Embed Size (px)

Citation preview

The Chamber of Tax Consultants

Workshop on Taxation of Foreign Remittances :Payment to firm / trust / PE and triangular situation

January 21, 2017

Presented by: Vishal J. Shah

Contents

• Tax treaty eligibility - general principles

• Tax treaty eligibility and related issues

• Firm

• Trust

• PE

• Triangular situation and practical issues

Slide 2

January 2017Workshop on Taxation of Foreign Remittances

Tax Treaty eligibility – General principles

1

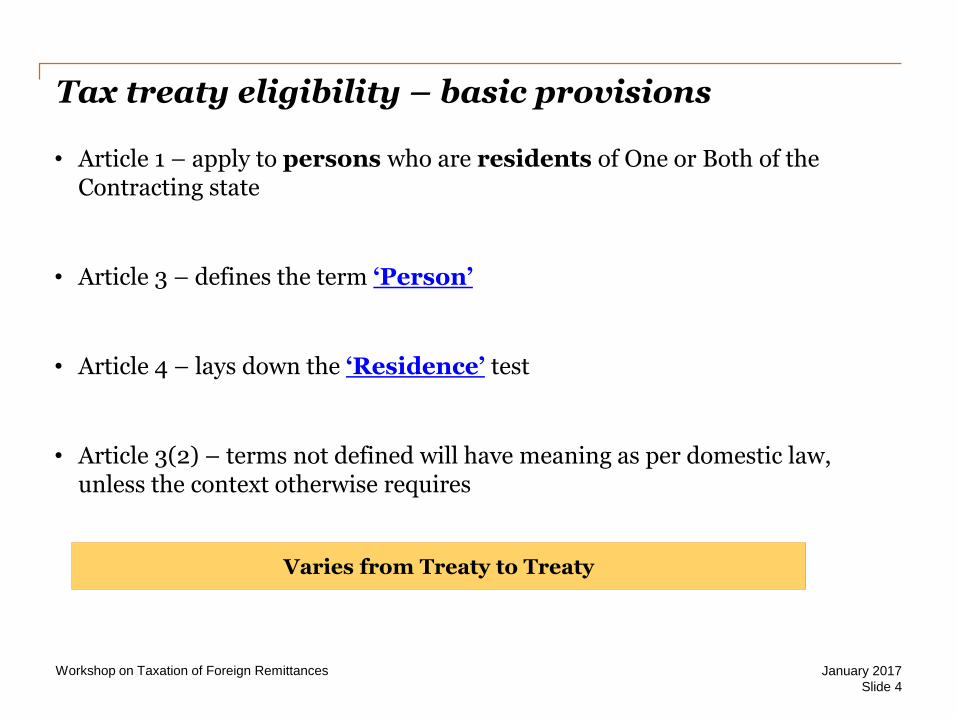

Tax treaty eligibility – basic provisions

• Article 1 – apply to persons who are residents of One or Both of the Contracting state

• Article 3 – defines the term ‘Person’

• Article 4 – lays down the ‘Residence’ test

• Article 3(2) – terms not defined will have meaning as per domestic law, unless the context otherwise requires

Slide 4

January 2017Workshop on Taxation of Foreign Remittances

Varies from Treaty to Treaty

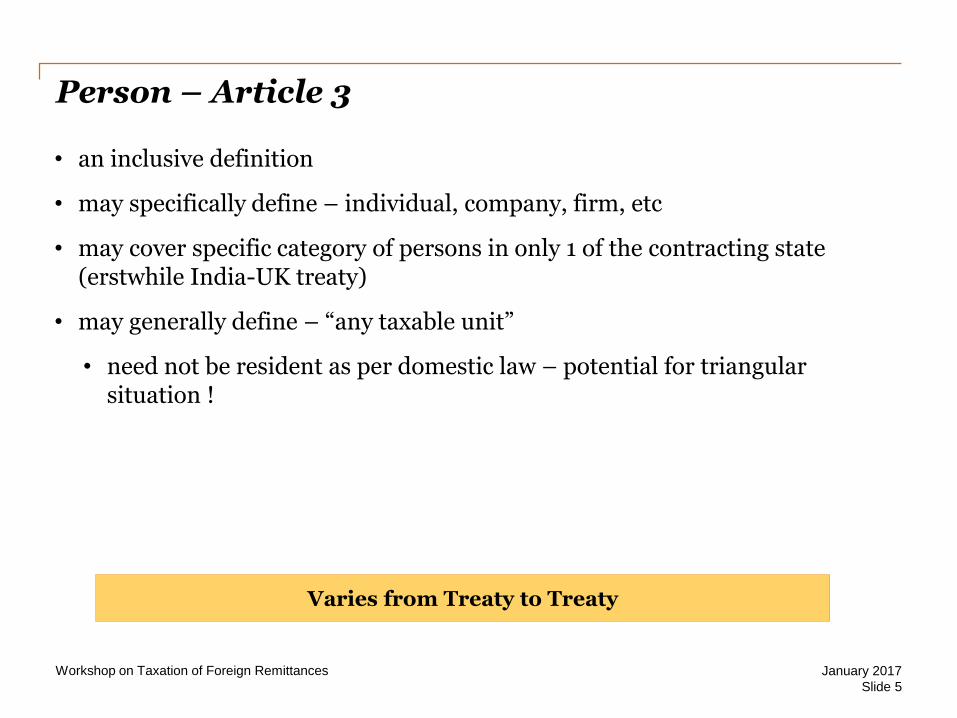

Person – Article 3

• an inclusive definition

• may specifically define – individual, company, firm, etc

• may cover specific category of persons in only 1 of the contracting state (erstwhile India-UK treaty)

• may generally define – “any taxable unit”

• need not be resident as per domestic law – potential for triangular situation !

Slide 5

January 2017Workshop on Taxation of Foreign Remittances

Varies from Treaty to Treaty

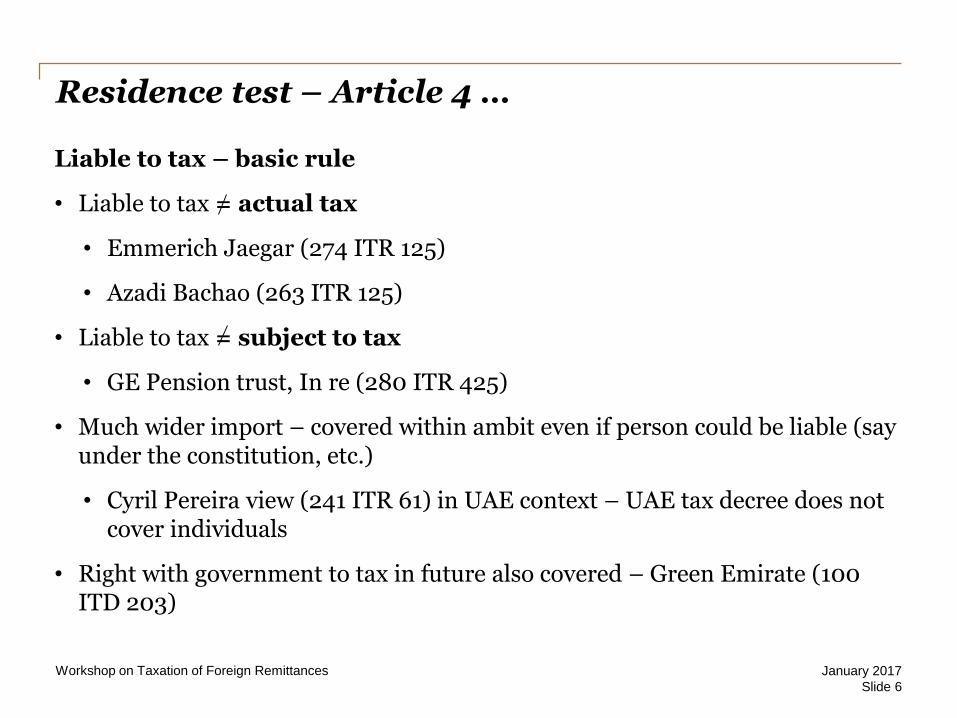

Residence test – Article 4 …

Liable to tax – basic rule

• Liable to tax = actual tax

• Emmerich Jaegar (274 ITR 125)

• Azadi Bachao (263 ITR 125)

• Liable to tax = subject to tax

• GE Pension trust, In re (280 ITR 425)

• Much wider import – covered within ambit even if person could be liable (say under the constitution, etc.)

• Cyril Pereira view (241 ITR 61) in UAE context – UAE tax decree does not cover individuals

• Right with government to tax in future also covered – Green Emirate (100 ITD 203)

Slide 6

January 2017Workshop on Taxation of Foreign Remittances

… Residence test – Article 4 …

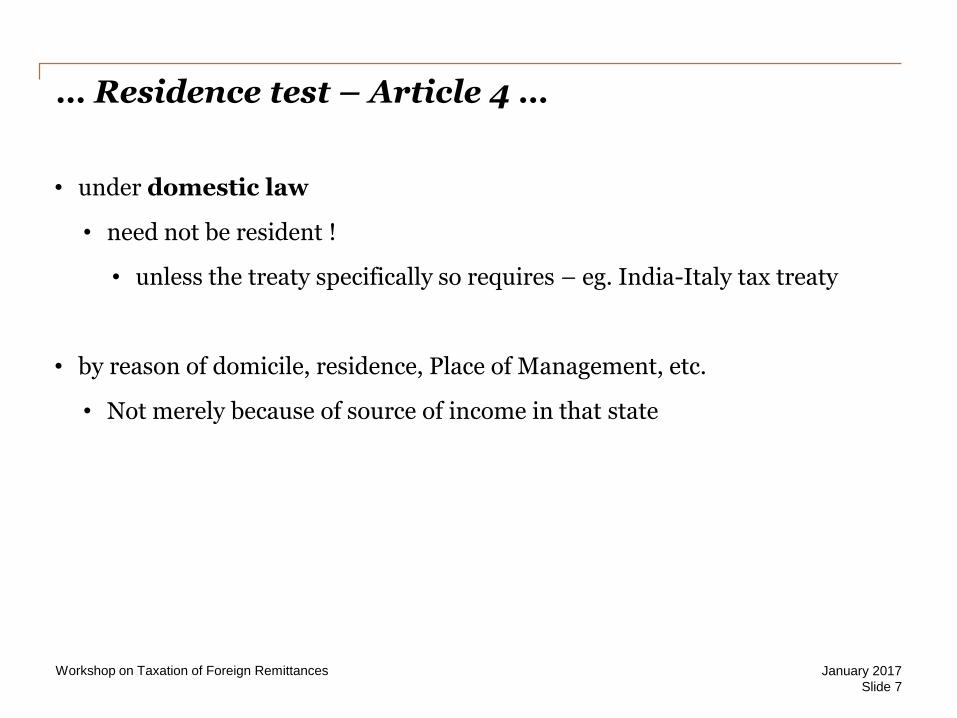

• under domestic law

• need not be resident !

• unless the treaty specifically so requires – eg. India-Italy tax treaty

• by reason of domicile, residence, Place of Management, etc.

