Embed Size (px)

Citation preview

The Canadian Financial System

Jean Roy PhD

École des HEC

June 1999

Content

1. Introduction

2. Legal framework

3. Present state

4. Current developments

5. Conclusion

1. Introduction

• Context: Many internal and external factors putting pressure for changes

• Objective: Providing a quick overview of the present situation and current trends

• Sections: Legal, Economic, Trends

2. Legal framework

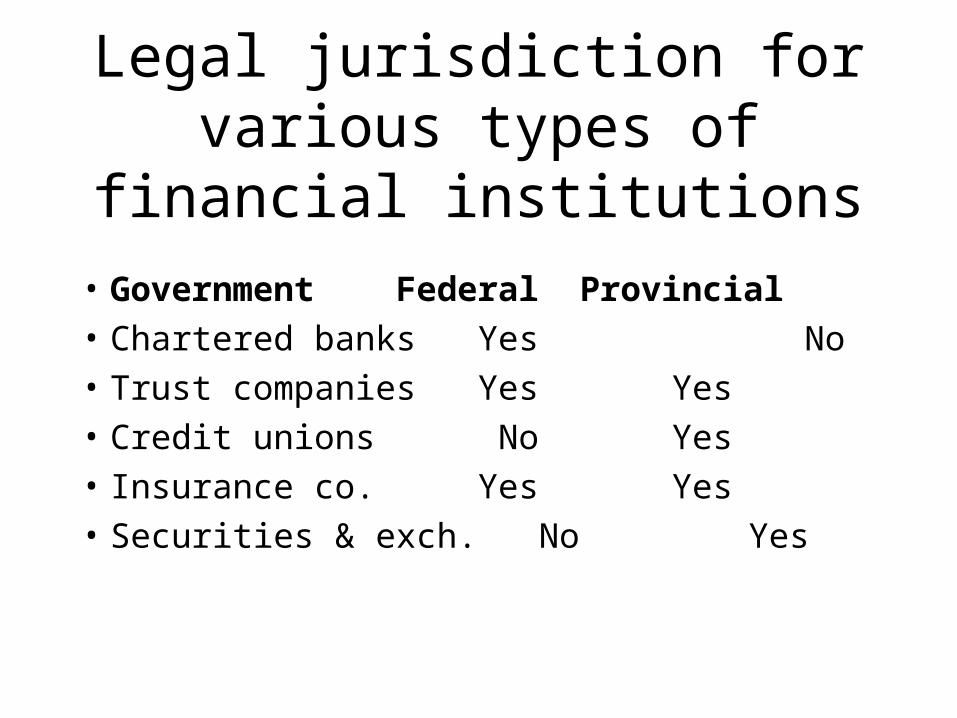

Legal jurisdiction for various types of financial

institutions

• Government Federal Provincial• Chartered banks Yes No• Trust companies Yes Yes• Credit unions No Yes• Insurance co. Yes Yes• Securities & exch. No Yes

