Embed Size (px)

Citation preview

1

TheCreationofaNewMiddleClass?:AHistoricalandAnalyticPerspectiveonJobandWageGrowthintheDigitalSector,PartI

2

Dr.MichaelMandel

ProgressivePolicyInstitute

March2017

3

Introduction

InaJanuary2017report,“AHistoricalPerspectiveonTechJobGrowth,”we

exploredtheparallelsbetweenbigindustrialjobcreatorsoftheearly1900sand

today’stechleaders.WeshowedthatcompaniessuchasAmazon,Apple,Google,

Facebook,andMicrosoftarecreatingjobsatahistoricallyrapidpace.Amazon,in

particular,hasreached300,000jobsfasterthananyothercompanyinU.S.

history.1Moreover,thesecompaniesshownosignsofslowingtheiremployment

growth.AmazonpromisedinJanuary2017toadd100,000full-timeworkersinthe

U.S.overthenext18months.2Googleexpandeditsworkforcebyalmost17

percentin2016alone.

Inthispaper,weturnourattentiontotheimpactofthisjobgrowthonwagesand

livingstandards.Ourhistoricalbenchmark,onceagain,comesfromFord,General

Motors,GeneralElectric,DuPont,andothergreatindustrialcompaniesofthefirst

halfofthe20thcentury.Thesefirmswereabletoadoptnewproductionand

distributiontechniquesfasterandmoresuccessfullythantheirrivals.Asaresult,

these“frontierfirms”wereabletoaccomplishwhathadseemedimpossibleatthe

time:createhundredsofthousandsofjobswhilepayinggoodwagesandoffering

consumerslowerpricesthantheirrivals.

Thekeytothiswin-winsituationwasproductivity.High-productivityfirmswould

beabletocutprices,whichwouldexpanddemandandbenefitconsumers.

Expandeddemandwouldcreatemorejobsathigherpay.Theresultwasthe

creationofanewmiddleclassoffactoryworkerswhocouldaffordtobuythe

productstheymade.

4

Yet,today,skepticsworrythatdigital-enabledproductivitygainsarenotyielding

thesamevirtuouscircleastheproductivitygainsofthepast.3Theypointoutthat

digitalcompaniesdonotseemtobegeneratingenoughjobstomakeupforthe

slowgrowthofjobsintherestoftheeconomy.Indeed,thecurrentconcernisthat

digitaldisruptionwilleliminatemillionsoftraditionaljobsinsectorssuchasretail

andtransportation.

Moreover,evenwhendigitalcompaniesarecreatinghundredsofthousandsof

jobs,criticsblamethemforthe“missingmiddle”—thelackofjobsrequiringmid-

levelskillsaccessibletomanyAmericans,andpayingmid-levelwages.Someworry

thesecompaniesarecreatingworkonlyforhighly-trainedandspecializedsoftware

developers.Otherdigitalleaders—inparticular,Amazon—arebeingaccusedof

hiringworkersintolow-wagetemporarypositions.4

Inthispaperweaddressbothoftheseconcernsdirectly.Usingdatafromthe

BureauofLaborStatistics,wemakethecasethatthehigh-productivitydigitalfirms

arestartingtogenerateanewmiddleclass.It’savirtuouscircle.Consumersflock

tothosefirmsbecausetheyofferlowerpricesandbetterservice.Workersmigrate

therefromlow-productivityfirmsbecausethehigh-productivityfirmsofferbetter

wagesforthesameoccupations—and,often,steadierhoursandbetterbenefits.

Thisshiftofjobsfromlow-productivitylow-wagefirmstohigh-productivityfirms

payingbetterwagesisclearlycausingsomedisruptionpolicymakersmustaddress.

Nevertheless,ifthisnewpatterncontinues,itwillraiserealwagesacrossthe

economyandrejuvenatethemiddleclass.

Thispaperisdividedintotwoparts.PartI,presentedhere,focusesontheoverall

digitalsector—ecommerce,inparticular.PartII,inafollowingpaper,examinesjob

5

andwagepatternsinthetelecomandtechindustriesandshowshowthese

industriesarecontributingtothenewmiddleclass.

Hereareourmainfindings:

JobCreation

• Workisshiftingtothehigh-productivitydigitalsector.Forexample,since

2007,hoursworkedbyproductionandnonsupervisoryemployeesinthe

digitalsectorhaverisenby8.5percentcomparedtoa3.4percentincreasein

thephysicalsector.Thiscontinuesa20-yearpattern.

• Theecommercesectorisaddingjobsmuchfasterthanthegeneralretail

sectorislosingthem.Wedefinetheecommercesectortoincludewhatthe

governmentcallsthe“electronicshopping”industry(NAICS4541)and

“generalwarehousing”(NAICS49311),inordertopickupthetremendous

growthoffulfillmentcentersandsimilarestablishments.Wedefinethe

generalretailsectortoincludethoseretailersthatcompetemostdirectly

withecommerce,includingelectronicsstores(NAICS443142);clothing,

shoes,andjewelrystores(NAICS448);sportinggoods,hobby,musical

instrument,andbookstores(NAICS451);andgeneralmerchandisestores,

includingdepartmentstoresandsupercenters(NAICS452).