• Not merely because of source of income in that state

Slide 7

January 2017Workshop on Taxation of Foreign Remittances

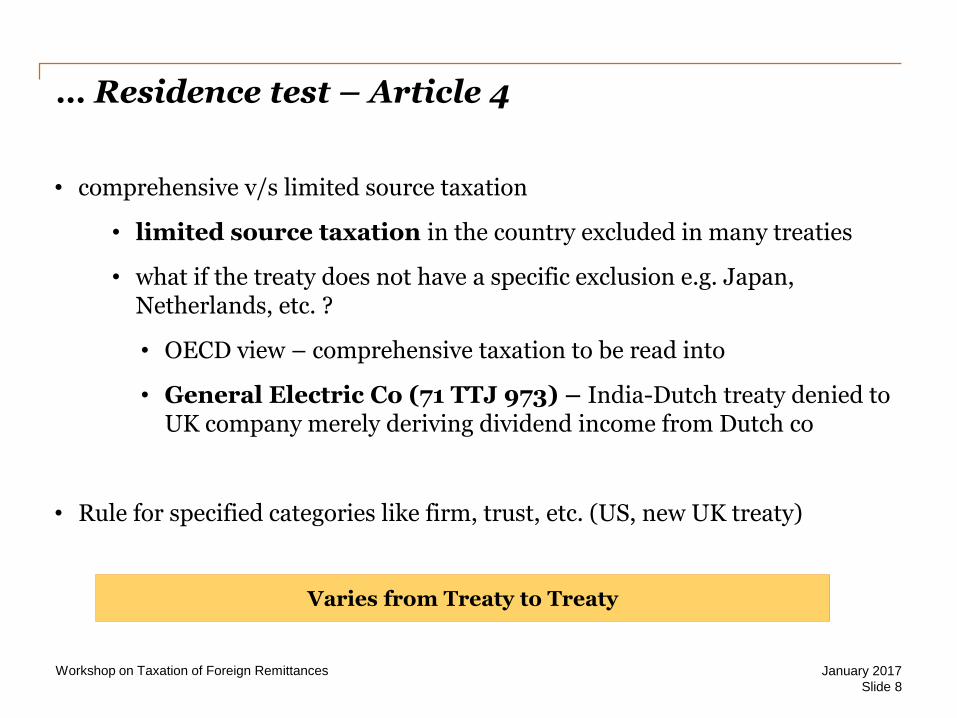

… Residence test – Article 4

• comprehensive v/s limited source taxation

• limited source taxation in the country excluded in many treaties

• what if the treaty does not have a specific exclusion e.g. Japan, Netherlands, etc. ?

• OECD view – comprehensive taxation to be read into

• General Electric Co (71 TTJ 973) – India-Dutch treaty denied to UK company merely deriving dividend income from Dutch co

• Rule for specified categories like firm, trust, etc. (US, new UK treaty)

Slide 8

January 2017Workshop on Taxation of Foreign Remittances

Varies from Treaty to Treaty

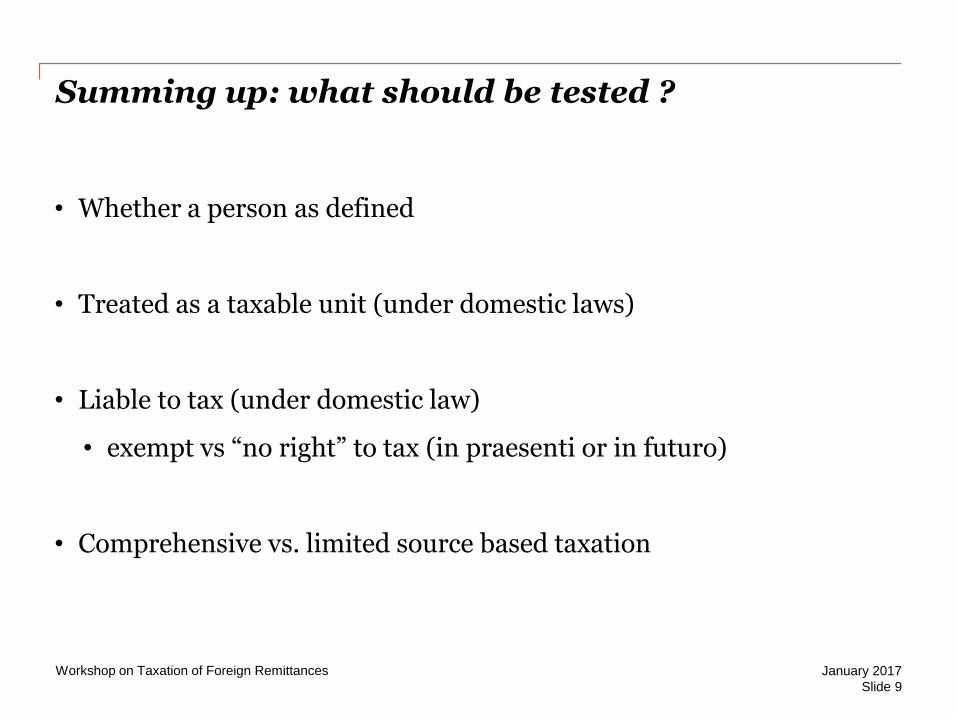

• Whether a person as defined

• Treated as a taxable unit (under domestic laws)

• Liable to tax (under domestic law)

• exempt vs “no right” to tax (in praesenti or in futuro)

• Comprehensive vs. limited source based taxation

Slide 9

January 2017Workshop on Taxation of Foreign Remittances

Summing up: what should be tested ?

Partnership firms: Tax treaty eligibility & related issues

2

Partnership firms – taxation approach

Slide 11

January 2017Workshop on Taxation of Foreign Remittances

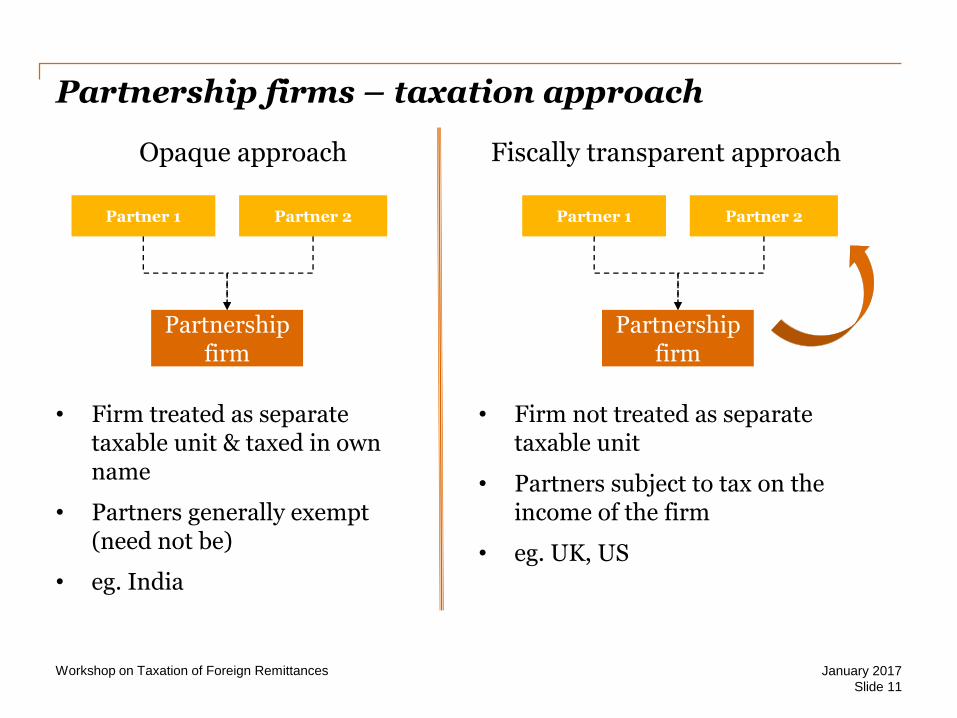

Opaque approach

• Firm treated as separate taxable unit & taxed in own name

• Partners generally exempt (need not be)

• eg. India

Fiscally transparent approach

• Firm not treated as separate taxable unit

• Partners subject to tax on the income of the firm

• eg. UK, US

Partner 1 Partner 2

Partnership firm

Partner 1 Partner 2

Partnership firm

Fiscally transparent firms – Treaty eligibility

Slide 12

January 2017Workshop on Taxation of Foreign Remittances

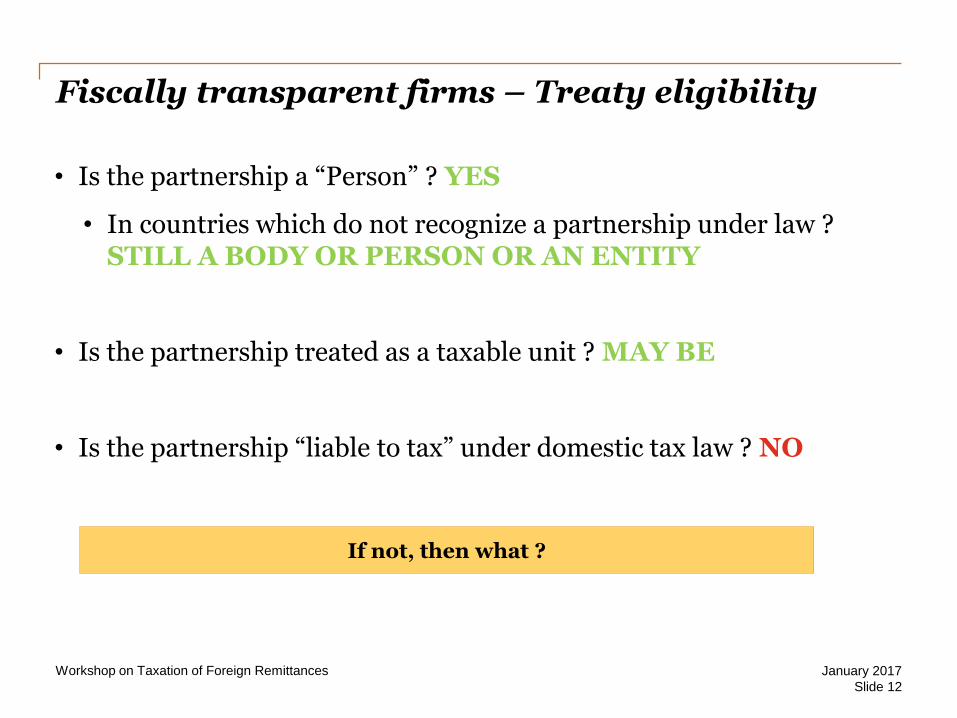

• Is the partnership a “Person” ? YES

• In countries which do not recognize a partnership under law ? STILL A BODY OR PERSON OR AN ENTITY

• Is the partnership treated as a taxable unit ? MAY BE

• Is the partnership “liable to tax” under domestic tax law ? NO

If not, then what ?

Treaty eligibility qua Partners

Slide 13

January 2017Workshop on Taxation of Foreign Remittances

Partners liable to tax in State R on income of partnership from State S

• Is the income derived by / paid to the partners from State S ?

• What if State S does not treat partnership as fiscally transparent ?

• Are the partners automatically entitled to the treaty ?

• Is a specific rule mandatorily required under the treaty to allow partner’s claim treaty benefit ?

