Embed Size (px)

Citation preview

The Biotech Ecosystem - Whatabout Switzerland?

Thomas Heimann

Life Science Forum Basel, June 23rd 2011

Page 2© SECA Team

Thursday, 23 June 2011

Switzerland – The unique Life Sciences Country

With Basel in the heart…

"Working together with international people in a local area is so easy - you just take the

bus or the tram for the meeting without being jet-lagged."

Dr. Jean-Paul Clozel (CEO Actelion), Keynote Speaker 2009.

Source: Actelion Presentation 2006

Page 3© SECA Team

Thursday, 23 June 2011

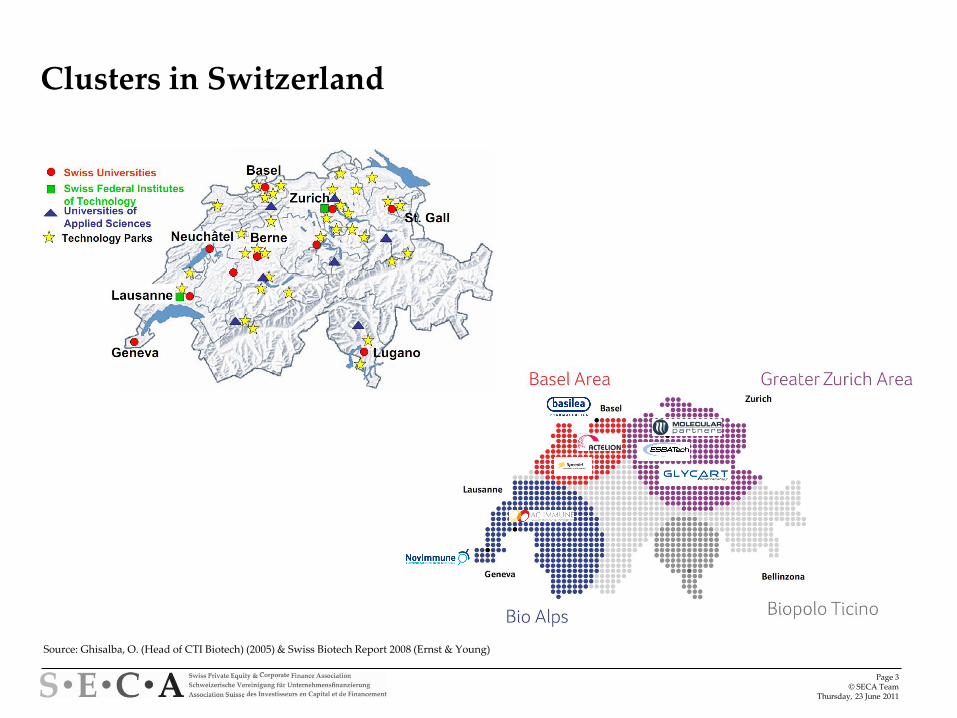

Clusters in Switzerland

Source: Ghisalba, O. (Head of CTI Biotech) (2005) & Swiss Biotech Report 2008 (Ernst & Young)

Page 4© SECA Team

Thursday, 23 June 2011

What makes Switzerland unique?

Switzerland - One of the most regarded Life Sciences areas worldwide!

Knowledge-based industry with the very latest technology

Highly qualified staff

Well-established network among industry, investors and universities

Well-known for universities and their spin-off‘s

4 geographical clusters linked by a high density of formal and informal networks

SIX Swiss Exchange- Europe‘s leading stock exchange for the Life Sciences Industry

Experienced and well funded investors concentrated in a small number of locations

High standard of living

Favourable tax situation

Page 5© SECA Team

Thursday, 23 June 2011

Agenda

Topics along the way…

Introduction

Switzerland: Facts & Figures

From invention to market: What you need to know?

Switzerland: Performance of the Life Sciences Industry & Success Stories

Challenges & Outlook

Page 6© SECA Team

Thursday, 23 June 2011

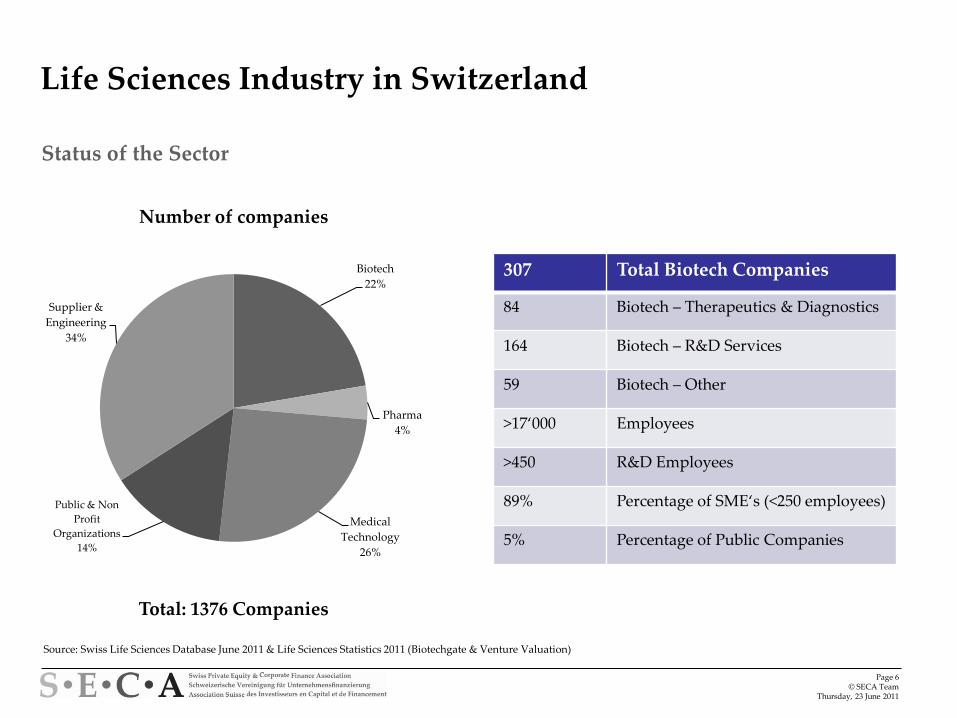

Life Sciences Industry in Switzerland

Status of the Sector

Biotech

22%

Pharma

4%

Medical

Technology

26%

Public & Non

Profit

Organizations

14%

Supplier &

Engineering

34%

Number of companies

Total: 1376 Companies

307 Total Biotech Companies

84 Biotech – Therapeutics & Diagnostics

164 Biotech – R&D Services

59 Biotech – Other

>17‘000 Employees

>450 R&D Employees

89% Percentage of SME‘s (<250 employees)

5% Percentage of Public Companies

Source: Swiss Life Sciences Database June 2011 & Life Sciences Statistics 2011 (Biotechgate & Venture Valuation)

Page 7© SECA Team

Thursday, 23 June 2011

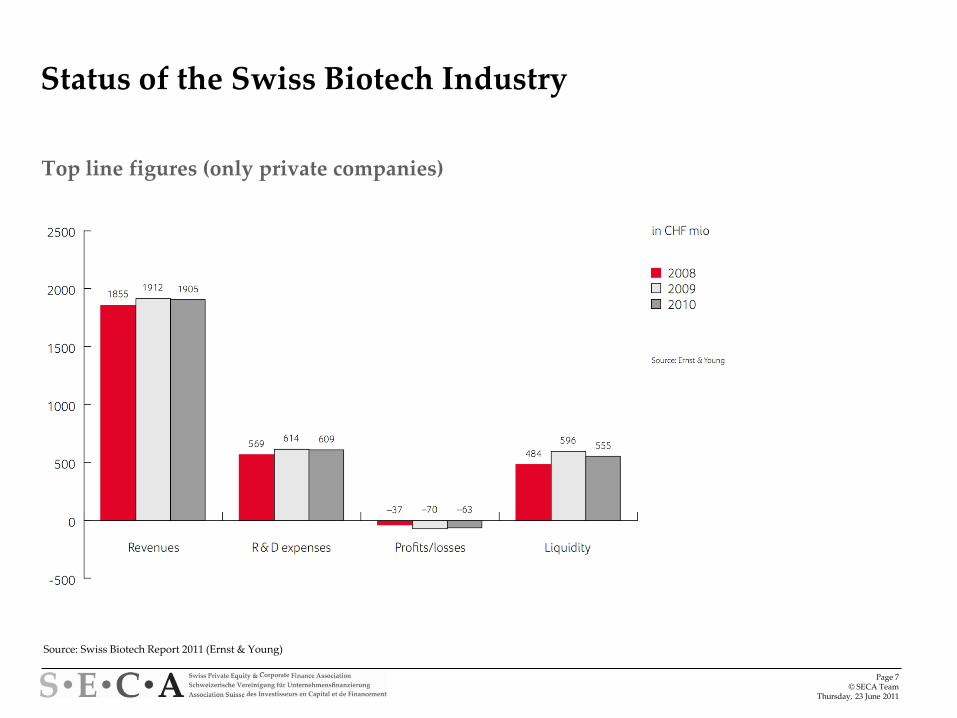

Status of the Swiss Biotech Industry

Source: Swiss Biotech Report 2011 (Ernst & Young)

