Embed Size (px)

Citation preview

The Black-Scholes Modelfor Option Pricing - 2

-Mahantesh Halappanavar

-Meeting-3, 09-11-2007

The Black-Scholes Model: Basics

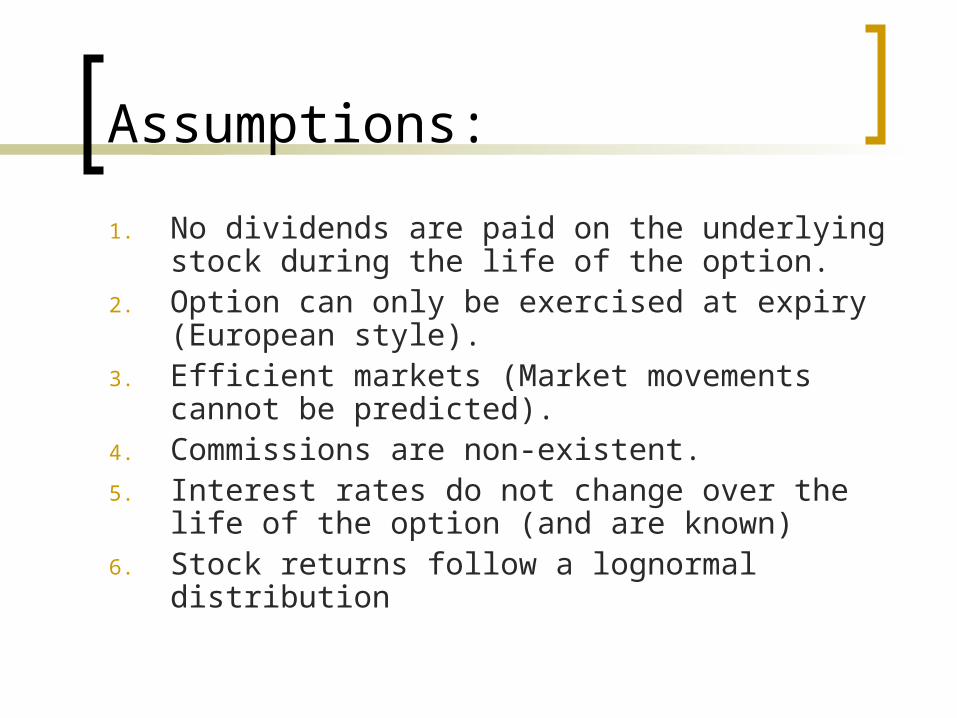

Assumptions:

1. No dividends are paid on the underlying stock during the life of the option.

2. Option can only be exercised at expiry (European style).

3. Efficient markets (Market movements cannot be predicted).

4. Commissions are non-existent.5. Interest rates do not change over the life of the

option (and are known)6. Stock returns follow a lognormal distribution

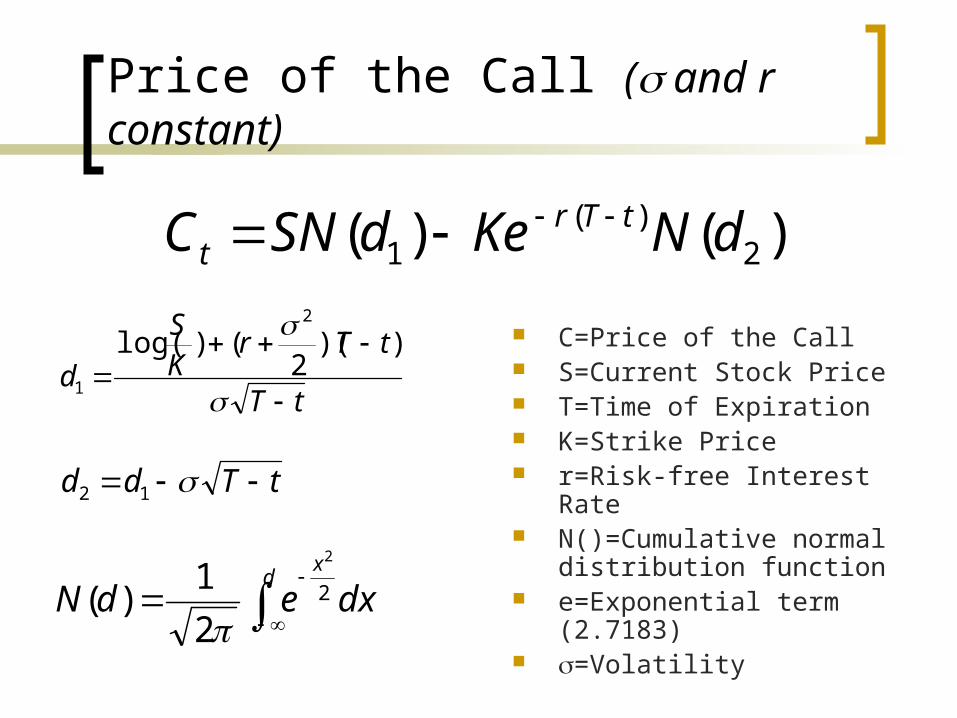

Price of the Call ( and r constant)

C=Price of the Call S=Current Stock Price T=Time of Expiration K=Strike Price r=Risk-free Interest Rate N()=Cumulative normal

