Embed Size (px)

Citation preview

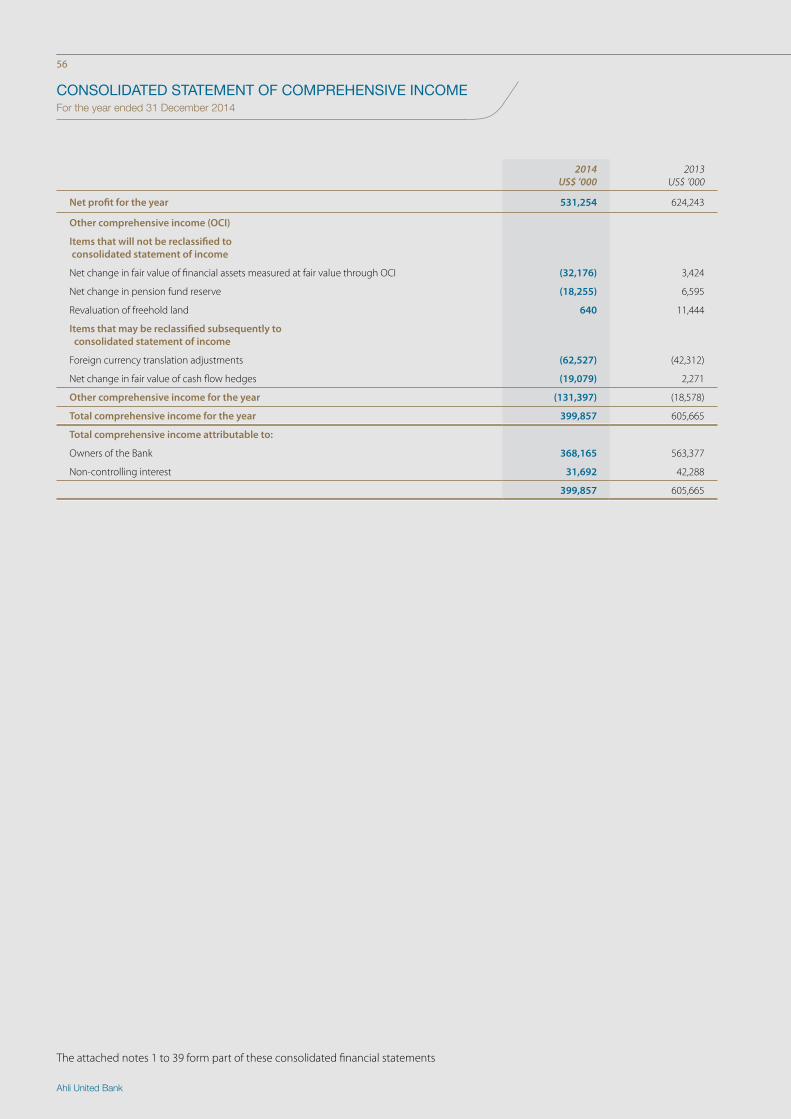

The consistent increase in AUB’s prof it underlines the success and viability of the Bank’s core regional business model, based on diversified and selective growth in operating income, proactive risk management and continuous focus on developing cross border opportunities.

Ahli United Bank

04 Group mission statement05 AUB operating divisions06 Financial highlights14 Board of Directors' report18 Board of Directors 20 Chairman's statement22 Group Chief Executive Officer & Managing Director’s statement26 Corporate governance42 Group business and risk review48 Group organisation49 Group management51 Contact details53 Consolidated financial statements107 Pillar III disclosures - Basel II

Contents

Ahli United Bank

GROUP MISSION STATEMENT

To create an unrivalled ability to meet customer needs, provide fulf illment and development for our staff and deliver outstanding shareholder value.

Objectives

• to maximize shareholder value on a sustainable basis.

• to maintain the highest international standards of corporate governance and regulatory compliance.

• to maintain solid capital adequacy and liquidity ratios.

• to entrench a disciplined risk and cost management culture.

• to develop a cross-cultural meritocratic management structure.

• to optimise staff development through business driven training and profit related incentive.

• to contribute to the social and economic advancement of the communities in which the Group operates.

AUB Vision & Strategy

• Develop an integrated pan regional financial services group model centered on commercial & retail banking, private banking, asset management and life insurance with an enhanced Shari’a compliant business contribution.

• Acquire banks and related regulated financial institutions in the Gulf countries (core markets) with minimum targeted 10% market share to be achieved through mergers, acquisitions and organic growth.

• Acquire complementary banking platforms in secondary markets enjoying strong cross border business flows with Gulf countries or with economic structures similar to the Gulf countries.

4

Ahli United Bank

AUB OPERATING DIVISIONS

Risk Management

This division is responsible for the identification, assessment and ongoing control of all material risks that could affect the Group’s business & operations.

• Risk Management

• Legal

• Compliance

Audit

This division is an integral part of the control environment of the Group. The role of audit is to understand the key risks of the Bank and examine and evaluate the adequacy and effectiveness of the system of risk management and internal control in order to identify legal, regulatory or policy shortcomings.

Support Services

These divisions provide back end banking services to support on-going business activities of the Group, as well as supporting the Group’s expansion through mergers and acquisitions.

• Finance

• Strategic Development

• Information Technology

• Operations

• Services

• Human Resources

Corporate Banking

This division covers all the Bank’s capital-intensive activities in risk asset generation and funding regionally and internationally.

• Corporate and Trade Finance

• Commercial Property Finance

• Residential Property Finance

• Acquisition and Structured Finance

• Correspondent Banking

• Shari'a Compliant Banking

Private Banking & Wealth Management

This division generally includes all the low capital-intensive sectors of the business, offering wealth management services to individuals and institutions based on performance and a balanced product mix.

• Private Banking and Asset Management

• Real Estate Fund Management

• Shari'a Compliant Banking

Retail Banking

This division covers both conventional and Shari'a Compliant individual customers’ deposits, loans, overdrafts, credit cards and residential mortgages.

Treasury and Investments

This division provides money market, trading and treasury services and is also responsible for the management of the Group’s funding. • Money Market Services

• Foreign Exchange Services

• Hedging and Trading Solutions

• Structured Products

• Investment Management

• Shari’a Compliant Treasury Products

Annual Report2014

Ahli United Bank

5

FINANCIAL HIGHLIGHTS

6

Ahli United Bank

CONSOLIDATED PERFORMANCE SUMMARY

AHLI UNITED BANK B.S.C.

US$ '000

Dec 14 Dec 13 Dec 12 Dec 11 Dec 10

Net profit* 482,529 579,374 335,703 310,610 265,499

Total assets 33,444,888 32,651,893 29,872,574 28,329,762 26,457,461

Total loans 18,464,536 17,305,682 15,972,219 15,495,961 14,477,713

Total liabilities 29,614,669 29,086,790 26,711,067 25,418,621 23,705,286

Shareholders' equity 3,390,874 3,148,824 2,776,209 2,537,431 2,392,181

Non-controlling interest 439,345 416,279 385,298 373,710 359,994

Return on average assets (ROAA) 1.6% 1.3% 1.3% 1.2% 1.2%

Return on average equity (ROAE) 15.2% 13.4% 13.0% 12.7% 12.0%

Cost to income ratio 29.7% 30.0% 31.5% 32.4% 33.6%

Financial leverage 7.7 8.2 8.4 8.7 8.6

Risk assets ratio** 15.5% 16.2% 15.6% 16.0% 14.1%

Net interest margin 2.40% 2.32% 2.20% 2.10% 2.30%

Earnings per share (US cents) - basic 8.0 10.0 5.8 5.4 4.7

Earnings per share (US cents) - diluted 8.0 9.9 5.7 5.3 4.7

* Attributable to Bank's equity shareholders

+ Net profit excluding exceptional non-recurring gain related to divested ABQ stake was US$ 366,464 thousands

(2013 Total ROAA including gain related to the divested ABQ stake was 2.0%)

(2013 Total ROAE including gain related to the divested ABQ stake was 20.1%)

** Under BASEL II

+

Annual Report2014

Ahli United Bank

7

PRINCIPAL SUBSIDIARIES

KUWAIT: AHLI UNITED BANK K.S.C.P.

KD' 000s

Dec 14 Dec 13 Dec 12 Dec 11 Dec 10

Net profit* 47,008 42,459 38,539 31,544 27,444

Total assets 3,596,928 3,164,976 2,632,922 2,627,839 2,454,337

Total loans (financing receivables) 2,480,431 2,140,922 1,728,082 1,617,722 1,609,986

Total liabilities 3,257,608 2,841,821 2,337,541 2,352,808 2,189,041

Shareholders' equity 326,868 309,792 282,809 262,190 245,679

Non-controlling interest 12,452 13,363 12,572 12,841 19,616

Return on average assets 1.4% 1.5% 1.4% 1.3% 1.1%

Return on average equity 15.1% 14.9% 14.5% 12.7% 12.2%

Cost to income ratio 32.1% 30.9% 34.2% 39.7% 38.7%

Financial leverage 9.6 8.8 7.9 8.6 8.3

Risk assets ratio ** 16.3% 19.2% 19.7% 21.3% 18.8%

Earnings per share (fils) 36.5 32.9 29.9 24.5 21.3

* Attributable to Bank's equity shareholders

** 2014 under BASEL III as mandated by the Central Bank of Kuwait

8

Ahli United Bank

PRINCIPAL SUBSIDIARIES

UNITED KINGDOM:AHLI UNITED BANK (UK) PLC

US$ '000s

Dec 14 Dec 13 Dec 12 Dec 11 Dec 10

Net profit 49,028 41,216 36,376 36,380 20,760

Total assets 3,671,428 4,151,944 3,434,061 3,419,561 2,718,253

Total loans 1,414,732 1,597,323 1,609,390 1,767,372 1,560,955

Total liabilities 3,376,748 3,854,676 3,174,424 3,158,780 2,478,638

Shareholders' equity 294,680 297,268 259,637 260,781 239,615

Return on average assets 1.3% 1.1% 1.0% 1.2% 0.9%

Return on average equity 16.6% 14.8% 13.5% 14.5% 9.1%

Cost to income ratio 36.6% 40.3% 35.6% 30.4% 38.1%

Financial leverage 11.5 13.0 12.2 12.1 10.3

Risk assets ratio* 19.5% 17.5% 18.9% 17.5% 15.3%

Earnings per share (US cents) 24.5 20.6 18.2 18.2 10.4

* Under BASEL II

Annual Report2014

Ahli United Bank

9

PRINCIPAL SUBSIDIARIES

IRAQ:COMMERCIAL BANK OF IRAQ P.S.C.