Top line figures (only private companies)

Page 8© SECA Team

Thursday, 23 June 2011

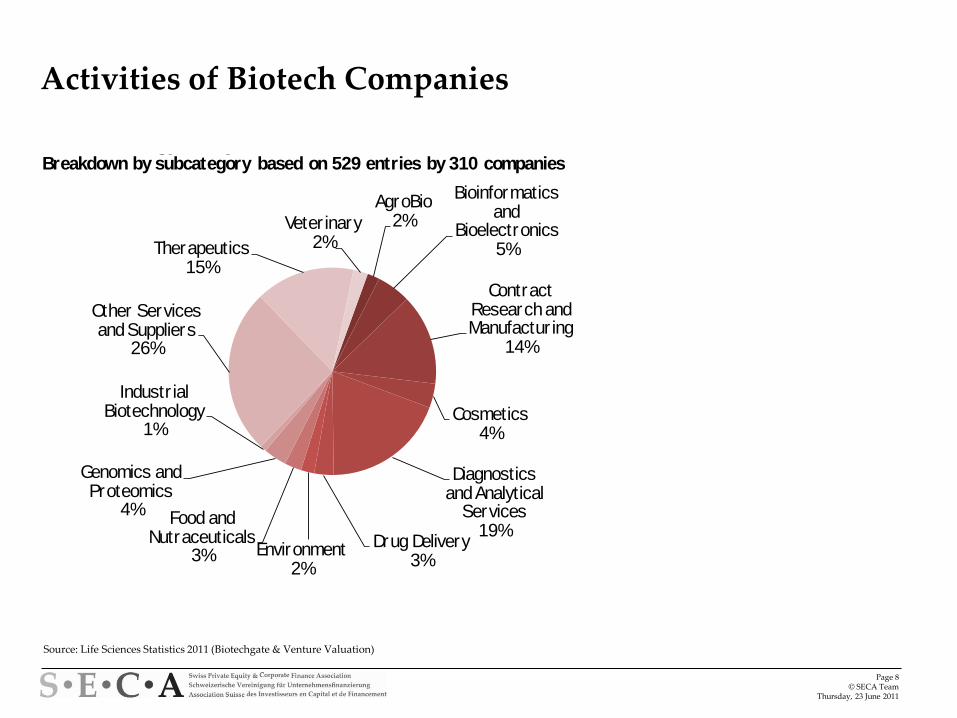

Activities of Biotech Companies

Source: Life Sciences Statistics 2011 (Biotechgate & Venture Valuation)

AgroBio 2%

Bioinformatics and

Bioelectronics 5%

Contract Research and Manufactur ing

14%

Cosmetics 4%

Diagnostics and Analytical

Services 19%

Drug Delivery 3%

Environment 2%

Food and Nutraceuticals

3%

Genomics and Proteomics

4%

Industr ial Biotechnology

1%

Other Services and Suppliers

26%

Therapeutics 15%

Veterinary 2%

Source: www.biotechgate.com

Biotechnology Companies in SwitzerlandBreakdown by subcategory based on 529 entries by 310 companies

Page 9© SECA Team

Thursday, 23 June 2011

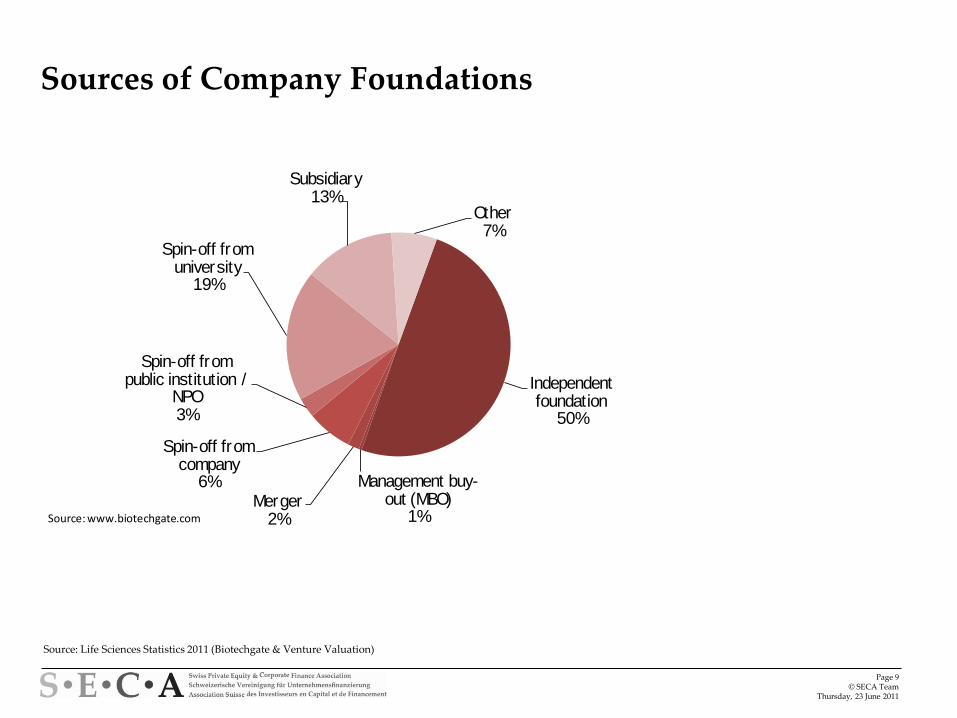

Sources of Company Foundations

Source: Life Sciences Statistics 2011 (Biotechgate & Venture Valuation)

Independent foundation

50%

Management buy-out (MBO)

1%Merger

2%

Spin-off from company

6%

Spin-off from public institution /

NPO 3%

Spin-off from university

19%

Subsidiary 13%

Other 7%

Company Foundations in Switzerland(by source of foundation)

Source: www.biotechgate.com

Page 10© SECA Team

Thursday, 23 June 2011

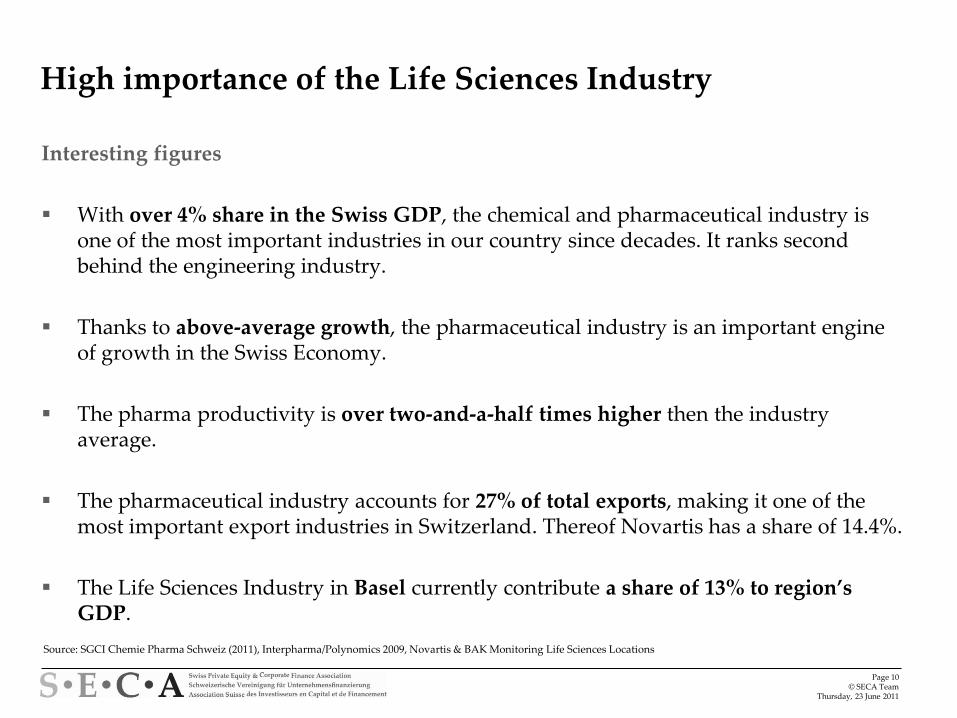

High importance of the Life Sciences Industry

Interesting figures

With over 4% share in the Swiss GDP, the chemical and pharmaceutical industry is one of the most important industries in our country since decades. It ranks second behind the engineering industry.