Wefoundthattheecommercesectoradded355,000jobsfrom2007to

2016—morethanenoughtocompensateforthe51,000jobslostinthe

generalretailsector.From2013to2016,thecombinationofecommerceand

generalretailaddedroughly373,000jobs.Toputthisinhistorical

perspective,thebestthree-yearstretchforjobgrowthingeneralretailinthe

6

past25yearswasa374,000-jobgainfrom1997to2000.

• Wageandsalarypaymentstoecommerceworkershaveincreasedby

almost$18billionsince2007,in2016dollars.Bycomparison,realwageand

salarypaymentstoworkersingeneralretailhaverisenbylessthan$1billion

overthesameperiod.

Pay

• Productionandnonsupervisoryworkersearnhigherpayinthedigital

sector.Averagehourlywagesforproductionandnonsupervisoryworkersin

thedigitalsectorin2016were$25.73perhour,ortheequivalentof$53,509

forafull-timeyear.5That’s29percenthigherthanaveragehourlywagesfor

productivityandnonsupervisoryworkersinthephysicalsector.

• Productionandnonsupervisoryworkersinthedigitalsectorareseeing

significantpayincreases.Realhourlywagesforproductionand

nonsupervisoryworkersinthedigitalsectorhavebeenrisingata1.2percent

annualratesince1996.Inthephysicalsector,realhourlyearningsfor

productionandnonsupervisoryworkersinthephysicalsectorhavebeen

risingatonlya0.6percentannualratesince1996.Thesamepatternholds

truesince2007aswell.

• Workersearnhigherpayinecommercecomparedtogeneralretail.Average

hourlyearningsinecommerce,includingfulfillmentcenters,are$21.13per

hour.That’s27percenthigherthanthe$16.65perhouringeneralretail.

Productionandnonsupervisoryworkersinecommerceearnanaverageof

$17.41perhour,comparedto$13.83ingeneralretail—a26percent

7

premium.

• Workersinmid-skilloccupationssuchasofficeandadministrativesupport;

sales;andinstallation,maintenance,andrepairgetpaidsignificantlymore

inthedigitalsector.Onaverage,officeandadministrativesupportworkers

getpaid10percentmoreinthedigitalsector.Installation,maintenance,and

repairgetpaid12percentmore.Andsalesandrelatedoccupationsgetpaid

68percentmore,onaverage,inthedigitalsector.

• Workersinmid-skilloccupationssuchasofficeandadministrativesupport,

sales,andcustomersupportgetpaidsignificantlymoreintheecommerce

sector.Officeandadministrativesupportworkersgetpaid28percentmore

intheecommercesectorcomparedtogeneralretail.Salesandrelated

occupationsgetpaid69percentmoreinecommerce.Customerservice

representativesgetpaid17percentmoreintheecommercesector.

• Ecommercehasenteredavirtuouscircle,withfasterproductivitygrowth

enablingsmallerincreasesingrossmarginsthaningeneralretail,evenas

thesectorpayshigherwages.Weestimatethatmarginsintheecommerce

sectorhaverisenathalftherateasingeneralretail.Ifweinclude

warehousing,theproducerpriceofecommercehasfallensince2007.

GeographicDistribution

• Thegainsfromrisingdigitalpayrollsarespreadacrossthecountry.

Between2007and2015,wageandsalarypaymentstoworkersinthedigital

sectorrosebymorethan10percentin30states,adjustedforinflation,with

noobviousregionalpatternindigitalsectorgrowth.

8

Between2007and2015,thedigitalsectorproducedbiggerwageandsalary

increasesthanthephysicalsector,adjustingforinflation,in30states—

includingmuchoftheMidwestandtheSouth.

• Thegainsfromrisingecommercepayrollsarespreadacrossthecountry.

From2007to2015,realecommercewageandsalarypaymentstoworkers

increasedbymorethan20percentin32states,includingtheDistrictof

Columbia.SomebiggainersincludedTennessee,SouthCarolina,and

Kentucky.

From2007to2015,thecombinationofecommerceandgeneralretail

producedrisingrealwageandsalarypaymentsin39outof51states

(includingtheDistrictofColumbia).

9

TheHistoricalParadigmforMiddle-ClassGrowth

Inrecentyears,economistshaveconclusivelydemonstratedtherearelargeand

persistentproductivitydifferencesbetweencompaniesinthesameindustry.6In

otherwords,somecompaniesaresimplymuchbetteratusingthesameinputs.A

recentOECDreportcalledthesehighperformers“frontierfirms.”7

Recentresearchalsosuggeststhataggregategainsinproductivityaredrivenbythe

shiftofworkersandmarketsharefromlow-productivitylaggardstohigh-

productivityfrontierfirms.8Itwouldbegreatifeverycompanycoulduptheir

game,butexistingbusinessesoftenhaveatoughtimeadoptingnewtechnologies

andwaysofdoingthings.9Expectingadonkeytosuddenlybecomearacehorseis

unreasonable.Ifyouwanttotravelfaster,youarebetteroffshiftingyoursaddle.

Lookingback,wecanseethisprocessatworkinthefirsthalfofthe20thcentury.

