Embed Size (px)

Citation preview

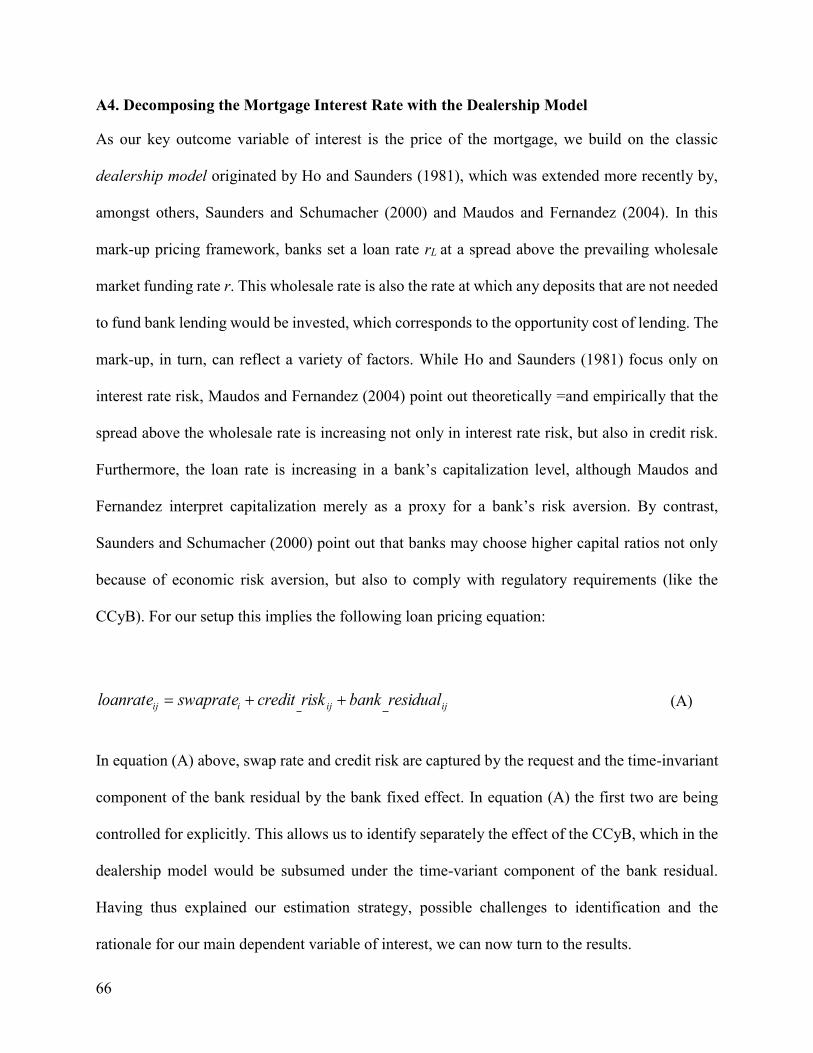

The Countercyclical Capital Buffer

15 February 2017

By CHRISTOPH BASTEN (FINMA) AND CATHÉRINE KOCH (BIS)*

We examine the first activation of the Countercyclical Capital Buffer (CCyB) as macroprudential

tool of Basel III. Our short-term analysis examines how banks adjust their rejections and pricing

of mortgages. We then study how bank capitalization and balance sheet structures respond over

the longer term. We combine unique records of responses from multiple banks per mortgage

application with supervisory bank-level information covering all Swiss banks. We find that the

CCyB causes more CCyB-sensitive banks to raise their mortgage rates relatively more. Over the

longer-term, these differential price increases reflect in differential balance sheet adjustments that

have likely strengthened the resilience of the Swiss banking system. Our results also suggest that

risk-weighting schemes do not amplify the CCyB effect.

Keywords: banks, macroprudential policy, capital requirements, mortgage pricing

JEL codes: E44; E5; G21; G28

* BASTEN: Swiss Financial Market Supervisory Authority FINMA; [email protected]; KOCH (corresponding author): Bank for

International Settlements BIS, Centralbahnplatz 2, 4002 Basel, Switzerland, [email protected]. An earlier, less comprehensive version has

been circulated as BIS Working Paper No. 511 under the title “Higher Bank Capital Requirements and Mortgage Pricing: Evidence from the Countercyclical Capital Buffer (CCB)”. We are grateful to Comparis for providing their data and to Katja Rüegg and Stefan Rüesch for many

helpful discussions. The views expressed here are those of the authors and may not be attributed to the BIS, Comparis or FINMA. For comments

and discussions we would like to thank Robert Bichsel, Urs Birchler, Martin Brown, Claudia Buch, Jill Cetina, Dietrich Domanski, Ingo Fender, Leonardo Gambacorta, Benjamin Guin, Mathias Hoffmann, Terhi Jokipii, Georg Junge, Jongsub Lee, Reto Nyffeler, Steven Ongena, George

Penacchi, José-Luis Peydró, John Schindler, Uwe Steinhauser, Kostas Tsatsaronis, Greg Udell and Simone Westerfeld, as well as conference

participants at the 2016 Carefin-BAFFI Conference, the 2016 ECB-IMF Macropru Conference, the 2016 ASSA Annual Meeting, the 2015 MoFiR

Workshop on Banking, the 2015 Workshop of the Basel Committee’s Research Task Force, the 2014 Cleveland Fed OFR Financial Stability

Conference and the 2014 GRETA Credit Conference, as well as seminar participants at the Bank for International Settlements, Bank of England, Deutsche Bundesbank, European Central Bank, FDIC, FINMA, Office of Financial Research (OFR) in the US Treasury Department, Swiss National

Bank, and various universities. Any remaining errors are solely our responsibility.

1 Introduction

Macroprudential policies have recently attracted considerable attention. They aim first at

strengthening the resilience of the financial system to adverse aggregate shocks and second at actively

limiting the build-up of financial risks in the sense of “leaning against the financial cycle”. To this

end, the Basel III regulatory standards feature the Countercyclical Capital Buffer (CCyB) as the

dedicated macroprudential tool designed to protect the banking sector from the detrimental effects of

the financial cycle (see BCBS, 2010a). This paper provides the first empirical analysis of the CCyB

based on data from Switzerland. In 2013, Switzerland was the first country to activate the CCyB,

requiring banks to hold extra equity capital worth 1% of their risk-weighted assets secured by domestic

residential property.

Little is known about the CCyB’s contribution towards the second macroprudential objective: higher

requirements might slow down bank lending or alter the quality of loans during the boom and thereby

enable policy-makers to “lean against the financial cycle”. Up to now, policy debates have focused mainly

on the quantity of aggregate credit growth. We aim to shift the focus of the debate towards the quality,

namely the composition of lenders and the composition of borrowers in terms of risk characteristics. Does

the CCyB have the potential to shift lending from less resilient to more resilient banks, or from riskier to

less risky borrowers? And how do banks adjust their balance sheets and capitalization in the longer run?

We use unique response-level data that feature individual mortgage applications submitted online, as

well as for each application responses from multiple different banks. With these data, we can uncover

how different banks respond differently to the same set of mortgage applications submitted

respectively before and after the CCyB activation. This differential response would be hidden in data

capturing only aggregate volumes of lending, or in bank-level data that do not allow to control for

3

selection of different types of borrowers into different types of banks.1 The procedures of the online

mortgage platform warrant that banks submit independent offers that draw precisely on the same set

of anonymized hard information observed by their competitors (and available to us), undistorted by

any private or soft information.

In addition to using these unique response-level data, we are able to add supervisory data that capture

at monthly frequency the full balance sheets of the population of all banks chartered in Switzerland.

This enables us to investigate not only differential rejection and pricing responses to the CCyB, but

also how these responses translate into changes in balance sheets and bank capitalization in the longer-

term.

Our results distinguish between the short-term response of banks in the mortgage market, and the

longer-term adjustment patterns as evidenced by bank balance sheet reports.

As an immediate response to its activation, we find that the CCyB impacts the composition of mortgage

supply. Instead of sending more outright rejections, banks reveal significant changes in their pricing

of mortgage applications. In fact, banks with low capital cushions and mortgage-specialized banks

raise prices relatively more. If customers prefer cheaper mortgages, these differential price increases

should shift new mortgage lending from relatively more to relatively less CCyB-sensitive banks.

Indeed our bank-level results lend strong empirical support to this procedure. By contrast, while banks

charge a credit risk premium for high loan-to-value customers in general, risk-weighting schemes do

not significantly interact with tighter capital requirements and hence appear not strong enough to

amplify the effectiveness of the CCyB.

1 This is a truly unique data feature in that multiple lenders per borrower are usually observed for syndicated loans or credit registers with

reporting thresholds for corporate lending only (e.g. Jiménez et al, 2012, Jiménez et al, 2014, or Jiménez et al, 2016).

4

Over the longer term, the differential pricing responses reflect also in balance sheet restructuring and

capitalization. Banks that had previously operated a very mortgage-specialized business model do

more to restore the cushion between their actual capitalization and the tightened regulatory

requirements. Supervisory bank-level data suggest that most banks preferred to draw on their retained

earnings and only a minor share of additional capital in the banking system accrued to banks asking

their shareholders.

We contribute to the literature as well as to the policy debate in at least three respects.

First, we contribute to the literature on the effects of macroprudential policy tools (see Jimenez et al,

2016, and further papers cited there and below), with the first paper on the actual Basel III CCyB: We

suggest and provide empirical evidence that a macroprudential policy may impact different lenders

differentially. This may change the supply composition of lending on top of any changes in the

aggregate volume of lending. Indeed, this shift would not be visible in more aggregate data and could

not be cleanly identified without separate data on loan-level demand and supply. By contrast, we are

able to examine the entire mortgage supply schedule in terms of the pricing and rejection of different

mortgage maturities and types of borrower risk.

Second, by analyzing the effects as the CCyB as a specific, namely temporary, type of bank capital

requirements, we also contribute to the broader literature on the effects of bank capitalization on banks

and the financial system (see Baker and Wurgler, 2015, and references therein). In particular, we

contribute rare evidence from the mortgage market to the literature on how bank capital requirements

impact loan pricing and volumes of lending. Here the setup closest to ours is that by Michelangeli and

Sette (2016), who submit simulated mortgage applications to different banks and find that less well

capitalized banks are more likely to reject applications from risky borrowers, but tend to offer lower

prices to less risky borrowers.

5

Third, we also contribute to the more policy focused debate on the effectiveness of risk-weighting

schemes, a tool much used in bank capital regulation. We assess the effectiveness of risk-weighting

schemes within one asset class and examine how they interact with a rise in capital requirements on

that particular asset class.

The remainder of the paper is structured as follows. Section 2 sketches the institutional background of

the Basel III regulation in general and its Swiss implementation, in particular. It then illustrates the

CCyB’s regulatory design with the help of a back-of-the-envelope calculation and develops four key

hypotheses. Section 3 presents the short-term mortgage market analysis based on our unique response-

level data. Section 4 broadens the scope with data on the entire Swiss banking population and examines

how banks adjusted their capitalization and balance sheet structure in the longer-run. Finally, Section

6 concludes. Our online appendix provides background material, with one specific part showing that

our mortgage market data are representative of the full Swiss mortgage market.

6

2 Basel III, the CCyB, and Hypotheses on its Effects

This section describes the framework of the new Basel III bank capital requirements, first in general

terms, and then in the particular Swiss context. Switzerland was the first country to activate the

countercyclical capital buffer (CCyB) as the key macroprudential tool of Basel III. Having introduced

the institutional setup, we review the literature and then develop hypotheses on the CCyB’s expected

effects in terms of short-term mortgage supply and longer-term adjustment patterns on bank balance

sheets.

2.1 The context of Basel III bank capital requirements

As one integral part of the Basel III banking regulation (BCBS, 2010b) that entered into Swiss law on

July 1, 2012, a new set of capital requirements became effective. The Swiss Federal Council adopted

the Basel III regulation through a revision of the “Capital Adequacy Ordinance” (CAO), one year after

the publication of the new standards by the BCBS. Thus, all Basel III requirements officially went into

force in Switzerland on January 1, 2013.