distribution function e=Exponential term (2.7183) =Volatility

tT

tTrKS

d

))(

2()log(

2

1

tTdd 12

)()( 2)(

1 dNKedSNC tTrt

dxedNd

x

2

2

2

1)(

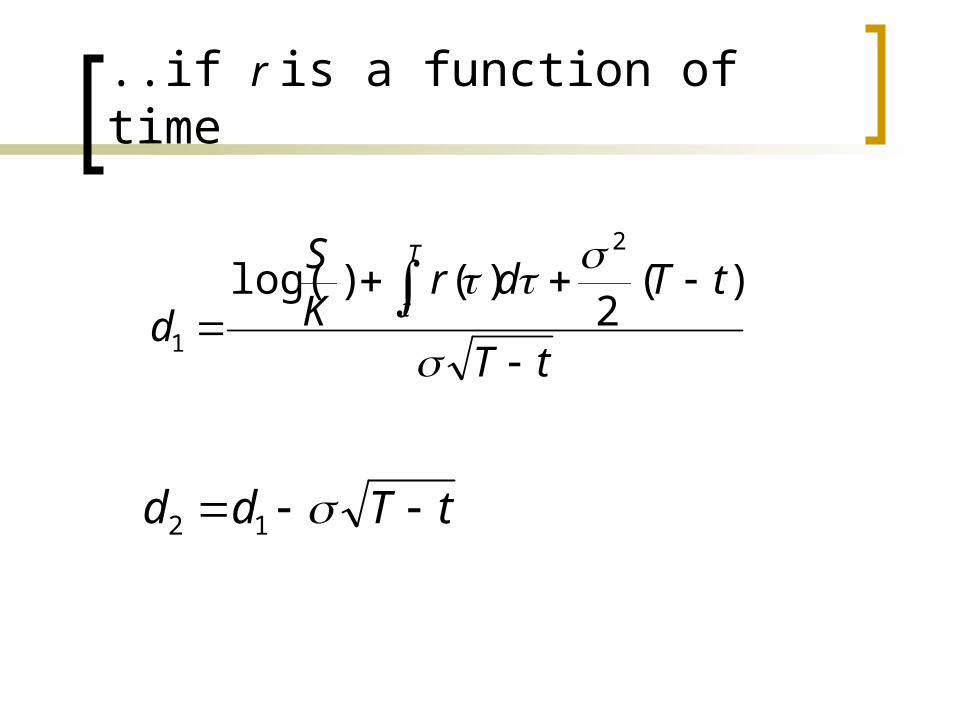

..if r is a function of time

tT

tTdrKS

d

T

t

)(2

)()log(2

1

tTdd 12

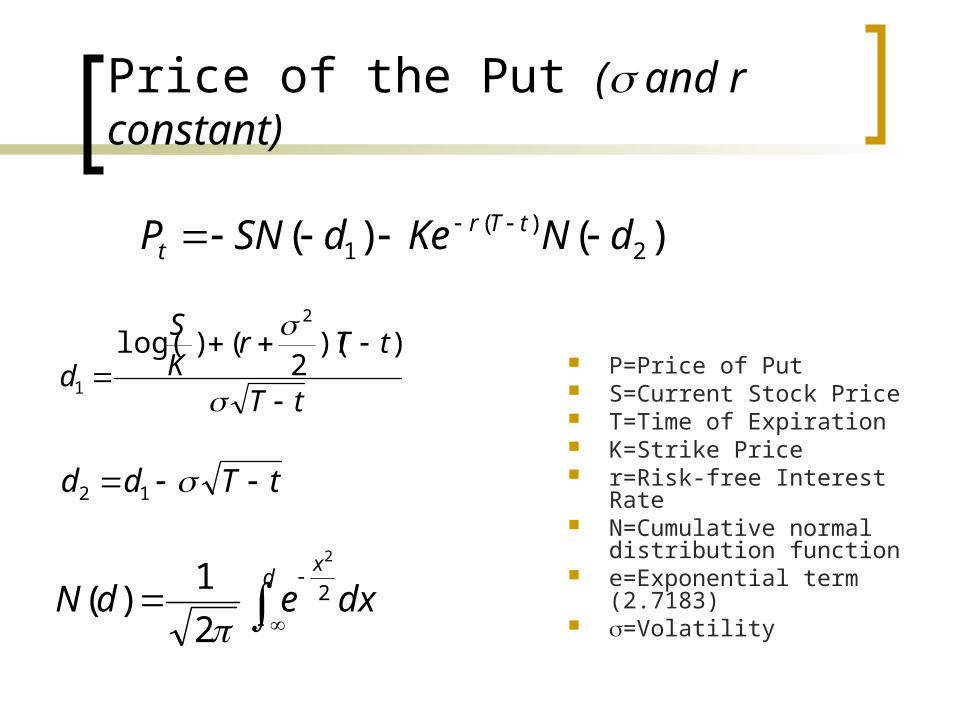

Price of the Put ( and r constant)

P=Price of Put S=Current Stock Price T=Time of Expiration K=Strike Price r=Risk-free Interest Rate N=Cumulative normal