IQD Millions

Dec 14 * Dec 13 Dec 12 Dec 11 Dec 10

Net profit 10,462 10,689 14,310 7,980 13,934

Total assets 449,273 334,843 293,437 247,446 204,164

Total loans 23,976 20,230 18,291 12,889 13,845

Total liabilities 164,888 138,264 150,237 112,261 109,625

Shareholders' equity 284,385 196,579 143,200 135,185 94,539

Return on average assets 2.7% 3.4% 5.3% 3.5% 6.8%

Return on average equity 4.4% 6.3% 10.3% 6.9% 15.6%

Cost to income ratio 45.7% 51.6% 41.0% 48.4% 50.5%

Financial leverage 0.6 0.7 1.0 0.8 1.2

Risk assets ratio 760.4% 489.7% 414.5% 566.3% 577.4%

Earnings per share (fils) 69.7 85.5 125.2 83.4 180.6

Based on financial statements under local GAAP.

* 2014 information are subject to approval at Annual General Meeting

10

Ahli United Bank

PRINCIPAL SUBSIDIARIES

EGYPT:AHLI UNITED BANK (EGYPT) S.A.E.

EGP' 000s

Dec 14 Dec 13 Dec 12 Dec 11 Dec 10

Net profit * 365,425 285,846 244,946 195,868 164,348

Total assets 24,983,857 19,972,167 15,602,707 12,854,828 10,012,348

Total loans 12,072,608 9,387,495 7,456,483 5,802,342 5,443,987

Total liabilities 22,858,290 18,095,779 14,040,037 11,749,022 8,985,425

Shareholders' equity 2,113,922 1,865,685 1,552,780 1,096,322 1,017,506

Return on average assets 1.7% 1.7% 1.7% 1.7% 1.9%

Return on average equity 18.7% 17.8% 19.6% 18.8% 17.0%

Cost to income ratio 25.8% 26.7% 30.9% 34.9% 39.4%

Financial leverage 10.8 9.6 9.0 10.6 8.7

Risk assets ratio ** 12.4% 13.7% 14.6% 13.1% 14.0%

Earnings per share (EGP) 2.2 1.7 1.7 1.8 1.5

* Attributable to Bank's equity shareholders

** Under Basel II from 2012

Annual Report2014

Ahli United Bank

11

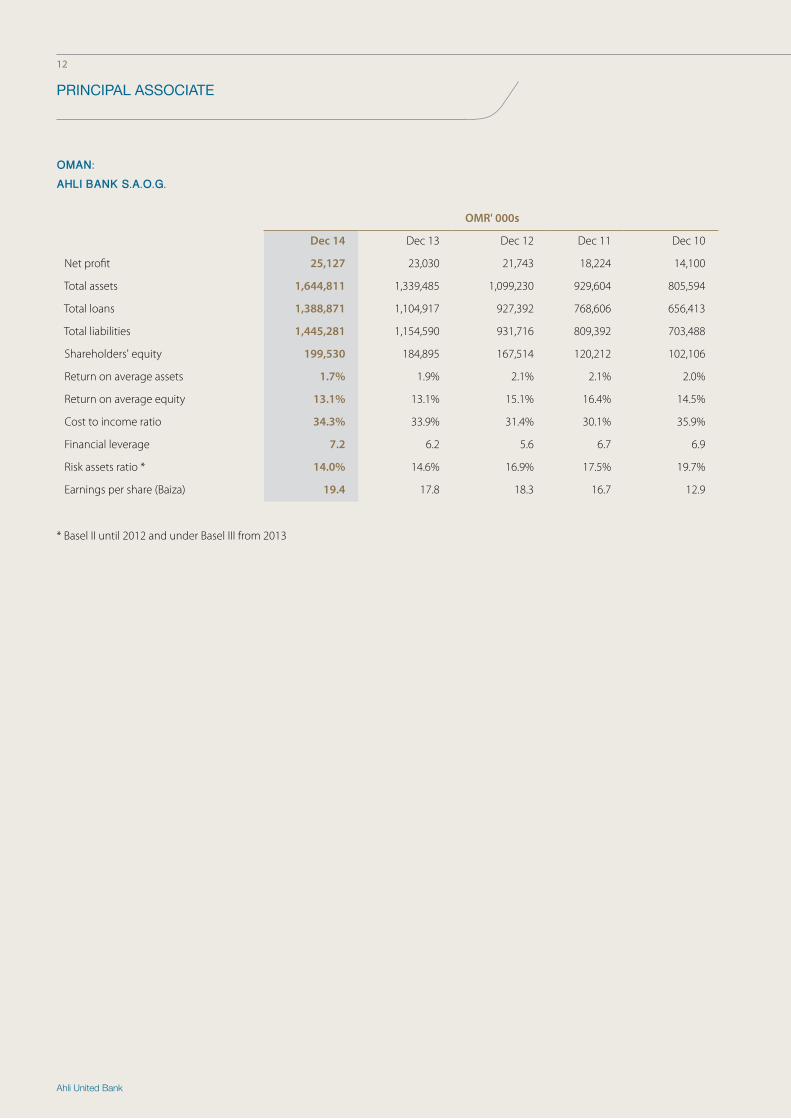

PRINCIPAL ASSOCIATE

OMAN:AHLI BANK S.A.O.G.

OMR' 000s

Dec 14 Dec 13 Dec 12 Dec 11 Dec 10

Net profit 25,127 23,030 21,743 18,224 14,100

Total assets 1,644,811 1,339,485 1,099,230 929,604 805,594

Total loans 1,388,871 1,104,917 927,392 768,606 656,413

Total liabilities 1,445,281 1,154,590 931,716 809,392 703,488

Shareholders' equity 199,530 184,895 167,514 120,212 102,106

Return on average assets 1.7% 1.9% 2.1% 2.1% 2.0%

Return on average equity 13.1% 13.1% 15.1% 16.4% 14.5%

Cost to income ratio 34.3% 33.9% 31.4% 30.1% 35.9%

Financial leverage 7.2 6.2 5.6 6.7 6.9

Risk assets ratio * 14.0% 14.6% 16.9% 17.5% 19.7%

Earnings per share (Baiza) 19.4 17.8 18.3 16.7 12.9

* Basel II until 2012 and under Basel III from 2013

12

Ahli United Bank

PRINCIPAL ASSOCIATE

Ahli United Bank

BOARD OF DIRECTORS' REPORT

Consolidated net profit, attributable to the Bank’s equity shareholders, of US$ 482.5 million as against US$ 579.4 million in 2013. 2013 net profit included a non-recurring gain of US$ 212.9 million realized on Bank’s divestment of its 29.4% stake in Ahli Bank, Qatar (ABQ), which was reported only in the 2013 result.

Excluding this item, the growth in the recurring operating profit of the Bank was 31.7% over the comparable result in 2013.

Total operating income crossed the US$ 1 billion mark for the first time since Bank’s inception in 2000 with an increase of 8.7% over 2013 to reach US$ 1,041.3 million. Increase in the operating income was broad based and underpinned by a rise in Net Interest Income of US$ 50.1 million (+7.0%) and fees and other income increasing by US$ 32.9 million (+13.4%).

•

•

The Directors of Ahli United Bank (“AUB” or the “Bank”) are pleased to submit the Annual Report and accompanying consolidated Financial Statements for the year ended 31 December 2014.

General Operating Environment

The global economic environment in 2014 remained sluggish with an IMF global world economy growth rate of 3.3% in line with 2013 while emerging market and developing economies achieved a growth rate of 4.4%, lower than the 4.7% reported in 2013.

This continued weakness has been due to adverse geo-political and security situations and to a slow-down in major emerging markets like China which recorded a lower growth rate of 7.4% from 7.7% in 2013. Given the lukewarm investment sentiment coupled with an excessive oil supply market led to a sharp decline in oil prices of circa 60% since June 2014 which remain sustained to date. Oil exporting countries, if current situation persists, will face a need to review fiscal spend and/or drawdown on resources with related economic ramifications. While in the near term oil importing economies will benefit from the low oil prices, this advantage is expected to be partially offset by diminished expectations about the growth prospects for developed and emerging economies resulting in lower projected FDI flows in the medium term particularly for regional MENA economies dependent on GCC investment and employment opportunities. Considerable downside risks therefore continue to exist on the international and regional fronts arising from both geo-political and economic risks. This is reflected in the revised lower IMF 2015 growth forecast for the world at 3.5% (2016:3.7%) while the World Bank has forecasted a smaller world GDP growth rate at 3.0% with a marginal improvement to 3.3% in 2016.

Performance Overview

Despite the continuing global uncertainties and continuing operating challenges faced in its main markets, AUB achieved another record performance in 2014, a 31.7% growth in the operating profits, clearly validating the success and viability of its core business model based on product and market diversification.

