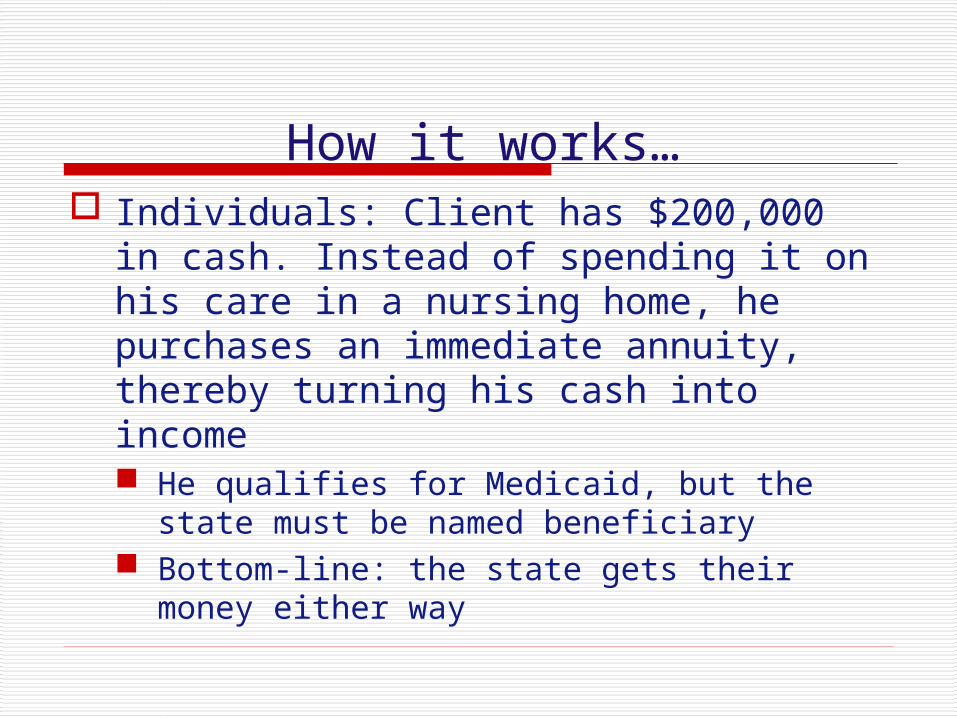

How it works… Individuals: Client has $200,000 in cash.

Instead of spending it on his care in a nursing home, he purchases an immediate annuity, thereby turning his cash into income He qualifies for Medicaid, but the state must be

