Embed Size (px)

Citation preview

THE COMING STORM OF CONVERGING TECHNOLOGIES

Research Report 1 in the NAW Series: How Technology Will Transform

Wholesale Distribution

Ian G. Heller

2 NAW Series: How Technology Will Transform Wholesale Distribution

IN THIS RESEARCH REPORT

3 Technology Disruption: This Time It Is Real

3 StaplesOfficeProducts:ASignofWhatIs to Come?

4 The Omnichannel Myth

5 ArtificialIntelligence:SupportingtheDisruptionofWholesaleDistribution

8 AConvergenceofTechnologiesatCollapsingPrices

9 TheImpactofAIonWholesaleDistribution

10 RemovingtheKeyboardandScreenfromtheOnlineOrder

12 TheProliferationofMarketplaces

13 ChannelConfusionandCompression

14 OtherTechnologyChallengesandOpportunities

14 HowtoSurviveandThenThrive

16 TheEraoftheCompany-SpecificWebsiteIsOver

17 TheFutureofTechnologyDisruption

About NAW and the NAW Institute for Distribution Excellence

The National Association of Wholesaler-Distributors (NAW) was created in 1946 to deal with issues of interest to the entire merchant wholesale distribution industry, thereby freeing affiliated associations to concentrate on the concerns specific to their lines of trade. NAW is a federation of wholesale distribution associations and thousands of individual firms that collectively total more than 30,000 companies.

The role of the NAW Institute for Distribution Excellence is to sponsor and disseminate research into strategic management issues affecting the wholesale distribution industry. The NAW Institute for Distribution Excellence aims to help merchant wholesaler-distributors remain the most effective and efficient channel in distribution.

© Copyright 2020 by the National Association of Wholesaler-Distributors. All rights reserved. No part of this research report may be reproduced or stored in a retrieval system, in any form or by any means, without the prior written permission of the publisher.

National Association of Wholesaler-Distributors1325 G Street, NW, Suite 1000Washington, DC 20005202.872.0885www.naw.org

Research Report 1: The Coming Storm of Converging Technologies 3

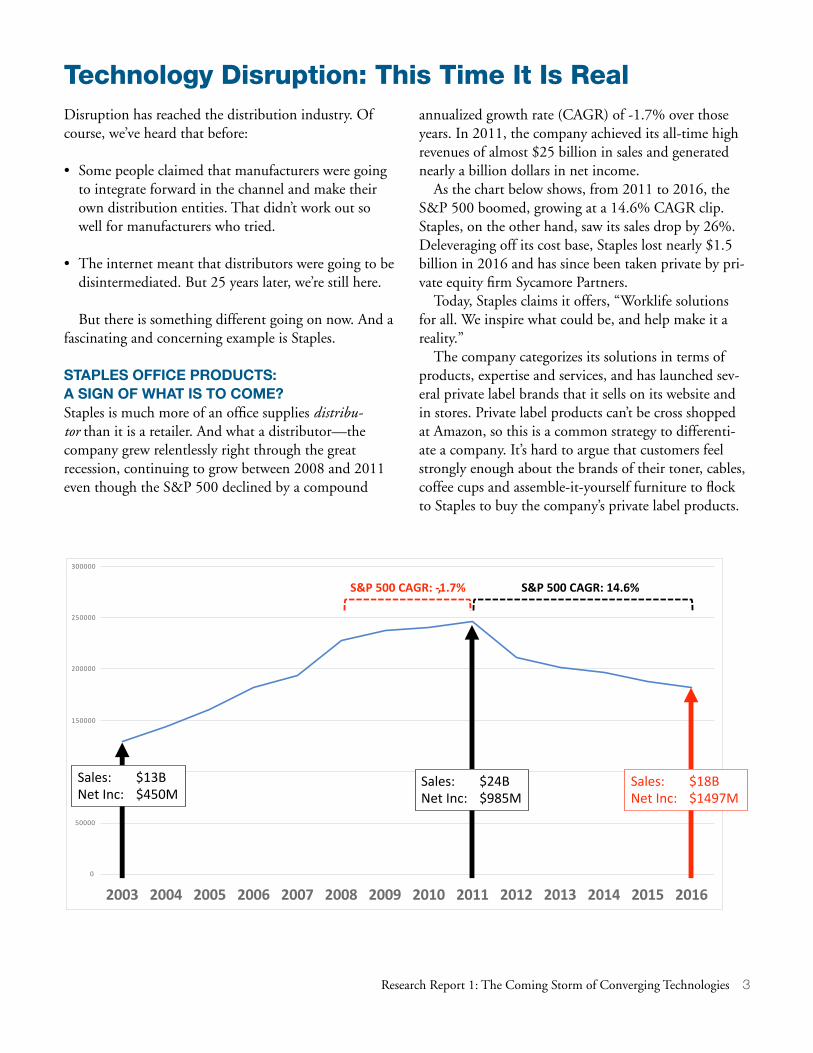

Technology Disruption: This Time It Is Realannualized growth rate (CAGR) of -1.7% over those years. In 2011, the company achieved its all-time high revenues of almost $25 billion in sales and generated nearly a billion dollars in net income.

As the chart below shows, from 2011 to 2016, the S&P 500 boomed, growing at a 14.6% CAGR clip. Staples, on the other hand, saw its sales drop by 26%. Deleveraging off its cost base, Staples lost nearly $1.5 billion in 2016 and has since been taken private by pri-vate equity firm Sycamore Partners.

Today, Staples claims it offers, “Worklife solutions for all. We inspire what could be, and help make it a reality.”

The company categorizes its solutions in terms of products, expertise and services, and has launched sev-eral private label brands that it sells on its website and in stores. Private label products can’t be cross shopped at Amazon, so this is a common strategy to differenti-ate a company. It’s hard to argue that customers feel strongly enough about the brands of their toner, cables, coffee cups and assemble-it-yourself furniture to flock to Staples to buy the company’s private label products.

Disruption has reached the distribution industry. Of course, we’ve heard that before:

• Some people claimed that manufacturers were going to integrate forward in the channel and make their own distribution entities. That didn’t work out so well for manufacturers who tried.

• The internet meant that distributors were going to be disintermediated. But 25 years later, we’re still here.

But there is something different going on now. And a fascinating and concerning example is Staples.

STAPLES OFFICE PRODUCTS: A SIGN OF WHAT IS TO COME?Staples is much more of an office supplies distribu-tor than it is a retailer. And what a distributor—the company grew relentlessly right through the great recession, continuing to grow between 2008 and 2011 even though the S&P 500 declined by a compound

0

50000

#!!!!!

150000

200000

250000

300000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sales: $13BNet Inc: $450M