The key highlights of its performance were:

•

•

Asset quality improved with the NPL ratio reducing to 2.0% (2013: 2.3%). The Group’s coverage ratio of total provisions to impaired loans increased to 159.4% at the end of the year (2013: 155.5%). Specific provision coverage stood at 83.8% at 31 December 2014 compared to 86.1% in 2013.

Total assets increased by 2.4% to US$ 33.4 billion (2013: US$ 32.7 billion) contributed by:

The Loans and Advances portfolio which increased by6.7% to US$ 18.5 billion (2013: US$ 17.3 billion).

The Non-trading Investments portfolio grew by 4.4% to reach US$ 5.8 billion as part of ongoing balance sheet management, effective deployment of liquidity with a view to optimizing yields and complying with regulatory liquidity regimes.

i)

ii)

•

•

•

•

•

•

•

Customers’ deposits were up by 4.4% to US$ 23.0 billion (2013: US$ 22.0 billion) to fund the balanced growth in loans and advances.

As part of its funding strategy, the Bank reduced its higher cost borrowings under re-purchase agreements by US$ 369.5 million to US$ 901.6 million as outstanding at 31 December 2014 (US$ 1,271.1 million at 31 December 2013).

Continuous focused cost management and higher operating income resulted in an improvement of the operating cost to income ratio during the year to 29.7% (2013: 30.0%).

Excluding the non-recurring gain related to the divested ABQ stake, operating return on Average Equity increased to 15.2% (2013: 13.4%) and the operating return on Average Assets increased to 1.6% (2013: 1.3%).

Strategic & Corporate Development

In November 2014, IFC converted US$ 100 million of its Optionally Convertible Subordinated Debt held in AUB into 118,609,884 AUB ordinary shares at an effective conversion price of US 84.31 cents. Post conversion, IFC along with the IFC Capitalization Fund, hold a 5.2% shareholding in AUB. IFC’s decision to exercise the conversion option represents a vote of confidence in AUB’s strong underlying financial and operational fundamentals.

Recognition

AUB Group has been a recipient of a number of prestigious banking awards during the year and includes the following:

Best Regional Bank – GCC in 2014 by Capital Financial International

Best Emerging Market Bank in Bahrain – 2014 awarded by Global Finance

14

Ahli United Bank

BOARD OF DIRECTORS' REPORT

Best Foreign Exchange Provider in Bahrain – 2015 awarded by Global Finance

Best Bank in Bahrain – 2014 awarded by Euromoney

Best Local Private Bank, Bahrain – 2014 awarded by Euromoney

Bank of the Year, Bahrain - 2014 awarded by The Banker magazine

Best Local Bank in Bahrain – 2014 awarded by Emea Finance magazine

Private Bank of the Year, Bahrain – 2014 awarded by The Banker and PWM

AUB Kuwait: Islamic Bank of the Year –2014 by The Banker magazine

AUB Kuwait: Private Bank of the year – 2014 by The Banker and PWM.

Directors’ Shareholdings & Remuneration

The number of shares held by directors, senior management and their related parties as at 31 December 2014 is disclosed in the Corporate Governance Report.

For Directors’ fees, allowances, expenses, salaries and remuneration please refer to Note 25 of the financial statements

Appropriations

On the basis of the results of the Bank for the year ended 31 December 2014, the Board of Directors recommends the following appropriations of the Bank’s net profit of US$ 482,529 thousands for approval by the shareholders:

•

•

•

•

•

•

•

•

US$ ’000

Net profit attributable to Bank’s equity shareholders 482,529

Transfer to statutory reserve 48,253

Proposed cash dividend – ordinary shares at US cents 4.5 per share

270,452

Proposed donations 1,000

Transfer to retained earnings 162,824

Conclusion

In my capacity as the Chairman of the Board, it is my pleasure to thank our shareholders for their continuing support and confidence reposed in AUB. Our achievements during 2014 were only made possible through the support and trust of our clients, business partners and customers and the dedication, professionalism and resilience of our staff as well as the guidance of our regulators.

While operating challenges remain, we start 2015 with clear plans and goals to improve on our past performances and we will continue to strive to meet the aspirations of all our stakeholders.

Mohammad J. Al-MarzooqChairman (acting)

22 February 2015

15Annual Report2014

Ahli United Bank

Ahli United Bank

Ahli United Bank

BOARD OF DIRECTORS

Hamad M. Al-Humaidhi Chairman of the Board and Executive Committee;Non-Executive Director

Chairman since 31 March 2015, holds a Bachelor of Art (Law) degree from University of Kuwait, 1975.Director General, The Public Institution for Social Security, Kuwait; Chairman & CEO, Wafra Intervest Corporation; Chairman, Ahli United Bank (UK) PLC; Chairman, Kuwait Medical City, Kuwait. Former Deputy General, The Public Institution for Social Security, Kuwait ; Former Legal Advisor, National Bank of Kuwait; Former Legal Department Manager, Administration Department Manager, Legal Researcher in Legal Department, The Public Institution for Social Security, Kuwait ; Former, Legal Researcher, The Civil Service Commission.

Mohammad Jassim Al-Marzooq Deputy Chairman and Member of the Executive Committee;Non-Executive Director

Director since, 27 March 2006, holds a Bachelor of Commerce (Finance Major) from Kuwait University, 1991. CEO, Tamdeen Real Estate Co. Kuwait; Chairman, Tamdeen Shopping Centre, Kuwait; Chairman, Tamdeen Bahraini Real Estate Co, Bahrain; Chairman, Trustees Bait Al Arab (Kuwait State Stud), Kuwait; Board Member, Fateh Al Khear Holding Co., Kuwait ; Board Member, The Supreme Council for Planning & Development, Kuwait; Former Chairman of Tamdeen Real Estate Co, Kuwait; Former Board Member of Al Maalem Holding Co, Bahrain; Former Board Member of Global Omani Development & Investment Co, Oman ; Former, Deputy Chairman, Tamdeen Shopping Centre Co, Kuwait ; Former Board Member, Bank of Kuwait & The Middle East, Kuwait ; Former , Vice Chairman, Tamdeen Investment Co, Kuwait; Former, Board Member, Al Ahli Bank of Kuwait, Kuwait; Former, Board Member, Kuwait National Cinema Co., Kuwait; Former Board Member, Arab Financial Consulting Co., Kuwait; Former, Chief of Executive Staff, Real Estate Investment Fund, Kuwait; Former, Board Member, The Public Warehousing Co., Kuwait ;

Rashed Ismail Al-MeerDeputy Chairman and Member of the Executive Committee;Non-Executive Director

Director since 29 March 2003, holds a High Diploma in Statistics from the University of Alexandria-Egypt, 1973 and a B.Com from Baghdad University, Iraq, 1969.Director, Ahli United Bank (UK) PLC; Chairman, Osool Assets Management Co.; Chairman, Esterad Investment Co.; Deputy Chairman of the Board of Directors, Solidarity Group Holding Co.; Director, Social Insurance Organisation, Director , Al Ahli Real Estate Co. S.P.C.; Former, Chairman, Former, Director General, Pension Fund Commission; Former, Asst. Undersecretary for Financial Affairs, Ministry of Finance & National Economy; Former, Asst. Undersecretary for Economic Affairs, Ministry of Finance & National Economy; Former, Director of Investment; Various Positions, Central Bank of Bahrain; Former, Head of Statistics Section, Ministry of Health.

Hamad M. Al-Humaidhi

Mohammad Jassim Al-Marzooq

Adnan Al-Marzouq

Mohammed Saleh Behbehani

Rashed Ismail Al-Meer

Mohammed Saleh BehbehaniMember of the Compensation Committee;Independent Director

Director since 30 July 2000. Partner & President, Mohammad Saleh & Reza Yousuf Behbehani Co; Partner, Mohammad Saleh Behbehani & Co. W.L.L; Partner, Behbehani Bros., W.L.L, Bahrain; President, Shereen Real Estate Co.; Chairman, Maersk Logistics Co.W.L.L.; Chairman, Kuwait Insurance Co. S.A.K; Partner & President, Behbehani Jeep Motors Co. W.L.L.; Partner & President, Shereen Investment Co; Partner & President, Shereen Motor Co.W.L.L; President, Behbehani Automall Co. W.L.L; Partner, Al Mulla & Behbehani Motor Co. W.L.L; Vice Chairman, United Beverage Co; Chairman, Maersk Kuwait Co. W.L.L; Board & Executive Committee Member, Ahli United Bank K.S.C; Former Director, Purchase & Imports, Public Works Dept., Govt. of Kuwait; Former Deputy. Chairman, Al Ahli Bank of Kuwait K.S.C.; Former Board Member, Ahli United Bank (UK) PLC; Former Director, Swiss Kuwaiti Bank.; Former Director, UBAF (Hong Kong) Limited.

Adnan Al-MarzouqMember of the Audit & Compliance Committee and Nominating Committee; Independent Director

Director Since, 25 March 2014. Holds a Bachelors Degree in Industrial Systems Engineering from University of Southern California, 1981.Managing Director, Al-Marzouq Company for Import & Export, Kuwait; Board Member, Ahli United Bank (UK) PLC. Vice Chairman, Rouyah Investment & Leasing Co, Kuwait; Formerly: Chairman, The Kuwaiti Manager Company, Kuwait; Board Member, Kuwait Finance House, Kuwait; Manager Treasury, Gulf Investment Corporation, Kuwait ; Asst. Manager-Treasury, National Bank of Kuwait.

18

Ahli United Bank

BOARD OF DIRECTORS

Mohammed Fouad Al-Ghanim

Abdulla MH Al-Sumait

Herschel Post Lama Al-Dakheel

Adel A. El-Labban

Michael Essex

Mohammed Fouad Al-GhanimMember of the Executive Committee;Independent Director

Director since 29 March 2003, holds a degree in Business Administration from Kuwait University, 1993. Vice Chairman & CEO Fouad Alghanim & Sons Group of Companies, Kuwait; Member of the Board of Directors, Tamdeen Real Estate Company KSCC, Kuwait; Chairman, Fluor Kuwait Co. K.S.C., Kuwait Former, Chairman, AlGhanaem Industrial Company K.S.C., Kuwait; Former, Member of the Supervisory Board, Jet Alliance Holding AG, Austria.

