Embed Size (px)

Citation preview

The Business Case for Financial Education

Personal Financial Wellnessand Employee Productivity

E. Thomas Garman

Presented to The Conference BoardAtlanta and San Diego

1998

Introduction

The majority of financial education programs are traditional, narrowly focused retirement education

Smart employers are broadening their perspectives about financial education

Want to help workers make good decisions about:– Investment choices within employer-

sponsored retirement plans

– Other employer-furnished fringe benefits

– Personal budgeting Are helping workers with money

problems learn to overcome such obstacles so they can fully fund their retirement plans

Smart Employers

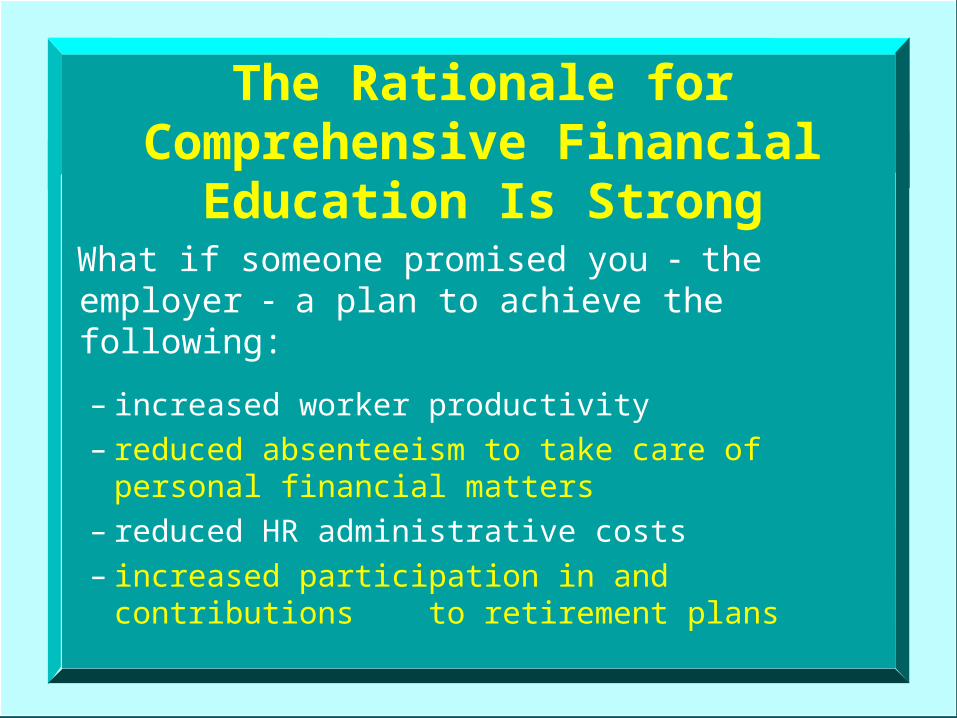

The Rationale for Comprehensive Financial Education Is Strong

What if someone promised you the employer a plan to achieve the following:

– increased worker productivity– reduced absenteeism to take care of personal

financial matters– reduced HR administrative costs– increased participation in and contributions to

retirement plans

- reduced social security payroll taxes

- reduced stress over financial matters and stress-related illnesses

- fewer accidents

- improved use of and satisfaction with employer-provided fringe benefits

- reduced hr administrative costs

- reduced turnover

- reduced pressure to increase salaries

- increased morale and loyalty

- increased number of worker retirements on time, rather than delayed

- reduced exposure to future litigation based upon fiduciary liability as fewer retirees have financial problems

- a positive return on every dollar invested in comprehensive financial education