Sales: $24BNet Inc: $985M

Sales: $18BNet Inc: $1497M

S&P 500 CAGR: -1.7%, S&P 500 CAGR: 14.6%

4 NAW Series: How Technology Will Transform Wholesale Distribution

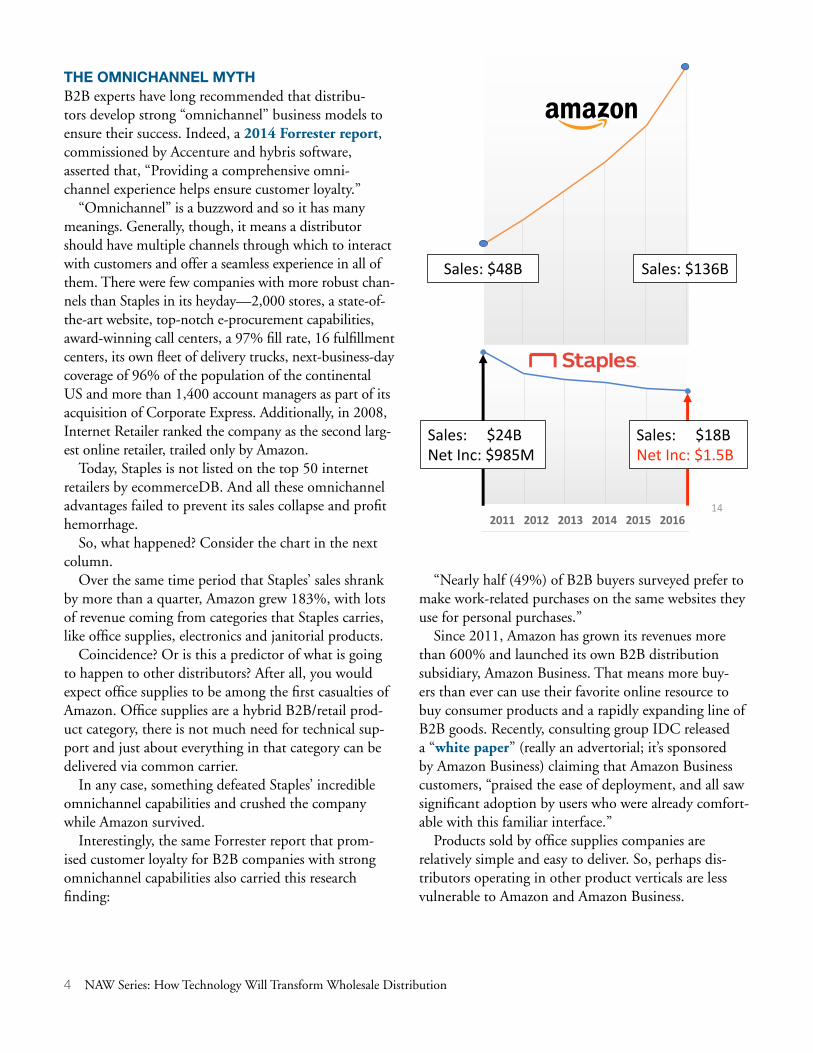

THE OMNICHANNEL MYTHB2B experts have long recommended that distribu-tors develop strong “omnichannel” business models to ensure their success. Indeed, a 2014 Forrester report, commissioned by Accenture and hybris software, asserted that, “Providing a comprehensive omni- channel experience helps ensure customer loyalty.”

“Omnichannel” is a buzzword and so it has many meanings. Generally, though, it means a distributor should have multiple channels through which to interact with customers and offer a seamless experience in all of them. There were few companies with more robust chan-nels than Staples in its heyday—2,000 stores, a state-of-the-art website, top-notch e-procurement capabilities, award-winning call centers, a 97% fill rate, 16 fulfillment centers, its own fleet of delivery trucks, next-business-day coverage of 96% of the population of the continental US and more than 1,400 account managers as part of its acquisition of Corporate Express. Additionally, in 2008, Internet Retailer ranked the company as the second larg-est online retailer, trailed only by Amazon.

Today, Staples is not listed on the top 50 internet retailers by ecommerceDB. And all these omnichannel advantages failed to prevent its sales collapse and profit hemorrhage.

So, what happened? Consider the chart in the next column.

Over the same time period that Staples’ sales shrank by more than a quarter, Amazon grew 183%, with lots of revenue coming from categories that Staples carries, like office supplies, electronics and janitorial products.

Coincidence? Or is this a predictor of what is going to happen to other distributors? After all, you would expect office supplies to be among the first casualties of Amazon. Office supplies are a hybrid B2B/retail prod-uct category, there is not much need for technical sup-port and just about everything in that category can be delivered via common carrier.

In any case, something defeated Staples’ incredible omnichannel capabilities and crushed the company while Amazon survived.

Interestingly, the same Forrester report that prom-ised customer loyalty for B2B companies with strong omnichannel capabilities also carried this research finding:

“Nearly half (49%) of B2B buyers surveyed prefer to make work-related purchases on the same websites they use for personal purchases.”

Since 2011, Amazon has grown its revenues more than 600% and launched its own B2B distribution subsidiary, Amazon Business. That means more buy-ers than ever can use their favorite online resource to buy consumer products and a rapidly expanding line of B2B goods. Recently, consulting group IDC released a “white paper” (really an advertorial; it’s sponsored by Amazon Business) claiming that Amazon Business customers, “praised the ease of deployment, and all saw significant adoption by users who were already comfort-able with this familiar interface.”

Products sold by office supplies companies are relatively simple and easy to deliver. So, perhaps dis-tributors operating in other product verticals are less vulnerable to Amazon and Amazon Business.

140

50000

100000

150000

200000

250000

300000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

50000

100000

150000

200000

250000

300000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sales: $24BNet Inc: $985M

Sales: $18BNet Inc: $1.5B

Sales: $136BSales: $48B

Research Report 1: The Coming Storm of Converging Technologies 5

Few, if any, distributors have omnichannel capabili-ties as robust as Staples. So, it’s important to understand how disruption is occurring in the wholesale distribu-tion industry, how to evaluate vulnerability and, most importantly, how to fight back.

The foundations of this disruption lie in the acceler-ating pace of technological change that is enabling new capabilities and creating new competitors.

ARTIFICIAL INTELLIGENCE: SUPPORTING THE DISRUPTION OF WHOLESALE DISTRIBUTIONArtificial intelligence (AI) is driving a revolution in the wholesale distribution industry and yet most executives think it’s just a fancy term for “advanced technology.” If that is what you believe, then you have a hole in your knowledge base that could doom your company.

You have to understand AI in order to grasp what is driving distribution industry disruption, so here is a primer:

We’re used to seeing AI-enabled robots in movies. If we’re having a good day, we think of Star Wars’ R2D2, but if we’re having a bad day, we think of The Terminator. However, that is not really where AI is today.

AI is about where the internet was in 1995. AI is very early in its existence. And, for those of you who remem-ber 1995, there were all kinds of terms we were hearing for the first time: HTML, the worldwide web, the inter-net. We didn’t really understand what the difference was between these terms and how they were related. But we knew that they had something to do with the “informa-tion superhighway.”

And some people back then claimed the internet was going to be bigger than the industrial revolution, which seemed crazy. After hundreds of years since the last economic revolu-tion, were we really going to experience one in our own lifetimes?

We did. The internet revolution was every bit the equal of the indus-trial revolution. Today we’re hearing a new set of terms: artificial

intelligence, machine learning, big data. We’re not really sure how these things are interrelated, either. They are kind of mysterious, just like those internet terms were, but people are telling us, “Hey, this is going to be bigger than the internet revolution.”

It’s hard not to be skeptical. “In 25 years, we’re going to go through two economic revolutions?”

But it’s true. AI is going to be as big a disruptor in the world and, thus, in distribution, as the internet was. And so, you have to get grounded in it, because you can’t formulate a strategy in 2020 without understand-ing AI, just like you couldn’t formulate a strategy in 1995 if you didn’t understand the internet.

In 1995, if you were doing a five-year plan for your company and you didn’t know what the inter-net was, and you couldn’t speculate about things like e-commerce or EDI, or e-procurement, how good would your strategy have been? Not very. It would have fallen apart pretty quickly.

Today, if you don’t understand AI, what it does, the implications of it, and how it might change your cus-tomers’ expectations and your competitive set, and the capabilities you can build using it, you won’t be able to formulate a good strategy going forward.

AI Use Case No. 1: Board GamesLet’s begin by reviewing an extraordinary event that happened in 1997. For the first time in history, a com-puter beat the world grandmaster of chess. The guy on the right in the photo below is Gary Kasparov. He thought no computer could ever beat him and, as you can tell by his body language, he was wrong.

6 NAW Series: How Technology Will Transform Wholesale Distribution

The screen on the left in that same photo represents IBM Deep Blue, the first computer ever to beat the best human chess player in the world.

But IBM Deep Blue was not artificial intelligence. This highly specialized computer came out of the lab able to play chess. How did that happen? IBM hired some chess masters, and they analyzed a lot of data and then programmed into the machine how it should respond to every conceivable situation on the board.

IBM Deep Blue didn’t actually learn how to play chess. It didn’t get better at playing chess without human intervention. With a lot of processing power and memory (for that era) and some highly special-ized programming, it beat the best human chess player in the world. But even one of the programmers, Joe Doane, said, “This is not an artificial intelligence proj-ect in any way.”

Powerful computers do not equate to artificial intel-ligence. AI is an entirely new class of technology. Let’s contrast IBM Deep Blue with something that happened in 2016, when a Google subsidiary called, DeepMind, came up with a system called AlphaGo, which played a much more complicated game than chess.

“Go” is a Chinese board game that has one quadril-lion times more possible moves than chess. Go has approximately the same number of legal moves as there are atoms in the known universe. As a result, it’s wildly more difficult for computers to master than chess and many people thought it could never ever be done.

In this photo below, you see AlphaGo facing off against one of the best Go players in the history of the

planet—Lee Sedol. Lee has been the world champion 18 times, but AlphaGo still beat him.