distribution function e=Exponential term

(2.7183) =Volatility

tT

tTrKS

d

))(

2()log(

2

1

tTdd 12

)()( 2)(

1 dNKedSNP tTrt

dxedNd

x

2

2

2

1)(

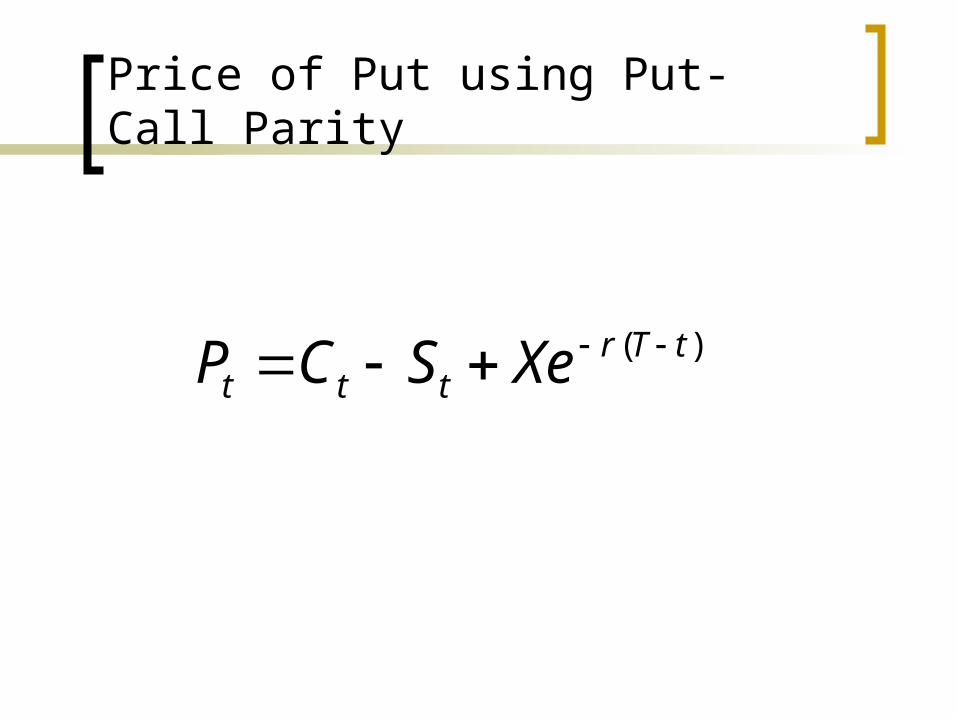

Price of Put using Put-Call Parity

)( tTrttt XeSCP

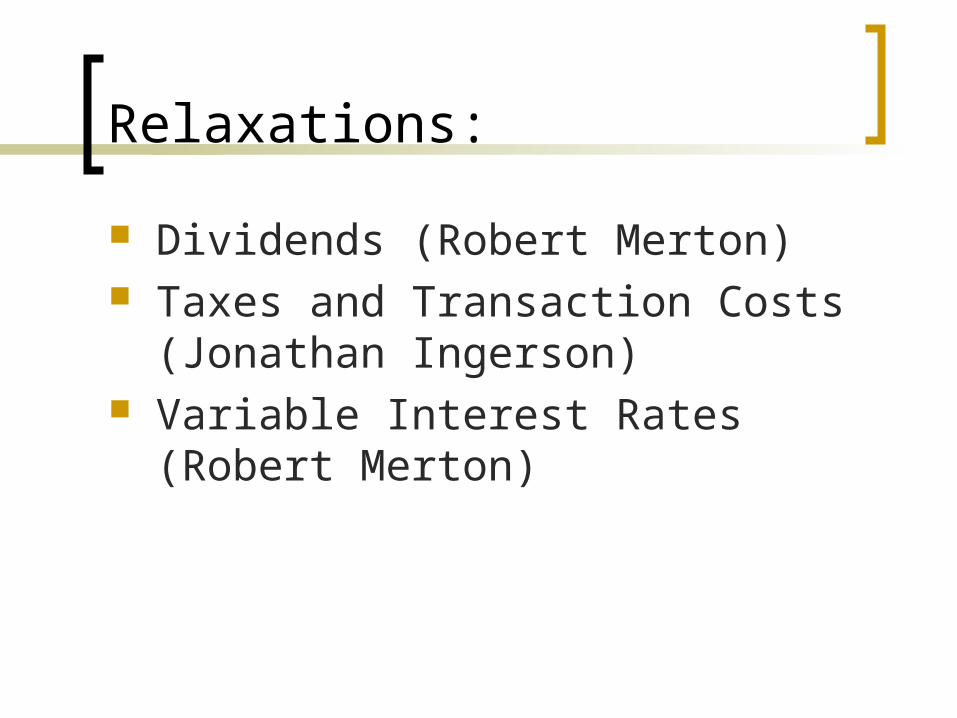

Relaxations:

Dividends (Robert Merton) Taxes and Transaction Costs

(Jonathan Ingerson) Variable Interest Rates (Robert

Merton)

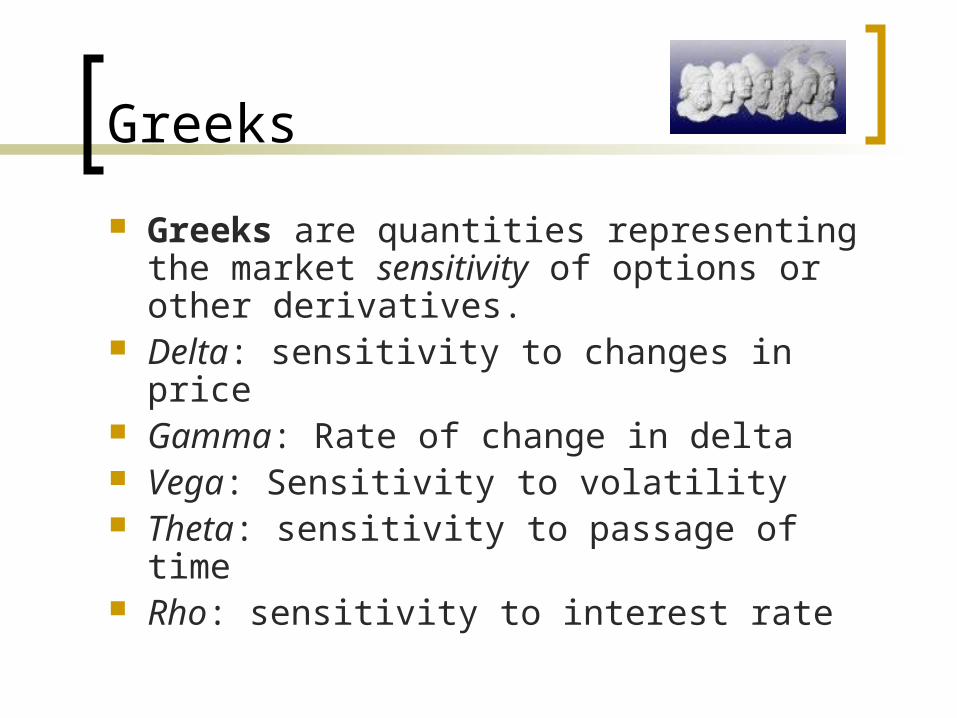

Greeks

Greeks are quantities representing the market sensitivity of options or other derivatives.

Delta: sensitivity to changes in price Gamma: Rate of change in delta Vega: Sensitivity to volatility Theta: sensitivity to passage of time Rho: sensitivity to interest rate

