Embed Size (px)

Citation preview

Canadian Securities Institute

The Canadian Financial Wealth Market: Adapting to Changing Household Priorities

Goshka Folda June 20, 2013

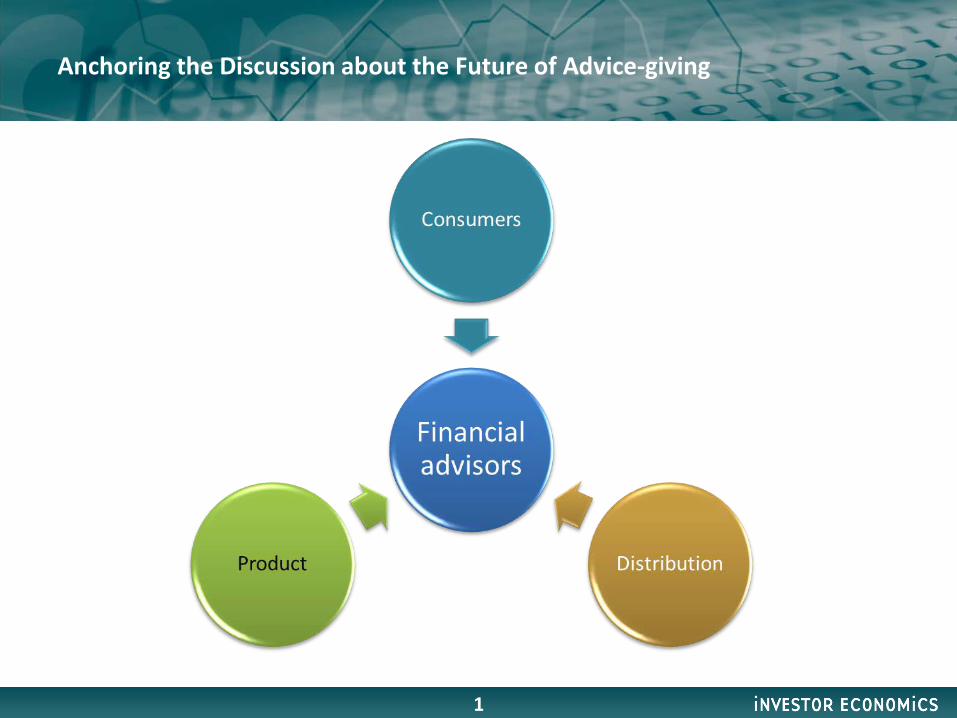

Anchoring the Discussion about the Future of Advice-giving

1

Consumers

Absolute Growth Opportunity Vast but Pace of Expansion Slows Down In billions of dollars

2012 2012-2022

CAGR

Total assets

Financial wealth

Residential real estate

Credit

$9,871

$3,118

$3,464

$1,744

Source: Household Balance Sheet Report, 2013 Edition.

3

2022

$14,059

$5,449

$4,225

$2050

Assets

3.6%

5.7%

1.6%

2.0%

Total assets

Financial wealth

Residential real estate

Credit

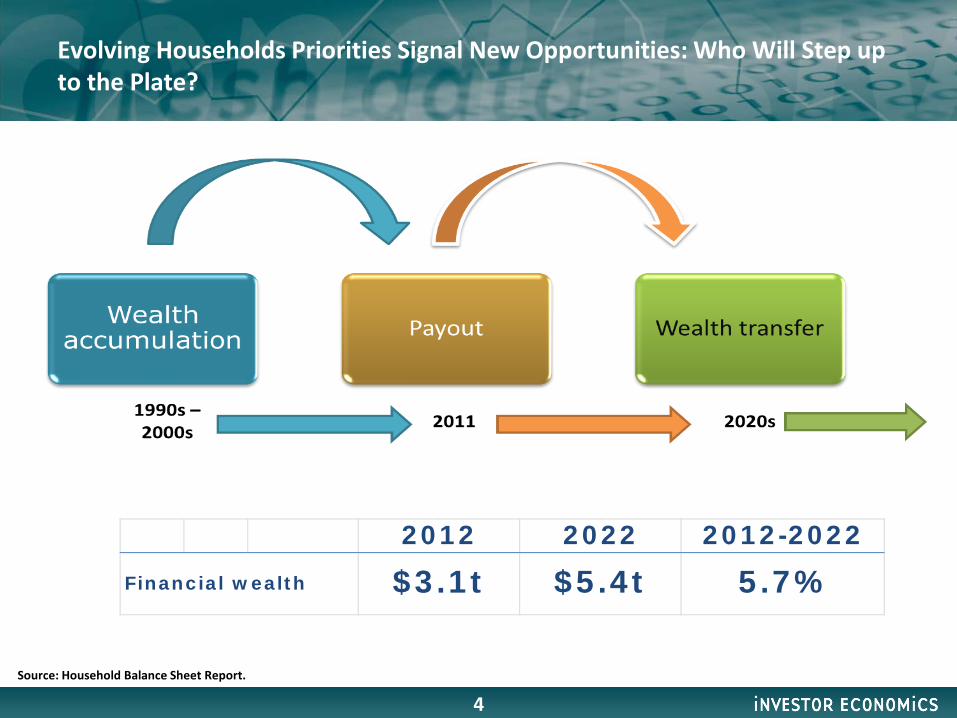

Evolving Households Priorities Signal New Opportunities: Who Will Step up to the Plate?