Article 1 (Para 5 & 6)

• Status in country of residence to be considered (and not source)

• If treaty benefits denied to partnerships, the same should be allowed to partners in proportion to their share of partnership income which is

- offered to tax

- in state of their residence

◦ Need not be the state of residence (or set-up) of partnership

• Income should be deemed to be paid to / derived by partners for tax purpose - even if paid to / earned by partnership

Article 4 (para 8.8)

• echoes the above principle – however, exclusion to provide separate article if states do not agree with the interpretation

Slide 14

January 2017Workshop on Taxation of Foreign Remittances

Partnerships – OECD Commentary

• India has not accepted OECD view - expressed reservation

• Partner’s entitled only if special provisions in Treaty of the State

- Not of the partner; but where the partnership is situated

• India Reservations on OECD commentary – views of Revenue – enforceable under law ?

- Linklaters LLP (132 TTJ 20) treat benefits (pre-2013) allowed to fiscally transparent UK firm – based on UK residency of partners

◦ UK treaty amended post that to include specific provision

◦ Whether rejected or disapproved the India reservation ?

- Schellenberg Wittmer (AAR 1029 of 2010)

Slide 15

January 2017Workshop on Taxation of Foreign Remittances

Partnerships – India reservation

Analysing some specific treaties

January 2017Workshop on Taxation of Foreign Remittances

Slide 16

• India – USA tax treaty, Article 4(1)(b)

“...in the case of income derived or paid by a partnership, estate, or trust, the term applies only to the extent that the income derived by such partnership, estate, or trust is subject to tax in that State as the income of a resident, either in its hands or in the hands of its partners or beneficiaries”

• India – UK tax treaty, Article 4(1)(b) (post-amendment)

“…in the case of income derived or paid by a partnership, estate, or trust, this term applies only to the extent that the income derived by such partnership, estate, or trust is subject to tax in that State as the income of a resident, either in its hands or in the hands of its partners or beneficiaries”

• Partners tax residents of the said state, are liable to tax therein in respect of the partnership income

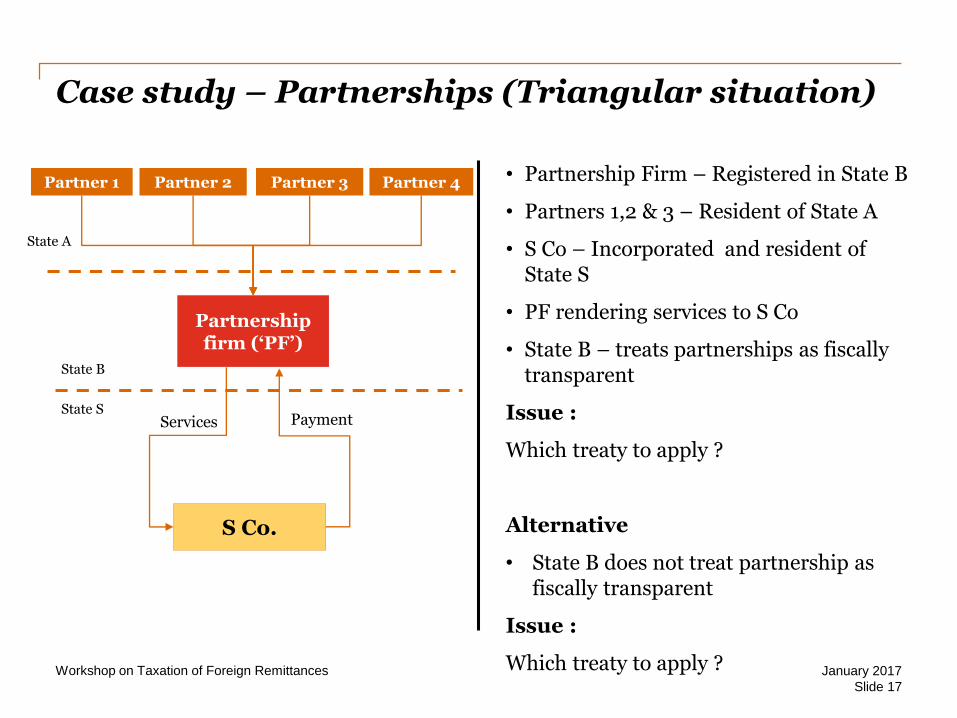

Case study – Partnerships (Triangular situation)

Slide 17

Partnership firm (‘PF’)

Partner 1 Partner 2 Partner 4

S Co.

PaymentServices

• Partnership Firm – Registered in State B

• Partners 1,2 & 3 – Resident of State A

• S Co – Incorporated and resident of State S

• PF rendering services to S Co

• State B – treats partnerships as fiscally transparent

Issue :

Which treaty to apply ?

Alternative

• State B does not treat partnership as fiscally transparent

Issue :

Which treaty to apply ? January 2017Workshop on Taxation of Foreign Remittances

State B

State S

State A

Partner 3

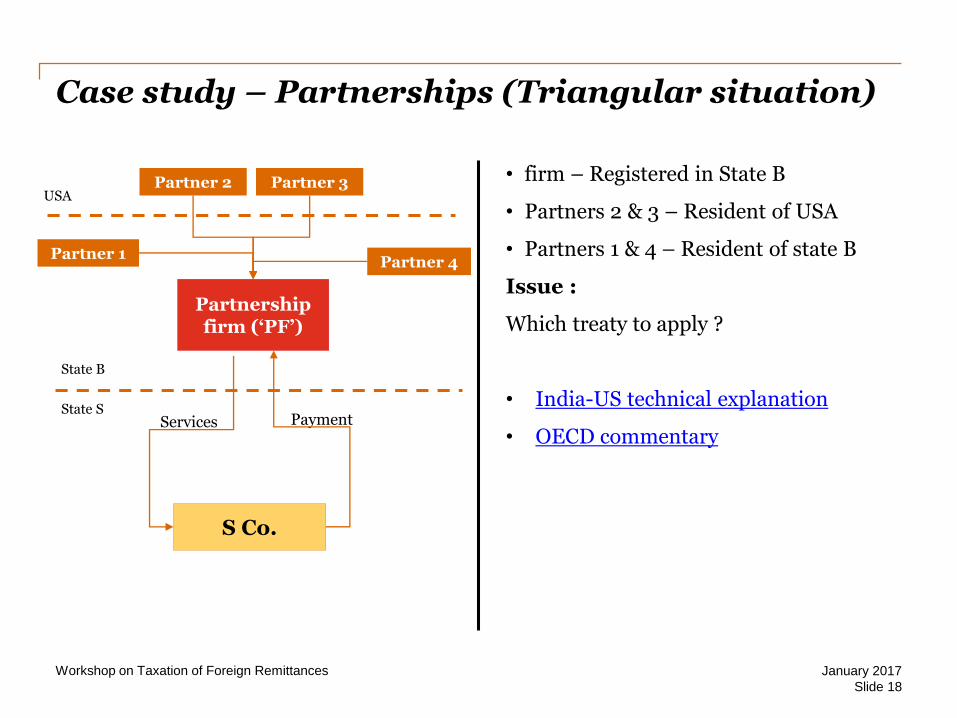

Case study – Partnerships (Triangular situation)

Slide 18

Partnership firm (‘PF’)

Partner 1

Partner 2

Partner 4

S Co.

PaymentServices

• firm – Registered in State B

• Partners 2 & 3 – Resident of USA

• Partners 1 & 4 – Resident of state B

Issue :

Which treaty to apply ?

• India-US technical explanation

• OECD commentary

January 2017Workshop on Taxation of Foreign Remittances

State B

State S

USAPartner 3

• LLC - Limited Liability Company, distinct legal entity separate from its members under US laws

• Under US domestic tax rules, LLC may opt to be taxed as a corporation or as a partnership firm – taxed in the hands of the member

• LLC a person and taxable unit per se; although option to take shareholders

- Is it different than a partnership ?

• Not specifically covered by Article 4(1)(b) of India-US tax treaty ?

• Tax court of Canada in case of TD Securities (USA) LLC (IBFD Case no 2008-2314(IT)G) – LLC allowed treaty benefits

• Linklaters logic applies ?

• will India allow ?

Slide 19

January 2017Workshop on Taxation of Foreign Remittances

Taxability of US LLC

Article 3(2)–Term not defined in the treaty shall have meaning as under domestic law, unless the context otherwise requires

S. 2(23) of IT Act

“ firm shall have the meaning assigned to it in Indian Partnership Act, 1932 and shall include a limited liability partnership as defined in LLP Act, 2008”

• Partnership as per IPA

• Sharing of profit / loss

• Agency relationship

• Joint and several liability - UNLIMITED

• Whether Foreign partnerships to satisfy test aid down in IPA ?

- OECD commentary

- Linklaters LLP case

Slide 20

January 2017Workshop on Taxation of Foreign Remittances

Partnership as per Indian law ?

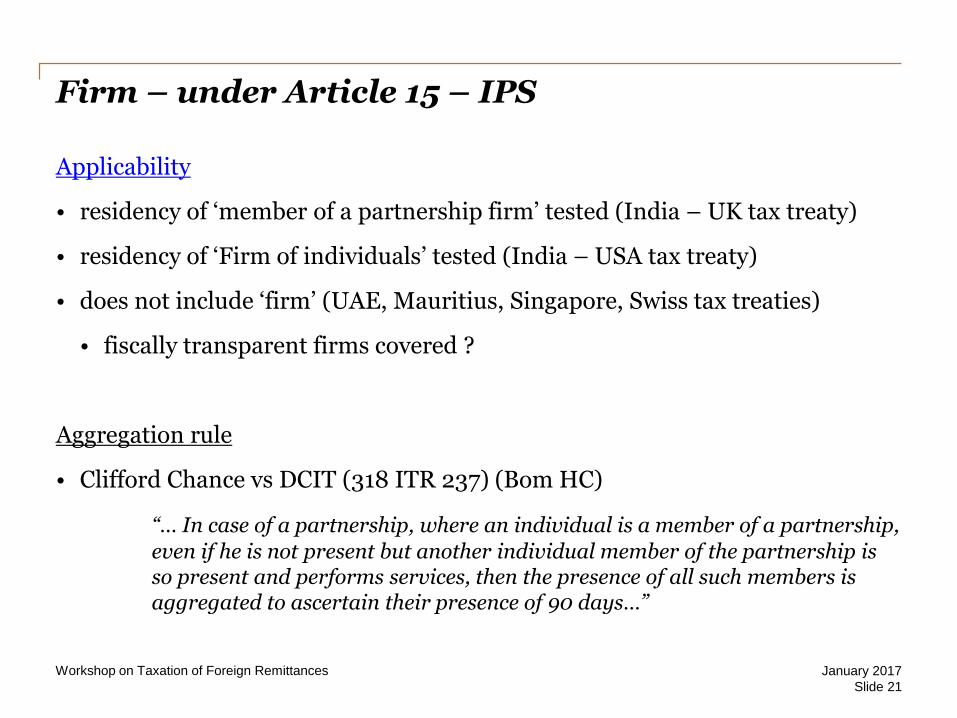

Applicability

• residency of ‘member of a partnership firm’ tested (India – UK tax treaty)

• residency of ‘Firm of individuals’ tested (India – USA tax treaty)

• does not include ‘firm’ (UAE, Mauritius, Singapore, Swiss tax treaties)

• fiscally transparent firms covered ?