It’s not just that AlphaGo won which is amazing; it’s how it won. One observer noted, “AlphaGo dazzled its opponent with creative moves, one of which overturned hundreds of years of Go wisdom.”

It’s impressive, of course, that a computer exhibits human-like characteristics such as creativity, but what is more amazing is that AlphaGo taught itself how to play Go. How did that happen? Developers programmed in the basic rules of Go and fed AlphaGo what they called “numerous games” of competent players. And then AlphaGo played against itself over and over and over again, until it taught itself to become the most incred-ible GO player on the planet.

And now it’s not even close; these systems are much better than any human. The current Go champion is called AlphaZero. DeepMind thought it would be interesting to see how well it could play chess, so they programmed AlphaZero with only the rules of the game and gave it four hours to practice. In that time frame, AlphaZero played 20 million games against itself; but, of course, it played both sides of the board, so that is like playing more than 40 million games.

And, it became the best chess player in the world, as well as the best Go player in the world—all by teaching itself both games.

That is why “artificial intelligence” is not synony-mous with “advanced technology.” AI is a whole differ-ent category of technology.

AI Use Case No. 2: Autonomous CarsHere is an example that we can all relate to. You’re driving down a dark road at night. You can’t see in any direction—and a deer jumps from the side of the road. What do you do?

Your survival reflexes are going to tell you to swerve left, swerve right, hit the brakes or some combination of these actions, because you don’t have time to think through each of these options and make a careful and deliberate choice.

Autonomous cars suffer none of these limitations. They are better drivers than we are because as humans, we can’t see in the dark and the data we use to decide what to do next is limited to our eyes and our ears.

Research Report 1: The Coming Storm of Converging Technologies 7

Consider all the data you’d like to have top of mind if a deer were to jump in the road as you were driving:

• Can I hit the brakes? What traffic is behind me? A school bus 50 feet back or a small sedan a hundred yards away?

• Can I swerve right or is there a ditch next to the road?

• Can I swerve left or is there a car coming over the hill in front of me?

• What is the deer likely to do next?

• What alternatives have other drivers tried in these circumstances and what were the outcomes?

It really doesn’t matter that we don’t have all that data. We couldn’t possibly think through it quickly enough to decide about taking the best action.

And, even if we had the data and could think it through, we couldn’t possibly move the controls of the car quickly enough to take the right evasive action. So, we rely on our survival reflexes, and we brake, swerve or both. And sometimes we get lucky, miss the deer and don’t cause an accident. And, sometimes bad things happen.

AI systems in autonomous cars suffer from none of these limitations:

• They see the deer coming long before you could, giving them much more time to react. Why? They can see in the dark and nothing escapes their notice.

• They know everything. They know where the traffic is around you. They know how fast you’re going, how long it’s going to take you to brake. AI systems even know what the deer’s next move is likely to be. And, they can instantly decide and act.

There are lots of systems in autonomous cars: lidar, radar, ultrasonic sensors and cameras for measuring dis-tance. When people hear of an “autonomous car,” these are the systems that come to mind.

Autonomous cars will soon be connected to data cen-ters and to each other. That means your autonomous car will not only keep you safe from hitting a deer, it will also coordinate a reaction with surrounding traffic so that you’re not causing an accident with another car by trying to avoid a deer.

It also means that your car will have immediate access to real-time history about what every other autonomous car has done in any situation. It will know the actions those other autonomous cars took and what the out-come was, and it will be able to factor that data into its decision about what to do in your situation.

AI is going to make it safer to sleep behind the wheel than to steer it. And, you’re not going to know that you barely missed a deer until you wake up, because the car jostled a little bit, and you’re going to rewind the video to see what happened.

This technology may sound miraculous to you. And, some people assert that fully autonomous cars are still 30 or 40 years out, or they will never happen.

But, remember that AI is a technology that learns on its own. It doesn’t depend on people to get better at its task. Plus, some key technologies required to make AI effective are rapidly dropping in price. That fact is driv-ing fast development of AI. That means you need to understand how it works, because it’s creating capabili-ties that your customers will require from you soon.

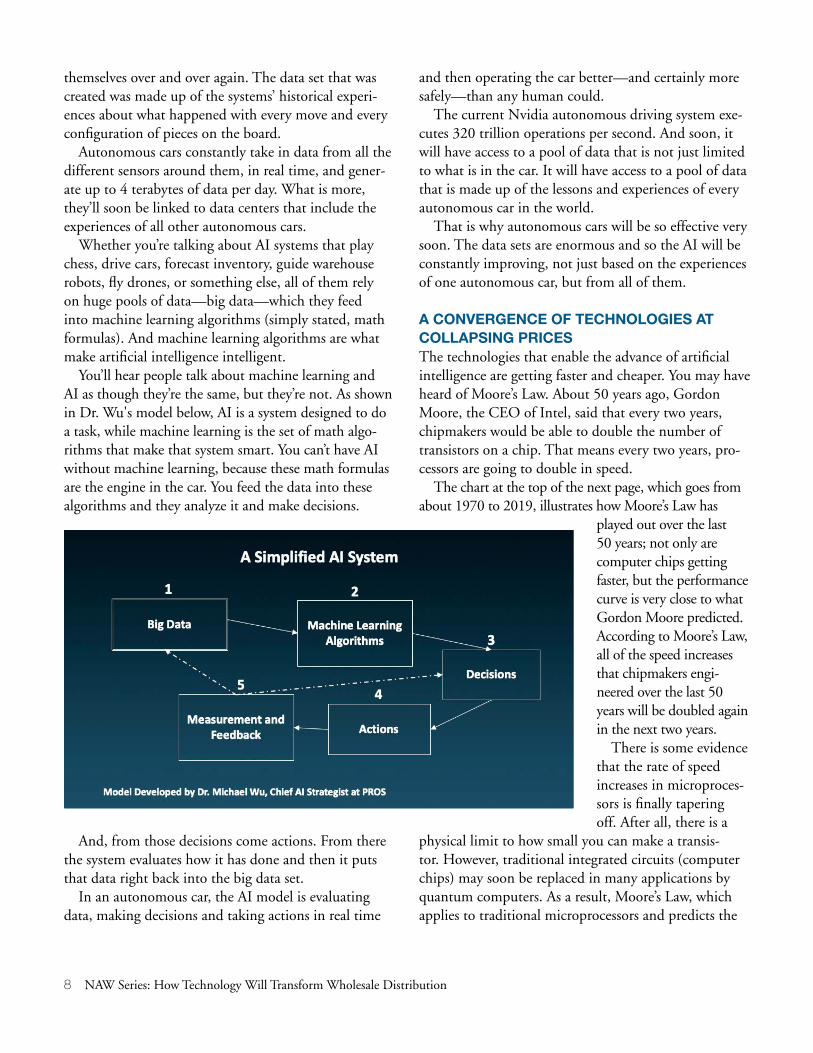

How Artificial Intelligence WorksLet’s explore how artificial intelligence works, using A Simplified AI System model by Dr. Michael Wu of PROS, and let’s start with “big data.”

Big data has many uses, but in this context, big data is an ever-growing pool of data that feeds raw data into AI so it can learn and get smarter. When AlphaGo and AlphaZero needed data to figure out how to get better at Go and at chess, they generated it by playing against

This is the distinguishing characteristic between AI and other forms of technology: AI is the first technology ever that improves

on its own—without human intervention.

8 NAW Series: How Technology Will Transform Wholesale Distribution

themselves over and over again. The data set that was created was made up of the systems’ historical experi-ences about what happened with every move and every configuration of pieces on the board.

Autonomous cars constantly take in data from all the different sensors around them, in real time, and gener-ate up to 4 terabytes of data per day. What is more, they’ll soon be linked to data centers that include the experiences of all other autonomous cars.

Whether you’re talking about AI systems that play chess, drive cars, forecast inventory, guide warehouse robots, fly drones, or something else, all of them rely on huge pools of data—big data—which they feed into machine learning algorithms (simply stated, math formulas). And machine learning algorithms are what make artificial intelligence intelligent.

You’ll hear people talk about machine learning and AI as though they’re the same, but they’re not. As shown in Dr. Wu's model below, AI is a system designed to do a task, while machine learning is the set of math algo-rithms that make that system smart. You can’t have AI without machine learning, because these math formulas are the engine in the car. You feed the data into these algorithms and they analyze it and make decisions.

and then operating the car better—and certainly more safely—than any human could.