Thanks to above-average growth, the pharmaceutical industry is an important engine of growth in the Swiss Economy.

The pharma productivity is over two-and-a-half times higher then the industry average.

The pharmaceutical industry accounts for 27% of total exports, making it one of the most important export industries in Switzerland. Thereof Novartis has a share of 14.4%.

The Life Sciences Industry in Basel currently contribute a share of 13% to region’s GDP.

Source: SGCI Chemie Pharma Schweiz (2011), Interpharma/Polynomics 2009, Novartis & BAK Monitoring Life Sciences Locations

Page 11© SECA Team

Thursday, 23 June 2011

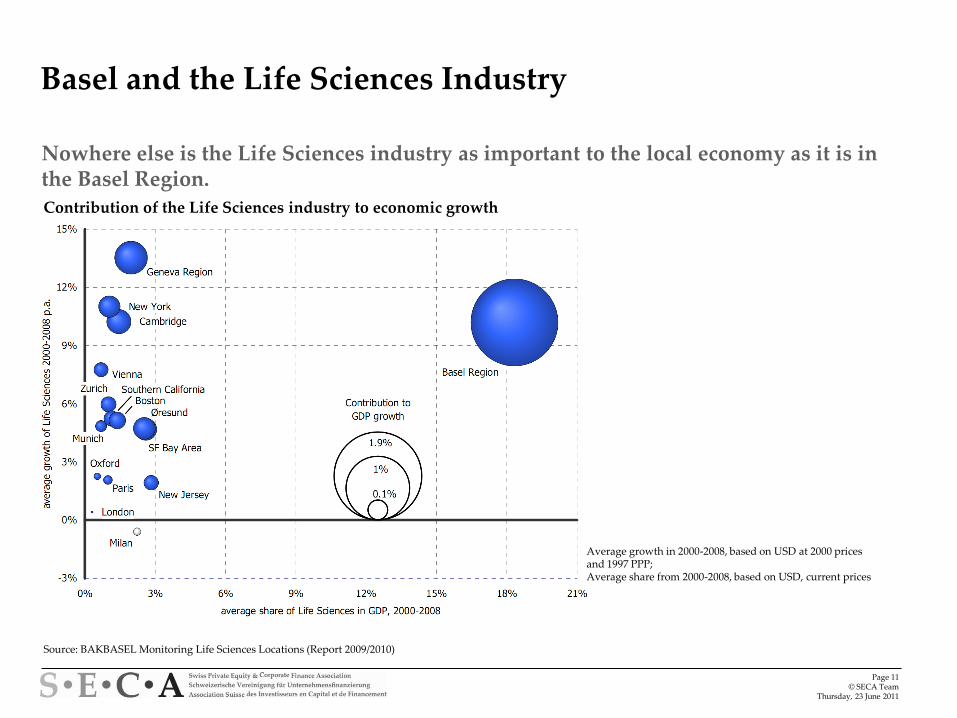

Basel and the Life Sciences Industry

Nowhere else is the Life Sciences industry as important to the local economy as it is in the Basel Region.

Source: BAKBASEL Monitoring Life Sciences Locations (Report 2009/2010)

Average growth in 2000-2008, based on USD at 2000 prices and 1997 PPP; Average share from 2000-2008, based on USD, current prices

Contribution of the Life Sciences industry to economic growth

Page 12© SECA Team

Thursday, 23 June 2011

Agenda

Topics along the way…

Introduction

Switzerland: Facts & Figures

From invention to market: What you need to know?

Switzerland: Performance of the Life Sciences Industry & Success Stories

Challenges & Outlook

Page 13© SECA Team

Thursday, 23 June 2011

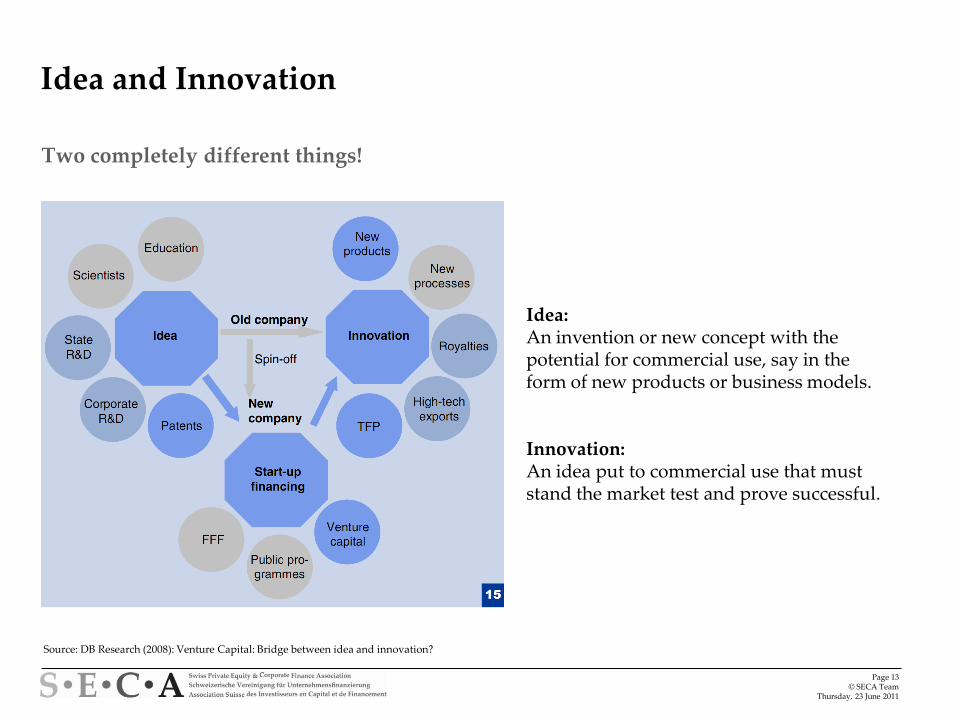

Idea and Innovation

Two completely different things!

Source: DB Research (2008): Venture Capital: Bridge between idea and innovation?

Idea:An invention or new concept with thepotential for commercial use, say in theform of new products or business models.

Innovation:An idea put to commercial use that muststand the market test and prove successful.

Page 14© SECA Team

Thursday, 23 June 2011

What is Venture Capital?