Research findings are promising,

although more research partners

are needed to definitively prove

the case for comprehensive

financial education

Research by Joo Shows Financial Wellness and Key

Measures of Work Productivity Are Positively Related

Those with poor financial wellness are more likely to be: Frequently absent from work Receive poor performance ratings Spend excessive time at work dealing

with personal financial problems Experience a decline in job productivity

from one year to the next

Workers That Employers Love -Those with Good Financial Wellness

Come to work Receive high performance ratings Use a minimum of time at work

attending to personal financial matters Enjoy consistent or increasing job

productivity

Additional Joo Conclusions

The likely first year return on investment for financial education that improves the personal financial behavior and wellness of a worker is about $400

The potential return comes from fewer absences, less work time spent on dealing with personal financial matters, and increases in job productivity

Traditional and Narrowly Focused Retirement Education Programs Have Limited Effectiveness

For many employers, retirement planparticipation rates have reached a plateau.

Some Workers Will Not or Cannot Contribute to

Their Retirement Plans

Two reasons exist:

1. Some workers have money problems and cannot afford to

save for retirement

2. Some workers are not convinced that they should save for

retirement

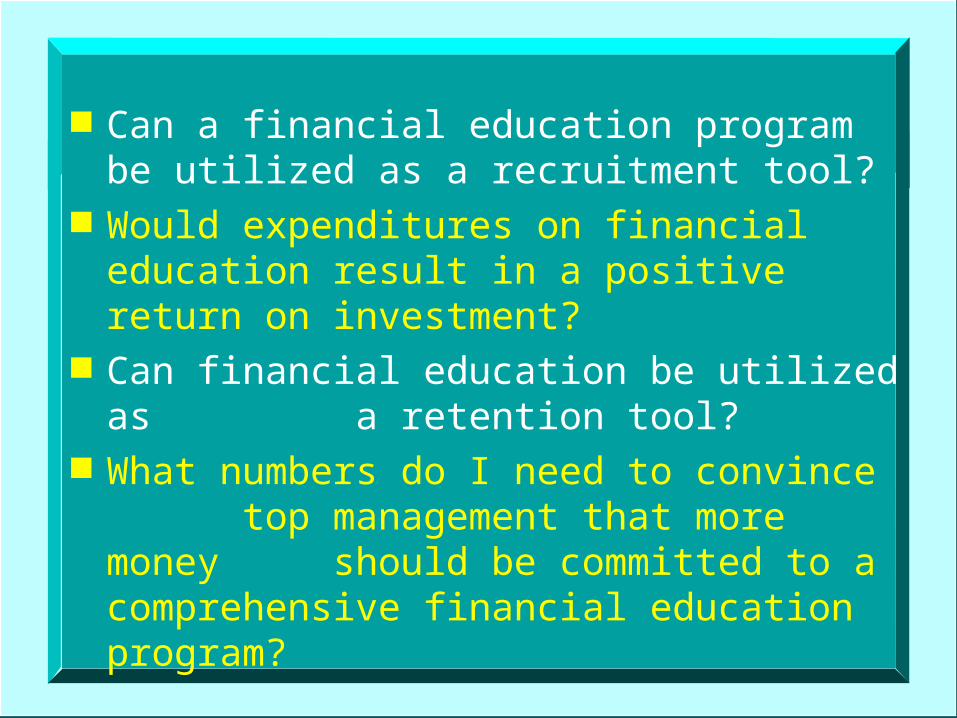

Employers Have Questions About What More to Do in Financial Education

What would it take to get the participation rate higher?

What would it take to help workers change their asset allocation to better diversify their investment portfolios?

How much would a comprehensive financial education program cost?

Does financial education work?

Can a financial education program be utilized as a recruitment tool?

Would expenditures on financial education result in a positive return on investment?

Can financial education be utilized as a retention tool?

What numbers do I need to convince top management that more money should be committed to a comprehensive financial education program?

The Cost of Providing Only Retirement Education

Is Horribly High Not all workers are secure in their money

matters A full 2/3 of Americans say “they have

trouble paying their bills and worry about money”

75% of Americans report that they recently faced at least one significant financial problem

Financial matters and financialstress affect not only an individual’s personal and family life, but also a person’s work life.