Aggregation rule

• Clifford Chance vs DCIT (318 ITR 237) (Bom HC)

“… In case of a partnership, where an individual is a member of a partnership,

even if he is not present but another individual member of the partnership is so present and performs services, then the presence of all such members is aggregated to ascertain their presence of 90 days…”

Slide 21

January 2017Workshop on Taxation of Foreign Remittances

Firm – under Article 15 – IPS

Trusts: Tax treaty eligibility & related issues

3

Trusts (some examples)

• Exempt charity trusts

• Investment funds (PE / VC fund, etc.)

• Collective investment vehicles

• Personal estates / family trusts

• Universities / NPOs

Slide 23

January 2017Workshop on Taxation of Foreign Remittances

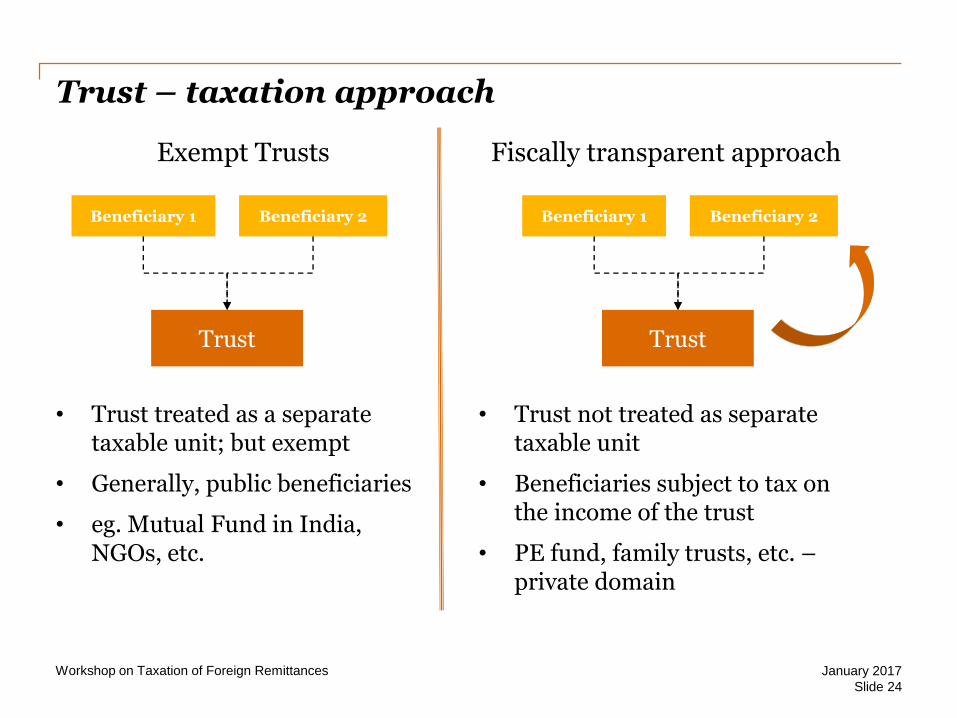

Trust – taxation approach

Slide 24

January 2017Workshop on Taxation of Foreign Remittances

Exempt Trusts

• Trust treated as a separate taxable unit; but exempt

• Generally, public beneficiaries

• eg. Mutual Fund in India, NGOs, etc.

Fiscally transparent approach

• Trust not treated as separate taxable unit

• Beneficiaries subject to tax on the income of the trust

• PE fund, family trusts, etc. –private domain

Beneficiary 1 Beneficiary 2

Trust

Beneficiary 1 Beneficiary 2

Trust

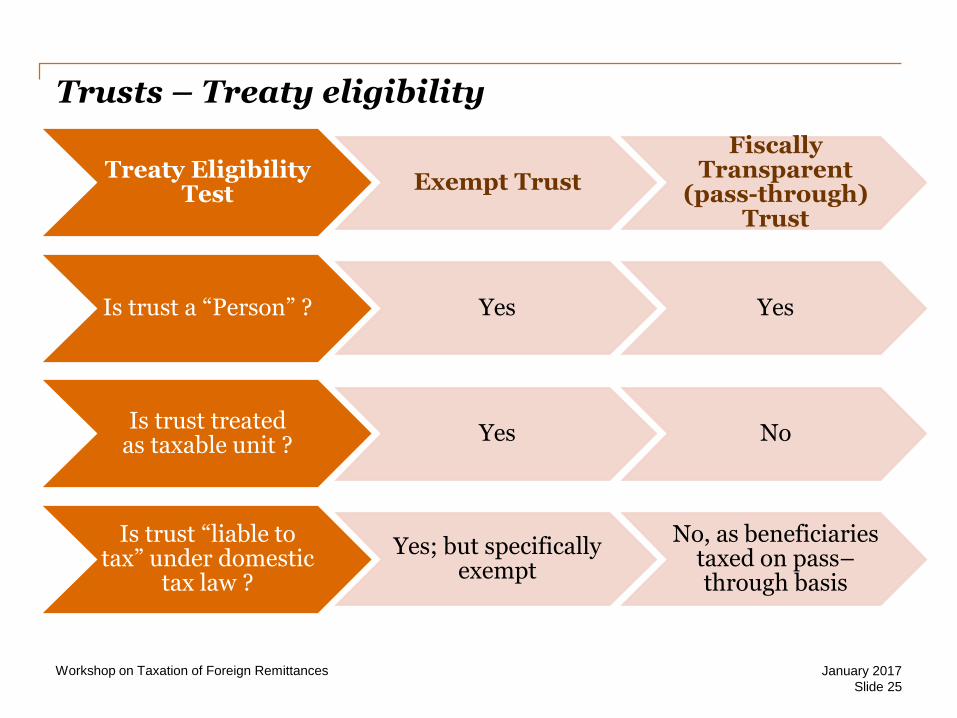

Trusts – Treaty eligibility

Slide 25

January 2017Workshop on Taxation of Foreign Remittances

Treaty Eligibility Test

Exempt Trust

Fiscally Transparent

(pass-through) Trust

Is trust a “Person” ? Yes Yes

Is trust treated as taxable unit ?

Yes No

Is trust “liable to tax” under domestic

tax law ?

Yes; but specifically exempt

No, as beneficiaries taxed on pass–through basis

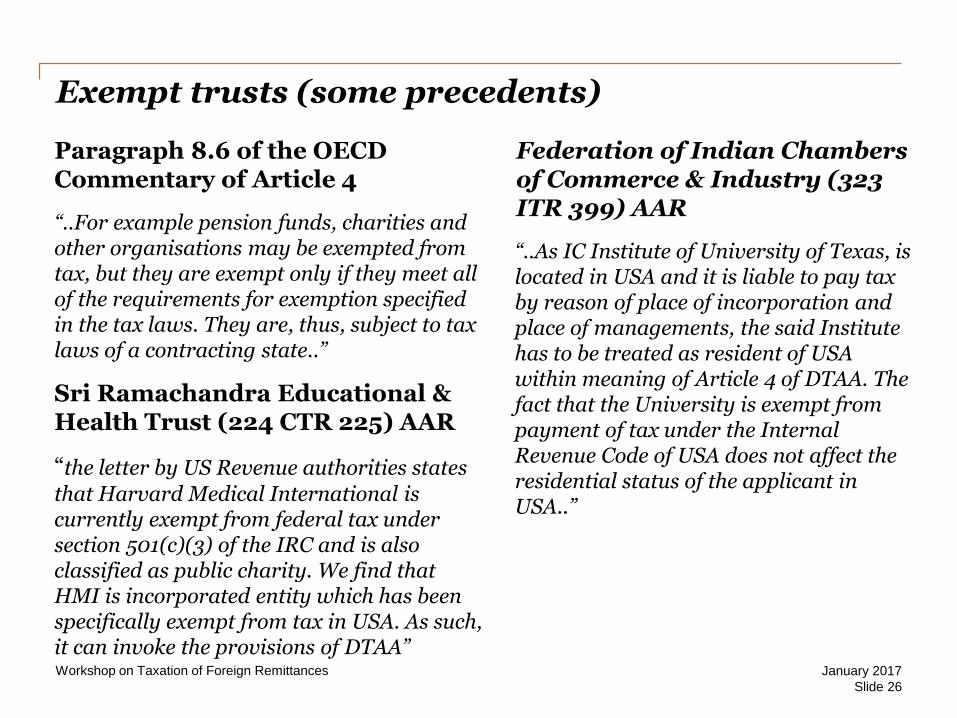

Exempt trusts (some precedents)

Paragraph 8.6 of the OECD Commentary of Article 4

“..For example pension funds, charities and other organisations may be exempted from tax, but they are exempt only if they meet all of the requirements for exemption specified in the tax laws. They are, thus, subject to tax laws of a contracting state..”

Sri Ramachandra Educational & Health Trust (224 CTR 225) AAR

“the letter by US Revenue authorities states

that Harvard Medical International is currently exempt from federal tax under section 501(c)(3) of the IRC and is also classified as public charity. We find that HMI is incorporated entity which has been specifically exempt from tax in USA. As such, it can invoke the provisions of DTAA”

Federation of Indian Chambers of Commerce & Industry (323 ITR 399) AAR

“..As IC Institute of University of Texas, is located in USA and it is liable to pay tax by reason of place of incorporation and place of managements, the said Institute has to be treated as resident of USA within meaning of Article 4 of DTAA. The fact that the University is exempt from payment of tax under the Internal Revenue Code of USA does not affect the residential status of the applicant in USA..”

Slide 26

January 2017Workshop on Taxation of Foreign Remittances

Fiscally transparent trusts

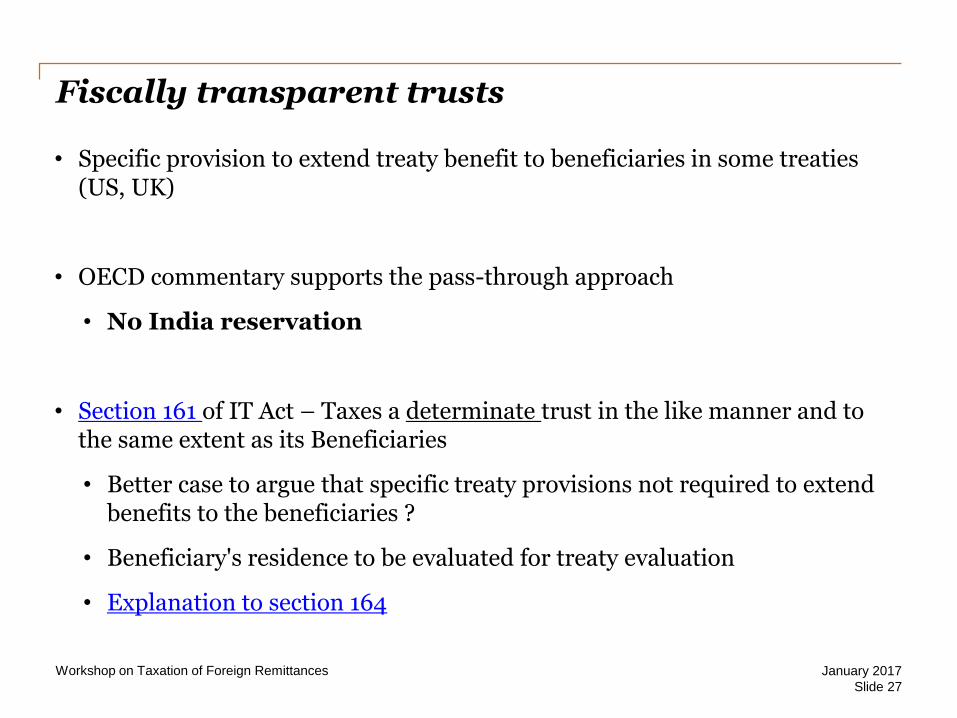

• Specific provision to extend treaty benefit to beneficiaries in some treaties (US, UK)

• OECD commentary supports the pass-through approach

• No India reservation

• Section 161 of IT Act – Taxes a determinate trust in the like manner and to the same extent as its Beneficiaries

• Better case to argue that specific treaty provisions not required to extend benefits to the beneficiaries ?