Seed

Start-up

Later-stage

venture

Growth

Restructuring/

turnaround

Replacement

capital

Buyout

Company

Maturity

Early-stage

Venture capital

Private equity

Source: EVCA

Page 15© SECA Team

Thursday, 23 June 2011

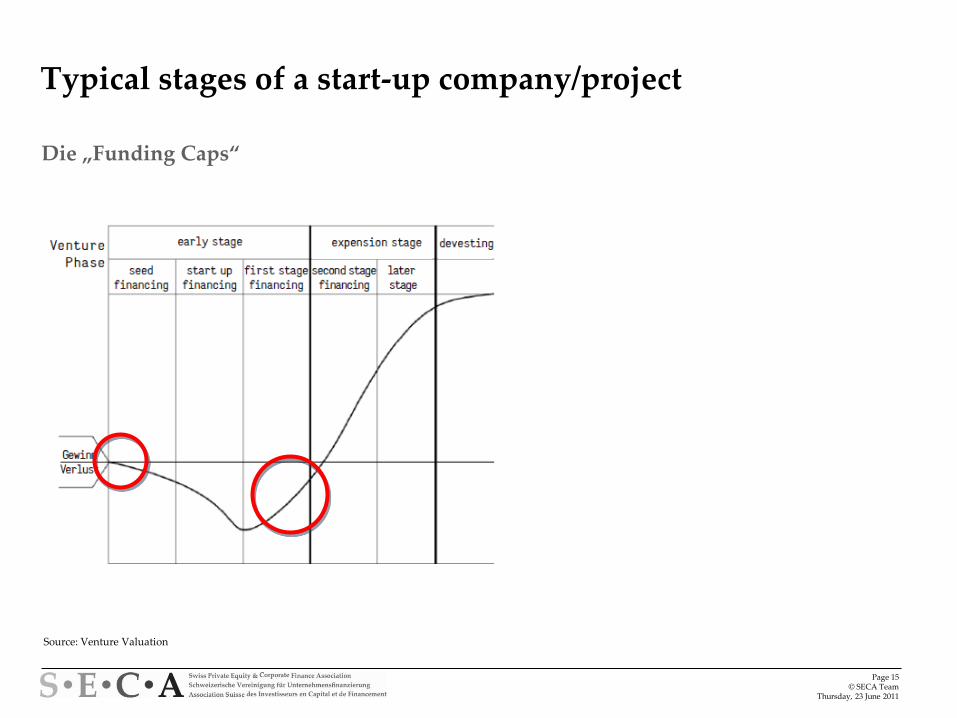

Typical stages of a start-up company/project

Die „Funding Caps‚

Source: Venture Valuation

Page 16© SECA Team

Thursday, 23 June 2011

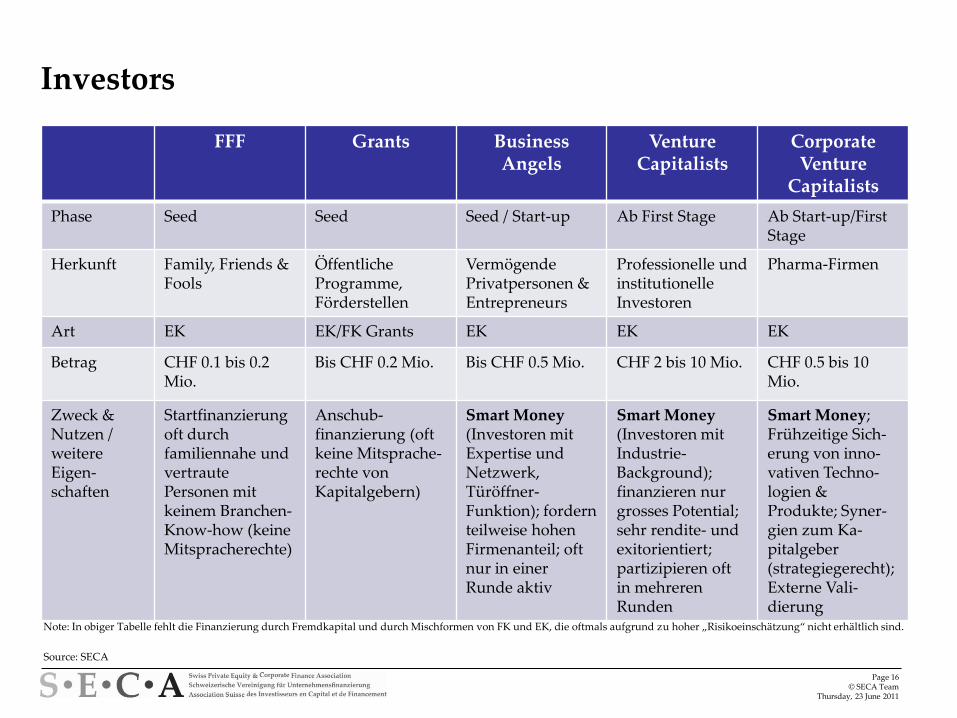

Investors

FFF Grants Business Angels

VentureCapitalists

Corporate Venture

Capitalists

Phase Seed Seed Seed / Start-up Ab First Stage Ab Start-up/FirstStage

Herkunft Family, Friends & Fools

ÖffentlicheProgramme, Förderstellen

VermögendePrivatpersonen & Entrepreneurs

Professionelle undinstitutionelle Investoren

Pharma-Firmen

Art EK EK/FK Grants EK EK EK

Betrag CHF 0.1 bis 0.2 Mio.

Bis CHF 0.2 Mio. Bis CHF 0.5 Mio. CHF 2 bis 10 Mio. CHF 0.5 bis 10 Mio.

Zweck & Nutzen / weitere Eigen-schaften

Startfinanzierung oft durchfamiliennahe und vertraute Personen mit keinem Branchen-Know-how (keine Mitspracherechte)

Anschub-finanzierung (oftkeine Mitsprache-rechte von Kapitalgebern)

Smart Money (Investoren mit Expertise und Netzwerk, Türöffner-Funktion); fordern teilweise hohen Firmenanteil; oft nur in einer Runde aktiv

Smart Money (Investoren mit Industrie-Background);finanzieren nur grosses Potential; sehr rendite- und exitorientiert; partizipieren oft in mehreren Runden

Smart Money; Frühzeitige Sich-erung von inno-vativen Techno-logien &Produkte; Syner-gien zum Ka-pitalgeber(strategiegerecht); Externe Vali-dierung

Source: SECA

Note: In obiger Tabelle fehlt die Finanzierung durch Fremdkapital und durch Mischformen von FK und EK, die oftmals aufgrund zu hoher „Risikoeinschätzung‚ nicht erhältlich sind.

Page 17© SECA Team

Thursday, 23 June 2011

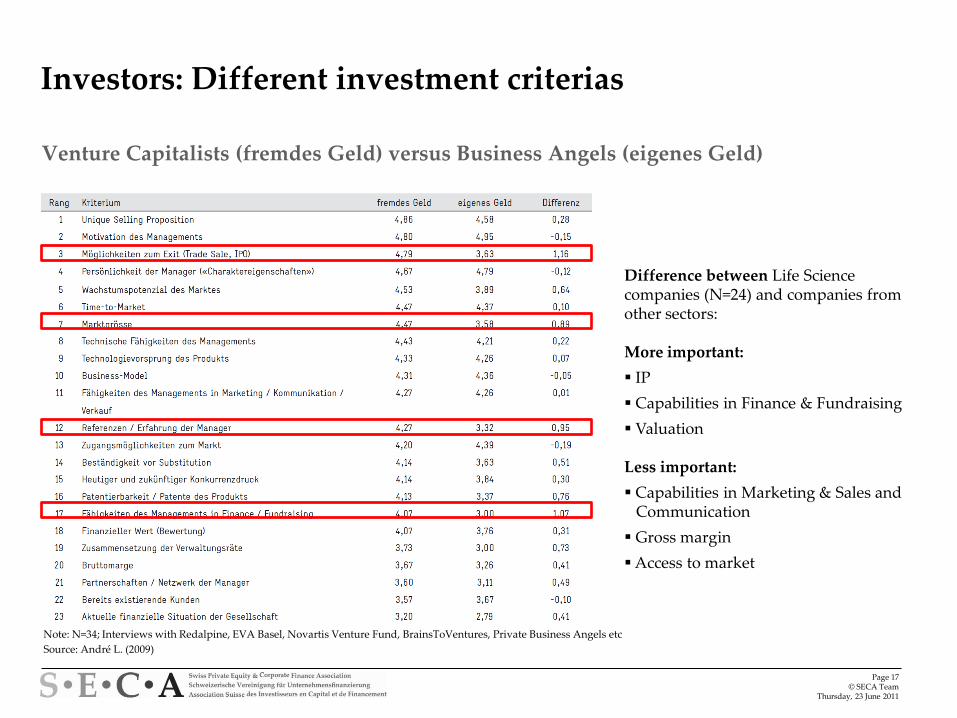

Investors: Different investment criterias

Venture Capitalists (fremdes Geld) versus Business Angels (eigenes Geld)

Source: André L. (2009)

Difference between Life Science companies (N=24) and companies fromother sectors:

More important:

IP

Capabilities in Finance & Fundraising

Valuation

Less important:

Capabilities in Marketing & Sales and Communication

Gross margin

Access to market

Note: N=34; Interviews with Redalpine, EVA Basel, Novartis Venture Fund, BrainsToVentures, Private Business Angels etc

Page 18© SECA Team

Thursday, 23 June 2011

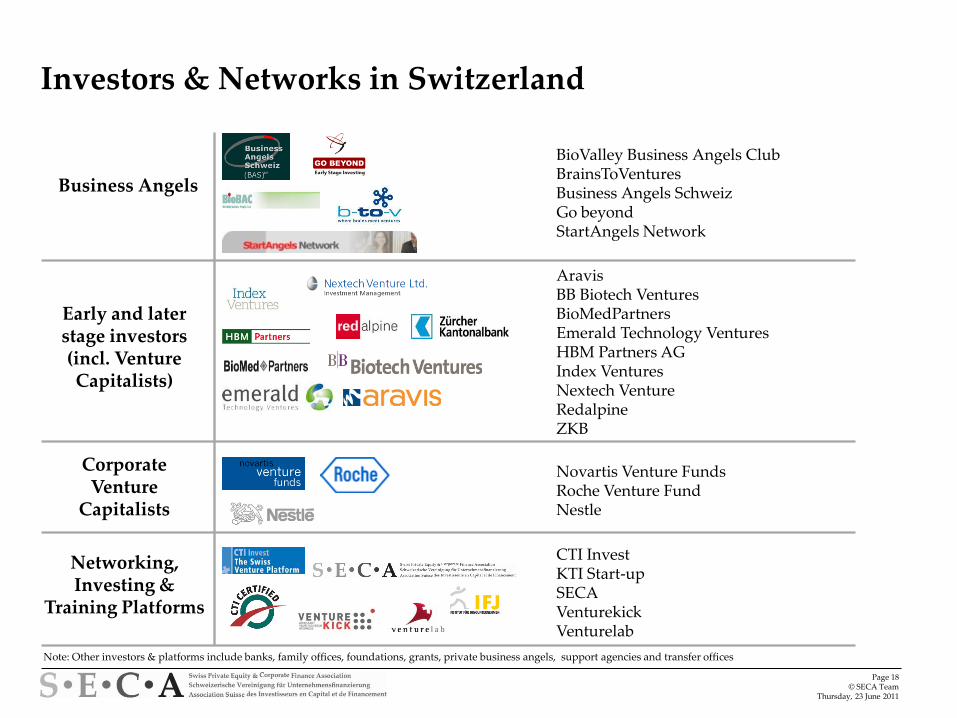

Investors & Networks in Switzerland

Business Angels

Early and laterstage investors(incl. VentureCapitalists)