Approximately 15% of workers in the U.S. are currently experiencing stress from poor financial behaviors to the extent that it negatively impacts their productivity.

Poor Financial Behaviors Result in Extremely High Costs Incurred by Employers

1. Absenteeism 2. Tardiness 3. Fighting with co-workers and supervisors 4. Sabotaging the work of co-workers 5. Job stress 6. Reduced employee productivity

7. Lowered employee morale

8. Loss of customers who seek better service

9. Loss of revenue from sales not made

10. Accidents and increased risk taking

11. Disability and worker compensation claims

12. Substance abuse

13. Suicide and murder

14. Increased use of available health

Care resources by the employee and relatives

15. Thefts from employers

16. Loss of security clearance

17. Nondeployment of employee to an overseas operation

18. Lack of employee focus on the strategic goals of the employer

19. Greater use of EAP services, including those for spouse and child abuse

20. Employer time to deal with poor financial behaviors of employees

21. Loss of trained personnel

Research by the Military Family Institute concludes that the direct and indirect costs to the Nnavy for poor personal financial behaviors of workers is between $208 and $294 million annually

The cost to the Department of Defense, an employer of 1.4 million, is about

$1 billion annually

New Research by Virginia Tech’s Joo Reveals:

54% of average income workers in a sample of white-collar occupations are dissatisfied with their financial wellness

30% feel they are always in financial trouble and 35% find it hard to pay bills

51% worry about how much they owe 44% do not set aside money for retirement 60% do not have enough money set aside

to live for longer than 2 months if they lost their jobs

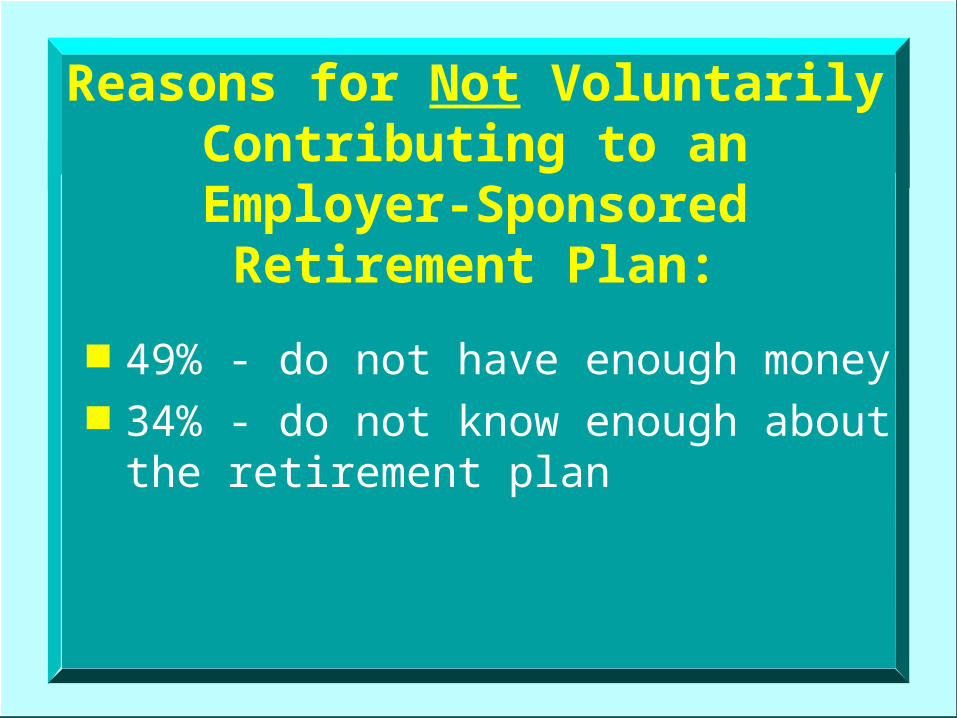

Reasons for Not Voluntarily Contributing to an Employer-Sponsored Retirement Plan:

49% - do not have enough money 34% - do not know enough about the

retirement plan

There is a growing national movement to offer financial education in the workplace, partially because so many workers are going to have extreme difficulty finding money for retirement

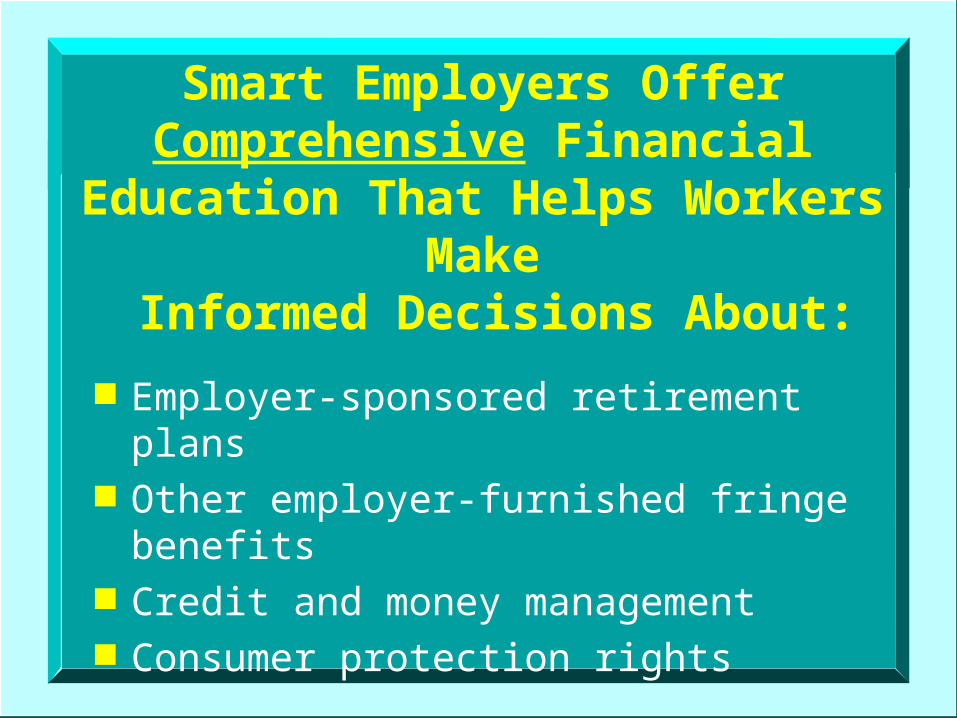

Smart Employers Offer Comprehensive Financial Education

That Helps Workers Make Informed Decisions About:

Employer-sponsored retirement plans Other employer-furnished fringe benefits Credit and money management Consumer protection rights

Smart Employers Realize Financial Education Is a

Key Factor in Recruitment and Retention

The best workers are typically: in control of their personal finances contribute to their pension plans

These workers are happier in theirfinancial lives and it shows in their work

Smart Employers Will Do Two Things

1. Provide employees with comprehensive financial education

2. Identify and help workers with money problems overcome obstacles to fully fund their retirement plans

How Can Employers Help Workers With Money Problems?

Smart employers provide workers with non-profit budget and credit counseling and basic information on consumer protection laws

Why?

Such information empowers people to get out of difficult situations and avoid them in the future

Two-thirds of workers with financial problems can improve their financial situations with professional help within about 12 months, and begin to save for retirement

Yet, fewer than 1/5 of large employers are offering financial education that includes emphasis on personal budgeting and credit management

The Best Employers Will Meet and Succeed

at Two Challenges:

1. Move from offering workers an average financial education

program to providing a model program

2. Partner with other organizations thatare currently helping people

resolve money problems

Employers Should Know That

It is not necessary for employers to get into the credit counseling business

Well-qualified, non-profit national providers of information on effective management of money and credit exist