named beneficiary Bottom-line: the state gets their money either

way

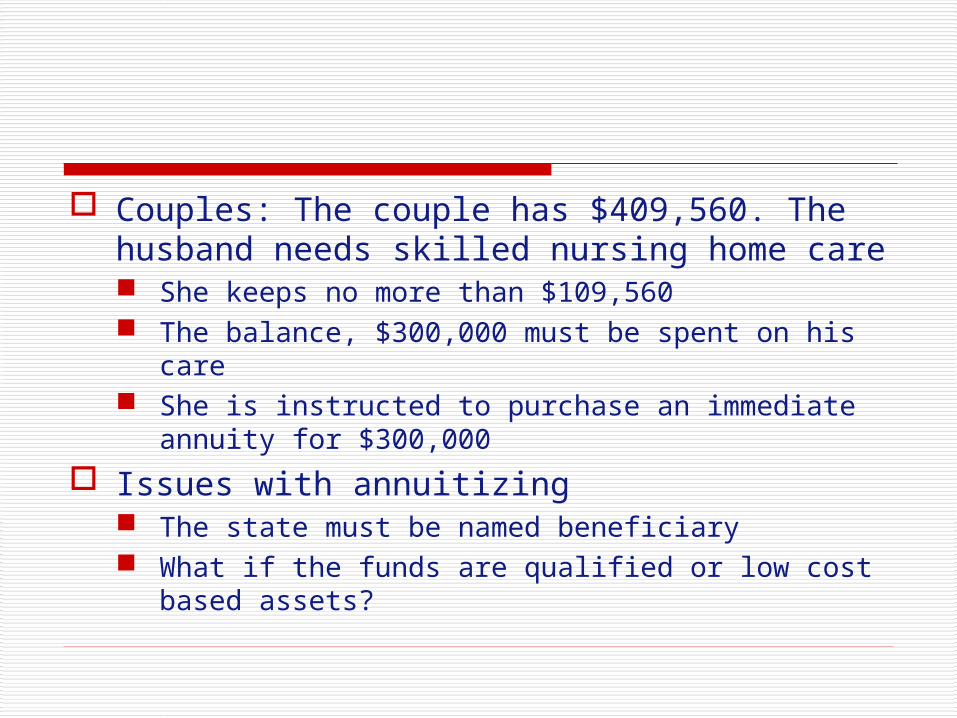

Couples: The couple has $409,560. The husband needs skilled nursing home care She keeps no more than $109,560 The balance, $300,000 must be spent on his care She is instructed to purchase an immediate annuity for

$300,000

Issues with annuitizing The state must be named beneficiary What if the funds are qualified or low cost based

assets?

Will this encourage people to buy LTCi?

No. Annuitizing almost always is used as a last resort.

If you try and explain that annuitizing won’t work, it’s likely the prospect will tell you…

That’s not what my attorney told me.

The meeting then becomes confrontational.

Lien’s and

Continuing Care Retirement Communities

The rule…

States are given the right to either Refuse eligibility if the applicant has a deposit

at a CCRC; or Qualify the individual, but send a notice to the

CCRC that the state has liened the deposit

Will this encourage people to buy LTCi?

Perhaps if the prospect / client is healthy. Once he understands that the deposit would end up going to Medicaid, not his family, there may be motivation to protect it.

Keep in mind that percentage wise, very few people end up in CCRC’s

Partnership

States are free to create partnerships and the majority have rushed to do so

The only formula will be dollar for dollar

Keep in mind that this is an asset, not income, protection program

Will this encourage people to buy LTCi?

It hasn’t in the past. Until recently, surveys conducted by AHIP and LTCi carriers, show that sales have barely moved.

Partnership has some issues: It does not protect income Many states mandate compound inflation into

70’s No state guarantees payment for home care,

adult day care, or assisted living

Suggestions on how to

use the Deficit Reduction Act

to your advantage

Don’t use it at all

The DRA only confuses the client. Remember Medicaid, not the DRA helps you sell LTCi It pays almost exclusively for SNF care. Client’s want to