Abdulla MH Al-SumaitMember of the Audit & Compliance Committee and Nominating Committee ;Independent Director

Director since 16 May 2001, holds a B.A. in Law from Kuwait University, 1976. Director, Kuwait Commercial Facilities Company; Director, Ahli United Bank (Egypt) SAE. Former, Legal Consultant for Director General, The Public Institution for Social Security, (Kuwait);

Michael Essex Member of the Audit & Compliance Committee, Nominating Committee and Compensation Committee; Independent Director

Director since, 28 March 2012, holds an Executive Development Program Certificate from Harvard Business School, Boston-USA, 1997, M.A. Public Administration from Carleton University, Ottawa-Canada, 1975, B.A. Economics & Political Science from The University of Western Ontario London- Canada 1972. Member of the Investment Committee, APIS Growth Fund; Director, Macquarie Bank India Infrastructure Fund; Formerly, International Finance Corporation’s Director of Investment & Advisory Operations for the MENA region- 20 Countries, Pakistan to Morocco; IFC-Deputy Director for Global Industry & Service Investments and Senior Risk Supervisor for Asia, Bank of Nova Scotia.

Herschel PostChairman of the Audit & Compliance Committee, Nominating Committee and Compensation Committee;Independent Director

Chairman of the Audit & Compliance Committee, Nominating Committee and Compensation Committee Director since 25 December 2001, holds a Financial Advisers Certificate from The Chartered Institute of Bankers, 2000, a B.A. & M.A. (Rhodes Scholar) from Oxford University 1984, L.L.B from Harvard Law School, 1966 and a Bachelor of Arts from Yale University, 1961. Director and Chairman of the Audit Committee, Ahli United Bank (UK) PLC; Director and Chairman of the Audit Committee, Ahli United Bank (Egypt) SAE.; Director and Chairman of the Audit Committee, Ahli United Bank K.S.C., Kuwait; Director and Chairman of the Audit Committee, Kuwait & Middle East Financial Investment Company (KMEFIC); Chairman , Almazaya Co.; Director and Chairman of the Audit Committee, Threadneedle Asset Management Holdings S.A.R.L.; Former Director, Investors Capital Trust PLC; Former Director, Program Planning Professionals Inc.; Former Director Christie’s International PLC; Trustee, Earthwatch Institute (Europe). Former Deputy Chairman of the London Stock Exchange; Former CEO and Deputy Chairman, Coutts & Co.; Former Chief Operating officer, Lehman Brothers International Ltd.; Former Director, Euroclearance System Ltd, Director & Chairman of Audit Committee, Euroclear UK & Ireland PLC.

Lama Al-DakheelMember of the Audit & Compliance Committee and Nominating Committee; Non-Executive Director

Director since, 31 March 2015. Holds a Bachelors Degree in Finance & Business Administration, Kuwait University, 1995. Manager, Direct Investment Department, The Public Institution for Social Security, Kuwait; Former, Supervisor and Analyst Direct Investment Department, The Public Institution for Social Security, Kuwait

Adel A. El-LabbanExecutive Committee Member;Executive Director

Director since 30 July 2000. Holds a Masters in Economics (Highest Honors) from the American University, Cairo, 1980, Bachelors in Economics (Highest Honors) from American University, Cairo, 1977. Group Chief Executive Officer & Managing Director, Ahli United Bank BSC, Bahrain; Director, Ahli United Bank (UK) PLC; Director, Ahli United Bank K.S.C., Kuwait; Deputy Chairman, Ahli United Bank (Egypt) SAE, Egypt; First Deputy Chairman, Ahli Bank SAOG, Oman; Deputy Chairman, Commercial Bank of Iraq,; Deputy Chairman, United Bank for Commerce & Investment S.A.C. Libya; Director Bahrain Association of Banks, Bahrain; Former Chief Executive Officer and Director of the United Bank of Kuwait PLC, UK; Former Managing Director, Commercial International Bank (Egypt) SAE; Former Chairman, Commercial International Investment Company, Egypt; Former Vice President, Corporate Finance, Morgan Stanley, USA; Former Assistant Vice President, Arab Banking Corporation, Bahrain.

19Annual Report2014

Ahli United Bank

CHAIRMAN'S STATEMENT

With clear plans to develop on existing initiatives, I am confident in the Group’s proven and tested capabilities to achieve sustainable growth and to continue meeting the aspirations of all stakeholders.

20

Ahli United Bank

CHAIRMAN'S STATEMENT

I am pleased to report that 2014 was another year of record

operating profitability and strong business performance for AUB

across all fronts. Notable success and significant progress was

achieved across the Group’s businesses and operations, clearly

demonstrating its ability to deliver sustainable growth, despite

varying degrees of uncertainty and volatility in market conditions

in its markets.

In the global economy, significant divergences were apparent

with the US showing signs of economic revival, China’s growth rate

slowing down while the Eurozone and Japan struggled to avoid

stagnation. The continued low level of oil prices, which fell by circa

60% in the latter half of the year, will impact oil exporting countries

including the GCC economies going forward, depending on the

duration and intensity of such a drop and will assist MENA oil

importing countries in reducing their balance of trade deficits.

In these challenging conditions, AUB reported a net profit of

US$ 482.5 million for the year 2014 attributable to a strong

multi-platform financial performance based on its prudent and

diversified business model. The growth in the operating profit of

the Bank represented a 31.7% growth over the comparable result

in 2013, excluding the exceptional non-recurring gain of US$ 212.9

million from its Qatari affiliate bank sale included in the previous

year’s profit of US$ 579.4 million.

The consistent increase in AUB’s operating profit underlined the

success and viability of the Bank’s core regional business model

based on diversified and selective growth in operating income,

proactive risk management, supported by an effective control

framework and continuous focus on developing cross border

opportunities while maintaining its intelligent spend culture.

A major milestone was reached with total operating income

surpassing the US$ 1 billion mark for the first time.

As a result, earnings per share were US cents 8.0 for the year ended

31 December 2014 (2013: US cents 10.0). Given the excellent

results achieved, the Board of Directors has recommended a cash

dividend of US cents 4.5 per share (2013: US cents 4.5) together

with a bonus ordinary share issue of 5% (2013: 5%).

During the year, confidence in AUB’s financial and operational

fundamentals was further demonstrated by IFC’s decision to

convert its optionally convertible subordinated debt into AUB

ordinary shares, which, together with the IFC Capitalisation Fund,

increased IFC’s share holding in AUB to 5.2%.

It was gratifying to note that AUB’s market leadership and superior

performance levels continued to achieve wider recognition among

key analysts in the banking industry. In 2014 no less than ten top

awards were received for pre-eminence in particular sectors –

private banking, Islamic banking, and foreign exchange – as well as

awards for ‘best bank’ at both the regional and country levels.

Looking ahead, with economic and socio-political uncertainty

expected to persist, AUB will remain focused on pursuing its

strategy of regional expansion while seeking opportunities to

develop cross border business. With clear plans to develop on

existing initiatives, I am confident in the Group’s proven and

tested capabilities to achieve sustainable growth and to continue

meeting the aspirations of all stakeholders.

Finally, it is my pleasure to thank our shareholders for their

continued support and confidence in AUB. What has been

achieved in 2014 would not have been possible without the

support and trust of our valued customers and business partners

and the firm commitment, dedication and hard work of the staff

as well as the guidance of our regulators.

Hamad M. Al-Humaidhi Chairman

Annual Report2014

21

Ahli United Bank

GROUP CHIEF EXECUTIVE OFFICER &MANAGING DIRECTOR'S STATEMENT

As testament to the Bank’s capacity to achieve sustainable growth, total operating income exceeded US$ 1 billion for the first time since the Bank’s inception in 2000.

22

Ahli United Bank

GROUP CHIEF EXECUTIVE OFFICER &MANAGING DIRECTOR'S STATEMENT

Despite prevailing global uncertainties and continuing operating

challenges in its major markets, AUB delivered another record

performance in 2014. The Bank’s net profit attributable to its equity

shareholders increased by 31.7% to US$ 482.5 million for the year

2014 compared with US$ 366.5 million in 2013. The overall 2013

net profit of US$ 579.4 million included an exceptional non-

recurring gain of US$ 212.9 million from the sale of a 29.4% stake

in its Qatari affiliate. The increase in the 2014 operating profit

reflected AUB’s strong underlying business fundamentals together

with its effective control framework and resilient business model.

As testament to the Bank’s capacity to achieve sustainable growth,

total operating income exceeded US$ 1 billion for the first time

since the Bank’s inception in 2000, rising by 8.7% to US$ 1,041.3

million compared with US$ 958.0 million in 2013. The surge in

operating income was largely driven by a 7.0% increase in Net

Interest Income to US$ 763.3 million, resulting from higher lending

volumes as well as prudent deployment of liquidity in non-trading

investments within a conservative risk framework complemented

by focused liability cost management. Fees and other income

grew by 13.4% from US$ 245.1 million to US$ 278.0 million. The

increased operating income together with a disciplined cost

culture aligned to “intelligent spend” on business and control

needs across the AUB Group further improved the operating cost

to income ratio to 29.7% from 30.0% in 2013.

The Group’s total assets grew by 2.4% amounting to US$ 33.4

billion at 31 December 2014 from US$ 32.7 billion at year end 2013.