Other experts can help workers avoid consumer rip-offs and frauds

#1 Finding Money for RetirementAfter receiving comprehensive financial education, a typical 45-year old married dual-earner couple with a family can find over $4000 a year to fund their retirement plans:

$300 a month by wisely choosing among employer-furnished fringe benefits

$80 a month by gaining control of consumer credit and managing money more effectively

$10 a month by avoiding consumer rip-offs and frauds

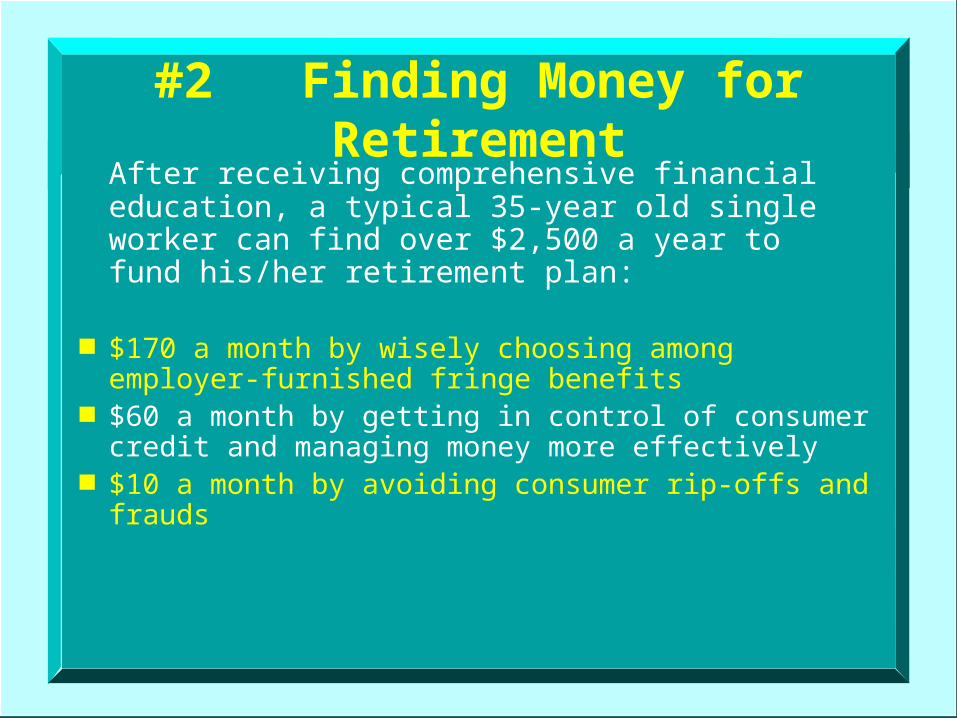

#2 Finding Money for RetirementAfter receiving comprehensive financial education, a typical 35-year old single worker can find over $2,500 a year to fund his/her retirement plan:

$170 a month by wisely choosing among employer-furnished fringe benefits

$60 a month by getting in control of consumer credit and managing money more effectively

$10 a month by avoiding consumer rip-offs and frauds

Results of Implementing a Comprehensive Financial

Education Program

Retirement education helps workers save for their retirements

Comprehensive financial education works even better!

Employers Reap the Benefits

Very high participation rates in 401(k) plans (90+ percent range)

Reduced net cost of operations

Workers Gain Benefits, Too Increased financial wellness Lower household debt-to-income ratio Increased self-esteem and improved attitude