• Beneficiary's residence to be evaluated for treaty evaluation

• Explanation to section 164

Slide 27

January 2017Workshop on Taxation of Foreign Remittances

Permanent Establishment: Tax treaty eligibility& related issues

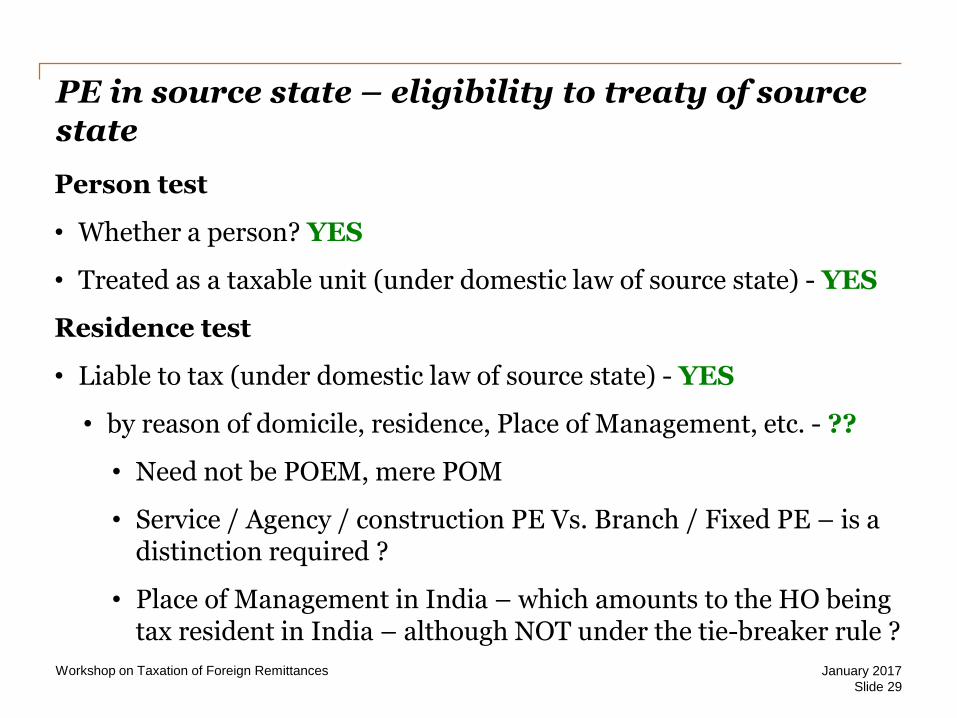

PE in source state – eligibility to treaty of source state

Person test

• Whether a person? YES

• Treated as a taxable unit (under domestic law of source state) - YES

Residence test

• Liable to tax (under domestic law of source state) - YES

• by reason of domicile, residence, Place of Management, etc. - ??

• Need not be POEM, mere POM

• Service / Agency / construction PE Vs. Branch / Fixed PE – is a distinction required ?

• Place of Management in India – which amounts to the HO being tax resident in India – although NOT under the tie-breaker rule ?

Slide 29

January 2017Workshop on Taxation of Foreign Remittances

PE in source state – Treaty eligibility

Residence test

• few treaties specifically require to be “Resident” (India-Italy) - NO

• Comprehensive vs. limited source based taxation ?

• Additional clause in Article 4(1) of the OECD model & most Indian treaties

“.. This term, however, does not include any person who is liable to tax in that State in respect only of income from sources in that State or capital situated therein..”

• Shell Technology India Private Limited (345 ITR 206) AAR – Philippines branch of Dutch Co denied India-Philippines tax treaty

• is it always presumed even if treaty does not provide ?

• OECD view supports comprehensive taxation

Slide 30

January 2017Workshop on Taxation of Foreign Remittances

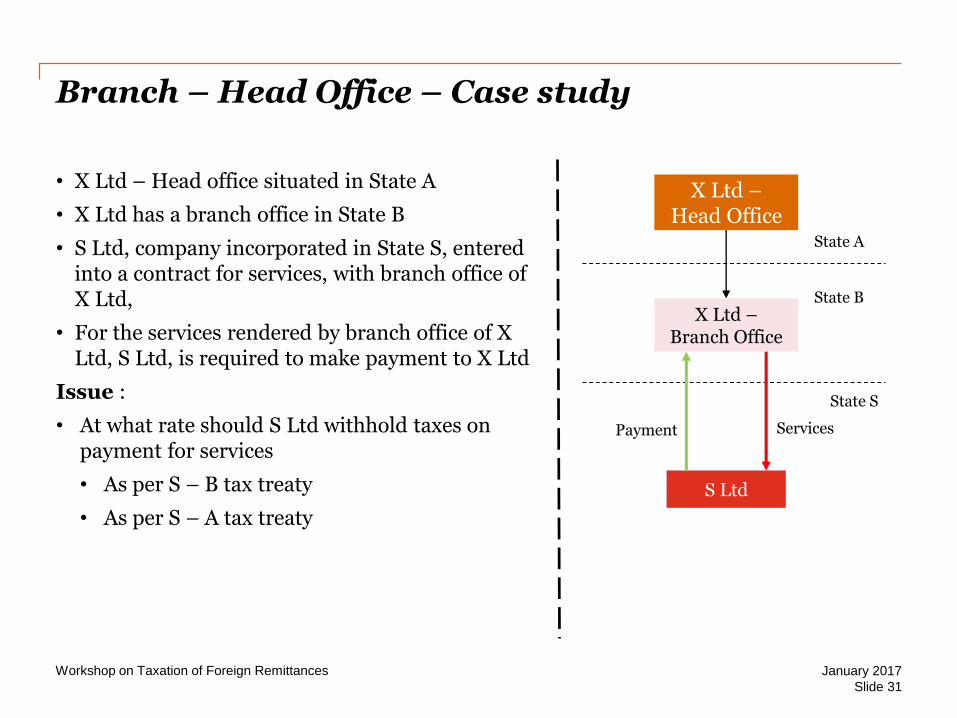

Branch – Head Office – Case study

January 2017

Slide 31

X Ltd –Head Office

S Ltd

Payment

• X Ltd – Head office situated in State A

• X Ltd has a branch office in State B

• S Ltd, company incorporated in State S, entered into a contract for services, with branch office of X Ltd,

• For the services rendered by branch office of X Ltd, S Ltd, is required to make payment to X Ltd

Issue :

• At what rate should S Ltd withhold taxes on payment for services

• As per S – B tax treaty

• As per S – A tax treaty

X Ltd –Branch Office

Services

Workshop on Taxation of Foreign Remittances

State A

State B

State S

Some other triangular situations & Practical challenges

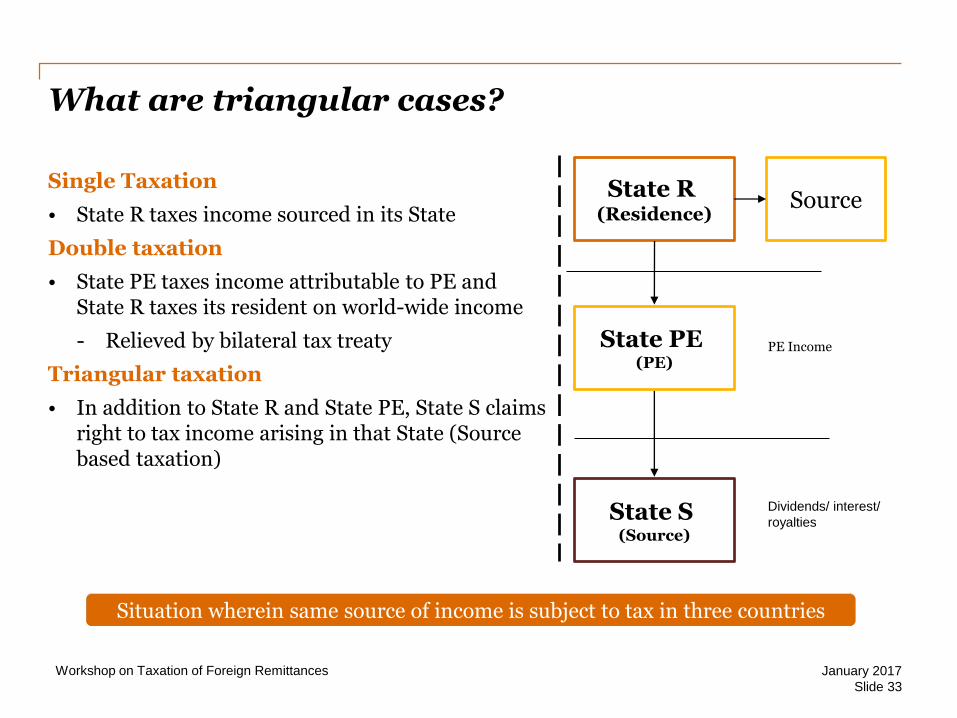

What are triangular cases?

Single Taxation

• State R taxes income sourced in its State

Double taxation

• State PE taxes income attributable to PE and State R taxes its resident on world-wide income

- Relieved by bilateral tax treaty

Triangular taxation

• In addition to State R and State PE, State S claims right to tax income arising in that State (Source based taxation)

Dividends/ interest/

royalties

State R (Residence)

State PE (PE)

State S (Source)

PE Income

Source

January 2017Workshop on Taxation of Foreign Remittances

Slide 33

Situation wherein same source of income is subject to tax in three countries

…What is triangular cases ?

• Key challenges arising due to such triangular situations

- Determination of taxing powers of Contracting States i.e. taxability in State R, State PE & State S ?