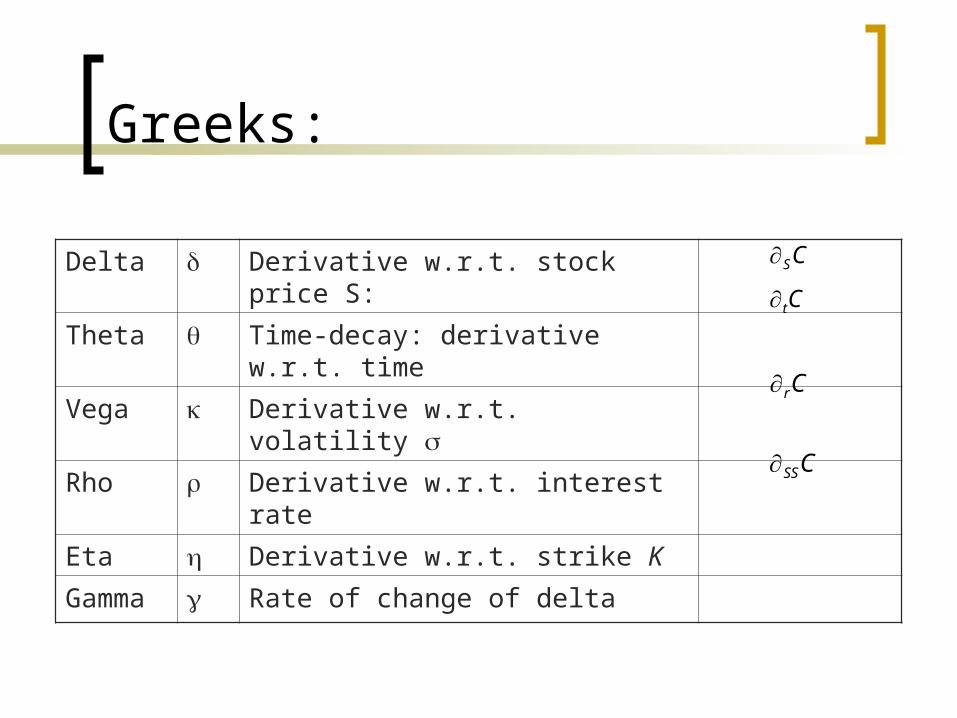

Greeks:

Delta Derivative w.r.t. stock price S:

Theta Time-decay: derivative w.r.t. time

Vega Derivative w.r.t. volatility

Rho Derivative w.r.t. interest rate

Eta Derivative w.r.t. strike K

Gamma Rate of change of delta

CS

Cr

Ct

CSS

Barrier Options:

A barrier option with payoff Qo and maturity T is a contract which yields a payoff Qo(ST) at maturity T, as long as the spot price St remains in the interval (a(t),b(t)) for all time t[0,T].

Monte-Carlo Methods

Observation:

“Because of the difficulty in solving PDEs, numerous methods exist to

solve them, including Backlund Transformations, Green’s Function,

Integral Transformation, or numerical methods such as finite difference

methods.”

-www.global-derivatives.com

Orientation:

A technique of employing statistical sampling to approximate solutions to quantitative problems.

Stochastic (nondeterministic) using pseudo-random numbers.

“When number of dimensions (degrees of freedom) in the problem is lerge, PDE’s and numerical integrals become intractable: Monte Carlo methods often give better results”

“MC methods converge to the solutions more quickly than numerical integration methods, require less memory and are easier to program”

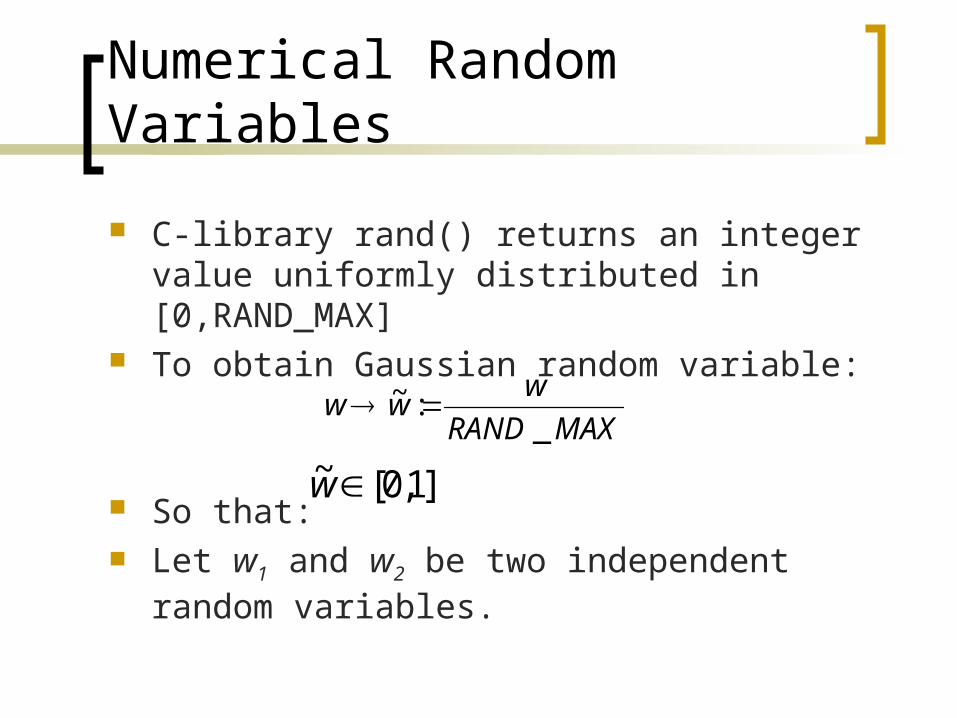

Numerical Random Variables

C-library rand() returns an integer value uniformly distributed in [0,RAND_MAX]

To obtain Gaussian random variable:

So that: Let w1 and w2 be two independent random

variables.