From1919to1955,manufacturingproductivitymorethantripled,whilereal

earningsforfactoryworkerssoared.10

Thejumpingoffpoint,ofcourse,wasHenryFord’s1914movetodoublethedaily

wageforworkersathisHighlandParkfactoryto$5perday,accompaniedbyhis

introductionofnewproductiontechniquesthatdramaticallyincreasedproduction

andreducedthecostofproducingtheModelT.ThepriceofaModelTTouringCar

fellfrom$950in1908to$360in1916.11

Ford’scombinationofhighproductivity,highwages,andlowpricesattractedboth

workersandcustomersandenabledFordtocreatejobsataspectacularrate.He

wentfrom14,000workersinhisHighlandParkfactoryin1914to36,000workersin

1917.By1955,whentheeconomywasstartingtosettleintonormalcyafterthe

10

GreatDepression,WorldWarII,andtheKoreanWar,FordMotoremployedmore

than180,000workers.

Otherhigh-productivity“frontierfirms,”tousetheOECDterminology,were

showingequallydramaticgainsinemploymentoverthatsameperiod.General

Motorswentfrom86,000employeesin1919tomorethan600,000workersin

1955.IBM’sworkforcewentfrom3,000workersto56,000,whileDuPontwent

from32,000to87,000workers.Meanwhile,GeneralElectricwentfromroughly

50,000workersin1914to215,000in1955.12

Onaverage,thesefivefrontierfirmsalonemorethanquintupledtheiremployment

between1919and1955.Thatgrowthfarexceededoverallmanufacturing

employment,whichincreasedby50percentoverthesamestretch.13Asthese

firmsexpandedtheirworkforce,theneteffectwastoreplacelow-wagejobswith

jobsthatofferedmiddle-classincomes,liftingrealearningsandlivingstandardsfor

thecountryasawhole.By1955,factoryworkerscametoepitomizetheAmerican

middleclass.

11

JobCreationintheDigitalSector

Isthesamevirtuouscircleatworktodayfordigitalcompanies?Skepticsworrythat

digitalcompaniesarenotgeneratingjobsfastenoughtomakeupforthelostjobs

intherestoftheeconomy.Second,theyareconcernedthatthedigitalboomis

onlygeneratinghigh-orlow-endjobswhileleavingoutthemiddle-skill,middle-pay

jobs.

Inthissectionwewilladdressthefirstoftheseissues.Firstwenotethatthe

industrialclassificationschemeusedbygovernmentstatisticiansisnotdesignedto

measurethecrosscuttingactivitiesofthemodernknowledgeeconomy.For

example,theBLSreportsthereareroughly200,000jobsinanindustry

called“Internetpublishingandbroadcastingandwebsearchportals.”Itwouldbe

easytoassumethatthisindustrycategoryencompassesallofthejobscreatedby

GoogleandFacebook.

However,theBLSassignsjobsbyestablishment,notbycompany,wherean

establishmentisdefinedasasinglelocationproducingasinglegoodorservice.So

acompanysuchasGoogle—whichprovidessearchservices,developssoftware,

runsanetworkofdatacenters,sellsadvertising,laysfiber,anddeliversan

astonishingamountofvideoeachday—mayreportitsU.S.employeesinmultiple

industries.

Similarly,Appledesignscomputersandsmartphones,developssoftware,andruns

retailandonlinestores,soitsdomesticemploymentmayappearinmultiple

industries.Amazonisknownasanecommercesite,butitalsorunshugedatabases

andoperatesfulfillmentcenters(whichprobablyarebeingreportedintheindustry

12

categoryforgeneralwarehousing).

Itgetsworse.Callcentershavetheirownindustrycategory,soacompany’scall

centeremploymentmightshowupinadifferentcategorythanthecompanyitself.

WorkersforonlinetravelsitessuchasExpediamightbereportedintheInternet

industryorintheindustryfor“AllOtherTravelArrangementandReservation

Services.”Etsy,theonlinemarketplace,mightbereportingitsjobsunderdata

hosting,electronicshopping,oranyofanumberofotherindustries.

Becauseofthisambiguityinhowdigitaljobsarereported,weuseabroad

definitionofthedigitalsector,asoriginallyoutlinedinour2016paper.14Wedivide

theprivatesectorintodigitalandphysicalindustries,wherethedigitalindustries

arelistedinTable1.

Digitalindustriestendtobeindustrieswheretheoutputcanbeeasilydigitized—or

anessentialpartofthetransactionwithcustomerscanbedonedigitally.These

includeInternet,techandsoftwareindustries;telecomandbroadcasting;

ecommerce;contentindustriessuchasjournalismandentertainment;anda

varietyoffinancial,professional,andtechnicalactivities.

Bycontrast,thephysicalindustries—suchasmanufacturing,transportation,health

careandconstruction—arenoteasilydigitized.Asaresult,thedigitalsector,as

definedinTable1,accountsforroughly25percentofprivatesectorjobs,but65-70

percentofinfo-techinvestment.