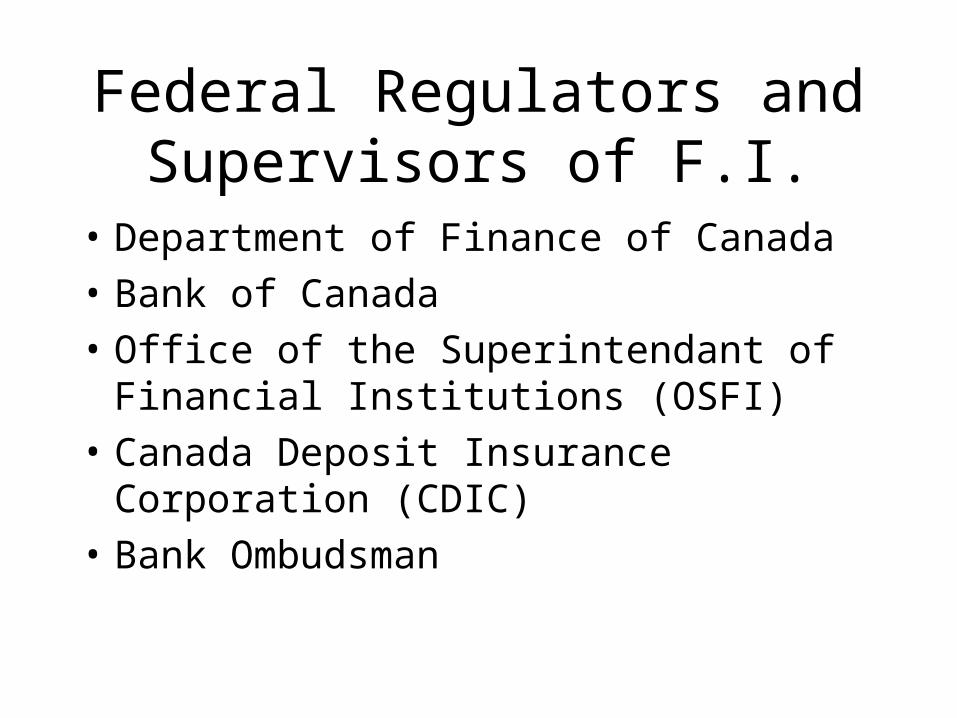

Federal Regulators and Supervisors of F.I.

• Department of Finance of Canada• Bank of Canada• Office of the Superintendant of

Financial Institutions (OSFI)• Canada Deposit Insurance

Corporation (CDIC)• Bank Ombudsman

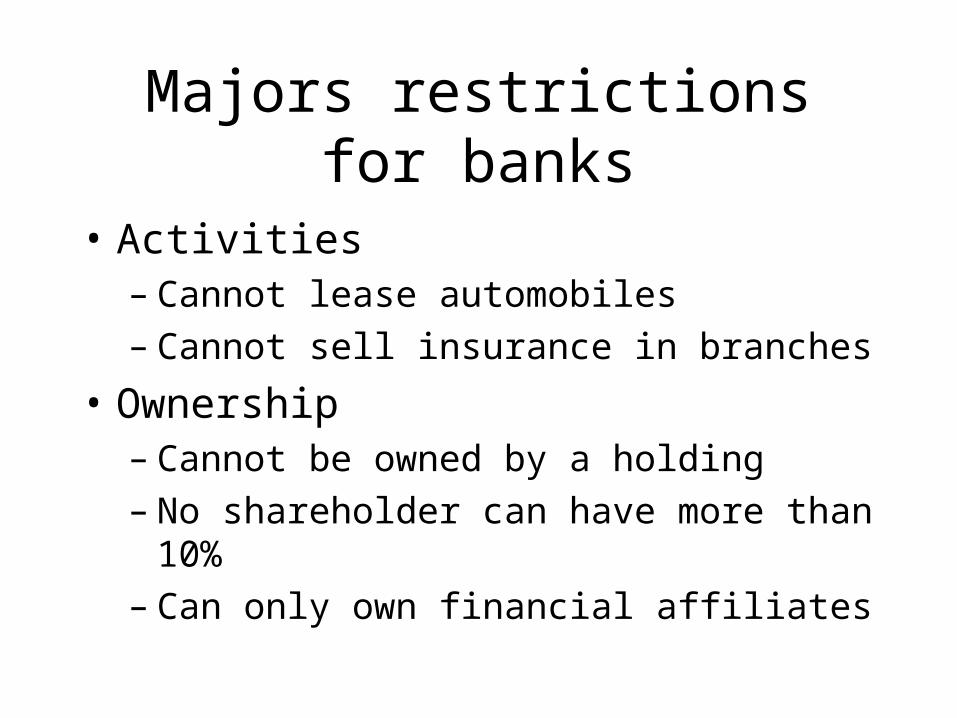

Majors restrictions for banks

• Activities– Cannot lease automobiles– Cannot sell insurance in branches

• Ownership– Cannot be owned by a holding– No shareholder can have more than 10%– Can only own financial affiliates