BioValley Business Angels ClubBrainsToVenturesBusiness Angels SchweizGo beyondStartAngels Network

AravisBB Biotech VenturesBioMedPartnersEmerald Technology VenturesHBM Partners AGIndex VenturesNextech VentureRedalpineZKB

Corporate Venture

Capitalists

Novartis Venture FundsRoche Venture FundNestle

Networking, Investing &

Training Platforms

CTI InvestKTI Start-upSECAVenturekickVenturelab

Note: Other investors & platforms include banks, family offices, foundations, grants, private business angels, support agencies and transfer offices

Page 19© SECA Team

Thursday, 23 June 2011

Agenda

Topics along the way…

Introduction

Switzerland: Facts & Figures

From invention to market: What you need to know?

Switzerland: Performance of the Life Sciences Industry & Success Stories

Challenges & Outlook

Page 20© SECA Team

Thursday, 23 June 2011

Venture Capital in Switzerland

Database - Venture Capital in Switzerland (1999-2009)

Source: Engelhardt & Gantenbein (2010). Venture Capital in Switzerland. An Empirical Analysis of the Market for Early-Stage Investments and their Economic Contribution.

0

50

100

150

99

80

00

150

01

144

02

113

03

100

04

87

05

84

06

80

07

109

08

126

09

108

Information and

Telecommunication Technology

Business and Industrial

Products and Services

Life Sciences

Consumer Products, Servicesand Retail

Other

Number of transactions

Note: Number of early and later stage capital transactions per year and sector

= 1,181

Page 21© SECA Team

Thursday, 23 June 2011

Venture Capital in Switzerland

Database - Venture Capital in Switzerland (1999-2009)

Source: Engelhardt & Gantenbein (2010). Venture Capital in Switzerland. An Empirical Analysis of the Market for Early-Stage Investments and their Economic Contribution.

Amount of Transactions

Note: Amount of Transactions (early and later stage) per year and sector

0

500

1,000

1,500

99

367

00

1,389

01

548

02

444

03

354

04

345

05

597

06

388

07

588

08

365

09

406

Information and

Telecommunication Technology

Business and Industrial

Products and Services

Life Sciences

Consumer Products, Servicesand Retail

Other

= CHF 5,791M

Page 22© SECA Team

Thursday, 23 June 2011

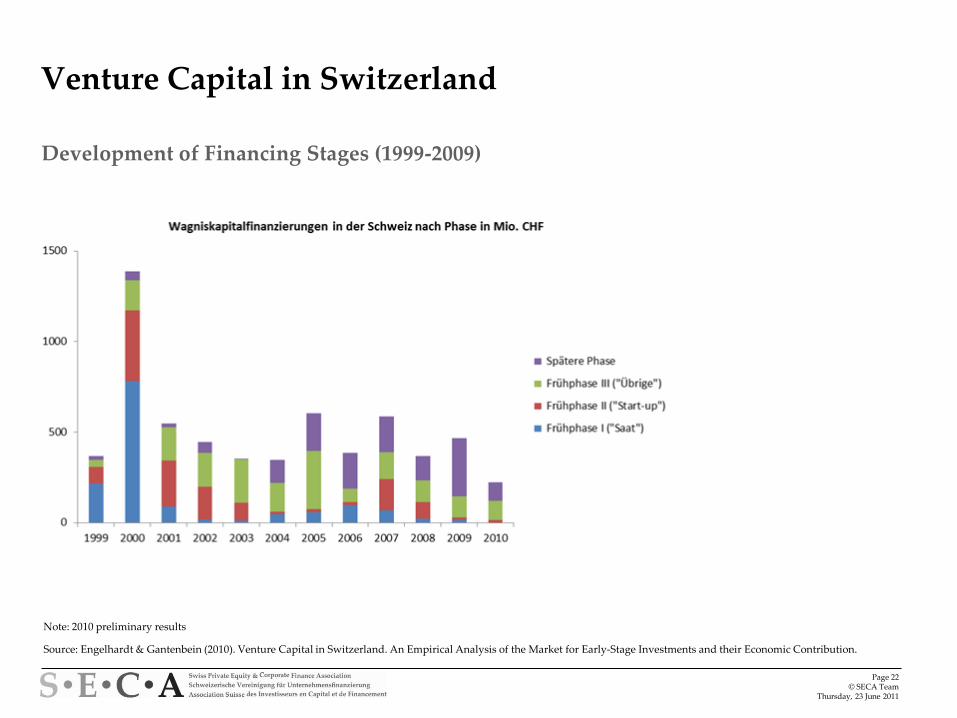

Venture Capital in Switzerland

Development of Financing Stages (1999-2009)

Source: Engelhardt & Gantenbein (2010). Venture Capital in Switzerland. An Empirical Analysis of the Market for Early-Stage Investments and their Economic Contribution.

Note: 2010 preliminary results

Page 23© SECA Team

Thursday, 23 June 2011

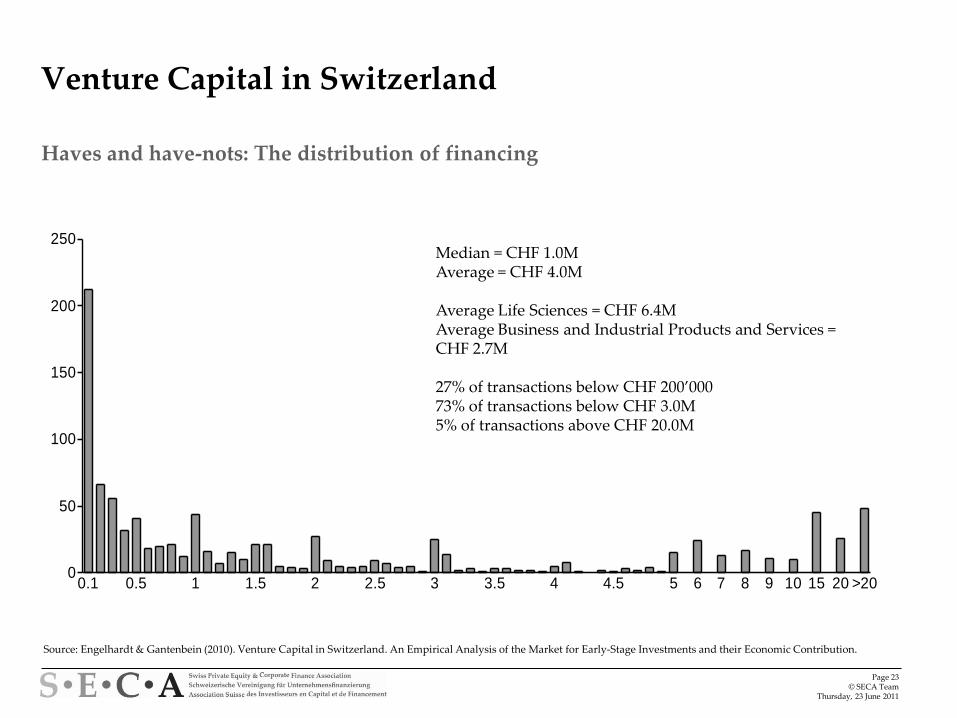

Venture Capital in Switzerland

Haves and have-nots: The distribution of financing

Source: Engelhardt & Gantenbein (2010). Venture Capital in Switzerland. An Empirical Analysis of the Market for Early-Stage Investments and their Economic Contribution.