Regulatory capital requirements are intended to strengthen the loss-bearing capacity of a bank and to

reduce moral hazard incentives. The Basel III rules feature two types of capital ratios, either referring

to total assets (like the leverage ratio) or risk-weighted assets in the denominator. For the latter, the

risk weights associated with a particular asset class can be specified either by the Standardized

Approach (SA) or the Internal Ratings Based Approach (IRB). In fact, all banks entering our analysis

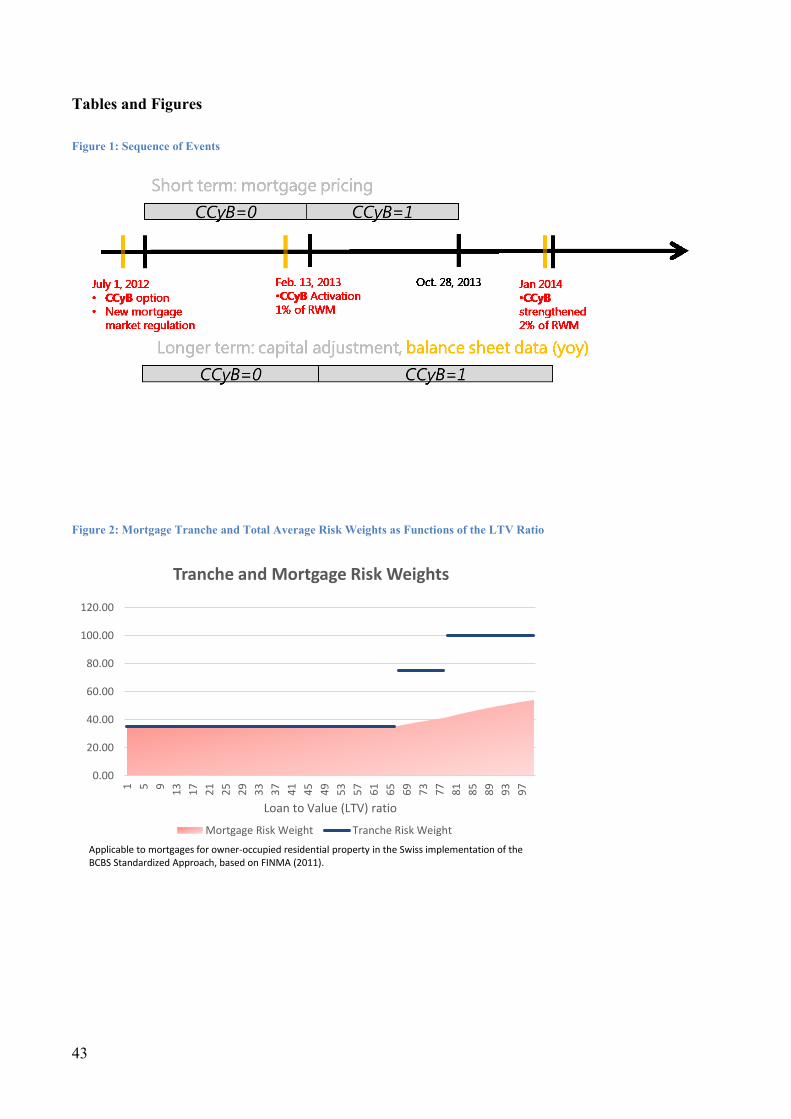

of mortgage supply in Section 3 followed the SA2. Figure 1 describes our sample period and the

sequence of regulatory events in Switzerland.

2 During our sample period of 2012 and 2013, only the two big banks UBS and Credit Suisse, and one smaller bank were allowed to use the IRB

Approach in Switzerland.

7

For the asset class of residential mortgages, the SA imposes a standard risk weight of 35% as long as

a bank adheres to “strict prudential lending standards”. Beyond these standards, Figure 2 illustrates the

corresponding risk-weighting schemes as applied in Switzerland. The tranche of a domestic residential

mortgage with a loan-to-value (LTV) ratio equal to or above 67% receives a risk-weight of 75%, and

the tranche with an LTV ratio equal to or above 80% receives a higher risk weight of 100%. Given the

overall resulting amount of risk-weighted mortgages (RWMs), the new Basel III rules impose a

minimum capital requirement of 8%, plus a Capital Conservation Buffer that ranges between 2.5 and

6.4% of RWMs depending on the supervisor’s (effectively time-invariant) assessment of bank-specific

risks. Further, Swiss authorities can add a Countercyclical Capital Buffer (CCyB) when they deem

new credit origination as "excessive" in the market.

2.2 The CCyB and its first activation

In general terms, the CCyB is the key macroprudential tool within the Basel III regulatory capital

standards. It is aimed specifically at addressing the procyclical effects of risk-based bank capital

requirements associated with previous versions of the Basel rules and its national implementations3

(see BCBS, 2010c). As a macroprudential device, it is geared towards two objectives. The first

objective is to strenghten individual banks on a standalone basis and thereby to improve financial

stability in the overall banking system. In terms of this resilience objective, the activated CCyB

requires banks to increase their risk-weighted capital ratios during boom periods, thus rendering them

more resilient to potential loan losses when risks materialize during downturns. The second objective,

also known as the “leaning against the financial cycle”, aims to slow down credit growth during boom

periods.

3 See for instance Aikman et al (2014), as well as the relevant papers cited therein.

8

When concerns about an overheating real estate sector intensified, and monetary policy was already

committed to defending a minimum bilateral exchange rate between the Swiss Franc and the euro,

Switzerland was the first country worldwide to activate the CCyB on February 13, 2013. Its tailor-

made design targeting domestic residential mortgages came as a surprise. Central to our analysis, the

CCyB applied to the entire domestic residential mortgage book, including the stock of outstanding

mortgages issued before the CCyB activation. The initial calibration was set at 1% of these risk-

weighted residential mortgages, granting banks a transition phase until September 1, 2013.4

Furthermore, the CCyB applies uniformly to all banks contained in our sample, including subsidiaries

of foreign banks.5,6,7

We focus on the effects of the activation of the CCyB rather than the policy option for the following

reasons. The CCyB becomes a legal option only once without imposing any binding restrictions. By

contrast, the activation may be exercised and adjusted whenever deemed appropriate and it becomes

binding either immediately, or at the latest, after a transition period will have expired. As the buffer

applies to all mortgages on the balance sheet, regardless of when they were issued, banks are expected

to respond to the activation as soon as it is known and not just after the transition phase. Given the

availability of the CCyB as a policy option, the period from July 1, 2012 to February 12, 2013 serves

as our pre-activation period (denoted as CCyB=0), and the period from February 13, 2013 (the

4 About a year later, in January 2014, that requirement was raised to 2%, to be fulfilled by July 2014. The 2014 increase in the CCyB’s

requirements is not captured by our short-term analysis, as Comparis.ch changed their mortgage brokerage business at the end of 2013.

5 By contrast, branches of foreign banks operating in Switzerland would not be covered, as full reciprocity has not yet been implemented.

However, these foreign branches do not play a significant role in the Swiss mortgage market and no branch enters our sample.

6 For further details on the adoption of the Basel III regulation and the first activation of the CCyB, see also FINMA (2012a), FINMA (2012b),

SNB (2013a) and SNB (2013b).

7 A complementary Appendix II contains more detailed information on the Swiss mortgage market and other equity capital regulation compulsory

for Swiss banks.

9

activation of the tool), until the end of our dataset on October 24, 2013 is the post-activation period

(denoted as CCyB=1).

To avoid any distorting effects, our focus on the activation guarantees that pre- and post-activation

period are otherwise comparable, which would not be the case if we started our sample earlier. Also

on June 1, 2012 two additional changes in the Swiss mortgage market regulation became effective.

The Swiss Financial Market Supervisory Authority FINMA declared the Swiss Bankers Association’s

self-regulation as a new minimum standard applicable to all banks. First, Loan-to-Value (LTV) ratios

have to be reduced to at most two-thirds within at most 20 years after mortgage issuance.8 Second,

home buyers had to pledge at least 10% of the underlying property’s market value as “hard equity”,

i.e. in terms of own liquid funds while disregarding any pension-related assets.9,10

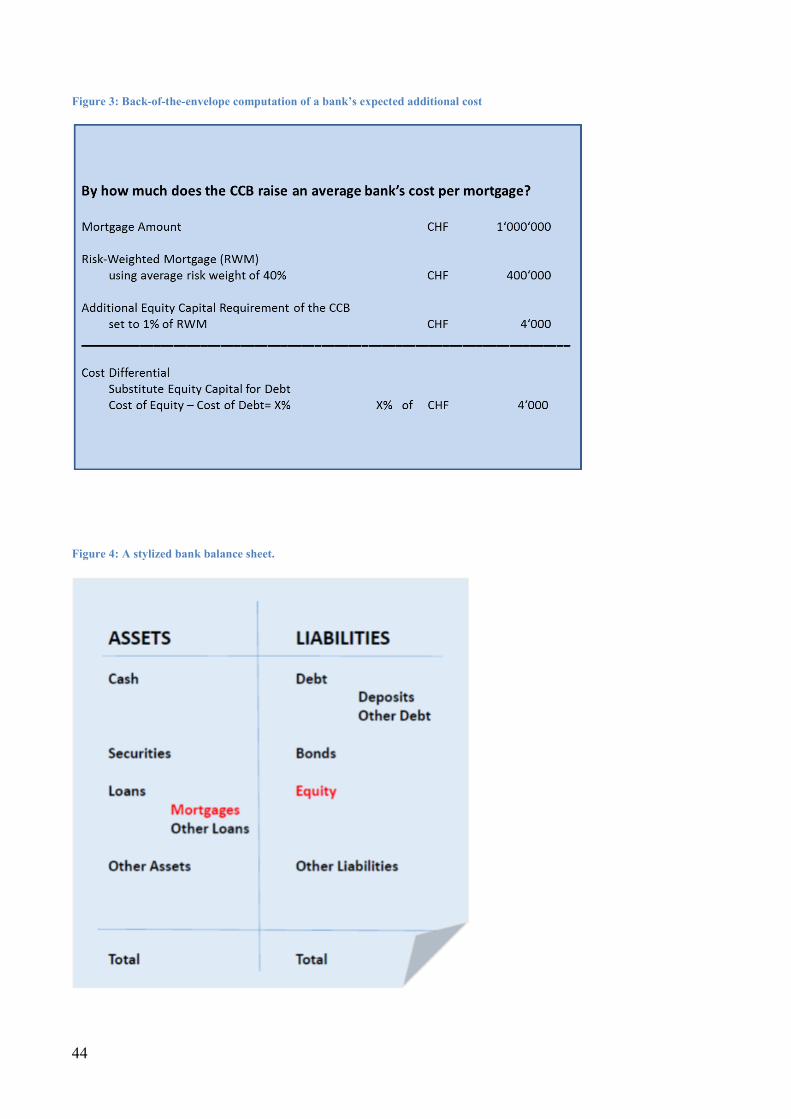

Figure 3 sketches a back-of-the-envelope calculation of the additional costs that arise from the CCyB’s

tighter capital requirments. It is based on a mortgage worth CHF 1 million, regardless of whether that

mortgage captures new lending or whether refers to a mortgage that is already listed on the bank’s

balance sheet (Figure 4). For a typical initial LTV ratio slightly below 80%, the SA suggests an average

risk weight of about 40% as presented by Figure 2 (see also SNB, 2012). This leads us to a risk-

weighted mortgage amount of CHF 400,000 in our example. The CCyB’s first activation requires all

banks to set aside additional CET 1 capital worth 1% of risk-weighted domestic residential mortgages.

For this reason, while keeping the balance sheet size constant, the CCyB prompts the bank to replace

debt or deposit funding worth CHF 4,000 withequity capital. If the Modigliani and Miller (see

Modigliani and Miller, 1985) theorem holds so that equity capital and debt finance are equally costly,

8 In a later revision, this amortization period was reduced to 15 years.

9 By contrast, Swiss mortgage market regulation does to this day not take any references to other common mortgage risk indicators like the Price-

to-Income (PTI), Debt-Service-to-Income (DSTI), or Payment-to-Income (PTI) ratio.

10 Further references on this self-regulation are available in the Appendix II.

10

the liability substitution imposed by the CCyB should not affect the bank’s total funding costs.11

However, if the Modigliani and Miller (1985) theorem fails, the bank has to bear the difference in

terms of funding costs. In our example, we thus multiply the extra capital requirement of CHF 4,000

with this cost differential, denoted as X. If that cost differential amounts to, for example, 10%, then the

CCyB will on average imply additional capital-related costs of CHF 400, or 4 basis points when set in

proportion to the requested total mortgage amount.12

2.3 Literature related to the CCyB

As Switzerland was the first country to activate the CCyB, empirical evidence on its immediate impact

and longer-term adjustment patterns is very scarce. A related stream of the literature investigates other

policy measures that share some specific features with the CCyB. Aiyar et al (2014a) evaluate the

effects of bank-specific capital requirements in the UK that used to vary counter-cyclically under Basel

I. They point out that, if there exists a set of lenders to whom such requirements do not apply, “policy

leakage” effects might ensue, which may defeat the purpose of countercyclical capital requirements.

The authors also find that the effectiveness of countercyclical capital requirements depends on banks’

existing levels of capitalization. In a parallel paper, Aiyar et al (2014b) study how shocks to minimum

capital requirements are transmitted internationally and they find a significantly negative effect on

cross-border lending. By contrast, Jiménez et al (2016) evaluate the effects of “dynamic provisioning”

– a measure introduced by the Spanish regulator in 2000.13 Using observations at the bank-loan-firm

11 Junge and Kugler (2013) find, for a sample of five publicly listed Swiss banks, that the elasticity between a bank’s leverage and its CAPM-β is

about 55% of what it would be if the Modigliani-Miller theorem did fully hold. Furthermore, in their analysis of the extra costs of Basel III, they

estimate a cost difference of 4.66% using the annual return of the Swiss SPI stock market index and the 12-month CHF LIBOR rate for 1990–2010.

12 While not relevant in the present case of a relatively small increase in capital requirements, in general X is possibly endogenous in that a stronger

capitalisation level will tend to reduce the bank’s overall risk profile and, hence, reduce the cost of other funding sources.

13 Crowe et al (2011) point out that countercyclical provisioning differs from countercyclical capital requirements in that provisioning requirements

can be binding also when banks are already better capitalized than required by regulators.