4 Source: Household Balance Sheet Report.

Financ ia l w ea lt h

2 0 1 2 2 0 2 2 2 0 1 2 -2 0 2 2

$3 .1 t $5 .4 t 5 .7%

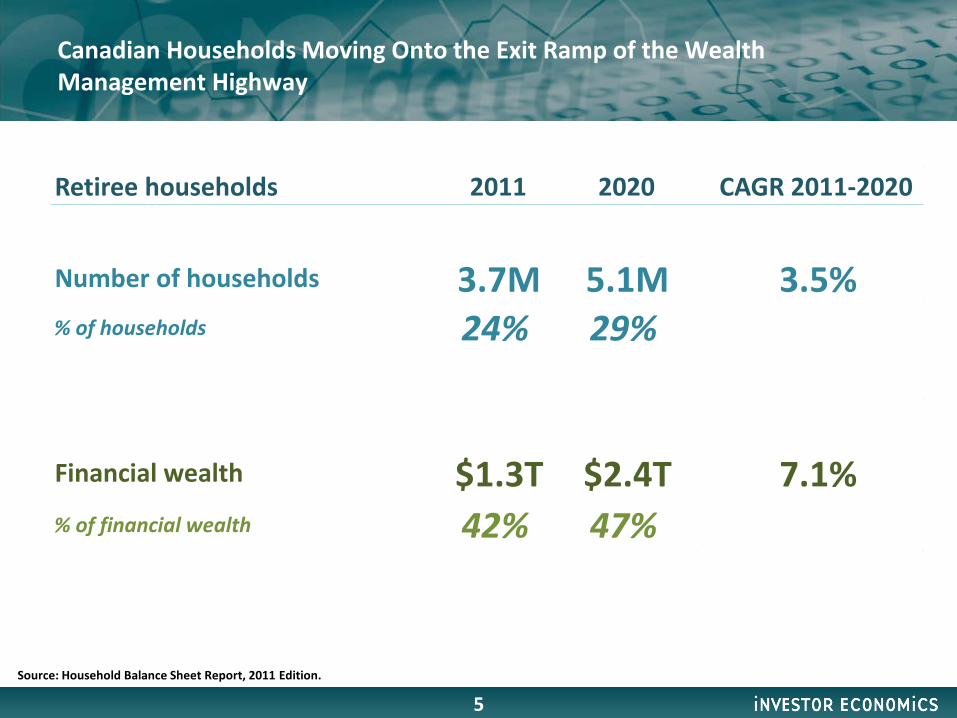

Canadian Households Moving Onto the Exit Ramp of the Wealth Management Highway

5 Source: Household Balance Sheet Report, 2011 Edition.

Retiree households 2011 2020 CAGR 2011-2020

Number of households 3.7M 5.1M 3.5% % of households 24% 29%

Financial wealth $1.3T $2.4T 7.1% % of financial wealth 42% 47%

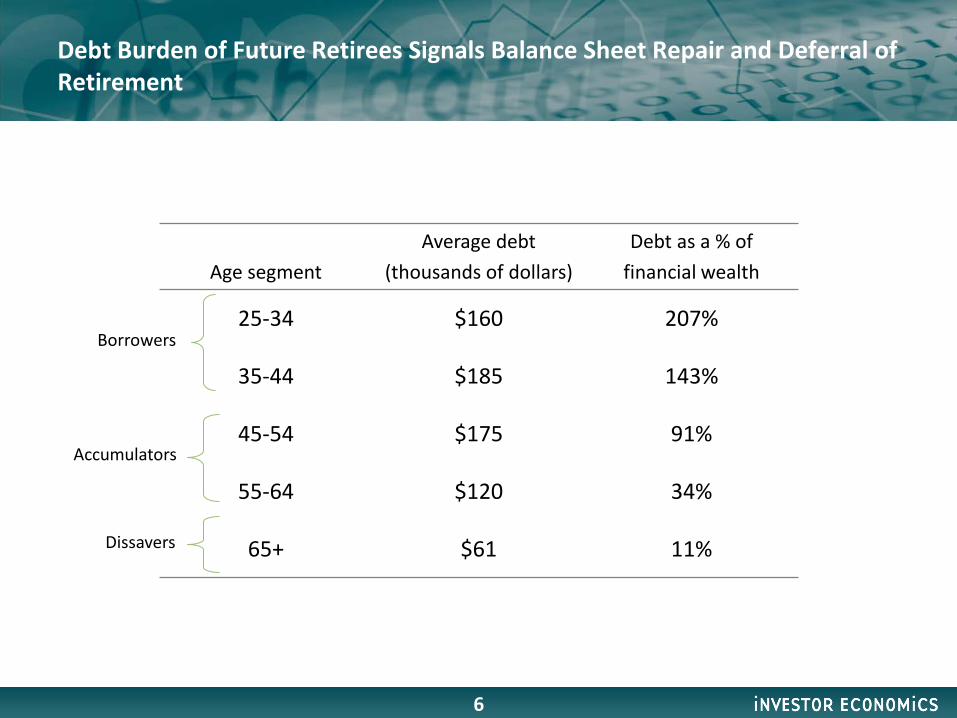

Debt Burden of Future Retirees Signals Balance Sheet Repair and Deferral of Retirement