0

50

100

150

200

250

0.1 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 6 7 8 9 10 15 20 >20

Median = CHF 1.0MAverage = CHF 4.0M

Average Life Sciences = CHF 6.4MAverage Business and Industrial Products and Services = CHF 2.7M

27% of transactions below CHF 200’00073% of transactions below CHF 3.0M5% of transactions above CHF 20.0M

Page 24© SECA Team

Thursday, 23 June 2011

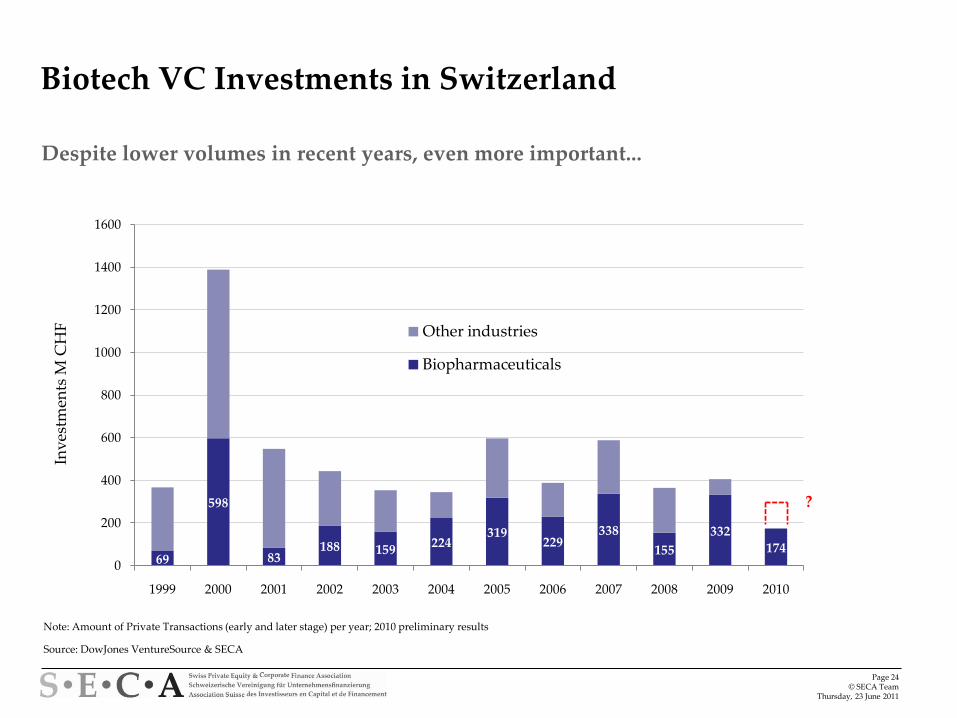

Biotech VC Investments in Switzerland

Despite lower volumes in recent years, even more important...

69

598

83188 159

224319

229338

155

332174

0

200

400

600

800

1000

1200

1400

1600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Other industries

Biopharmaceuticals

Inv

estm

ents

M C

HF

Note: Amount of Private Transactions (early and later stage) per year; 2010 preliminary results

Source: DowJones VentureSource & SECA

?

Page 25© SECA Team

Thursday, 23 June 2011

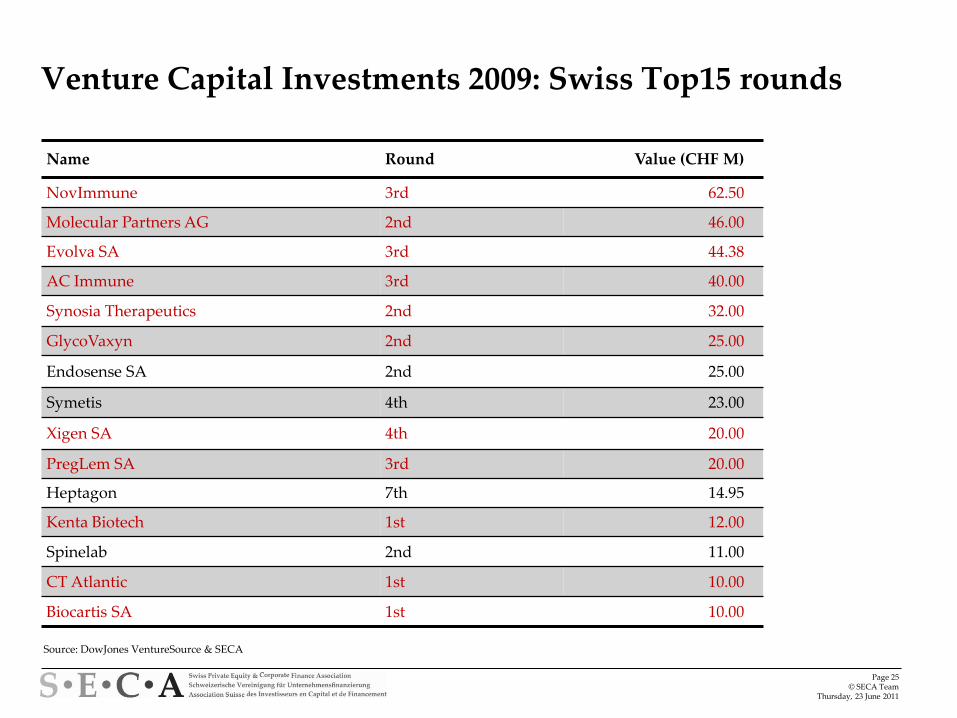

Venture Capital Investments 2009: Swiss Top15 rounds

Name Round Value (CHF M)

NovImmune 3rd 62.50

Molecular Partners AG 2nd 46.00

Evolva SA 3rd 44.38

AC Immune 3rd 40.00

Synosia Therapeutics 2nd 32.00

GlycoVaxyn 2nd 25.00

Endosense SA 2nd 25.00

Symetis 4th 23.00

Xigen SA 4th 20.00

PregLem SA 3rd 20.00

Heptagon 7th 14.95

Kenta Biotech 1st 12.00

Spinelab 2nd 11.00

CT Atlantic 1st 10.00

Biocartis SA 1st 10.00

Source: DowJones VentureSource & SECA

Page 26© SECA Team

Thursday, 23 June 2011

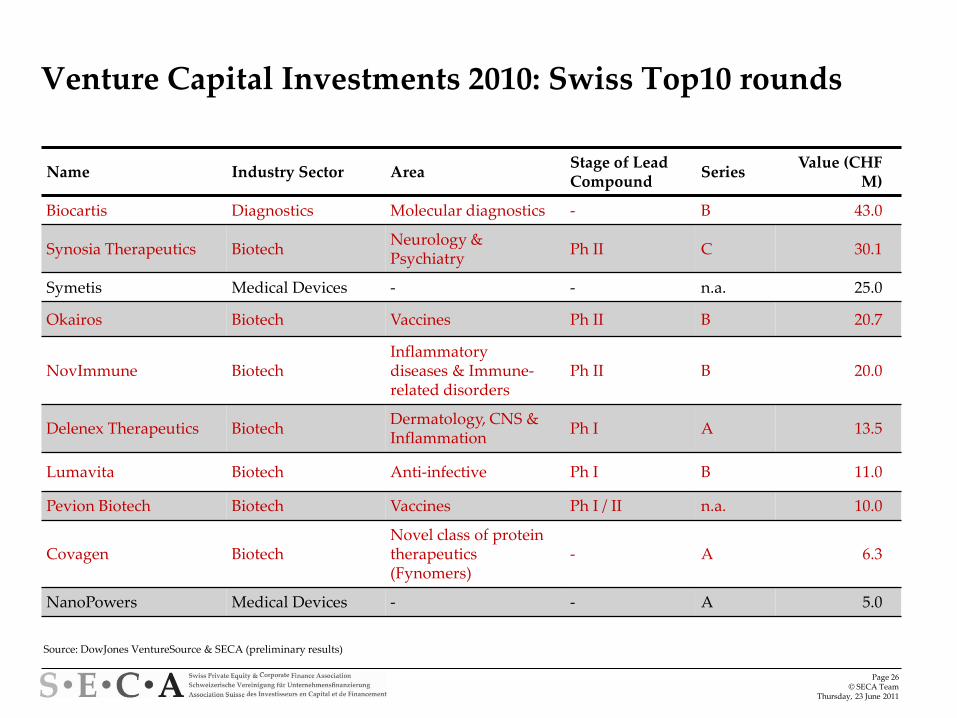

Venture Capital Investments 2010: Swiss Top10 rounds

Name Industry Sector AreaStage of Lead Compound

SeriesValue (CHF

M)

Biocartis Diagnostics Molecular diagnostics - B 43.0

Synosia Therapeutics BiotechNeurology & Psychiatry

Ph II C 30.1

Symetis Medical Devices - - n.a. 25.0

Okairos Biotech Vaccines Ph II B 20.7

NovImmune BiotechInflammatory diseases & Immune-related disorders

Ph II B 20.0

Delenex Therapeutics BiotechDermatology, CNS & Inflammation

Ph I A 13.5

Lumavita Biotech Anti-infective Ph I B 11.0

Pevion Biotech Biotech Vaccines Ph I / II n.a. 10.0

Covagen BiotechNovel class of protein therapeutics (Fynomers)