The increase in total assets was due primarily to a 6.7% growth in

the loans and advances portfolio to US$ 18.5 billion (31 December

2013: US$ 17.3 billion). The non-trading investments portfolio

rose by 4.4% to US$ 5.8 billion reflecting vigilant balance sheet

management and pursuit of asset profitability and diversified

opportunities as well as effective liquidity deployment to comply

with regulatory liquidity requirements.

Balanced credit growth was underpinned by a 4.4% increase in

customer deposits totalling US$ 23.0 billion (31 December 2013:

US$ 22.0 billion). As part of its funding strategy, the Bank was

successful in reducing higher cost borrowings under repurchase

agreements by US$ 369.5 million. The asset quality of the Group

continued to improve with the non-performing loan ratio

reducing to 2.0% at year end 2014 compared with 2.3% for the

prior year. The total provision coverage ratio, inclusive of collective

impairment provisions, was 159.4% at year end 2014 (2013: 155.5%)

and specific provision coverage stood at 83.8% compared with

86.1% in 2013.

Further improvement was also notable in key financial indicators

with the return on average equity increasing to 15.2% (2013:

13.4%) and return on average assets rising to 1.6% (2013: 1.3%),

adjusted for the exceptional non-recurring item credited in 2013.

During the year, AUB made significant progress in developing

cross-border trade finance business among the Group’s operating

countries, in increasing share of wallet from existing customers

and in securing significant new clients. Notable success was also

achieved in expanding the B2B platform for corporate customers,

providing a one-stop solution for cash management including

payments, collections and reconciliations. In continuing to

strengthen the Group’s corporate responsibilities, various ‘green’

initiatives were adopted to conserve natural resources as practical

steps to deliver on AUB's responsibilities as a signatory to the

Equator Principles, a global benchmark for managing social and

environmental risks in project finance.

Finally, I would like to express my gratitude to the Board of

Directors for their active support and guidance. My sincere thanks

are also due to all my colleagues, the management and the staff

of the AUB Group, whose professionalism, commitment and

hard work have been fundamental in achieving another year of

excellent performance and sustainable growth.

Adel A. El-LabbanGroup Chief Executive Officer & Managing Director

23Annual Report2014

Ahli United Bank

CORPORATE GOVERNANCE

Good Corporate Governance practices are important in creating

and sustaining shareholder value and ensuring appropriate

disclosure and transparency. The Bank’s Corporate Governance

Policy provides the framework for the principles of effective

Corporate Governance standards across the AUB Group.

The Board of Directors is committed to implementing robust

Corporate Governance practices and to continually review and

align these practices with international best practices, where

appropriate.

The Bank’s management are committed to ensuring that procedures

and processes are in place to reflect and support the Board approved

Corporate Governance practices to ensure the highest standards of

Corporate Governance throughout the AUB Group.

Shareholder Information

The Bank’s shares are listed on the Bahrain Bourse and the Kuwait

Stock Exchange. As at 31 December 2014, the Bank had issued

6,121,883,913 ordinary shares, each with a nominal value of $ 0.25.

All ordinary shares are fully paid up.

The Annual General Ordinary and Extraordinary Meetings were

held on 25 March 2014.

Ordinary Shareholders as at 31 December 2014 (holding 5% and above)

NameCountryof origin

No. of shares

% of Total

Shares

Public Institution For Social Security

Kuwait 1,158,572,382 18.93%

Social Insurance Organization

Bahrain 611,400,548 9.99%

Tamdeen Investment Company

Kuwait 466,526,017 7.62%

Sh. Salim Al-Nasser Al-Sabah

Kuwait 333,835,556 5.45%

International Finance Corporation

USA 315,551,499 5.16%

Distribution of Shares

Table -1 Distribution of Ordinary Shares as at 31 December 2014

Category No of shares

% of Total

Shares

50% and above - -

20% up to less than 50% - -

10% up to less than 20% 1,158,572,382 18.93%

5% up to less than 10% 1,727,313,620 28.22%

1% up to less than 5% 1,307,346,327 21.35%

Less than 1% 1,928,651,584 31.50%

Total 6,121,883,913 100.0%

Table- 2 Government Holdings and the distribution of Ordinary

Shares by Nationality

No. Name No. of Shares

% of Total

shares

1Kuwait Quasi Government

1,158,572,382 18.93%

2Bahrain Quasi Government

617,731,976 10.09%

3Qatar Quasi Government

94,898,026 1.55%

4Kuwait Individuals and Corporates

2,898,969,067 47.35%

5Bahrain Individuals and Corporates

975,453,311 15.93%

6 Others 376,259,151 6.15%

Total 6,121,883,913 100%

26

Ahli United Bank

CORPORATE GOVERNANCE

Notes :1. Fahad Al-Rajaan - Resigned effective 22 January 2015.2. Mohammad Al-Marzooq - Appointed as a Deputy Chairman on 19 February 2014 and Acting Chairman on 22 January 2015.3. Turki Bin Mohamed Al-Khater – Term of Directorship ceased on 31 March 2015 following Director elections4. Adnan Al-Marzouq - Appointed on 25 March 2014.

In compliance with the Central Bank of Bahrain (CBB) Corporate Governance requirements, the Board of Directors has outlined its criteria and materiality thresholds for the definition of “Independence” in relation to Directors. The independence criteria are reassessed annually by the Board and for the year 2014, the 11 Directors comprising the Board were classified as follows:

• 7 Independent Directors• 3Non-ExecutiveDirectors• 1ExecutiveDirector

The Role and Responsibilities of the Board of Directors

The Board is responsible to shareholders for creating and delivering sustainable shareholder value through the prudent management of the Bank’s business. The Board, as a whole, is collectively responsible to ensure that an effective, comprehensive and transparent corporate governance framework is in place. The Board’s role is to:

1. ensure adherence to prevailing laws and regulations and to best business ethics; 2. provide entrepreneurial leadership of the Bank within a framework of prudent and effective controls, which enable all types of relevant risks to be assessed and managed; 3. set the Bank’s strategic goals, ensure that the necessary

financial and human resources are in place for the Bank to meet its objectives and review management performance; and 4. set the Bank’s values and standards and ensure that its obligations to its shareholders and others are understood and met. In carrying out these responsibilities, the Board must ensure that management strikes an appropriate balance between promoting long term growth and delivering short term objectives and have regard to what is appropriate for the Bank’s business and reputation, the materiality of the financial and other risks inherent in the business and the relative costs and benefits of implementing specific controls.

All Directors must act in the way they consider, in good faith, would be the most likely to promote the success of the Bank for the benefit of its shareholders as a whole. In doing so, each director, must have regard (among other matters) to the:

1. likely consequences of any decision in the long term; 2. interests of the Bank's employees and shareholders; 3. need to foster the Bank's business relationships with suppliers, customers and others; 4. impact of the Bank's operations on the community and the environment; 5. desirability of the Bank maintaining a reputation for high standards of business conduct and ethics; and 6. need to act fairly as between the shareholders of the Bank.

When carrying out their responsibilities, Directors must 1. act with integrity; 2. act with due skill, care and attention; 3. observe proper standards of market conduct; 4. deal with the regulatory authorities in an open and co-operative way and must disclose appropriately any information of which the regulator would reasonably expect notice.

Board

The Board composition represents an appropriate mix of professional skills and expertise. The current Board of Directors was elected at the Annual General Meeting held on 28 March 2012 for a period of three years. The Board periodically reviews its composition and performance as well as the performance of each Director. The name and classification of each Director as of 31 December 2014 is listed below:

Directors Classification

Fahad Al-Rajaan Chairman 1 Independent

Rashed Ismail Al-Meer - Deputy Chairman Non-Executive

Mohammad Jassim Al-Marzooq – Deputy Chairman 2 Non-Executive

Mohammed Saleh Behbehani Independent

Mohammed Fouad Al-Ghanim Independent

Abdulla MH Al-Sumait Non-Executive

Turki Bin Mohamed Al-Khater 3 Independent

Herschel Post Independent

Michael Essex Independent

Adnan Al-Marzouq 4 Independent

Adel A. El-Labban Executive

(continued)

Annual Report2014

Ahli United Bank

27

CORPORATE GOVERNANCE

Board Meetings and Attendance

The Board is required to meet at least four times per year.

The Board convenes upon the invitation of the Chairman or upon the request of at least two Directors. All Directors are expected to attend each meeting, unless there are exceptional circumstances that prevent them from doing so.

A summary of the Board meetings held during 2014 and attendance of each Director are detailed below:

Members’ Names No. ofMeetings

Meeting Dates

MeetingsAttended

Fahad Al-Rajaan - Chairman 4

Rashed Ismail Al-Meer 5

Mohammad Jassim Al-Marzooq 3

Mohammed Saleh Behbehani 2

Mohammed Fouad Al-Ghanim 19 Feb 2014 4

Abdulla MH Al-Sumait 25 Mar 2014 5

Turki Bin Mohamed Al-Khater 5 14 May 2014 2

Herschel Post 17 Sept 2014 4

Michael Essex 3 Dec 2014 5

Adnan Al-Marzouq 1

Adel A. El-Labban 5

The CBB Rulebook module HC – 1.3.4 requires individual board members to attend at least 75% of all board meetings in a given financial year. During the year, all directors, except four have attended at least 75% of all Board meetings in the year. The Directors in question have, on each occasion provided their prior explanations for not attending the Board meetings, which indicated that their absence was reasonable and justified. The attendance of all Directors at the Board meetings is reported to the CBB on an annual basis.

Meeting papers are prepared and circulated in advance of meetings and include minutes of meetings of Board Committees held since the previous Board meeting.

Election and Termination of Appointment of Directors Directors are elected for a 3 year term. Elections take place in accordance with the Memorandum and Articles of the Bank, the Bahrain Commercial Companies Law and the CBB Rulebook. There is no maximum age limit at which a Director must retire from the Board. Each Director’s membership shall terminate upon the expiry of his term, pursuant to the terms of his Letter of Appointment and/or the provisions of the law.