Age segment Average debt

(thousands of dollars) Debt as a % of

financial wealth

25-34 $160 207%

35-44 $185 143%

45-54 $175 91%

55-64 $120 34%

65+ $61 11%

Borrowers

Accumulators

Dissavers

6

Households and Financial Wealth Assets by Asset Threshold Number of households in thousands, assets in billions of dollars

Households Assets

Mass market

Mid- market

Upscale market

Affluent market

7

Average financial wealth per household $195⇒$300K

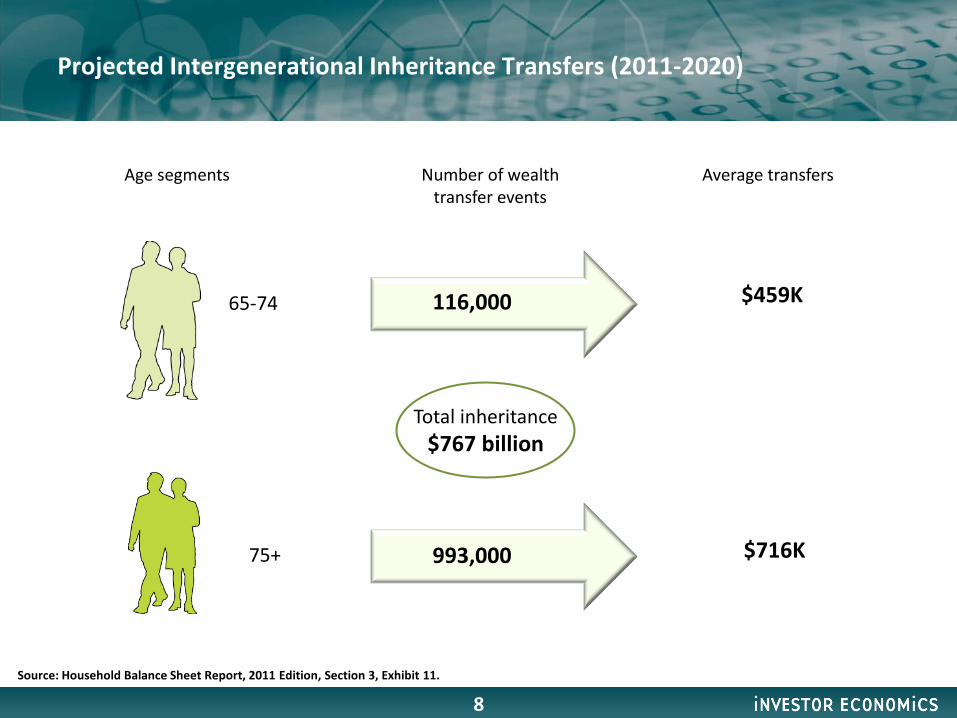

Projected Intergenerational Inheritance Transfers (2011-2020)

Average transfers

$459K

$716K

Number of wealth transfer events

Age segments

116,000

993,000

65-74

75+

Total inheritance $767 billion

8 Source: Household Balance Sheet Report, 2011 Edition, Section 3, Exhibit 11.

Products

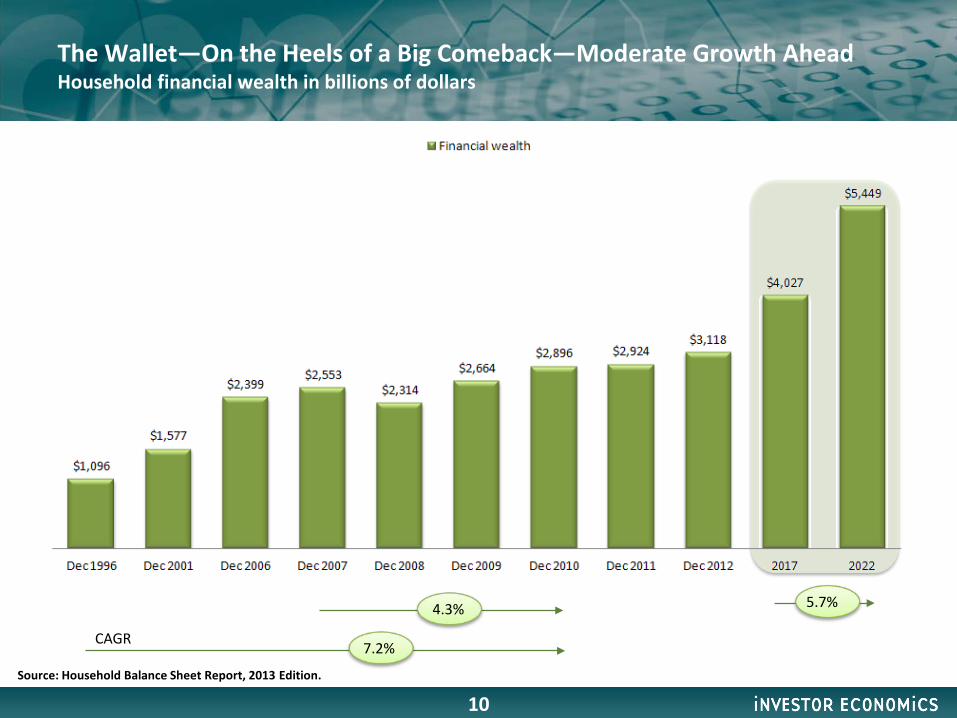

The Wallet—On the Heels of a Big Comeback—Moderate Growth Ahead Household financial wealth in billions of dollars

CAGR

5.7%

10

4.3%

7.2%

Source: Household Balance Sheet Report, 2013 Edition.