The current Nvidia autonomous driving system exe-cutes 320 trillion operations per second. And soon, it will have access to a pool of data that is not just limited to what is in the car. It will have access to a pool of data that is made up of the lessons and experiences of every autonomous car in the world.

That is why autonomous cars will be so effective very soon. The data sets are enormous and so the AI will be constantly improving, not just based on the experiences of one autonomous car, but from all of them.

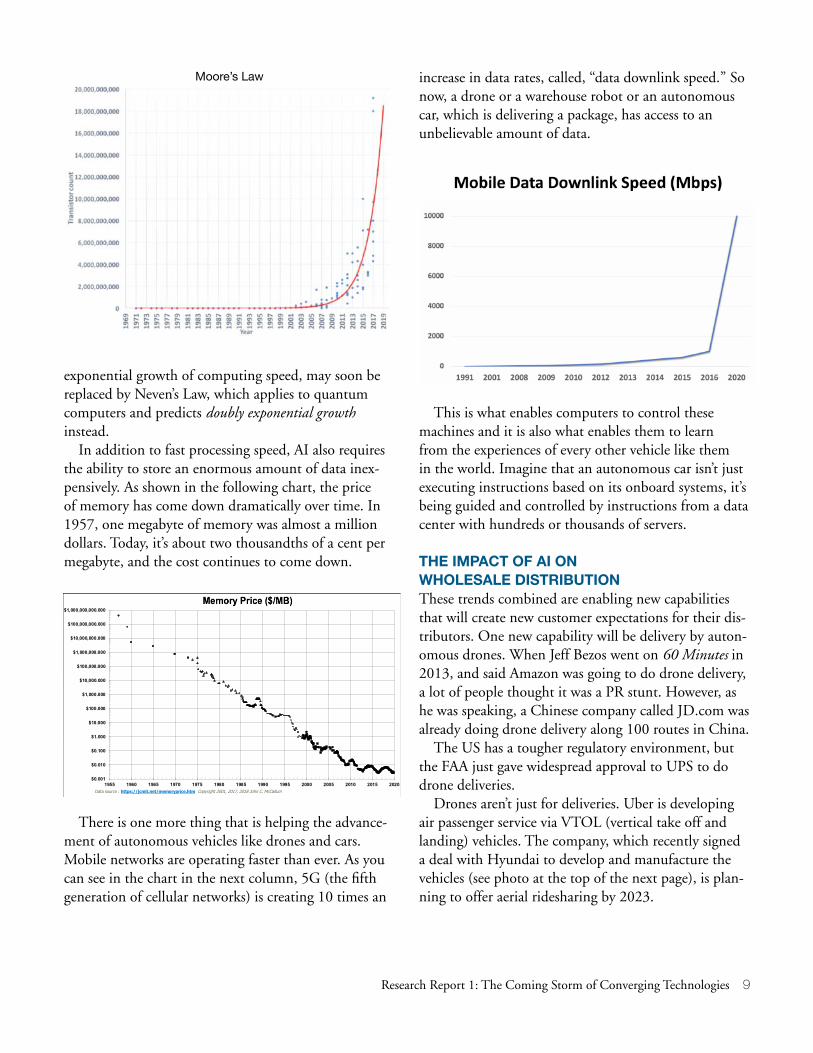

A CONVERGENCE OF TECHNOLOGIES AT COLLAPSING PRICESThe technologies that enable the advance of artificial intelligence are getting faster and cheaper. You may have heard of Moore’s Law. About 50 years ago, Gordon Moore, the CEO of Intel, said that every two years, chipmakers would be able to double the number of transistors on a chip. That means every two years, pro-cessors are going to double in speed.

The chart at the top of the next page, which goes from about 1970 to 2019, illustrates how Moore’s Law has

And, from those decisions come actions. From there the system evaluates how it has done and then it puts that data right back into the big data set.

In an autonomous car, the AI model is evaluating data, making decisions and taking actions in real time

played out over the last 50 years; not only are computer chips getting faster, but the performance curve is very close to what Gordon Moore predicted. According to Moore’s Law, all of the speed increases that chipmakers engi-neered over the last 50 years will be doubled again in the next two years.

There is some evidence that the rate of speed increases in microproces-sors is finally tapering off. After all, there is a

physical limit to how small you can make a transis-tor. However, traditional integrated circuits (computer chips) may soon be replaced in many applications by quantum computers. As a result, Moore’s Law, which applies to traditional microprocessors and predicts the

Research Report 1: The Coming Storm of Converging Technologies 9

exponential growth of computing speed, may soon be replaced by Neven’s Law, which applies to quantum computers and predicts doubly exponential growth instead.

In addition to fast processing speed, AI also requires the ability to store an enormous amount of data inex-pensively. As shown in the following chart, the price of memory has come down dramatically over time. In 1957, one megabyte of memory was almost a million dollars. Today, it’s about two thousandths of a cent per megabyte, and the cost continues to come down.

increase in data rates, called, “data downlink speed.” So now, a drone or a warehouse robot or an autonomous car, which is delivering a package, has access to an unbelievable amount of data.

25

$0.001

$0.010

$0.100

$1.000

$10.000

$100.000

$1,000.000

$10,000.000

$100,000.000

$1,000,000.000

$10,000,000.000

$100,000,000.000

$1,000,000,000.000

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020Data source : https://jcmit.net/memoryprice.htm Copyright 2001, 2017, 2018 John C. McCallum

Moore’s Law

There is one more thing that is helping the advance-ment of autonomous vehicles like drones and cars. Mobile networks are operating faster than ever. As you can see in the chart in the next column, 5G (the fifth generation of cellular networks) is creating 10 times an

This is what enables computers to control these machines and it is also what enables them to learn from the experiences of every other vehicle like them in the world. Imagine that an autonomous car isn’t just executing instructions based on its onboard systems, it’s being guided and controlled by instructions from a data center with hundreds or thousands of servers.

THE IMPACT OF AI ON WHOLESALE DISTRIBUTIONThese trends combined are enabling new capabilities that will create new customer expectations for their dis-tributors. One new capability will be delivery by auton-omous drones. When Jeff Bezos went on 60 Minutes in 2013, and said Amazon was going to do drone delivery, a lot of people thought it was a PR stunt. However, as he was speaking, a Chinese company called JD.com was already doing drone delivery along 100 routes in China.

The US has a tougher regulatory environment, but the FAA just gave widespread approval to UPS to do drone deliveries.