11

level, the authors analyze the impact of these provisions on bank lending to firms. They find that the

counter-cyclical provisioning rules did indeed help to smooth the Spanish credit cycle, even though

they failed to avert the build-up of vulnerabilities in the property sector. More recently, Auer and

Ongena (2016) also analyze effects of the CCyB in Switzerland. In distinct from our paper which is

focused on mortgage lending, they examine the impact on commercial lending, which was not

subjected to the CCyB and find some evidence of an increase in such lending.

Our paper also relates to the more general literature on the nexus between bank capitalization and bank

lending. On the theory side, Boot et al (1993), Sharpe (1990), and Diamond and Rajan (2000) develop

models that examine how changes to equity capital should affect bank lending. Gersbach and Rochet

(2012), in turn, show that the volatility of lending can be reduced by requiring higher capital ratios in

boom times. With respect to the regulatory framework, Repullo and Suarez (2004) investigate how the

transition from Basel I to Basel II translates into changes in a theoretical loan pricing equation. On the

empirical side, Kishan and Opiela (2000) stress that the degree of capitalization matters in that small

and less well capitalized banks respond most strongly to monetary policy. The impact of capital

cushions or “excess capitalization” is also investigated by Gambacorta and Mistrulli (2004 and 2014).

More specifically on the effects of regulatory capital requirements, several papers conduct mostly

accounting-based quantitative impact studies (QIS) on the effect of capital requirements on loan

pricing. These include King (2010), Cosimano and Hakura (2011) and Hanson et al (2011). Demir et

al (2014) find that the introduction of the Basel II standardized approach to risk weights in Turkey

affected real activity in the economy.

2.4 Hypotheses on the Effects of the CCyB

There are several possibilities for a bank to adjust to the CCyB’s additional capital requirements, both

over the short-term and over the longer term. Beyond the regulatory capital standards, Berger et al

(2008) present evidence that banks put aside so-called capital cushions which vary along the individual

12

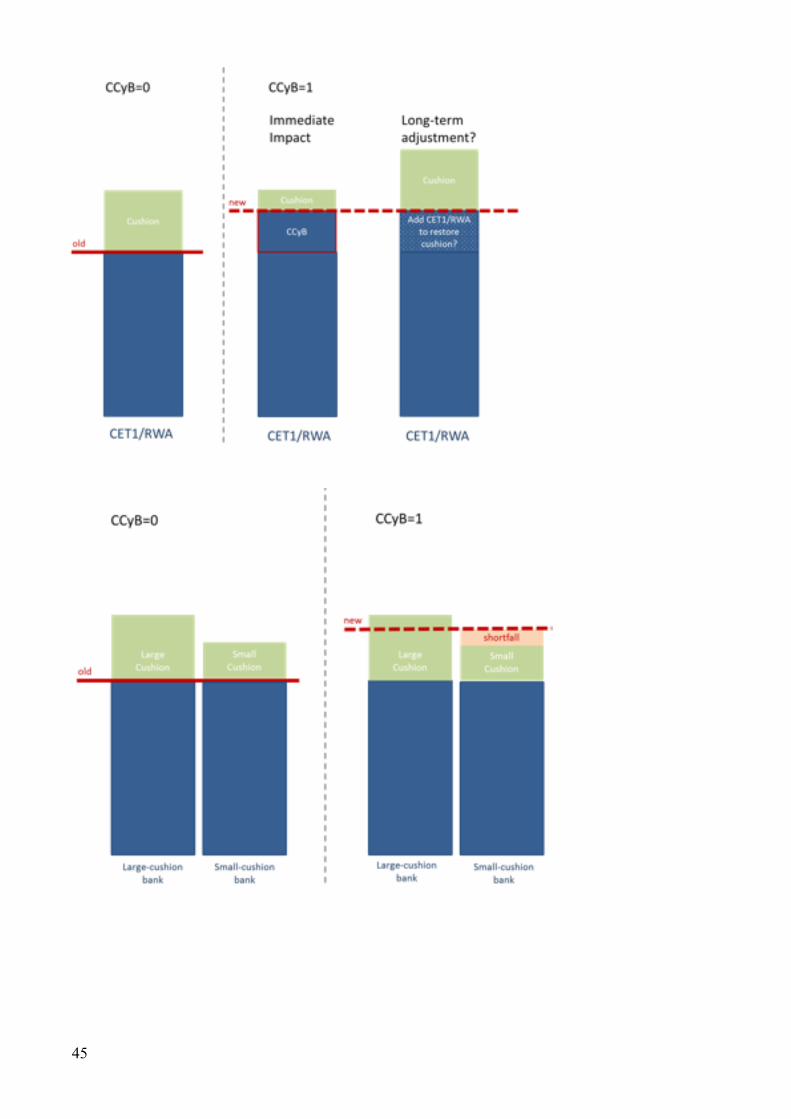

bank’s risk preferences.14 Figure 5 illustrates these cushions for the pre- and the post-activation

periods. As an immediate effect, the CCyB activation shrinks the capital cushion and banks might

either prefer to accept a lower level in the long run, or restore the cushion over time.

To restore the cushion after the CCyB activation has consumed part of it, a bank can either target the

numerator of the envisaged new capital ratio by raising capital, or the denominator by constraining

the growth of its RWAs, or both, see Aiyar et al (2014)

The focus of our short-term analyses is on how banks adjust their mortgage supply. By rejecting more

applications, a bank can shrink the denominator. By raising prices, a bank can simultaneously gear the

numerator and denominator of its capital ratio: On the one hand, higher prices might (the more, the

less elastic demand) enable the bank to boost retained earnings and thereby to strengthen its capital

basis. On the other hand, higher prices might constrain new mortgage issuance (the more, the more

elastic demand).

The size of the cushion before higher capital requiments come into force matters. A bank which had

maintained a lower capital cushion might even see a capital shortfall if the additional capital

requirements imposed by the CCyB exceeded its cushion. Figure 6 reflects this situation for low-

cushion banks and their need to raise capital urgently.

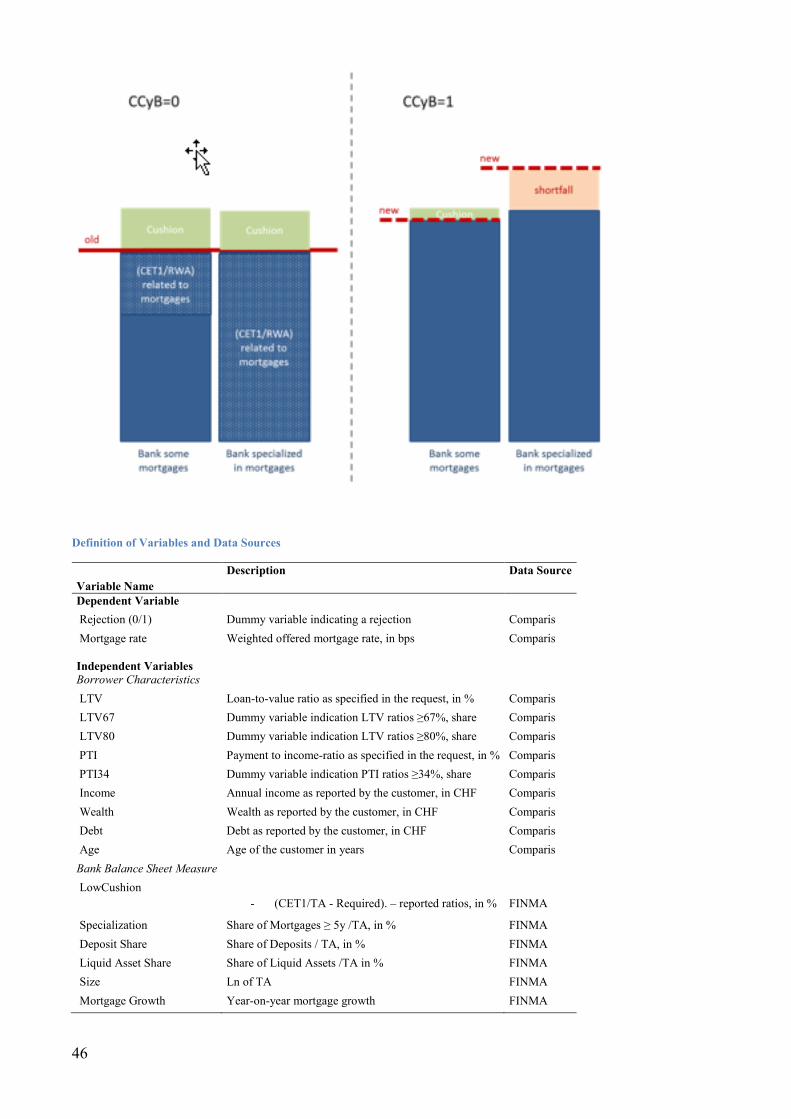

The CCyB applies to both the stock of outstanding mortgages and new mortgage lending. For those

banks which operate a very mortgage-specialized business model, the CCyB implies a higher burden

in terms of additional capital requirements. Figure 7 shows that a higher burden absorbs more of the

potential capital cushion. Mortgages with longer remaining maturities will require relatively more

capital, for even longer time horizons which renders them even more costly. As rates on existing

14 Similar results are obtained for European banks by Jokipii and Milne (2011). They speak of “capital buffers”, while Berger et al speak of

“capital cushions” and Gambacorta and Mistrulli (2004) speak of “excess capital”. We follow Berger et al and speak of “capital cushions”.

13

mortgages cannot be adjusted,15 we expect that banks with a very mortgage-intensive business model

raise prices on new lending even more in order to cross-subsidize outstanding mortgages by passing

on the burden to new customers. The extent to which such cross-subsidization can be realized, depends

on the effective elasticity of the demand function faced by the individual bank. We hence hypothesize

that

Hypothesis 1

Banks that exhibit balance sheet characteristics that render them more sensitive to the regulatory

design of the CCyB, raise their mortgage rates relatively more in response to the CCyB’s tighter

capital requirements than their competitors. In particular,

a. relatively more capital-constrained banks with lower capital cushions and

b. banks which are relatively more specialized in the mortgage business, listing a higher stock

of outstanding mortgages with long-term remaining maturities on their balance sheets

… charge higher rates after the CCyB activation.

Furthermore, the additional CCyB-related capital requirements are determined by their stock of risk-

weighted domestic residential mortgages. Figure 7 illustrates how risk-weighting schemes translate the

individual customer’s loan-to-value (LTV) ratio, the credit risk of a borrower, into capital requirements

for a bank and thereby link the underlying borrower risk of a mortgage to the CCyB.16 In this way,

15 While some banks in Switzerland stipulate in loan contracts that they are also entitled to adjust fixed rates when regulatory costs change, doing

so in practice is reported to be difficult for reputational reasons.

16 Basel II implied a default risk weight of 35% for residential mortgages given “strict prudential lending standards” and mandated national authorities

to impose higher risk weights when such standards were not met. The risk-weighting scheme illustrated in Figure 3 reflects the Swiss

implementation of those more general principles applicable during our sample period. For details, see FINMA (2013a).

14

risk-weighting schemes put an extra capital levy on mortgages with LTV ratios equal to or above 67%,

and again on those with LTV ratios equal to or above 80%. We expect banks to claim extra

compensation for granting these more capital-consuming mortgages and even more so after the CCyB

imposes higher capital standards.17 This leads to our second hypothesis on the characteristics of

mortgage applicants.

Hypothesis 2

Risk-weighting schemes that are linked to the LTV ratio of a mortgage amplify the CCyB effect and

might trigger a relatively larger increase in mortgage rates for potential borrowers

with LTV ratios equal to or above 67%

and a yet larger increase for LTV ratios equal to or above 80%.

The focus of our longer-term analyses is on how banks adjust their capitalization, asset portfolio and

overall balance sheet structure in order to comply with the new overall capital requiments including

the CCyB. Higher rejection rates and higher prices will lower the pace of mortgage growth on bank

balance sheets. In the context of the Swiss mortgage market, this speaks to the “leaning against the

financial cycle”. Overall, mortgage lending might even decline and, thereby reduce the amount of risk-

weighted assets, and maybe even total assets at the bank-level, when keeping other asset classes

unchanged. The effects might again be stronger for banks with lower initial capital cushions and banks

with a specialization in the mortgage business. We hence expect that:

17 Higher credit risk is also implied by higher Price-To-Income (PTI) ratios. In our regressions, we implicitly control for PTI ratios.

15

Hypothesis 3

In the longer-term adjustment process, the response-level responses listed in Hypothesis 1 will

translate into changes on bank balance sheets. In this line of argument,

a. relatively more capital-constrained banks with lower capital cushions, and

b. banks which are relatively more specialized in the mortgage business, listing a higher stock

of outstanding mortgages with long-term remaining maturities

… will slow down their mortgage growth relatively more.

If banks succed in charging higher rates and passing on their burden to the customer, banks can

strenghten their capital basis by higher retained earnings. Raising corporate capital is more time

consuming and less likely to happen in the course of the subsequent months. Further, existing

shareholders prefer not to see the value of their shares decline by the bank issuing new shares. If all

banks adjust to the new capital standards including the CCyB by restoring their capital cushions, the

overall banking system will become more resilient and the first objective of the CCyB would be

achived. We hypothesize that

Hypothesis 4

Banks will strenghten their capital basis and restore their capital cushions in response to the CCyB.