3. Present state of the canadian financial system

McKinsey Report

Reference:http://finservtaskforce.fin.gc.ca/research/research.htm

Exhibits 2-9 to 2-16, 2-24, 2-27

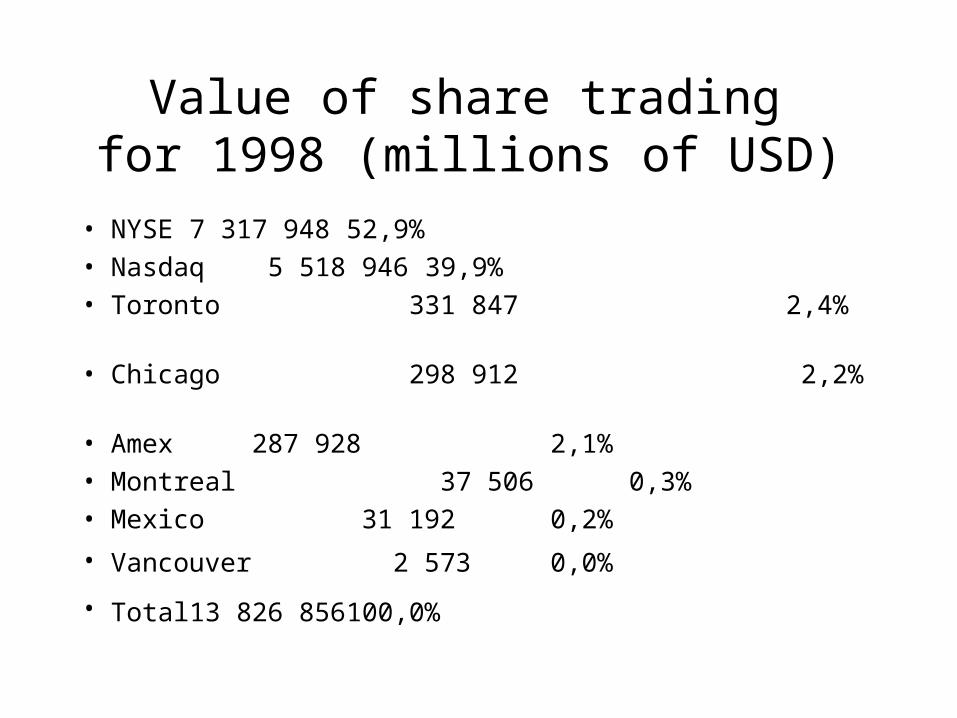

Value of share trading for 1998 (millions of USD)

• NYSE 7 317 948 52,9%

• Nasdaq 5 518 946 39,9%

• Toronto 331 847 2,4%

• Chicago 298 912 2,2%

• Amex 287 928 2,1%

• Montreal 37 506 0,3%

• Mexico 31 192 0,2%

• Vancouver 2 573 0,0%

• Total 13 826 856 100,0%

4. Current developments

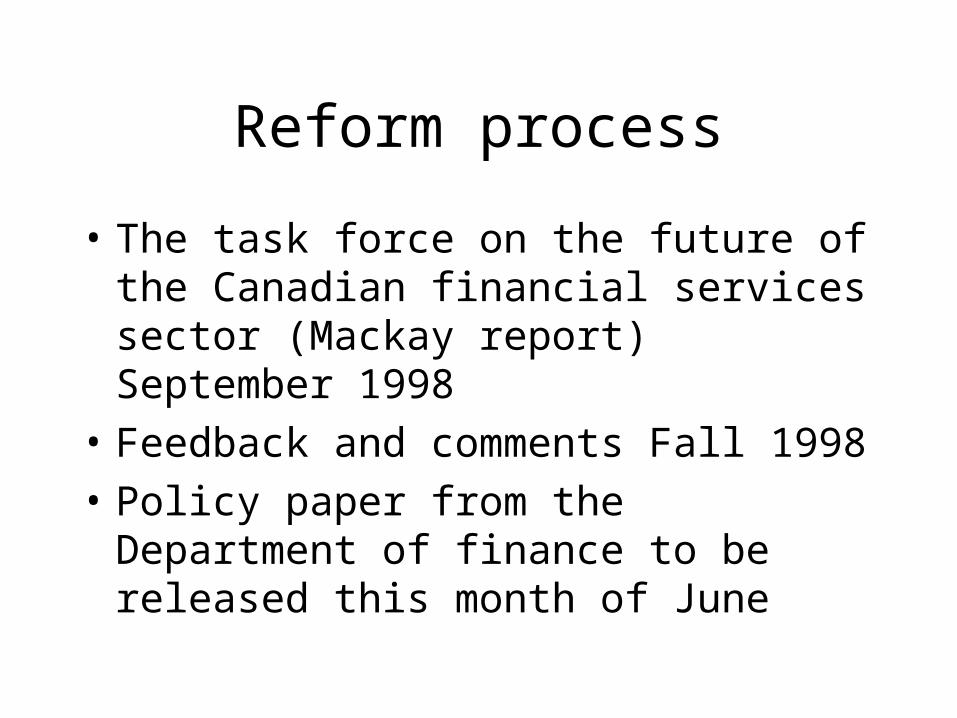

Reform process

• The task force on the future of the Canadian financial services sector (Mackay report) September 1998