stay at home Medicaid is not free. Think about taxes if assets are

gifted Once on Medicaid, the spouse in the community loses

most, if not all, of her husband’s income

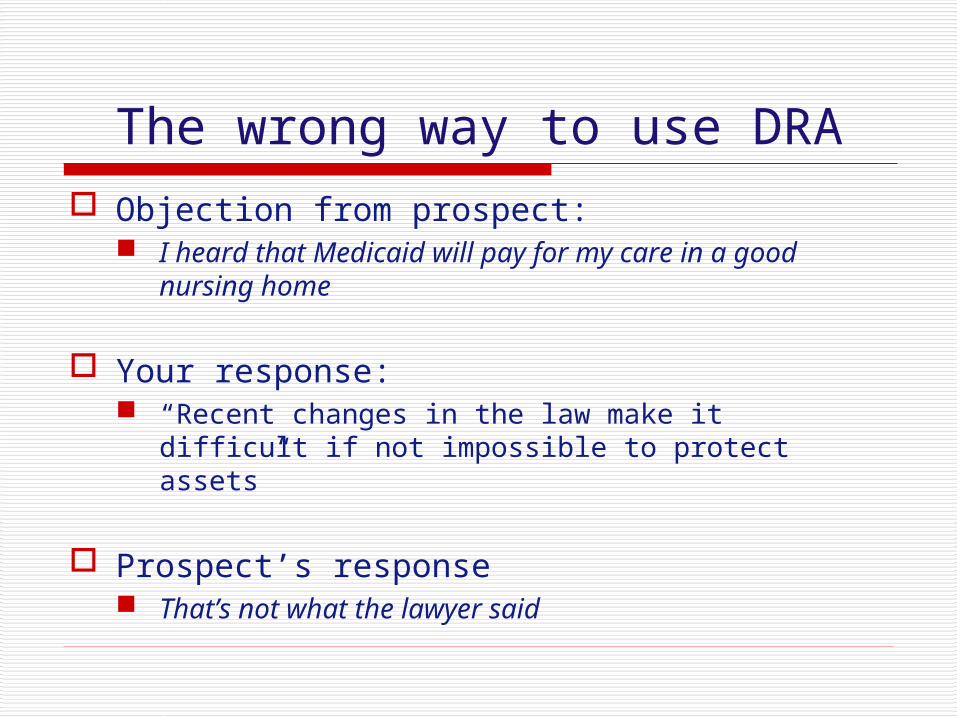

The wrong way to use DRA

Objection from prospect: I heard that Medicaid will pay for my care in a good

nursing home

Your response: “Recent changes in the law make it difficult if not

impossible to protect assets”

Prospect’s response That’s not what the lawyer said

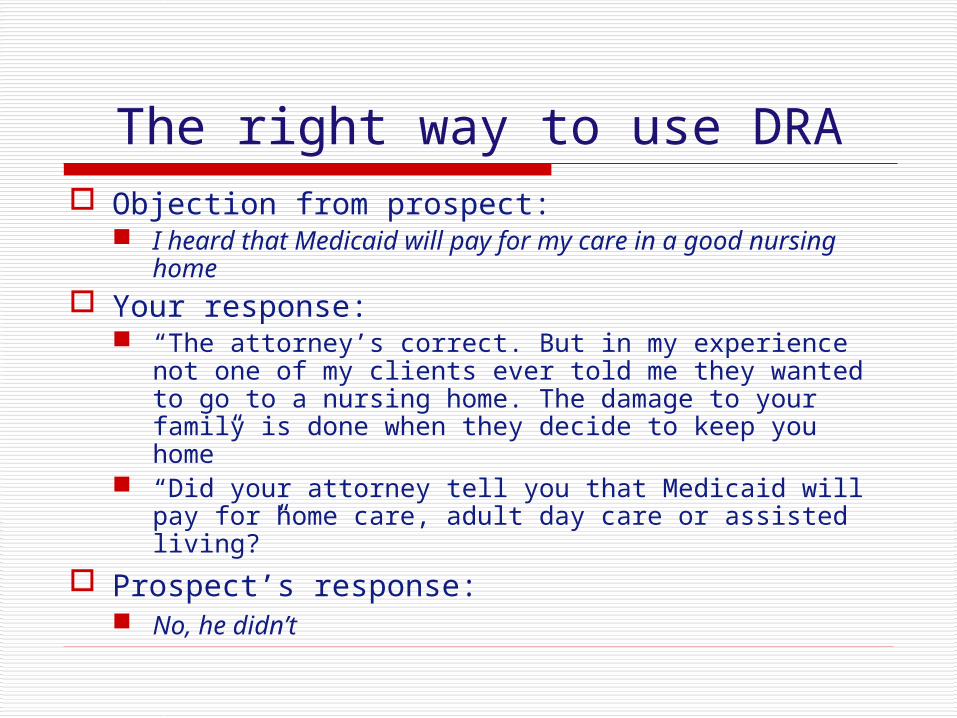

The right way to use DRA Objection from prospect:

I heard that Medicaid will pay for my care in a good nursing home

Your response: “The attorney’s correct. But in my experience not one of

my clients ever told me they wanted to go to a nursing home. The damage to your family is done when they decide to keep you home”

“Did your attorney tell you that Medicaid will pay for home care, adult day care or assisted living?”