As raising corporate capital is unlikely to happen over a few months, banks will most likely resort to

their accumulated profits or retained earnings to raise capital. Again the effect will be stronger for

those banks which had reported lower capital cushions and operated a more mortgage-focused

business model in the pre-activation period.

16

3 Short-term mortgage market response to the CCyB activation

3.1 Data

Unique features of the Comparis mortgage market dataset and bank characteristics

Our data on mortgage applications and bank responses were provided by the Swiss online platform

Comparis.ch. Comparis is a comparison website for various financial services including bank products,

health insurance plans, real estate markets and tax advice. Between 2008 and 2013, Comparis operated

a mortgage brokerage that allowed households to submit personalized mortgage applications in order

to receive different binding quotes from participating lenders.18 To access the service and compare

offers, customers paid CHF 148 (about USD 150) and gave comprehensive information on the property

to be bought, the requested mortgage amount, the desired maturity model, household finances, and

personal details such as their age. Comparis then sent the anonymized request to different lenders,

including banks from all major banking groups, except for the two big banks UBS and Credit Suisse

(CS).1920 After having assessed the customer’s financial situation, mortgage lenders decided whether

to make a binding offer and at which mortgage rate and conditions. While banks were allowed to split

the mortgage into different tranches with tranche-specific rates, they were not allowed to deviate from

the requested amount in total.

The Comparis dataset forms the backbone of our paper and it has several remarkable features that suit

our empirical approach. First, it allows us to disentangle mortgage demand and supply, as we observe

how different banks respond to the same mortgage application with customer-specific features. Such

18 Comparis has changed its mortgage platform and business model significantly in late 2013. Since then, customers pre-select from a list of lenders

and discuss their needs with an advisor before receiving offers from different lenders. The period for which we have data ends with the end of the previous business model on October 24, 2013.

19 UBS and CS are also the only ones computing their risk weights with the Internal Ratings Based (IRB) approach rather than the Standardized

Approach (SA), which has changed during the sample period. All other banks in our sample homogeneously use the SA.

20 Three insurance companies also offered mortgages via Comparis. We do not include them in this analysis, as we lack information on their

balance sheets.

17

a comparison of multiple lenders per borrower is typically available from the syndicated loan market

for corporate or interbank lending, or if a country maintains a credit register. Those datasets provide

information on contracted loans, whereas our data is collected at the application-response-level, hence,

before signing a mortgage contract. As Comparis sent the customer-specific data to all participating

lenders without asking for a deliberate choice by applicants, we can rule out any potential self-selection

of customers into different types of banks. Second, we are able to observe both the willingness to make

a loan (like Jiménez et al, 2012) and comprehensive details on the pricing of the mortgage including

tranche-specific rates by maturity and borrower risk as assessed by the potential lender. Third, all

lenders receive the same anonymized information, which rules out that they could take advantage of

additional soft information, considerations of relationship lending or cross-selling of products.

Furthermore, we observe exactly the same set of detailed information that banks receive, so banks

cannot act on any information that we would not be able to control for. Fourth, lenders do neither know

which competitors are participating, nor which rates they are offering. These features warrant that

lenders submit binding, independent offers that truly reflect their eagerness to bid for the mortgage.

Fifth, the customer incurs a fee on submitting his application and, as offers are binding conditional on

verifiable information, they have an incentive to submit correct information.

Bank-level data for participating banks

We complement the Comparis dataset with supervisory reports from the Swiss Financial Market

Supervisory Authority (FINMA). Bank-level data of the 21 participating lenders help us to analyze

how their CCyB response in the mortgage market varies with their reported capitalization, their asset

portfolio and other balance sheet characteristics before the activation. To measure capitalization, we

focus on Core Equity Tier 1 (CET 1) as a percentage of risk-weighted assets (RWA). Specifically, our

empirical analysis draws on the “capital cushion”, defined as the reported level of capital

(CET1/RWA) that a bank holds in excess of the regulatory requirements to be fulfilled by the end of

the Basel III transition period. As a measure of mortgage market specialization, we use the share of

18

mortgages with a remaining maturity of at least 5 years relative to a bank’s total assets. To isolate the

effects of capitalization and specialization, we control for other time-varying balance sheet

characteristics like the banks’ funding model, liquidity, size and recent month-on-month mortgage

growth.

Demand and Supply before and after the CCyB Activation

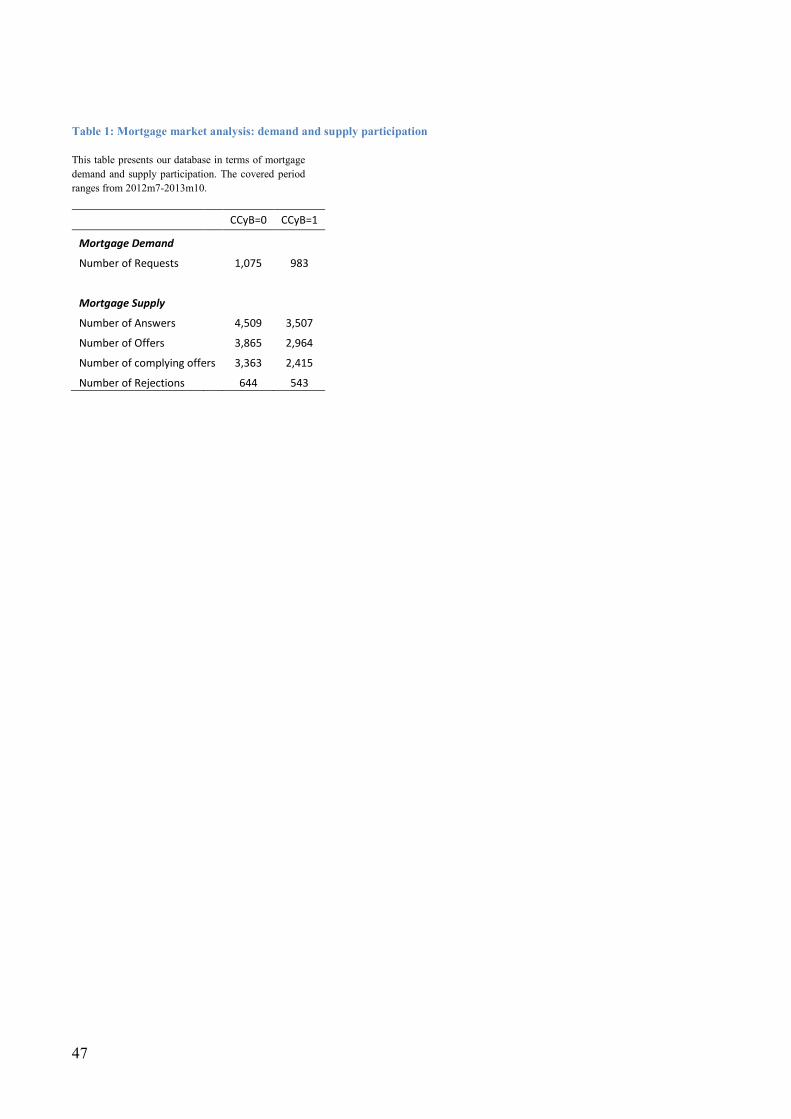

Table 1 introduces our Comparis dataset in terms of demand and supply. The first column refers to the

period CCyB=0 starting on July 1, 2012, while the second column ranges from the activation of the

CCyB on February 13, 2012, until the end of our sample on October 24, 2013 (CCyB=1). Our data on

mortgage demand shows that the number of applications per months remains relatively constant over

both periods. Turning to mortgage supply, Table 1 shows that customers receive on average 4.2

(=4509/1075) answers in the period before the CCyB activation and 3.6 (=3507/983) answers after it.

More importantly, the shares of offers and rejections relative to the total number of answers is almost

stable. On average, 86% of all received responses are offers before the activation of the CCyB and

85% after it. This mitigates potential selection concerns in that banks might constrain their lending by

rejecting more applications after the CCyB went into force. We will return to various types of potential

selection biases below.

The structure of our dataset is unique in that it allows us to follow a very clean identification strategy

at the mortgage-response-level. Unfortunately, we cannot observe which offer the customer ultimately

chooses and hence, we can only draw inferences on new mortgage lending based on the cheapest

quotes that the customer is most likely to accept. The question then arises whether this dataset is

actually representative of the entire Swiss mortgage market. In Section 4, we examine how banks

adjust their capitalization, mortgage lending and overall balance sheet structure in the longer run. It

draws on the full sample of all banks chartered in Switzerland and provides findings that are consistent

with our short-term mortgage market response based on a subsample of the banking population.

19

Further, Appendix II offers a host of comparisons and tests based on publicly available statistics on

the entire Swiss mortgage market. These analyses confirm that the data are representative, both in

terms of the mortgage demand (geographical distribution, borrower risk, etc.) and supply.

One might also raise the concern that the CCyB impacts mortgage demand and supply in terms of the

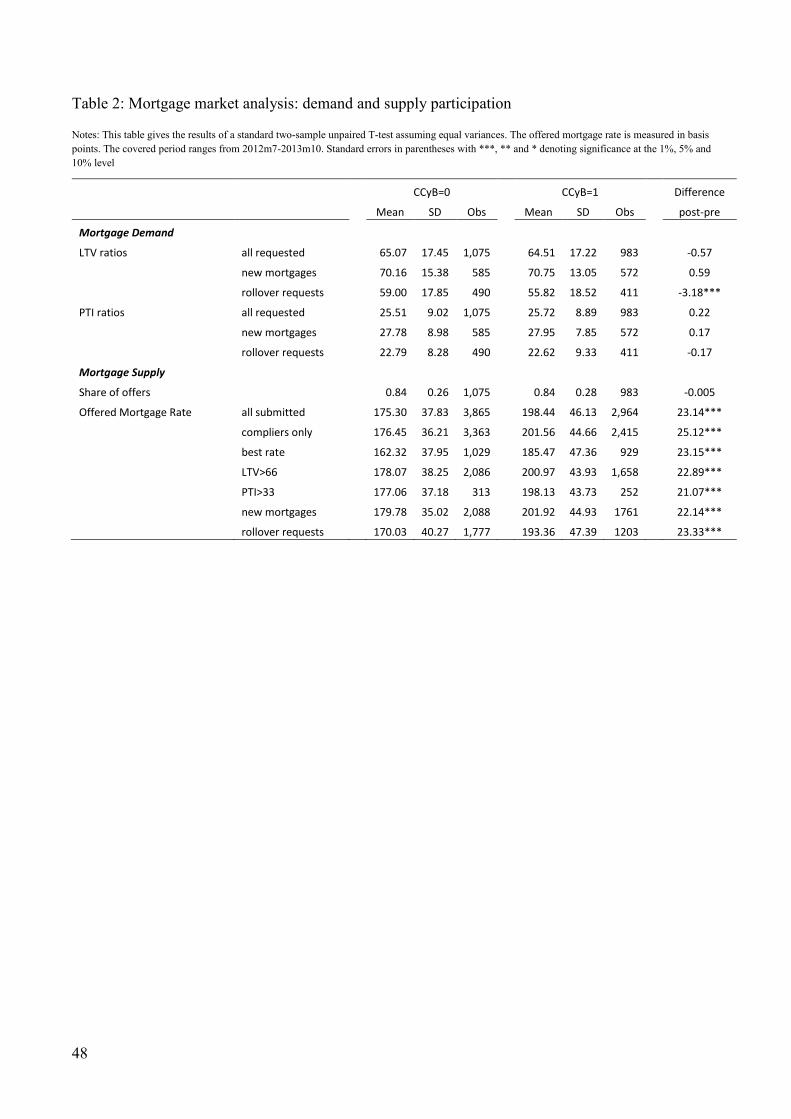

submitted and accepted borrower risk profiles. As a simple first step, Table 2 presents simple T-tests

to address this issue. With respect to mortgage demand, customers might expect banks to reject more

requests with high loan-to-value (LTV) ratios and therefore shy away from requesting riskier

mortgages in the first place. If that was the case, our analyses of mortgage rates might suffer from a

selection bias, as fewer risky mortgages would enter the sample after the CCyB activation. The

Mortgage Demand panel of Table 2 shows that in the full sample, neither applicants’ LTV nor PTI

ratios change significantly across periods. We then split our sample into customers asking for a new

mortgage and customers requesting to roll over their outstanding mortgage with a new bank. Our

results suggest that there is no significant difference in the borrower risks profiles for new customers.

Only the requested LTV ratios for rollover requests decline slightly after the activation of the CCyB.

For this reason, our more sophisticated empirical analysis in Section 3 will distinguish between

rollover and new mortgage applications and control for different types of borrower risk.

With respect to mortgage supply, the second panel of Table 2 confirms our previous finding that the

share of offers remains constant over timer. We conclude that banks do not constrain lending by

rejecting more applications. We infer from this finding, that any CCyB effect should operate through

the pricing of mortgages. The remainder of Table 2 provides evidence for these significant differences

in the pricing of all mortgages across activation periods. However, simple t-tests can neither

accommodate the complexity of our mortgage pricing data, nor can they account for any concomitant

macro factors. The next sub-sections offers more sophisticated regression specifications to gain more

detailed insights.