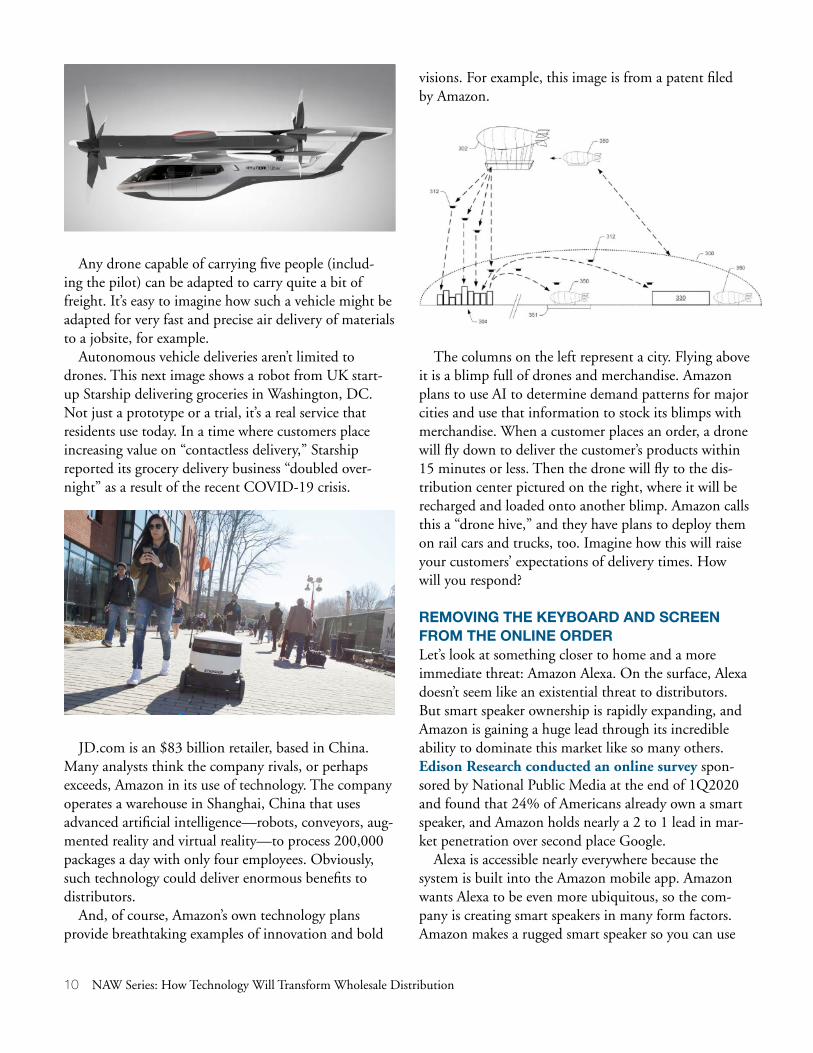

Drones aren’t just for deliveries. Uber is developing air passenger service via VTOL (vertical take off and landing) vehicles. The company, which recently signed a deal with Hyundai to develop and manufacture the vehicles (see photo at the top of the next page), is plan-ning to offer aerial ridesharing by 2023.

10 NAW Series: How Technology Will Transform Wholesale Distribution

Any drone capable of carrying five people (includ-ing the pilot) can be adapted to carry quite a bit of freight. It’s easy to imagine how such a vehicle might be adapted for very fast and precise air delivery of materials to a jobsite, for example.

Autonomous vehicle deliveries aren’t limited to drones. This next image shows a robot from UK start-up Starship delivering groceries in Washington, DC. Not just a prototype or a trial, it’s a real service that residents use today. In a time where customers place increasing value on “contactless delivery,” Starship reported its grocery delivery business “doubled over-night” as a result of the recent COVID-19 crisis.

JD.com is an $83 billion retailer, based in China. Many analysts think the company rivals, or perhaps exceeds, Amazon in its use of technology. The company operates a warehouse in Shanghai, China that uses advanced artificial intelligence—robots, conveyors, aug-mented reality and virtual reality—to process 200,000 packages a day with only four employees. Obviously, such technology could deliver enormous benefits to distributors.

And, of course, Amazon’s own technology plans provide breathtaking examples of innovation and bold

visions. For example, this image is from a patent filed by Amazon.

The columns on the left represent a city. Flying above it is a blimp full of drones and merchandise. Amazon plans to use AI to determine demand patterns for major cities and use that information to stock its blimps with merchandise. When a customer places an order, a drone will fly down to deliver the customer’s products within 15 minutes or less. Then the drone will fly to the dis-tribution center pictured on the right, where it will be recharged and loaded onto another blimp. Amazon calls this a “drone hive,” and they have plans to deploy them on rail cars and trucks, too. Imagine how this will raise your customers’ expectations of delivery times. How will you respond?

REMOVING THE KEYBOARD AND SCREEN FROM THE ONLINE ORDERLet’s look at something closer to home and a more immediate threat: Amazon Alexa. On the surface, Alexa doesn’t seem like an existential threat to distributors. But smart speaker ownership is rapidly expanding, and Amazon is gaining a huge lead through its incredible ability to dominate this market like so many others. Edison Research conducted an online survey spon-sored by National Public Media at the end of 1Q2020 and found that 24% of Americans already own a smart speaker, and Amazon holds nearly a 2 to 1 lead in mar-ket penetration over second place Google.

Alexa is accessible nearly everywhere because the system is built into the Amazon mobile app. Amazon wants Alexa to be even more ubiquitous, so the com-pany is creating smart speakers in many form factors. Amazon makes a rugged smart speaker so you can use

Research Report 1: The Coming Storm of Converging Technologies 11

Alexa in harsher environments. Another device sits on the dash of your car. If you travel frequently, you can buy a compact smart speaker that plugs into a wall. You can also order a smart speaker for your house or your office, so you can ask Alexa to reserve meeting rooms, order supplies, schedule appointments and initiate phone calls with your voice.

Here are three Alexa options that are a little bit dif-ferent: Alexa in your ears, Alexa on your eyes and Alexa on your finger —Alexa Loop.

Apparently, Amazon believes that having Alexa on your phone or in the same room isn’t close enough. They want customers to have Alexa on their bodies.

What is Amazon’s motivation for building Alexa/human mechanical/biological clones? To answer this question, we need to look at some of the job descrip-tions Amazon has posted to see what kind of talent the company is hiring to support its Alexa development.

Here is language Amazon commonly uses in job postings for software development engineers and managers who work on Alexa:

Our vision is that Alexa will be the world’s most knowledgeable product expert who knows you, in a store that sells everything. All those moments when we need or want to know more about the products we use every day will

have instant satisfaction of an answer: just ask Alexa. We are building a digital product expert that is always available, with super-human knowledge of every product ever made.

One obvious implication of this is that Amazon wants customers to be able to place orders without using a keyboard or a screen and only using their own voices. That is a very profound change. Since the first day of the internet, if you wanted to order something, you used a keyboard on a desktop computer or a laptop, or a tablet, or on a mobile device. We just assume that is how it’s done. And, that is the way our customers order from us.

But what if you could take the keyboard out of the equation? It would actually make a lot of sense because the keyboard is a ridiculously slow interface between the computer that is your brain and the computer that you’re trying to put data into. And yet, we connect these two computers with 30 mechanical keys acti-vated manually by 10 fingers. The average adult types 40 words per minute on a computer keyboard and 20 words per minute on a phone.

If you could get around that, you could speed up the purchasing process and deliver vastly better accuracy. And, if you happen to be the only game in town, the only provider that offers that type of ordering, then you would get all the orders.

What are the alternatives to keyboards and screens? It would be ideal to control a computer with your mind. Sound far-fetched? Elon Musk launched a company called Neuralink, which is making good progress, but that is a long way off from mass implementation.

For now, the best alternative to keyboards is voice control and image recognition. Today, smart speakers can easily handle 130 words per minute. And you can interface with the computer while you’re doing other things. You don’t have to be in front of a screen and a keyboard—you can be driving or working.

Now imagine that you combine voice with image recognition as you interface with Alexa. For example, imagine a maintenance worker is using a grinder on steel. He can speak into his voice and camera-enabled helmet to say, “Hey, Alexa, I don’t know what these blades are, but please figure out what they are and deliver 20 to me right here by drone in the next half hour or 15 minutes.”

12 NAW Series: How Technology Will Transform Wholesale Distribution

How much B2B purchasing will happen through this method? Probably not a lot, at least not for a long time. But it can still be an essential service for many customers who want it when they need it, even if they don’t need it often. As a comparison, remember that many B2B customers demand that their suppliers have a good website or mobile app even if they only use that ordering method occasionally. Such innovations raise customer expectations, and so many buyers who didn’t previously purchase from Amazon Business will set up accounts there so they can use this capability when they need it. Of course, once they have those accounts and become familiar with Amazon Business’ value proposi-tion, they are likely to buy more from the company, and that is going to take share from distributors.