about work Increased satisfaction with employer-provided

fringe benefits Increased capability to participate in and

contribute to retirement plans Increased saving for retirement

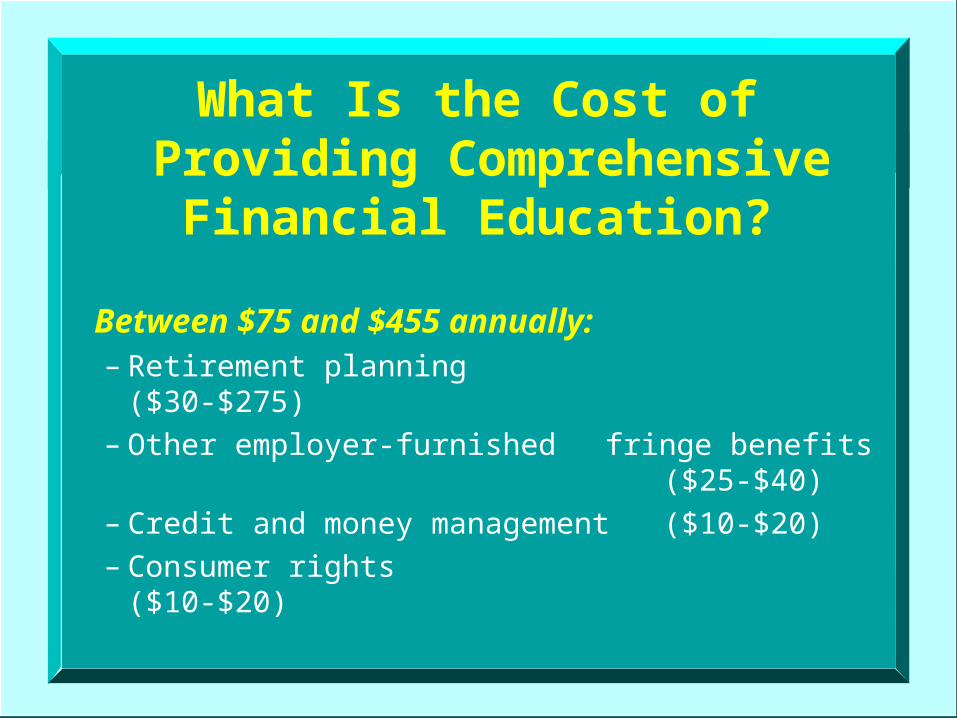

What Is the Cost of Providing Comprehensive

Financial Education?

Between $75 and $455 annually:– Retirement planning ($30-$275)– Other employer-furnished

fringe benefits ($25-$40)– Credit and money management ($10-$20)– Consumer rights ($10-$20)

Return on Investment for Comprehensive

Financial Education

Research shows that it ranges from 3:1 to 10:1, depending upon a number of factors