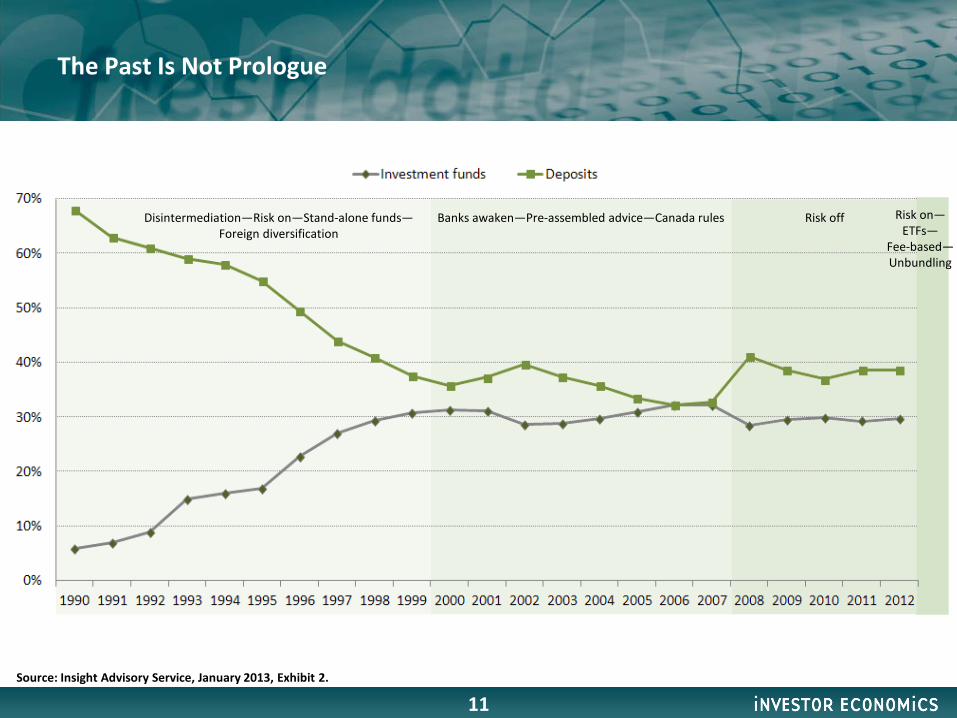

The Past Is Not Prologue

Source: Insight Advisory Service, January 2013, Exhibit 2.

Disintermediation—Risk on—Stand-alone funds— Foreign diversification

Banks awaken—Pre-assembled advice—Canada rules Risk off Risk on— ETFs—

Fee-based— Unbundling

11

Appetite For Risk-averse Vehicles Still Large and Growing; “Money on the Sidelines” Breaches $1 Trillion In billions of dollars

29% 29% 36% 34% 34% Total liquid instruments as a % of financial wealth

12

Fund Industry Flows Are on the Rise—with ETFs Leading the Charge Long-term investment fund net flows and ETF net creations in billions of dollars

Net flowsMarket effect Net flows

Market effect Net flows

Market effect Net flows

Market effect

Mutual funds 10.1% 4.8% 4.0% 6.0% 2.1% 2.0% 4.1% 7.0%Segregated funds 22.6% 4.3% 5.3% 5.2% 4.5% 0.7% 2.0% 4.6%ETFs – – 9.3% 14.0% 23.8% 2.7% 27.9% 2.2%

1997-2001 2002-2007 2008-2012As % of beginning assets

2012

Source: Insight Advisory Service, January 2013, Exhibit 3.

13

The Changing Asset Class Mix of Net Flows—Reprise of Foreign Diversification Long-term mutual fund net flows in billions of dollars

Canadian 96.3% 67.6% 72.5% 42.1% 41.8% 59.4% 39.0%

Foreign mandates 3.7% 32.4% 27.5% 57.9% 58.2% 40.6% 61.0%

Share of net flows

14

Growth of Fund Wraps Signals Importance of Pre-Assembled Advice Growth indexed to 1999, assets in billions of dollars

*Excludes ETFs.

Source: Insight Advisory Service, January 2013, Exhibit 9.