• Feedback and comments Fall 1998

• Policy paper from the Department of finance to be released this month of June

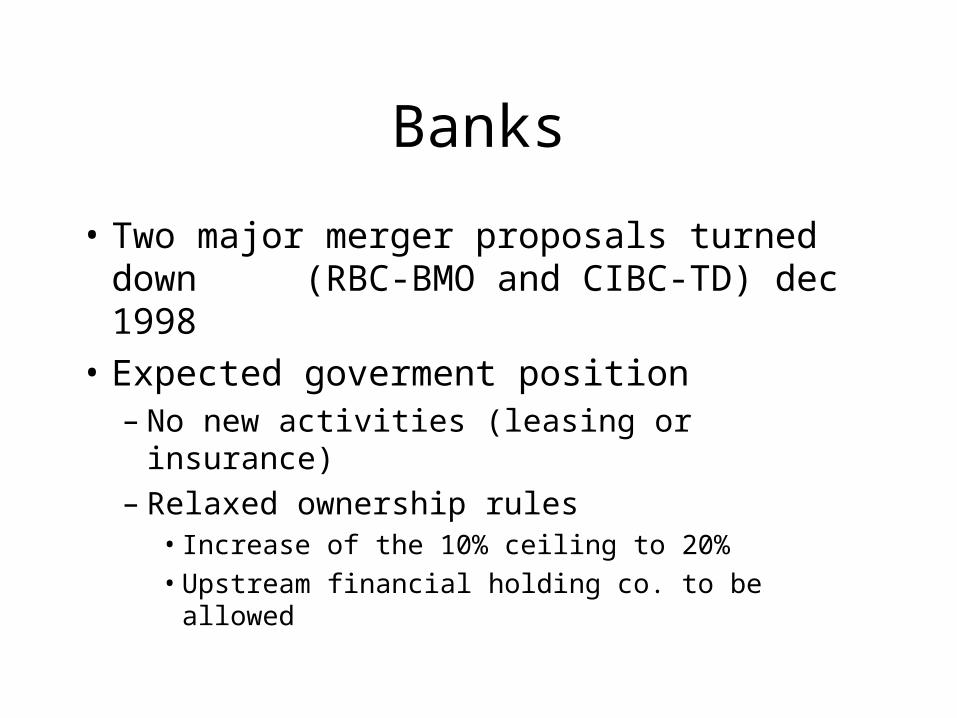

Banks

• Two major merger proposals turned down (RBC-BMO and CIBC-TD) dec 1998

• Expected goverment position– No new activities (leasing or insurance)– Relaxed ownership rules

• Increase of the 10% ceiling to 20%

• Upstream financial holding co. to be allowed

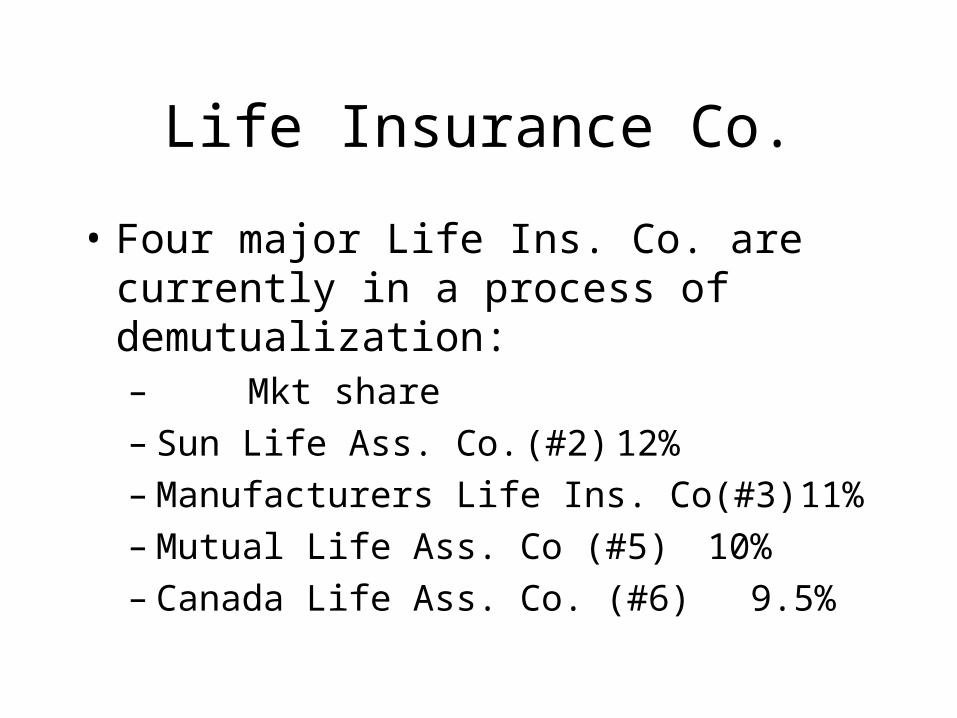

Life Insurance Co.