- A 6.3

NanoPowers Medical Devices - - A 5.0

Source: DowJones VentureSource & SECA (preliminary results)

Page 27© SECA Team

Thursday, 23 June 2011

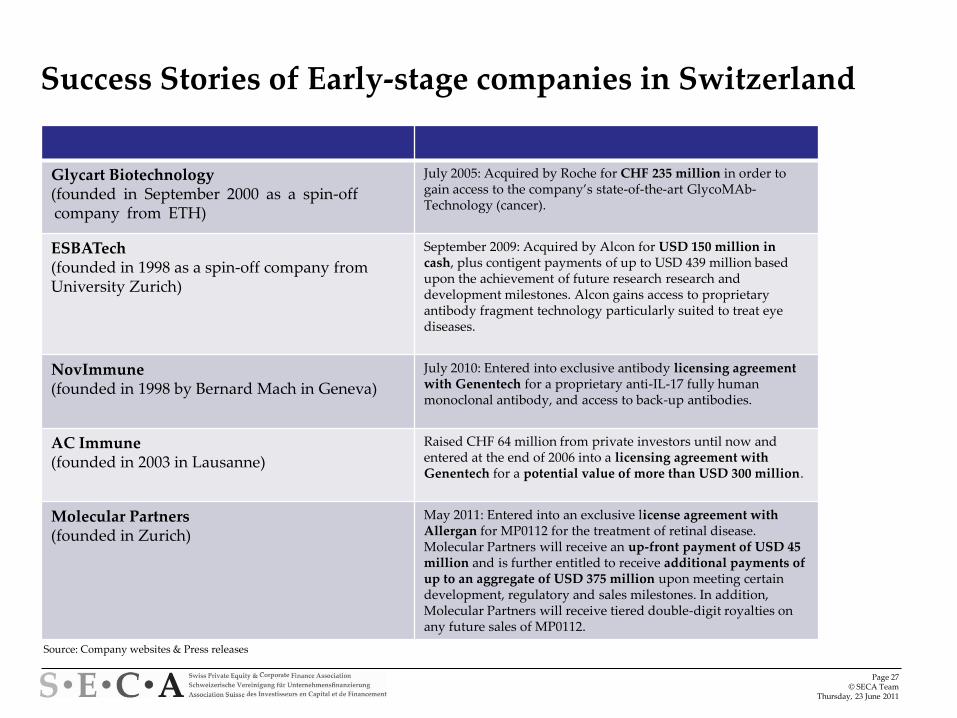

Success Stories of Early-stage companies in Switzerland

Glycart Biotechnology(founded in September 2000 as a spin-off company from ETH)

July 2005: Acquired by Roche for CHF 235 million in order to gain access to the company’s state-of-the-art GlycoMAb-Technology (cancer).

ESBATech(founded in 1998 as a spin-off company fromUniversity Zurich)

September 2009: Acquired by Alcon for USD 150 million in cash, plus contigent payments of up to USD 439 million basedupon the achievement of future research research and development milestones. Alcon gains access to proprietaryantibody fragment technology particularly suited to treat eyediseases.

NovImmune(founded in 1998 by Bernard Mach in Geneva)

July 2010: Entered into exclusive antibody licensing agreement with Genentech for a proprietary anti-IL-17 fully human monoclonal antibody, and access to back-up antibodies.

AC Immune (founded in 2003 in Lausanne)

Raised CHF 64 million from private investors until now and entered at the end of 2006 into a licensing agreement with Genentech for a potential value of more than USD 300 million.

Molecular Partners (founded in Zurich)

May 2011: Entered into an exclusive license agreement with Allergan for MP0112 for the treatment of retinal disease.Molecular Partners will receive an up-front payment of USD 45 million and is further entitled to receive additional payments of up to an aggregate of USD 375 million upon meeting certain development, regulatory and sales milestones. In addition, Molecular Partners will receive tiered double-digit royalties on any future sales of MP0112.

Source: Company websites & Press releases

Page 28© SECA Team

Thursday, 23 June 2011

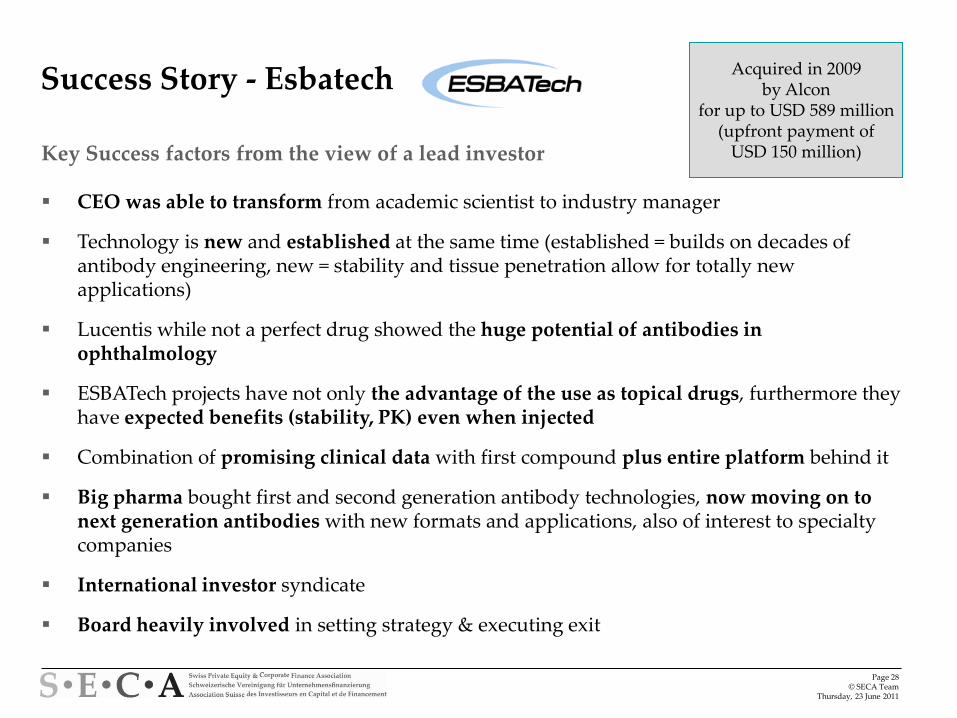

Success Story - Esbatech

Key Success factors from the view of a lead investor

CEO was able to transform from academic scientist to industry manager

Technology is new and established at the same time (established = builds on decades of antibody engineering, new = stability and tissue penetration allow for totally new applications)

Lucentis while not a perfect drug showed the huge potential of antibodies in ophthalmology

ESBATech projects have not only the advantage of the use as topical drugs, furthermore theyhave expected benefits (stability, PK) even when injected

Combination of promising clinical data with first compound plus entire platform behind it

Big pharma bought first and second generation antibody technologies, now moving on to next generation antibodies with new formats and applications, also of interest to specialty companies

International investor syndicate

Board heavily involved in setting strategy & executing exit

Acquired in 2009 by Alcon

for up to USD 589 million(upfront payment of

USD 150 million)

Page 29© SECA Team

Thursday, 23 June 2011

Agenda

Topics along the way…

Introduction

Switzerland: Facts & Figures

From invention to market: What you need to know?

Switzerland: Performance of the Life Sciences Industry & Success Stories

Challenges & Outlook

Page 30© SECA Team

Thursday, 23 June 2011

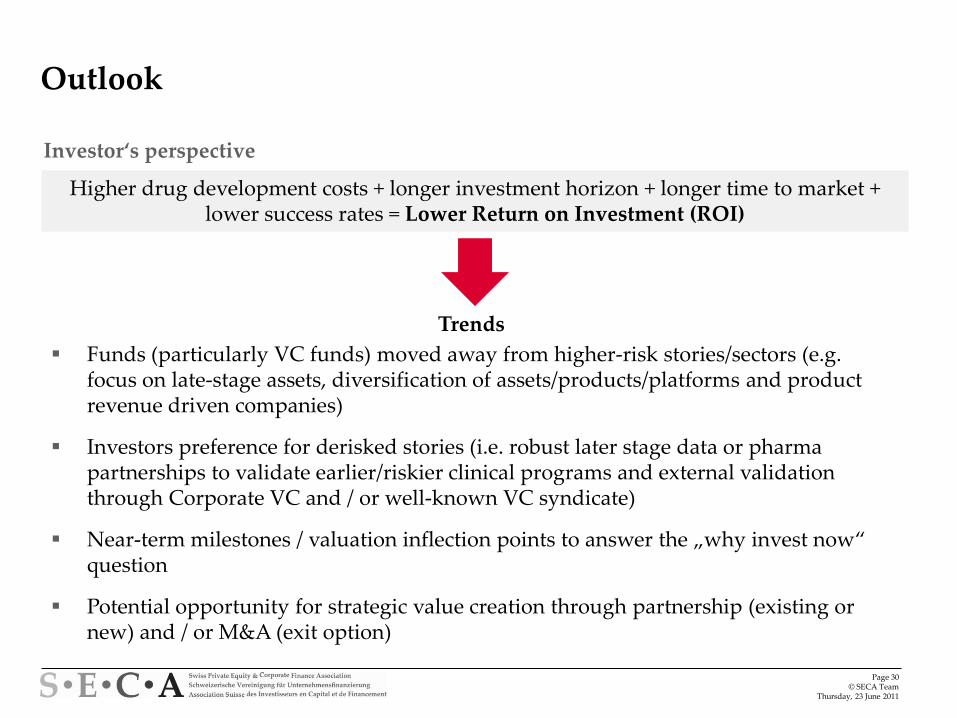

Higher drug development costs + longer investment horizon + longer time to market + lower success rates = Lower Return on Investment (ROI)