15

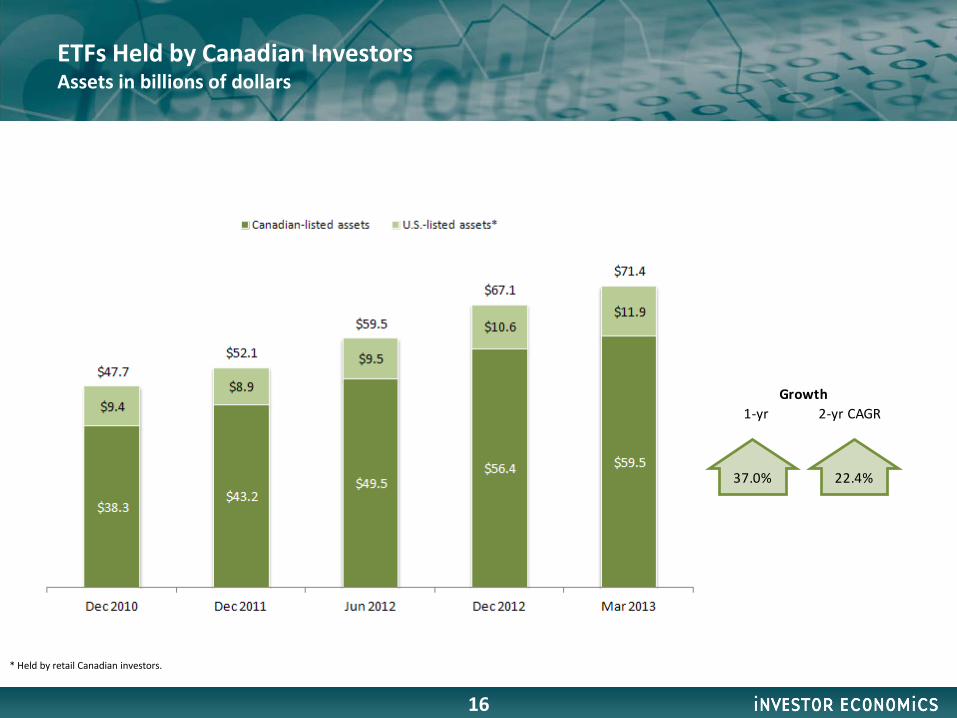

ETFs Held by Canadian Investors Assets in billions of dollars

* Held by retail Canadian investors.

16

1-yr 2-yr CAGRGrowth

22.4%37.0%

The Retirement Market Product Field – A 360° View

17

Hybrid retirement income solution

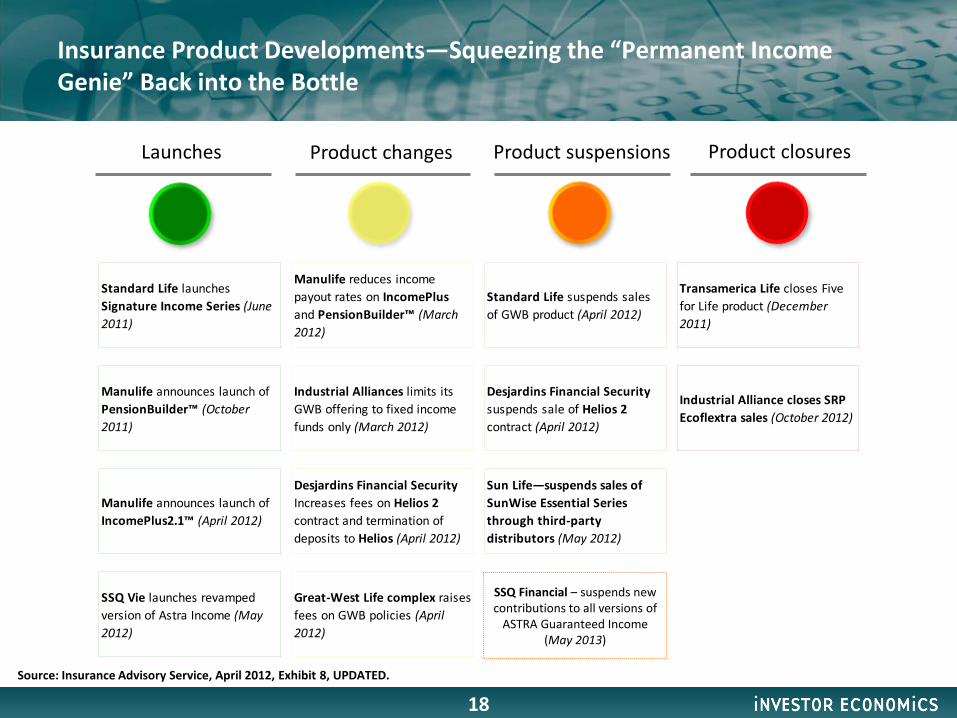

Insurance Product Developments—Squeezing the “Permanent Income Genie” Back into the Bottle

Launches Product changes Product suspensions Product closures

18

Standard Life launches Signature Income Series (June 2011)

Manulife reduces income payout rates on IncomePlus and PensionBuilder™ (March 2012)

Standard Life suspends sales of GWB product (April 2012)

Transamerica Life closes Five for Life product (December 2011)

Manulife announces launch of PensionBuilder™ (October 2011)

Industrial Alliances limits its GWB offering to fixed income funds only (March 2012)

Desjardins Financial Security suspends sale of Helios 2 contract (April 2012)

Industrial Alliance closes SRP Ecoflextra sales (October 2012)

Manulife announces launch of IncomePlus2.1™ (April 2012)

Desjardins Financial Security Increases fees on Helios 2 contract and termination of deposits to Helios (April 2012)

Sun Life—suspends sales of SunWise Essential Series through third-party distributors (May 2012)

SSQ Vie launches revamped version of Astra Income (May 2012)

Great-West Life complex raises fees on GWB policies (April 2012)

SSQ Financial – suspends new contributions to all versions of

ASTRA Guaranteed Income (May 2013)

Source: Insurance Advisory Service, April 2012, Exhibit 8, UPDATED.