Prospect’s response: No, he didn’t

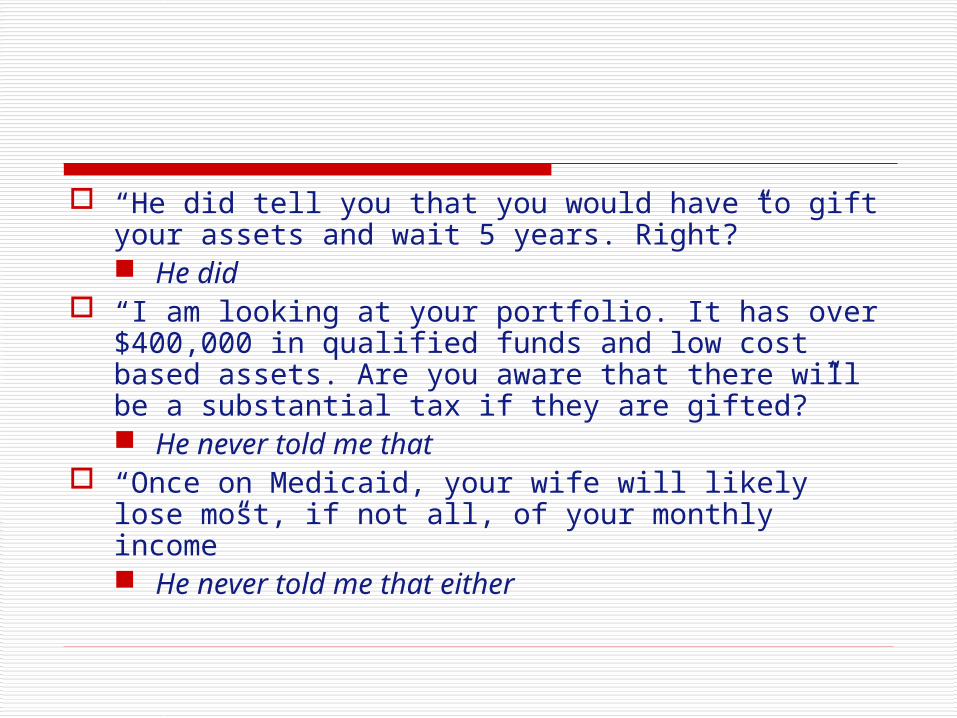

“He did tell you that you would have to gift your assets and wait 5 years. Right?” He did

“I am looking at your portfolio. It has over $400,000 in qualified funds and low cost based assets. Are you aware that there will be a substantial tax if they are gifted?” He never told me that

“Once on Medicaid, your wife will likely lose most, if not all, of your monthly income” He never told me that either

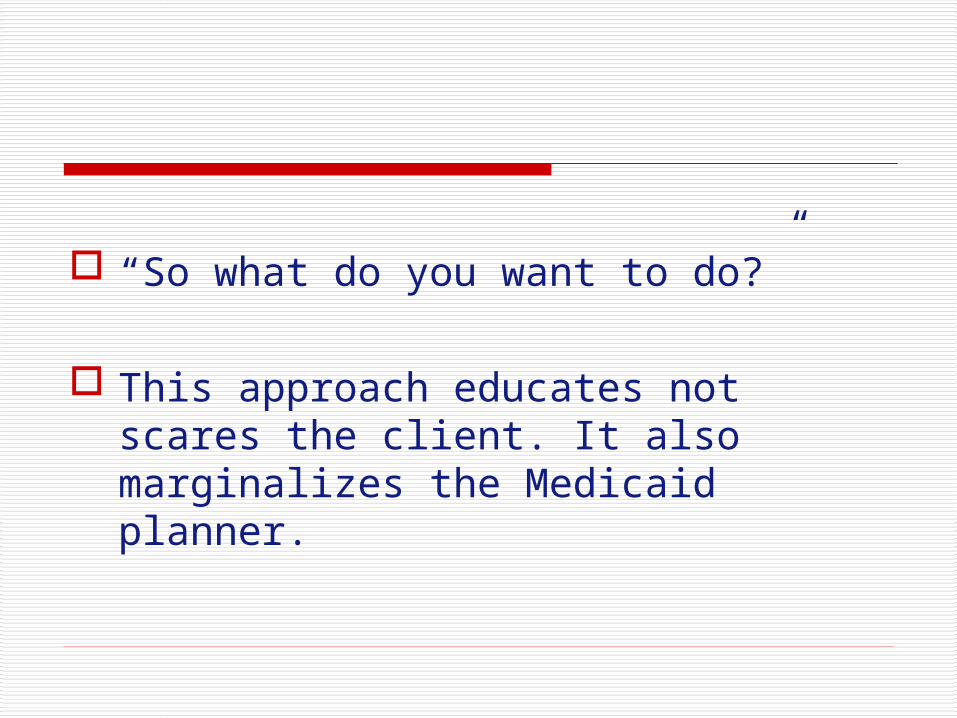

“So what do you want to do?”

This approach educates not scares the client. It also marginalizes the Medicaid planner.