Byatleastonemeasure,workersinthedigitalsectoraresignificantlymore

productivethanworkersinthephysicalsector.In2015,thetotalvalue-added

generatedinthedigitalsectorperfull-timeequivalentworkerwas26percent

13

higherthanthetotalvalue-addedgeneratedinthephysicalsectorperfull-time

equivalentworker.Wenotethatthisgapwasonly19percentin2000,soit’sbeen

wideningovertime.

Table1:IndustriesintheDigitalSector

TechComputer,communications,andelectronics

manufacturingComputer,peripheral,andsoftwarewholesalers*

Softwarepublishing Dataprocessing,hostingandrelatedservices

InternetpublishingandwebsearchComputersystemsdesign

TelecomandBroadcasting Wiredandwirelesstelecommunications

SatellitetelecommunicationsTelevisionandcable

EcommerceElectronicshoppingandmailorder*Generalwarehousing*

ContentPrintandinternetpublishing

Video,movies,andmusicproductionanddistribution

Financial,professional,andtechnicalactivitiesProfessionalandtechnicalactivities(including

accounting,engineering,design,marketresearch,advertising)

Financeandinsurance**ManagementofenterprisesAdministrativesupport(includingcallcenters,travelagencies,andtemporaryagencies)*TheseindustriesexpandthedefinitionofthedigitalsectoroverMandel(2016).**Dependingonthedataset,wesometimesusethebroadercategoryoffinancialactivities.

Data:CenterforEmergingEmployment(PPI)

14

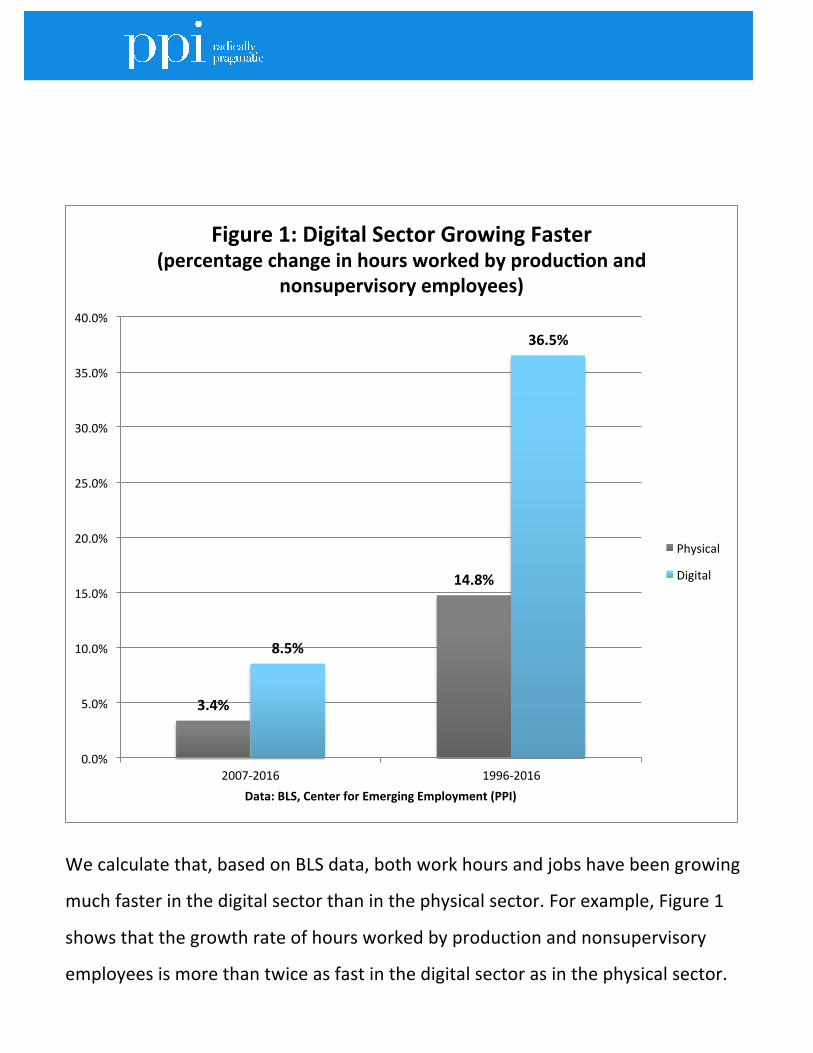

Wecalculatethat,basedonBLSdata,bothworkhoursandjobshavebeengrowing

muchfasterinthedigitalsectorthaninthephysicalsector.Forexample,Figure1

showsthatthegrowthrateofhoursworkedbyproductionandnonsupervisory

employeesismorethantwiceasfastinthedigitalsectorasinthephysicalsector.

3.4%

14.8%

8.5%

36.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2007-2016 1996-2016Data:BLS,CenterforEmergingEmployment(PPI)

Figure1:DigitalSectorGrowingFaster(percentagechangeinhoursworkedbyproducXonand

nonsupervisoryemployees)

Physical

Digital

15

Withinthedigitalsector,oneofthefastestgrowingareasisecommerce.Asnoted

above,thegovernment’sindustryclassificationincludesanindustrylabeled

“electronicshoppingandmail-orderhouses”(NAICS4541).However,an

examinationofthestate-leveldatasuggeststhatthisindustryclassificationdoes

notpickupthefulfillmentcentersusedbyAmazonandothers.Forexample,

Amazonreports12,000employeesinKentuckyasofFebruary2017.15ButtheBLS

reportsonly2,640workersintheNAICS4541industryinKentuckyasof2015.By

contrast,thegeneralwarehouseindustry(NAICS49311)hadmorethan23,000

workersinKentucky.