2007 2008 2009 2010 2011 2012

PPNs PARNs

7.6%

8.3% 70.4%40.9%

25.5%15.7%

92.4% 91.7% 29.6%59.1%74.5%84.3%

467411

282261

375

485

Market-linked Notes Issued by Protection Type

19

Number of notes outstanding as of Dec 2012 2,276

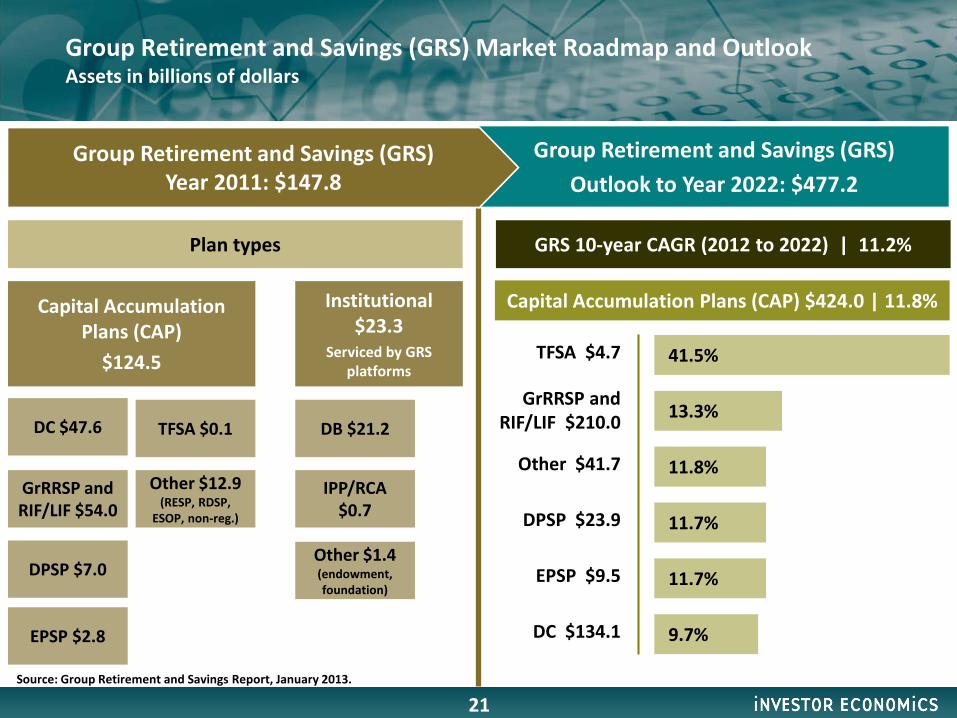

Big Business—Group Retirement and Savings by the Numbers

20 Source: Group Retirement and Savings Report, January 2013.

TFSA $4.7

GrRRSP and RIF/LIF $210.0

Other $41.7

DPSP $23.9

EPSP $9.5

DC $134.1

Group Retirement and Savings (GRS) Market Roadmap and Outlook Assets in billions of dollars

21

DC $47.6

GrRRSP and RIF/LIF $54.0

DPSP $7.0

EPSP $2.8

TFSA $0.1

Other $12.9 (RESP, RDSP,

ESOP, non-reg.)

Capital Accumulation Plans (CAP)

$124.5

Institutional $23.3

Serviced by GRS platforms

DB $21.2

IPP/RCA $0.7

Other $1.4 (endowment, foundation)

Plan types

GRS 10-year CAGR (2012 to 2022) | 11.2%

Group Retirement and Savings (GRS) Outlook to Year 2022: $477.2

Group Retirement and Savings (GRS)

Year 2011: $147.8

Capital Accumulation Plans (CAP) $424.0 | 11.8%

41.5%

13.3%

11.8%

11.7%

11.7%

9.7%

Source: Group Retirement and Savings Report, January 2013.