MAXRAND

www

_:~

]1,0[~w

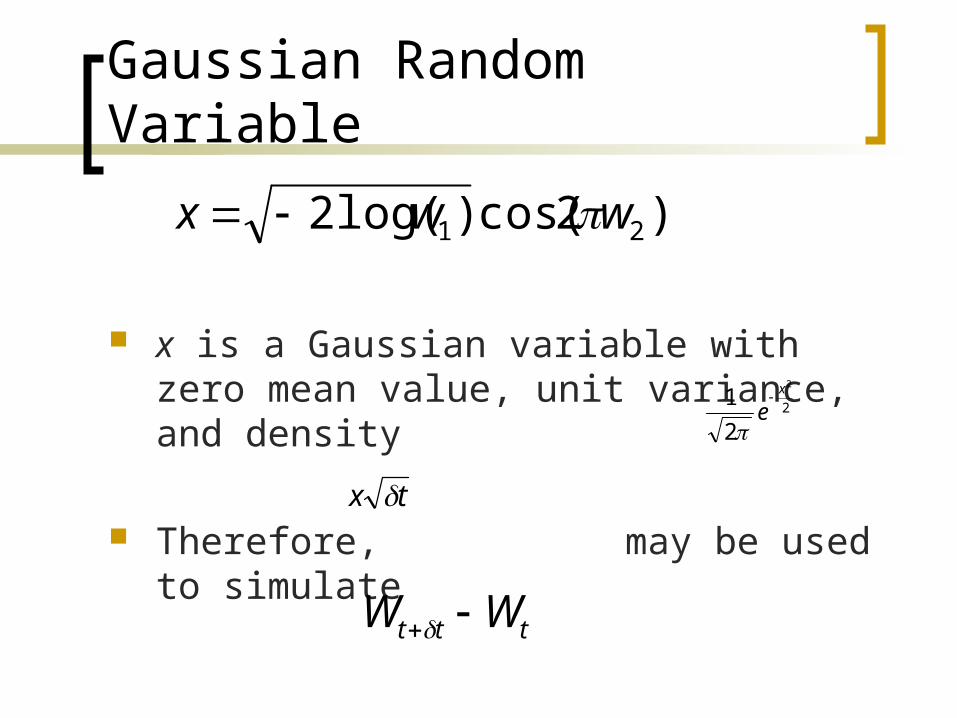

Gaussian Random Variable

x is a Gaussian variable with zero mean value, unit variance, and density

Therefore, may be used to simulate

2

2

2

1 x

e

tx

ttt WW

)2cos()log(2 21 wwx

C++ Code:

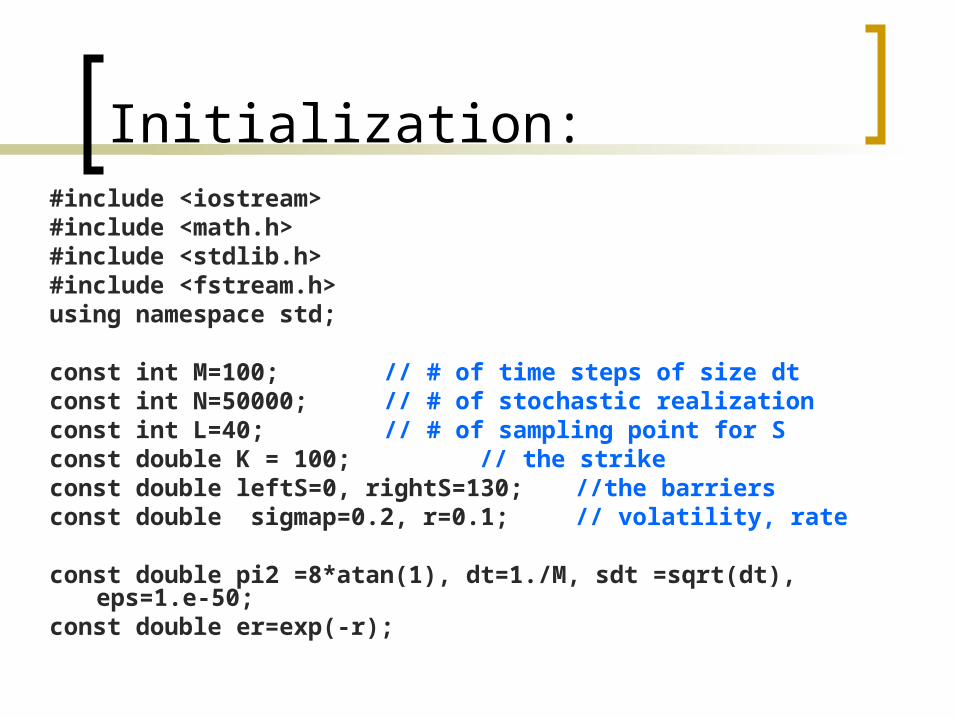

Initialization:#include <iostream>#include <math.h>#include <stdlib.h>#include <fstream.h>using namespace std;

const int M=100; // # of time steps of size dtconst int N=50000; // # of stochastic realizationconst int L=40; // # of sampling point for Sconst double K = 100; // the strikeconst double leftS=0, rightS=130; //the barriersconst double sigmap=0.2, r=0.1; // volatility, rate

const double pi2 =8*atan(1), dt=1./M, sdt =sqrt(dt), eps=1.e-50;

const double er=exp(-r);

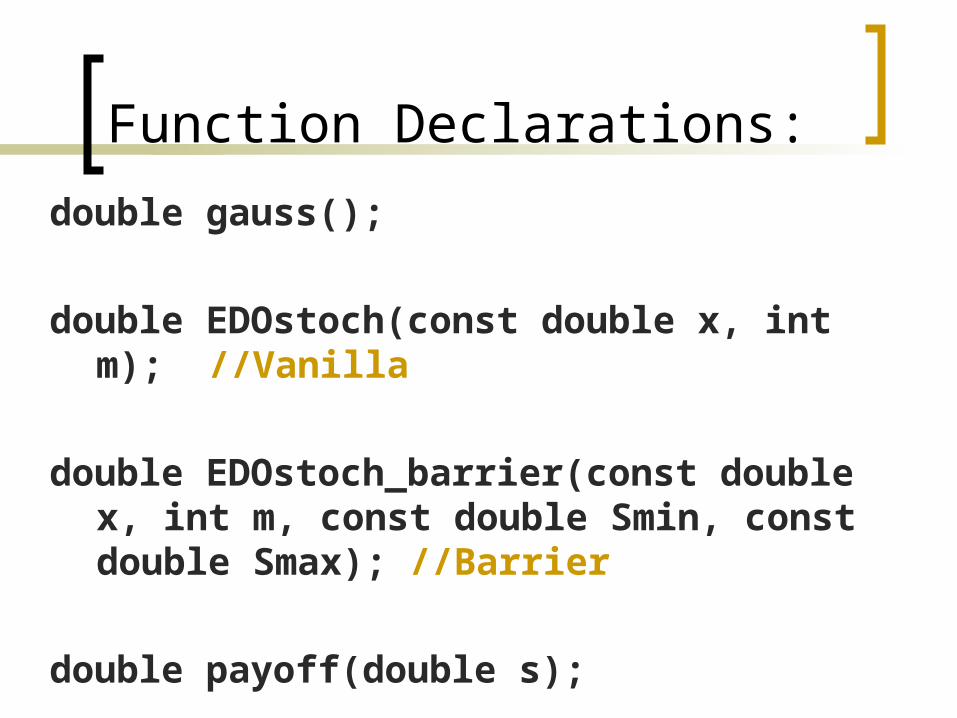

Function Declarations:

double gauss();

double EDOstoch(const double x, int m); //Vanilla

double EDOstoch_barrier(const double x, int m, const double Smin, const double Smax); //Barrier

double payoff(double s);