- Which treaty to be applied to withhold taxes at the time of making payment

- Credit for taxes withheld

• Instances of Triangular situations, discussed in detail in subsequent slides

− Dual Residency

− Branch – Head Office situation

− Beneficial Owner in a 3rd Country

January 2017Workshop on Taxation of Foreign Remittances

Slide 34

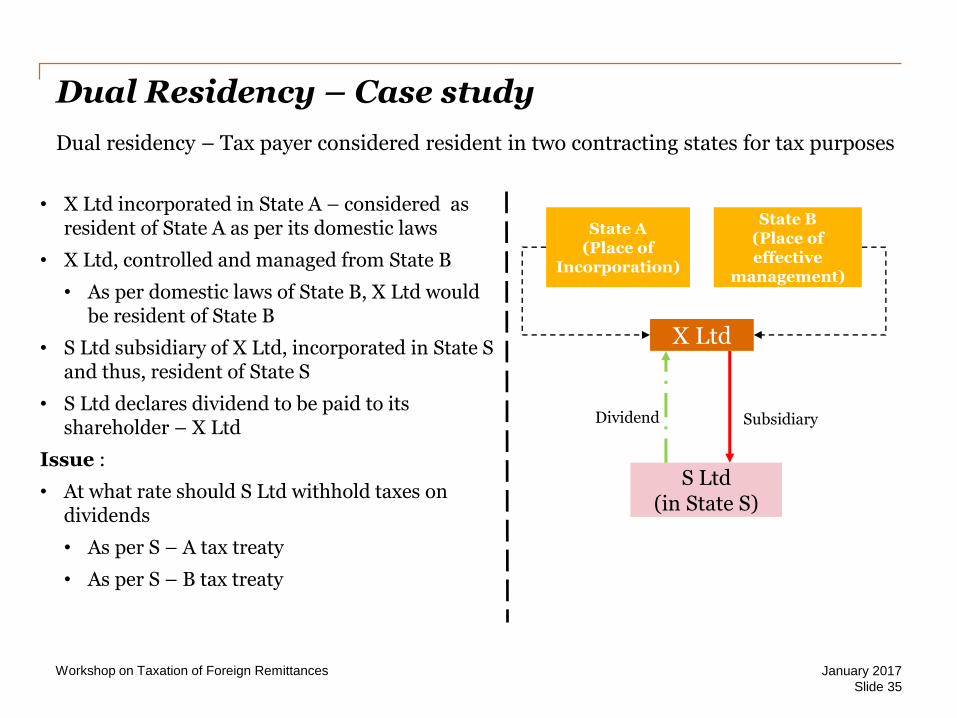

Dual Residency – Case study

Dual residency – Tax payer considered resident in two contracting states for tax purposes

January 2017

Slide 35

State A(Place of

Incorporation)

State B(Place of effective

management)

X Ltd

S Ltd (in State S)

SubsidiaryDividend

• X Ltd incorporated in State A – considered as resident of State A as per its domestic laws

• X Ltd, controlled and managed from State B

• As per domestic laws of State B, X Ltd would be resident of State B

• S Ltd subsidiary of X Ltd, incorporated in State S and thus, resident of State S

• S Ltd declares dividend to be paid to its shareholder – X Ltd

Issue :

• At what rate should S Ltd withhold taxes on dividends

• As per S – A tax treaty

• As per S – B tax treaty

Workshop on Taxation of Foreign Remittances

Dual Residency – Analysis

• Option I: Beneficial of the two treaties apply

• Option II: Apply tie-breaker rule between State A and State B, resultant treaty apply qua source state

• Nothing in the S–A treaty or S–B treaty to support this view

January 2017

Slide 36

Workshop on Taxation of Foreign Remittances

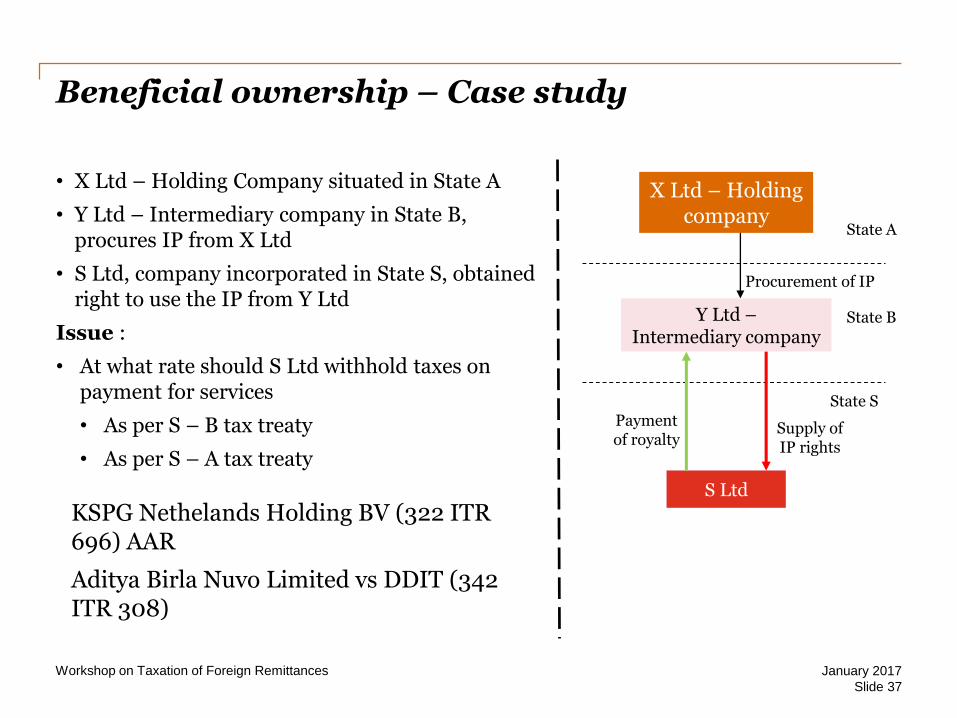

Beneficial ownership – Case study

January 2017

Slide 37

X Ltd – Holding company

S Ltd

Payment of royalty

• X Ltd – Holding Company situated in State A

• Y Ltd – Intermediary company in State B, procures IP from X Ltd

• S Ltd, company incorporated in State S, obtained right to use the IP from Y Ltd

Issue :

• At what rate should S Ltd withhold taxes on payment for services

• As per S – B tax treaty

• As per S – A tax treaty

Y Ltd –Intermediary company

Workshop on Taxation of Foreign Remittances

State A

State B

State S

Procurement of IP

Supply of IP rights

KSPG Nethelands Holding BV (322 ITR 696) AAR

Aditya Birla Nuvo Limited vs DDIT (342 ITR 308)

Indian context – Practical challenges in triangular situations

Slide 38

• Whether TRC for partners / beneficiaries of fiscally transparent entity available ? Would the tax authorities of such country issue a TRC ?

• would Form No 10-F be sufficient compliance ? Who would sign such form –Partners / beneficiaries – who are not payers?

• PAN to be obtained for fiscally transparent partnership in India ? Members ?

• Tax deduction on PAN of partnership ? Or on PAN of Partners ?

• proportionate ?

January 2017Workshop on Taxation of Foreign Remittances

Annexure

5

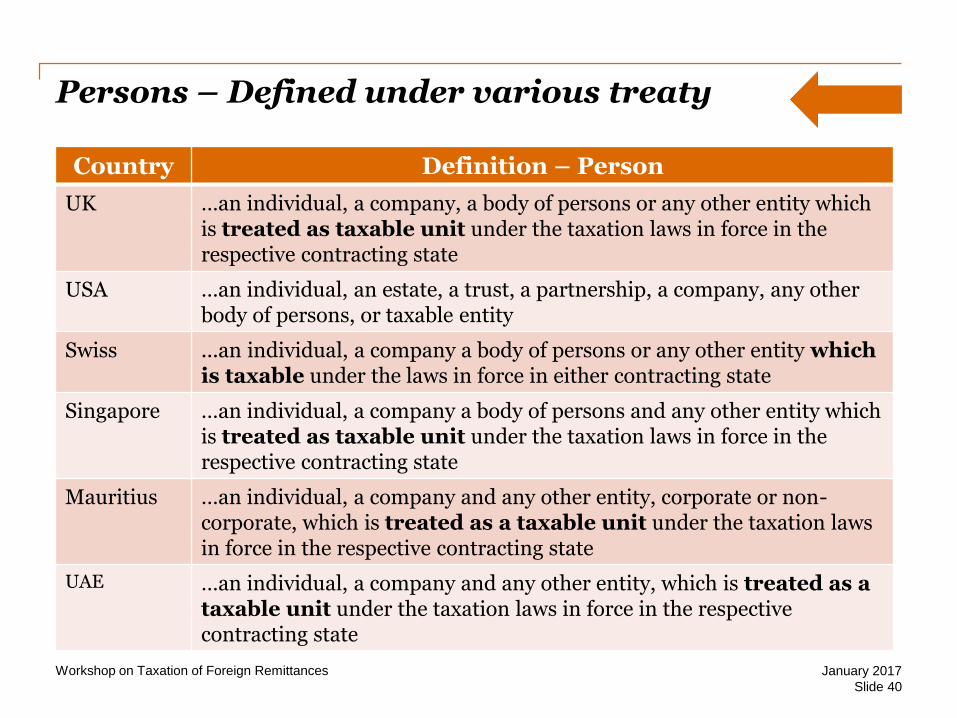

Persons – Defined under various treaty

Slide 40

January 2017Workshop on Taxation of Foreign Remittances

Country Definition – Person

UK …an individual, a company, a body of persons or any other entity which is treated as taxable unit under the taxation laws in force in the respective contracting state

USA …an individual, an estate, a trust, a partnership, a company, any other body of persons, or taxable entity

Swiss ...an individual, a company a body of persons or any other entity which is taxable under the laws in force in either contracting state

Singapore …an individual, a company a body of persons and any other entity which is treated as taxable unit under the taxation laws in force in the respective contracting state

Mauritius …an individual, a company and any other entity, corporate or non-corporate, which is treated as a taxable unit under the taxation laws in force in the respective contracting state

UAE …an individual, a company and any other entity, which is treated as a taxable unit under the taxation laws in force in the respective contracting state

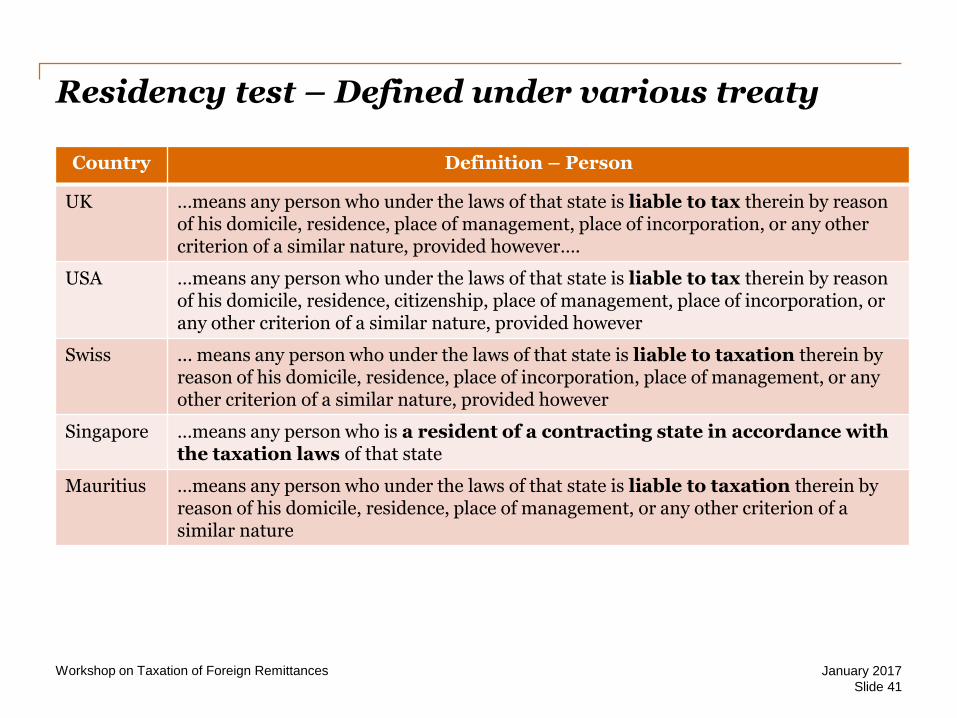

Residency test – Defined under various treaty

Slide 41

January 2017Workshop on Taxation of Foreign Remittances

Country Definition – Person

UK …means any person who under the laws of that state is liable to tax therein by reason of his domicile, residence, place of management, place of incorporation, or any other criterion of a similar nature, provided however….