Moreover,overthepastseveralyears,therehasbeenanunprecedentedsurgein

employmentinthegeneralwarehouseindustry,coincidingwiththeboomin

ecommerce.Indeed,someofthebiggestincreasesingeneralwarehouse

employmentarefoundinstatessuchasIndiana,Kentucky,Pennsylvania,and

Tennessee,whereAmazonhasbuiltfulfillmentcentersandreportsemploying

thousandsofworkers.

Forthatreason,weincludegeneralwarehousingintheecommercesector.We

choosenottoincludetruckdriversaspartoftheecommercesectorbecausethey

aretypicallynotemployedbytheecommercecompanies.

Wecontrastjobsintheecommercesectorwithjobsinwhatwecall“general

retail”—industriesthatcompetedirectlywithonlinesellers.Forthepurposesof

thispaper,wedefined“generalretail”toincludegeneralmerchandisestores,such

asdepartmentstores,warehousestores,andsupercenters;clothingandclothing

accessorystores;sportinggoods,hobby,andbookstores;andelectronicsstores.

16

Inrecentyearswehaveseenashiftofjobsfromthegeneralretailsectortothe

ecommercesector,asecommercehasbecomemoreimportant.Figure2compares

jobgrowthinecommercewithjobgrowthingeneralretail.Wecanseethat,from

2007to2016,therewasasmalldecreaseingeneralretailjobs.Butthosejobs

didn’tdisappear.Instead,theywereshiftedtotheecommercesector;plus,many

morewerecreated.From2007to2016,therewere355,000newjobscreatedin

theecommercesector.Intotal,therewasanetincreaseof304,000jobsinthe

combinedecommerce/generalretailbusinesses.

Table 2: Defining the Ecommerce and General Retail Sector

Ecommerce

Electronicshoppingandmail-orderhousesGeneralwarehousingandstorage

General Retail

Generalmerchandisestores(includingdepartmentstores,warehousestores,andsupercenters)ClothingandclothingaccessorystoresSportinggoods,hobby,bookstoresElectronicsstores**Dependingontheparticulardataset,itissometimesnecessarytousethebroadercategoryofelectronicsandappliancestores.Data:CenterforEmergingEmployment(PPI)

17

Evenmoreremarkableisthejobcreationduringthethree-yearperiodfrom2013

to2016.Combined,ecommerceandgeneralretailaddedatotalof373,000jobs

overthatstretch.Thatroughlyequalsthebestthree-yearstretchforjobcreation

bygeneralretailinthe1990s(1997-2000).

Theseresultsdonotsupportthecriticismthattheriseofecommerceisdestroying

jobs.Instead,itappearstobecreatingmorejobs.Thiscounter-intuitiveoutcome

makesmoresensewhenyouthinkabouthowecommerceactuallyoperatesin

practice.Aconsumerpreviouslyhadtotakeasignificantamountoftimetodriveto

theshoppingmall,walkthroughtheaislesofthestoretoidentifytheshirtthey

wanted,standonlinetopay,andthendrivehome.Ecommercemovesthese

formerlynon-marketactivitiesintopaidworkinordertoincreaseconvenienceand

allowconsumerstousethattimeforother,morepleasurableactivities.

Whataboutthequalityofthesenewjobsinecommerce?Laterinthispaper,we

-51

112

355

261304

373

-100

-50

0

50

100

150

200

250

300

350

400

2007-2016 2013-2016

Data:BLS,CenterforEmergingEmployment(PPI)

FIgure2:GeneralRetailvsEcommerceEmployment

(changeinjobs,thousands)

Generalretail

Ecommerce

Total

18

willcomparewagesintheecommerceandgeneralretailsectorsindetail.To

foreshadowthatanalysis,jobsintheecommercesectorpay27percentmoreper

hourthanjobsinthegeneralretailsector.

But,ratherthanlookingataverages,whichcanbemisleading,itisusefulto

examinetheaggregatetotalofwagesandsalariespaidoutbytheecommerce

sectorwiththeaggregatetotalofwagesandsalariespaidoutbythegeneralretail

sector.Iftheshifttoecommerceisaboutcuttinglaborcosts,ascriticsallege,then

wewouldexpecttheaggregatewagesandsalariesinecommercetorisebyless

thanthedeclineingeneralretailaggregatewagesandsalaries.

Figure3showsthechangeinaggregatewagesandsalariesinecommerceand

generalretail,adjustedforinflationandcomparedto2007.Wecanseethatreal

wagesandsalariesingeneralretailfellsharplyduringtherecessionandrecovered

onlyslowly.Asof2016,theyareonlyabout$1billionabovetheir2007level,

measuredin2016dollars.Bycontrast,realwagesandsalariesintheecommerce

sectorbarelydippedintherecessionandarenowalmost$18billionabovetheir

2007level,measuredin2016dollars.