20

3.2 Empirical Analysis: Which banks are most sensitive to the CCyB activation?

Empirical Strategy

Equation (2) describes our regression specification. We first use a binary rejection indicator as

response variable, and then turn to the tranche-weighted21 mortgage rate offered by bank j to requesting

borrower i in month t.

ijttjittjtjijt CONTFECCyBSENSSENSresponse 1,

'

1,

'

1,

'

1 * (2)

More specifically, 1, tjSENS denotes a 2×1-vector which captures our continuous sensitivity measures

of low excess capitalization 1, tjLowCushion , and specialization in the mortgage business

1, tjtionSpecializa . We further add their interaction effects with the CCyB shock dummy, assuming

the value of 1 after the activation day (February 12, 2013) and zero otherwise. Other standard balance

sheet characteristics, in particular the share of deposits and liquid assets, bank size and mortgage

growth, enter equation (2) via 1, tjCONT , denoting a 4×1 vector to control for time-varying

heterogeneity among banks. To mitigate endogeneity concerns, we use these bank control variables

with a time lag based on the respective bank’s FINMA report of the previous month t-1. We let request

fixed effects itFE enter our specification (see Khwaja and Mian, 2008) to absorb any borrower

characteristics. As each request i appears only once in our dataset, it pertains to a unique point in time

and thereby picks up any time-specific, macroeconomic development (see Aiyar et al, 2014b).

21 While banks cannot deviate from the requested mortgage amount, they have the possibility to slice the offer into (up to three) tranches which

might carry different mortgage rates. To render offers comparable, we use the share of each tranche in the composite mortgage offer to weight

tranche-specific mortgage rates and compute their weighted average.

21

Standard errors are clustered by bank and activation period to obtain a reasonable number of clusters

with a relatively balanced number of observations per cluster.22,23

Capital-Constrained Banks with low capital cushions (Hypothesis 1a)

First, we examine the role of low capital cushions, defined as the negative, percentage point deviation

of a bank’s reported capital ratio (total capital as a percentage of risk-weighted assets) from the capital

ratio below which the supervisor would intervene.24 ,25, Banks with more comfortable capital cushions

dispose of more degrees of freedom, but they might also charge higher prices to preserve their

cushions. On the flip side, banks with lower capital cushions might pursue more aggressive pricing

strategies 01 . Yet, once the CCyB imposes an additional capital charge, these banks become

relatively more constrained, and for this reason, they might reject more mortgage applications. In case

of submitting an offer, we assume that banks with lower capital cushions most likely charge higher

rates as a compensation for granting a mortgage 01 in an attempt to boost their profits and

ultimately to bolster their capital position.

Specialized banks with mortgage-intensive business models (Hypothesis 1b)

Specialization in the mortgage business, defined as the total asset share of mortgages with a remaining

maturity of 5 years and beyond, might render a bank more sensitive to the CCyB’s particular Swiss

design. These banks benefit from economies of scale and they might pass on part of those to their

customers by charging lower mortgage rates 02 , on average. Another possibility might be that

22 See Wooldridge (2003) or Petersen (2009) for a general discussion on the computation of standard errors in finance panel datasets.

23 As a robustness check, we use robust standard errors and cluster them by request. Our results remain virtually unaffected.

24 As distinct from the previous section and Figures 5-7, we believe that it is more intuitive to use the “low capital cushion” measure, inversely

defined, as this suits the idea that more capital-constrained banks charge higher prices.

25 The intervention threshold in Switzerland differs across five risk categories, into which the supervisor has allocated banks depending on amongst

others a bank’s total assets.

22

they lack diversification and hence add a premium to their mortgage rates in which case we might find

that 02 . After the activation, we expect more specialized banks to reject more applications, as

the CCyB applies to all residential mortgages listed on balance sheets. Given that specialized banks

submit an offer, they most likely raise their rates substantially 02 as their mortgage portfolio

consumes a higher share of their capital.

Descriptive Statistics

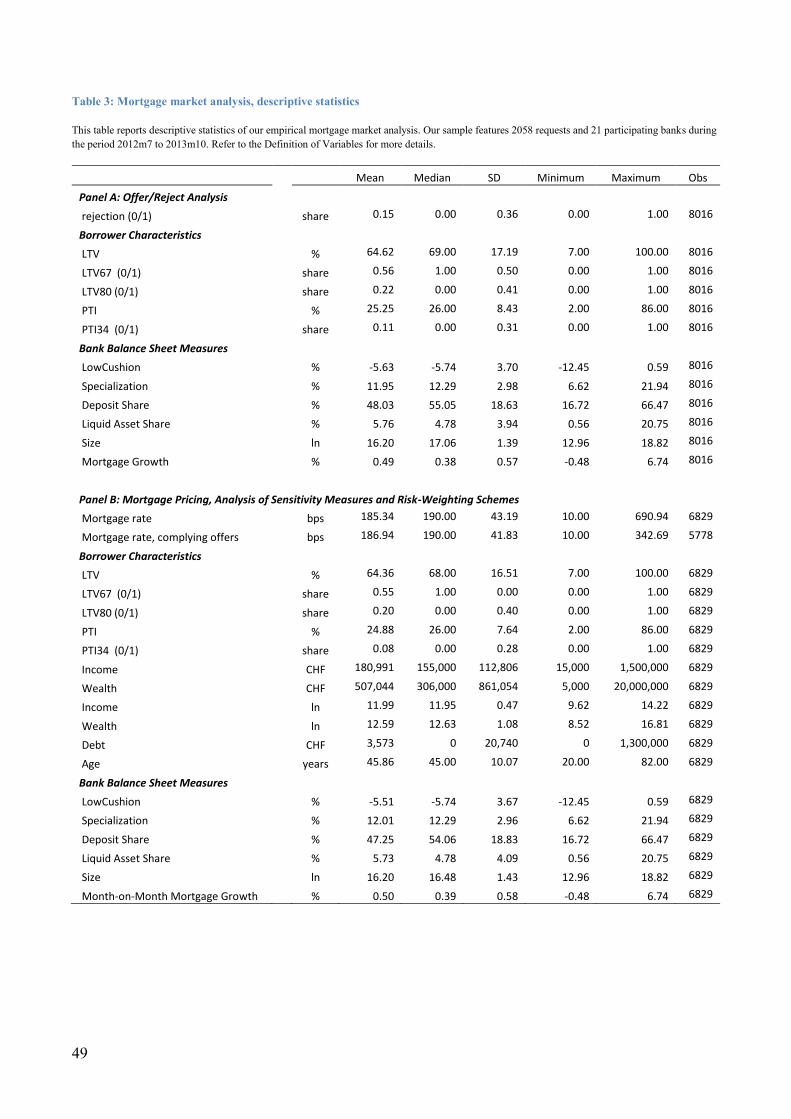

Table 3 reports the descriptive statistics for the Comparis estimation sample. Panel A refers to our

binary rejection analysis, while Panel B draws on the analysis of mortgage pricing. A difference in the

number of observations emerges from the fact that we drop all rejections in Panel B. This might also

give rise to a slightly different weighting scheme of borrower and lender characteristics when

computing summary statistics. The average LTV ratio hovers around 64% in both panels. About 55% of

all submitted LTV ratios in Panel A (and 56% in Panel B) equal to or exceed 66%. The average offer is

sent to an applicant aged about 46 years, who reports an average annual household income of CHF 181,000

(about USD 181,000) and average household wealth, including retirement savings, worth about CHF

507,000 (about USD 507,000). With respect to the participating bank’s balance sheet setup, Panel A and B

reveal hardly any difference. Banks set aside capital cushions between 0.5% and 12% of risk-weighted

assets during the sample period. Our measure of bank specialization in the mortgage business, the

outstanding stock of mortgages with residual maturity of 5 years or longer, ranges between 7 % and 22%

of total assets.

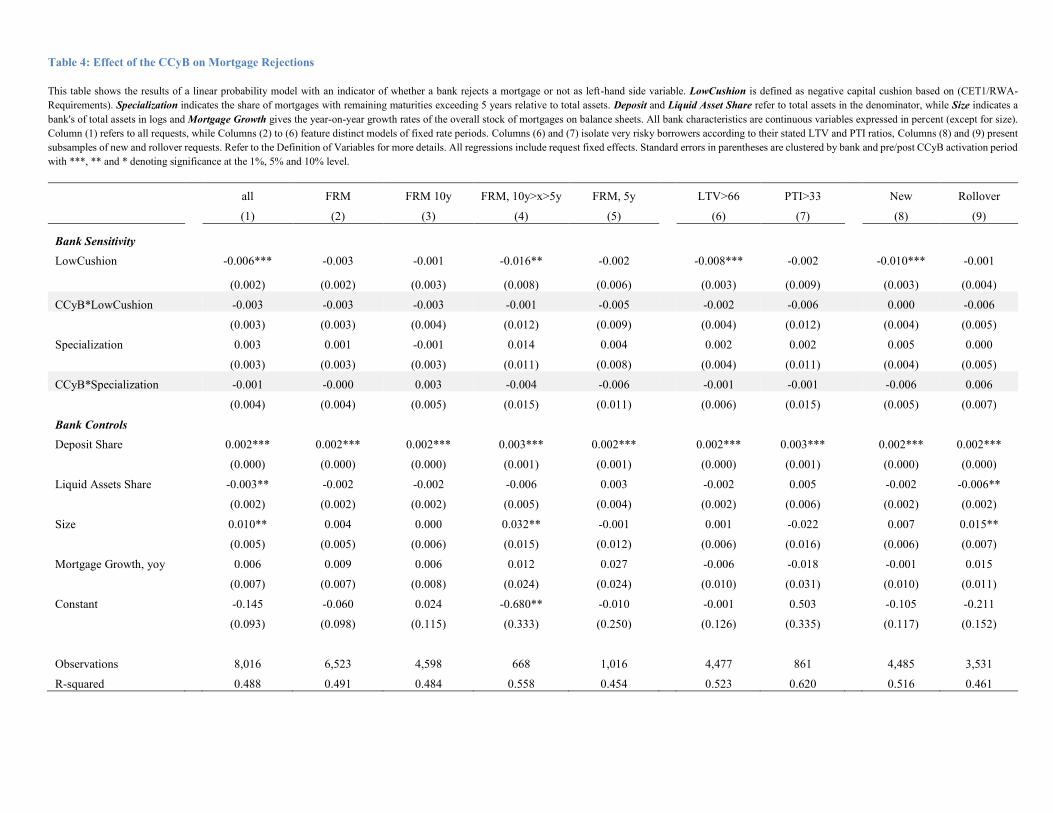

Bank Sensitivity Measures: Results

Table 4 tells us whether more sensitive banks reject more applications after the CCyB activation, while

Tables 5 and 6 analyze their pricing behavior to provide formal tests of Hypotheses 1a and 1b. In each

table, Column 1 refers to the full sample of mortgage requests, Columns 2-5 isolate requested fixed

rate mortgages (FRMs) with Columns 3- 5, in turn, splitting those by distinct requested fixed term

23

maturities26 spanning 10 years, 5 to 10 years, and 5 years. According to the information provided by

the applicant, Columns 6 and 7 distinguish between different types of borrower risk, and Columns 8

and 9 separate requests for new mortgages from rollover requests.

Our results in Table 4 suggest that banks with a lower capital cushion are less likely to reject a mortgage

in general, however this equally holds before and after the CCyB activation. Sample splits reveal that

this result is driven by medium-term maturity mortgages, mortgages with higher credit risk and new

mortgage applications. Table 4 further suggests that the degree of bank specialization in the mortgage

business does not shape its accept-reject decision – again, independent from the period under

consideration. These results align well with Edelberg (2006) in that banks prefer to attract or discard

a customer along the price dimension rather than by sending outright rejections. As Table 4 does not

provide any evidence for a change in the rejection behavior over time, we can safely refute any

concerns about selection biases and proceed to the analysis of mortgage pricing.