• Four major Life Ins. Co. are currently in a process of demutualization:– Mkt share– Sun Life Ass. Co. (#2) 12%– Manufacturers Life Ins. Co(#3) 11%– Mutual Life Ass. Co (#5) 10%– Canada Life Ass. Co. (#6)

9.5%

Other federaly regulated F.I.

• Insurance co., Trust co and Stock brokers to be allowed to participate directly in the payment system

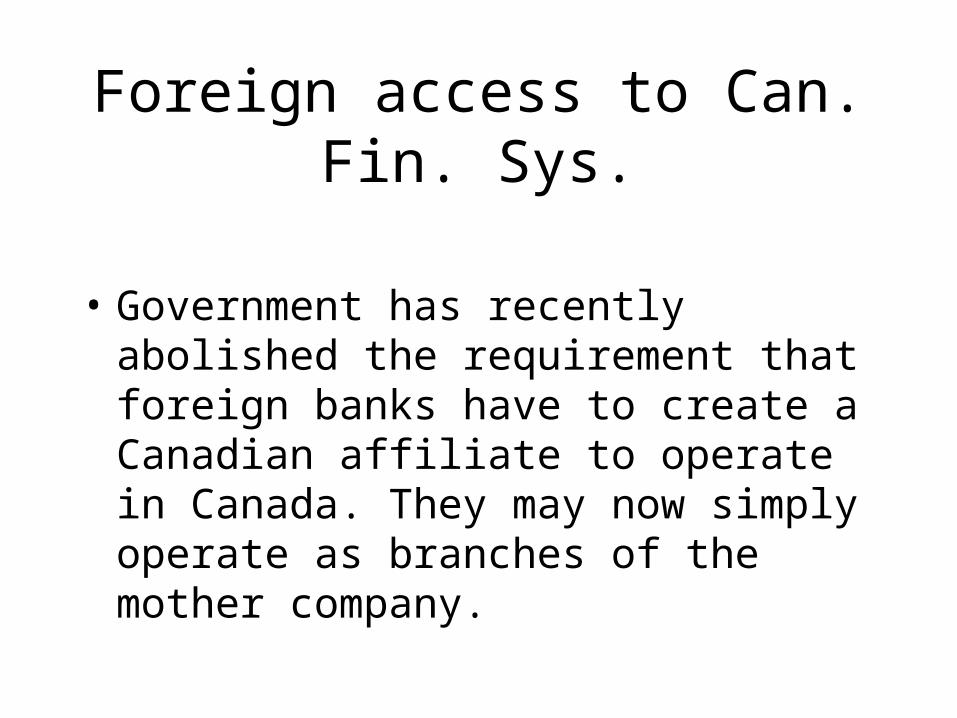

Foreign access to Can. Fin. Sys.

• Government has recently abolished the requirement that foreign banks have to create a Canadian affiliate to operate in Canada. They may now simply operate as branches of the mother company.

Canada Deposit Insurance Corp.

• CDIC has now (Spring 1999) put in place a system of premium that is risk-adjusted.

• Premium vary from 1/6 to 1/3 of 1% of deposits

Stock exchanges

• The four Canadian stock exchanges have agreed on a major reorganization plan– Toronto to trade senior equities– Montreal to specialize in derivatives– Vancouver and Alberta to merge and trade

junior equities

• Plan is still to be approved by regulators

5. Conclusion

Characteristics of the Canadian Financial System

It used to be:

• protected

• bank dominated

• concentrated

• secure and stable

Nature of current evolution

• Protection is being lifted both by NAFTA and commitments to WTO

• Non bank institutions will be favored by the coming reform

• Stock exchanges will go through a major reorganization to survive against US competition

Final word

• Whereas the Canadian Financial System used to evolve quietly,

• it is now in a process of rapid and substantial changes to cope with technological progress and internationalization.