Trends

Funds (particularly VC funds) moved away from higher-risk stories/sectors (e.g. focus on late-stage assets, diversification of assets/products/platforms and productrevenue driven companies)

Investors preference for derisked stories (i.e. robust later stage data or pharmapartnerships to validate earlier/riskier clinical programs and external validationthrough Corporate VC and / or well-known VC syndicate)

Near-term milestones / valuation inflection points to answer the „why invest now‚ question

Potential opportunity for strategic value creation through partnership (existing ornew) and / or M&A (exit option)

Outlook

Investor‘s perspective

Page 31© SECA Team

Thursday, 23 June 2011

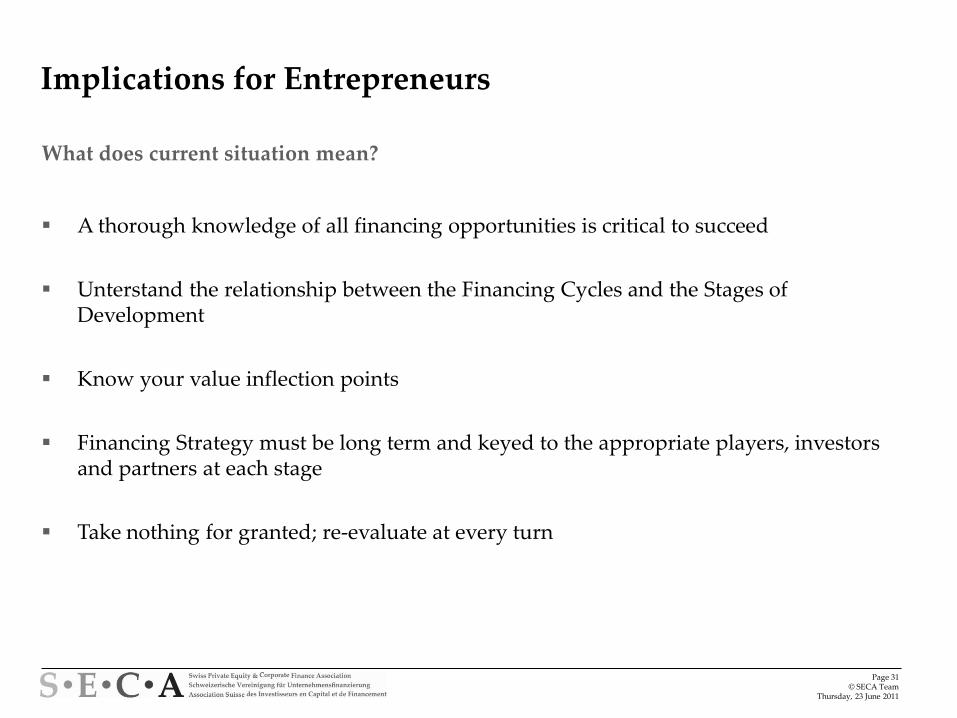

Implications for Entrepreneurs

What does current situation mean?

A thorough knowledge of all financing opportunities is critical to succeed

Unterstand the relationship between the Financing Cycles and the Stages of Development

Know your value inflection points

Financing Strategy must be long term and keyed to the appropriate players, investorsand partners at each stage

Take nothing for granted; re-evaluate at every turn

Page 32© SECA Team

Thursday, 23 June 2011

‚It does not mean necessarily that a situation is becoming better when changing, but you know, if it should become better, situation has to change.‛

Georg Christoph LichtenbergGerman physicist and writer(1742-1799)

Page 33© SECA Team

Thursday, 23 June 2011

Appendix

Page 34© SECA Team

Thursday, 23 June 2011

Biotech at SECA

Biotech als Assetklasse

Kapitalanlagen, Performance,

Investorenbeziehung und Märkte

Von Thomas Heimann, Yann C. Crozat

Herausgeber:

SECA Swiss Private Equity & Corporate Finance Association

SECA Booklet Nr. 5

196 Seiten

1. Auflage Mai 2010

ISBN 3-906488-28-4

Page 35© SECA Team

Thursday, 23 June 2011

SECA Schriftenreihe

Äusserst praxisrelevante Forschung…

Page 36© SECA Team

Thursday, 23 June 2011

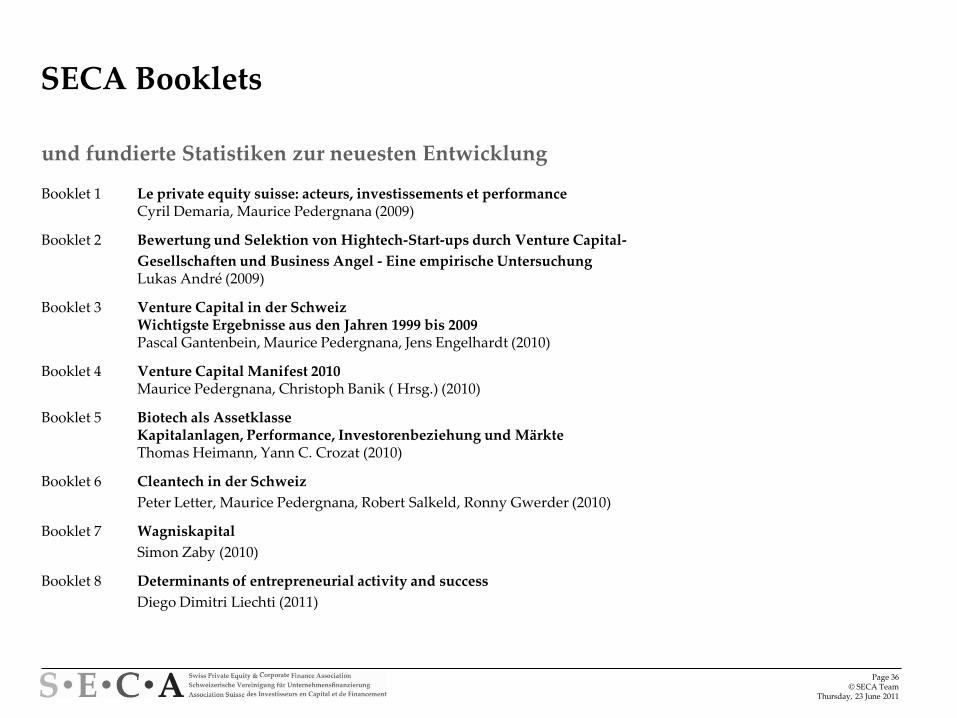

SECA Booklets

und fundierte Statistiken zur neuesten Entwicklung

Booklet 1 Le private equity suisse: acteurs, investissements et performance Cyril Demaria, Maurice Pedergnana (2009)

Booklet 2 Bewertung und Selektion von Hightech-Start-ups durch Venture Capital-

Gesellschaften und Business Angel - Eine empirische UntersuchungLukas André (2009)

Booklet 3 Venture Capital in der SchweizWichtigste Ergebnisse aus den Jahren 1999 bis 2009Pascal Gantenbein, Maurice Pedergnana, Jens Engelhardt (2010)

Booklet 4 Venture Capital Manifest 2010Maurice Pedergnana, Christoph Banik ( Hrsg.) (2010)

Booklet 5 Biotech als AssetklasseKapitalanlagen, Performance, Investorenbeziehung und MärkteThomas Heimann, Yann C. Crozat (2010)

Booklet 6 Cleantech in der Schweiz

Peter Letter, Maurice Pedergnana, Robert Salkeld, Ronny Gwerder (2010)

Booklet 7 Wagniskapital

Simon Zaby (2010)

Booklet 8 Determinants of entrepreneurial activity and success

Diego Dimitri Liechti (2011)