USA …means any person who under the laws of that state is liable to tax therein by reason of his domicile, residence, citizenship, place of management, place of incorporation, or any other criterion of a similar nature, provided however

Swiss ... means any person who under the laws of that state is liable to taxation therein by reason of his domicile, residence, place of incorporation, place of management, or any other criterion of a similar nature, provided however

Singapore …means any person who is a resident of a contracting state in accordance with the taxation laws of that state

Mauritius …means any person who under the laws of that state is liable to taxation therein by reason of his domicile, residence, place of management, or any other criterion of a similar nature

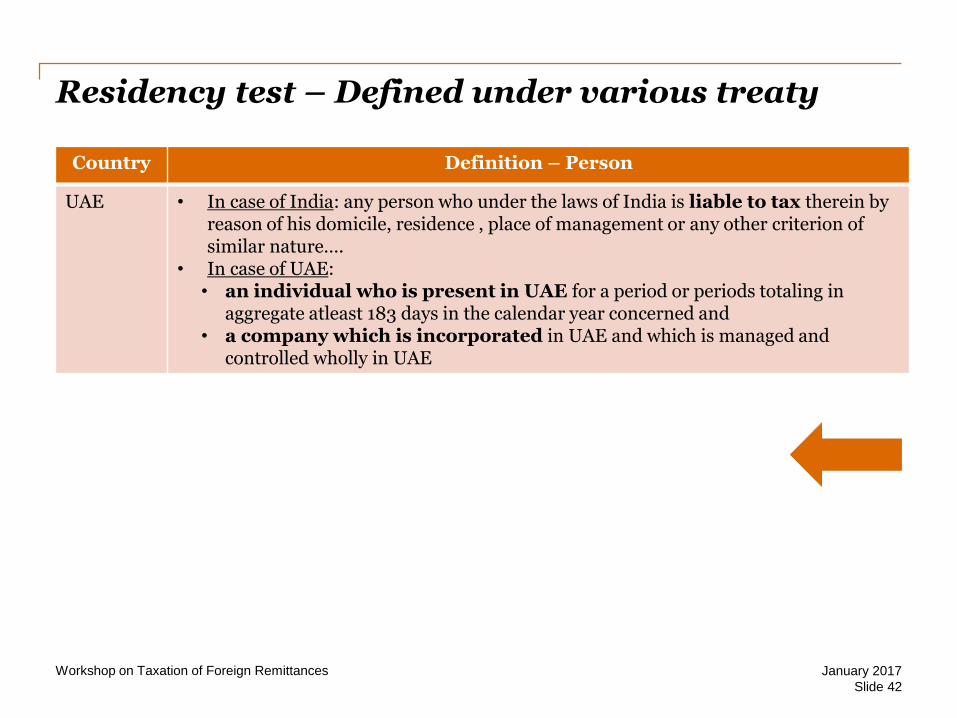

Residency test – Defined under various treaty

Slide 42

January 2017Workshop on Taxation of Foreign Remittances

Country Definition – Person

UAE • In case of India: any person who under the laws of India is liable to tax therein by reason of his domicile, residence , place of management or any other criterion of similar nature….

• In case of UAE:• an individual who is present in UAE for a period or periods totaling in

aggregate atleast 183 days in the calendar year concerned and • a company which is incorporated in UAE and which is managed and

controlled wholly in UAE

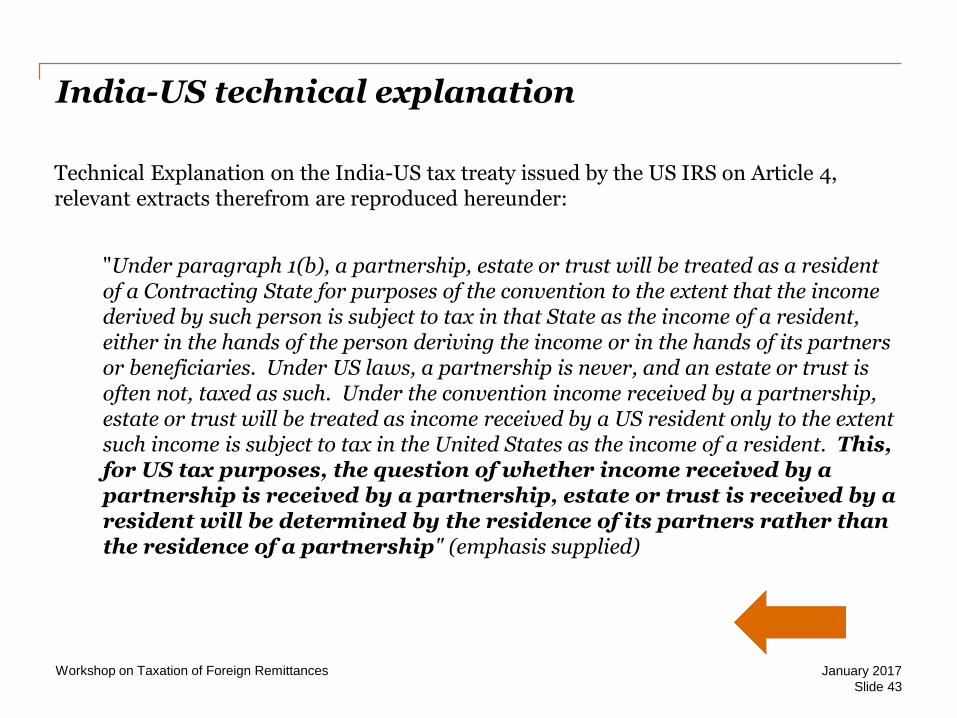

India-US technical explanation

Technical Explanation on the India-US tax treaty issued by the US IRS on Article 4, relevant extracts therefrom are reproduced hereunder:

"Under paragraph 1(b), a partnership, estate or trust will be treated as a resident of a Contracting State for purposes of the convention to the extent that the income derived by such person is subject to tax in that State as the income of a resident, either in the hands of the person deriving the income or in the hands of its partners or beneficiaries. Under US laws, a partnership is never, and an estate or trust is often not, taxed as such. Under the convention income received by a partnership, estate or trust will be treated as income received by a US resident only to the extent such income is subject to tax in the United States as the income of a resident. This, for US tax purposes, the question of whether income received by a partnership is received by a partnership, estate or trust is received by a resident will be determined by the residence of its partners rather than the residence of a partnership" (emphasis supplied)

Slide 43

January 2017Workshop on Taxation of Foreign Remittances

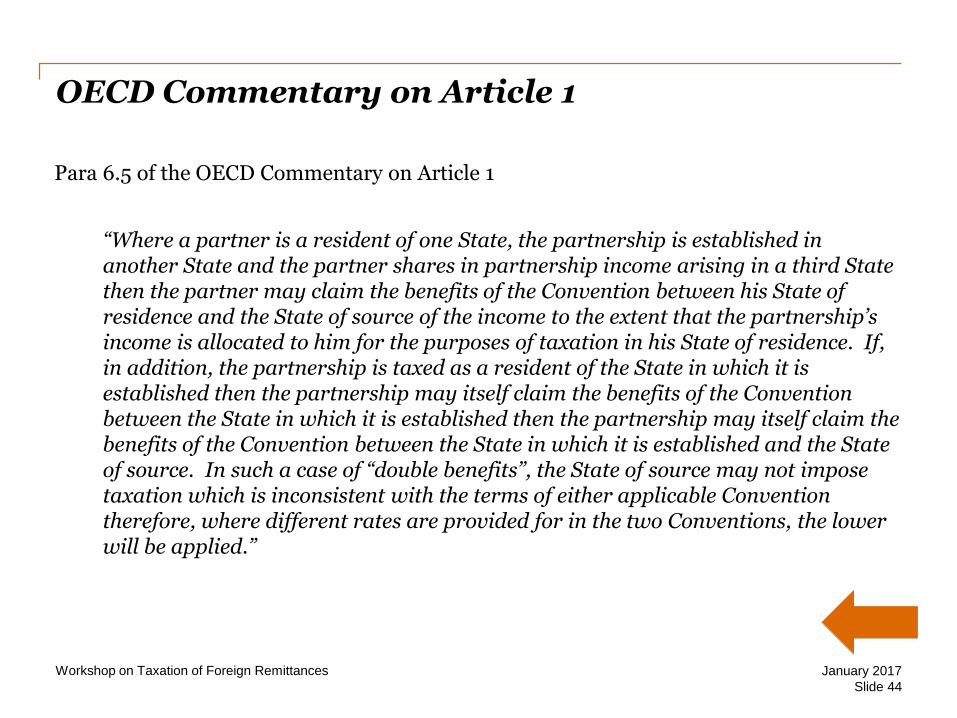

OECD Commentary on Article 1

Para 6.5 of the OECD Commentary on Article 1

“Where a partner is a resident of one State, the partnership is established in another State and the partner shares in partnership income arising in a third State then the partner may claim the benefits of the Convention between his State of residence and the State of source of the income to the extent that the partnership’s income is allocated to him for the purposes of taxation in his State of residence. If, in addition, the partnership is taxed as a resident of the State in which it is established then the partnership may itself claim the benefits of the Convention between the State in which it is established then the partnership may itself claim the benefits of the Convention between the State in which it is established and the State of source. In such a case of “double benefits”, the State of source may not impose taxation which is inconsistent with the terms of either applicable Convention therefore, where different rates are provided for in the two Conventions, the lower will be applied.”