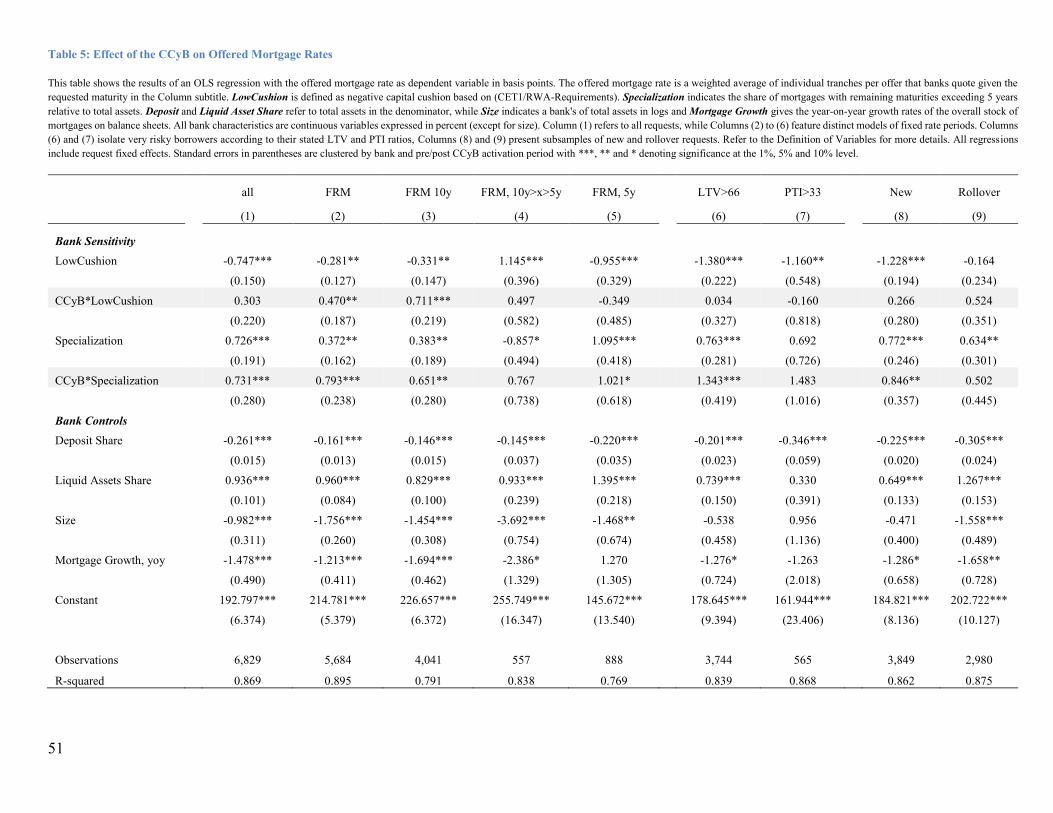

Our results in Table 5 point out that more capital-constrained banks with lower capital cushions raise

their rates relatively more after the CCyB than their less constrained peers. Fixed rate mortgage (FRM)

models, while accounting for more than 80% of all our observations, especially those with a 10y

maturity (making up almost 60% of the entire sample), drive this result. After the CCyB activation,

banks with lower capital cushions charge on average 72 bps more for a 10y fixed rate mortgage which

reflects their tradeoff between hitting the now even closer capital requirement threshold and reaping

additional profits. Before the activation period, Table 5 shows that less well capitalized banks had on

average submitted cheaper offers. Remarkably, we do not find a significant interaction effect for the

sub-sample of requests with higher LTV ratios or credit risk, as the risk-weighting schemes for those

26 This list of mortgage models that customers can request is not exhaustive. Fixed rate mortgages are available for each annual maturity between 1

and 10 years apart from different models of adjustable rate maturities. We focus on longer-term fixed rate models here as we expect an

immediate effect on the bank’s rejection and pricing behavior to be observable as those mortgages would be part of their balance sheet after the

transition period ending in September 2013 and the CCyB becomes binding. Columns 6 -10 refer to all mortgage maturity models.

24

mortgages impose an even higher capital surcharge. Section 3.4 provides a more detailed analysis of

how the risk-weighting schemes might amplify the CCyB effect.

Our findings also show that banks that are more specialized in the mortgage business raise their

mortgage rates after the CCyB activation by on average 73 bps in the full sample, and about 79 bps for

the most populated category of FRMs. Longer maturities, mortgage requests with higher LTV ratios

and new mortgage applications stand behind this finding. As the CCyB’s higher capital requirements

force banks to hold more equity capital for the total stock of mortgages already on their balance sheets,

apparently, specialized banks pass on this higher burden to their new customers, especially to those

requesting longer fixation periods and those being perceived as more risky borrowers.27 One might

interpret this as the bank’s attempt to blend the capital surcharge with higher term and risk premiums.

While higher risk premiums might serve as a reasonable explanation due to the risk-weighting schemes

(see Section 2), the temporary design of the CCyB does not justify the higher term premiums for 10y

FRMs. Further, as 10y FRM are the most common type of mortgages in Switzerland, competition

should be fiercest which renders this finding very interesting in that banks try to pass on their burden

in the most liquid and deepest market segment. The specialized indicator is mostly positive and

significant on a standalone basis, suggesting that more specialized banks charge higher mortgage rates

on average, possibly due to their expertise and lack of risk diversification.

The coefficient estimates on our control variable yield reasonable results and thus lend support to our

specification. More traditional banks with a higher share of deposit funding submit cheaper mortgage

rates, and so do larger banks with potential economies of scale. Banks with more liquid assets are on

average perceived as more risk averse or cautious and hence demand higher prices. Banks which have

expanded their mortgage portfolio at faster pace over the previous year seem to continue following

27 This behavior is in line with the observation made by SNB (2015) that the asset margin on new mortgages was also banks’ adjustment margin of

choice in response to the falling liability margins brought about by ultra-low interest rates in 2014 and 2015.

25

that strategy by underbidding their competitors’ prices. A robustness check below discusses whether

these expansionary banks switch strategies after the CCyB activation.

In brief, we find evidence consistent with Hypotheses 1a and 1b that capital-constrained as well as

mortgage-specialized banks raise their mortgage rates relatively more. We infer that the composition

of mortgage supply changes in that banks with a higher exposure to the CCyB’s regulatory design

substantially adjust their mortgage pricing. We highlight these two results as core findings of our paper.

Robustness Checks

As a first robustness check, we restrict our sample to those mortgage offers that fully comply with the

requested mortgage maturity model. Banks might deviate from the specified request along several

dimensions. We hence need to justify that our distinct approach by using a weighted-average mortgage

rate, by adding request fixed effects and by the specific set of bank control variables yields reliable

results while taking all those dimensions into account. If a strict subsample of only complying offers

produces very similar results, we claim that our baseline setup does not suffer from an omitted variable

or any other type of biases that tilt our coefficient estimates and pick up any other then the specified

factors. Table 6 replicates our previous analysis on how bank sensitivity measures interact with the

CCyB activation based on this subset of fully compliant offers. Again, we find that banks with a lower

capital cushion and higher degrees of specialization raise their mortgage rate after the activation, albeit

the surcharge appears to be a bit lower than in the set of baseline results displayed by Table 5. Further,

coefficient estimates based on different subsamples closely match our baseline findings in terms of

overall sign and significance.

As a second robustness challenge, we check whether the change in mortgage pricing merely reflects a

reversal of expansionary plans rather than the impact of a macroprudential policy tool. As the CCyB

also applies to the stock of outstanding mortgages already on the balance sheet, but does not explicitly

depend on recent growth rates, the pace of a bank’s mortgage growth investment should not interact

26

with the CCyB effect per se. We would expect that banks pursuing an ambitious mortgage growth

strategy submit cheaper rates 0m on average. However, if at some point in time they decide to

reverse their strategy, we might see the overall price effect losing its significance or switching signs

(if the interaction effect was positive and significant, we would use an F-test to assess the overall

pricing effect as the sum of standalone plus the interaction coefficients: mm ). Our empirical tests,

however, reveal that banks exhibiting strong mortgage growth do not scale back their expansion plans

after the CCyB’s activation. We hence conclude that our baseline coefficient estimates reflect a policy

implication instead of accidentally picking up a concomitant reversal in business strategies.

3.4 Empirical Analysis: Do risk-weighting schemes amplify the CCyB?

To examine the impact of risk-weighting schemes before and after the CCyB activation, we focus on

the credit risk risk premium associated with loan-to-value (LTV) ratios and potentially amplifying the

CCyB effect.

ijtjtiitii

iiiii

ijt

FECustContrefinptiCCyBptipti

ltvCCyBltvCCyBltvltvltv

rate

'33*33

8067*8067

2120222221

13121312112 (3)

In line with equation (3), we regress the tranche-weighted mortgage rate ijrate offered by bank j to

requesting customer i in month t on the customer-specific, continuous LTV ratio, two dummies ltv67

and ltv80 indicating whether this LTV ratio equals or exceeds 67% or 80%, respectively, and we add

their interactions with the CCyB activation indicator. Due to the higher credit risk and risk weights, we

expect that banks charge a linear credit risk premium 011 . Further, the two kinks generated by

risk weighting schemes in Figure 7 suggests that banks put an extra levy on LTV ratios which equal

or exceed 67% and 80% 0,0 1312 , respectively. After the activation of the CCyB, very high

LTV mortgages consume even more of the equity capital. For this reason, we assume that banks expand

27

these levies after the CCyB shock, as they require extra compensation for the additional capital that

they have to hold 0,0 1312

To control for a second, different type of customer risk, the payments-to-income (PTI) ratio enters as

a continuous ( ipti ) and a dummy ( ipti33 ) variable. Typically, banks perceive PTI ratios equal to or

exceeding 33% as risky since these households might struggle to meet their monthly installments. Most

notably, PTI ratios reflecting debt service risks are not subject to any capital requirements or risk-

weighting schemes28 and should hence not interact with the CCyB activation.

To account for contemporaneous refinancing conditions and other macroeconomic factors, we include

the tranche-weighted swap rate ( irefin ) that prevails when customer i submits her request. Vector

iCustCon captures further individual customer data such as income, wealth, debt and age. We include

bank-by-month fixed effects to control for time-varying bank characteristics and cluster standard errors

by bank-activation period to render our estimates robust to serial correlation and a regime-change.

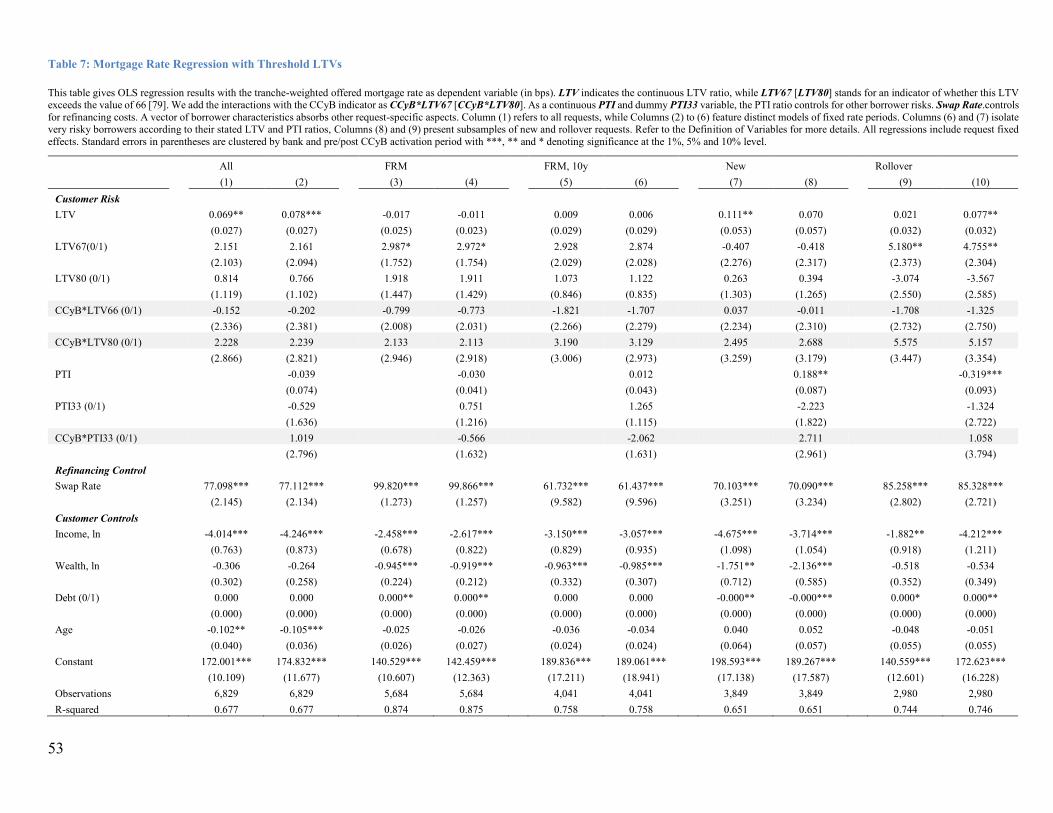

Risk-Weighting Schemes: Results

Table 7 presents our results, while distinguishing between different maturity subsamples (Columns 3-

6) and separating new (Columns 7-8) from rollover applications (Columns 9-10). We find that banks

charge higher rates for higher LTV ratios, denoting a credit risk premium. In the full sample (Column

1), the linear LTV effect turns out to be significant, while subsample splits isolating FRMs and rollover

requests reveal a non-linear extra premium. Our estimates suggest that banks impose an extra levy of

about 3 bps on FRMs and 5 bps on rollover mortgages, on average, for LTV ratios29 equal to or

28 Banks in our sample follow the Standard Approach when calculating risk weights. Please look at Section X for further details.

29 As the average LTV ratio is lower for rollover mortgages, those with very high LTV ratios stand out and seem to be perceived as particularly

risky by banks.

28

exceeding 66%. These coefficient estimates reflect the first kink at LTV ratios of 66%, associated with

risk-weighting schemes and additional capital requirements in Figure 7. The second kink at 80% turns

out to be insignificant.

Most central to the risk-weighting schemes, we find that the interaction effects of the CCyB activation

dummy with LTV indicators turn out to be insignificant which shows that risk-weighting schemes do

not amplify the CCyB effect. This result holds for new as well as rollover mortgages, and it is also

confirmed across all subsample estimations by maturity model. Given that escalating risk weighs only

apply to the tranches exceeding LTV ratios of 66% and 80%, respectively, instead of the entire

mortgage, the additional capital that banks need to hold for high-LTV mortgages does apparently not

induce them to expand the levy after the CCyB activation.