Intotal,thecombinedwagesandsalariesinecommerceandgeneralretailhave

risenbyalmost$19billionsince2007,measuredin2016dollars.Thatsuggeststhe

shifttoecommerceisimprovingthequalityofjobsratherthanreducingit.

19

-20000

-15000

-10000

-5000

0

5000

10000

15000

20000

25000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Calculatedfromweeklypayrollsassuming52weeksinyearData:BLS,CenterforEmergingEmployment(PPI)

Figure3:GeneralRetailPayRecovers,EcommercePaySoars

(Changeinrealwagesandsalariessince2007,millionsof2016dollars)

Ecommerce

Generalretail

total

20

RelativePay

Isthedigitalboomcreatingmiddle-classjobs?Sofarwehaveshowntheexpansion

ofthedigitalsectorcomparedtothephysicalsector—andtheecommercesector

relativetothegeneralretailsector.Inotherwords,workersareshiftingfromolder,

slow-growingindustriestonewerindustriesthatareinvestingheavilyin

informationtechnology.

Butwhatkindofjobsaretheygetting?WestartbyusingBLSdatatocalculate

averagehourlyearningsforproductionandnonsupervisoryworkersinthedigital

andthephysicalsectors,adjustedforinflation.

21

In2016,theaveragehourlywageinthedigitalsectorwas$25.72,whichisroughly

29percenthigherthanthe$19.89earnedinthephysicalsector(Figure4).

Moreover,realhourlyearningsarerisingata1.2percentannualrateinthedigital

sector,roughlytwiceasfastthe0.6percentannualrateinthephysicalsector.

Here’showtomakesenseofthesenumbers:Workersinthedigitalsectorare

averagingmiddle-classwages.Moreover,realwagesinthedigitalsectorarerising

atahistoricallyreasonablerate.

Bycontrast,workersinthephysicalsectoraredeepinahole.Atthecurrentrate

theirwagesareincreasing,workersinthephysicalsectorwouldtake40yearsto

25.72

19.89

15.00

17.00

19.00

21.00

23.00

25.00

27.00

Data:BLS,CenterforEmergingEmployment(PPI)

Figure4:ProducXonandNonsupervisoryWorkersinDigitalIndustriesMakeMiddle-ClassWages

(AverageHourlyEarnings,2016dollars)

Digital

Physical

22

catchuptothewagesbeingpaidtoworkersinthedigitalsectortoday.Butthat

calculation—whichassumesworkersstayinthephysicalsector—underscoresthe

potentialbenefitsofshiftingtohigher-productivityemployers.

Wecandoasimilarcomparisonbetweenthewagesbeingpaidtoworkersinthe

ecommercesectorandinthegeneralretailsector.Averagingoverallemployees,

thepaypremiumforworkingintheecommercesectorasopposedtothegeneral

retailsectoris27percent(Figure5).Forproductionandnonsupervisoryworkers,

averagehourlyearningsare26percenthigherintheecommercesectorcompared

tothegeneralretailsector.

21.13

17.4016.65

13.82

0.00

5.00

10.00

15.00

20.00

25.00

Allemployees producXonandnonsupervisoryData:BLS,CenterforEmergingEmployment(PPI)

Figure5:EcommerceWorkersEarn25-30%More

(averagehourlyearnings,2016)

Ecommerce

Generalretail

23

Ofcourse,wemustpointouttheobvioushere—wehavenotyetactuallyshown

thatworkersinthesameoccupationgetpaidmoreinthedigitalorecommerce

sectorscomparedtothephysicalorgeneralretailsectors.Thewagepremium

couldreflectabifurcatedworkforce,withamixofhigh-wageandlow-wagejobs,

withnothinginbetween.

Sonowwefocusonthepayindifferentoccupationalcategories.(Thisanalysisis

basedonMay2015datafromtheOccupationalEmploymentStatisticsfromthe

BureauofLaborStatistics.)Inparticular,welookatmid-skilloccupationssuchas

officeandadministrativesupport;salesandrelatedoccupations;andinstallation,

maintenanceandrepairoccupations.

24

Table3.DigitalIndustriesPayMoreforMid-SkillOccupations

Hourlymeanwage,May2015

Digital Physical

Digitalpremium(percent)

Officeandadministrativesupport 18.14 16.42 10%Salesandrelated 31.74 18.93 68%Installation,maintenance,andrepair 24.14 21.54 12%Computerandmath 43.18 36.85 17%

Data:BLS,CenterforEmergingEmployment(PPI)

Weseethat,inthesemiddle-skilljobs,digitalindustriespaymorethanphysical

industriesonaverage.Forexample,firmsinthedigitalsectoremployedalmost8

millionworkersinofficeandadministrativesupportoccupationsin2015.These

workersearned10percentmoreinthedigitalsectorthaninthephysicalsector,in

partbecausedigitalfirmsaremoreproductiveandcanaffordtopaymore.That10

percentisworth15yearsofwagegainsatcurrentrates.

Similarly,firmsinthedigitalsectorpay12percentmore,onaverage,for

installation,maintenanceandrepairoccupations,and68percentmoreforsales

occupations.