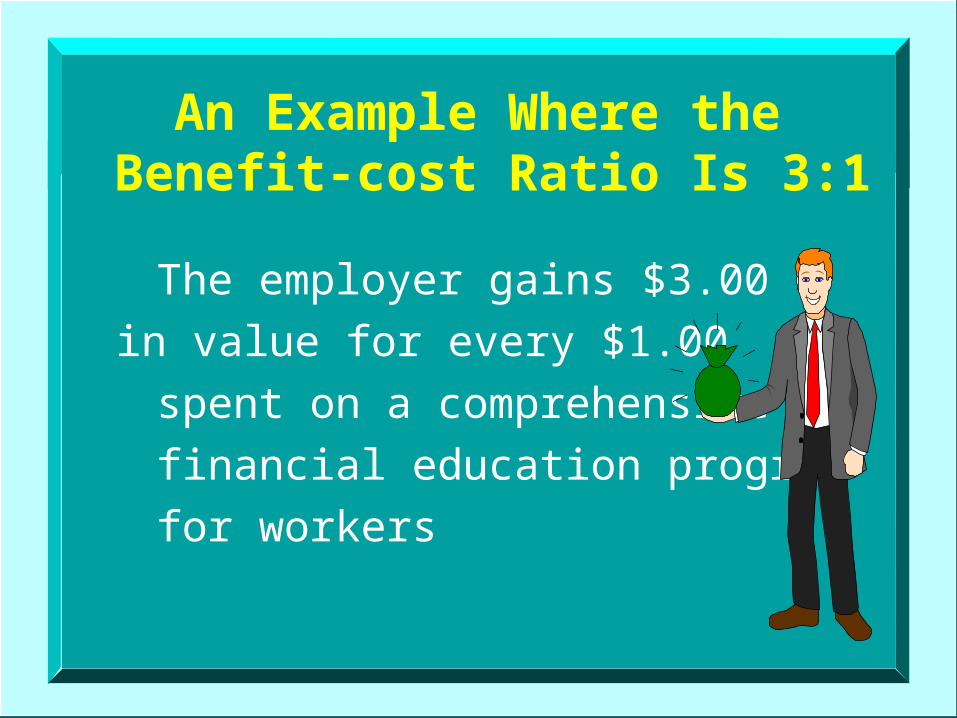

An Example Where the Benefit-cost Ratio Is 3:1

The employer gains $3.00

in value for every $1.00

spent on a comprehensive

financial education program

for workers

Situation:- 1,000 workers. Average salary of $40,000

- 60% participation rate in the 401(k) plan

- 20% participation rate in the pre-tax health and dependent care programs

- 15% experience personal financial difficulties to the extent that it negatively affects their job productivity

- $200,000 (or $200 per worker) invested in a comprehensive financial education program

1. $125,000 - increased job productivity

from 100 workers who resolved money problems 2/3 of workers who formerly had money problems (150 workers x 2/3 = 100) improved their situations and job productivity by 15 minutes per day 15 minutes = 3.13% of one workday

x $40,000 salary = $125.20 savings per worker x 100 workers

Results:

2.$80,000 - Reduced absenteeism from the same 100 workers who no

longer take time off work to attend to personal financial matters

2/3 of workers who formerly had personal money problems (n=100)

now do not take 5 days off each year

to attend to money matters $800 a week x 100 workers

3. $12,000 - Reduced administrative

time to process wage garnishments,

requests for payroll advances,

and 401(k) loans for the same 100

workers who formerly had personal

money problems - $120 x100

workers

Important!

The entire $200,000 cost of the financial education program already has been returned to the employer based solely upon the gains from the 100 workers who resolved their personal money problems

In fact, the employer is already $17,200 ahead!

4. Increased job productivity from 200 workers who formerly did not participate in the employer’s retirement plan and now do contribute

5. Increased job productivity from 150 workers who increased their contributions to retirement plans

6. Increased job productivity from the majority of the remaining workers - 400 of 650 - who participated in the financial education program

7. Reduced social security payroll taxes on employers because 500 more employees utilize pre-tax health and dependent care

8. Reduced stress-related illnesses from alcohol and other substances

9. Reduced premiums for health care

10. Fewer accidents

11. Improved use of and satisfaction with fringe benefits

12. Reduced human resource administrative costs

13. Reduced turnover

14. Reduced pressure to increase salaries

15. Increased morale

16. Increased acceleration of employee retirements

17. Reduced exposure to future litigation

A Positive Return on Dollars Invested in Comprehensive

Financial Education This illustrative 3:1 ratio is calculated by

dividing the $651,050 in benefits by the $200,000 cost of the financial education program ($651,050/$200,000)

Note that comprehensive financial education is less expensive and more effective than the alternative of offering workers a 3% match

What Is Virginia Tech’s Personal Finance

Employee Education Effort?

The mission of the PFEE outreach effort is to host national conferences that demonstrate model financial education programs which motivate and enable workers to overcome obstacles to fully fund their retirement plans.

At the time of this speech, Garman was Professor and Fellow, Center for Organizational and Technological Advancement, and Director of the National Institute for Personal Finance Employee Education, Virginia Tech, Blacksburg, VA 24061. Garman retired in 2000 as Professor Emeritus at Virginia Tech. E. Thomas Garman, Distinguished Scholar and Director of Educational Services, InCharge Institute of America, 1768 Park Center Drive, Suite 400, Orlando, FL 32835; E-mail: [email protected]; Phone: 407-532-5883; Fax: 407-532-5750; Web: InCharge.org