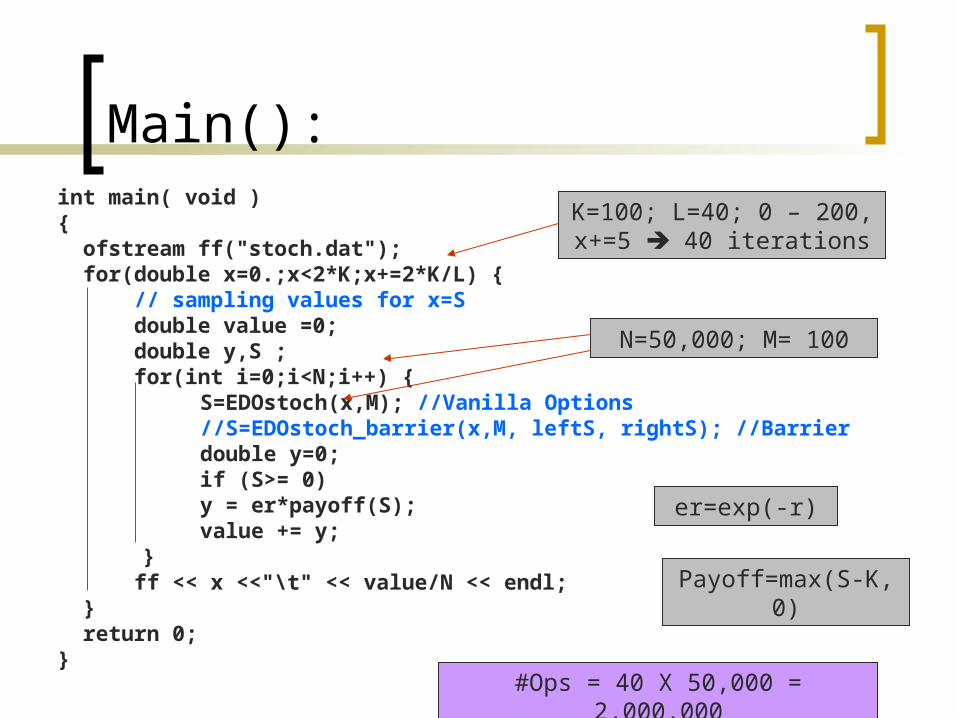

Main():int main( void ){ ofstream ff("stoch.dat"); for(double x=0.;x<2*K;x+=2*K/L) { // sampling values for x=S double value =0; double y,S ; for(int i=0;i<N;i++) { S=EDOstoch(x,M); //Vanilla Options

//S=EDOstoch_barrier(x,M, leftS, rightS); //Barrier double y=0; if (S>= 0) y = er*payoff(S); value += y; }

ff << x <<"\t" << value/N << endl; } return 0;}

K=100; L=40; 0 – 200, x+=5 40 iterations

N=50,000; M= 100

er=exp(-r)

Payoff=max(S-K, 0)

#Ops = 40 X 50,000 = 2,000,000

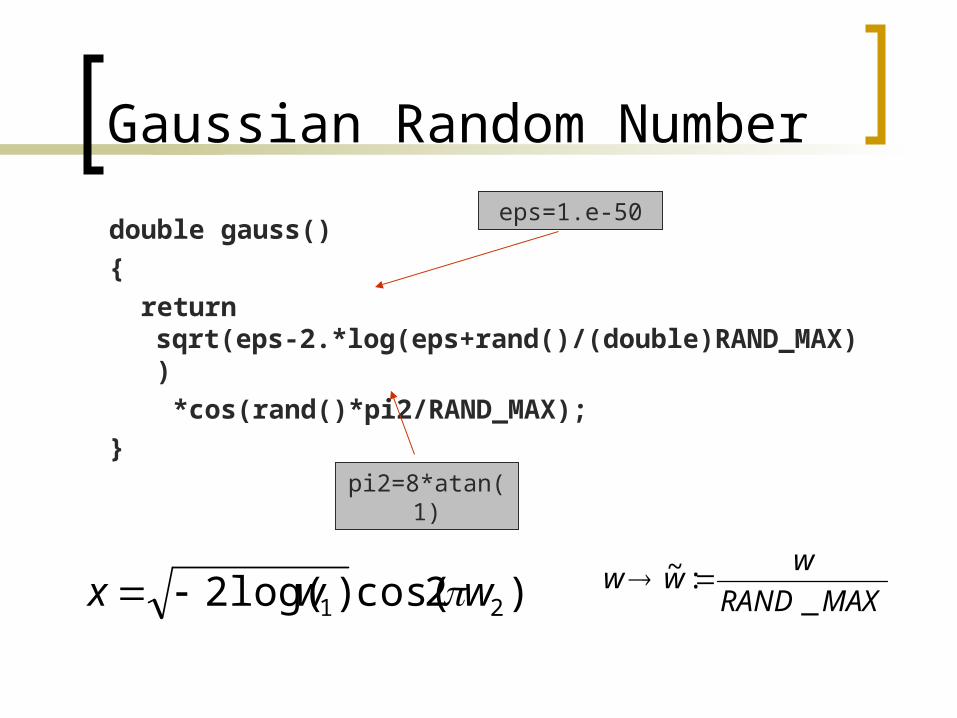

Gaussian Random Number

double gauss()

{

return sqrt(eps-2.*log(eps+rand()/(double)RAND_MAX))

*cos(rand()*pi2/RAND_MAX);

}

MAXRAND

www

_:~ )2cos()log(2 21 wwx

eps=1.e-50

pi2=8*atan(1)