Induction and Training of Directors

The Bank has an induction programme in place which is designed for each new Director to ensure his contribution to the Board from the beginning of his term. The induction programme includes: i) an introductory pack containing, amongst other things, the Group Overview, Group Organisational Chart, Terms of Reference of the Board and Board Committees and key policies; ii) presentations

on significant financial, strategic and risk issues; and iii) orientation meetings with key management as may be required. As a standing procedure, all continuing Directors are invited to attend orientation meetings.

Ongoing professional development for Directors was conducted during the year.

Board Evaluation

Evaluations of the performance of the Board and the performance of each Director, for 2014, were conducted. Applying a scoring methodology proposed by Ernst & Young, rating of “Good” was achieved for the performance of the Board and a rating of “Excellent” was achieved for the performance of each director, indicating that the views of the majority of the Directors are similar and that the Board is functioning as per its stated role and responsibilities.

Directors’ and Related Parties’ Interests

No Director has entered into, either directly or indirectly, any material contract with the Bank or any of its subsidiaries, nor does any Director have any material conflict of interest with the Bank. The Directors are required to declare any conflict of interest or any potential conflict of interest that exists or that Directors become aware of, to the Chairman and Corporate Secretary as soon as they become aware of them. This disclosure must include all relevant material facts.

The Bank has a procedure for dealing with transactions involving Directors and related parties. Any such transaction will require the approval of the Board, excluding the conflicted Director(s).

(continued)

28

Ahli United Bank

CORPORATE GOVERNANCE

Refer note 25 to the audited consolidated financial statements of the Group for the year ended 31 December 2014 for related party transactions disclosures.

The Terms of Reference of the Board require that all Directors, whether Non-Executive or Executive, should exercise independence in their decision-making and should abstain from any decisions involving any actual or potential conflicts of interest. Should any Director have any doubts with respect to conflicts of interest or potential conflict of interest, the Director should consult the Chairman prior to taking any action that might compromise the Bank.

No Name Purchases Sales No. of shares as of 31-Dec-2014

1 Fahad Al-Rajaan1 - - 181,744

2 Rashed Ismail Al-Meer - - 323,513

3 Mohammad Jassim Al-Marzooq - - 167,197

4 Hershel Post - - -

5 Mohammed Saleh Behbehani 8,325,687 - 164,118,387

6 Mohammad Fouad Al-Ghanim - - 509,570

7 Abdullah MH Al-Sumait - - -

8 Turki Bin Mohamed Al-Khater2 - - -

9 Michael Essex - - -

10 Adnan Al Marzouq 115,500 - 115,500

11 Adel A.El-Labban - - -

Total 165,415,911

Percentage 2.70%

Note : 1. Fahad Al Rajan - Resigned on 22 January 2015.

2. Turki Bin Mohamed Al-Khater - Term of Directorship ceased on 31 March 2015 following Director elections.

As at 31 December 2014, the Directors also held 44,177,565 convertible notes (2013: 68,232,928 convertible notes) that are subject to vesting and other criteria.

All Directors and other Approved Persons have declared all of their interests in other enterprises or activities (whether as a shareholder of above 5% of the voting capital of a company, a manager, or other form of significant participation) in writing to the Board.

The number of shares owned directly and indirectly by Directors as at 31 December 2014 are as follows:

(continued)

Annual Report2014

Ahli United Bank

29

CORPORATE GOVERNANCE

The numbers of shares owned by Senior Management as at 31 December 2014 are as follows:

No Name Purchases SalesNo of shares as of

31-Dec-2014

1 Adel A. El-Labban - - -

2 Sanjeev Baijal - - 1,920,221

3 Keith Gale 1,179,110 - 4,557,488

4 Shafqat Anwar - 200,000 497,285

5 Abdulla Al-Raeesi 1,054,736 1,772,020 1,604,736

6 Sawsan Abulhassan 1,783,264 1,465,265 1,300,105

7 Amr Gadallah - - -

8 Robert Jones - - -

9 Iman Al-Madani - - 10,993

10 James Forster - - -

11 Nevine El-Messeery - - -

12 Nouri Aldubaysi - - -

13 Lloyd Maddock - - -

14 Ayman El-Gammal - - -

As at 31 December 2014, senior management held 11,526,312 convertible notes (2013: 9,885,885 convertible notes) that are subject to vesting and other criteria.

Material Transactions Besides large credit transactions that require Board approval as per the Credit Policy, the Board also approves senior unsecured medium term (greater than 1 year) funding initiatives, strategic investments decisions, as well as any other decisions which have or could have a material financial or reputational impact on the Bank.

Board Committee

The Board may, where appropriate, delegate certain of its powers to an individual Director or to a Committee of Directors and other persons, constituted in the manner most appropriate to those tasks.

The Board has constituted a number of Board Committees, membership of which is drawn from the Directors and to which it has delegated specific responsibilities, through Terms of Reference which are reviewed and adopted by the Board on an annual basis.

All Board Committee members are expected to attend each Committee meeting unless there are exceptional circumstances that prevent them from doing so.

Each Board Committee has access to independent expert advice at the Bank’s expense.

(continued)

30

Ahli United Bank

CORPORATE GOVERNANCE

Notes:

1. Mohammed Al-Ghanim was appointed as an Executive Committee member on 19 February 2014.2. Mohammed Al-Ghanim resigned from Audit & Compliance Committee on 19 February 2014. 3. Adnan Al-Marzouq was appointed as a member of Audit & Compliance Committee and Nominating Committee on 25 March 2014.

The principal Board Committees are:

Executive Committee

The Executive Committee assists the Board in discharging the Board’s responsibilities relating to, amongst other things, credit and market risk.

The Executive Committee consists of 5 members comprising 2 Independent, 2 Non-Executive Directors and 1 Executive Director, the Group CEO & Managing Director.

The Board Committees are each composed of an appropriate mix of professional skills and expertise. The Board periodically evaluates the performance of the Board Committees. The names of the Committee members and their memberships in the Board Committees and attendance at meetings held during 2014 are detailed below:

Board Committees Members Classification No. of Meetings Meeting Dates Meetings

attended

Executive Committee

Fahad Al-Rajaan - Chairman Independent

4

19 Feb 2014 14 May 2014 17 Sept 2014 3 Dec 2014

3

Rashed Ismail Al-Meer Non-Executive 4

Mohammad Jassim Al- Marzooq Non-Executive 2

Mohammed Al-Ghanim1 Independent 4

Adel A. El-Labban Executive 4

Audit and Compliance Committee

Herschel Post - Chairman Independent

4

19 Feb 2014 20 May 2014 17 Sept 2014 2 Dec 2014

4

Mohammed Fouad Al-Ghanim2 Independent 1

Abdulla MH Al-Sumait Non- Executive 4

Turki Bin Mohamed Al-Khater Independent 2

Adnan Al-Marzouq 3 Independent 2

Michael Essex Independent 4

Compensation Committee

Fahad Al-Rajaan- Chairman Independent

220 Jan 14

2 Dec 14

2

Herschel Post Independent 2

Mohammed Saleh Behbehani Independent 2

Nominating Committee

Herschel Post - Chairman Independent

2

16 Sep 14

3 Dec 14

2

Abdulla MH Al-Sumait Non- Executive 2

Turki Bin Mohamed Al-Khater Independent 0

Adnan Al-Marzouq3 Independent 1

Michael Essex Independent 2

Audit & Compliance Committee

The Audit and Compliance Committee is combined with the Corporate Governance Committee and assists the Board in discharging its responsibilities relating to the Bank’s accounting, corporate governance and key persons dealings and market abuse practices, internal audit controls, compliance procedures, risk management systems, financial reporting functions and in liaising with the Bank’s external auditors and regulators to ensure compliance with all relevant regulatory requirements and consistency with best market practices.

The Audit and Compliance Committee consists of 5 members comprising 4 Independent Directors, including the Chairman and 1 Non-executive Director.

Compensation Committee

The Compensation Committee provides an efficient mechanism for reviewing the Bank’s compensation arrangements for its staff and Directors and making recommendations for the Board’s own approval in line with CBB guidelines. The Compensation Committee, amongst other things, sets the remuneration framework for the Bank’s Directors, senior management and staff.

The Compensation Committee consists of 3 members comprising 3 Independent Directors including the Chairman.

(continued)

31Annual Report2014

Ahli United Bank

CORPORATE GOVERNANCE

Senior Management

Names Title

Adel A. El-Labban Group CEO & Managing Director

Sanjeev Baijal Deputy Group CEO - Finance & Strategic Development

Keith Gale Deputy Group CEO - Risk, Legal & Compliance

Shafqat Anwar Deputy Group CEO - Operations & Technology

Abdulla Al-Raeesi Deputy Group CEO - Retail Banking

Sawsan Abulhassan Deputy Group CEO - Private Banking & Wealth Management

Amr Gadallah Deputy Group CEO - Treasury & Investments

Robert Jones Group Head of Audit

Iman Al-Madani Group Head Human Resources & Development

James Forster CEO - Ahli United Bank (UK) P.L.C

Nevine El-Messeery CEO - Ahli United Bank (Egypt) S.A.E.

Nouri Aldubaysi CEO - Commercial Bank of Iraq P.S.C.

Lloyd Maddock CEO - Ahli Bank S.A.O.G

Ayman El-Gammal CEO -United Bank for Commerce & Investment S.A.C

The CBB Rulebook Module HC-5.3.1A requires the Chairman of the Compensation Committee to be independent of risk taking function or Committees. During 2014, the Chairman of Compensation Committee was also the Chairman of the Executive Committee. Following the resignation of the Chairman of these Committees and the reconstitution of the Board Committees pursuant to Board elections to be held in March 2015, the bank will be in compliance with this requirement.