We stress this as the second core finding of our paper, while rejecting Hypothesis 2. One interpretation

of this finding might be that LTV threshold indictors just set apart riskier mortgages, inducing lenders

to charge a credit risk premium. In that case, risk-weighting schemes might indeed prove to be

ineffective when capital requirements on behalf of the bank become stricter, while lending standards

with respect to the customer risk characteristics in general remain unaffected.

Related to PTI ratios as a proxy for a different kind of borrower risk, we find differential effects for

new and rollover mortgages. Banks charge extra for new mortgages in proportion to their reported PTI

ratios, but not for rollover mortgages. Indeed, the linear PTI effect on rollover mortgage is slightly

negative, but dwarfed by the extra premium that banks impose on very high LTV ratios.

As the CCyB’s design only captures higher LTV ratios, we challenge our results by also looking at the

interaction effects with high PTI indicators. Given that customer risk is sanctioned only by tighter

capital requirements in terms of credit risk, but not in terms of debt service risk, one might image that

banks extend more lending to high PTI customers. Our results, however, do not support such a

substitution effect.

29

We now briefly discuss our results on control variables in Columns (1) to (5) in order to assess whether

our regression specification overall yields reasonable results. The estimated coefficient on the swap

rate states that a 100 bps increase in the swap rate translates into an increase of the average mortgage

rate of about 77 bps. A hint at the fact that many of our participating banks substantially draw on retail

instead of wholesale funding can rationalize this number. We further find that a one percentage point

increase in the customer’s income reduces the offered mortgage rate by up to 4 basis points. Banks

charge lower mortgage rates for customers with higher specified levels of wealth requesting FRM and

new mortgages and give a discount for older customers in the full sample.

We conclude from these results that LTV thresholds do not amplify the CCyB effects for banks, which

hints at the weak nexus between risk-weighting schemes and capital requirements. However, it is still

possible that a signaling mechanism is at work. If the aggregate risk perception for all mortgages has

surged, but not for riskier ones in particular, our time fixed effects would absorb the effect.

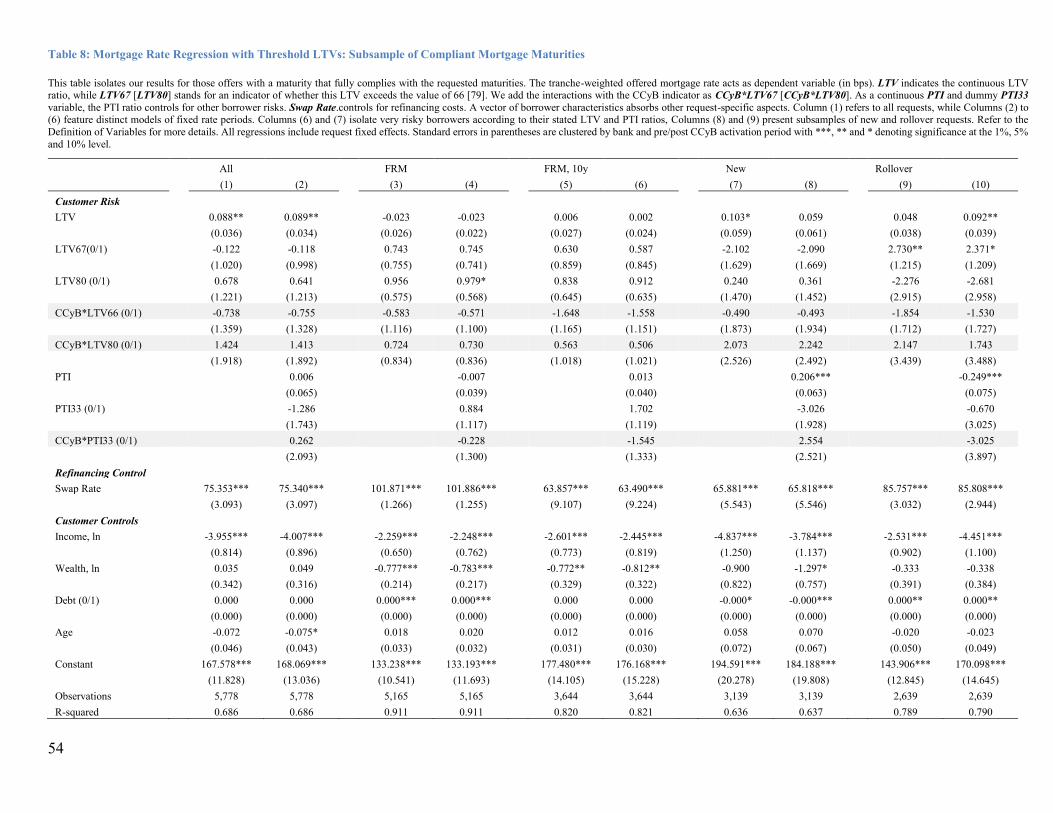

Robustness Checks

To challenge our findings, we again isolate those offers which offer a fully compliant mortgage

maturity. Our results turn out to be robust with only slight deviations in terms the size of coefficient

estimates.

Another concern might be that banks become in general more risk averse after the CCyB activation

and rise their risk premiums on average. As the interactions effect with both indicators of borrower

risk, credit risk and debt service risk reveal to be insignificant, we can also safely reject this concern.

30

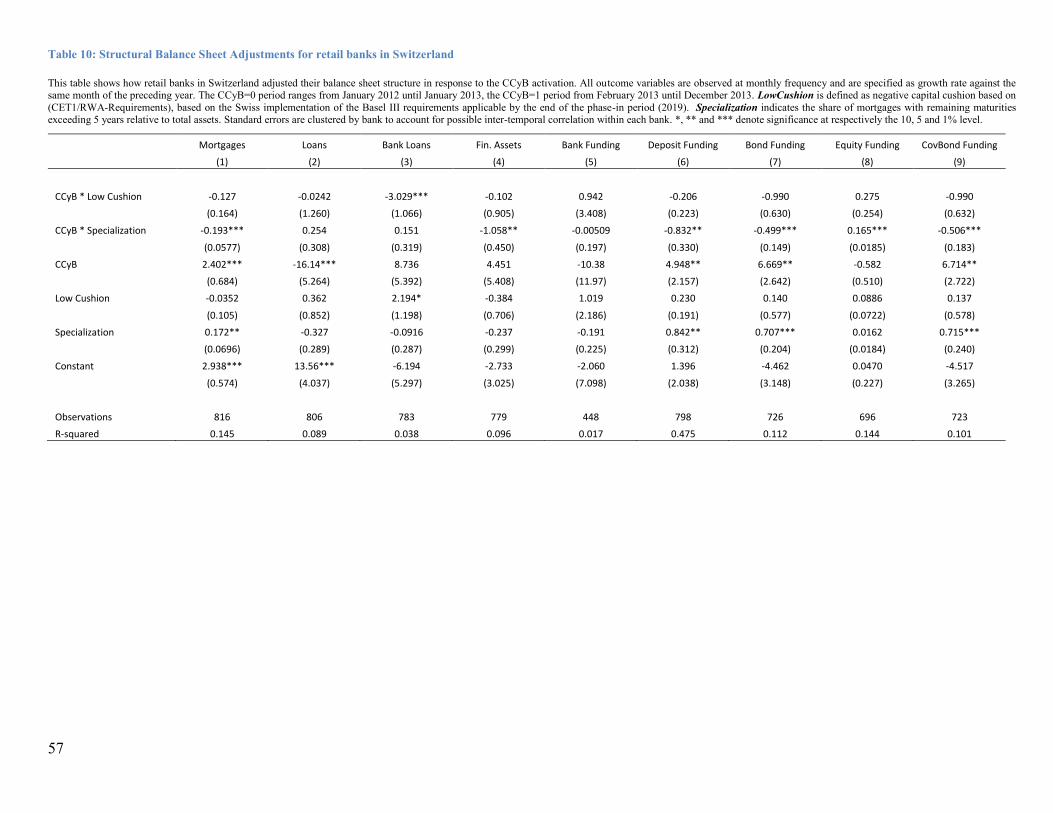

4 Analysis of Balance Sheet Adjustments using Supervisory Data on all Swiss Banks

In this section, we investigate how the differential price increases at the response-level have affected

banks' overall balance sheets and capitalization in the months after the activation. To do so, we start

with supervisory bank balance sheet data covering not only the Comparis sample, but all banks

chartered in Switzerland.

Data

Starting with all Swiss banks, we focus on the subsample of retail banks in order to compare their

adjustments with those shown by banks in our Comparis sample.30 Based on banking groups as defined

by FINMA, we refer to retail banks as those banks whose balance sheet effective activities account for

earn at least 85% of their income, i.e. as net interest income, as opposed to fees and commissions31.

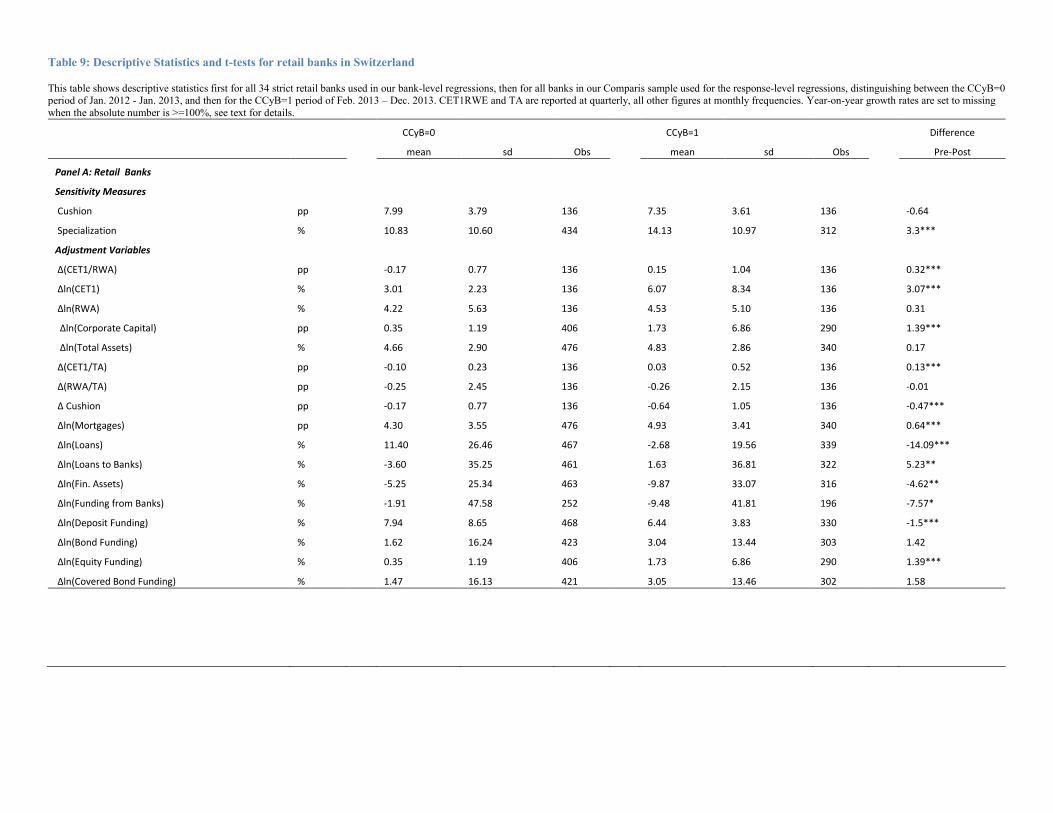

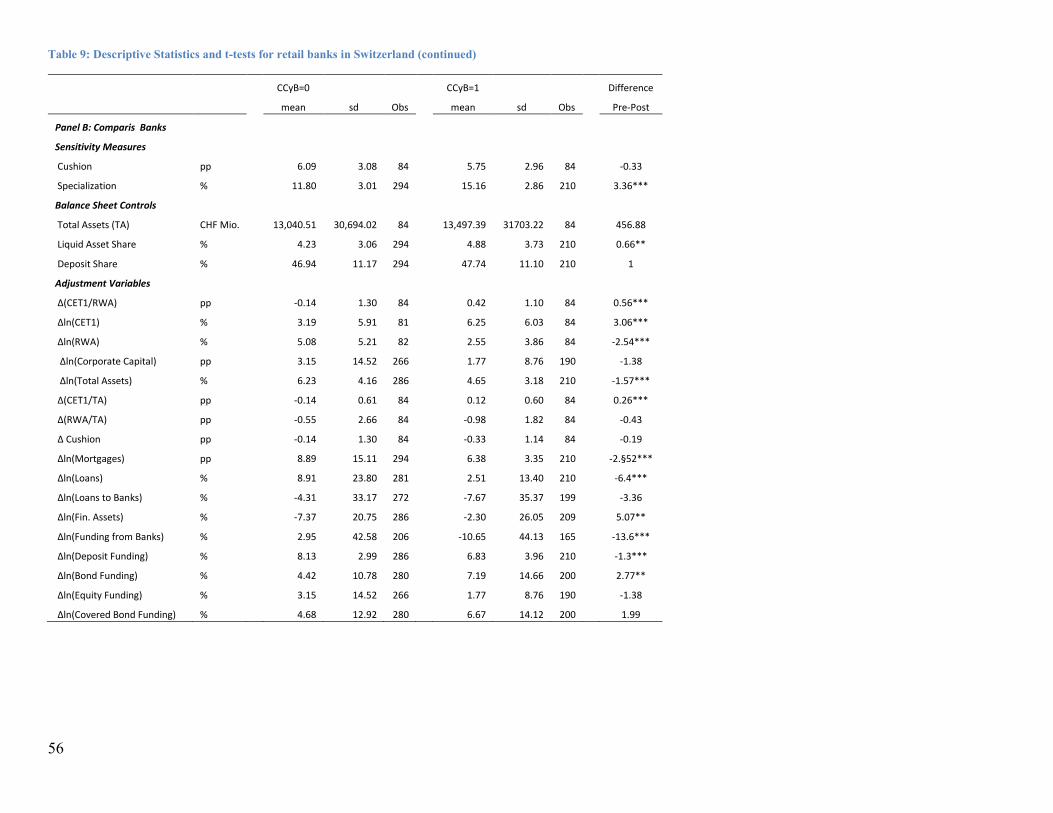

Table 9 shows summary statistics of our variables for the pre- and the post-activation periods and it

provides T-tests to compare how averages evolve over time. The top panel describes all retail banks

used for our baseline analyses in this section, while the bottom panel draws on the Comparis sample

as analyzed in the previous section. Our restrictive retail bank sample contains 36 banks, observed

over 14 months (January 2012 – February 2013, a total of 504 monthly observations) before and 10

months (March 2013 – December 2013, 360 observations) after the CCyB activation. Core Equity Tier

1 (CET1) capital and Risk-Weighted Assets (RWA), as well as all variables building on those, are

observed only at quarterly frequency32. The first rows show our two bank sensitivity measures, capital

30 By contrast, focusing the bank level analyses even more narrowly only on the 21 banks contained in the Comparis sample would not yield

enough observations.