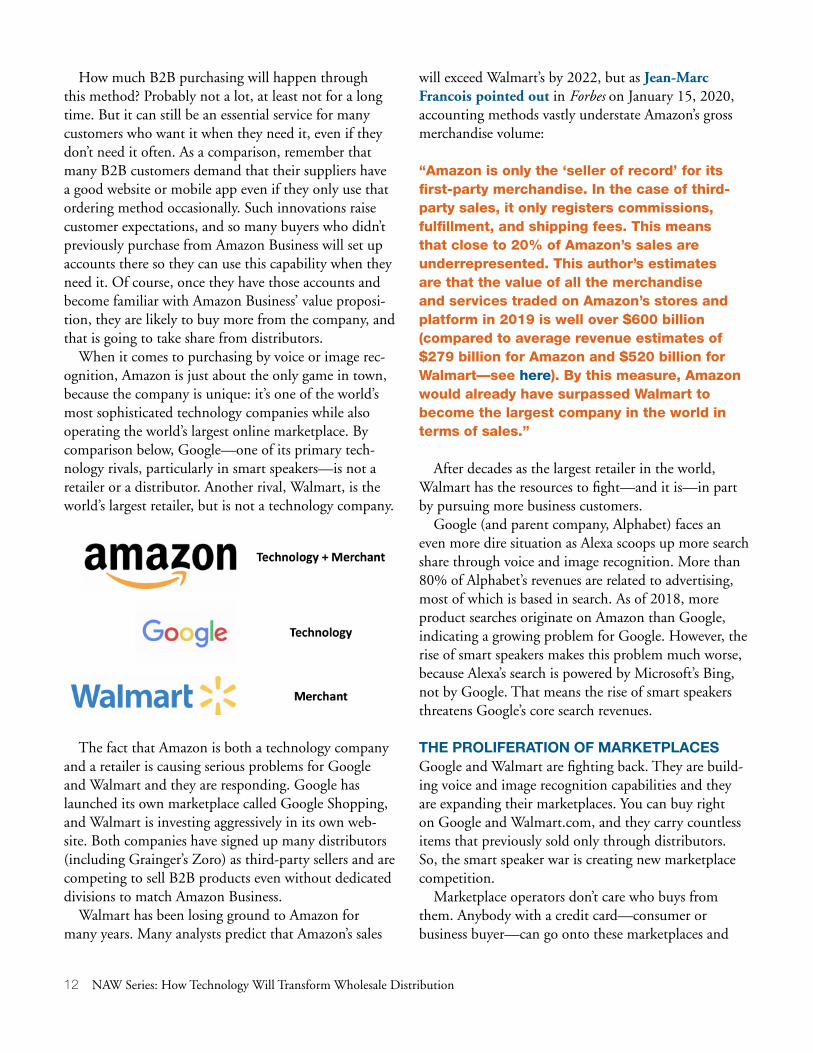

When it comes to purchasing by voice or image rec-ognition, Amazon is just about the only game in town, because the company is unique: it’s one of the world’s most sophisticated technology companies while also operating the world’s largest online marketplace. By comparison below, Google—one of its primary tech-nology rivals, particularly in smart speakers—is not a retailer or a distributor. Another rival, Walmart, is the world’s largest retailer, but is not a technology company.

The fact that Amazon is both a technology company and a retailer is causing serious problems for Google and Walmart and they are responding. Google has launched its own marketplace called Google Shopping, and Walmart is investing aggressively in its own web-site. Both companies have signed up many distributors (including Grainger’s Zoro) as third-party sellers and are competing to sell B2B products even without dedicated divisions to match Amazon Business.

Walmart has been losing ground to Amazon for many years. Many analysts predict that Amazon’s sales

will exceed Walmart’s by 2022, but as Jean-Marc Francois pointed out in Forbes on January 15, 2020, accounting methods vastly understate Amazon’s gross merchandise volume:

“Amazon is only the ‘seller of record’ for its first-party merchandise. In the case of third-party sales, it only registers commissions, fulfillment, and shipping fees. This means that close to 20% of Amazon’s sales are underrepresented. This author’s estimates are that the value of all the merchandise and services traded on Amazon’s stores and platform in 2019 is well over $600 billion (compared to average revenue estimates of $279 billion for Amazon and $520 billion for Walmart—see here). By this measure, Amazon would already have surpassed Walmart to become the largest company in the world in terms of sales.”

After decades as the largest retailer in the world, Walmart has the resources to fight—and it is—in part by pursuing more business customers.

Google (and parent company, Alphabet) faces an even more dire situation as Alexa scoops up more search share through voice and image recognition. More than 80% of Alphabet’s revenues are related to advertising, most of which is based in search. As of 2018, more product searches originate on Amazon than Google, indicating a growing problem for Google. However, the rise of smart speakers makes this problem much worse, because Alexa’s search is powered by Microsoft’s Bing, not by Google. That means the rise of smart speakers threatens Google’s core search revenues.

THE PROLIFERATION OF MARKETPLACESGoogle and Walmart are fighting back. They are build-ing voice and image recognition capabilities and they are expanding their marketplaces. You can buy right on Google and Walmart.com, and they carry countless items that previously sold only through distributors. So, the smart speaker war is creating new marketplace competition.

Marketplace operators don’t care who buys from them. Anybody with a credit card—consumer or business buyer—can go onto these marketplaces and

Research Report 1: The Coming Storm of Converging Technologies 13

purchase. This means that not only are distributors fac-ing new competition from Amazon, but other major players are entering the B2B supplies market as well: Google and Walmart to name two.

For decades, customers relied on distributors because they carried a wide assortment, including hard-to-find products, and delivered them quickly. Because every-thing is commoditized now, is there any “hard-to-find” stuff left? It seems that everything is available from mul-tiple sources.

Marketplace competition is likely to get worse because the financials around this new business model are incredibly favorable. Morgan Stanley thinks that Amazon is making a 20% EBITDA (earnings before interest, taxes, and amortization) on third-party market-place sales. Bank of America/Merrill Lynch estimated that Amazon Business alone will reach $34 billion in gross merchandise sales by 2023, and $125 to $245 bil-lion by 2029.

New players keep emerging. We are currently aware of several B2B marketplace initiatives, including eBay Business & Industrial, Digi-Key, Zoro, Alibaba and Shopify.

It’s important to remember that marketplaces don’t create demand. They serve demand. The revenues these marketplaces generate will come out of the pockets of distributors that do not sell on them.

For B2B buyers, marketplaces will:

• Carry a wider assortment than any distributor• Reach more buyers than any distributor • Make buying easier because you can consolidate

orders• Make buying easier because customers can order

without a keyboard• Muddy the difference between B2B and retail • Create highly loyal customers• Take share from traditional distributors

CHANNEL CONFUSION AND COMPRESSIONFor decades, wholesale distribution was a straight-forward business. Distributors played a “matching” function that filled the gap between the capabilities of manufacturers and the needs of business buyers. That meant they developed a useful assortment of products, held inventory, hired sales reps to capture demand, built branches, provided technical support and filled orders.

Over the last few years, there has been an explosion of complexity in the supply chain: Marketplaces, frac-tional freight carriers, new technology demands and a blurring of the lines between retail and wholesale. One particularly worrisome trend is what appears to be an increasing number of manufacturers that are now sell-ing directly to business buyers and going around dis-tributors entirely.

We identify several reasons for this trend:

• Manufacturers are increasingly dissatisfied with the lack of e-commerce capabilities that is still common for many distributors.

• A growing number of distributors have limited SKUs (stock-keeping units) to “A” and “B” items and so have asked manufacturers to fulfill full lines, which is essentially pushing them to develop fulfillment capabilities.

• Direct fulfillment allows the manufacturer to control messaging, product data, pricing, technical support, service levels and warranty management.

• The manufacturer can capture more of the available gross margin.

• Third-party marketplaces like Amazon/Amazon Business have encouraged manufacturer-direct fulfillment.

Artificial intelligence is a fundamental new technology. If you’re a distributor, formulating a strategy in 2020 without considering the implications of artificial intelligence, is like living in 1995 and doing

a strategy without understanding the internet.

14 NAW Series: How Technology Will Transform Wholesale Distribution

Ultimately, distributors must add value to earn their gross margin. Yet, many distributors participate in Amazon’s FBA (“Fulfillment by Amazon”) program. With FBA, “you store your products in Amazon’s ful-fillment centers, and we pick, pack, ship, and provide customer service for these products.” As a result, the distributor’s role is reduced to creating product listings on Amazon.

It’s hard to imagine this as a sustainable business model. As Amazon gains history about the performance of the SKUs that a distributor lists and has stocked in Amazon’s fulfillment centers, what is the incentive to keep the distributor? Isn’t this really a way for Amazon to identify new, profitable SKUs so they can buy them directly from manufacturers? What value does a distrib-utor add when it no longer distributes anything?

OTHER TECHNOLOGY CHALLENGES AND OPPORTUNITIESAs part of NAW’s How Technology Will Transform Wholesale Distribution series of research reports and accompanying webinars, we’ll explore several other technologies, including 3D printing (additive manufac-turing), blockchain, bitcoin, 5G networks and various AI-enabled tools like virtual and augmented reality and robotics.

Of these, 3D printing likely has the most potential to disrupt wholesale distribution. Obviously, as customers use 3D printing to fabricate more parts themselves, the need to buy them from distributors will go away.

A bigger risk might be a potential move toward decentralization in manufacturing. Some analysts believe that widespread adoption of 3D printing will reduce the scale advantages of large manufacturing plants. A larger number of smaller production facili-ties would, on average, reduce the distance between manufacturers and their end customers, thus making distributors less important in the supply chain.