Slide 44

January 2017Workshop on Taxation of Foreign Remittances

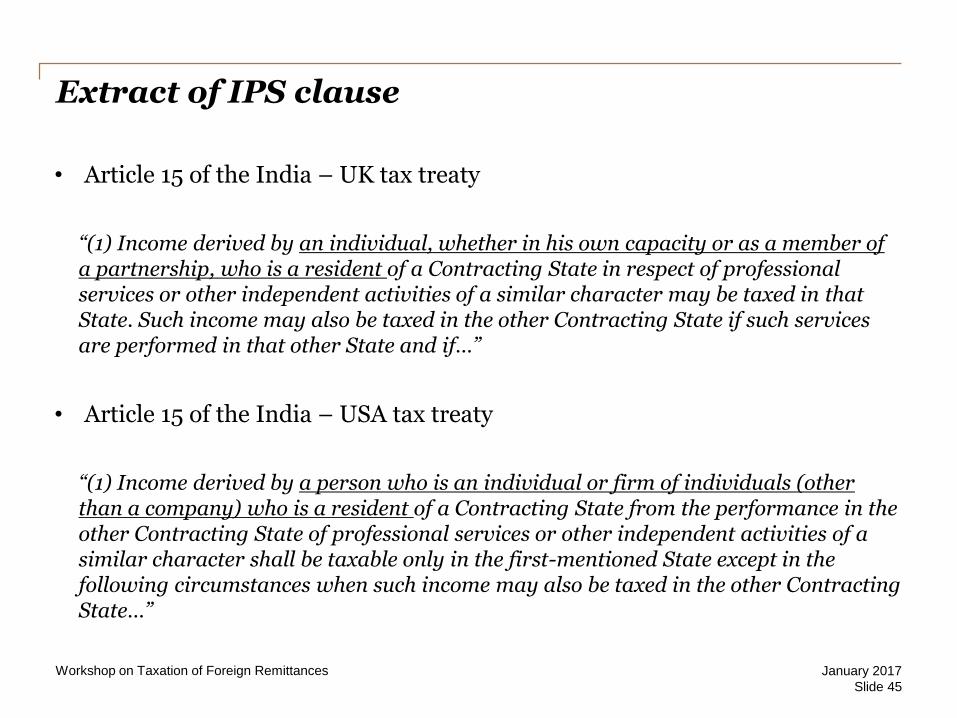

Extract of IPS clause

• Article 15 of the India – UK tax treaty

“(1) Income derived by an individual, whether in his own capacity or as a member of a partnership, who is a resident of a Contracting State in respect of professional services or other independent activities of a similar character may be taxed in that State. Such income may also be taxed in the other Contracting State if such services are performed in that other State and if…”

• Article 15 of the India – USA tax treaty

“(1) Income derived by a person who is an individual or firm of individuals (other than a company) who is a resident of a Contracting State from the performance in the other Contracting State of professional services or other independent activities of a similar character shall be taxable only in the first-mentioned State except in the following circumstances when such income may also be taxed in the other Contracting State…”

Slide 45

January 2017Workshop on Taxation of Foreign Remittances

Extract of IPS clause

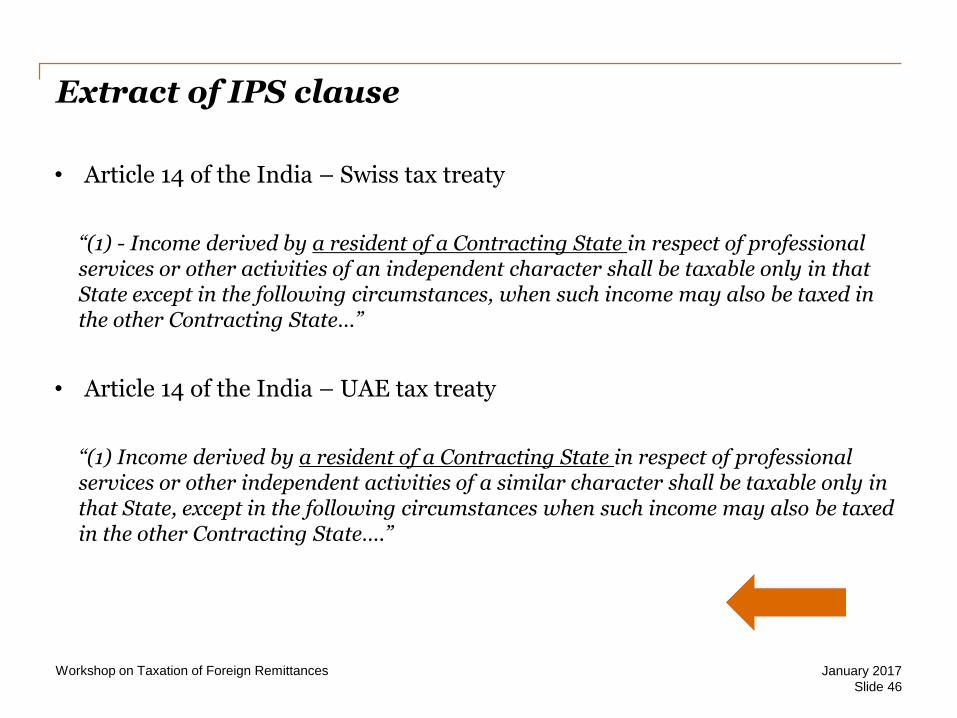

• Article 14 of the India – Swiss tax treaty

“(1) - Income derived by a resident of a Contracting State in respect of professional services or other activities of an independent character shall be taxable only in that State except in the following circumstances, when such income may also be taxed in the other Contracting State…”

• Article 14 of the India – UAE tax treaty

“(1) Income derived by a resident of a Contracting State in respect of professional services or other independent activities of a similar character shall be taxable only in that State, except in the following circumstances when such income may also be taxed in the other Contracting State….”

Slide 46

January 2017Workshop on Taxation of Foreign Remittances

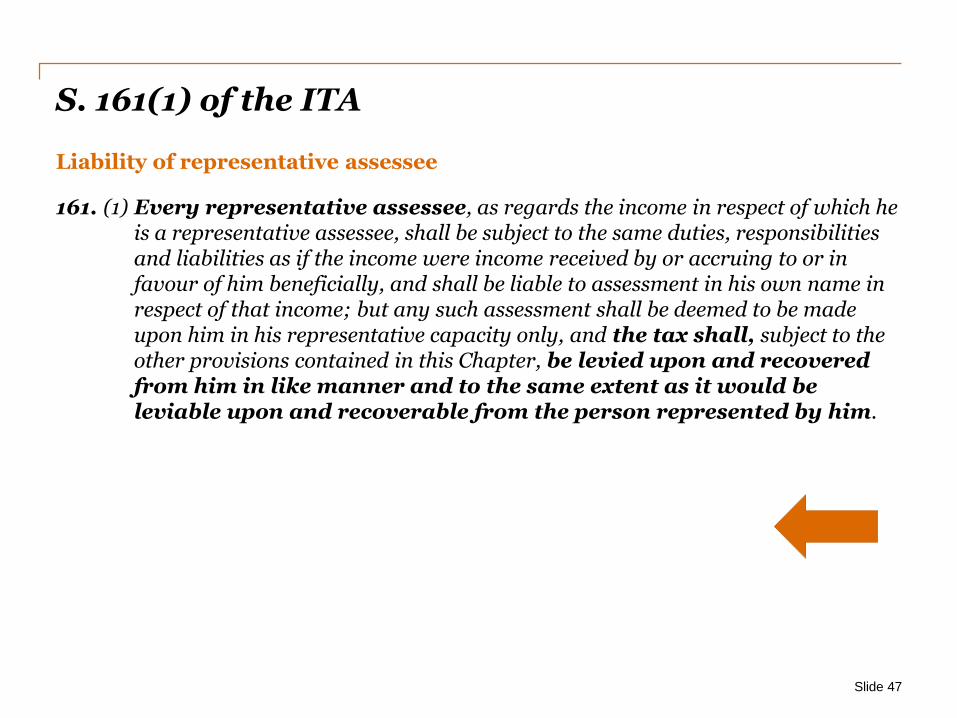

S. 161(1) of the ITA

Liability of representative assessee

161. (1) Every representative assessee, as regards the income in respect of which he is a representative assessee, shall be subject to the same duties, responsibilities and liabilities as if the income were income received by or accruing to or in favour of him beneficially, and shall be liable to assessment in his own name in respect of that income; but any such assessment shall be deemed to be made upon him in his representative capacity only, and the tax shall, subject to the other provisions contained in this Chapter, be levied upon and recovered from him in like manner and to the same extent as it would be leviable upon and recoverable from the person represented by him.

Slide 47

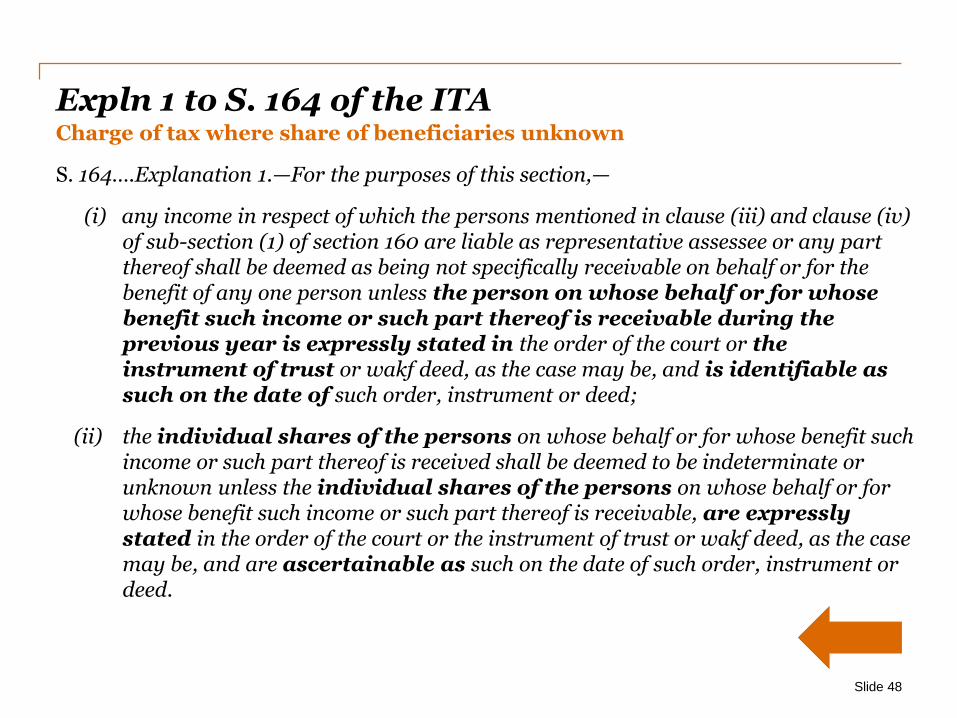

Expln 1 to S. 164 of the ITACharge of tax where share of beneficiaries unknown

S. 164….Explanation 1.—For the purposes of this section,—

(i) any income in respect of which the persons mentioned in clause (iii) and clause (iv) of sub-section (1) of section 160 are liable as representative assessee or any part thereof shall be deemed as being not specifically receivable on behalf or for the benefit of any one person unless the person on whose behalf or for whose benefit such income or such part thereof is receivable during the previous year is expressly stated in the order of the court or the instrument of trust or wakf deed, as the case may be, and is identifiable as such on the date of such order, instrument or deed;

(ii) the individual shares of the persons on whose behalf or for whose benefit such income or such part thereof is received shall be deemed to be indeterminate or unknown unless the individual shares of the persons on whose behalf or for whose benefit such income or such part thereof is receivable, are expressly stated in the order of the court or the instrument of trust or wakf deed, as the case may be, and are ascertainable as such on the date of such order, instrument or deed.

Slide 48