Embed Size (px)

Citation preview

THE

COTTON SECTOR of

TAJIKISTAN

NEW OPPORTUNITIES

for the

INTERNATIONAL COTTON TRADE

PRESENTED BY THE GOVERNMENT OF TAJIKISTAN APRIL 2007

1

Index Page Foreword 4 1.0 Overview of Tajikistan and the Agricultural Sector 5 1.1 Geography and Demographics 1.2 Macro-Economic and Political Economic Background 1.3 Political structure 1.4 Agricultural sector overview 2.0 The Cotton Sector – Current situation and Reforms 8 2.1 Overview 2.2 Production trends 2.3 Seed cotton quality 2.4 Baled Cotton Quality classification 2.5 Cotton farmers, Processing, Market Infrastructure and Exports 2.6 Seed sector 3.0 Tajikistan - The Investment and Operating Environment 13 3.1 Financial sector 3.2 Reform of Business Licensing and Inspections 3.3 Legal Environment 3.3.1 Company structures available in Tajikistan 3.3.2 Company structure overview 3.3.3 Company Registration Procedures 3.3.4 Import duties for equipment 3.3.5 General taxation 3.3.6 Cotton exportation 3.4 Overview of other agricultural sector projects

3.4.1 World Bank Projects 3.4.2 Projects of other donors

4.0 Government of Tajikistan and World Bank Cotton Sector Recovery Project 19 4.1 Overview 4.2 Project objective and phases 4.3 Project Components

4.3.1 Debt Resolution 4.3.2 Support for Policy Analysis and Reform 4.3.3 Cotton Supply Chain Development

a) Cotton Ginneries b) Cotton Seed Supply c) Producer Support

4.4 Project Districts 4.4.1 Criteria for district selection 4.4.2 Preliminary selected districts

5.0 IFC 25 5.1 About IFC 5.2 IFC’s added value to potential investors 5.3 IFC’s Products and Services

5.3.1 Equity and Quasi-Equity 5.3.2 Loans and Intermediary Services 5.3.3 Syndicated Loans 5.3.4 Structured Finance 5.3.5 Risk Management 5.3.6 Technical Assistance and Advisory Services

5.4 Eligibility of the project 5.5 How can an investor apply for financing? 5.6 Where can an investor go for more information on IFC?

- 2 -

6.0 Multilateral Investment Guarantee Agency (MIGA) 27 6.1 What is MIGA? 6.2 What is the relevance of MIGA for potential investors under the proposed project? 6.3 What investments would be eligible? 6.4 What is an SME as covered by SIP? 6.5 Who is an eligible investor as defined by SIP? 6.6 What is offered under a SIP guarantee?

6.6.1 Risk definitions 6.7 How to apply? 7.0 Way forward 29 Appendices Appendix 1.0 – Government of Tajikistan Cotton Sector Road Map 31 Appendix 1.1 - Methodica – minimum export price calculation and regulations 36 Appendix 2.1 – Production statistics 40 Appendix 2.2 – Quality production splits 41 Appendix 2.3 – Land Reform Statistics 42 Appendix 3.1 - Tax information 43 Appendix 4.1 – District statistics – Kumsangir 45 Appendix 4.2 – District statistics – Bohtar 47 Appendix 4.3 – District statistics – Farkhor 49 Appendix 4.4 – District statistics – Kabadian 51 Appendix 4.5 – District statistics – Vakhsh 53 Appendix 4.6 – District statistics – Shaartuz 55 Appendix 4.7 - District statistics – Vosse 57 Appendix 7.0 - Investor criteria 59 Figures Figure 1 – Map of Tajikistan Figure 2 – Administrative map of Tajikistan Figure 2.1 – Area and production data Figure 2.2 – MS production data Figure 2.3 – ELS production data Figure 2.4 – MS seed cotton quality Figure 2.5 - ELS seed cotton quality Figure 4.1 – Irrigated land Khatlon (by district) Figure 4.2 – Yield of seed cotton per hectare Khatlon (by district) Figure 4.3 – Total seed cotton production Khatlon (by district) Figure 4.4 – Percentage arable land under private use Khatlon (by district) Figure 4.5 – Percentage land sown to cotton Khalton (by district) Figure 4.6 – Average debt per hectare Khalton as of 01/01/2005 (by district)

- 3 -

Foreword Cotton is not only an important crop for our Republic; it is entwined with our history and with the lives and future of our people. Since Independence we have gone through a very marked transition, the beneficial effects of which were initially hampered by a period of Civil Unrest. Therefore, unlike many of the other countries in the Former Soviet Union, our real reform to a market economy was delayed and only really began in 1999. Equally, the after affects of the unrest and the post-conflict situation created further difficulties for our Government and the people of our Republic. However, we are now benefiting from a period of political and economic stability, a situation that many of our neighbouring countries are not benefiting from. We, the Government of the Republic of Tajikistan, feel that the time is now right for a deepening of reforms, encouragement of foreign investment and a determined effort to support the private sector development of our economy. We are working closely with the wider international development community to foster and strengthen the enabling environment that will provide the structure within which the private sector will work. A number of important reforms have already been implemented in many areas of our economy. The most dramatic program for development and reform lies in the agricultural sector and specifically cotton. The President of the Republic and his Government have been working closely with donors for the past year to develop a vision for the cotton sector – a “Road Map” - that will lead to the true realisation of the potential of the sector in our Republic. We appreciate that certain international companies may have previously had less than satisfactory experiences in investing in the cotton sector in our Republic and in exporting our baled cotton. Whilst these experiences were not connected with the actions of our Government, we can ensure investors and the wider international cotton community that we are making all possible efforts to ensure the existence of a more transparent, equitable, dependable and profitable sector for all. This document gives a short outline of the recent and planned reforms for the cotton sector of Tajikistan. It also identifies a number of investment opportunities connected with a new project being undertaken in partnership with the International Development Association (World Bank). In general terms these opportunities are in the ginning sector where we actively seek new foreign investors for whom the project will make available seasonal finance lines. We are also seeking to attract new investors in the seed sector, for whom there will also be credit lines available for the purchase of modern seed treatment equipment. For specific details on these opportunities, please refer to section 4 of this document. We would like to draw to your attention that expressions of interest from potential investors should be presented to ourselves by 30th July 2007. However, we would like to bring to your attention the fact that we are also interested to further develop and strengthen our working relationships with yourselves in many other areas, be they export, warehousing, textiles or finance. Sharif Rahimov Chairman State Committee on Investments and State Property Management Republic of Tajikistan

- 4 -

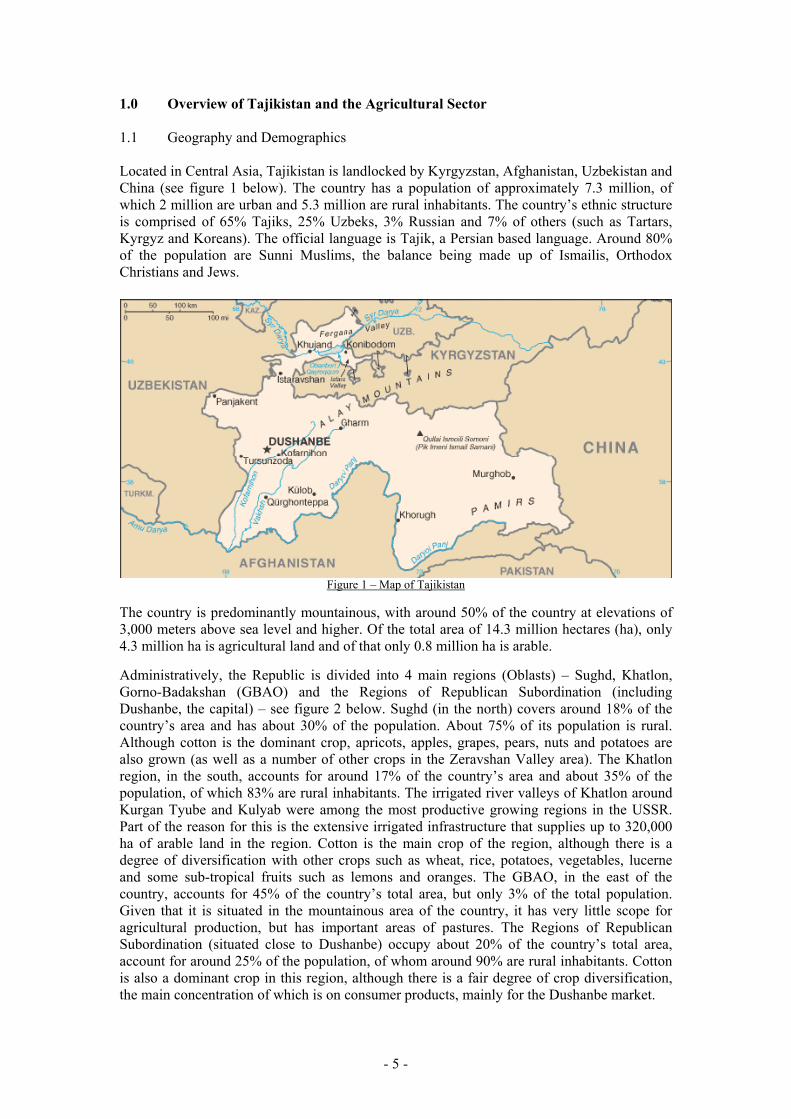

1.0 Overview of Tajikistan and the Agricultural Sector 1.1 Geography and Demographics Located in Central Asia, Tajikistan is landlocked by Kyrgyzstan, Afghanistan, Uzbekistan and China (see figure 1 below). The country has a population of approximately 7.3 million, of which 2 million are urban and 5.3 million are rural inhabitants. The country’s ethnic structure is comprised of 65% Tajiks, 25% Uzbeks, 3% Russian and 7% of others (such as Tartars, Kyrgyz and Koreans). The official language is Tajik, a Persian based language. Around 80% of the population are Sunni Muslims, the balance being made up of Ismailis, Orthodox Christians and Jews.

Figure 1 – Map of Tajikistan

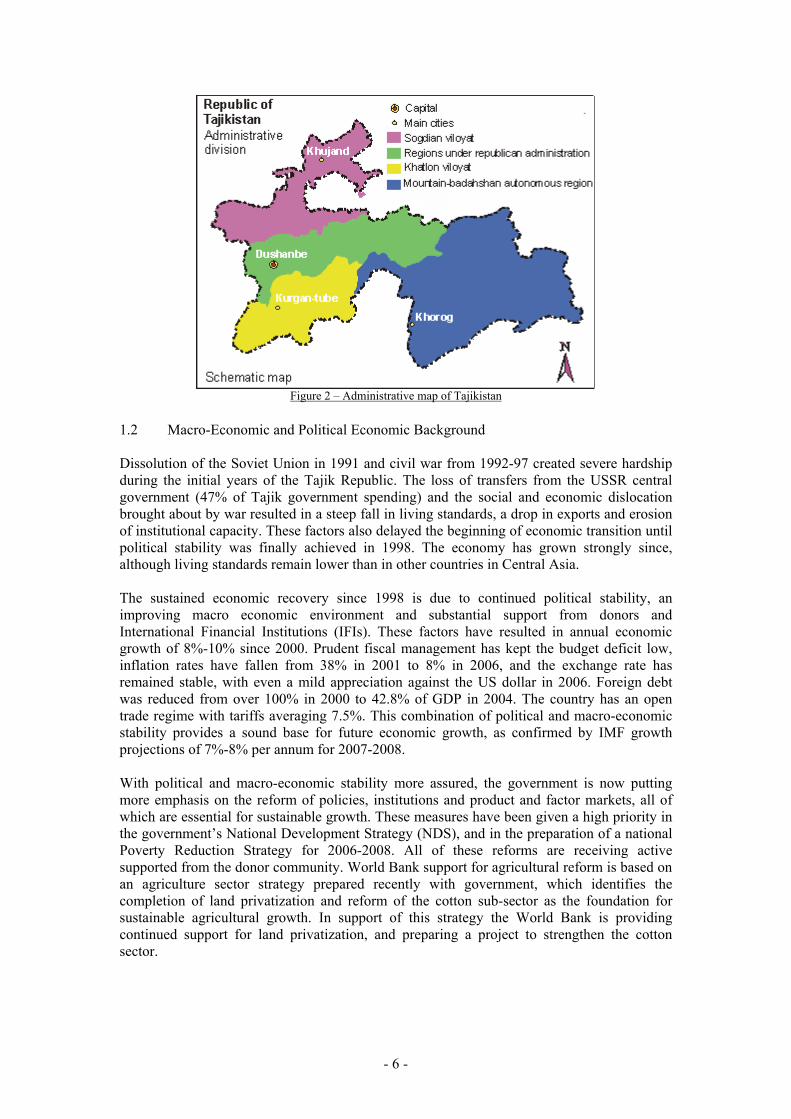

The country is predominantly mountainous, with around 50% of the country at elevations of 3,000 meters above sea level and higher. Of the total area of 14.3 million hectares (ha), only 4.3 million ha is agricultural land and of that only 0.8 million ha is arable. Administratively, the Republic is divided into 4 main regions (Oblasts) – Sughd, Khatlon, Gorno-Badakshan (GBAO) and the Regions of Republican Subordination (including Dushanbe, the capital) – see figure 2 below. Sughd (in the north) covers around 18% of the country’s area and has about 30% of the population. About 75% of its population is rural. Although cotton is the dominant crop, apricots, apples, grapes, pears, nuts and potatoes are also grown (as well as a number of other crops in the Zeravshan Valley area). The Khatlon region, in the south, accounts for around 17% of the country’s area and about 35% of the population, of which 83% are rural inhabitants. The irrigated river valleys of Khatlon around Kurgan Tyube and Kulyab were among the most productive growing regions in the USSR. Part of the reason for this is the extensive irrigated infrastructure that supplies up to 320,000 ha of arable land in the region. Cotton is the main crop of the region, although there is a degree of diversification with other crops such as wheat, rice, potatoes, vegetables, lucerne and some sub-tropical fruits such as lemons and oranges. The GBAO, in the east of the country, accounts for 45% of the country’s total area, but only 3% of the total population. Given that it is situated in the mountainous area of the country, it has very little scope for agricultural production, but has important areas of pastures. The Regions of Republican Subordination (situated close to Dushanbe) occupy about 20% of the country’s total area, account for around 25% of the population, of whom around 90% are rural inhabitants. Cotton is also a dominant crop in this region, although there is a fair degree of crop diversification, the main concentration of which is on consumer products, mainly for the Dushanbe market.

- 5 -

Figure 2 – Administrative map of Tajikistan

1.2 Macro-Economic and Political Economic Background Dissolution of the Soviet Union in 1991 and civil war from 1992-97 created severe hardship during the initial years of the Tajik Republic. The loss of transfers from the USSR central government (47% of Tajik government spending) and the social and economic dislocation brought about by war resulted in a steep fall in living standards, a drop in exports and erosion of institutional capacity. These factors also delayed the beginning of economic transition until political stability was finally achieved in 1998. The economy has grown strongly since, although living standards remain lower than in other countries in Central Asia. The sustained economic recovery since 1998 is due to continued political stability, an improving macro economic environment and substantial support from donors and International Financial Institutions (IFIs). These factors have resulted in annual economic growth of 8%-10% since 2000. Prudent fiscal management has kept the budget deficit low, inflation rates have fallen from 38% in 2001 to 8% in 2006, and the exchange rate has remained stable, with even a mild appreciation against the US dollar in 2006. Foreign debt was reduced from over 100% in 2000 to 42.8% of GDP in 2004. The country has an open trade regime with tariffs averaging 7.5%. This combination of political and macro-economic stability provides a sound base for future economic growth, as confirmed by IMF growth projections of 7%-8% per annum for 2007-2008. With political and macro-economic stability more assured, the government is now putting more emphasis on the reform of policies, institutions and product and factor markets, all of which are essential for sustainable growth. These measures have been given a high priority in the government’s National Development Strategy (NDS), and in the preparation of a national Poverty Reduction Strategy for 2006-2008. All of these reforms are receiving active supported from the donor community. World Bank support for agricultural reform is based on an agriculture sector strategy prepared recently with government, which identifies the completion of land privatization and reform of the cotton sub-sector as the foundation for sustainable agricultural growth. In support of this strategy the World Bank is providing continued support for land privatization, and preparing a project to strengthen the cotton sector.