HOW TO SURVIVE AND THEN THRIVETo navigate this technology-driven disruption within the industry successfully you will need to incorporate these requirements into your business strategies.

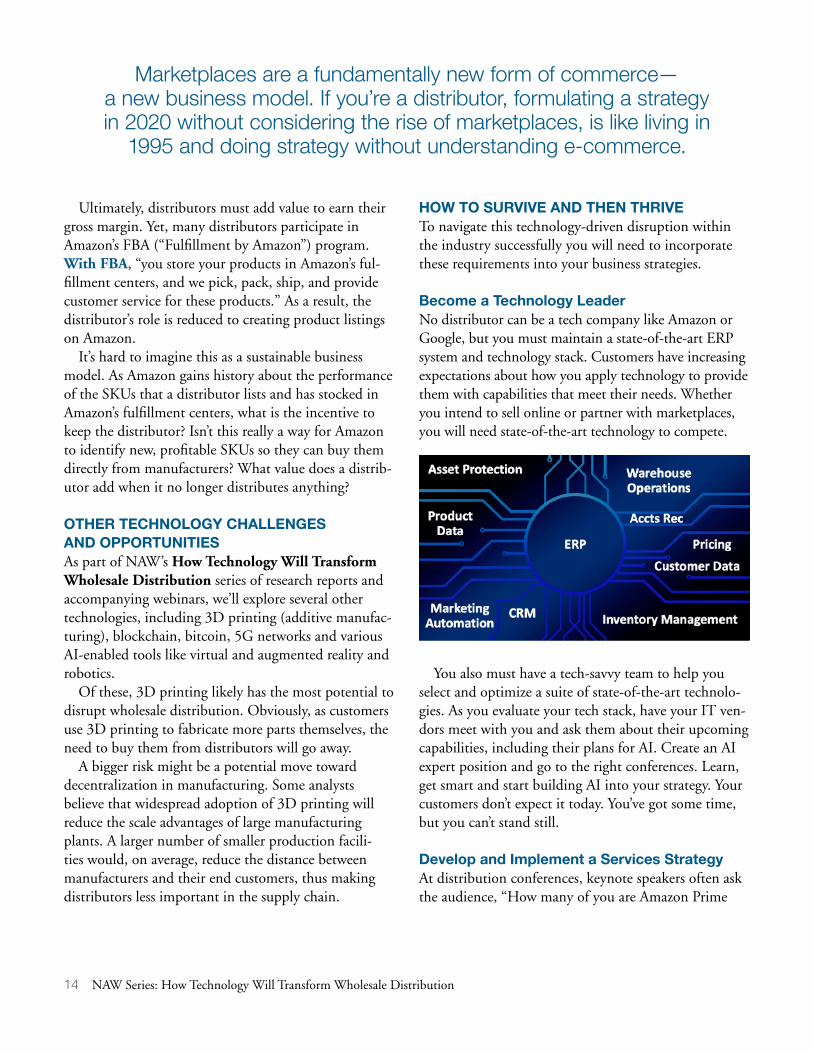

Become a Technology LeaderNo distributor can be a tech company like Amazon or Google, but you must maintain a state-of-the-art ERP system and technology stack. Customers have increasing expectations about how you apply technology to provide them with capabilities that meet their needs. Whether you intend to sell online or partner with marketplaces, you will need state-of-the-art technology to compete.

Marketplaces are a fundamentally new form of commerce— a new business model. If you’re a distributor, formulating a strategy in 2020 without considering the rise of marketplaces, is like living in

1995 and doing strategy without understanding e-commerce.

You also must have a tech-savvy team to help you select and optimize a suite of state-of-the-art technolo-gies. As you evaluate your tech stack, have your IT ven-dors meet with you and ask them about their upcoming capabilities, including their plans for AI. Create an AI expert position and go to the right conferences. Learn, get smart and start building AI into your strategy. Your customers don’t expect it today. You’ve got some time, but you can’t stand still.

Develop and Implement a Services StrategyAt distribution conferences, keynote speakers often ask the audience, “How many of you are Amazon Prime

Research Report 1: The Coming Storm of Converging Technologies 15

customers?” Perhaps a better question is, “How many of you have called Amazon to place an order?”

Obviously, no one has called Amazon, because no one can. Now, consider how much time and effort distribu-tors invest in offering their customers great telephone service. Distributors carefully hire, train and compen-sate employees who answer customer calls, and, very often, their customers’ strongest relationships are with their inside sales reps.

And yet, Amazon and Amazon Business don’t offer this service at all. Does that mean distributors should be more like Amazon and stop employing inside sales reps? Not at all. Instead, this reveals the difference between how marketplaces operate in comparison to how dis-tributors operate.

For marketplaces, involving people in the ordering process prevents them from scaling off of a fixed cost base. Since this is one of the main benefits of operating a marketplace model for investors, it is unlikely that Amazon Business, or other marketplaces, are going to implement strategies that require them to add value with people.

The good thing about competing with companies like Amazon and Google is that they are smart and deliberate as strategic planners. They are making deci-sions about what they are going to do and, inversely, what they are not going to do. If you have a pretty good idea about what a competitor is not likely to do, that gives you a lot of white space where you can grow your business.

B2B is different than retail. Most B2B customers want services from their distributors. Often, they want relationships. In contrast, few consumers buy services from Target or have a relationship with the company.

A key opportunity for you to differentiate your firm from marketplaces is by developing and implementing a more robust set of services:

• Stop bundling many of your services with prod-ucts. If you bundle services, you don’t have to prove that anybody wants them and that they are making money for you or adding value to the customer.

• Create a general manager of services. Bring the same rigor to developing services that manufacturers bring to developing products. Do your research to deter-mine which services your customers would buy from you. Look for ways to monetize your services and start measuring your costs and performance.

• Take credit for the services you offer today. Start by writing compelling copy about them and aggregate them on a “services” tab on your homepage.

• Visit the websites of your competitors and of other distributors that have similar business models as yours. Make an inventory of services that your competitors and other distributors offer. Then take that list to your customers and ask them if they would buy those ser-vices from you if you offered them. If your customers say “yes,” add those services to your portfolio.

Develop and Implement a Marketplace StrategyYou must have a marketplace strategy. You can begin by tracking your exposure to marketplaces. A simple way to start is to bring together a group of employees who understand your business thoroughly. Have them review a few hundred transactions that you’ve selected at random.

Make two piles: • One pile includes the orders that customers could

have bought from anyone, including from a market-place. Customers didn’t need anything besides what a marketplace offers: products, basic product informa-tion, an easy transaction and availability.

• The other pile includes the orders that customers would probably not buy on a marketplace. Perhaps the customer relied on technical advice or value-added services, or the order was shipped from customized product or reserved inventory.

Do this exercise regularly and start developing strat-egies for lowering the proportion of your business (by number of transactions and sales dollars) that is

Remember: the more you make your customers dependent on you for services, the less they can abandon you

for competitors that only sell products.

16 NAW Series: How Technology Will Transform Wholesale Distribution

vulnerable to marketplaces. As valuable as it will be to quantify the risk and set goals for managing it down-ward, the real value will come from having the dialogue with your team, because it will result in powerful ideas that will feed your strategy to build walls between you and marketplaces.

You should also meet with representatives of market-places. You’ll see that the marketplaces that only carry third-party SKUs (such as eBay, Alibaba and Google Shopping) don’t have “merchant” capabilities. It is much less likely that they will analyze your data and use it to compete with you with their own products.