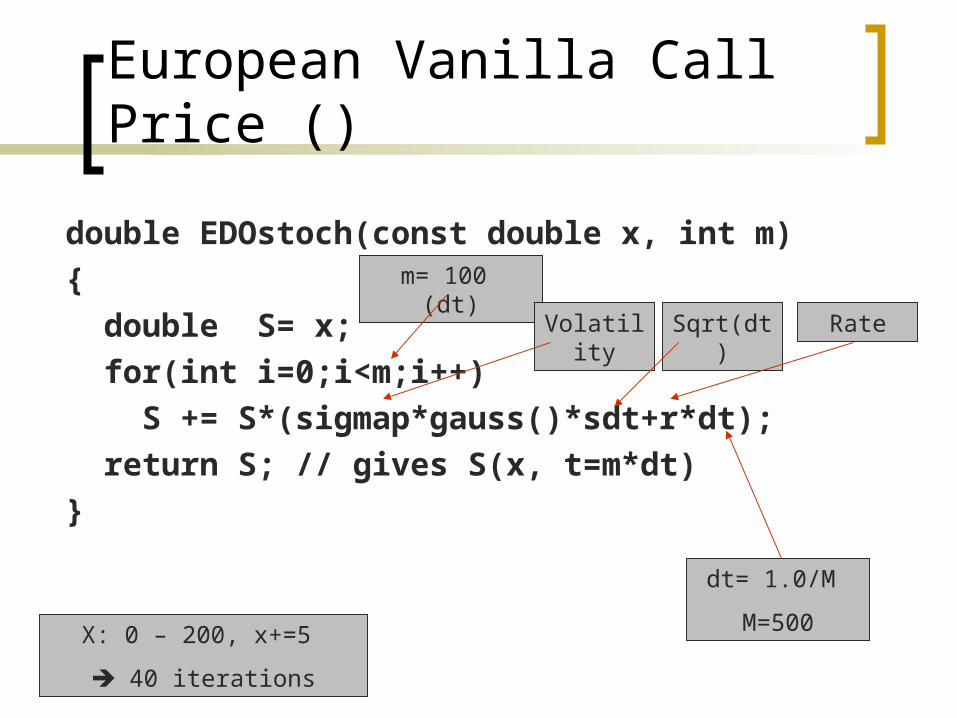

European Vanilla Call Price ()

double EDOstoch(const double x, int m)

{

double S= x;

for(int i=0;i<m;i++)

S += S*(sigmap*gauss()*sdt+r*dt);

return S; // gives S(x, t=m*dt)

}

X: 0 – 200, x+=5

40 iterations

m= 100 (dt)

Volatility RateSqrt(dt)

dt= 1.0/M

M=500

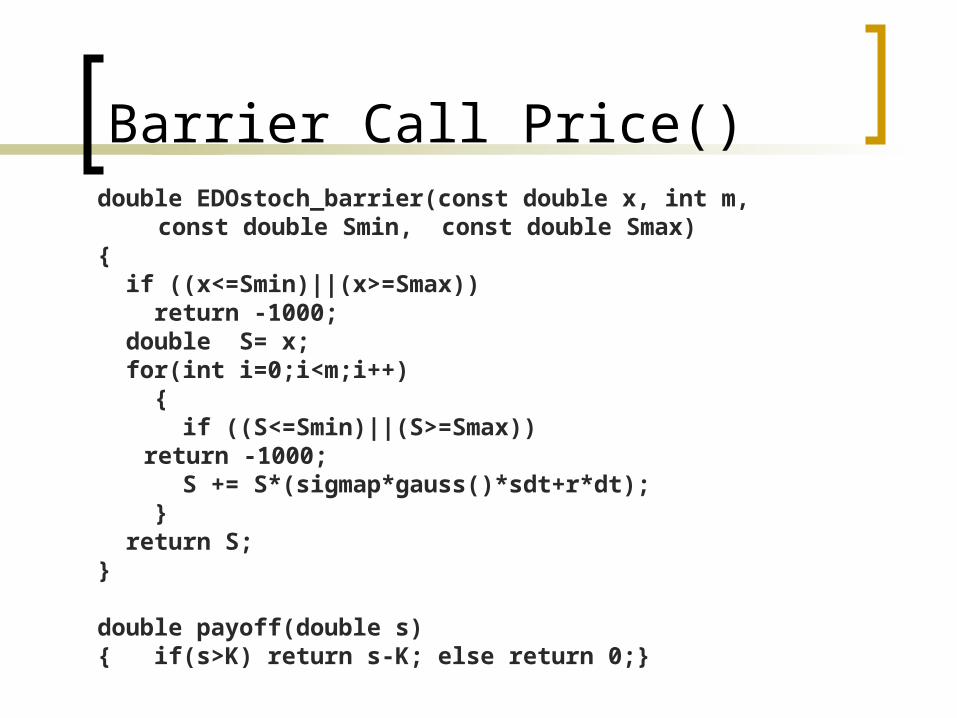

Barrier Call Price()double EDOstoch_barrier(const double x, int m,

const double Smin, const double Smax)

{ if ((x<=Smin)||(x>=Smax)) return -1000; double S= x; for(int i=0;i<m;i++) { if ((S<=Smin)||(S>=Smax))

return -1000; S += S*(sigmap*gauss()*sdt+r*dt); } return S; }

double payoff(double s){ if(s>K) return s-K; else return 0;}

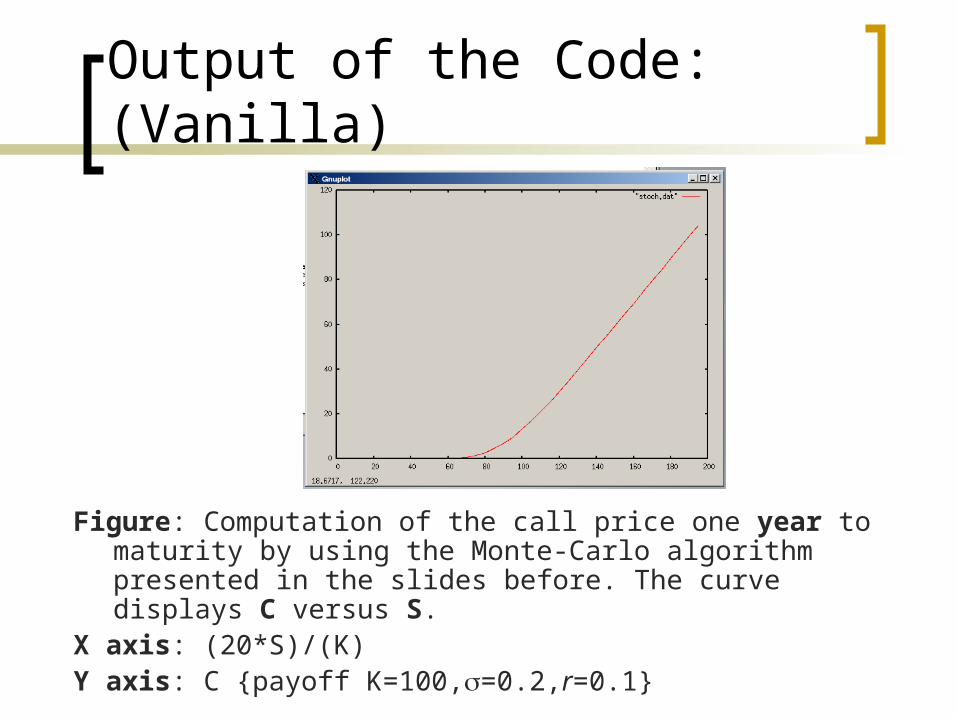

Output of the Code: (Vanilla)

Figure: Computation of the call price one year to maturity by using the Monte-Carlo algorithm presented in the slides before. The curve displays C versus S.