- 6 -

1.3 Political structure The main framework is a Presidential Republic, whereby the President is both head of the state and government, as well as of the pluriform, multi-party system. Legislative power exists in both the executive branch and the two chambers of parliament. The executive branch of government is headed by the President, who is elected by popular vote for a seven year term (the last election having been in 2006). The prime minister is appointed by the President, as is the council of ministers (although these appointments require the approval of the Supreme Assembly. The legislative branch of government is made up of the Supreme Assembly, which has 2 chambers. Firstly there is the Assembly of Representatives, which has 63 members, who are elected for 5 year terms. 22 members are elected by proportional representation, the remaining 41 in single seat constituencies. The National Assembly has 33 members, also elected for 5 years. 25 members are elected by local assembly deputies and 8 are appointed by the President. 1.4 Agricultural sector overview Agriculture is the second largest sector of the economy, after services. In 2004, it accounted for 24% of GDP, 66% of employment, 26% of exports and 39% of tax revenue. Cotton is the main agricultural export crop, contributing 90% of agricultural exports. In 2003 cotton accounted for 24.2% of total export revenue and 17.3% in 2004 (the difference largely being due to a fall in the international prices for cotton. Other agricultural exports include fresh and processed fruit and vegetables and silk products. Overall around 70% of the population lives in rural areas, with the majority of them involved in agriculture and over 60% of those mainly engaged in the cotton sector. To date there has been limited development of the non-farm rural economy. Tajikistan has good climatic conditions for growing a wide range of crops. It has a continental climate, with hot dry summers in the lowland areas, yet cooler and wetter weather in the mountain valleys and foothills. Soils are reasonably good in the south and in the upland valley areas, although less fertile in the northern valleys. Low precipitation levels limit the scope for rain-fed agriculture and necessitate a heavy reliance on irrigation for crop production. However, water resources are abundant and approximately 85% of arable land is located within the coverage area of the irrigation system. As with many other areas of the Tajik economy, agricultural output and productivity sharply declined following the dissolution of the Soviet Union and continued through the difficult period of the Civil War. However, recovery in this sector began to appear in 1996 and since 2000 it has grown at 2 digit levels. In fact, agriculture sector growth has made a powerful contribution to post-war economic recovery, accounting for approximately one third of overall economic growth from 1998 to 2004. Sector output increased by 65% in real terms during this period, and has now returned to the level extant at independence in 1990. Rural poverty has fallen significantly in response to these trends; with 65% of rural people below the poverty line ($2.15/day PPP) in 2004, compared to 82% in 1999. It should also be noted that the growth of the sector exceeded other areas of the economy (it was in excess of actual GDP growth between 2001 and 2004). The reason behind this growth is largely attributed to increases in actual yields, rather than in prices or planted area and this is largely due to improved macro-economic and political stability and enhanced access to inputs.

- 7 -

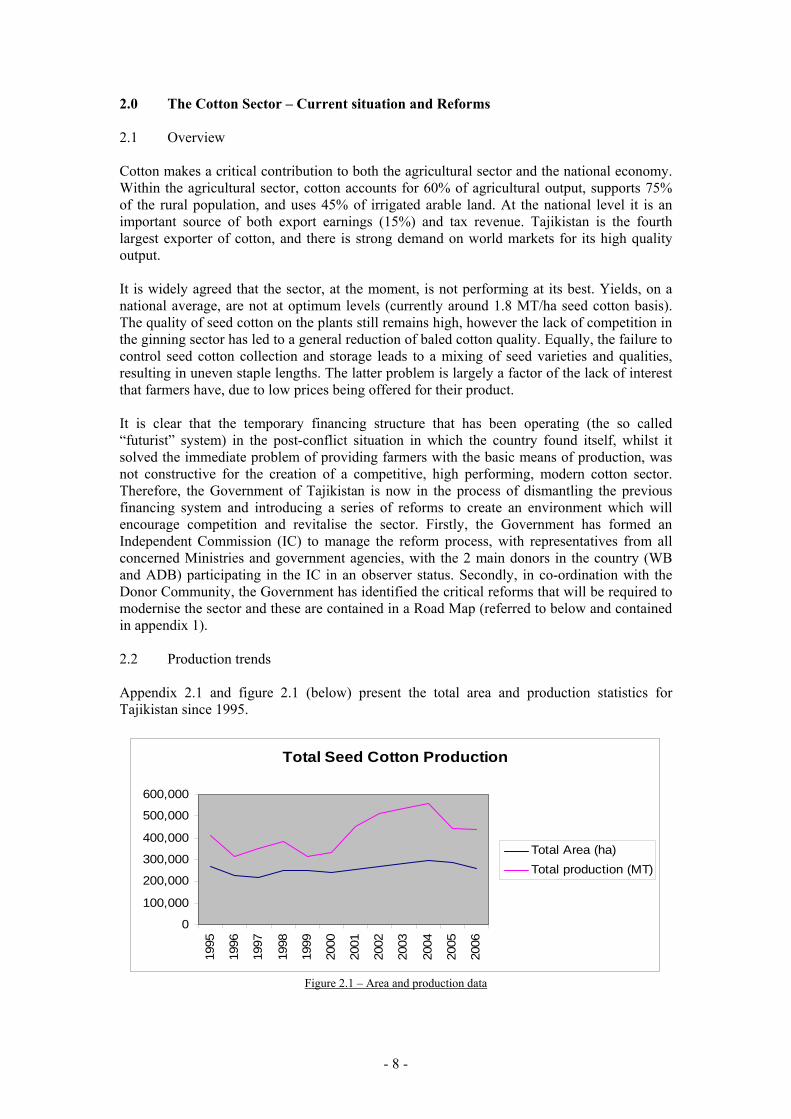

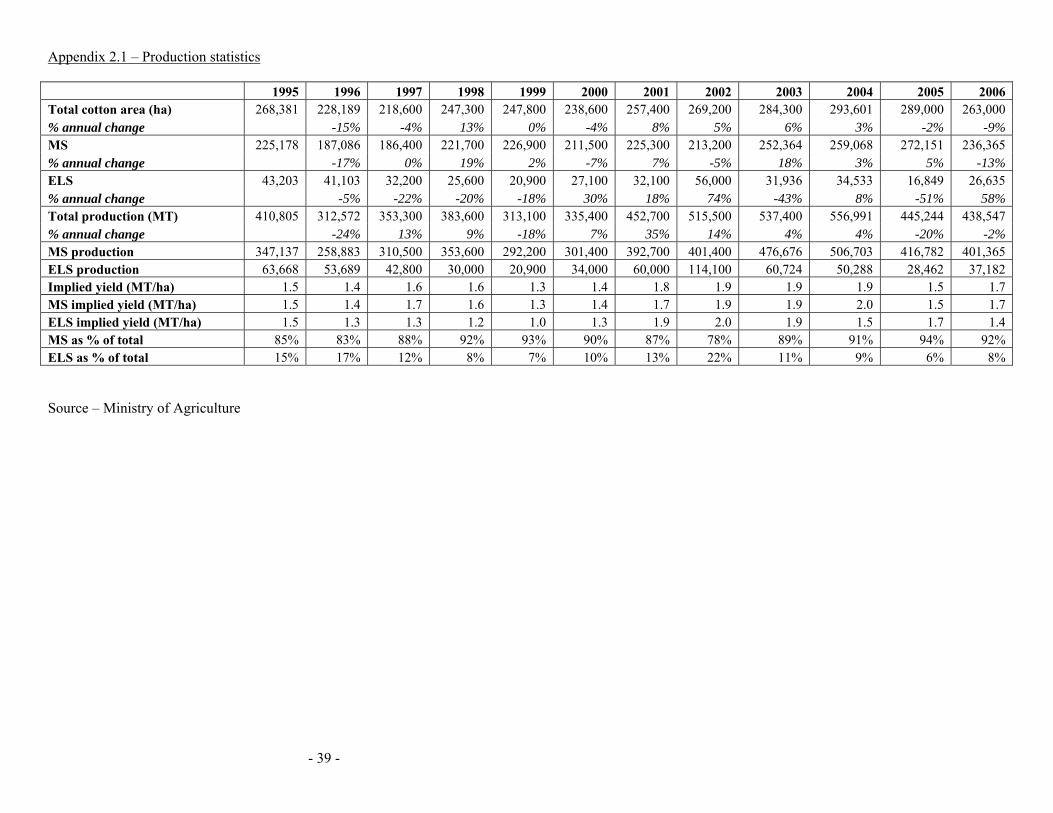

2.0 The Cotton Sector – Current situation and Reforms 2.1 Overview Cotton makes a critical contribution to both the agricultural sector and the national economy. Within the agricultural sector, cotton accounts for 60% of agricultural output, supports 75% of the rural population, and uses 45% of irrigated arable land. At the national level it is an important source of both export earnings (15%) and tax revenue. Tajikistan is the fourth largest exporter of cotton, and there is strong demand on world markets for its high quality output. It is widely agreed that the sector, at the moment, is not performing at its best. Yields, on a national average, are not at optimum levels (currently around 1.8 MT/ha seed cotton basis). The quality of seed cotton on the plants still remains high, however the lack of competition in the ginning sector has led to a general reduction of baled cotton quality. Equally, the failure to control seed cotton collection and storage leads to a mixing of seed varieties and qualities, resulting in uneven staple lengths. The latter problem is largely a factor of the lack of interest that farmers have, due to low prices being offered for their product. It is clear that the temporary financing structure that has been operating (the so called “futurist” system) in the post-conflict situation in which the country found itself, whilst it solved the immediate problem of providing farmers with the basic means of production, was not constructive for the creation of a competitive, high performing, modern cotton sector. Therefore, the Government of Tajikistan is now in the process of dismantling the previous financing system and introducing a series of reforms to create an environment which will encourage competition and revitalise the sector. Firstly, the Government has formed an Independent Commission (IC) to manage the reform process, with representatives from all concerned Ministries and government agencies, with the 2 main donors in the country (WB and ADB) participating in the IC in an observer status. Secondly, in co-ordination with the Donor Community, the Government has identified the critical reforms that will be required to modernise the sector and these are contained in a Road Map (referred to below and contained in appendix 1). 2.2 Production trends Appendix 2.1 and figure 2.1 (below) present the total area and production statistics for Tajikistan since 1995.

Total Seed Cotton Production

0

100,000

200,000

300,000

400,000

500,000

600,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Total Area (ha)Total production (MT)

Figure 2.1 – Area and production data

- 8 -

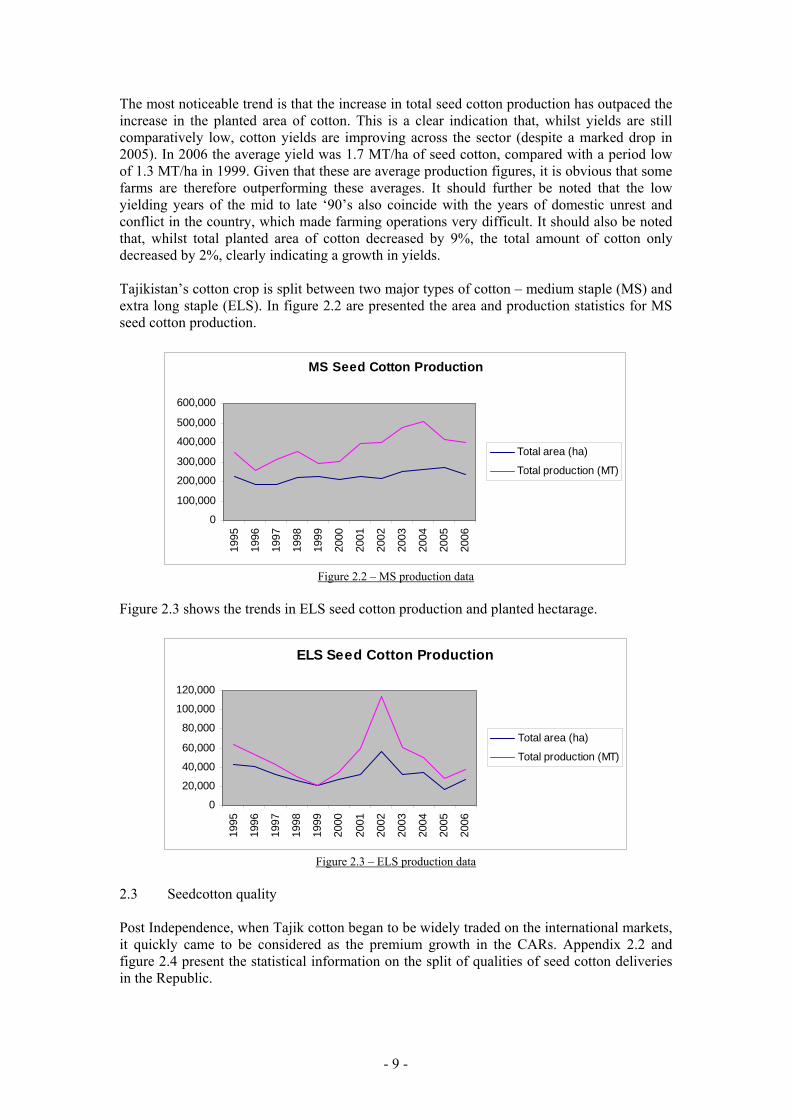

The most noticeable trend is that the increase in total seed cotton production has outpaced the increase in the planted area of cotton. This is a clear indication that, whilst yields are still comparatively low, cotton yields are improving across the sector (despite a marked drop in 2005). In 2006 the average yield was 1.7 MT/ha of seed cotton, compared with a period low of 1.3 MT/ha in 1999. Given that these are average production figures, it is obvious that some farms are therefore outperforming these averages. It should further be noted that the low yielding years of the mid to late ‘90’s also coincide with the years of domestic unrest and conflict in the country, which made farming operations very difficult. It should also be noted that, whilst total planted area of cotton decreased by 9%, the total amount of cotton only decreased by 2%, clearly indicating a growth in yields. Tajikistan’s cotton crop is split between two major types of cotton – medium staple (MS) and extra long staple (ELS). In figure 2.2 are presented the area and production statistics for MS seed cotton production.

MS Seed Cotton Production

0

100,000

200,000

300,000

400,000

500,000

600,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Total area (ha)

Total production (MT)

Figure 2.2 – MS production data

Figure 2.3 shows the trends in ELS seed cotton production and planted hectarage.

ELS Seed Cotton Production

0

20,000

40,000

60,000

80,000

100,000

120,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Total area (ha)

Total production (MT)

Figure 2.3 – ELS production data

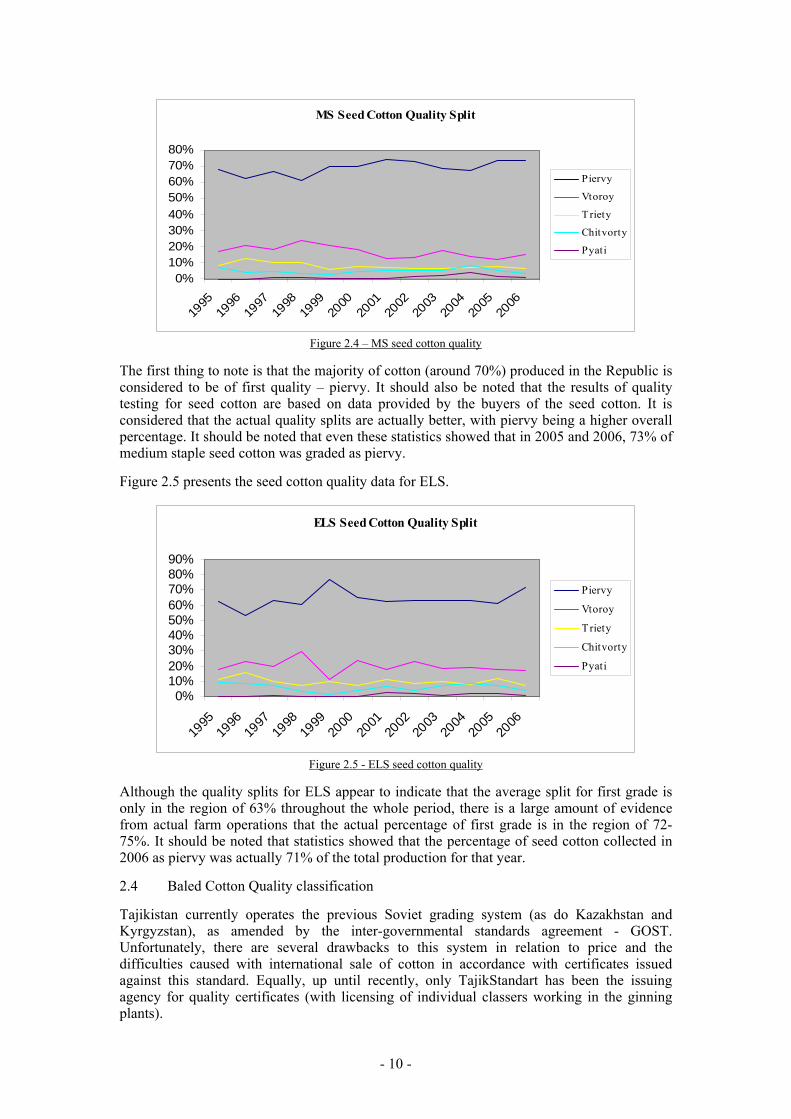

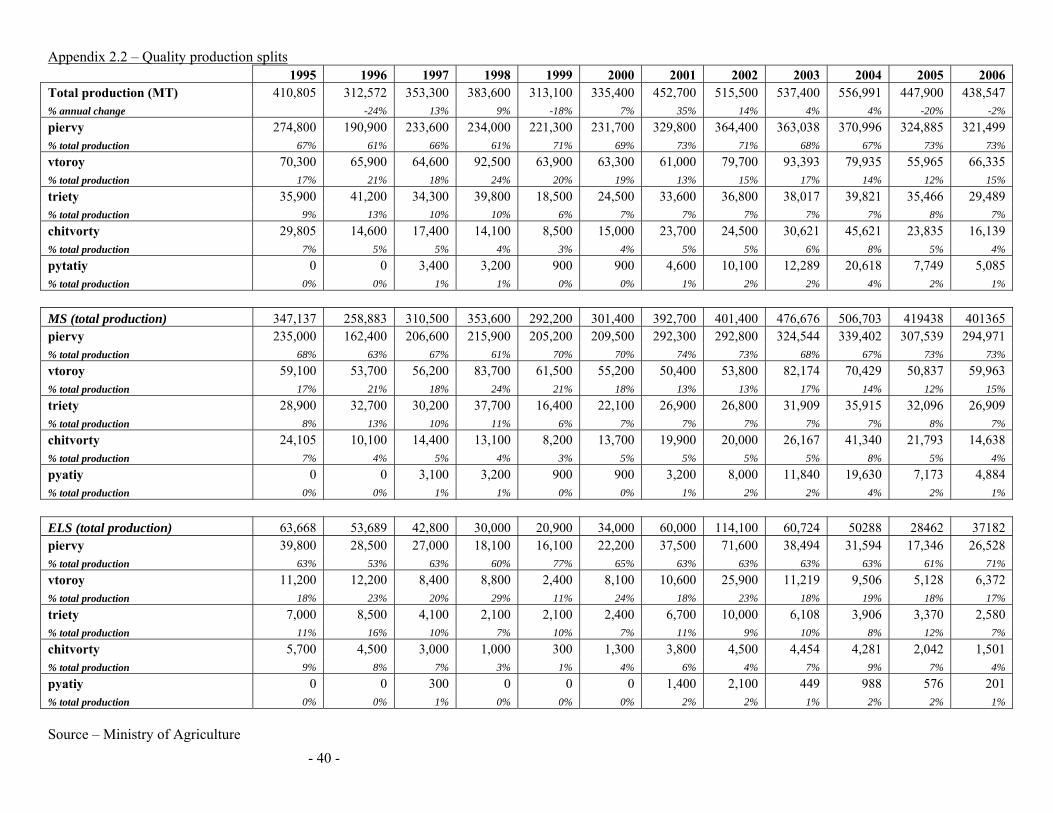

2.3 Seedcotton quality Post Independence, when Tajik cotton began to be widely traded on the international markets, it quickly came to be considered as the premium growth in the CARs. Appendix 2.2 and figure 2.4 present the statistical information on the split of qualities of seed cotton deliveries in the Republic.