Distribution

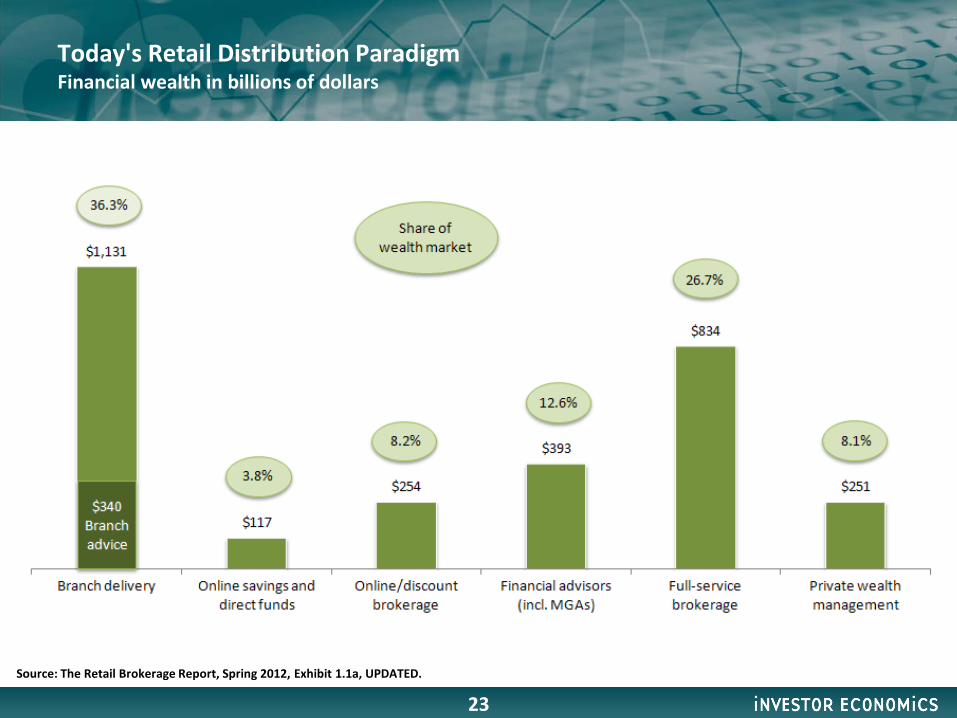

Today's Retail Distribution Paradigm Financial wealth in billions of dollars

Source: The Retail Brokerage Report, Spring 2012, Exhibit 1.1a, UPDATED.

23

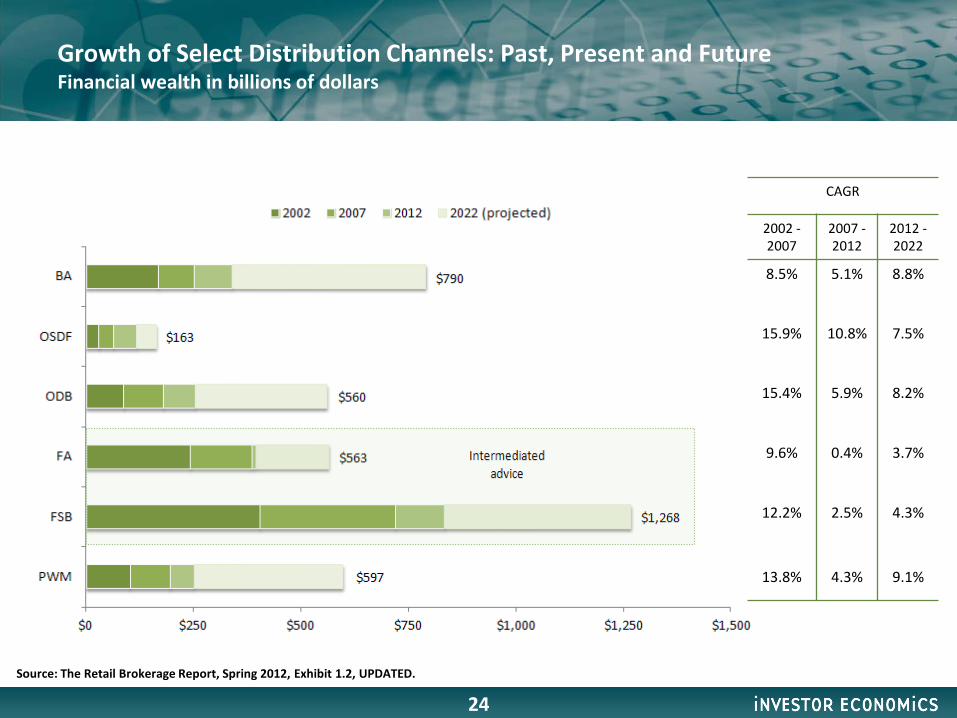

Growth of Select Distribution Channels: Past, Present and Future Financial wealth in billions of dollars

CAGR

2002 - 2007

2007 - 2012

2012 - 2022

8.5% 5.1% 8.8%

15.9% 10.8% 7.5%

15.4% 5.9% 8.2%

9.6% 0.4% 3.7%

12.2% 2.5% 4.3%

13.8% 4.3% 9.1%

Source: The Retail Brokerage Report, Spring 2012, Exhibit 1.2, UPDATED.