25

Table4.EcommercePaysMoreforMid-SkillOccupations

Hourlymeanwage,May2015

Ecommerce GeneralRetail

EcommercePremium(Percent)

Officeandadministrativesupport 16.36 12.81 28%Salesandrelated 20.75 12.28 69%Customerservice 15.63 13.36 17%Computerandmath 36.92 27.18 36%

Data:BLS,CenterforEmergingEmployment(PPI)

Wecandoasimilaranalysiscomparingpayformid-skilloccupationsinthe

ecommercesectorversusgeneralretail.Forexample,customerservice

representativesgetpaid17percentmore,onaverage,intheecommercesector.

Thissuggeststhatpaylevelsforsimilaroccupationsarehigherinecommerce.

26

TheAmazonCritique

OneoftheodditiesofthecurrentdebateoverjobsisthatecommercegiantAmazonhascomeunder

attackforreplacinglow-paidjobswithbetter-payingjobs.Forexample,onerecentarticlewrote:

WhileAmazonisaddingjobs,retailerssuchasMacy’s(M)andSearsareslashingstaffand

closingstores,partlyduetoincreasedcompetitionfromtheonlineretailinggiant,LaVecchia

pointsout.“Amazonisdestroyingmorejobsthanitcreates,”shesaid.“Itemploysfewer

peoplethanothercompaniesforthesameamountofsales.”

This,ofcourse,istheverydefinitionofhigherproductivity,whichshouldleadtohigherpayfor

workersintheecommerceindustry.Andthat’swhatappearstohappen.Amazonreports:“Wepay

ourfulfillmentcenteremployees30percentmorethantraditionalretailstores.”Whilethereisno

waytoindependentlyverifythesefigures,theyaregenerallyconsistentwiththewagepremiums

betweentheecommerceandgeneralmerchandisestoresreportedbyBLS.

Moreover,itispeculiarthatactivistsaretryingtopresentconventionaljobsintheretailsectoras

desirable.That’sodd,consideringthatgeneralmerchandisestores—includingdepartmentstores

anddiscountretailers—payonly$12.28perhour,onaverage,forproductionandnonsupervisory

workers.Realwagesinthisindustryhavefallensince2007.

Toallappearances,AmazonisfollowinginthefootstepsofindustrialgiantssuchasGeneralMotors

andGeneralElectric:high-productivityenterprisesthatcanaffordtopayhigherwagesandgradually

enableworkerstoshifttothesehigherpayingopportunities.

27

GeographicDistribution

Tothedegreethatthedigitalboomiscreatinganewmiddleclass,it’simportantto

knowwhetherthegainsaregeographicallyconcentrated.DatafromtheBureauof

LaborStatisticsenableustoassesstheeconomicimpactofthedigitaland

ecommercesectorsonastate-by-statebasis.Westartbycalculating,foreach

state,thepercentagechangeinrealwageandsalaryoutlaysbythedigitalsector

since2007.

28

Figure6:PercentageChangeinRealWageandSalaryOutlays

intheDigitalSector,2007-2015

29

ThestatescoloreddarkbrowninFigure6havemorethana20percentincreasein

digitalsectorpaysince2007.Notsurprisingly,thePacificCoaststateshavefast-

growingdigitalsectors,asdoesTexas.Lessanticipatedarethebiggainsin

TennesseeandNorthCarolina,whicharedriveninpartbyecommerceexpansion

andbyagrowingtechsector.

Butthegainsareevenmorewidespreadthanthat.Asthemapshows,30states

havemorethana10percentgaininrealdigitalpayfrom2007to2015.Theyare

spreadacrosstheentirecountry,fromGeorgiathroughKansasandupto

Washington.Infact,thereisnoobviousregionalpatternindigitalsectorgrowth.

Thesamecannotbesaidforthenextmap.Figure7identifiesthestateswherethe

gaininrealdigitalwagesandsalariesexceedsthegaininrealwagesandsalariesin

thephysicalsector.Weseeastronglyregionalpattern,wherethePacificstates

havearelativelystrongdigitalsector,asdotheMidwestandSouthernstates—

perhapsreflectingtheweaknessofthephysicalsector.

30

Figure7:DigitalvsPhysical:Stateswheregaininrealpayin

thedigitalsectorexceedsgaininrealpayinthephysical

sector,2007-2015

Nowweturnourattentiontoecommerce.Figure8showsthegaininreal

ecommercepayrollsfrom2007to2015.Onceagain,thereisnoobviousregional

patterninthedistributionofstrongperformers.StatessuchasIndiana,Kentucky,

andTennesseearebenefitingfromtheircentralpositionforfulfillingquickdelivery

orders.Buttherearebiggainersallaroundthecountry.

31

Figure8:GrowthofEcommerceRealWagesandSalaries,

2007-2015

32

Ourfinalmapcombinestherealwageandsalaryspendingforboththeecommerce

andgeneralretailsectors(Figure9).TopperformersincludeWashingtonstate,

Delaware,andKentucky,butnotCaliforniaorMassachusetts.Inotherwords,the

benefitsofecommerceshownosignofbeingconcentratedinanyoneregionof

thecountry.