- 9 -

MS Seed Cotton Quality Split

0%10%20%30%40%50%60%70%80%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Piervy

Vtoroy

Triety

Chitvorty

Pyati

Figure 2.4 – MS seed cotton quality

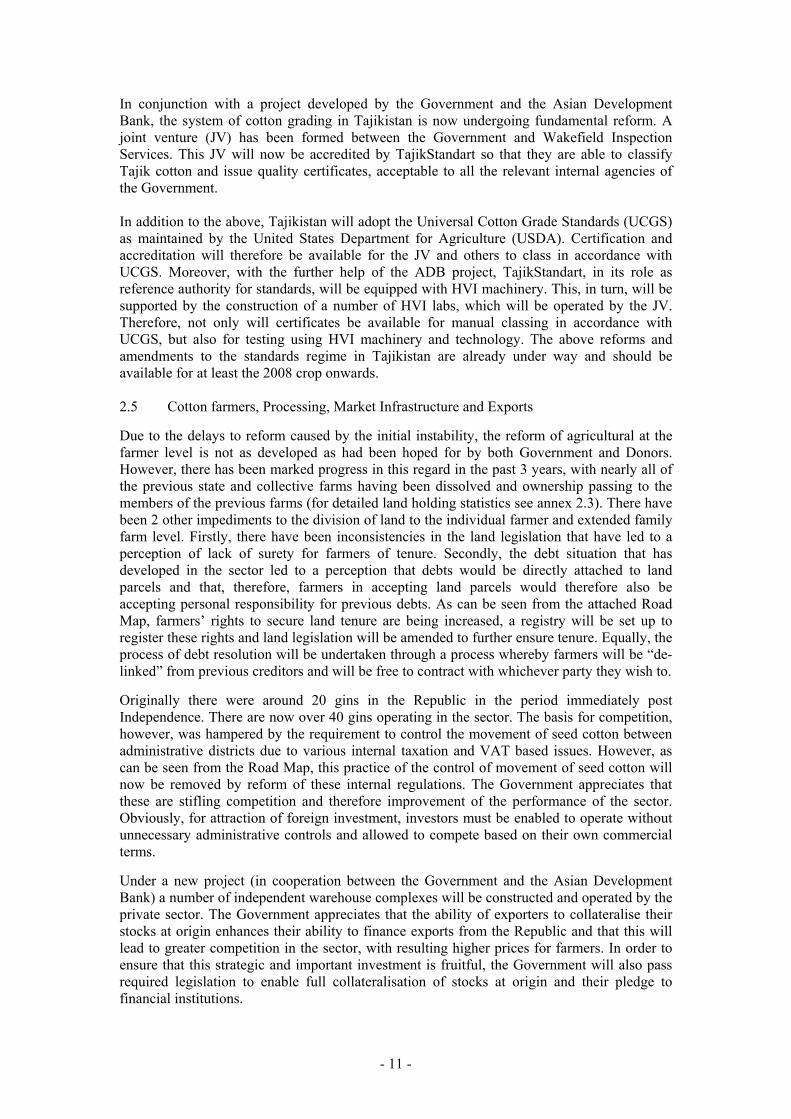

The first thing to note is that the majority of cotton (around 70%) produced in the Republic is considered to be of first quality – piervy. It should also be noted that the results of quality testing for seed cotton are based on data provided by the buyers of the seed cotton. It is considered that the actual quality splits are actually better, with piervy being a higher overall percentage. It should be noted that even these statistics showed that in 2005 and 2006, 73% of medium staple seed cotton was graded as piervy. Figure 2.5 presents the seed cotton quality data for ELS.

ELS Seed Cotton Quality Split

0%10%20%30%40%50%60%70%80%90%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Piervy

Vtoroy

Triety

Chitvorty

Pyati

Figure 2.5 - ELS seed cotton quality

Although the quality splits for ELS appear to indicate that the average split for first grade is only in the region of 63% throughout the whole period, there is a large amount of evidence from actual farm operations that the actual percentage of first grade is in the region of 72-75%. It should be noted that statistics showed that the percentage of seed cotton collected in 2006 as piervy was actually 71% of the total production for that year. 2.4 Baled Cotton Quality classification Tajikistan currently operates the previous Soviet grading system (as do Kazakhstan and Kyrgyzstan), as amended by the inter-governmental standards agreement - GOST. Unfortunately, there are several drawbacks to this system in relation to price and the difficulties caused with international sale of cotton in accordance with certificates issued against this standard. Equally, up until recently, only TajikStandart has been the issuing agency for quality certificates (with licensing of individual classers working in the ginning plants).

- 10 -

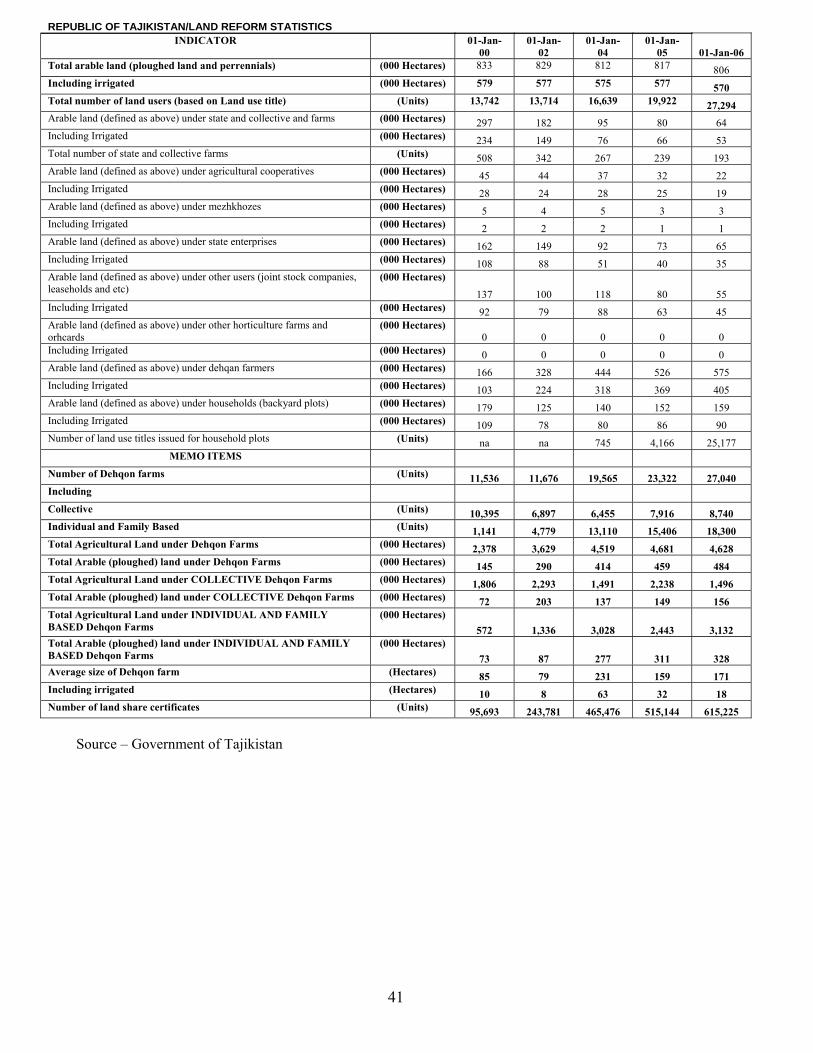

In conjunction with a project developed by the Government and the Asian Development Bank, the system of cotton grading in Tajikistan is now undergoing fundamental reform. A joint venture (JV) has been formed between the Government and Wakefield Inspection Services. This JV will now be accredited by TajikStandart so that they are able to classify Tajik cotton and issue quality certificates, acceptable to all the relevant internal agencies of the Government. In addition to the above, Tajikistan will adopt the Universal Cotton Grade Standards (UCGS) as maintained by the United States Department for Agriculture (USDA). Certification and accreditation will therefore be available for the JV and others to class in accordance with UCGS. Moreover, with the further help of the ADB project, TajikStandart, in its role as reference authority for standards, will be equipped with HVI machinery. This, in turn, will be supported by the construction of a number of HVI labs, which will be operated by the JV. Therefore, not only will certificates be available for manual classing in accordance with UCGS, but also for testing using HVI machinery and technology. The above reforms and amendments to the standards regime in Tajikistan are already under way and should be available for at least the 2008 crop onwards. 2.5 Cotton farmers, Processing, Market Infrastructure and Exports Due to the delays to reform caused by the initial instability, the reform of agricultural at the farmer level is not as developed as had been hoped for by both Government and Donors. However, there has been marked progress in this regard in the past 3 years, with nearly all of the previous state and collective farms having been dissolved and ownership passing to the members of the previous farms (for detailed land holding statistics see annex 2.3). There have been 2 other impediments to the division of land to the individual farmer and extended family farm level. Firstly, there have been inconsistencies in the land legislation that have led to a perception of lack of surety for farmers of tenure. Secondly, the debt situation that has developed in the sector led to a perception that debts would be directly attached to land parcels and that, therefore, farmers in accepting land parcels would therefore also be accepting personal responsibility for previous debts. As can be seen from the attached Road Map, farmers’ rights to secure land tenure are being increased, a registry will be set up to register these rights and land legislation will be amended to further ensure tenure. Equally, the process of debt resolution will be undertaken through a process whereby farmers will be “de-linked” from previous creditors and will be free to contract with whichever party they wish to. Originally there were around 20 gins in the Republic in the period immediately post Independence. There are now over 40 gins operating in the sector. The basis for competition, however, was hampered by the requirement to control the movement of seed cotton between administrative districts due to various internal taxation and VAT based issues. However, as can be seen from the Road Map, this practice of the control of movement of seed cotton will now be removed by reform of these internal regulations. The Government appreciates that these are stifling competition and therefore improvement of the performance of the sector. Obviously, for attraction of foreign investment, investors must be enabled to operate without unnecessary administrative controls and allowed to compete based on their own commercial terms. Under a new project (in cooperation between the Government and the Asian Development Bank) a number of independent warehouse complexes will be constructed and operated by the private sector. The Government appreciates that the ability of exporters to collateralise their stocks at origin enhances their ability to finance exports from the Republic and that this will lead to greater competition in the sector, with resulting higher prices for farmers. In order to ensure that this strategic and important investment is fruitful, the Government will also pass required legislation to enable full collateralisation of stocks at origin and their pledge to financial institutions.

- 11 -

The current system of control of exports through licensing by crediting banks, the Central Bank and the Commodities Exchange developed to ensure that such issues as capital flight, tax avoidance and failure to pay for exported cotton were minimised. As with other issues in the sector, these were necessary measures in the immediate post-conflict situation. However, whilst these measures served a clear purpose at the time, it is clear to Government that their usefulness in the modern setting is lessened and that they now constitute barriers to the transparent and competitive development of the sector. Therefore, as per the Road Map, the practice of export passports being required from the Central Bank and others financing the sector will be removed. Equally importantly, the roles and functions of the Commodities Exchange are currently under review and will be amended so that the Exchange can perform a function more suitable to those of an actual trading platform, as opposed to a licensing authority. It should also be noted that a number of important amendments have been made to the minimum export pricing formula operating in Tajikistan – the “methodica”. Previously, the export pricing formula was very restrictive in the terms of sale available to exporters (basically FOB only). The new methodica enables exporters to contract on any terms covered by Incoterms 2000. This allows much greater flexibility and access to many more markets. In addition, whilst the previous versions of methodica were largely in the form of unofficial directions to the Commodity Exchange, the new methodica benefits from far greater transparency, the method of calculation available to all interested parties and exists as an official inter-ministerial directive, having the weight of law behind it. In order to enable farmers, processors and exporters to manage their price risk and therefore maximise their revenues, the new methodica also allows for forward contracting of bale cotton at fixed prices. The new Methodica is presented in appendix 1.1 to this document and we would very much encourage you to acquaint yourselves with it. 2.6 Seed sector Whilst Tajikistan was a leader during the Soviet period of cotton seed breeding (especially extra long staple varieties), budgetary constraints since Independence have meant that Government has not been able to maintain investment in this important sector. It is widely held that some of the falls in yields at the farm level are directly connected with the reduction in seed vigour and lack of introduction and development of new varieties. In order to encourage domestic development of the seed industry and enable the short term introduction of foreign varieties, a number of legislative steps need to be taken and these are also referred to in the attached Road Map.

- 12 -

3.0 Tajikistan - The Investment and Operating Environment 3.1 Financial sector The financial sector in Tajikistan is based on a 2 tier system, with a total of 12 banks, 6 credit societies and 7 Non-Bank Financial Institutions (NBFIs) as of October 2006. The central bank of Tajikistan is known as the National Bank of Tajikistan (NBT). It has the main responsibilities of monetary oversight, as well as the supervision and regulation of the banking system (which includes commercial banks, NBFIs and Microfinance Organisations {MFOs}). The supervision of the banking sector has been substantially improved in recent years and the minimum capital requirement for commercial banks was increased to USD 5 million in January 2005. Various other reforms have reduced restrictions on banks’ operating parameters, leading to higher lending and increased liquidity, but within prudential requirements. The overall effect of the reforms has led to the emergence of a smaller, but more viable banking sector. Of the 12 banks in the country, 10 of them are commercial banks, one is a Microfinance Bank and the other one is a branch of a foreign bank. As of the end of 2004 AgroinvestBank (AIB), OrionBank, TodjiksodirotBank (TSOB) and Amonatbank held about 85% of total deposits and about 75% of outstanding loans in the banking system. It should be further noted that 6 of the banks have foreign shareholders. The 2 main banks with rural branch networks are AgroInvestBank (61 branches) and Orion Bank (30 branches). The microfinance sector in the country, although still in its infancy, is developing. It consists of micro-credit NGOs which evolved as part of various programmes developed by donors. Many development programmes and NGOs have started with in-kind lending, e.g. through the provision of agricultural inputs such as improved seeds. Credit was complemented by non-financial services such as extension and Business Development Services. A new Microfinance Law, passed in April 2004, clarified previous legal ambiguities under which MFOs were operating before. Just as with the microfinance sector, the leasing industry is also in its initial stages of development. A leasing law was passed in April 2003 with the help of the IFC under the first phase of its Central Asia Leasing Facility Project. The law sets out a framework for financial leasing and related accounting, in accordance with international standards. There is expected to be a follow-on second phase to this project which will assist banks and institutions active in this sector to develop and improve their leasing operations. For further information on the structure of the financing sector and macro economic information, please refer to the website of the National Bank of Tajikistan – www.nbt.tj/en 3.2 Reform of Business Licensing and Inspections Enormous progress has been achieved in the past 2 years in the fields of business licensing. In 2005 the Government adopted a new licensing law that reduced the number of activities subject to licensing from around 1,500 to 113. Another important facet if this law was that it also adopted a regulatory framework to implement and administer the law. Further to this, amendments were passed to the 2005 law that reduced the number of activities down to 65. Work is continuing, with the help of a number of donors, to further reduce this number and to continue to clarify implementation practices to continue enhancement of the improved business climate. According to a recent report of the World Bank (Doing Business 2007), the burden imposed by Tajikistan’s licensing regime is now less than that of 28 comparator countries in Eastern Europe and Central Asia and now much more resembles the situation prevalent in OECD countries.