Nominating Committee

The Nominating Committee supports the Corporate Governance regime of the Bank and instills a best practice approach to the matters assigned to its responsibilities, at all times acting within the criteria set by the CBB Rulebook, the relevant sections of the Bahrain Commercial Companies Law and any other applicable legislation, following a fair and balanced approach.

The principal responsibilities of the Nominating Committee include, identifying and recommending to the Board persons qualified to become a Director of the Board, or any other officer of the Bank, as considered appropriate by the Board. The Committee also oversees the Director’s educational activities in the form of a formal induction program and on-going orientation activities and programs.

The Nominating Committee consists of 5 members comprising 4 independent Directors, including the Chairman and 1 Non-Executive Director.

Board Committee Evaluation

Evaluations of the performance of the Board Committees have been conducted. Applying a scoring methodology proposed by Ernst &Young, a rating of “Excellent” was achieved for each, indicating that the Board Committees continue to operate with a high degree of effectiveness.

(continued)

32

Ahli United Bank

Ahli United Bank

CORPORATE GOVERNANCE(continued)

Management Committees

The Board of Directors has established a management structure with clearly defined roles, responsibilities and reporting lines. The Bank’s management monitors the performance of the Bank and each of its subsidiaries and associates on an ongoing basis and reports this performance to the Board. The monitoring of performance is carried out through a regular assessment of performance trends against budget, and prior periods and peer Banks in each of the markets and collectively through AUB Group committees and sub committees at the parent bank and its subsidiary / affiliated banks’ level. Specific responsibilities as explained below, have been delegated to each committee, and the minutes of all management committees are sent to the Audit and Compliance Committee, that assesses the effectiveness of these committees.

Group Management Committee

The Group Management Committee is the collective AUB Group management forum providing a formal framework for effective consultation and transparent decision-making by the Group CEO & Managing Director and senior management on cross-organisational matters. Appropriate checks and balances ensure the “four eyes” regulatory requirement is met. The Committee has broad mandate encompassing group wide as well as Bank and unit specific issues as determined by the Group CEO & Managing Director and other members of the committee. It is chaired by the Group CEO & Managing Director and comprises of thirteen other members, including all Deputy Group CEO’s and CEO’s of subsidiary and affiliated banks.

Group Asset and Liability Committee

The Group Asset and Liability Committee sets, reviews and manages the liquidity, market risk and funding strategy of the AUB Group and reviews and allocates capacity on the balance sheet to achieve targeted return on capital, return on asset and liquidity ratios. It is chaired by the DGCEO-Treasury & Investment and has eight other members.

Group New Product Committee

The Group New Product Committee reviews and approves new products, processes and services for wealth management, treasury, retail, commercial banking and other areas of the AUB Group. The committee assesses all related reputational, operational, credit, liquidity and market risk, IT, legal, compliance, control, staffing and capital/profit allocation issues related to approving new products. The approval by the Group New Product Committee follows the new product or process development requirements according to the New Product Approval and Development Procedure. It is chaired by DGCEO-Private Banking & Wealth Management and has seven other members.

Group Information Technology Steering Committee

The Group Information Technology Steering Committee oversees the information technology role, strategy formulation, prioritized implementation and delivery of IT projects of the AUB Group within an acceptable, secure and standardised framework. It

recommends the annual IT budget to the Group CEO & Managing Director as part of the annual business planning/budgetary exercise for submission to the Board of Directors for review and final approval. It supervises the implementation of the approved IT annual plan within set deadlines and budgetary/Board approved allocations within the Bank’s overall capital expenditure policy. It is chaired by the DGCEO-Retail Banking and comprises of seven other members.

Group Risk Committee

The Group Risk Committee reviews and manages the risk asset policies, approvals, exposures and recoveries related to credit, operational and compliance risks. It acts as a general forum for the discussions of any aspect of risk facing or which could potentially face the Bank or its subsidiaries and affiliates resulting in reputational or financial loss to the AUB Group. It also oversees the operation of the Group Operational Risk Sub-Committee and Group Special Assets Sub-Committee. It is chaired by the DGCEO-Risk, Legal & Compliance and has four other members.

Group Operational Risk Sub-Committee

Group Operational Risk Sub-Committee administers the management of operational risk throughout the AUB Group. It is chaired by the DGCEO-Operations & Technology and has eight other members.

Group Special Assets Sub-Committee The Group Special Assets Sub-Committee is responsible for the management of the criticized and non-performing assets of the Bank. It has responsibility for monitoring accounts downgraded to watch list and criticized asset status and ensuring that a focused and disciplined recovery strategy is adopted to maximize recoveries. It is chaired by DGCEO Risk, Legal & Compliance and has seven other members.

Management Committee

The Management Committee is the senior collective management forum of the Bank, providing a formal framework for effective consultation and transparent decision-making on organizational matters. Appropriate checks and balances ensure the “four eyes” regulatory requirement is met. The committee operates in a flexible way with a minimum of formality and a broad mandate encompassing both Bank-wide and unit specific issues as determined by the GCEO & Managing Director and its other members in relation to the business of the Bank, as a legal entity. It is chaired by the DGCEO Finance & Strategic Development and has seven other members.

AUB Asset and Liability Committee

AUB Asset and Liability Committee sets, reviews and manages the liquidity, market risk and funding strategy of AUB, the parent bank reviews and allocates capacity on the balance sheet to achieve targeted return on capital, return on asset and liquidity ratios. It is chaired by Group Head of Treasury and has eight other members.

34

Ahli United Bank

CORPORATE GOVERNANCE

Other Governance Measures

In addition to the Board and Management Committee structures, the Board of Directors has approved a number of AUB Group policies to ensure clarity and consistency in the operation of the AUB Group. These policies, which are communicated to staff, include Credit, Anti-money Laundering, Corporate Governance, Personal Account Dealing, Key Persons Dealings, Banking Integrity, Compliance, Legal and Human Resources policies.

Underpinning these policies is the Board approved Group Code of Business Conduct which prescribes standards of ethical business behavior and personal conduct for the Bank’s Directors, its senior management (officers) and its staff.

The Board of Directors of Ahli United Bank B.S.C. (BoD) annually reviews and adopts compensation and related policies and closely monitors the implementation of these policies and processes with respect to the Bank’s staff and Directors. The AUB Compensation Policy provides the remuneration framework for motivating employees and directors with financial motivation to deliver optimum Group performance. The policy aims at rewarding performance by individual contribution within a team oriented approach, remunerating individuals who achieve personal, divisional and Group results and providing a long term incentive to performing staff.

The Banking Integrity Policy, which includes detailed policy and procedures on whistle blowing is specifically designed to facilitate concerns raised with regard to misconduct occurring within, or associated with, the AUB Group.

The Board has also adopted a Group Communications Policy. This policy sets out the authority of AUB Group employees with respect to the communication of information to third parties in the course and scope of their employment. The Bank has an open policy on communication with its stakeholders, which includes: (i) The disclosure of all relevant information to stakeholders on a timely basis in a timely manner; and

(ii) The provision of at least the last three years of financial data on the bank’s website.

Shareholders are invited by the AUB Chairman to attend the AGM. The AUB Chairman and other Directors attend the AGM and are available to answer any questions. The Bank is at all times mindful of its regulatory and statutory obligations regarding dissemination of information to its stakeholders.

The Bank provides information on all events that merit announcement, either on it’s website, www.ahliunited.com, Bahrain Bourse, and other forms of publications, such as press releases, the Bank’s annual report and quarterly financial statements, and the Corporate Governance Policy are all published on it’s website.

As a supporting governance measure, the Board also relies on the ongoing reviews performed by internal and external auditors on the AUB Group’s internal control functions. These reviews are conducted in order to identify any weaknesses, which then enable management to take remedial action.

Compensation disclosures

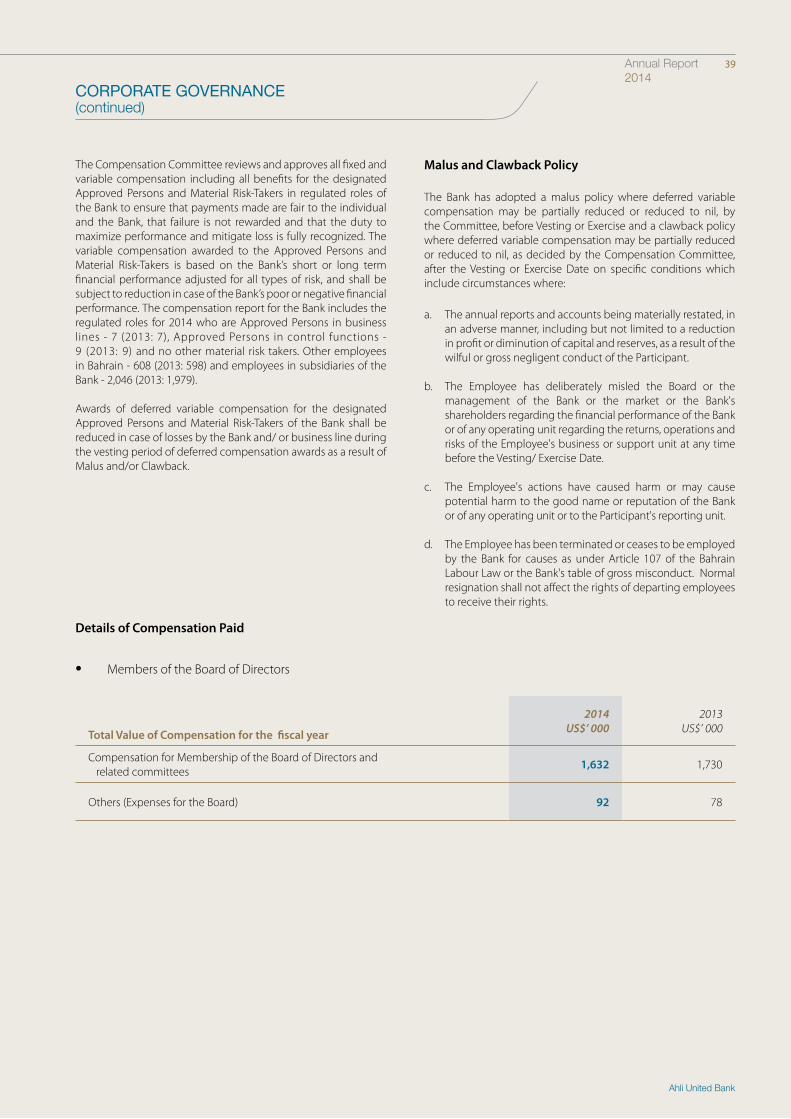

Ahli United Bank's Compensation Policy (the "Policy") provides the framework for the Bank to attract, retain and motivate employees and directors with financial compensation to deliver optimum personal, functional and Bank performance and reduce the individual's motivation to take excessive and undue risk. This is delivered through a compensation system consisting of Fixed Compensation for employees and directors and Variable Compensation of short term and long term incentives for performing employees.