33

Figure9:GrowthofRealWagesandSalariesforCombined

EcommerceandGeneralRetail,2007-2015

34

BetterJobsforWorkers,LowerPricesforConsumers

We’vemadethecaseinthispaperthatthesuccessfulcompaniesinthedigital

sectorhavereachedasizewheretheyarehavingamajoremploymentimpact.

Theyareofferinghigherwages.Thus,thenumberofbetter-payingjobsgrowsand

beginstoraiselivingstandards.

Indeed,wearebeginningtoseetheshapeofanewmiddleclass:mid-pay,mid-

skilledadministrativeandcustomersupport;sales;andinstallation,maintenance,

andrepairpositions.Theprocesscouldandshouldcontinueforyearsoreven

decades.Indeed,inanearlierpaper,weestimatedthatonlyabout25percentof

theeconomyhadbeendigitized.

Whataboutthebenefitstoconsumers?Pricesinthedigitalsectorhaverisenonly

0.8percentperyear—farslowerthanthe2.4percentrateofpriceincreasesinthe

physicalsector.Inotherwords,evenslowincomegrowthenablesAmericansto

havearisingstandardoflivingfordigitalproductsandservices.

Theecommercesituationisinteresting.TheBLStracksproducerpricesforretail

industries,whichitmeasuresasgrossmargins.16Between2007and2016,gross

marginsinecommerceroseby4.6percent.Bycomparison,grossmarginsin

generalretailroseby9.7percent—morethandoubletheincrease.Thisdifference

reflects,inpart,slowercostincreasesinecommercebecauseoffasterproductivity

growth.Inaddition,a2014reportfromtheBLSnotesthat“marginsforthe

electronicandmail-ordershoppingindustrygrouphavebeenshrinking,likely

becauseofincreasedcompetitioninthee-commercemarket.Brick-and-mortar

retailers,bycontrast,havebroadenedtheirmarginstocovertheirrisingrentand

marketingexpenses.”17

35

Inotherwords,asfaraswecandetermine,thegrowthofecommerceisshifting

workersfromlow-paidjobsatretailstorestobetter-paidjobsinecommerce.This

isexactlywhatwewouldexpectgiventherapidgrowthofproductivityin

ecommerce—partofthegainsgotocustomersintheformofslowergrowthof

retailmargins,andpartofthegainsgotoworkers.

36

Coda

Thispaper(PartI)analyzedjobandwagepatternsinthedigitalsectorandthe

ecommercesector.InPartII,wewillexaminejobandwagepatternsinthetelecom

andtechindustries,showinghowtheseindustriesarecontributingtothenew

middleclass.Thenwewilladdresspolicyprescriptions.

37

References 1MichaelMandel.2017.“AHistoricalPerspectiveonTechJobGrowth,”ProgressivePolicyInstitute,http://www.progressivepolicy.org/wp-content/uploads/2017/01/tech-job-boom-1-12c-17-formatted.pdf2https://www.amazon.com/p/feature/onsg5ynd2pet3t33http://www.pewsocialtrends.org/2015/12/09/1-the-hollowing-of-the-american-middle-class/4“AmazonandWalmartarehiring,buthowgoodarethesejobs?,”January19,2017.http://www.cbsnews.com/news/amazon-walmart-retail-hiring-wages/5Assuming2,080hoursinafullyear.6ChadSyverson.2011.“WhatDeterminesProductivity?”JournalofEconomicLiterature49:2,326–3657DanAndrews,ChiaraCriscuoloandPeterN.Gal.2015“FrontierFirms,TechnologyDiffusionandPublicPolicy:MicroEvidencefromOECDCountries,”OECD8Foster,Lucia,JohnHaltiwanger,andC.J.Krizan.2006.“MarketSelection,Reallocation,andRestructuringintheU.S.RetailTradeSectorinthe1990s.”ReviewofEconomicsandStatistics,88(4):748–58.9ThatstructuralproblemisthewholepointofClayChristenson’sInnovator’sDilemma10CensusBureau,1975.HistoricalStatisticsoftheUnitedStatesChapterD,page162,166.11http://www.autonews.com/article/20030616/SUB/30616072212Thisdataismostlypulledfromcontemporaryannualreports.Wepick1919toavoidWorldWarIandthedownturnof1920-21,and1955astheinitialreturntoanormaleconomyaftertheKoreanWar,WorldWarII,andtheGreatDepression.13Animportantcaveat:Theemploymentfiguresfromtheannualreportsincludeoverseasjobsaswellasjobsoutsideofmanufacturing,sowecan’tdoadirectcomparison.14“Long-termProductivityGrowthandMobileBroadband:TheRoadAhead”http://www.progressivepolicy.org/issues/economy/long-term-u-s-productivity-growth-and-mobile-broadband-the-road-ahead/15Amazonreportsemployeesperstateherehttps://www.amazon.com/p/feature/nsog9ct4onemec9#IN16Producerpricesforretailindustriestrack“changesinpricesreceived,lesstheacquisitionpriceofgoods.”https://www.bls.gov/opub/btn/volume-1/wholesale-and-retail-producer-price-indexes-margin-prices.htm17https://www.bls.gov/opub/btn/volume-3/trends-in-producer-prices-between-e-commerce-and-brick-and-mortar-retail-trade-establishments.htm