- 13 -

In addition to the above, work is ongoing with the help of donors such as the IFC with regards to the minimisation of the requirement to obtain permits for business purposes. A study was recently completed (January 2007) and further work and reforms will be undertaken in light of this. It should also be noted that a law on inspections and amendments to the tax code have recently been adopted and it is foreseen that, by the end of 2007 a number of further Decrees and amendments to various laws will be introduced and passed by Parliament to strengthen the work done to date and reduce the burden on business of inspections by government agencies and ministries. 3.3 Legal Environment 3.3.1 Company structures available in Tajikistan The current Civil Code (CC) of the Republic (RT) allows for the formation of legal entities as commercial and non-commercial organizations. According to article 50 of CC RT, commercial organizations are defined as legal entities which pursue profit as the basic purpose of their activity. The current law provides for the following types of commercial organizations: a) Partnerships b) Companies (Limited Liability Company {LLC}; Additional liability company {ALC}; Joint- stock companies {close and open types}) c) Other commercial organizations (Producers’ cooperative; Unitary enterprise {state}) Given the nature of the planned investments under this proposal, it is likely that the “company” structure will be of most interest to investors. 3.3.2 Company structure overview The legal status of an LLC and an ALC is overall provided by CC RT. LLCs are also covered by the Law “On limited liability companies” № 53 dated May 10, 2002. Article 5 of the Law “On LLC” defines that a company is a commercial organization whose authorized capital is divided into shareholdings, the size of which is defined by the constituent documents of the company and that shareholders only carry liabilities in accordance with the value of their contribution. Article 105 of CC RT defines an ALC the same as an LLC, except that shareholders liabilities can be more than their contribution. Shareholders in LLCs and ALCs can be both physical persons and legal entities. The number of shareholders of an LLC or ALC cannot exceed 30. According to article 17 of the present Law “On foreign investments”, the minimum size of the contribution of a foreign shareholder in the authorized capital of a company should be not less than ten thousands minimum wages (currently 200 000 Somoni, or approximately USD 58,000). At the moment of registration of a company at least 50 % of the authorized capital should be fully paid up. The balance should be paid within a year of registration of the company. Joint stock companies (JSCs) can either be of a closed or open format. For the former type, the number of shareholders cannot exceed 50 and are available only to the founders or initially defined group. The latter type can be made up of any number of shareholders and each shareholder has the right to dispose of or sell their shares without the express consent of the other shareholders. The operations and rules pertaining to JSCs are contained in the Law “On Joint Stock Companies”. The size of charter capital and pay up requirements for a JSC with foreign investment is the same as for LLCs and ALCs.

- 14 -

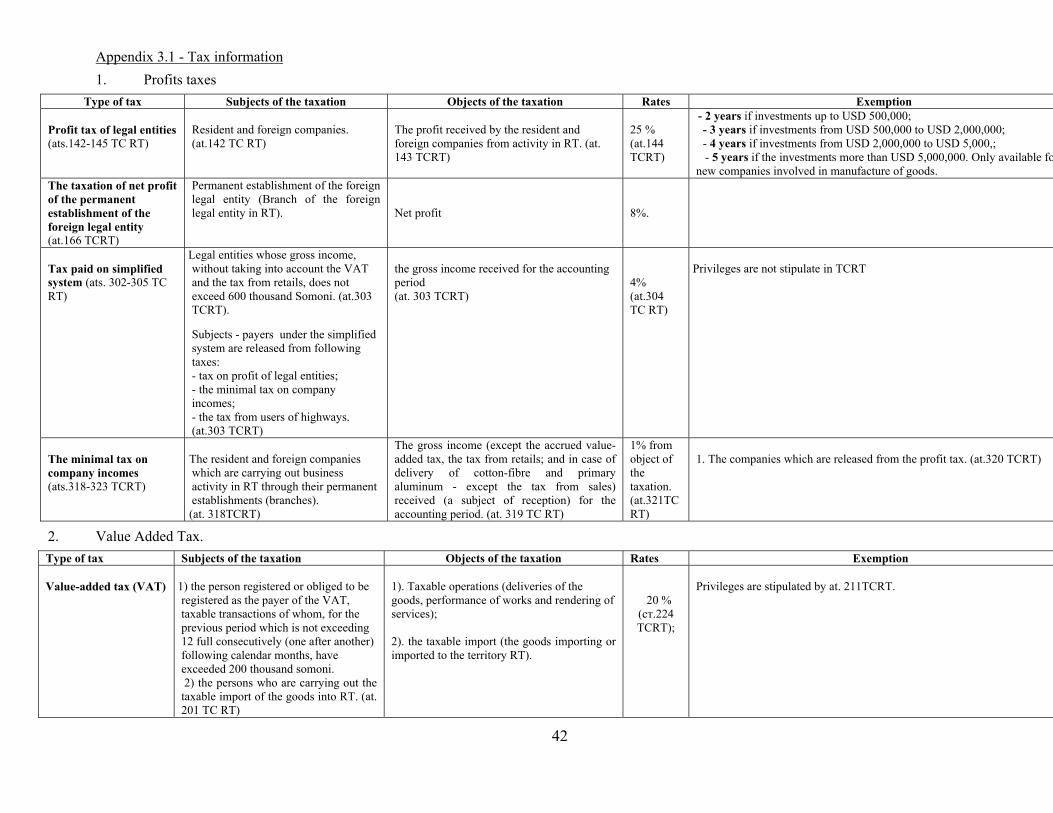

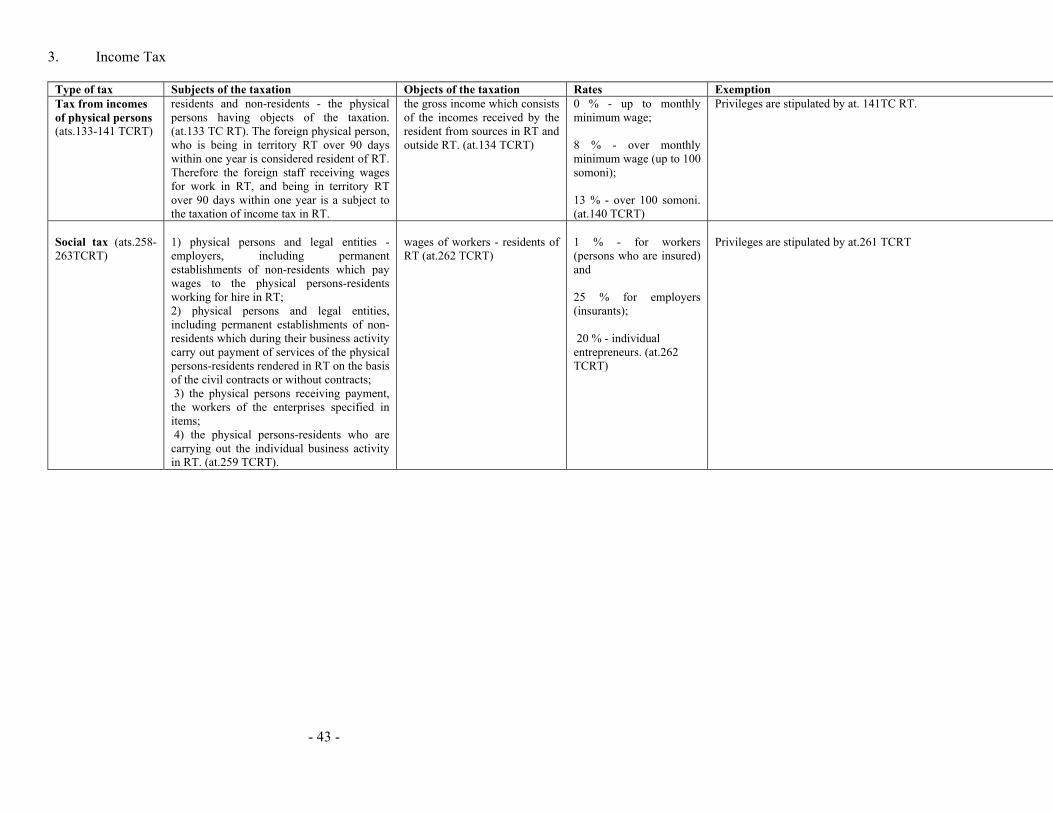

3.3.3 Company Registration Procedures The state registration of a JSC or LLC/ALC is carried out in accordance with the Law «On state registration of the legal entity» №5, dated April 22, 2003. According to this Law the body registering all legal persons within the Republic is the Ministry of Justice. Documents required for registration should be presented to the Ministry within one month after the formal decision to create the company. The state registration should be completed within 10 working days from the moment of presentation of the documents, at which time it should receive the certificate of registration. Within 10 days after registration, the company should apply and receive statistic codes from the State Committee of Statistics (subject to presentation of required documentation). The company should receive the codes within 3 days of its application. Finally the company should register with the tax authorities of the Republic and this should be done within 30 calendar days of the company’s registration with the Ministry of Justice. 3.3.4 Import duties for equipment Import of goods to the Republic are subject to Customs duties. At the moment, Customs duties vary from 5 to 15% of the value of the goods, depending on their nature and origin. However, article 345 of the Customs Code does provide for certain privileges with regards to the standard duties. For example, there is an exemption from duties if the imports are of industrial or technical equipment (and their components) if the imports are for the formation of or addition to the authorised capital of the company or modernisation of the means of production. 3.3.5 General taxation Taxes are levied on companies at the national and local governmental levels. National level taxes include:

a) the income tax from physical persons b) profit tax from legal entities c) value-added tax (VAT) d) excises e) social tax f) land-tax g) tax from users of highways h) the customs duties and other customs payments i) State Duty j) sales tax (of cotton-fibre – 10% of FOB value) k) minimal tax on incomes of the enterprises

Local taxes include:

a) tax on real estate b) tax from owners of vehicles

A detailed list of taxes, their current levels and exemptions are contained in appendix 3.1. 3.3.6 Cotton exportation In order to export cotton from the Republic, registration of the contract and permission from TUGE is required. In order to obtain such permission, the following documents need to be presented to the TUGE:

- 15 -

(i) Covering letter from the Seller in stating efficiency and expediency of the contract.

(ii) The certificates of verification made and signed by the parties to the contract on financing of cotton production (the farmer and the Investor).

(iii) The warehouse information which should include data concerning the location of the goods and a year of a crop.

(iv) Quality certificate (v) Phyto-sanitory certificate (vi) Certificate of origin (vii) Acknowledgement that the producer of the cotton did not have contractual

obligations to other investors for the cotton in question.

In addition to the above documents, in order to execute export, the following documents are required: i) Letter of attorney of owners of production on each sold lot

ii) Bank acknowledgement of payment iii) Acknowledgement of payment of all appropriate taxes (the tax from sales)

3.4 Overview of other agricultural sector projects In order to support the Government’s ongoing work in reforming the agricultural sector, a number of international financial institutions are active in the sector. Following is a list of such projects and short descriptions of them. 3.4.1 World Bank Projects a) Ferghana Valley Water Resources Management Project. The project objectives are (i)

to improve the capacity for increased productivity of irrigated agriculture in the Ferghana Valley by improving land and water management and (ii) to improve safety and regulation of the Kayrakum Dam and Reservoir, thereby contributing to enhanced water management security and efficiency at the basin level.

b) Land Registration & Cadastre System for Sustainable Agriculture Project. To expand

farm privatization through a repeater project to enable more rural people to become independent farmers and take management decisions in response to market forces, by providing them secure land use rights certificates distributed in a transparent and fair manner, and providing essential complementary support services.

c) Community Agriculture & Watershed Management Project. The project objective is

to build the productive assets of rural communities in selected mountain watersheds, in ways that sustainably increase productivity and curtail degradation of fragile lands and ecosystems.

d) Rural Infrastructure Rehabilitation Project. The project’s objective is to increase

water supply and efficiency in the main and secondary irrigation canals supplying the farms being privatized under the Farm Privatization Support Project and adjoining farms.

e) Farm Privatization Support Project. The project objective was to develop procedures

and institutional mechanisms at the state level and selected regions to ensure fair, secure and equitable transfer of land and other farm assets to private individuals or groups and create sustainable private family farming units and provide them with the enabling conditions to operate independently in a market economy.

- 16 -

3.4.2 Projects of other donors a) Sustainable Cotton Subsector Project (ADB). The project consists of two

components: 1) farm-by-farm analysis and debt resolution, 2) market development project with four sub-components: (i) Tajik standard upgrade, (ii) joint venture on cotton grading, (iii) export facilitation methods including facilitation of bonded warehouse establishment for cotton, and (iv) training and cotton upgrading awareness.

b) Agriculture Rehabilitation Project (ADB) The main thrust of the Project is

rehabilitation of the selected irrigation and drainage facilities, which are in a critical state of disrepair; provision of associated farm production support services; and construction of rural water supply in main cotton production regions of Khatlon and Sughd. In parallel with these, the Project aims to accelerate the ongoing agriculture reform process by building capacity of the public sector agencies as well as farmers’ organizations.

c) Rural Development Project (ADB). The Project (i) address land use security; (ii)

develop policies and strategy for more effective pasture land management and capacity development; (iii) improve the administration and institutional aspects of business development; (iv) address the capacity and technical aspects of degradation of arable, pasture, and forest lands; (v) establish independent agriculture and rural business advisory services; (vi) establish an effective market information system; (vii) provide microcredit; and (viii) improve rural infrastructure in communities and raions.

d) Support to Seed Sector Development in Tajikistan (SIDA). The overall objective of

the project is to create a seed industry in Tajikistan which works according to internationally accepted standards, enabling it to produce high-quality seed of modern varieties for Tajik farmers.

e) Support for Development of Third Party Arbitration Court (DFID). The project is

implemented by the team of consultants who had the necessary experience accumulated under a similar project in Russia. The aim of the farm debt restructuring component is to develop a debt restructuring mechanism that will make it possible to reduce the debt burden on cotton-growing farms, including options available under third party arbitration.

f) Increase Agricultural Sector Productivity (USAID). The objective is to invest in

agricultural development through Agricultural Finance Plus (AgFin+) by working with targeted groups and markets, and assisting them to identify opportunities and overcome constraints in the farm-to-market value chain. USAID also provide assistance to Water User Associations, including replication of efficient irrigation demonstration models; expanding public outreach to farmers, government, and other donors; and implementation of a competitive small grants program.

g) Farm Ownership Model (IFC). The project consisted of establishing SudAgroSerice

(SAS), a company owned by farmer shareholders, which provided financing, technical advice, inputs supply and marketing services to cotton farmers as an alternative to the “futurist” financing model. The company operates in the northern oblast of the country, but has also recently begun assisting IFC with the provision of consulting services to on bank in the southern part of Tajikistan to assist that bank in expanding its cotton lending activities.

- 17 -

4.0 Government of Tajikistan and World Bank Cotton Sector Recovery Project 4.1 Overview The total value of project is USD 15 million. It addresses a number of issues. Debt resolution will be the initial focus, but the broad emphasis will be on measures to reform policy, increase competition, encourage private sector investment and increase producer incomes. The project therefore provides a means to translate the newly completed agriculture strategy into action, a strategy that identifies land reform and cotton sector recovery as the two pillars of future sector growth. The various activities foreseen under the project will also act as a support to the Government’s recently adopted Road Map for reform of the sector. The project was approved by the Independent Commission on February 20th, 2007 and is expected to be submitted for the World Bank Board's consideration in May 2007. It is currently planned that an international conference about investment opportunities will be held in Dushanbe in September 2007. It is expected that the project will become fully operational and have available funding in the last quarter of 2007. 4.2 Project objective and phases The aim of the project is to support government efforts to rejuvenate the cotton sub-sector and create the conditions for sustainable growth of Tajik cotton production. In addition to resolving the debt crisis, the project will guide and support policy reforms conducive to increased competition and higher producer returns; and demonstrate the capacity of privately owned family farms to drive future cotton production given suitable conditions. These conditions, which represent the vision for future sector development, include: possession of a secure land use certificate specifying individual ownership rights; the right to choose how farm land is used as the basis for profitable and sustainable land use; ready access to essential resources for farming (finance, farm inputs, machinery and water); unrestricted access to a range of input and output market outlets; producer rights to choose who they associate with; and ready access to relevant information on modern farm technology. The project will focus on debt resolution and policy reform during the first two years of operation, accompanied by the establishment of new ginneries in 4 to 5 selected districts in Khatlon, by international cotton companies. These ginneries will service at least 40% of cotton output in a region that is the main cotton producing area of Tajikistan. As these ginneries strengthen and grow during years 2-5 they will demonstrate the benefits of active competition for producers, processors and exporters and provide guidance on how this experience can be extended to other cotton growing areas. The potential beneficiaries would be a rural population of 525,000 people living on 66,000 hectares of irrigated land, and the people providing goods and services to farms in 4 to 5 participating districts. Their incomes are expected to rise as a result of the project through increased yields, lower costs of production and better access to markets. 4.3 Project Components 4.3.1 Debt Resolution A transparent, rule-based mechanism for debt repayment is being prepared jointly with ADB as the basis for debt resolution. This mechanism will ensure that producer payments are commensurate with their ability to repay, and that the viability of the current financial system is preserved. Farmer participation will be subject to possession of a land certificate, and farmers will receive project support to obtain their land titles. Most notably, farmers will be “de-linked” from their creditors and a special Agency and financial vehicle (SPV) will be created to facilitate collections of repayments and transfer of monies owed to creditors. Therefore, farmers will be free to contract with whoever they wish and on the basis of competitive pricing for their outputs. This system will be applied nationally, not only in the selected project districts.