The Board of Directors reviews and approves on an annual basis, the HR policy and as its integral part, the Compensation and related policies and closely monitors the implementation and administration of these policies and processes with respect to the Bank's employees and directors.

The CBB has issued mandatory regulations relating to Sound Remuneration Practices through an amendment to its rulebook [HC-5 Remuneration of Approved Persons and Material Risk-Takers], effective 1 July 2014 applicable to Approved Persons and Material Risk-Takers of the Bank whose total annual remuneration (including all benefits) is in excess of BD100,000 equivalent. As advised by the CBB, the revisions in the Policy and related schemes have been approved by the shareholders of the Bank in their Annual General Meeting on 31 March 2015 and applied to performance related employee compensation payments made for the financial year 2014. The salient features of the Bank's Policy including the key changes are summarized below:

The Compensation System

The compensation system includes a fixed component (consisting of cash salary, allowances and benefits) that rewards the capacity to hold a role/ position in a satisfactory manner through the employee displaying the required skills and, a variable component (consisting of performance related compensation) that aims to reward collective and individual performance, depending on objectives defined at the beginning of the year and conditional on meeting said objectives, according to performance standards and risk parameters defined by the Bank.

The Compensation system is based on the Bank’s long and short term performance and matches the full gamut of the Bank’s risks and their timeline. The system links and adjusts compensation with all types of risks in the Bank to reduce the incentive for individuals to take excessive and undue risk. It specifies the proportion of fixed and variable remuneration to be consistent with the Board approved Risk Framework. It defers portions of the variable compensation awards for 2014 and subsequent years for the designated Approved Persons and Material Risk-Takers of the Bank over a period of 3 years as required by the CBB. It reduces the awarded deferred variable remuneration in case of losses by the Bank and/ or business line during and after the exercise/ vesting period of the deferred variable compensation as a result of malus and clawback arrangements.

The policy also outlines the basis and methodology for arriving at variable compensation, making allocations, implementing risk adjustments to compensation, the framework for compensation of Approved Persons and Material Risk-Takers, conditions for

(continued)

Annual Report2014

Ahli United Bank

35

CORPORATE GOVERNANCE(continued)

deferral malus and claw-back clauses, compliance and disclosure requirements. It also establishes the terms of the Mandatory Share Plan (MSP) scheme and the extension of the existing Employee Share Purchase Plan (ESPP) scheme to comply with CBB regulations and deliver deferred variable compensation in equity/ shares. All equity schemes awards being limited so as not to exceed an aggregate 10% of the total issued outstanding ordinary share capital of the Bank, at any given time.

Compensation levels for each grade/ role are determined by industry measurable statistics, relative to size of operations, business needs, cost control and long term business goals which attracts the appropriate talent to the Bank. Compensation is determined through job evaluation, market benchmarks, performance outcome and aligned to long-term value creation and prudent risk-taking. The Bank ensures that compensation is equitable and team oriented, clearly communicated and adjusted for all types of risk, including reputation risk, liquidity risk and costs of capital. Annual performance and compensation reviews are conducted in March of each year. Employees are not entitled to any additional compensation from their membership of or attendance at Board or Board Committee meetings as a nominee or representative of the Bank. All such fees are assigned to the Bank.

Role of the Compensation Committee

The Compensation Committee (the "Committee") is vested by the Board of Directors through its Terms of Reference with the essential responsibility, inter alia, to provide effective oversight and assure governance over the compensation strategy, structure and systems, to ensure that they are properly implemented. Such responsibilities include, but are not limited to, review and oversight of AUB's compensation and related policies and arrangements for its employees and directors and ensures that any amendments or

updates are annually applied to meet the Bank’s objectives and aligned to CBB regulations, the Kingdom of Bahrain Labour Law for the Private Sector ("Labour Law") and the Bahrain Commercial Companies Law, 2001 (the "Companies Law") , where necessary.

The Chairman and members of the Committee are appointed by the Board from amongst its Directors. The Committee comprises at least 3 members, which should include only Independent Directors or, alternatively, only Non-Executive Directors, of whom a majority are Independent Directors. The Chairman may appoint an alternate member in case of absence of a member. Committee details and meeting dates in 2014 are reproduced in the Corporate Governance Report in this Annual Report. The aggregate compensation/ fees paid to Committee members for 2014 amounted to US$ 12,000.

The Committee approves the annual aggregate amounts payable under fixed and performance related variable compensation schemes for employees. The Committee reviews and approves any material changes in employee benefits as per market competitive trends and cost considerations and makes recommendations with regard to any other employee matters, as brought before it. The Committee reviews compensation payable to the members of the Board of Directors and makes recommendations to the Board of Directors in this regard in line with applicable regulations.

The Committee reviews and tests at least on an annual basis, the Policy and framework to ensure that compensation arrangements comply with regulations and internal policies and to ensure that the compensation system operates as intended and that effective controls exist through testing of compensation outcomes as per the Bank’s risk framework with any breaches of the risk framework used in the evaluation of malus and/ or clawback clauses on deferred compensation by the Committee.

The authority matrix for compensation approvals are as follows:

Action Recommended by Approved by

a) Approve the Bank's annual performance bonus pool funding model based on KPI and KPI and KRI adjustments.

Group Head of HR&DCompensation

Committee

b) Approve the Bank's annual performance bonus amount pool. Group Head of HR&DCompensation

Committee

c) Approve the criteria for performance management and distribution of the Bank's annual performance bonus.

Group Head of HR&DCompensation

Committee

d) Approve the list of designated "Approved Persons and Material Risk Takers" for previous financial year.

Group Head of HR&DCompensation

Committee

e) Approve the performance scores, annual increment and annual performance bonus amounts for the GCEO & MD and his direct reports.

Group Head of HR&D (except self )

Compensation Committee

f ) Approve the performance scores, annual increment and annual performance bonus amounts for the Group Head of Audit and Group Head of Compliance

Audit & Compliance Committee

Compensation Committee

g) Approve the aggregate performance scores, annual increment and annual performance bonus amounts for all other bank employees.

Group Head of HR&DCompensation

Committee

36

Ahli United Bank

CORPORATE GOVERNANCE

Types of Compensation

Compensation for employees includes fixed compensation, benefits and performance related incentives (short-term and long-term variable compensation) in cash or shares each as defined and approved by the Compensation Committee. Compensation for the Board of Directors is explained later in this report.

External Consultants

Consultants were appointed during the year to advise the Bank on revisions to the Policy and alignment to the new regulations and market best practices including providing consulting advice for the deferred share/ equity-linked schemes.

Compensation of the Board of Directors

The Compensation Committee periodically reviews the compensation for the Board of Directors and its related Committees to ensure compliance with the CBB Rule Book, within the relevant Commercial Companies Law requirements and with the Articles of Association of the Bank. The Bank is in compliance with the CBB Rule Book High Level Controls Module Article No.5.2.1 (c) requiring that compensation of the Board of Directors is linked to attendance and performance with members of the Board of Directors being paid 1/3rd of their total compensation pro-rated on the basis of actual attendance of meetings and the remaining 2/3rd paid for membership unrelated to attendance. Compensation for the Board of Directors and its related committees for 2014 has been approved by the shareholders in the Annual General Meeting on 31 March 2015. The Bank is in compliance with its Articles of Association requiring that total compensation for Directors (excluding sitting fees) is capped at 10% of the Bank's NPAT for 2014, after all the required deductions outlined in Article 188 of the Bahrain Commercial Companies Law, 2001. The compensation of Non-Executive Directors in 2014 does not include any performance-related elements such as shares, share options or other deferred stock-related incentive schemes, bonuses or pension benefits, in compliance with the CBB Rule Book High Level Controls Module Article No.5.5.1. AUB Management Directors who represent or are nominated by AUB or of any of its subsidiaries or affiliates on the Boards or their related Committees are excluded from the compensation/ fees structure as per their contractual arrangements. All Board of Directors' and related Committee fees or other terms of remuneration (except actual expenses) related to representation as AUB nominated Directors are fully credited to AUB. Directors are reimbursed reasonable and customary expenses for communication, transportation, boarding and lodging as per AUB HR policy.

Variable Compensation (Performance Bonus) Pool and Risk Adjustment

Performance-related variable compensation aims at recognizing and rewarding employee’s contribution beyond their regular job requirements, particularly those contributions that increase Bank's productivity and profitability. Performance-related pay could be paid for positive employee performance and/or Bank’s performance. The variable compensation pool is aligned to and

due based on the Bank’s short or long term financial performance, and is subject to reduction in case of the Bank’s poor or negative financial performance.