24

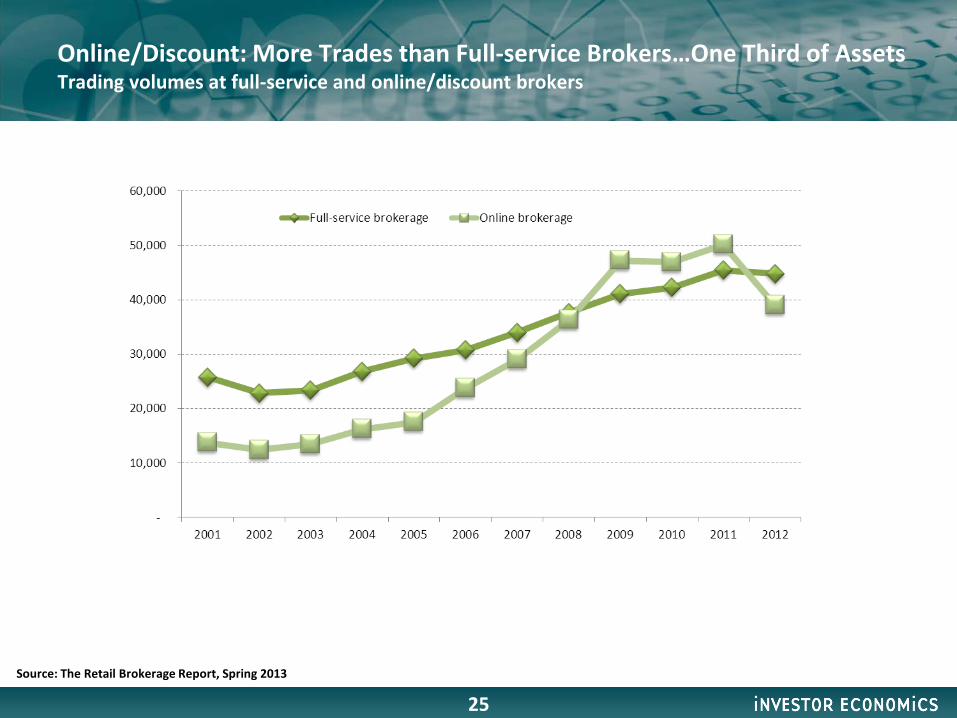

Online/Discount: More Trades than Full-service Brokers…One Third of Assets Trading volumes at full-service and online/discount brokers

Source: The Retail Brokerage Report, Spring 2013

25

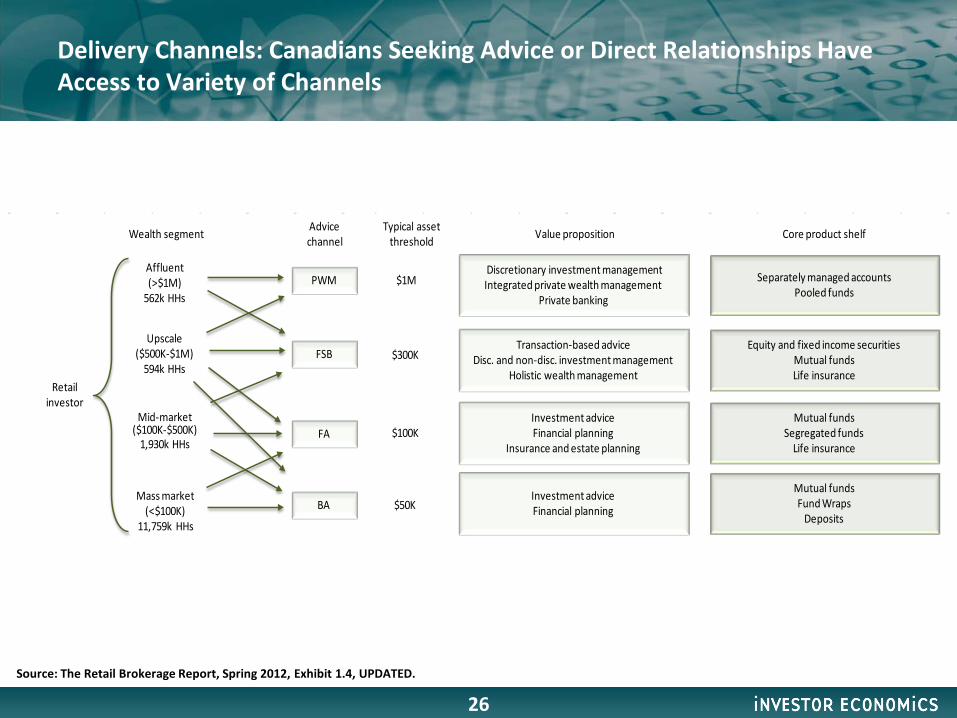

Delivery Channels: Canadians Seeking Advice or Direct Relationships Have Access to Variety of Channels

26

Retail investor

Affluent(>$1M)

562k HHs

Upscale($500K-$1M)

594k HHs

Mid-market($100K-$500K)

1,930k HHs

Mass market(<$100K)

11,759k HHs

PWM

FSB

FA

BA

$1M

$300K

$100K

$50K

Typical asset threshold

Separately managed accountsPooled funds

Core product shelf

Equity and fixed income securitiesMutual fundsLife insurance

Mutual fundsSegregated funds

Life insurance

Mutual fundsFund Wraps

Deposits

Value proposition

Discretionary investment managementIntegrated private wealth management

Private banking

Transaction-based adviceDisc. and non-disc. investment management

Holistic wealth management

Investment adviceFinancial planning

Insurance and estate planning

Investment adviceFinancial planning

Advice channelWealth segment

Source: The Retail Brokerage Report, Spring 2012, Exhibit 1.4, UPDATED.

Shift to Fee-based Pricing Models Poised to Accelerate in Intermediated Advice Channels Assets in billions of dollars

27

56% 57% 52% 53%

44%

10%14%

20%

28%

27%

34%29%

28%

16%

12%

$41$90

$140

$242

$625

2002 2005 2007 2012 2022

FBP/FBA

DWs

AM

FBB

Source: Household Balance Sheet Report, 2013 UPDATED.

Future of Advice-giving

Advisors Must Adapt to Changing Client Need and a Broader Competitive Landscape

• Adapt to evolving consumer needs by executing a “Growing with Your Customers” strategy and focusing on holistic wealth and insurance management

• Expand expertise in emerging areas, such as risk management, retirement income planning and estate planning

• Crystallize and articulate value of advice to combat competitive challenge from branch advisors

• Address time constraints and rising compliance and technology costs

• Develop new revenue opportunities and business efficiencies to strengthen economic model

29

1996: $10 million 2011: $23.4 million Advisor mutual fund book size needed to generate equivalent revenues