- 18 -

4.3.2 Support for Policy Analysis and Reform The project’s impact at the national level will depend heavily on the capacity of government to act decisively in the areas of debt resolution, competition, land use and local government activity. To strengthen policy analysis and advice on policy reform in these areas a senior international policy adviser will be appointed to work with designated counterparts in the Independent Commission and the President’s Office. This input has been directly requested by the President. In addition to daily contact with senior government personnel, the international policy adviser will prepare policy briefs on all major issues, conduct national and regional seminars on critical policy issues, manage the input of short-term advisers brought in to strengthen particular areas of analysis, and organize training and study visits. 4.3.3 Cotton Supply Chain Development Cotton production is hampered by serious deficiencies throughout the cotton supply chain. Producers lack the incentives, resources and knowledge to raise production as a result of: inadequate access to inputs, low producer prices, and sub-optimal crop husbandry and farm management. Processing efficiency is low as a result of minimal competition between ginneries and marketing is hampered by inadequate grading and certification procedures and minimal competition between current operators. The project will address deficiencies associated with production, seed, processing and competition. a) Cotton Ginneries This sub-component will promote foreign direct investment in ginneries in selected districts and demonstrate the impact of increased competition on producer incentives. Foreign direct investment will be conditional on local government agreement to allow producers to use their land as they choose and to choose the enterprises with whom they contract for ginning and input supply. Farmers will benefit from more transparent business and contractual relationships, more efficient processing and fairer prices for inputs and output. Foreign partners will be required to bring not only capital, but also operational experience, access to premium sales markets, working capital and technical expertise as the basis for maximizing processing efficiency. To this end, the project will seek partnerships with strategic investors who have experience in cotton processing and international trading. These investors will be encouraged to finance cotton gins in 4 to 5 project districts, potentially together with IFC who will, subject to review of the business proposal and potential partner, take a minority shareholding and/or provide debt finance. It is envisaged, therefore, that the foreign investor will retain a majority (85– 90%) shareholding of the enterprise. Incentives to invest will also be enhanced by the availability of a MIGA guarantee against losses incurred as a result of political instability (see section 6 below). To supplement FDI and IFC equity/debt investments, the project will provide a revolving credit line to be used for working capital. Each ginning enterprise will sign a sub-credit agreement with the Ministry of Finance, acting for and on behalf of the Government of the Republic of Tajikistan, with a designated commercial bank as the channel for disbursement and collector for repayment. Prior to signing the sub-credit agreement, each application will have to be reviewed and approved by a loans committee and IDA. The maximum loan allowed under the credit line will be 50% of the total seasonal finance extended by the ginning venture to its contracted farmers in any one season. The marketing arrangements between farmers and the gin venture will be based on commercial negotiation, subject to the following provision: all marketing arrangements must be based on a clear price formula which relates seed cotton deliveries to the international price for baled cotton, as provided for in the Minimum Price Methodica maintained by the Commodities Exchange in Dushanbe. This formula, which denotes the minimum prices to be paid for seed cotton, will allow transparent management of the credit line and also improve the transparency of transactions between farmers and the ginning ventures.

- 19 -

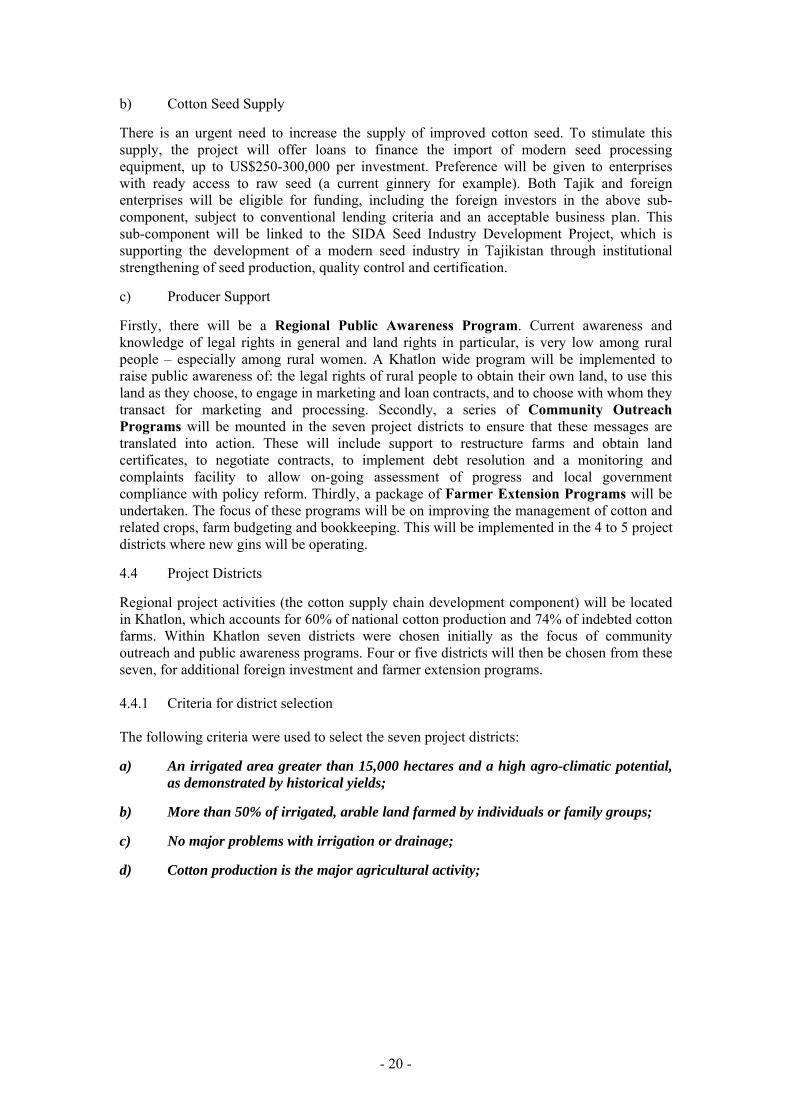

b) Cotton Seed Supply There is an urgent need to increase the supply of improved cotton seed. To stimulate this supply, the project will offer loans to finance the import of modern seed processing equipment, up to US$250-300,000 per investment. Preference will be given to enterprises with ready access to raw seed (a current ginnery for example). Both Tajik and foreign enterprises will be eligible for funding, including the foreign investors in the above sub-component, subject to conventional lending criteria and an acceptable business plan. This sub-component will be linked to the SIDA Seed Industry Development Project, which is supporting the development of a modern seed industry in Tajikistan through institutional strengthening of seed production, quality control and certification. c) Producer Support Firstly, there will be a Regional Public Awareness Program. Current awareness and knowledge of legal rights in general and land rights in particular, is very low among rural people – especially among rural women. A Khatlon wide program will be implemented to raise public awareness of: the legal rights of rural people to obtain their own land, to use this land as they choose, to engage in marketing and loan contracts, and to choose with whom they transact for marketing and processing. Secondly, a series of Community Outreach Programs will be mounted in the seven project districts to ensure that these messages are translated into action. These will include support to restructure farms and obtain land certificates, to negotiate contracts, to implement debt resolution and a monitoring and complaints facility to allow on-going assessment of progress and local government compliance with policy reform. Thirdly, a package of Farmer Extension Programs will be undertaken. The focus of these programs will be on improving the management of cotton and related crops, farm budgeting and bookkeeping. This will be implemented in the 4 to 5 project districts where new gins will be operating. 4.4 Project Districts Regional project activities (the cotton supply chain development component) will be located in Khatlon, which accounts for 60% of national cotton production and 74% of indebted cotton farms. Within Khatlon seven districts were chosen initially as the focus of community outreach and public awareness programs. Four or five districts will then be chosen from these seven, for additional foreign investment and farmer extension programs. 4.4.1 Criteria for district selection The following criteria were used to select the seven project districts: a) An irrigated area greater than 15,000 hectares and a high agro-climatic potential,

as demonstrated by historical yields; b) More than 50% of irrigated, arable land farmed by individuals or family groups; c) No major problems with irrigation or drainage; d) Cotton production is the major agricultural activity;

- 20 -

Figure 4.1 – Irrigated land Khatlon (by district)

Figure 4.2 – Yield of seed cotton per hectare Khatlon (by district)

Figure 4.3 – Total seed cotton production Khatlon (by district)

- 21 -

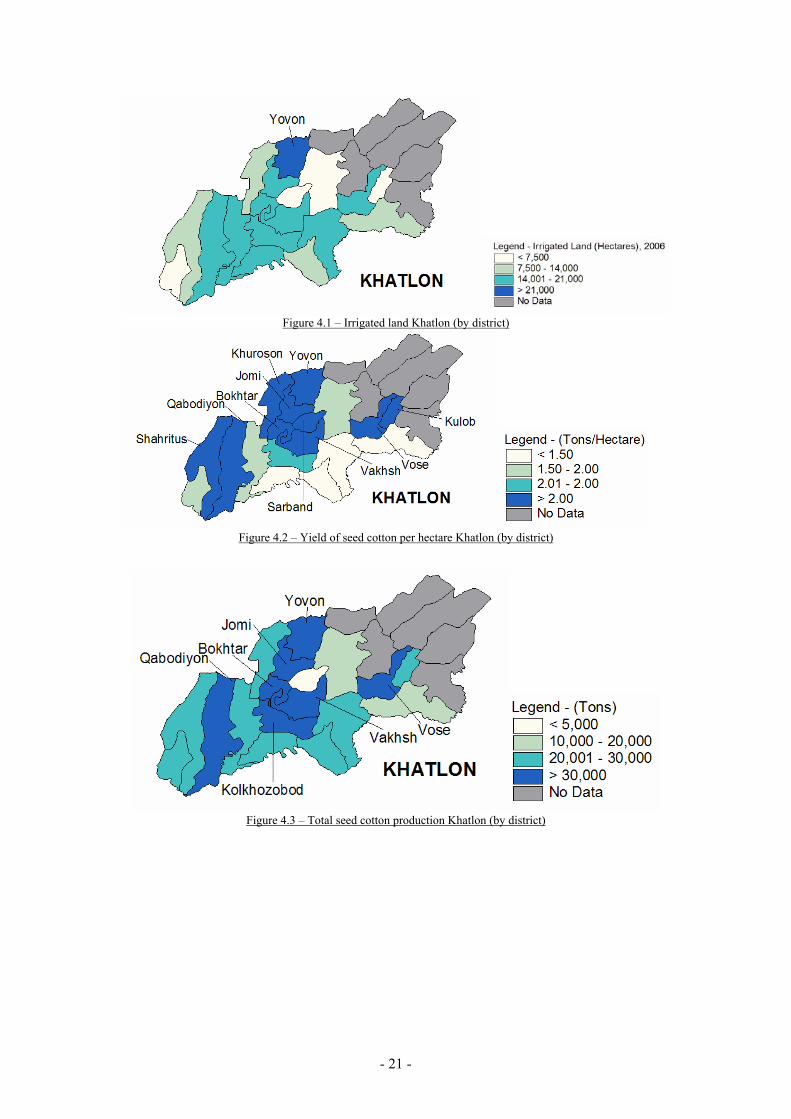

Figure 4.4 – Percentage arable land under private use Khatlon (by district)

Figure 4.5 – Percentage land sown to cotton Khalton (by district)

e) Selected project districts represent both Kurgan-Tyube and Kulyab zones; f) An average cotton debt greater than $500/ha;

Figure 4.6 – Average debt per hectare Khalton as of 01/01/2005 (by district)

g) A high incidence of rural poverty (over 50%); h) At least four investors are operating in the selected districts, without preferential support from local authorities; i) Proximity of other World Bank agricultural projects to enhance project activity.