X axis: (20*S)/(K)Y axis: C {payoff K=100,=0.2,r=0.1}

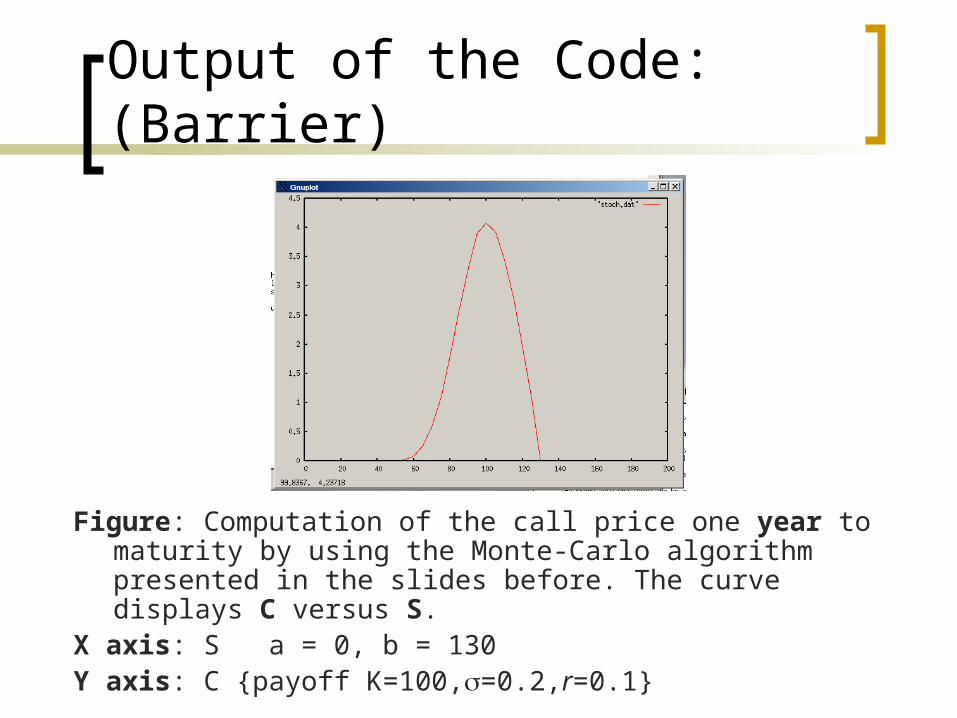

Output of the Code: (Barrier)

Figure: Computation of the call price one year to maturity by using the Monte-Carlo algorithm presented in the slides before. The curve displays C versus S.

X axis: S a = 0, b = 130Y axis: C {payoff K=100,=0.2,r=0.1}

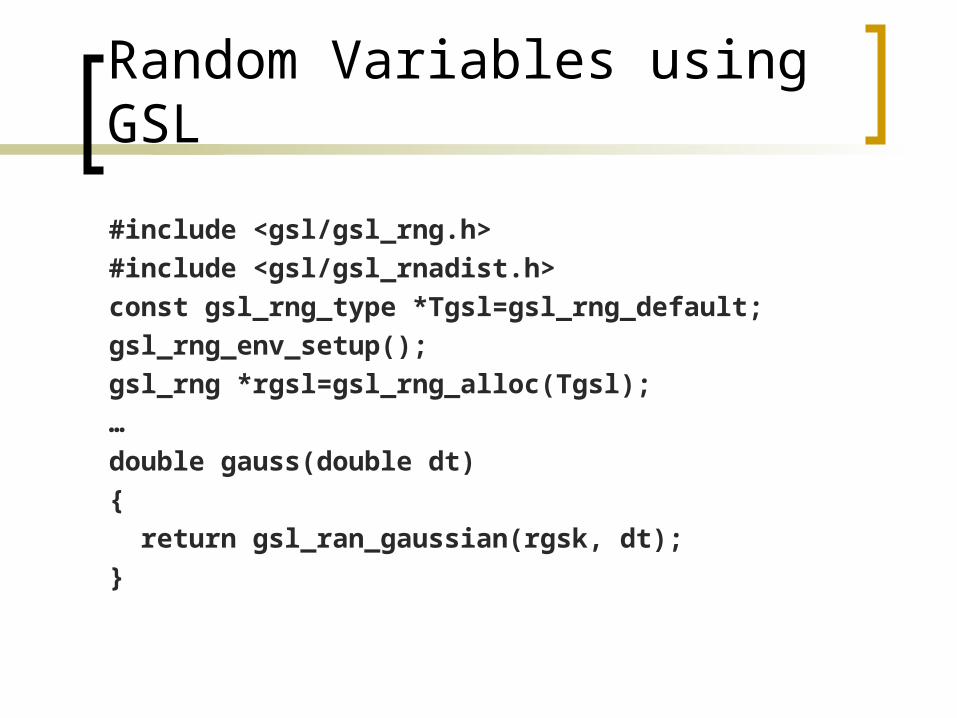

Random Variables using GSL

#include <gsl/gsl_rng.h>

#include <gsl/gsl_rnadist.h>

const gsl_rng_type *Tgsl=gsl_rng_default;

gsl_rng_env_setup();

gsl_rng *rgsl=gsl_rng_alloc(Tgsl);

…

double gauss(double dt)

{

return gsl_ran_gaussian(rgsk, dt);

}

Central Limit Theorem

… to come

Variance Reduction

…to come