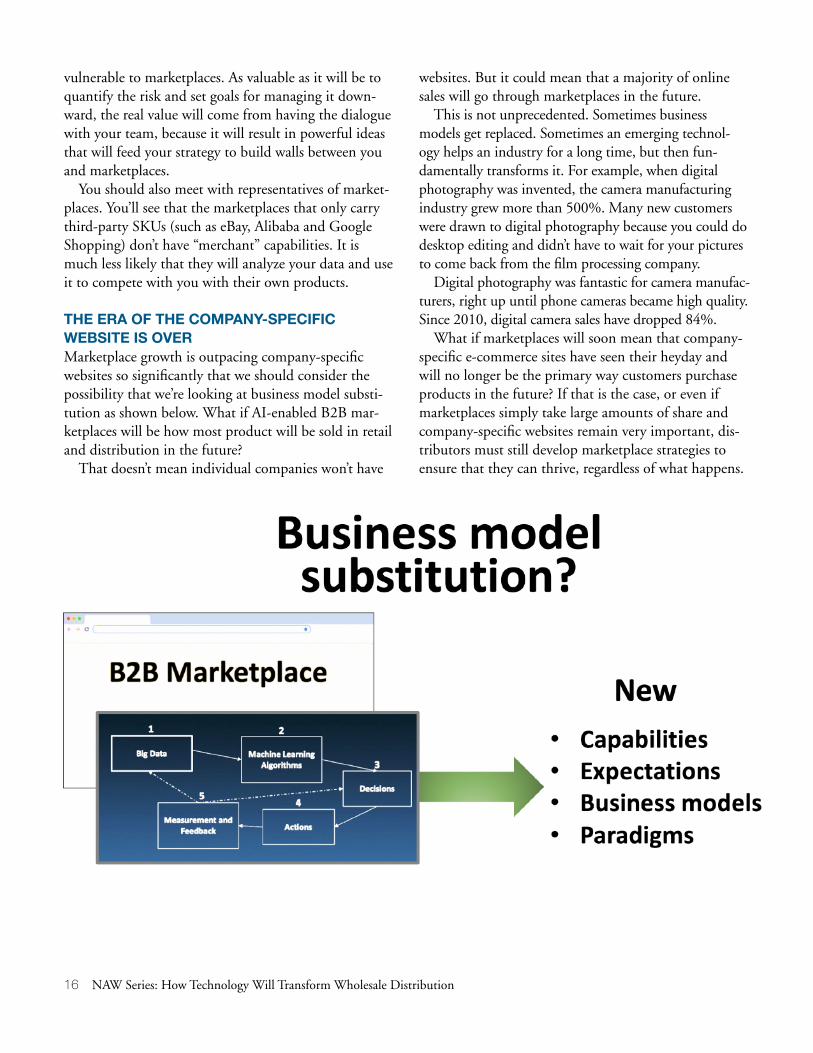

THE ERA OF THE COMPANY-SPECIFIC WEBSITE IS OVERMarketplace growth is outpacing company-specific websites so significantly that we should consider the possibility that we’re looking at business model substi-tution as shown below. What if AI-enabled B2B mar-ketplaces will be how most product will be sold in retail and distribution in the future?

That doesn’t mean individual companies won’t have

websites. But it could mean that a majority of online sales will go through marketplaces in the future.

This is not unprecedented. Sometimes business models get replaced. Sometimes an emerging technol-ogy helps an industry for a long time, but then fun-damentally transforms it. For example, when digital photography was invented, the camera manufacturing industry grew more than 500%. Many new customers were drawn to digital photography because you could do desktop editing and didn’t have to wait for your pictures to come back from the film processing company.

Digital photography was fantastic for camera manufac-turers, right up until phone cameras became high quality. Since 2010, digital camera sales have dropped 84%.

What if marketplaces will soon mean that company-specific e-commerce sites have seen their heyday and will no longer be the primary way customers purchase products in the future? If that is the case, or even if marketplaces simply take large amounts of share and company-specific websites remain very important, dis-tributors must still develop marketplace strategies to ensure that they can thrive, regardless of what happens.

Research Report 1: The Coming Storm of Converging Technologies 17

IAN G. HELLER Founder and Chief Strategy Officer, Distribution Strategy Group

About the Author

A popular and compelling speaker and consultant, Ian Heller spent more than 30 years in the distri-bution industry. Rising from truck unloader to Vice President at Grainger, Ian has since worked or consulted for dozens of other leading distribu-tors. He holds an MBA from The Kellogg School of Management at Northwestern University.

THE FUTURE OF TECHNOLOGY DISRUPTIONAssortment, availability and delivery used to be the core of the distributor’s value proposition. Thanks to technology-enabled marketplaces, that value has been commoditized.

Distributors have innovated new means of adding value for decades. From vending to kitting, labeling and light assembly to rentals, energy audits to technical training, distributors have found ways to make them-selves essential to their customers.

However, the industry has never seen disruption like this. A number of the world’s largest and best-capitalized companies have entered distribution. Some directly, like Amazon, Alibaba and Berkshire Hathaway; others indirectly, like Google. Traditional distributors must find new ways to compete and non-traditional ways of adding value.

In NAW’s How Technology Will Transform Wholesale Distribution series, we’ll look at the under-lying technologies that are driving disruption, and we’ll get quantitative feedback from distributors as well as from their suppliers and their customers. We’ll evaluate how these technologies will change customer expecta-tions and how distributors should change to meet them.

Forward-thinking distributors that move swiftly to adapt to the new competitive environment will find new ways to thrive. However, companies that choose to stand still will likely find their competitiveness erod-ing quickly, and, potentially, their business will die. Distributors can be technology winners in this digital transformation era, so let’s continue on this journey together.

Distribution Strategy Group provides consulting, research and other services to distributors and their business partners. We also publish a variety of distribution-centric content on our website, distributionstrategy.com.

Amazing Digital Commerce Experiences Start with Unilog

A powerful, affordable B2B eCommerce platform that will delight your customers.

• Complete integration with your ERP• Promotions & merchandising• Customer self-service features• Site search configuration• Content management system• Dashboards & analytics• Expedited checkout page• Easy punchout configuration

• Mobile app includes offline cart• PIM & digital asset management• Predictive site search with images• Sales reps can build carts for customers• Product browsing with attribute filters• Quick order pad; copy/paste from Excel• Event registration management• And so much more!

“The amount of functionality and features Unilog provides compares with platforms that cost 5x the amount.”

Ben Lichtenwalner, Etna Supply

www.unilogcorp.com

CLIENT: SAP Global Marketing, Inc.PRODUCT: National Association of Wholesale Distributors-GeneralJOB#: 734267_2_Ntnl_Assc_Whsl_Dist_Pg_BestRunSPACE: 4CBLEED: 8.75" x 11.25"TRIM: 8.5" x 11"SAFETY: 8" x 10.5"GUTTER: NonePUBS: National Association of Wholesale DistributorsISSUE: NoneTRAFFIC: Kevin CherryART BUYER: NoneACCOUNT: Margaret DeshotelRETOUCH: NonePRODUCTION: NoneART DIRECTOR: None

Fonts: BentonSans Book, Bold, Regular , RegularTT Slug OTF Bold

Proof #: 1 Path: Macintosh HD:Users:joe.casanova:Desktop:Kevin SAP:734267_2_Ntnl_Assc_Whsl_Dist_Pg_BestRun:734267_2_Mechanicals:734267_2_Ntnl_Assc_Whsl_Dist_Pg_BestRun_v1.inddOperators: Joe Casanova / joe-casanova

Ink Names: Cyan Magenta Yellow Black

OOH Scaling Info:Build Scale: 100%Final Safety : 10.5" H x 8" WFinal Viewing Area : 11" H x 8.5" WFinal Trim : 11" H x 8.5" WFinal Bleed : 11.25" H x 8.75" W

Filename: 734267_2_Ntnl_Assc_Whsl_Dist_Pg_BestRun_v1.indd

Ink Density: None

IMAGES: 726799-1_728087_2_Mountains_V1_CMYK_HR.psd CMYK 359 ppi, 354 ppiThe_Best_Run_SAP_wht.ai

Agency Job Number: None Cradle Job Number: 734267_2

Page: 1 of 1

Created: 7-2-2020 3:49 PMSaved: 7-2-2020 4:12 PMPrinted: 7-2-2020 4:12 PMPrint Scale: None

© 2

02

0 S

AP

SE

or

an S

AP

aff

iliat

e co

mp

any.

All

righ

ts r

eser

ved

.

Because making the world betteris everyone’s business. THE BEST RUN SAP. A great organization can do great things. For its shareholders. Its employees. And for the world. Together with SAP, you can transform your business and helpit run better. And when businesses run better, communities, the environment,and people everywhere do too.THE BEST-RUN BUSINESSES MAKE THE WORLD RUN BETTER.Learn more at sap.com/bestrun

X1A

T:8.5"T:11"

B:8.75"B:11.25"

We thank our sponsors

National Association of Wholesaler-Distributors1325 G Street, Suite 1000

Washington, DC 20005–3134202.872.0885

Email: [email protected]