- 22 -

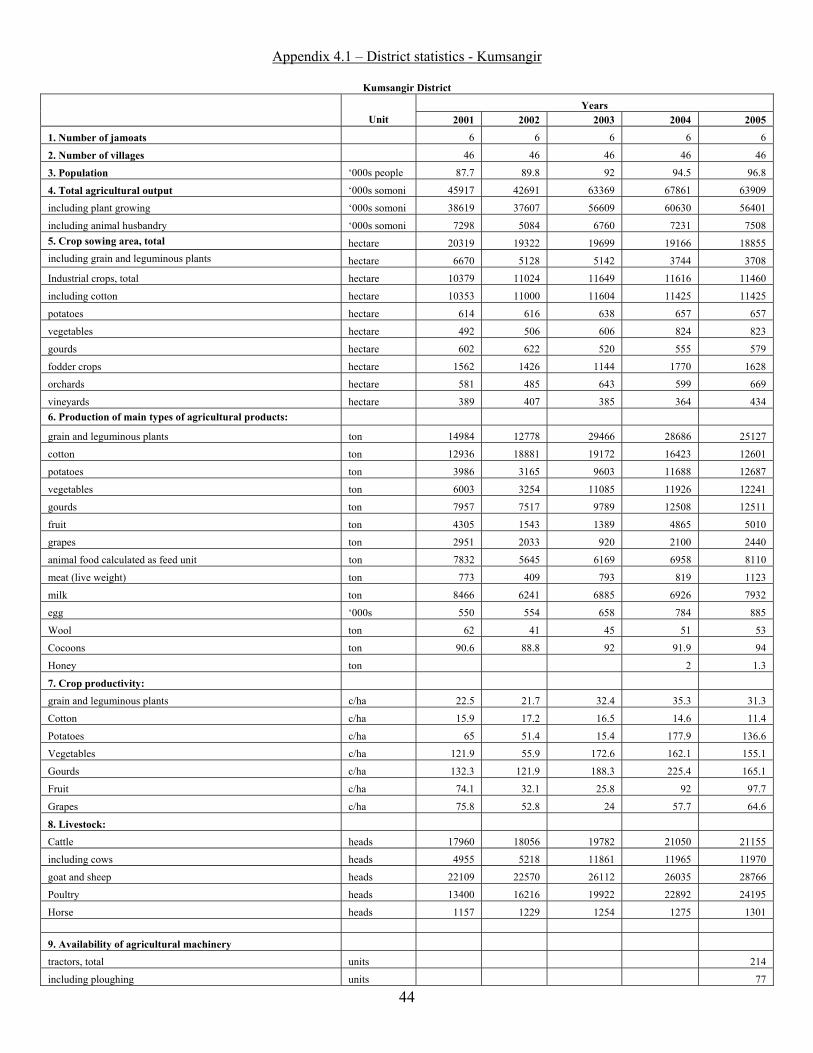

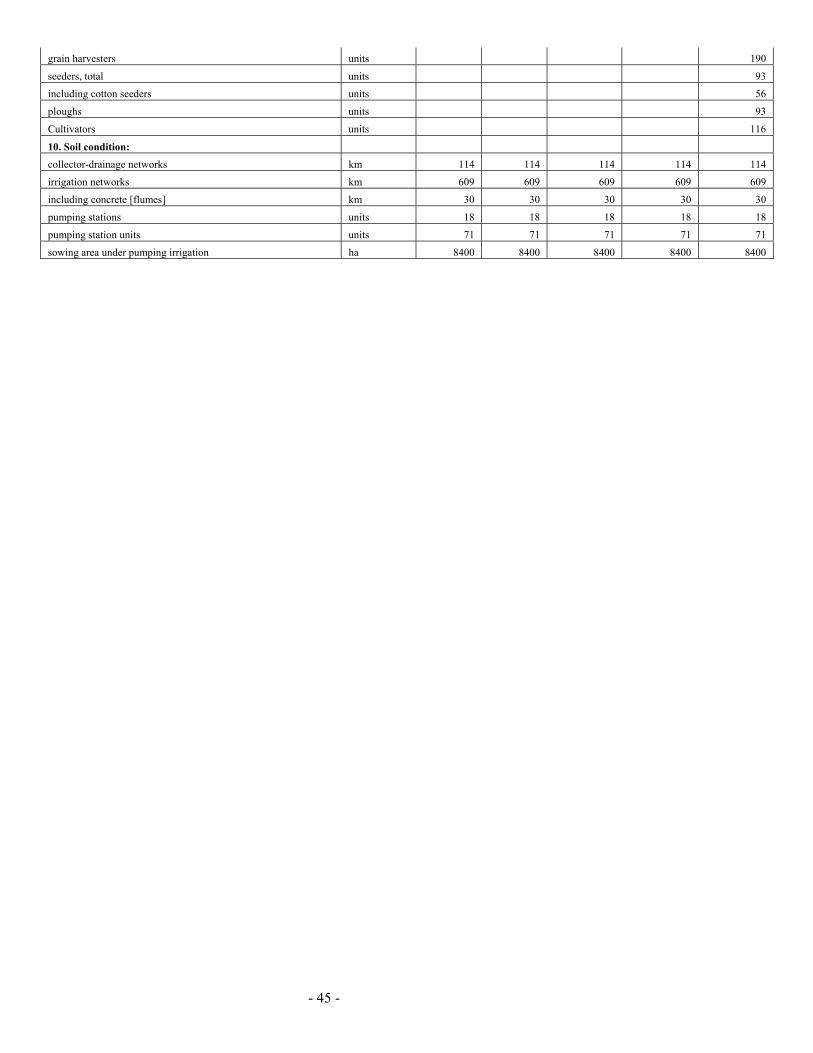

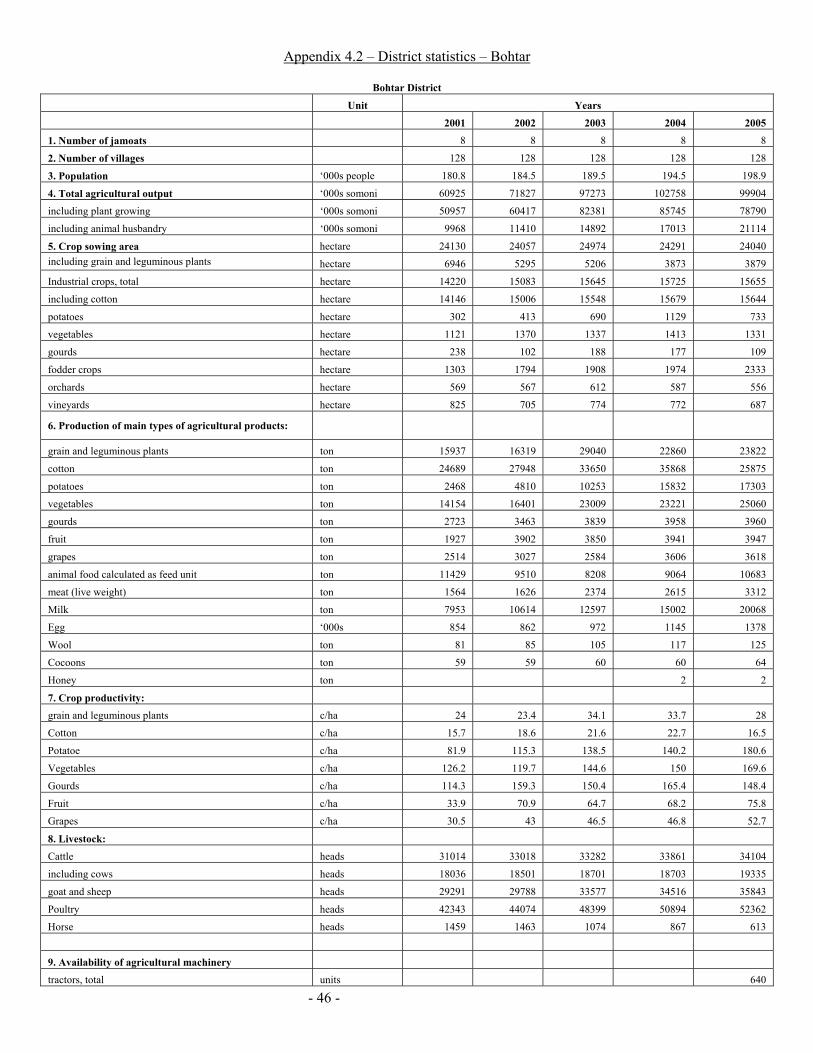

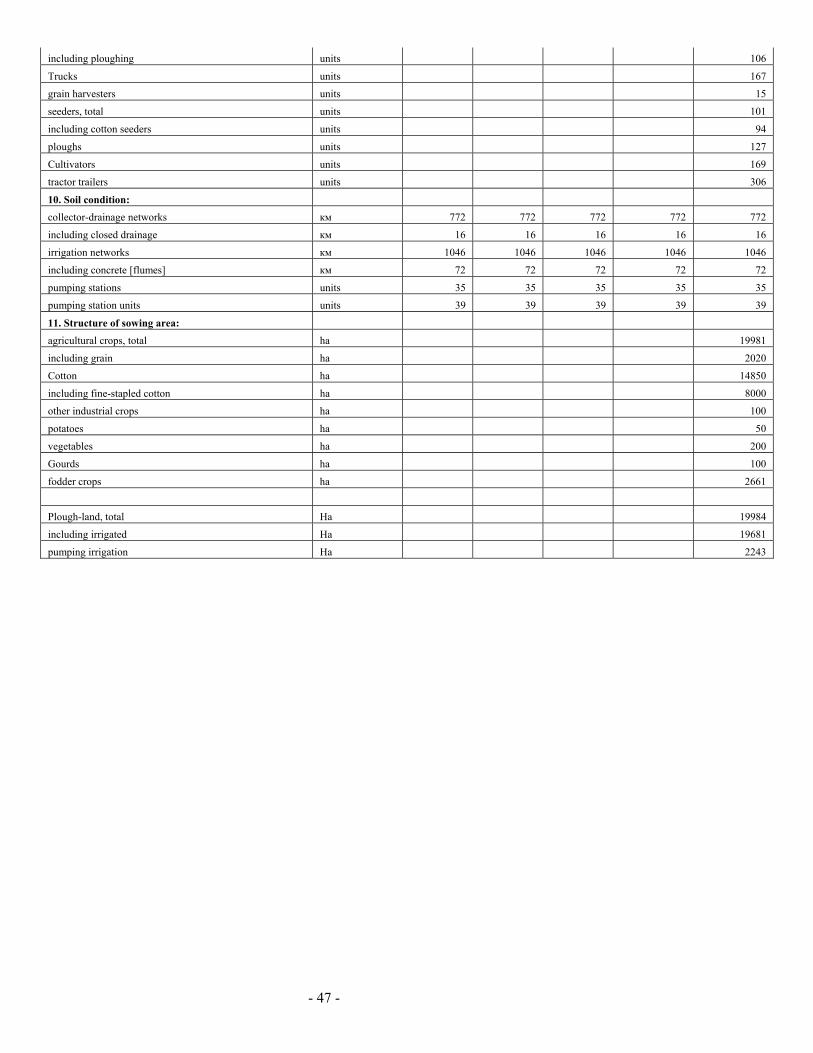

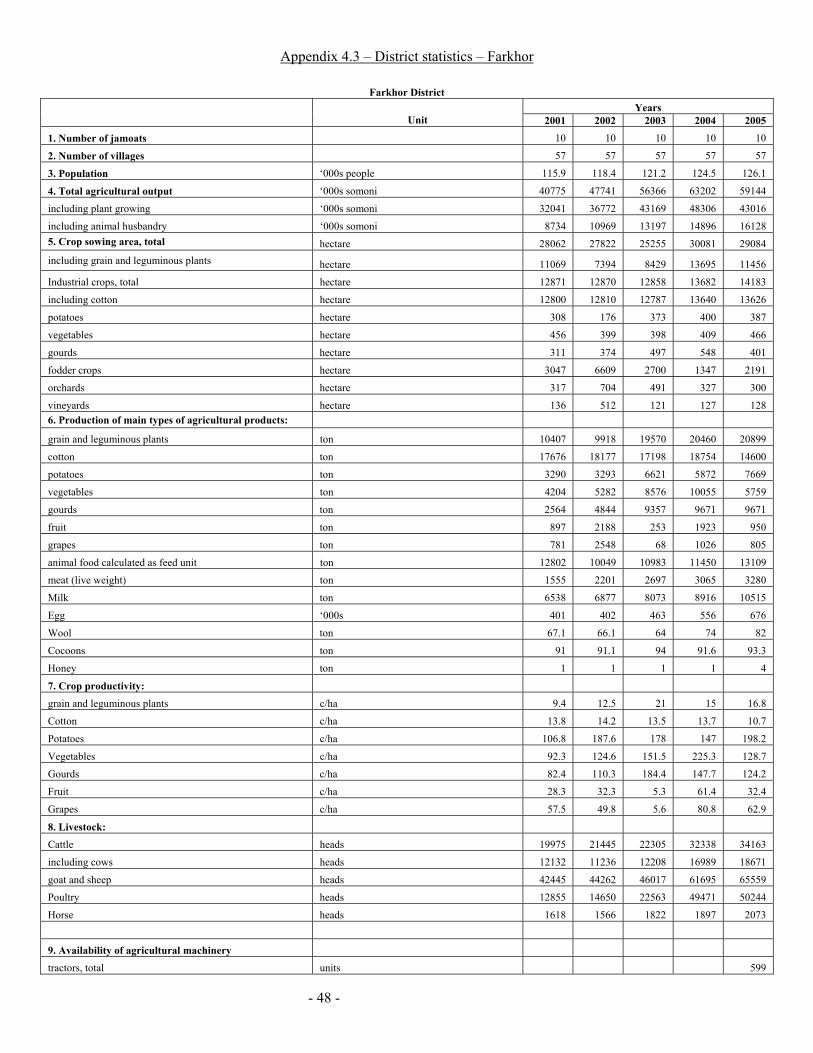

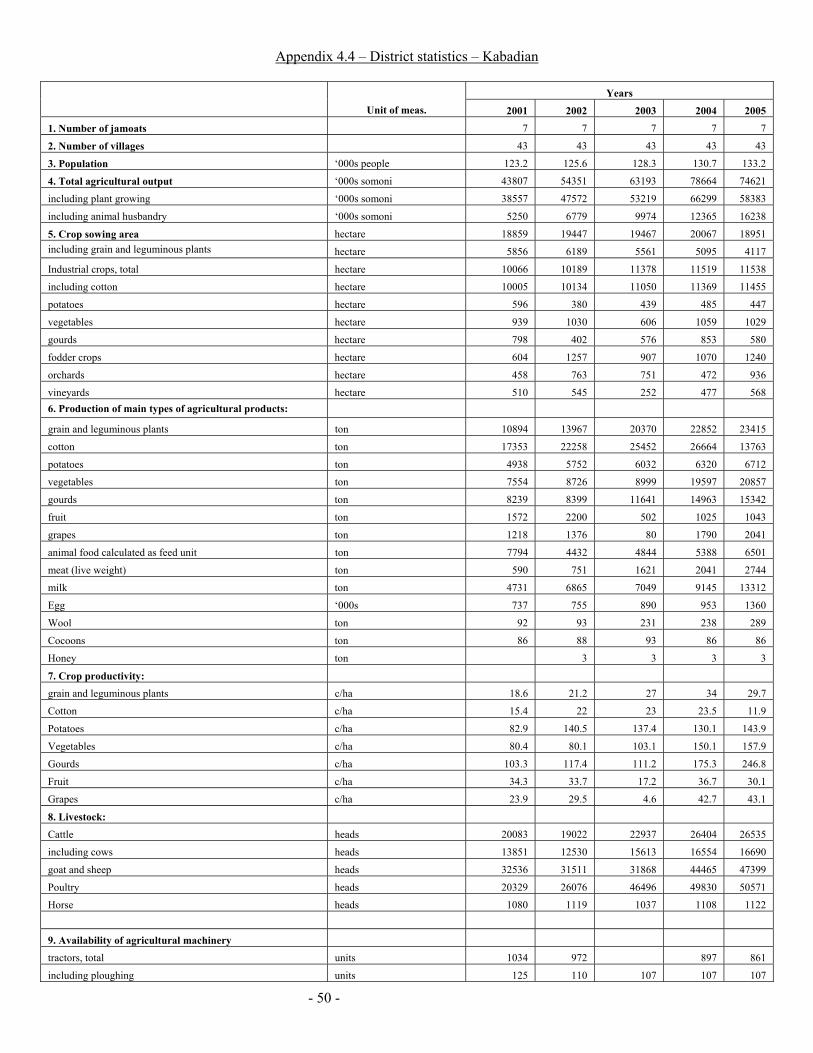

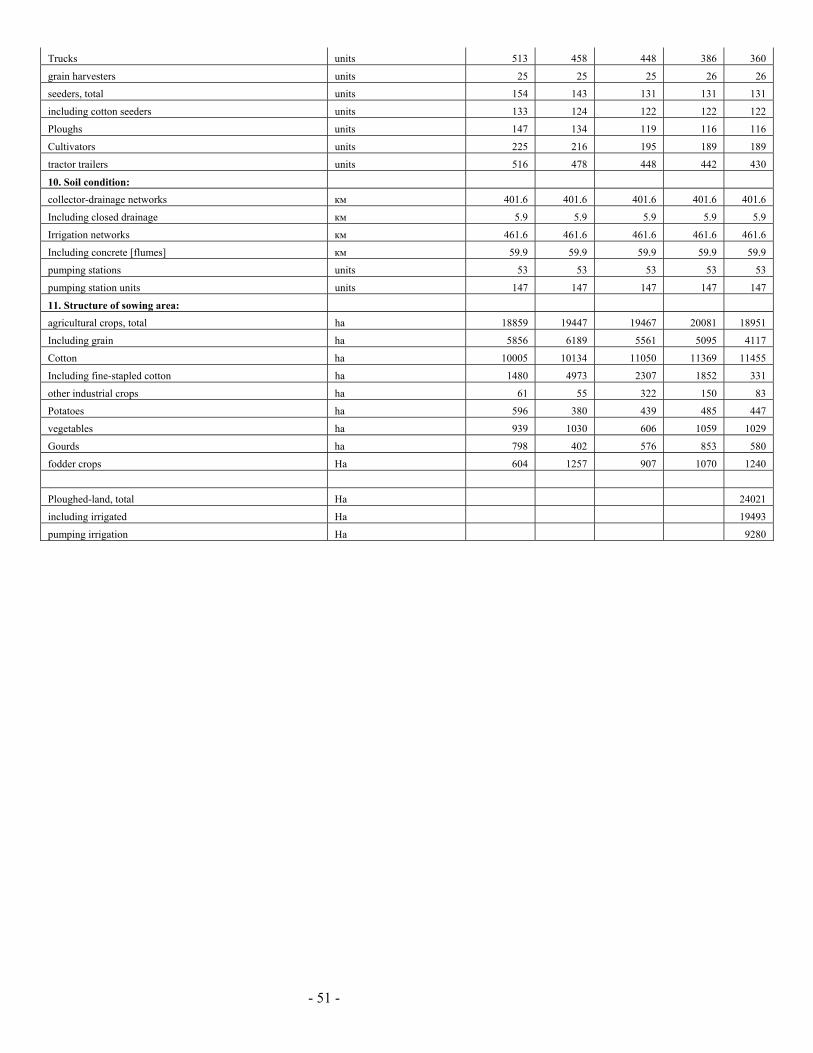

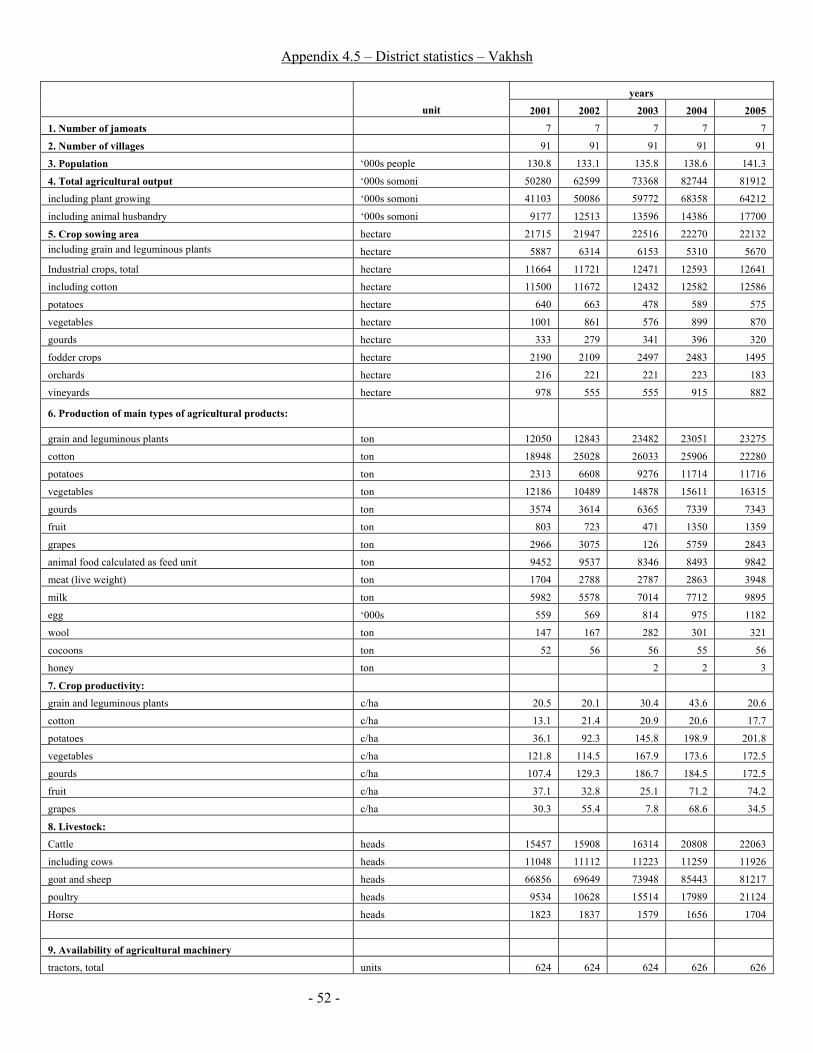

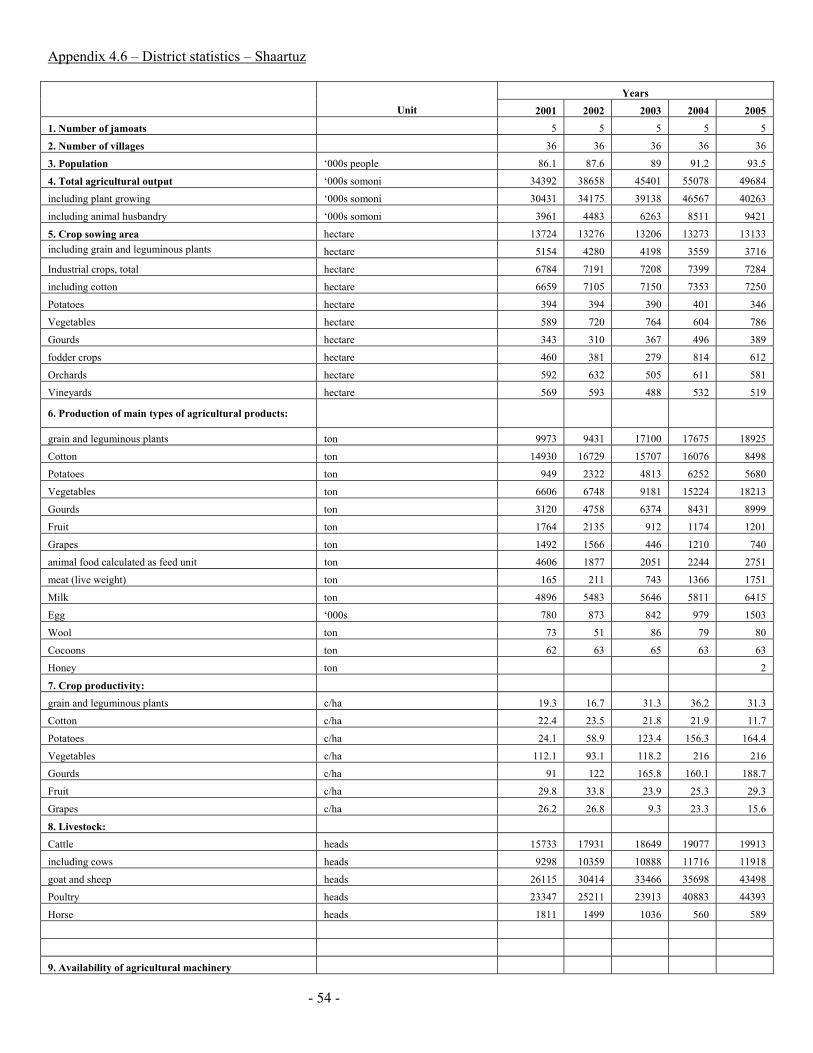

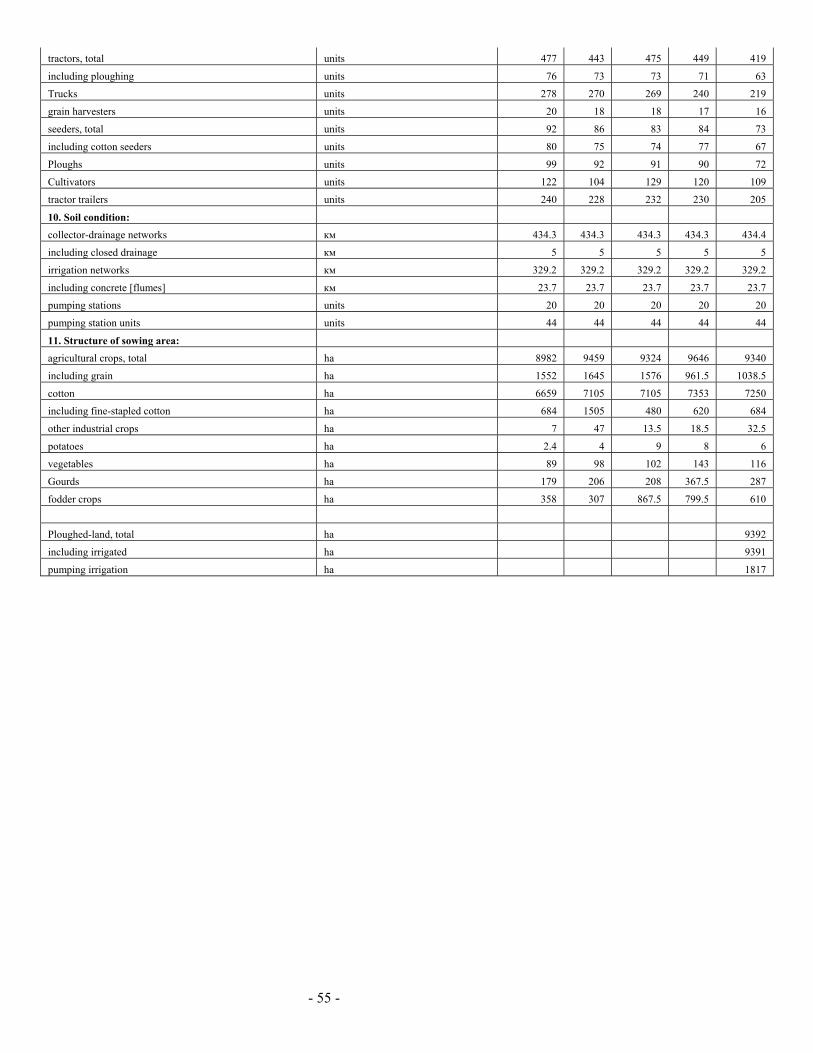

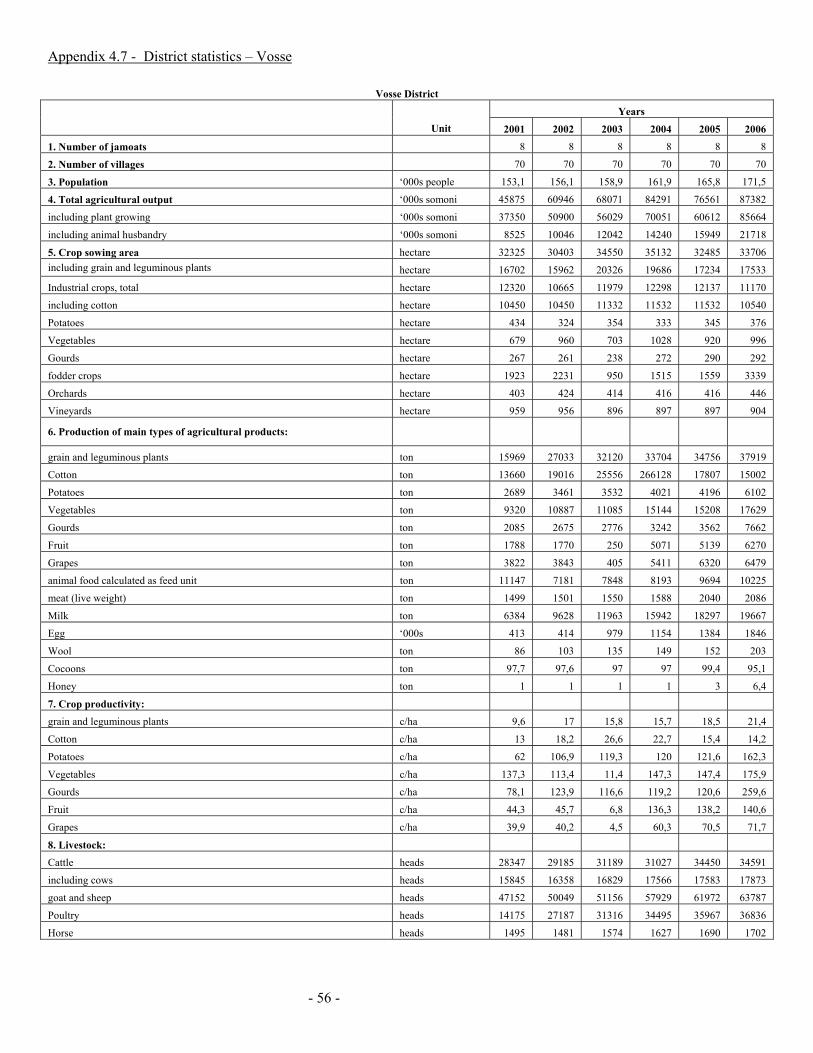

4.4.2 Preliminary selected districts Based on the above criteria Bokhtar, Kumsangir, Farkhor, Kabadian, Vaksh, Vosse and Shaartuz were chosen as the seven districts for project activity. Foreign investment and farmer extension programs will be implemented in four to five of these districts. Government approved this selection during the meeting of the Independent Commission on June 26, 2006 (minutes #7). Agriculture is the main economic activity in all project districts. Cotton is the most important crop, with 62%-74% of total agricultural production. Agro-climatic conditions are well suited to cotton production and are typical of the Khatlon region. Current yields are low but national experts estimate that they could be increased to 3.0 to 3.5 t/ha with higher input use. The major cotton investors in the project districts are: Ismoili Somoni Century ХХI, Tamer, Olimi Karimzod, Rakhsh, Pakhtai Khatlon, Zamin-textil, Somoni, Faizi Vakhsh. Generally, a single investor operates in each district currently. All districts are served by at least one ginnery and although there is ample ginning capacity, outturn rates are low (range from 28%-33%) and competition basically non-existent. Statistical data on the 7 districts can be found in appendices 4.1 to 4.7. Further information on the districts will be made available to potential investors, meeting with the initial investor criteria and how demonstrate concrete interest in the project.

- 23 -

5.0 IFC 5.1 About IFC The International Finance Corporation is the private sector arm of the World Bank Group. IFC’S mission is to help reduce poverty and improve people’s lives by promoting sustainable private sector investment in developing countries. IFC invests primarily in enterprises majority-owned by the private sector, in addition to providing technical assistance and advisory services. 5.2 IFC’s added value to potential investors Although IFC lends on market terms, it does not compete with, but complements, private capital. IFC is a long-term partner for good and bad times. IFC invests in projects that meet its investment criteria, but that cannot get financing or technical expertise elsewhere on reasonable terms. IFC has extensive knowledge of how to do business in developing countries and excellent relationships with developing country governments. As an independent international organization, IFC can help companies and sponsors negotiate with host governments. By working with IFC, companies draw on the expertise and reputation of a partner recognized for its strong social and environmental safeguards. Companies worldwide are recognizing that long-term profitability is best enhanced when investments are made in a sustainable way. 5.3 IFC’s Products and Services 5.3.1 Equity and Quasi-Equity IFC risks its own capital by buying shares in project companies, other project entities, financial institutions, and portfolio or private equity funds. IFC can generally subscribe to between 5 and 20 percent of a company’s equity. IFC will not normally hold more than a 35 percent stake or be the largest stakeholder in a project. With quasi-equity instruments, IFC invest through products that have both debt and equity characteristics. 5.3.2 Loans and Intermediary Services IFC finance projects and companies through A-loans, which are for IFC’s own account. IFC cannot accept government guarantees as security for its loans. The maturities of A-loans generally range between seven and 12 years at origination, but some loans have been extended to as long as 20 years. IFC’s loans are provided in major currencies and in an increasing number of emerging market currencies. IFC also make loans to intermediary banks, leasing companies, and other financial institutions through credit lines that result in further on-lending. These credit lines are often targeted to smaller businesses. 5.3.3 Syndicated Loans Syndicated loans, or B-loans, play a critical role in IFC’s efforts to mobilize private sector financing in developing countries, thereby broadening their development impact. Through this mechanism, financial institutions share fully in the commercial credit risk of projects, while IFC remains the lender of record. Participants in IFC’s loans benefit from their status as a multilateral development institution, including their de facto preferred access to foreign exchange. 5.3.4 Structured Finance IFC also offers structured finance solutions to clients, enabling them to raise a significantly larger amount of capital than that represented by IFC’s own exposure. Through partial credit guarantees of debt instruments, IFC use their triple-A rating to help clients diversify their funding sources, extend maturities and obtain financing in their currency of choice. IFC also helps clients structure securitizations and risk-sharing facilities, transactions that allow a client to sell off part of the risk associated with a pool of assets.

- 24 -

5.3.5 Risk Management IFC’s risk management products provide clients with access to long-term derivatives markets. Currency hedging instruments allow clients to hedge foreign exchange exposures typically related to foreign currency borrowings. 5.3.6 Technical Assistance and Advisory Services Technical assistance complements IFC’s investment activities by offering advisory and training services to private companies in developing countries. IFC deliver many of these services through donor-supported technical assistance facilities that focus on either a region or a strategic aspect of development 5.4 Eligibility of the project To be eligible for IFC funding, a project:

- Must be located in a developing country that is a member of IFC - Must be in the private sector, with the exception of sub-national entities in

which IFC invests without a government guarantee - Must be technically sound - Must have good prospects of being profitable - Must benefit the local economy - Must be environmentally and socially sound, satisfying IFC environmental

and social standards as well as those of the host country 5.5 How can an investor apply for financing? A company or entrepreneur, foreign or domestic, seeking to establish a new venture or expand an existing enterprise can approach IFC directly by submitting an Investment Proposal. After this initial contact and a preliminary review, IFC may proceed by requesting a detailed feasibility study or business plan to determine whether or not to appraise the project. IFC can never be the sole source of financing; it typically provides up to 25 percent of the project costs for its own account and usually makes a minimum commitment of $1 million. The proposal can be submitted to an IFC industry sector department or to the IFC field office in Tajikistan; 91-10 Shevchenko Street Dushanbe, 734025 Tajikistan, Fax: (992-372) 51-00-42. 5.6 Where can an investor go for more information on IFC? IFC’s Web site is www.ifc.org . The Corporate Relations Unit (202-473-3800) directs callers to the right source for more specific information. The Webmaster ([email protected]) answers e-mail requests. Information on “Sustainable Investor”, IFC’s free, online newsletter on private sector development trends and issues, may be accessed from IFC’s Web site, www.ifc.org.

- 25 -

6.0 Multilateral Investment Guarantee Agency (MIGA) 6.1 What is MIGA? MIGA is a member of the World Bank Group and its mission is to promote foreign direct investment into developing countries. The Agency actively cooperates with public and private political risk insurers through coinsurance and reinsurance arrangements for joint coverage of eligible investment projects. 6.2 What is the relevance of MIGA for potential investors under the proposed project? MIGA has developed a guarantee program called the Small Investment Program (SIP) that is specifically designed for Small and Medium Investors (SMIs) investing in Small and Medium Enterprises (SMEs). MIGA helps the SME sector in emerging economies in two ways: (1) by providing political risk insurance (guarantees) to foreign investors who wish to invest in SMEs, and (2) by providing political risk insurance to financial institutions that will then lend to SMEs through affiliates. 6.3 What investments would be eligible? MIGA insures new investments destined for any developing country (such as Tajikistan) as well as investments directed at the expansion or restructuring of existing projects. The types of investments than can be covered include:

- equity - shareholder loans - shareholder loan guarantees (provided loan maturity minimum of 3 years) - commercial bank loans (subject to conditions) - other types of investments (subject to review and acceptance by MIGA)

6.4 What is an SME as covered by SIP? Investments in the non-financial sector (for example cotton or seed processing) are eligible for coverage if they are related to the establishment of an SME or to an existing SME in a developing member country such as Tajikistan. The SME must fulfil two out of three of the following criteria:

- No more than 300 employees - Total assets should not be more than USD 15 million - Total annual sales should not be more than USD 15 million

6.5 Who is an eligible investor as defined by SIP? Eligible investors include:

- Nationals of MIGA member countries - Corporations if they are either incorporated and have a principal place of

business in a member country, or if they are majority owned by nationals of member countries.

There are no restrictions under the SIP with regard to the size of the investor. However, the program is specifically designed to assist SMIs with their foreign direct investment activities. The application fee is therefore waived for SMIs. In order to qualify as an SMI, the company must have:

- No more than 375 employees - Have no more than USD 50 million in assets OR - Have no more than USD 100 million in annual sales

- 26 -

6.6 What is offered under a SIP guarantee? SIP guarantees have a term of up to 10 years (3 years minimum) with the possibility of an extension of up to another 5 years (at MIGA’s discretion). The maximum value of the guarantee is USD 5 million. There is no minimum amount of guarantee. The SIP covers up to 90% of the investment for equity and up to 95% for debt. While the total size of the investment may be larger than USD 5 million, the investment must be for an SME in the host country (i.e. Tajikistan). The SIP contract guarantee includes coverage for 3 types of risk:

- Currency Inconvertibility and Transfer Restriction - Expropriation - War and Civil Disturbance

6.6.1 Risk definitions

- Currency Inconvertibility and Transfer Restriction Protects against losses arising from an investor’s inability to convert local currency (capital, interest, principal, profits, royalties and other remittances) into foreign exchange for transfer outside of the host country. It also insures against excessive delays in acquiring foreign exchange due to host government action or failure to act.

- Expropriation Protects against losses arising from host government actions that may reduce or eliminate ownership of, control over, or rights to the insured investment. Coverage is also available for “creeping expropriation” – a series of acts that, over time, have an expropriatory effect. The terms of level of insurance cover for each of these types of risk are available upon request from MIGA.

- War and Civil Disturbance Protects against loss from, damage to, or the destruction or disappearance of tangible assets caused by politically motivated acts of war or civil disturbance in the host country. Such acts include revolution, insurrection, coups d’etat, sabotage and terrorism.