31 The latter are more relevant for Switzerland's many wealth management banks, and trading income. As a robustness check, we include also

banks with interest income accounting for 55-85% of total income, as well as "universal" banks with interest income below 55%, fee income below 55%, and trading income below 20% of total income.

32 We assign missing values to those periods in which the underlying value was either zero or missing, and to periods in which absolute growth

rates equaled or exceeded 100% to avoid distorting our sample by capturing complete sell-offs or new acquisition of a portfolio that would

typically occur as part of a merger.

31

cushion and specialization. They are followed by the bank-level controls used in our response-level

analyses, and then we turn to other variables as analyzed in this section. Within the set of adjustment

variables, for all fractions we display the year-on-year difference in percentage points and for all other

variables the year-on-year percentage growth rate.

Against the regulatory requirements to be satisfied by the end of the Basel III phase-in period (2019),

retail banks report a CET1 capital cushion worth 7.99% of RWA over the pre-activation period,

compared to the economically similar value of 6.09 for Comparis banks. Capital cushions for both

groups contract in the second period, when requirements increase, however, for the average bank none

of these contractions is statistically significant.

Before the CCyB activation, specialization in the mortgage business, measured as the share of

outstanding long-term mortgages maturing in 5 years or beyond, amounts to about 10.8% of total assets

for the average retail bank, and to about 11.8% for the average bank in the Comparis sample. Over the

post-activation period, these shares rose significantly by more than 3 percentage points, respectively.

These outcomes seemingly contrast with the intended effects, and deserve some closer investigation.

Of course, averages as displayed in Table 9 mask the heterogeneinity across banks and their differential

sensitivities to the CCyB's design. For this reason, we argue that only our regression approach in

Section 3 can disentangle differential adjustment patterns, while revealing a change in the overall

composition of mortgage supply.

Our regression analyses below draw on annual growth rates and absolute changes. Looking at our

outcome variables of interest, we see that the annual growth rate of CET1 capital increased from about

3% to about 6% in both sets. The average retail bank kept its pace of RWA expansion almost stable

(the change is actually insignificant), such that the average annual change in capitalization ratios

CET1/RWA rose significantly by 0.3 percentage points. In parallel, the average Comparis bank

reduced the pace of RWA growth and strengthened its capital ratio significantly, resulting in a 0.5

32

percentage point rise in the year-on-year changes in the ratio of CET1 over RWA. Based on these

facts, we infer that the sample of retail banks mirrors the behavior that of the Comparis subset and vice

versa. In our empirical analysis below, we can hence resort to the broader sample of retail banks with

more observations to yield some meaningful results.

Empirical Approach

To identify the effects of the CCyB on bank balance sheets, we apply a Difference-in-Difference (DiD)

approach. We compare changes in the outcomes of interest between the pre- and post-CCyB periods

and across banks with different a priori levels of capital cushions and mortgage specialization. This

leads to the following estimation:

jjjt tionSpecializaCCyBLowCushionCCyBoutcome ** 21

jtjj tionSpecializaLowCushionCCyB 543 (4)

For our baseline estimations, we use only these basic DiD regressors. Robustness analyses with bank-

level controls or bank and time fixed effects yield similar results and are available on request.

Results

Table 10, Column 1 shows that the analyzed effects on mortgage pricing in Section 2 do indeed

translate into differential changes in mortgage growth: More specialized banks, while expanding their

mortgage business year-on-year during the pre-activation period, reduce their pace by 0.19 percentage

points after the activation. This finding is statistically significant at the 1% level, while clustering

standard errors by bank to account for serial correlation. By contrast, banks with a relatively lower

capital cushion were already trimming their mortgage lending before the CCyB activation and even

more so after it. However, none of these estimates is significant at the conventional levels when

33

clustering by bank. Instead of scaling back the mortgage business, banks with lower capital cushions

significantly reduced their growth rates in interbank lending.

Our effects are economically significant and remarkable, as retails banks actually expanded their

mortgage portfolio by almost 3% year-on-year before the CCyB activation, and accelerated the annual

pace by 2.4 percentage points during the post CCyB activation period, on average.. These results point

to a significant change in the composition of mortgage supply. New mortgage issuance shifted away

from very specialized banks with higher volumes of long-term mortgages on balance sheets and those

with lower capital cushions to those banks less specialized and more resilient in terms of capitalization.

Table 10 also shows that the overall expansion of retail banks in the mortgage business contrasts with

a general trend during the post-activation period. Column 2 suggests that banks significantly cut back

on lending to all sectors during this time. The 16 percentage point decline must hence be driven by

other business segments, like lending to the non-bank corporate sector. Before the activation, banks

reported strong annual growth rates of overall loan issuance reaching 14%, on average.

When turning to the liability side, we find that more specialized banks actually reversed their funding

strategies across periods. Before the activation, they had increasingly relied on deposit and bond

funding, covered bond funding in particular. Our estimates for the post CCyB period reveal that, they

revised their funding patterns and raised more equity capital. Due to a lack of significance, we do not

elaborate on the funding strategies of low cushion banks.

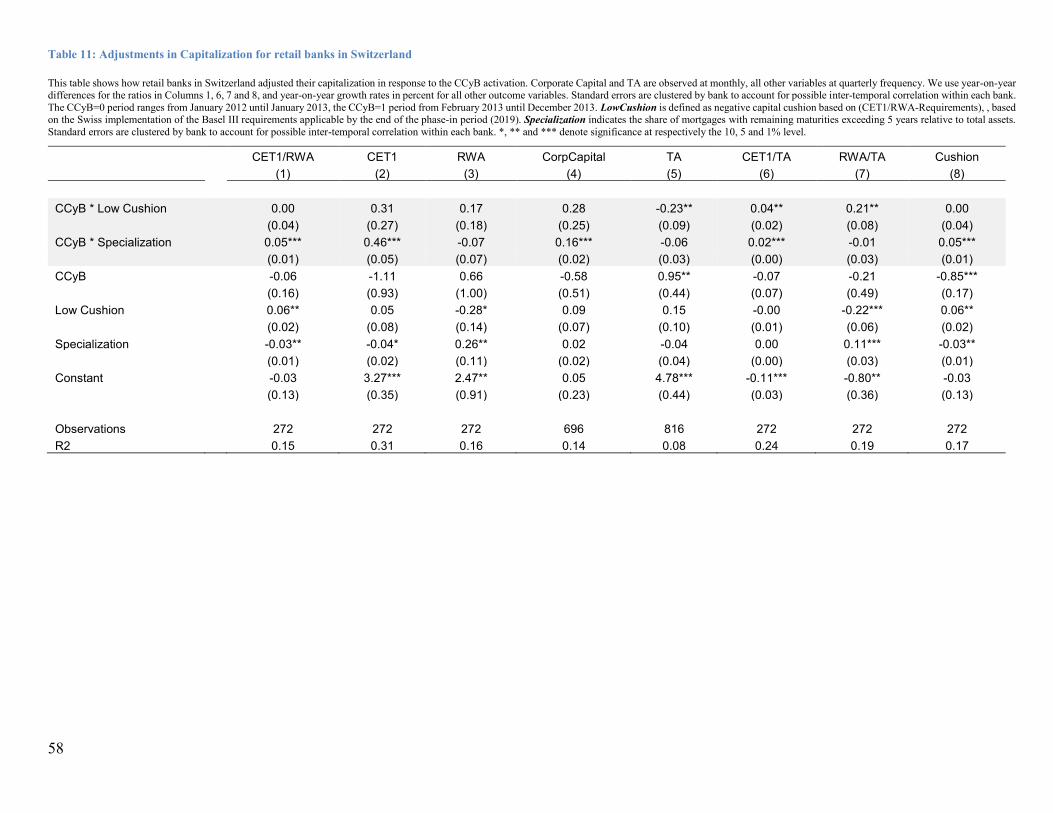

Table 11 analyzes the effects on capitalization in more detail. Here, we focus specifically on Core

Equity Tier 1 (CET1) capital, in which the CCyB requirements are specified. Column 1 shows that for

each percentage point of mortgage specialization, banks increased their CET1/RWA ratio by 0.05

percentage points more. Columns 2 and 3 indicate that for the average bank in the sample, this increase

was achieved entirely through an uplift in CET1 capital, rather than through a reduction of RWA. For

this reason, the increase is confirmed for the unweighted capitalization (leverage ratio) in Column 6.

34

Finally, a comparison of Columns 2 and 4 reveals that only about one-third of the CET1 increase was

achieved by expanding Corporate Capital (coefficient estimate of 0.16 pp in Column 4, against a

coefficient estimate of 0.46 pp in Column 2), with the larger part presumably achieved through the

retained earnings channel.

With respect to the analysis of low-cushion banks, our baseline indicates that the CET1 absolute

increase of 0.31 percentage points reported in Column 2 is not statistically significant at conventional

levels, only the 0.04 percentage point extra increase in CET1/TA in Column 6 is. As pointed out by

Column 5, this strengthening of capital ratios, however, was achieved by a balance sheet contraction,

rather than a rise in the level of capital per se.

We conclude from these results, that specialized banks made an effort to strengthen their capital basis

by raising capital, most likely by drawing on their retained earnings. Only a minor share of capital in

the banking system accrued to banks asking their shareholders. By contrast, banks with a lower capital

cushions contracted their balance sheets especially by scaling back on their interbank lending business

to strengthen their capitalization. When combing these findings with our results from the Comparis

data analysis, we conclude that the shift ensued from a significant change in the pricing of mortgages,

especially of those with fixed term and longer maturities.

In Tables A3 and A4 of our Online Appendix, we replicate both of the regression tables based on a

larger sample featuring 118 retail and universal banks. Overall results there are similar to those of our

baseline estimates. The effect of Specialization is slightly less statistically significant, whereas that of

Low Cushions on the year-on-year growth of CET1 remains significant at the 5% level there.

35

5 Conclusions

Our paper provides a comprehensive assessment of the first activation of the Counter-Cyclical Capital

Buffer (CCyB), the macroprudential tool of the Basel III set of banking regulation. The CCyB, as

implemented in Switzerland, requires banks to set aside extra CET1 capital worth 1% of their risk-

weighted domestic residential mortgages. We examine how, as an immediate response, banks adjust

their mortgage supply in terms of rejecting and pricing mortgage applications along different types of

borrower risk and maturity models. In the longer run, we study how banks re-structure their balance

sheets in terms of asset portfolio, capitalization and funding sources.

We use a unique dataset featuring multiple bank responses per mortgage request, and furthermore

combine this with supervisory bank-level data on the entire population of Swiss banks. With these

data, we are able to cleanly identify how different types of banks respond to the policy change.

Our findings on the immediate impact on the mortgage market uncover shifts of new lending from

relatively more to relatively less affected banks, an effect concealed in the aggregate data.

Specifically, banks with low capital cushions and mortgage-specialized banks raise prices more. We

do not find a significant change in the rejection behaviour of banks per se, and infer that our highly

significant mortgage pricing effects are sufficient to shift new mortgage issuance to those banks which

are less sensitive to the particular design of the CCyB. While banks charge a credit risk premium for

high loan-to-value customers in general, our results do not provide empirical support that risk-

weighting schemes amplify the effectiveness of tighter capital requirements. The interaction effects

with the CCyB reveal to be robustly insignificant across multiple specifications, mortgage models and

subsamples.

Our results on the longer-term balance sheet and capitalization adjustments show that mortgage-

specialized banks made an effort to strengthen their capital basis. Supervisory bank-level data suggest

that, in order to strengthen their capital basis, most banks preferred to draw on their retained earnings

36

and only a minor share of additional capital in the banking system accrued to banks asking their

shareholders. By contrast, those banks with a lower capital cushions contracted their balance sheets,