6.7 How to apply? The investor will need to complete a definitive application and submit it to MIGA. The application form can be completed on-line, however a signed copy should be submitted to MIGA by fax or mail. The application asks for the amount and type of investment, the development and environment impacts of the project and its financial and economic viability. The approval process should take no longer than 4 weeks to complete if all the information requested in the definitive application is filled completely and MIGA is supplied with all relevant project documentation. While the registration of the application is in effect, the implementation of the investment may commence. However, until MIGA’s analysis and due diligence is complete, the agency will not be able to commit to providing the requested guarantees. For further information or questions regarding SIP or the application process please refer to: Web site : www.miga.orgEmail : [email protected] : + 1 202 458 4798 Fax : + 1 202 522 2630

- 27 -

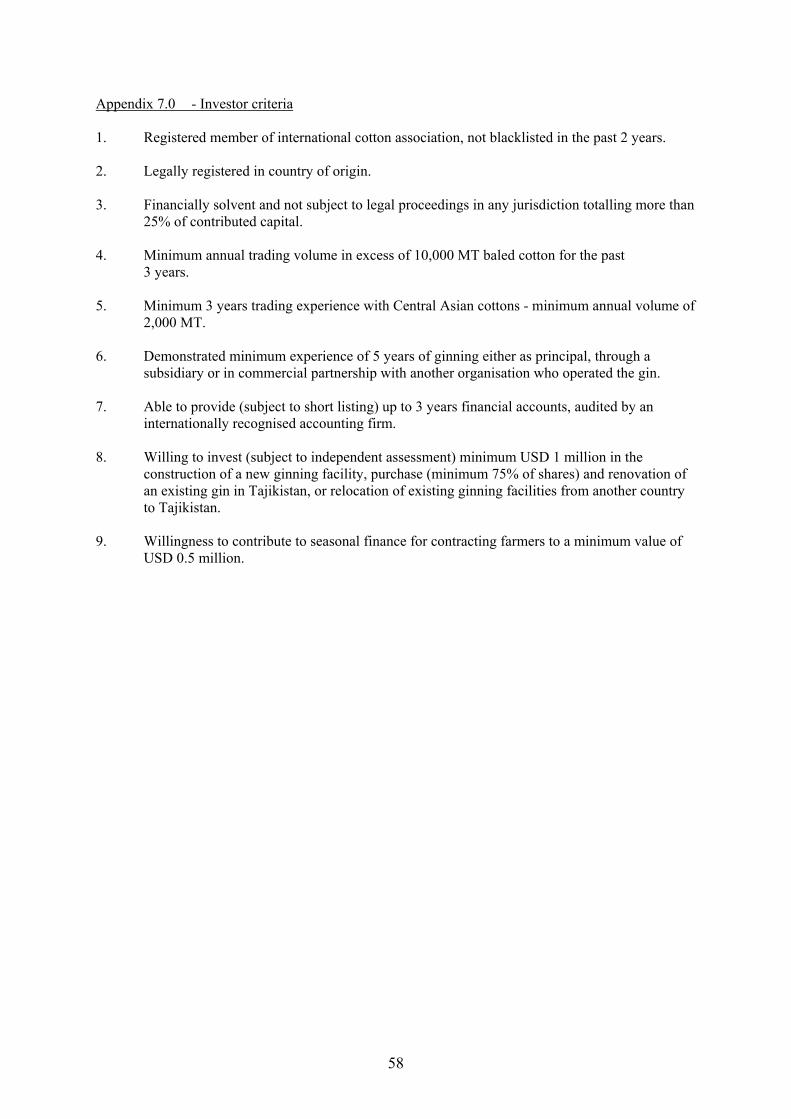

7.0 Way forward As you can see from the foregoing, we are seeking to attract new investors to our cotton sector. As you will appreciate, given the favourable conditions that will be available to investors and the need to develop our cotton sector in accordance with best international practice, we are seeking investors with strong financial backgrounds, clear experience of ginning cotton, established reputations in the trading of cotton and who can demonstrate clear intention of making solid investment in our country. Given the foregoing, we would like to make it clear that we are interested in attracting not only companies who possess these qualities individually, but also commercial consortia made up of companies who collectively possess the attributes that we require. The initial criteria for companies or consortia that would be acceptable for inclusion within the IDA project are set out in appendix 7.0 In order to proceed with the attraction of suitable investors and creation of these new ginning companies, we are hereby calling for expressions of interest from companies or consortia who are interested in this unique opportunity and feel that they meet the criteria set out in the appendix. Such expressions of interest should be sent directly to the below addresses preferably before the 30th of July 2007. Interested parties meeting the investor criteria will then be contacted and invited to submit detailed investment proposals and to begin discussions with IDA and the IFC. At this time, investors will be required to provide any required documentation in connection with the criteria. Interested parties will then be invited to Tajikistan to visit potential project sites, to hold discussion with relevant government and private sector participants and to finalise negotiations. We very much look forward to co-operating with you in the near future. Should you have any questions with regard to the contents of this document or interests outside of those we have highlighted in the foregoing, then we would obviously be very willing to discuss these with you.

- 28 -

APPENDICES

- 29 -

- 30 -

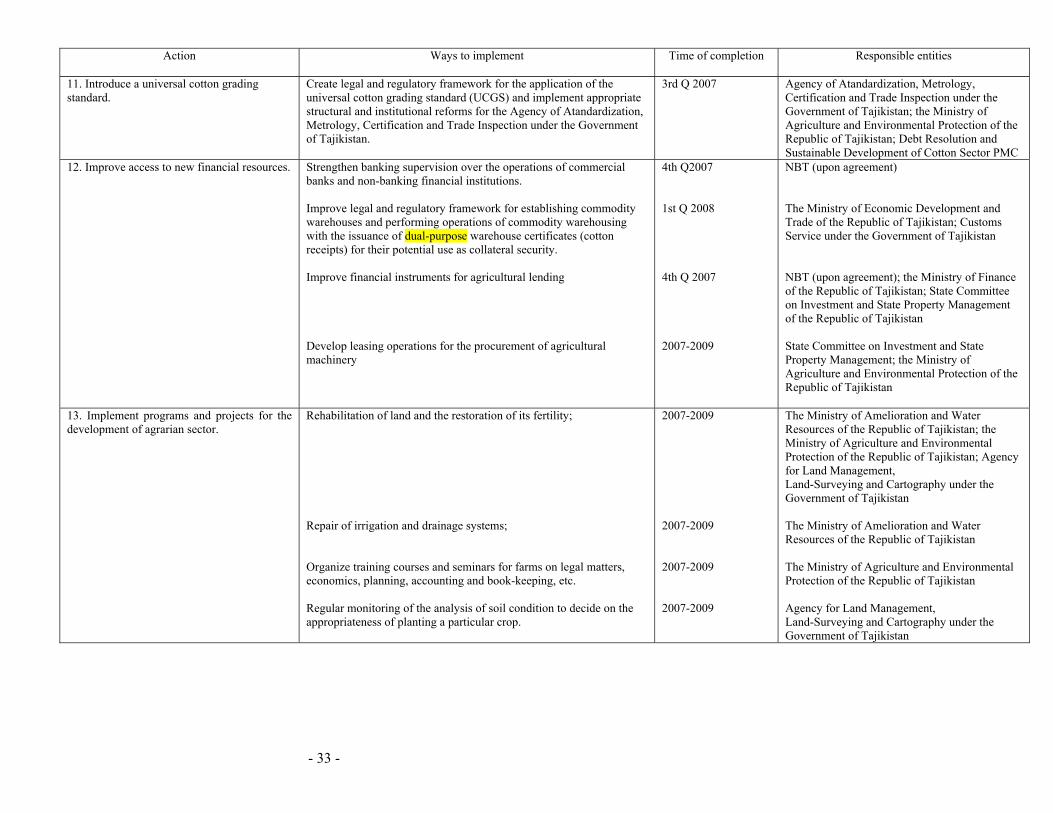

Appendix 1.0 – Government of Tajikistan Cotton Sector Road Map

DECREE OF THE GOVERNMENT OF THE REPUBLIC OF TAJIKISTAN

05 March, 2007 No 111 Dushanbe

On Approval of Plan of Measures for Cotton Farm Debt Resolution in the Republic of Tajikistan for 2007-2009

In order to improve competitiveness and profitability in cotton sector and cotton farm debt resolution, the Government of Tajikistan decrees: 1. Approve (as attached) Plan of Measures for Cotton Farm Debt Resolution in the Republic

of Tajikistan for 2007-2009. 2. Heads of ministries and agencies, state organizations, local state executive bodies to ensure

implementation of measures proposed in the Plan in timely manner and to submit to the Government of Tajikistan quarterly information on undertaken steps for implementation of measures.

3. The State Committee on Investment and State Property Management of Tajikistan and the

National Bank of Tajikistan to take actions to attract funds from donors for implementation the present Decree.

Emomali Rahmonov Chairman of the Government of Tajikistan

- 31 -

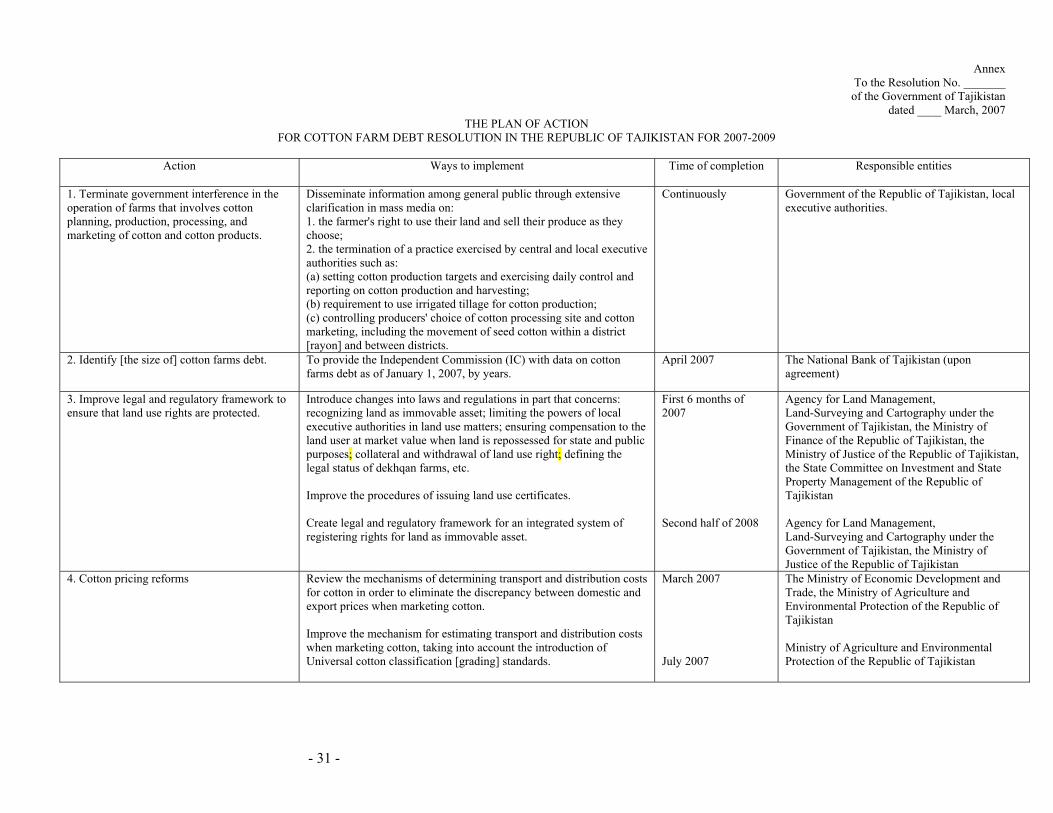

Annex

To the Resolution No. _______ of the Government of Tajikistan

dated ____ March, 2007 THE PLAN OF ACTION

FOR COTTON FARM DEBT RESOLUTION IN THE REPUBLIC OF TAJIKISTAN FOR 2007-2009

Action Ways to implement

Time of completion Responsible entities

1. Terminate government interference in the operation of farms that involves cotton planning, production, processing, and marketing of cotton and cotton products.

Disseminate information among general public through extensive clarification in mass media on: 1. the farmer's right to use their land and sell their produce as they choose; 2. the termination of a practice exercised by central and local executive authorities such as: (a) setting cotton production targets and exercising daily control and reporting on cotton production and harvesting; (b) requirement to use irrigated tillage for cotton production; (c) controlling producers' choice of cotton processing site and cotton marketing, including the movement of seed cotton within a district [rayon] and between districts.

Continuously Government of the Republic of Tajikistan, local executive authorities.

2. Identify [the size of] cotton farms debt. To provide the Independent Commission (IC) with data on cotton farms debt as of January 1, 2007, by years.

April 2007 The National Bank of Tajikistan (upon agreement)

3. Improve legal and regulatory framework to ensure that land use rights are protected.

Introduce changes into laws and regulations in part that concerns: recognizing land as immovable asset; limiting the powers of local executive authorities in land use matters; ensuring compensation to the land user at market value when land is repossessed for state and public purposes; collateral and withdrawal of land use right; defining the legal status of dekhqan farms, etc. Improve the procedures of issuing land use certificates. Create legal and regulatory framework for an integrated system of registering rights for land as immovable asset.

First 6 months of 2007 Second half of 2008

Agency for Land Management, Land-Surveying and Cartography under the Government of Tajikistan, the Ministry of Finance of the Republic of Tajikistan, the Ministry of Justice of the Republic of Tajikistan, the State Committee on Investment and State Property Management of the Republic of Tajikistan Agency for Land Management, Land-Surveying and Cartography under the Government of Tajikistan, the Ministry of Justice of the Republic of Tajikistan

4. Cotton pricing reforms Review the mechanisms of determining transport and distribution costs for cotton in order to eliminate the discrepancy between domestic and export prices when marketing cotton. Improve the mechanism for estimating transport and distribution costs when marketing cotton, taking into account the introduction of Universal cotton classification [grading] standards.

March 2007 July 2007

The Ministry of Economic Development and Trade, the Ministry of Agriculture and Environmental Protection of the Republic of Tajikistan Ministry of Agriculture and Environmental Protection of the Republic of Tajikistan

- 32 -

Action Ways to implement

Time of completion Responsible entities

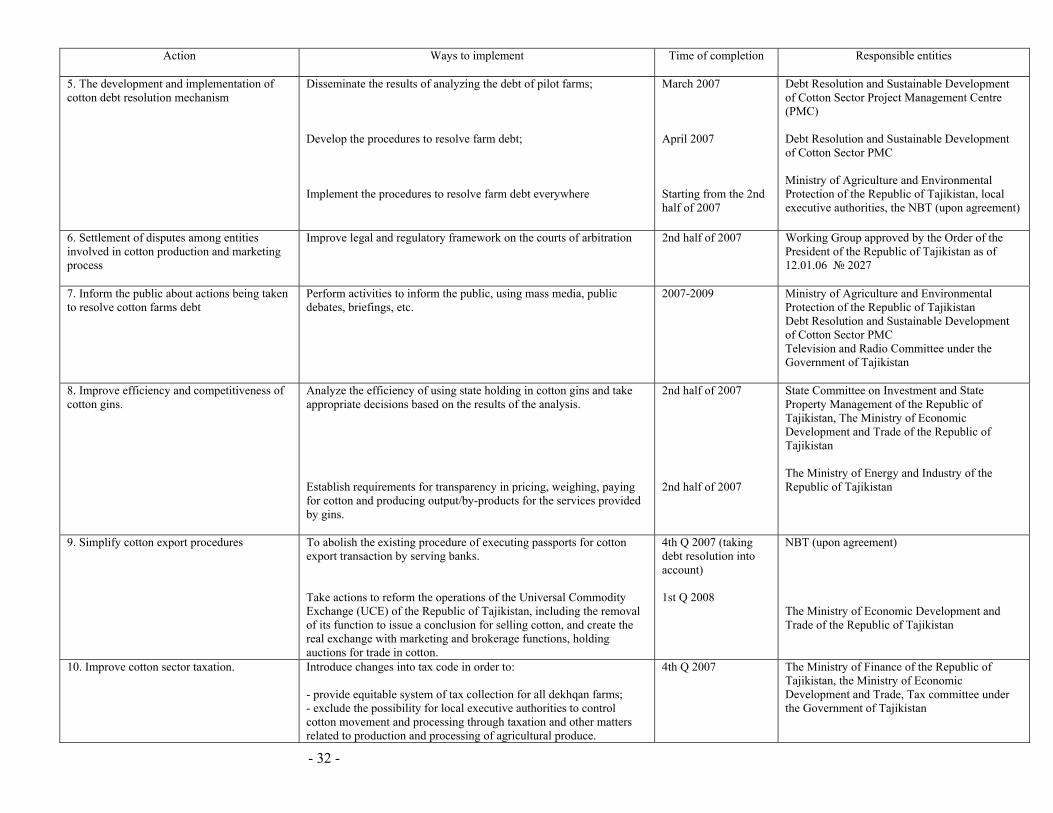

5. The development and implementation of cotton debt resolution mechanism

Disseminate the results of analyzing the debt of pilot farms; Develop the procedures to resolve farm debt; Implement the procedures to resolve farm debt everywhere

March 2007 April 2007 Starting from the 2nd half of 2007

Debt Resolution and Sustainable Development of Cotton Sector Project Management Centre (PMC) Debt Resolution and Sustainable Development of Cotton Sector PMC Ministry of Agriculture and Environmental Protection of the Republic of Tajikistan, local executive authorities, the NBT (upon agreement)

6. Settlement of disputes among entities involved in cotton production and marketing process

Improve legal and regulatory framework on the courts of arbitration 2nd half of 2007 Working Group approved by the Order of the President of the Republic of Tajikistan as of 12.01.06 № 2027

7. Inform the public about actions being taken to resolve cotton farms debt

Perform activities to inform the public, using mass media, public debates, briefings, etc.

2007-2009

Ministry of Agriculture and Environmental Protection of the Republic of Tajikistan Debt Resolution and Sustainable Development of Cotton Sector PMC Television and Radio Committee under the Government of Tajikistan

8. Improve efficiency and competitiveness of cotton gins.

Analyze the efficiency of using state holding in cotton gins and take appropriate decisions based on the results of the analysis. Establish requirements for transparency in pricing, weighing, paying for cotton and producing output/by-products for the services provided by gins.

2nd half of 2007 2nd half of 2007

State Committee on Investment and State Property Management of the Republic of Tajikistan, The Ministry of Economic Development and Trade of the Republic of Tajikistan The Ministry of Energy and Industry of the Republic of Tajikistan